EXHIBIT 3

EXPORT DEVELOPMENT CANADA

2008 ANNUAL REPORT

EDC’s mandate — to support and develop, directly or indirectly, Canada’s export trade and Canadian capacity to engage in that trade as well as respond to international business opportunities — guides everything we do.

Contents

Cover photo: © Ryan McVay/Getty Images

2008 PERFORMANCE MEASURES

| | | | | | | | | |

| | | 2008 Corporate Plan | | | 2008 Results | |

Connecting with exporters and investors | | | | | | | | |

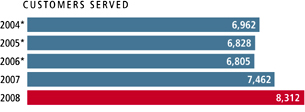

| Customers served | | 3% growth | | | 11% growth – 8,312 | |

| Number of multiple program users | | 15% growth | | | 19% growth – 1,000 | |

| Net Promoter Score | | 64.5 – 67.3 | | | 62.1 | |

Facilitating integrative trade | | | | | | | | |

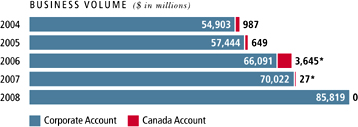

Total business volume 1 | | 7% growth | | | 23% growth – $85.8 billion | |

Volume in emerging markets 1 | | 8% growth | | | 31% growth – $22 billion | |

Volume of foreign investments 1 | | 5% decline | | | 15.5% decline – $4.7 billion | |

Number of investment transactions 2 | | 12% growth | | | 16% growth – 383 | |

Partnership volume1 | | 8% growth | | | 20% growth – $14.1 billion | |

| Number of partnership transactions | | | n/a | | | 4,450 | |

Leveraging the organization | | | | | | | | |

VfM to TCO ratio 3 | | 43:57 | | | 43:57 | |

Employee engagement 4 | | | n/a | | | | n/a | |

Employee retention (%) 5 | | > CB rate | | | 91.83% | |

Sound financial management | | | | | | | | |

| Net income ($M) | | | 543 | | | | 206 | |

| Return on Equity (ROE) | | | 8.6 | % | | | 3.4 | % |

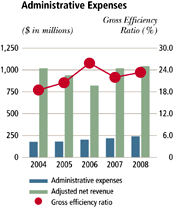

| Gross Efficiency Ratio | | | 25.3 | % | | | 23.3 | % |

| Financial sustainability ratio | | | 8.7 | % | | | 9.1 | % |

| | |

| 1 | | In 2008, EDC began reporting some of its Credit Insurance volume on a net basis, and began reporting its Political Risk Insurance volume net of reinstatements. In order to provide an appropriate year-over-year comparison, all business volume results are shown on a basis consistent with these changes in reporting. |

| |

| 2 | | The 12% growth rate shown in the table incorporates the original Corporate Plan 30% growth targeted for transactions under the Financing and PRI programs, as well as 5% growth under the ARI program. |

| |

| 3 | | Value for Money (VfM) — investments in IT that increase business performance. Total cost of ownership (TCO) — the costs of maintaining core business infrastructure and technology assets. |

| |

| 4 | | Measured on the climate assessment independently reported by Hay. The next survey will be conducted in 2009. |

| |

| 5 | | Conference Board data for financial institutions suggests a rate of 90.4%. |

EDC Annual Report 2008 | 1

2008 PERFORMANCE HIGHLIGHTS

Canadian exports maintain 1 out of 5 jobs in Canada and generate nearly 25% of national income

The business EDC facilitated during 2008 helped generate $57.8 billion of Canadian GDP, about 4.4% of GDP, and supported 572,000 jobs

Canada’s total exports of goods and services reached $522 billion in 2008

EDC served 8,312 customers

EDC facilitated $85.8 billion in exports and investments in 184 markets, a 23% increase over 2007

| | | 4 $22 billion in 145 emerging markets, up 31% over 2007 |

| |

| | | 4 $17.8 billion in exports and investments by small- and medium-sized businesses |

| |

| | | 4 $4.7 billion in Canadian direct investment abroad |

| |

| | | 4 $14 billion done in partnership with financial institutions |

EDC was named one of Canada’s Best Diversity Employers as reported in Maclean’s Magazine, the only Crown corporation out of 25 winning companies

2 | Managing Risk. Maximizing Opportunities.

2008 PERFORMANCE HIGHLIGHTS

FIVE-YEAR REVIEW

| | |

| * | | Includes activity pursuant to the softwood lumber deposit refund mechanism transactions. |

| | |

| * | | Includes accumulated other comprehensive income. |

| |

| ** | | In late 2008, the Minister of Finance announced that EDC would receive a $350 million injection of new capital in exchange for 3.5 million shares with a par value of $100 each. The additional capital will increase EDC’s credit capacity during this period of global economic uncertainty. The $350 million was received from the Government of Canada in January 2009. |

EDC Annual Report 2008 | 3

Message from the Chair

SERVING EXPORTERS IN TIMES OF NEED

As we report on 2008, I am mindful that the world economy — and EDC’s role within it — has dramatically changed, and that new challenges we can’t yet predict will have arrived by the time you read this.

Last year, we could not have known the depth and severity of the economic recession Canadians would face today. We’re fortunate that EDC entered this global crisis in a strong financial position, backed by more than six decades of proven risk management practices. This experience served EDC well at a time when so many once-trusted financial institutions started to crumble under the weight of the U.S. sub-prime mortgage crisis.

Given our Board members’ diverse make-up, we could offer EDC’s executives a broad range of risk management experience as we worked together to make sense of a financial environment that was changing daily. We rolled up our sleeves to debate tough issues around tight credit markets and plunging industry sectors. Our goals were to minimize the impact on EDC’s customers, manage our own credit exposures and enhance EDC’s capital strength.

In this wavering landscape, what remained rock-solid was our common purpose to support and develop Canada’s much-needed international trade. I believe this shared vision, determination and bank of knowledge underpins EDC’s strength and capacity to serve Canadian business and the people of Canada alike.

As you’ll read in this report, EDC reached or exceeded nearly all the performance targets set out in its Corporate Plan for 2008. We take pride in having grown the number of customers served to over 8,300, an 11% increase over 2007. Our volume of business in emerging markets grew 31% to reach $22 billion. That’s more than a quarter of the $85.8 billion in business volume EDC facilitated, vitally important as exports to the United States fall off.

EDC’s results stem from a well thought-out strategic plan. Early in 2008 the Board provided guidance on EDC’s five-year rolling business plan for 2009-2013. By the time the Board approved the plan in late October, the financial turmoil was in full motion and the economic picture had completely shifted. Clearly, the challenges of long-term planning were exceptional this past year.

Still, EDC’s goals remain valid: connecting even more closely with exporters and investors; continuing to facilitate Canadian participation in integrative trade; and leveraging the full weight of EDC, its capital and its people. Those goals set the stage for success beyond this recession.

As the credit crunch continues so will the heightened demand — and the risks that come with it. Now more than ever, it’s essential the Board remains focused on our stewardship role, especially our active oversight of EDC’s risk management practices.

Much of the Board’s work is about setting the right goals; inspiring the organization to exceed them; upholding the values befitting a public sector corporation; and holding management accountable for performance. We’re proud of EDC’s high standards of ethical business conduct and its commitment to transparency, while respecting commercial confidentiality. We work hard to ensure EDC is aligned with the Government’s trade agenda through our relations with the Minister of International Trade and his key staff. We appreciate the Government’s confidence in EDC by signaling new domestic responsibilities and greater capacity to assist Canadian companies during this credit crisis. We welcome the challenge.

4 | Managing Risk. Maximizing Opportunities.

EDC’s new responsibilities build on the partnerships we’ve developed with our colleagues at the Business Development Bank of Canada (BDC) and Canada’s banks. We’re proud of these vital partnerships because they mean better services for Canadian companies. And they’re working. 2008 saw a 20% increase in EDC-facilitated transactions with our banking partners.

The Board monitored EDC’s participation in the Government’s independent review of the Export Development Act through a special sub-committee. The independent review team’s key recommendations are well aligned with EDC’s new responsibilities.

EDC reached out to more stakeholders last year by web-casting its Annual Public Meeting, held in Ottawa. That event, along with directors’ meetings in Toronto and Calgary, gave our Board members an opportunity to meet and hear from our customers and other stakeholders. EDC’s 2009 Annual Public Meeting will be held in Toronto.

As we conduct our business, we are fortunate to have a strong and diverse Board of Directors. Four highly skilled Canadians became directors this year: Jeff Burghardt of British Columbia, Adam Chowaniec and Ajit Someshwar of Ontario and Donald A. MacLeod of Nova Scotia. They are valuable additions to EDC’s Board. We also appreciate the contributions made by those directors whose terms expired in 2008: J. Bernard Boudreau of Nova Scotia, Lise Lachapelle of Quebec and Rowland W. Fleming, Robert A. Fung and Irene So of Ontario. These remarkable men and women gave generously over their years of service and their hard work has made EDC a stronger institution.

We also appreciate the support we received throughout 2008 from the Ministers of International Trade, including our collaborative relationship with former Minister David Emerson and now with Minister Stockwell Day.

Our real strength is the people who work at EDC. They are a talented team of professionals who don’t waver in the face of this financial crisis. They’re capably led by Eric Siegel and his remarkable executive team focused on doing the right things right. As directors, we’re fortunate to work with the talent spread across the corporation. Their efforts earned EDC membership in the ranks of Canada’s Top 100 Employers for the eighth year in a row. Not to be outdone, EDC became the first Crown corporation to be named Best Diversity Employer in 2008.

On behalf of the Board, I want to thank the EDC team for an exceptional year. We challenged them and they exceeded expectations. Now we ask them to “step it up a notch” in both the domestic and international markets and help Canadian companies get past this tsunami so they can thrive and be ready for whatever comes next.

Jim Dinning

Jim DinningChair

EDC Annual Report 2008 | 5

Message to the Shareholder

MANAGING RISK. MAXIMIZING OPPORTUNITIES.

In 2008 we all witnessed global financial turmoil that in scope, complexity and breadth of impact was unprecedented.

What started as a U.S. economic slowdown triggered by the sub-prime mortgage crisis transformed into a full blown credit crunch touching every economy. Virtually every national government has had to take unprecedented measures to bolster their financial systems.

Trade is vital to Canada’s prosperity. Access to credit keeps that trade flowing. As 2008 began we had anticipated lower business volumes as economic conditions softened, slowing export growth. By the last quarter, the extent of the slowdown had created an escalating demand for our services far beyond any prediction, in an environment of far greater risk. Like our customers, we have done our best to rise to the challenge.

EDC’s vision is to be a trusted partner for Canada’s exporters and investors, the financial industry and Canada’s customers worldwide. Our focus is on our customers: to know their business, understand their international needs, connect them with buyers and partners and offer the best financial solutions. We have the capital, financial and human resources, to make that difference.

In 2008 we facilitated trade for more companies than ever — 8,312 firms in 184 markets. That 11% jump is the largest annual increase in our history. Our combined financing and insurance volumes reached $85.8 billion, a 23% increase from 2007. While some of the growth can be explained by higher commodity prices through much of the year and a weaker Canadian dollar at year’s end, it mainly reflects higher demand for EDC programs as liquidity in the private sector tightened.

The results underscore something we always believed at EDC: while our services are needed in good times, they are needed even more when times are difficult.

We were able to meet this surge in large part because of the work begun over the past two years to enhance customer focus and increase productivity. We modeled those changes on the best practices of our customers — investing wisely, and taking advantage of technology to work as efficiently as we can in a competitive world. These changes produced important results. In applying Lean Methodology to our organization, for example, the streamlining accomplished through our Loans Transformation Project reduced issuance times for term sheets by 82% and overall processing times on loans by 60%. The result was increased productivity at every stage of our loans processes. Similarly, the launch of our Customer Relationship Management system helps us better capture and share customer information to serve our customers more effectively with relevant solutions.

Our goal was to increase value to customers. When the credit crunch hit, it meant we were ready with the latest information, our best advice, faster responses, and more effective service delivery. Our internal decision making has improved through greater delegation, engaging all relevant players on a just-in-time basis. This provides customers with greater clarity and consistency while improving the timeliness of decisions in a period of high risk and greater uncertainty.

We are now better aligned with our customers’ processes and their structures. They have changed the way we work and think. Like our customers, we are a business operating on commercial principles. We too are accountable to our shareholder, who measures our success by how successful we make our customers. We will continue to innovate and change in anticipation of customer needs.

A measure of that success is our performance in the eyes of our customers as evidenced by the Net Promoter Score (NPS). A customer’s willingness to recommend is a leading recognized industry measure of satisfaction. EDC already enjoyed a high level in this score, and hoped to raise it further in 2008. While we fell short of our target, our results improved steadily over the year, and we expect our continued investment in service standards and continuing improvement of processes will raise the NPS in 2009.

Risk management is a core competency and at the heart of EDC’s ability to perform its mandate. In a year of market turmoil, new market gaps emerged and EDC was being asked to fill them. We proceeded expeditiously, aggressively, but wisely. EDC’s capability is guided by

6 | Managing Risk. Maximizing Opportunities.

our Credit Risk Management and Capital Adequacy policies supported by extensive investments in processes, technology and people. Asset and portfolio management took on a heightened importance for EDC in 2008 and we actively benchmark our capabilities against international leaders incorporating new tools wherever appropriate.

EDC kept in close contact with Canada’s financial institutions and business and industry associations to identify where EDC capabilities could be better utilized to meet growing needs. In 2008, $14.1 billion of EDC’s business volume was facilitated in partnership with financial institutions, a 20% increase over 2007. In its January 2009 Budget, the Government has broadened our mandate for at least two years to increase our role in domestic financing and insurance to help fill additional gaps occurring under current market conditions. Our efforts will complement those of Canada’s private financial institutions and other Crown corporations like the Business Development Bank of Canada (BDC).

In 2008 we continued to expand our representation across Canada and abroad. We opened new offices in Regina and Windsor, and placed additional small business representatives in Montreal, Halifax and Calgary. We introduced underwriting capability in the regions to bring that process closer to customers and produce faster turnaround times in our approval process. Our investment in new wireless technologies to support our Mobile Workforce Project gives our employees access to corporate systems from anywhere, making frontline staff highly mobile. They now spend the majority of their time on the road with customers.

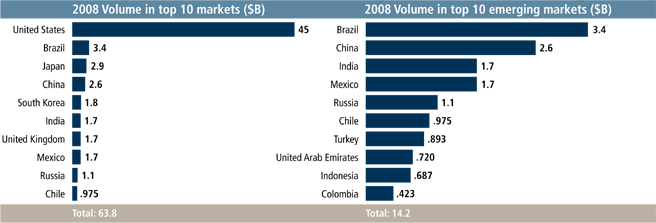

Internationally, we established representation in Mumbai, Santiago and Abu Dhabi and relocated our South East Asia representation to the region’s financial hub, Singapore. EDC has located foreign representatives in 14 centres in high-growth markets to build relationships with potential buyers of Canadian goods and services. That representation has helped grow our emerging market business volume to $22 billion in 2008, a 31% increase. Much of that was in the high-growth markets of India, Brazil, China, Russia and Mexico. In Brazil in 2008 we saw a 131% increase to $3.4 billion, in China 56% to $2.6 billion and in India 50% to $1.7 billion.

As the global financial crisis escalated in the last months of 2008, EDC was an integral part of the Government’s response. To ensure we would be able to meet our customers’ increasing credit needs, the Government authorized an increase in our short-term borrowing authority from USD 4 billion to USD 6 billion. Additionally, the Government’s November Fiscal Update announced its decision to subscribe for an additional $350 million in share capital in anticipation of a continuing credit crisis.

The Government also involved EDC in its program to assist Canada’s auto sector, including its emergency loans to the Canadian subsidiaries of Chrysler and General Motors through the mechanism of the Canada Account. In 2008, EDC provided over $4.2 billion in support to the sector through its financing and insurance products and services.

In 2009 the Government will proceed with the Parliamentary phase of its legislative review of the Export Development Act, following last year’s public consultations. EDC’s business now contributes to 14% of Canada’s total exports and direct investment abroad, generates an estimated $57.8 billion in Canadian GDP, and supports an estimated 572,000 jobs. It is a highly appropriate time for the Government to engage stakeholders in a discussion of our performance and our potential to contribute more, not only through the lens of the present economic situation, but for the long term.

I would like to thank our Chair, Jim Dinning, and our Board for their commitment and guidance, our shareholder for its support, and of course our many customers for the privilege of working with them to develop solutions in a very volatile year.

I also thank the employees of EDC for the exceptional knowledge, commitment and passion they brought to the workplace to help our customers succeed. While Canadian companies will find 2009 extremely challenging, we believe there are excellent opportunities for growth and significant business to be won. We will be there to support their success — managing their risks, and maximizing their opportunities.

Eric D. Siegel

Eric D. SiegelPresident and CEO

EDC Annual Report 2008 | 7

Message from the Chief Economist

EXPORTERS’ PROSPECTS NOT EXTINGUISHED BY TRYING TIMES

Canadian exporters and investors were harshly affected by the global economy in 2008.

Economic conditions deteriorated steadily throughout the year, and the severity of the downturn became fully evident when financial markets, and demand, collapsed in the fall. By year-end, it was clear that a deep recession was underway, further eroding confidence among lenders, exporters, and investors.

The deep and rapid descent was extraordinary. At the beginning of the year, optimists believed signs of trouble in the United States were localized, and economic data from early months of 2008 seemed to confirm that the rest of the world was decoupling from its sputtering growth engine. Commodity prices soared and central banks the world over were preoccupied with inflationary pressures. However, 16 years of virtually uninterrupted global expansion came to a halt in the second half of the year.

Triggering the crisis was the bursting U.S. housing bubble and the decline in U.S. consumer spending that accompanied it. As the number of mortgage defaults reached critical mass, the toxicity of investment products derived from the bundling of high-risk mortgages became apparent. Investors were saddled with substantial bad assets, and a shocking number of respected corporations and financial institutions were crippled by their exposure. Capital quickly became constrained, further increasing pressure on companies using credit to finance their operations and growth. Needing more credit than was available from private sector financial institutions, Canadian exporters and investors turned to EDC in greater numbers than ever.

Beyond the credit crunch, the global malaise hit Canadian exporters in other ways. Removing the effect of wild swings in prices, merchandise exports fell 6%. Commodity prices were extremely volatile, reaching unprecedented heights at mid-year but crashing towards year-end, driving uncertainty about prices of inputs and inflation, and raising concerns that speculative investing was masking estimates of true demand. Where commodities go, the Canadian dollar follows, and after weathering five years of relentless Canadian dollar appreciation, exporters saw the dollar drop late in the year, a result that was also influenced by a resurgent U.S. dollar.

In response to the crisis, governments around the world announced hefty fiscal stimulus programs and accepted short-run deficits as unavoidable. Shared concern about the marked deterioration of the global financial system led to massive and coordinated liquidity injections. At the same time, central banks sharply reduced interest rates at the tail end of 2008 to historically low levels.

8 | Managing Risk. Maximizing Opportunities.

Time will tell just how much bottom-line impact these measures will have over the next two years. Much depends on the willingness of consumers and businesses to spend and borrow, and on the willingness of financial institutions to lend. Given global conditions, a further 10 to 15% drop in Canadian merchandise exports is forecast for 2009, followed by modest growth in 2010. Most industry sectors will follow this near-term pattern.

In the current environment, the sheer number of opportunities for Canadian exporters and investors is lower. However, opportunities do exist on a few fronts.

First, Canadian exporters have a much lower dollar. The loonie is likely to stay in the USD 80 to 85 cent level for the next two years, which will have a direct effect on profit margins. Second, although lower, the Canadian dollar will still be high enough to help companies pursue globalization initiatives such as the creation and expansion of global supply chains and distribution networks. Third, input costs, especially for primary goods, will be lower.

Fourth, sales prospects are grim for Canada’s traditional markets, such as the United States, which are experiencing the worst of the global slowdown. However, non-traditional emerging markets are still a good bet. Although affected by the general recession, growth in these markets will still outperform the average. Add modest market share gains, and Canadian export growth prospects look decent.

Finally, governments worldwide have announced intentions to dedicate a significant portion of their stimulus spending to infrastructure development. In some cases, grand-scale infrastructure projects are occurring in economies that have very little domestic production to draw on. As such, these projects do not simply require construction and engineering services companies, but also a wide array of goods and services that could well be supplied by Canadian enterprises. Many Canadian companies have the needed products, knowledge, and experience to participate in the substantial near-term demand generated by these projects.

The next two years will hold many challenges for Canadian exporters. The risks will be higher, and exporters will not be able to rely on traditional markets. Prospering in this environment almost certainly requires breaking new ground.

In normal times, necessity is often the mother of invention. It could well be said that crisis is the mother of transformation; heeding this adage will be critical to short-term success.

Peter G. Hall

Peter G. HallVice-President and Chief Economist

EDC Annual Report 2008 | 9

Risk-taking is integral to EDC’s mandate to help expand Canada’s international trade. The financial and economic turmoil of 2008 called on EDC to broaden its risk management approach, sharpen its effectiveness and stretch its risk capacity as never before.

Many businesses thrive on risk. But when U.S. and global financial conditions started spiraling downward at an unprecedented pace in fall 2008, the risk became more than businesses bargained for — often more than they could bear.

Before the U.S. sub-prime mortgage crisis led to a series of financial institution failures, the U.S. financial sector was one of the most dependable in the world. As the situation worsened, financial institutions everywhere were managing greatly increased risks and doing far less lending. While private sector financial institutions were retrenching, Canadian companies continued to need credit to manage their operations and carry out their growth strategies. A record 8,312 companies used EDC to help them manage their credit risk during the unusual circumstances of 2008.

EDC’s 64 years of prudent risk management practices and steady revenue growth, especially when Canada’s economy was booming, allowed it to enter the downturn in a strong financial position. In essence, EDC had the cash and capabilities to help Canadian firms cope with the latest set of market challenges. In addition, EDC’s exposure to some of the hardest-hit financial institutions was minimal and EDC did not experience major losses as a result of any defaults in 2008.

10 | Managing Risk. Maximizing Opportunities.

The ongoing recession brings to the forefront the importance of EDC’s risk management expertise and strategies. EDC has the policies, procedures and knowledge in place to regularly monitor, report on and manage our loan and credit insurance risks, market risks (treasury-related investments) and capital position in a timely way.

In 2008, those policies and practices continued to evolve, particularly in two key areas: managing our mounting volume of transactions more efficiently without compromising oversight, and setting the groundwork for a more proactive approach to asset management for the difficult times still to come.

To illustrate, our Risk Management Office (RMO) handled 968 transaction approvals in 2008, nearly a third more than in 2007. This represents $62 billion of financing and insurance volume that required credit authorization, up from $44 billion the year before. The risk profile of transactions also increased, reflecting the deteriorating environment — 64% of loans and 34% of accounts receivable insurance policies approved in 2008 were in higher risk categories (based on borrowers or buyers with lower credit ratings).

Risk management is about constant balance. It’s about managing the amount of risk we take on and the capacity to carry that level of risk for a greater number of clients, while maintaining enough capital to serve future clients. It means taking a measured approach to existing risks and anticipating what could go wrong in the future.

– Derek Layne

EDC, Vice-President and Chief Risk Officer,

Risk Management Office

Over the past two years, EDC improved its ability to handle the increased workload on financing deals through what EDC calls the Loans Transformation Project. Applying a step-by-step diagnosis and streamlining of the corporate lending process, EDC accelerated loan turnaround and customer response times by up to 80%, compared to 2007.

On the insurance side, EDC also tiered transactions according to risk level and pushed more decision-making closer to the working level, within defined parameters. Overall, this freed up time for senior management to focus on the more complex financing, insurance, contract bonding and guarantee activities.

As a result, EDC can respond more quickly to customers in this volatile environment. In achieving these results, EDC retained the integrity of its risk management process, ensuring that at least two pairs of eyes are on every deal.

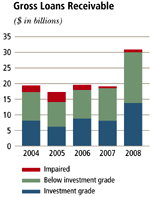

In 2008, EDC also started to see the impact of the credit crunch and economic slowdown on its existing portfolios and expects greater challenges ahead. For example, EDC experienced a 75% increase in requests for loan changes and extensions (waivers, amendments and consents to terms and conditions) by existing borrowers. It also saw an increase in impaired borrowers from 33 to 58. Insurance claims were up 73% in value.

In anticipation of further challenges to loan and insurance portfolios, RMO made process changes in 2008 to ensure its people are deployed as needed to where they can have the greatest impact.

EDC has also put in place a new process and systems to manage its credit portfolio and capital more effectively. This means EDC will be better able to anticipate the sectors and companies where new risks could emerge, track how loans are trading in secondary markets and do more hedging — selling or swapping — of EDC ‘s large credit exposures.

In addition, EDC executives are meeting regularly with their counterparts in Canadian-based banks to develop new ways to help viable Canadian businesses export and invest more abroad. Through greater public-private cooperation and risk sharing, EDC can help sustain Canada’s essential global trade activities, even in these turbulent times.

EDC is as well-prepared as possible under the circumstances to manage increasing levels of risk — in its own portfolio, with its financial partners and for its customers.

EDC Annual Report 2008 | 11

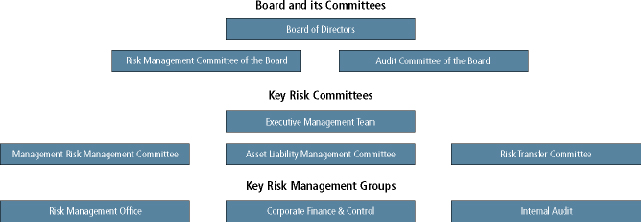

RISK MANAGEMENT OVERSIGHT

Essya Ferjani

Special Risks Manager, Special Risks

Special Risks maximizes recovery on EDC’s current portfolio of distressed loans and guarantees.

“We are a small group of experienced lenders who manage the most challenging assets in EDC’s portfolio. We have an extensive network of global financial contacts who help each other understand and mitigate the risks of distressed assets. In 2008, we were able to rapidly assess the needs of external parties, which is key to finding a resolution to an impaired loan/guarantee — either by restructuring the debt, selling the asset or managing the loan through the bankruptcy process. We are now starting to see a dramatic increase in borrowers who need to have their financial profile restructured.”

The vast majority of EDC’s employees participate in some form of risk management, whether they are assessing commercial, technical, environmental or country risk for EDC or our customers. At an organization-wide level, EDC’s Risk Management Office (RMO) manages our overall financial risk, including timely reporting of major exposures to EDC’s management and the Board. RMO establishes the credit and market risk policies and strategies that maintain sufficient capital and the solvency of EDC. Here, we look at a small cross-section of the expertise, responsibilities and challenges of managing financial risk today.

David Stevenson

Loan Portfolio Manager, Asset Management (Equipment & Services)

Asset Management supervises EDC’s loan and guarantee assets, after their first disbursement, using strategies that mitigate the risks, preserve capital and optimize the portfolio, ensuring further risk capacity to support EDC’s mandate.

“In 2008, we saw a large increase in requests to restructure loan agreements across the entire portfolio, especially among automotive parts makers and our small business clients. In many cases, we supported increased flexibility to allow for companies to restructure or to give them more time to pay. As risk continues to increase across our portfolio, many of our clients have to renegotiate their existing loans. Just managing the workload is one of the biggest challenges facing us in 2009.”

12 | Managing Risk. Maximizing Opportunities.

Viren Joshi

Senior Corporate Risk Manager, Credit Authorization

Credit Authorization works with EDC’s Business Teams to provide independent confirmation of risk acceptability consistent with our risk appetite and policy guidelines. Credit Authorization also shares its expertise on best practices from its broad sector perspective.

“At the beginning of 2008, transactions were being underwritten in the market with longer tenors and weaker structures. Refinancing risk was not a key concern with so much access to capital globally. It was a borrower’s market. By the end of the year the trend had reversed to a lender’s market; deals were being structured more prudently. Through daily interactions with the business teams, our credit authorization group was able to help our colleagues understand the current credit market and deal with difficult transactions. This integration with the underwriting function was key to our success in 2008.”

David Ford

Director, Market Risk Management

Market Risk Management enhances EDC’s risk-taking capacity by actively managing market and treasury credit risk, including analyzing treasury counterparties and setting credit limits. EDC’s goal in managing market risks (liquidity, interest rate and foreign exchange risks) is to ensure the financial sustainability to fulfill our mandate.

“Like all market investors, EDC faced increased risk in 2008 as many top-rated U.S. institutions in which we had investment holdings or other exposure experienced serious credit problems. In this scenario, EDC was served well by the diversification in our portfolio of risks, the different sources and methods we used to determine credit risk and our conservative risk management practices, including collateral requirements. This strategy means that we were not heavily exposed to the most troubled institutions in 2008 and we are well positioned for any surprises going forward.”

Robert Kelly

Senior Risk Transfer Manager, Risk Transfer

Risk Transfer implements strategies and transactions that transfer risk in EDC’s commercial loan portfolio to other counterparties through the secondary market. EDC may reallocate risk for reasons such as mitigating asset-specific risks, strengthening the portfolio, preserving capital or increasing risk capacity.

“In previous years we were able to mitigate our exposure to key sectors, such as aerospace, by insuring or selling portions of our loans to the secondary market (hedging). Our transfer activity was greatly reduced last year because the cost of executing our hedging strategies increased dramatically. As a result our efforts were mainly focused on developing a framework for future hedging so that we can act quickly when the right opportunities arise.”

EDC Annual Report 2008 | 13

MANAGING ACCELERATED RISK IN THE AUTOMOTIVE SECTOR

In 2008 the automotive sector reached an uncommon depth of distress after more than a year of steady sales declines. In the midst of this turbulence, EDC provided $4.2 billion in financing and insurance services to some 595 auto parts and tooling suppliers.

By the end of 2008, the slump in the U.S. automotive sector had reverberated throughout the North American automotive industry and abroad. Declines in sales of cars and light trucks reached a massive 18% in the U.S. In Canada, the overall decline was 1% for 2008, but results were far worse in the latter months of the year and the slide is not abating.

The global credit crunch has been particularly hard on this industry, reflected in severely reduced financing and credit insurance being offered by banks and insurers worldwide. In this environment, EDC clearly demonstrated its commitment to Canada’s automotive sector — mainly Tier 1, 2 and 3* auto parts and tooling suppliers to the Big Three (GM, Chrysler and Ford) and other original equipment manufacturers (OEMs) — by providing $4.2 billion in commercial loans, guarantees and credit insurance last year to some 595 customers.

EDC maintained existing insurance coverage, and continued to do new business where it made sense. EDC’s Transportation Credit Insurance team assisted policyhold-ers through various buyer bankruptcy or workout arrangements. Similarly, EDC’s Financing team was swamped with requests for increased and new financing, while Asset Management was kept busy restructuring many existing loans, mainly to Tier 1 and 2 players. This often meant amending loan terms and conditions or giving customers more time to repay.

To protect both our ability to serve these companies now and in the future, and our fiscal responsibility to Canadian citizens, EDC reinforced two key areas of its automotive risk management strategy in 2008:

More collaboration and monitoring

EDC is in constant contact with bankers, insurers and brokers, exporters and automotive industry experts to monitor the credit situation as it happens. EDC’s management reviews automotive transactions and risk strategy for the sector on a weekly basis.

EDC’s ability to stretch its support to exporters also stems from the increased integration of our teams involved in the automotive value chain. The collaborative approach between risk management, financing, insurance and business development lets us see the whole picture and do more for our customers.

| | |

| * | | Tier 1 — design and manufacture of large sub-assembled vehicle parts and sections. |

| |

| | | Tier 2 — producer of vehicle parts, including minor sub-assembly. |

| |

| | | Tier 3 — engineered materials & special services, from sheet-steel to surface treatments. |

14 | Managing Risk. Maximizing Opportunities.

More strategic use of capital

By thoroughly understanding the sector, predicting potential future problems, and tracking our exposure to the sector as a whole, EDC can deploy our expertise and capital more strategically.

For example, EDC recognizes that many suppliers are strategically important to the supply chain and therefore have good leverage with their buyers. Those companies have the potential to successfully transition through the industry’s current turmoil with EDC’s insurance and other financial backing.

We also worked with our policyholders to ensure that existing coverages continued to meet their needs and any surplus coverage identified was re-deployed to other suppliers.

With these strategies in place, EDC was able to take on more risk for our customers and financial partners.

In 2008, EDC saw its policyholders throughout the auto sector reporting more overdue invoices and bankruptcies. This translated into a five-fold increase in insurance claims.

EDC’s risk management advice and claim payments have helped several policyholders avert bankruptcy, reducing the domino effect in the supply chain. For example, when a large U.S. auto parts maker went into bankruptcy protection last year, several Canadian tooling policyholders had millions of dollars in accounts receivable outstanding. EDC’s insurance proceeds buffered the smaller suppliers from the short-term impact of their buyer declaring bankruptcy. Several of our policyholders also placed liens on the tooling equipment, which gave them more leverage to maximize their recoveries.

In some cases, by working closely with the customer, EDC was able to assist in recovering not only the losses on claims already paid to the policyholder, but also the policyholder’s 10% uninsured portion. That’s a material amount for most companies in the automotive supply chain.

The situation in the automotive sector will remain fluid in 2009. Working together, EDC’s various risk assessment, portfolio management and business sector teams on both the credit insurance and financing side will continue to monitor the volatile situation daily and examine each exporter’s situation individually. This will allow for continued flexibility and prudent risk management.

EDC Annual Report 2008 | 15

OPERATING PRINCIPLES

RESPECTING INTERNATIONAL AGREEMENTS

EDC conducts its business in a manner that is respectful of applicable international agreements to which Canada is a party, consistent with its Corporate Social Responsibility commitments, and ensures the sound financial management of its activities.

EDC supports business on terms consistent with and respectful of Canada’s international obligations related to trade. These include the World Trade Organization’s (WTO) Agreement on Subsidies and Countervailing Measures and the Organization for Economic Co-operation and Development’s Arrangement on Officially Supported Export Credits (OECD Arrangement).

In 2008 we marked the first year in the implementation of the revised OECD Sector Understanding on Export Credits for Civil Aircraft under the OECD Arrangement and EDC was actively involved in follow up discussions related to the monitoring and implementation of the agreement.

EDC also supported OECD discussions that led to the adoption of principles and guidelines to promote sustainable lending practices in the provision of official export credits to low-income countries. An agreement was concluded in April 2008, and EDC put in place internal procedures to ensure the provisions were implemented.

As a member of the OECD Export Credit Group, EDC participates in the ongoing monitoring and reporting on the implementation of the OECD Recommendation on Bribery in Officially Supported Export Credits. This Recommendation strengthens international efforts to combat bribery in export contracts and supports Canada’s commitment to combat bribery in international transactions as per the OECD’s 1997 Convention on Combating Bribery of Foreign Public Officials in International Transactions.

2008 also marked the first year of implementation of the revised OECD Recommendation on Common Approaches on Environment and Officially Supported Export Credits, which was adopted in 2007. The revised Recommendation, which is more aligned with EDC environmental review practices, provides a more level playing field for Canadian exporters in the area of export credits. EDC also participates in the ongoing reporting on the implementation for the OECD Common Approaches on Environment. The next review of the Common Approaches is scheduled for 2010.

The current text of the Sector Understanding on Export Credits for Nuclear Power Plant (NSU) under the OECD Arrangement on Officially Supported Export Credits was adopted in the 1980s. Given the renewed interest, OECD participants identified a need to update the NSU. Initial discussions on the NSU took place in late 2008 and negotiations are expected to conclude in 2009. EDC is working closely with The Department of Foreign Affairs and International Trade (DFAIT) and the Department of Finance to develop Canada’s position for this negotiation.

EDC is actively involved in OECD discussions related to the monitoring and implementation of the OECD Arrangement on Officially Supported Export Credits. In 2008 EDC was actively involved in discussions on the development of a mandate for the OECD Working Group on Premia to give a new impetus to these negotiations with a view to achieving a breakthrough in 2009. Since the adoption of this new mandate, EDC has been promoting compromises among participants. The achievement of an agreement on buyer risk premia will provide a more level playing field for our exporters, which is critical in times of financial crisis where officially supported export credits are playing an increasingly important role in supporting international trade flows.

EDC is a member of the Berne Union, whose mandate is to foster international acceptance of sound principles of export credit and foreign investment insurance. In October 2008, EDC hosted the 65th Annual General Meeting of the Berne Union in Banff, Alberta. The event provided a timely opportunity for Berne Union Members to discuss the financial crisis and members’ own experience. This was also the first Berne Union meeting designed to minimize the environmental footprint of the event, and as such, discussions also focused on how members can minimize their impact on the environment.

16 | Managing Risk. Maximizing Opportunities.

CORPORATE SOCIAL RESPONSIBILITY

At EDC, Corporate Social Responsibility (CSR) is an operating principle that guides all of our business decisions and enables us to build public confidence and trust in what we do to facilitate Canada’s international trade. Our commitment to CSR is rooted in five pillars: business ethics, the environment, transparency, community investment and organizational climate.

In 2008, we focused on refining our structures, systems, practices and training in order to strengthen and reinforce our commitment to CSR. Specifically, we created a distinct Corporate Responsibility team and established a new senior role of Chief CSR Advisor. The role of the team is to support all business teams throughout the corporation to ensure our commitments to CSR are fulfilled.

The Corporate Responsibility team also developed a new strategy to further embed CSR principles into EDC’s corporate and business strategy. In developing this strategy we sought external expertise from various sources including Dirk Matten, Hewlett Packard Chair in CSR at the Schulich School of Business.

CSR Advisory Council

Our CSR Advisory Council also played a pivotal role in advancing our CSR practices throughout 2008. The Advisory Council, comprised of accomplished Canadians with diverse backgrounds representing the private sector, academia and civil society, guided us on best practices on key CSR issues such as the development of a statement on human rights, the consultation process for a review of our environmental policy, support for environmental technologies and CSR practices in emerging markets.

With Maureen O’Neil, former President of the International Development Research Centre, serving as Chair, the Advisory Council also included Dr. Randy Gossen, Vice President, Safety, Environment and Social Responsibility at Nexen Inc.; Jean-Claude Villiard, a retired public servant currently serving as an Associate Professor at the École nationale d’administration publique; Ed Waitzer, Senior Partner at the law firm Stikeman Elliott LLP; David Runnalls, President and CEO of the International Institute for Sustainable Development; and David Zussman, Jarislowsky Chair in Public Sector Management, University of Ottawa.

Statement of Commitment on Human Rights

In accordance with its social responsibilities as a Crown corporation and as a good corporate citizen, EDC values and promotes the protection of internationally recognized human rights, consistent with the policies of the Government of Canada. In April 2008, following recommendations by the UN Special Representative of the Secretary General on Human Rights that outlined a role for Export Credit Agencies, EDC released a Statement of Commitment on Human Rights. The statement defines EDC’s current practices in considering human rights issues associated with potential business:

“EDC values human rights and provides its financing and insurance services with a view to the promotion and protection of internationally recognized human rights. Investment projects may have potentially significant impacts on the human rights of individuals. EDC recognizes that financial institutions must endeavour to assess the potential for adverse human rights outcomes for individuals directly affected by such projects.” For more information, please visit www.edc.ca/ethics.

Forum on Socially Responsible Mining in Peru

While emerging markets present many opportunities for Canadian companies, they also present higher levels of risk with respect to corporate social responsibility. In May 2008, EDC hosted a Forum on Best Practices for Socially Responsible Mining in Peru. The forum encouraged the discussion of divergent views and the development of networks among stakeholders, including representatives from governments, financial institutions, NGOs and the private sector. The objective was to help EDC make informed decisions on how best to conduct business in challenging markets to the benefit of all stakeholders, including local communities. Moving forward, EDC will continue the dialogue with a variety of stakeholders in order to refine its understanding of the challenges facing sustainable mining in difficult environments.

EDC Annual Report 2008 | 17

Operating Principles

Evolving environmental policies and practices

Our Environmental Policy, introduced in 2005, outlines the environmental review processes that are applied to EDC’s financial products and the markets we serve across all industry sectors to ensure our environmental commitments are fulfilled. Since that time, our environmental procedures and policies have evolved significantly. We initiated a review of the Environmental Policy in the fall of 2008, which will include a comprehensive public consultation process in the first half 2009. We plan to introduce a revised Policy later in 2009. Key issues for discussion throughout the consultation process will include project benchmarking standards, community engagement, project conditions and monitoring, disclosure practices, climate change and EDC’s environmental footprint. More information is available at www.edc.ca/environment.

Conducting business in an ethical manner

EDC’s Code of Business Ethics and Code of Conduct guide the actions of EDC and its employees, officers and directors to ensure they continue to live up to EDC’s reputation as an ethical organization. The codes define EDC’s obligation to ethical business conduct, the environment, prohibitions against bribery and corruption, promoting the protection of human rights, avoiding conflicts of interest and maintaining confidentiality of information. EDC requires that directors and employees be familiar with and adhere to the standard of conduct reflected in the Code of Conduct and sign an annual Statement of Compliance to this effect.

In the first year of our partnership with CARE Canada, EDC will assign volunteers to provide business development assistance to small businesses in Peru. Future assignments might see EDC staff assisting in various CARE Canada-sponsored micro-financing projects, such as helping small agricultural enterprises develop their business and expand into larger supply chains.

Transparency

Public accountability guides the Corporation’s reporting and Communications Policy. We disclose a wide range of information on our services, programs and activities and make this information publicly accessible through our website, publications, correspondence and an ongoing program of consultation and engagement with customers, partners and stakeholders.

Under our Disclosure Policy we provide, ex ante, details on our Category A projects (those likely to have significant, adverse environmental impacts), as well as environmental information for Category B projects (projects that are less likely to have adverse affects), such as the type of information we review and the environmental standards we apply. For information on EDC’s disclosure practices and the disclosure of transactions, visit www.edc.ca/disclosure.

The Access to Information Act (ATI) makes documents under EDC’s control accessible to the public, subject to exemptions provided under ATI and the Export Development Act. In 2008, EDC processed 37 ATI-related requests.

EDC also produces an annual Corporate Social Responsibility Report, available at www.edc.ca/csr.

EDC’s commitment to the community

In 2008, EDC shifted community investment initiatives towards global projects and increased employee involvement in these initiatives.

Partnership with CARE Canada

In October 2008, EDC announced that it was sponsoring a four-year community investment partnership with CARE Canada for small business enterprise development and micro-financing related projects in emerging markets. EDC has long been an advocate for community investment, and, through this initiative, has broadened its notion of “community” by extending the scope of its community involvement to those markets where we conduct business.

In mid-2009, EDC volunteers will be assigned to CARE projects, beginning in Peru. Projects could include developing marketing plans for small exporters, developing a risk assessment program for a micro-finance lender, or improving information technology systems, among others. Given CARE Canada’s enterprise development initiatives in emerging markets and EDC’s own skill sets and mandate, this partnership is an ideal alignment of expertise to contribute to poverty alleviation through business development.

Local and national communities

Our employees continue to make a contribution to local and national communities. EDC supported employee efforts to organize our Government of Canada Workplace Charitable Campaign, which raised $249,350. Employees also participated in the United Way Day of Caring™, where EDC employees participated in local community development activities.

18 | Managing Risk. Maximizing Opportunities.

Education & Youth Employment Strategy

Our Education and Youth Employment (EYE) Strategy focuses on educating and building knowledge of international business issues among Canadian students and other stakeholders. The goal of the program is to prepare Canada’s youth for careers in international trade. Scholarships, research and trade education are the principal tools for delivering on this strategy. In 2008, we awarded 30 scholarships, 25 of which went to undergraduate university students pursuing a career or furthering their studies in international business, and five new scholarships to students enrolled in combined environment and business studies. The new emphasis on combined studies brings attention and support to Canada’s future capacity to engage in international trade in an environmentally responsible manner. We work with partners such as AIESEC and the Forum for International Trade Training (FITT) to increase knowledge of international trade among Canadian university students. More information about the EYE Strategy is available at www.edc.ca/youth.

EDC Research Chair in Environmental Finance

In 2008, the Faculty of the Environment at the University of Waterloo and EDC announced the creation of a new research chair, funded by EDC, to identify financial trends, tools and practices that will help businesses develop “green” technologies, services and market opportunities. The EDC Research Chair in Environmental Finance, based in Waterloo’s Centre for Environment and Business, will explore financial tools such as carbon financing and clean energy funds.

SOUND FINANCIAL MANAGEMENT

| | | | | | | | | | | | | |

| | | 2008 Plan | | | 2008 Results | | | 2009 Plan | |

Measure | | | | | | | | | | | | |

| Net income ($ millions) | | | 543 | | | | 206 | | | | 148 | |

| Return on equity % | | | 8.6 | | | | 3.4 | | | | 2.4 | |

| Gross efficiency ratio % | | | 25.3 | | | | 23.3 | | | | 27.6 | |

| Financial sustainability ratio %* | | | 8.7 | | | | 9.1 | | | | — | |

| | |

| * | | Beginning in 2009, FSR will no longer be used by the Corporation as a performance ratio. |

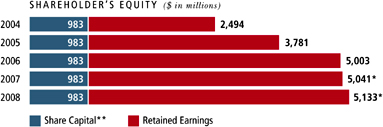

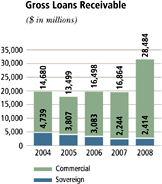

Through sound financial management, we ensure that we have an adequate capital base to fulfill our mandate now and in the future. Operating on a self-sustaining basis with no annual appropriations from Parliament, we achieve self-sustainability by obtaining adequate return for risks taken, containing costs and appropriately managing risk. This approach has enabled us to support more than $770 billion in exports and investments from the approximately $1 billion in share capital* invested in the Corporation by the Government of Canada since 1944.

We track our financial performance in four key performance measures: net income, return on equity, gross efficiency and financial sustainability ratios.

Net income in 2008 of $206 million was $337 million below the 2008 Corporate Plan. The lower net income was primarily due to an increased provision for credit losses and higher claims-related expenses reflecting the impact of the difficult economic environment on our financing and insurance portfolios. In addition, we received no debt relief in 2008, whereas the Plan assumed $124 million. The reduction in net income had a corresponding impact on the return on equity ratio, reducing the ratio to 3.4% versus the Plan amount of 8.6%

| | |

| * | | In late 2008, the Minister of Finance announced that EDC would receive a $350 million injection of new capital in exchange for 3.5 million shares with a par value of $100 each. The additional capital will increase EDC’s credit capacity during this period of global economic uncertainty. The $350 million injection was received from the Government of Canada in January 2009. |

EDC Annual Report 2008 | 19

PERFORMANCE VS OBJECTIVES

OBJECTIVE 1: CONNECTING WITH EXPORTERS AND INVESTORS

| | | | | | | | | | | | | | | | | |

| | | 2007 Result | | | 2008 Plan | | | 2008 Result | | | 2009 Plan | |

Performance measures | | | | | | | | | | | | | | | | |

| Customers served | | | 7,462 | * | | 3% growth | | | 11% growth (8,312) | | | Maintain | |

| Number of multiple program users | | | 841 | ** | | 15% growth | | | 19% growth (1,000) | | | 10% growth | |

| Net Promoter Score*** | | | n/a | | | | 64.5 – 67.3 | | | | 62.1 | | | | 61.1 | |

| | |

| * | | In 2008, we revised the calculation of Customers served to include the number of customers who may have been acquired in previous years, but who continue to be served by the Corporation through, for example, disbursements, or policy coverage. To allow for an appropriate year-over-year comparison, the 2007 Customers served result has been shown on a basis consistent with 2008. |

| |

| ** | | For 2007, the number of multiple program users reported was 513. In 2008, we revised the calculation of MPU to include the total number of active policies or products used by a customer, regardless of the start date. Previously, MPU scores were calculated based on products initiated within one calendar year. |

| |

| *** | | New measure introduced in 2008. |

Connecting with exporters and investors means that we put our customers at the centre of everything we do, focus all of our finance and risk management expertise and our sector and market knowledge on their needs.

In 2008, we faced higher demand than we forecast across all our programs and services as constraints on liquidity in the private sector drove more companies to seek our assistance. EDC served 8,312 customers in 2008, 11% more than 2007.

To better serve our customers in Canada and around the world, we broadened our network of Canadian and international representatives, improved our processes and account management and worked with our private sector partners to bring Canadian companies the services they need. These efforts helped us to increase our customers’ knowledge of the full breadth of our products and services. As a result, the total of multiple program users — customers that use more than one product or service — increased by 19% over 2007 to 1,000.

In 2008, we introduced a new customer satisfaction measure, the Net Promoter Score (NPS), which replaced Customer Service and Customer Value indices. NPS measures the likelihood that our customers would recommend EDC to other businesses; the results provide a better reflection of how customers perceive the value that EDC brings to their business. Based on monthly surveys, NPS provides us with ongoing feedback on how well we are connecting with customers and how improvements to our products and services are perceived by them. We did not meet our projected target for the initial year of this measure, however, monthly results did show progress towards the end of the year. One of the tools we are using to improve our connections to customers is C3, the technology that supports our Customer Relationship Management system. Phase 1 of C3 was launched in 2008 and is providing employees with a more effective means to capture, share and translate customer intelligence into relevant solutions.

Strengthening our representation in Canada and internationally

Our network of offices across Canada allows us to connect and respond locally to our customers’ needs. This is particularly relevant for our mid-market customers. In 2008, the Commercial Markets & Small Business team deployed 10 new account managers, opened new offices in Regina and Windsor, and placed additional small business representatives in Montreal, Halifax and Calgary, bringing our regional representation to 90 staff located in 14 offices across the country.

20 | Managing Risk. Maximizing Opportunities.

| | |

| * | | Figures prior to 2007 were not restated. |

We also expanded our regional underwriting capability by placing local underwriters in Montreal, Mississauga and Vancouver, in order to address customers’ underwriting needs more effectively on a local basis.

EDC has 14 permanent representations located in the world’s fastest growing emerging markets, who are charged with developing relationships with foreign buyers of Canadian goods and services. We connected 2,150 Canadian companies to opportunities in these markets in 2008, 19% more than in 2007.

We added to our network of representations in 2008, placing representatives in Mumbai, Santiago and in Abu Dhabi, to serve the Gulf Cooperation Council (GCC). We announced a representation in Peru that will be established early in 2009, and moved our representative in Kuala Lumpur to Singapore, a key financial hub in Asia. We also established a representative in Beijing to focus exclusively on EDC’s portfolio of equity investments in Asia. We will continue to expand this international network, and by 2010 we plan to have 20 foreign representations in place.

A strong network of partners

EDC has built extensive relationships with a wide range of partners from the private and public sector to better serve the needs of our customers. By leveraging this network in 2008, we were able to enhance market capacity in support of trade and investment, and share information and expertise related to international business.

National Industry Stakeholder Panel: Our National Industry Stakeholder Panel brings together 18 key national business and trade association leaders from across Canada to discuss trade and investment challenges facing business and provide us with feedback on their needs. In 2008 the panel discussed what Canadian companies will need to succeed under the intensifying pressures of global competition, and how EDC can continue to respond to these changing needs.

Partnering with the Public Sector: EDC continued to work with partners from the Government of Canada to raise awareness regarding the services available to Canadian companies. We strengthened our partnership with DFAIT’s Trade Commissioner Service (TCS) through training sessions, providing information about EDC, our solutions and how they can benefit Canadian companies. We also launched the Trade Commissioner Service Partner website to provide a more streamlined process for Trade Commissioners to access information about EDC’s products and services while receiving priority service on their requests.

In 2008, we led a trade mission to the United Arab Emirates and Saudi Arabia in collaboration with Industry Canada, DFAIT, Canada Mortgage and Housing Corporation (CHMC), the Canadian Embassies in Abu Dhabi and Saudi Arabia, and the Canadian Consulate in Dubai. The purpose of the mission was to introduce qualified Canadian companies in construction and related fields to buyers in the Middle East that are involved in the large number of infrastructure projects currently underway in the region.

We also increased collaboration and information sharing with other financial Crown corporations such as the Business Development Bank of Canada (BDC) and the Canadian Commercial Corporation (CCC). Working in partnership with the Trade Commissioner Service, CCC and BDC, we hosted an outbound Heads of Mission training session in 2008 to generate awareness and identify potential areas for collaboration to promote international trade.

In partnership with DFAIT, EDC offers employees the opportunity to participate in a secondment program. Through this partnership, DFAIT employees can spend work terms at EDC, enhancing their technical skills in export trade, and EDC employees have the opportunity to gain front-line experience in a DFAIT foreign assignment. To date, EDC has welcomed two DFAIT employees in work terms, while one EDC employee is currently on assignment abroad for DFAIT.

Our Canadian regional offices work closely with provincial trade groups and officials to promote international trade opportunities and the complementary services available to assist companies. For example, EDC began discussions with Investissement Quebec (IQ) about providing Quebec companies with solutions to finance their Research and Development tax credits.

EDC Annual Report 2008 | 21

Performance vs Objectives

OBJECTIVE 2: FACILITATING INTEGRATI VE TRADE

| | | | | | | | | | | | | | | | | |

| Performance measures | | 2007 Result | | | 2008 Plan | | | 2008 Result | | 2009 Plan |

Business volume | | | | | | | | | | | | | | | | |

| Total business volume ($B)* | | | 70.0 | | | 7% growth | | 23% growth (85.8) | | 8% decline |

| Volume in emerging markets* | | | 16.7 | | | 8% growth | | 31% growth (22.0) | | 5% growth |

Investments facilitated | | | | | | | | | | | | | | | | |

| Volume of foreign investments ($B)* | | | 5.6 | | | 5% decline | | 15.5% decline (4.7) | | 3% growth |

| Number of investment transactions** | | | 329 | | | 12% growth | | 16% growth (383) | | 5% growth |

Partnerships with financial institutions | | | | | | | | | | | | | | | | |

| Partnership volume ($B)* | | | 11.7 | | | 8% growth | | 20% growth (14.1) | | 7% growth |

| Number of partnership transactions*** | | | n/a | | | | | | | | 4,450 | | 6% growth |

| | |

| * | | In 2008, EDC began reporting some of its Credit Insurance volume on a net basis, and began reporting its Political Risk Insurance volume net of reinstatements. Due to these changes in reporting, and in order to provide an appropriate year-over-year comparison, all business volume results for 2007 in this table are shown on a basis consistent with 2008. |

| |

| ** | | The 12% growth rate shown in the table incorporates the original Corporate Plan 30% growth targeted for transactions under the Financing and PRI programs, as well as 5% growth under the ARI program. |

| |

| *** | | The 2008-2012 Corporate Plan indicated that EDC would be introducing a new partnership transaction measure but gave no target at that time. The 2007 Annual Report indicated that Number of partnership transactions would be introduced as a new measure during 2008 with a growth target of 6%. Subsequently, this performance measure was formally introduced in the 2009-2013 Corporate Plan and the 2008 result is the baseline for the 2009 growth rate. |

Integrative trade means that companies separate production processes into a series of activities — such as R&D, procurement, manufacturing, marketing and sales, distribution and logistics, and after-sale support — then locate those activities wherever it is most efficient to do so. Companies use advanced communications technologies and transportation logistics to integrate all these activities into global supply chains. This integration requires companies to invest in operations in foreign markets and/or partner with other companies in order to save costs and get closer to their customers and suppliers.

Maximizing global opportunities

EDC facilitated a total of $85.8 billion in exports and investments in 2008, a 23% increase over 2007 and higher than our forecast. This result was driven by higher demand for EDC’s programs that intensified towards the end of the year as liquidity in the private sector became severely constrained. Record-high commodity prices for much of the year, and the Canadian dollar’s drop in value towards year-end also greatly boosted our export volumes.

It was urgent that we adapt to these circumstances and respond rapidly to our customers’ needs. Helping us to react quickly were changes made at EDC in recent years that we modeled on our customers’ best practices in efficiency and process improvement. Other recent changes also created efficiencies such as our reorganization according to industry sectors and supply chains in which our customers operate.

One-quarter of our total business volume — $22 billion — took place in emerging markets that continue to show strong economic growth and rising demand for the goods and services Canadian companies provide. Business volumes were particularly strong in those emerging markets where we have had permanent representatives in place for several years, reflecting the strong relationships we have developed with foreign buyers of Canadian goods and services.

Brazil, Russia and the Commonwealth of Independent States (CIS), India, China and Mexico remained the priority emerging markets for Canadian companies, and EDC business volumes in those markets totalled $11 billion, a 45% increase over 2007. We expect that new representations established in Chile and the Gulf Cooperation Council (GCC) in 2008 will be instrumental in growing opportunities in those regions for Canadian companies. In 2008, we facilitated $975 million in trade with Chile and a combined $1.3 billion with the United Arab Emirates, Saudi Arabia and Qatar.

Canadian companies are also investing in emerging markets as a means to lower costs, improve productivity, get closer to their customers or to link into the supply chains of their larger partners. Through our financing, credit insurance and political risk insurance programs, we completed 383 transactions in support of Canadian Direct Investment Abroad. Our efforts to increase customer awareness of our foreign affiliate coverage contributed to a 16% increase in investment transactions over 2007. The dollar value of foreign investments declined 15.5% to $4.7 billion in 2008, as some Canadian companies did not pursue or divested themselves of large investments, reducing the total dollar value of the investments facilitated by EDC.

22 | Managing Risk. Maximizing Opportunities.

Maximizing financial capacity

EDC is a key part of the network of financial institutions serving Canadian exporters and investors. Working in partnership with Canadian banks, sureties and other financial institutions worldwide, we add to the financial capacity available to Canadian businesses through a range of financial services including loan and contract bonding guarantees, shared financing, and insurance programs.

The volume of business EDC conducted through these partnerships reached $14.1 billion in 2008, 20% more than in 2007. We also facilitated 4,450 partnership transactions, a new performance measure introduced in 2008 to track our support for mid-market companies and our success at identifying opportunities to partner with private sector financial institutions.

Contributing to these results, our Canadian Financial Intermediaries Group (CFIG) continued its work with Canadian financial institutions to improve their understanding of and access to EDC products and services, and to improve EDC’s own understanding of their needs and expectations and to develop joint business strategies. Our Financial Institutions Team (FIT) also contributed to these results by providing risk management solutions to Canadian banks, which help mitigate their foreign bank counterparty risk in international trade transactions. In that regard, FIT supported 1,501 partnership transactions and partnership volume of $5.4 billion in 2008, 80% more than in 2007 for both measures.

A key partnership initiative of 2008 was the introduction of enhancements to our Export Guarantee Program (EGP) that is designed to encourage financial institutions to advance loans to small- and medium-sized enterprises (SMEs) in Canada. The enhanced EGP increases the coverage we provide to banks that are financing export transactions or investments. The program now provides greater coverage for a broader range of client needs such as financing support for single and multiple export contracts, financing of work in progress and the purchase of equipment related to exports, and margining of foreign accounts receivables, working capital financing for foreign- domiciled inventory, and Canadian Direct Investments abroad. In 2008, reflecting growing demand for this type of support, approximately 314 SMEs benefited from the EGP product, compared to 172 in 2007. The overall guarantee coverage provided in partnership with Canadian financial institutions was valued at over $323 million, an increase from $220 million in 2007. More than 22 financial institutions took advantage of the program to help meet the needs of their clients.

Venture capital and private equity are essential sources of capital for small- and mid-sized enterprises, especially those in new technology sectors. EDC’s Equity Investment Program enables qualified companies to leverage our access to a unique combination of financial tools, expertise and international networks, and acquire the private equity and venture capital they need to grow their export business. EDC adds capacity to domestic private equity firms by investing in a variety of professionally managed funds that provide equity and venture capital to small- and medium-sized companies with fast-growth potential and that are exporting next generation technologies.

We also invest in foreign private equity and infrastructure funds that help us open up new networks of potential partners and customers for Canadian companies. In 2008, 66 Canadian companies benefited from investments made by EDC through our Equity Program. EDC completed approximately $224 million in investment commitments. Of these commitments, $169 million were in international funds, $28 million were in domestic venture capital and $27 million were in domestic middle-market private equity.

EDC Annual Report 2008 | 23

Performance vs Objectives

OBJECTIVE 3: LEVERAGING THE ORGANIZATION

| | | | | | | | | | | | | |

| | | 2007 Result | | 2008 Plan | | 2008 Result | | 2009 Plan |

Performance measures | | | | | | | | | | | | |

| VfM to TCO ratio* | | | 58:42 | | 43:57 | | | 43:57 | | 52:48 |

| Employee engagement** | | rank same as

high-quality organizations | | n/a | | | n/a | | rank same as

high-quality organizations |

| Employee retention (%)*** | | | | 94.88% | | > CB rate | | | | 91.83% | | > CB rate |

| | |

| * | | Value for Money (VfM) — investments in IT that increase business performance. Total cost of ownership (TCO) — the costs of maintaining core business infrastructure and technology assets. |

| |

| ** | | Measured on the climate assessment independently reported by Hay. The next biennial survey will be conducted in 2009. |

| |

| *** | | Conference Board data for financial institutions suggests a rate of 90.4%. |

Our ability to help Canadian companies succeed in international trade is rooted in the strengths of our organization, our knowledge of global markets and our customers, and our ability to provide innovative solutions and to manage risk. We leverage our capital, processes, technology and, most importantly, our people in serving the trade needs of thousands of Canadian companies.

Leveraging capital

Canadian exporters and investors need timely and predictable access to capital or other financial instruments in order to build their business and stay competitive. Our contribution to their growth is directly tied to our ability to manage and assess risk. This was particularly true in 2008, a year when growth slowed dramatically and capital became increasingly difficult to access.

EDC entered the financial downturn with a very strong capital position; our portfolio was well-diversified and our exposure to some of the hardest-hit financial institutions was limited. As a result of this position we were able to take on more risk for our customers and financial partners, serving 11% more companies in 2008. Our Risk Management Office handled 968 transaction approvals in 2008, nearly a third more than in 2007.

To continue to leverage our strong capital position, we also allocate a portion of capital as Strategic Risk Capital (SRC), to support higher-risk opportunities of strategic importance but outside our typical operations.

In 2008, EDC facilitated $1.8 billion of trade and investment through the use of SRC. This was primarily allocated to initiatives that included equity investments, unsecured loans to small businesses, financing to sub-sovereign obligors and transactions in certain emerging markets where the legal and regulatory systems are undeveloped.

Leaner processes, faster response

EDC continuously looks for ways to refine processes and create efficiencies. Throughout 2008, we continued to apply the Lean Methodology to various aspects of our organization, and the impact was significant, specifically with respect to our loans process. After full implementation of the Loans Transformation Project (LTP), which involved a comprehensive streamlining of the lending process, we were able to reduce processing times on loan transactions by about 60% and we were able to service an average of 63% more loan deals.