Exhibit 99(c)(2)

The Seibels Bruce Group, Inc. |

| CONFIDENTIAL |

11.06.03

PRESENTATION TO THE BOARD OF DIRECTORS

This presentation and its analyses are only for the use of the Board of Directors and are not intended to, nor should they be, relied upon by any other party, including shareholders of The Seibels Bruce Group, Inc. The consent of Capitalink is required prior to the disclosure to any third party of this presentation, its analyses, or of the assessments made by Capitalink. These materials are based solely on information contained in publicly available documents and certain other information provided to Capitalink by management and the Board of Directors. Capitalink has not attempted to investigate or verify the accuracy or completeness of such publicly available information or other information provided to Capitalink. Capitalink has relied upon the accuracy and completeness of such publicly available information and other information supplied to Capitalink. These materials are being furnished, and should be considered only in connection with, the oral presentation being provided by Capitalink in connection herewith. The preparation of these materials was completed on November 4, 2003 based on information publicly available or supplied to Capitalink through such date. Capitalink is not obligated to update this presentation or its analyses to reflect any information that becomes publicly available or that is provided to Capitalink after such date.

|

|

|

TABLE OF CONTENTS

|

|

|

|

|

|

|

|

2

TRANSACTION OVERVIEW

3

INTRODUCTION

• The Board of Directors of The Seibels Bruce Group, Inc. (“Seibels” or the “Company”) has retained Capitalink, L.C. (“Capitalink”) as financial advisor and to render an opinion as to the fairness, from a financial point of view, to the Company’s shareholders of a proposal by the Company to undertake a reverse stock split (the “Reverse Split”) in which all shareholders whose shares are converted into less than 1 share in the Reverse Split will receive a per share cash payment (the “Fractional Share Consideration”) (the Reverse Split and the Fractional Share Consideration are collectively the “Transaction”).

• As a result of the Transaction, it is anticipated that there will be less than 300 shareholders of record. Therefore, the Company intends to make the appropriate filings with the United States Securities and Exchange Commission (the “SEC”) and thereafter will no longer be required to file annual and periodic reports under the federal securities laws that are applicable to public companies. Additionally, the Company’s common stock will no longer be traded on the OTC Bulletin Board.

• As of November 4, 2003, there were 7,816,044 shares of the Company’s common stock outstanding.

• The closing price of the Company’s common stock on November 3, 2003 (date presentation materials completed) was $2.00.

4

TRANSACTION RATIONALE

• Public company costs are high:

• Costs associated with retaining public status, servicing shareholders and continuing public communication.

• Additional costs related to Sarbanes-Oxley, increasing D&O insurance expenses and audit costs.

• Time demands on management and employees associated with public status are significant:

• Investor relations and communications.

• Preparing public reports, filings, press releases and Regulation FD compliance.

• Shareholders are unable to benefit fully from public company status due to limited liquidity and micro-cap classification resulting in issues relating to:

• Shareholders ability to move into or out of large positions.

• The Company’s ability to use shares for acquisitions and raise capital in public markets.

• The Company’s attractiveness as an investment vehicle for institutional investors.

• Maintaining the status quo and continuing to bear public company costs do not present any tangible benefits.

• The Transaction provides several benefits:

• Reduces direct and indirect costs.

• Saves management and employee time.

• Small shareholders can exit their investment in the Company at a premium to current market prices.

• Small shareholders are able to sell without a commission.

• Small shareholders can retain ownership by acquiring additional shares.

5

BACKGROUND OF THE TRANSACTION

• At a meeting of the Company’s Board of Directors on May 7, 2003, the Board discussed generally the concept of going private and authorized one of its directors to undertake research on the topic and prepare a report for the Board.

• The Board’s interest in a going private transaction at that time was precipitated by the substantial new internal and external accounting requirements and procedures imposed by the Sarbanes-Oxley legislation that would be expected to have a direct impact on the Company’s 2003 audit. The Company had also received communications from both its securities counsel and accountants about the increased burdens, time and expense the new legislation and related regulations would be expected to impose on public companies.

• During Summer 2003, the Company received an unsolicited letter from an investment banking firm offering to make a presentation and consult with the Board about various possible transactions, including a going private transaction. The Board decided to accept the offered presentation and it was made on August 14, 2003. Based on the information presented at that meeting and consultations with the Company’s accountants and securities lawyers, the Board decided to pursue the possibility of a going private transaction further.

• The Board instructed management to contact other investment bankers and offer them the opportunity to make presentations and bid on offering advisory services. On September 4, 2003, Capitalink and one additional investment banker made presentations along with the original investment banker, and subsequently the Board retained Capitalink to advise it with respect to the Transaction and to render an opinion as to its fairness from a financial point of view.

6

SHAREHOLDER DISTRIBUTION ANALYSIS

• The shareholder distribution analysis provides the Company with data setting forth the number of record holders of its common stock at varying share distributions. The information provides the Board with information to determine the most appropriate ratio necessary to effectuate the Reverse Split in order to reduce the number of record holders to less than 300.

• Information is presented on both a record and beneficial ownership basis. Approximately 1,579,000 shares are owned by shareholders who have not provided the Company with specific shareholding data. Therefore, all beneficial shareholder distribution calculations are estimated.

• It is noted that shareholders owning less than 1,000 shares represent approximately 89.5% and 81.0% of record and beneficial shareholders, respectively, and such holders own approximately only 1.2% and 4.1%, respectively, of the Company’s common stock.

7

(Shares in thousands)

|

| Record Shareholders |

| Benefical Shareholders (1) |

| ||||||||||||||||||||

Share |

| Holders |

| Shares Owned |

| Holders |

| Shares Owned |

| ||||||||||||||||

Distribution |

| Number |

| Cumulative |

| Cum % |

| Number |

| Cumulative |

| Cum % |

| Number |

| Cumulative |

| Cum % |

| Number |

| Cumulative |

| Cum % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0 - 99 |

| 546 |

| 546 |

| 59.1 | % | 14 |

| 14 |

| 0.2 | % | 920 |

| 920 |

| 39.0 | % | 29 |

| 29 |

| 0.4 | % |

100 - 249 |

| 154 |

| 700 |

| 75.8 | % | 24 |

| 38 |

| 0.5 | % | 463 |

| 1,383 |

| 58.7 | % | 69 |

| 98 |

| 1.2 | % |

250 - 499 |

| 81 |

| 781 |

| 84.5 | % | 26 |

| 64 |

| 0.8 | % | 331 |

| 1,714 |

| 72.7 | % | 101 |

| 198 |

| 2.5 | % |

500 - 749 |

| 31 |

| 812 |

| 87.9 | % | 17 |

| 81 |

| 1.0 | % | 144 |

| 1,858 |

| 78.8 | % | 80 |

| 278 |

| 3.6 | % |

750 - 999 |

| 15 |

| 827 |

| 89.5 | % | 12 |

| 93 |

| 1.2 | % | 52 |

| 1,910 |

| 81.0 | % | 41 |

| 319 |

| 4.1 | % |

1,000 - 1,999 |

| 32 |

| 859 |

| 93.0 | % | 43 |

| 137 |

| 1.7 | % | 196 |

| 2,106 |

| 89.3 | % | 232 |

| 552 |

| 7.1 | % |

2,000 - 2,999 |

| 5 |

| 864 |

| 93.5 | % | 11 |

| 148 |

| 1.9 | % | 81 |

| 2,187 |

| 92.7 | % | 177 |

| 728 |

| 9.3 | % |

3,000 - 3,999 |

| 5 |

| 869 |

| 94.0 | % | 16 |

| 164 |

| 2.1 | % | 32 |

| 2,219 |

| 94.1 | % | 102 |

| 831 |

| 10.6 | % |

4,000 - 4,999 |

| 2 |

| 871 |

| 94.3 | % | 10 |

| 173 |

| 2.2 | % | 19 |

| 2,238 |

| 94.9 | % | 81 |

| 912 |

| 11.7 | % |

5,000 - 9,999 |

| 13 |

| 884 |

| 95.7 | % | 83 |

| 256 |

| 3.3 | % | 48 |

| 2,286 |

| 96.9 | % | 288 |

| 1,200 |

| 15.4 | % |

10,000 - 19,999 |

| 8 |

| 892 |

| 96.5 | % | 114 |

| 370 |

| 4.7 | % | 35 |

| 2,321 |

| 98.4 | % | 433 |

| 1,633 |

| 20.9 | % |

20,000 - 29,999 |

| 2 |

| 894 |

| 96.8 | % | 53 |

| 423 |

| 5.4 | % | 5 |

| 2,326 |

| 98.6 | % | 122 |

| 1,755 |

| 22.5 | % |

30,000 - 39,999 |

| 4 |

| 898 |

| 97.2 | % | 142 |

| 565 |

| 7.2 | % | 4 |

| 2,330 |

| 98.8 | % | 138 |

| 1,893 |

| 24.2 | % |

40,000 - 49,999 |

| 1 |

| 899 |

| 97.3 | % | 42 |

| 606 |

| 7.8 | % | 4 |

| 2,334 |

| 99.0 | % | 165 |

| 2,057 |

| 26.3 | % |

50,000 - 74,999 |

| 9 |

| 908 |

| 98.3 | % | 578 |

| 1,185 |

| 15.2 | % | 7 |

| 2,341 |

| 99.3 | % | 434 |

| 2,492 |

| 31.9 | % |

75,000 - 99,999 |

| — |

| 908 |

| 98.3 | % | — |

| 1,185 |

| 15.2 | % | 3 |

| 2,344 |

| 99.4 | % | 258 |

| 2,749 |

| 35.2 | % |

100,000 - 249,999 |

| 9 |

| 917 |

| 99.2 | % | 1,300 |

| 2,485 |

| 31.8 | % | 6 |

| 2,350 |

| 99.7 | % | 900 |

| 3,650 |

| 46.7 | % |

250,000 - 499,999 |

| 4 |

| 921 |

| 99.7 | % | 1,279 |

| 3,764 |

| 48.2 | % | 5 |

| 2,355 |

| 99.9 | % | 1,352 |

| 5,002 |

| 64.0 | % |

500,000 - 999,999 |

| 1 |

| 922 |

| 99.8 | % | 894 |

| 4,658 |

| 59.6 | % | 1 |

| 2,356 |

| 99.9 | % | 529 |

| 5,531 |

| 70.8 | % |

1,000,000 > |

| 2 |

| 924 |

| 100.0 | % | 3,158 |

| 7,816 |

| 100.0 | % | 2 |

| 2,358 |

| 100.0 | % | 2,285 |

| 7,816 |

| 100.0 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 924 |

|

|

|

|

| 7,816 |

|

|

|

|

| 2,358 |

|

|

|

|

| 7,816 |

|

|

|

|

|

(1) Company stock benefit plan is included as one stockholder. In addition, may include shareholders with holdings in multiple accounts.

Sources of information: Company management, American Stock Transfer and CEDE.

8

PRO FORMA SHAREHOLDER AND FRACTIONAL SHARE CONSIDERATION ANALYSIS

• The pro forma shareholder analysis provides data at various split ratios and prices per share relating to (i) the estimated number of record holders remaining subsequent to the Transaction, (ii) the resulting fractional number of shares required to be purchased as part of the Transaction, and (iii) the expected aggregate cost of such Fractional Share Consideration.

9

($ and shares in thousands, except per share)

Reverse |

| Pro Forma Shareholders |

| Pro Forma |

| Pro Forma Aggregate Fractional Share Consideration (1) (2) |

| |||||||||||||||

Split |

| Record |

| Beneficial (1) (2) |

| Purchased (1) |

| $2.75 |

| $2.87 |

| $3.00 |

| $3.12 |

| $3.25 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

100 |

| 378 |

| 1,438 |

| 77 |

| $ | 212 |

| $ | 221 |

| $ | 231 |

| $ | 240 |

| $ | 250 |

|

250 |

| 224 |

| 975 |

| 154 |

| $ | 423 |

| $ | 441 |

| $ | 461 |

| $ | 480 |

| $ | 500 |

|

500 |

| 143 |

| 644 |

| 271 |

| $ | 745 |

| $ | 777 |

| $ | 812 |

| $ | 845 |

| $ | 880 |

|

750 |

| 112 |

| 500 |

| 428 |

| $ | 1,176 |

| $ | 1,228 |

| $ | 1,283 |

| $ | 1,335 |

| $ | 1,390 |

|

1,000 |

| 97 |

| 448 |

| 413 |

| $ | 1,135 |

| $ | 1,185 |

| $ | 1,238 |

| $ | 1,288 |

| $ | 1,341 |

|

2,000 |

| 65 |

| 252 |

| 696 |

| $ | 1,913 |

| $ | 1,997 |

| $ | 2,087 |

| $ | 2,171 |

| $ | 2,261 |

|

(1) Company stock benefit plan is included as one stockholder. In addition, may include shareholders with holdings in multiple accounts.

(2) Range of Fractional Share Consideration is based upon analyses provided hereafter.

Sources of information: Company management, American Stock Transfer and CEDE.

10

PRO FORMA BOOK VALUE AND EARNINGS PER SHARE ANALYSIS

• The pro forma book value analysis provides a range of pro forma net common book value and net tangible common book value per share at various split ratios and ranges of Fractional Share Consideration per share prices.

• It is noted that the minor movement of the net common book value per share subsequent to the Transaction (at both varying levels of the ratio in the Reverse Split and the range of the Fractional Share Consideration) is due to the large number of holders that maintain small shareholdings prior to the Transaction (see the shareholder distribution analysis).

• The pro forma earnings per share analysis provides a pro forma adjusted basic earnings per share (“EPS”) for the latest twelve month (“LTM”) period ended September 30, 2003 and the year ended December 31, 2002 at various split ratios.

11

($ and shares in thousands, except per share)

|

|

|

| Reverse Split |

| Pro Forma |

| Pro Forma Value Per Share at Fractional Share Consideration (1) (2) |

| ||||||||||||||

$ 2.75 |

| $ 2.87 |

| $ 3.00 |

| $ 3.12 |

| $ 3.25 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Net Common Book Value as of Sept 30, 2003 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Net Common Book Value |

| $ | 23,085 |

| 100 |

| 7,739 |

| $ | 2.96 |

| $ | 2.95 |

| $ | 2.95 |

| $ | 2.95 |

| $ | 2.95 |

|

Shares Outstanding |

| 7,816 |

| 250 |

| 7,662 |

| $ | 2.96 |

| $ | 2.96 |

| $ | 2.95 |

| $ | 2.95 |

| $ | 2.95 |

| |

Net Common Book Value per Share |

| $ | 2.95 |

| 500 |

| 7,545 |

| $ | 2.96 |

| $ | 2.96 |

| $ | 2.95 |

| $ | 2.95 |

| $ | 2.94 |

|

|

|

|

| 750 |

| 7,388 |

| $ | 2.97 |

| $ | 2.96 |

| $ | 2.95 |

| $ | 2.94 |

| $ | 2.94 |

| |

|

|

|

| 1,000 |

| 7,403 |

| $ | 2.96 |

| $ | 2.96 |

| $ | 2.95 |

| $ | 2.94 |

| $ | 2.94 |

| |

|

|

|

| 2,000 |

| 7,120 |

| $ | 2.97 |

| $ | 2.96 |

| $ | 2.95 |

| $ | 2.94 |

| $ | 2.92 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Net Tangible Common Book Value as of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Net Tangible Common Book Value |

| $ | 19,272 |

| 100 |

| 7,739 |

| $ | 2.46 |

| $ | 2.46 |

| $ | 2.46 |

| $ | 2.46 |

| $ | 2.46 |

|

Shares Outstanding |

| 7,816 |

| 250 |

| 7,662 |

| $ | 2.46 |

| $ | 2.46 |

| $ | 2.45 |

| $ | 2.45 |

| $ | 2.45 |

| |

Net Tangible Common Book Value per Share |

| $ | 2.47 |

| 500 |

| 7,545 |

| $ | 2.46 |

| $ | 2.45 |

| $ | 2.45 |

| $ | 2.44 |

| $ | 2.44 |

|

|

|

|

| 750 |

| 7,388 |

| $ | 2.45 |

| $ | 2.44 |

| $ | 2.43 |

| $ | 2.43 |

| $ | 2.42 |

| |

|

|

|

| 1,000 |

| 7,403 |

| $ | 2.45 |

| $ | 2.44 |

| $ | 2.44 |

| $ | 2.43 |

| $ | 2.42 |

| |

|

|

|

| 2,000 |

| 7,120 |

| $ | 2.44 |

| $ | 2.43 |

| $ | 2.41 |

| $ | 2.40 |

| $ | 2.39 |

| |

(1) Company stock benefit plan is included as one stockholder. In addition, may include shareholders with holdings in multiple accounts.

(2) Range of Fractional Share Consideration is based upon analyses provided hereafter.

Sources of information: Company management, American Stock Transfer and CEDE.

12

|

|

|

| Reverse |

| Pro Forma |

| Pro Forma |

| ||

|

|

|

|

|

|

|

|

|

| ||

Basic Earnings Per Share for LTM September 30, 2003 |

|

|

|

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

| ||

Adjusted Net Income |

| $ | (2,379 | ) | 100 |

| 7,739 |

| $ | (0.31 | ) |

Weighted Average Shares Outstanding |

| 7,674 |

| 250 |

| 7,662 |

| $ | (0.31 | ) | |

Adjusted Earnings (Loss) per Share |

| $ | (0.31 | ) | 500 |

| 7,545 |

| $ | (0.32 | ) |

|

|

|

| 750 |

| 7,388 |

| $ | (0.32 | ) | |

|

|

|

| 1,000 |

| 7,403 |

| $ | (0.32 | ) | |

|

|

|

| 2,000 |

| 7,120 |

| $ | (0.33 | ) | |

|

|

|

|

|

|

|

|

|

| ||

Basic Earnings Per Share for FYE December 31, 2002 |

|

|

|

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

| ||

Adjusted Net Income |

| $ | 2,302 |

| 100 |

| 7,739 |

| $ | 0.30 |

|

Weighted Average Shares Outstanding |

| 7,832 |

| 250 |

| 7,662 |

| $ | 0.30 |

| |

Adjusted Earnings (Loss) per Share |

| $ | 0.29 |

| 500 |

| 7,545 |

| $ | 0.31 |

|

|

|

|

| 750 |

| 7,388 |

| $ | 0.31 |

| |

|

|

|

| 1,000 |

| 7,403 |

| $ | 0.31 |

| |

|

|

|

| 2,000 |

| 7,120 |

| $ | 0.32 |

| |

(1) Company stock benefit plan is included as one stockholder. In addition, may include shareholders with holdings in multiple accounts.

Sources of information: Company management, American Stock Transfer and CEDE.

13

SCOPE OF ENGAGEMENT

• In arriving at its analysis and opinion, Capitalink took into account its assessment of general economic, market and financial conditions as well as its experience in connection with similar transactions and securities valuations generally and, among other things:

• Reviewed documents relating to the Transaction.

• Reviewed publicly available financial information and other data with respect to the Company, including the Annual Report on Form 10-K for the fiscal year ended December 31, 2002, and the draft Quarterly Report on Form 10-Q for the nine months ended September 30, 2003.

• Reviewed and analyzed a range of Fractional Share Consideration at various different possible per share prices, a range of pro forma shares outstanding at various different Reverse Split a range of ratios, a range of pro forma common book values per share and a range of pro forma earnings per share.

• Reviewed and analyzed the Company’s projected unlevered free cash flows and prepared discounted cash flows.

• Reviewed and analyzed certain financial characteristics of companies that were deemed to have characteristics comparable to those of the Company.

• Reviewed and analyzed certain financial characteristics of comparable transactions that involved the acquisition of companies that were deemed to have characteristics comparable to those of the Company.

• Reviewed and analyzed recent transaction premiums paid in going-private transactions involving a reverse stock split.

• Reviewed and analyzed the premiums implied by the Fractional Share Consideration.

• Reviewed and discussed with representatives of the management of the Company certain financial and operating information furnished by them, including financial analyses and projections and related assumptions with respect to the business, operations and prospects of the Company.

• Considered the historical financial results and present financial condition of the Company.

• Reviewed certain publicly available information concerning the trading of, and the trading market for, the common stock of the Company.

• Inquired about and discussed the Transaction and other matters related thereto with Company management, the Board of Directors and its legal counsel.

• Performed such other analyses and examinations as were deemed appropriate.

14

• The Capitalink analysis and opinion are necessarily based upon market, economic and other conditions, as they exist on, and could be evaluated as of November 6, 2003. Accordingly, although subsequent developments may affect its opinion, Capitalink does not assume any obligation to update, review or reaffirm its opinion.

• Capitalink assumes that the Transaction will be consummated substantially in accordance with the terms set forth, without any further amendments thereto, and without waiver by the Company of any of the conditions to any obligations or in the alternative that any such amendments, revisions or waivers thereto will not be detrimental to the Company or the shareholders of the Company.

• Capitalink has relied upon and assumed the accuracy and completeness of all of the financial and other information that was used by it without assuming any responsibility for any independent verification of any such information and has further relied upon the assurances of Company management that it is not aware of any facts or circumstances that would make any such information inaccurate or misleading. With respect to the financial projections utilized, Capitalink assumed that such projections have been reasonably prepared on a basis reflecting the best currently available estimates and judgments, and that such projections provide a reasonable basis upon which it could make its analysis and form an opinion.

• Capitalink has not made a physical inspection of the properties and facilities of the Company and has not made or obtained any evaluations or appraisals of the assets and liabilities (contingent or otherwise) of the Company.

• Capitalink assumed that the Transaction will be consummated in a manner that complies in all respects with the applicable provisions of the Securities Act of 1933, as amended, the Securities Exchange Act of 1934, as amended, and all other applicable federal and state statutes, rules and regulations. In addition, based upon discussions with the Company, it is assumed that the receipt of the Fractional Share Consideration will be a taxable event to the Company’s shareholders that receive such consideration.

• Capitalink has not been requested to opine as to, and the opinion does not in any manner address, the underlying business decision of the Company to proceed with or affect the Transaction.

15

• Capitalink was not asked to consider, and its opinion does not address, the relative merits of the Transaction as compared to any alternative business strategy that might exist for the Company. Capitalink was not engaged to seek alternatives to the Transaction that might exist for the Company.

• The opinion is for the use and benefit of the Board of Directors in connection with its consideration of the Transaction and is not intended to be and does not constitute a recommendation to any shareholder of the Company as to how such shareholder should vote with respect to the Transaction. We do not express any opinion as to the underlying valuation or future performance of the Company or the price at which the Company’s common stock would trade at any time in the future.

16

17

SUMMARY

• Seibels, a South Carolina corporation, is a provider of a wide range of services to the insurance industry, as well as a provider of automobile, flood and other property and casualty insurance products.

• The Company is a holding company for four property and casualty insurance companies that offer commercial and non-standard automobile insurance. In addition, Seibels offers claim administration services to insurance companies and other businesses through Insurance Network Services, Inc. (“INS”), flood zone determination and related services through America’s Flood Services, Inc. (“AFS”), and managing general agency services through Seibels, Bruce & Company (“SBC”).

• The Company seeks to balance its fee-based operations with selective risk underwriting in an effort to increase value for its shareholders, agents and employees by pursuing growth with an element of limited risk exposure. The Company’s risk-bearing property and casualty insurance operations include non-standard automobile, commercial lines and workers’ compensation.

• The Company’s operations can be described within five main categories:

• Automobile – Includes Universal Insurance Company’s (“UIC”) retained risk nonstandard automobile and run-off premium finance operations, Catawba Insurance Company’s (“Catawba”) retained risk non-owners and non-standard automobile programs, the runoff of the Company’s retained risk Nashville and South Carolina automobile operations, and the fee-based NC Facility, SC Facility and South Carolina Associated Auto Insurers Plan operations.

• Flood – Includes the fee-based flood zone determinations and flood zone mapping services of AFS, and the fee based flood insurance agency of AFS.

• Commercial – Includes the retained risk commercial operations of Catawba and UIC, the fee-based commercial automobile activity for the NC Facility and SC Facility, and the runoff retained risk commercial operations of South Carolina Insurance Company.

18

• Adjusting Services – Includes all the fee-based operations of INS, a full claims organization that conducts automobile appraisals, catastrophe claims adjusting and glass claim services

• Other – Includes various runoff risk bearing environmental, workers compensation programs, and the fee-based managing general agency services of SBC.

• INS’ primary operation includes the claim administration services to QualSure Holdings Corporation, under a reduced rate contract that expires from October 4, 2005 through January 21, 2010. The Company is currently seeking to renew this contract on more favorable terms and/or seek other similar contracts in different regions.

• In January 2002, the Company issued two workers compensation insurance master policies to Human Dynamics Corporation (“HDC”), a professional employment organization. The Company did not obtain the approval of the South Carolina Department of Insurance (“SCDOI”) prior to issuing the master policies and therefore subsequently canceled them. Litigation was brought against the Company by HDC for breach of contract, good faith and fair dealing and is seeking actual and punitive damages. Litigation is currently ongoing with the Company presenting numerous counterclaims.

• In August 2002, the SCDOI issued an order imposing administrative supervision for at least six months as a result of the disputes associated with the HDC program. Provisions of the administrative order provided for the Company’s subsidiaries to immediately cease writing risk-bearing business and to immediately cease renewal of existing risk-bearing business.

• In September 2002, the SCDOI provided approval to Catawba to write new and renewal premiums on both automobile and commercial lines of business in the states of South Carolina, Georgia and Tennessee. Additional approval was given to UIC to renew the North Carolina commercial lines businesses of SCIC. However, Catawba’s application to the Kentucky Department of Insurance was withdrawn and this business is currently being runoff.

19

• In November 2002, the Company sold the renewal rights to its National Flood Insurance Program (“NFIP”) business to The Hartford Financial Services Group, Inc (“Hartford”) for $3.8 million. Provisions of the underlying sales agreement provide that Hartford administer the Company’s business to the NFIP over the transition period that ends September 30, 2003.

• The Company’s operations have reduced significantly over the past year as a result of the SCDOI Order, the sale of its NFIP book of business, the runoff of its managing general agent operations, the final runoff of the SC Facility and the SCAAIP, and the loss of its commercial lines business in the state of Kentucky. The Company has been forced to scale back its operations significantly, and is currently exploring opportunities for additional sources of revenue. This includes gaining approval to write additional lines of insurance in both South Carolina and North Carolina, and to obtain additional claims-adjusting service contracts in other regions.

• In April 2003, the Company announced an odd-lot tender offer for shareholders with less than 100 shares at $2.50 per share. The tender offer was completed on July 31, 2003 with 15,646 shares purchased.

• In November 2003, the Company entered into letters of intent with unaffiliated third parties pursuant to which the Company will sell 100% of the common stock of South Carolina Insurance Company and Consolidated American Insurance Company. These transactions are subject to due diligence, approval by the respective board of directors and approval by the SCDOI.

• Capitalink noted several general factors to be considered in connection with the status of Seibels as a publicly traded company:

• The Company’s common stock historically has a limited trading volume and therefore a lack of liquidity for the Company’s shareholders.

• The Company is not part of a high-growth industry that attracts investor interest and a high trading multiple.

20

• The Company has a significant number of shareholders with small holdings in the Company’s stock. The cost of servicing the large number of shareholders are high relative to the size of their holdings and the market valuation of the Company.

• The Company has not realized the benefits of public company status (i.e., ability to raise capital, use of stock as currency in acquisitions), but incurs the increased expenses necessary to comply with reporting requirements and other public company obligations.

21

22

• Capitalink reviewed the Company’s historical and draft financial data for the five fiscal years (“FY”) ended December 31, 2002, and the nine months ended September 30, 2003. In addition, Capitalink reviewed the Company’s projections for the FY ending December 31, 2004 through December 31, 2008.

• The Company’s revenues and earnings are adjusted to remove any unusual or extraordinary sources of revenue and expenses. The adjustments provide a more accurate portrayal of the Company’s underlying earnings.

• Seibels’s revenues are derived from four main sources: (i) net premium revenue from the writing of premiums for the automobile, commercial and homeowners markets, (ii) commission and service income, (iii) investment income, and (iv) other income which includes various run-off risk bearing activities. For the nine months ended September 30, 2003, net premiums and commission and service income made up 45.1% and 46.2%, respectively of total adjusted revenue.

• The Company’s revenue streams (as a percentage of total revenue for the nine months ended September 30, 2003) can also be grouped into five main categories; (i) automobile-35.1%, (ii) flood-9.5%, (iii) commercial-24.5%, (iv) adjusting services-16.8%, and (v) other-3.8%.

• Revenue for the Company fell significantly over the reviewed period – from a high of $108.3 million in FY1999 to $29.4 million for the LTM ended September 30, 2003. The fall in revenues was primarily due to several factors including the discontinuation of two of its unprofitable, nonstandard automobile insurance operations in Nashville (Graward) and South Carolina. In addition, the sale of the Company’s NFIP business, the discontinuation of the HDC workers compensation program and other unprofitable service lines, and the Company’s problems with respect to the SCDOI administrative order, have also contributed to the fall in revenues and earnings.

• The Company’s adjusted earning before interest, taxes, depreciation and amortization (“EBITDA”) has been extremely volatile over the past five years and has ranged from a high of $4.8 million for FY2001 to $(3.9) million for FY2000. The EBITDA for the LTM ended September 30, 2003 was $(1.2) million. The Company’s losses in FY2000 were primarily attributable to the unprofitable nonstandard automobile insurance operations in Nashville and South Carolina, which have since been discontinued.

23

• On March 28, 2002, the Company issued $8.0 million in adjustable rate cumulative non-voting, non-convertible, non-redeemable preferred special stock to Charles H. Powers, the Company’s Chairman and Chief Executive Officer. As of September 30, 2003, the Company had no other interest bearing obligations.

• In connection with a potential new investment in a Florida based operation, the Company has negotiated a new $2.5 million credit facility. In addition, the Company expects to fund the Transaction from an additional credit facility.

• The Company’s net premiums written to surplus ratio has been relatively low and has ranged from a high of 1.72 times in FY1999 to 0.28 times for the LTM period ended September 30, 2003. Although the low ratio suggests the significant ability of the Company to write additional insurance policies, it is understated on an aggregate basis because of the significant portion of the Company’s operations derived from commission and fees.

• The Company’s average loss ratio has also fallen significantly from a high of 110.7% for FY1998 to 53.4% for the LTM period ended September 30, 2003. The improvement in the loss ratio is caused by steps taken by the Company, to discontinue unprofitable lines of business.

• The Company’s common shareholders equity has also improved significantly from $11.9 million as of December 31, 2000 to $23.1 million as of September 30, 2003. The improvement in the Company’s common shareholders equity is primarily a result of several unusual items including the gain on the sale of stock in Insurance Services Offices, Inc. of $2.1 million, the gain on the sale to Hartford, and the sale and leaseback of the corporate office building.

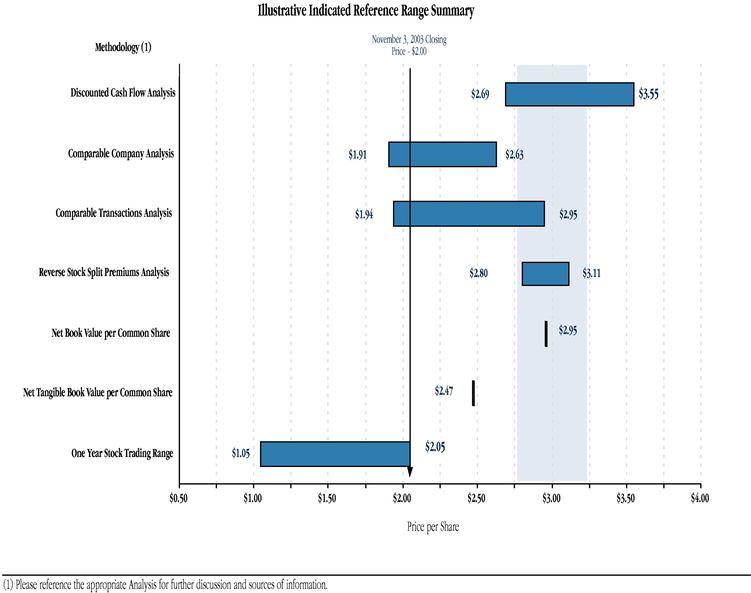

• The Company’s net book value and net tangible book value per share as of September 30, 2003 was $2.95 and $2.47, respectively.

24

Normalized Comparative Summary Income Statements

($ in thousands except per share)

|

| for years ended December 31, |

| for the 9 months ended |

| LTM |

| ||||||||||||||||||

|

| 1998 |

| 1999 |

| 2000 |

| 2001 |

| 2002 |

| 2002 |

| 2003 |

| 2003 |

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Net Premiums |

| $ | 22,775 |

| $ | 53,344 |

| $ | 25,137 |

| $ | 14,433 |

| $ | 15,661 |

| $ | 20,726 |

| $ | 11,443 |

| $ | 6,378 |

|

Commission and Service Income |

| 49,298 |

| 45,652 |

| 35,890 |

| 36,272 |

| 33,853 |

| 26,490 |

| 11,701 |

| 19,064 |

| ||||||||

Investment Income |

| 4,699 |

| 4,558 |

| 4,593 |

| 3,205 |

| 2,843 |

| 1,769 |

| 1,452 |

| 2,526 |

| ||||||||

Other |

| 4,645 |

| 4,779 |

| 4,502 |

| 2,767 |

| 1,398 |

| 737 |

| 758 |

| 1,419 |

| ||||||||

Total Revenue |

| 81,417 |

| 108,333 |

| 70,122 |

| 56,677 |

| 53,755 |

| 49,722 |

| 25,354 |

| 29,387 |

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Losses and Loss Adjustment Expenses |

| 25,223 |

| 46,010 |

| 24,445 |

| 7,740 |

| 9,434 |

| 15,164 |

| 9,137 |

| 3,407 |

| ||||||||

Policy Acquisition Costs |

| 10,222 |

| 33,721 |

| 25,003 |

| 23,162 |

| 22,814 |

| 18,600 |

| 7,307 |

| 11,521 |

| ||||||||

Other Operating Costs and Expenses |

| 46,823 |

| 34,885 |

| 26,461 |

| 21,438 |

| 18,625 |

| 13,547 |

| 11,328 |

| 16,406 |

| ||||||||

Total Operating Expenses |

| 82,268 |

| 114,616 |

| 75,909 |

| 52,340 |

| 50,873 |

| 47,311 |

| 27,772 |

| 31,334 |

| ||||||||

Operating Income (Loss) |

| (851 | ) | (6,283 | ) | (5,787 | ) | 4,337 |

| 2,882 |

| 2,411 |

| (2,418 | ) | (1,947 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Interest Income (Expense) |

| (981 | ) | (1,216 | ) | (1,436 | ) | (728 | ) | (180 | ) | (164 | ) | (9 | ) | (25 | ) | ||||||||

Pre-tax Income (Loss) |

| (1,832 | ) | (7,499 | ) | (7,223 | ) | 3,609 |

| 2,702 |

| 2,247 |

| (2,427 | ) | (1,972 | ) | ||||||||

Income Tax (Benefit) |

| (85 | ) | 37 |

| — |

| 30 |

| (30 | ) | (30 | ) | 15 |

| 15 |

| ||||||||

After-tax Income (Loss) |

| (1,747 | ) | (7,536 | ) | (7,223 | ) | 3,579 |

| 2,732 |

| 2,277 |

| (2,442 | ) | (1,987 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Preferred Stock dividends |

| (160 | ) | (168 | ) | (168 | ) | (161 | ) | (430 | ) | (323 | ) | (285 | ) | (392 | ) | ||||||||

Normalized Net Income to Common |

| $ | (1,907 | ) | $ | (7,704 | ) | $ | (7,391 | ) | $ | 3,418 |

| $ | 2,302 |

| $ | 1,954 |

| $ | (2,727 | ) | $ | (2,379 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Normalized EBIT |

| $ | (851 | ) | $ | (6,283 | ) | $ | (5,787 | ) | $ | 4,337 |

| $ | 2,882 |

| $ | 2,411 |

| $ | (2,418 | ) | $ | (1,947 | ) |

Total Depreciation & Amortization |

| $ | 2,115 |

| $ | 2,552 |

| $ | 1,847 |

| $ | 496 |

| $ | 488 |

| $ | 391 |

| $ | 626 |

| $ | 723 |

|

Normalized EBITDA |

| $ | 1,264 |

| $ | (3,731 | ) | $ | (3,940 | ) | $ | 4,833 |

| $ | 3,370 |

| $ | 2,802 |

| $ | (1,792 | ) | $ | (1,224 | ) |

Capital Expenditures, net of Disposals (CAPEX, net) |

| $ | 1,392 |

| $ | 1,506 |

| $ | 212 |

| $ | 581 |

| $ | 655 |

| $ | 655 |

| $ | 253 |

| $ | 253 |

|

Normalized EBITDA - CAPEX |

| $ | (128 | ) | $ | (5,237 | ) | $ | (4,152 | ) | $ | 4,252 |

| $ | 2,715 |

| $ | 2,147 |

| $ | (2,045 | ) | $ | (1,477 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Earnings per Share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Basic Normalized EPS |

| $ | (0.25 | ) | $ | (0.99 | ) | $ | (0.94 | ) | $ | 0.44 |

| $ | 0.29 |

| $ | 0.25 |

| $ | (0.35 | ) | $ | (0.31 | ) |

Basic Reported EPS |

| $ | (0.39 | ) | $ | (0.99 | ) | $ | (1.98 | ) | $ | 0.54 |

| $ | 0.73 |

| $ | 0.64 |

| $ | 0.04 |

| $ | 0.13 |

|

Weighted Average Shares Outstanding (thousands) |

| 7,763 |

| 7,774 |

| 7,832 |

| 7,832 |

| 7,832 |

| 7,832 |

| 7,825 |

|

|

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Diluted Normalized EPS |

| $ | (0.25 | ) | $ | (0.99 | ) | $ | (0.94 | ) | $ | 0.42 |

| $ | 0.28 |

| $ | 0.24 |

| $ | (0.35 | ) | $ | (0.31 | ) |

Diluted Reported EPS |

| $ | (0.39 | ) | $ | (0.99 | ) | $ | (1.98 | ) | $ | 0.51 |

| $ | 0.70 |

| $ | 0.61 |

| $ | 0.04 |

| $ | 0.13 |

|

Weighted Average Shares Outstanding (thousands) |

| 7,763 |

| 7,774 |

| 7,832 |

| 8,206 |

| 8,088 |

| 8,164 |

| 7,854 |

|

|

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Normalizing Reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Restructuring/Goodwill Impairment |

| $ | (546 | ) | $ | — |

| $ | — |

| $ | — |

| $ | — |

| $ | — |

| $ | (700 | ) | $ | (700 | ) |

Other Unusual (Expense) Gain Items |

| — |

| — |

| (8,138 | ) | 787 |

| 3,391 |

| 3,041 |

| 3,779 |

| 4,129 |

| ||||||||

Income Tax Shelter (Charge) from Unusual Items |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| ||||||||

Unusual (Expense) Gain Items, net of Taxes |

| (546 | ) | — |

| (8,138 | ) | 787 |

| 3,391 |

| 3,041 |

| 3,079 |

| 3,429 |

| ||||||||

Accounting Changes, net of Taxes |

| (601 | ) | — |

| — |

| — |

| — |

| — |

| — |

| — |

| ||||||||

Total Reconciling Items, net of Taxes |

| $ | (1,147 | ) | $ | — |

| $ | (8,138 | ) | $ | 787 |

| $ | 3,391 |

| $ | 3,041 |

| $ | 3,079 |

| $ | 3,429 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Reported Income Tax (Benefit) |

| $ | (85 | ) | $ | 37 |

| $ | — |

| $ | 30 |

| $ | (30 | ) | $ | (30 | ) | $ | 15 |

| $ | 15 |

|

Reported Net Income (Loss) to Common |

| $ | (3,054 | ) | $ | (7,704 | ) | $ | (15,529 | ) | $ | 4,205 |

| $ | 5,693 |

| $ | 4,995 |

| $ | 352 |

| $ | 1,050 |

|

Comprehensive Gain/(Loss) |

| $ | 860 |

| $ | (1,512 | ) | $ | 962 |

| $ | 777 |

| $ | 557 |

| $ | 776 |

| $ | (450 | ) | $ | (669 | ) |

Reported Comprehensive Net Income (Loss) to Common |

| $ | (2,194 | ) | $ | (9,216 | ) | $ | (14,567 | ) | $ | 4,982 |

| $ | 6,250 |

| $ | 5,771 |

| $ | (98 | ) | $ | 381 |

|

Sources of information: Company financial statements and management

25

Normalized Common Sized Summary Income Statements

|

| for years ended December 31, |

| for the 9 months ended |

| LTM |

| ||||||||||

|

| 1998 |

| 1999 |

| 2000 |

| 2001 |

| 2002 |

| 2002 |

| 2003 |

| 2003 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Premiums |

| 28.0 | % | 49.2 | % | 35.8 | % | 25.5 | % | 29.1 | % | 41.7 | % | 45.1 | % | 21.7 | % |

Commission and Service Income |

| 60.6 | % | 42.1 | % | 51.2 | % | 64.0 | % | 63.0 | % | 53.3 | % | 46.2 | % | 64.9 | % |

Investment Income |

| 5.8 | % | 4.2 | % | 6.6 | % | 5.7 | % | 5.3 | % | 3.6 | % | 5.7 | % | 8.6 | % |

Other |

| 5.7 | % | 4.4 | % | 6.4 | % | 4.9 | % | 2.6 | % | 1.5 | % | 3.0 | % | 4.8 | % |

Total Revenue |

| 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Losses and Loss adjustment expenses |

| 31.0 | % | 42.5 | % | 34.9 | % | 13.7 | % | 17.5 | % | 30.5 | % | 36.0 | % | 11.6 | % |

Policy Acquisition Costs |

| 12.6 | % | 31.1 | % | 35.7 | % | 40.9 | % | 42.4 | % | 37.4 | % | 28.8 | % | 39.2 | % |

Other Operating Costs and Expenses |

| 57.5 | % | 32.2 | % | 37.7 | % | 37.8 | % | 34.6 | % | 27.2 | % | 44.7 | % | 55.8 | % |

Total Operating Expenses |

| 101.0 | % | 105.8 | % | 108.3 | % | 92.3 | % | 94.6 | % | 95.2 | % | 109.5 | % | 106.6 | % |

Operating Income (Loss) |

| -1.0 | % | -5.8 | % | -8.3 | % | 7.7 | % | 5.4 | % | 4.8 | % | -9.5 | % | -6.6 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest Income (Expense) |

| -1.2 | % | -1.1 | % | -2.0 | % | -1.3 | % | -0.3 | % | -0.3 | % | 0.0 | % | -0.1 | % |

Pre-tax Income (Loss) |

| -2.3 | % | -6.9 | % | -10.3 | % | 6.4 | % | 5.0 | % | 4.5 | % | -9.6 | % | -6.7 | % |

Income Tax (Benefit) |

| -0.1 | % | 0.0 | % | 0.0 | % | 0.1 | % | -0.1 | % | -0.1 | % | 0.1 | % | 0.1 | % |

After-tax Income (Loss) |

| -2.1 | % | -7.0 | % | -10.3 | % | 6.3 | % | 5.1 | % | 4.6 | % | -9.6 | % | -6.8 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preferred Stock dividends |

| -0.2 | % | -0.2 | % | -0.2 | % | -0.3 | % | -0.8 | % | -0.6 | % | -1.1 | % | -1.3 | % |

Normalized Net Income to Common |

| -2.3 | % | -7.1 | % | -10.5 | % | 6.0 | % | 4.3 | % | 3.9 | % | -10.8 | % | -8.1 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Normalized EBIT |

| -1.0 | % | -5.8 | % | -8.3 | % | 7.7 | % | 5.4 | % | 4.8 | % | -9.5 | % | -6.6 | % |

Total Depreciation & Amortization |

| 2.6 | % | 2.4 | % | 2.6 | % | 0.9 | % | 0.9 | % | 0.8 | % | 2.5 | % | 2.5 | % |

Normalized EBITDA |

| 1.6 | % | -3.4 | % | -5.6 | % | 8.5 | % | 6.3 | % | 5.6 | % | -7.1 | % | -4.2 | % |

Capital Expenditures, net of Disposals (CAPEX, net) |

| 1.7 | % | 1.4 | % | 0.3 | % | 1.0 | % | 1.2 | % | 1.3 | % | 1.0 | % | 0.9 | % |

Normalized EBITDA - CAPEX |

| -0.2 | % | -4.8 | % | -5.9 | % | 7.5 | % | 5.1 | % | 4.3 | % | -8.1 | % | -5.0 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Normalizing Reconciliation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Restructuring/Goodwill Impairment |

| 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % |

Other Unusual (Expense) Gain Items |

| -0.7 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | -2.8 | % | -2.4 | % |

Income Tax Shelter (Charge) from Unusual Items |

| 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % |

Unusual (Expense) Gain Items, net of Taxes |

| -0.7 | % | 0.0 | % | -11.6 | % | 1.4 | % | 6.3 | % | 6.1 | % | 12.1 | % | 11.7 | % |

Accounting Changes, net of Taxes |

| -0.7 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % |

Discontinued Operations, net of Taxes |

| 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % |

Extraordinary Items, net of Taxes |

| 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % | 0.0 | % |

Total Reconciling Items, net of Taxes |

| -1.4 | % | 0.0 | % | -11.6 | % | 1.4 | % | 6.3 | % | 6.1 | % | 12.1 | % | 11.7 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reported Income Tax (Benefit) |

| -0.1 | % | 0.0 | % | 0.0 | % | 0.1 | % | -0.1 | % | -0.1 | % | 0.1 | % | 0.1 | % |

Reported Net Income (Loss) to Common |

| -3.8 | % | -7.1 | % | -22.1 | % | 7.4 | % | 10.6 | % | 10.0 | % | 1.4 | % | 3.6 | % |

Comprehensive Gain/(Loss) |

| 1.1 | % | -1.4 | % | 1.4 | % | 1.4 | % | 1.0 | % | 1.6 | % | -1.8 | % | -2.3 | % |

Reported Comprehensive Net Income (Loss) to Common |

| -3.8 | % | -7.1 | % | -22.1 | % | 7.4 | % | 10.6 | % | 10.0 | % | 1.4 | % | 1.3 | % |

Sources of information: Company financial statements and management

26

Comparative Summary Balance Sheets

($ in thousands, except per share)

|

| as of December 31, |

| as of September 30, |

| |||||||||||||||||

|

| 1998 |

| 1999 |

| 2000 |

| 2001 |

| 2002 |

| 2002 |

| 2003 |

| |||||||

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Cash & Equivalents |

| $ | 23,141 |

| $ | 26,722 |

| $ | 10,410 |

| $ | 6,375 |

| $ | 10,423 |

| $ | 5,561 |

| $ | 8,711 |

|

Investments |

| 41,109 |

| 32,892 |

| 38,297 |

| 39,499 |

| 39,216 |

| 41,305 |

| 39,272 |

| |||||||

Premium Receivables |

| 19,334 |

| 11,591 |

| 6,897 |

| 6,272 |

| 3,492 |

| 3,511 |

| 4,743 |

| |||||||

Reinsurance Recoverable on Paid Losses & LAE |

| 29,972 |

| 18,528 |

| 14,031 |

| 10,246 |

| 7,289 |

| 10,121 |

| 6,739 |

| |||||||

Reinsurance Recoverable on Unpaid Losses & LAE |

| 83,654 |

| 74,017 |

| 50,012 |

| 40,832 |

| 30,786 |

| 33,991 |

| 28,078 |

| |||||||

Prepaid Reinsurance Premiums |

| 59,619 |

| 56,724 |

| 40,997 |

| 36,548 |

| 30,224 |

| 35,000 |

| 8,844 |

| |||||||

Deferred Policy Acquisition Costs |

| 2,472 |

| 1,373 |

| 400 |

| 1,200 |

| 1,168 |

| 1,525 |

| 1,490 |

| |||||||

Property & Equipment |

| 6,028 |

| 5,421 |

| 917 |

| 807 |

| 993 |

| 1,146 |

| 699 |

| |||||||

Intangible Assets, net |

| 20,892 |

| 19,876 |

| 4,638 |

| 4,513 |

| 4,513 |

| 4,513 |

| 3,813 |

| |||||||

Other Assets |

| 9,342 |

| 7,659 |

| 4,067 |

| 4,346 |

| 5,570 |

| 12,460 |

| 2,568 |

| |||||||

Total Assets |

| $ | 295,563 |

| $ | 254,803 |

| $ | 170,666 |

| $ | 150,638 |

| $ | 133,674 |

| $ | 149,133 |

| $ | 104,957 |

|

Liabilities & Stockholders’ Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Loss and Loss Adjustment Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Reported & Est. Claims & Losses - Retained |

| $ | 28,950 |

| $ | 34,733 |

| $ | 30,574 |

| $ | 21,334 |

| $ | 18,857 |

| $ | 25,857 |

| $ | 19,260 |

|

Reported & Est. Claims & Losses - Ceded |

| 74,746 |

| 67,904 |

| 46,612 |

| 38,785 |

| 29,717 |

| 32,753 |

| 27,417 |

| |||||||

Adj Expenses - Retained |

| 7,372 |

| 5,100 |

| 5,247 |

| 4,709 |

| 4,067 |

| 5,175 |

| 3,849 |

| |||||||

Adj Expenses - Ceded |

| 8,908 |

| 6,113 |

| 3,400 |

| 2,047 |

| 1,069 |

| 1,238 |

| 661 |

| |||||||

Unearned Premiums - Retained |

| 12,919 |

| 5,796 |

| 5,056 |

| 6,116 |

| 6,134 |

| 7,232 |

| 6,918 |

| |||||||

Unearned Premiums - Ceded |

| 59,619 |

| 56,724 |

| 40,997 |

| 36,548 |

| 30,224 |

| 35,000 |

| 8,844 |

| |||||||

Accounts Payable & Accrued Expenses |

| 39,024 |

| 20,460 |

| 4,592 |

| 3,372 |

| 3,158 |

| 5,632 |

| 1,449 |

| |||||||

Interest Bearing Debt |

| 16,250 |

| 14,986 |

| 10,159 |

| 7,721 |

| — |

| — |

| — |

| |||||||

Other Liabilities |

| 9,487 |

| 13,730 |

| 9,337 |

| 10,442 |

| 9,224 |

| 5,501 |

| 5,474 |

| |||||||

Total Liabilities |

| 257,275 |

| 225,546 |

| 155,974 |

| 131,074 |

| 102,450 |

| 118,388 |

| 73,872 |

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Preferred Stock |

| 2,700 |

| 2,700 |

| 2,700 |

| 2,590 |

| 8,000 |

| 8,000 |

| 8,000 |

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Common Stockholders’ Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Common Stock |

| 7,773 |

| 7,831 |

| 7,832 |

| 7,832 |

| 7,832 |

| 7,832 |

| 7,816 |

| |||||||

Paid in Capital |

| 61,861 |

| 61,988 |

| 61,989 |

| 61,989 |

| 61,989 |

| 61,989 |

| 61,964 |

| |||||||

Accumulated Earnings (Deficit) |

| (34,046 | ) | (43,262 | ) | (57,829 | ) | (52,847 | ) | (46,597 | ) | (47,076 | ) | (46,695 | ) | |||||||

Total Stockholders’ Equity |

| 35,588 |

| 26,557 |

| 11,992 |

| 16,974 |

| 23,224 |

| 22,745 |

| 23,085 |

| |||||||

|

| $ | 295,563 |

| $ | 254,803 |

| $ | 170,666 |

| $ | 150,638 |

| $ | 133,674 |

| $ | 149,133 |

| $ | 104,957 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Common Shares Outstanding (thousands) |

| 7,773 |

| 7,831 |

| 7,832 |

| 7,832 |

| 7,832 |

| 7,832 |

| 7,816 |

| |||||||

Book Value per Common Share |

| $ | 4.58 |

| $ | 3.39 |

| $ | 1.53 |

| $ | 2.17 |

| $ | 2.97 |

| $ | 2.90 |

| $ | 2.95 |

|

Tangible Book Value Per Common Share |

| $ | 1.89 |

| $ | 0.85 |

| $ | 0.94 |

| $ | 1.59 |

| $ | 2.39 |

| $ | 2.33 |

| $ | 2.47 |

|

Sources of information: Company financial statements and management

27

Common Sized Summary Balance Sheets

|

| as of December 31, |

| as of September 30, |

| ||||||||||

|

| 1998 |

| 1999 |

| 2000 |

| 2001 |

| 2002 |

| 2002 |

| 2003 |

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash & Equivalents |

| 7.8 | % | 10.5 | % | 6.1 | % | 4.2 | % | 7.8 | % | 3.7 | % | 8.3 | % |

Investments |

| 13.9 | % | 12.9 | % | 22.4 | % | 26.2 | % | 29.3 | % | 27.7 | % | 37.4 | % |

Premium Receivables |

| 6.5 | % | 4.5 | % | 4.0 | % | 4.2 | % | 2.6 | % | 2.4 | % | 4.5 | % |

Reinsurance Recoverable on Paid Losses & LAE |

| 10.1 | % | 7.3 | % | 8.2 | % | 6.8 | % | 5.5 | % | 6.8 | % | 6.4 | % |

Reinsurance Recoverable on Unpaid Losses & LAE |

| 28.3 | % | 29.0 | % | 29.3 | % | 27.1 | % | 23.0 | % | 22.8 | % | 26.8 | % |

Prepaid Reinsurance Premiums |

| 20.2 | % | 22.3 | % | 24.0 | % | 24.3 | % | 22.6 | % | 23.5 | % | 8.4 | % |

Deferred Policy Acquisition Costs |

| 0.8 | % | 0.5 | % | 0.2 | % | 0.8 | % | 0.9 | % | 1.0 | % | 1.4 | % |

Property & Equipment |

| 2.0 | % | 2.1 | % | 0.5 | % | 0.5 | % | 0.7 | % | 0.8 | % | 0.7 | % |

Intangible Assets, net |

| 7.1 | % | 7.8 | % | 2.7 | % | 3.0 | % | 3.4 | % | 3.0 | % | 3.6 | % |

Other Assets |

| 3.2 | % | 3.0 | % | 2.4 | % | 2.9 | % | 4.2 | % | 8.4 | % | 2.4 | % |

Total Assets |

| 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % |

Liabilities & Stockholders’ Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loss and Loss Adjustment Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reported & Est. Claims & Losses - Retained |

| 9.8 | % | 13.6 | % | 17.9 | % | 14.2 | % | 14.1 | % | 17.3 | % | 18.4 | % |

Reported & Est. Claims & Losses - Ceded |

| 25.3 | % | 26.6 | % | 27.3 | % | 25.7 | % | 22.2 | % | 22.0 | % | 26.1 | % |

Adj Expenses - Retained |

| 2.5 | % | 2.0 | % | 3.1 | % | 3.1 | % | 3.0 | % | 3.5 | % | 3.7 | % |

Adj Expenses - Ceded |

| 3.0 | % | 2.4 | % | 2.0 | % | 1.4 | % | 0.8 | % | 0.8 | % | 0.6 | % |

Unearned Premiums - Retained |

| 4.4 | % | 2.3 | % | 3.0 | % | 4.1 | % | 4.6 | % | 4.8 | % | 6.6 | % |

Unearned Premiums - Ceded |

| 20.2 | % | 22.3 | % | 24.0 | % | 24.3 | % | 22.6 | % | 23.5 | % | 8.4 | % |

Accounts Payable & Accrued Expenses |

| 13.2 | % | 8.0 | % | 2.7 | % | 2.2 | % | 2.4 | % | 3.8 | % | 1.4 | % |

Interest Bearing Debt |

| 5.5 | % | 5.9 | % | 6.0 | % | 5.1 | % | 0.0 | % | 0.0 | % | 0.0 | % |

Other Liabilities |

| 3.2 | % | 5.4 | % | 5.5 | % | 6.9 | % | 6.9 | % | 3.7 | % | 5.2 | % |

Total Liabilities |

| 87.0 | % | 88.5 | % | 91.4 | % | 87.0 | % | 76.6 | % | 79.4 | % | 70.4 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preferred Stock |

| 0.9 | % | 1.1 | % | 1.6 | % | 1.7 | % | 6.0 | % | 5.4 | % | 7.6 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common Stockholders’ Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common Stock |

| 2.6 | % | 3.1 | % | 4.6 | % | 5.2 | % | 5.9 | % | 5.3 | % | 7.4 | % |

Paid in Capital |

| 20.9 | % | 24.3 | % | 36.3 | % | 41.2 | % | 46.4 | % | 41.6 | % | 59.0 | % |

Accumulated Earnings (Deficit) |

| -11.5 | % | -17.0 | % | -33.9 | % | -35.1 | % | -34.9 | % | -31.6 | % | -44.5 | % |

Total Stockholders’ Equity |

| 12.0 | % | 10.4 | % | 7.0 | % | 11.3 | % | 17.4 | % | 15.3 | % | 22.0 | % |

|

| 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % |

Sources of information: Company financial statements and management

28

Comparative Financial Analysis

($ in thousands, except per share)

|

| as of & for years ended December 31, |

| as of & for the 9 months ended |

| as of & for LTM |

| ||||||||||||||||||

1998 |

| 1999 |

| 2000 |

| 2001 |

| 2002 | 2002 |

| 2003 | 2003 | |||||||||||||

Financial Review |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Revenue |

| $ | 81,417 |

| $ | 108,333 |

| $ | 70,122 |

| $ | 56,677 |

| $ | 53,755 |

| $ | 49,722 |

| $ | 25,354 |

| $ | 29,387 |

|

Total Operating Expenses |

| $ | 82,268 |

| $ | 114,616 |

| $ | 75,909 |

| $ | 52,340 |

| $ | 50,873 |

| $ | 47,311 |

| $ | 27,772 |

| $ | 31,334 |

|

Operating Income |

| $ | (851 | ) | $ | (6,283 | ) | $ | (5,787 | ) | $ | 4,337 |

| $ | 2,882 |

| $ | 2,411 |

| $ | (2,418 | ) | $ | (1,947 | ) |

Pre-tax Income (Loss) |

| $ | (1,832 | ) | $ | (7,499 | ) | $ | (7,223 | ) | $ | 3,609 |

| $ | 2,702 |

| $ | 2,247 |

| $ | (2,427 | ) | $ | (1,972 | ) |

Normalized Net Income (Loss) |

| $ | (1,907 | ) | $ | (7,704 | ) | $ | (7,391 | ) | $ | 3,418 |

| $ | 2,302 |

| $ | 1,954 |

| $ | (2,727 | ) | $ | (2,379 | ) |

Normalized EBIT |

| $ | (851 | ) | $ | (6,283 | ) | $ | (5,787 | ) | $ | 4,337 |

| $ | 2,882 |

| $ | 2,411 |

| $ | (2,418 | ) | $ | (1,947 | ) |

Normalized EBITDA |

| $ | 1,264 |

| $ | (3,731 | ) | $ | (3,940 | ) | $ | 4,833 |

| $ | 3,370 |

| $ | 2,802 |

| $ | (1,792 | ) | $ | (1,224 | ) |

Normalized Basic EPS |

| $ | (0.25 | ) | $ | (0.99 | ) | $ | (0.94 | ) | $ | 0.44 |

| $ | 0.29 |

| $ | 0.25 |

| $ | (0.35 | ) | $ | (0.31 | ) |

Normalized Diluted EPS |

| $ | (0.25 | ) | $ | (0.99 | ) | $ | (0.94 | ) | $ | 0.42 |

| $ | 0.28 |

| $ | 0.24 |

| $ | (0.35 | ) | $ | (0.31 | ) |

Total Assets |

| $ | 295,563 |

| $ | 254,803 |

| $ | 170,666 |

| $ | 150,638 |

| $ | 133,674 |

| $ | 149,133 |

| $ | 104,957 |

| $ | 104,957 |

|

Net Worth |

| $ | 35,588 |

| $ | 26,557 |

| $ | 11,992 |

| $ | 16,974 |

| $ | 23,224 |

| $ | 22,745 |

| $ | 23,085 |

| $ | 23,085 |

|

Tangible Net Worth |

| $ | 14,696 |

| $ | 6,681 |

| $ | 7,354 |

| $ | 12,461 |

| $ | 18,711 |

| $ | 18,232 |

| $ | 19,272 |

| $ | 19,272 |

|

Total Interest Bearing Debt |

| $ | 18,950 |

| $ | 17,686 |

| $ | 12,859 |

| $ | 10,311 |

| $ | 8,000 |

| $ | 8,000 |

| $ | 8,000 |

| $ | 8,000 |

|

Total Capitalization |

| $ | 54,538 |

| $ | 44,243 |

| $ | 24,851 |

| $ | 27,285 |

| $ | 31,224 |

| $ | 30,745 |

| $ | 31,085 |

| $ | 31,085 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Financial Strength |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Net Premiums Written to Surplus |

| na |

| 1.72 |

| 1.30 |

| 1.00 |

| 0.78 |

| na |

| na |

| 0.28 |

| ||||||||

Total Liabilities to Net Worth |

| 722.9 | % | 849.3 | % | 1300.7 | % | 772.2 | % | 441.1 | % | 520.5 | % | 320.0 | % | 320.0 | % | ||||||||

Total Interest Bearing Debt to Net Worth |

| 53.2 | % | 66.6 | % | 107.2 | % | 60.7 | % | 34.4 | % | 35.2 | % | 34.7 | % | 34.7 | % | ||||||||

Total Interest Bearing Debt to Total Capitalization |

| 34.7 | % | 40.0 | % | 51.7 | % | 37.8 | % | 25.6 | % | 26.0 | % | 25.7 | % | 25.7 | % | ||||||||

Interest Expense to Interest Bearing Debt |

| 5.2 | % | 6.9 | % | 11.2 | % | 7.1 | % | 2.3 | % | 2.1 | % | 0.1 | % | 0.3 | % | ||||||||

Total Interest Bearing Debt to Normalized EBITDA |

| 15.0 |

| na |

| na |

| 2.1 |

| 2.4 |

| 2.9 |

| na |

| na |

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Effectiveness and Efficiency |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Premiums Receivable Turnover |

| na |

| 3.4 |

| 2.7 |

| 2.2 |

| 3.2 |

| 4.2 |

| 2.8 |

| 1.5 |

| ||||||||

Asset Turnover |

| na |

| 0.4 |

| 0.3 |

| 0.4 |

| 0.4 |

| 0.3 |

| 0.2 |

| 0.2 |

| ||||||||

Days Sales Outstanding |

| na |

| 105.8 |

| 134.2 |

| 166.5 |

| 113.8 |

| 64.4 |

| 98.2 |

| 236.2 |

| ||||||||

Days Payable Outstanding |

| na |

| 94.7 |

| 60.2 |

| 27.8 |

| 23.4 |

| 26.0 |

| 22.6 |

| 41.2 |

| ||||||||

Normalized EBIT to Average Assets |

| na |

| -2.3 | % | -2.7 | % | 2.7 | % | 2.0 | % | na |

| na |

| -1.5 | % | ||||||||

Normalized EBIT to Net Worth |

| na |

| -20.2 | % | -30.0 | % | 29.9 | % | 14.3 | % | na |

| na |

| -8.5 | % | ||||||||

Normalized EBITDA to Average Assets |

| na |

| -1.4 | % | -1.9 | % | 3.0 | % | 2.4 | % | na |

| na |

| -1.0 | % | ||||||||

Normalized EBITDA to Net Worth |

| na |

| -12.0 | % | -20.4 | % | 33.4 | % | 16.8 | % | na |

| na |

| -5.3 | % | ||||||||

Normalized Net Income to Average Assets |

| na |

| -2.8 | % | -3.5 | % | 2.1 | % | 1.6 | % | na |

| na |

| -1.9 | % | ||||||||

Normalized Net Income to Net Worth |

| na |

| -24.8 | % | -38.3 | % | 23.6 | % | 11.5 | % | na |

| na |

| -10.4 | % | ||||||||

Net Investment Yield |

| na |

| 7.4 | % | 8.5 | % | 6.8 | % | 6.0 | % | na |

| na |

| 5.2 | % | ||||||||

Loss Ratio |

| 110.7 | % | 86.3 | % | 97.2 | % | 53.6 | % | 60.2 | % | 73.2 | % | 79.8 | % | 53.4 | % | ||||||||

Sources of information: Company financial statements and management

29

|

| as of & for years ended December 31, |

| as of & for the 9 months ended |

| as of & for LTM |

| ||||||||||

|

| 1998 |

| 1999 |

| 2000 |

| 2001 |

| 2002 |

| 2002 |

| 2003 |

| 2003 |

|

Profitability Ratios (as % of Revenue) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loss & Loss Adjustment Expenses |

| 31.0 | % | 42.5 | % | 34.9 | % | 13.7 | % | 17.5 | % | 30.5 | % | 36.0 | % | 11.6 | % |

Total Operating Expenses |

| 101.0 | % | 105.8 | % | 108.3 | % | 92.3 | % | 94.6 | % | 95.2 | % | 109.5 | % | 106.6 | % |

Operating Income |

| -1.0 | % | -5.8 | % | -8.3 | % | 7.7 | % | 5.4 | % | 4.8 | % | -9.5 | % | -6.6 | % |

Pre-tax Income (Loss) |

| -2.3 | % | -6.9 | % | -10.3 | % | 6.4 | % | 5.0 | % | 4.5 | % | -9.6 | % | -6.7 | % |

Normalized Net Income (Loss) |

| -2.3 | % | -7.1 | % | -10.5 | % | 6.0 | % | 4.3 | % | 3.9 | % | -10.8 | % | -8.1 | % |

Normalized EBIT |

| -1.0 | % | -5.8 | % | -8.3 | % | 7.7 | % | 5.4 | % | 4.8 | % | -9.5 | % | -6.6 | % |

Normalized EBITDA |

| 1.6 | % | -3.4 | % | -5.6 | % | 8.5 | % | 6.3 | % | 5.6 | % | -7.1 | % | -4.2 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Growth Rates |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

| na |

| na |

| -13.9 | % | -19.2 | % | -5.2 | % | na |

| -49.0 | % | -45.3 | % |

Operating Income |

| na |

| na |

| na |

| na |

| -33.5 | % | na |

| -200.3 | % | -167.6 | % |

Pre-tax Income (Loss) |

| na |

| na |

| na |

| na |

| -25.1 | % | na |

| -208.0 | % | -173.0 | % |

Normalized Net Income (Loss) |

| na |

| na |

| na |

| na |

| -32.7 | % | na |

| -239.6 | % | -203.3 | % |

Normalized EBIT |

| na |

| na |

| na |

| na |

| -33.5 | % | na |

| -200.3 | % | -167.6 | % |

Normalized EBITDA |

| na |

| na |

| -411.7 | % | na |

| -30.3 | % | na |

| -164.0 | % | -136.3 | % |

Normalized Basic EPS |

| na |

| na |

| na |

| na |

| -34.1 | % | na |

| -240.0 | % | -206.9 | % |

Normalized Diluted EPS |

| na |

| na |

| na |

| na |

| -33.3 | % | na |

| -245.8 | % | -210.7 | % |

Total Assets |

| na |

| na |

| -42.3 | % | -11.7 | % | -11.3 | % | na |

| -29.6 | % | -21.5 | % |

Net Worth |

| na |

| na |

| -66.3 | % | 41.5 | % | 36.8 | % | na |

| 1.5 | % | -0.6 | % |

Tangible Net Worth |

| na |

| na |

| -50.0 | % | 69.4 | % | 50.2 | % | na |

| 5.7 | % | 3.0 | % |

CAPEX, net |

| na |

| na |

| -84.8 | % | 174.1 | % | 12.7 | % | na |

| -61.4 | % | -61.4 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cumulative Average Growth Rate (CAGR) Statistics |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

| na |

| 33.1 | % | -7.2 | % | -11.4 | % | -9.9 | % | na |

| na |

| na |

|

Operating Income |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

|

Pre-tax Income (Loss) |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

|

Normalized Net Income (Loss) |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

|

Normalized EBIT |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

|

Normalized EBITDA |

| na |

| na |

| na |

| 56.4 | % | 27.8 | % | na |

| na |

| na |

|

Normalized Basic EPS |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

|

Normalized Diluted EPS |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

| na |

|

Total Assets |

| na |

| -13.8 | % | -24.0 | % | -20.1 | % | -18.0 | % | na |

| na |

| na |

|

Net Worth |

| na |

| -25.4 | % | -42.0 | % | -21.9 | % | -10.1 | % | na |

| na |

| na |

|

Tangible Net Worth |

| na |

| -54.5 | % | -29.3 | % | -5.4 | % | 6.2 | % | na |

| na |

| na |

|

CAPEX, net |

| na |

| 8.2 | % | -61.0 | % | -25.3 | % | -17.2 | % | na |

| na |

| na |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation & Capital Spending |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation to CAPEX, net |

| 151.9 | % | 169.5 | % | 871.2 | % | 85.4 | % | 74.5 | % | 59.7 | % | 247.4 | % | 285.8 | % |

CAPEX, net to Revenue |

| 1.7 | % | 1.4 | % | 0.3 | % | 1.0 | % | 1.2 | % | 1.3 | % | 1.0 | % | 0.9 | % |

Sources of information: Company financial statements and management

30

Selected Normalized Income Statement Graphs

($ in thousands, except per share)

| |

|

|

|

|

|

|

|

|

Sources of information: Company financial statements and management

31

Selected Normalized Profitability Cost (as % of Revenue) Graphs

|

|

|

|

|

|

|

|

32

Selected Normalized Financial Strength Graphs

($ in thousands)

|

|

|

|

|

|

Sources of information: Company financial statements and management

33

Selected Normalized Efficiency Graphs

|

|

|

|

|

|

|

|

|

|

Sources of information: Company financial statements and management

34

COMPANY MARKET PERFORMANCE

35

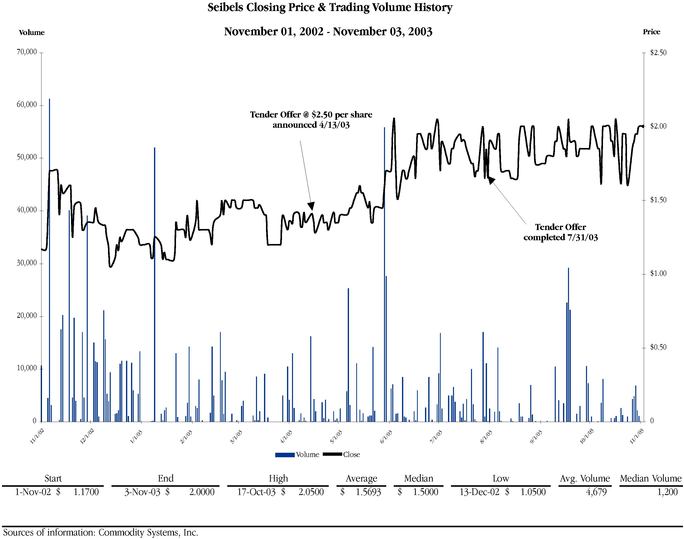

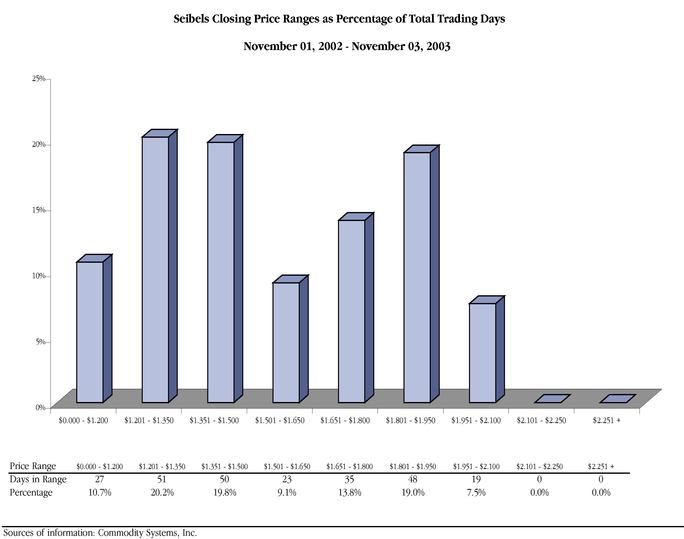

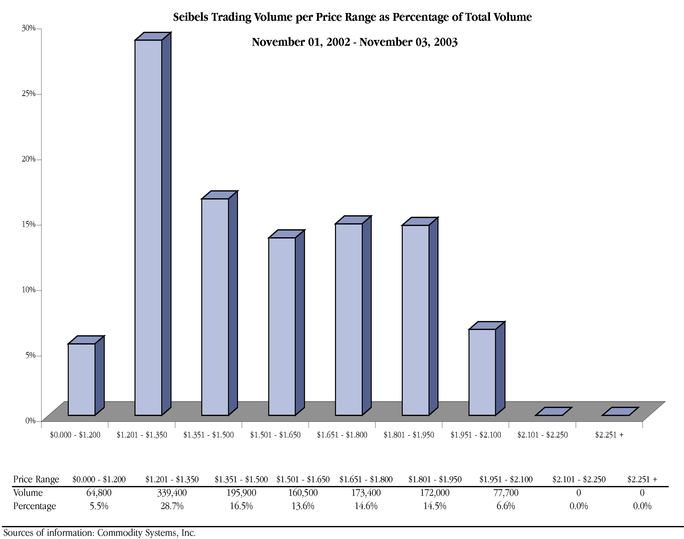

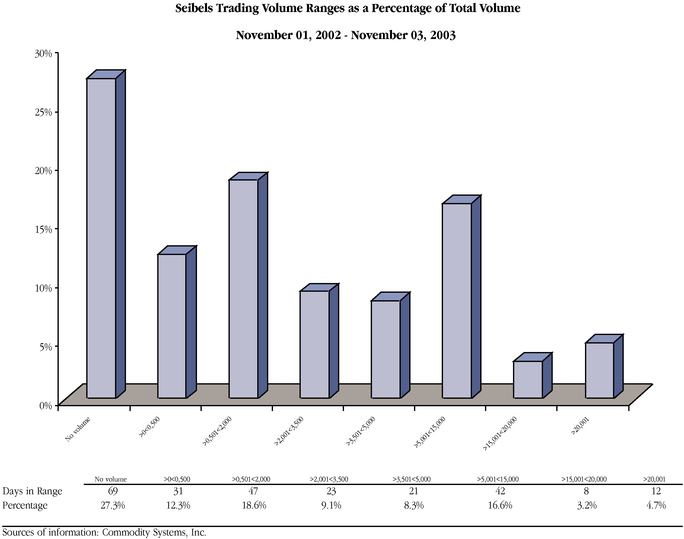

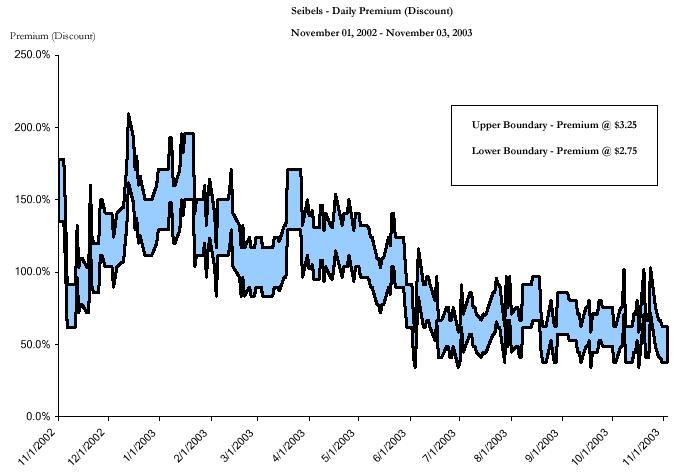

• Capitalink reviewed the daily closing market price and trading volume of the Company’s common stock over the one-year period ended November 3, 2003.