Table of Contents

January 4, 2011

VIA EDGAR

Ms. Kimberly Browning

Securities and Exchange Commission

Division of Investment Management

100 F Street, N.E.

Mailstop 4720, Washington, D.C. 20549

| Re: | Barrett Opportunity Fund, Inc. (the “Fund”) Responses to Comments on Post-Effective Amendment No. 39 to Registration Statement on Form N-1, filed on October 29, 2010 Securities Act File No. 2-63023; Investment Company Act File No. 811-2884 |

Dear Ms. Browning:

This letter responds to comments from the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) on the above-referenced Post-Effective Amendment (the “Amendment”) filed by the Fund that you provided in phone conversations with me on December 22, 2010. For ease of reference, the substance of the comments has been restated below, followed by the Fund’s response. All capitalized terms used but not defined in this letter have the meanings given to them in Amendment No. 39.

General

| 1. | Please file a “Tandy” representation with your response to the following comments. |

In response to the Staff’s comment, the Fund has included Tandy representations at the end of this comment response letter.

Prospectus

| 2. | Disclosure under “Investment Objectives” on page 1 of the prospectus states “These investment objectives may be changed without shareholder approval.” This sentence should be moved from this section to the “Principal Investment Strategies” section. In addition, please state the Fund’s policy, if any, regarding notifying shareholders prior to a change of investment objective. |

In response to the Staff’s comment, the Fund has moved the above-referenced sentence under “Principal Investment Objectives” to “Principal Investment Strategies” on page 2 of the prospectus.

In addition, in response to the Staff’s comment, the Fund has revised page 2 of the prospectus to state:

“The fund’s investment objectives are not fundamental and may be changed by the Board of Directors upon 60 days’ written notice to holders of the fund’s common shares.”

Batterymarch • Brandywine Global • ClearBridge Advisors • Legg Mason Capital Management • Legg Mason Global Equities Group

Permal • Private Capital Management • Royce & Associates • Western Asset Management

Table of Contents

| 3. | The word “accompanying” should be deleted from the lead-in sentence under “Fees and Expenses of the Fund” on page 1 of the prospectus. |

In response to the Staff’s comment, the Fund has deleted the word “accompanying” from the lead-in sentence under “Fees and Expenses of the Fund” on page 2 of the prospectus.

| 4. | The Annual Fund Operating Expenses table should have been completed prior to filing the 485(a). Without this information in the table, the prospectus is incomplete on its face. |

The Fund advises the Staff that final audited financial statements for the Fund’s most recently completed fiscal year were not available as of the time of the Amendment. In response to the Staff’s comment, the Fund has provided the Staff supplementally, as correspondence dated December 22, 2010, a copy of the completed “Fee Table” and “Example” and accompanying footnotes.

| 5. | Please revise the “Example” under “Fees and Expenses of the Fund” to conform to Item 3 of Form N-1A. In particular, the third bullet under this section which states “You reinvest all distributions and dividends without a sales charge” goes beyond the confines of Item 3. In addition, the heading titled “Number of Years You Own Your Shares” is not permitted by Form N-1A. “Your costs would be” that appears in the Example table should also be deleted because it is repetitive. |

In response to the Staff’s comment, the Fund has revised the “Example” under the section titled “Fees and Expenses of the Fund” pursuant to Item 3 of Form N-1A by removing the third bullet under this section and adding the following language after the Example: “The Example does not reflect sales charges (loads) on reinvested dividends (and other distributions). If these sales charges (loads) were included, your costs would be higher.”

The Fund has also removed “Your costs would be” and “Number of Years You Own Your Shares” that previously appeared in the Example table.

| 6. | Please revise the use of open-ended terms including “such as”, “including”, “a variety of” and “all types”. The disclosure should list in complete detail all of the securities that should be listed as part of the Fund’s principal investment strategies. Examples of the use of this type of open ended terminology include: |

| • | The first sentence in the Principal Investment Strategies section which begins on page 1 of the filing: “The fund invests primarily in common stocks and securities convertible into or exchangeable for common stocksuch as convertible preferred stock or convertible debt securities.” (emphasis added) |

| • | The disclosure in Item 9 under “Equity Investments” which reads “Subject to its particular investment policies, the fund may invest inall types of equity securities.” (emphasis added) |

| • | The disclosure under Derivatives and Hedging Techniques which reads “The fund may engage ina variety of transactions using derivatives, such as options on securities and securities indexes.” (emphasis added) |

The Fund respectfully submits that the use of examples and qualifying phrases such as “a variety of” helps the reader better understand the information provided and indicates the breadth of a policy or strategy, without indicating that the examples are exclusive.

| 7. | Please note that disclosure under Item 4 of Form N-1A should list a summary of all types of securities in which the Fund may invest and their attendant risks and that disclosure under Item 9 should include additional detail, but that the Fund is not permitted to introduce new information in Item 9 that is not previously disclosed under Item 4 in asummary fashion. Please revise the prospectus such that the disclosure under Items 4 and 9 correspond in this way. |

2

Table of Contents

The Fund respectfully submits that the current disclosure is consistent with the requirements of Form N-1A. The Fund’s principal investment strategies and risks are described in full in the prospectus in “More on the fund’s investment strategies, investments and risks.” The Fund does not believe that breaking the section into additional subsections would be useful to the investor when the principal strategies are already summarized in the summary section of the prospectus.

| 8. | Please revise the heading “More on the Fund’s Investment Strategies, Investments and Risks” to state “More on the Fund’s Principal Investment Strategies, Investments and Risks.” Note that only information on principal investment strategies, investments and risks is permitted in this section, as only information which is truly principal to the Fund’s investment strategy should be disclosed under Items 4 and 9 of Form N-1A. The Staff advises that the Fund may choose to include a section in the prospectus clearly labeled “Non-Principal Investment Strategies.” |

As described in the response to Item 7 above, the Fund respectfully submits that the current disclosure is consistent with the requirements of Form N-1A. The Fund’s principal investment strategies and risks are described in full in the prospectus in “More on the fund’s investment strategies, investments and risks.” The Fund does not believe that breaking the section into additional subsections would be useful to the investor when the principal strategies are already summarized in the summary section of the prospectus.

| 9. | Disclosure in the third paragraph under “More on the Fund’s Investment Strategies, Investments and Risks” on page 6 of the prospectus states “The fund may invest up to 5% of its net assets in fixed-income securities that are high yield, lower quality securities rated by a rating organization below its top four long-term rating categories…” Please note that the Staff typically considers 20% or more in any one type of security to be “principal”. Please confirm whether or not the fund is limited to 5% in junk bonds and if so, remove the disclosure from the section on principal investment strategies. Please also confirm that all of the investments listed in this section are principal investment strategies. If not, disclosure on certain items should be relocated to a section on non-principal investment strategies and their attendant risks. |

The Fund confirms that it is limited to investing 5% of its net assets in junk bonds. The Fund is permitted to invest without limit in fixed-income securities, including junk bonds, and has revised the disclosure in the section titled “Principal Investment Strategies” to read as follows: “The fund may also invest without limit in fixed-income securities (including up to 5% of its net assets in fixed-income securities that are high yield, lower quality securities rated by a rating organization below its top four long-term rating categories (i.e., below investment grade securities, commonly referred to as “junk bonds”)) or unrated securities determined by the manager to be of equivalent quality. “As described in the Fund’s responses to Items 7 and 8 above, the Fund respectfully submits that the remaining disclosure is consistent with the requirements of Form N-1A.

| 10. | Disclosure under “Principal Investment Strategies” on page 2 of the prospectus states “The fund may invest without limit in foreign securities and American Depository Receipts that are publicly traded in the United States and up to 5% of its net assets in foreign securities that are not publicly traded in the United States.” Please confirm whether or not the fund could also invest without limit in securities of U.S. issuers. If so, please provide relevant disclosure in this section of the prospectus. In addition, please clarify whether the ADRs in which the Fund is permitted to invest are sponsored, unsponsored or both and disclose any attendant risks. With respect to the 5% limit cited in this Item 11, please confirm in your response that this is a principal investment strategy. |

3

Table of Contents

The Fund confirms that it is permitted to invest without limit in securities of U.S. issuers. The Fund has revised the disclosure in the section titled “Principal Investment Strategies” to read as follows: “The fund may invest without limit in securities of issuers located in the United States, as well as in other securities that are publicly traded in the United States, including sponsored American Depositary Receipts. The fund may invest up to 5% of its net assets in foreign securities that are not publicly traded in the United States.”

The Fund has also added the following disclosure to “Foreign investments risk” under the heading “More on Risks of Investing in the Fund” on page 8 of the prospectus: “Generally, American Depositary Receipts (“ADRs”), in registered form, are denominated in U.S. dollars and are designed for use in the domestic market. Usually issued by a U.S. bank or trust company, ADRs are receipts that demonstrate ownership of underlying foreign securities. For purposes of the fund’s investment policies and limitations, ADRs are considered to have the same characteristics as the securities underlying them. ADRs may be sponsored or unsponsored; issuers of securities underlying unsponsored ADRs are not contractually obligated to disclose material information in the United States. Accordingly, there may be less information available about such issuers than there is with respect to domestic companies and issuers of securities underlying sponsored ADRs.”

As described in the Fund’s responses to Items 7, 8 and 9 above, the Fund respectfully submits that the remaining disclosure is consistent with the requirements of Form N-1A.

| 11. | Disclosure under “Selection Process” on page 7 of the prospectus states “The manager evaluates companies of all sizes – from established large capitalization companies to young start-up companies.” If this is a principal investment strategy of the Fund, please disclose that large cap, small cap, mid cap and micro cap companies are principal investment strategies and the attendant risks of each of those types of companies. |

The Fund has revised the disclosure under the sub-section titled “Selection Process” under the heading “More on the Fund’s Investment Strategies, Investments and Risks” to read: “While the manager evaluates companies of all sizes, as a principal investment strategy, the fund intends to invest primarily in companies with large- and mid-capitalizations (normally, $1 billion in market capitalization and above).” As described in the Fund’s responses to Items 7, 8, 9 and 10 above, the Fund respectfully submits that the remaining disclosure is consistent with the requirements of Form N-1A.

| 12. | Disclosure under “Foreign investments risk” on page 3 of the prospectus states that “Foreign countries in which the fund may invest may have markets that are less liquid and more volatile than U.S. markets and may suffer from political or economic instability.” To the extent the manager has identified any particular countries that fall under this description, such countries should be disclosed along with their attendant risks. In addition, please disclose any investments in emerging markets, if any, along with the attendant risks of such investments. |

The Fund intends to invest primarily in developed countries and has no current intention to invest in emerging markets issuers. The Fund’s management has not identified any particular country or countries upon which its investment strategy will focus. The Fund respectfully submits that the purpose of this disclosure is to highlight the different risk profiles of U.S. and non-U.S. issuers and is in compliance with the requirements of Form N-1A.

| 13. | Please revise the first paragraph under “Performance” on page 4 of the prospectus in accordance with Item 4(b)(2)(i) to include specific references to 1-, 5- and 10-year performance numbers. In addition, please move the paragraph following the “Average Annual Total Returns” table to follow the heading which appears on page 4 of the prospectus. |

4

Table of Contents

In response to the Staff’s comment, the Fund has revised the first paragraph of the Performance section on page 4 of the filing as follows:

“The table shows the average annual total returns of the fundfor 1, 5, and 10 years and also compares the fund’s performance with the average annual total returns of an index or other benchmark.”

In addition, the Fund has moved the paragraph following the Average Annual Total Returns table on page 5 of the prospectus so that it follows the heading instead of the table.

| 14. | The “Purchase and Sale of Fund Shares” section on page 5 of the prospectus contains disclosure beyond what is permitted by Item 6 of Form N-1A. In particular, the description of the process for redeeming shares is not responsive to Form N-1A requirements because there is no explanation of how to redeem shares for shareholders who are directly invested in the fund. Please revise accordingly. The Staff notes that the use of cross-references should also be avoided. |

The Fund respectfully submits that the current disclosure is in compliance with Form N-1A requirements and that no further changes are necessary.

| 15. | Please revise the disclosure under “Payments to Broker/Dealers and Other Financial Intermediaries” on page 5 of the prospectus to conform with the requirements of Item 8 of Form N-1A. |

The Fund respectfully submits that the current disclosure is in compliance with Form N-1A requirements and that no further changes are necessary.

| 16. | Please confirm whether the Fund can leverage and revise the disclosure pursuant to Item 4 accordingly. If the Fund cannot leverage, please include appropriate disclosure in the Statement of Additional Information. For example, the Statement of Additional Information might include an anti-leverage carve-out stating that “the fund may not purchase additional securities while outstanding borrowings exceed 5% of assets…” |

In response to the Staff’s comment, the Fund confirms that it may leverage through borrowing and/or the use of derivatives. The disclosure on page 10 of the prospectus states that “Certain derivatives transactions may have a leveraging effect on the fund.” The Fund further respectfully notes the following disclosure on page 6 of the prospectus.

“The fund may borrow money from banks for either investment or temporary purposes. Borrowings (excluding borrowings for temporary purposes) may be secured by up to 33 1/3% of the value of the fund’s total assets. The fund may borrow an additional amount of up to 5% of the fund’s total assets for temporary purposes.”

The fund is also permitted to engage in reverse repurchase agreements. Disclosure pertaining to reverse repurchase agreements is addressed in Item 30 below.

| 17. | Please confirm that the investment strategy under “Securities Lending” on page 7 of the prospectus is a principal investment strategy. If not, please note that it should be included in a separate section of the prospectus for non-principal investment strategies. |

The Fund confirms that securities lending is not a principal investment strategy and it is first described in the section titled “More on the Fund’s Investment Strategies, Investments and Risks.” The Fund respectfully submits that, as described earlier in Items 7 and 8, the current disclosure is consistent with the requirements of Form N-1A. The Fund’s principal investment

5

Table of Contents

strategies and risks are described in full in the prospectus in “More on the fund’s investment strategies, investments and risks.” The Fund does not believe that breaking the section into additional subsections would be useful to the investor when the principal strategies are already summarized in the summary section of the prospectus.

| 18. | The Staff advises that principal investment strategies should appear for the first time in the prospectus under Item 4. Please confirm that disclosure on derivatives and hedging techniques, which appear for the first time on page 7 of the prospectus pursuant to Item 9 are not principal investment strategies. |

The Fund confirms that the use of derivatives and hedging techniques is not a principal investment strategy and it is first described in the section titled “More on the Fund’s Investment Strategies, Investments and Risks.” The Fund respectfully submits that, as described earlier in Items 7, 8 and 17, the current disclosure is consistent with the requirements of Form N-1A. The Fund’s principal investment strategies and risks are described in full in the prospectus in “More on the fund’s investment strategies, investments and risks.” The Fund does not believe that breaking the section into additional subsections would be useful to the investor when the principal strategies are already summarized in the summary section of the prospectus.

| 19. | With respect to the section titled “Derivatives and Hedging Techniques” which appears on page 7, please advise whether the Fund may use derivatives or hedging techniques for speculative purposes or only for hedging purposes; if for speculative purposes, please disclose any attendant risks. |

The Fund confirms that it does not engage in the use of derivatives and hedging techniques for speculative purposes.

| 20. | Please confirm that the disclosure regarding junk bonds pursuant to Item 9 of Form N-1A under “Principal Investment Strategies” on page 9 of the prospectus is a principal investment strategy. |

As described above in Item 9, disclosure has been added to the prospectus to address this point. The Fund confirms that it is limited to investing 5% of its net assets in junk bonds. The Fund is, however, permitted to invest without limit in fixed-income securities, including junk bonds, and has revised the disclosure in the section titled “Principal Investment Strategies” to read as follows: “The fund may also invest without limit in fixed-income securities (including up to 5% of its net assets in fixed-income securities that are high yield, lower quality securities rated by a rating organization below its top four long-term rating categories (i.e., below investment grade securities, commonly referred to as “junk bonds”)) or unrated securities determined by the manager to be of equivalent quality. “As described in the Fund’s responses to Items 7 and 8 above, the Fund respectfully submits that the remaining disclosure is consistent with the requirements of Form N-1A.

| 21. | Please disclose under “Purchase and Sale of Fund Shares” on page 5 of the prospectus that in order for shareholders to receive the day’s net asset value (“NAV”), the Fund must receive the shareholder’s redemption request in good order by 4 PM that day. Please include disclosure identifying who must receive the shareholder’s request in good order. |

The Fund respectfully submits that the current prospectus disclosure is in compliance with Form N-1A and that no further changes are necessary.

| 22. | Please disclose under “Redemptions in Kind” on page 17 of the prospectus that shareholders bear any market risk of the securities until the securities are sold. |

6

Table of Contents

In response to the Staff’s comment, page 17 has been revised as follows:

“The Fund reserves the right to pay redemption proceeds by giving you securities. You may pay transaction costs to dispose of the securities. You will bear the risks associated with owning the securities, including the risk that the market price of the securities will go down, until you dispose of the securities.”

| 23. | Please refer to the “Frequent Trading of Fund Shares” disclosure on page 17 of the prospectus. Please clarify the disclosure regarding whether the Fund accommodates frequent purchases and sales, in accordance with the requirements of Item 11(e)(4)(ii) of Form N-1A. |

The Fund respectfully submits that the current prospectus disclosure is in compliance with Form N-1A and that no further changes are necessary.

| 24. | Disclosure in paragraph 6 under “Share Price” on page 21 of the prospectus states “When such prices or quotations are not available, or when LMPFA believes that they are unreliable, LMPFA may price securities using fair value procedures approved by the Board.” Please revise this sentence and add disclosure so that the sentence ends with “…and under the Board’s ultimate supervision.” In addition, please add disclosure identifying who must receive the request in good order in order for the shareholder to receive the day’s NAV. |

In response to the Staff’s comment, page 21 has been revised as follows:

When such prices or quotations are not available, or when LMPFA believes that they are unreliable, LMPFA may price securities using fair value procedures approved by the Board. The Board retains ultimate responsibility for the valuation process.

In addition. the Fund has added disclosure to the sections on Buying Shares, Redeeming Shares and Share Price to identify who must receive the request in good order in order for the shareholder to receive the day’s NAV.

Statement of Additional Information

| 25. | Please confirm in your response to the Staff that all non-principal investment strategies and their attendant risks are disclosed in the Statement of Additional Information in accordance with Item 16 of Form N-1A. |

The Fund confirms that all material non-principal investment strategies and their attendant risks are disclosed in the Statement of Additional Information in accordance with Item 16 of Form N-1A.

| 26. | Please confirm in your response to the Staff that any principal investment strategies and their attendant risks are appropriately disclosed in the prospectus. |

The Fund confirms that all principal investment strategies and their attendant risks are disclosed in the prospectus.

| 27. | Please revise the Statement of Additional Information so that non-principal strategy and risk information is disclosed separately from any principal strategy and risk information. |

7

Table of Contents

The Fund respectfully submits that the current SAI disclosure is in compliance with Form N-1A and that no further changes are necessary.

| 28. | Please note that there should not be any duplication of the prospectus in the Statement of Additional Information unless such duplication is needed in order to make the Statement of Additional Information comprehensible as a document independent of the prospectus. |

The Fund confirms that it has not duplicated any parts of the prospectus in the Statement of Additional Information other than as necessary to make the Statement of Additional Information comprehensible as a document independent of the prospectus.

| 29. | Disclosure under “Investment Restrictions and Limitations” on page 5 of the Statement of Additional Information states in fundamental policy no. 3 that “The Fund may lend money or other assets….” Please clarify what is meant by “other assets.” In addition, please further explain in the paragraph following the list of fundamental policies, with respect to fundamental policy no. 3, the effect on voting rights that attach to securities which are loaned. Please also include in earlier disclosure a general paragraph on lending. |

In response to the Staff’s comment, the Fund confirms that “other assets” refer to portfolio securities. The Fund is permitted to lend portfolio securities and has revised the disclosure on page 2 of the SAI, currently sub-headed “Loans of Portfolio Securities” to read as follows (such revised disclosure also describing the effect on voting rights that attach to securities that are loaned):

Securities Lending

Consistent with applicable regulatory requirements, the fund may lend portfolio securities to brokers, dealers and other financial organizations meeting capital and other credit requirements or other criteria established by the Board. The fund will not lend portfolio securities to affiliates of the manager unless it has applied for and received specific authority to do so from the SEC. From time to time, the fund may pay to the borrower and/or a third party which is unaffiliated with the fund or Legg Mason and is acting as a “finder” a part of the interest earned from the investment of collateral received for securities loaned. Although the borrower will generally be required to make payments to the fund in lieu of any dividends the fund would have otherwise received had it not loaned the shares to the borrower, such payments will not be treated as “qualified dividend income” for purposes of determining what portion of the fund’s regular dividends received by individuals may be taxed at the rates generally applicable to long-term capital gains.

Requirements of the SEC, which may be subject to future modification, currently provide that the following conditions must be met whenever the fund lends its portfolio securities: (a) the fund must receive at least 100% cash collateral or equivalent securities from the borrower; (b) the borrower must increase such collateral whenever the market value of the securities rises above the level of such collateral; (c) the fund must be able to terminate the loan at any time; (d) the fund must receive reasonable interest on the loan, as well as any dividends, interest or other distributions on the loaned securities, and any increase in market value; (e) the fund may pay only reasonable custodian fees in connection with the loan; and (f) voting rights on the loaned securities may pass to the borrower. However, if a material event adversely affecting the investment in the loaned securities occurs, the fund must terminate the loan and regain the right to vote the securities.

The risks in lending portfolio securities, as with other extensions of secured credit, consist of possible delay in receiving additional collateral or in the recovery of the securities or possible loss of rights in the collateral should the borrower fail financially. The fund could also lose money if its short-term investment of the cash collateral declines in value over the period of the loan. Loans will be made to firms deemed by the subadviser to be of good standing and will not be made unless, in the judgment of the subadviser, the consideration to be earned from such loans would justify the risk.

The Fund has also revised the description of lending which appears on page 7 of the Statement of Additional Information and corresponds to the fundamental policy 3. which appears on page 6 of the Statement of Additional Information to read as follows:

8

Table of Contents

With respect to the fundamental policy relating to lending set forth in (3) above, the 1940 Act does not prohibit the fund from making loans; however, SEC staff interpretations currently prohibit funds from lending more than one-third of their total assets, except through the purchase of debt obligations or the use of repurchase agreements. (A repurchase agreement is an agreement to purchase a security, coupled with an agreement to sell that security back to the original seller on an agreed-upon date at a price that reflects current interest rates. The SEC frequently treats repurchase agreements as loans.) While lending securities may be a source of income to the fund, as with other extensions of credit, there are risks of delay in recovery or even loss of rights in the underlying securities should the borrower fail financially. However, loans would be made only when the fund’s manager believes the income justifies the attendant risks. The fund also will be permitted by this policy to make loans of money, including to other funds. The fund would have to obtain exemptive relief from the SEC to make loans to other funds. The policy in (3) above will be interpreted not to prevent the fund from purchasing or investing in debt obligations and loans. In addition, collateral arrangements with respect to options, forward currency and futures transactions and other derivative instruments, as well as delays in the settlement of securities transactions, will not be considered loans.

| 30. | Refer to the disclosure under “Investment Restrictions and Limitations” on page 6 of the Statement of Additional Information discussing fundamental policies relating to borrowing, which states “To limit the risks attendant to borrowing, the 1940 Act requires the fund to maintaining at all times an “asset coverage” of at least 300% of the amount of its borrowings, include reverse repurchase agreements…”. Please advise whether the fund will engage in reverse repurchase agreements. If so, please refer to such disclosure in the document. In addition, please provide disclosure on the fund’s reverse repurchase agreement policy, if any. |

The Fund advises the Staff that it may engage in reverse repurchase agreements and has revised the disclosure on page 5 as follows:

Reverse Repurchase Agreements

The fund may enter into reverse repurchase agreements, which involve the sale of fund securities with an agreement to repurchase the securities at an agreed-upon price, date and interest payment and have the characteristics of borrowings. Since the proceeds of borrowings under reverse repurchase agreements are invested, this would introduce the speculative factor known as “leverage.” The securities purchased with the funds obtained from the agreement and securities collateralizing the agreement will have maturity dates no later than the repayment date. Generally the effect of such a transaction is that the fund can recover all or most of the cash invested in the portfolio securities involved during the term of the reverse repurchase agreement, while in many cases it will be able to keep some of the interest income associated with those securities. Such transactions are advantageous only if the fund has an opportunity to earn a greater rate of interest on the cash derived from the transaction than the interest cost of obtaining that cash. Opportunities to realize earnings from the use of the proceeds equal to or greater than the interest required to be paid may not always be available, and the fund intends to use the reverse repurchase technique only when the manager believes it will be advantageous to the fund. The use of reverse repurchase agreements may exaggerate any interim increase or decrease in the value of the fund’s assets. The fund’s custodian bank will maintain a separate account for the fund with securities having a value equal to or greater than such commitment of the fund.

9

Table of Contents

| 31. | Please disclose the Fund’s non-fundamental or operating policy with respect to investing in illiquid securities, including what actions the Fund would take in the event the 15% limit is reached. Please add disclosure regarding the monitoring process for reaching various investment limits and what the Fund would do in the event such limits are reached. For example, the disclosure might clarify for certain types of investments that the Fund is under no obligation to sell, but this is not the case with respect to borrowings and illiquid securities and the Fund must always be in compliance with these limitations. Please explain that the Fund will not deviate from these limitations and that it continuously adheres to percentage limits. |

The Fund notes that the Fund’s policy on investing in illiquid securities is stated on page 5 of the SAI and reads as follows: “The fund will not invest more than 15% of the value of its net assets in illiquid securities, such as “restricted securities” and securities that are not readily marketable, or other illiquid assets.”

The Fund further notes the following disclosure which appears under the heading “Investment Restrictions and Limitations” on page 6 of the SAI: “The percentage limitations contained in the investment restrictions described above and the description of the fund’s investment policies are all applied solely at the time of any proposed transaction on the basis of values or amounts determined at that time. If a percentage restriction on investment or utilization of assets in a policy or restriction is adhered to at the time an investment is made, a later change in percentage ownership of a security or kind of security resulting from changing market values or a similar type of event will not be considered a violation of such policy or restriction.”

| 32. | Please advise as to whether the Fund would pledge assets to cover borrowings. |

The Fund advises the Staff that it is permitted to pledge assets to cover borrowings and has revised the disclosure on page 6 of the SAI as follows:

The fund is authorized to borrow, and to pledge assets to secure such borrowings, up to the maximum extent permissible under the 1940 Act.

| 33. | As discussed in Item 16, please include an anti-leverage carve-out in the Statement of Additional Information, if appropriate. |

As discussed in response to Item 16 above, the Fund confirms that it may leverage through borrowing and/or the use of derivatives. The Fund may also engage in reverse repurchase agreements, as discussed in Item 30 above.

| 34. | Please note that the Statement of Additional Information is missing disclosure that is responsive to Item 17 of Form N-1A and the filing is incomplete on its face as a result of this deficiency. Please include a summary in the response letter that the Fund is aware of the deficiency and will cure it by including the required disclosure in the fund’s 485(b) filing. Please note that the disclosure can also be submitted via a correspondence filing before the 485(b) is filed in order to give the Staff the opportunity to comment on the disclosure. |

In response to the Staff’s comment, the Fund has provided the Staff supplementally, as correspondence dated December 22, 2010, additional disclosure that is responsive to Item 17 of Form N-1A.

10

Table of Contents

Please note that we have included certain changes to Amendment No. 40 other than those in response to the Staff’s comments. Included as Exhibit A to this letter is a copy of the prospectus and Statement of Additional Information marked to reflect cumulative changes to Post-Effective Amendment No. 39 to the Registration Statement filed with the Commission on October 29, 2010. Furthermore, please note that Post-Effective Amendment No. 40 was filed by the Fund on December 29, 2010.

In connection with the above-referenced filing, the Fund hereby acknowledges that:

| 1. | The Fund is responsible for the adequacy and accuracy of the disclosure in the filing; |

| 2. | Should the Commission or the Staff, acting pursuant to delegated authority, declare the filing effective, it does not foreclose the Commission from taking any action with respect to the filing; |

| 3. | The action of the Commission or the Staff, acting pursuant to delegated authority, in declaring the filing effective, does not relieve the Fund from its full responsibility for the adequacy and accuracy of the disclosure in the filing; and |

| 4. | The Fund may not assert Staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

Please call me at 203-703-7027 with any questions you may have regarding this filing or if you wish to discuss the above responses.

Very truly yours,

/s/ Rosemary Emmens

Rosemary Emmens

11

Table of Contents

BARRETT OPPORTUNITY FUND, INC.

PROSPECTUS

December 31, 2010

Class: Ticker Symbol

O: SAOPX

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

INVESTMENT PRODUCTS: NOT FDIC INSUREDŸ NO BANK GUARANTEEŸ MAY LOSE VALUE

Table of Contents

BARRETT OPPORTUNITY FUND, INC.

PROSPECTUS

December 31, 2010

| Page | ||||

| 2 | ||||

| 2 | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 5 | ||||

| 5 | ||||

Payments to Broker/Dealers and Other Financial Intermediaries | 5 | |||

More on the Fund’s Investment Strategies, Investments and Risks | 6 | |||

| 12 | ||||

| 14 | ||||

| 15 | ||||

| 16 | ||||

| 19 | ||||

| 21 | ||||

| 23 | ||||

Prior to December 1, 2006, the fund was named Salomon Brothers Opportunity Fund Inc.

Table of Contents

The fund seeks to achieve above average long-term capital appreciation. Current income is a secondary objective.

The table describes the fees and expenses that you may pay if you buy and hold shares of the fund.

Shareholder Fees

(Paid directly from your investment)

Maximum sales charge (load) imposed on purchases | None | |||

Maximum deferred sales charge (load) (as a % of amount redeemed) | None |

Annual Fund Operating Expenses

(Expenses that you pay each year as a percentage of the value of your investment)

Management fees | 0.75% | |||

Distribution and service (12b-1) fees | None | |||

Other expenses | 0.45% | |||

Total annual fund operating expenses | 1.20% |

Example

This example is intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The example assumes:

| • | You invest $10,000 in the fund for the time periods indicated |

| • | Your investment has a 5% return each year and the fund’s operating expenses remain the same |

Although your actual costs may be higher or lower, based on these assumptions your costs would be:

1 year | 3 years | 5 years | 10 years | |||||||||||

| $ | 122 | $ | 381 | $ | 660 | $ | 1,455 | |||||||

The Example does not reflect sales charges (loads) on reinvested dividends (and other distributions). If these sales charges (loads) were included, your costs would be higher.

Portfolio turnover. The fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the fund’s performance. During the most recent fiscal year, the fund’s portfolio turnover rate was 3% of the average value of its portfolio.

Principal Investment Strategies

The fund’s investment objectives are not fundamental and may be changed by the Board of Directors upon 60 days’ written notice to holders of the fund’s common shares.

The fund invests primarily in common stocks and securities convertible into or exchangeable for common stock such as convertible preferred stock or convertible debt securities.

The fund may invest without limit in securities of issuers located in the United States, as well as other securities that are publicly traded in the United States, including sponsored American Depositary Receipts.

- 2 -

Table of Contents

The fund may also invest up to 5% of its net assets in foreign securities that are not publicly traded in the United States.

The fund may also invest without limit in fixed-income securities (including up to 5% of its net assets in fixed-income securities that are high yield, lower quality securities rated by a rating organization below its top four long-term rating categories (i.e., below investment grade securities, commonly referred to as “junk bonds”)) or unrated securities determined by the manager to be of equivalent quality.

Risk is inherent in all investing. There is no assurance that the fund will meet its investment objectives. The value of your investment in the fund, as well as the amount of return you receive on your investment, may fluctuate significantly. You may lose part or all of your investment in the fund or your investment may not perform as well as other similar investments. The following is a summary description of certain risks of investing in the fund.

Stock market and equity securities risk. The securities markets are volatile and the market prices of the fund’s securities may decline generally. Securities fluctuate in price based on changes in a company’s financial condition and overall market and economic conditions. If the market prices of the securities owned by the fund fall, the value of your investment in the fund will decline. The recent financial crisis has caused a significant decline in the value and liquidity of many securities. In response to the crisis, the U.S. and other governments and the Federal Reserve and certain foreign central banks have taken steps to support financial markets. The withdrawal of this support could also negatively affect the value and liquidity of certain securities. In addition, legislation recently enacted in the U.S. calls for changes in many aspects of financial regulation. The impact of the legislation on the markets, and the practical implications for market participants, may not be known for some time.

Issuer risk. The value of a stock can go up or down more than the market as a whole and can perform differently from the value of the market as a whole, often due to disappointing earnings reports by the issuer, unsuccessful products or services, loss of major customers, major litigation against the issuer or changes in government regulations affecting the issuer or the competitive environment. The fund may experience a substantial or complete loss on an individual stock. Historically, the prices of securities of small and medium capitalization companies have generally gone up or down more than those of large capitalization companies, although even large capitalization companies may fall out of favor with investors.

Liquidity risk. Some securities held by the fund may be difficult to sell, or illiquid, particularly during times of market turmoil. Illiquid securities may also be difficult to value. If the fund is forced to sell an illiquid asset to meet redemption requests or other cash needs, the fund may be forced to sell at a loss.

Foreign investments risk.The fund’s investments in securities of foreign issuers involve greater risk than investments in securities of U.S. issuers. Foreign countries in which the fund may invest may have markets that are less liquid and more volatile than U.S. markets and may suffer from political or economic instability. In some foreign countries, less information is available about issuers and markets because of less rigorous accounting and regulatory standards than in the United States. Currency fluctuations could erase investment gains or add to investment losses.

Portfolio selection risk. The value of your investment may decrease if the portfolio managers’ judgment about the attractiveness, value or market trends affecting a particular security, industry or sector or about market movements is incorrect.

Value investing risk. The value approach to investing involves the risk that stocks may remain undervalued. Value stocks may underperform the overall equity market while the market concentrates on growth stocks. Although the fund will not concentrate its investments in any one industry or industry group, it may, like many value funds, weight its investments toward certain industries, thus increasing its exposure to factors adversely affecting issuers within those industries.

- 3 -

Table of Contents

Non-diversification risk. The fund is classified as “non-diversified,” which means it may invest a larger percentage of its assets in a small number of issuers than a diversified fund. To the extent the fund invests its assets in fewer issuers, the fund will be more susceptible to negative events affecting those issuers.

Risk of increase in expenses. Your actual costs of investing in the fund may be higher than the expenses shown in “Annual fund operating expenses” for a variety of reasons. For example, expense ratios may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and fund expense ratios are more likely to increase when markets are volatile.

Net unrealized appreciation. The fund currently has a substantial amount of net unrealized appreciation. At November 30, 2010, the amount of the net unrealized appreciation was $58,764,747, representing approximately 85% of the fund’s net assets. The manager (as defined below) no longer pursues a strategy of retaining unrealized long-term capital gain and avoiding the tax impact of realizing such gain. Subject to market conditions and fund performance, the manager anticipates that, in managing the fund’s investment portfolio in pursuit of the fund’s investment objectives, a moderate portion of the fund’s current built-in long-term capital gains will be realized gradually in each of the next several years. If these long-term capital gains are realized as anticipated, this will result in an increase in the fund’s annual distributions of net capital gains and, accordingly, an increase in taxable distributions to shareholders to the extent there are no offsetting losses. Under normal market conditions, the manager currently expects that no more than 10% of the total amount of the fund’s current built-in long-term capital gains will be realized in any one year. See “Dividends, Distributions and Taxes.”

These risks are discussed in more detail later in this Prospectus or in the Statement of Additional Information (the “SAI”).

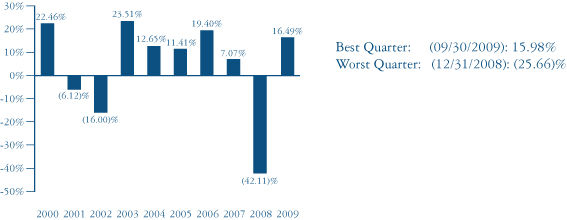

The accompanying bar chart and table provide some indication of the risks of investing in the fund. The bar chart shows changes in the fund’s performance from year to year. The table shows the average annual total returns of the fund for 1, 5, and 10 years and also compares the fund’s performance with the average annual total returns of an index or other benchmark. The fund makes updated performance information available at the fund’s website, http://www.leggmason.com/individualinvestors/products/mutual-funds/annualized_performance, or by calling the fund at 1-877-721-1926.

The fund’s past performance (before and after taxes) is not necessarily an indication of how the fund will perform in the future.

Total Returns (before taxes)

The year-to-date return as of the most recent calendar quarter, which was 09/30/2010, was 3.18%

- 4 -

Table of Contents

Average Annual Total Returns (for Periods Ended December 31, 2009)

| 1 Year | 5 Years | 10 Years | ||||||||||

Return before taxes | 16.49% | (0.80 | )% | 2.58 | % | |||||||

Return after taxes on distributions | 15.23% | (1.98 | )% | 1.32 | % | |||||||

Return after taxes on distributions and sale of fund shares | 11.65% |

| (0.84 | )% | 1.90 | % | ||||||

S&P 500 Index | 26.46% | 0.42 | % | (0.95 | )% | |||||||

The after-tax returns, are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and the after-tax returns shown are not relevant to investors who hold their fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.

Investment manager: Barrett Associates, Inc. (“Barrett Associates” or the “manager”)

Portfolio managers: Robert J. Milnamow and E. Wells Beck, CFA, are responsible for the day-to-day management of the fund. Mr. Milnamow has served as a portfolio manager of the fund since 2006. Mr. Beck has served as a portfolio manager of the fund since April 2010.

Purchase and Sale of Fund Shares

You may purchase or redeem shares of the fund each day the New York Stock Exchange (the “NYSE”) is open, at the fund’s net asset value determined after receipt of your request in good order.

The fund’s initial and subsequent investment minimums generally are as follows:

Investment Minimums Initial/Additional Investments

General | $ | 1,000/$100 | ||

IRAs | $ | 250/NA | ||

SEP IRAs | $ | 250/NA | ||

Systematic Investment Plans | $ | 25/$50 |

Your financial intermediary may impose different investment minimums.

For more information about how to purchase or redeem shares, you should contact your financial intermediary, or, if you hold your shares or plan to purchase shares through the fund, you should contact the fund at 1-877-721-1926) or by mail (Barrett Opportunity Fund, Inc., P.O. Box 55214, Boston, MA 02205-8504).

The fund’s distributions are taxable as ordinary income or capital gain, except when your investment is through an IRA, 401(k) or other tax-advantaged account.

Payments to Broker/Dealers and Other Financial Intermediaries

The fund’s related companies may pay broker/dealers or other financial intermediaries (such as a bank or an insurance company) for the sale of fund shares and related services. These payments create a conflict of interest by influencing your broker/dealer or other intermediary or its employees or associated persons to recommend the fund over another investment. Ask your financial adviser or visit your financial intermediary’s website for more information.

- 5 -

Table of Contents

More on the Fund’s Investment Strategies, Investments and Risks

The fund seeks to achieve above average long-term capital appreciation. Current income is a secondary objective.

The fund invests primarily in common stocks and securities convertible into or exchangeable for common stock such as convertible preferred stock or convertible debt securities.

The fund may also invest without limit in fixed-income securities (including up to 5% of its net assets in fixed-income securities that are high yield, lower quality securities rated by a rating organization below its top four long-term rating categories (i.e., below investment grade securities, commonly referred to as “junk bonds”)) or unrated securities determined by the manager to be of equivalent quality or hold assets in cash or cash equivalents, such as U.S. Government obligations, investment grade debt securities and other money market instruments, for temporary defensive purposes due to economic or market conditions.

The fund’s investment objective and investment strategies may be changed by the Board of Directors (the “Board”) without shareholder approval.

The fund is classified as “non-diversified,” which means it may invest a larger percentage of its assets in a small number of issuers than a diversified fund.

Cash Management

The fund may hold cash pending investment, and may invest in money market instruments for cash management purposes. The amount of assets the fund may hold for cash management purposes will depend on market conditions and the need to meet expected redemption requests.

Equity Investments

Subject to its particular investment policies, the fund may invest in all types of equity securities. Equity securities include exchange-traded and over-the-counter (OTC) common and preferred stocks, warrants and rights, securities convertible into common stocks, and securities of other investment companies and of real estate investment trusts.

Borrowing

The fund may borrow money from banks for either investment or temporary purposes. Borrowings (excluding borrowings for temporary purposes) may be secured by up to 33 1/3% of the value of the fund’s total assets. The fund may borrow an additional amount of up to 5% of the fund’s total assets for temporary purposes.

Securities Lending

The fund may lend portfolio securities representing up to 10% of the value its of total assets in order to increase its net investment income. The loans are continuously secured by cash or liquid securities equal to no less than the market value, determined daily, of the securities loaned.

- 6 -

Table of Contents

Derivatives and Hedging Techniques

Derivatives are financial instruments whose value depends upon, or is derived from, the value of an asset, such as one or more underlying investments, currencies or indexes. The fund may engage in a variety of transactions using derivatives, such as options on securities and securities indexes. Derivatives may be used by the fund for any of the following purposes:

| • | As a hedging technique in an attempt to manage risk in the fund’s portfolio |

| • | As a substitute for buying or selling securities |

| • | To enhance the fund’s return |

| • | As a cash flow management technique |

A derivative contract will obligate or entitle the fund to deliver or receive an asset or cash payment based on the change in value of one or more investments, currencies or indexes. When the fund enters into derivatives transactions, it may be required to segregate assets or enter into offsetting positions, in accordance with applicable regulations. Such segregation is not a hedging technique and will not limit the fund’s exposure to loss. The fund will, therefore, have investment risk with respect to both the derivative itself and the assets that have been segregated to offset the fund’s derivative exposure. If such segregated assets represent a large portion of the fund’s portfolio, portfolio management may be affected as covered positions may have to be reduced if it becomes necessary for the fund to reduce the amount of segregated assets in order to meet redemptions or other obligations.

Should the fund invest in derivatives, the fund will, in determining compliance with any percentage limitation or requirement regarding the use or investment of fund assets, take into account the market value of the fund’s derivative positions that are intended to reduce or create exposure to the applicable category of investments.

Repurchase Agreements

The fund may enter into repurchase agreements for cash management purposes. A repurchase agreement is a transaction in which the seller of a security commits itself at the time of the sale to repurchase that security from the buyer at a mutually agreed upon time and price. The fund will enter into repurchase agreements only with dealers, domestic banks or recognized financial institutions which, in the opinion of the manager, based on guidelines established by the fund’s Board, are deemed creditworthy. The manager will monitor the value of the securities underlying the repurchase agreement at the time the transaction is entered into and at all times during the term of the repurchase agreement to ensure that the value of the securities always exceeds the repurchase price.

Defensive Investing

The fund may depart from its principal investment strategies in response to adverse market, economic or political conditions by taking temporary defensive positions in any type of money market instruments, short-term debt securities or cash without regard to any percentage limitations. Although the manager has the ability to take defensive positions, it may choose not to do so for a variety of reasons, even during volatile market conditions.

Other Investments

The fund may also use other strategies and invest in other securities that are described, along with their risks, in the SAI. However, the fund might not use all of the strategies and techniques or invest in all of the types of securities described in this prospectus or in the SAI.

Selection Process

The manager emphasizes individual security selection while varying the fund’s investments across industries, which may help to reduce risk. While the manager evaluates companies of all sizes, as a principal investment strategy, the fund intends to invest primarily in companies with large- and mid-capitalizations (normally,

- 7 -

Table of Contents

$1 billion in market capitalization and above). The manager seeks to identify those companies whose securities are undervalued based on the manager’s judgment of the company’s sustainable earnings growth. The manager employs fundamental analysis to analyze each company in detail, ranking the management, strategy and competitive market position.

In selecting individual companies for investment, the manager considers how the following would affect a company’s earnings, the market price of its shares and the market’s evaluation of the company’s future earnings:

| • | Changes in management, policies, corporate control or capitalization |

| • | Changes in technology, marketing or production, the development of new products or services or the demand for existing products or services |

| • | The effect of recent and anticipated capital expenditures |

| • | The effect of social, economic, political, legal and international developments |

More on Risks of Investing in the Fund

Stock market and equity securities risk.Securities fluctuate in price based on changes in a company’s financial condition and overall market and economic conditions. The value of a particular security may decline due to factors that affect a particular industry or industries, such as an increase in production costs, competitive conditions or labor shortages; or due to general market conditions, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates or generally adverse investor sentiment.

Issuer risk. The value of a security can be more volatile than the market as a whole and can perform differently from the value of the market as a whole. The value of a company’s stock may deteriorate because of a variety of factors, including disappointing earnings reports by the issuer, unsuccessful products or services, loss of major customers, major litigation against the issuer or changes in government regulations affecting the issuer or the competitive environment.

Large capitalization company risk. Large capitalization companies may fall out of favor with investors.

Small and medium capitalization company risk. The fund will be exposed to additional risks as a result of its investments in the securities of small and medium capitalization companies. Small and medium capitalization companies may fall out of favor with investors; may have limited product lines, operating histories, markets or financial resources; or may be dependent upon a limited management group. The prices of securities of small and medium capitalization companies generally are more volatile than those of large capitalization companies and are more likely to be adversely affected than large capitalization companies by changes in earnings results and investor expectations or poor economic or market conditions, including those experienced during a recession. Securities of small and medium capitalization companies may underperform large capitalization companies, may be harder to sell at times and at prices the portfolio manager believes appropriate and may offer greater potential for losses.

Liquidity risk.Liquidity risk exists when particular investments are difficult to sell. Although most of the fund’s investments must be liquid at the time of investment, investments may become illiquid after purchase by the fund, particularly during periods of market turmoil. When the fund holds illiquid investments, the portfolio may be harder to value, especially in changing markets, and if the fund is forced to sell these investments to meet redemption requests or for other cash needs, the fund may suffer a loss. In addition, when there is illiquidity in the market for certain investments, the fund, due to limitations on illiquid investments, may be unable to achieve its desired level of exposure to a certain sector.

Foreign investments risk. The fund’s investments in securities of foreign issuers involve greater risk than investments in securities of U.S. issuers. Foreign countries in which the fund may invest may have markets that are less liquid and more volatile than markets in the United States, may suffer from political or economic instability and may experience negative government actions, such as currency controls or seizures of private businesses or property. In some foreign countries, less information is available about issuers and markets because of less rigorous accounting and regulatory standards than in the United States. Foreign

- 8 -

Table of Contents

withholdings may reduce the fund’s returns. Currency fluctuations could erase investment gains or add to investment losses. Because the value of a depositary receipt is dependent upon the market price of an underlying foreign security, depositary receipts are subject to most of the risks associated with investing in foreign securities directly.

The risks of investing in foreign securities are heightened when investing in issuers in emerging market countries.

Generally, American Depositary Receipts (“ADRs”), in registered form, are denominated in U.S. dollars and are designed for use in the domestic market. Usually issued by a U.S. bank or trust company, ADRs are receipts that demonstrate ownership of underlying foreign securities. For purposes of the fund’s investment policies and limitations, ADRs are considered to have the same characteristics as the securities underlying them. ADRs may be sponsored or unsponsored; issuers of securities underlying unsponsored ADRs are not contractually obligated to disclose material information in the United States. Accordingly, there may be less information available about such issuers than there is with respect to domestic companies and issuers of securities underlying sponsored ADRs.

High yield or “junk” bond risk.Debt securities that are below investment grade, or “junk bonds,” are speculative, have a higher risk of default, tend to be less liquid and are more difficult to value than higher grade securities. Junk bonds tend to be volatile and more susceptible to adverse events and negative sentiments. Investing in these securities subjects the fund to increased price sensitivity to changing interest rates; greater risk of loss because of default or declining credit quality or an issuer’s inability to make interest and/or principal payments due to adverse company specific events. Junk bonds are also subject to the risk of negative perceptions of the high yield market depressing the price and liquidity of high yield securities. These negative perceptions could last for a significant period of time.

Portfolio selection risk.The value of your investment may decrease if the portfolio managers’ judgment about the attractiveness, value or market trends affecting a particular security, industry or sector or about market movements is incorrect.

Value investing risk.The value approach to investing involves the risk that value stocks may remain undervalued. Value stocks as a group may be out of favor and underperform the overall equity market for a long period of time, while the market concentrates on growth stocks. Although the fund will not concentrate its investments in any one industry or industry group, it may, like many value funds, weight its investments toward certain industries, thus increasing its exposure to factors adversely affecting issuers within those industries.

Non-diversification risk. The fund is classified as “non-diversified,” which means it may invest a larger percentage of its assets in a small number of issuers than a diversified fund. To the extent the fund invests its assets in fewer issuers, the fund will be more susceptible to negative events affecting those issuers.

Cash management and defensive investing risk.The value of the investments held by the fund for cash management or defensive investing purposes may be affected by changing interest rates and by changes in credit ratings of the investments. If the fund holds cash uninvested it will be subject to the credit risk of the depository institution holding the cash. If a significant amount of the fund’s assets are used for cash management or defensive investing purposes, it will be more difficult for the fund to achieve its investment objective.

Borrowing risk. Certain borrowings may create an opportunity for increased return but, at the same time, create special risks. For example, borrowing may exaggerate changes in the net asset value of the portfolio’s shares and in the return on the fund’s securities holdings. The fund may be required to liquidate fund securities at a time when it would be disadvantageous to do so in order to make payments with respect to any borrowing. Interest on any borrowing will be a fund expense and will reduce the value of the fund’s shares.

Securities lending risk. Lending securities involves the risk of possible delay in receiving additional collateral, delay in recovery of securities when the loan is called or possible loss of collateral should the

- 9 -

Table of Contents

borrower fail financially. The fund could also lose money if its short-term investment of the cash collateral declines in value over the period of the loan.

Derivatives risk. Using derivatives, especially for non-hedging purposes, may involve greater risks to the fund than investing directly in securities, particularly as these instruments may be very complex and may not behave in the manner anticipated. Certain derivatives transactions may have a leveraging effect on the fund. Even a small investment in derivative contracts can have a significant impact on the fund’s stock market, interest rate currency or exposure. Therefore, using derivatives can disproportionately increase losses and reduce opportunities for gains when stock prices, currency rates or interest rates are changing. The fund may not fully benefit from or may lose money on derivatives if changes in their value do not correspond as anticipated to changes in the value of the fund’s holdings. Using derivatives may increase volatility, which is the characteristic of a security, an index or a market to fluctuate significantly in price within a short time period. Holdings of derivatives also can make the fund less liquid and harder to value, especially in declining markets.

Derivatives are subject to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation.

The impact of recent legislation calling for new regulation of the derivatives markets is not yet known and may not be known for some time. Any new regulation could increase the risks of investing in derivative instruments.

Repurchase agreements risk: Repurchase agreements could involve certain risks in the event of default or insolvency of the seller, including losses and possible delays or restrictions upon the fund’s ability to dispose of the underlying securities. To the extent that, in the meantime, the value of the securities that the fund has purchased has decreased, the fund could experience a loss.

Valuation risk. Many factors may influence the price at which the fund could sell any particular portfolio investment. The sales price may well differ — higher or lower — from the fund’s last valuation, and such differences could be significant, particularly for illiquid securities and securities that trade in relatively thin markets and/or markets that experience extreme volatility. If market conditions make it difficult to value some investments, the fund may value these investments using more subjective methods, such as fair value methodologies. Investors who purchase or redeem fund shares on days when the fund is holding fair-valued securities may receive a greater or lesser number of shares, or greater or lower redemption proceeds, than they would have received if the fund had not fair-valued the security or had used a different valuation methodology. The value of foreign securities and currencies may be materially affected by events after the close of the market on which they are valued, but before the fund determines its net asset value.

Portfolio turnover risk.While the fund has traditionally had very low portfolio turnover, there can be no assurance that this will be the case in the future. In addition, because the manager no longer pursues a strategy of retaining unrealized long-term capital gain and avoiding the tax impact of realizing such gain, the fund’s portfolio turnover rate may increase moderately in the future. Frequent trading increases transaction costs (including brokerage expenses), which could detract from the fund’s performance.

Recent market events risk. The equity and debt capital markets in the United States and internationally have experienced unprecedented volatility. This financial crisis has caused a significant decline in the value and liquidity of many securities. This environment could make identifying investment risks and opportunities especially difficult for the manager. These market conditions may continue or get worse. In response to the crisis, the U.S. and other governments and the Federal Reserve and certain foreign central banks have taken steps to support financial markets. The withdrawal of this support could also negatively affect the value and liquidity of certain securities. In addition, legislation recently enacted in the U.S. calls for changes in many aspects of financial regulation. The impact of the legislation on the markets, and the practical implications for market participants, may not be known for some time.

Please note that there are other factors that could adversely affect your investment and that could prevent the fund from achieving its investment objective. More information about risks appears in the SAI. Before investing, you should carefully consider the risks that you will assume.

- 10 -

Table of Contents

Portfolio Holdings

A description of the fund’s policies and procedures with respect to the disclosure of its portfolio holdings is available in the SAI. The fund posts its complete portfolio holdings at http://www.leggmason.com/individualinvestors/prospectuses (click on the name of the fund) on a quarterly basis. The fund intends to post its complete portfolio holdings 14 calendar days following the quarter-end. The fund intends to post partial information concerning the fund’s portfolio holdings (such as top 10 holdings or sector breakdowns, for example) on the Legg Mason funds’ website on a monthly basis. The fund intends to post this partial information 10 business days following each month-end. Such information will remain available until the next month’s or quarter’s holdings are posted.

- 11 -

Table of Contents

Manager and Sub-Administrator

The fund’s investment manager is Barrett Associates, Inc., a wholly-owned subsidiary of Legg Mason Investment Counsel & Trust Company, which in turn is a wholly-owned subsidiary of Legg Mason, Inc. (“Legg Mason”). Barrett Associates, with offices at 90 Park Avenue, 34th Floor, New York, New York 10016, selects the fund’s investments, oversees its operations and provides administrative services. As of September 30, 2010, Barrett Associates managed approximately $1.1 billion of client assets.

Legg Mason Partners Fund Advisor, LLC (“LMPFA” or the “sub-administrator”), located at 620 Eighth Avenue, New York, New York 10018, serves as the sub-administrator for the fund, providing certain administrative services for the fund pursuant to a sub-administration agreement between Barrett Associates and LMPFA. LMPFA is a wholly-owned subsidiary of Legg Mason and an affiliate of Barrett Associates. LMPFA was formed in April 2006 as a result of an internal reorganization to consolidate advisory services after Legg Mason acquired substantially all of Citigroup’s asset management business in December 2005. Barrett Associates, and not the fund, pays LMPFA for its services as sub-administrator.

Legg Mason, whose principal executive offices are at 100 International Drive, Baltimore, Maryland 21202, is a global asset management company. As of September 30, 2010, Legg Mason’s asset management operation had aggregate assets under management of approximately $673.5 billion.

Portfolio Managers

Robert J. Milnamow and E. Wells Beck, CFA, of Barrett Associates are responsible for the day-to-day management of the fund.

Mr. Milnamow joined Barrett Associates in 2003 as a Managing Director. Prior to joining Barrett Associates, Mr. Milnamow was Managing Member at Thayer Pond Capital, LLC from 2001 to 2003 and a senior portfolio manager at Rockefeller & Co. from 1998 to 2001. While at Rockefeller & Co., Mr. Milnamow was responsible for managing individual high net worth, foundation and endowment accounts. Mr. Milnamow has over 32 years of experience in the investment management industry.

Mr. Beck joined Barrett Associates in 2006 as a Managing Director. Prior to joining Barrett Associates, Mr. Beck was an analyst and portfolio manager at Haven Capital Management in New York from 2001 to 2006. From 2000 to 2001, Mr. Beck was a sell-side analyst in the research department at Prudential Securities covering a number of areas, including financial services. He also has investment experience from positions he held at HSBC Investment Banking PLC and Oppenheimer Capital International. Mr. Beck has 18 years of experience in the investment management industry.

The SAI provides information about the compensation of the portfolio managers, other accounts managed by the portfolio managers and any fund shares held by the portfolio managers.

Management Fee

The fund pays a management fee at an annual rate that decreases as assets increase, as follows: 0.750% of the fund’s average daily net assets up to $1 billion; 0.725% of the next $1 billion of average daily net assets; 0.700% of the next $3 billion of average daily net assets; 0.675% of the next $5 billion of average daily net assets; and 0.650% of the average daily net assets over $10 billion.

For the fiscal year ended August 31, 2010, the fund paid a management fee of 0.75% of the fund’s average daily net assets for management services.

A discussion regarding the basis for the Board’s approval of the fund’s management agreement is available in the fund’s Semi-Annual Report for the period ended February 28, 2010.

- 12 -

Table of Contents

Distributor

Legg Mason Investor Services, LLC (“LMIS”), a wholly-owned broker/dealer subsidiary of Legg Mason, serves as the fund’s sole and exclusive distributor.

The distributor, the manager and/or their affiliates make payments for distribution, shareholder servicing, marketing and promotional activities and related expenses out of their profits and other available sources, including profits from their relationships with the fund. These payments are not reflected as additional expenses in the fee table contained in this Prospectus. The recipients of these payments may include the fund’s distributor and affiliates of the manager, as well as non-affiliated broker/dealers, insurance companies, financial institutions and other financial intermediaries through which investors may purchase shares of the fund, including your financial intermediary. The total amount of these payments is substantial, may be substantial to any given recipient and may exceed the costs and expenses incurred by the recipient for any fund-related marketing or shareholder servicing activities. The payments described in this paragraph are often referred to as “revenue sharing payments.” Revenue sharing arrangements are separately negotiated.

Revenue sharing payments create an incentive for an intermediary or its employees or associated persons to recommend or sell shares of the fund to you. Contact your financial intermediary for details about revenue sharing payments it receives or may receive. Revenue sharing payments, as well as payments under the shareholder services and distribution plan (where applicable), also benefit the manager, the distributor and their affiliates to the extent the payments result in more assets being invested in the fund on which fees are being charged.

Transfer Agent and Shareholder Servicing Agent

Boston Financial Data Services, Inc. (“BFDS”) serves as the fund’s transfer agent and shareholder servicing agent. The transfer agent maintains the shareholder account records for the fund, handles certain communications between shareholders and the fund and distributes dividends and distributions payable by the fund.

BNY Mellon Investment Servicing Inc. serves as co-transfer agent with BFDS with respect to shares purchased by clients of certain service providers.

- 13 -

Table of Contents

General