As filed with the Securities and Exchange Commission

on February 6, 2015

REGISTRATION NO. 333-200782

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

☑ Pre-Effective Amendment No. 1 ☐ Post-Effective Amendment No. _____

(Check appropriate box or boxes)

JANUS INVESTMENT FUND

(Exact Name of Registrant as Specified in Charter)

151 Detroit Street

Denver, Colorado 80206-4805

(Address of Principal Executive Offices)

303-333-3863

(Registrant’s Area Code and Telephone Number)

Stephanie Grauerholz, Esq.

151 Detroit Street

Denver, Colorado 80206-4805

(Name and Address of Agent for Service)

APPROXIMATE DATE OF PROPOSED PUBLIC OFFERING: As soon as practicable after this Registration Statement becomes effective under the Securities Act of 1933.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to Section 8(a), may determine.

No filing fee is required because an indefinite number of shares of beneficial interest with $0.01 par value, of the Registrant have previously been registered pursuant to Section 24(f) of the Investment Company Act of 1940, as amended.

| | For shareholders of

INTECH U.S. Managed Volatility Fund II | | | | |

February 6, 2015

Dear Shareholder:

We are writing to inform you, as a shareholder of INTECH U.S. Managed Volatility Fund II (formerly named INTECH U.S. Growth Fund), that the Trustees of your Fund have approved Janus’ and INTECH’s proposal to merge the Fund into INTECH U.S. Managed Volatility Fund (formerly named INTECH U.S. Value Fund), effective on or about April 24, 2015. As described in the enclosed Prospectus/Information Statement, each Fund recently transitioned to INTECH’s managed volatility investment strategy and the merger is designed to streamline the Janus mutual funds platform by consolidating similar funds. Effective December 17, 2014, each Fund’s name, principal investment strategies, and benchmark index were changed to reflect a managed volatility investment strategy that seeks to provide returns in excess of the Fund’s benchmark index and to reduce or “manage” portfolio volatility to a level less than such benchmark index. As a result of these changes, the Funds now have identical investment strategies and risks, and the same benchmark index, and each Fund continues to have an investment objective of long-term growth of capital. The merger will provide you with the opportunity to invest in a larger fund that has the potential for lower expense ratios because of its increased size. The Trustees of your Fund have unanimously approved the merger.

The merger does not require shareholder approval, and you are not being asked to vote. As of the merger closing date, you will automatically receive the same class of shares of INTECH U.S. Managed Volatility Fund as you currently hold in INTECH U.S. Managed Volatility Fund II. You do not need to take any action related to the merger as your shares will be transferred automatically on the merger date. The merger is expected to qualify as a tax-free reorganization for federal income tax purposes, so you should not realize a tax gain or loss as a direct result of the merger, nor will you pay expenses associated with the merger.

Enclosed you will find a Prospectus/Information Statement with additional details describing the merger. If you have additional questions, please contact your financial advisor/intermediary for assistance, or call a Janus representative at 1-800-525-0020.

We value the trust and confidence you have placed with us and look forward to continuing our relationship with you.

| | | | | Sincerely, | |

| | | | | /s/ Bruce L. Koepfgen | |

| | | | | Bruce L. Koepfgen

Chief Executive Officer and President

Janus Investment Fund | |

PROSPECTUS/INFORMATION STATEMENT

February 6, 2015

Relating to the acquisition of the assets of

INTECH U.S. Managed Volatility Fund II

(formerly named INTECH U.S. Growth Fund)

by and in exchange for shares of beneficial interest of

INTECH U.S. Managed Volatility Fund

(formerly named INTECH U.S. Value Fund)

each, a series of Janus Investment Fund

151 Detroit Street

Denver, Colorado 80206-4805

1-800-525-0020

INTRODUCTION

This Prospectus/Information Statement is being furnished to shareholders of INTECH U.S. Managed Volatility Fund II (formerly named INTECH U.S. Growth Fund) in connection with an Agreement and Plan of Reorganization (the “Plan”), pursuant to which INTECH U.S. Managed Volatility Fund II (“your Fund” or the “Acquired Fund”) will merge into INTECH U.S. Managed Volatility Fund (together with your Fund, the “Funds” and each, a “Fund”). Under the Plan, you will receive shares of INTECH U.S. Managed Volatility Fund approximately equal in value to your holdings in the Acquired Fund as of the closing date of the reorganization, referred to herein as the “Merger.” After the Merger is complete, your Fund will be liquidated. The Merger is expected to be completed on or about April 24, 2015 (the “Closing Date”).

The Merger is designed to streamline the Janus mutual funds platform by consolidating similar funds. Recently, beginning on December 17, 2014, the Funds’ names, principal investment strategies, and benchmark indices were changed to reflect a new managed volatility investment strategy, which seeks to provide returns in excess of the Funds’ benchmark index and to reduce or “manage” portfolio volatility to a level less than such benchmark index. As a result of these changes, the Funds now have identical investment strategies and risks, and the same benchmark index. The Funds also have the same management fee structure and investment personnel, and same investment objective of long-term growth of capital, none of which will change as a result of the Merger.

After careful consideration, the Board of Trustees of the Janus Funds determined that the Merger is in the best interests of your Fund and of INTECH U.S. Managed Volatility Fund. The Board considered many factors in making this determination, which are summarized below in the Q&A section and discussed in detail in this Prospectus/Information Statement. Among the factors considered, the Board noted that the Merger will permit you to continue to invest in a fund that pursues an identical investment objective and investment strategies as your Fund and to do so in the context of a larger fund with expense ratios that are expected to be the same as, or lower than, both your Fund and INTECH U.S. Managed Volatility Fund prior to the Merger. In addition, the Board considered that Janus Capital Management LLC (“Janus Capital” or “Janus”) is paying all costs of the Merger, that the Merger is expected to be a tax-free reorganization for federal income tax purposes, and the belief of Janus Capital that a combined fund will have the potential for better growth prospects.

Shares of the Funds have not been approved or disapproved by the Securities and Exchange Commission nor has the Securities and Exchange Commission passed upon the adequacy of this Prospectus/Information Statement. Any representation to the contrary is a criminal offense.

Your Fund and INTECH U.S. Managed Volatility Fund are each a series of Janus Investment Fund (the “Trust”), an open-end, registered management investment company organized as a Massachusetts business trust. INTECH Investment Management LLC (“INTECH”) is responsible for the day-to-day management of each Fund’s investment portfolio subject to the general oversight of Janus Capital. Janus Capital provides certain administration and other services and is responsible for other business affairs of each Fund. After the Merger, Janus Capital will remain the investment adviser of INTECH U.S. Managed Volatility Fund, INTECH will remain the subadviser of INTECH U.S. Managed Volatility Fund, and the Fund’s investment personnel will continue as the investment personnel of INTECH U.S. Managed Volatility Fund. As one of the larger mutual fund sponsors in the United States, Janus sponsored 59 mutual funds and had approximately $107.4 billion in mutual fund assets under management as of December 31, 2014. INTECH sponsored 7 mutual funds and had approximately $1.6 billion in mutual fund assets under management as of December 31, 2014. The Merger is expected to offer shareholders the potential for increased operational efficiencies while giving them continued access to Janus’ and INTECH’s experience and resources in managing mutual funds.

This Prospectus/Information Statement, which you should read carefully and retain for future reference, sets forth the information that you should know about your Fund, INTECH U.S. Managed Volatility Fund, and the Merger. This Prospectus/Information Statement is being mailed to you on or about February 13, 2015.

Incorporation by Reference

For more information about the investment objectives, strategies, restrictions and risks of the Funds, see:

•

INTECH U.S. Managed Volatility Fund’s Prospectus for Class A Shares, Class C Shares, Class S Shares, Class I Shares, Class N Shares, and Class T Shares, filed in Post-Effective Amendment No. 208 to Janus Investment Fund’s registration statement on Form N-1A (File Nos. 811-01879 and 002-34393) (Accession No. 0000950123-14-010561), dated October 28, 2014, as supplemented;

•

your Fund’s Prospectus for Class A Shares, Class C Shares, Class S Shares, Class I Shares, Class N Shares, and Class T Shares filed in Post-Effective Amendment No. 208 to Janus Investment Fund’s registration statement on Form N-1A (File Nos. 811-01879 and 002-34393) (Accession No. 0000950123-14-010561), dated October 28, 2014, as supplemented;

•

INTECH U.S. Managed Volatility Fund’s Statement of Additional Information, filed in Post-Effective Amendment No. 208 to Janus Investment Fund’s registration statement on Form N-1A (File Nos. 811-01879 and 002-34393) (Accession No. 0000950123-14-010561), dated October 28, 2014;

•

your Fund’s Statement of Additional Information, filed in Post-Effective Amendment No. 208 to Janus Investment Fund’s registration statement on Form N-1A (File Nos. 811-01879 and 002-34393) (Accession No. 0000950123-14-010561), dated October 28, 2014;

•

INTECH U.S. Managed Volatility Fund’s Annual Report, filed on Form N-CSR (File No. 811-01879), for the fiscal year ended June 30, 2014 (Accession No. 0000950123-14-009518); and

•

your Fund’s Annual Report, filed on Form N-CSR (File No. 811-01879), for the fiscal year ended June 30, 2014 (Accession No. 0000950123-14-009518).

These documents have been filed with the U.S. Securities and Exchange Commission (“SEC”) and are incorporated by reference herein as appropriate. Your Fund’s Prospectus and its Annual Report and most recent Semiannual Report have previously been provided to third-party intermediaries for delivery to you.

The Funds provide annual and semiannual reports to their shareholders that highlight relevant information, including investment results and a review of portfolio changes. Additional copies of each Fund’s most recent annual and semiannual report are available, without charge, by contacting your plan sponsor, broker-dealer, or financial intermediary, or by contacting a Janus representative at 1-877-335-2687. The reports are also available, without charge, at janus.com/info, or by sending a written request to the Secretary of the Trust at 151 Detroit Street, Denver, Colorado 80206-4805.

A Statement of Additional Information dated February 6, 2015 relating to the Merger has been filed with the SEC and is incorporated by reference into this Prospectus/Information Statement. You can obtain a free copy of that document by contacting your plan sponsor, broker-dealer, or financial intermediary or by contacting a Janus representative at 1-800-525-0020.

The shares of the Funds are not deposits or obligations of, or guaranteed or endorsed by, any financial institution or the U.S. Government, are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other government agency, and involve risk, including the possible loss of the principal amount invested.

Each Fund is subject to the informational requirements of the Securities Exchange Act of 1934, as amended and the Investment Company Act of 1940, as amended (the “1940 Act”), and, in accordance therewith, files reports, proxy materials, and other information with the SEC. These reports and other information can be inspected and copied at the public reference facility maintained by the SEC at 100 F Street, NE, Washington, DC 20549 and the following regional offices of the SEC: Northeast Regional Office, 3 World Financial Center, Suite 400, New York, New York 10281; Midwest Regional Office, 175 West Jackson Boulevard, Suite 900, Chicago, Illinois 60604. Reports and other information about the Funds are available on the Electronic Data Gathering Analysis and Retrieval (EDGAR) Database on the SEC’s website at http://www.sec.gov. Copies of such material can also be obtained from the Public Reference Branch, Office of Consumer Affairs and Information Services, SEC, 100 F Street, NE, Washington, DC 20549 at prescribed rates.

This Prospectus/Information Statement is for informational purposes only. You do not need to take any action in response to this Prospectus/Information Statement. We are not asking you for a proxy or written consent, and you are requested not to send us a proxy or written consent.

The following chart outlines the impacted share classes and their respective ticker symbols:

| | Fund/Class | | | Ticker |

| | INTECH U.S. Managed Volatility Fund | | | |

| | Class A Shares | | | JRSAX |

| | Class C Shares | | | JRSCX |

| | Class I Shares | | | JRSIX |

| | Class N Shares | | | JRSNX |

| | Class S Shares | | | JRSSX |

| | Class T Shares | | | JRSTX |

| | Your Fund | | | |

| | Class A Shares | | | JDRAX |

| | Class C Shares | | | JCGCX |

| | Class I Shares | | | JRMGX |

| | Class N Shares | | | JGRNX |

| | Class S Shares | | | JCGIX |

| | Class T Shares | | | JDRTX |

PROSPECTUS/INFORMATION STATEMENT

February 6, 2015

TABLE OF CONTENTS

Q&A / SYNOPSIS

This Prospectus/Information Statement provides a brief overview of the key features and other matters typically of concern to shareholders affected by a merger between mutual funds. These responses are qualified in their entirety by the remainder of this Prospectus/Information Statement, which you should read carefully. It contains additional information and further details regarding the Merger. The description of the Merger is qualified by reference to the full text of the Plan, a form of which is attached as Appendix A.

Q.

What is happening?

A.

The Merger is part of a restructuring that is designed to streamline the Janus mutual funds platform. On September 17, 2014, the Board of Trustees of the Trust (the “Board of Trustees,” the “Board,” or the “Trustees”) approved changes to the investment strategies, names, and benchmark indices of the Funds to reflect a new managed volatility investment strategy. The managed volatility strategy seeks to reduce or “manage” portfolio volatility to a level less than each Fund’s benchmark index. Specifically, the managed volatility strategy seeks, over time, returns above each Fund’s benchmark index, with absolute volatility lower than the benchmark index, as described below. In approving these changes, the Board concluded, among other things, that moving to a managed volatility strategy could assist the Funds in growing in size over time and could benefit shareholders. As a result of these changes, which became effective on December 17, 2014, the Funds have identical investment strategies and risks, and the same benchmark index.

At a meeting held on November 5, 2014, the Board approved the Plan, which authorizes the Merger of your Fund with and into INTECH U.S. Managed Volatility Fund, with INTECH U.S. Managed Volatility Fund being the surviving entity. The Merger is part of an effort to streamline the number of funds on the Janus mutual funds platform. Your Fund and INTECH U.S. Managed Volatility Fund are each a series of the Trust and are managed by INTECH subject to the general oversight of Janus Capital. The Board of Trustees concluded that the Merger is in the best interest of both Funds, and that the interests of shareholders of the Funds will not be diluted as a result of the Merger. You are receiving this Prospectus/Information Statement because you are a shareholder of the Acquired Fund and will be impacted by the Merger. This Prospectus/Information Statement is being provided to you for informational purposes only, and you need not take any action with regard to the Merger.

Q.

What did the Board consider in approving the Merger?

A.

In approving the Merger, the Board considered a number of factors, including the following:

•

The Merger will permit you to continue to invest in a fund that pursues an identical investment objective and investment strategies as your Fund and to do so in the context of a larger fund with expense ratios that are expected to be lower than or the same as both your Fund and INTECH U.S. Managed Volatility Fund prior to the Merger.

•

The investment personnel that currently manage your Fund and INTECH U.S. Managed Volatility Fund will continue to manage INTECH U.S. Managed Volatility Fund after the Merger.

•

Comparative performance of the Funds over various time periods.

•

The Merger is expected to be a tax-free reorganization for federal income tax purposes.

•

The structure of the Merger.

•

The impact of the Merger on each Fund’s tax-loss carryforward positions.

•

Janus Capital is paying all costs associated with the Merger.

•

Janus Capital will benefit from greater operational efficiencies by overseeing a single Fund versus two separate Funds with identical investment strategies, policies, and risks.

•

The Merger is designed to streamline the number of INTECH subadvised Funds within the Trust, encourage a more focused marketing and distribution effort for the combined fund, reduce investor confusion, and generally make INTECH U.S. Managed Volatility Fund a more attractive vehicle to the investing public, which Janus Capital believes could provide the potential for better growth prospects as compared to the two Funds operating separately.

Q.

What is happening in the Merger?

A.

All or substantially all of the assets of your Fund will be transferred to INTECH U.S. Managed Volatility Fund solely in exchange for shares of INTECH U.S. Managed Volatility Fund with a value approximately equal to the value of your Fund’s assets net of liabilities, and the assumption by INTECH U.S. Managed Volatility Fund of all liabilities of your Fund. Immediately following the transfer, the shares of INTECH U.S. Managed Volatility Fund received by your Fund will be distributed pro rata to you as a shareholder of record as of the Closing Date (on or about April 24, 2015). After the Merger is completed, your Fund will be liquidated. The Merger is conditioned upon receipt of an opinion of counsel substantially to the

effect that the Merger qualifies as a tax-free reorganization for federal income tax purposes, and any other conditions as outlined in the Plan.

Q.

Will I own the same number of shares of INTECH U.S. Managed Volatility Fund as I currently own of the Acquired Fund?

A.

Immediately after the Closing Date, you will own a number of full and fractional shares of INTECH U.S. Managed Volatility Fund approximately equivalent in dollar value to your shares held in the Acquired Fund as of the close of business on the Closing Date. You will receive the same class of shares of INTECH U.S. Managed Volatility Fund as the class of shares of the Acquired Fund you own as of the Merger. However, the number of shares you receive will depend on the relative net asset values of the shares of your Fund and INTECH U.S. Managed Volatility Fund as of the close of trading on the New York Stock Exchange (“NYSE”) on the business day prior to the closing of the Merger. Therefore, although the dollar value of your shares will be approximately the same, the number of shares you own may change.

Q.

How do the Funds’ investment objectives, strategies, and risks compare?

A.

As discussed above, in connection with the Funds’ transition to a new managed volatility strategy beginning on December 17, 2014, the Funds’ principal investment strategies and benchmark indices were changed to reflect this new investment approach. As a result of these changes, the Funds have identical investment strategies and risks, and the same benchmark index. Each Fund seeks long-term growth of capital by investing, under normal circumstances, at least 80% of its net assets in U.S. common stocks from the universe of the Russell 1000® Index, utilizing INTECH’s mathematical investment process, applying a managed volatility approach. The Funds seek to produce returns in excess of the Russell 1000® Index, but with lower absolute volatility. In this context, absolute volatility refers to the variation in the returns of each Fund and the benchmark index as measured by standard deviation. This range is expected to be closer to 0% in less volatile markets and will increase as market conditions become more volatile. Each Fund’s principal risks include market risk, investment process risk, real estate securities risk, portfolio turnover risk, and securities lending risk.

Prior to December 17, 2014, the Funds had different names, principal investment strategies, and benchmark indices. Your Fund’s name was INTECH U.S. Growth Fund and it invested, under normal circumstances, at least 80% of its net assets in U.S. common stocks from the universe of the Russell 1000® Growth Index, utilizing INTECH’s mathematical process, but without applying a managed volatility approach. Similarly, prior to December 17, 2014, INTECH Managed Volatility Fund’s name was INTECH U.S. Value Fund and it invested, under normal circumstances, at least 80% of its net assets in U.S. common stocks from the universe of the Russell 1000® Value Index, utilizing INTECH’s mathematical process, but without applying a managed volatility approach.

Q.

How do the Funds compare in size?

A.

As of December 31, 2014, your Fund’s net assets were approximately $285.0 million, and INTECH U.S. Managed Volatility Fund’s net assets were approximately $84.3 million. The asset size of each Fund fluctuates on a daily basis, and the asset size of INTECH U.S. Managed Volatility Fund after the Merger may be larger or smaller than the combined assets of the Funds as of December 31, 2014. More current total net asset information is available at janus.com/advisor/mutual-funds.

Q.

Will the Merger result in a higher management fee rate for current Acquired Fund shareholders?

A.

No. Each Fund currently has the same management fee structure, which will not change as a result of the Merger. Pro forma fee, expense, and other financial information is included in this Prospectus/Information Statement.

Q.

Will the Merger result in higher Fund expense ratios?

A.

Fund expense ratios are expected to be lower than or the same as those of your Fund after the Merger. The estimated fees and expenses are shown in the pro forma fee, expense, and financial information included later in this Prospectus/Information Statement.

Q.

What are the federal income tax consequences of the Merger?

A.

The Merger is expected to qualify as a tax-free reorganization for federal income tax purposes (under section 368(a) of the Internal Revenue Code of 1986, as amended) and will not take place unless counsel provides an opinion substantially to that effect. Shareholders should not recognize any capital gain or loss as a direct result of the Merger. If you choose to redeem or exchange your shares before or after the Merger, you may realize a taxable gain or loss; therefore, consider consulting a tax adviser before doing so. Prior to the Closing Date, the Acquired Fund may make a distribution to its shareholders, which together with all previous distributions, will have the effect of distributing to shareholders at least all its net investment income

and realized net capital gains (after reduction by any available capital loss carryforwards), if any, through the Closing Date of the Merger. This distribution will be taxable to shareholders who are subject to federal income tax and may include gains resulting from the sale of portfolio assets related to the transitioning of your Fund’s portfolio.

Q.

Will the services provided by Janus Capital or INTECH change?

A.

No. INTECH currently manages both your Fund and INTECH U.S. Managed Volatility Fund and will continue as the subadviser, with Janus Capital continuing as the investment adviser and administrator, of INTECH U.S. Managed Volatility Fund following the Merger. The custodian, transfer agent, and distributor are the same for the Funds and will not change as a result of the Merger. You will also have the same purchase and redemption privileges from INTECH U.S. Managed Volatility Fund as you currently enjoy. Please consult your financial intermediary for information on any services provided by them to the Funds.

Q.

Will there be any sales load, commission, or other transactional fee in connection with the Merger?

A.

No. There will be no sales load, commission, or other transactional fee in connection with the Merger. The full and fractional value of shares of your Fund will be exchanged for full and fractional corresponding shares of INTECH U.S. Managed Volatility Fund having approximately equal value, without any sales load, commission or other transactional fee being imposed.

Q.

Can I still add to my existing Acquired Fund account until the Merger?

A.

Yes. You may continue to make additional investments in the Acquired Fund until the Closing Date (anticipated to be on or about April 24, 2015) unless the Board of Trustees determines to limit future investments to ensure a smooth transition of shareholder accounts or for any other reason. Effective at the close of trading on Friday, December 26, 2014, the Acquired Fund closed to new investors.

Q.

Will I need to open an account in INTECH U.S. Managed Volatility Fund prior to the Merger?

A.

No. An account will be set up in your name, and your shares of the Acquired Fund will automatically be converted to corresponding shares of INTECH U.S. Managed Volatility Fund. You will receive confirmation of this transaction following the Merger.

Q.

Will my cost basis for federal income tax purposes change as a result of the Merger?

A.

Your total cost basis for federal income tax purposes is not expected to change as a result of the Merger. However, since the number of shares you hold after the Merger may be different than the number of shares you held prior to the Merger, your cost basis per share may change. Since the Merger will be treated as a tax-free reorganization for federal income tax purposes, you should not recognize any capital gain or loss for federal income tax purposes as a direct result of the Merger.

Q.

Will either Fund pay fees associated with the Merger?

A.

The Funds will not pay any fees associated with the Merger. Janus Capital will bear those fees, which are estimated to be $100,000, plus out-of-pocket expenses.

Q.

When will the Merger take place?

A.

The Merger will occur on or about April 24, 2015. After completion of the Merger, your financial intermediary, plan sponsor, or Janus (if you hold Class I Shares directly with the Fund) is responsible for sending you a confirmation statement reflecting your new Fund account number and number of shares owned.

Q.

What if I want to exchange my shares into another Janus fund prior to the Merger?

A.

You may exchange your shares into another Janus fund before the Closing Date (on or about April 24, 2015) in accordance with your pre-existing exchange privileges by contacting your plan sponsor, broker-dealer, or financial intermediary or by contacting a Janus representative at 1-800-525-0020. If you choose to exchange your shares of the Acquired Fund for another Janus fund, your request will be treated as a normal exchange of shares and will be a taxable transaction unless your shares are held in a tax-deferred account, such as an individual retirement account (“IRA”). Exchanges may be subject to minimum investment requirements. Any applicable contingent deferred sales charges charged to Class A and Class C Shares will be waived for exchanges and redemptions through the date of the Merger.

Q.

Why are shareholders not being asked to vote on the Merger?

A.

The Funds’ Amended and Restated Agreement and Declaration of Trust dated March 18, 2003, as amended from time to time (“Trust Instrument”) permits mergers between series of the Trust to occur without seeking a shareholder vote provided that certain conditions are met. The conditions permitting the Merger to occur without seeking a shareholder vote have been met.

SUMMARY OF THE FUNDS

This section provides a summary of each Fund, including but not limited to, comparative information regarding each Fund’s investment objective, primary investment strategies, restrictions, fees, and historical performance. Please note that this is only a brief discussion and is qualified in its entirety by reference to the complete information contained herein. There is no assurance that a Fund will achieve its stated objective.

Investment Objectives

Both Funds seek long-term growth of capital.

Comparison of Fees and Expenses

The types of expenses currently paid by each class of shares of your Fund are the same types of expenses to be paid by the corresponding share classes of INTECH U.S. Managed Volatility Fund. Currently, the Funds have substantially similar investment advisory agreements and each pays the same investment advisory fee rate. The annual investment advisory fee rate payable under the advisory agreements for your Fund and INTECH U.S. Managed Volatility Fund is currently 0.50% of each Fund’s average daily net assets. After the Merger, INTECH U.S. Managed Volatility Fund will continue to pay the annual investment advisory fee rate of 0.50%. Janus Capital, and not the Funds, pays INTECH a subadvisory fee at the annual rate of 50% of the advisory fee rate paid by the Fund to Janus Capital.

Current and Pro Forma Fees and Expenses

The following tables compare the fees and expenses you may bear directly or indirectly as an investor in your Fund versus INTECH U.S. Managed Volatility Fund, and show the projected (“pro forma”) estimated fees and expenses of INTECH U.S. Managed Volatility Fund, calculated assuming the Merger had occurred on June 30, 2014. Fees and expenses shown for your Fund and INTECH U.S. Managed Volatility Fund were determined based on each Fund’s average net assets as of the fiscal year ended June 30, 2014. The pro forma fees and expenses are estimated in good faith by Janus Capital and are hypothetical, and do not reflect any change in expense ratios resulting from a change in assets under management since June 30, 2014 for either Fund. More current total net asset information is available at janus.com/advisor/mutual-funds. It is important for you to know that a decline in a Fund’s average net assets during the current fiscal year and after the Merger, as a result of market volatility or other factors, could cause the Fund’s expense ratio to be higher than the fees and expenses shown, which means you could pay more if you buy or hold shares of the Fund. The Funds will not pay any fees of the Merger.

Annual Fund Operating Expenses

Annual Fund Operating Expenses are paid out of a Fund’s assets and include fees for portfolio management and administrative services, including recordkeeping, accounting or subaccounting, and other shareholder services. You do not pay these fees directly, but as the examples in the table below show, these costs are borne indirectly by all shareholders.

The Annual Fund Operating Expenses shown in the table below represent annualized expenses for your Fund and for INTECH U.S. Managed Volatility Fund, as well as those estimated for your Fund on a pro forma basis, assuming consummation of the Merger, for the fiscal year ended June 30, 2014.

Expense Limitations

Currently, through November 1, 2015, pursuant to a contract between Janus Capital and your Fund, Janus Capital reduces its annual investment advisory fee rate paid by your Fund by the amount by which the total annual fund operating expenses allocated to any class of the Fund exceed 0.83% of average daily net assets for the fiscal year (after reduction of any applicable share class level expenses). For purposes of this waiver, operating expenses do not include the distribution and shareholder servicing (12b-1) fees (applicable to Class A Shares, Class C Shares, and Class S Shares), administrative services fees payable pursuant to the Transfer Agency Agreement (including out-of-pocket expenses), or items not normally considered operating expenses, such as acquired fund fees and expenses, interest, dividends, taxes, brokerage commissions and extraordinary expenses (including, but not limited to, legal claims and liabilities and litigation costs, and any indemnification related thereto). Janus Capital has a similar expense limitation agreement for INTECH U.S. Managed Volatility Fund whereby Janus Capital reduces its annual investment

advisory fee rate paid by INTECH U.S. Managed Volatility Fund by the amount by which the total annual fund operating expenses allocated to any class of the Fund exceed 0.79% of average daily net assets for the fiscal year (after reduction of any applicable share class level expenses and excluding the same expenses noted above). During the period shown in the table below, INTECH U.S. Managed Volatility Fund’s total annual fund operating expenses, after reduction of any applicable share class level expenses, did not exceed 0.79% of average daily net assets.

Changes to expenses and asset levels of both your Fund and INTECH U.S. Managed Volatility Fund at the time of the Merger could trigger application of INTECH U.S. Managed Volatility Fund’s 0.79% expense limit, resulting in a possible reduction of other expenses for certain classes and the investment advisory fee rate payable to Janus Capital by INTECH U.S. Managed Volatility Fund.

SHAREHOLDER FEES (fees paid directly from your investment)

Class A Shares | | | Your Fund | | | INTECH

U.S. Managed

Volatility Fund | | | INTECH

U.S. Managed

Volatility Fund

Pro Forma | |

| Maximum Sales Charge (load) Imposed on Purchases (as a percentage of offering price) | | | 5.75% | | | 5.75% | | | 5.75% | |

| Maximum Deferred Sales Charge (load) (as a percentage of the lower of original purchase price or redemption proceeds) | | | None | | | None | | | None | |

ANNUAL FUND OPERATING EXPENSES

(expenses that you pay each year as a percentage of the value of your investment)(1) | | | | | | | | | | |

| Management Fees(2) | | | 0.50% | | | 0.50% | | | 0.50% | |

| Distribution/Service (12b-1) Fees(3) | | | 0.25% | | | 0.25% | | | 0.25% | |

| Other Expenses(4) | | | 0.20% | | | 0.28% | | | 0.20% | |

| Acquired Fund Fees and Expenses(5) | | | 0.00% | | | 0.01% | | | 0.00% | |

| Total Annual Fund Operating Expenses | | | 0.95% | | | 1.04% | | | 0.95% | |

SHAREHOLDER FEES (fees paid directly from your investment)

Class C Shares | | | Your Fund | | | INTECH

U.S. Managed

Volatility Fund | | | INTECH

U.S. Managed

Volatility Fund

Pro Forma | |

| Maximum Sales Charge (load) Imposed on Purchases (as a percentage of offering price) | | | None | | | None | | | None | |

| Maximum Deferred Sales Charge (load) (as a percentage of the lower of original purchase price or redemption proceeds) | | | 1.00% | | | 1.00% | | | 1.00% | |

ANNUAL FUND OPERATING EXPENSES

(expenses that you pay each year as a percentage of the value of your investment)(1) | | | | | | | | | | |

| Management Fees(2) | | | 0.50% | | | 0.50% | | | 0.50% | |

| Distribution/Service (12b-1) Fees(3) | | | 1.00% | | | 1.00% | | | 1.00% | |

| Other Expenses(4) | | | 0.09% | | | 0.24% | | | 0.08% | |

| Acquired Fund Fees and Expenses(5) | | | 0.00% | | | 0.01% | | | 0.00% | |

| Total Annual Fund Operating Expenses | | | 1.59% | | | 1.75% | | | 1.58% | |

SHAREHOLDER FEES (fees paid directly from your investment)

Class S Shares | | | Your Fund | | | INTECH

U.S. Managed

Volatility Fund | | | INTECH

U.S. Managed

Volatility Fund

Pro Forma | |

| Maximum Sales Charge (load) Imposed on Purchases (as a percentage of offering price) | | | None | | | None | | | None | |

| Maximum Deferred Sales Charge (load) (as a percentage of the lower of original purchase price or redemption proceeds) | | | None | | | None | | | None | |

ANNUAL FUND OPERATING EXPENSES

(expenses that you pay each year as a percentage of the value of your investment)(1) | | | | | | | | | | |

| Management Fees(2) | | | 0.50% | | | 0.50% | | | 0.50% | |

| Distribution/Service (12b-1) Fees(3) | | | 0.25% | | | 0.25% | | | 0.25% | |

| Other Expenses(4) | | | 0.31% | | | 0.48% | | | 0.30% | |

| Acquired Fund Fees and Expenses(5) | | | 0.00% | | | 0.01% | | | 0.00% | |

| Total Annual Fund Operating Expenses | | | 1.06% | | | 1.24% | | | 1.05% | |

SHAREHOLDER FEES (fees paid directly from your investment)

Class I Shares | | | Your Fund | | | INTECH

U.S. Managed

Volatility Fund | | | INTECH

U.S. Managed

Volatility Fund

Pro Forma | |

| Maximum Sales Charge (load) Imposed on Purchases (as a percentage of offering price) | | | None | | | None | | | None | |

| Maximum Deferred Sales Charge (load) (as a percentage of the lower of original purchase price or redemption proceeds) | | | None | | | None | | | None | |

ANNUAL FUND OPERATING EXPENSES

(expenses that you pay each year as a percentage of the value of your investment)(1) | | | | | | | | | | |

| Management Fees(2) | | | 0.50% | | | 0.50% | | | 0.50% | |

| Distribution/Service (12b-1) Fees(3) | | | None | | | None | | | None | |

| Other Expenses(4) | | | 0.11% | | | 0.16% | | | 0.09% | |

| Acquired Fund Fees and Expenses(5) | | | 0.00% | | | 0.01% | | | 0.00% | |

| Total Annual Fund Operating Expenses | | | 0.61% | | | 0.67% | | | 0.59% | |

SHAREHOLDER FEES (fees paid directly from your investment)

Class N Shares | | | Your Fund | | | INTECH

U.S. Managed

Volatility Fund | | | INTECH

U.S. Managed

Volatility Fund

Pro Forma | |

| Maximum Sales Charge (load) Imposed on Purchases (as a percentage of offering price) | | | None | | | None | | | None | |

| Maximum Deferred Sales Charge (load) (as a percentage of the lower of original purchase price or redemption proceeds) | | | None | | | None | | | None | |

ANNUAL FUND OPERATING EXPENSES

(expenses that you pay each year as a percentage of the value of your investment)(1) | | | | | | | | | | |

| Management Fees(2) | | | 0.50% | | | 0.50% | | | 0.50% | |

| Distribution/Service (12b-1) Fees(3) | | | None | | | None | | | None | |

| Other Expenses(4) | | | 0.07% | | | 0.16% | | | 0.06% | |

| Acquired Fund Fees and Expenses(5) | | | 0.00% | | | 0.01% | | | 0.00% | |

| Total Annual Fund Operating Expenses | | | 0.57% | | | 0.67% | | | 0.56% | |

SHAREHOLDER FEES (fees paid directly from your investment)

Class T Shares | | | Your Fund | | | INTECH

U.S. Managed

Volatility Fund | | | INTECH

U.S. Managed

Volatility Fund

Pro Forma | |

| Maximum Sales Charge (load) Imposed on Purchases (as a percentage of offering price) | | | None | | | None | | | None | |

| Maximum Deferred Sales Charge (load) (as a percentage of the lower of original purchase price or redemption proceeds) | | | None | | | None | | | None | |

ANNUAL FUND OPERATING EXPENSES

(expenses that you pay each year as a percentage of the value of your investment)(1) | | | | | | | | | | |

| Management Fees(2) | | | 0.50% | | | 0.50% | | | 0.50% | |

| Distribution/Service (12b-1) Fees(3) | | | None | | | None | | | None | |

| Other Expenses(4) | | | 0.31% | | | 0.40% | | | 0.31% | |

| Acquired Fund Fees and Expenses(5) | | | 0.00% | | | 0.01% | | | 0.00% | |

| Total Annual Fund Operating Expenses | | | 0.81% | | | 0.91% | | | 0.81% | |

EXAMPLES:

These Examples are intended to help you compare the cost of investing in your Fund and INTECH U.S. Managed Volatility Fund before the Merger, and INTECH U.S. Managed Volatility Fund after the Merger with the cost of investing in other mutual funds. The Examples assume that you invest $10,000 in your Fund, INTECH U.S. Managed Volatility Fund, and the combined Fund after the Merger for the time periods indicated and reinvest all dividends and distributions. The Examples also assume that your investment has a 5% return each year and that the Funds’ operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| If Shares are redeemed: | | | 1 Year(6)(7)(8) | | | 3 Years(6)(9) | | | 5 Years(6)(9) | | | 10 Years(6)(9) | |

| Class A Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 666 | | | | | $ | 860 | | | | | $ | 1,070 | | | | | $ | 1,674 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 675 | | | | | $ | 887 | | | | | $ | 1,116 | | | | | $ | 1,773 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 666 | | | | | $ | 860 | | | | | $ | 1,070 | | | | | $ | 1,674 | | |

| Class C Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 262 | | | | | $ | 502 | | | | | $ | 866 | | | | | $ | 1,889 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 278 | | | | | $ | 551 | | | | | $ | 949 | | | | | $ | 2,062 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 261 | | | | | $ | 499 | | | | | $ | 860 | | | | | $ | 1,878 | | |

| Class S Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 108 | | | | | $ | 337 | | | | | $ | 585 | | | | | $ | 1,294 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 126 | | | | | $ | 393 | | | | | $ | 681 | | | | | $ | 1,500 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 107 | | | | | $ | 334 | | | | | $ | 579 | | | | | $ | 1,283 | | |

| Class I Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 62 | | | | | $ | 195 | | | | | $ | 340 | | | | | $ | 762 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 68 | | | | | $ | 214 | | | | | $ | 373 | | | | | $ | 835 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 60 | | | | | $ | 189 | | | | | $ | 329 | | | | | $ | 738 | | |

| If Shares are redeemed: | | | 1 Year(6)(7)(8) | | | 3 Years(6)(9) | | | 5 Years(6)(9) | | | 10 Years(6)(9) | |

| Class N Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 58 | | | | | $ | 183 | | | | | $ | 318 | | | | | $ | 714 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 68 | | | | | $ | 214 | | | | | $ | 373 | | | | | $ | 835 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 57 | | | | | $ | 179 | | | | | $ | 313 | | | | | $ | 701 | | |

| Class T Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 83 | | | | | $ | 259 | | | | | $ | 450 | | | | | $ | 1,002 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 93 | | | | | $ | 290 | | | | | $ | 504 | | | | | $ | 1,120 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 83 | | | | | $ | 259 | | | | | $ | 450 | | | | | $ | 1,002 | | |

| If Shares are not redeemed: | | | 1 Year(6)(7)(9) | | | 3 Years(6)(9) | | | 5 Years(6)(9) | | | 10 Years(6)(9) | |

| Class A Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 666 | | | | | $ | 860 | | | | | $ | 1,070 | | | | | $ | 1,674 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 675 | | | | | $ | 887 | | | | | $ | 1,116 | | | | | $ | 1,773 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 666 | | | | | $ | 860 | | | | | $ | 1,070 | | | | | $ | 1,674 | | |

| Class C Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 162 | | | | | $ | 502 | | | | | $ | 866 | | | | | $ | 1,889 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 178 | | | | | $ | 551 | | | | | $ | 949 | | | | | $ | 2,062 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 161 | | | | | $ | 499 | | | | | $ | 860 | | | | | $ | 1,878 | | |

| Class S Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 108 | | | | | $ | 337 | | | | | $ | 585 | | | | | $ | 1,294 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 126 | | | | | $ | 393 | | | | | $ | 681 | | | | | $ | 1,500 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 107 | | | | | $ | 334 | | | | | $ | 579 | | | | | $ | 1,283 | | |

| Class I Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 62 | | | | | $ | 195 | | | | | $ | 340 | | | | | $ | 762 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 68 | | | | | $ | 214 | | | | | $ | 373 | | | | | $ | 835 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 60 | | | | | $ | 189 | | | | | $ | 329 | | | | | $ | 738 | | |

| Class N Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 58 | | | | | $ | 183 | | | | | $ | 318 | | | | | $ | 714 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 68 | | | | | $ | 214 | | | | | $ | 373 | | | | | $ | 835 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 57 | | | | | $ | 179 | | | | | $ | 313 | | | | | $ | 701 | | |

| Class T Shares | | | | | | | | | | | | | | | | | | | | | | | | | |

| Your Fund | | | | $ | 83 | | | | | $ | 259 | | | | | $ | 450 | | | | | $ | 1,002 | | |

| INTECH U.S. Managed Volatility Fund | | | | $ | 93 | | | | | $ | 290 | | | | | $ | 504 | | | | | $ | 1,120 | | |

INTECH U.S. Managed Volatility Fund (pro forma assuming consummation of the Merger) | | | | $ | 83 | | | | | $ | 259 | | | | | $ | 450 | | | | | $ | 1,002 | | |

(1)

All expenses are shown without the effect of expense offset arrangements. Pursuant to such arrangements, credits realized as a result of uninvested cash balances are used to reduce custodian and transfer agent expenses.

(2)

The “Management Fee” is the management fee rate paid by each Fund to Janus under each Investment Advisory Agreement. Refer to the “Management Expenses” section in this Prospectus/Information Statement for additional information, with further description in the Funds’ Statement of Additional Information, which are incorporated by reference herein.

(3)

If applicable to the share class, because 12b-1 fees are charged as an ongoing fee, over time the fee will increase the cost of your investment and may cost you more than paying other types of sales charges. Distribution/Service (12b-1) Fees include a shareholder servicing fee of up to 0.25% for Class C Shares.

(4)

“Other Expenses” for Class A Shares, Class C Shares, and Class I Shares may include administrative fees charged by intermediaries for the provision of administrative services, including recordkeeping, subaccounting, order processing for omnibus or networked accounts, or other shareholder services provided

on behalf of shareholders of the Funds. “Other Expenses” for Class S Shares and Class T Shares include an administrative services fee of up to 0.25% of the average daily net assets of each class to compensate Janus Services LLC (“Janus Services”), the Funds’ transfer agent, for providing, or arranging for the provision by intermediaries of, administrative services, including recordkeeping, subaccounting, order processing for omnibus or networked accounts, or other shareholder services provided on behalf of retirement plan participants, pension plan participants, or other underlying investors investing through institutional channels. “Other Expenses” for all classes may include reimbursement to Janus of its out-of-pocket costs for services as administrator and to Janus Services of its out-of-pocket costs for serving as transfer agent and providing, or arranging by others the provision of, servicing to shareholders.

(5)

“Acquired Fund” refers to any underlying fund (including, but not limited to, exchange-traded funds) in which a fund invests or has invested during the period. Acquired fund fees and expenses are indirect expenses a Fund incurs as a result of investing in shares of an underlying fund. A Fund’s “Total Annual Fund Operating Expenses” may not correlate to the “ratio of gross expenses to average net assets” presented in the Financial Highlights tables because that ratio includes only the direct operating expenses incurred by the Fund, not the indirect costs of investing in Acquired Funds. Acquired Fund Fees and Expenses are based on the estimated expenses each Fund expects to incur. If applicable, or unless otherwise indicated in a Fund’s Fees and Expenses table, such amounts are less than 0.01% and are included in the Fund’s “Other Expenses.”

(6)

Assumes the payment of the maximum initial sales charge on Class A Shares at the time of purchase for the Funds. The sales charge may be waived or reduced for certain investors, which would reduce the expenses for those investors.

(7)

A contingent deferred sales charge of up to 1.00% may be imposed on certain redemptions of Class A Shares bought without an initial sales charge and then redeemed within 12 months of purchase. The contingent deferred sales charge is not reflected in the Examples.

(8)

A contingent deferred sales charge of 1.00% generally applies on Class C Shares redeemed within 12 months of purchase. The contingent deferred sales charge may be waived for certain investors, as described in Appendix C.

(9)

Contingent deferred sales charge is not applicable.

Portfolio Turnover

Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Examples, affect the Funds’ performance. During the fiscal year ended June 30, 2014, your Fund’s portfolio turnover rate was 110% of the average value of its portfolio and INTECH U.S. Managed Volatility Fund’s portfolio turnover rate was 150% of the average value of its portfolio.

Comparison of Principal Investment Strategies

In connection with the Funds’ transition to a new managed volatility strategy beginning on December 17, 2014, the principal investment strategies and benchmark indices of the Funds were changed, resulting in their becoming identical. The following table summarizes the Funds’ principal investment strategies, as set forth more fully in the Prospectuses and Statement of Additional Information relating to the Funds.

| | | | | Both Funds | |

| | Principal Investment Strategies | | | The Funds invest, under normal circumstances, at least 80% of their net assets in U.S. common stocks from the universe of the Russell 1000® Index, utilizing INTECH’s mathematical investment process, applying a managed volatility approach. The Russell 1000® Index is an unmanaged index that measures the performance of the large-cap segment of the U.S. equity universe. The Funds seek to produce returns in excess of the Russell 1000® Index, but with lower absolute volatility than the benchmark index. The Funds seek to generate such excess returns with absolute volatility that can range from approximately 0% to 40% lower than the Russell 1000® Index. In this context, absolute volatility refers to the variation in the returns of each Fund and the benchmark index as measured by standard deviation. This range is expected to be closer to 0% in less volatile markets and will increase as market conditions become more volatile. | |

| | | | | Each Fund pursues its investment objective by applying a mathematical investment process to construct an investment portfolio from the universe of stocks within the named benchmark index. The goal of this process is to combine stocks that individually have higher relative volatility, lower absolute volatility, and lower correlations with each other in an effort to reduce each Fund’s absolute volatility, while still generating returns that exceed the named benchmark index over a full market cycle (a time period representing a significant market decline and recovery). Although each Fund may underperform its named benchmark index in sharply rising markets, this strategy seeks to participate in normal rising markets and lessen losses in down markets. In applying this strategy, INTECH establishes target proportions of its holdings from stocks within the named benchmark index using an optimization process designed to determine the most effective weightings of each stock in each Fund. Once INTECH determines such proportions and each Fund’s investments are selected, each Fund is periodically rebalanced to the set target proportions and re-optimized. The rebalancing techniques used by INTECH may result in a higher portfolio turnover rate compared to a “buy and hold” fund strategy. | |

Principal Investment Risks

The Funds have identical principal risk factors. The following summarizes the principal risks of investing in either of the Funds.

•

Market Risk. The value of the Fund’s portfolio may decrease if the value of an individual company or security, or multiple companies or securities, in the portfolio decreases. Further, regardless of how well individual companies or securities perform, the value of the Fund’s portfolio could also decrease if there are deteriorating economic or market conditions. It is important to understand that the value of your investment may fall, sometimes sharply, in response to changes in the market and you could lose money.

•

Investment Process Risk. The focus on managed volatility may keep the Fund from achieving excess returns over the named benchmark index. In this regard, INTECH’s managed volatility strategy may underperform the Fund’s named benchmark index during certain periods of up markets, and in particular, most likely will underperform the benchmark index in sharply rising markets, and may not achieve the desired level of protection in down markets. As INTECH’s mathematical investment process has evolved, it has experienced periods of both underperformance and outperformance relative to an identified benchmark index. Even when the proprietary mathematical investment process is working appropriately, INTECH expects that there will be periods of underperformance relative to the benchmark index. On an occasional basis, INTECH makes changes to its mathematical investment process that do not require shareholder notice. These changes may result in changes to the portfolio, might not provide the intended results, and may adversely impact the Fund’s performance.

•

Real Estate Securities Risk. The Fund’s performance may be affected by the risks associated with investments in real estate related companies. The value of real estate-related companies’ securities is sensitive to changes in real estate values and rental income, property taxes, interest rates, tax and regulatory requirements, supply and demand, and the management skill and creditworthiness of the company. Investments in real estate investment trusts (“REITs”) involve the same risks as other real estate investments. In addition, a REIT could fail to qualify for tax-free pass-through of its income under the Internal Revenue Code or fail to maintain its exemption from registration under the Investment Company Act of 1940, as amended, which could produce adverse economic consequences for the REIT and its investors, including the Fund.

•

Portfolio Turnover Risk. Increased portfolio turnover may result in higher costs, which may have a negative effect on the Fund’s performance. In addition, higher portfolio turnover may result in the acceleration of capital gains and the recognition of greater levels of short-term capital gains, which are taxed at ordinary federal income tax rates when distributed to shareholders.

•

Securities Lending Risk. The Fund may seek to earn additional income through lending its securities to certain qualified broker-dealers and institutions. There is the risk that when portfolio securities are lent, the securities may not be returned on a timely basis, and the Fund may experience delays and costs in recovering the security or gaining access to the collateral provided to the Fund to collateralize the loan. If the Fund is unable to recover a security on loan, the Fund may use the collateral to purchase replacement securities in the market. There is a risk that the value of the collateral could decrease below the cost of the replacement security by the time the replacement investment is made, resulting in a loss to the Fund.

An investment in a Fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Comparison of Fund Performance

Your Fund

The following information provides some indication of the risks of investing in your Fund showing how your Fund’s performance has varied over time. Class S Shares, Class A Shares, Class C Shares, and Class I Shares of the Fund commenced operations on July 6, 2009, after the reorganization of each corresponding class of shares of Janus Adviser INTECH Risk-Managed Growth Fund (“JAD predecessor fund”) into each respective share class of the Fund. Class T Shares of the Fund commenced operations on July 6, 2009.

•

The performance shown for Class S Shares for periods prior to July 6, 2009, reflects the historical performance of the JAD predecessor fund’s Class S Shares prior to the reorganization, calculated using the fees and expenses of the JAD predecessor fund’s Class S Shares, net of any applicable fee and expense limitations or waivers.

•

The performance shown for Class A Shares reflects the performance of the JAD predecessor fund’s Class A Shares from September 30, 2004 to July 6, 2009 (prior to the reorganization), calculated using the fees and expenses of Class A Shares of the JAD predecessor fund, net of any applicable fee and expense limitations or waivers. Performance shown for certain

periods prior to September 30, 2004 reflects the historical performance of the JAD predecessor fund’s Class S Shares (formerly named Class I Shares), calculated using the fees and expenses of Class S Shares of the JAD predecessor fund, net of any applicable fee and expense limitations or waivers.

•

The performance shown for Class C Shares for periods prior to July 6, 2009, reflects the historical performance of the JAD predecessor fund’s Class C Shares prior to the reorganization, calculated using the fees and expenses of the JAD predecessor fund’s Class C Shares, net of any applicable fee and expense limitations or waivers.

•

The performance shown for Class I Shares reflects the performance of the JAD predecessor fund’s Class I Shares from November 28, 2005 to July 6, 2009 (prior to the reorganization), calculated using the fees and expenses of Class I Shares of the JAD predecessor fund, net of any applicable fee and expense limitations or waivers. Performance shown for certain periods prior to November 28, 2005 reflects the historical performance of the JAD predecessor fund’s Class S Shares (formerly named Class I Shares), calculated using the fees and expenses of Class S Shares of the JAD predecessor fund, net of any applicable fee and expense limitations or waivers.

•

The performance shown for Class T Shares for periods prior to July 6, 2009, reflects the historical performance of the JAD predecessor fund’s Class S Shares prior to the reorganization, calculated using the fees and expenses of Class S Shares, net of any applicable fee and expense limitations or waivers.

•

The performance shown for Class N Shares reflects the historical performance of the Fund’s Class S Shares, calculated using the fees and expenses of Class S Shares, net of any applicable fee and expense limitations or waivers. If Class N Shares of the Fund had been available during the periods shown, the performance may have been different.

If Class A Shares, Class I Shares, and Class T Shares of the Fund had been available during periods prior to July 6, 2009, the performance shown for each respective share class may have been different. The performance shown for periods following the Fund’s commencement of Class S Shares, Class A Shares, Class C Shares, Class I Shares, and Class T Shares reflects the fees and expenses of each respective share class, net of any applicable fee and expense limitations or waivers.

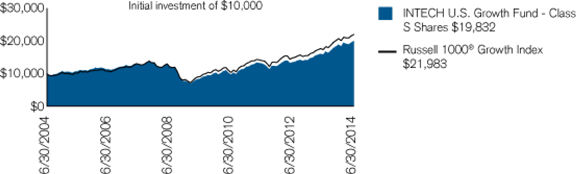

The bar chart depicts the change in performance from year to year during the periods indicated. The bar chart figures do not include any applicable sales charges that an investor may pay when they buy or sell Class A Shares or Class C Shares of the Fund. If sales charges were included, the returns would be lower. The table compares the Fund’s average annual returns for the periods indicated to broad-based securities market indices. The indices are not actively managed and are not available for direct investment. All figures assume reinvestment of dividends and distributions. For certain periods, the Fund’s performance reflects the effect of expense waivers. Without the effect of these expense waivers, the performance shown would have been lower.

Your Fund’s past performance (before and after taxes) does not necessarily indicate how the Fund will perform in the future. Updated performance information is available at janus.com/advisor/mutual-funds or by calling 1-877-335-2687.

| | Annual Total Returns for Class S Shares (calendar year-end) | |

| | | |

| | Best Quarter: Second Quarter 2009 15.04% | | | Worst Quarter: Fourth Quarter 2008 –25.11% | |

Average Annual Total Returns (periods ended 12/31/14) | |

| | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception of

Predecessor Fund

(1/2/03) | |

| Class S Shares | |

| Return Before Taxes | | | | | 9.38% | | | | | | 15.06% | | | | | | 6.82% | | | | | | 8.69% | | |

| Return After Taxes on Distributions | | | | | 9.28% | | | | | | 14.94% | | | | | | 6.56% | | | | | | 8.26% | | |

| Return After Taxes on Distributions and Sale of Fund Shares | | | | | 5.38% | | | | | | 12.16% | | | | | | 5.49% | | | | | | 7.09% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 7.96% | | | | | | 9.63% | | |

Russell 1000® Growth Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.05% | | | | | | 15.81% | | | | | | 8.49% | | | | | | 9.63% | | |

| Class A Shares | |

| Return Before Taxes(1) | | | | | 3.24% | | | | | | 13.88% | | | | | | 6.41% | | | | | | 8.35% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 7.96% | | | | | | 9.63% | | |

Russell 1000® Growth Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.05% | | | | | | 15.81% | | | | | | 8.49% | | | | | | 9.63% | | |

| Class C Shares | |

| Return Before Taxes(2) | | | | | 7.87% | | | | | | 14.35% | | | | | | 6.20% | | | | | | 8.07% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 7.96% | | | | | | 9.63% | | |

Russell 1000® Growth Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.05% | | | | | | 15.81% | | | | | | 8.49% | | | | | | 9.63% | | |

| Class I Shares | |

| Return Before Taxes | | | | | 9.92% | | | | | | 15.57% | | | | | | 6.82% | | | | | | 8.69% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 7.96% | | | | | | 9.63% | | |

Russell 1000® Growth Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.05% | | | | | | 15.81% | | | | | | 8.49% | | | | | | 9.63% | | |

| Class N Shares | |

| Return Before Taxes | | | | | 9.38% | | | | | | 15.06% | | | | | | 6.82% | | | | | | 8.69% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 7.96% | | | | | | 9.63% | | |

Russell 1000® Growth Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.05% | | | | | | 15.81% | | | | | | 8.49% | | | | | | 9.63% | | |

| Class T Shares | |

| Return Before Taxes | | | | | 9.68% | | | | | | 15.35% | | | | | | 6.82% | | | | | | 8.69% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 7.96% | | | | | | 9.63% | | |

Russell 1000® Growth Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.05% | | | | | | 15.81% | | | | | | 8.49% | | | | | | 9.63% | | |

(1)

Calculated assuming maximum permitted sales loads.

(2)

The one year return is calculated to include the contingent deferred sales charge.

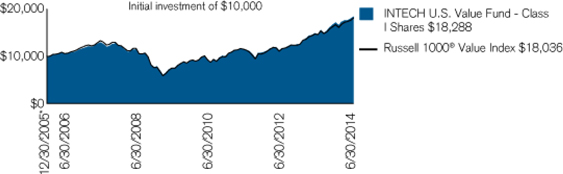

INTECH U.S. Managed Volatility Fund

The following information provides some indication of the risks of investing in INTECH U.S. Managed Volatility Fund by showing how the Fund’s performance has varied over time. Class I Shares, Class A Shares, Class C Shares, and Class S Shares of the Fund commenced operations on July 6, 2009, after the reorganization of each corresponding class of shares of Janus Adviser INTECH Risk-Managed Value Fund (“JAD predecessor fund”) into each respective share class of the Fund. Class T Shares of the Fund commenced operations on July 6, 2009. Class N Shares of the Fund commenced operations on October 28, 2014.

•

The performance shown for Class I Shares, Class A Shares, Class C Shares, and Class S Shares for periods prior to July 6, 2009, reflects the historical performance of the JAD predecessor fund’s Class I Shares, Class A Shares, Class C Shares, and Class S Shares prior to the reorganization, calculated using the fees and expenses of each respective share class of the JAD predecessor fund, net of any applicable fee and expense limitations or waivers.

•

The performance shown for Class T Shares for periods prior to July 6, 2009, reflects the historical performance of the JAD predecessor fund’s Class I Shares prior to the reorganization, calculated using the fees and expenses of Class T Shares, without the effect of any fee and expense limitations or waivers. If Class T Shares of the Fund had been available during periods prior to July 6, 2009, the performance shown may have been different.

•

The performance shown for Class N Shares reflects the performance of the Fund’s Class I Shares from July 6, 2009 to December 31, 2013, calculated using the fees and expenses of Class I Shares, net of any applicable fee and expense limitations or waivers. The performance shown for Class N Shares for periods prior to July 6, 2009, reflects the historical performance of the JAD predecessor fund’s Class I Shares prior to the reorganization, calculated using the fees and expenses of Class I Shares of the JAD predecessor fund, net of any applicable fee and expense limitations or waivers. If Class N Shares of the Fund had been available during periods prior to December 31, 2013, the performance shown may have been different.

The performance shown for periods following the Fund’s commencement of Class I Shares, Class A Shares, Class C Shares, Class S Shares, and Class T Shares reflects the fees and expenses of each respective share class, net of any applicable fee and expense limitations or waivers.

The bar chart depicts the change in performance from year to year during the periods indicated. The bar chart figures do not include any applicable sales charges that an investor may pay when they buy or sell Class A Shares or Class C Shares of the Fund. If sales charges were included, the returns would be lower. The table compares the Fund’s average annual returns for the periods indicated to broad-based securities market indices. The indices are not actively managed and are not available for direct investment. All figures assume reinvestment of dividends and distributions. For certain periods, the Fund’s performance reflects the effect of expense waivers. Without the effect of these expense waivers, the performance shown would have been lower.

INTECH U.S. Managed Volatility Fund’s past performance (before and after taxes) does not necessarily indicate how the Fund will perform in the future. Updated performance information is available at janus.com/advisor/mutual-funds or by calling 1-877-335-2687.

| | Annual Total Returns for Class I Shares (calendar year-end) | |

| | | |

| | Best Quarter: Third Quarter 2009 17.79% | | | Worst Quarter: Fourth Quarter 2008 –21.39% | |

Average Annual Total Returns (periods ended 12/31/14) | |

| | | | 1 Year | | | 5 Years | | | Since

Inception of

Predecessor Fund

(12/30/05) | |

| Class I Shares | |

| Return Before Taxes | | | | | 9.32% | | | | | | 15.18% | | | | | | 7.16% | | |

| Return After Taxes on Distributions | | | | | 1.01% | | | | | | 12.20% | | | | | | 5.38% | | |

| Return After Taxes on Distributions and Sale of Fund Shares(1) | | | | | 8.94% | | | | | | 11.64% | | | | | | 5.40% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 8.15% | | |

Russell 1000® Value Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.45% | | | | | | 15.42% | | | | | | 7.33% | | |

| Class A Shares | |

| Return Before Taxes(2) | | | | | 2.82% | | | | | | 13.49% | | | | | | 6.19% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 8.15% | | |

Russell 1000® Value Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.45% | | | | | | 15.42% | | | | | | 7.33% | | |

| Class C Shares | |

| Return Before Taxes(3) | | | | | 7.44% | | | | | | 14.01% | | | | | | 6.10% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 8.15% | | |

Russell 1000® Value Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.45% | | | | | | 15.42% | | | | | | 7.33% | | |

| Class S Shares | |

| Return Before Taxes | | | | | 9.14% | | | | | | 14.77% | | | | | | 6.73% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 8.15% | | |

Russell 1000® Value Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.45% | | | | | | 15.42% | | | | | | 7.33% | | |

| Class N Shares | |

| Return Before Taxes | | | | | 9.32% | | | | | | 15.18% | | | | | | 7.16% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 8.15% | | |

Russell 1000® Value Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.45% | | | | | | 15.42% | | | | | | 7.33% | | |

| Class T Shares | |

| Return Before Taxes | | | | | 9.18% | | | | | | 14.96% | | | | | | 6.79% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 8.15% | | |

Russell 1000® Value Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.45% | | | | | | 15.42% | | | | | | 7.33% | | |

(1)

If the Fund incurs a loss, which generates a tax benefit, the Return After Taxes on Distributions and Sale of Fund Shares may exceed the Fund’s other return figures.

(2)

Calculated assuming maximum permitted sales loads.

(3)

The one year return is calculated to include the contingent deferred sales charge.

For your Fund, after-tax returns are calculated using distributions for the Fund’s Class S Shares for periods following July 6, 2009; and for the JAD predecessor fund’s Class S Shares (formerly named Class I Shares) for periods prior to July 6, 2009. For INTECH U.S. Managed Volatility Fund, after-tax returns are calculated using distributions for the Fund’s Class I Shares for periods following July 6, 2009; and for the JAD predecessor fund’s Class I Shares for periods prior to July 6, 2009. After-tax returns are calculated using the historically highest individual federal marginal income tax rates and do not reflect the impact of state and local

taxes. Actual after-tax returns depend on your individual tax situation and may differ from those shown in the preceding tables. The after-tax return information shown above does not apply to Fund shares held through a tax-deferred account, such as a 401(k) plan or an IRA.

After-tax returns are only shown for Class S Shares of your Fund and Class I Shares of INTECH U.S. Managed Volatility Fund. After-tax returns for the other classes of shares will vary from those shown due to varying sales charges (as applicable), fees, and expenses among the classes.

Supplementary Performance Information

The following information supplements the “Comparison of Fund Performance” section of this Prospectus/Information Statement. This information is being provided in order to assist you with comparing the performance of the Class I Shares of your Fund to the performance of the Class I Shares of INTECH U.S. Managed Volatility Fund, which is shown above. As discussed in “Comparison of Fund Performance – Your Fund,” the performance shown for Class I Shares of your Fund reflects the performance of the JAD predecessor fund’s Class I Shares from November 28, 2005 to July 6, 2009 (prior to the reorganization), calculated using the fees and expenses of Class I Shares of the JAD predecessor fund, net of any applicable fee and expense limitations or waivers. Please note that the information in the below table does not reflect the since-inception performance of the JAD predecessor fund because Class I Shares commenced operations on November 28, 2005, whereas the JAD predecessor fund commenced operations on January 2, 2003.

The bar chart depicts the change in performance from year to year for Class I Shares of your Fund during the periods indicated. The table compares the average annual returns for Class I Shares of your Fund for the periods indicated to broad-based securities market indices. The indices are not actively managed and are not available for direct investment. All figures assume reinvestment of dividends and distributions. For certain periods, the Fund’s performance reflects the effect of expense waivers. Without the effect of these expense waivers, the performance shown would have been lower.

The past performance of your Fund’s Class I Shares (before and after taxes) does not necessarily indicate how the Fund will perform in the future.

| | Annual Total Returns for Class I Shares (calendar year-end) | |

| | | |

| | Best Quarter: Second Quarter 2009 15.15% | | | Worst Quarter: Fourth Quarter 2008 –25.07% | |

Average Annual Total Returns (periods ended 12/31/14) | |

| | | | 1 Year | | | 5 Years | | | Since

Inception of

Class I Shares

(11/28/05) | |

| Class I Shares | |

| Return Before Taxes | | | | | 9.92% | | | | | | 15.57% | | | | | | 7.38% | | |

| Return After Taxes on Distributions | | | | | 9.66% | | | | | | 15.35% | | | | | | 6.99% | | |

| Return After Taxes on Distributions and Sale of Fund Shares | | | | | 5.78% | | | | | | 12.59% | | | | | | 5.90% | | |

Russell 1000® Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.24% | | | | | | 15.64% | | | | | | 8.02% | | |

Russell 1000® Growth Index

(reflects no deduction for expenses, fees, or taxes) | | | | | 13.05% | | | | | | 15.81% | | | | | | 8.68% | | |

Management of the Funds

Investment Adviser: Janus Capital is the investment adviser for each Fund and will remain the investment adviser of INTECH U.S. Managed Volatility Fund after the Merger.

Investment Subadviser: INTECH Investment Management LLC is the investment subadviser for each Fund and will remain the subadviser of INTECH U.S. Managed Volatility Fund after the Merger.