UNITED STATES | |||

SECURITIES AND EXCHANGE COMMISSION | |||

Washington, D.C. 20549 | |||

| |||

SCHEDULE 14A | |||

| |||

Proxy Statement Pursuant to Section 14(a) of | |||

| |||

Filed by the Registrant o | |||

| |||

Filed by a Party other than the Registrant x | |||

| |||

Check the appropriate box: | |||

o | Preliminary Proxy Statement | ||

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | ||

o | Definitive Proxy Statement | ||

o | Definitive Additional Materials | ||

x | Soliciting Material under §240.14a-12 | ||

| |||

CREDO PETROLEUM CORPORATION | |||

(Name of Registrant as Specified In Its Charter) | |||

| |||

FORESTAR GROUP INC. | |||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | |||

| |||

Payment of Filing Fee (Check the appropriate box): | |||

x | No fee required. | ||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | ||

| (1) | Title of each class of securities to which transaction applies: | |

|

|

| |

| (2) | Aggregate number of securities to which transaction applies: | |

|

|

| |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

|

|

| |

| (4) | Proposed maximum aggregate value of transaction: | |

|

|

| |

| (5) | Total fee paid: | |

|

|

| |

o | Fee paid previously with preliminary materials. | ||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | ||

| (1) | Amount Previously Paid: | |

|

|

| |

| (2) | Form, Schedule or Registration Statement No.: | |

|

|

| |

| (3) | Filing Party: | |

|

|

| |

| (4) | Date Filed: | |

|

|

| |

Filed by Forestar Group Inc.

Pursuant to Rule 14a-12 under the Securities

Exchange Act of 1934

Subject Company: CREDO Petroleum Corporation

Commission File No.: 001-34281

| Investor Presentation June 2012 Recognizing and Responsibly Delivering the Greatest Value From Every Acre and Growing Through Disciplined Investments |

| This presentation contains “forward-looking statements” within the meaning of the federal securities laws. Forward-looking statements are typically identified by words or phrases such as “will,” “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “target,” “forecast,” and other words and terms of similar meaning. These statements reflect management’s current views with respect to future events and are subject to risk and uncertainties. We note that a variety of factors and uncertainties could cause our actual results to differ significantly from the results discussed in the forward-looking statements, including the timing to consummate the proposed merger, the risk that a condition to closing of the proposed merger may not be satisfied; our ability to achieve the synergies and value creation contemplated by the proposed merger; our ability to promptly and effectively integrate Credo’s businesses, and the diversion of management time on merger-related matters. Other factors and uncertainties that might cause such differences include, but are not limited to: general economic, market, or business conditions; changes in commodity prices; the opportunities (or lack thereof) that may be presented to us and that we may pursue; fluctuations in costs and expenses including development costs; demand for new housing, including impacts from mortgage credit availability; lengthy and uncertain entitlement processes; cyclicality of our businesses; accuracy of accounting assumptions; competitive actions by other companies; changes in laws or regulations; and other factors, many of which are beyond our control. Except as required by law, we expressly disclaim any obligation to publicly revise any forward-looking statements contained in this presentation to reflect the occurrence of events after the date of this presentation. Important Additional Information and Where to Find It Credo intends to file with the SEC and mail to its stockholders a Proxy Statement on Schedule 14A pursuant to Section 14(a) of the Exchange Act in connection with the merger. This document will contain important information about Forestar, Credo, the merger and other related matters. Credo’s investors and security holders are urged to read this document carefully when it is available. Credo’s investors and security holders will be able to obtain free copies of the Proxy Statement and other documents to be filed with the SEC by Credo through the web site maintained by the SEC at www.sec.gov. Credo’s investors and security holders may also obtain these documents, free of charge, from Credo’s website (www.credopetroleum.com) under the tab “Corporate Governance” and then under the heading “SEC Filings” or by contacting Credo’s Investor Relations Department at 303-297-2200. Credo and its directors and executive officers may be deemed to be participants in the solicitation of proxies in respect of the transactions contemplated by the merger agreement. Information regarding the persons who may, under the rules of the SEC, be deemed participants in the solicitation of Credo stockholders in connection with the merger will be set forth in the proxy statement when it is filed with the SEC. Credo’s investors and security holders can find information about Credo’s executive officers and directors in its definitive proxy statement filed with the SEC on February 28, 2012. Notice to Investors 2 |

| Strategically located in key growth regions and active oil and gas basins Focused strategy to deliver the greatest value from real estate and natural resources Experienced management team with proven ability to deliver Strong balance sheet Disciplined investment approach; well positioned to capitalize on growth opportunities The Forestar Difference 3 |

| Forestar is a real estate and natural resources company with a strategy focused on maximizing the value of its assets by: Recognizing and responsibly delivering the greatest value from every acre Growing through strategic and disciplined investments 5 7 4 Our Strategy – The Dimensional Land Model TM |

| 594,000 net mineral acres principally located in 5 basins and 7 states 1,600,000 acres of water interest* 17,800 acres of groundwater leases in central Texas 146,000 acres of low-basis land 130,000 real estate acres generating fiber growth and sales 89 projects residential and mixed-used communities in 7 states and 11 markets 4 significant commercial and income producing assets 3 Multifamily Properties (Austin - 2, Houston - 1) Radisson Hotel (Austin, TX) Note: Information as of Q1 2012 and includes ventures. 5 Delivering The Greatest Value From Every Acre * Includes a 45% non-participating royalty interest from approximately 1.4 million acres in TX, LA, GA & AL |

| Forestar Minerals - Oil and Gas 6 Building Momentum By Driving Leasing and Exploration to Increase Production and Reserves 6 |

| Minerals Greatest Value Pipeline (Acres) 1 Terms – Activity Financials 32,000 20% - 27% Royalty and Working Interest 534 Wells 2 Cash Flow = $134mm3 49,000 3 – 5 year term Delay rentals Drilling requirements $250 - $1,500 per acre lease rate 58,000 Seismic, Ventures and Prospects Up to $100 per acre Knowledge gain 455,000 Market and promote through multiple channels Low Basis Low Cost 594,000 Total Net Mineral Acres Production - Reserves Lease - Bonus Explore Market - Promote 1 Acres as of Q1 2012; includes ventures 2 Wells owned and operated by third party lessees / operators as of Q1 2012 3 Undiscounted future net cash flows before income taxes as of YE 2011 7 Delivering The Greatest Value From Every Acre |

| Forestar’s Share of Quarterly Oil & Gas Production Q1 2011 – Q1 2012 Growth in Drilling Activity Well Count YE 2009 – Q1 2012 Note: Includes ventures; wells owned and operated by third party lessees / operators 534 8 Increased Oil Production Driving Higher Royalties Well Count oil Produced (Bbls) Natural Gas Produced (MMcf) |

| Accelerating Value Realization of Minerals Through Proven Reserve Growth Note: Includes ventures ($ in millions) ($ in millions) Future Net Cash Flows * 9 *PV-10 represents present value of estimated future oil and gas revenues, net of estimated direct expenses, discounted at an annual discount rate of 10%. Future Net Cash flows represents an undiscounted value based upon estimate of future net cash flows from proved developed reserves after deducting estimated severance and ad valorem taxes, but before deducting estimates of future income taxes These are Non-GAAP financial measures. The reconciliation between GAAP and Non-GAAP financial measures is provided in the tables following this presentation, and on the company’s investor relations website. $134 $57 74% Oil Significant Oil Exploration and Development Drives 246% Reserve Replacement in 2011 Proven Reserves (Before Income Taxes) PV-10 |

| Target Formations 2011-2012 Well Completions East Texas & Louisiana* 10 Acres Leased Available for Lease Held by Production Acres with Option New Oil Wells New Gas Wells * Map excludes six wells located in Barnett Shale in North Texas and ten wells in Colorado completed in 2011 East Texas and Wells Drilled Gulf Coast Basins Last 12 months Target |

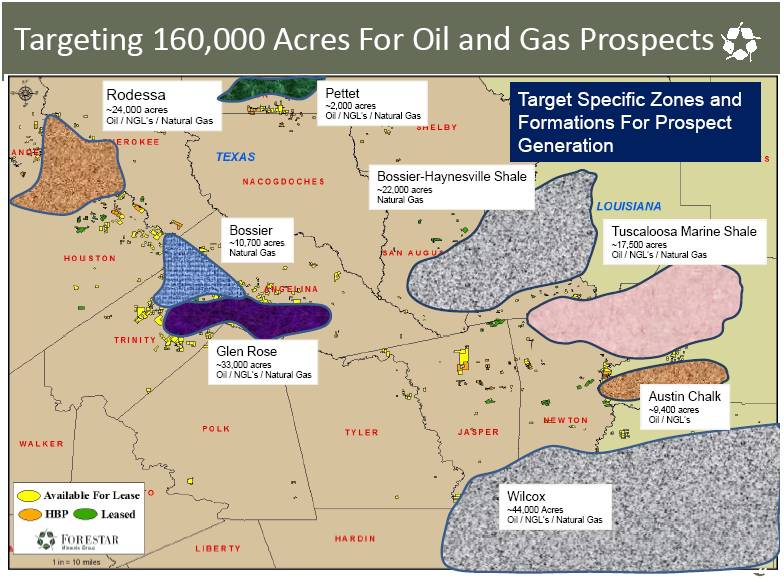

| Rodessa ~24,000 acres Oil / NGL’s / Natural Gas Target Specific Zones and Formations For Prospect Generation Pettet ~2,000 acres Oil / NGL’s / Natural Gas Glen Rose ~33,000 acres Oil / NGL’s / Natural Gas Bossier ~10,700 acres Natural Gas Tuscaloosa Marine Shale ~17,500 acres Oil / NGL’s / Natural Gas Bossier-Haynesville Shale ~22,000 acres Natural Gas Wilcox ~44,000 Acres Oil / NGL’s / Natural Gas Austin Chalk ~9,400 acres Oil / NGL’s 11 Targeting 160,000 Acres For Oil and Gas Prospects |

| Vernon Rapides Newton Allen Beauregard 12 12 TEXAS LOUISIANA Austin Chalk Drilling Activity Increasing Masters Creek Trend Byerley A-32 Unit 2-1 Byerley A-32 Unit 2-2 Keaghey A-2 1 Blackstone A-90 1 Leased Available For Lease HBP FOR Interest in Austin Chalk wells Brookeland Trend |

| 13 ($ in millions) Estimated Ultimate Recoveries Well Completion Date FOR Net Royalty Interest Condensate MB Natural Gas Liquids MB Dry Gas MMCF Total MMBOE Forestar Blackstone A-90 Unit 1 Nov-09 7.6% 29 38 482 0.1 Forestar Keaghey A-253 Unit 1 Jan-11 5.1% 13 15 172 0.1 Forestar Byerley A-32 Unit 1 Nov-11 14.4% 52 51 475 0.2 Forestar Byerley A-32 Unit 2 No 1 Apr-12 14.3% 43 45 472 0.2 Total 136 148 1,601 0.6 12-Month NYMEX Strip Pricing, $/bbl or $/mcf or $/boe $97.46 $48.73* $3.08 $46.09 Potential Royalties to Forestar (Current Pricing) $13.2 $7.2 $4.9 $25.4 Austin Chalk Drilling Activity Increasing * Based upon 50% of NYMEX 12-month strip price as of May 9, 2012 Note: Wells owned and operated by third-party lessees; EUR’s based upon internal estimates, actual future results may vary |

| Tuscaloosa Marine Shale Prospect Generation Evaluating 17,500 acres for Drilling Prospects 14 |

| Haynesville Bossier Prospect Generation Evaluating 22,000 acres for Drilling Prospects 15 |

| Value Components % of Well Economics Capital Wells Operating 50 - 75% Moderate -- Working Interest 10 – 50% Low 10 Royalties 20 – 25% None 534 Leases < 5% None -- Total 100% 534* Value Creation & Realization Q1 2012 * FOR may have a working interest and royalty interest in same well 16 Enhancing Minerals Value Creation and Realization |

| Minerals - Oil and Gas Acquisition of Credo Petroleum Corporation Doubles Production and Reserves, Provides Meaningful Ownership in Strategic Oil and Gas Basins, Further Enhances Transparency and Disclosure, and Creates Solid Platform for Additional Growth 17 |

| Credo Acquisition Overview Acquisition of CREDO Petroleum (NASDAQ:CRED) for $14.50 per share Total equity value $146 million - all cash Consistent with Strategy and Triple in FOR initiatives Accelerate value realization Optimize transparency and disclosure Raise net asset value through strategic and disciplined investments 18 Note: Acquisition price represents 34% premium based on Credo pre-announcement closing price of $10.86 per share on June 1, 2012 Note: Credo is an oil and gas company based in Denver, CO which owns leasehold interests in almost 125,000 net mineral acres, with operations in the Bakken and Three Forks formations of North Dakota, the Lansing – Kansas City formation in Kansas and Nebraska, and the Tonkawa and Cleveland formations in the Texas Panhandle. |

| Acquisition Benefits Doubles production and reserves, enhances disclosure Creates meaningful scale, ownership and operations in strategic basins Maintains solid financial position, enhanced by recurring cash flows Provides a strong operating platform for growth and investment Exceeds return requirements and drives additional shareholder value Operating option accelerates Forestar Minerals value realization 19 |

| Attractive Leasehold Interests In Prolific Basins CREDO Leasehold Interests – Q1 2012 Market Net Acres Basins Formations North Dakota 6,000 Williston Bakken & Three Forks Kansas 43,000 Central Uplift Lansing – Kansas City Nebraska 41,000 Denver – Julesburg Central Uplift Lansing – Kansas City Oklahoma 17,000 Anadarko Morrow Texas 4,000 Anadarko Tonkawa & Cleveland Other* 14,000 Total 125,000 Q1 2012 Producing Wells Working Interest** 337 Royalty Interest 1,180 Total Wells 1,517 Q1 2012 Leasehold Interest (Acres) Held By Production 30,000 Undeveloped 95,000 Total Net Mineral Acres 125,000 * Includes approximately 8,000 net mineral acres located in various states related to overriding royalty interests **Includes approximately 108 wells operated by CREDO Note: Acres may vary 20 |

| Bakken Provides Significant Value Creation Potential 6,000 net mineral acres in core of Bakken & Three Forks Bakken Well Assumptions Avg. Well production (EUR) >500 Mboe Average working interest 8.0% Units 50 Wells Completed* 16 Wells Drilling* 9 Add’l Wells Planned by YE 2012* 9 Total Potential Wells 400 * Source: Credo Petroleum news release dated April 17, 2012 FORT BERTHOLD RESERVATION PARSHALL FIELD Bakken / Three Forks Acres Locator Map Leasehold Mineral Interests Locations Leasehold Interests Drilling Locations Units Bakken Vertical Wells Historical Production Three Forks Vertical Well Bakken Horizontal Well Three Forks Horizontal Well 21 |

| Acquisition Provides Meaningful Scale and Solid Platform For Future Growth and Additional Investment Acquisition Provides Meaningful Ownership in Strategic Oil and Gas Basins Combined Mineral Interests Market Net Acres* Texas 256,000 Georgia 156,000 Louisiana 144,000 Kansas 43,000 Nebraska 41,000 Alabama 40,000 Oklahoma 17,000 North Dakota 6,000 Other** 16,000 Total 719,000 * Note: As of first quarter 2012; includes both fee and leasehold interests ** Includes approximately 8,000 net mineral acres located in various states related to overriding royalty interests 22 |

| Compelling Combination Value Drivers Combination creates meaningful scale through production and reserve growth, additional ownership and operations in strategic basins and improves transparency and disclosures Value Drivers 2011 Metrics* CRED FOR Combined Increased Scale / Doubles Production and Reserves Meaningful Ownership and Operations in Prolific Basins Disclosure Benefits Additional transparency on Forestar minerals FOR YE 2011 reserves 98% PDP’s – Yet to report PUD’s ($ in millions) Production (BOE) 301,000 422,200 723,200 Reserves (MMBOE) 4.1 3.0 7.1 % Oil 48% 35% 42% PV-10 $62 $81 $143 Future Net Cash Flows $116 $134 $250 Net Mineral Acreage** 125,000 594,000 719,000 Basins 5 5 10 States 7 7 14 ** Note: Includes both fee and leasehold interests; Forestar acres as of Q1 2012 *Note: Based on Credo Form 10-K for the year ended 10/31/11 and Forestar Form 10-K for the year ended 12/31/11, before income taxes 23 |

| Proved Developed Proved Developed Non-Prod Proved Undeveloped Probable Possible Resource Reserve reporting beyond proved developed requires the ability and intent to drill 24 Proved Developed Reserves Represent Only One Component of Reserve Value and Opportunity Acquisition Accelerates Value Realization of Forestar Minerals Reserve Disclosures Forestar Forestar YE 2011 YE 2011 Reserves (MMBOE) Net Acres |

| Acquisition Analysis Credo Acquisition Price Per Share $14.50 Equity Purchase $146 + Closing Costs* 7 Total Purchase Price $153 Financing** Committed Loan $75 Revolver Availability & Cash 78 $153 Leverage & Liquidity (Post transaction) Total Debt / Total Capitalization 38% Available Liquidity >$100 ($ in millions) Following the acquisition of Credo, Forestar will have a solid balance sheet, improved cash flow profile and ample liquidity *Excludes financing costs **Forestar intends to pursue amendments to its existing credit facilities to fund a significant portion of the purchase price. 25 |

| Credo Acquisition Will Generate Scale, Create Platform for Growth and Investment, and Accelerate Value Realization Q1 2012 Proforma Combined Portfolio of Assets Acquisition Benefits Oil & Gas ($ in millions) Net Minerals Acres* 719,000 Increases exposure to Oil and NGLs Reserves (MMBOE) 7.1 Enhances reserve reporting PV-10 Reserves $143 Meaningful scale; ownership in strategic basins Future Net Cash Flows $250 Experienced team with proven track record Proforma Investment $200 Accretive to earnings in first full year Real Estate Acres 146,000 Projects 99 Acres in Entitlement 27,600 Commercial Properties 4 Investment $570 Maintain solid balance sheet and ample liquidity Water Acres 1.6 million** *Includes both fee and leasehold mineral acreage; Based on Credo Form 10-K for the year ended 10/31/11 and Forestar Form 10-K for the year ended 12/31/11 ** Includes a 45% nonparticipating royalty interest in groundwater produced or withdrawn for commercial purposes or sold from approximately 1.4 million acres in TX, LA, GA, and AL Note: Reserve information before income taxes 26 |

| Real Estate - Community Development Page Building Momentum by Increasing Residential Lot Sales And Developing Exceptional Master Plan Communities 27 |

| Real Estate Greatest Value Development Entitled Entitle Timberland Pipeline (Acres) 1 Activity – Uses Financials 2 2,000 63 projects 1,348 acres – 2,815 lots 498 commercial acres $50K per lot $90K per acre (avg sales price) 14,000 18 projects Approved uses, ready for development High Value Creation 28,000 16 projects Planned Lifestyle Communities (1st and 2nd move-up focus) Low Basis Low Cost 102,000 Timberland Sales Fiber Sales Recreational Leases $2K per acre (avg sales price) 146,000 Total Real Estate Acres - 97 Projects 1 Acres as of Q1 2012; Includes ventures. 2 Based on historical sales activity. 28 Delivering The Greatest Value From Every Acre |

| Note: MSA performance based on Employment, Gross Metropolitan Product (GMP) and House Price Index Source: Brookings Institute Salt Lake City 1 - $0.4 Oakland 1 - $8.8 Strongest Quartile Weakest Quartile Los Angeles 2 - $14.4 Kansas City 1 - $2.9 Tampa 3 - $4.9 Atlanta 33 - $84.9 San Antonio 4 - $89.5 Denver 5 - $31.3 Austin 16 - $116.1 Dallas/Ft. Worth 14 - $75.0 Gulf Coast 5 - $37.2 Houston 12 - $117.1 Projects and investment as of Q1 2012; includes ventures Note: Excludes investment in Light Farms which was sold in April 2012; includes $21 million note secured by Discovery at Springs Trail Project in Houston, TX TEXAS 51 - $434.9 Texas Markets Represent 75% of our Investment in Real Estate 29 Low Basis Assets Located in Stronger Markets |

| Increased Residential Lot Sales Reflect Stable Demand and Reduced Finished Lot Inventories in Texas 30 * Represents developed and under development residential lots Note: Includes ventures; excludes sale of undeveloped paper lots Annual Lot Sales 1,117 642 1,060 2006 Peak Sales = 3,600 lots Annual Lot Sales & Avg. Lot Margin Forestar Residential Lot Inventory* |

| Real Estate Pipeline Well Positioned For Recovery Note: Information as of Q1 2012; includes ventures * Includes 4 significant commercial and income producing properties. Real Estate Undeveloped In Entitlement Process Entitled Developed and Under Development Total Acres Undeveloped Land Owned 95,360 102,261 Ventures 6,901 Residential Owned 24,867 9,669 734 38,811 Ventures --- 3,240 301 Commercial Owned 2,723 1,246 614 5,179 Ventures --- 399 197 Total Acres 102,261 27,590 14,554 1,846 146,251 Estimated Residential Lots 24,108 2,815 26,923 Projects 16 18 63* 97 In addition, Forestar owns a 58% interest in a venture which controls over 16,000 acres of undeveloped land in Georgia with minimal investment 31 |

| Triple in FOR Strategic Initiatives 32 Building Momentum By Increasing Oil Production, Proven Reserves and Residential Lot Sales |

| Initiatives Historical Avg. (2008-2011) Target Focus on Accelerating Value Realization Triple Residential Lot Sales 850 lots 2,500 lots Triple Oil & Gas Production (Mcfe) 2.3 Bcfe 6.7 Bcfe Triple Total Segment Earnings $33 million > $100 million Optimize Transparency & Disclosure Expand Reported Oil and Gas Resource Potential PDP’s Additional Reserve / Resource Categories Additional Transparency on Water Interests Acres Sustainable Production Potential Report Corporate Sustainability Results - Responsibly integrating economic, social, and environmental resources Raise NAV Through Strategic and Disciplined Investments Growth Opportunities which Prove Up Net Asset Value and Exceed Return Requirements - Target 35% ROC (20-25% IRR) Maintain Financial Flexibility Accelerate Participation in Oil & Gas Working Interests - Lower Risk – Proven Formations Target > 20% Return on Capital Develop Low-Capital, High-Return Multifamily Business - Minimal Capital Investment (10-20% of project equity) 33 Our Focus: Triple in FOR |

| Kingwood 34 April 2012: Light Farms Sale FOR / RPG Land Company sold 800 acres from proposed residential community near Dallas, TX for $56 million in total consideration FOR received $25 million in cash proceeds and reduced consolidated debt by $31 million Sale eliminated over $2 million in annual carrying costs Gain on sale of $3.4 million in Q2 2012 ($ in millions) 1st Quarter 2012 Pro forma Light Farms Sale Credit Facility Borrowings $136 $136 Other Consolidated Debt 92 61 Total Debt $228 $197 Total Debt/Capital 31% 28% Cash $5 $30 Credit Availability 155 155 Total Liquidity $160 $185 Focused on investments that provide near-term cash flow and earnings Increasing Our Financial Flexibility Light Farms Venture Sold 800 Acres for $56 Million |

| Accelerating Value Realization Building momentum by increasing oil production and proven reserves Growing lot sales and increasing market share Harvesting value from stabilized commercial assets Capitalizing on growth opportunities and investments to generate near-term cash flow and earnings, accelerate value realization and raise NAV Building Momentum By Accelerating Value Realization, Optimizing Transparency and Growing NAV 35 |

| Appendix 36 Recognizing and Responsibly Delivering the Greatest Value From Every Acre and Growing Through Disciplined Investments |

| 1st Quarter 2012 1st Quarter 2011 Full Year 2011 Full Year 2010 Leasing Activity Net Acres Leased 800 4,900 8,100 16,900 Avg. Bonus / Acre $360 $340 $279 $457 Royalties* Oil Produced (Barrels) 69,200 32,000 151,900 115,400 Average Price / Barrel $97.57 $82.49 $96.84 $73.09 Natural Gas Produced (MMCF) 452.2 466.8 1,622.0 1,796.4 Average Price / MCF $3.23 $3.72 $3.95 $4.26 Total MMcfe 867.4 658.6 2,533.4 2,489.1 Average Price / Mcfe $9.47 $6.64 $8.34 $6.46 Segment Revenues ($ in Millions) $9.4 $7.3 $24.6 $24.8 Segment Earnings ($ in Millions)** $5.9 $5.6 $16.0 $22.8 Producing Wells* (end of period) 534 496 530 494 * Includes our share of venture production: 1st Qtr. 2012 = 90 MMCf; 1st Qtr. 2011 = 159 MMCf; FY 2011 = 493 MMcf; FY 2010 = 573 MMcf ** Note: Segment results include costs associated with the development of our water initiatives: $1.3 million in Q1 2012; $1.1 million in Q1 2011; and $3.9 million in FY 2011. 37 Mineral Resources Segment KPI’s |

| 1st Quarter 2012 1st Quarter 2011 Full Year 2011 Full Year 2010 Residential Lot Sales * Lots Sold 285 214 1,117 804 Average Price / Lot $53,000 $48,200 $47,400 $49,500 Gross Profit / Lot $20,800 $18,500 $17,500 $16,600 Commercial Tract Sales * Acres Sold - 20 26.4 17.8 Average Price / Acre - $152,500 $193,700 $90,100 Land Sales * Acres Sold 455 2,630 17,100 5,800 Average Price / Acre $2,400 $2,300 $2,400 $3,500 Segment Revenues ($ in Millions) $17.9 $21.1 $106.2 $68.3 Segment Earnings (Loss) ($ in Millions) $11.5 $2.6 ($25.7) ($4.6) ** Q1 2012 results include $11.7 million gain on sale of interest in Palisades West * Includes ventures 38 ** **** Real Estate Segment KPI’s **** KPI’s include venture activity; but 2010 excludes sale of 625 acres for about $20 million at Summer Creek venture located near Fort Worth, TX *** Note: Full year 2011 real estate segment earnings include pre-tax non-cash asset impairment charges of $45.2 million *** |

| 1st Quarter 2012 1st Quarter 2011 Full Year 2011 Full Year 2010 Fiber Sales Pulpwood Tons Sold 24,400 65,600 266,200 392,900 Average Pulpwood Price / Ton $10.18 $9.18 $8.69 $9.93 Sawtimber Tons Sold 4,400 15,500 56,800 144,300 Average Sawtimber Price / Ton $19.48 $16.98 $16.13 $17.94 Total Tons Sold 28,800 81,100 323,000 537,200 Average Price / Ton $11.59 $10.67 $10.00 $12.08 Recreational Leases Average Acres Leased 131,000 200,000 174,500 208,100 Average Lease Rate / Acre $8.80 $8.91 $8.80 $8.32 Segment Revenues ($ in Millions) $0.7 $1.4 $4.8 $8.3 Segment Earnings ($ in Millions) $0.4 $0.6 $1.9* $5.1 * Includes $0.2 million gain on termination of timber lease in connection with the Ironstob venture Note: Fiber resources segment earnings negatively impacted by sale of over 74,000 acres of timberland during 2011. 39 Fiber Resources Segment KPI’s |

| ($ in millions) 2011 2010 % Change Proved Developed Reserves 1 Oil Reserves MBBL 1,053.7 608.7 73% Gas Reserves BCF 11.4 10.5 9% Future Net Revenues* $132.7 $77.5 71% PV-10 3* $81.0 $45.3 79% Proved Developed Non-Producing1 Oil Reserves MBBL 10.7 - nm Gas Reserves BCF 0.1 - nm Future Net Revenues* $1.0 - nm PV-10 3* $0.9 - nm Total Proven Reserves1 Oil Reserves MBBL 1,064.4 608.7 75% Gas Reserves BCF 11.5 10.5 10% Reserves Bcfe2 17.9 14.2 26% Future Net Revenues* $133.7 $77.5 73% PV-10 3* $81.9 $45.3 81% Note: PV-10 analysis based on 2011 average benchmark prices of $92.71 for oil and $4.12 for natural gas; compared with 2010 average benchmark prices of $75.96 for oil and $4.38 for natural gas for 2010. 1 Includes Forestar’s share of equity method ventures 2 Bcfe – Billion Cubic Feet Equivalent (converting oil to natural gas at 6 Mcf / Bbl) 3 PV-10 – Present Value at 10% (before income taxes) 40 *These are Non-GAAP financial measures. The reconciliation between GAAP and Non-GAAP financial measures is provided in the tables following this presentation, and on the company’s investor relations website. YE 2011 Proven Reserves |

| In our full year and fourth quarter 2011 earnings release and conference call presentation materials furnished to the Securities and Exchange Commission on Form 8-K on February 22, 2012, we used certain non-GAAP financial measures. The non-GAAP financial measures should not be relied upon to the exclusion of GAAP financial measures. These non-GAAP financial measures reflect an additional way of viewing aspects of our operations that, when viewed with our GAAP financial statements and the accompanying reconciliations to corresponding GAAP financial measures, may provide a more complete understanding of our business. We strongly encourage investors to review our consolidated financial statements and publicly filed reports in their entirety. Reconciliation of Non-GAAP Financial Measures (Unaudited) The following table shows a reconciliation of PV-10 (discounted future net cash flows before income taxes) to the standardized measure of discounted future net cash flows (the most directly comparable measure calculated and presented in accordance with generally accepted accounting principles, or GAAP). PV-10 is an estimate of the present value of future net cash flows from proved developed reserves after deducting estimated severance and ad valorem taxes, but before deducting any estimates of future income taxes. The estimated future net cash flows are discounted at an annual rate of 10%. A reconciliation of PV-10 to the standardized measure of discounted future net cash flows as computed under GAAP is illustrated below: ($ in 000’s) Year-End 2011* Year-End 2010* PV – 10 (discounted future net cash flows before income taxes) $81,919 $45,267 Less: discounted future income taxes (effective tax rate of 38%) (25,713) (14,130) Standardized measure of discounted future net cash flows $56,206 $31,137 The undiscounted value represents an estimate of future net cash flows from proved developed reserves after deducting estimated severance and ad valorem taxes, but before deducting estimates of future income taxes. A reconciliation of undiscounted future net cash flows before income taxes to the undiscounted future net cash flows after income taxes is illustrated below: ($ in 000’s) Year-End 2011* Year-End 2010* Undiscounted future net cash flows before income taxes $133,729 $77,464 Less: undiscounted future income taxes (effective tax rate of 38%) (41,835) (24,112) Undiscounted future net cash flows after income taxes $91,894 $53,352 We believe both PV-10 and undiscounted values are important for evaluating the relative significance of our oil and gas interests and that the presentation of the non-GAAP financial measures provides useful information to investors because they are widely used by professional analysts and sophisticated investors in evaluating oil and gas companies. Because there are many unique factors that can impact an individual company when estimating the amount of future income taxes to be paid, we believe the use of a pre-tax measure is valuable for evaluating our mineral assets. * Includes our share of proved developed reserves in equity-method ventures Reconciliation of Non-GAAP Financial Measures (Unaudited) 41 |

| Anna Torma SVP Corporate Affairs Forestar Group Inc. 6300 Bee Cave Road Building Two, Suite 500 Austin, TX 78746 512-433-5312 annatorma@forestargroup.com 42 Forestar A Vision for Every Acre For questions, please contact: |