UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (X) | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 28, 2007

OR

| ( ) | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the transition period from __________ to __________ |

| Commission File Number 1-8022 |

| |

| CSX CORPORATION |

(Exact name of registrant as specified in its charter) |

| Virginia | | 62-1051971 |

| (State or other jurisdiction of incorporation or organization) | | | | (I.R.S. Employer Identification No.) |

| |

| 500 Water Street, 15th Floor, Jacksonville, FL | | 32202 | | (904) 359-3200 |

| (Address of principal executive offices) | | (Zip Code) | | (Telephone number, including area code) |

| Securities registered pursuant to Section 12(b) of the Act: |

| |

| Title of each class | | Name of exchange on which registered |

| Common Stock, $1 Par Value | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer (as defined in Rule 405 of the Securities Act).

Yes (X) No ( )

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ( ) No (X)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes (X) No ( )

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ( )

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer (as defined in Exchange Act Rule 12b-2).

Large Accelerated Filer (X) Accelerated Filer ( ) Non-accelerated Filer ( )

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2).

Yes ( ) No (X)

On June 29, 2007 (which is the last day of the second quarter and the required date to use), the aggregate market value of the Registrant’s voting stock held by non-affiliates was approximately $19.7 billion (based on the New York Stock Exchange closing price on such date).

There were 403,363,273 shares of Common Stock outstanding on February 15, 2008 (the latest practicable date that is closest to the filing date).

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Definitive Proxy Statement (the “Proxy Statement”) to be filed not later than April 25, 2008 with respect to its 2008 annual meeting of shareholders.

| |

| FORM 10-K | |

| TABLE OF CONTENTS | |

| | | | | |

| Item No. | | Page |

| | | | | |

| PART I |

| 1. | | 3 |

| | | 8 |

| | | 12 |

| 2. | | 12 |

| 3. | | 17 |

| 4. | | 18 |

| | | | | |

| PART II |

| 5. | | |

| | | | 21 |

| 6. | | 24 |

| 7. | | |

| | | | 26 |

| | | | | 26 |

| | | | | 27 |

| | | | | 30 |

| | | | | 33 |

| | | | | 35 |

| | | | | 48 |

| | | | | 50 |

| | | | | 51 |

| | | | | 51 |

| 7A. | | 61 |

| 8. | | 64 |

| 9. | | |

| | | | 131 |

| 9A. | | 131 |

| 9B. | | 134 |

| |

| PART III |

| 10. | | 135 |

| 11. | | 135 |

| 12. | | 135 |

| 13. | | 135 |

| 14. | | 135 |

| |

| PART IV |

| 15. | | 136 |

| | | | | |

| 142 |

Item 1. Business by Segment

CSX Corporation (“CSX” and together with its subsidiaries, the “Company”), based in Jacksonville, Florida, is one of the nation's leading transportation companies. Surface Transportation, which includes the Company’s rail and intermodal businesses, provides rail-based transportation services including traditional rail service and the transport of intermodal containers and trailers.

Rail

CSX’s principal operating company, CSX Transportation, Inc. (“CSXT”), provides a crucial link to the transportation supply chain through its approximately 21,000 route mile rail network, which serves every major population center in 23 states east of the Mississippi River, the District of Columbia, and the Canadian provinces of Ontario and Quebec. It serves 70 ocean, river and lake ports along the Atlantic and Gulf Coasts, the Mississippi River, the Great Lakes and the St. Lawrence Seaway. CSXT also serves thousands of production and distribution facilities through track connections to more than 230 short-line and regional railroads.

Other Entities

In addition to CSXT, the rail segment includes Total Distribution Services, Inc. (“TDSI”), Transflo Terminal Services, Inc. (“Transflo”), CSX Technology, Inc. (“CSX Technology”) and other subsidiaries. TDSI serves the automotive industry with distribution centers and storage locations, while Transflo provides logistical solutions for transferring products from rail to trucks. Technology and other support services are provided by CSX Technology and other subsidiaries.

Intermodal

CSX Intermodal, Inc. (“Intermodal”), one of the nation’s largest coast-to-coast intermodal transportation providers, is a stand-alone, integrated intermodal company linking customers to railroads via trucks and terminals. Containers and trailers are loaded and unloaded from trains, and trucks provide the link between intermodal terminals and the customer.

Surface Transportation Businesses

The rail and intermodal segments are designated by the Company on a combined basis as Surface Transportation businesses. Together, they generated $10 billion of revenue during 2007 and served four primary lines of business:

| | · | The merchandise business is the most diverse market with nearly 2.7 million carloads per year of aggregates, which includes crushed stone, sand and gravel, metal, phosphate, fertilizer, food, consumer, agricultural, paper and chemical products. The merchandise business generated approximately 50% of the Company’s revenue in 2007 and 38% of volume. |

| | · | Coal, which delivered approximately 1.9 million carloads of coal, coke and iron ore to electricity generating power plants, ocean, river and lake piers and terminals, steel makers and industrial plants, accounted for approximately 26% of the Company’s revenue and volume in 2007. The Company transports almost one-third of every ton of coal used for generating electricity in the areas served by CSX. |

| | · | Automotive, which delivers both finished vehicles and auto parts, generated 8% of the Company’s revenue and 6% of the Company’s volume in 2007. The Company delivers approximately one-third of North America’s light vehicles, serving both traditional manufacturers and the increasing number of global manufacturers. |

| | · | Intermodal offers a competitive cost advantage over long-haul trucking by combining the superior economics of rail transportation with the short-haul flexibility of trucks. Through its network of more than 50 terminals, Intermodal serves all major markets east of the Mississippi River and transports mainly manufactured consumer goods in containers, providing customers with truck-like service for longer shipments. For 2007, Intermodal accounted for approximately 14% of the Company’s total revenue and 30% of volume. |

Other revenue, which includes revenue from regional railroads (that are partially owned by CSX), demurrage, switching and other incidental charges, accounted for 2% of the Company’s total 2007 revenue. Revenue from regional railroads includes shipments by railroads that CSX does not directly operate. Demurrage represents charges assessed by railroads when shippers or receivers of freight hold railcars beyond a specified period of time. Switching revenue is generated when CSXT switches cars between trains for a customer or another railroad.

Other Businesses

CSX’s other holdings include CSX Real Property, Inc., a subsidiary responsible for the Company’s real estate sales, leasing, acquisition and management and development activities, and CSX Hotels, Inc., a resort doing business as The Greenbrier, located in White Sulphur Springs, West Virginia. Pretax earnings of $42 million, $24 million and $85 million for 2007, 2006 and 2005, respectively, from these activities are classified as a component of other income. These items are classified in other income because they are not considered by the Company to be operating activities and may fluctuate with the timing of real estate sales and resort seasonality.

The Company also has certain residual activities from formerly owned companies that include leasing of equipment and vessels. These results are included in consolidated operating income and totaled $5 million, $12 million and $1 million in 2007, 2006 and 2005, respectively.

Financial Information about Operating Segments

See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations for operating revenue, operating income and total assets by segment for each of the last three fiscal years.

Company History

A leader in freight rail transportation for 180 years, the Company’s roots date back to the early nineteenth century when the Baltimore and Ohio Railroad (“B&O”) – the nation’s first common carrier – was chartered in 1827. Since that time, CSX has built on the foundation laid by early pioneers who had a vision to create a railroad that safely and reliably services the ever-increasing demands of a growing nation.

In those 180 years, numerous railroads have combined with the former B&O through merger and consolidation to create what has become CSX. Each of the railroads that combined into the CSX family brought to CSX unique and valuable geographical reach to new markets, gateways, cities, ports and transportation corridors.

CSX was incorporated in 1978, under the laws of the Commonwealth of Virginia. In 1980, the Company completed the merger of the Chessie System (“Chessie”) and Seaboard Coast Line Industries (“Seaboard”) into CSX. The merger allowed CSX to connect northern population centers and Appalachian coal fields to growing southeastern markets. In 1986, the Chessie and Seaboard operating entities were transferred to the rail entity CSXT, which was created through the merger. Intermodal was originally formed in 1986 in order to provide nationwide, door-to-door intermodal service.

In 1997, CSXT and Norfolk Southern jointly acquired the rights to operate Conrail, Inc. (“Conrail”) and then in 2004, CSXT acquired an allocated portion of Conrail’s assets, which CSXT operated. Conrail was formed in 1976 from several financially troubled northeast railroads to restructure and revive the region’s railroads. CSX’s acquisition of key portions of Conrail allowed CSXT to link the northeast, including New England and the New York metropolitan area, with Chicago, Midwest markets and the growing areas in the southeast that were already served by CSXT. This current rail network allows the Company to directly serve every major market in the eastern United States with dependable, environmentally friendly and fuel efficient freight transportation and intermodal service.

Regulatory Environment

The Company's operations are subject to a variety of federal, state and local laws and regulations, generally applicable to many businesses in the United States. The railroad operations conducted by the Company's subsidiaries, including CSXT, are subject in many respects to the regulatory jurisdiction of the Surface Transportation Board (“STB”) and the Federal Railroad Administration (“FRA”), which are both part of the Department of Transportation (“DOT”). Additionally, the Transportation Security Administration (“TSA”), a component of the Department of Homeland Security (“DHS”), has the authority to issue regulations and other directives that may also affect railroad operations. In some cases, state and local laws and regulations can be preempted in their application to railroads by the operation of these and other federal authorities.

Although the Staggers Act of 1980 significantly deregulated rail rates and much of the rail traffic of the Company's subsidiaries is currently exempt from rate regulation by agency decision, the STB has broad jurisdiction over railroad commercial practices. This includes jurisdiction over freight car rent, the transfer, extension or abandonment of rail lines, rates charged on certain regulated rail traffic and any acquisition of control over rail common carriers. In 2007, for example, the STB issued decisions changing its long-standing policy on fuel surcharges, its rules for large freight rate cases and a new process for rate cases where smaller amounts are at issue.

The FRA and its sister agency within the DOT, the Pipeline and Hazardous Materials Administration, have broad jurisdiction over railroad operating standards and practices, including track, freight cars and locomotives, and hazardous materials requirements. The TSA has broad authority over railroad operating practices that may have homeland security implications. The TSA has proposed regulations that would apply to the transportation of certain kinds of highly hazardous materials. Decisions of these and other agencies can affect the profitability of the Company’s business. For further discussion on regulatory risks to the Company, see Item 1A. Risk Factors beginning on page 8.

Competition

The business environment in which the Company operates is highly competitive. Shippers typically select transportation providers that offer the most compelling combination of service and price. Service requirements, both in terms of transit time and reliability, vary by shipper and commodity. As a result, the Company’s primary competition varies by commodity, geographic location and mode of available transportation.

CSX’s primary rail competitor is the Norfolk Southern, which operates throughout much of CSX’s territory. Other railroads also operate in parts of the territory. Depending on the specific market, competing railroads and deregulated motor carriers may exert pressure on price and service levels. For further discussion on the risk of competition to the Company, see Item 1A. Risk Factors beginning on page 8.

Other Information

CSX makes available on its website www.csx.com, free of charge, its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after such reports are filed with or furnished to the Securities and Exchange Commission (“SEC”). Additionally, the Company has posted its code of ethics on its website, which is also available to any shareholder who requests it. This Form 10-K and other SEC filings are also accessible through the SEC’s website at www.sec.gov.

CSX has included the certifications of its Chief Executive Officer (“CEO”) and the Chief Financial Officer (“CFO”) regarding the Company’s public disclosure required by Section 302 of the Sarbanes-Oxley Act of 2002 (“the Act”) as Exhibits 31.1 and 31.2, as well as Section 906 of the Act as Exhibits 32.1 and 32.2 to this Form 10-K report. Additionally, on May 31, 2007, CSX filed its annual CEO certification with the New York Stock Exchange (“NYSE”) confirming the Company’s compliance with the NYSE Corporate Governance Listing Standards. The CEO was not aware of any violations of these standards by the Company as of January 31, 2008 (the latest practicable date that is closest to the filing of this Form 10-K).

The Company’s annual average number of employees was approximately 35,000 in 2007, which includes approximately 29,000 union employees. Most of the Company’s employees provide or support transportation services. The information set forth in Item 6. Selected Financial Data is incorporated herein by reference.

For additional information concerning business conducted by the Company during 2007, see Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations and Item 8. Financial Statements and Supplementary Data - Note 15, Business Segments.

The following risk factors could have a materially adverse effect on the Company’s results of operations, financial condition and liquidity, and could cause those results to differ materially from those expressed or implied in the Company’s forward-looking statements. Although the risks described below are those that management believes are the most significant, these are not the only risks facing the Company. Additional risks and uncertainties not currently known to the Company or that the Company currently does not deem to be material also may materially impact the Company’s financial position, results of operations and liquidity.

New legislation or regulatory changes could impact the Company’s earnings or regulate its ability to independently negotiate prices.

The Company is subject to the jurisdiction of various regulatory agencies, including the STB, the FRA and other state and federal regulatory agencies for a variety of economic, health, safety, labor, environmental, tax, legal and other matters. Legislation passed by Congress or regulations issued by these agencies can significantly affect the revenues, costs and profitability of the Company’s business. For example, regulations imposing price constraints or affecting rail-to-rail competition could adversely affect the Company’s profitability. Also, additional regulations related to environmental matters such as greenhouse gas emissions or legislative changes impacting hours of service requirements could adversely affect the Company’s financial position, results of operations and liquidity.

CSXT, as a common carrier by rail, is required by law to transport hazardous materials, which could expose the Company to significant costs and claims.

Under federal regulations, CSXT is required to transport hazardous materials under its common carrier obligation. A train accident involving the transport of hazardous materials could result in significant claims arising from personal injury, property damage, and environmental penalties and remediation. CSXT is also required to comply with regulations regarding the handling of hazardous materials. Failure to comply with these regulations can subject the Company to significant penalties and could be a factor in litigation arising out of a train accident. Finally, legislation preventing the transport of hazardous materials through certain cities could result in network congestion and increase the length of haul for hazardous substances.

The Company is subject to environmental laws and regulations that may result in significant costs.

The Company’s operations are subject to wide-ranging federal, state and local environmental laws and regulations concerning, among other things, emissions into the air, discharges into water, the handling, storage, transportation and disposal of waste and other materials and clean-up of hazardous material or petroleum releases. In certain circumstances, environmental liability can extend to formerly owned or operated properties, leased properties, adjacent properties and properties owned by third parties or Company predecessors, as well as to properties currently owned and used by the Company.

The Company has been, and may be subject to, allegations or findings to the effect that it has violated, or is strictly liable under, environmental laws or regulations, and such violations can result in the Company’s incurring fines, penalties or costs relating to the clean-up of environmental contamination. Although the Company believes it has appropriately recorded current and long-term liabilities for known future environmental costs, it could incur significant costs as a result of any of the foregoing and may be required to incur significant expenses to investigate and remediate known, unknown or future environmental contamination.

General economic, geo-political and compliance risks may affect the Company’s operations and financial results.

Changes in general economic conditions that affect demand for rail or intermodal services could adversely affect the Company’s financial position, results of operations and liquidity. In addition, abrupt political change or terrorist activity poses a risk of general economic disruption and could require changes in the operations and security arrangements, thus increasing the operating costs. These conditions may lend additional uncertainty to the timing and purchasing decisions by the Company’s customers.

Fuel prices and supply are influenced by international political and economic circumstances. Although a fuel recovery program is in place with a considerable number of customers, the Company could be negatively impacted if it were unable to realize fuel surcharges. Additionally, if a fuel supply shortage were to arise, whether due to the Organization of the Petroleum Exporting Countries (OPEC) or other production restrictions, lower refinery outputs, a disruption of oil imports or otherwise, the Company would be negatively impacted.

The FRA regulates several of the Company’s core operations including track and mechanical equipment standards, signaling systems, inspection of grade crossing warning devices, locomotive engineer certifications and employee injury reporting, among other areas. The Company’s unintentional failure to comply with applicable laws or regulations could erode public confidence in CSX. In addition, a change in these regulations could have a material adverse effect on the Company’s financial position, results of operations and liquidity.

Network congestion, caused by unanticipated increases in freight or passenger activity, could have a negative impact on service and operating efficiency.

The Company may experience rail network difficulties related to network capacity, unplanned increases in demand for rail service, increased passenger activities in capacity-constrained areas or regulatory changes impacting when CSXT can transport freight or its service routes that could have a negative effect on the Company’s operational fluidity, leading to deterioration of service, asset utilization and overall efficiency. In addition, the Company may face external factors such as severe weather and other natural occurrences, including floods, fires, hurricanes and earthquakes, which may disrupt the Company’s operations.

Increases in the number and magnitude of property damage and personal injury claims could adversely affect the Company’s operating results.

The Company faces inherent business risk from exposure to property damage, occupational injury claims, and personal injury claims resulting from train accidents, worker injury claims under FELA and claims from outside parties resulting from the Company’s operations. Although the Company is working diligently to enhance its safety programs and to continue to raise the awareness levels of its employees concerning safety, the Company could experience material property damage, personal injury or occupational claims in the future and it may incur significant costs to defend such claims.

Existing claims may suffer adverse developments not currently reflected in reserve estimates, as the ultimate outcome of existing claims is subject to numerous factors outside of the Company’s control. The Company establishes reserves to cover all of these types of claims. However, final amounts determined to be due on any outstanding matters may differ materially from the recorded reserves.

The Company may be subject to various claims and lawsuits that could result in significant expenditures.

The Company is subject to various existing lawsuits and potential unknown litigation. The Company may experience material judgments or incur significant costs to defend any such lawsuits. Additionally, existing litigation may suffer adverse development not currently reflected in the Company’s reserve estimates as the ultimate outcome of existing litigation is subject to numerous factors outside of the Company’s control. While the Company uses its best efforts to evaluate existing litigation, the final judgments may differ materially from the recorded reserves.

Future acts of terrorism, war or regulatory changes to combat the risk of terrorism may cause significant disruptions in the Company’s operations.

Terrorist attacks, such as those that occurred in the United States in September 2001, in Spain in March 2004, in England in July 2005, and in India in July 2006, along with any government response to those attacks, may adversely affect the Company’s financial position, results of operations and liquidity. CSXT’s rail lines or other key infrastructure may be direct targets or indirect casualties of acts of terror or war. This could cause significant business interruption and result in increased costs and liabilities and decreased revenues. In addition, insurance premiums charged for some or all of the coverage currently maintained by the Company could increase dramatically or the coverage may no longer be available.

Furthermore, in response to the heightened risk of terrorism, federal, state and local governmental bodies are proposing and beginning to adopt various legislation and regulations relating to security issues that impact the transportation industry. For example, the DHS proposed regulations that would require freight railroads to implement additional security protocols when transporting hazardous materials.

Failure to complete negotiations on collective bargaining agreements could result in strikes and/or work stoppages.

Most of CSXT's employees are represented by labor unions and are covered by collective bargaining agreements. Generally speaking, these agreements are bargained nationally by the National Carriers Committee. In the rail industry, negotiations have generally taken place over a number of years and previously have not resulted in any extended work stoppages. Over the last 30 years, there were only six days of work stoppage related to labor disputes over national handling. If the Company is unable to negotiate acceptable agreements, it could result in strikes by the affected workers, loss of business and increased operating costs as a result of higher wages or benefits paid to union members, any of which could have an adverse effect on the Company’s financial position, results of operations and liquidity. Under the Railway Labor Act’s procedures (which include mediation, cooling-off periods and the possibility of Presidential intervention), neither party may exercise self-help until the procedures are exhausted.

The Company relies on the stability and availability of its technology systems to operate its business.

The Company relies on information technology in all aspects of its business. A significant disruption or failure of our information technology systems, including computer hardware, software and communications equipment, could result in a service interruption, safety failure, security breach or other operational difficulties. While the Company has taken steps to mitigate these risks, the performance and reliability of its technology systems are critical to its ability to compete effectively.

The Company faces competition from rail carriers and other transportation providers.

The Company experiences competition in the form of pricing, service, reliability and other factors from other transportation providers including railroads and motor carriers that operate similar routes across its service area and, to a less significant extent, barges, ships and pipelines. Transportation providers such as motor carriers and barges utilize public rights-of-way that are built and maintained by governmental entities while CSXT and other railroads must build and maintain rail networks using largely internal resources. Any future improvements or expenditures materially increasing the quality or reducing the cost of alternative modes of transportation, or legislation providing for less stringent size or weight restrictions on trucks, could negatively impact the Company’s financial position, results of operations and liquidity.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties by Segment

Rail Property

CSXT’s properties primarily consist of track and its related infrastructure, locomotives and freight cars. These categories and the geography of the network are described below.

Track and Infrastructure

Serving 23 states, the District of Columbia, and the Canadian provinces of Ontario and Quebec, the CSXT rail network serves, among other markets, New York, Philadelphia and Boston in the northeast and mid-Atlantic, the southeast markets of Atlanta, Miami and New Orleans, and the Midwestern cities of St. Louis, Memphis and Chicago.

CSXT’s track structure includes main thoroughfares connecting terminals and yards (known as mainline track); track within terminals and switching yards; track adjacent to the mainlines used for passing trains; track connecting the mainline track to customer locations; and track that diverts trains from one track to another known as turnouts. Total track miles are greater than the Company’s approximately 21,000 route miles, which reflect the size of CSX’s rail network that connects markets, customers and western railroads. At December 2007, the breakdown of track miles was as follows:

| | Track |

| | Miles |

| Mainline track | 26,712 |

| Terminals and switching yards | 9,626 |

| Passing sidings and turnouts | 1,037 |

| Total | 37,375 |

In addition to its physical track structure, CSXT operates numerous yards and terminals. These serve as the hubs between CSXT and its local customers and as sorting facilities where rail cars often are received, re-sorted and placed onto new outbound trains.

The following 36 yards are identified as key to the CSXT system (listed in alphabetical order by state):

| |

| Rail Yards or Terminals |

| Birmingham, AL | Detroit, MI |

| Mobile, AL | Hamlet, NC |

| Montgomery, AL | Rocky Mount, NC |

| Baldwin, FL | Buffalo, NY |

| Moncrief (Jacksonville), FL | Selkirk, NY |

| Tampa, FL | Syracuse, NY |

| Atlanta, GA | Cincinnati, OH |

| East Savannah, GA | Cleveland, OH |

| Waycross, GA | Columbus, OH |

| Avon (Indianapolis), IN | Stanley (Toledo), OH |

| Chicago, IL | Walbridge (Toledo), OH |

| Evansville, IN | Willard, OH |

| Louisville, KY | Greenwich (Philadelphia), PA |

| Russell, KY | Charleston, SC |

| New Orleans, LA | Florence, SC |

| Cumberland, MD | Erwin, TN |

| Curtis Bay (Baltimore), MD | Nashville, TN |

| Locust Point (Baltimore), MD | Richmond, VA |

For a list of Intermodal’s terminals, see page 16.

Network Geography

CSXT’s train operations are primarily focused around the following four major transportation networks, which are defined geographically or by line of business and are described below.

Coal Network – Coal is used to generate more than half of the electricity in the United States. The CSXT coal network connects mining operations in nine states with industrial areas in the northeast and mid-Atlantic, as well as many river, lake and seaport facilities. This network also supports the strong, growing utility market in the southeast.

Southeastern Corridor – This section of the network runs from the western gateways of Chicago, Memphis and St. Louis through the growing cities of Nashville, Birmingham and Atlanta and into the expanding markets in the southeast. CSXT’s capacity investment in this corridor clearly strengthens this route and makes it the premier rail route connecting these key cities and gateways with the growing southeast. The corridor extends through the coal reserves of the southern Illinois basin and provides direct rail service between these coal sources and the increasing demand for coal in the southeast. The increase in capacity on this corridor positions CSXT well to handle the projected traffic volumes of intermodal, coal, automotive and general merchandise traffic.

Interstate 90 (I-90) Corridor – Chicago and metropolitan areas in New York and New England are linked by CSXT’s I-90 Corridor. Much of this route has two lanes of track side-by-side (referred to as double mainline track) supporting high-speed intermodal and automotive services. The I-90 Corridor is also a primary route for import traffic moving across the country, through Chicago and into the population centers in the northeast. Continued growth in consumption in the east and northeast makes this corridor a critical element in the Company’s overall system.

Interstate 95 (I-95) Corridor – Charleston, Jacksonville, Miami and many other cities throughout the growing southeast are connected to the heavily populated northeastern cities of Baltimore, Philadelphia and New York along CSXT’s I-95 Corridor. This route is primarily used to ship food and consumer products, as well as metals and chemicals. It is the only rail corridor along the east coast south of Washington, D.C., and provides access to all the major eastern ports.

Locomotives

CSXT focuses on maximum use of its fleet and prudent investment in new units to drive the rail network. Better locomotive management helps CSXT move freight more efficiently, while continued investment in CSXT’s power source means CSXT is operating more locomotives better.

CSXT operates more than 4,000 locomotives, of which over 95% are owned by CSXT. Freight locomotives are the power source used primarily to pull rail cars. Switching locomotives are used in yards to sort railcars so that the right railcar gets attached to the right train in order to get it to its final destination. Auxiliary units are typically used to provide extra traction for heavy trains in hilly terrain. At December 2007, CSXT’s owned and long-term leased locomotives consisted of the following:

| |

| | Locomotives | | % |

| Freight | 3,495 | | 87% |

| Switching | 324 | | 8% |

| Auxiliary Units | 188 | | 5% |

| Total | 4,007 | | 100% |

Freight Car Fleet

The average daily fleet of cars-on-line consists of approximately 222,000 cars, but at any point in time, over half of the railcars on the CSXT system are not owned or leased by CSXT. Examples of these are: railcars owned by other railroads (which are utilized by CSXT), shipper-furnished or private cars (which are generally used only in that shipper’s service) and multi-level railcars.

CSXT’s freight car fleet consists of six main types of cars:

Gondolas – Support CSXT’s metals markets and provide transport for woodchips and other bulk commodities. Some gondolas are equipped with special hoods for protecting products like coil and sheet steel.

Open-top hoppers – Transport heavy dry bulk commodities such as coal, coke, stone, sand, ores and gravel that are resistant to weather conditions.

Box cars – Include a variety of tonnages, sizes, door configurations and heights to accommodate a wide range of finished products, including paper, auto parts, appliances and building materials. Insulated box cars deliver food products, canned goods, beer and wine.

Covered hoppers – Have a permanent roof and are segregated based upon commodity density. Lighter bulk commodities such as grain, fertilizer, flour, salt, sugar, clay and lime are shipped in large cars called jumbo covered hoppers. Heavier commodities like cement, ground limestone and glass sand are shipped in small cube covered hoppers.

Multi-level flat cars – Transport finished automobiles and are differentiated by the number of levels: bi-levels for large vehicles such as pickup trucks and SUVs and tri-levels for sedans and smaller automobiles.

Flat cars – Used for shipping intermodal containers and trailers or bulk and finished goods, such as lumber, pipe, plywood, drywall and pulpwood.

Other cars owned or leased on the network include, but are not limited to, center beam cars for transporting lumber and building products.

CSXT owns more than 60% of its freight cars. At December 2007, CSXT’s owned and long-term leased freight car fleet consisted of the following:

| |

| | Freight Cars | | % |

| Gondolas | 26,490 | | 28% |

| Open-top hoppers | 19,604 | | 21% |

| Box cars | 13,911 | | 15% |

| Covered hoppers | 13,555 | | 14% |

| Multi-level flat cars | 12,340 | | 13% |

| Flat cars | 7,189 | | 8% |

| Other cars | 1,275 | | 1% |

| Total | 94,364 | | 100% |

Intermodal Property

Infrastructure

Intermodal serves 51 terminals in 22 states. These terminals serve as a transfer point between rail and trucks. If the city has more than one terminal, it is indicated by the number next to it.

| Intermodal Terminals |

| Mobile, AL | Kansas City, MO |

| Lathrop, CA | Charlotte, NC |

| Los Angeles/Long Beach, CA (3) | North Bergen, NJ |

| Oakland, CA | Blasdell, NY |

| Jacksonville, FL (2) | Syracuse, NY |

| Orlando, FL | New York, NY/NJ (5) |

| Tampa, FL | Cincinnati, OH |

| Atlanta, GA (2) | Cleveland, OH |

| Savannah, GA (2) | Columbus, OH (2) |

| Chicago, IL (2) | Marion, OH |

| East St. Louis, IL | Portland, OR |

| Avon, IN | Chambersburg, PA |

| Evansville, IN | Philadelphia, PA |

| New Orleans, LA | Charleston, SC |

| Boston, MA | Memphis, TN |

| Springfield, MA | Nashville, TN |

| Worcester, MA (3) | Mesquite, TX |

| Baltimore, MD | Portsmouth, VA |

| Detroit, MI | Seattle, WA |

Equipment

Intermodal equipment consists primarily of containers, chassis and other equipment (such as lift equipment). Containers are weather-proof boxes used for bulk shipment of freight, and chassis are the wheeled support framework for a container that allows it to be attached to a tractor. All of Intermodal’s chassis are leased. Intermodal also has other types of equipment such as doublestack railcars, which are railcars that allow for two containers to be mounted one above the other.

At December 28, 2007, Intermodal owned or long-term leased equipment consisted of the following:

| | Equipment | | % |

| Chassis | 25,980 | | 67% |

| Containers | 12,503 | | 32% |

| Other | 433 | | 1% |

| Total | 38,916 | | 100% |

Item 3. Legal Proceedings

The Company is subject to various legal proceedings and claims that arise in the ordinary course of business. For more information on legal proceedings, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations under the caption “Critical Accounting Estimates – Casualty, Environmental and Legal Reserves” and Item 8. Financial Statements and Supplementary Data - Note 7, Commitments and Contingencies under the caption “Other Legal Proceedings.”

Item 4. Submission of Matters to a Vote of Security Holders

There were no matters submitted to a vote of security holders in the fourth quarter of 2007.

Executive Officers of the Registrant

Executive officers of CSX are elected by the CSX Board of Directors and generally hold office until the next annual election of officers. There are no family relationships or any arrangement or understanding between any officer and any other person pursuant to which such officer was elected. As of December 2007, the executive officers are:

Name and Age | Business Experience During Past 5 Years |

Michael J. Ward, 57 Chairman, President and Chief Executive Officer | A 30-year veteran of the Company, Ward has served as Chairman, President and Chief Executive Officer since January 2003. In 2000, he was named President of CSXT, and he was later appointed President of CSX and elected to the Board of Directors in 2002. His distinguished railroad career has included key executive positions in nearly all aspects of the Company’s business, including sales and marketing, operations and finance. |

Oscar Munoz, 48 Executive Vice President and Chief Financial Officer | Munoz has served as Executive Vice President and Chief Financial Officer of CSX and CSXT since May 2003 and is responsible for management and oversight of all financial, strategic planning, information technology, purchasing and real estate activities of CSX. He brings to the Company years of experience from a variety of industries. Before joining CSX in 2003, Munoz served as Chief Financial Officer and Vice President of AT&T Consumer Services. He has also held key executive positions within the telecommunication and beverage industries. |

Name and Age | Business Experience During Past 5 Years |

| Tony L. Ingram, 61 Executive Vice President and Chief Operating Officer | Ingram has served as Executive Vice President and Chief Operating Officer of CSXT since March 2004 and manages all aspects of the Company’s operations across its 21,000-mile network, including transportation, service design, customer service, engineering and mechanical. Prior to joining CSX in 2004, Ingram spent more than 30 years at Norfolk Southern where he served as Senior Vice President – Transportation, Network and Mechanical from February 2003 to March 2004 and Vice President, Transportation – Operations from March 2000 to February 2003. |

Clarence W. Gooden, 56 Executive Vice President of Sales and Marketing and Chief Commercial Officer | Gooden has been the Executive Vice President and Chief Commercial Officer of CSX and CSXT since April 2004 and is responsible for generating customer revenue, forecasting business trends and developing CSX’s model for future revenue growth. A member of the CSX family for more than 35 years, Gooden has held key executive positions in both operations and sales and marketing, including being appointed President of CSX Intermodal in 2001 and Senior Vice President of the Merchandise Service Group in 2002. |

Ellen M. Fitzsimmons, 47 Senior Vice President of Law and Public Affairs, General Counsel and Corporate Secretary | Fitzsimmons has been the Senior Vice President of Law and Public Affairs, General Counsel, and Corporate Secretary since December 2003. She serves as the Company’s chief legal officer and oversees all government relations and public affairs activities. During her 16-year tenure with the Company, her broad responsibilities have included key roles in major risk and corporate governance-related areas such as Senior Vice President – Law and Corporate Secretary from May to December 2003 and as Senior Vice President – Law from February 2001 to May 2003. |

Name and Age | Business Experience During Past 5 Years |

Robert J. Haulter, 54 Senior Vice President of Human Resources and Labor Relations | Haulter has served as Senior Vice President – Human Resources and Labor Relations of CSX and CSXT since December 2003 and is responsible for employee compensation and benefits, labor relations, organizational development and transformation, recruitment, training and various administrative activities. His 30-year career with the Company has included key executive positions in operations, finance and human resources before being appointed Vice President of Human Resources in 2000. |

Carolyn T. Sizemore, 44 Vice President and Controller | Sizemore has served as Vice President and Controller of CSX and CSXT since April 2002 and is responsible for financial and regulatory reporting, paying the Company’s 35,000 employees, accounts payable and billing and collections for outside party expenditures along with various other accounting processes. Her responsibilities during her 18-year tenure with the Company have included roles in finance and audit-related areas including a variety of positions in accounting, finance strategies, budgets and performance analysis. |

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

CSX’s common stock is listed on the NYSE, which is its principal trading market, and is traded over-the-counter and on exchanges nationwide. The official trading symbol is “CSX.”

Description of Common and Preferred Stock

A total of 600 million shares of common stock is authorized, of which 407,864,394 shares were outstanding as of December 28, 2007. Each share is entitled to one vote in all matters requiring a vote of shareholders. There are no pre-emptive rights. At January 31, 2008, the latest practicable date, there were 46,749 common stock shareholders of record. The weighted average of common shares outstanding, which was used in the calculation of diluted earnings per share, was approximately 448 million as of December 28, 2007. (See Note 2, Earnings Per Share.)

A total of 25 million shares of preferred stock is authorized, none of which is currently outstanding.

The following table sets forth, for the quarters indicated, the dividends declared and the high and low share prices of CSX common stock as required by SEC Regulation S-K.

| | Quarter | |

| | | | 1st | 2nd | 3rd | 4th | | Year |

| 2007 |

| | Dividends | $0.12 | $0.12 | $0.15 | $0.15 | | $0.54 |

| | Common Stock Price | |

| | High | $42.53 | $47.38 | $51.88 | $46.49 | | $51.88 |

| | Low | $33.50 | $39.36 | $38.09 | $40.17 | | $33.50 |

| |

| 2006 |

| | Dividends | $0.065 | $0.065 | $0.10 | $0.10 | | $0.33 |

| | Common Stock Price | |

| | High | $30.20 | $37.33 | $35.58 | $38.30 | | $38.30 |

| | Low | $24.29 | $30.05 | $28.60 | $32.51 | | $24.29 |

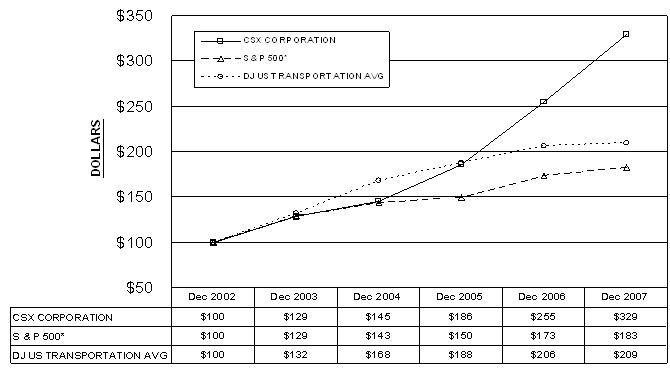

Stock Performance Graph

The cumulative shareholder returns, assuming reinvestment of dividends, on $100 invested at December 31, 2002 is illustrated on the graph below. The Company references the Standard & Poor 500 Stock Index (“S&P 500”) and the Dow Jones U.S. Transportation Average Index, which provide comparisons to a broad-based market index and other companies in the transportation industry. As shown in the graph, CSX’s five-year stock returns significantly outpaced those of the S&P 500. Additionally the Company’s stock has increased 120% over the past three years under the direction of the current management team.

* The S&P 500 is a registered trademark of the McGraw-Hill Companies, Inc.

CSX Purchases of Equity Securities

CSX is required to disclose any purchases of its own common stock for the most recent quarter. CSX purchases its own shares for two primary reasons: to further the goals under its share repurchase program and to fund the Company’s contribution required to be paid in CSX common stock under 401(k) plans which cover certain union employees.

Currently, CSX has purchased $2.1 billion of its outstanding common stock, which represents 50 million shares or about 70% of the $3 billion share repurchase program that was authorized in 2007. CSX intends to complete this repurchase program during 2008. The timing, method, amount of repurchase transactions and the sources of funds to affect any repurchases will be determined by the Company's management based on their evaluation of market conditions, share price and other factors. While it is not management’s intention, the program could be suspended or discontinued at any time.

Share repurchase activity for fourth quarter 2007 was as follows:

| | CSX Purchases of Equity Securities for the Quarter | |

| |

| Fourth Quarter | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs |

| |

| Beginning Fourth Quarter Balance | | $ 1,439,716,780 |

| |

| October |

| | (September 29, 2007 - October 26, 2007) | 5,724,300 | $ 43.11 | 5,724,300 | | $ 1,192,930,945 |

| | | | | | | |

| November |

| | (October 27, 2007 - November 23, 2007) | 4,933,700 | $ 43.60 | 4,933,700 | | $ 977,804,729 |

| |

| December |

| | (November 24, 2007 - December 28, 2007) | 2,510,900 | $ 41.20 | 2,510,900 | | $ 874,363,982 |

| | | |

| Total/Ending Balance | 13,168,900 | $ 42.93 | 13,168,900 | | $ 874,363,982 |

Including previous share repurchase programs, CSX has purchased over $2.6 billion of its outstanding common stock over the past two years.

Item 6. Selected Financial Data

Selected financial data and significant events related to the Company’s financial results for the last five fiscal years are listed below.

| | Fiscal Years |

| (Dollars in Millions, Except Per Share Amounts) | 2007 | 2006 | 2005 | 2004 | 2003 |

| |

| Earnings From Continuing Operations |

| | Operating Revenue | $ 10,030 | $ 9,566 | $ 8,618 | $ 8,040 | $ 7,573 |

| | Operating Expense | 7,774 | 7,428 | 7,068 | 7,040 | 7,053 |

| | Operating Income | $ 2,256 | $ 2,138 | $ 1,550 | $ 1,000 | $ 520 |

| |

| Earnings from Continuing Operations | $ 1,226 | $ 1,310 | $ 720 | $ 418 | $ 137 |

| |

| Earnings Per Share: |

| | From Continuing Operations | $ 2.85 | $ 2.98 | $ 1.67 | $ 0.97 | $ 0.32 |

| | From Continuing Operations, Assuming Dilution | 2.74 | 2.82 | 1.59 | 0.94 | 0.31 |

| |

| Financial Position |

| | Cash, Cash Equivalents and Short-term Investments | $ 714 | $ 900 | $ 602 | $ 859 | $ 368 |

| | Total Assets | 25,534 | 25,129 | 24,232 | 24,605 | 21,760 |

| | Long-term Debt | 6,470 | 5,362 | 5,093 | 6,248 | 6,886 |

| | Shareholders' Equity | 8,685 | 8,942 | 7,954 | 6,811 | 6,448 |

| |

| Other Data Per Common Share |

| | Dividend Per Share | $ .54 | $ 0.33 | $ 0.215 | $ 0.20 | $ 0.20 |

| |

| Employees -- Annual Averages |

| | Rail | 32,477 | 32,987 | 32,033 | 32,074 | 32,892 |

| | Other | 2,966 | 3,018 | 3,076 | 3,833 | 4,624 |

| | Total | 35,443 | 36,005 | 35,109 | 35,907 | 37,516 |

Significant Events

| | 2007 | -- | Recognized gains of $27 million before tax, or $17 million after tax, on insurance recoveries from claims related to Hurricane Katrina. (See Note 5, Hurricane Katrina.) |

| | 2006 | -- | Two-for-one split of the Company’s common stock effective 2006. All periods have been retroactively restated to reflect the stock split. |

| | -- | Recognized gains of $168 million before tax, or $104 million after tax, on insurance recoveries from claims related to Hurricane Katrina. (See Note 5, Hurricane Katrina.) |

| | -- | Recognized an income tax benefit of $151 million primarily related to the resolution of certain tax matters, including resolution of ordinary course federal income tax audits for 1994 – 1998. |

| | -- | Recognized a $26 million after-tax non-cash gain on additional Conrail property received. |

| Significant events, continued: |

| | 2005 | -- | Recognized a charge of $192 million pretax, $123 million after tax, to repurchase $1.0 billion of outstanding debt, for costs of the increase in current market value above original issue value. (See Note 9, Debt and Credit Agreements.) |

| | -- | Recognized an income tax benefit of $71 million for the Ohio legislative change to gradually eliminate its corporate franchise tax. |

| | 2004 | -- | Recognized a charge of $71 million pretax, $44 million after tax, for separation expenses related to management restructuring. |

| | -- | Recognized a $16 million after-tax non-cash gain on the Conrail spin-off transaction. |

| | -- | Completed a corporate reorganization of Conrail that resulted in the direct ownership of certain Conrail assets by CSXT and caused a significant increase in total assets. |

| | 2003 | -- | Recognized a charge of $232 million pretax, $145 million after tax, in conjunction with the change in estimate of casualty reserves to include an estimate of incurred but not reported claims for asbestos and other occupational injuries to be received over the next seven years. |

| | -- | Recognized a charge of $108 million pretax, $67 million after tax, for two settlement agreements with Maersk that resolved all material disputes pending between the companies arising out of the 1999 sale of the international container-shipping assets. |

| | -- | Recognized a net charge of $22 million pretax, $13 million after tax. This includes a charge of $44 million pretax, $26 million after tax, which is comprised of the initial charge for separation expenses related to the management restructuring announced in 2003 of $34 million pretax and an additional separation charge of $10 million pretax included in the Company’s third quarter results. These amounts were offset by a net credit of $22 million pretax, $13 million after tax, related to revised estimates for railroad retirement taxes and the amount of benefits that will be paid to individuals under the 1991 and 1992 separation plans. |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

STRATEGIC OVERVIEW

The Company provides customers access to a modern transportation network that connects ports, production and distribution centers to markets in the Northeast, Midwest and the rapidly growing southern states. The Company transports a diversified portfolio of products, from domestically abundant coal to new energy sources such as ethanol, from automobiles produced by traditional American manufacturers to “new domestic” factories owned by European, Japanese and Korean companies, and from life-essential chemicals to life-enriching consumer electronics. Additionally, the Company serves every major market in the eastern United States and has direct access to all Atlantic and Gulf Coast ports, as well as the Mississippi River, The Great Lakes and the St. Lawrence Seaway. Furthermore, the Company has access to Pacific ports through alliances with western railroads. Overall, the Company’s transportation network encompasses approximately 21,000 route miles of track in 23 states, the District of Columbia and the Canadian provinces of Ontario and Quebec.

As the nation consumes increasingly higher quantities of imported goods, those products must be transported across the country in a way that minimizes the impact on the environment, takes traffic off an already congested highway system and minimizes fuel consumption and transportation costs. The Company’s transportation network, located in the largest and fastest-growing population centers in the nation, is well-positioned to capitalize on consumption growth trends. In this regard, more than two-thirds of Americans live within the Company’s service territory, accounting for about three-quarters of the nation’s consumption.

The Company has made substantial strides in operating performance in order to capitalize on these consumption growth trends. In 2004, the Company implemented the ONE Plan, which continues to focus on optimizing the train network and utilizing rail assets more efficiently. Anchored by the ONE Plan and a variety of other initiatives implemented after the ONE Plan was introduced, the Company has achieved significant operational improvements that have enhanced safety, service reliability and productivity. These strong results include the highest customer satisfaction scores ever achieved by the Company as measured by independent surveys of its customers.

In addition to the ONE Plan, the Company recently embarked on a new initiative called Total Service Integration (“TSI”), which aims to better align the Company’s capabilities with customer demands. TSI aims to optimize train size and increase asset utilization while delivering more reliable service to customers.

These initiatives delivered strong results for shareholders while higher levels of customer service have led to improved pricing. These efforts combined with operational efficiencies have resulted in substantial improvements in CSX’s operating income and operating ratio.

In addition to driving better financial results to create value for shareholders, CSX also employs a balanced approach in deploying its capital for the benefit of shareholders. This approach includes investments in the future, share repurchases and dividends. Through this balanced use of financial resources, CSX will continue to capitalize on an economic environment that is increasingly favoring rail transportation.

Surface Transportation

| | · | Revenue grew $464 million or 5% to over $10 billion. |

| | · | Expenses increased $339 million or 5% to $7.8 billion, which included $141 million of higher prior year gains on insurance recoveries (which reduced operating expenses) and $98 million of higher fuel costs. |

| | · | Surface Transportation Operating Income, which excludes other operating income, increased $125 million to $2.3 billion. |

| | · | Service and safety measurements improved in all categories. |

Leadership, discipline and execution resulted in excellent 2007 results, which included the lowest Surface Transportation operating ratio in a decade. Revenue and revenue per unit increased 5% and 8%, respectively, from a year ago reflecting the improving value CSX provides its customers through better service. The Company was able to achieve substantial pricing gains predominantly due to CSXT service improvements and the overall cost advantages that the Company’s rail-based solutions provide to customers versus other modes of transportation.

The strong results in revenue were achieved despite volume declines in all of the Company’s four major lines of business. The overall 3% volume decrease versus last year was primarily driven by continued weakness in the merchandise market relating to housing construction and associated markets, as well as lower automotive production.

Expenses were higher due to the effects of rising fuel prices and higher prior year gains on insurance recoveries, which were recorded as a reduction to operating expenses. Lower 2007 volume and better productivity from improved operations partially offset the effects of inflation for certain expense categories.

For additional information, refer to Rail and Intermodal Results of Operations discussed on pages 40 through 43.

The Company’s continued focus on safety and operating plan execution helped all service measurements improve compared to last year. Within the service measures, CSX achieved record performance on both of its key safety measures (FRA Personal Injuries Frequency Index and FRA Train Accident Rate) in 2007 despite some costly train accidents. Improved safety is the result of the safety leadership and train accident prevention processes. Both of these use training, awareness, compliance measurement and root cause analysis to prevent incidents and create a safer work environment.

In addition, CSX continues to improve its train operations with gains of 4% and 12% in On-Time Train Originations and On-Time Destination Arrivals, respectively. Velocity, a measure of overall network fluidity, increased 5% in 2007. More important was the consistent week-to-week velocity, which indicates more reliable service to customers. Improved network operations also drove increased asset utilization, including an improvement of 8% in Dwell, which is the average time cars spend in terminals when being switched. The table below shows these key measurements and resources.

| RAIL OPERATING STATISTICS (Estimated) | Fiscal Years | |

| | 2007 | 2006 | Improvement | % |

| Service |

| Measurements | FRA Personal Injuries Frequency Index | 1.21 | 1.46 | 17 | % |

| |

| | FRA Train Accident Rate | 2.83 | 3.54 | 20 | |

| |

| | On-Time Train Originations | 79.3% | 76.0% | 4 | |

| | On-Time Destination Arrivals | 70.4% | 62.7% | 12 | |

| |

| | Dwell (hours) | 23.2 | 25.1 | 8 | |

| | Cars-On-Line | 221,943 | 224,680 | 1 | |

| |

| | System Train Velocity (miles per hour) | 20.8 | 19.9 | 5 | |

| |

| | Recrews (per day) | 57 | 59 | 3 | % |

| |

| | Increase/ | |

| | (Decrease) | |

| Resources | Route Miles | 21,166 | 21,114 | - | % |

| | Locomotives (owned and long-term leased) | 4,007 | 3,851 | 4 | |

| | Freight Cars (owned and long-term leased) | 94,364 | 101,602 | (7) | % |

Key Performance Measures Definitions

FRA Personal Injuries Frequency Index – Number of FRA-reportable injuries per 200,000 man-hours

FRA Train Accident Rate – Number of FRA-reportable train accidents per million train-miles

On-Time Train Originations – Percent of scheduled road trains that depart the origin yard on-time or ahead of schedule per the ONE Plan

On-Time Destination Arrivals – Percent of scheduled trains that arrive at the destination yard on-time to two hours late (30 minutes for intermodal trains) per the ONE Plan

Dwell – Measures the time (in hours) cars spend in each yard (does not include cars moving through the yard on the same train)

Cars-On-Line – A count of all cars on the CSX network, including those at customer locations (does not include locomotives, cabooses, trailers, containers or maintenance equipment)

System Train Velocity – Average train speed between terminals in miles per hour (does not include locals, yard jobs, work trains or passenger trains)

Recrews – Number of relief crews called, a measure of line of road efficiency in the use of crews

Other Highlights

While operating activities generated higher cash, free cash flow, which includes dividend payments, declined $216 million to $145 million during 2007. The decline was primarily due to higher capital expenditures and dividends, along with lower insurance recoveries from claims related to Hurricane Katrina. See page 32 for further details on the changes in free cash flow during 2007.

Surface Transportation capital expenditures, which exclude The Greenbrier, were $1.7 billion in 2007. This level of investment highlights the Company’s commitment to maintain and improve its existing infrastructure and to position itself for long-term growth through expanding network and terminal capacity. The increase compared to prior year was largely due to refinancing a portion of its locomotive capacity by replacing 150 leased units with newly owned locomotives.

CSX also announced three significant financial events in 2007. First, CSX increased its quarterly dividend from $0.10 to $0.12 during the first quarter of 2007. It then increased the dividend again during the third quarter of 2007 to $0.15, which represented a 50% increase from the quarterly dividend level at fourth quarter 2006. Finally, CSX announced a total of $3 billion in share repurchase programs during 2007 and has completed about 70% of the repurchases. See Note 1, Nature of Operations and Significant Accounting Policies.

Long-term Transportation Demand

Transportation demand is based on increases in population and higher consumption levels, which in turn drive the production of goods domestically and abroad that must be transported from factories and ports to the markets where they will be consumed.

Recent census projections estimate that today’s population of 301 million people will grow to more than 330 million by 2020. Major metropolitan areas in the southeast, where CSX has a strong presence, are projected to grow at significantly faster rates. Even in slower-growing areas over the remainder of the Company’s territory, consumption levels are projected to increase.

Freight tonnage – domestic and international – is expected to increase nearly 50% by 2020, according to the American Association of State Highway and Transportation Officials (AASHTO), placing further strain on the transportation system of America and requiring reliable solutions for shippers worldwide.

Impact on CSX

The Company is well positioned to meet the nation’s growing transportation demand. For example, due to factors such as highway congestion, new regulations on hours of service and driver shortages in the trucking industry, trucking companies are beginning to partner with the Company to outsource their long-haul services and reduce their cost of shipping due to the superior cost structure of the railroads for long-haul shipments.

Additionally, the need for environmentally sensitive transportation solutions also favors CSX because railroads are three times more fuel efficient than highway transportation. A single train can carry the load of more than 280 trucks, reducing highway congestion and pollution while moving goods more efficiently.

Industry analysts predict that the pricing environment will reflect the increasing importance of railroads in serving America’s growing transportation needs and the cost of the infrastructure investments needed to maintain the safety and security of these networks and to expand them. This will drive revenue growth as volumes increase. Furthermore, while the market for transportation services remains competitive, tighter capacity and improved service levels through initiatives such as the ONE Plan and TSI are expected to sustain this favorable pricing environment, reflecting the overall value that CSX provides to its customers.

Forecasts

The Company bases its performance expectations on external forecasts of economic indicators such as gross domestic product, industrial production and overall import levels. Although certain markets will remain weak, such as those that are impacted by the housing and automotive sectors, the indicators that influence CSX’s businesses are expected to be favorable in 2008. Considering these and other factors, the Company believes that its business environment remains strong and will support consistent, continuous financial improvements for the next several years.

Considering the Company’s solid overall business environment, along with momentum in its underlying business performance, CSX expects that its financial performance in 2008 will be consistent with its long-term financial targets, which include compounded annual growth rates (“CAGR”) as shown below:

| Long-term Financial Targets | 2008-2010 Targets |

| · | Operating Income Growth | 10% - 12% CAGR |

| · | Earnings Per Share Growth | 15% - 17% CAGR |

| · | Operating Ratio | Mid- to low- 70s by 2010 |

| · | Free Cash Flow (before the payment of dividends) | $800 million to $1 billion in 2010 |

To reinforce its long-term vision, the Company’s Surface Transportation capital budget is expected to be nearly $5 billion between 2008 and 2010. These investments come at a time when the return on investment in the railroad industry is improving. Approximately 60% of the Company’s capital is targeted for infrastructure investment to improve network reliability and recoverability and to drive even better performance in safety. Another 20% of the Company’s capital will be invested in its locomotive and freight car fleets. The remaining 20% of CSX’s capital spending will further expand network terminal capacity, improve technology and position the Company for long-term growth.

Free Cash Flow

Free cash flow is considered a non-GAAP financial measure under SEC Regulation G, Disclosure of Non-GAAP Measures. Management believes, however, that free cash flow is important in evaluating the Company’s financial performance and measures an ability to generate cash without incurring additional external financing. Free cash flow should be considered in addition to, rather than a substitute for, cash provided by operating activities.

Free cash flow is calculated by using net cash from operations and adjusting for property additions, dividends and certain other investing activities such as insurance proceeds. Also, added to free cash flow is the Company’s 42% economic interest in Conrail’s free cash flow which is not consolidated in CSX amounts. Other deposits, which are included in cash provided by operating activities, are not included in the Company’s free cash flow because these deposits represent assets that were set aside for specific debt payments.

The following table reconciles cash provided by operating activities (GAAP measure) to free cash flow (non-GAAP measure).

| | Fiscal Years | |

| | 2007 | 2006 | | Change |

| (Dollars in Millions) |

| Net cash provided by operating activities | $ 2,184 | $ 2,058 | | $ 126 |

| Property additions | (1,773) | (1,639) | | (134) |

| Insurance proceeds within investing activities | 16 | 147 | | (131) |

| Other investing activities | (57) | 4 | | (61) |

| Dividends | (231) | (145) | | (86) |

| Other deposits and Conrail free cash flow | 6 | (64) | | 70 |

| Free Cash Flow (after payment of dividends) | $ 145 | $ 361 | | $ (216) |

Certain statements in this report and in other materials filed with the SEC, as well as information included in oral statements or other written statements made by the Company, are forward-looking statements within the meaning of the Securities Act of 1933 and the Securities Exchange Act of 1934. These forward-looking statements include, among others, statements regarding:

| | · | Expectations as to results of operations and operational improvements; |

| | · | Expectations as to the effect of claims, lawsuits, environmental costs, commitments, contingent liabilities, labor negotiations or agreements on the Company’s financial condition; |

| | · | Management’s plans, goals, strategies and objectives for future operations and other similar expressions concerning matters that are not historical facts, and management’s expectations as to future performance and operations and the time by which objectives will be achieved; and |

| | · | Future economic, industry or market conditions or performance, including, but not limited to, the discussion regarding Expectations on page 30. |

Forward-looking statements are typically identified by words or phrases such as “believe,” “expect,” “anticipate,” “project,” “estimate” and similar expressions. The Company cautions against placing undue reliance on forward-looking statements, which reflect its good faith beliefs with respect to future events and are based on information currently available to it as of the date the forward-looking statement is made. Forward-looking statements should not be read as a guarantee of future performance or results and will not necessarily be accurate indications of the timing when, or by which, such performance or results will be achieved.

Forward-looking statements are subject to a number of risks and uncertainties and actual performance or results could differ materially from those anticipated by these forward-looking statements. The Company undertakes no obligation to update or revise any forward-looking statement. If the Company does update any forward-looking statement, no inference should be drawn that the Company will make additional updates with respect to that statement or any other forward-looking statements. The following important factors, in addition to those discussed elsewhere, may cause actual results to differ materially from those contemplated by these forward-looking statements:

| | · | Legislative, regulatory or legal developments involving transportation, including rail or intermodal transportation, the environment, hazardous materials, taxation, including the outcome of tax claims and litigation, the potential enactment of initiatives to re-regulate the rail industry and the ultimate outcome of shipper and rate claims subject to adjudication; |

| | · | The outcome of litigation and claims, including, but not limited to, those related to fuel surcharge, environmental contamination, personal injuries and occupational illnesses; |

| | · | Material changes in domestic or international economic or business conditions, including those affecting the transportation industry such as access to capital markets, ability to revise debt arrangements as contemplated, customer demand, customer acceptance of price increases, effects of adverse economic conditions affecting shippers and adverse economic conditions in the industries and geographic areas that consume and produce freight; |

| | · | Changes in fuel prices, surcharges for fuel and the availability of fuel; |

| | · | The impact of increased passenger activities in capacity-constrained areas or regulatory changes affecting when CSXT can transport freight or service routes; |

| | · | Natural events such as severe weather conditions, including floods, fire, hurricanes and earthquakes, a pandemic crisis affecting the health of the Company’s employees, its shippers or the consumers of goods, or other unforeseen disruptions of the Company’s operations, systems, property or equipment; |

| | · | An unintentional failure to comply with applicable laws or regulations; |

| | · | The inherent risks associated with safety and security, including the availability and cost of insurance, the availability and vulnerability of information technology, adverse economic or operational effects from actual or threatened war or terrorist activities and any governmental response; |

| | · | Labor costs and labor difficulties, including stoppages affecting either the Company’s operations or the customers’ ability to deliver goods to the Company for shipment; |

| | · | Competition from other modes of freight transportation, such as trucking and competition and consolidation within the transportation industry generally; |

| | · | The Company’s success in implementing its strategic plans and operational objectives and improving Surface Transportation operating efficiency; and |

| | · | Changes in operating conditions and costs or commodity concentrations. |

Other important assumptions and factors that could cause actual results to differ materially from those in the forward-looking statements are specified elsewhere in this report and in CSX’s other SEC reports, accessible on the SEC’s website at www.sec.gov and the Company’s website at www.csx.com.

2007 vs. 2006 Consolidated Results of Operations

| | CONSOLIDATED(a) | |

| | Includes Surface Transportation and Other Operating Income | |

| | |

| (Dollars in Millions) | 2007 | | 2006 | | $ Change | | % Change | |

| Operating Revenue | $ 10,030 | | $ 9,566 | | $ 464 | | 5 | % |

| Operating Expense | 7,774 | | 7,428 | | 346 | | 5 | |

| | Operating Income | 2,256 | | 2,138 | | 118 | | 6 | |

| | |

| Other Income | 93 | | 95 | | (2) | | (2) | |

| Interest Expense | (417) | | (392) | | (25) | | 6 | |

| Income Tax Expense | (706) | | (531) | | (175) | | 33 | |

| | Earnings from Continuing Operations | 1,226 | | 1,310 | | (84) | | (6) | |

| | |

| Discontinued Operations | 110 | | - | | 110 | | NM | |

| | Net Earnings | $ 1,336 | | $ 1,310 | | $ 26 | | 2 | % |

| | |

| Earnings Per Diluted Share | |

| From Continuing Operations | $ 2 .74 | | $ 2.82 | | $ (0.08) | | (3) | % |

| Discontinued Operations | 0.25 | | - | | 0.25 | | NM | |

| Net Earnings | $ 2.99 | | $ 2.82 | | $ 0.17 | | 6 | % |

Prior periods have been reclassified to conform to the current presentation.

NM - - not meaningful

(a) Other operating income was $5 million and $12 million for 2007 and 2006, respectively.

Operating Revenue

Operating revenue increased $464 million to over $10 billion in 2007 due to continued pricing efforts and service improvements. These gains were partially offset by lower volume due to weakness in housing construction, domestic automobile production and related markets.

Operating Income

Operating income increased $118 million to $2.3 billion in 2007. Improvements in revenue and productivity from improved operations were partially offset by lower gains on insurance recoveries and increased fuel costs.

Other Income

Other income of $93 million in 2007 was relatively flat compared to the prior year.

Interest Expense

Interest expense increased $25 million to $417 million in 2007 primarily due to higher average debt balances.

Income Tax Expense

Income tax expense increased $175 million to $706 million. This change is primarily due to higher earnings in 2007 and a prior year income tax benefit of $151 million related to the resolution of certain tax matters that were not repeated.

Net Earnings

Consolidated net earnings increased $26 million and totaled $1.3 billion, and earnings per diluted share increased $0.17 to $2.99. The principal elements of these increases are:

| | · | Operating income increased $118 million driven by strong Surface Transportation results. These strong results were more than offset by $151 million of prior year income tax benefits that were not repeated. The net of these and other items decreased earnings from continuing operations by $84 million or $.08 per diluted share. |

| | · | The $110 million or $.25 per diluted share gain in discontinued operations on the Company’s consolidated income statement in 2007 related to the resolution of certain tax matters associated with previously discontinued operations. |

2006 vs. 2005 Consolidated Results of Operations

| | CONSOLIDATED(a) |

| | Includes Surface Transportation and Other Operating Income | |

| | |

| (Dollars in Millions) | 2006 | | 2005 | | $ Change | | % Change | |

| Operating Revenue | $ 9,566 | | $ 8,618 | | $ 948 | | 11 | % |

| Operating Expense | 7,428 | | 7,068 | | 360 | | 5 | |

| | Operating Income | 2,138 | | 1,550 | | 588 | | 38 | |

| | |

| Other Income | 95 | | 101 | | (6) | | (6) | |

| Debt Repurchase | - | | (192) | | 192 | | (100) | |

| Interest Expense | (392) | | (423) | | 31 | | (7) | |

| Income Tax Expense | (531) | | (316) | | (215) | | 68 | |

| | Earnings from Continuing Operations | 1,310 | | 720 | | 590 | | 82 | |

| | |

| Discontinued Operations - Net of Tax | - | | 425 | | (425) | | (100) | |

| | Net Earnings | $ 1,310 | | $ 1,145 | | $ 165 | | 14 | % |

| | |

| Earnings Per Diluted Share | |

| From Continuing Operations | $ 2.82 | | $ 1.59 | | $ 1.23 | | 77 | % |