UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the transition period from . . . . . . . . . . . . to . . . . . . . . . . . . . . |

| | Commission File No. 001-10852 |

| | International Shipholding Corporation |

| | (Exact name of registrant as specified in its charter) |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

11 North Water St. Suite 18290 Mobile, AL | | 36602 |

(Address of principal executive offices) | | (Zip Code) |

| | Registrant's telephone number, including area code: (251) 243-9100 |

| | Securities registered pursuant to Section 12(b) of the Act: |

Title of each class | Name of each exchange on which registered |

Common Stock, $1 Par Value | | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☐ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ☐ Accelerated filer þ Non-accelerated filer ☐ Smaller reporting company ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

State the aggregate market value of the voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

Date Amount

June 30, 2010 $119,610,127

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date.

Common stock, $1 par value. . . . . . . . 7,244,986 shares outstanding as of March 3, 2011

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy statement to be furnished in connection with registrant’s 2011annual meeting of stockholders are incorporated by reference into Part III of this Form 10-K.

INTERNATIONAL SHIPHOLDING CORPORATION

TABLE OF CONTENTS

In this report, the terms “we,” “us,” “our” and the “Company” refer to International Shipholding Corporation and its subsidiaries. In addition, the term “COA” means a Contract of Affreightment, the term “MPS” means the maritime prepositioning ship program of the U.S. Navy, the term “MSC” means the U.S. Military Sealift Command, the term “Newbuildings” means a vessel that is under construction, the term “Notes” means the Notes to our Consolidated Financial Statements contained elsewhere in this report, the term “PCTC” means a Pure Car/Truck Carrier vessel, the term “RO/RO” means a Roll-On/Roll-Off vessel, and the term “SEC” means the U.S. Securities and Exchange Commission.

General

Through our subsidiaries, we operate a diversified fleet of U.S. and International Flag vessels that provide international and domestic maritime transportation services to commercial and governmental customers primarily under medium to long-term time charters or contracts of affreightment. As of March 3, 2011 we owned or operated 33 ocean-going vessels and had seven Newbuildings on order for future delivery.

Our current operating fleet of 33 ocean-going vessels consists of:

| · | Six U.S. flag Pure Car/Truck Carriers specifically designed to transport fully assembled automobiles, trucks and larger vehicles, |

| · | Three International flag Pure Car/Truck Carriers with the capability of transporting heavyweight and large dimension trucks and buses, as well as automobiles, |

| · | Two multi-purpose vessels, two container vessels and one tanker vessel, which are used to transport supplies for the Indonesian operations of a mining company, |

| · | One U.S. flag Molten Sulphur Carrier, which is used to carry molten sulphur from Texas to a processing plant on the Florida Gulf Coast, |

| · | Two special purpose vessels modified as Roll-On/Roll-Off vessels to transport loaded rail cars between the U.S. Gulf and Mexico, |

| · | One U.S. flag conveyor belt-equipped self-unloading Coal Carrier, which carries coal in the coastwise trade, |

| · | Three Roll-On/Roll-Off vessels that permit rapid deployment of rolling stock, munitions, and other military cargoes requiring special handling, |

| · | Two U.S. flag container vessels which began operating on time charters in 2008, |

| · | Three Double Hull Handy-Size Bulk Carriers, which are trading worldwide under a revenue sharing agreement with European partners, |

| · | Two Capesize Bulk Carriers trading worldwide on time charters in which we own a 50% interest of each, and |

| · | Five Mini-Bulkers trading worldwide under a commercial management agreement in which we own a 25% interest of each. |

As described further in Item 2 below, we own 14 of these 33 vessels.

We also have the following interests in the following seven newbuildings:

| · | Two Handymax Bulk Carriers newbuildings in which we own a 50% interest of each, and |

| · | Five Mini-Bulker newbuildings in which we own a 25% interest of each. |

Our fleet is operated by our principal subsidiaries, Central Gulf Lines, Inc. (“Central Gulf”), LCI Shipholdings, Inc. (“LCI”), Waterman Steamship Corporation (“Waterman”), CG Railway, Inc. (“CG Railway”), Enterprise Ship Company, Inc. (“ESC”), and East Gulf Shipholding, Inc. (“EGS”). Other of our subsidiaries provide ship charter brokerage, agency and other specialized services.

Additional information on our vessels appears on the Fleet Statistics Schedule located in the front of our combined Annual Report and 10-K report furnished to our stockholders.

Operating Segments

We have five operating segments, Time Charter Contracts – U.S. Flag, Time Charter Contracts – International Flag, Contracts of Affreightment (“COA”), Rail-Ferry Service, and Other, as described below. Most of our revenues and gross voyage profits are contributed by our time charter contracts segment. Beginning with the second quarter Form 10-Q report, we split Time Charter Contracts into two different operating segments, Time Charter Contracts – U.S. Flag and Time Charter Contracts – International Flag. Although our previous segment reporting was appropriate, this change further aligns our segment disclosures with the information reviewed by our chief operating decision maker. In this report, we recast all prior period data for the previous Time Charter Contracts Segment based on the new operating segments.

For additional information about our operating segments and markets see Note K - Significant Operations. In addition to our five operating segments, we have investments in several unconsolidated entities of which we own 50% or less and have the ability to exercise significant influence over operating and financial activities. A sixth operating segment, Liner Services, was discontinued in 2007. During the first quarter of 2008, we sold the one remaining LASH vessel and the remaining LASH barges for scrapping and these results are reflected as discontinued operations. (See Note P – Discontinued Operations).

Time Charter Contracts-U.S. Flag: Time charters are contracts by which our charterer obtains the right for a specified period to direct the movements and utilization of the vessel in exchange for payment of a specified daily rate, but we retain operating control over the vessel. Typically, we fully equip the vessel and are responsible for normal operating expenses, repairs, crew wages, and insurance, while the charterer is responsible for voyage expenses, such as fuel, port and stevedoring expenses. Our Time Charter Contracts-U.S. Flag segment includes contracts for commercial and supplementary cargo for six PCTCs, and an electric utility for a conveyor-equipped, self-unloading Coal Carrier. Also included in this segment are contracts under which the MSC charters three RO/ROs that are under operating contracts described further below, and contracts with another shipping company for two container vessels.

Time Charter Contracts-International Flag: We operate this segment in the same manner as our Time Charter Contracts – U.S. Flag segment, except with International flagged vessels. This segment included contracts for most of 2010 with Far Eastern and South American shipping companies for three PCTCs. Also included in this segment are two multi-purpose vessels, one tanker and two container vessels, which service ISC’s long-term contract to transport supplies for a mining company’s Indonesian operations.

Contract of Affreightment: Contracts of Affreightments are contracts by which we undertake to provide space on our vessel for the carriage of specified goods or a specified quantity of goods on a single voyage or series of voyages over a given period of time between named ports or within certain geographical areas in return for the payment of an agreed amount per unit of cargo carried. Generally, we are responsible for all operating and voyage expenses. Our COA segment includes one contract, serviced by one vessel, which is for the transportation of molten sulphur through December 31, 2013, subject to additional renewal options in favor of the charterer.

Rail-Ferry Service: This service uses our two Roll-on/Roll-off Special Purpose double-deck vessels, which carry loaded rail cars between the U.S. Gulf Coast and Mexico. We began operations out of our new terminal in Mobile, Alabama and the upgraded terminal in Mexico during the third quarter of 2007. The upgrades to the Mexican terminal were made to accommodate the second decks, which were added to our vessels in the second and third quarters of 2007 to double the capacity of the vessels. (See Item 1a., Risk Factors, for a description of material risks relating to this service).

Other: This segment consists of operations that include more specialized services than the above-mentioned four segments and ship charter brokerage and agency services. Also included in the Other category are corporate related items, results of insignificant operations, and income and expense items not allocated to reportable segments.

Unconsolidated Entities. We have a 50% interest in a company that (i) owns two Cape-Size Bulk Carriers and (ii) has two Handymax Bulk Carrier Newbuildings on order for delivery in 2012. We also have a 49% interest in a company that operates the rail terminal in Coatzacoalcos, Mexico that is used by our Rail-Ferry Service, and a 50% interest in a company that owns and operates a transloading and rail and truck service warehouse storage facility in New Orleans, Louisiana. In December 2009, we acquired a 25% interest in Oslo Bulk AS (“Oslo”) for $6,250,000, which owns four newly built Mini-Bulkers and has four Mini-Bulker Newbuildings to be delivered in early 2011. In December 2009, we acquired a 25% interest in Tony Bulkers Pte Ltd (“Tony Bulkers”) for $2,269,000, which owns one newly built Mini-Bulker and has one Mini-Bulker Newbuilding to be delivered in early 2011. This investment is accounted for under the equity method and our share of earnings or losses will be reported in our consolidated statements of income net of taxes.

Business Strategy

The company operates a diversified fleet of U.S. and International Flag vessels that provide international and domestic maritime transportation services to customers primarily under medium to long-term contracts. Our business strategy consists of identifying growth opportunities as market needs change, utilizing our extensive experience to meet those needs, and continuing to maintain a diverse portfolio of medium to long-term contracts, under which we can serve our long-standing customer base by providing quality transportation services. We plan to continue this strategy by expanding our relationships with existing customers, seeking new customers, and selectively pursuing acquisitions.

Because our strategy is to seek medium to long-term contracts and because we have diversified customer and cargo bases, we believe we are generally insulated from the cyclical nature of the shipping industry to a greater degree than those companies who operate in the spot markets.

History

The Company was originally founded as Central Gulf Steamship Corporation in 1947 by the late Niels F. Johnsen and his sons, Niels W. Johnsen, a retired past CEO and Director, and Erik F. Johnsen, a past CEO and current Director of the Company. Central Gulf was privately held until 1971 when it merged with Trans Union Corporation. In 1978, International Shipholding Corporation was formed to act as a holding company for Central Gulf, LCI, and certain other affiliated companies in connection with the 1979 spin-off by Trans Union of our common stock to Trans Union’s stockholders. In 1986, we acquired the assets of Forest Lines, and in 1989 we acquired Waterman. Since our spin-off from Trans Union, we have continued to act solely as a holding company, and our only significant assets are the capital stock of our subsidiaries.

Competitive Strengths

Diversification. Our strategy for many years has been to seek and obtain contracts that provide predictable cash flows and contribute to a diversification of operations. These diverse operations vary from chartering vessels to the United States government, to chartering vessels for the transportation of automobiles, transportation of paper, steel, wood and wood pulp products, carriage of supplies for a mining company, transporting molten sulphur, transporting coal for use in generating electricity, and transporting standard size railroad cars.

Predictable Operating Cash Flows. Our operations have historically generated cash flows sufficient to cover our debt service requirements and operating expenses, including the recurring drydocking requirements of our fleet. For the years ending December 31, 2010 and December 31, 2009, approximately 62% and 47%, respectively, of our revenues were generated from fixed contracts. The length and structure of our contracts, the creditworthiness of our customers, and our diversified customer and cargo bases all contribute to our ability to consistently meet such requirements in an industry that tends to be cyclical in nature. Our medium to long-term time charters provide for a daily charter rate that is payable whether or not the charterer utilizes the vessel. These time charters generally require the charterer to pay certain voyage operating costs, including fuel, port, and stevedoring expenses, and in some cases include cost escalation features covering certain of our expenses. In addition, our COA operation guarantees a minimum amount of cargo for transportation. Our cash flow from operations was approximately $64.4 million, $62.7 million and $42.2 million for the years ended December 31, 2010, 2009 and 2008, respectively, after deducting cash used for drydocking payments of $2.5 million, $16.0 million and $4.2 million for each of those years, respectively. Regularly scheduled repayment of debt was $14.5 million, $14.2 million and $13.0 million for the years ended December 31, 2010, 2009 and 2008, respectively.

Longstanding Customer Relationships. We currently have medium to long-term time charters or contracts of affreightment with a variety of creditworthy customers. Most of these companies have been customers of ours for over ten years. Substantially all of our current cargo contracts and time charter agreements are renewals or extensions of previous agreements. In recent years, we have been successful in winning extensions or renewals of a substantial majority of all of the contracts. We believe that our longstanding customer relationships are in part due to our excellent reputation for providing quality specialized maritime service in terms of on-time performance, minimal cargo damage claims and reasonable timecharter and freight rates.

Experienced Management Team. Our management team has substantial experience in the shipping industry. Our CEO, President, and Chief Financial Officer have over 105 years of collective experience with the Company. We believe that the experience of our management team is important to maintaining long-term relationships with our customers.

Types of Service

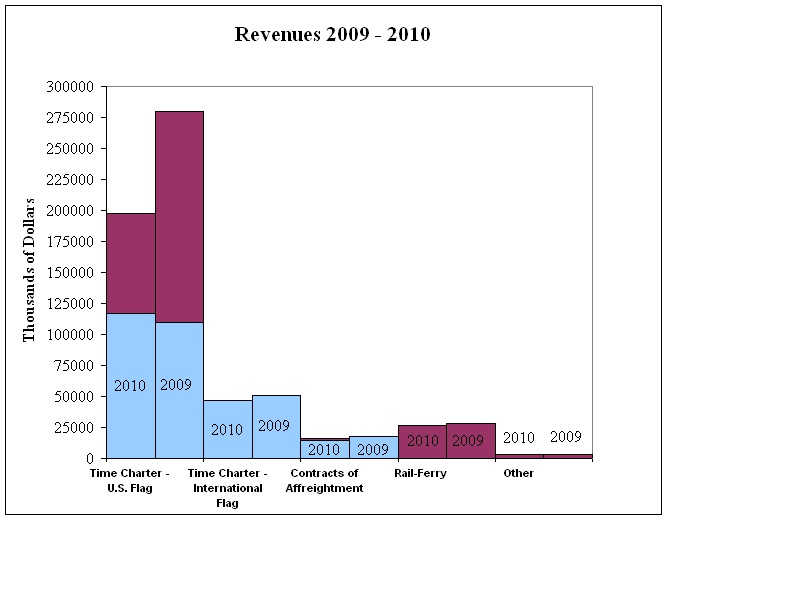

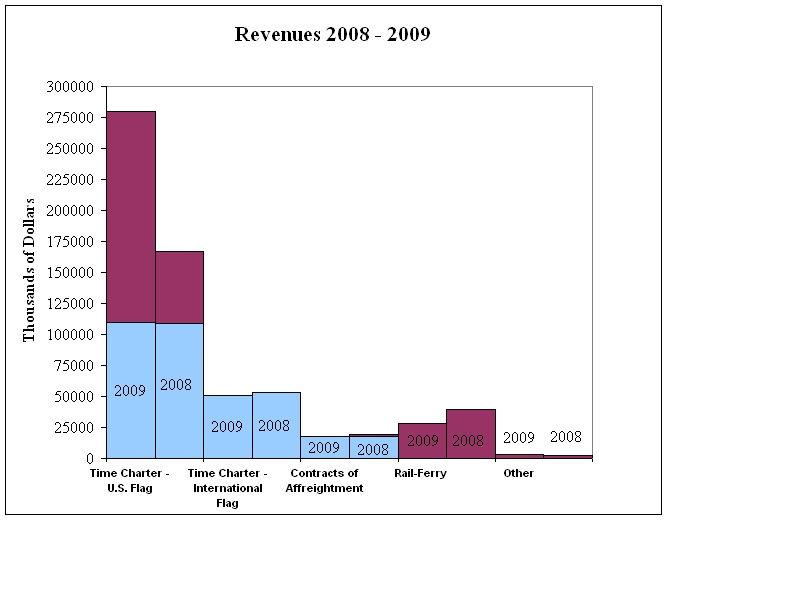

Through our principal operating subsidiaries, we provide specialized maritime transportation services to our customers primarily under medium to long-term contracts. Our five operating segments, Time Charter Contracts – U.S. Flag, Time Charter Contracts – International Flag, Contracts of Affreightment, Rail-Ferry Service, and Other are described below. For further information on the amount of revenues and gross voyage profits contributed by each segment, please see Item 7 of this report.

I. Time Charter Contracts

Military Sealift Command Charters

We have had contracts with the MSC (or its predecessor) almost continuously for over 30 years. In 1983, Waterman was awarded a contract to operate three U.S. Flag RO/RO vessels under time charters to the MSC for use by the United States Navy in its maritime prepositioning ship (“MPS”) program. These vessels currently represent three of the 16 MPS vessels which are part of the MSC’s worldwide fleet and provide support to the U.S. Marine Corps. These ships are designed primarily to carry rolling stock and containers. One of the current agreements is set to expire by the end of March 2011. On February 24, 2011, the MSC notified us of their intent to exercise the option to extend the agreement for up to an additional four months. The remaining two agreements are set to expire in May 2011, with the MSC holding options to further extend these agreements. In July 2010, MSC notified us that we would be excluded from further consideration for extending the current operating agreements on the three U.S. Flag roll on-roll off vessels. Shortly thereafter, we protested this action and were reinstated for consideration by MSC. These three contracts represented 11.9% of our total revenue in 2010. Even if we successfully retain any one or more of these MSC contracts, we anticipate materially reduced revenues.

Pure Car/Truck Carriers

U.S. Flag. Our fleet currently includes six U.S. Flag PCTCs, of which five are owned by us and one is leased. In 1986, we entered into multi-year time charters to carry Toyota and Honda automobiles from Japan to the United States. To service these charters, we had constructed two car carriers that were specially designed to carry 4,000 and 4,660 fully assembled automobiles, respectively. Both vessels were built in Japan and were registered under the U.S. Flag. In 2000 and 2001, we replaced these two vessels with larger PCTCs, which are operating under time charters with a Japanese shipping company. On January 3, 2011 we exercised our option to purchase the one leased vessel effective July 17, 2011.

In 1998, we acquired a 1994-built PCTC, which we reflagged as a U.S. Flag vessel. After being delivered to us in April of 1998, this vessel entered a long-term charter, with the aforementioned Japanese shipping company. In 1999, we acquired a newly built PCTC, which we reflagged as a U.S. Flag vessel, which immediately after being delivered to us in September 1999 entered into a long-term charter with the same Japanese shipping company. This contract may be extended beyond the initial term at the option of the Japanese shipping company.

In 2005, we acquired a 1998-built PCTC, which we reflagged as a U.S. Flag vessel. Immediately after being delivered to us in September of 2005, we chartered this vessel to the same Japanese shipping company.

In 2007, we acquired a 2007-built PCTC, which we reflagged to U.S. Flag. Immediately after being delivered to us in September of 2007, we chartered this vessel through August of 2010 to a Far East based shipping company, which held an option to purchase the vessel at the end of the contract. On February 5, 2010, the charterer notified us of its intention to not exercise their option to purchase the vessel. Subsequently, the charterer did not exercise its purchase option, and we also negotiated a mutually acceptable early redelivery of the vessel effective February 14, 2010. The vessel is currently employed on a long-term time charter with a Japanese shipping company.

International Flag. Our current fleet includes three International Flag PCTCs. Of the three, two are owned by us and one is leased. In 1988, we had two new car carriers constructed by a shipyard affiliated with Hyundai Motor Company, each with a carrying capacity of 4,800 fully assembled automobiles, to transport Hyundai automobiles from South Korea primarily to the United States under two long-term time charters. In 1998 and 1999, we sold these car carriers and replaced them with two newly built PCTCs, each with the capacity to carry heavy and large size rolling stock in addition to automobiles and trucks. We immediately entered into long-term time charters of these vessels to a Korean shipping company. One of these PCTCs was subsequently sold to an unaffiliated party and leased back under an operating lease. On January 13, 2011 we exercised our option to purchase this vessel effective July 3, 2011.

In April 2010, we acquired a newly built 6400 Car Equivalent Units PCTC. The vessel is employed on a medium term time charter.

Under each of our international Flag PCTC contracts, the charterers are responsible for voyage operating costs such as fuel, port, and stevedoring expenses, while we are responsible for other operating expenses including crew wages, repairs, and insurance. During the terms of these charters, we are entitled to our full time charter hire irrespective of the number of voyages completed or the number of cars carried per voyage.

Coal Carrier

In 1995, we purchased an existing U.S. Flag conveyor belt-equipped, self-unloading Coal Carrier that was time-chartered to a New England electric utility to carry coal in the coastwise trade. Effective December 2010, the time charter was extended for a further period.

Southeast Asia Transportation Contract

Our contract to transport supplies for a mining company in Indonesia which commenced in 1995, is serviced by two multi-purpose vessels, a small tanker, and two container vessels. The contract was renewed in 2009. We own the tanker and manage the other four vessels.

Container Vessels

We currently operate two U.S. Flag vessels that are bareboat chartered in and time chartered out.

Bulk Carriers

We currently operate three newly built International Flag double hull Handy-Size Bulk Carriers, delivered to us in January 2011.

II. Contracts of Affreightment

In 1994, we entered into a 15-year transportation contract with an affiliate of Freeport-McMoRan Sulphur LLC for which we had built a 28,000 dead-weight ton Molten Sulphur Carrier that carries molten sulphur from Louisiana and Texas to a fertilizer plant on the Florida Gulf Coast. Under a December 2008 contract amendment, the initial term of the contract was extended. Under the terms of this contract, we are guaranteed the transportation of a minimum of 1.8 million tons of molten sulphur per year. The amended contract also gives the charterer renewal options.

III. Rail-Ferry Service

This service uses two of our special purpose vessels, which carry loaded rail cars between the U.S. Gulf and Mexico. The service provides departures every four days from Mexico and the U.S. Gulf Coast, respectively, for a three-day transit between ports. We began operations out of our new terminal in Mobile, Alabama and the upgraded terminal in Mexico during the third quarter of 2007. The upgrades to the Mexican terminal were made to accommodate the second decks added to our vessels in 2007 to double their carrying capacity. (See Item 1a., Risk Factors, for a description of material risks relating to this service).

IV. Other

Several of our subsidiaries provide ship charter brokerage, agency, and other specialized services to our operating subsidiaries and, in the case of ship charter brokerage and agency services, to unaffiliated companies. The income produced by these services substantially covers the related overhead expenses. These services facilitate our operations by allowing us to avoid reliance on third parties to provide these essential shipping services.

Marketing

We maintain marketing staffs in New York, Mobile, Singapore, and Shanghai and a network of marketing agents in major cities around the world who market our time charter and contracts of affreightment services. We market our Rail-Ferry Service under the name “CG Railway.” We market our remaining transportation services under the names Central Gulf Lines, Waterman Steamship Corporation and East Gulf Shipholding. We advertise our services in trade publications in the United States and abroad.

Insurance

We maintain protection and indemnity (“P&I”) insurance to cover liabilities arising out of our ownership and operation of vessels with the Standard Steamship Owners’ Protection & Indemnity Association (Bermuda) Ltd., which is a mutual shipowners’ insurance organization commonly referred to as a P&I club. The club is a participant in and subject to the rules of its respective international group of P&I associations. The premium terms and conditions of the P&I coverage provided to us are governed by the rules of the club.

We maintain hull and machinery insurance policies on each of our vessels in amounts related to the value of each vessel. This insurance coverage, which includes increased value and time charter hire, is maintained with a syndicate of hull underwriters from the U.S., British, Dutch, Japanese and French insurance markets. We maintain war risk insurance on each of our vessels in an amount equal to each vessel’s total insured hull value. War risk insurance is placed through U.S., British, Norwegian and French insurance markets and covers physical damage to the vessels and P&I risks for which coverage would be excluded by reason of war exclusions under either the hull policies or the rules of the P&I club. Our war risk insurance also covers liability to third parties caused by war or terrorism, but does not cover damages to our land-based assets caused by war or terrorism. (See Item 1a., Rick Factors, for a description of material risks relating to terrorism).

The P&I insurance also covers our vessels against liabilities arising from the discharge of oil or hazardous substances in U.S., international, and foreign waters, subject to various exclusions.

We also maintain loss of hire insurance with U.S., British, Dutch and French insurance markets to cover our loss of revenue in the event that a vessel is unable to operate for a certain period of time due to loss or damage arising from the perils covered by the hull and machinery policy and war risk policy.

Insurance coverage for shoreside property, shipboard consumables and inventory, spare parts, workers’ compensation, office contents, and general liability risks is maintained with underwriters in U.S. and British markets.

Insurance premiums for the coverage described above vary from year to year depending upon our loss record and market conditions. In order to reduce premiums, we maintain certain deductible and co-insurance provisions that we believe are prudent and generally consistent with those maintained by other shipping companies. Certain exclusions under our insurance policies could limit our ability to receive payment for our losses. (See Note D – Self-Retention Insurance).

Tax Matters

Under United States tax laws in effect prior to 2005, U.S. companies such as ours and their domestic subsidiaries generally were taxed on all income, which in our case includes income from shipping activities, whether operated in the United States or abroad. With respect to any foreign subsidiary in which we hold more than a 50 percent interest (referred to in the tax laws as a controlled foreign corporation, or “CFC”), we were treated as having received a current taxable distribution of our pro rata share of income derived from foreign shipping operations when earned.

The American Jobs Creation Act of 2004 (“Jobs Creation Act”), which became effective for us on January 1, 2005, changed the United States tax treatment of the foreign operations of our U.S. Flag vessels and the operations of our International Flag vessels. As a result of the Jobs Creation Act, the taxable income from the shipping operations of CFCs is not subject to United States income tax until that income is repatriated. We have a plan to re-invest indefinitely some of our foreign earnings, and accordingly have not provided deferred taxes against those earnings. As permitted under the Jobs Creation Act, we have elected to have our U.S. Flag operations (other than those of two ineligible vessels used exclusively in United States coastwise commerce) taxed under a “tonnage tax” regime rather than under the usual U.S. corporate income tax regime. Because we made the tonnage tax election in December 2004 referred to above, our gross income for United States income tax purposes with respect to our eligible U.S. Flag vessels for 2005 and subsequent years does not include (1) income from qualifying shipping activities in U.S. foreign trade (such as transportation between the U.S. and foreign ports or between foreign ports), (2) income from cash, bank deposits and other temporary investments that are reasonably necessary to meet the working capital requirements of our qualifying shipping activities, and (3) income from cash or other intangible assets accumulated pursuant to a plan to purchase qualifying shipping assets. Our taxable income with respect to the operations of our eligible U.S. Flag vessels is based on a “daily notional taxable income,” which is taxed at the highest corporate income tax rate. The daily notional taxable income from the operation of a qualifying vessel is 40 cents per 100 tons of the net tonnage of the vessel up to 25,000 net tons, and 20 cents per 100 tons of the net tonnage of the vessel in excess of 25,000 net tons. The taxable income of each qualifying vessel is the product of its daily notional taxable income and the number of days during the taxable year that the vessel operates in United States foreign trade. All other domestic operations are taxed at the U.S. corporation statutory rate.

As of December 31, 2010, our net deferred tax asset/liability was reduced to zero as a result of the establishment of a full valuation allowance with respect to our net deferred tax asset during the fourth quarter of 2010. The valuation allowance was established as a result of recent losses incurred with respect to our operations taxed at the U.S. Corporate Statutory rate. The establishment of the valuation allowance resulted in a higher effective tax rate during 2010.

Regulation

Our operations between the United States and foreign countries are subject to the Shipping Act of 1984 (the “Shipping Act”), which is administered by the Federal Maritime Commission, and certain provisions of the Federal Water Pollution Control Act, the Oil Pollution Act of 1990, the Act to Prevent Pollution from Ships, and the Comprehensive Environmental Response Compensation and Liability Act, all of which are administered by the U.S. Coast Guard and other federal agencies, and certain other international, federal, state, and local laws and regulations, including international conventions and laws and regulations of the Flag nations of our vessels. On October 16, 1998, the Ocean Shipping Reform Act of 1998 was enacted, which amended the Shipping Act to promote the growth and development of United States exports through certain reforms in the regulation of ocean transportation. This legislation, in part, repealed the requirement that a common carrier or conference file tariffs with the Federal Maritime Commission, replacing it with a requirement that tariffs be open to public inspection in an electronically available, automated tariff system. Furthermore, the legislation required that only the essential terms of service contracts be published and made available to the public.

On October 8, 1996, Congress adopted the Maritime Security Act of 1996, which created the Maritime Security Program (MSP) and authorized the payment of $2.1 million per year per ship for 47 U.S. Flag ships through the fiscal year ending September 30, 2005. This program eliminated the trade route restrictions imposed by the previous federal program and provides flexibility to operate freely in the competitive market. On December 20, 1996, Waterman entered into four MSP operating agreements with the United States Maritime Administration (“MarAd”), and Central Gulf entered into three MSP operating agreements with MarAd. We also participate in the Voluntary Intermodal Sealift Agreement (“VISA”) program administered by MarAd. Under this VISA program, and as a condition of participating in the MSP, we have committed to providing vessel capacity for the movement of military cargoes in times of war or national emergency. By law, the MSP is subject to annual appropriations from Congress. In the event that sufficient appropriations are not made for the MSP by Congress in any fiscal year, the Maritime Security Act of 1996 permits MSP participants, such as Waterman and Central Gulf, to re-flag their vessels under foreign registry expeditiously. In 2003, Congress authorized an extension of the MSP through 2015, increased the number of ships eligible to participate in the program from 47 to 60, and increased MSP payments to companies in the program, all made effective on October 1, 2005. Authorized annual payments per fiscal year for each vessel for the current MSP program were $2.6 million for years 2007 and 2008, and $2.9 million for years 2009 to 2011, and $3.1 million for years 2012 to 2015, subject to annual appropriation by the Congress, which is not assured. On October 15, 2004, Waterman and Central Gulf each filed applications to extend their MSP operating agreements for another ten years through September 30, 2015, all seven of which were effectively grandfathered in the MSP reauthorization. Simultaneously, we offered additional ships for participation in the MSP. On January 12, 2005, MarAd awarded Central Gulf four MSP operating agreements and Waterman four MSP operating agreements, effective October 1, 2005, for a net increase of one MSP operating agreement. In January of 2011, the President signed into law legislation that extends the MSP under its current terms and conditions through September 30, 2025. The terms of the MSP contracts of Waterman and Central Gulf currently run though September 30, 2015. It is anticipated that, as a result of the recent law extending the MSP for an additional ten years, MarAd will initiate a process to allow MSP contractors to submit applications to extend their current MSP contracts, but this process has not yet commenced.

Under the Merchant Marine Act, U.S. Flag vessels are subject to requisition or charter to the United States Navy’s Military Sealift Command (“MSC”) by the United States whenever the President declares that national security requires such action. The owners of any such vessels must receive just compensation as provided in the Merchant Marine Act, but there is no assurance that lost profits, if any, will be fully recovered. In addition, during any extension period under each MSC charter or contract, the MSC has the right to terminate the charter or contract on 30 days’ notice.

Certain laws governing our operations, as well as our U.S. Coastwise transportation contracts, require us to be 75% owned by U.S. citizens. We monitor our stock ownership to verify our continuing compliance with these requirements. Our certificate of incorporation allows our board of directors to restrict the acquisition of our capital stock by non-U.S. citizens. Under our certificate of incorporation, our board of directors may, in the event of a transfer of our capital stock that would result in non-U.S. citizens owning more than 23% (the “permitted amount”) of our total voting power, declare such transfer to be void and ineffective. In addition, our board of directors may, in its sole discretion, deny voting rights and withhold dividends with respect to any shares of our capital stock owned by non-U.S. citizens in excess of the permitted amount. Furthermore, our board of directors is entitled under our certificate of incorporation to redeem shares owned by non-U.S. citizens in excess of the permitted amount in order to reduce the ownership of our capital stock by non-U.S. citizens to the permitted amount.

We are required by various governmental and quasi-governmental agencies to obtain permits, licenses, and certificates with respect to our vessels. The kinds of permits, licenses, and certificates required depend upon such factors as the country of registry, the commodity transported, the waters in which the vessel operates, the nationality of the vessel’s crew, the age of the vessel, and our status as a vessel owner or charterer. We believe that we have, or can readily obtain, all permits, licenses, and certificates necessary to permit our vessels to operate.

The International Maritime Organization (“IMO”) amended the International Convention for the Safety of Life at Sea (“SOLAS”), to which the United States is a party, to require nations that are parties to SOLAS to implement the International Safety Management (“ISM”) Code. The ISM Code requires that responsible companies, including owners or operators of vessels engaged on foreign voyages, develop and implement a safety management system to address safety and environmental protection in the management and operation of vessels. Companies and vessels to which the ISM Code applies are required to receive certification and documentation of compliance. Vessels operating without such certification and documentation in the U.S. and ports of other nations that are parties to SOLAS may be denied entry into ports, detained in ports or fined. We implemented a comprehensive safety management system and obtained timely IMO certification and documentation for our companies and all of our vessels. In addition, our ship management subsidiary, LMS Shipmanagement, Inc., is certified under the ISO 9001-2008 Quality Standard.

In 2003, SOLAS was again amended to require parties to the convention to implement the International Ship and Port Facility Security (“ISPS”) Code. The ISPS Code requires owners and operators of vessels engaged on foreign voyages to conduct vulnerability assessments and to develop and implement company and vessel security plans, as well as other measures, to protect vessels, ports and waterways from terrorist and criminal acts. In the U.S., these provisions were implemented through the Maritime Transportation Security Act of 2002 (“MTSA”). These provisions became effective on July 1, 2004. As with the ISM Code, companies and vessels to which the ISPS Code applies must be certificated and documented. Vessels operating without such certification and documentation in the U.S. and ports of other nations that are parties to SOLAS may be denied entry into ports, detained in ports or fined. Vessels subject to fines in the U.S. are liable in rem, which means vessels may be subject to arrest by the U.S. government. For U.S. Flag vessels, company and vessel security plans must be reviewed and approved by the U.S. Coast Guard. We have conducted the required security assessments and submitted plans for review and approval as required, and we believe that we are in compliance in all material respects with all ISPS Code and MTSA security requirements.

The Coast Guard and Maritime Transportation Act of 2004 amended the Oil Pollution Act of 1990 (“OPA”) to require owners or operators of all non-tanker vessels of 400 gross tons or greater to develop and submit plans for responding, to the maximum extent practicable, to worst case discharges and substantial threats of discharges of oil from these vessels. This statute extends to all types of vessels of 400 gross tons or greater. The vessel response planning requirements of the OPA had previously only applied to tanker vessels. We have submitted response plans timely for our vessels, and have received Coast Guard approval for all of our vessels.

Also, under the OPA, vessel owners, operators and bareboat charterers are jointly, severally and strictly liable for all response costs and other damages arising from oil spills from their vessels in waters subject to U.S. jurisdiction, with certain limited exceptions. Other damages include, but are not limited to, natural resource damages, real and personal property damages, and other economic damages such as net loss of taxes, royalties, rents, profits or earning capacity, and loss of subsistence use of natural resources. For non-tanker vessels, the OPA limits the liability of responsible parties to the greater of $1,000 per gross ton or $854,400. The limits of liability do not apply if it is shown that the discharge was proximately caused by the gross negligence or willful misconduct of, or a violation of a federal safety, construction or operating regulation by, the responsible party, an agent of the responsible party or a person acting pursuant to a contractual relationship with the responsible party. Further, the limits do not apply if the responsible party fails or refuses to report the incident, or to cooperate and assist in oil spill removal activities. Additionally, the OPA specifically permits individual states to impose their own liability regimes with regard to oil discharges occurring within state waters, and some states have implemented such regimes.

The Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) also applies to owners and operators of vessels, and contains a similar liability regime for cleanup and removal of hazardous substances and natural resource damages. Liability under CERCLA is limited to the greater of $300 per gross ton or $5 million per vessel.

Under the OPA, vessels are required to establish and maintain with the U.S. Coast Guard evidence of financial responsibility sufficient to meet the highest limit of their potential liability under the act. Under Coast Guard regulations, evidence of financial responsibility may be demonstrated by insurance, surety bond, self-insurance or guaranty. An owner or operator of more than one vessel must demonstrate financial responsibility for the entire fleet in an amount equal to the financial responsibility of the vessel having greatest maximum liability under the OPA and CERCLA. We insure each of our vessels with pollution liability insurance in the amounts required by law. A catastrophic spill could exceed the insurance coverage available, in which event our financial condition and results of operations could be adversely affected.

Many countries have ratified and follow the liability plan adopted by the IMO as set out in the International Convention on Civil Liability for Oil Pollution Damage of 1969 (the “1969 Convention”) and the Convention for the Establishment of an International Fund for Oil Pollution of 1971. Under these conventions, the registered owner of a vessel is strictly liable for pollution damage caused in the territorial seas of a state party by the discharge of persistent oil, subject to certain defenses. Liability is limited to approximately $183 per gross registered ton (a unit of measurement of the total enclosed spaces in a vessel) or approximately $19.3 million, whichever is less. If a country is a party to the 1992 Protocol to the International Convention on Civil Liability for Oil Pollution Damage (the “1992 Protocol”), the maximum liability limit is $82.7 million. The limit of liability is tied to a unit of account that varies according to a basket of currencies. The right to limit liability is forfeited under the 1969 Convention when the discharge is caused by the owner's actual fault, and under the 1992 Protocol, when the spill is caused by the owner's intentional or reckless misconduct. Vessels operating in waters of states that are parties to these conventions must provide evidence of insurance covering the liability of the owner. In jurisdictions that are not parties to these conventions, various legislative schemes or common law govern. We believe that our pollution insurance policy covers the liability under the IMO regimes.

Competition

The shipping industry is intensely competitive and is influenced by events largely outside the control of shipping companies. Varying economic factors can cause wide swings in freight rates and sudden shifts in traffic patterns. Vessel redeployments and new vessel construction can lead to an overcapacity of vessels offering the same service or operating in the same market. Changes in the political or regulatory environment can also create competition that is not necessarily based on normal considerations of profit and loss. Our strategy is to reduce the effects of cyclical market conditions by operating specialized vessels in niche market segments and deploying a substantial number of our vessels under medium to long-term time contracts with creditworthy customers and on trade routes where we have established market share. We also seek to compete effectively in the traditional areas of price, reliability, and timeliness of service.

Our Time Charter Contract and Contracts of Affreightment segments primarily include medium and long-term contracts with long standing customers. While our PCTCs in our Time Charter Contract segment operate worldwide in markets where International Flag vessels with foreign crews predominate, we believe that our U.S. Flag PCTCs can compete effectively in obtaining renewals of existing contracts if we are able to continue to participate in the MSP and continue to receive cooperation from our seamen’s unions in controlling costs.

Our Rail-Ferry Service faces competition principally from companies who transport cargo over land rather than water, including railroads and trucking companies that cross land borders.

Employees

As of December 31, 2010, we employed approximately 377 shipboard personnel and 124 shoreside personnel. We consider relations with our employees to be excellent.

All of Central Gulf, Waterman, and our other U.S. shipping companies’ shipboard personnel are covered by collective bargaining agreements. Some of these agreements relate to particular vessels and have terms corresponding with the terms of their respective vessel’s charter. We have experienced no strikes or other significant labor problems during the last ten years.

Available Information

Our internet address is www.intship.com. We make available free of charge through our website our annual report on Form 10-K, proxy statement for our annual meeting of stockholders, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The information found on our website is not part of this or any other report.

Unless otherwise indicated, information contained in this annual report and other documents filed by us under the federal securities laws concerning our views and expectations regarding the marine transportation industry are based on estimates made by us using data from industry sources, and on assumptions made by us based on our management’s knowledge and experience in the markets in which we operate and the marine transportation industry generally. We believe these estimates and assumptions are accurate on the date made. However, this information may prove to be inaccurate because it cannot always be verified with certainty. You should be aware that we have not independently verified data from industry or other third-party sources and cannot guarantee its accuracy or completeness. Our estimates and assumptions involve risks and uncertainties and are subject to change based on various factors, including those discussed immediately below in Item 1A of this annual report.

Our revenues decreased in 2010 and could decrease further in 2011.

Beginning in 2008, our revenues and gross voyage profits benefited from significant increases in the volume of supplemental cargos carried by our vessels. These supplemental cargoes peaked during the fourth quarter of 2009, and have decreased every quarter since then to levels comparable to 2008. If our supplemental cargo volumes continue to decrease, our revenues and gross voyage profits will be negatively impacted.

We may not be able to renew our time charters and contracts when they expire at favorable rates or at all.

During 2010, we received approximately 62% of our revenue from time charters (excluding supplemental cargoes), bareboat charters or contracts of affreightment. However, there can be no assurance that any of these charters or contracts, which are generally for periods of one year or more, will be renewed at favorable rates, or at all. Shipping rates are based on several factors that are unpredictable and beyond our control. If upon expiration of our existing charters and contracts, we are unable to obtain new charters or contracts at rates comparable to those received under the expired charters or contracts, our revenues and earnings may be adversely affected.

In particular, we cannot assure that we will be able to renew the three contracts we have with the MSC that are currently scheduled to end in March and May 2011. These three contracts represented 11.9% of our total revenue in 2010.

We operate in a highly competitive industry.

The shipping industry is intensely competitive and can be influenced by economic and political events that are outside the control of shipping companies. We compete with companies that have greater resources than we have, or who may be better positioned to adapt to changes in market or economic conditions. Consequently, there can be no assurance that we will be able to deploy our vessels on economically attractive terms, maintain attractive freight rates, pass cost increases through to our customers or otherwise successfully compete against our competitors. Any failure to remain competitive in the shipping industry could have an adverse effect on our results of operations and financial condition.

Changes in the demand for our services or vessels could cause our charter and cargo rates to decline, which could have a material adverse effect on our revenues and earnings.

Historically, the shipping industry has been cyclical. The nature, timing and degree of changes to industry conditions are generally unpredictable and may adversely affect the values of our assets or our financial performance. Various factors influence the demand for our transportation services, including worldwide demand for the products we carry and changes in the supply and demand of vessels. The worldwide supply of vessels generally increases with deliveries of new, refurbished or converted vessels and decreases with the scrapping of older vessels. If the available supply of vessels exceeds the number of vessels being scrapped, vessel capacity and competition in the markets where we operate may increase. In the absence of a corresponding increase in the demand for these vessels, the charter hire and cargo rates for our vessels could fluctuate significantly and result in, among other things, lower operating revenues and reduced earnings.

If Congress does not make sufficient appropriations under the Maritime Security Act of 1996, we may not continue to receive certain payments.

If Congress does not make sufficient appropriations under the Maritime Security Act of 1996 in any fiscal year, we may not continue to receive annual payments with respect to certain of our vessels that we have committed to the federal government under the U.S. Maritime Security Program. Under this program, each participating vessel received an annual payment of $2.9 million in 2009 and 2010. These vessels are eligible to receive $2.9 million in year 2011, and $3.1 million in years 2012 to 2015. As of December 31, 2010, eight of our vessels operated under contracts issued under this program. Since payments under this program are subject to annual appropriations by Congress and are not guaranteed, we cannot assure you that we will continue to receive these annual payments, in full or in part.

We cannot assure that we will be able to comply with all of our loan covenants.

Substantially all of our credit agreements require us to comply with various loan covenants, including financial covenants that stipulate minimum levels of net worth and maximum amounts of debt leverage. We are currently evaluating several alternatives designed to alleviate potential covenant breaches that we project could otherwise arise in the near future based on current operating trends. While we currently believe that we have available options to prevent or mitigate such breaches, we cannot assure that we will be able to implement them timely or at all, or that they will enable us to meet all of our current covenants

Recent turmoil in the credit markets could negatively impact our business, results of operations, financial condition or liquidity, or those of our customers.

Our operations are affected by local, national and worldwide economic conditions and the condition of the shipping industry in general. Over the last couple of years, worldwide economic conditions have experienced a significant downturn as a result of, among other things, the failure of several financial institutions, slower overall economic activity, fluctuations in commodity prices, and other adverse business conditions and related concerns. Any continuation or worsening of these trends could ultimately have a negative impact on our financial performance and condition, including our ability to borrow money from current credit sources or secure additional financing to fund our ongoing operations.

We are subject to certain risks with respect to our counterparties on contracts, and failure of such counterparties to meet their obligations could cause us to suffer losses or otherwise adversely affect our business.

The ability of our counterparties to perform their obligations under their contracts with us will depend upon a number of factors that are beyond our control and may include, among other things, general economic conditions and the overall financial condition of these counterparties, especially in light of the recent global financial crisis. If our counterparties fail to honor their obligations under their agreements with us, we could sustain significant losses or a reduction in our vessel usage, both of which could have an adverse effect on our financial condition, results of operations and cash flows.

Older vessels have higher operating costs and are potentially less desirable to charterers.

The average age of the vessels in our fleet that we own or lease is approximately 12 years, including the average age of our owned and leased Pure Car/Truck Carrier Fleet, which is approximately 10 years. In general, capital expenditures and other costs necessary for maintaining a vessel in good operating condition increase and become more difficult to estimate with accuracy as the age of the vessel increases. Moreover, customers generally prefer modern vessels over older vessels, which places the older vessels at a competitive disadvantage, especially in weak markets. In addition, changes in governmental regulations, compliance with classification society standards and customer requirements or competition may require us to make additional expenditures for alternations or the addition of new equipment. In order to make such alterations or add such equipment, we may be required to take our vessels out of service, thereby reducing our revenues. Expenditures such as these may also require us to incur additional debt or raise additional capital. There can be no assurance that market or general economic conditions will enable us to replace our existing vessels with new vessels, justify the expenditures necessary to maintain our older vessels in good operating condition or enable us to operate our older vessels profitably during the remainder of their estimated useful lives.

Our Rail-Ferry Service has a history of losses, and we can give no assurances as to its future profitability.

This service began operating in February of 2001 and has been unprofitable every year except 2008, when the two vessels used to provide this service averaged approximately 75% capacity utilization. Beginning in 2009, the worldwide economic downturn negatively impacted the volumes and cargo rates for this service, especially on its northbound route to the U.S. As a result of a reduction in future anticipated cash flows generated by this service, we recognized a non-cash impairment charge of $25.4 million in the third quarter of 2010 to reduce the carrying value of these assets to their estimated fair value. We cannot assure you that this service will be operated profitably in the future, however even at unprofitable levels, the service remains cash positive.

We are subject to the risk of continuing high prices, and increasing prices, of the fuel we consume in our Rail-Ferry operations.

We are exposed to commodity price risks with respect to fuel consumption in our Rail-Ferry operations, and we can give no assurance that we will be able to offset higher fuel costs due to the competitive nature of these operations. Although we currently have fuel surcharges in place, a material increase in current fuel prices that we cannot recover through these fuel cost surcharges could adversely affect our results of operations and financial condition.

Our business and operations are highly regulated, which can adversely affect our operations.

Our business and the shipping industry in general are subject to increasingly stringent laws and regulations governing our vessels, including worker’s health and safety, and the staffing, construction, operation, insurance and transfer of our vessels. Compliance with or the enforcement of these laws and regulations could have an adverse effect on our business, results of operations or financial condition. For example, in the event of war or national emergency, our U.S. Flag vessels are subject to requisition by the U.S. government. Although we would be entitled to compensation in the event of a requisition of one or more of our vessels, the amount and timing of such payments would be uncertain and there would be no guarantee that such amounts would be paid, or if paid, would fully satisfy lost profits associated with the requisition.

In addition, we are required by various governmental and quasi-governmental agencies to obtain and maintain certain permits, licenses and certificates with respect to our operations. In certain instances, the failure to obtain or maintain these authorizations could have an adverse effect on our business. We may also be required to periodically modify operating procedures or alter or introduce new equipment for our existing vessels to appropriately respond to changes in governmental regulation.

Our operations are also subject to laws and regulations related to environmental protection. Compliance with these laws and regulations can be costly. Failure to comply with these laws and regulations may result in penalties, sanctions or, in certain cases, the ultimate suspension or termination of our operations. Additionally, some environmental laws impose strict and, under certain circumstances, joint and several liability for remediation of spills and the release of hazardous materials. As a result, we could become subject to liability irrespective of fault or negligence. These laws and regulations may also expose us to liability for the conduct of or conditions caused by our charterers or other parties.

Terrorist attacks, piracy and international hostilities can affect the transportation industry, which could adversely affect our business.

Terrorist attacks or piracy attacks against merchant ships, particularly in the Gulf of Aden and off the East Coast of Africa, the outbreak of war, or the existence of international hostilities could damage the world economy, adversely affect the availability of and demand for transportation services, and adversely affect our ability to profitably operate and deploy our vessels. We operate in a sector of the economy that we believe is particularly likely to be adversely impacted by the effects of political instability, terrorist attacks, war, international hostilities or piracy.

Marine transportation is inherently risky, and insurance may be insufficient to cover losses that may occur to our assets or result from our operations.

The operation of our vessels are subject to inherent risks, such as: (i) catastrophic marine disaster; (ii) adverse weather conditions; (iii) mechanical failure; (iv) collisions; (v) hazardous substance spills; (vi) seizure or expropriation of our vessels by governments, pirates, combatants or others; and (vii) navigation and other human errors. The occurrence of any of these events may result in, among other things, damage to or loss of our vessels and our vessels' cargo or other property, delays in delivery of cargo, damage to other vessels and the environment, loss of revenues, termination of vessel charters or other contracts, fines or other restrictions on conducting business, damage to our reputation and customer relationships, and injury to personnel. Such occurrences may also result in a significant increase in our operating costs or liability to third parties. In addition, such occurrences may result in our company being held strictly liable for pollution damages under the Oil Pollution Act of 1990, the Comprehensive Environmental Response Compensation and Liability Act or one of the international conventions to which our vessels operating in foreign waters may be subject.

Although we maintain insurance coverage against most of these risks at levels our management considers to be customary in the industry, risks may arise for which we are not adequately insured. Additionally, any particular claim may not be covered by our policies, or may be subject to deductibles, the aggregate amount of which could be material. Any uninsured or underinsured loss could have an adverse effect on our financial performance or condition. We also make no assurances that we will be able to renew our existing insurance coverage at commercially reasonable rates or that such coverage will be adequate to cover future claims that may arise.

Additionally, certain of our insurance coverage is maintained through mutual “protection and indemnity” associations. As a mutual club, a substantial portion of its continued viability to effectively manage liability risks is reliant upon the premiums paid by its members. As a member of such associations, we may incur the obligation to satisfy payments in addition to previously established or budgeted premiums to the extent member claims would surpass the reserves of the association. We may be subject to calls or premiums in amounts based not only on our own claim records, but also the claim records of all other members over which we have no control. Our payment of these calls could result in significant additional expenses.

We are subject to risks associated with operating internationally.

Our international shipping operations are subject to risks inherent in doing business in countries other than the United States. These risks include, among others: (i) economic, political and social instability; (ii) potential vessel seizure, terrorist attacks, piracy, kidnapping, the expropriation of assets and other governmental actions, many of which are not covered by our insurance; (iii) currency restrictions and exchange rate fluctuations; (iv) potential submission to the jurisdiction of a foreign court or arbitration panel; (v) pandemics or epidemics that disrupt worldwide trade or the movement of vessels; (vi) import and export quotas; and (vii) the imposition of unanticipated or increased taxes, increased environmental and safety regulations or other forms of public and governmental regulation that increase our operating expenses. Many of these risks are beyond our control, and we cannot predict the nature or the likelihood of the occurrence or corresponding affect of any such events, each of which could have an adverse effect on our financial condition and results of operations.

Our vessels could be seized by maritime claimants, which could result in a significant loss of earnings and cash flow for the related off-hire period.

Crew members, suppliers of goods and services to a vessel, shippers of cargo and other parties may be entitled to a maritime lien against a vessel for unsatisfied debts or claims for damages. In many jurisdictions, a maritime lienholder may enforce its lien by either arresting or attaching a vessel through foreclosure proceedings. The arrest or attachment of one or more of our vessels could result in a significant loss of earnings and cash flow during the detainment period.

In addition, international vessel arrest conventions and certain national jurisdictions allow so-called “sister ship” arrests, that allow the arrest of vessels that are within the same legal ownership as the vessel which is subject to the claim or lien. Certain jurisdictions go further, permitting not only the arrest of vessels within the same legal ownership, but also any “associated” vessel. In nations with these laws, an “association” may be recognized when two vessels are owned by companies controlled by the same party. Consequently, a claim may be asserted against us or any of our subsidiaries or our vessels for the liability of one or more of the other vessels we own. While we have insurance coverage for these types of claims, we cannot guarantee it will cover all of our potential exposure.

A substantial number of our shipboard employees are unionized. In the event of a strike or other work stoppage, our business and operations may be adversely affected.

As of December 31, 2010, approximately 76% of our 377 shipboard personnel were unionized employees covered by collective bargaining agreements. Given the prevalence of maritime trade unions and their corresponding influence over its members, the shipping industry is vulnerable to work stoppages and other potentially disruptive actions by employees. We may also have difficulty successfully negotiating renewals to our collective bargaining agreements with these unions or face resistance to any future efforts to place restrains on wages, reduce labor costs or moderate work practices. Any of these events may result in strikes, work disruptions and have other potentially adverse consequences. While we have experienced no strikes, work stoppages or other significant labor problems during the last ten years, we cannot assure that such events will not occur in the future or be material in nature. In the event we experience one or more strikes, work stoppages or other labor problems, our business and, in turn, our results of operations may be adversely affected.

The market value of vessels fluctuates significantly, which could adversely affect our liquidity, result in breaches of our financing agreements or otherwise adversely affect our financial condition.

The market value of vessels fluctuates over time. The fluctuation in market value of vessels over time is based upon various factors, including:

| · | general economic and market conditions affecting the transportation industry, including the availability of vessel financing, |

| · | number of vessels in the world fleet, |

| · | types and sizes of vessels available, |

| · | changes in trading patterns affecting demand for particular sizes and types of vessels, |

| · | prevailing levels of charter rates, |

| · | competition from other shipping companies and other modes of transportation, and |

| · | technological advances in vessel design and propulsion. |

Declining values of our vessels could adversely affect our liquidity by limiting our ability to raise cash by refinancing vessels. Declining vessel values could also result in a breach of loan covenants or trigger events of default under relevant financing agreements that require us to maintain certain loan-to-value ratios. In such instances, if we are unable or unwilling to pledge additional collateral to offset the decline in vessel values, our lenders could accelerate our debt and foreclose on our vessels pledged as collateral for the loans.

Delays or cost overruns in building new vessels (including the failure to deliver new vessels) could harm us.

Building new vessels is subject to risks of delay (including the failure to timely deliver new vessels to customers) or cost overruns caused by one or more of the following:

| · | financial difficulties of the shipyard building a vessel, including bankruptcy, |

| · | unforeseen quality or engineering problems, |

| · | unanticipated cost increases, |

| · | delays in receipt of necessary materials or equipment, |

| · | changes to design specifications, and |

| · | inability to obtain the requisite permits, approvals or certifications from governmental authorities and the applicable classification society upon completion of work. |

Significant delays, cost overruns and failure to timely deliver new vessels to customers could adversely affect us in several ways, including delaying the implementation of our business strategies or materially increasing our expected contract commitments to customers.

We face periodic drydocking costs for our vessels, which can be substantial.

Vessels must be drydocked periodically for regulatory compliance and for maintenance and repair. Our drydocking requirements are subject to associated risks, including delay and cost overruns, lack of necessary equipment, unforeseen engineering problems, employee strikes or other work stoppages, unanticipated cost increases, inability to obtain necessary certifications and approvals and shortages of materials or skilled labor. A significant delay in drydockings could have an adverse effect on our contract commitments. The cost of repairs and renewals required at each drydock are difficult to predict with certainty and can be substantial. Our insurance does not cover these costs.

Some of our employees are covered by laws limiting our protection from exposure to certain claims.

Some of our employees are covered by several maritime laws, statutes and regulations which circumvent and nullify certain liability limits established by state workers’ compensation laws, including provisions of the Jones Act, the Death on the High Seas Act, and the Seamen’s Wage Act. We are not generally protected by the limits imposed by state workers’ compensation statutes for these particular employees, and as a result our exposure for claims asserted by these employees may be greater than would otherwise be the case.

We are subject to the control of our principal stockholders.

As of March 3, 2011, three of our directors, Erik F. Johnsen, Niels M. Johnsen and Erik L. Johnsen, and their respective family members and affiliated entities, beneficially owned an aggregate of 24.36% of our common stock. Niels M. Johnsen and Erik L. Johnsen are also executive officers of the Company, and their respective fathers are former executive officers. Erik F. Johnsen continued to provide consulting services to us through December 31, 2010. As a result, the Johnsen family may have the ability to exert significant influence over our affairs and management, including the election of directors and other corporate actions requiring stockholder approval.

As a holding company with no operations of our own, we rely on payments from our operating companies to meet our obligations.

As a holding company without any material assets or operations, substantially all of our income and operating cash flow is dependent upon the earnings of our subsidiaries and the distribution of those earnings to us or upon loans or other payments of funds by those subsidiaries to us. As a result, we rely upon our subsidiaries to generate the funds necessary to meet our obligations, including the payment of amounts owed under our long-term debt. The ability of our subsidiaries to generate sufficient cash flow from operations to allow us and them to make scheduled payments on our respective obligations will depend on their future financial performance, which will be affected by a range of economic, competitive and business factors, many of which are outside of our control. Additionally, our subsidiaries are separate and distinct legal entities and have no obligation to pay any amounts owed by us or, subject to limited exceptions for tax-sharing purposes, to make any funds available to us to pay dividends or to repay our debt or other obligations. Our rights to receive assets of any subsidiary upon its liquidation or reorganization will also be effectively subordinated to the claims of creditors of that subsidiary, including trade creditors. The footnotes to our consolidated financial statements incorporated by reference herein describe these matters in additional detail.

The agreements governing certain of our debt instruments impose restrictions on our business.

The agreements governing certain of our debt instruments contain a number of covenants imposing restrictions on our business. The restrictions these covenants place on us include limitations on our ability to: (i) consolidate or merge; (ii) incur new debt; (iii) engage in transactions with affiliates; (iv) create or permit to exist liens on our assets: and (v) in the case of a breach in certain financial covenants, pay cash dividends. These agreements also require us to attain a number of financial ratios that measure our financial position and performance. Our ability to satisfy these and other covenants depends on our results of operations and ability to respond to changes in business and economic conditions. Several of these matters are beyond our control or may be significantly restricted, and, as a result, we may be prevented from engaging in transactions that otherwise might be considered beneficial to us and our common stockholders.

In addition, as our debt obligations are represented by separate agreements with different lenders, in some cases the breach of any of these covenants or other default under one agreement may create an event of default under other agreements, resulting in the acceleration of our obligation to pay principal, interest and potential penalties under such other agreements (even though we may otherwise be in compliance with all of our obligations under those agreements). Thus, an event of default under a single agreement, including one that is technical in nature or otherwise not material, could result in the acceleration of significant indebtedness under multiple lending agreements. If amounts outstanding under such agreements were to be accelerated, there can be no assurance that our assets would be sufficient to generate sufficient cash flow to repay the accelerated indebtedness, or that our lenders would not proceed against the collateral securing that indebtedness.

We are highly leveraged when considering commitments under operating leases.

Our leverage could have material adverse consequences for us, including:

| · | hindering our ability to adjust to changing market, industry or economic conditions, |

| · | limiting our ability to access the capital markets to refinance maturing debt or to fund acquisitions of vessels or businesses, |

| · | limiting the amount of free cash flow available for future operations, dividends, stock repurchases or other uses, |

| · | making us more vulnerable to economic or industry downturns, including interest rate increases, and |

| · | placing us at a competitive disadvantage to those of our competitors that have less indebtedness. |

In connection with executing our business strategies, from time to time we evaluate the possibility of acquiring additional vessels or businesses, and we may elect to finance such acquisitions by incurring additional indebtedness. Moreover, if we were to suffer uninsured material losses or liabilities, we could be required to raise substantial additional capital to fund liabilities that we could not pay with our free cash flow. Our ability to arrange additional financing will depend on, among other factors, our financial position and performance, as well as prevailing market conditions and other factors beyond our control. We cannot assure you that we will be able to obtain additional financing on terms acceptable to us or at all. If we are able to obtain additional financing, our credit may be adversely affected and our ability to satisfy our obligations under our current indebtedness could be adversely affected.