QuickLinks -- Click here to rapidly navigate through this document

Exhibit 99.3

Management's

Discussion and

Analysis

For the year ended December 31, 2019

(Prepared in accordance with International

Financial Reporting Standards)

AGNICO EAGLE MINES LIMITED MANAGEMENT'S DISCUSSION AND ANALYSIS

Table of

Contents

| Executive Summary | 1 | ||||

| Strategy | 1 | ||||

| Portfolio Overview | 2 | ||||

| Key Performance Drivers | 7 | ||||

| Balance Sheet Review | 9 | ||||

| Results of Operations | 10 | ||||

| Revenues from Mining Operations | 10 | ||||

| Production Costs | 11 | ||||

| Exploration and Corporate Development Expense | 15 | ||||

| Amortization of Property, Plant and Mine Development | 16 | ||||

| General and Administrative Expense | 16 | ||||

| Finance Costs | 16 | ||||

| Impairment and Impairment Reversal | 17 | ||||

| Foreign Currency Translation Loss | 17 | ||||

| Income and Mining Taxes Expense | 17 | ||||

| Liquidity and Capital Resources | 17 | ||||

| Operating Activities | 18 | ||||

| Investing Activities | 18 | ||||

| Financing Activities | 19 | ||||

| Off-Balance Sheet Arrangements | 20 | ||||

| Contractual Obligations | 20 | ||||

| 2020 Liquidity and Capital Resources Analysis | 21 | ||||

| Quarterly Results Review | 21 | ||||

| Outlook | 22 | ||||

| Operations Outlook | 22 | ||||

| Financial Outlook | 26 | ||||

| Risk Profile | 27 | ||||

| Impact of COVID-19 | 27 | ||||

| Financial Instruments | 28 | ||||

| Interest Rates | 28 | ||||

| Commodity Prices and Foreign Currencies | 29 | ||||

| Cost Inputs | 29 | ||||

| Operational Risk | 30 | ||||

| Regulatory Risk | 30 | ||||

| Controls Evaluation | 30 | |||

| Outstanding Securities | 31 | |||

| Sustainable Development | 31 | |||

| Employee Health and Safety | 32 | |||

| Community | 32 | |||

| Environmental | 33 | |||

| Critical IFRS Accounting Policies and Accounting Estimates | 33 | |||

| Mineral Reserve Data | 34 | |||

| Non-GAAP Financial Performance Measures | 36 | |||

| Summarized Quarterly Data | 47 | |||

| Three Year Financial and Operating Summary | 53 | |||

This Management's Discussion and Analysis ("MD&A") dated March 27, 2020 of Agnico Eagle Mines Limited ("Agnico Eagle" or the "Company") should be read in conjunction with the Company's annual consolidated financial statements for the year ended December 31, 2019 that were prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB") (the "Annual Financial Statements"). The annual consolidated financial statements and this MD&A are presented in United States dollars ("US dollars", "$" or "US$") and all units of measurement are expressed using the metric system unless otherwise specified. Certain information in this MD&A is presented in Canadian dollars ("C$"), Mexican pesos or European Union euros ("Euros" or "€"). Additional information relating to the Company, including the Company's Annual Information Form for the year ended December 31, 2019 (the "AIF"), is available on the Canadian Securities Administrators' (the "CSA") SEDAR website at www.sedar.com and on the United States Securities and Exchange Commission's (the "SEC") website at www.sec.gov.

NOTE TO INVESTORS CONCERNING FORWARD-LOOKING INFORMATION

Certain statements in this MD&A, referred to herein as "forward-looking statements", constitute "forward-looking information" under the provisions of Canadian provincial securities laws and constitute "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995. These statements relate to, among other things, the Company's plans, objectives, expectations, estimates, beliefs, strategies and intentions and can generally be identified by the use of words such as "anticipate", "believe", "budget", "could", "estimate", "expect", "forecast", "likely", "may", "plan", "project", "schedule", "should", "target", "will", "would" or other variations of these terms or similar words. Forward-looking statements in this MD&A include, but are not limited to, the following:

- •

- the Company's outlook for 2020 and future periods;

- •

- statements regarding future earnings and the sensitivity of earnings to gold and other metal prices;

- •

- anticipated levels or trends for prices of gold and by-product metals mined by the Company or for exchange rates between currencies in which capital is raised, revenue is generated or expenses are incurred by the Company;

- •

- estimates of future mineral production and sales;

- •

- estimates of future costs, including mining costs, total cash costs per ounce, all-in sustaining costs per ounce, minesite costs per tonne and other costs;

- •

- estimates of future capital expenditures, exploration expenditures and other cash needs, and expectations as to the funding thereof;

- •

- statements regarding the projected exploration, development and exploitation of ore deposits, including estimates of exploration, development and production and other capital costs and estimates of the timing of such exploration, development and production or decisions with respect thereto;

- •

- estimates of mineral reserves and mineral resources and their sensitivities to gold prices and other factors, ore grades and mineral recoveries and statements regarding anticipated future exploration results;

- •

- estimates of cash flow;

- •

- estimates of mine life;

- •

- anticipated timing of events at the Company's mines, mine development projects and exploration projects;

- •

- estimates of future costs and other liabilities for environmental remediation;

- •

- statements regarding anticipated legislation and regulations, including with respect to climate change, and estimates of the impact on the Company;

- •

- other anticipated trends with respect to the Company's capital resources and results of operations;

- •

- statements regarding the Company's plans to suspend all mining activities at its operations in the Abitibi region of Quebec and the expected duration of such suspension;

- •

- statements regarding the Company's plans to reduce activities at the Meliadine mine and the Meadowbank Complex and the operations that are expected to be carried out during, and the duration of, the period of such reduced activities;

- •

- statements regarding the Company's plans to suspend exploration activities in Canada;

- •

- statements regarding the timeline for resuming normal operating levels at each of the Company's operations;

- •

- statements regarding the Company's plans with respect to the use of the $1.0 billion drawn on its US$1.2 billion unsecured revolving bank credit facility; and

- •

- other statements regarding the impact of the COVID-19 pandemic and measures taken to reduce the spread of COVID-19 on the Company's operations and overall business.

Forward-looking statements are necessarily based upon a number of factors and assumptions that, while considered reasonable by Agnico Eagle as of the date of such statements, are inherently subject to significant business, economic and competitive uncertainties and contingencies. The factors and assumptions of Agnico Eagle upon which the forward-looking statements in this MD&A are based, and which may prove to be incorrect, include the assumptions set out elsewhere in this MD&A as well as: that the duration or scope of the order by the Government of Quebec issued on March 23, 2020 to close all non-essential businesses in response to the COVID-19 outbreak is not extended or modified; that governments, the Company

or others do not take other measures in response to the COVID-19 pandemic or otherwise that, individually or in the aggregate, materially affect the Company's ability to operate its business and that there are no other significant disruptions affecting Agnico Eagle's operations, whether due to labour disruptions, supply disruptions, damage to equipment, natural or man-made occurrences, disruptions related to the COVID-19 pandemic or other health and safety issues, or the responses of governments, communities, Agnico Eagle and others to such pandemic or other issues, mining or milling issues, political changes, title issues, community protests, including by First Nations groups, or otherwise; that permitting, development, expansion and the ramp up of operations at each of Agnico Eagle's mines, mine development projects and exploration projects proceed on a basis consistent with expectations and that Agnico Eagle does not change its exploration or development plans relating to such projects; that the exchange rates between the Canadian dollar, Euro, Mexican peso and the US dollar will be approximately consistent with current levels or as set out in this MD&A; that prices for gold, silver, zinc and copper will be consistent with Agnico Eagle's expectations; that prices for key mining and construction supplies, including labour costs, remain consistent with Agnico Eagle's expectations; that production meets current expectations; that Agnico Eagle's current estimates of mineral reserves, mineral resources, mineral grades and mineral recoveries are accurate; that there are no material delays in the timing for completion of development projects; and that there are no material variations in the current tax and regulatory environments that affect Agnico Eagle.

The forward-looking statements in this MD&A reflect the Company's views as at the date of this MD&A and involve known and unknown risks, uncertainties and other factors which could cause the actual results, performance or achievements of the Company or industry results to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, the risk factors set out in "Risk Factors" in our most recent Form 40-F/AIF on file with the SEC and Canadian provincial securities regulatory authorities. Given these uncertainties, readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date made. Except as otherwise required by law, the Company expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any such statements to reflect any change in the Company's expectations or any change in events, conditions or circumstances on which any such statement is based.

Unless otherwise expressly stated, milestones set out in this MD&A have not been based on a technical report under NI 43-101 (as defined below).

Meaning of "including" and "such as": When used in this MD&A, the terms "including" and "such as" mean including and such as, without limitation.

NOTE TO INVESTORS CONCERNING ESTIMATES OF MINERAL RESERVES AND MINERAL RESOURCES

The mineral reserve and mineral resource estimates contained in this MD&A have been prepared in accordance with the CSA National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101"). These standards are similar to those used by SEC Industry Guide No. 7, as interpreted by Staff at the SEC ("Guide 7"). However, the definitions in NI 43-101 differ in certain respects from those under Guide 7. Accordingly, mineral reserve and mineral resource information contained in this MD&A may not be comparable to similar information disclosed by United States companies. Under Guide 7, mineralization may not be classified as a "reserve" unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made.

For United States reporting purposes, the SEC has adopted amendments to its disclosure rules (the "SEC Modernization Rules") to modernize the mining property disclosure requirements for issuers whose securities are registered with the SEC under the United States Securities Exchange Act of 1934, as amended (the "Exchange Act"), which became effective February 25, 2019. The SEC Modernization Rules more closely align the SEC's disclosure requirements and policies for mining properties with current industry and global regulatory practices and standards, including NI 43-101, and replace the historical property disclosure requirements for mining registrants that were included in Guide 7. Issuers must begin to comply with the SEC Modernization Rules in their first fiscal year beginning on or after January 1, 2021, though Canadian issuers that report in the United States using the Multijurisdictional Disclosure System ("MJDS") may still use NI 43-101 rather than the SEC Modernization Rules when using the SEC's MJDS registration statement and annual report forms. Guide 7 will remain effective until all issuers are required to comply with the SEC Modernization Rules, at which time Guide 7 will be rescinded.

As a result of the adoption of the SEC Modernization Rules, the SEC now recognizes estimates of measured mineral resources", "indicated mineral resources" and "inferred mineral resources." In addition, the SEC has amended the definitions of "proven mineral reserves" and "probable mineral reserves" in the SEC Modernization Rules, with definitions that are substantially similar to those used in NI 43-101.

United States investors are cautioned that while the SEC now recognizes "measured mineral resources", "indicated mineral resources" and "inferred mineral resources", investors should not assume that any part or all of the mineral deposits in these categories will ever be converted into a higher category of mineral resources or into mineral reserves. These terms have a great amount of uncertainty as to their economic and legal feasibility. Accordingly, investors are cautioned not to assume that any "measured mineral resources", "indicated mineral resources", or "inferred mineral resources" that the Company reports in this management's discussion and analysis are or will be economically or legally mineable.

Further, "inferred mineral resources" have a great amount of uncertainty as to their existence and as to their economic and legal feasibility. It cannot be assumed that any part or all of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian regulations, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in limited circumstances.Investors are cautioned not to assume that any part or all of an inferred mineral resource exists, or is or will ever be economically or legally mineable.

The mineral reserve and mineral resource data set out in this MD&A are estimates, and no assurance can be given that the anticipated tonnages and grades will be achieved or that the indicated level of recovery will be realized. The Company does not include equivalent gold ounces for by-product metals contained in mineral reserves in its calculation of contained ounces and mineral reserves are not reported as a subset of mineral resources. See "Mineral Reserves and Mineral Resources" in the AIF for additional information.

NOTE TO INVESTORS CONCERNING CERTAIN MEASURES OF PERFORMANCE

This MD&A discloses certain measures, including "total cash costs per ounce", "all-in sustaining costs per ounce", "minesite costs per tonne" and "adjusted net income" that are not recognized measures under IFRS. These measures may not be comparable to similar measures reported by other gold mining companies. For a reconciliation of these measures to the most directly comparable financial information presented in the Annual Financial Statements prepared in accordance with IFRS, and for an explanation of how management uses these measures, see Non-GAAP Financial Performance Measures in this MD&A.

The total cash costs per ounce of gold produced is reported on both a by-product basis (deducting by-product metal revenues from production costs) and co-product basis (without deducting by-product metal revenues). The total cash costs per ounce of gold produced on a by-product basis is calculated by adjusting production costs as recorded in the consolidated statements of income (loss) for by-product revenues, inventory production costs, smelting, refining and marketing charges and other adjustments, and then dividing by the number of ounces of gold produced. The total cash costs per ounce of gold produced on a co-product basis is calculated in the same manner as the total cash costs per ounce of gold produced on a by-product basis, except that no adjustment is made for by-product metal revenues. Accordingly, the calculation of total cash costs per ounce of gold produced on a co-product basis does not reflect a reduction in production costs or smelting, refining and marketing charges associated with the production and sale of by-product metals. The total cash costs per ounce of gold produced is intended to provide information about the cash-generating capabilities of the Company's mining operations. Management also uses these measures to monitor the performance of the Company's mining operations. As market prices for gold are quoted on a per ounce basis, using the total cash costs per ounce of gold produced on a by-product basis measure allows management to assess a mine's cash-generating capabilities at various gold prices. Unless otherwise specified, all references to total cash costs per ounce in this MD&A are to total cash costs per ounce reported on a by-product basis.

All-in sustaining costs per ounce is used to show the full cost of gold production from current operations. The Company calculates all-in sustaining costs per ounce of gold produced on a by-product basis as the aggregate of total cash costs per ounce on a by-product basis, sustaining capital expenditures (including capitalized exploration), general and administrative expenses (including stock options), lease payments related to sustaining assets and reclamation expenses, and then dividing by the number of ounces of gold produced. The all-in sustaining costs per ounce of gold produced on a co-product basis is calculated in the same manner as the all-in sustaining costs per ounce of gold produced on a by-product basis, except that the total cash costs per ounce on a co-product basis is used, meaning no adjustment is made for by-product metal revenues. The Company's methodology for calculating all-in sustaining costs per ounce may differ from the methodology used by other gold mining companies that disclose all-in sustaining costs per ounce. The Company may change the methodology it uses to calculate all-in sustaining costs per ounce in the future. Unless otherwise specified, all references to all-in sustaining costs per ounce in this MD&A are to all-in sustaining costs per ounce reported on a by-product basis.

Management is aware that these per ounce measures of performance can be affected by fluctuations in exchange rates and, in the case of total cash costs per ounce of gold produced on a by-product basis, by-product metal prices. Management compensates for these inherent limitations by using these measures in conjunction with minesite costs per tonne as well as other data prepared in accordance with IFRS. The World Gold Council ("WGC") is a non-regulatory market development

organization for the gold industry. Although the WGC is not a mining industry regulatory organization, it has worked closely with its member companies to develop relevant non-GAAP measures. The Company follows the guidance on all-in sustaining costs released by the WGC in November 2018. Adoption of the all-in sustaining costs metric is voluntary and, notwithstanding the Company's adoption of the WGC's guidance, all-in sustaining costs per ounce of gold produced reported by the Company may not be comparable to data reported by other gold mining companies. The Company believes that this measure provides helpful information about operating performance. However, this non-GAAP measure should be considered together with other data prepared in accordance with IFRS as it is not necessarily indicative of operating costs or cash flow measures prepared in accordance with IFRS.

Minesite costs per tonne are calculated by adjusting production costs as recorded in the consolidated statements of income (loss) for inventory production costs and other adjustments, and then dividing by tonnes of ore processed. As the total cash costs per ounce of gold produced can be affected by fluctuations in by-product metal prices and foreign exchange rates, management believes that minesite costs per tonne provide additional information regarding the performance of mining operations, eliminating the impact of varying production levels. Management also uses this measure to determine the economic viability of mining blocks. As each mining block is evaluated based on the net realizable value of each tonne mined, in order to be economically viable the estimated revenue on a per tonne basis must be in excess of the minesite costs per tonne. Management is aware that this per tonne measure of performance can be impacted by fluctuations in processing levels and compensates for this inherent limitation by using this measure in conjunction with production costs prepared in accordance with IFRS.

Adjusted net income is calculated by adjusting the net income as recorded in the consolidated statements of income for foreign currency translation gains and losses, mark-to-market adjustments, non-recurring gains and losses and unrealized gains and losses on financial instruments. Management uses adjusted net income to evaluate the underlying operating performance of the Company and to assist with the planning and forecasting of future operating results. Management believes that adjusted net income is a useful measure of performance because foreign currency translation gains and losses, mark-to-market adjustments, non-recurring gains and losses and unrealized gains and losses on financial instruments do not reflect the underlying operating performance of the Company and may not be indicative of future operating results.

Management also performs sensitivity analyses in order to quantify the effects of fluctuating exchange rates and metal prices. The Company, from time to time, also provides information as to estimated future total cash costs per ounce, all-in sustaining costs per ounce and minesite costs per tonne. Such estimates are based upon the total cash costs per ounce, all-in sustaining costs per ounce and minesite costs per tonne that the Company expects to incur to mine gold at its mines and projects and, consistent with the reconciliation of these actual costs referred to above, do not include production costs attributable to accretion expense and other asset retirement costs, which will vary over time as each project is developed and mined. It is therefore not practicable to reconcile these forward-looking non-GAAP financial measures to the most comparable IFRS measure.

Unless otherwise indicated herein all references to total cash costs per ounce and all-in sustaining costs per ounce refer to such measures as calculated on a by-product basis. For information regarding these measures as calculated on a co-product basis, please see "Non-GAAP Financial Performance Measures".

Payable production (a non-GAAP non-financial performance measure) is the quantity of mineral produced during a period contained in products that have been or will be sold by the Company, whether such products are sold during the period or held as inventories at the end of the period.

Executive Summary

Agnico Eagle is a senior Canadian gold mining company that has produced precious metals since its formation in 1972. The Company's mines are located in Canada, Mexico and Finland, with exploration and development activities in Canada, Europe, Latin America and the United States. The Company and its shareholders have full exposure to gold prices due to its long-standing policy of no forward gold sales. Agnico Eagle has declared a cash dividend every year since 1983.

Agnico Eagle earns a significant proportion of its revenue and cash flow from the production and sale of gold in both dore bar and concentrate form. The remainder of revenue and cash flow is generated by the production and sale of by-product metals, primarily silver, zinc and copper. In 2019, Agnico Eagle recorded production costs per ounce of gold of $735(i) and total cash costs per ounce of gold produced of $673(i) on a by-product basis and $745(i) on a co-product basis on payable gold production of 1,782,147 ounces. The average realized price of gold increased by 11.1% from $1,266 per ounce in 2018 to $1,406 per ounce in 2019.

Agnico Eagle's operating mines and development projects are located in what the Company believes to be politically stable countries that are supportive of the mining industry. The political stability of the regions in which Agnico Eagle operates helps to provide confidence in its current and future prospects and profitability. This is important for Agnico Eagle as it believes that many of its new mines and recently acquired mining projects have long-term mining potential.

Highlights

- •

- Continued strong operational performance with payable gold production of 1,782,147 ounces and production costs per ounce of gold of $735(i) during 2019.

- •

- Total cash costs per ounce of gold produced of $673(i) on a by-product basis and $745(i) on a co-product basis in 2019.

- •

- All-in sustaining costs per ounce of gold produced of $938(i) on a by-product basis and $1,010(i) on a co-product basis in 2019.

- •

- Proven and probable gold reserves totaled 21.6 million ounces at December 31, 2019, a 2.1% decrease compared with 22.0 million ounces at December 31, 2018 while the gold reserve grade increased by 4.8%.

- •

- As at December 31, 2019, Agnico Eagle had strong liquidity with $327.9 million in cash and cash equivalents and short-term investments along with approximately $1.2 billion in undrawn credit lines.

- •

- The Company's operations are located in mining-friendly regions that the Company believes have low political risk and long-term mining potential.

- •

- The Company continues to maintain its investment grade credit rating and has adequate financial flexibility to finance capital requirements at its mines and development projects from operating cash flow, cash and cash equivalents, short-term investments and undrawn credit lines.

- •

- The Company has strong senior management continuity as its Chief Executive Officer has over 30 years of service with the Company.

- •

- In February 2020, the Company declared a quarterly cash dividend of $0.20 per common share, an increase of $0.025 per share or approximately 14%. Agnico Eagle has now declared a cash dividend every year since 1983.

Strategy

Agnico Eagle's ability to consistently execute its business strategy has provided a solid foundation for growth.

The Company's goals are to:

- •

- Deliver high quality growth while meeting market expectations and maintaining highperformance standards in health, safety, environment and community development;

- •

- Build a strongpipeline of projects to drive future production; and

Note:

- (i)

- Excludes 85,699 ounces of payable gold production associated with the Meliadine mine, the Amaruq satellite deposit at the Meadowbank Complex and the Barnat deposit at the Canadian Malartic mine which were produced prior to the achievement of commercial production at such sites, and 5 ounces of payable gold production credited to the Company as a result of final refining reconciliation following the cessation of mining and processing operations at the Lapa mine.

- •

- Employ the bestpeople and motivate them to reach their potential.

MANAGEMENT'S DISCUSSION AND ANALYSIS AGNICO EAGLE 1

These three pillars – performance, pipeline and people – form the basis of Agnico Eagle's success and competitive advantage. By delivering on them, the Company strives to continue to build its production base and generate increased value for shareholders, while making meaningful contributions to its employees and communities.

Portfolio Overview

Northern Business

Canada – LaRonde Complex

The 100% owned LaRonde Complex in northwestern Quebec, includes the LaRonde mine, the Company's oldest mine, which achieved commercial production in 1988 and the LaRonde Zone 5 mine ("LZ5"). In 2019, the Company was granted a revision to the Certificate of Authorization at the LaRonde Complex, which allowed for the processing of ore from LZ5 through the LaRonde mill circuit. As a result, the Company now reports the operational parameters from both the LaRonde mine and the LZ5 mine on a combined basis as of the first quarter of 2020.

LaRonde Mine

The LaRonde mine extension, the portion of the mine below the 245 level, achieved commercial production in December 2011, and under current mine plans is expected to be in production through 2029.

In early December 2019, the Company saw an increase in seismicity in the West mine area outside of normal protocols, which resulted in lower anticipated gold production. In addition, as development has progressed in the West mine area, additional geological structures (faulting and fracturing) have been recognized. This information has now been incorporated into a revised ground support plan for the West mine area.

This revised plan has been developed to ensure the safety of the Company's employees, secure the higher-grade orebody to the west and preserve existing mine infrastructure in the area. To implement this plan, mining activity in the West mine area was temporarily suspended in mid-December 2019 and refocused in the East mine area.

In the West mine area, the Company is currently reinforcing ground support including installation of additional support (shotcrete, bolts and cables) in the main ramp and access points on various levels. Seismicity is expected to continue but ground support will be better adapted to manage stress levels.

The LaRonde mine's proven and probable mineral reserves were approximately 2.9 million ounces at December 31, 2019.

LaRonde Zone 5 Mine

In 2003, the Company acquired the Bousquet gold property, which adjoins the LaRonde complex to the west and hosts the Bousquet Zone 5, which the Company has renamed LZ5 due to the proximity to the LaRonde mine. Commercial production at LZ5 was achieved in June 2018 and under current mine plans, is expected to be in production through 2027.

Given the success in mining the upper portions of the LZ5 deposit (from surface to 330 metres), mining activities will be extended to 480 metres depth. The Company is also evaluating the potential to develop deeper portions of LZ5 (480 metres to 700 metres) and potentially mine portions of the neighboring Ellison property from the LZ5 underground infrastructure.

The LZ5 mine's proven and probable mineral reserves were approximately 0.7 million ounces at December 31, 2019.

Canada – Goldex Mine

The 100% owned Goldex mine in northwestern Quebec achieved commercial production from the M and E satellite zones in October 2013. The Deep 1 Zone achieved commercial production in July 2017. Production from the Deep 1 Zone is expected to extend the Goldex mine life through 2027 under current mine plans.

In 2019, mining in the South Zone continued with a total of 11 stopes mined. Stopes mined to date have shown better grades than anticipated and have confirmed dilution and recovery assumptions. The South Zone consists of quartz veins that have higher grades than those in the primary mineralized zones at Goldex. The Company continues to evaluate the potential for increased throughput from Deep 1 and the potential for additional development of Deep 2 and also the potential for increased gold production from the South Zone.

Following a successful test stope in 2018, the eastern part of the South Zone was added to the mine plan. Additional stopes were added to the mine plan for 2020 to 2026 based on the successful conversion drilling in 2019.

The Goldex mine's proven and probable mineral reserves were approximately 1.1 million ounces at December 31, 2019.

2 AGNICO EAGLE MANAGEMENT'S DISCUSSION AND ANALYSIS

Canada – Meadowbank Complex (Including the Meadowbank Mine and Amaruq Satellite Deposit)

In 2007, the Company acquired Cumberland Resources Ltd., which held a 100% interest in the Meadowbank gold project in Nunavut, Canada. Commercial production was achieved at the Meadowbank mine in March 2010. Mining operations at the Meadowbank site ceased in 2019.

The 100% owned Amaruq satellite deposit is located approximately 50 kilometres northwest of the Meadowbank mine and was identified by the Company in 2013. In 2016, the Company approved the project for development. Commercial production was achieved at the Amaruq satellite deposit in September 2019.

At December 31, 2019, the Company reported an initial underground probable mineral reserve in the Whale Tail deposit of approximately 0.6 million ounces of gold (3.3 million tonnes grading 5.43 g/t gold). Work is continuing at Amaruq to evaluate the potential for an underground operation, which could run concurrently with mining the open pit deposits.

Preliminary work suggests that there is an opportunity to selectively mine portions of the higher-grade underground deposits at Amaruq in permafrost only. This approach is expected to reduce operating and capital costs (limited heating requirements) and lower water management risk, while preserving the optionality to mine additional underground mineral reserves and/or mineral resources. The Company will continue to use a phased approach to the underground development program at Amaruq.

The Meadowbank Complex's proven and probable mineral reserves were approximately 3.3 million ounces at December 31, 2019.

Canada – Meliadine Mine

In 2010, Agnico Eagle acquired its 100% interest in the Meliadine mine project in Nunavut, Canada through its acquisition of Comaplex Minerals Corp.

In 2016, the Company's Board of Directors ("Board") approved the construction of the Meliadine mine project. Commercial production was achieved at the Meliadine mine in May 2019. In 2020, the Company approved the Phase 2 expansion which accelerates the Tiriganiaq open pits from year five of the mine life.

In the fourth quarter of 2019, the processing plant averaged approximately 3,543 tpd, with average recoveries of 94.6%. Bottlenecks at the front end of the crushing circuit and wear issues with the apron feeder hampered maximization of throughput in the mill.

In order to optimize production and lower operating costs at Meliadine, an action plan has been put in place with a primary focus on improvements to the process plant area, improving mining flexibility and water management. The plan includes:

- •

- apron feeder and chute re-engineering to correct wear issues;

- •

- filter press corrosion mitigation;

- •

- paste backfill capacity optimization;

- •

- underground maintenance continuous improvement, focus on trucks and scoops;

- •

- phase 2 expansion acceleration, development of Tiriganiaq open pits; and

- •

- saline water line discharge to sea.

The current Meliadine water management plan includes segregation of underground dewatering and surface runoff waters in specific ponds, treatment and year-round discharge to Meliadine Lake or seasonal discharge to Hudsons Bay, depending on the type of water. One of the objectives of the water management plan is to minimize the volume of water in the water containment infrastructures prior to the freshet (spring melt). In 2019, the total dissolved solids ("TDS") in the runoff water pond was higher than predicted and the volume of water that could be discharged within the prescribed TDS limit was reduced. This water was subjected to a series of tests and was deemed non-toxic. The Company is in discussion with the regulatory agencies to modify the discharge criteria and allow flexibility for the mine to manage precipitation variations and the freshet while preserving the integrity of water containment infrastructures and protecting aquatic life.

While discharge to Hudsons Bay is currently performed by trucks, the Company is investigating the possibility of installing a permanent pipeline. This is expected to reduce costs and the environmental impact of trucking. Consultations are currently underway with local stakeholders and regulatory agencies.

The Meliadine mine project had proven and probable mineral reserves of approximately 4.1 million ounces at December 31, 2019.

MANAGEMENT'S DISCUSSION AND ANALYSIS AGNICO EAGLE 3

Canada – Canadian Malartic Mine

Agnico Eagle and Yamana Gold Inc. ("Yamana") jointly acquired 100% of Osisko Mining Corporation now Canadian Malartic Corporation ("CMC"). In 2014 pursuant to a court-approved plan of arrangement under theCanada Business Corporations Act (the "Osisko Arrangement"). As a result of the Osisko Arrangement, Agnico Eagle and Yamana each indirectly own 50% of CMC and Canadian Malartic General Partnership ("CMGP"), a general partnership (the "Partnership"), which now holds the Canadian Malartic mine in northwestern Quebec.

Deep drilling east of the open pit in late 2018 resulted in the discovery of a new gold mineralized zone, located south of the East Malartic and Odyssey zones, named the East Gouldie Zone. The East Gouldie Zone has a strike length of 1,300 metres in an east-west direction, dips 60 degrees north, and extends from 700 metres to 1,900 metres depth below surface. East Gouldie is a silicified and carbonatized mineralized zone with fine disseminated pyrite developed in sheared greywacke units. There was a total of 82,379 metres (100% basis) drilled in 2019 aimed to reduce drill spacing in the central portion of the East Gouldie Zone. This drilling allowed for the estimation of initial inferred mineral resources at East Gouldie of 1.4 million ounces of gold (12.8 million tonnes grading 3.34 g/t gold) (reflecting the Company's 50% interest), as of December 31, 2019.

At the Odyssey project, the Partnership is evaluating the underground potential of several other gold deposits close to the Canadian Malartic/Barnat open pit. These include the East Malartic, Sladen, South Sladen, Sheehan, Odyssey North and Odyssey South Zones, located under and immediately east of the pit, extending approximately 2.5 kilometres to the east.

At the East Malartic Zone, the inclusion of deeper mineral resources (between 1,000 metres and 1,800 metres depth) has increased inferred mineral resources by 85% or 1.2 million ounces of gold (reflecting the Company's 50% interest), bringing total inferred mineral resources at East Malartic to 2.6 million ounces of gold (39.0 million tonnes grading 2.05 g/t gold). In addition, the East Malartic Zone has indicated mineral resources of 0.3 million ounces of gold (5.0 million tonnes grading 2.18 g/t gold) (50% interest), as of December 31, 2019.

Mineral resources at the nearby Odyssey deposit were basically unchanged between 2018 and 2019, with indicated mineral resources of 0.1 million ounces of gold (1.0 million tonnes grading 2.10 g/t gold) and inferred mineral resources of 0.8 million ounces of gold (11.7 million tonnes grading 2.22 g/t gold) (50% basis), as of December 31, 2019.

In the fourth quarter of 2019, pre-commercial production began at the Barnat extension project. Mining activities at the Barnat pit are expected to continue to ramp up during 2020.

Agnico Eagle's attributable share of proven and probable mineral reserves at the Canadian Malartic mine were approximately 2.4 million ounces at December 31, 2019.

Canada – Kirkland Lake Assets

On March 28, 2018, the Company acquired 100% of the Canadian exploration assets (the "CMC Exploration Assets") of Canadian Malartic Corporation ("CMC"), including the Kirkland Lake and Hammond Reef gold projects for an effective purchase price of $162.5 million. On the closing of the transaction, Agnico acquired all of Yamana's indirect 50% interest in the CMC Exploration Assets, giving Agnico Eagle 100% ownership. The transaction did not affect the ownership of the Canadian Malartic mine and related assets including Odyssey, East Malartic, Midway and East Amphi properties, which will continue to be jointly owned and operated by the Company and Yamana through CMC and the Partnership.

In 2019, the total exploration drilling at the Kirkland Lake project in 2019 was 40,693 metres (103 holes) comprised of 27,010 metres (73 holes) at the Upper Beaver deposit and 13,683 metres (30 holes) at the Upper Canada deposit.

The Company is still investigating various opportunities and potential synergies in terms of engineering concepts for future development of the Upper Beaver and Upper Canada deposits.

The Company is undertaking work at Upper Beaver that is expected to lead to an updated mineral resource estimate for the deposit. An increase in the mineral resources in the shallow basalts would have a significant positive impact on project economics, and could provide added flexibility for a future underground operation.

The Upper Canada deposit lies approximately six kilometres southwest of the Upper Beaver deposit, within a 300- to 400-metre wide strongly altered deformation corridor. Gold mineralization is associated with intensely altered shear zones with fine pyrite and ancillary sulphide mineralization.

Upper Beaver deposit's proven and probable mineral reserves were approximately 1.4 million ounces at December 31, 2019. No proven and probable mineral reserves have been declared for the Upper Canada or the Hammond Reef projects.

4 AGNICO EAGLE MANAGEMENT'S DISCUSSION AND ANALYSIS

Finland – Kittila Mine

The 100% owned Kittila mine in northern Finland was added to the Company's portfolio through the acquisition of Riddarhyttan Resources AB in 2005. Construction at the Kittila mine was completed in 2008 and commercial production was achieved in May 2009.

In February 2018, the Company's Board of Directors approved an expansion to increase throughput rates at Kittila to 2.0 million tonnes per annum ("mtpa") from the current rate of 1.6 mtpa. Permitting is ongoing for the increase in throughput. This expansion includes the construction of a 1,044-metre deep shaft, a processing plant expansion as well as other infrastructure and service upgrades.

The expansion project is expected to increase the efficiency of the mine and maintain or decrease operating costs while providing access to the deeper mining horizons. In addition, the shaft is expected to provide access to the mineral resources located below 1,150 metres depth, where recent exploration programs have shown promising results. The shaft and mill expansion are continuing to advance.

In the fourth quarter of 2019, Kittila expansion work continued on underground excavations for the new rock handling system and the construction of the headframe. The ultimate height of the headframe was reached on November 1, 2019, and since then work is on-going to install the required steel structures. Shaft sinking is expected to begin once final support and steel sets are installed in the first segment.

As a result of higher than expected costs in shaft sinking and in the rock handling system, the Kittila expansion project is now forecast to cost between 160 to 170 million euros (previous forecast was 160 million euros).

Exploration at the Kittila mine is focused on extending the Main and Sisar zones northward, southward and at depth in the Roura and Rimpi areas to increase the mineral reserves in the large orebody. Sisar is subparallel to and 50 to 300 metres east of the main Kittila mineralization.

Proven and probable mineral reserves at the Kittila mine were approximately 4.1 million ounces at December 31, 2019.

Southern Business

Mexico – Pinos Altos Mine

In 2006, the Company completed the acquisition of the Pinos Altos property, which was then an advanced stage exploration property in northern Mexico. Commercial production was achieved at the Pinos Altos mine in November 2009. A shaft sinking project was completed in June 2016 at the Pinos Altos mine and during 2018, the site transitioned into being a predominantly underground mining operation.

In 2019, the Company began testing samples from the Pinos Altos and La India mines relating to an ore sorting project. To-date, sorting of open pit ore from the Sinter deposit has yielded favourable preliminary results. Similar ore sorting pilot testing is being considered at the Company's other operating sites. In the fourth quarter of 2019, ore from various assets of the Company were tested at the ore sorting pilot plant at the Pinos Altos mine.

At the Cerro Colorado underground operations, mining activities in 2019 encountered an area with challenging ground conditions. To address this, the Company adjusted the mining sequence, and as a result, the mining capacity at Cerro Colorado was reduced by 75% in the third quarter of 2019. Despite efforts to mitigate the challenging ground conditions, the change in mining sequence at Cerro Colorado continued to have adverse effect on fourth quarter production as this zone was expected to provide higher grade ore feed. The Company is continuing to take measures to mitigate the challenging ground conditions at Cerro Colorado and increase the amount of ore extracted. These measures include:

- •

- decreasing the speed of the mining sequence; and

- •

- reducing stope size by 25%,

- •

- potential to add additional stopes at the Santo Nino underground;

- •

- potential to add higher grades at the Sinter deposit.

MANAGEMENT'S DISCUSSION AND ANALYSIS AGNICO EAGLE 5

Exploration at Pinos Altos is focused on the Reyna East Zone (formerly called Reyna de Plata East) in the southeast of the property and at the Cubiro deposit in the property's northwest, where the exploration ramp development is providing additional access for drilling exploration targets from underground.

The Pinos Altos mine's proven and probable mineral reserves (including satellite deposits) were approximately 1.0 million ounces at December 31, 2019.

Mexico – Creston Mascota Mine

The 100% owned Creston Mascota mine is located approximately 7.0 kilometres northwest of the Pinos Altos mine in northern Mexico. First mining activity commenced at the Creston Mascota deposit in 2010 and commercial production was achieved at the mine in March 2011. During 2017, the Bravo zone located south of the Creston Mascota facilities was added to the mine plan. Construction activities continued through 2018 and mining at the main Bravo zone began in the third quarter of 2018.

Creston Mascota open pit mineral reserves are now expected to be depleted by the end of the first half of 2020, largely due to the discovery of additional ore outside of the mineral reserve model. Gold leaching is expected to continue through the end of 2020.

The Creston Mascota mine's proven and probable mineral reserves were approximately 0.1 million ounces at December 31, 2019.

Mexico – La India Mine

Agnico Eagle acquired 100% of Grayd Resource Corporation ("Grayd") in January 2012. Grayd owned the La India project, which is located approximately 70 kilometres northwest of the Pinos Altos mine in northern Mexico. In September 2012, development and construction of the La India mine were approved by the Board and commercial production was achieved in February 2014.

In 2019, production was affected by the high clay content of the ore, which negatively affected recoveries. To mitigate this effect in the short term, belt agglomeration (adding cement to the ore delivered by conveyor from the crusher to the heap leach pad) was initiated in the third quarter of 2019, adjustments were made to the stacking sequence and irrigation rates were decreased on the leach pads to help improve percolation.

During the second half of 2019, modifications were also made to the screens and transfer chutes on the conveyors. An automatic radial stacker was acquired to improve transfer of ore to the leach pads and two agglomeration units were ordered to improve percolation and are expected to be commissioned once all the civil work has been completed.

Additional drilling is also being carried out to better define areas with higher clay content in the geological model. These improvements are expected to result in more normal production rates going forward.

The regional exploration program continues to return encouraging results at the Chipriona polymetallic sulphide target, located approximately one kilometre north of the North Zone at the La India mine. The positive drill results have led to a new indicated mineral resource and a 48% year-over-year increase of gold contained in inferred mineral resources at the Chipriona project, all at open pit depth. As of December 31, 2019, the Chipriona deposit has indicated mineral resources of 0.05 million ounces of gold, 2.1 million ounces of silver, 359 tonnes of copper and 17,000 tonnes of zinc (1.3 million tonnes grading 1.11 g/t gold, 50.99 g/t silver, 0.03% copper and 1.36% zinc) and inferred mineral resources of 0.2 million ounces of gold, 29.5 million ounces of silver, 15,400 tonnes of copper and 86,900 tonnes of zinc (10.7 million tonnes grading 0.69 g/t gold, 85.44 g/t silver, 0.14% copper and 0.81% zinc).

The La India mine's proven and probable mineral reserves (including satellite deposits) were approximately 0.5 million ounces at December 31, 2019.

Mexico – Santa Gertrudis Project

In November 2017, the Company acquired its 100% interest in the Santa Gertrudis property which is located approximately 180 kilometers north of Hermosillo in Sonora, Mexico.

The property was the site of historic heap leach operations that produced approximately 0.6 million ounces of gold at a grade of 2.10 g/t gold between 1991 and 2000. The project also has a substantial surface infrastructure already in place including pre-stripped pits, haul roads, water sources and buildings.

6 AGNICO EAGLE MANAGEMENT'S DISCUSSION AND ANALYSIS

Extensive drilling in 2019 has led to initial indicated mineral resources of 0.1 million ounces of gold (5.1 million tonnes grading 0.64 g/t gold) at open pit depth, and an increased inferred mineral resource of 1.2 million ounces of gold (22.1 million tonnes grading 1.64 g/t gold) mainly at open pit depth, as of December 31, 2019.

The full-year 2019 exploration program at Santa Gertrudis totaled 143 holes (19,352 metres in Amelia and 23,426 metres in the rest of the project), compared with an initial budget of 29,000 metres of drilling. The focus of the program was on mineral resource expansion and refining the understanding of new targets within the Trinidad Zone.

Amelia is one of three deposits that comprise the Trinidad Zone and is the site of a previously operating open-pit gold mine. High-grade gold mineralization can be found in multiple parallel structures that commonly correspond to lithological contacts. The Amelia deposit has been extended 100 metres to an east-west strike length of approximately 900 metres and dips steeply to the north; it includes an ore shoot on the west side that plunges steeply to the east. Most of the open pit (oxide) material lies between surface and 100 metres depth, while the underground material reaches below the open pit mineral resources to a depth of approximately 350 metres, but recent drilling has intersected an extension of the mineralization at 677 metres below surface. The Amelia deposit remains open along strike and at depth. The Company has updated the inferred mineral resources at Amelia to 1.6 million tonnes grading 1.38 g/t gold (0.1 million ounces of gold) at open pit depth, as well as an initial underground inferred mineral resource of 3.1 million tonnes grading 4.58 g/t gold (0.5 million ounces of gold) in the high-grade sulphide material. The Amelia mineral resources are part of the Santa Gertrudis project estimate as of December 31, 2019.

Key Performance Drivers

The key drivers of financial performance for Agnico Eagle include:

- •

- the spot price of gold, silver, zinc and copper;

- •

- production volumes;

- •

- production costs; and

- •

- US dollar/Canadian dollar, US dollar/Mexican peso and US dollar/Euro exchange rates.

Spot Price of Gold, Silver, Zinc and Copper

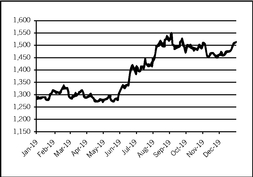

| 2019 | 2018 | % Change | |||||

| High price | $1,557 | $1,366 | 14.0% | ||||

| Low price | $1,266 | $1,160 | 9.1% | ||||

| Average market price | $1,393 | $1,269 | 9.8% | ||||

| Average realized price | $1,406 | $1,266 | 11.1% | ||||

In 2019, the average market price per ounce of gold was 9.8% higher than in 2018. The Company's average realized price per ounce of gold in 2019 was 11.1% higher than in 2018.

MANAGEMENT'S DISCUSSION AND ANALYSIS AGNICO EAGLE 7

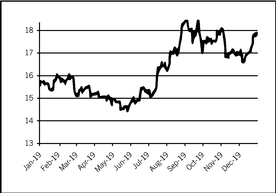

| 2019 | 2018 | % Change | |||||

| High price | $19.65 | $17.71 | 11.0% | ||||

| Low price | $14.29 | $13.89 | 2.9% | ||||

| Average market price | $16.21 | $15.71 | 3.2% | ||||

| Average realized price | $16.38 | $15.51 | 5.6% | ||||

In 2019, the average market price per ounce of silver was 3.2% higher than in 2018. The Company's average realized price per ounce of silver in 2019 was 5.6% higher than in 2018.

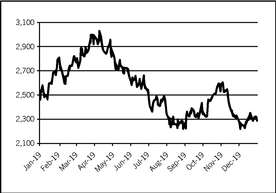

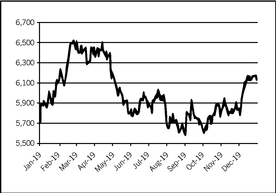

| ZINC ($ per tonne) | COPPER ($ per tonne) |

|---|---|

|  |

Agnico Eagle's average realized sales price year-over-year for zinc decreased by 14.1% and the average realized sales price for copper year-over-year decreased by 9.9%. Significant quantities of by-product metals are produced by the LaRonde mine (silver, zinc and copper) and the Pinos Altos mine (silver).

Net by-product (primarily silver, zinc and copper) revenue is treated as a reduction of production costs in calculating total cash costs per ounce of gold produced on a by-product basis and all-in sustaining costs per ounce of gold produced on a by-product basis.

The Company has never sold gold forward, allowing the Company to take full advantage of rising gold prices. Management believes that low cost production is the best protection against a decrease in gold prices.

Production Volumes and Costs

Changes in production volumes have a direct impact on the Company's financial results. Total payable gold production was 1,782,147 ounces in 2019, an increase of 9.6% compared with 1,626,669 ounces in 2018. The increase was primarily due to the achievement of commercial production at the Meliadine mine during the second quarter of 2019. Partially offsetting the overall increase in gold production was a decrease in tonnes processed at the Meadowbank Complex as the site transitioned to the Amaruq satellite deposit which achieved commercial production at the end of the third quarter of 2019.

Production costs are discussed in detail in the Results of Operations section below.

8 AGNICO EAGLE MANAGEMENT'S DISCUSSION AND ANALYSIS

Foreign Exchange Rates (Ratio to US$)

The exchange rate of the Canadian dollar, Mexican peso and Euro relative to the US dollar is an important financial driver for the Company for the following reasons:

- •

- all revenues are earned in US dollars;

- •

- a significant portion of operating costs at the Meadowbank Complex, LaRonde, LaRonde Zone 5, Goldex, Canadian Malartic, and Meliadine mines are incurred in Canadian dollars;

- •

- a significant portion of operating costs at the Pinos Altos, Creston Mascota and La India mines are incurred in Mexican pesos; and

- •

- a significant portion of operating costs at the Kittila mine are incurred in Euros.

The Company mitigates part of its foreign currency exposure by using currency hedging strategies.

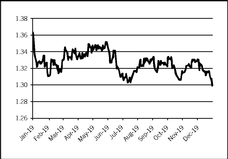

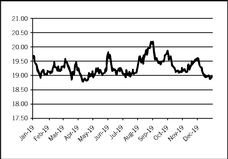

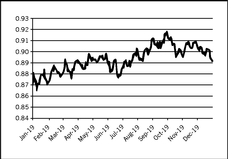

| CANADIAN DOLLAR | MEXICAN PESO | EURO | ||

|---|---|---|---|---|

|  |  |

On average, the Canadian dollar, Euro and Mexican peso weakened relative to the US dollar in 2019 compared with 2018, decreasing costs denominated in the local currency when translated into US dollars for reporting purposes.

Balance Sheet Review

Total assets at December 31, 2019 of $8,789.9 million increased compared to December 31, 2018 total assets of $7,852.8 million. The $937.1 million increase in total assets between periods was primarily comprised of a $769.4 million increase in property, plant and mine development and an $85.9 million increase in inventories. The December 31, 2017 balance of $7,865.6 million was largely consistent with the total assets as at December 31, 2018.

Cash and cash equivalents were $321.9 million at December 31, 2019, an increase of $20.1 million compared with December 31, 2018 primarily due to an increase in cash provided by operating activities of $881.7 million and proceeds on the exercise of stock options of $140.6 million, partially offset by $882.7 million in capital expenditures and $105.4 million in dividends paid during 2019.

Current inventory balances increased by $85.9 million from $494.2 million at December 31, 2018 to $580.1 million at December 31, 2019 primarily due to a $45.5 million increase in supplies inventories and a $23.8 million increase in concentrate inventories from the ramp up at the Meliadine mine and the Amaruq satellite deposit at the Meadowbank Complex which both achieved commercial production during 2019. Non-current ore in stockpiles and on leach pads increased by $28.9 million from $116.8 million at December 31, 2018 to $145.7 million at December 31, 2019 primarily due to the the increase in the stockpiles balance not expected to be processed within 12 months at the Canadian Malartic mine, partially offset by the reclassification from current inventory at the La India mine.

Equity securities increased from $76.5 million at December 31, 2018 to $86.3 million at December 31, 2019 primarily due to $9.6 million in unrealized fair value gains and $6.0 million in new investments, partially offset by $5.7 million in disposals during 2019.

Property, plant and mine development increased by $769.4 million to $7,003.7 million at December 31, 2019 compared with December 31, 2018 due to $882.7 million in capital expenditures, primarily at the Meadowbank Complex, Kittila and Meliadine mines, and an impairment reversal at the Meliadine mine of $345.8 million in 2019. This increase was partially offset by amortization expense of $546.1 million incurred during 2019.

Total liabilities increased to $3,678.4 million at December 31, 2019 from $3,302.8 million at December 31, 2018 primarily due to the net capitalization of $114.9 million of lease obligations during 2019 in accordance with the adoption of IFRS 16 – Leases ("IFRS 16") effective January 1, 2019. Total liabilities increased to $3,302.8 million at December 31, 2018 from

MANAGEMENT'S DISCUSSION AND ANALYSIS AGNICO EAGLE 9

$2,918.6 million at December 31, 2017 primarily due to $350.0 million related to the issuance of guaranteed senior unsecured notes on April 5, 2018.

Accounts payable and accrued liabilities increased by $35.0 million between December 31, 2018 and December 31, 2019 primarily due to the timing of expenditures.

Net income taxes payable increased by $23.0 million between December 31, 2018 and December 31, 2019 primarily due to the current tax expense exceeding payments to tax authorities.

Long-term debt decreased by $357.2 million between December 31, 2018 and December 31, 2019 primarily due to $360.0 million of the Company's long-term debt that was reclassified to current liabilities.

Reclamation provision increased by $53.6 million between December 31, 2018 and December 31, 2019 primarily due to the re-measurement of the Company's reclamation provisions by applying updated expected cash flows and assumptions at the Meadowbank Complex as well as Meliadine and Kittila mines as at December 31, 2019.

Deferred income and mining tax liabilities increased by $151.4 million between December 31, 2018 and December 31, 2019 primarily due to the origination and reversal of net taxable temporary differences, including the tax effect of the Meliadine impairment reversal.

Fair Value of Derivative Financial Instruments

The Company occasionally enters into contracts to limit the risk associated with decreased by-product metal prices, increased foreign currency costs (including capital expenditures) and input costs. The contracts act as economic hedges of underlying exposures and are not held for speculative purposes. Agnico Eagle does not use complex derivative contracts to hedge exposures. The fair value of the Company's derivative financial instruments is outlined in the financial instruments note to the Company's annual consolidated financial statements.

Results of Operations

Agnico Eagle reported net income of $473.2 million, or $2.00 per share, in 2019 compared with a net loss of $326.7 million, or $1.40 per share, in 2018. In 2017, the Company reported net income of $240.8 million, or $1.05 per share. Agnico Eagle reported adjusted net income(i) of $229.4 million, or $0.97 per share, in 2019 compared with adjusted net income of $71.9 million, or $0.31 per share, in 2018. In 2017, the Company reported adjusted net income of $233.8 million, or $1.02 per share. In 2019, operating margin (revenues from mining operations less production costs) increased to $1,247.2 million from $1,030.9 million in 2018. In 2017, operating margin was $1,184.8 million.

Revenues from Mining Operations

Revenues from mining operations increased by $303.7 million, or 13.9%, to $2,494.9 million in 2019 from $2,191.2 million in 2018 primarily due to an 11.1% increase in the average realized price of gold between periods. Revenues from mining operations were $2,242.6 million in 2017.

Revenues from the Northern Business increased by $313.8 million, or 18.0%, to $2,053.0 million in 2019 from $1,739.2 million in 2018 primarily due to a higher average realized price of gold and an increase in the sales volume of gold ounces(ii). Revenues from the Southern Business decreased by $10.1 million, or 2.2%, to $441.9 million in 2019 from $452.0 million in 2018, primarily due to a decrease in the sales volume of gold ounces, partially offset by a higher average realized price of gold. Revenues from the Northern Business were $1,790.9 million and revenues from the Southern Business were $451.7 million in 2017.

Sales of precious metals (gold and silver) accounted for 98.9% of revenues from mining operations in 2019, an increase from 98.4% in 2018 and a decrease from 99.3% in 2017. The slight increase in the percentage of revenues from precious metals in 2019 compared with 2018 was primarily due to a higher average realized price of gold.

Notes:

- (i)

- Adjusted net income is a non-GAAP measure. For a discussion of the Company's use of non-GAAP measures and a reconciliation to the nearest GAAP measure, seeNon-GAAP Financial Performance Measures in this MD&A.

- (ii)

- Excludes 64,034 ounces of payable gold production sold associated with the Meliadine mine, the Amaruq satellite deposit at the Meadowbank Complex and the Barnat deposit at the Canadian Malartic mine which were sold prior to the achievement of commercial production.

10 AGNICO EAGLE MANAGEMENT'S DISCUSSION AND ANALYSIS

The table below sets out revenues from mining operations, production volumes and sales volumes by metal:

| 2019 | 2018 | 2017 | ||||||||

(thousands of United States dollars) | ||||||||||

| Revenues from mining operations: | ||||||||||

| Gold | $ | 2,393,869 | $ | 2,080,545 | $ | 2,140,890 | ||||

| Silver | 73,312 | 75,310 | 86,262 | |||||||

| Zinc | 14,711 | 14,397 | 9,177 | |||||||

| Copper | 13,000 | 20,969 | 6,275 | |||||||

| Total revenues from mining operations | $ | 2,494,892 | $ | 2,191,221 | $ | 2,242,604 | ||||

Payable production (i): | ||||||||||

| Gold (ounces) | 1,782,147 | 1,626,669 | 1,713,533 | |||||||

| Silver (thousands of ounces) | 4,310 | 4,524 | 5,016 | |||||||

| Zinc (tonnes) | 13,161 | 7,864 | 6,510 | |||||||

| Copper (tonnes) | 3,397 | 4,193 | 4,501 | |||||||

Payable metal sold: | ||||||||||

| Gold (ounces) | 1,755,334 | 1,629,785 | 1,693,774 | |||||||

| Silver (thousands of ounces) | 4,273 | 4,545 | 4,852 | |||||||

| Zinc (tonnes) | 12,292 | 8,523 | 6,316 | |||||||

| Copper (tonnes) | 3,390 | 4,195 | 4,599 | |||||||

Revenues from gold increased by $313.3 million or 15.1% in 2019 compared with 2018 primarily due to an 11.1% increase in the average realized price of gold and a 3.8% increase in the sales volume of gold(ii). The Company's average realized price of gold increased to $1,406 in 2019 compared to $1,266 in 2018, and the sales volume of gold increased to 1,691,300 ounces(ii) in 2019 compared to 1,629,785 gold ounces in 2018

Revenues from silver decreased by $2.0 million or 2.7% in 2019 compared with 2018 primarily due to a 6.0% decrease in the sales volume of silver which was partially offset by a 5.6% increase in average realized price of silver to $16.38 in 2019 from $15.51 in 2018. Revenues from zinc increased by $0.3 million or 2.2% to $14.7 million in 2019 compared with $14.4 million in 2018 primarily due to a 44.2% increase in the sales volume of zinc, partially offset by a 14.1% decrease in the average realized price of zinc between periods. Revenues from copper decreased by $8.0 million or 38.0% in 2019 compared with 2018 primarily due to a 19.2% decrease in the sales volume of copper and a 9.9% decrease in the average realized price of copper.

Production Costs

Production costs increased to $1,247.7 million in 2019 compared with $1,160.4 million in 2018 primarily due to the ramp up of the Meliadine mine which achieved commercial production in the second quarter of 2019. Partially offsetting the overall increase was an expected decrease in the mining and milling costs at the Meadowbank Complex as production at Meadowbank transitioned to the Amaruq satellite deposit, which achieved commercial production at the end of the third quarter of 2019. Production costs were $1,057.8 million in 2017.

Notes:

- (i)

- Payable production is a non-GAAP, non-financial performance measure. See "Notes to Investors Concerning Certain Measures of Performance".

- (ii)

- Excludes 64,034 ounces of payable gold production sold associated with the Meliadine mine, the Amaruq satellite deposit at the Meadowbank Complex and the Barnat deposit at the Canadian Malartic mine which were sold prior to the achievement of commercial production.

MANAGEMENT'S DISCUSSION AND ANALYSIS AGNICO EAGLE 11

The table below sets out production costs by mine:

| 2019 | 2018 | 2017 | ||||||||

| (thousands of United States dollars) | ||||||||||

| LaRonde mine | $ | 215,012 | $ | 228,294 | $ | 185,488 | ||||

| LaRonde Zone 5 mine | 41,212 | 12,991 | – | |||||||

| Lapa mine | 2,844 | 27,870 | 38,786 | |||||||

| Goldex mine | 82,533 | 78,533 | 71,015 | |||||||

| Meadowbank Complex | 180,848 | 211,147 | 224,364 | |||||||

| Meliadine mine | 142,932 | – | – | |||||||

| Canadian Malartic mine (attributable 50%) | 208,178 | 199,761 | 188,568 | |||||||

| Kittila mine | 142,517 | 157,032 | 148,272 | |||||||

| Pinos Altos mine | 130,190 | 138,362 | 108,726 | |||||||

| Creston Mascota mine | 35,801 | 37,270 | 31,490 | |||||||

| La India mine | 65,638 | 69,095 | 61,133 | |||||||

| Total production costs | $ | 1,247,705 | $ | 1,160,355 | $ | 1,057,842 | ||||

Production costs at the LaRonde mine were $215.0 million in 2019, a 5.8% decrease compared with 2018 production costs of $228.3 million primarily due to the timing of inventory sales and the weakening of the Canadian dollar relative to the US dollar between periods. During 2019, the LaRonde mine processed an average of 5,636 tonnes of ore per day compared with 5,775 tonnes of ore per day during 2018. Production costs per tonne of C$139 were the same between 2019 and 2018. Minesite costs per tonne increased to C$125 in 2019 compared with C$119 in 2018 primarily due to increased underground costs and slightly lower throughput.

Production costs at the LZ5 mine were $41.2 million in 2019, compared to $13.0 million in 2018. The LZ5 mine achieved commercial production in June 2018; therefore, the financial results for the year ended December 31, 2019 represented the first full year of production. During 2019, the LZ5 mine processed an average of 2,384 tonnes of ore per day compared with 1,940 tonnes of ore per day during 2018. The increase in throughput between periods was primarily due to mill optimization and the partial utilization of milling facilities at the LaRonde mine. Production costs per tonne decreased to C$63 in 2019 compared with C$76 in 2018 due to higher throughput and the timing of inventory sales, partially offset by higher re-handling costs. Minesite costs per tonne decreased to C$66 in 2019 compared with C$80 in 2018 primarily due to higher throughput, partially offset by higher re-handling costs.

Production costs at the Lapa mine were $2.8 million in 2019, an 89.8% decrease compared with 2018 production costs of $27.9 million due to the cessation of mining and processing operations at the site. In 2019, only residual gold ounces that remained in inventory at the end of 2018 were recovered from the mill facility and subsequently sold.

Production costs at the Goldex mine were $82.5 million in 2019, a 5.1% increase compared with 2018 production costs of $78.5 million primarily due to an increase in underground production and maintenance costs. During 2019, the Goldex mine processed an average of 7,630 tonnes of ore per day compared with 7,192 tonnes of ore per day processed during 2018. The increase in throughput between periods was primarily due to optimization of the Rail-Veyor system during the year. Production costs and minesite costs per tonne of C$39 were the same between 2019 and 2018.

Production costs at the Meadowbank Complex were $180.8 million in 2019, a 14.3% decrease compared with 2018 production costs of $211.1 million primarily due to lower open pit mining and processing costs as the mining transitioned to the Amaruq satellite deposit, the timing of inventory sales and the weakening of the Canadian dollar relative to the US dollar, partially offset by higher re-handling costs. During 2019, the Meadowbank Complex processed an average of 7,731 tonnes of ore per day compared with 8,937 tonnes of ore per day during 2018. The decrease in throughput between periods was expected as the mine transitioned to the Amaruq satellite deposit throughout the year. Production costs per tonne increased to C$101 in 2019 compared with C$83 in 2018 primarily due to lower throughput and higher contractor, mine maintenance, re-handling and long-haul costs associated with the transportation of ore from the Amaruq satellite deposit to the

12 AGNICO EAGLE MANAGEMENT'S DISCUSSION AND ANALYSIS

Meadowbank mill. The increase in production costs per tonne was partially offset by the timing of inventory sales. Minesite costs per tonne increased to C$103 in 2019 compared with C$82 in 2018 primarily due to the factors noted above.

The Meliadine mine achieved commercial production on May 14, 2019. During 2019, the Meliadine mine processed an average of 3,346 tonnes of ore per day and incurred production costs of $142.9 million. Production costs per tonne were C$244 and minesite costs per tonne were C$246 in 2019. As 2019 was Meliadine mine's first year of production, there is no comparable period in 2018.

Attributable production costs at the Canadian Malartic mine were $208.2 million in 2019, a 4.2% increase compared with 2018 production costs of $199.8 million, primarily due to higher open pit production costs and a lower amount of stripping costs being capitalized, partially offset by lower re-handling costs and the weakening of the Canadian dollar relative to the US dollar between periods. During 2019, the Canadian Malartic mine processed an average of 57,669 tonnes of ore per day on a 100% basis compared with 56,121 tonnes of ore per day in 2018. The increase in throughput between periods was primarily due to mill optimization and the availability of additional crushed ore from the portable crusher. Production costs per tonne and minesite costs per tonne increased to C$26 in 2019 compared with C$25 in 2018 primarily due to the factors noted above, other than the impact of foreign exchange.

Production costs at the Kittila mine were $142.5 million in 2019, a 9.2% decrease compared with 2018 production costs of $157.0 million primarily due to the planned 58-day mill shutdown for autoclave relining during the year, lower re-handling costs and the weakening of the Euro relative to the US dollar, partially offset by higher contractor costs related to underground development. During 2019, the Kittila mine processed an average of 4,359 tonnes of ore per day compared with the 5,005 tonnes of ore per day during 2018. The decrease in throughput was primarily due to the planned mill shutdown as noted above. Production costs per tonne decreased to €80 in 2019 compared with €73 in 2018 primarily due to lower throughput and higher underground development costs, partially offset by lower re-handling costs. Minesite costs per tonne increased to €76 in 2019 compared with €75 in 2018 due to the factors noted above.

Production costs at the Pinos Altos mine were $130.2 million in 2019, a 5.9% decrease compared with 2018 production costs of $138.4 million primarily due to lower re-handling costs and the timing of inventory sales. During 2019, the Pinos Altos mine mill processed an average of 5,214 tonnes of ore per day compared with the 5,329 tonnes of ore per day during 2018. In 2019, approximately 103,500 tonnes of ore were stacked on the Pinos Altos mine leach pad, compared with approximately 273,000 tonnes of ore stacked in 2018. The lower number of tonnes processed at the mill and leach pad was primarily due to mine sequencing. Production costs per tonne increased to $65 in 2019 compared with $62 in 2018 due to lower throughput and slightly higher underground mining costs as the mine transitioned into a predominantly underground operation, partially offset by lower re-handling costs and the timing of inventory sales. Minesite costs per tonne increased to $66 in 2019 compared with $61 in 2018 primarily due to the factors noted above, other than the timing of inventory sales.

Production costs at the Creston Mascota mine were $35.8 million in 2019, a 3.9% decrease compared with 2018 production costs of $37.3 million primarily due to the timing of inventory sales, partially offset by an increase in open pit mining costs associated with the extension of the Bravo pit. During 2019, approximately 1,066,900 tonnes of ore were processed at the Creston Mascota mine compared with approximately 1,422,400 tonnes of ore stacked in 2018. The decrease in tonnes stacked was the result of the mine approaching the end of operations. Production costs per tonne increased to $34 in 2019 compared with $26 in 2018 primarily due to lower tonnes stacked and higher open pit mining costs, partially offset by the timing of inventory sales. Minesite costs per tonne increased to $33 in 2019 compared with $27 in 2018 primarily due to the factors noted above, other than the timing of inventory sales.

Production costs at the La India mine were $65.6 million in 2019, a 5.0% decrease compared with 2018 production costs of $69.1 million primarily due to the timing of inventory sales, partially offset by increased heap leach costs, resulting from the higher consumption of reagents and higher contractor costs to facilitate recovery of gold ounces due to higher clay content contained in the ore. During 2019, the La India mine stacked approximately 5,402,400 tonnes of ore on the leach pad compared with approximately 6,127,500 tonnes of ore stacked in 2018. The decrease in tonnes stacked was primarily due to lower crushing capacity as a result of additional maintenance required to process ore with higher clay content. Production costs per tonne increased to $12 in 2019 compared with $11 in 2018 primarily due to the factors noted above. Minesite costs per tonne increased to $13 in 2019 compared with $12 in 2018 primarily due to increased heap leach costs and lower tonnes stacked.

MANAGEMENT'S DISCUSSION AND ANALYSIS AGNICO EAGLE 13

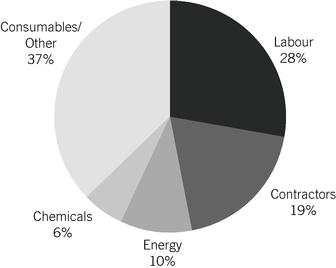

Total Production Costs by Category 2019

Total production costs per ounce of gold production, representing the weighted average of all of the Company's producing mines, increased to $735 in 2019 compared with $713 in 2018 and $621 in 2017. Total cash costs per ounce of gold produced on a by-product basis increased to $673 in 2019 compared with $637 in 2018 and $558 in 2017. Total cash costs per ounce of gold produced on a co-product basis increased to $745 in 2019 compared with $710 in 2018 and $637 in 2017. Set out below is an analysis of the change in total production costs per ounce and cash costs per ounce at each of the Company's mining operations.

- •

- At the LaRonde mine, total production costs per ounce of gold produced decreased to $627 in 2019 compared with $664 in 2018 primarily due to the timing of inventory sales. Total cash costs per ounce of gold produced on a by-product basis increased to $464 in 2019 compared with $445 in 2018 primarily due to an increase in treatment and refining fees associated with the processing of zinc concentrate. Total cash costs per ounce of gold produced on a co-product basis increased to $660 in 2019 compared with $634 in 2018 due to the factors noted above.

- •