Table of Contents

As filed with the Securities and Exchange Commission on June 22, 2005

Registration No. 333-124201

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

FORM S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

COMTECH GROUP, INC.

(Exact Name of Registrant as Specified in its Charter)

| Maryland | 3670 | 52-0466460 | ||

(State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (IRS Employer Identification Number) |

Suite 1001, Tower C, Skyworth Building

High-Tech Industrial Park

Nanshan, Shenzhen 518057

People’s Republic of China

011-86-755-2674-3210

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Jeffrey Kang

Chief Executive Officer

Suite 1001, Tower C, Skyworth Building

High-Tech Industrial Park

Nanshan, Shenzhen 518057

People’s Republic of China

011-86-755-2674-3210

(Name, address, including zip code, and telephone number, including area code of agent for service)

Copies to:

Greg Miao, Esq. Robert G. Wray, Esq. Skadden, Arps, Slate, Meagher & Flom LLP 30/F Lippo Centre 89 Queensway Central, Hong Kong SAR PRC

Tel: 011-852-2820-0700 Fax: 011-852-2820-0727 | Jeffrey Saper, Esq. Don Williams, Esq. Wilson Sonsini Goodrich & Rosati, P.C. 650 Page Mill Road Palo Alto, CA 94304-1050 USA

Tel: 1-650-493-9300 Fax: 1-650-493-6811 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434 under the Securities Act of 1933, please check the following box. ¨

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | Subject to Completion | June 22, 2005 |

Shares

Common Stock

We are offering shares of our common stock and the selling shareholders identified in this prospectus are offering shares of our common stock. We will not receive any proceeds from the sale of our common stock by the selling shareholders.

Our common stock is quoted on the Nasdaq National Market under the symbol “COGO.” On June 21, 2005, the last reported sale price of our common stock on the Nasdaq National Market was $6.01 per share.

Investing in our common stock involves a high degree of risk. Before buying any shares, you should read the discussion of material risks of investing in our common stock in “Risk factors” beginning on page 8 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| Per share | Total | |||

| Public offering price | $ | $ | ||

| Underwriting discounts and commissions | $ | $ | ||

| Proceeds, before expenses, to us | $ | $ | ||

| Proceeds, before expenses, to the selling shareholders | $ | $ |

The underwriters may also purchase up to an additional shares of our common stock at the public offering price, less the underwriting discounts and commissions, to cover over-allotments, if any, within 30 days of the date of this prospectus. Of these additional shares that the underwriters may purchase to cover over-allotments, if any, up to shares will be offered by us and up to shares will be offered by the selling shareholders. If the underwriters exercise this option in full, the total underwriting discounts and commissions will be $ , our total proceeds, before expenses, will be $ , and the total proceeds, before expenses, to the selling shareholders will be $ .

The underwriters are offering the common stock as set forth under “Underwriting.” Delivery of the shares will be made on or about , 2005.

UBS Investment Bank

C.E. Unterberg, Towbin

WR Hambrecht + Co

Maxim Group LLC

Table of Contents

Table of Contents

You should only rely on the information contained in this prospectus. We have not, and the underwriters have not, authorized anyone to provide you with additional information or information different from that contained in this prospectus. We are offering to sell, and seeking offers to buy, shares only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of shares of our common stock.

| 1 | ||

| 8 | ||

| 22 | ||

| 23 | ||

| 24 | ||

| 25 | ||

| 26 | ||

| 27 | ||

| 28 | ||

| 31 | ||

Management’s discussion and analysis of financial condition and results of operations | 33 | |

| 50 | ||

| 53 | ||

| 60 | ||

| 68 | ||

| 70 | ||

| 72 | ||

| 74 | ||

Certain United States federal income tax consequences to non-U.S. holders | 76 | |

| 78 | ||

| 79 | ||

| 83 | ||

| 83 | ||

| 84 | ||

| F-1 |

Table of Contents

This summary highlights selected information appearing elsewhere in this prospectus and may not contain all of the information that is important to you. This prospectus includes information about the shares of common stock we are offering as well as information regarding our business and detailed financial data. You should read this prospectus and the registration statement of which this prospectus is part in their entirety, especially the risks of investing in our common stock, which we discuss under “Risk Factors,” and our financial statements and related notes beginning on page F-1.

Unless the context requires otherwise, the words “Comtech,” “we,” “us,” “our” and “our company” refer to Comtech Group, Inc. and its subsidiaries, including its PRC operating companies.

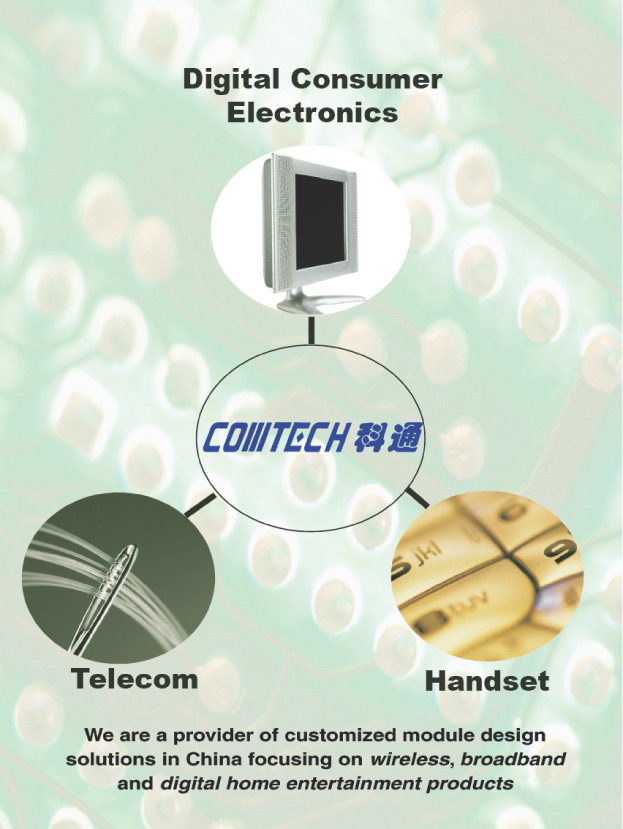

OUR BUSINESS

We are a provider of customized module design solutions in China and serve as a gateway for our suppliers to access leading electronics manufacturers in China. Our customized module design solutions allow our customers to use technology components from established suppliers in a timely and cost-effective manner, reducing their time-to-market and lowering their overall costs. Our close collaboration with our customers’ product development teams gives us an understanding of their needs, and enables us to provide customization of our suppliers’ technology components with module designs to suit each of our many customers’ specific needs.

We have historically focused on the mobile handset and telecom equipment end-markets in China, but have recently expanded our addressable market to include the digital consumer electronics end-market. Within these industries we focus on wireless, broadband and digital home entertainment products. Over the last three years, we have worked with over 200 customers, including a majority of the largest and most well-known manufacturers in the mobile handset and telecom equipment end-markets in China. In addition to these original equipment manufacturers, or OEMs, our other customers include industry participants that support these OEMs, such as subsystem designers and manufacturers. In developing customized module design solutions for use in our customers’ products, we work closely with over 30 suppliers of technology components, including many large multinational companies such as Broadcom Corporation, JDS Uniphase Corporation and Matsushita Electric Works Ltd.

Based on a given customer’s specific design requirements, we propose a customized module reference design, which typically incorporates technology components from our suppliers. If the customer accepts our design, it will generally agree to purchase from us some of the specific components contained in our proposed design. Our customers and their third-party contract manufacturers are responsible for the manufacture and assembly of the customized module design solutions based on our designs. Our business model is to generate revenue by reselling a limited number of specific components required in our module reference designs. The difference between the purchase price we pay our suppliers for these components and our sales price to our customers for these components compensates us for our design, technical support and distribution services.

From 2002 to 2004, our net revenue grew from RMB207.6 million to RMB625.7 million ($75.6 million), representing a CAGR of 73.6%, and our net income grew from RMB9.2 million to RMB62.2 million ($7.5 million) during the same period, representing a CAGR of 159.8%. For the three months ended March 31, 2005, we recorded net revenue of RMB172.0 million ($20.8 million) and net income of RMB15.8 million ($1.9 million).

1

Table of Contents

Prospectus summary

OUR INDUSTRY

China has emerged as a major participant in the global electronics market and has experienced rapid growth in domestic demand for electronics products. With increasingly advanced technology requirements within various segments of the mobile handset, telecom equipment and digital consumer electronics end-markets, manufacturers in these end-markets in China are ever more demanding for more customized module design solutions to ensure that their products can incorporate the latest technology and innovation. We believe that the development of a highly-skilled, low-cost manufacturing base has enabled China’s domestic manufacturers to be competitive in the global marketplace and has resulted in the growth of exports internationally. As a result, global technology companies are increasingly using China as a global manufacturing base for design and production, leveraging the comparative cost advantages in both product design and manufacturing. We also believe that OEMs’ greater reliance on outsourcing will continue to drive demand for customized applications of standard components, requiring more design and customization work from providers such as ourselves.

OUR COMPETITIVE STRENGTHS

We believe that our customized module design solutions allow our customers to more effectively utilize our suppliers’ technology components to more efficiently compete in their target end-markets. We believe our competitive strengths include:

| Ø | Differentiated business model. We facilitate our customers’ use of technology components in their end-products, both reducing their time-to-market and lowering their overall costs. We do not directly charge a design fee for our customized module solutions. Instead, we are compensated for the value added by our design work through a markup on the components we sell, determined principally by the extent of the design work we provide. |

| Ø | Broad and diversified customer base and deep customer relationships. Our broad and diversified customer base includes all of the major domestic mobile handset and telecom equipment manufacturers in China and many of their supporting subsystem suppliers. |

| Ø | Strong relationships with technology components suppliers. We work closely with more than 30 technology components suppliers, including some of the leading global suppliers. |

OUR STRATEGY

Our objective is to be the leading provider of customized module design solutions for customers in China’s mobile handset, telecom equipment and digital consumer electronics end-markets. To achieve this objective, we plan to execute the following key business strategies:

| Ø | Strengthen our design and development capabilities. Given the shortening product life cycles in our targeted end-markets, we believe that we must continue to build and maintain strong, in-depth and diversified solution development and design capabilities to meet the changing needs of our customers, and continue to differentiate ourselves from our competitors. |

| Ø | Leverage our strong customer relationships into new opportunities. We believe that we are well positioned to capture significant growth and higher margin opportunities in the digital consumer electronics end-market, as many of our key customers in China’s mobile handset end-market have expanded into the digital consumer electronics end-markets. |

2

Table of Contents

Prospectus summary

| Ø | Make strategic investments, acquisitions or form strategicalliances. We intend to grow and expand our business by making investments, acquisitions or forming strategic relationships with companies that possess complementary design capabilities and technology. For example, we have recently established a company, 55% owned by us, to distribute semiconductors and other products for Broadcom, a leading global producer of broadband communications semiconductors, and have recently licensed and agreed to acquire technology to apply to our newly initiated storage solutions business in China. |

RISK FACTORS

An investment in our common stock involves a high degree of risk that includes risks related to our company, the industries in which we operate, the PRC, the ownership of our common stock and this offering, including the following specific risks:

| Ø | We must continually develop new customized module design solutions that help our customers respond to competitive pressures, achieve shorter time-to-market or broaden and improve their product offerings. Once we develop our proposed customized module design solutions, there is no obligation for customers to accept our proposed reference designs. |

| Ø | Because we do not charge a design fee for our solutions, but rather generate revenue through the resale of specified components contained in our module reference designs, if our customers do not accept our module reference designs, we will not capitalize on the invested resources, time and effort that we expended on a project. |

| Ø | Our business greatly relies on the continued services of our principal shareholder and chief executive officer, Jeffrey Kang, who has been responsible for developing and maintaining many relationships with our key suppliers and customers. |

| Ø | We depend on a limited number of key customers and key suppliers, the loss of which could materially impact our business. |

| Ø | Pressure from current or future competitors could cause our module reference designs to lose acceptance by our customers or require us to significantly reduce the price of our solutions to keep existing and attract new customers. |

See “Risk factors” beginning on page 8 for a more detailed description of these and other risks related to an investment in our common stock.

OUR CORPORATE INFORMATION

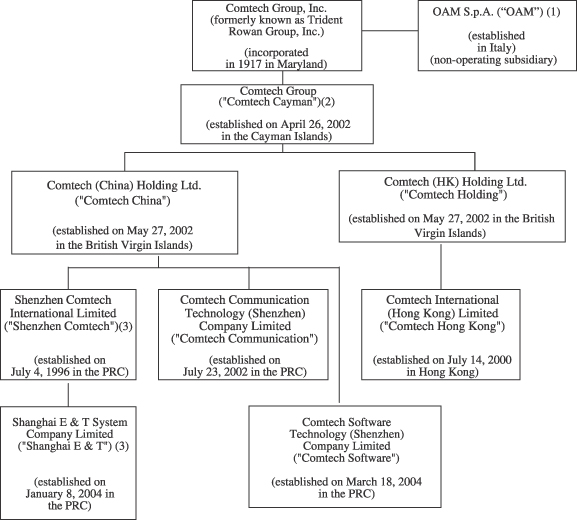

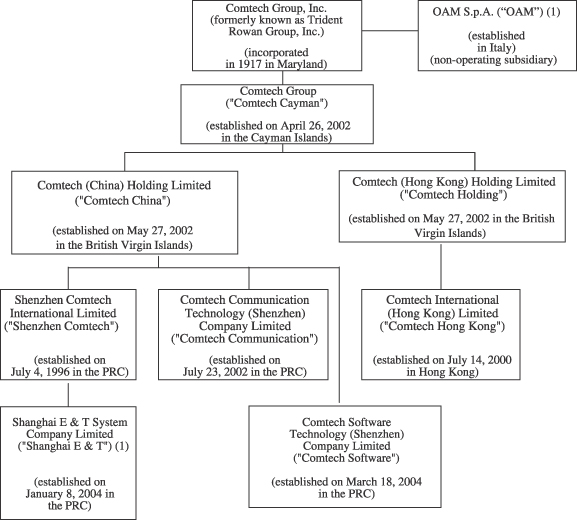

We were formerly known as Trident Rowan Group, Inc., or Trident, which was incorporated in Maryland in 1917. On July 22, 2004, Trident, which was a public reporting company that ceased operations in 2000, acquired all of the outstanding capital stock of Comtech Group, a Cayman Islands company, or Comtech Cayman, in exchange for the issuance of approximately 91.2% of the then- outstanding shares of its common stock to the shareholders of Comtech Cayman. On August 2, 2004, we changed our name from Trident to Comtech Group, Inc. For a complete description of the share exchange transaction, our corporate structure and our operating companies, see “Corporate structure.”

Our principal executive offices are located at Suite 1001, Tower C, Skyworth Building, High-Tech Industrial Park, Nanshan, Shenzhen 518057, PRC, and our telephone number is 011-86-755-2674-3210. We maintain an Internet website atwww.comtech.com.cn.We have not incorporated by reference into this prospectus the information on our website, and you should not consider it to be a part of this prospectus.

3

Table of Contents

The offering

Common stock we are offering | shares |

Common stock being offered by selling shareholders | shares |

Common stock to be outstanding after this offering | shares |

Over-allotment option | We and the selling shareholders have granted the underwriters a 30-day option to purchase up to and additional shares, respectively, to cover any over-allotments. |

Use of proceeds after expenses | We estimate that the net proceeds from this offering will be approximately $ million, or approximately $ million if the underwriters exercise their over-allotment option in full. We expect to use the net proceeds from this offering to fund possible strategic alliances or acquisitions, to expand our research and development efforts relating to new products, and for working capital and other general corporate purposes. |

Dividend policy | We do not have any present plan to pay any cash dividends on our shares of common stock in the foreseeable future. |

Nasdaq symbol | COGO |

The number of shares of our common stock outstanding immediately after the closing of this offering is based on shares of our common stock outstanding as of , 2005. The number of shares of our common stock outstanding immediately after this offering excludes:

| Ø | shares of common stock issuable upon the exercise of outstanding options and warrants to purchase our common stock, with a weighted average exercise price of per share; and |

| Ø | shares of common stock reserved for issuance under our 2004 Incentive Stock Option Plan. |

4

Table of Contents

Conventions that apply to this prospectus

Unless otherwise indicated, references in this prospectus to:

| Ø | “CAGR” are to the compound annual growth rate; |

| Ø | “China” or the “PRC” are to the People’s Republic of China, including for the purpose of this prospectus Hong Kong, but excluding Macau and Taiwan; |

| Ø | “Nasdaq” is to the Nasdaq National Stock Market, Inc.; |

| Ø | “RMB” are to Renminbi, the legal currency of China; |

| Ø | “shares” are to our shares of common stock, with par value $0.01 per share; |

| Ø | “U.S. GAAP” are to generally accepted accounting principles in the United States; |

| Ø | “$” are to U.S. dollars, the legal currency of the United States; and |

| Ø | “Comtech”, “we”, “us”, “our” and “our company” are to Comtech Group, Inc. and its subsidiaries, including its PRC operating companies. |

Unless otherwise indicated, all information in this prospectus:

| Ø | assumes that the underwriters do not exercise their option to purchase up to additional shares of our common stock from us and the selling shareholders to cover over-allotments, if any; and |

| Ø | gives effect to the one-for-two reverse stock split of our common stock completed on January 14, 2005. |

Solely for your convenience, this prospectus contains translations of certain Renminbi amounts into U.S. dollars at specified rates. All translations from Renminbi to U.S. dollars are made (unless otherwise indicated) at the rate of RMB8.2765 per $1.00, the noon buying rate in effect on March 31, 2005. No representation is made that the Renminbi or U.S. dollars amounts referred to in this prospectus could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all.

5

Table of Contents

Summary consolidated financial data

The following summary consolidated statement of operations data for the three years ended December 31, 2004 and the consolidated balance sheet data as of December 31, 2004, 2003 and 2002, presented below are derived from our audited consolidated financial statements and related notes thereto, which for the three years ended December 31, 2004 have been included elsewhere in this prospectus. These audited consolidated financial statements and the related notes have been prepared in accordance with U.S. GAAP, and have been audited by Deloitte Touche Tohmatsu, an independent registered public accounting firm.

The consolidated statement of operations data for the three months ended March 31, 2005 and 2004, and the consolidated balance sheet as of March 31, 2005, are derived from our unaudited condensed consolidated financial statements and related notes which have been included elsewhere in this prospectus. These unaudited condensed consolidated financial statements have been prepared in accordance with U.S. GAAP. We have prepared the unaudited condensed consolidated financial statements on the same basis as the audited consolidated financial statements, and have included in our opinion, all adjustments, consisting only of normal and recurring adjustments, that we consider necessary for a fair presentation of the financial information set forth in those statements. Our historical results for any prior or interim period are not necessarily indicative of results to be expected for a full fiscal year or for any future period.

The consolidated financial statements are reported in Renminbi because all of our material operating entities are based in and operated entirely within the PRC. Renminbi and U.S. dollar amounts are presented in thousands, except share and per share data. This data should be read in conjunction with our “Management’s discussion and analysis of financial condition and results of operations” and our audited consolidated financial statements and the related notes included elsewhere in this prospectus.

6

Table of Contents

Summary consolidated financial data

Consolidated Statement of Operations Data:

| Three months ended March 31, | Year ended December 31, | |||||||||||||||||||||||||||

| 2005 | 2005 | 2004 | 2004 | 2004 | 2003 | 2002 | ||||||||||||||||||||||

| (in thousands, except share and per share data) | ||||||||||||||||||||||||||||

Net revenue | $ | 20,782 | RMB | 172,001 | RMB | 153,754 | $ | 75,594 | RM | B625,656 | RMB | 357,805 | RMB | 207,607 | ||||||||||||||

Cost of revenue | (17,606 | ) | (145,716 | ) | (130,092 | ) | (64,133 | ) | (530,800 | ) | (306,939 | ) | (190,265 | ) | ||||||||||||||

Gross profit | 3,176 | 26,285 | 23,662 | 11,461 | 94,856 | 50,866 | 17,342 | |||||||||||||||||||||

Selling, research and development, general and administrative expenses | (953 | ) | (7,894 | ) | (3,329 | ) | (3,289 | ) | (27,213 | ) | (20,341 | ) | (7,461 | ) | ||||||||||||||

Other operating income | 134 | 1,110 | — | — | ||||||||||||||||||||||||

Income from operations | 2,223 | 18,391 | 20,333 | 8,306 | 68,753 | 30,525 | 9,881 | |||||||||||||||||||||

Interest expense | (47 | ) | (393 | ) | (322 | ) | (260 | ) | (2,156 | ) | (801 | ) | — | |||||||||||||||

Interest income | 3 | 29 | 11 | 5 | 38 | 54 | 157 | |||||||||||||||||||||

Income before income tax | 2,179 | 18,027 | 20,022 | 8,051 | 66,635 | 29,778 | 10,038 | |||||||||||||||||||||

Income tax | (180 | ) | (1,487 | ) | (465 | ) | (278 | ) | (2,300 | ) | (1,295 | ) | (820 | ) | ||||||||||||||

Net income before minority interest | 1,999 | 16,540 | 19,557 | 7,773 | 64,335 | 28,483 | 9,218 | |||||||||||||||||||||

Minority interest | (88 | ) | (729 | ) | (697 | ) | (258 | ) | (2,133 | ) | — | — | ||||||||||||||||

Net income | $ | 1,911 | RMB | 15,811 | RMB | 18,860 | $ | 7,515 | RMB | 62,202 | RMB | 28,483 | RMB | 9,218 | ||||||||||||||

Earnings per share | ||||||||||||||||||||||||||||

Basic | $ | 0.08 | RMB | 0.62 | RMB | 0.93 | $ | 0.35 | RMB | 2.87 | RMB | 1.41 | RMB | 0.46 | ||||||||||||||

Diluted | $ | 0.07 | RMB | 0.59 | RMB | 0.93 | $ | 0.34 | RMB | 2.84 | RMB | 1.41 | RMB | 0.46 | ||||||||||||||

Dividends declared per share | RMB | 2.04 | RMB | — | ||||||||||||||||||||||||

Weighted average number of shares outstanding | ||||||||||||||||||||||||||||

Basic | 25,381,853 | 25,381,853 | 20,251,075 | 21,690,560 | 21,690,560 | 20,251,075 | 20,251,075 | |||||||||||||||||||||

Diluted | 26,871,865 | 26,871,865 | 20,251,075 | 21,885,053 | 21,885,053 | 20,251,075 | 20,251,075 | |||||||||||||||||||||

| Consolidated Balance Sheet Data: | ||||||||||||||||||||||||||||

| As of March 31, | As of December 31, | |||||||||||||||||||||||||||

| 2005 | 2005 | 2004 | 2004 | 2003 | 2002 | |||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||||

Cash |

| $ 5,168 | RMB | 42,771 | $ | 5,007 | RMB | 41,444 | RMB | 30,683 | RMB | 12,194 | ||||||||||||||||

Trade accounts receivable, net of allowance for doubtful amounts |

| 24,350 | 201,532 | 20,418 | 168,989 | 92,259 | 67,597 | |||||||||||||||||||||

Property and equipment, net |

| 419 | 3,467 | 401 | 3,317 | 2,961 | 2,371 | |||||||||||||||||||||

Total assets |

| 38,754 | 320,748 | 37,355 | 309,167 | 160,200 | 97,072 | |||||||||||||||||||||

Total current liabilities |

| 13,906 | 115,098 | 14,372 | 118,955 | 142,546 | 66,514 | |||||||||||||||||||||

Total liabilities and minority interest |

| 14,502 | 120,031 | 14,880 | 123,159 | 142,546 | 66,514 | |||||||||||||||||||||

Total shareholders’ equity |

| 24,252 | 200,717 | 22,475 | 186,008 | 17,654 | 30,558 | |||||||||||||||||||||

7

Table of Contents

You should carefully consider the risks described below, in conjunction with other information and our consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment decision. You should pay particular attention to the fact that we conduct substantially all of our operations in China and are governed by a legal and regulatory environment that in some respects differ significantly from the environment that may prevail in other countries that you may be familiar with. Our business, financial condition or operating results could be affected materially and adversely by any or all of these risks. The trading price of our common stock could decline due to any or all of these risks, and you may lose all or part of your investment. An investment in our common stock consequently involves a high degree of risk that you should be aware of.

RISKS RELATED TO OUR BUSINESS

Our operating results fluctuate from quarter to quarter.

Our quarterly revenue, income and other operating results have fluctuated in the past and may fluctuate significantly in the future due to a number of factors, including the following:

| Ø | the ability of our suppliers to meet our supply requirements; |

| Ø | the cancellation of large orders; |

| Ø | competitive pressures; |

| Ø | the time required for research and development; |

| Ø | changing design requirements resulting from rapid technology shifts; and |

| Ø | industry trends impacting the overall market for our customers’ end-products. |

As a result of these and other factors, our results of operations may vary on a quarterly basis and net revenue may be adversely affected from period to period. For example, our net revenue relating to sales of our mobile handset solutions was adversely affected in the third and fourth quarters of 2004 due to excess inventory held by our customers during those periods, which was a result of reduced demand in the mobile handset end-market. Our results of operations for a particular quarter may not be indicative of our future performance. If our operating results in a quarter fall below our expectations or the expectations of market analysts or investors, the price of our common stock is likely to decrease.

Our operating results are substantially dependent on development of new customized module design solutions.

We may be unable to develop new customized module design solutions in a timely or cost-efficient manner, and these new solutions may fail to meet the requirements of our customers’ end-markets. If we fail to develop new solutions that help our customers respond to competitive pressures, achieve shorter time-to-market or broaden and improve their product offerings, we will lose business and our results of operations will be materially and adversely affected.

8

Table of Contents

Risk factors

If our customers do not accept our proposed customized module design solutions or do not purchase from us the specified components contained in the proposed module reference design, our net revenue will be adversely affected.

While approximately 50% of our proposed customized module design solutions are accepted by our customers, there is no obligation for customers to accept our proposed solutions. We dedicate personnel, management and financial resources to research and development and technical support in developing new customized module design solutions for our customers. The time frames for most research and development projects typically range from two to 18 months. Because we do not charge a design fee for our services, but rather generate revenue through the resale of specified components contained in our proposed reference designs, if our customers do not accept our proposed designs, we will fail to capitalize on the invested resources, time and effort that we expended on a project.

Furthermore, our customers typically make purchases on a purchase order basis. Prior to submission of a purchase order, our customers are not obligated to purchase from us any quantity of specific components that we propose to sell in our proposed module reference design. Our customers may cancel or defer their purchase orders on short notice without significant penalty. Even if a customer accepts our proposed module reference design, the customer could bypass us and contract with our competitors or possibly our suppliers directly for the purchase of the specific components we otherwise had proposed to sell. The failure to accept our proposed module reference design, the loss of ongoing business from our customers or the transition away from us in favor of direct purchases from our competitors or suppliers could each result in our failure to realize potentially significant net revenue.

Reliance on our suppliers, with whom we often do not have long-term supply agreements, makes us vulnerable to the loss of one or more key suppliers or the delivery capabilities of our suppliers.

We typically rely on a limited number of key suppliers, and many customized module design solutions that we develop are designed around technology components provided by our suppliers. We typically do not have long-term supply agreements or other forms of exclusive arrangements with our suppliers. In 2004, for example, Matsushita Electric Works, Ltd. and its affiliated entities, or Matsushita, and JDS Uniphase Corp. accounted for approximately 52% and 24%, respectively, of our cost of revenue. Furthermore, although we deal with approximately ten different divisions within Matsushita, purchases of relays and connectors from Matsushita accounted for a substantial portion of our cost of revenue attributable to Matsushita. If we lose a key supplier or a supplier reduces the quantity of products it sells to us, does not maintain a sufficient inventory level of products required by us or is otherwise unable to meet our demand for its components, we may have to expend significant time, effort and other resources to locate a suitable alternative supplier and secure replacement components. For example, when a key supplier recently relocated its production facilities, interruption in its production capacity resulted in its inability to meet our quarterly supply requirements. If suitable replacement components are unavailable, we may be forced to redevelop certain of our solutions, which ultimately may not be accepted by our customers.

Also, if our suppliers fail to introduce new products that keep up with new technologies, they may be surpassed by other suppliers entering the market with whom we may not have existing relationships. The costs and delays related to finding new suppliers or redeveloping solutions could significantly harm our business.

9

Table of Contents

Risk factors

If we fail to attract and retain key personnel, particularly our chief executive officer, our business will be materially impaired and our financial condition and results of operations will suffer.

Our business greatly relies on the continued services of Jeffrey Kang, our principal shareholder and chief executive officer. Many relationships with our key suppliers and key customers have been developed by and continue to be maintained by Mr. Kang. Our future success will depend to a significant degree upon the performance and contribution of Mr. Kang and other members of our senior management team in areas including sales, research and development, information technology and finance. Therefore, our business and results of operations may be materially and adversely affected if Mr. Kang or another member of our senior management team leaves us, which they may do at any time since, as with the exception of our chief financial officer, they do not have an employment or non-compete agreement with us. In addition, we will incur additional expenses to recruit and develop senior management members if one or more of our key employees is unwilling or unable to continue his or her employment with us. We do not maintain key man life insurance covering our senior management or any of our key employees.

Our future success also depends on our ability to identify, attract, hire, train, retain and motivate highly-skilled personnel. If we cannot attract and retain the personnel we require at a reasonable cost, our cost of revenue will increase and the profitability of our business could be negatively affected. Our business is especially dependent on sales, marketing and research and development personnel. Competition in China for executive-level and skilled technical and sales and marketing personnel is strong, and recruiting, training, and retaining qualified key personnel are important factors affecting our ability to meet our growth objectives. Should key employees leave our company, we may lose both an important internal asset and net revenue from customer projects in which those employees were involved.

Loss of key customers may adversely impact our net revenue.

We generate the majority of our net revenue from a small number of key customers, and we anticipate that a small number of key customers will continue to account for a significant portion of our net revenue in the foreseeable future, particularly in the telecom equipment segment. In 2004, our sales to ZTE, UTStarcom and Huawei accounted for approximately 13%, 12% and 11%, respectively, of our net revenue, although sales to UTStarcom fell substantially in the first quarter of 2005 compared to the fourth quarter of 2004, as for some of our module design solutions, our existing component suppliers were unable to produce on a timely basis the components needed to meet the more advanced technological specifications of UTStarcom. Sales to our top 10 customers represented approximately 58% of our net revenue in 2004. Should we lose, receive reduced orders from, or experience any adverse change in our relationship with any of our key customers, we will suffer a substantial loss in net revenue.

The end-markets in which we operate are highly competitive and fragmented. We expect competition to intensify in the future, and if we fail to compete effectively, our business will be harmed.

Pressures from current or future competitors could cause our solutions to lose market acceptance or require us to significantly reduce our sales prices to keep and attract customers. Our competitors often have longer operating histories, stronger customer and supplier relationships, larger technical staffs and sales forces, and/or greater financial, technical and marketing resources than we do. Although we believe that there are no direct competitors of any meaningful size who operate using the same business model as ours, we face indirect competition from:

| Ø | Other technology component suppliers. For each project, we work with one enabling technology component supplier to compete against other enabling technology component suppliers. Consequently, we indirectly compete against our suppliers’ competitors. For example, by working with JDS Uniphase, we compete against companies such as Avanex Corp. and Bookham Inc. in supplying optical transmission module design solutions. |

10

Table of Contents

Risk factors

| Ø | Component manufacturers and distributors. We compete indirectly with component manufacturers such as Vishay Intertechnology and Epcos AG, and component distributors such as Arrow Electronics, Inc., Avnet Inc. and Memec Inc., which may seek to expand their product/service offerings to include customized module design solutions. |

We may also face indirect competition from customers and suppliers. Currently many of our customers and suppliers do not focus on customized module design. If our customers or suppliers decide to devote more time and resources to in-house module design, the demand for our solutions may decline. In addition, our customers may change their procurement strategy or decide to rely on us primarily for component delivery and not for integration or design work. Similarly, component suppliers may also seek to offer their component products or modules incorporating key components from our solutions directly to our customers. The loss of customers for our customized module design solutions as a result of these competitive factors would have a material adverse effect on our business, financial condition and results of operations.

As we expand our business, we intend to develop new customized module design solutions and technological capabilities in end-markets where we do not currently have extensive experience or technological capability. Failure to develop or execute this growth strategy will have a material adverse effect on our net revenue.

Historically we have derived substantially all of our net revenue from our customized module design solutions provided to customers in the mobile handset and telecom equipment end-markets. We recently began targeting the digital consumer electronics and storage solution end-markets in which we have not had extensive experience or developed significant technological capability to date. In particular, we have not had any prior experience or technological capability in the storage solutions end-market. Over time, we hope to develop our integrated circuit and application software design capabilities and provide solutions based on our own proprietary technology, primarily for Internet protocol television, or IPTV, set-top boxes and digital televisions, or DTV. Our success in the digital consumer electronics end-market will depend, in significant part, on our ability to develop the necessary technological capability and to leverage our existing customer base that has expanded into this end-market. We expect to incur significant research and development expenses, through hiring additional engineering personnel to develop new solutions and expanding our intellectual property capabilities. If we are unable to quickly develop technological expertise, increase our research and development capabilities and leverage our customer base as anticipated, our return on our investment with respect to these efforts may be lower than anticipated and our operating results may suffer. Moreover, market acceptance of our customers’ new digital consumer electronics products, such as IPTV set-top boxes and DTV, is unproven, and our new markets for digital consumer electronics and storage solutions may not develop as anticipated, or at all. Finally, our customer base may not respond to our efforts to expand our proprietary capabilities and may be unwilling to utilize these enhanced capabilities.

We may be unable to manage rapid growth and a changing operating environment, which could adversely affect our ability to serve our customers and harm our business.

We have experienced rapid growth over the last five years, with our net revenue increasing from RMB55.9 million in 2000 to RMB625.7 million ($75.6 million) in 2004. Over the same period, our number of employees has also increased from approximately 30 to 94. We have limited operational, administrative and financial resources, which may be inadequate to sustain our current growth rate. If we are unable to manage our growth effectively, the quality of our solutions could deteriorate and our business may suffer. As our customer base increases and we enter new end-markets, such as the digital consumer electronics end-market, or as we expand our technological capabilities to include integrated circuit and application software design, we will need to:

| Ø | increase our investments in personnel, research and development capabilities, facilities and other operational areas; |

11

Table of Contents

Risk factors

| Ø | continue training, motivating and retaining our existing employees, and attract and integrate new qualified employees; |

| Ø | develop and improve our operational, financial, accounting and other internal systems and controls; and |

| Ø | take enhanced measures to protect any proprietary technology or technological capability we develop. |

Any failure to manage our growth successfully could distract management’s attention and result in our failure to serve our customers and harm our business.

We may not have sufficient funds to pay our accounts payable when due, which could adversely affect our operations and net revenue.

We experience a time lag in our accounts payable and accounts receivable cycles. Consequently, we may experience periods during which our cash from operations is insufficient to fund our working capital requirements. We have historically funded our working capital requirements through cash on hand, operating cash flows, as well as short-term credit facilities, factoring arrangements and loans from our principal shareholder and chief executive officer, Jeffrey Kang, and his affiliated companies. As we grow and our working capital requirements increase, these facilities may not be sufficient to meet our needs. We may be unable to maintain these liquidity sources or obtain additional liquidity sources on commercially reasonable terms to meet our increased funding requirements. For additional details regarding our working capital needs and arrangements, please see “Management’s discussion and analysis of financial condition and results of operations—Liquidity and Capital Resources.”

We generally cannot replace a supplier without the need to redevelop the modules that incorporate its components, and in doing so, we would incur significant expenses and consume additional development time. If we do not have sufficient working capital to pay our suppliers on a timely basis, we may be unable to grow our business, and our suppliers may reduce the quantity of components they supply or may no longer sell components to us, either of which would have a material adverse effect on our net revenue and results of operations.

We face risks associated with future investments or acquisitions.

An important component of our growth strategy is to invest in or acquire companies that possess complementary design capabilities and technologies. We may be unable to identify suitable investment or acquisition candidates or to make these investments or acquisitions on a commercially reasonable basis, if at all. If we complete an investment or acquisition, we may not realize the anticipated benefits from the transaction.

Integrating an acquired company or technology is complex, distracting and time consuming, as well as a potentially expensive process. The successful integration of an acquisition would require us to:

| Ø | integrate and retain key management, sales, research and development, and other personnel; |

| Ø | incorporate the acquired products or capabilities into our offerings both from an engineering and sales and marketing perspective; |

| Ø | coordinate research and development efforts; |

| Ø | integrate and support pre-existing supplier, distribution and customer relationships; and |

| Ø | consolidate duplicate facilities and functions and combine back office accounting, order processing and support functions. |

12

Table of Contents

Risk factors

The geographic distance between the companies, the complexity of the technologies and operations being integrated and the disparate corporate cultures being combined may increase the difficulties of combining an acquired company or technology. Acquired businesses are likely to have different standards, controls, contracts, procedures and policies, making it more difficult to implement and harmonize company-wide financial, accounting, billing, information and other systems. Management’s focus on integrating operations may distract attention from our day-to-day business and may disrupt key research and development, marketing or sales efforts.

Our acquisition strategy also depends on our ability to obtain necessary government approvals that may be required, as described under “—Risks Related to Doing Business in China—Our acquisition strategy depends on government regulatory approvals in China.”

The unauthorized use of our module design solutions could have a material adverse impact on our net revenue.

Our in-house design engineering teams develop our customized module design solutions. We typically do not have patent or other intellectual property protection for our solutions, nor do we typically have non-disclosure or confidentiality agreements with most of our suppliers or customers to keep our design specifications confidential. Suppliers or other competitors may attempt to circumvent us by selling products or providing module design solutions directly to our customers.

A component of our growth strategy is to begin to develop proprietary solutions in-house, specifically integrated circuits and application software design, and to make strategic investments in, form strategic alliances with or acquire, companies that possess complementary design capabilities and technology. Therefore, we expect that proprietary intellectual property will become increasingly important to our business. The unauthorized use by our suppliers or other competitors of our module design solution specifications or other intellectual property in the future would result in a substantial loss of our net revenue. The validity, enforceability and scope of protection of intellectual property in China is uncertain and still evolving, and PRC laws may not protect intellectual property rights to the same extent as the laws of some other jurisdictions, such as the United States. Moreover, litigation may be necessary in the future to enforce any intellectual property rights we may establish or acquire in the future, which could result in substantial costs and diversion of our resources, and have a material adverse effect on our business, financial condition and results of operations.

We became a public company through a share exchange with a non-operating public shell company, where we were the accounting acquirer and assumed all known and unknown potential liabilities of our predecessor entity.

Our July 2004 share exchange with Trident, as described more fully under “Corporate structure” was accounted for as a reverse merger in which Comtech Cayman was deemed the accounting acquirer and Trident, which was originally incorporated in 1917, was the legal acquirer. We have retained all the known and unknown liabilities of Trident. In addition to the threatened litigation discussed under “Our business—Legal Proceedings”, we cannot guarantee that other potential liability will not come to our knowledge in the future.

13

Table of Contents

Risk factors

We depend upon contractual agreements with the two shareholders of Shenzhen Comtech in conducting our business through Shenzhen Comtech and Shanghai E&T and receiving payments, which may not be as effective in providing operational control as direct ownership and may be difficult to enforce. Further, if the PRC government finds these contractual agreements violate or conflict with PRC governmental regulations, our business would be materially adversely affected.

At the time of the incorporation of Shenzhen Comtech, foreign shareholding in a trading business such as ours could not exceed 65%. With subsequent PRC deregulation, foreign shareholding in a trading business can now reach 100%. However, general trading with foreign investments is still restricted, requiring special approval, which is difficult to obtain. Because foreign investments in general trading businesses such as Shenzhen Comtech’s are restricted in the PRC, in order to exercise control over Shenzhen Comtech and Shanghai E&T without direct shareholding by our offshore entities, our principal shareholder and chief executive officer, Jeffery Kang and his wife own through contractual agreements and for the benefit of our 100% directly owned subsidiary, Comtech China, all of the equity interest in our PRC operating company, Shenzhen Comtech, which, in turn, owns 60% equity interest in another of our PRC operating companies, Shanghai E&T. While we do not have any equity interest in Shenzhen Comtech, through these contractual agreements, we enjoy voting control and are entitled to the economic interests associated with Jeffery Kang’s and his wife’s equity interest in Shenzhen Comtech. For additional details regarding these contractual agreements, see “Corporate structure” and “Related party transactions.” These contractual agreements may not be as effective in providing us with control over Shenzhen Comtech as direct ownership because we rely on the performance of Jeffery Kang and his wife under the agreements. If Jeffrey Kang or his wife fail to perform his or her respective obligations under the agreements, we may have to incur substantial costs and resources to enforce such agreements and may not be able to do so in any case. Also, we must rely on legal remedies under applicable law, which may not be as effective as those in the United States. Because we rely on Shenzhen Comtech and Shanghai E&T in conducting our business operations in China, the realization of any of these risks relating to our corporate structure could result in a material disruption of our business, diversion of our resources and the incurrence of substantial costs, any of which could materially and adversely affect our operating results and financial condition.

In the opinion of our PRC counsel, Grandall Legal Group, the ownership structure of Shenzhen Comtech and the contractual agreements among Comtech China, Mr. Kang and his wife do not violate existing PRC laws, rules and regulations. There are, however, substantial uncertainties regarding the interpretation and application of current or future PRC laws and regulations, including but not limited to the laws and regulations governing the validity and enforcement of these contractual agreements. In particular, this type of contractual agreement is not commonly seen in China and accordingly, we cannot assure you that PRC regulatory authorities will not determine that these contractual agreements with Jeffrey Kang and his wife violate or conflict with PRC laws or regulations, including those regarding restrictions on foreign investments in trading businesses.

If we or our PRC operating company, Shenzhen Comtech, are found to violate any existing or future PRC laws or regulations, the relevant regulatory authorities will have broad discretion in dealing with such violation, which would cause significant disruptions to our business operations or render us unable to conduct our business operations and may materially adversely affect our business, financial condition and results of operations.

RISKS RELATED TO OUR INDUSTRY

Historically, we have focused on the mobile handset and telecom equipment end-markets in China, but recently expanded our focus to include the digital consumer electronics end-market in China. We currently do not derive a significant portion of our net revenue from the consumer electronics end-market.

14

Table of Contents

Risk factors

Our inability to respond quickly and effectively to rapid technological advances and market demands would adversely impact our competitive position and our results of operations.

The mobile handset and telecom equipment end-markets are characterized by rapid technological advances, intense competition, frequent introduction of new products and services and consumer demand for greater functionality, lower costs, smaller products and better performance. We must constantly seek out new products and develop new solutions to maintain in our portfolio. We have experienced and will continue to experience some solution design obsolescence. We expect our customers’ demands for improvements in product performance to increase, which means that we must continue to improve our design solutions and develop new solutions to remain competitive and grow our business. Our failure to compete successfully for customers will result in price reductions, reduced margins or loss of market share, any of which would harm our business, results of operations and financial condition.

Substantially all of our net revenue currently comes from sales to manufacturers in the highly cyclical mobile handset and telecom equipment end-markets, and cyclical downturns could harm our operating results.

The mobile handset and telecom equipment end-markets are highly cyclical and have experienced severe and prolonged downturns, often in connection with maturing product cycles and declines in general economic conditions. These downturns have been characterized by diminished product demand, production overcapacity, high inventory levels and accelerated erosion of average selling prices. For example, during the second half of 2004, our net revenue relating to sales in the mobile handset end-market was adversely affected due to excess inventory being held by our customers during the period, which was a result of reduced demand in the mobile handset end-market. The impact of slowing end-customer demand was compounded by higher than normal levels of equipment and inventories among our customers and our customers’ adjustments in their order levels, resulting in increased pricing pressure.

In addition, our recent and significant growth in net revenue resulted, in large part, from the high growth in sales of products manufactured by domestic mobile handset and telecom equipment manufacturers in China. These domestic manufacturers may not continue to grow their sales at historical levels, if at all. The stagnation or reduction in overall demand for mobile handset and telecom equipment products would materially affect our results of operations and financial condition.

The mobile handset end-market is characterized by a short product lifecycle, making time-to-market and sensitivity to customer needs critical to our success and our failure to respond will harm our business.

Mobile handsets typically have a lifecycle of approximately six months before the technology becomes obsolete. Time-to-market, both with respect to our customers’ ability to supply consumers with timely and marketable products and our ability to provide our customers with a wide array of latest generation customized module design solutions, is critical to our success. As design cycles in the industry shorten, we face logistical challenges in providing our solutions in an increasingly shorter timeframe. If we are unable to respond to the shortened lifecycles and time-to-market, our business will suffer.

RISKS RELATED TO DOING BUSINESS IN CHINA

There are substantial risks associated with doing business in China, including those set forth in the following risk factors.

15

Table of Contents

Risk factors

Our operations may be adversely affected by China’s economic, political and social conditions.

Substantially all of our operations and assets are located in China and substantially all of our net revenue derived from our operations in China. Accordingly, our results of operations and future prospects are subject to economic, political and social developments in China. In particular, our results of operations may be adversely affected by:

| Ø | changes in China’s political, economic and social conditions; |

| Ø | changes in policies of the government or changes in laws and regulations, or the interpretation of laws and regulations; |

| Ø | changes in foreign exchange regulations; |

| Ø | measures that may be introduced to control inflation, such as interest rate increases; and |

| Ø | changes in the rate or method of taxation. |

The PRC economy has historically been a planned economy. The majority of productive assets in China are still owned by various levels of the PRC government. In recent years the government has implemented economic reform measures emphasizing decentralization, utilization of market forces in the development of the economy and a high level of management autonomy. Such economic reform measures may be inconsistent or ineffectual, and we may not benefit from all such reforms. Furthermore, these measures may be adjusted or modified, possibly resulting in such economic liberalization measures being applied inconsistently from industry to industry, or across different regions of the country.

In the past twenty years, China has been one of the world’s fastest growing economies in terms of gross domestic product, or GDP. This growth may not be sustainable. Moreover, a slowdown in the economies of the United States, the European Union and certain Asian countries may adversely affect economic growth in China which depends on exports to those countries. Our financial condition and results of operations, as well as our future prospects, would be materially and adversely affected by an economic downturn in China.

Our financial results benefit from tax concessions granted by the PRC government, the change to or expiration of which would materially change our results of operations.

Our results of operation may be adversely affected by changes to or expiration of preferential tax concessions that some of our PRC operating companies currently enjoy or expect to enjoy in the future. The statutory tax rate generally applicable to Chinese companies is 33%. As a result of preferential tax rate incentives, our operations have been subject to relatively low tax liabilities. Tax that would otherwise have been payable without preferential tax treatment amounted to approximately RMB19.9 million ($2.4 million), RMB10.2 million and RMB2.4 million in 2004, 2003, and 2002, respectively. For additional details regarding these tax incentives, please see “Management’s discussion and analysis of financial condition and result of operations—Taxation.”

Tax laws in China are subject to interpretations by relevant tax authorities. The preferential tax treatment may not remain in effect or may change, in which case we may be required to pay the higher income tax rate generally applicable to Chinese companies, or such other rate as is required by the laws of China.

The telecom equipment market is extensively regulated in China.

The telecom equipment end-market accounted for 39.9% of our net revenues in 2004. China’s telecom industry is heavily regulated. Changes in regulations affecting sales of these customers could negatively affect the telecom equipment end-market for our solutions, which will materially harm our business.

16

Table of Contents

Risk factors

Government control of currency conversion may affect the value of your investment.

Because the majority of our net revenue is denominated in Renminbi, any restrictions on currency exchange may limit our ability to use revenue generated in Renminbi to meet our foreign currency obligations, primarily denominated in U.S. dollars. The principal regulation governing foreign currency exchange in China is the Foreign Currency Administration Rules (1996), or the Rules, as amended. Under the Rules, once certain procedural requirements are met, Renminbi is convertible for current account transactions, including trade and service-related foreign exchange transactions and dividend payments, but not for capital account transactions, including direct investment, loans or investments in securities outside China, without prior approval of the State Administration of Foreign Exchange of the People’s Republic of China, or its local counter-parts. Since a significant amount of our future revenues will continue to be denominated in Renminbi, any existing and future restrictions on currency exchange may limit our ability to utilize revenue generated to fund our business activities outside of China, if any, or expenditures denominated in foreign currencies, or our ability to meet our foreign currency obligations, which could have a material adverse effect on our business, financial condition and results of operations. We cannot be certain that the PRC regulatory authorities will not impose more stringent restrictions on the convertibility of Renminbi with respect to foreign exchange transactions.

Our acquisition strategy depends on government regulatory approvals in China.

Regulations were recently promulgated by State Development and Reform Commission, or SDRC, and the State Administration of Foreign Exchange, or SAFE, that require registration with, and approval from, PRC government authorities in connection with direct or indirect offshore investment activities by individuals who are PRC residents and PRC corporate entities. These regulations may apply to our future offshore or cross-border acquisitions, as well as to the equity interests in offshore companies held by our PRC shareholders who are considered PRC residents. We intend to make all required application and filings, and will require the shareholders of the offshore entities in our corporate group who are considered PRC residents to make the application and filings, as required under these regulations and under any implementing rules or approval practices that may be established under these regulations. However, because these regulations are relatively new and lacking implementing rules or reconciliation with other approval requirements, it remains uncertain how these regulations, and any future legislation concerning offshore or cross-border transactions, will be interpreted and implemented by the relevant government authorities. The approval criteria by SDRC agencies for outbound investment by PRC residents are not provided under the relevant SDRC regulations. Also, the criteria for registration with SAFE agencies, and whether such registration procedure is discretionary, are still uncertain as the criteria, if any, are not provided for under relevant SDRC regulations. Furthermore, there is a lack of relevant registration precedents for us to determine the registration criteria in practice. Accordingly, we cannot provide any assurances that we will be able to, nor can we ensure that our shareholders will be considered PRC residents and they must comply with or register under the relevant regulations and that they will be able to, comply with, qualify under or obtain any registration or approval as required by these regulations or other related legislations. Our failure or the failure of our PRC resident shareholders to obtain these approvals or registrations may restrict our ability to acquire a company outside of China or use our entities outside of China to acquire or establish companies inside of China, which could negatively affect our business and future prospects.

PRC laws and our corporate structure may restrict our ability to receive dividends and payments from, and transfer funds to, our PRC operating companies, which may negatively affect our results of operations and restrict our ability to act in response to changing market conditions.

Substantially all of our operations are conducted through our PRC operating companies. The ability of our PRC operating companies to make dividend and other payments to us may be restricted by factors such as changes in applicable foreign exchange and other laws and regulations. For example, under the

17

Table of Contents

Risk factors

new SAFE regulations discussed in the previous risk factor, the foreign exchange activities of our present or prospective PRC subsidiaries are conditioned upon the compliance with the SAFE registration requirements by the shareholders of our offshore entities who are PRC residents. Failure to comply with these SAFE registration requirements may result in substantial restriction on the foreign exchange inflow to and outflow from our PRC subsidiaries, including, remittance of dividends and foreign-currency- denominated borrowings by our PRC subsidiaries. In addition, our PRC operating companies are required, where applicable, to allocate a portion of their net profit to certain funds before distributing dividends, including at least 10% of their net profit to certain reserve funds until the balance of such fund has reached 50% of their registered capital. These reserves can only be used for specific purposes, including making-up cumulative losses of previous years, conversion to equity capital, and application to business expansion, and are not distributable as dividends. Our PRC operating companies are also required, where applicable, to allocate an additional 5% to 10% of their net profits to a statutory common welfare fund. The net profit available for distribution from our PRC operating companies is determined in accordance with generally accepted accounting principles in China, which may materially differ from a determination performed in accordance with U.S. GAAP. As a result, we may not receive sufficient distributions or other payments from these entities to enable us to make dividend distributions to our shareholders in the future, even if our U.S. GAAP financial statements indicate that our operations have been profitable.

We do not directly own the equity interest in Shenzhen Comtech, which accounted for approximately 30% of our net revenue in 2004, as well as Shenzhen Comtech’s 60% owned subsidiary, Shanghai E&T, which accounted for approximately 10% of our net revenue in 2004. Our principal shareholder and chief executive officer, Jeffrey Kang, and his wife, the shareholders of Shenzhen Comtech, have contractually agreed, among others things, to apply all dividends or other payments they receive from Shenzhen Comtech to payments to our 100% directly owned subsidiary, Comtech China, or its designated entities, to the extent permitted by applicable PRC law, including PRC foreign exchange law. PRC law and regulatory requirements would currently restrict the ability of Mr. Kang and his wife, based solely upon the contractual agreements, to directly apply the dividends or other payments they receive from Shenzhen Comtech in U.S. dollars to payments to Comtech China or in Renminbi to Comtech China’s designated entities in China. If Jeffrey Kang and his wife fail to apply such dividends or other payments received from Shenzhen Comtech, which might include profit distributions from Shanghai E&T to Shenzhen Comtech, to payments to Comtech China or its designated entities, our financial condition would be negatively affected.

Apart from the dividend distribution from our PRC subsidiaries to us, the transfer of funds from our company to our PRC operating companies, either as a shareholder loan or as an increase in registered capital or otherwise, is subject to registration or approval with or by PRC governmental authorities, including the relevant administration of foreign exchange and/or other relevant examining and approval authorities. These limitations on the free flow of funds between us and our PRC operating companies may restrict our ability to act in response to changing market conditions.

Fluctuations in the value of the Renminbi relative to foreign currencies could affect our financial condition, results of operations and the price of our common stock.

The majority of our net revenue is denominated in Renminbi, while a portion of our cost of revenue is denominated in foreign currencies, primarily U.S. dollars. Since 1994, the official exchange rate of Renminbi to U.S. dollars has been based on rates set by the People’s Bank of China and generally has been stable. However, recently there has been increased political pressure on the PRC government to decouple the Renminbi from the U.S. dollar, and the PRC government may in the future relinquish the U.S. dollar peg or increase the current trading range. Future movements in the exchange rate of Renminbi and other currencies may have an adverse effect on our financial condition and results of operations. For example, a depreciation of the Renminbi relative to the U.S. dollar would have the effect

18

Table of Contents

Risk factors

of reducing our U.S. dollar-translated net revenue and increasing the debt servicing requirements for our U.S. dollar-denominated debt. On the other hand, the appreciation of the Renminbi would make our customers’ products more expensive to purchase outside of China because many of our customers are involved in the export of goods, which could adversely affect their sales, thereby eroding our customer base and adversely affecting our results of operations.

The legal system in China has inherent uncertainties that may limit the legal protections available to you as an investor or to us in the event of any claims or disputes with third parties.

The legal system in China is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. Since 1979, the central government has promulgated laws and regulations dealing with economic matters such as foreign investment, corporate organization and governance, commerce, taxation and trade. As China’s foreign investment laws and regulations are relatively new and the legal system is still evolving, the interpretation of many laws, regulations and rules is not always uniform and enforcement of these laws, regulations and rules involve uncertainties, which may limit the remedies available to you as an investor and to us in the event of any claims or disputes with third parties. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention.

You may experience difficulties in effecting service of legal process and enforcing judgments against us and our management.

Substantially all of our operations and assets are located in China. In addition, most of our directors, executive officers and some of the experts named in this document reside within China, and many of the assets of these persons are also located within China. As a result, it may not be possible to effect service of process within the United States or elsewhere outside China upon these directors or executive officers or some of the experts named in this document, including with respect to matters arising under U.S. federal securities laws or applicable state securities laws. Moreover, our PRC legal counsel, Grandall Legal Group, has advised us that China does not have treaties with the United States or many other countries providing for the reciprocal recognition and enforcement of court judgments. As a result, recognition and enforcement in China of judgments of a court of the United States or any other jurisdiction, including judgments against us or our directors, executive officers, or the named experts, may be difficult or impossible.

RISKS RELATED TO OUR COMMON STOCK

Our principal shareholder and chief executive officer and his wife together control a substantial majority of our common stock. As a result, the trading price for our shares may be depressed due to market perception, and our principal shareholder and chief executive officer will be able to take actions that may be adverse to your interests.

Jeffrey Kang, our principal shareholder and chief executive officer, and his wife, Nan Ji, directly and through entities they control, together currently beneficially own approximately 72.6% of our issued and outstanding common stock and will continue to beneficially own approximately % after this offering. This significant concentration of share ownership may adversely affect the trading price of our common stock because investors, often perceive a disadvantage in owning shares in a company with only one or very few controlling shareholders. Furthermore, Mr. Kang, and his wife, Nan Ji, together have the ability to control the outcome of all matters requiring shareholder approval, including the election of directors and approval of significant corporate transactions, such as mergers, consolidations or the sale of substantially all of our assets. This concentration of ownership may have the effect of delaying or preventing a change of control, including a merger, consolidation or other business combination involving us, or discouraging a potential acquirer from making a tender offer or otherwise attempting to obtain control, even if such a change of control would benefit you.

19

Table of Contents

Risk factors

Efforts to comply with recently enacted changes in securities laws and regulations will increase our costs and require additional management resources. Our failure to comply could adversely affect our stock price.

We have only recently begun to evaluate our internal controls over financial reporting. Given the status of our efforts, coupled with the fact that guidance from regulatory authorities in the area of internal controls continues to evolve, substantial uncertainty exists regarding our ability to comply by applicable deadlines. As directed by Section 404 of the Sarbanes-Oxley Act of 2002, public companies are required to include a report of management on the company’s internal controls over financial reporting in their annual reports on Form 10-K and the public accounting firm auditing a company’s financial statements must attest to and report on management’s assessment of the effectiveness of the company’s internal controls over financial reporting. This requirement will first apply to our annual report on Form 10-K for our fiscal year ending December 31, 2006. If we are unable to conclude that we have effective internal controls over financial reporting, or if our independent auditors are unable to provide us with an unqualified report as to the effectiveness of our internal controls over financial reporting as of December 31, 2006 and future year ends, as required by Section 404 of the Sarbanes-Oxley Act, we could experience delays or inaccuracies in our reporting of financial information, or non-compliance with SEC reporting and other regulatory requirements. This could subject us to regulatory scrutiny and result in a loss of public confidence in our management, which could, among other things, adversely affect our stock price.

Significant dilution may result from the indemnification provisions of our share exchange agreement.

The terms of the share exchange with Trident provide for the issuance of up to 30,173,047 additional shares of our common stock to the original holders of Comtech Cayman in the event there is a breach of any representations, warranties, covenants or obligations made by Trident in the share exchange agreement for an amount of damages in excess of $625,000. This indemnification provision expired on April 30, 2005, except in the case of known claims, which will survive until such matters are resolved finally by a court of law. Prior to the expiration of this period, we were notified of a possible claim relating to a transaction entered into by Trident prior to the consummation of the share exchange agreement, as discussed under “Business—Legal Proceedings” that could trigger this indemnification provision. The potential issuance of additional shares of our common stock under this indemnification provision could result in dilution to other shareholders.

RISKS RELATING TO THIS OFFERING

There has not been significant trading in our common stock, and our stock price may fluctuate dramatically in the future.

From March 1999 to January 30, 2005, our common stock was quoted on the Over-The-Counter Market, known as the “pink sheets”, or on the Electronic Bulletin Board of the Over-The-Counter Market, or OTCBB. Since January 31, 2005, our common stock has been quoted on Nasdaq under the symbol “COGO”. To date, there has been a limited trading market for our common stock. There is a significant risk that our stock price may fluctuate dramatically in the future in response to any of the following factors, some of which are beyond our control:

| Ø | variations in our quarterly operating results; |

| Ø | announcements that our net revenue or income are below research analysts’ expectations; |

| Ø | general economic slowdowns; |

20

Table of Contents

Risk factors