Exhibit 99.1

THE DIXIE GROUP

March 10, 2005

1

Forward Looking Statements

Statements in this presentation, which relate to the future, are subject to risk factors and uncertainties that could cause actual results to differ materially from those indicated in such forward-looking statements. Such factors include the levels of demand for the products produced by the Company. Other factors that could affect the Company’s results include, but are not limited to, raw material and transportation costs related to petroleum prices, the cost and availability of capital, and general economic and competitive conditions related to the Company’s business. Issues related to the availability and price of energy may adversely affect the Company’s operations. Additional information regarding these and other risk factors and uncertainties may be found in the Company’s filings with the Securities and Exchange Commission.

General information set forth in this presentation concerning market conditions, sales data and trends in the U.S carpet and rug markets are derived from various public and , in some cases, non-public sources. Although we believe such data and information to be accurate, we have not attempted to independently verify such information.

2

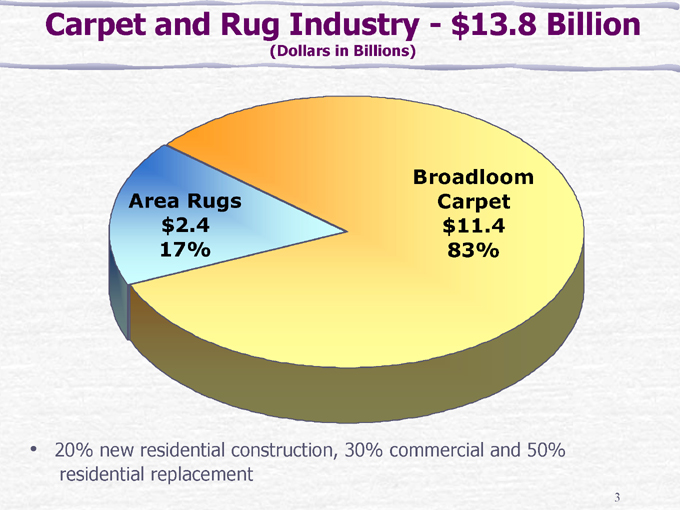

Carpet and Rug Industry—$13.8 Billion

(Dollars in Billions)

Area Rugs $2.4 17%

Broadloom Carpet $11.4 83%

20% new residential construction, 30% commercial and 50% residential replacement

3

Broadloom Carpet Not Import Sensitive

Efficient scale—U. S. has approximately 50% share of world’s broadloom carpet production

Retail placement and distribution

Service

Hundreds of SKUs and numerous colors Retailers reluctant to carry inventory 24 hr. to 48 hr. delivery expected

Labor cost content

7% to 11% of sales price

Freight cost

Carpet too bulky and heavy to ship cost effectively Shipping cost overseas can equal or exceed labor cost

Technology

4

Carpet vs. Traditional Textile Industry

20 Largest Public Textile Companies in 1980

1. Burlington (1), (3)

2. J. P. Stevens (1), (2), (3)

3. West Point (1), (3)

4. Springs (1)

5. Cone (3)

6. Cannon (2), (3)

7. UM & M (2), (3)

8. M. Lowenstein (2), (3)

9. Dan River (1), (3) 10. Collins & Aikman (1)

11. Fieldcrest (1), (2), (3)

12. Reigel (2)

13. Graniteville (2)

14. Avondale

15. Bibb (2)

16. Ti-Caro (2)

17. Guilford Mills (3)

18. Dixie Yarns (4)

19. Shaw Industries (4)

20. Mohasco (Mohawk) (4)

1 – In the carpet business at one time 2 – No longer operating as a separate entity 3 – Have gone through bankruptcy 4 – Principally in floorcovering business today

5

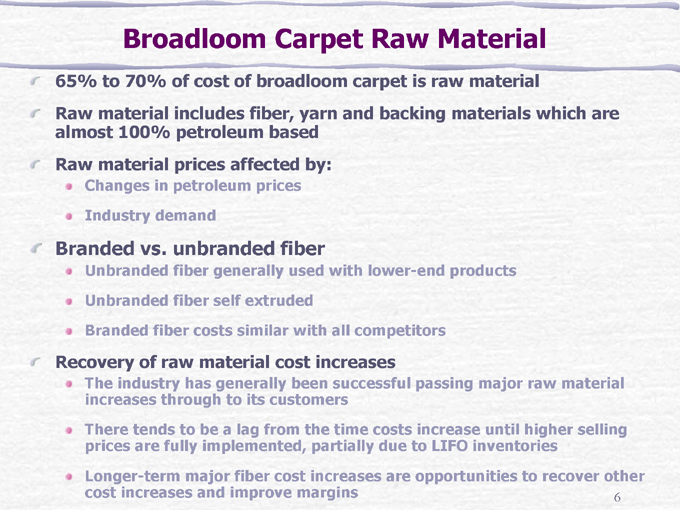

Broadloom Carpet Raw Material

65% to 70% of cost of broadloom carpet is raw material

Raw material includes fiber, yarn and backing materials which are almost 100% petroleum based Raw material prices affected by:

Changes in petroleum prices Industry demand

Branded vs. unbranded fiber

Unbranded fiber generally used with lower-end products Unbranded fiber self extruded Branded fiber costs similar with all competitors

Recovery of raw material cost increases

The industry has generally been successful passing major raw material increases through to its customers There tends to be a lag from the time costs increase until higher selling prices are fully implemented, partially due to LIFO inventories

Longer-term major fiber cost increases are opportunities to recover other cost increases and improve margins 6

Dixie Strategic Positioning

Grew floorcovering business from 1993 and exited textiles in 1999 –now 100% floorcovering

Eight acquisitions from 1993 Through 2000 Demise of factory built housing 65% Commitment to brands and upper-end market led to the sale of our North Georgia operations

7

Shaw Transaction

Sold North Georgia carpet and yarn operations to Shaw for $212 million

One-time P & L charge $16.2 million

Debt reduced $150 million

8

Dixie Today

Smaller, more profitable, growing company with strong balance sheet and strong brands in the upper-end Vastly improved risk profile

Financially Customer base

Top 20 carpet customers – 16% of total carpet sales Top 40 carpet customers – 20% of total carpet sales

High-end business (Fabrica, Masland & Dixie Home) – carpet sales growing in 2003 and 2004

11% in 2003

26% in 2004, driven by 31% residential and 15% commercial growth Dixie Home sales running at an annualized rate of over $60.0 million in 4th QT 2004 and expected to reach $100.0 million annualized run rate by 2006 Approximately half of the increases have been at Masland & Fabrica

Carpet sales for the 1st 9 weeks of 2005 up VS prior year:

Residential Carpet Sales – up 23% Commercial Carpet Sales – up 18% Total Carpet Sales – up 21%

9

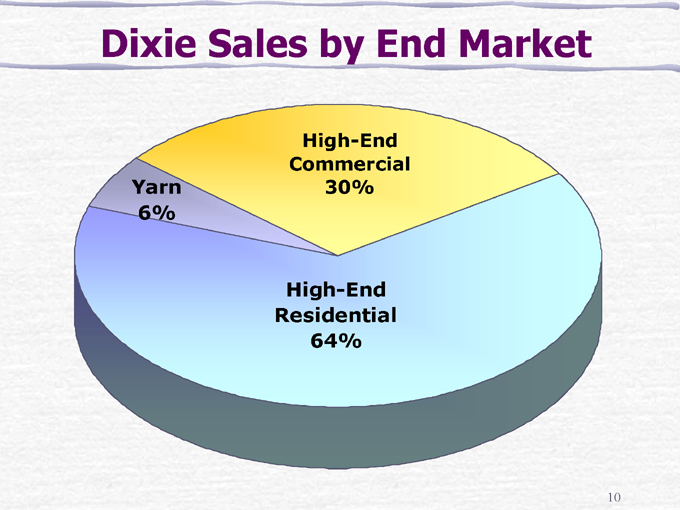

Dixie Sales by End Market

Yarn

6%

High-End Commercial

30%

High-End Residential

64%

10

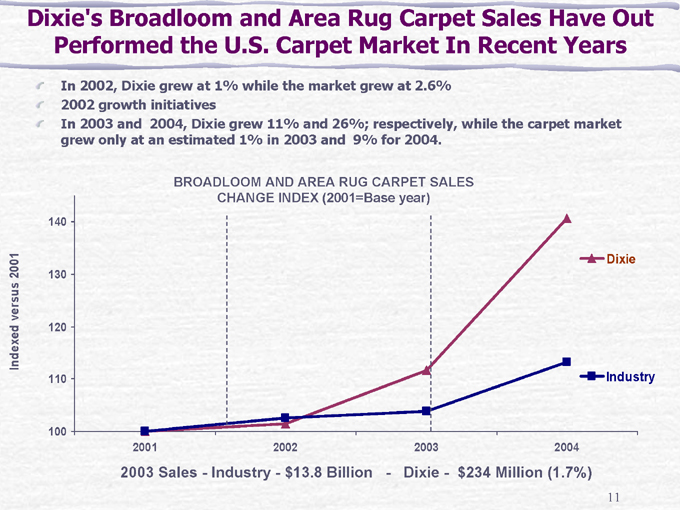

Dixie’s Broadloom and Area Rug Carpet Sales Have Out Performed the U.S. Carpet Market In Recent Years

In 2002, Dixie grew at 1% while the market grew at 2.6% 2002 growth initiatives

In 2003 and 2004, Dixie grew 11% and 26%; respectively, while the carpet market grew only at an estimated 1% in 2003 and 9% for 2004.

BROADLOOM AND AREA RUG CARPET SALES

CHANGE INDEX (2001=Base year)

Indexed versus 2001

140 130 120 110 100

2001 2002 2003 2004

Dixie

Industry

2003 Sales—Industry—$13.8 Billion—Dixie—$234 Million (1.7%)

11

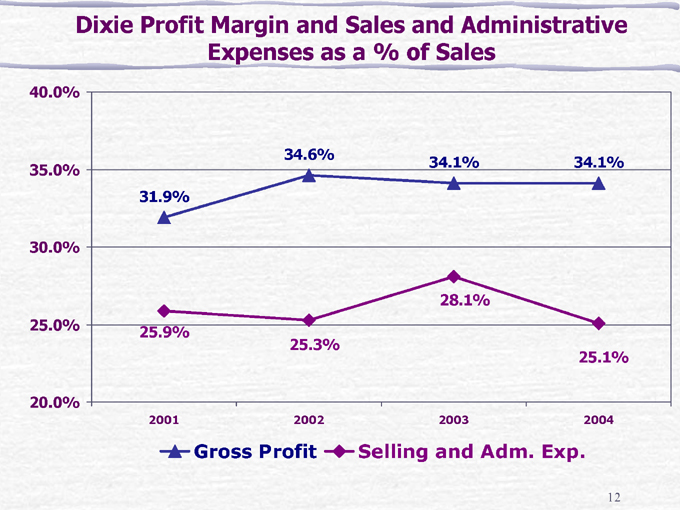

Dixie Profit Margin and Sales and Administrative Expenses as a % of Sales

40.0% 35.0% 30.0% 25.0% 20.0%

2001 2002 2003 2004

31.9%

34.6%

34.1%

34.1%

25.9%

25.3%

28.1%

25.1%

Gross Profit

Selling and Adm. Exp.

12

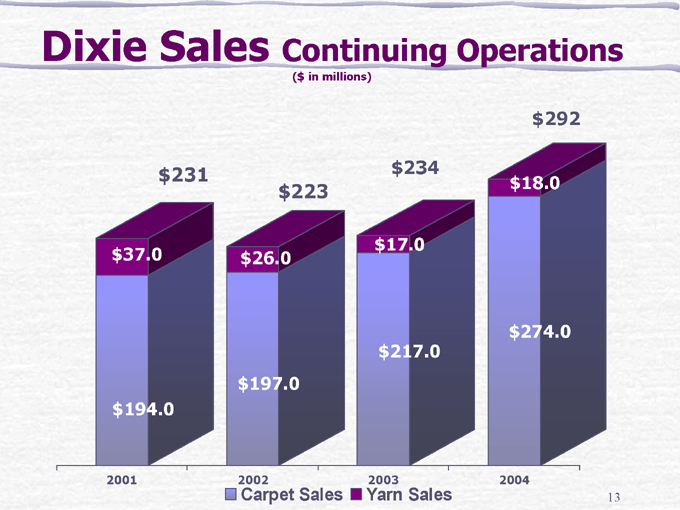

Dixie Sales Continuing Operations

($ in millions) $231 $37.0 $194.0 $223 $26.0 $197.0 $234 $17.0 $217.0 $292 $18.0 $274.0

2001 2002 2003 2004

Carpet Sales

Yarn Sales

13

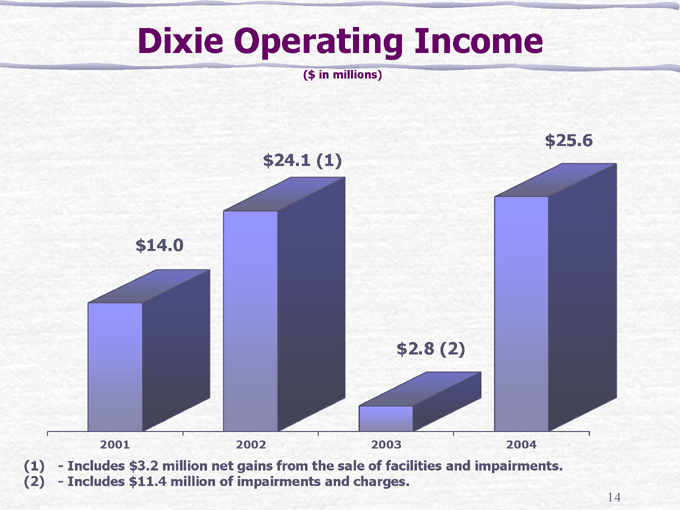

Dixie Operating Income

($ in millions) $14.0 $24.1 (1) $2.8 (2) $25.6

2001 2002 2003 2004

(1)—Includes $3.2 million net gains from the sale of facilities and impairments. (2)—Includes $11.4 million of impairments and charges.

14

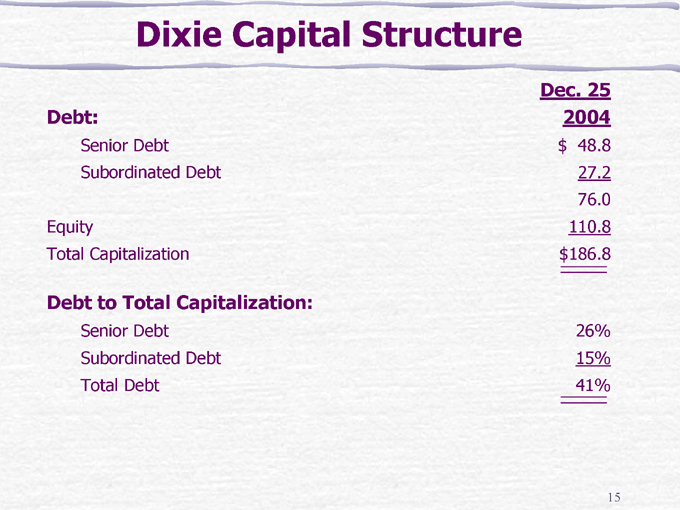

Dixie Capital Structure

Dec. 25

Debt: 2004

Senior Debt $ 48.8

Subordinated Debt 27.2

76.0

Equity 110.8

Total Capitalization $ 186.8

Debt to Total Capitalization:

Senior Debt 26%

Subordinated Debt 15%

Total Debt 41%

15

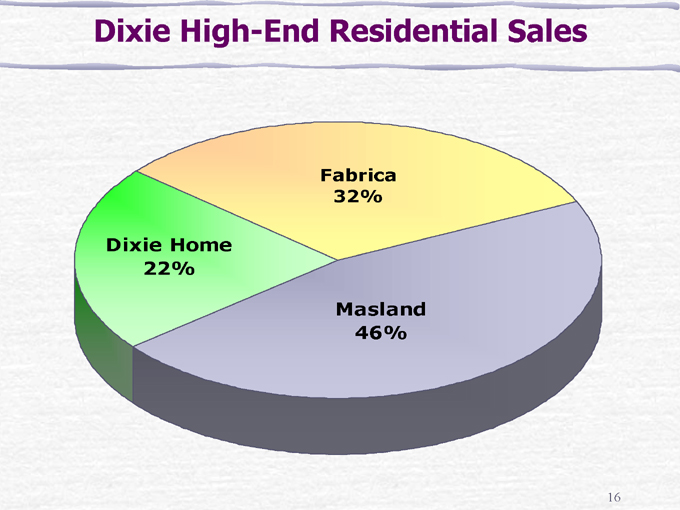

Dixie High-End Residential Sales

Dixie Home

22%

Fabrica

32%

Masland

46%

16

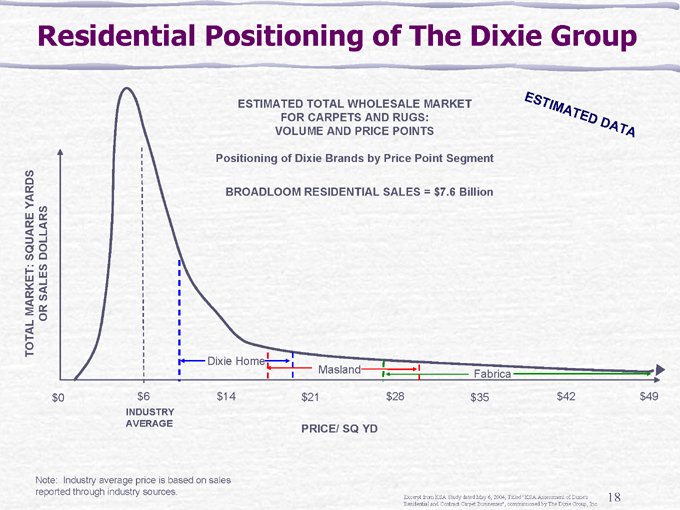

Residential Positioning

Goal is to be a highly profitable, high-styled supplier at the upper-end of the residential marketplace Retailers rate the Masland and Fabrica lines as leaders in quality, service and innovation. Together, these lines have the largest market share in the > $22 price range However, we see the $10—$20 price range having a much larger potential market that fits Dixie’s high-end strategy Our objective is to make Dixie Home the “go to” line in the $10—$20 range for styling, service and quality

17

Residential Positioning of The Dixie Group

TOTAL MARKET: SQUARE YARDS

OR SALES DOLLARS

$0$ 6 $14 $21 $28 $35 $42 $49

ESTIMATED TOTAL WHOLESALE MARKET

FOR CARPETS AND RUGS: VOLUME AND PRICE POINTS

Positioning of Dixie Brands by Price Point Segment

BROADLOOM RESIDENTIAL SALES = $7.6 Billion

ESTIMATED DATA

Dixie Home

Masland

Fabrica

INDUSTRY AVERAGE

PRICE/ SQ YD

Note: Industry average price is based on sales reported through industry sources.

Excerpt from KSA Study dated May 6, 2004, Titled “KSA Assessment of Dixie’s Residential and Contract Carpet Businesses”, commissioned by The Dixie Group, Inc.

18

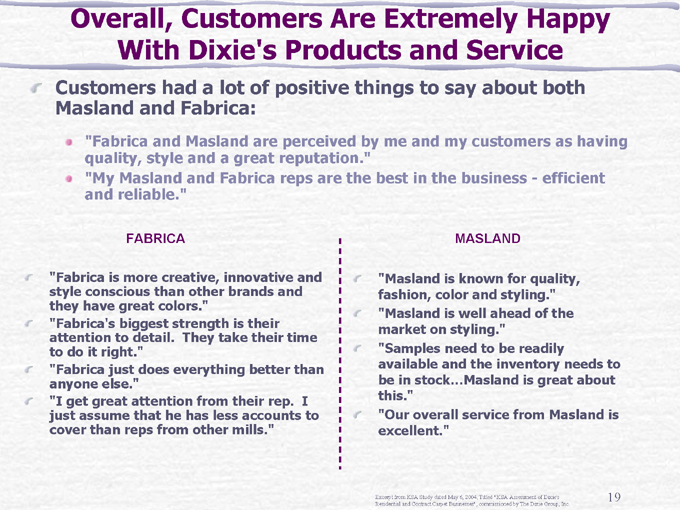

Overall, Customers Are Extremely Happy With Dixie’s Products and Service

Customers had a lot of positive things to say about both Masland and Fabrica:

“Fabrica and Masland are perceived by me and my customers as having quality, style and a great reputation.” “My Masland and Fabrica reps are the best in the business—efficient and reliable.”

FABRICA

“Fabrica is more creative, innovative and style conscious than other brands and they have great colors.”

“Fabrica’s biggest strength is their attention to detail. They take their time to do it right.”

“Fabrica just does everything better than anyone else.”

“I get great attention from their rep. I just assume that he has less accounts to cover than reps from other mills.”

MASLAND

“Masland is known for quality, fashion, color and styling.”

“Masland is well ahead of the market on styling.”

“Samples need to be readily available and the inventory needs to be in stock…Masland is great about this.”

“Our overall service from Masland is excellent.”

Excerpt from KSA Study dated May 6, 2004, Titled “KSA Assessment of Dixie’s Residential and Contract Carpet Businesses”, commissioned by The Dixie Group, Inc.

19

Retailers Appreciate Dixie’s Products And Service

In the retail segment, Fabrica and Masland are rated stronger than the competition in providing high quality, innovative products, responsive customer service and fast sample turn-around time

Base: Retailers

Importance Ranking Performance Ranking

Key Functions RETAILERS FABRICA MASLAND MOHAWK SHAW

High quality products with minimal claims 9.56 9.04 8.58 6.80 6.96

On-time delivery 9.41 8.14 8.26 7.98 8.16

Responsive and helpful customer service 9.02 8.04 8.49 7.81 7.52

Offers innovative and good-looking product designs 9.02 8.49 8.49 7.37 6.92

Offers strong support from the sales force 8.83 7.39 8.06 8.04 7.18

Products are a good value for the money 8.61 6.10 6.91 8.04 8.08

Fast sample turn-around time 8.31 8.51 8.58 7.23 6.66

Has effective merchandising like displays and sample books 7.07 7.63 7.74 7.65 7.00

Favorable credit plan 6.72 6.55 6.72 7.76 7.28

Has supportive marketing, for example co- op and national advertising 6.02 5.13 5.38 7.11 6.04

Excerpt from KSA Study dated May 6, 2004, Titled “KSA Assessment of Dixie’s Residential and Contract Carpet Businesses”, commissioned by The Dixie Group, Inc.

20

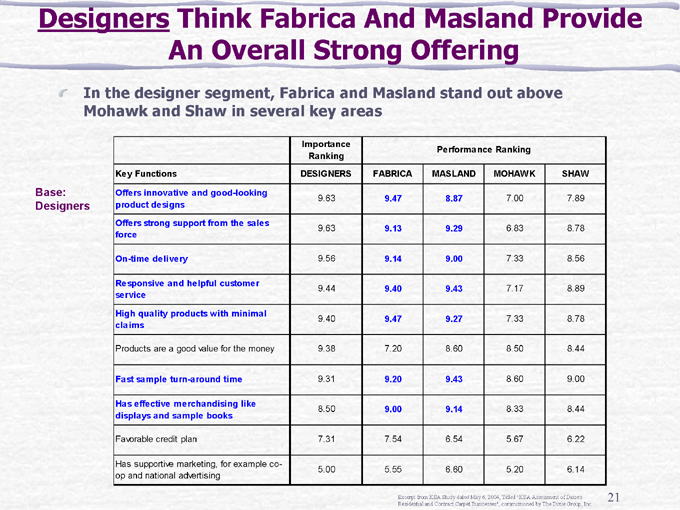

Designers Think Fabrica And Masland Provide An Overall Strong Offering

In the designer segment, Fabrica and Masland stand out above Mohawk and Shaw in several key areas

Base: Designers

Importance Ranking Performance Ranking

Key Functions DESIGNERS FABRICA MASLAND MOHAWK SHAW

Offers innovative and good-looking product designs 9.63 9.47 8.87 7.00 7.89

Offers strong support from the sales force 9.63 9.13 9.29 6.83 8.78

On-time delivery 9.56 9.14 9.00 7.33 8.56

Responsive and helpful customer service 9.44 9.40 9.43 7.17 8.89

High quality products with minimal claims 9.40 9.47 9.27 7.33 8.78

Products are a good value for the money 9.38 7.20 8.60 8.50 8.44

Fast sample turn-around time 9.31 9.20 9.43 8.60 9.00

Has effective merchandising like displays and sample books 8.50 9.00 9.14 8.33 8.44

Favorable credit plan 7.31 7.54 6.54 5.67 6.22

Has supportive marketing, for example co- op and national advertising 5.00 5.55 6.60 5.20 6.14

Excerpt from KSA Study dated May 6, 2004, Titled “KSA Assessment of Dixie’s Residential and Contract Carpet Businesses”, commissioned by The Dixie Group, Inc.

21

Residential Summary

Fabrica and Masland are among the most respected brands in high-end residential carpet Fabrica’s and Masland’s combined residential sales are estimated to be about 35% of total U.S. industry sales at $22.00 and higher Dixie Home at $10-$20

Provides access for Dixie to a larger sector of the market Creates an opportunity to utilize Masland’s assets, thereby reducing overall costs Helps Dixie become more important to upper-middle & high-end customers

Excerpt from KSA Study dated May 6, 2004, Titled “KSA Assessment of Dixie’s Residential and Contract Carpet Businesses”, commissioned by The Dixie Group, Inc.

22

Residential Broadloom—Dixie Home

Fulfill market need for third player.

Well-styled moderate to upper priced line

Leverage need by fiber suppliers for market access.

Branded high-styled goods – not “me too” Support fiber suppliers’ branded products

Limited distribution strategy attractive to retailers.

Drive more volume on existing capacity at Masland/Dixie.

23

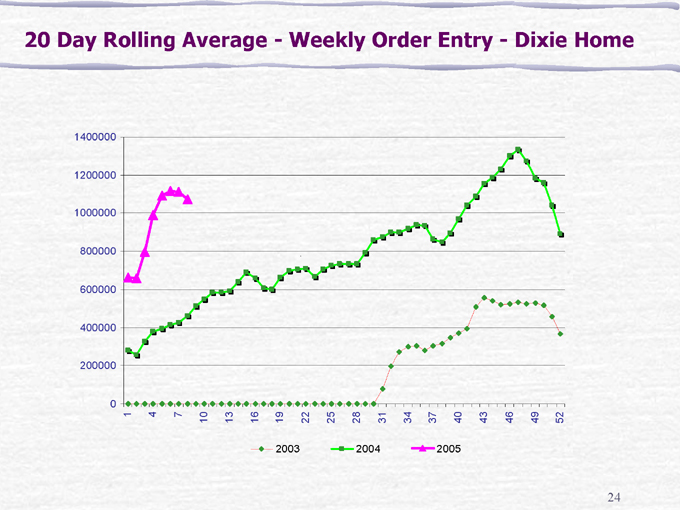

20 Day Rolling Average—Weekly Order Entry—Dixie Home

1400000 1200000 1000000 800000 600000 400000 200000 0

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

2003

2004

2005

24

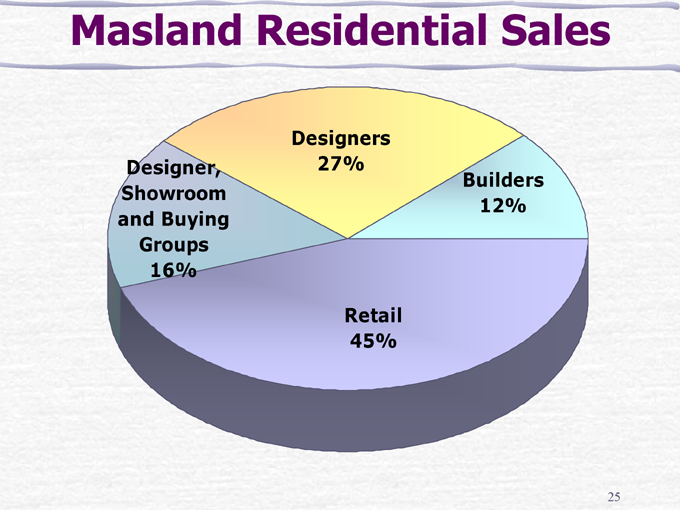

Masland Residential Sales

Designer, Showroom and Buying Groups 16%

Designers 27%

Builders 12%

Retail 45%

25

Masland Residential

Leading high-end brand with reputation for development of products with innovative styling, design and color Doubling product introductions to increase market penetration Drive more volume on existing capacity at Masland/Dixie

26

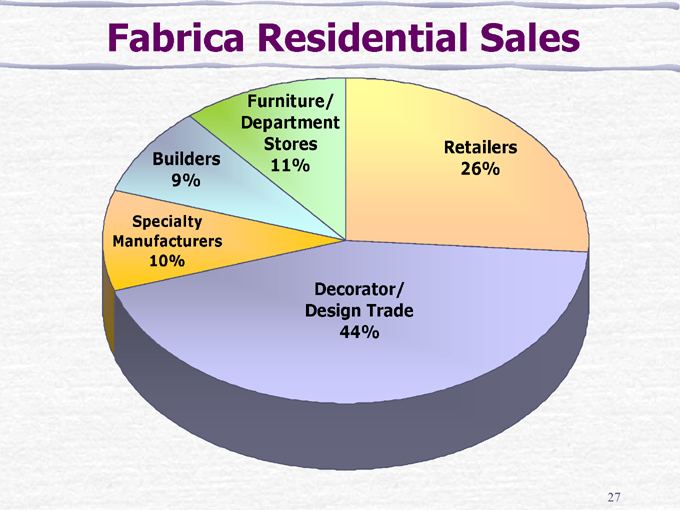

Fabrica Residential Sales

Specialty Manufacturers 10%

Builders 9%

Furniture/ Department Stores 11%

Retailers 26%

Decorator/ Design Trade 44%

27

Fabrica Residential

Premium high-end brand

Leader in styling/patterns/color

Consistent sales and profit growth

12 years consecutive sales growth Over 50% profit growth since July 2000 acquisition

28

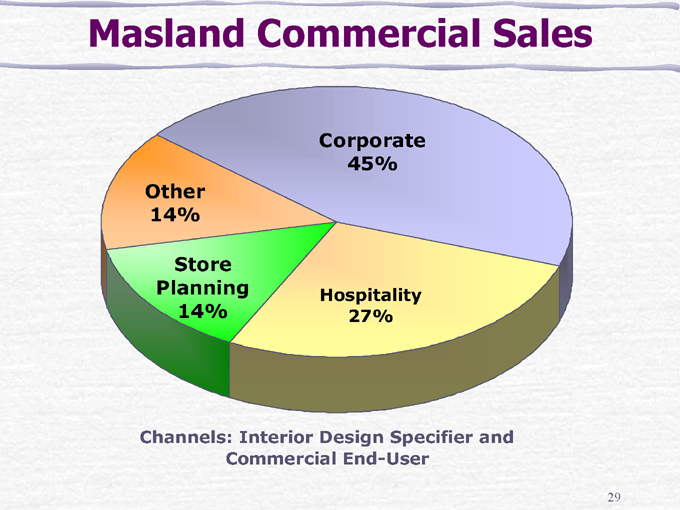

Masland Commercial Sales

Corporate 45%

Other 14%

Store Planning 14%

Hospitality 27%

Channels: Interior Design Specifier and Commercial End-User

29

Masland Commercial

Good and growing position with premium brand Designer focused Strong national account base Strong growth from new “Energy

Collection”

KSA study – identified potential opportunities

Invest in carpet tile.

30

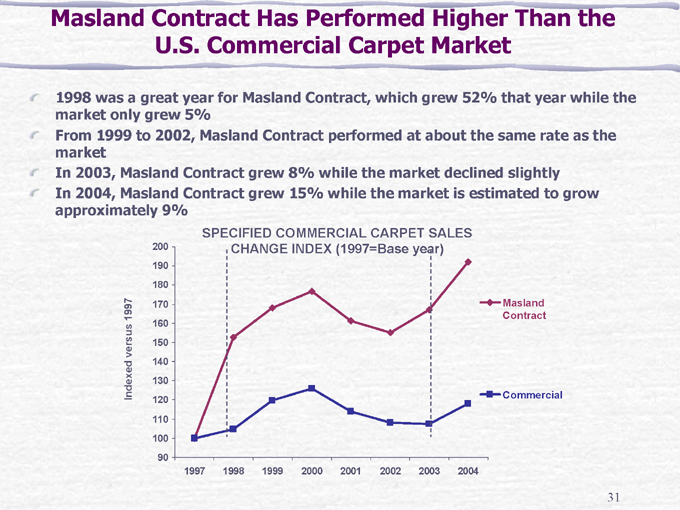

Masland Contract Has Performed Higher Than the U.S. Commercial Carpet Market

1998 was a great year for Masland Contract, which grew 52% that year while the market only grew 5% From 1999 to 2002, Masland Contract performed at about the same rate as the market In 2003, Masland Contract grew 8% while the market declined slightly In 2004, Masland Contract grew 15% while the market is estimated to grow approximately 9%

SPECIFIED COMMERCIAL CARPET SALES

CHANGE INDEX (1997=Base year)

Indexed versus 1997

200 190 180 170 160 150 140 130 120 110 100 90

1997 1998 1999 2000 2001 2002 2003 2004

Masland Contract

Commercial

31

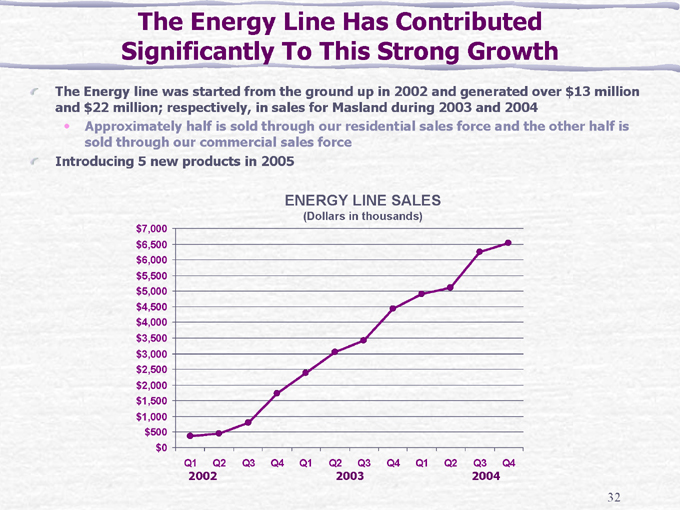

The Energy Line Has Contributed Significantly To This Strong Growth

The Energy line was started from the ground up in 2002 and generated over $13 million and $22 million; respectively, in sales for Masland during 2003 and 2004

Approximately half is sold through our residential sales force and the other half is sold through our commercial sales force

Introducing 5 new products in 2005

ENERGY LINE SALES

(Dollars in thousands) $7,000 $6,500 $6,000 $5,500 $5,000 $4,500 $4,000 $3,500 $3,000 $2,500 $2,000 $1,500 $1,000 $500 $0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2002 2003 2004

32

Summary

Smaller, highly profitable, growing company with strong brands in the upper-end Vastly improved risk profile

Financially – strong balance sheet Customer base

Focused on internal profitable growth

33