Omnicom Group

SECOND QUARTER 2006 RESULTS

Investor Presentation

July 25, 2006

Exhibit 99.2

The following materials have been prepared for use in the July 25, 2006 conference call on Omnicom’s results of

operations for the quarter ended June 30, 2006. The call will be archived on the Internet at

http://www.omnicomgroup.com/financialwebcasts.

Forward-Looking Statements

Certain of the statements in this document constitute forward-looking statements within the meaning of the Private

Securities Litigation Act of 1995. These statements relate to future events or future financial performance and involve

known and unknown risks and other factors that may cause our actual or our industry’s results, levels of activity or

achievement to be materially different from those expressed or implied by any forward-looking statements. These risks

and uncertainties include, but are not limited to, our future financial condition and results of operations, changes in

general economic conditions, competitive factors, changes in client communication requirements, the hiring and

retention of human resources and our international operations, which are subject to the risks of currency fluctuations and

exchange controls. In some cases, forward-looking statements can be identified by terminology such as “may,” “will,”

“could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “believe,” “estimate,” “predict,” “potential” or “continue”

or the negative of those terms or other comparable terminology. These statements are present expectations. Actual

events or results may differ materially. We undertake no obligation to update or revise any forward-looking statement.

Other Information

All dollar amounts are in millions except for EPS. The following financial information contained in this document has not

been audited, although some of it has been derived from Omnicom’s historical financial statements, including its audited

financial statements. In addition, industry, operational and other non-financial data contained in this document have been

derived from sources we believe to be reliable, but we have not independently verified such information, and we do not,

nor does any other person, assume responsibility for the accuracy or completeness of that information.

The inclusion of information in this presentation does not mean that such information is material or that disclosure of

such information is required.

1

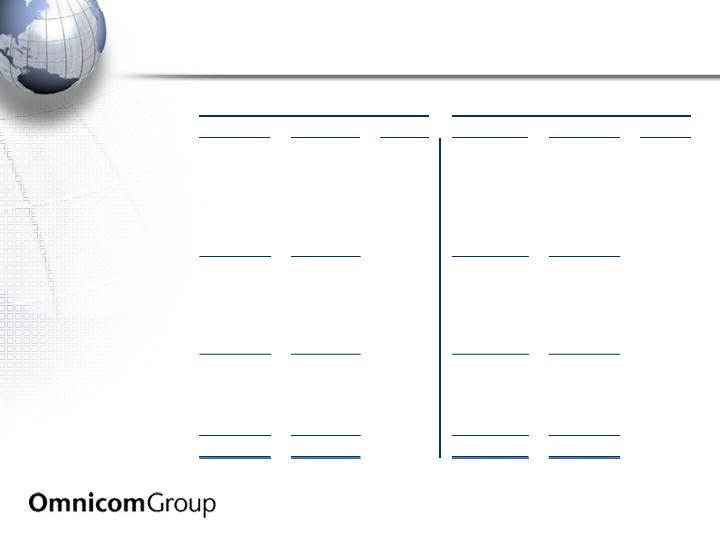

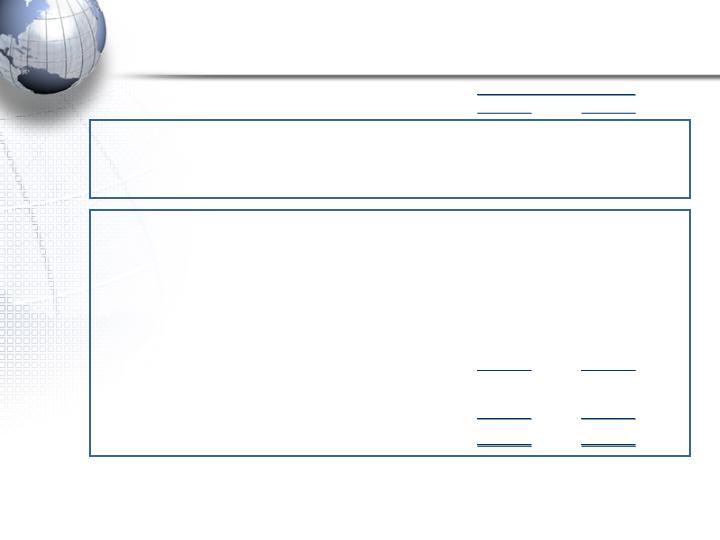

2006 vs. 2005 P&L Summary

2

2006

2005

%

2006

2005

%

Revenue

2,823.4

$

2,615.8

$

7.9%

5,386.3

$

5,018.8

$

7.3%

Operating Income

417.4

382.0

9.3%

701.9

639.3

9.8%

% Margin

14.8%

14.6%

13.0%

12.7%

Net Interest Expense

25.5

14.3

40.7

26.4

Profit Before Tax

391.9

367.7

6.6%

661.2

612.9

7.9%

% Margin

13.9%

14.1%

12.3%

12.2%

Taxes

131.7

124.3

222.6

210.5

% Tax Rate

33.6%

33.8%

33.7%

34.3%

Profit After Tax

260.2

243.4

6.9%

438.6

402.4

9.0%

Equity in Affiliates

6.3

5.0

11.2

10.2

Minority Interest

(22.4)

(22.6)

(40.1)

(36.3)

Net Income

244.1

$

225.8

$

8.1%

409.7

$

376.3

$

8.9%

Second Quarter

Year to Date

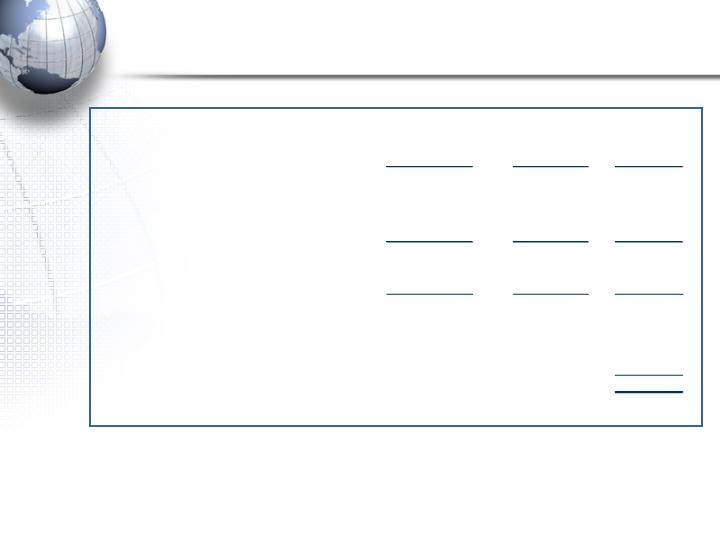

2006 vs. 2005 Earnings Per Share

Earnings per Share:

Basic

Diluted

Growth Rate, Diluted

Weighted Average Shares (millions):

Basic

Diluted

Dividend Declared Per Share

$ 1.43

1.42

14.5

170.2

172.0

$0.250

2005

2006

Second Quarter

$ 1.24

1.24

181.4

182.8

$0.225

$ 2.36

2.34

14.1

173.6

175.2

$0.500

2005

2006

Year to Date

$ 2.07

2.05

182.0

183.5

$0.450

%

%

3

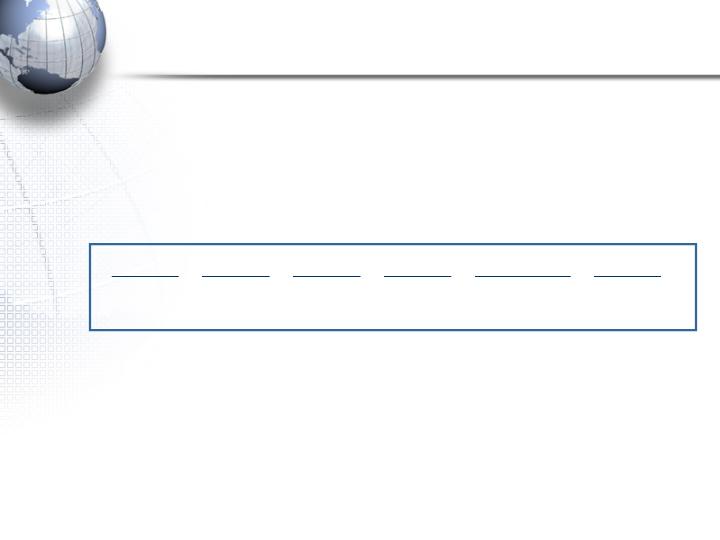

2006 Total Revenue Growth

(a)

To calculate the FX impact, we first convert the current period’s local currency revenue using the average exchange rates from the

equivalent prior period to arrive at constant currency revenue. The FX impact equals the difference between the current period

revenue in U.S. dollars and the current period revenue in constant currency.

(b)

Acquisition revenue is the aggregate of the applicable prior period revenue of the acquired businesses. Netted against this number

is the revenue of any business included in the prior period reported revenue that was disposed of subsequent to the prior period.

(c)

Organic revenue is calculated by subtracting both the acquisition revenue and the FX impact from total revenue growth.

$

%

$

%

Prior Period Revenue

2,615.8

$

5,018.8

$

Foreign Exchange (FX) Impact (a)

3.8

0.1%

(61.4)

-1.2%

Acquisition Revenue (b)

16.5

0.6%

33.8

0.7%

Organic Revenue (c)

187.3

7.2%

395.1

7.9%

Current Period Revenue

2,823.4

$

7.9%

5,386.3

$

7.3%

Second Quarter

Year to Date

4

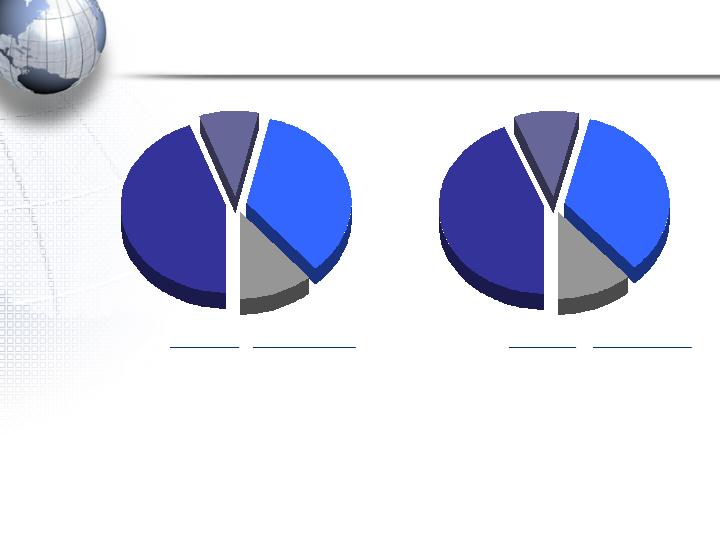

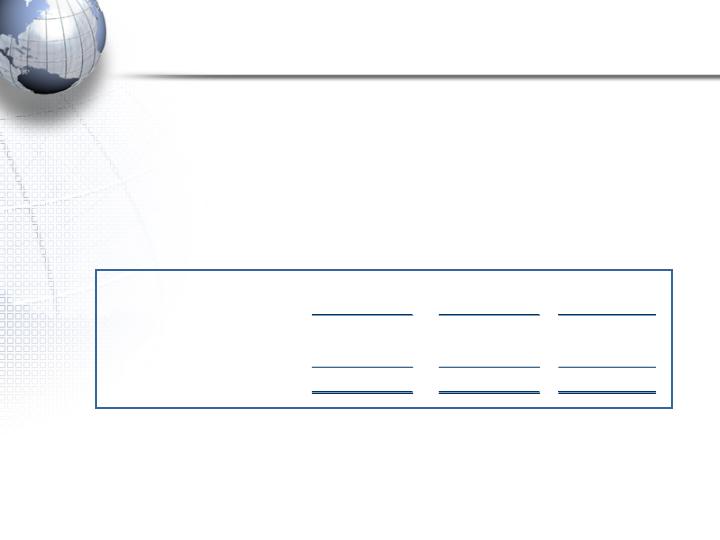

2006 Revenue By Discipline

(a) “Growth” is the year-over-year growth from the prior period.

Advertising

43.2%

PR

10.2%

CRM

34.7%

Specialty

11.9%

Advertising

43.2%

PR

10.2%

CRM

34.7%

Specialty

11.9%

Year to

Date

Second Quarter

2006

$ Mix

% Growth

(a)

$ Mix

% Growth

(a)

Advertising

1,219.3

5.7%

####

Advertising

2,324.3

5.5%

CRM

978.6

9.6%

####

CRM

1,870.4

9.8%

PR

288.6

8.9%

####

PR

548.4

5.2%

Specialty

336.9

10.8%

####

Specialty

643.2

8.9%

5

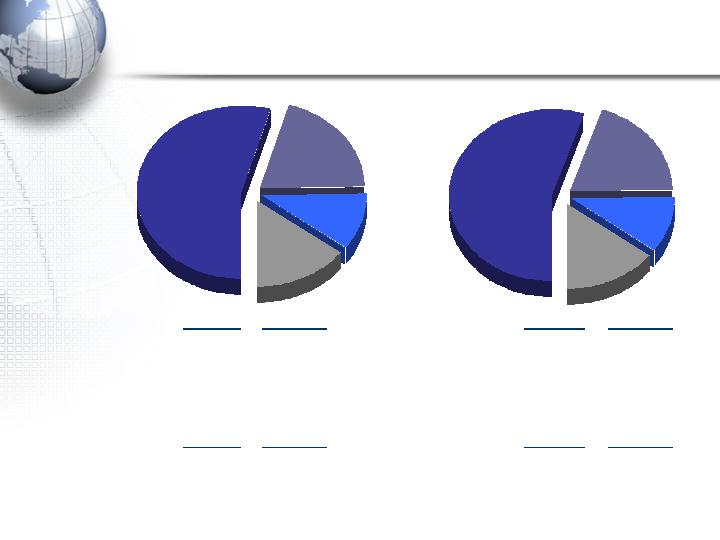

Second Quarter

2006

2006 Revenue By Geography

United

States

55.1%

UK

10.7%

Euro

Markets

19.6%

Other

14.6%

Year to Date

United

States

54.4%

UK

10.8%

Euro

Markets

20.2%

Other

14.6%

(a) “Growth” is the year-over-year growth from the prior period.

$ Mix

$ Growth

(a)

$ Mix

$ Growth

(a)

United States

1,535.4

$

107.7

$

United States

2,968.4

$

228.6

$

Organic

91.1

Organic

195.1

Acquisition

16.6

Acquisition

33.5

International

1,288.0

$

99.9

$

International

2,417.9

$

138.9

$

Organic

96.2

Organic

200.0

Acquisition

(0.1)

Acquisition

0.3

FX

3.8

FX

(61.4)

$ Mix

% Growth

(a)

$ Mix

% Growth

(a)

United States

1,535.4

$

7.5%

United States

2,968.4

$

8.3%

Euro Currency Markets

570.1

3.8%

Euro Currency Markets

1,053.9

-0.1%

United Kingdom

304.0

12.8%

United Kingdom

577.7

8.0%

Other

413.9

12.1%

Other

786.3

14.2%

6

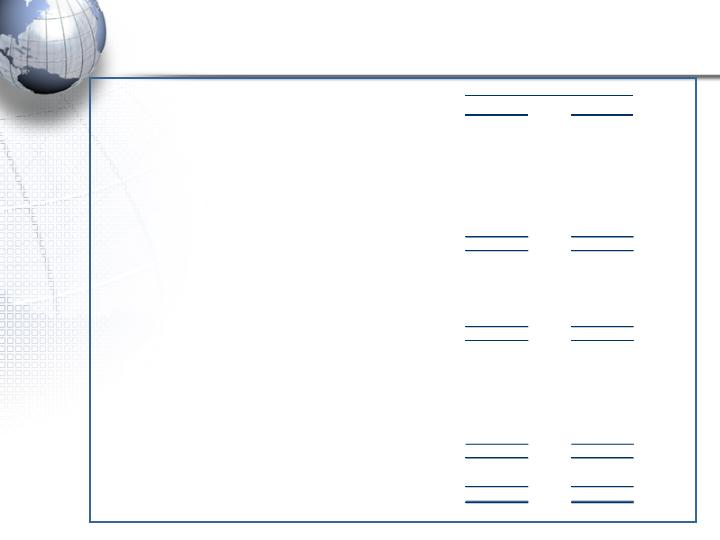

Cash Flow – GAAP Presentation (condensed)

2006

2005

Net Income

409.7

$

376.3

$

Stock-Based Compensation Expense

33.9

47.4

Windfall Tax Benefit on Stock Compensation

-

14.0

Depreciation and Amortization

90.3

85.5

Other Non-Cash Items to Reconcile to Net Cash Provided by Operations

37.4

27.1

Other Changes in Working Capital

(374.6)

(1,120.5)

Excess Tax Benefit on Stock Compensation

(10.1)

-

Net Cash Provided by (Used in) Operations

186.6

(570.2)

Capital Expenditures

(73.0)

(67.2)

Acquisitions

(138.5)

(132.4)

Proceeds from Sale of Businesses

-

29.3

Repayment of LT Notes Receivable

13.5

72.1

Other Investing Activities, net

332.4

552.1

Net Cash Provided by Investing Activities

134.4

453.9

Dividends

(89.8)

(82.4)

Proceeds from Issuance of Debt

995.8

0.4

Repayment of Debt

(134.1)

(188.6)

Stock Repurchases

(958.6)

(524.0)

Share Transactions Under Employee Stock Plans

153.5

34.2

Excess Tax Benefit on Stock Compensation

10.1

-

Other Financing Activities

(42.7)

67.3

Net Cash Used in Financing Activities

(65.8)

(693.1)

Effect of exchange rate changes on cash and cash equivalents

1.0

(12.7)

Net Increase (Decrease) in Cash and Cash Equivalents

256.2

$

(822.1)

$

6 Months Ended June 30,

7

Current Credit Picture

(a) “Operating Income (EBIT)” and “Net Interest Expense” calculations shown are the latest twelve month (“LTM”) figures for the periods specified.

Although our bank agreements reference EBITDA, we have used EBIT for this presentation because EBITDA is a non-GAAP measure.

(b) Holders of our Convertible Notes Due 6/15/33 were offered a supplemental interest payment not to put the notes to us and to consent to certain

amendments to the notes. Holders of $427.1 million of notes consented to the amendments and were paid the supplemental interest thus

creating the Convertible Notes Due 7/1/38. Holders of $40.4 million of notes did not put or consent to the amendments and the notes

remained unchanged. The remaining holders of $132.5 million of notes put the notes to us for repurchase.

2006

2005

Operating Income (EBIT)

(a)

$

1,402

$

1,282

Net Interest Expense

(a)

$

73.5

$

45.2

EBIT / Net Interest

19.1

x

28.4

x

Net Debt / EBIT

1.5

x

1.7

x

Debt:

Bank Loans (Due Less Than 1 Year)

$

17

$

132

CP Issued Under $2.4B - 5 Year Revolver Due 6/23/11

-

-

Convertible Notes Due 2/7/31

847

847

Convertible Notes Due 7/31/32

892

892

Convertible Notes Due 6/15/33

(b)

40

600

Convertible Notes Due 7/1/38

(b)

427

-

10 Year Notes Due 4/15/16

995

-

Other Debt

19

20

Total Debt

$

3,237

$

2,491

Cash and Short Term Investments

1,135

365

Net Debt

$

2,102

$

2,126

LTM ended June 30,

8

Current Liquidity Picture

(a)

Credit facility expires June 23, 2011.

(b)

Represents uncommitted facilities in the U.S., U.K. and Canada. These amounts are excluded from our available

liquidity for purposes of this presentation.

Total Amount

Of Facility

Outstanding

Available

Committed Facilities

5 Year Revolver

(a)

2,400

$

-

$

2,400

$

Other Committed Credit Facilities

16

16

-

Total Committed Facilities

2,416

16

2,400

Uncommitted Facilities

(b)

345

-

-

(b)

Total Credit Facilities

2,761

$

16

$

2,400

$

Cash and Short Term Investments

1,135

Total Liquidity Available

3,535

$

As of June 30, 2006

9

Acquisitions Summary

10

Acquisition Related Expenditures

Note: See appendix for subsidiary acquisition profiles.

Includes acquisitions of a majority interest in new agencies resulting in their consolidation.

Includes acquisitions of additional equity interests in existing affiliate agencies resulting in their majority ownership and consolidation.

Includes acquisitions of less than a majority interest in agencies in which Omnicom did not have a prior equity interest and the acquisition

of additional interests in existing affiliated agencies that did not result in majority ownership.

Includes the acquisition of additional equity interests in already consolidated subsidiary agencies.

Includes additional consideration paid for acquisitions completed in prior periods.

(a)

(b)

(c)

(d)

(e)

New Subsidiary Acquisitions

(a)

36

$

Affiliates to Subsidiaries

(b)

-

Affiliates

(c)

3

Existing Subsidiaries

(d)

18

Earn-outs

(e)

94

Total Acquisition Expenditures

151

$

6 Months YTD 2006

11

Potential Earn-out Obligations

The following is a calculation of future earn-out obligations as of

June 30, 2006, assuming that the underlying acquired agencies

continue to perform at their current levels: (a)

(a)

The ultimate payments will vary as they are dependent on future events and changes in FX rates.

12

2006

2007

2008

2009

Thereafter

Total

44

$

146

$

105

$

55

$

55

$

405

$

Potential Obligations

(a) The ultimate payments will vary as they are dependent on future events and changes in FX rates.

In conjunction with certain transactions Omnicom has agreed to

acquire (at the sellers’ option) additional equity interests. If these rights

are exercised, there would likely be an increase in our net income as a

result of our increased ownership and the reduction of minority interest

expense. The following is a calculation of these potential future

obligations (as of June 30, 2006), assuming these underlying acquired

agencies continue to perform at their current levels: (a)

Currently

Exercisable

Not Currently

Exercisable

Total

Subsidiary Agencies

131

$

82

$

213

$

Affiliated Agencies

48

7

55

Total

179

$

89

$

268

$

13

Second Quarter Acquisitions

Entertainment Marketing Partners

Entertainment Marketing Partners ("EMP") is an entertainment-

based media and marketing solutions company. EMP provides

clients with access to the entertainment community through

relationships with studios, networks and production companies,

sports leagues around the world, and video game developers.

EMP is located in Los Angeles and New York City and will become

part of Ketchum Public Relations.

14

Second Quarter Acquisitions

Harrison & Wolf

Harrison & Wolf (H&W) is a corporate communications agency

providing strategic consultancy, contract publishing, advertising

and corporate design services.

The agency is located in Paris, France and will be part of the

Corporate Communications Group of TBWA.

15

Second Quarter Acquisitions

EVB

EVB is a full-service advertising agency that specializes in using

immersive content to create engaging brand experiences. EVB's

consumer-centric approach blends strategy with entertainment

and interactivity to develop new marketing campaigns that

generate brand awareness, deepen consumer relationships and

instill long-term brand loyalty.

EVB is located in San Francisco, California and will be part of the

DAS Group of Companies.

16