Omnicom Group

THIRD QUARTER 2008 RESULTS

Investor Presentation

October 21, 2008

Exhibit 99.2

1

The following materials have been prepared for use in the October 21, 2008 conference call on Omnicom’s results of operations

for the period ended September 30, 2008. The call will be archived on the Internet at

http://www.omnicomgroup.com/financialwebcasts.

Forward-Looking Statements

Certain of the statements in this document constitute forward-looking statements within the meaning of the Private Securities

Litigation Act of 1995. These statements relate to future events or future financial performance and involve known and

unknown risks and other factors that may cause our actual or our industry’s results, levels of activity or achievement to be

materially different from those expressed or implied by any forward-looking statements. These risks and uncertainties

include, but are not limited to, our future financial condition and results of operations, changes in general economic

conditions, competitive factors, changes in client communication requirements, the hiring and retention of human resources

and our international operations, which are subject to the risks of currency fluctuations and exchange controls. In some

cases, forward-looking statements can be identified by terminology such as “may,” “will,” “could,” “would,” “should,” “expect,”

“plan,” “anticipate,” “intend,” “believe,” “estimate,” “predict,” “potential” or “continue” or the negative of those terms or other

comparable terminology. These statements are present expectations. Actual events or results may differ materially. We

undertake no obligation to update or revise any forward-looking statement, except as required by law.

Other Information

All dollar amounts are in millions except for EPS. The financial information contained in this document has not been audited,

although some of it has been derived from Omnicom’s historical financial statements, including its audited financial

statements. In addition, industry, operational and other non-financial data contained in this document have been derived

from sources we believe to be reliable, but we have not independently verified such information, and we do not, nor does

any other person, assume responsibility for the accuracy or completeness of that information.

The inclusion of information in this presentation does not mean that such information is material or that disclosure of such

information is required.

2

2008 vs. 2007 P&L Summary

2008

2007

%

2008

2007

%

Revenue

3,316.2

$

3,101.4

$

6.9%

9,988.5

$

9,068.1

$

10.1%

Operating Income

373.4

350.2

6.6%

1,241.0

1,127.3

10.1%

% Margin

11.3%

11.3%

12.4%

12.4%

Net Interest Expense

20.7

19.3

50.4

59.8

Profit Before Tax

352.7

330.9

6.6%

1,190.6

1,067.5

11.5%

% Margin

10.6%

10.7%

11.9%

11.8%

Taxes

118.2

112.1

400.6

361.4

% Tax Rate

33.5%

33.9%

33.6%

33.9%

Equity in Affiliates

6.8

8.0

26.0

25.8

Minority Interest

(27.7)

(24.6)

(86.7)

(70.0)

Net Income

213.6

$

202.2

$

5.6%

729.3

$

661.9

$

10.2%

Third Quarter

Year to Date

3

2008 vs. 2007 Earnings Per Share

Earnings per Share:

Basic

Diluted

Growth Rate, Diluted

Weighted Average Shares (millions):

Basic

Diluted

Dividend Declared Per Share

$ 0.69

0.69

11.3

309.1

310.7

$0.150

2007

2008

Third Quarter

$ 0.62

0.62

324.0

328.2

$0.150

$ 2.32

2.30

15.0

315.0

317.7

$0.450

2007

2008

Year to Date

$ 2.02

2.00

327.0

331.8

$0.425

%

%

4

2008 Total Revenue Growth

(a)

To calculate the FX impact, we first convert the current period’s local currency revenue using the average exchange

rates from the equivalent prior period to arrive at constant currency revenue. The FX impact equals the difference

between the current period revenue in U.S. dollars and the current period revenue in constant currency.

(b)

Acquisition revenue is the aggregate of the applicable prior period revenue of the acquired businesses. Netted against

this number is the revenue of any business included in the prior period reported revenue that was disposed of

subsequent to the prior period.

(c)

Organic revenue is calculated by subtracting both the acquisition revenue and the FX impact from total revenue growth.

$

%

$

%

Prior Period Revenue

3,101.4

$

9,068.1

$

Foreign Exchange (FX) Impact (a)

66.0

2.1%

374.5

4.1%

Acquisition Revenue (b)

22.9

0.7%

88.9

1.0%

Organic Revenue (c)

125.9

4.1%

457.0

5.0%

Current Period Revenue

3,316.2

$

6.9%

9,988.5

$

10.1%

Third Quarter

Year to Date

5

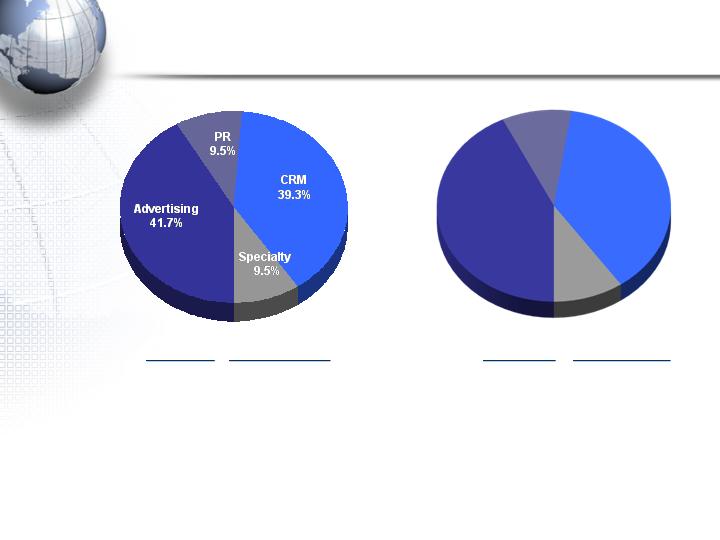

Third Quarter

Year to Date

Advertising

42.8%

PR

9.6%

CRM

37.9%

Specialty

9.7%

(a) “Growth” is the year-over-year increase or decrease from the prior period.

2008 Revenue By Discipline

$ Mix

% Growth(a)

$ Mix

% Growth(a)

Advertising

1,382.0

6.9%

Advertising

4,273.2

10.0%

CRM

1,305.5

12.0%

CRM

3,786.8

14.6%

PR

314.1

-1.2%

PR

962.5

3.1%

Specialty

314.6

-3.2%

Specialty

966.0

2.1%

6

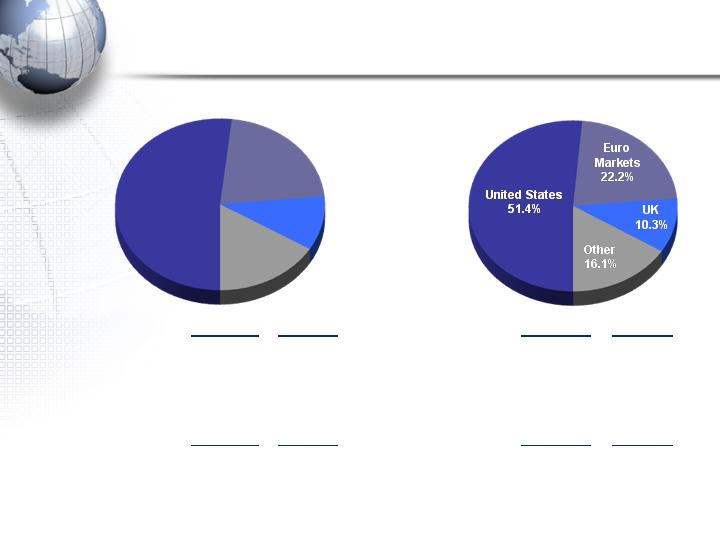

Third Quarter

2008 Revenue By Geography

Year to Date

Euro

Markets

21.7%

United States

51.8%

UK

10.2%

Other

16.3%

(a) “Growth” is the year-over-year increase or decrease from the prior period.

$ Mix

$ Growth(a)

$ Mix

$ Growth(a)

United States

1,718.0

$

63.1

$

United States

5,130.5

$

272.1

$

Organic

46.9

Organic

221.9

Acquisition

16.2

Acquisition

50.2

International

1,598.2

$

151.7

$

International

4,858.0

$

648.3

$

Organic

79.0

Organic

235.1

Acquisition

6.7

Acquisition

38.7

FX

66.0

FX

374.5

$ Mix

% Growth(a)

$ Mix

% Growth(a)

United States

1,718.0

$

3.8%

United States

5,130.5

$

5.6%

Euro Currency Markets

718.3

13.0%

Euro Currency Markets

2,217.9

18.1%

United Kingdom

337.5

-4.3%

United Kingdom

1,026.4

0.0%

Other

542.4

18.3%

Other

1,613.7

23.6%

7

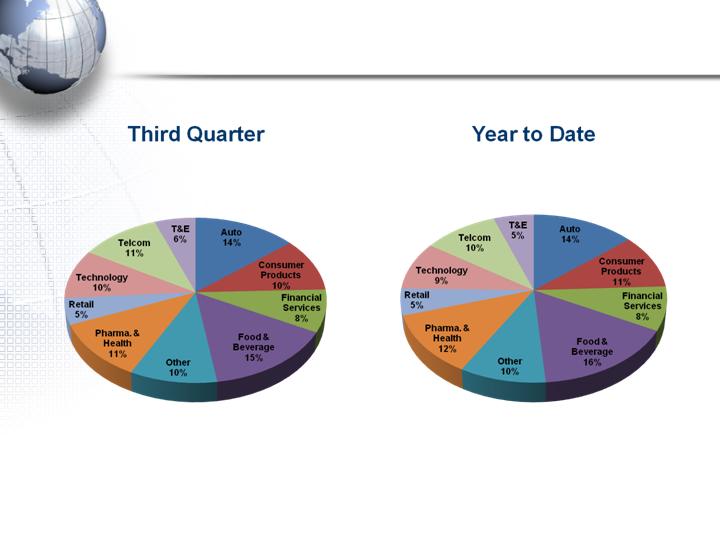

2008 Revenue By Industry

Charts represent the amount of revenue attributable to each industry expressed as a percentage of the total revenue

from Omnicom’s 1,000 largest clients for the period ended September 30, 2008.

8

Cash Flow – GAAP Presentation (condensed)

2008

2007

Net Income

729.3

$

661.9

$

Share-Based Compensation Expense

44.3

53.4

Depreciation and Amortization

176.2

150.8

Other Non-Cash Items to Reconcile to Net Cash Provided by Operations

86.7

70.6

Other Changes in Working Capital

(789.2)

(752.6)

Excess Tax Benefit on Share-Based Compensation

(12.9)

(15.4)

Net Cash Used by Operations

234.4

168.7

Capital Expenditures

(151.6)

(160.8)

Acquisitions

(387.8)

(317.9)

Other Investing Activities, net

19.1

132.3

Net Cash Used by Investing Activities

(520.3)

(346.4)

Dividends

(145.3)

(133.7)

Stock Repurchases

(846.0)

(846.5)

Share Transactions Under Employee Stock Plans

77.8

68.4

Proceeds from Issuance of Debt

115.3

0.8

Excess Tax Benefit on Stock Compensation

12.9

15.4

Other Financing Activities

(49.0)

(46.3)

Net Cash Used by Financing Activities

(834.3)

(941.9)

Effect of exchange rate on cash and cash equivalents

(142.4)

(42.7)

Net Decrease in Cash and Cash Equivalents

(1,262.6)

$

(1,162.3)

$

9 Months Ended September 30,

9

Current Credit Picture

(a)

“EBITDA” and “Gross Interest Expense” calculations shown are the latest twelve month (“LTM”) figures for the

periods specified. EBITDA is defined as operating income before interest, taxes, depreciation and amortization.

Although EBITDA is a non-GAAP measure, we believe EBITDA is more meaningful for purposes of this analysis

because the financial covenants in our credit facilities are based on EBITDA (see reconciliation of Operating

Income to EBITDA on page 21).

2008

2007

EBITDA (a)

$

2,007

$

1,805

Gross Interest Expense (a)

$

115.2

$

117.3

EBITDA / Gross Interest Expense

17.4

x

15.4

x

Total Debt / EBITDA

1.6

x

1.7

x

Debt:

Short-term borrowings (Due Less Than 1 Year)

$

64

$

18

CP Issued Under $2.5B - 5 Year Revolver Due 6/23/11

113

-

Convertible Notes Due 2/7/31

847

847

Convertible Notes Due 7/31/32

727

727

Convertible Notes Due 6/15/33

-

-

Convertible Notes Due 7/1/38

467

467

10 Year Notes Due 4/15/16

996

996

Other Debt

20

20

Total Debt

$

3,234

$

3,075

Cash and Short Term Investments

553

635

Net Debt

$

2,681

$

2,440

LTM Ended September 30,

10

Current Liquidity Picture

(a)

Credit facility expires June 23, 2011.

(b)

Represents uncommitted facilities in the U.S., U.K. and Canada as of September 30, 2008. These amounts are

excluded from our available liquidity for purposes of this presentation.

Total Amount

Of Facility

Outstanding

Available

Committed Facilities

5 Year Revolver (a)

2,500

$

113

$

2,387

$

Other Committed Credit Facilities

64

64

-

Total Committed Facilities

2,564

177

2,387

Uncommitted Facilities (b)

331

-

-

(b)

Total Credit Facilities

2,895

$

177

$

2,387

$

Cash and Short Term Investments

553

Total Liquidity Available

2,940

$

As of September 30, 2008

11

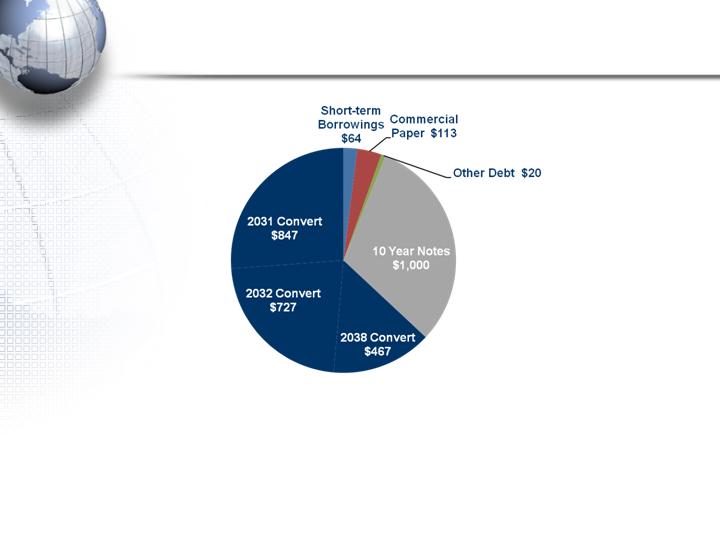

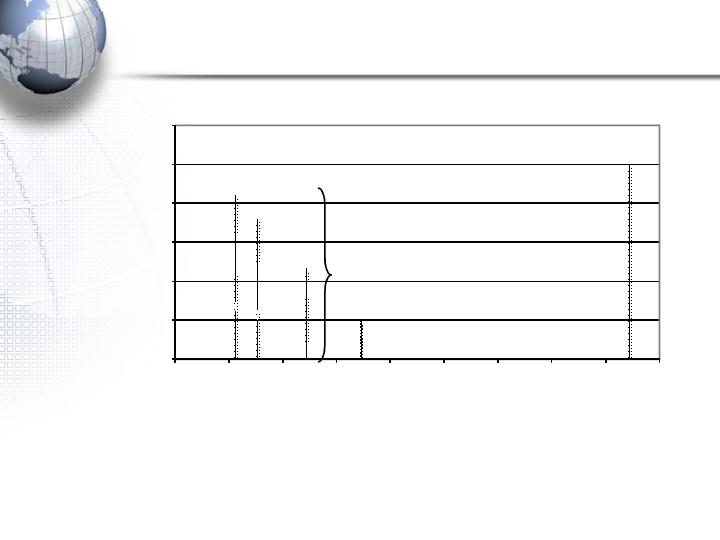

Omnicom Debt Structure

Supplemental Information

Omnicom Debt Structure

12

The above chart reflects Omnicom’s debt outstanding at September 30, 2008. The

amount reflected above for the 10 Year Notes represents the value of these notes at

maturity on April 15, 2016.

13

Omnicom Debt Structure

The Bank

Facility and

Commercial

Paper Program

together provide

liquidity in the

event any

convertible

notes are put.

We then have

flexibility to

refinance in

different debt

capital markets.

Our 2031 Notes are putable annually, with the next put date in February 2009. Our 2032 Notes are putable annually, with the next put date in July

2009. Our 2038 Notes are putable in June 2010, 2013, 2018, 2023 and annually thereafter.

For purposes of this presentation we have included the following borrowings as of September 30, 2008 as outstanding through June 2011, the

date of expiration of our five-year credit facility: commercial paper of $113 million, short-term borrowings of $64 million and other debt of $20

million. We believe that this presentation is more meaningful for purposes of understanding how we evaluate the maturities of our debt structure.

$

0

$

200

$

400

$

600

$

800

$

1

,

000

$

1

,

200

Jan

-

08

Jan

-

09

Jan

-

10

Jan

-

11

Jan

-

12

Jan

-

13

Jan

-

14

Jan

-

15

Jan

-

16

2031

2032

2038

$

1

.

0

B

10

-

Year

$

2

.

04

Billion

Senior Convertible

Notes

Other

Borrowings

14

Senior Notes Due 2016

Principal Amount

$1 Billion

Co - Issuers

Omnicom Group, Omnicom Finance, Omnicom Capital

Date

March 29, 2006

Maturity

April 15, 2016

Security

Unsecured, pari passu with Bank Facility

Coupon

5.90%

Spread Over Comparable

Treasury at Issue

1.30%

Rating

Moody’s: Baa1

S&P: A-

Fitch: A-

15

2031 Convertible Notes

Principal Amount

$847 Million

Co - Issuers

Omnicom Group, Omnicom Finance, Omnicom Capital

Date

February 7, 2001

Maturity

February 7, 2031 with annual puts each February

Security

Unsecured, pari passu with Bank Facility

Coupon

0.00%

Conversion Price

$55

Rating

Moody’s: Baa1

S&P: A-

Fitch: A-

16

2032 Convertible Notes

Principal Amount

$727 Million

Co - Issuers

Omnicom Group, Omnicom Finance, Omnicom Capital

Date

March 6, 2002

Maturity

July 31, 2032 with puts each July

Security

Unsecured, pari passu with Bank Facility

Coupon

0.00%

Conversion Price

$55

Rating

Moody’s: Baa1

S&P: A-

Fitch: A-

17

2038 Convertible Notes

Principal Amount

$467 Million

Co - Issuers

Omnicom Group, Omnicom Finance, Omnicom Capital

Date

June 10, 2003

Maturity

June 15, 2038 with puts in June of 2010, 2013, 2018, 2023 and

annually thereafter until maturity

Security

Unsecured, pari passu with Bank Facility

Coupon

0.00%

Conversion Price

$51.50

Rating

Moody’s: Baa1

S&P: A-

Fitch: A-

18

Current Bank Credit Facility

Amount

$2.5 Billion

Type

Unsecured Revolving Credit

Maturity

5 Years – June 2011

Facility Fee

13BP per annum

Drawn Rate

Libor +17BP

Covenants

-Maximum Debt to EBITDA 3:1

-Minimum Interest Coverage 5:1

19

Current Bank Credit Facility –

Distribution of 32 Banks

North America

Bank of America

($200)

Wells Fargo ($175)

Northern Trust ($50)

PNC ($50)

Union Bank

of California ($50)

US Bancorp ($50)

Scotia ($40)

Comerica ($25)

Key ($25)

Fifth Third ($15)

Europe

Societe Generale ($150)

Deutsche ($150)

BNP Paribas ($130)

BBVA ($100)

Commerzbank ($80)

Barclays ($50)

Den Danske ($50)

UBS ($35)

Intesa San Paolo ($30)

ING ($25)

Nordea ($25)

Unicredit ($25)

Global

Citigroup ($100) JP Morgan ($200) HSBC ($200) Royal Bank of Scotland ($150)

Asia

Sumitomo ($100)

Bank of Tokyo ($50)

Mizuho ($50)

ANZ ($50)

Standard Chartered ($45)

Westpac ($25)

($ in Millions)

Current Omnicom Credit Ratings

Moody’s

S&P

Fitch

Long Term Ratings

Baa1

A-

A-

Short Term

Ratings

P2

A2

F2

Outlook

Stable

Stable

Stable

20

21

Reconciliation of Operating Income to

EBITDA

The covenants contained in our credit facility are based on the EBITDA ratios as presented on page 9 of this presentation. The above

reconciles our GAAP Operating Income to EBITDA for the periods presented.

EBITDA is a non-GAAP financial measure within the meaning of applicable SEC rules and regulations Our credit facility defines EBITDA as

earnings before deducting interest expense, income taxes, depreciation and amortization. Our credit facility uses EBITDA to measure our

compliance with covenants, such as interest coverage and leverage. EBITDA is not, and should not, be used as a substitute for Operating

Income as determined in accordance with GAAP and is only used to measure our compliance with our debt covenants. Management does not

use EBITDA for any other measurement purpose.

2008

2007

Operating Income

$

1,773

$

1,601

Depreciation

184

159

Amortization

50

45

EBITDA

$

2,007

$

1,805

LTM Ended September 30,

22

Acquisitions Summary

23

Acquisition Related Expenditures

Note: See appendix for acquisition profiles.

Includes acquisitions of a majority interest in agencies resulting in their consolidation.

Includes acquisitions of additional equity interests in existing affiliate agencies resulting in their majority ownership and consolidation.

Includes acquisitions of less than a majority interest in agencies in which Omnicom did not have a prior equity interest and the

acquisition of additional interests in existing affiliated agencies that did not result in majority ownership.

Includes the acquisition of additional equity interests in already consolidated subsidiary agencies.

Includes additional consideration paid for acquisitions completed in prior periods.

(a)

(b)

(c)

(d)

(e)

New Subsidiary Acquisitions (a)

77

$

Affiliates to Subsidiaries (b)

12

Affiliates (c)

87

Existing Subsidiaries (d)

66

Earn-outs (e)

164

Total Acquisition Expenditures

406

$

9 Months YTD 2008

24

Potential Earn-out Obligations

The following is a calculation of future earn-out obligations as of

September 30, 2008, assuming that the underlying acquired agencies

continue to perform at their current levels: (a)

(a)

The ultimate payments will vary as they are dependent on future events and changes in FX rates.

2008

2009

2010

2011

Thereafter

Total

20

$

107

$

94

$

41

$

41

$

303

$

25

Potential Obligations

(a) The ultimate payments will vary as they are dependent on future events and changes in FX rates.

In conjunction with certain transactions, Omnicom has agreed to

acquire (at the sellers’ option) additional equity interests. If these rights

are exercised, there would likely be an increase in our net income as a

result of our increased ownership and the reduction of minority interest

expense. The following is a calculation of these potential future

obligations (as of September 30, 2008), assuming these underlying

acquired agencies continue to perform at their current levels: (a)

Currently

Exercisable

Not Currently

Exercisable

Total

Subsidiary Agencies

164

$

86

$

250

$

Affiliated Agencies

42

1

43

Total

206

$

87

$

293

$

26

Third Quarter Acquisitions

Barefoot

Barefoot is a fully integrated interactive marketing communication

agency. The company’s service programs include strategy, on-line,

consumer promotion, planning and advertising. From this platform the

company offers high quality end to end service in brand strategy, media

strategy & planning, relationship marketing and results measurement,

reporting and tracking.

Barefoot will be a part of Proximity within the BBDO network and is located

in Cincinnati, Ohio.

27

Third Quarter Acquisitions

Paul Wilmot Communications

Paul Wilmot Communications provides public relations, communications

and publicity services within the fashion and luxury goods arenas.

The agency is comprised of five divisions: Fashion, Beauty &

Wellness, Accessories, Culture & Lifestyle and Special Events.

Paul Wilmot Communications is based in New York and will operate

within Fleishman Hillard.

28

Third Quarter Acquisitions

TRO

TRO (The Russell Organization) is a leading experiential marketing and events agency, specializing in the use of face-to-face

communication and the live medium. TRO designs, produces and

delivers brand experiences and environments which achieve real

results for B2C and B2B clients. The spectrum of work includes road

shows, shopping center campaigns, live promotions exhibitions,

sponsorship activation, conferencing, new product launches, training and hospitality.

Located in Isleworth, England, TRO will become a part of CPM's

experiential marketing services delivery network.

29

Third Quarter Acquisitions

The Eleven Agency

The Eleven Agency is a field marketing communications company

specializing in Sales Training, Training Video Production, E-Learning,

Recruiting, Assisted Sales at Retail, Retail Merchandising and Field &

Event Marketing.

The Eleven Agency is located in Irvine, California and will become a

member of GMR Marketing.

30

Third Quarter Acquisitions

Tarek Nour

The DDB network acquired a 49% affiliate interest in TN Holdings, the

holding company for the Tarek Nour group.

Established in 1978, TN Holdings is one of Egypt’s largest marketing and

corporate communications companies. The group’s twenty companies

provide a wide range of services including advertising, media

research, planning & buying, brand design, television production,

event management & outdoor advertising services.

Tarek Nour is headquartered in Cairo, Egypt.