UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-02201

Insight Select Income Fund

(Exact name of registrant as specified in charter)

200 Park Avenue, 7th Floor

New York, NY 10166

(Address of principal executive offices) (Zip code)

Gautam Khanna

200 Park Avenue, 7th Floor

New York, NY 10166

(Name and address of agent for service)

Registrant’s telephone number, including area code: 212-527-1800

Date of fiscal year end: March 31

Date of reporting period: September 30, 2022

Item 1. Reports to Stockholders.

| (a) | The Report to Shareholders is attached herewith. |

Online:

Visit www.computershare.com/investor to log into your account and select “Communication Preferences” to set your preference.

Telephone:

Contact the Fund at 866-333-6685

Overnight Mail:

Computershare Investor Services, 462 South 4th Street, Suite 1600, Louisville, KY, 40202

Regular Mail:

Computershare Investor Services, PO Box 505000, Louisville, KY, 40233-5000

| 1 |

For the Six-Month Period Ended 09/30/22

November 2, 2022

DEAR SHAREHOLDERS:

The reporting period was marked by rising inflation and aggressive Federal Reserve (the “Fed”) monetary tightening, resulting in rising recession concerns. Further, Russia’s ongoing war in Ukraine added to market uncertainty. Most financial assets lost value across the globe.

The Fed took an increasingly aggressive stance with respect to monetary policy, driven by stronger-than-expected inflation. Initially, at the start of the period, the Fed was still not noticeably concerned about pricing pressures. However, as the Consumer Price Index (“CPI”) increased north of 9% the Fed became increasingly concerned, and vocal, about the risk of inflation becoming structurally embedded within the economy, which then drove it towards a more aggressive pace of monetary policy tightening. After peaking at 9.1%, the CPI has retreated towards 8% perhaps indicative that some of the policy tightening already in place is having the intended affect. A more concerning aspect of CPI has been a recent shift in pricing pressure from flexible components of the index, such as food, energy, and goods, to ‘stickier’ components of the index such as core services including rents, medical services, and education-related costs. In these stickier segments, inflation is more likely to be persistent.

Consistent with the concerns that inflation was not longer considered transitory, the Fed became increasingly hawkish, with its median forecast for end-2022 interest rates rising from 1.875% being predicted in March 2022 to 4.4% being predicted in September 20221. For end-2023, the forecast shifted from 2.75% to 4.6%. The Fed began tapering its bond purchases by $15 billion a month in November 2021, then swiftly accelerated the tapering to $30 billion a month later and that pace continues to this day. The Fed began raising interest rates in March 2022, including three consecutive 75 basis points (bps) hikes in June, July, and September. The Fed Funds rate ended the reporting period at 3.25%, well above its previous long-term estimate of the neutral rate being at 2.5% as of the same period end.

The US entered two quarters of negative real growth, at -0.41% and -0.14% for the first and second quarters of 2022 respectively, albeit real growth remained positive in nominal terms. It remains to be seen if the US will fall into an official recession (as will be determined by NBER, the National Bureau of Economic Research).

Other major central banks continued to adjust their monetary tightening policies. As a result, government bonds issued by the US and by other governments weakened significantly, with the 10-year US Treasury yield rising by 149bps to 3.8% during the period. Credit markets generally declined more than government bonds, as spreads widened by 44bps for US investment grade corporate bonds, albeit US credit markets significantly outperformed European credit markets generally.

Geopolitical events contributed to roiled markets early in 2022. The February 2022 invasion of Ukraine and the global sanctions imposed on Russia have led to spikes in energy and commodity prices. With these two countries being major producers of wheat and corn, those prices, as well as other industrial commodities, have risen since the start of the period. While Russian authorities may have expected to swiftly achieve their objective, their military advances slowed and, in some cases, have been reversed, leading to expectations that the conflict will persist for the foreseeable future.

| 1 | Federal Reserve quarterly projections, September 2022, https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20220921.htm |

| 2 |

Toward the end of the period, US and global markets also suffered volatility attributable to geopolitical developments when Chancellor of the Exchequer, Kwasi Kwarteng, a minister of the Crown within the Government of the United Kingdom, announced unfunded tax cuts aimed at stimulating the UK economy. This called into question the UK’s fiscal health, resulting in investors selling UK assets. Sharply rising UK government bond yields forced certain pension funds with liability-driven investment strategies to liquidate assets to meet collateral calls, setting off a feedback loop of further rising yields and more collateral calls. The Bank of England intervened by buying long-dated gilts and postponing planned sales of assets, which calmed UK and international markets with respect to this market event.

Towards the end of the period, the Fund began to moderate its high-yield and emerging market exposure given the aggressive pace of monetary policy tightening by many developed nations’ central banks which could increase the odds of the current economic expansion coming to an end. The current market volatility does create market dislocations and the Fund maintains adequate liquidity to capitalize on idiosyncratic opportunities that may present themselves. While being generally exposed to the credit markets, we continue to adjust the Fund’s portfolio positioning to focus on the parts of the credit curve that we believe provide the best tradeoff between risk and reward, in a volatile interest rate environment that we expect to continue to be volatile over the next year. Balance remains paramount as there are risks on both sides of any forecast. The Fund’s performance was a function of navigating a difficult rate environment while positioning the Fund to effectively target, durable and high-quality sources of predictable income from the now higher level of prevailing interest rates and credit spreads. We continue to resist the temptation to sacrifice portfolio liquidity in the hunt for yield, and we want to own assets we see exhibiting good visibility into the credit worthiness of issuers, stability of balance sheets, and overall staying power.

As of September 30, 2022, the Fund had a net asset value (NAV) of $16.67 per share. This represents a 14.91% decrease from $19.59 per share on March 31, 2022. On September 30, 2022, the Fund’s closing price on the New York Stock Exchange was $15.37 per share, representing a 7.80% discount to NAV per share, compared with an 8.78% discount as of March 31, 2022. One of the primary objectives of the Fund is to maintain a high level of income. On September 8, 2022, the Board of Trustees declared a dividend payment of $0.18 per share payable on October 12, 2022 to shareholders of record on September 30, 2022. On an annualized basis, including the pending dividend, the annual dividend payment from ordinary income equates to a total of $0.74 per share, representing a 4.94% dividend yield based on the market price on November 3, 2022 of $14.99 per share. The dividend is evaluated on a quarterly basis and is based on the income generation capability of the portfolio and is not guaranteed for any period of time.

Yield represents the major component of return in most fixed income portfolios. Given this Fund’s emphasis on income and the dividend, we generally will not have material exposure to low-yielding US Treasuries and will maintain meaningful exposure to corporate bonds. When it comes to management of credit risk, we try to look through periods of volatility to focus on an investment’s long-term creditworthiness to assess whether it will provide an attractive yield to the Fund over time.

| 3 |

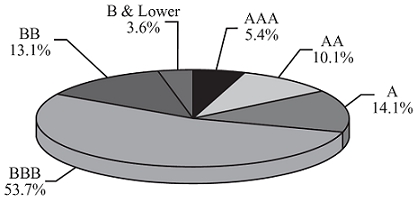

The Fund’s performance will continue to be subject to trends in long-term interest rates and to corporate yield spreads. Consistent with our investment discipline, we continue to emphasize diversification and risk management within the bounds of income stability. The pie chart below summarizes the portfolio quality of the Fund’s assets as of September 30, 2022:

Percent of Total Investment (Lower of S&P and Moody’s Ratings)1

| 1 | For financial reporting purposes, credit quality ratings shown above reflect the lowest rating assigned by either Standard & Poor’s (“S&P”) or Moody’s Investors Service (“Moody’s”) if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated NR are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings and the Fund’s allocation to the ratings categories are subject to change at any time without notice. |

We would like to remind shareholders of the opportunities presented by the Fund’s dividend reinvestment plan referred to in the Shareholder Information section of this report. The dividend reinvestment plan affords shareholders a price advantage by allowing them to purchase additional shares at NAV or market price, whichever is lower. This means that the reinvestment price is at market price when the Fund is trading at a discount to NAV, as is currently the situation, or at NAV per share when market trading is at a premium to that value. To participate in the plan, please contact Computershare Investor Services, the Fund’s Transfer Agent and Dividend Paying Agent, at 1-866-333-6685. The Fund’s investment adviser, Insight North America LLC, may be reached at 1-212-527-1800.

Gautam Khanna

President

Mr. Khanna’s comments reflect the investment adviser’s views generally regarding the market and the economy and are compiled from the investment adviser’s research. These comments reflect opinions as of the date written and are subject to change at any time.

Opinions expressed herein are current opinions of Insight and are subject to change without notice. Insight assumes no responsibility to update such information or to notify a client of any changes. Any outlooks, forecasts or portfolio

| 4 |

weightings presented herein are as of the date appearing on this material only and are also subject to change without notice. Insight disclaims any responsibility to update such views. No forecasts can be guaranteed.

Information herein may contain, include or is based upon forward-looking statements within the meaning of the federal securities laws, specifically Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements include all statements, other than statements of historical fact, that address future activities, events or developments, including without limitation, business or investment strategy or measures to implement strategy, competitive strengths, goals expansion and growth of our business, plans, prospects and references to future or success. You can identify these statements by the fact that they do not relate strictly to historical or current facts. Words such as ‘anticipate,’ ‘estimate,’ ‘expect,’ ‘project,’ ‘intend,’ ‘plan,’ ‘believe,’ and other similar words are intended to identify these forward-looking statements. Forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Many such factors will be important in determining our actual future results or outcomes. Consequently, no forward-looking statement can be guaranteed. Our actual results or outcomes may vary materially. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

Past performance is not a guide to future performance, which will vary. The value of investments and any income from them will fluctuate and is not guaranteed (this may partly be due to exchange rate changes). Future returns are not guaranteed and a loss of principal may occur.

The quoted benchmarks within this presentation do not reflect deductions for fees, expenses or taxes. These benchmarks are unmanaged and cannot be purchased directly by investors. Benchmark performance is shown for illustrative purposes only and does not predict or depict the performance of any investment. There may be material factors relevant to any such comparison such as differences in volatility, and regulatory and legal restrictions between the indices shown and the strategy.

| 5 |

Total Return-Percentage Change (Annualized for periods longer than 1 year)

In Net Asset Value Per Share with All Distributions Reinvested1

| 6 Months to 9/30/22 | 1 Year to 9/30/22 | 3 Years to 9/30/22 | 5 Years to 9/30/22 | 10 Years | |||||

| Insight Select Income Fund | -12.03% | -18.12% | -2.66% | 0.69% | 2.94% | ||||

| Bloomberg U.S. Credit Index2 | -7.21% | -4.16% | 2.81% | 3.18% | 3.44% |

| 1 − | Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment return does not reflect brokerage commissions. The total investment return, if for less than a full year, is not annualized. Past performance is not a guarantee of future results. |

| 2 − | Source: Bloomberg as of September 30, 2022. Comprised primarily of US investment grade corporate bonds (Fund’s Benchmark). |

| 6 |

| SCHEDULE OF INVESTMENTS (Unaudited) | September 30, 2022 |

| Moody’s/ Standard & Poor’s Rating(a) | Principal Amount (000’s) | Value (Note1) | ||||||||

| CORPORATE DEBT SECURITIES (76.96%) | ||||||||||

| AEROSPACE/DEFENSE (1.93%) | ||||||||||

| Boeing Co., Sr. Unsec. Notes, 4.875%, 05/01/25(b) | Baa2/BBB- | $ | 1,657 | $ | 1,618,726 | |||||

| Boeing Co., Sr. Unsec. Notes, 5.805%, 05/01/50(b) | Baa2/BBB- | 463 | 403,285 | |||||||

| Northrop Grumman Corp., Sr. Unsec. Notes, 3.250%, 01/15/28(b) | Baa1/BBB+ | 365 | 332,674 | |||||||

| Northrop Grumman Corp., Sr. Unsec. Notes, 7.750%, 06/01/29 | Baa1/BBB+ | 500 | 560,057 | |||||||

| Raytheon Technologies Corp., Sr. Unsec. Notes, 3.750%, 11/01/46(b) | Baa1/A- | 700 | 526,448 | |||||||

| 3,441,190 | ||||||||||

| AGRICULTURE (0.41%) | ||||||||||

| Altria Group, Inc., Co. Gty., 4.800%, 02/14/29(b) | A3/BBB | 97 | 89,576 | |||||||

| Altria Group, Inc., Co. Gty., 5.950%, 02/14/49(b) | A3/BBB | 329 | 272,437 | |||||||

| BAT International Finance PLC, Co. Gty., 1.668%, 03/25/26(b) | Baa2/BBB+ | 425 | 367,507 | |||||||

| 729,520 | ||||||||||

| AIRLINES (3.70%) | ||||||||||

| Air Canada, Sr. Sec. Notes, 3.875%, 08/15/26, 144A(b) | Ba2/BB- | 56 | 48,090 | |||||||

| Air Canada Pass Through Certs., Series 2020-2, Class A, 5.250%, 04/01/29, 144A | NA/A | 226 | 212,075 | |||||||

| American Airlines Group, Inc. Pass Through Certs., Series 2017-1, Class AA, 3.650%, 02/15/29 | Baa1/NA | 809 | 714,054 | |||||||

| American Airlines Group, Inc. Pass Through Certs., Series 2017-2, Class AA, 3.350%, 10/15/29 | Baa1/NA | 1,243 | 1,084,944 | |||||||

| American Airlines Group, Inc. Pass Through Certs., Series 2019-1, Class AA, 3.150%, 02/15/32 | Baa1/A- | 704 | 586,993 | |||||||

| American Airlines, Inc., Sr. Sec. Notes, 5.500%, 04/20/26, 144A | Ba2/NA | 354 | 332,466 | |||||||

| American Airlines, Inc., Sr. Sec. Notes, 5.750%, 04/20/29, 144A | Ba2/NA | 162 | 141,345 | |||||||

| British Airways PLC Pass Through Certs., Series 2020-1, Class A, 4.250%, 11/15/32, 144A | NA/A | 109 | 97,867 | |||||||

| Delta Air Lines, Inc., Sr. Sec. Notes, 4.500%, 10/20/25, 144A | Baa1/NA | 120 | 116,489 | |||||||

| Delta Air Lines, Inc., Sr. Sec. Notes, 4.750%, 10/20/28, 144A | Baa1/NA | 209 | 194,740 | |||||||

| JetBlue Airways Corp. Pass Through Certs., Series 2020-1, Class A, 4.000%, 11/15/32 | A2/NA | 968 | 861,306 | |||||||

| United Airlines, Inc., Sr. Sec. Notes, 4.375%, 04/15/26, 144A(b) | Ba1/BB- | 65 | 58,013 | |||||||

| United Airlines, Inc., Sr. Sec. Notes, 4.625%, 04/15/29, 144A(b) | Ba1/BB- | 318 | 263,940 | |||||||

| United Airlines, Inc. Pass Through Certs., Series 2018-1, Class B, 4.600%, 03/01/26 | Baa3/NA | 570 | 519,537 | |||||||

| United Airlines, Inc. Pass Through Certs., Series 2019-1, Class AA, 4.150%, 08/25/31 | A2/NA | 364 | 327,351 | |||||||

| United Airlines, Inc. Pass Through Certs., Series 2019-2, Class AA, 2.700%, 05/01/32 | A2/NA | 995 | 794,223 | |||||||

| United Airlines, Inc. Pass Through Certs., Series 2020-1, Class A, 5.875%, 10/15/27 | A3/A | 260 | 251,128 | |||||||

| 6,604,561 | ||||||||||

| AUTO MANUFACTURERS (2.94%) | ||||||||||

| Ford Holdings LLC, Co. Gty., 9.300%, 03/01/30 | Ba2/BB+ | 1,000 | 1,102,900 | |||||||

| Ford Motor Credit Co. LLC, Sr. Unsec. Notes, 3.370%, 11/17/23 | Ba2/BB+ | 500 | 483,715 | |||||||

| Ford Motor Credit Co. LLC, Sr. Unsec. Notes, 2.300%, 02/10/25(b) | Ba2/BB+ | 1,199 | 1,062,765 | |||||||

| Ford Motor Credit Co. LLC, Sr. Unsec. Notes, 4.542%, 08/01/26(b) | Ba2/BB+ | 1,356 | 1,206,972 | |||||||

| General Motors Co., Sr. Unsec. Notes, 6.800%, 10/01/27(b) | Baa3/BBB | 405 | 409,211 | |||||||

| General Motors Financial Co., Inc., Sr. Unsec. Notes, 3.600%, 06/21/30(b) | Baa3/BBB | 1,027 | 831,702 | |||||||

| Stellantis Finance US, Inc., Co. Gty., 2.691%, 09/15/31, 144A(b) | Baa2/BBB | 221 | 157,611 | |||||||

| 5,254,876 | ||||||||||

| BANKS (11.18%) | ||||||||||

| AIB Group PLC, Sr. Unsec. Notes, (3M LIBOR + 1.874%), 4.263%, 04/10/25, 144A(b),(c) | A3/BBB- | 582 | 557,987 | |||||||

| Citigroup, Inc., Jr. Sub. Notes, (H15T5Y + 3.597%), 4.000%, 12/10/25(b),(c),(d) | Ba1/BB+ | 635 | 533,489 | |||||||

| Citigroup, Inc., Sr. Unsec. Notes, 8.125%, 07/15/39 | A3/BBB+ | 70 | 82,910 | |||||||

| Citigroup, Inc., Sr. Unsec. Notes, (3M LIBOR + 1.563%), 3.887%, 01/10/28(b),(c) | A3/BBB+ | 1,100 | 1,012,774 | |||||||

| Citigroup, Inc., Sr. Unsec. Notes, (SOFRRATE + 1.887%), 4.658%, 05/24/28(b),(c) | A3/BBB+ | 1,302 | 1,239,395 | |||||||

| Citigroup, Inc., Sub. Notes, 4.600%, 03/09/26 | Baa2/BBB | 988 | 955,577 | |||||||

| Citigroup, Inc., Sub. Notes, 5.300%, 05/06/44 | Baa2/BBB | 926 | 807,046 | |||||||

| Credit Agricole SA, Sub. Notes, (SW5+ 1.644%), 4.000%, 01/10/33, 144A(b),(c) | Baa1/BBB+ | 1,025 | 883,773 | |||||||

| Credit Suisse AG, Sr. Unsec. Notes, (SOFRINDX + 1.260%), 3.969%, 02/21/25(e) | A2/A | 1,250 | 1,218,774 | |||||||

The accompanying notes are an integral part of these financial statements.

| 7 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

| Moody’s/ Standard & Poor’s Rating(a) | Principal Amount (000’s) | Value (Note1) | ||||||||

| CORPORATE DEBT SECURITIES (Continued) | ||||||||||

| BANKS (Continued) | ||||||||||

| Credit Suisse Group AG, Sr. Unsec. Notes, (SOFRRATE + 1.560%), 2.593%, 09/11/25, 144A(b),(c) | Baa2/BBB | $ | 1,242 | $ | 1,129,075 | |||||

| Goldman Sachs Group, Inc., Sr. Unsec. Notes, (3M LIBOR + 1.750%), 4.543%, 10/28/27(b),(e) | A2/BBB+ | 550 | 546,682 | |||||||

| Goldman Sachs Group, Inc., Sr. Unsec. Notes, (SOFRRATE + 1.725%), 4.482%, 08/23/28(b),(c) | A2/BBB+ | 703 | 660,378 | |||||||

| HSBC Capital Funding Dollar 1 LP, Co. Gty., (3M LIBOR + 4.980%), 10.176%, 06/30/30, 144A(b),(c),(d) | Baa3/BB+ | 2,180 | 2,753,159 | |||||||

| HSBC USA, Inc., Sr. Unsec. Notes, 3.750%, 05/24/24 | A1/A- | 1,955 | 1,916,588 | |||||||

| ING Groep NV, Sr. Unsec. Notes, (SOFRRATE + 1.640%), 3.869%, 03/28/26(b),(c) | Baa1/A- | 782 | 741,460 | |||||||

| Morgan Stanley, Sub. Notes, 4.350%, 09/08/26 | Baa1/BBB+ | 1,500 | 1,429,188 | |||||||

| PNC Financial Services Group, Inc., Jr. Sub. Notes, (3M LIBOR + 3.300%), 5.000%, 11/01/26(b),(c),(d) | Baa2/BBB- | 757 | 660,129 | |||||||

| Synchrony Bank, Sr. Unsec. Notes, 5.400%, 08/22/25(b) | NA/BBB | 305 | 297,431 | |||||||

| Truist Financial Corp., Jr. Sub. Notes, (H15T5Y + 3.003%), 4.800%, 09/01/24(b),(c),(d) | Baa2/BBB- | 1,136 | 1,011,346 | |||||||

| Wells Fargo & Co., Jr. Sub. Notes, (H15T5Y + 3.453%), 3.900%, 03/15/26(b),(c),(d) | Baa2/BB+ | 1,162 | 981,890 | |||||||

| Westpac Banking Corp., Sub. Notes, (H15T5Y + 1.750%), 2.668%, 11/15/35(b),(c) | Baa1/BBB+ | 753 | 553,491 | |||||||

| 19,972,542 | ||||||||||

| BEVERAGES (0.56%) | ||||||||||

| Anheuser-Busch Cos. LLC, Co. Gty., 4.700%, 02/01/36(b) | Baa1/BBB+ | 645 | 582,158 | |||||||

| Anheuser-Busch Cos. LLC, Co. Gty., 4.900%, 02/01/46(b) | Baa1/BBB+ | 446 | 386,528 | |||||||

| Anheuser-Busch InBev Worldwide, Inc., Co. Gty., 8.200%, 01/15/39 | Baa1/BBB+ | 27 | 32,601 | |||||||

| 1,001,287 | ||||||||||

| BIOTECHNOLOGY (0.53%) | ||||||||||

| Royalty Pharma PLC, Co. Gty., 2.200%, 09/02/30(b) | Baa3/BBB- | 930 | 709,982 | |||||||

| Royalty Pharma PLC, Co. Gty., 2.150%, 09/02/31(b) | Baa3/BBB- | 326 | 240,016 | |||||||

| 949,998 | ||||||||||

| BUILDING MATERIALS (0.71%) | ||||||||||

| Builders FirstSource, Inc., Co. Gty., 6.375%, 06/15/32, 144A(b) | Ba2/BB- | 64 | 56,857 | |||||||

| Cemex SAB de CV, Co. Gty., 7.375%, 06/05/27, 144A(b) | NA/BB | 200 | 198,000 | |||||||

| Masco Corp., Sr. Unsec. Notes, 1.500%, 02/15/28(b) | Baa2/BBB | 647 | 522,338 | |||||||

| Masonite International Corp., Co. Gty., 3.500%, 02/15/30, 144A(b) | Ba1/BB+ | 53 | 40,510 | |||||||

| SRM Escrow Issuer LLC, Sr. Sec. Notes, 6.000%, 11/01/28, 144A(b) | Ba3/B+ | 548 | 442,456 | |||||||

| 1,260,161 | ||||||||||

| CHEMICALS (2.88%) | ||||||||||

| Alpek SAB de CV, Co. Gty., 3.250%, 02/25/31, 144A(b) | Baa3/BBB- | 418 | 309,283 | |||||||

| Braskem Idesa SAPI, Sr. Sec. Notes, 7.450%, 11/15/29, 144A(b) | NA/B+ | 273 | 206,791 | |||||||

| Braskem Idesa SAPI, Sr. Sec. Notes, 6.990%, 02/20/32, 144A(b) | NA/B+ | 528 | 353,760 | |||||||

| Braskem Netherlands Finance BV, Co. Gty., 5.875%, 01/31/50, 144A | NA/BBB- | 1,181 | 836,739 | |||||||

| Celanese US Holdings LLC, Co. Gty., 6.165%, 07/15/27(b) | Baa3/BBB | 787 | 742,500 | |||||||

| Orbia Advance Corp. SAB de CV, Co. Gty., 2.875%, 05/11/31, 144A(b) | Baa3/BBB- | 574 | 417,988 | |||||||

| Trinseo Materials Operating SCA, Co. Gty., 5.125%, 04/01/29, 144A(b) | B2/B | 105 | 61,950 | |||||||

| Union Carbide Corp., Sr. Unsec. Notes, 7.750%, 10/01/96 | Baa1/BBB | 2,000 | 2,212,425 | |||||||

| 5,141,436 | ||||||||||

| COMMERCIAL SERVICES (1.78%) | ||||||||||

| Ashtead Capital, Inc., Co. Gty., 4.000%, 05/01/28, 144A(b) | Baa3/BBB- | 555 | 485,228 | |||||||

| Ashtead Capital, Inc., Co. Gty., 4.250%, 11/01/29, 144A(b) | Baa3/BBB- | 200 | 174,576 | |||||||

| Atento Luxco 1 SA, Sr. Sec. Notes, 8.000%, 02/10/26, 144A(b) | Ba3/NA | 249 | 105,162 | |||||||

| ERAC USA Finance LLC, Co. Gty., 7.000%, 10/15/37, 144A | Baa1/A- | 1,500 | 1,565,569 | |||||||

| Global Payments, Inc., Sr. Unsec. Notes, 5.400%, 08/15/32(b) | Baa3/BBB- | 274 | 253,092 | |||||||

The accompanying notes are an integral part of these financial statements.

| 8 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

| Moody’s/ Standard & Poor’s Rating(a) | Principal Amount (000’s) | Value (Note1) | ||||||||

| CORPORATE DEBT SECURITIES (Continued) | ||||||||||

| COMMERCIAL SERVICES (Continued) | ||||||||||

| Prime Security Services Borrower LLC, Sr. Sec. Notes, 3.375%, 08/31/27, 144A(b) | Ba3/BB- | $ | 559 | $ | 469,655 | |||||

| Triton Container International, Ltd., Co. Gty., 3.150%, 06/15/31, 144A(b) | NA/BBB- | 167 | 122,258 | |||||||

| 3,175,540 | ||||||||||

| COMPUTERS (0.62%) | ||||||||||

| Dell International LLC, Co. Gty., 3.450%, 12/15/51, 144A(b) | Baa2/BBB | 529 | 300,755 | |||||||

| Dell International LLC, Sr. Unsec. Notes, 5.850%, 07/15/25(b) | Baa2/BBB | 342 | 344,676 | |||||||

| Dell International LLC, Sr. Unsec. Notes, 8.350%, 07/15/46(b) | Baa2/BBB | 209 | 225,453 | |||||||

| Kyndryl Holdings, Inc., Sr. Unsec. Notes, 2.050%, 10/15/26(b) | NR/BBB- | 153 | 122,938 | |||||||

| Western Digital Corp., Sr. Unsec. Notes, 2.850%, 02/01/29(b) | Baa3/BB+ | 146 | 114,351 | |||||||

| 1,108,173 | ||||||||||

| DIVERSIFIED FINANCIAL SERVICES (1.33%) | ||||||||||

| AerCap Ireland Capital DAC, Co. Gty., 3.300%, 01/30/32(b) | Baa3/BBB | 519 | 389,786 | |||||||

| Intercontinental Exchange, Inc., Sr. Unsec. Notes, 4.350%, 06/15/29(b) | A3/A- | 358 | 338,827 | |||||||

| LSEGA Financing PLC, Co. Gty., 1.375%, 04/06/26, 144A(b) | A3/A | 612 | 536,394 | |||||||

| LSEGA Financing PLC, Co. Gty., 2.500%, 04/06/31, 144A(b) | A3/A | 264 | 214,319 | |||||||

| PennyMac Financial Services, Inc., Co. Gty., 5.750%, 09/15/31, 144A(b) | Ba3/BB- | 522 | 374,162 | |||||||

| Synchrony Financial, Sr. Unsec. Notes, 2.875%, 10/28/31(b) | NA/BBB- | 747 | 530,650 | |||||||

| 2,384,138 | ||||||||||

| ELECTRIC (6.52%) | ||||||||||

| AES Andes SA, Jr. Sub. Notes, (H15T5Y + 4.917%), 6.350%, 10/07/79, 144A(b),(c) | Ba2/BB | 878 | 755,269 | |||||||

| AES Panama Generation Holdings Srl, Sr. Sec. Notes, 4.375%, 05/31/30, 144A(b) | Baa3/NA | 549 | 432,337 | |||||||

| American Electric Power Co., Inc., Jr. Sub. Notes, 2.031%, 03/15/24 | Baa3/BBB+ | 1,952 | 1,868,586 | |||||||

| Berkshire Hathaway Energy Co., Sr. Unsec. Notes, 2.850%, 05/15/51(b) | A3/A- | 1,000 | 615,507 | |||||||

| Black Hills Corp., Sr. Unsec. Notes, 3.875%, 10/15/49(b) | Baa2/BBB+ | 1,175 | 843,587 | |||||||

| CMS Energy Corp., Jr. Sub. Notes, (H15T5Y + 2.900%), 3.750%, 12/01/50(b),(c) | Baa3/BBB- | 238 | 174,930 | |||||||

| Consorcio Transmantaro SA, Sr. Unsec. Notes, 4.700%, 04/16/34, 144A | Baa3/NA | 200 | 172,613 | |||||||

| Edison International, Jr. Sub. Notes, (H15T5Y + 4.698%), 5.375%, 03/15/26(b),(c),(d) | Ba2/BB+ | 638 | 528,742 | |||||||

| Edison International, Sr. Unsec. Notes, 3.550%, 11/15/24(b) | Baa3/BBB- | 575 | 552,205 | |||||||

| Evergy Metro, Inc., Sr. Sec. Notes, 4.200%, 06/15/47(b) | A2/A+ | 917 | 745,262 | |||||||

| FirstEnergy Corp., Sr. Unsec. Notes, 5.350%, 07/15/47(b),(f) | Ba1/BB+ | 1,570 | 1,325,064 | |||||||

| IPALCO Enterprises, Inc., Sr. Sec. Notes, 4.250%, 05/01/30(b) | Baa3/BBB- | 462 | 400,674 | |||||||

| Jersey Central Power & Light Co., Sr. Unsec. Notes, 2.750%, 03/01/32, 144A(b) | A3/BBB | 323 | 255,345 | |||||||

| Light Servicos de Eletricidade SA, Co. Gty., 4.375%, 06/18/26, 144A(b) | Ba3/NA | 456 | 378,740 | |||||||

| MidAmerican Funding LLC, Sr. Sec. Notes, 6.927%, 03/01/29 | A2/A- | 500 | 530,171 | |||||||

| Pacific Gas and Electric Co., 2.100%, 08/01/27(b) | Baa3/BBB- | 391 | 316,225 | |||||||

| Pacific Gas and Electric Co., 3.500%, 08/01/50(b) | Baa3/BBB- | 617 | 375,536 | |||||||

| Puget Energy, Inc., Sr. Sec. Notes, 2.379%, 06/15/28(b) | Baa3/BBB- | 247 | 205,626 | |||||||

| Transelec SA, Sr. Unsec. Notes, 4.250%, 01/14/25, 144A(b) | Baa1/BBB | 750 | 727,500 | |||||||

| Transelec SA, Sr. Unsec. Notes, 3.875%, 01/12/29, 144A(b) | Baa1/BBB | 490 | 436,713 | |||||||

| 11,640,632 | ||||||||||

| ENGINEERING & CONSTRUCTION (0.21%) | ||||||||||

| Sydney Airport Finance Co. Pty, Ltd., Sr. Sec. Notes, 3.375%, 04/30/25, 144A(b) | Baa1/BBB+ | 400 | 375,217 | |||||||

| ENTERTAINMENT (0.39%) | ||||||||||

| Lions Gate Capital Holdings LLC, Co. Gty., 5.500%, 04/15/29, 144A(b) | B3/CCC+ | 386 | 287,570 | |||||||

| Warnermedia Holdings, Inc., Co. Gty., 3.638%, 03/15/25, 144A | Baa3/BBB- | 441 | 417,692 | |||||||

| 705,262 | ||||||||||

| FOOD (0.56%) | ||||||||||

| Bimbo Bakeries USA, Inc., Co. Gty., 4.000%, 05/17/51, 144A(b) | Baa2/BBB | 363 | 266,178 | |||||||

| JBS USA LUX SA, Co. Gty., 3.750%, 12/01/31, 144A(b) | Baa3/BBB- | 54 | 43,229 | |||||||

| JBS USA LUX SA, Co. Gty., 3.625%, 01/15/32, 144A(b) | Baa3/NA | 211 | 164,844 | |||||||

| Kraft Heinz Foods Co., Co. Gty., 5.500%, 06/01/50(b) | Baa3/BBB- | 346 | 311,296 | |||||||

The accompanying notes are an integral part of these financial statements.

| 9 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

| Moody’s/ Standard & Poor’s Rating(a) | Principal Amount (000’s) | Value (Note1) | ||||||||

| CORPORATE DEBT SECURITIES (Continued) | ||||||||||

| FOOD (Continued) | ||||||||||

| Kroger Co., Sr. Unsec. Notes, 5.400%, 01/15/49(b) | Baa1/BBB | $ | 68 | $ | 63,253 | |||||

| MARB BondCo PLC, Co. Gty., 3.950%, 01/29/31, 144A(b) | NA/BB+ | 213 | 154,159 | |||||||

| 1,002,959 | ||||||||||

| FOREST PRODUCTS & PAPER (0.42%) | ||||||||||

| Inversiones CMPC SA, Co. Gty., 3.850%, 01/13/30, 144A(b) | Baa3/BBB- | 580 | 468,350 | |||||||

| Suzano Austria GmbH, Co. Gty., 3.750%, 01/15/31(b) | NA/BBB- | 351 | 274,991 | |||||||

| 743,341 | ||||||||||

| GAS (2.18%) | ||||||||||

| NiSource, Inc., Jr. Sub. Notes, (H15T5Y + 2.843%), 5.650%, 06/15/23(b),(c),(d) | NA/BBB- | 696 | 642,060 | |||||||

| Piedmont Natural Gas Co., Inc., Sr. Unsec. Notes, 3.500%, 06/01/29(b) | A3/BBB+ | 1,120 | 985,546 | |||||||

| Southern Co. Gas Capital Corp., Co. Gty., 5.875%, 03/15/41(b) | Baa1/BBB+ | 992 | 951,079 | |||||||

| Southern Co. Gas Capital Corp., Co. Gty., 3.950%, 10/01/46(b) | Baa1/BBB+ | 539 | 395,082 | |||||||

| Southern Co. Gas Capital Corp., Co. Gty., 4.400%, 05/30/47(b) | Baa1/BBB+ | 1,164 | 915,281 | |||||||

| 3,889,048 | ||||||||||

| HEALTHCARE-PRODUCTS (0.14%) | ||||||||||

| STERIS Irish FinCo UnLtd Co., Co. Gty., 2.700%, 03/15/31(b) | Baa2/BBB- | 329 | 258,420 | |||||||

| HEALTHCARE-SERVICES (0.36%) | ||||||||||

| CommonSpirit Health, Sr. Sec. Notes, 2.782%, 10/01/30(b) | Baa1/A- | 432 | 344,630 | |||||||

| HCA, Inc., Co. Gty., 3.125%, 03/15/27, 144A(b) | Baa3/BBB- | 119 | 105,396 | |||||||

| Tenet Healthcare Corp., Sr. Sec. Notes, 4.875%, 01/01/26, 144A(b) | B1/BB- | 201 | 186,783 | |||||||

| 636,809 | ||||||||||

| HOUSEWARES (0.16%) | ||||||||||

| Newell Brands, Inc., Sr. Unsec. Notes, 6.375%, 09/15/27(b) | Ba1/BBB- | 157 | 155,466 | |||||||

| Newell Brands, Inc., Sr. Unsec. Notes, 6.625%, 09/15/29(b) | Ba1/BBB- | 139 | 135,905 | |||||||

| 291,371 | ||||||||||

| INSURANCE (8.43%) | ||||||||||

| Allianz SE, Jr. Sub. Notes, (H15T5Y + 2.165%), 3.200%, 10/30/27, 144A(b),(c),(d) | Baa1/A | 200 | 128,999 | |||||||

| Allianz SE, Jr. Sub. Notes, (H15T5Y + 2.973%), 3.500%, 11/17/25, 144A(b),(c),(d) | Baa1/A | 400 | 306,176 | |||||||

| Allstate Corp., Jr. Sub. Notes, (3M LIBOR + 2.120%), 6.500%, 05/15/57(b),(c) | Baa1/BBB | 2,200 | 2,154,432 | |||||||

| Farmers Exchange Capital, Sub. Notes, 7.200%, 07/15/48, 144A | Baa2/BBB+ | 2,250 | 2,397,715 | |||||||

| Guardian Life Insurance Co. of America, Sub. Notes, 4.850%, 01/24/77, 144A | Aa3/AA- | 148 | 120,285 | |||||||

| Jackson National Life Global Funding, 1.750%, 01/12/25, 144A | A2/A | 656 | 602,911 | |||||||

| Liberty Mutual Group, Inc., Co. Gty., 3.951%, 10/15/50, 144A(b) | Baa2/BBB | 250 | 168,229 | |||||||

| Liberty Mutual Group, Inc., Co. Gty., (3M LIBOR + 7.120%), 10.750%, 06/15/58, 144A(b),(c) | Baa3/BB+ | 1,000 | 1,309,630 | |||||||

| Massachusetts Mutual Life Insurance Co., Sub. Notes, 3.729%, 10/15/70, 144A | A2/AA- | 243 | 161,441 | |||||||

| Massachusetts Mutual Life Insurance Co., Sub. Notes, 4.900%, 04/01/77, 144A | A2/AA- | 980 | 790,797 | |||||||

| MetLife, Inc., Jr. Sub. Notes, 6.400%, 12/15/36(b) | Baa2/BBB | 637 | 614,567 | |||||||

| MetLife, Inc., Jr. Sub. Notes, 10.750%, 08/01/39(b) | Baa2/BBB | 1,000 | 1,302,259 | |||||||

| MetLife, Inc., Jr. Sub. Notes, 9.250%, 04/08/38, 144A(b) | Baa2/BBB | 1,059 | 1,215,569 | |||||||

| Nationwide Mutual Insurance Co., Sub. Notes, 8.250%, 12/01/31, 144A | A3/A- | 500 | 562,997 | |||||||

| Nationwide Mutual Insurance Co., Sub. Notes, 9.375%, 08/15/39, 144A | A3/A- | 215 | 273,006 | |||||||

| New York Life Insurance Co., Sub. Notes, 6.750%, 11/15/39, 144A | Aa2/AA- | 103 | 111,998 | |||||||

| Principal Financial Group, Inc., Co. Gty., (3M LIBOR + 3.044%), 5.949%, 05/15/55(b),(e) | Baa2/BBB | 1,135 | 1,084,842 | |||||||

| Prudential Financial, Inc., Jr. Sub. Notes, (3M LIBOR + 2.665%), 5.700%, 09/15/48(b),(c) | Baa1/BBB+ | 1,241 | 1,158,784 | |||||||

| Prudential Financial, Inc., Jr. Sub. Notes, (3M LIBOR + 3.920%), 5.625%, 06/15/43(b),(c) | Baa1/BBB+ | 600 | 591,156 | |||||||

| 15,055,793 | ||||||||||

The accompanying notes are an integral part of these financial statements.

| 10 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

| Moody’s/ Standard & Poor’s Rating(a) | Principal Amount (000’s) | Value (Note1) | ||||||||

| CORPORATE DEBT SECURITIES (Continued) | ||||||||||

| INTERNET (0.42%) | ||||||||||

| Meta Platforms, Inc., Sr. Unsec. Notes, 4.450%, 08/15/52, 144A(b) | A1/AA- | $ | 500 | $ | 408,101 | |||||

| Prosus NV, Sr. Unsec. Notes, 4.987%, 01/19/52, 144A(b) | Baa3/BBB | 540 | 350,266 | |||||||

| 758,367 | ||||||||||

| MEDIA (6.94%) | ||||||||||

| AMC Networks, Inc., Co. Gty., 4.250%, 02/15/29(b) | Ba3/BB | 885 | 654,182 | |||||||

| CCO Holdings LLC, Sr. Unsec. Notes, 4.500%, 05/01/32(b) | B1/BB- | 1,017 | 775,635 | |||||||

| Charter Communications Operating LLC, Sr. Sec. Notes, 5.750%, 04/01/48(b) | Ba1/BBB- | 389 | 314,003 | |||||||

| Comcast Corp., Co. Gty., 7.050%, 03/15/33 | A3/A- | 2,000 | 2,192,219 | |||||||

| Cox Communications, Inc., Sr. Unsec. Notes, 6.800%, 08/01/28 | Baa2/BBB | 1,500 | 1,540,309 | |||||||

| Cox Enterprises, Inc., Sr. Unsec. Notes, 7.375%, 07/15/27, 144A. | Baa2/BBB | 500 | 526,393 | |||||||

| CSC Holdings LLC, Co. Gty., 6.500%, 02/01/29, 144A(b) | Ba3/BB- | 954 | 845,793 | |||||||

| CSC Holdings LLC, Sr. Unsec. Notes, 4.625%, 12/01/30, 144A(b) | B3/B | 1,336 | 906,944 | |||||||

| Grupo Televisa SAB, Sr. Unsec. Notes, 6.625%, 01/15/40 | Baa2/BBB+ | 159 | 156,030 | |||||||

| Paramount Global, Sr. Unsec. Notes, 4.200%, 05/19/32(b) | Baa2/BBB | 641 | 518,701 | |||||||

| Paramount Global, Sr. Unsec. Notes, 6.875%, 04/30/36 | Baa2/BBB | 179 | 167,469 | |||||||

| Radiate Holdco LLC, Sr. Sec. Notes, 4.500%, 09/15/26, 144A(b) | B1/B | 124 | 101,709 | |||||||

| Scripps Escrow II, Inc., Sr. Sec. Notes, 3.875%, 01/15/29, 144A(b) | Ba3/BB | 42 | 33,742 | |||||||

| Time Warner Entertainment Co. LP, Sr. Sec. Notes, 8.375%, 07/15/33 | Ba1/BBB- | 1,360 | 1,450,163 | |||||||

| Virgin Media Finance PLC, Co. Gty., 5.000%, 07/15/30, 144A(b) | B2/B | 200 | 150,094 | |||||||

| VTR Finance NV, Sr. Unsec. Notes, 6.375%, 07/15/28, 144A(b) | B1/B | 443 | 244,757 | |||||||

| Walt Disney Co., Co. Gty., 7.900%, 12/01/95 | A2/BBB+ | 1,400 | 1,815,506 | |||||||

| 12,393,649 | ||||||||||

| MINING (0.64%) | ||||||||||

| Alcoa Nederland Holding BV, Co. Gty., 5.500%, 12/15/27, 144A(b) | Baa3/BB+ | 655 | 610,886 | |||||||

| AngloGold Ashanti Holdings PLC, Co. Gty., 3.750%, 10/01/30(b) | Baa3/BB+ | 339 | 262,764 | |||||||

| Newcrest Finance Pty, Ltd., Co. Gty., 3.250%, 05/13/30, 144A(b) | Baa2/BBB | 319 | 265,715 | |||||||

| 1,139,365 | ||||||||||

| MISCELLANEOUS MANUFACTURING (0.16%) | ||||||||||

| GE Capital International Funding Co Unlimited Co., Co. Gty., 4.418%, 11/15/35 | Baa1/BBB+ | 318 | 285,432 | |||||||

| OIL & GAS (3.02%) | ||||||||||

| Aker BP ASA, Co. Gty., 3.100%, 07/15/31, 144A(b) | Baa2/BBB | 426 | 333,382 | |||||||

| CITGO Petroleum Corp., Sr. Sec. Notes, 7.000%, 06/15/25, 144A(b) | B3/B+ | 248 | 236,971 | |||||||

| Endeavor Energy Resources LP, Sr. Unsec. Notes, 5.750%, 01/30/28, 144A(b) | Ba2/BB+ | 473 | 451,124 | |||||||

| EQT Corp., Sr. Unsec. Notes, 5.678%, 10/01/25(b) | Ba1/BBB- | 124 | 123,362 | |||||||

| Exxon Mobil Corp., Sr. Unsec. Notes, 4.227%, 03/19/40(b) | Aa2/AA- | 1,402 | 1,217,438 | |||||||

| Parkland Corp., Co. Gty., 4.500%, 10/01/29, 144A(b) | Ba3/BB | 667 | 538,511 | |||||||

| Petroleos Mexicanos, Co. Gty., 5.950%, 01/28/31(b) | B1/BBB | 552 | 372,821 | |||||||

| Petroleos Mexicanos, Co. Gty., 6.950%, 01/28/60(b) | B1/BBB | 195 | 108,011 | |||||||

| Saudi Arabian Oil Co., Sr. Unsec. Notes, 2.250%, 11/24/30, 144A(b) | A1/NA | 853 | 687,931 | |||||||

| Valero Energy Corp., Sr. Unsec. Notes, 8.750%, 06/15/30 | Baa2/BBB | 1,000 | 1,164,424 | |||||||

| Valero Energy Corp., Sr. Unsec. Notes, 4.000%, 06/01/52(b) | Baa2/BBB | 215 | 155,151 | |||||||

| 5,389,126 | ||||||||||

| OIL & GAS SERVICES (0.16%) | ||||||||||

| Baker Hughes Holdings LLC, Sr. Unsec. Notes, 2.061%, 12/15/26(b) | A3/A- | 326 | 286,661 | |||||||

| PACKAGING & CONTAINERS (0.51%) | ||||||||||

| Ardagh Metal Packaging Finance USA LLC, Sr. Sec. Notes, 6.000%, 06/15/27, 144A(b) | Ba2/BB | 200 | 188,341 | |||||||

| Ardagh Metal Packaging Finance USA LLC, Sr. Unsec. Notes, 4.000%, 09/01/29, 144A(b) | B3/B+ | 200 | 147,000 | |||||||

| LABL, Inc., Sr. Sec. Notes, 5.875%, 11/01/28, 144A(b) | B2/B- | 173 | 140,112 | |||||||

| Sealed Air Corp., Sr. Sec. Notes, 1.573%, 10/15/26, 144A(b) | Baa2/BBB- | 524 | 438,885 | |||||||

| 914,338 | ||||||||||

The accompanying notes are an integral part of these financial statements.

| 11 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

| Moody’s/ Standard & Poor’s Rating(a) | Principal Amount (000’s) | Value (Note1) | ||||||||

| CORPORATE DEBT SECURITIES (Continued) | ||||||||||

| PHARMACEUTICALS (1.12%) | ||||||||||

| AbbVie, Inc., Sr. Unsec. Notes, 4.050%, 11/21/39(b) | Baa2/BBB+ | $ | 615 | $ | 496,086 | |||||

| Astrazeneca Finance LLC, Co. Gty., 1.750%, 05/28/28(b) | A3/A- | 475 | 399,438 | |||||||

| Organon & Co, Sr. Sec. Notes, 4.125%, 04/30/28, 144A(b) | Ba2/BB | 200 | 170,106 | |||||||

| Takeda Pharmaceutical Co., Ltd., Sr. Unsec. Notes, 5.000%, 11/26/28(b) | Baa2/BBB+ | 500 | 484,265 | |||||||

| Takeda Pharmaceutical Co., Ltd., Sr. Unsec. Notes, 3.175%, 07/09/50(b) | Baa2/BBB+ | 684 | 453,837 | |||||||

| 2,003,732 | ||||||||||

| PIPELINES (6.73%) | ||||||||||

| Cheniere Energy Partners LP, Co. Gty., 3.250%, 01/31/32(b) | Ba1/BB+ | 91 | 70,687 | |||||||

| DT Midstream, Inc., Sr. Sec. Notes, 4.300%, 04/15/32, 144A(b) | Baa2/BBB- | 432 | 370,290 | |||||||

| EIG Pearl Holdings Sarl, Sr. Sec. Notes, 4.387%, 11/30/46, 144A | A1/NA | 700 | 493,704 | |||||||

| Enbridge, Inc., Sub. Notes, (3M LIBOR + 3.890%), 6.000%, 01/15/77(b),(c) | Baa3/BBB- | 750 | 670,887 | |||||||

| Energy Transfer LP, Sr. Unsec. Notes, 3.750%, 05/15/30(b) | Baa3/BBB- | 398 | 336,881 | |||||||

| Enterprise Products Operating LLC, Co. Gty., (3M LIBOR + 2.570%), 5.375%, 02/15/78(b),(c) | Baa2/BBB- | 342 | 256,780 | |||||||

| Florida Gas Transmission Co. LLC, Sr. Unsec. Notes, 9.190%, 11/01/24, 144A | Baa2/BBB+ | 30 | 29,927 | |||||||

| Global Partners LP, Co. Gty., 7.000%, 08/01/27(b) | B2/B+ | 1,076 | 979,730 | |||||||

| Hess Midstream Operations LP, Co. Gty., 5.500%, 10/15/30, 144A(b) | Ba2/BB+ | 70 | 60,092 | |||||||

| Howard Midstream Energy Partners LLC, Sr. Unsec. Notes, 6.750%, 01/15/27, 144A(b) | B3/B | 110 | 98,116 | |||||||

| Kinder Morgan, Inc., Co. Gty., 8.050%, 10/15/30 | Baa2/BBB | 1,000 | 1,067,771 | |||||||

| Kinder Morgan, Inc., Co. Gty., 5.550%, 06/01/45(b) | Baa2/BBB | 1,755 | 1,529,837 | |||||||

| MPLX LP, Sr. Unsec. Notes, 4.250%, 12/01/27(b) | Baa2/BBB | 901 | 839,218 | |||||||

| MPLX LP, Sr. Unsec. Notes, 5.500%, 02/15/49(b) | Baa2/BBB | 694 | 589,093 | |||||||

| MPLX LP, Sr. Unsec. Notes, 4.900%, 04/15/58(b) | Baa2/BBB | 561 | 418,709 | |||||||

| NGPL PipeCo LLC, Sr. Unsec. Notes, 7.768%, 12/15/37, 144A | Baa3/BBB- | 880 | 888,984 | |||||||

| Panhandle Eastern Pipe Line Co. LP, Sr. Unsec. Notes, 7.000%, 07/15/29 | Baa3/BBB- | 1,000 | 1,007,592 | |||||||

| Targa Resources Partners LP, Co. Gty., 5.500%, 03/01/30(b) | Baa3/BBB- | 1,177 | 1,062,125 | |||||||

| Transcontinental Gas Pipe Line Co. LLC, Sr. Unsec. Notes, 3.950%, 05/15/50(b) | Baa1/BBB | 384 | 283,386 | |||||||

| Williams Cos., Inc., Sr. Unsec. Notes, 7.500%, 01/15/31 | Baa2/BBB | 911 | 976,831 | |||||||

| 12,030,640 | ||||||||||

| REITS (1.78%) | ||||||||||

| EPR Properties, Sr. Unsec. Notes, 3.600%, 11/15/31(b) | Baa3/BBB- | 533 | 380,640 | |||||||

| Extra Space Storage LP, Co. Gty., 3.900%, 04/01/29(b) | Baa2/BBB | 371 | 330,467 | |||||||

| Extra Space Storage LP, Co. Gty., 2.350%, 03/15/32(b) | Baa2/BBB | 267 | 196,626 | |||||||

| GLP Capital LP, Co. Gty., 3.250%, 01/15/32(b) | Ba1/BBB- | 154 | 115,923 | |||||||

| Iron Mountain, Inc., Co. Gty., 5.000%, 07/15/28, 144A(b) | Ba3/BB- | 59 | 50,740 | |||||||

| SBA Tower Trust, 2.593%, 10/15/31, 144A(b) | A2/NA | 454 | 354,239 | |||||||

| Scentre Group Trust 2, Co. Gty., (H15T5Y + 4.379%), 4.750%, 09/24/80, 144A(b),(c) | Baa1/BBB+ | 2,007 | 1,723,602 | |||||||

| WEA Finance LLC, Co. Gty., 4.625%, 09/20/48, 144A(b) | Baa2/BBB+ | 36 | 25,029 | |||||||

| 3,177,266 | ||||||||||

| RETAIL (1.01%) | ||||||||||

| Macy’s Retail Holdings LLC, Co. Gty., 5.875%, 03/15/30, 144A(b) | Ba2/BB | 314 | 248,358 | |||||||

| Murphy Oil USA, Inc., Co. Gty., 3.750%, 02/15/31, 144A(b) | Ba2/BB+ | 119 | 95,638 | |||||||

| Starbucks Corp., Sr. Unsec. Notes, 4.450%, 08/15/49(b) | Baa1/BBB+ | 1,781 | 1,455,554 | |||||||

| 1,799,550 | ||||||||||

| SEMICONDUCTORS (1.25%) | ||||||||||

| Broadcom, Inc., Co. Gty., 3.750%, 02/15/51, 144A(b) | Baa3/BBB- | 166 | 108,877 | |||||||

| Broadcom, Inc., Sr. Unsec. Notes, 3.469%, 04/15/34, 144A(b) | Baa3/BBB- | 1,655 | 1,241,000 | |||||||

| Broadcom, Inc., Sr. Unsec. Notes, 3.187%, 11/15/36, 144A(b) | Baa3/BBB- | 1,109 | 758,017 | |||||||

| Micron Technology, Inc., Sr. Unsec. Notes, 2.703%, 04/15/32(b) | Baa3/BBB- | 164 | 119,111 | |||||||

| 2,227,005 | ||||||||||

| SOFTWARE (1.60%) | ||||||||||

| Oracle Corp., Sr. Unsec. Notes, 2.300%, 03/25/28(b) | Baa2 -/BBB | 1,130 | 944,250 | |||||||

The accompanying notes are an integral part of these financial statements.

| 12 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

| Moody’s/ Standard & Poor’s Rating(a) | Principal Amount (000’s) | Value (Note1) | ||||||||

| CORPORATE DEBT SECURITIES (Continued) | ||||||||||

| SOFTWARE (Continued) | ||||||||||

| Oracle Corp., Sr. Unsec. Notes, 3.650%, 03/25/41(b) | Baa2 -/BBB | $ | 1,745 | $ | 1,185,769 | |||||

| Take-Two Interactive Software, Inc., Sr. Unsec. Notes, 3.700%, 04/14/27(b) | Baa2/BBB | 165 | 153,240 | |||||||

| VMware, Inc., Sr. Unsec. Notes, 2.200%, 08/15/31(b) | Baa3/BBB- | 788 | 573,291 | |||||||

| 2,856,550 | ||||||||||

| TELECOMMUNICATIONS (3.13%) | ||||||||||

| AT&T, Inc., Sr. Unsec. Notes, 4.500%, 05/15/35(b) | Baa2/BBB | 515 | 445,178 | |||||||

| AT&T, Inc., Sr. Unsec. Notes, 4.750%, 05/15/46(b) | Baa2/BBB | 425 | 356,257 | |||||||

| AT&T, Inc., Sr. Unsec. Notes, 3.550%, 09/15/55(b) | Baa2/BBB | 2,195 | 1,439,690 | |||||||

| Deutsche Telekom International Finance BV, Co. Gty., 8.750%, 06/15/30(f) | Baa1/BBB | 2,000 | 2,290,597 | |||||||

| Frontier Communications Holdings LLC, Sr. Sec. Notes, 5.000%, 05/01/28, 144A(b) | B3/B | 255 | 218,841 | |||||||

| Verizon Communications, Inc., Sr. Unsec. Notes, 2.550%, 03/21/31(b) | Baa1/BBB+ | 457 | 365,277 | |||||||

| Verizon Communications, Inc., Sr. Unsec. Notes, 3.550%, 03/22/51(b) | Baa1/BBB+ | 674 | 474,004 | |||||||

| 5,589,844 | ||||||||||

| TRANSPORTATION (0.55%) | ||||||||||

| BNSF Funding Trust I, Co. Gty., (3M LIBOR + 2.350%), 6.613%, 12/15/55(b),(c) | Baa2/A | 250 | 234,004 | |||||||

| Simpar Europe SA, Co. Gty., 5.200%, 01/26/31, 144A(b) | NA/BB- | 544 | 383,068 | |||||||

| Union Pacific Corp., Sr. Unsec. Notes, 3.839%, 03/20/60(b) | A3/A- | 503 | 372,265 | |||||||

| 989,337 | ||||||||||

| TOTAL CORPORATE DEBT SECURITIES (Cost of $156,162,556) | 137,463,136 | |||||||||

| ASSET-BACKED SECURITIES (12.51%) | ||||||||||

| Aligned Data Centers Issuer LLC, Series 2021-1A, Class A2, 1.937%, 08/15/46, 144A(b) | NA/A- | 904 | 771,010 | |||||||

| Amur Equipment Finance Receivables XI LLC, Series 2022-2A, Class A2, 5.300%, 06/21/28, 144A(b) | Aaa/NA | 100 | 99,396 | |||||||

| Antares CLO, Ltd., Series 2017-1A, Class CR, (3M LIBOR + 2.700%), 5.410%, 04/20/33, 144A(b),(e) | NA/A | 1,092 | 959,400 | |||||||

| Apidos CLO XXXIX, Series 2022-39A, Class A1, (TSFR3M + 1.300%), 2.039%, 04/21/35, 144A(b),(e) | Aaa/AA+ | 950 | 901,908 | |||||||

| Blackbird Capital Aircraft, Series 2021-1A, Class B, 3.446%, 07/15/46, 144A(b) | Baa1/NA | 348 | 261,485 | |||||||

| Cerberus Loan Funding XXXVII LP, Series 2022-1A, Class A1, (TSFR3M + 1.780%), 4.108%, 04/15/34, 144A(b),(e) | Aaa/NA | 1,500 | 1,426,209 | |||||||

| CF Hippolyta Issuer LLC, Series 2020-1, Class A1, 1.690%, 07/15/60, 144A(b) | NA/AA- | 626 | 556,108 | |||||||

| DataBank Issuer, Series 2021-2A, Class A2, 2.400%, 10/25/51, 144A(b) | NA/NA | 583 | 502,047 | |||||||

| DB Master Finance LLC, Series 2021-1A, Class A2I, 2.045%, 11/20/51, 144A(b) | NA/BBB | 603 | 513,971 | |||||||

| Domino’s Pizza Master Issuer LLC, Series 2021-1A, Class A2I, 2.662%, 04/25/51, 144A(b) | NA/BBB+ | 545 | 450,816 | |||||||

| DRB Prime Student Loan Trust, Series 2017-A, Class A2B, 2.850%, 05/27/42, 144A(b) | NA/NA | 61 | 60,884 | |||||||

| Eaton Vance CLO, Ltd., Series 2020-1A, Class AR, (3M LIBOR + 1.170%), 3.682%, 10/15/34, 144A(b),(e) | NA/AAA | 1,500 | 1,435,437 | |||||||

| Flexential Issuer, Series 2021-1A, Class A2, 3.250%, 11/27/51, 144A(b) | NA/NA | 555 | 482,832 | |||||||

| Ford Credit Auto Owner Trust, Series 2022-C, Class B, 5.030%, 02/15/28(b) | Aaa/AA+ | 565 | 559,509 | |||||||

| Fortress Credit Opportunities IX CLO, Ltd., Series 2017-9A, Class A1TR, (3M LIBOR + 1.550%), 4.062%, 10/15/33, 144A(b),(e) | NA/AAA | 600 | 567,987 | |||||||

| Golub Capital Partners CLO 36m, Ltd., Series 2018-36A, Class C, (3M LIBOR + 2.100%), 4.932%, 02/05/31, 144A(b),(e) | NA/A | 2,250 | 2,031,014 | |||||||

| ITE Rail Fund Levered LP, Series 2021-1A, Class A, 2.250%, 02/28/51, 144A(b) | NA/A | 188 | 160,183 | |||||||

| IVY Hill Middle Market Credit Fund XII, Ltd., Series 12A, Class BR, (3M LIBOR + 2.900%), 5.610%, 07/20/33, 144A(b),(e) | NA/A- | 866 | 756,933 | |||||||

| LoanCore Issuer, Ltd., Series 2018-CRE1, Class A, (1M LIBOR + 1.130%), 3.948%, 05/15/28, 144A(b),(e) | Aaa/AA+ | 6 | 6,136 | |||||||

| Marlette Funding Trust, Series 2022-3A, Class A, 5.180%, 11/15/32, 144A(b) | NA/NA | 129 | 128,469 | |||||||

| MCF CLO IX, Ltd., Series 2019-1A, Class A1R, (TSFR3M + 1.500%), 3.981%, 07/17/31, 144A(b),(e) | NA/AAA | 556 | 540,397 | |||||||

| MF1, Ltd., Series 2021-FL7, Class AS, (1M LIBOR + 1.450%), 4.443%, 10/16/36, 144A(b),(e) | NA/NA | 923 | 885,607 | |||||||

The accompanying notes are an integral part of these financial statements.

| 13 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

| Moody’s/ Standard & Poor’s Rating(a) | Principal Amount (000’s) | Value (Note1) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||||

| MF1, Ltd., Series 2022-FL8, Class C, (SOFRRATE 30 Day Average + 2.200%), 4.484%, 02/19/37, 144A(b),(e) | NA/NA | $ | 448 | $ | 427,201 | |||||

| Navient Private Education Refi Loan Trust, Series 2021-A, Class A, 0.840%, 05/15/69, 144A(b) | NA/AAA | 113 | 99,414 | |||||||

| Neuberger Berman Loan Advisers CLO 47, Ltd., Series 2022-47A, Class A, (TSFR3M + 1.300%), 3.598%, 04/14/35, 144A(b),(e) | Aaa/NA | 937 | 896,791 | |||||||

| New Economy Assets Phase 1 Sponsor LLC, Series 2021-1, Class A1, 1.910%, 10/20/61, 144A(b) | NA/AA- | 1,063 | 899,791 | |||||||

| PMT Issuer Trust - FMSR, Series 2021-FT1, Class A, (1M LIBOR + 3.000%), 6.084%, 03/25/26, 144A(b),(e) | NA/NA | 566 | 528,680 | |||||||

| Purewest Funding LLC, Series 2021-1, Class A1, 4.091%, 12/22/36, 144A(b) | NA/NA | 236 | 223,980 | |||||||

| Santander Drive Auto Receivables Trust, Series 2022-5, Class C, 4.740%, 10/16/28(b) | Aa1/A | 352 | 342,725 | |||||||

| Slam, Ltd., Series 2021-1A, Class A, 2.434%, 06/15/46, 144A(b) | A1/NA | 1,240 | 1,017,420 | |||||||

| SMB Private Education Loan Trust, Series 2017-B, Class A2B, (1M LIBOR + 0.750%), 3.568%, 10/15/35, 144A(b),(e) | Aaa/AAA | 341 | 336,949 | |||||||

| Sofi Professional Loan Program LLC, Series 2017-C, Class B, 3.560%, 07/25/40, 144A(b),(e) | NA/AA+ | 1,099 | 1,023,085 | |||||||

| Textainer Marine Containers VII, Ltd., Series 2021-1A, Class A, 1.680%, 02/20/46, 144A(b) | NA/A | 900 | 761,073 | |||||||

| TIF Funding II LLC, Series 2021-1A, Class A, 1.650%, 02/20/46, 144A(b) | NA/A | 480 | 397,194 | |||||||

| United States Small Business Administration, Series 2010-20F, Class 1, 3.880%, 06/01/30 | Aaa/AA+ | 43 | 42,289 | |||||||

| Willis Engine Structured Trust IV, Series 2018-A, Class A, 4.750%, 09/15/43, 144A(b),(g) | NA/A | 1,132 | 813,409 | |||||||

| Willis Engine Structured Trust VI, Series 2021-A, Class A, 3.104%, 05/15/46, 144A(b) | NA/NA | 643 | 470,915 | |||||||

| TOTAL ASSET-BACKED SECURITIES (Cost of $25,004,461) | 22,338,654 | |||||||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES (0.67%) | ||||||||||

| Angel Oak Mortgage Trust I LLC, Series 2019-2, Class A1, 3.628%, 03/25/49, 144A(b),(e) | NA/NA | 1 | 636 | |||||||

| BXHPP Trust, Series 2021-FILM, Class C, (1M LIBOR + 1.100%), 3.918%, 08/15/36, 144A(b),(e) | NA/NA | 167 | 154,261 | |||||||

| New Residential Mortgage Loan Trust, Series 2022-NQM1, Class A1, 2.277%, 01/25/26, 144A(b),(e) | NA/NA | 962 | 814,253 | |||||||

| New Residential Mortgage Loan Trust, Series 2021-NQ2R, Class A1, 0.941%, 10/25/58, 144A(b),(e) | NA/NA | 235 | 220,377 | |||||||

| TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES (Cost of $1,364,920) | 1,189,527 | |||||||||

| RESIDENTIAL MORTGAGE-BACKED SECURITIES (0.12%) | ||||||||||

| FHLMC Pool #A15675, 6.000%, 11/01/33 | Aaa/AA+ | 40 | 42,431 | |||||||

| FNMA Pool #754791, 6.500%, 12/01/33 | Aaa/AA+ | 118 | 121,592 | |||||||

| FNMA Pool #763852, 5.500%, 02/01/34 | Aaa/AA+ | 54 | 54,877 | |||||||

| GNSF Pool #417239, 7.000%, 02/15/26. | Aaa/AA+ | 2 | 1,599 | |||||||

| GNSF Pool #780374, 7.500%, 12/15/23(h) | Aaa/AA+ | 0 | 139 | |||||||

| TOTAL RESIDENTIAL MORTGAGE-BACKED SECURITIES (Cost of $204,056) | 220,638 | |||||||||

| MUNICIPAL BONDS (1.30%) | ||||||||||

| City of San Francisco CA Public Utilities Commission Water Revenue, Build America Bonds, 6.000%, 11/01/40 | Aa2/AA- | 145 | 155,932 | |||||||

| State of California, Build America Bonds, GO, 7.625%, 03/01/40 | Aa2/AA- | 1,500 | 1,860,767 | |||||||

| University of Michigan, 3.599%, 04/01/47 | Aaa/AAA | 365 | 303,156 | |||||||

| TOTAL MUNICIPAL BONDS (Cost of $2,041,467) | 2,319,855 | |||||||||

| U.S. TREASURY OBLIGATIONS (5.16%) | ||||||||||

| United States Treasury Bonds, 2.375%, 02/15/42 | Aaa/AA+ | 169 | 129,293 | |||||||

| United States Treasury Bonds, 3.250%, 05/15/42 | Aaa/AA+ | 637 | 565,526 | |||||||

| United States Treasury Bonds, 1.250%, 05/15/50 | Aaa/AA+ | 4,254 | 2,381,797 | |||||||

| United States Treasury Bonds, 2.875%, 05/15/52 | Aaa/AA+ | 553 | 463,913 | |||||||

| United States Treasury Bonds, 3.000%, 08/15/52 | Aaa/AA+ | 77 | 66,842 | |||||||

| United States Treasury Notes, 0.500%, 04/30/27 | Aaa/AA+ | 466 | 396,695 | |||||||

| United States Treasury Notes, 0.500%, 06/30/27 | Aaa/AA+ | 45 | 38,286 | |||||||

| United States Treasury Notes, 2.250%, 08/15/27 | Aaa/AA+ | 519 | 477,255 | |||||||

The accompanying notes are an integral part of these financial statements.

| 14 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

Moody’s/ Standard & Poor’s Rating(a) | Principal Amount (000’s) | Value (Note1) | ||||||||

| U.S. TREASURY OBLIGATIONS (Continued) | ||||||||||

| United States Treasury Notes, 0.625%, 11/30/27 | Aaa/AA+ | $ | 623 | $ | 523,594 | |||||

| United States Treasury Notes, 1.250%, 09/30/28 | Aaa/AA+ | 231 | 196,747 | |||||||

| United States Treasury Notes, 2.375%, 03/31/29 | Aaa/AA+ | 845 | 765,566 | |||||||

| United States Treasury Notes, 3.250%, 06/30/29 | Aaa/AA+ | 195 | 186,645 | |||||||

| United States Treasury Notes, 1.625%, 08/15/29 | Aaa/AA+ | 95 | 81,780 | |||||||

| United States Treasury Notes, 3.125%, 08/31/29 | Aaa/AA+ | 110 | 104,543 | |||||||

| United States Treasury Notes, 1.875%, 02/15/32 | Aaa/AA+ | 438 | 371,153 | |||||||

| United States Treasury Notes, 2.875%, 05/15/32 | Aaa/AA+ | 999 | 923,387 | |||||||

| United States Treasury Notes, 2.750%, 08/15/32 | Aaa/AA+ | 1,701 | 1,554,280 | |||||||

| TOTAL U.S. TREASURY OBLIGATIONS (Cost of $10,230,468) | 9,227,302 | |||||||||

| GOVERNMENT BONDS (1.63%) | ||||||||||

| Hungary Government International Bond, Sr. Unsec. Notes, 5.500%, 06/16/34, 144A | Baa2/BBB | 410 | 345,773 | |||||||

| Hydro-Quebec, 8.250%, 04/15/26 | Aa2/AA- | 1,550 | 1,728,502 | |||||||

| Korea National Oil Corp., Sr. Unsec. Notes, 1.750%, 04/18/25, 144A | Aa2/AA | 208 | 191,310 | |||||||

| Mexico Government International Bond, Sr. Unsec. Notes, 5.000%, 04/27/51(b) | Baa2/BBB | 711 | 546,795 | |||||||

| Ukraine Government International Bond, Sr. Unsec. Notes, 7.253%, 03/15/35, 144A | NA/CCC+ | 551 | 101,181 | |||||||

| TOTAL GOVERNMENT BONDS (Cost of $3,347,357) | 2,913,561 | |||||||||

| Shares | ||||||||||

| PREFERRED STOCKS (1.12%) | ||||||||||

| CoBank ACB, Series F, (3M LIBOR + 4.557%), 6.250%, 10/01/22(b),(c),(d) | NA/BBB+ | 20,000 | 2,000,000 | |||||||

| TOTAL INVESTMENTS (99.47%) (Cost of $200,440,285) | 177,672,673 | |||||||||

| OTHER ASSETS AND LIABILITIES (0.53%) | 950,841 | |||||||||

| NET ASSETS (100.00%) | $ | 178,623,514 | ||||||||

At September 30, 2022, the Fund had the following open futures contracts:

| Long Futures Outstanding | Expiration Month | Number of Contracts | Notional Amount | Value | Unrealized Appreciation (Depreciation) | |||||||||||

| U.S. Treasury 2-Year Notes | 12/22 | 9 | $ | 1,862,914 | $ | 1,848,516 | $ | (14,398 | ) | |||||||

| U.S. Treasury Long Bonds | 12/22 | 136 | 18,474,223 | 17,191,250 | (1,282,973 | ) | ||||||||||

| U.S. Treasury Ultra Bonds | 12/22 | 30 | 4,411,311 | 4,110,000 | (301,311 | ) | ||||||||||

| (1,598,682 | ) | |||||||||||||||

| Short Futures Outstanding | ||||||||||||||||

| U.S. Treasury 10-Year Notes | 12/22 | 28 | (3,254,668 | ) | (3,137,750 | ) | 116,918 | |||||||||

| U.S. Treasury 5-Year Notes | 12/22 | 137 | (15,016,092 | ) | (14,728,570 | ) | 287,522 | |||||||||

| U.S. Treasury Ultra 10-Year Notes | 12/22 | 128 | (16,028,153 | ) | (15,166,001 | ) | 862,152 | |||||||||

| 1,266,592 | ||||||||||||||||

| Net unrealized depreciation on open futures contracts | $ | (332,090 | ) | |||||||||||||

| (a) | Ratings for debt securities are unaudited. All ratings are as of September 30, 2022 and may have changed subsequently. |

| (b) | This security is callable. |

| (c) | Fixed to floating rate security. Fixed rate indicated is rate effective at September 30, 2022. Security will convert at a future date to a floating rate of reference rate and spread in the description above. |

| (d) | Security is perpetual. Date shown is next call date. |

| (e) | Variable rate security. Rate indicated is rate effective at September 30, 2022. |

| (f) | Multi-Step Coupon. Rate disclosed is as of September 30, 2022. |

The accompanying notes are an integral part of these financial statements.

| 15 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

| (g) | Denotes a step-up bond. The rate indicated is the current coupon as of September 30, 2022. |

| (h) | Principal amount less than $1,000. |

| 144A | Securities were purchased pursuant to Rule 144A under the Securities Act of 1933 and may not be resold subject to that rule except to qualified institutional buyers. At September 30, 2022, these securities amounted to $66,143,937 or 37.03% of net assets. |

Legend

Certs. – Certificates

CLO – Collateralized Loan Obligation

Co. Gty. – Company Guaranty

FHLMC – Federal Home Loan Mortgage Corporation

FNMA – Federal National Mortgage Association

GNSF – Government National Mortgage Association (Single Family)

GO – Government Obligation

H15T5Y – US Treasury Yield Curve Rate T Note Constant Maturity 5 Year

Jr. – Junior

LIBOR – London Interbank Offered Rate

LLC – Limited Liability Company

LP – Limited Partnership

Ltd. – Limited

PLC – Public Limited Company

REIT – Real Estate Investment Trust

Sec. – Secured

SOFRRATE – Secured Overnight Financing Rate

Sr. – Senior

Sub. – Subordinated

SW5 – 5-year USD Swap Semiannual 30/360

TSFR3M – 3 Month Term Secured Overnight Financing Rate

Unsec. – Unsecured

The accompanying notes are an integral part of these financial statements.

| 16 |

SCHEDULE OF INVESTMENTS (Unaudited) — continued

Following is a description of the valuation techniques applied to the Fund’s major categories of assets measured at fair value on a recurring basis as of September 30, 2022.

| Assets: | Total Market Value at 09/30/22 | Level 1 Quoted Price | Level 2 Significant Observable Inputs | Level 3 Significant Unobservable Inputs | ||||||||||||

| LONG-TERM INVESTMENTS | ||||||||||||||||

| CORPORATE DEBT SECURITIES | $ | 137,463,136 | $ | — | $ | 137,463,136 | $ | — | ||||||||

| U.S. TREASURY OBLIGATIONS | 9,227,302 | — | 9,227,302 | — | ||||||||||||

| MUNICIPAL BONDS | 2,319,855 | — | 2,319,855 | — | ||||||||||||

| GOVERNMENT BONDS | 2,913,561 | — | 2,913,561 | — | ||||||||||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES | 1,189,527 | — | 1,189,527 | — | ||||||||||||

| ASSET-BACKED SECURITIES | 22,338,654 | — | 22,338,654 | — | ||||||||||||

| PREFERRED STOCKS | 2,000,000 | 2,000,000 | — | — | ||||||||||||

| RESIDENTIAL MORTGAGE-BACKED SECURITIES | 220,638 | — | 220,638 | — | ||||||||||||

| DERIVATIVES | ||||||||||||||||

| SHORT FUTURES | 1,266,592 | 1,266,592 | — | — | ||||||||||||

| TOTAL ASSETS | $ | 178,939,265 | $ | 3,266,592 | $ | 175,672,673 | $ | — | ||||||||

| Liabilities: | ||||||||||||||||

| FUTURES CONTRACTS | $ | 1,598,682 | $ | 1,598,682 | $ | — | $ | — | ||||||||

The accompanying notes are an integral part of these financial statements.

| 17 |

STATEMENT OF ASSETS AND LIABILITIES (Unaudited)

September 30, 2022

| Assets: | ||||

| Investment in securities, at value (amortized cost $200,440,285) (Note 1) | $ | 177,672,673 | ||

| Cash | 607,709 | |||

| Interest receivable | 2,200,496 | |||

| Receivable from broker—variation margin on open futures contracts | 1,266,592 | |||

| Dividend receivable | 31,250 | |||

| Deposits with brokers for open futures contracts | 676,694 | |||

| TOTAL ASSETS | 182,455,414 | |||

| Liabilities: | ||||

| Dividend payable (Note 9) | 1,928,414 | |||

| Payable to broker—variation margin on open futures contracts | 1,598,682 | |||

| Securities purchased | 124,000 | |||

| Management fees payable | 69,655 | |||

| Audit fees payable | 44,090 | |||

| Printing fees payable | 20,925 | |||

| Administration and accounting fees payable | 13,864 | |||

| Custodian fees payable | 11,578 | |||

| Transfer agency fees payable | 1,980 | |||

| Accrued fees payable | 18,712 | |||

| TOTAL LIABILITIES | 3,831,900 | |||

| Net assets: (equivalent to $16.67 per share based on 10,713,411 shares of capital stock outstanding) | $ | 178,623,514 | ||

| NET ASSETS consisted of: | ||||

| Par value | $ | 107,134 | ||

| Capital paid-in | 206,647,413 | |||

| Distributable earnings | (28,131,033 | ) | ||

| $ | 178,623,514 |

The accompanying notes are an integral part of these financial statements.

| 18 |

STATEMENT OF OPERATIONS (Unaudited)

For the six months ended September 30, 2022

| Investment Income: | ||||||||

| Interest | $ | 4,459,041 | ||||||

| Dividends | 62,500 | |||||||

| Total Investment Income | 4,521,541 | |||||||

| Expenses: | ||||||||

| Investment advisory fees (Note 4) | $ | 439,031 | ||||||

| Administration fees | 85,541 | |||||||

| Trustees’ fees (Note 4) | 76,562 | |||||||

| Legal fees and expenses | 51,051 | |||||||

| Reports to shareholders | 25,524 | |||||||

| Custodian fees | 18,811 | |||||||

| Insurance | 17,991 | |||||||

| NYSE fee | 15,463 | |||||||

| Transfer agent fees | 14,957 | |||||||

| Audit fees | 14,590 | |||||||

| ICI fee | 9,046 | |||||||

| Interest expense (Note 6) | 1,834 | |||||||

| Miscellaneous | 42,269 | |||||||

| Total Expenses | 812,670 | |||||||

| Net Investment Income | 3,708,871 | |||||||

| Realized and unrealized (loss) from: | ||||||||

| Net realized (loss) from: | ||||||||

| Investment securities | (904,002 | ) | ||||||

| Futures contracts | (275,729 | ) | ||||||

| Swap agreements | (29,404 | ) | ||||||

| Net Realized Loss | (1,209,135 | ) | ||||||

| Change in net unrealized (depreciation) of: | ||||||||

| Investment securities | (27,557,447 | ) | ||||||

| Futures contracts | (383,004 | ) | ||||||

| Change in Net Unrealized Depreciation | (27,940,451 | ) | ||||||

| Net loss on investments and futures contracts | (29,149,586 | ) | ||||||

| Net decrease in net assets resulting from operations | $ | (25,440,715 | ) | |||||

The accompanying notes are an integral part of these financial statements.

| 19 |

STATEMENTS OF CHANGES IN NET ASSETS

| Six months ended September 30, 2022 (Unaudited) | Year ended March 31, 2022 | |||||||

| Increase (decrease) in net assets: | ||||||||

| Operations: | ||||||||

| Net investment income | $ | 3,708,871 | $ | 7,536,451 | ||||

| Net realized gain (loss) | (1,209,135 | ) | 2,002,564 | |||||

| Change in unrealized depreciation | (27,940,451 | ) | (15,198,222 | ) | ||||

| Net decrease in net assets resulting from operations | (25,440,715 | ) | (5,659,207 | ) | ||||

| Distributions: | ||||||||

| From distributed earnings | (5,785,242 | ) | (12,199,801 | ) | ||||

| Fund Share Transactions: | ||||||||

| Increase from shares issued under the dividend and distribution reinvestment plan (Note 5) | — | 71,360 | ||||||

| Decrease in net assets | (31,225,957 | ) | (17,787,648 | ) | ||||

| Net Assets: | ||||||||

| Beginning of period | 209,849,471 | 227,637,119 | ||||||

| End of period | $ | 178,623,514 | $ | 209,849,471 | ||||

The accompanying notes are an integral part of these financial statements.

| 20 |

FINANCIAL HIGHLIGHTS

The table below sets forth financial data for a share of capital stock outstanding throughout each period presented.

| Six-months ended September 30, 2022 | Year ended March 31, | |||||||||||||||||||||||

| (Unaudited) | 2022 | 2021 | 2020 | 2019 | 2018 | |||||||||||||||||||

| Per Share Operating Performance | ||||||||||||||||||||||||

| Net asset value, beginning of period | $ | 19.59 | $ | 21.25 | $ | 19.67 | $ | 20.57 | $ | 20.55 | $ | 20.75 | ||||||||||||

| Net investment income | 0.35 | 0.70 | 0.77 | 0.79 | 0.85 | 0.87 | ||||||||||||||||||

| Net gain (loss) on investments and futures contracts | (2.73 | ) | (1.22 | ) | 2.10 | (0.50 | ) | (0.03 | ) | (0.03 | ) | |||||||||||||

| Total from investment operations | (2.38 | ) | (0.52 | ) | 2.87 | 0.29 | 0.82 | 0.84 | ||||||||||||||||

| Less distributions: | ||||||||||||||||||||||||

| Dividends from net investment income | (0.54 | ) | (0.80 | ) | (0.80 | ) | (0.97 | ) | (0.67 | ) | (0.80 | ) | ||||||||||||

| Distributions from net realized gains | — | (0.34 | ) | (0.49 | ) | (0.22 | ) | (0.13 | ) | (0.24 | ) | |||||||||||||

| Total distributions | (0.54 | ) | (1.14 | ) | (1.29 | ) | (1.19 | ) | (0.80 | ) | (1.04 | ) | ||||||||||||

| Net asset value, end of period | $ | 16.67 | $ | 19.59 | $ | 21.25 | $ | 19.67 | $ | 20.57 | $ | 20.55 | ||||||||||||

| Per share market price, end of period | $ | 15.37 | $ | 17.87 | $ | 20.45 | $ | 19.74 | $ | 19.22 | $ | 19.37 | ||||||||||||

| Total Investment Return(1) | ||||||||||||||||||||||||

| Based on net asset value | (12.03 | )% | (2.80 | )% | 14.71 | % | 1.51 | % | 4.52 | % | 4.26 | % | ||||||||||||

| Based on market value | (11.09 | )% | (7.87 | )% | 10.00 | % | 9.03 | % | 3.60 | % | 6.43 | % | ||||||||||||

| Ratios/Supplemental Data | ||||||||||||||||||||||||

| Net assets, end of period (000s) | $ | 178,624 | $ | 209,849 | $ | 227,637 | $ | 210,632 | $ | 220,355 | $ | 220,141 | ||||||||||||

| Ratio of expenses to average net assets (gross of waivers/reimbursements) | 0.84 | % | 0.85 | % | 0.81 | % | 0.76 | % | 0.80 | % | 0.75 | % | ||||||||||||

| Ratio of expenses to average net assets (net of waivers/reimbursements) | 0.84 | % | 0.85 | % | 0.79 | % | 0.76 | % | 0.77 | % | 0.74 | % | ||||||||||||

| Ratio of net investment income to average net assets | 3.82 | % | 3.31 | % | 3.56 | % | 3.76 | % | 4.24 | % | 4.15 | % | ||||||||||||

| Portfolio turnover rate | 20.13 | % | 51.47 | % | 88.81 | % | 59.99 | % | 63.00 | % | 55.62 | % | ||||||||||||

| Number of shares outstanding at the end of the period (in 000’s) | 10,713 | 10,713 | 10,710 | 10,710 | 10,710 | 10,710 | ||||||||||||||||||

| (1) | Total investment return is calculated assuming a purchase of common shares at the market price on the first day and a sale at the market price on the last day of the period reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment return does not reflect brokerage commissions. The total investment return, if for less than a full year, is not annualized. Past performance is not a guarantee of future results. |

The accompanying notes are an integral part of these financial statements.

| 21 |

NOTES TO FINANCIAL STATEMENTS (Unaudited)

Note 1 − Significant Accounting Policies – The Insight Select Income Fund (the “Fund”), a Delaware statutory trust, is registered under the Investment Company Act of 1940, as amended (“1940 Act”), as a diversified closed-end, management investment company. The Fund’s investment objective is to seek a high rate of return, primarily from interest income and trading activity, from a portfolio principally consisting of debt securities. The Fund follows the accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification Topic 946, “Financial Services – Investment Companies”. The following is a summary of significant accounting policies consistently followed by the Fund in preparation of its financial statements. The policies are in conformity with generally accepted accounting principles within the United States of America (“GAAP”).

| A. | Security Valuation – In valuing the Fund’s net assets, all securities for which representative market quotations are available will be valued at the last quoted sales price on the security’s principal exchange on the day of valuation. If there are no sales of the relevant security on such day, the security will be valued at the bid price at the time of computation. For securities traded in the over-the-counter market, including listed debt and preferred securities, whose primary market is believed to be over-the-counter, the Fund uses recognized industry pricing services which are unaffiliated with Insight North America LLC (‘‘INA’’ or the ‘‘Adviser’’) - and uses broker quotes provided by market makers of securities not valued by these and other recognized pricing sources. |

In the event that market quotations are not readily available, or when such quotations are deemed not to reflect current market value, the securities will be valued at their respective fair value as determined by the Fund’s Valuation Designee pursuant to its procedures and subject to oversight by the Board. The Valuation Designee considers all relevant facts that are reasonably available when determining the fair value of a security, including but not limited to the last sale price or initial purchase price (if a when-issued security) and subsequently adjusting the value based on changes in company specific fundamentals, changes in an appropriate securities index, or changes in the value of similar securities which may be further adjusted for any discounts related to security-specific resale restrictions. When possible, observable market inputs such as unadjusted quoted prices of similar securities, observable interest rates, currency rates and yield curves are utilized. At September 30, 2022, there were no securities valued using fair value procedures.

The Fund adopted policies to comply with the SEC’s new Rule 2a-5 under the 1940 Act, which established a new regulatory framework for registered investment company fair valuation practices. The Fund’s fair value policies and procedures and valuation practices were updated prior to the rule’s required compliance date of September 8, 2022. Under Rule 2a-5, the Fund’s Board of Directors designated the Advisor as the Fund’s “Valuation Designee” to make fair value determinations.

Fair Value Measurements – The Fund has adopted authoritative fair value accounting standards which establish a definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value, a discussion in changes in valuation techniques and related inputs during the period and expanded disclosure of valuation levels for major security types. These inputs are summarized in the three broad levels listed below:

| • Level 1 – | Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. |

| 22 |

NOTES TO FINANCIAL STATEMENTS (Unaudited) — continued

| • Level 2 – | Observable inputs other than quoted prices included in level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. | |

| • Level 3 – | Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

At the end of each calendar quarter, management evaluates the Level 1, 2 and 3 assets and liabilities for changes in liquidity, including but not limited to: whether a broker is willing to execute at the quoted price, the depth and consistency of prices from third party services, and the existence of contemporaneous, observable trades in the market. Additionally, management evaluates Level 1 and 2 assets and liabilities on a quarterly basis for changes in listings or delistings on national exchanges. Due to the inherent uncertainty of determining the fair value of investments that do not have a readily available market value, the fair value of the Fund’s investments may fluctuate from period to period. Additionally, the fair value of investments may differ significantly from the values that would have been used had a ready market existed for such investments and may differ materially from the values the Fund may ultimately realize. Further, such investments may be subject to legal and other restrictions on resale or otherwise less liquid than publicly traded securities.

Level 3 investments are categorized as Level 3 with values derived utilizing prices from prior transactions or third party pricing information without adjustment (broker quotes, pricing services and net asset values). A significant change in third party pricing information could result in a significantly lower or higher value in such Level 3 investments. As of September 30, 2022, the Fund did not hold any Level 3 securities.

When-Issued Securities — The Fund may enter into commitments to purchase securities on a forward or when-issued basis. When-issued securities are securities purchased for delivery beyond the normal settlement date at a stated price and yield. In the Fund’s case, these securities are subject to settlement within 45 days of the purchase date. The interest rate realized on these securities is fixed as of the purchase date. The Fund does not pay for such securities prior to the settlement date and no interest accrues to the Fund before settlement. These securities are subject to market fluctuation due to changes in market interest rates. The Fund will enter into these commitments with the intent of buying the security but may dispose of such security prior to settlement. At the time the Fund makes the commitment to purchase securities on a when-issued basis, it will record the transaction and thereafter reflect the value of such security purchased in determining its net asset value (‘‘NAV’’). At the time of delivery of the security, its value may be more or less than the fixed purchase price.

Futures Contracts — The Fund uses futures contracts generally to gain exposure to, or hedge against, changes in interest rates or gain exposure to, or hedge against, changes in certain asset classes. A futures contract represents a commitment for the future purchase or sale of an asset at a specified price on a specified date.

Upon entering into a futures contract, the Fund is required to deposit cash or cash equivalents with a broker in an amount equal to a certain percentage of the contract amount. This is known as the ‘‘initial margin’’ and

| 23 |

NOTES TO FINANCIAL STATEMENTS (Unaudited) — continued

subsequent payments (‘‘variation margin’’) are made or received by the Fund each day, depending on the daily fluctuation in the value of the contract. For certain futures, including foreign denominated futures, variation margin is not settled daily, but is recorded as a net variation margin payable or receivable. The daily changes in contract value are recorded as unrealized gains or losses in the Statement of Operations and the Fund recognizes a realized gain or loss when the contract is closed.

Futures contracts involve, to varying degrees, risk of loss in excess of the amounts reflected in the financial statements. In addition, there is the risk that the Fund may not be able to enter into a closing transaction because of an illiquid secondary market.

Swap Contracts — Fund may enter into swap transactions to help enhance the value of its portfolio or manage its exposure to different types of investments. Swaps are financial instruments that typically involve the exchange of cash flows between two parties on specified dates (settlement dates), where the cash flows are based on agreed-upon prices, rates, indexes, etc. The nominal amount on which the cash flows are calculated is called the notional amount. Swaps are individually negotiated and structured to include exposure to a variety of different types of investments or market factors, such as interest rates, foreign currency rates, mortgage securities, corporate borrowing rates, security prices, indexes or inflation rates.

Swap agreements may increase or decrease the overall volatility of the investments of a Fund and its share price. The performance of swap agreements may be affected by a change in the specific interest rate, currency, or other factors that determine the amounts of payments due to and from a Fund. If a swap agreement calls for payments by a Fund, the Fund must be prepared to make such payments when due. In addition, if the counterparty’s creditworthiness declines, the value of a swap agreement would be likely to decline, potentially resulting in losses.

Generally, bilateral swap agreements, OTC swaps have a fixed maturity date that will be agreed upon by the parties. The agreement can be terminated before the maturity date only under limited circumstances, such as default by one of the parties or insolvency, among others, and can be transferred by a party only with the prior written consent of the other party. A Fund may be able to eliminate its exposure under a swap agreement either by assignment or by other disposition, or by entering into an offsetting swap agreement with the same party or a similarly creditworthy party. If the counterparty is unable to meet its obligations under the contract, declares bankruptcy, defaults or becomes insolvent, a Fund may not be able to recover the money it expected to receive under the contract.