UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811 - 0523 | |||||

|

| |||||

| The Dreyfus Fund Incorporated |

| ||||

| (Exact name of Registrant as specified in charter) |

| ||||

|

|

| ||||

|

c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 |

| ||||

| (Address of principal executive offices) (Zip code) |

| ||||

|

|

| ||||

| John Pak, Esq. 200 Park Avenue New York, New York 10166 |

| ||||

| (Name and address of agent for service) |

| ||||

| ||||||

Registrant's telephone number, including area code: | (212) 922-6000 | |||||

|

| |||||

Date of fiscal year end:

| 12/31 |

| ||||

Date of reporting period: | 12/31/13 |

| ||||

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Contents | |

THE FUND | |

| 2 | A Letter from the President |

| 3 | Discussion of Fund Performance |

| 6 | Fund Performance |

| 7 | Understanding Your Fund’s Expenses |

| 7 | Comparing Your Fund’s Expenses With Those of Other Funds |

| 8 | Statement of Investments |

| 12 | Statement of Assets and Liabilities |

| 13 | Statement of Operations |

| 14 | Statement of Changes in Net Assets |

| 15 | Financial Highlights |

| 16 | Notes to Financial Statements |

| 25 | Report of Independent Registered Public Accounting Firm |

| 26 | Important Tax Information |

| 26 | Proxy Results |

| 27 | Information About the Renewal of the Fund’s Management Agreement |

| 32 | Board Members Information |

| 35 | Officers of the Fund |

FOR MORE INFORMATION | |

Back Cover |

The Dreyfus Fund

Incorporated

The Fund

A LETTER FROM THE PRESIDENT

Dear Shareholder:

We are pleased to present this annual report for The Dreyfus Fund Incorporated, covering the 12-month period from January 1, 2013, through December 31, 2013. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

The year 2013 proved to be outstanding for U.S. equities. Large-cap stocks delivered their strongest calendar-year performance in well over a decade, and small- and midcap stocks fared even better in an environment of low short-term interest rates, rising corporate earnings, sustained economic growth, and low inflation. In our view, 2013 provided ample evidence of the value of patience and discipline in equity investing, as those who favored a long-term perspective over a focus on news headlines and short-term volatility reaped the rewards provided by rising markets.

Will stocks continue to rally in 2014? We believe that they can. We expect the domestic economy to continue to strengthen over the next year, particularly if U.S. fiscal policy is less restrictive and short-term interest rates remain near historical lows. Stronger growth could convince businesses and consumers to spend more freely, unleashing pent up demand as economic uncertainty wanes. However, we caution that gains in 2014 are unlikely to match those of the past year, and a highly selective approach to security selection could be key to greater relative investment success in the months ahead. As always, we urge you to speak with your financial adviser to identify the investment strategies that are right for you.

Thank you for your continued confidence and support.

Sincerely,

J. Charles Cardona

President

The Dreyfus Corporation

January 15, 2014

2

DISCUSSION OF FUND PERFORMANCE

For the period of January 1, 2013, through December 31, 2013, as provided by Sean P. Fitzgibbon, David Sealy, and Barry K. Mills, Primary Portfolio Managers

Market and Fund Performance Overview

For the 12-month period ended December 31, 2013,The Dreyfus Fund Incorporated produced a total return of 32.33%.1 In comparison, the Standard & Poor’s 500® Composite Stock Price Index (“S&P 500 Index”), the fund’s benchmark, provided a total return of 32.37% for the same period.2

Equities rallied strongly in 2013 as U.S. economic growth accelerated in the midst of an aggressively accommodative monetary policy from the Federal Reserve Board (the “Fed”).The fund participated in the market’s rise, roughly matching its benchmark’s returns, with particularly strong contributions from investments in the consumer discretionary and financial sectors.

The Fund’s Investment Approach

The fund seeks long-term capital growth consistent with the preservation of capital. Current income is a secondary goal. To pursue these goals, the fund focuses on large-capitalization U.S. companies with strong positions in their industries and catalysts that can trigger a price increase. We use fundamental analysis to create a broadly diversified portfolio composed of a blend of growth stocks, value stocks, and stocks that exhibit characteristics of both investment styles. We select stocks based on how shares are priced relative to the underlying company’s perceived intrinsic worth, the sustainability or growth of earnings or cash flow, and the company’s financial health.

Economic Growth and Fed Policies Drove Markets Higher

Stocks gained substantial ground in 2013 during a sustained economic recovery that saw U.S. GDP accelerate from a 1.1% annualized rate during the first quarter of the year to 4.1% for the third quarter. Economic gains were fueled by falling unemployment, rebounding housing markets, low short-term interest rates, and further quantitative easing from the Fed.

The Fund 3

DISCUSSION OF FUND PERFORMANCE (continued)

After rallying in early 2013, stocks encountered heightened volatility in late May when relatively hawkish remarks by Fed Chairman Ben Bernanke were widely interpreted as a signal that monetary policymakers would begin to back away from quantitative easing sooner than most analysts had expected. As a result, equities lost value in June before stabilizing over the summer. The stock market resumed its advance in the fall, when the Fed unexpectedly refrained from tapering its bond purchasing program. Even a 16-day federal government shutdown in October failed to derail the market rally.

Stocks continued to advance over the final two months of the year amid new releases of encouraging economic data.A modest reduction in the Fed’s bond buying program in mid-December had little impact on stock prices, enabling several major measures of stock market performance to end the year near record highs.

Fund Participated Fully in the Market’s Gains

The fund kept pace with the U.S. stock market’s climb during a year in which the S&P 500 Index rose by its largest percentage since the late 1990s. In this constructive environment, our disciplined stock selection strategy enhanced returns in several areas. For example, the fund held overweighted exposure to the consumer discretionary sector, where returns were bolstered by investments in media content providers, such as Viacom and Twenty-First Century Fox. Among top consumer durable holdings, apparel maker Under Armour took market share from competitors through effective product innovation, while household and commercial products manufacturer Newell Rubbermaid benefited from increasing activity in the housing industry.

The financials sector proved to be another area of strength for the fund, where returns were bolstered by our decision to avoid most real estate investment trusts (REITs), a high yielding market segment that was hurt by concerns regarding rising long-term interest rates. Instead, we focused on companies leveraged to upward trending equity markets, rising interest rates, and improved consumer spending. Leading financial holdings included wealth managers Ameriprise Financial and Affiliated Managers Group.

4

On the other hand, a few investments in other sectors undermined performance relative to the benchmark. In the information technology sector, delays in capital spending by wary corporate customers undermined returns from enterprise services companies such as Oracle, EMC and Cisco Systems. However, better results from the fund’s investment in social media provider Facebook helped cushion the impact of these disappointments. Among energy stocks, a weak oil and gas pricing environment took a toll on some holdings, such as oil services provider Schlumberger and exploration-and-production companies Apache and Anadarko Petroleum.

Finding Opportunities in Cyclical Industry Groups

As of the end of the reporting period, the fund was positioned in an effort to benefit from continued U.S. economic growth through overweighted exposure to some of the more economically sensitive areas of the financials and consumer discretionary sectors. We also identified a relatively large number of investment opportunities among pharmaceutical companies in the health care sector. In contrast, the fund held no exposure to the telecommunications services and utilities sectors, which we considered vulnerable to weak commodity prices in a low inflation environment.

January 15, 2014

| Please note, the position in any security highlighted with italicized typeface was sold during the reporting period. |

| Equity funds are subject generally to market, market sector, market liquidity, issuer and investment style risks, among |

| other factors, to varying degrees, all of which are more fully described in the fund’s prospectus. |

| 1 Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future |

| results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less |

| than their original cost. |

| 2 SOURCE: LIPPER INC. — Reflects reinvestment of dividends and, where applicable, capital gain distributions. |

| The Standard & Poor’s 500® Composite Stock Price Index is a widely accepted, unmanaged index of U.S. stock |

| market performance. Investors cannot invest directly in an index. |

The Fund 5

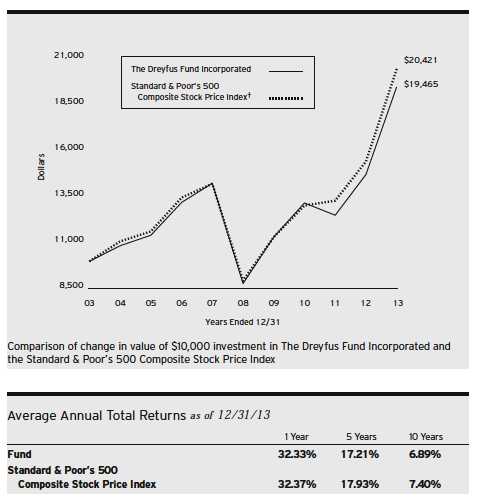

FUND PERFORMANCE

| † Source: Lipper Inc. |

| Past performance is not predictive of future performance.The fund’s performance shown in the graph and table does not |

| reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| The above graph compares a $10,000 investment made in The Dreyfus Fund Incorporated on 12/31/03 to a $10,000 |

| investment made in the Standard & Poor’s 500 Composite Stock Price Index (the “Index”) on that date.All dividends |

| and capital gain distributions are reinvested. |

| The fund’s performance shown in the line graph above takes into account all applicable fees and expenses.The Index is a |

| widely accepted, unmanaged index of U.S. stock market performance. Unlike a mutual fund, the Index is not subject to |

| charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund |

| performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the |

| prospectus and elsewhere in this report. |

6

The Fund 7

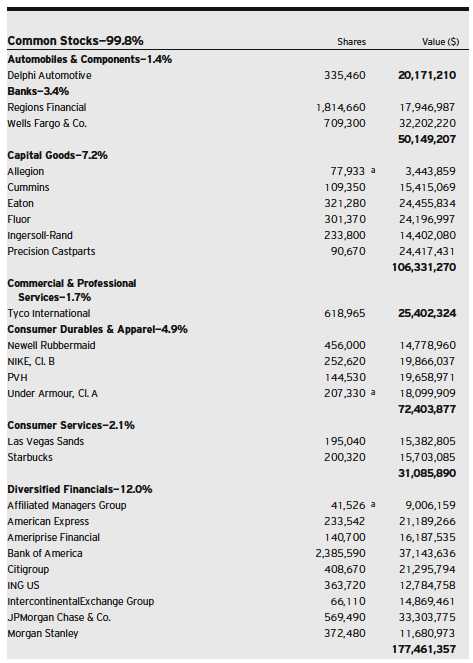

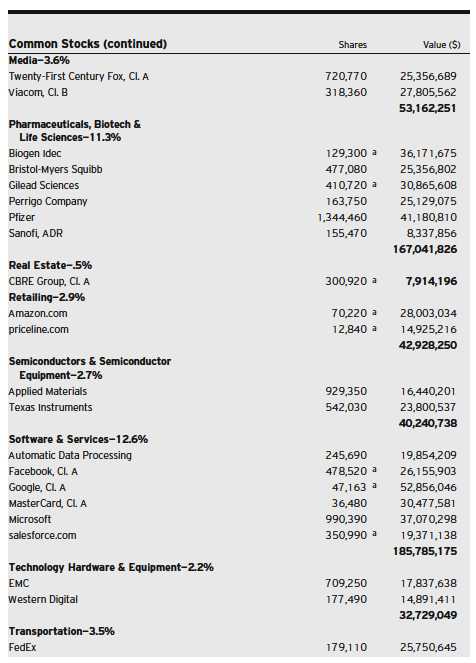

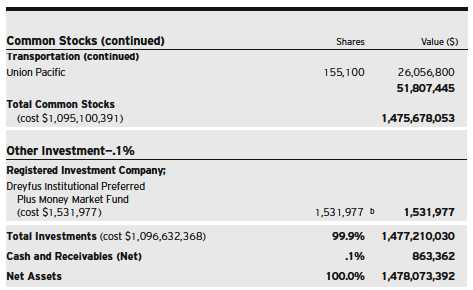

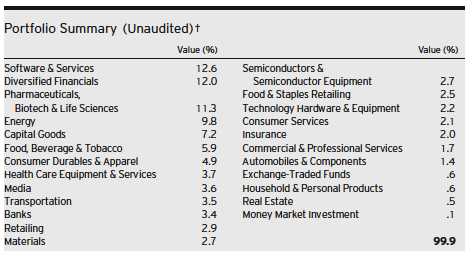

STATEMENT OF INVESTMENTS

December 31, 2013

8

The Fund 9

STATEMENT OF INVESTMENTS (continued)

10

| ADR—American Depository Receipts | |

| ETF—Exchange-Traded Funds | |

| a | Non-income producing security. |

| b | Investment in affiliated money market mutual fund. |

| † Based on net assets. |

| See notes to financial statements. |

The Fund 11

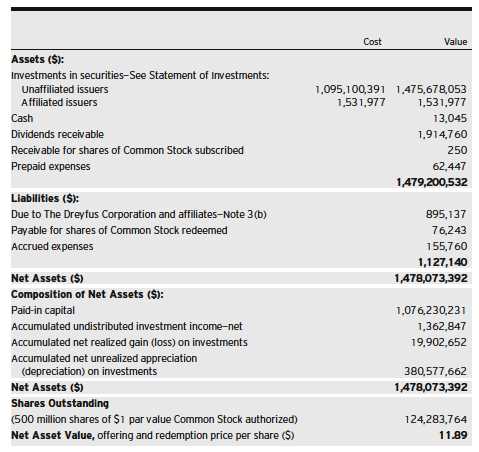

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2013

| See notes to financial statements. |

12

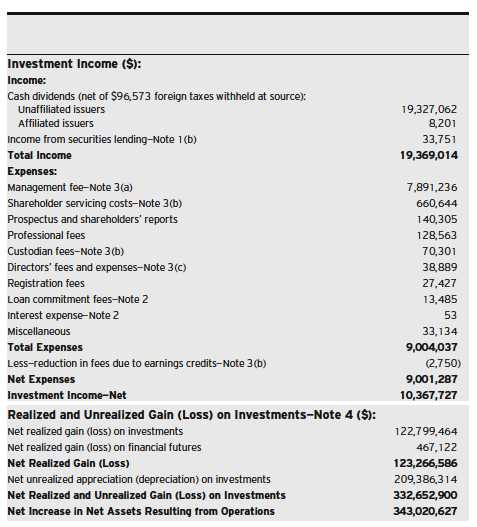

STATEMENT OF OPERATIONS

Year Ended December 31, 2013

| See notes to financial statements. |

The Fund 13

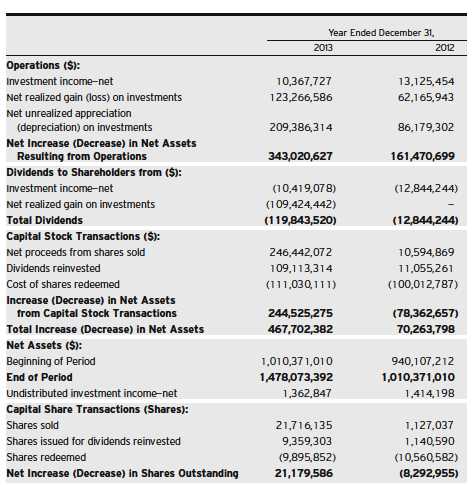

STATEMENT OF CHANGES IN NET ASSETS

| See notes to financial statements. |

14

FINANCIAL HIGHLIGHTS

The following table describes the performance for the fiscal periods indicated. Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| a Based on average shares outstanding at each month end. |

| See notes to financial statements. |

The Fund 15

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

The Dreyfus Fund Incorporated (the “fund”) is registered under the Investment Company Act of 1940, as amended (the “Act”), as a diversified open-end management investment company. The fund’s investment objective is to seek long-term capital growth consistent with the preservation of capital. The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser. MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares, which are sold to the public without a sales charge.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions.Actual results could differ from those estimates.

The fund enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown.The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value. This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

16

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements.These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. Valuation techniques used to value the fund’s investments are as follows:

Investments in securities are valued at the last sales price on the securities exchange or national securities market on which such securities are primarily traded. Securities listed on the National Market System for which market quotations are available are valued at the official closing price or, if there is no official closing price that day, at the last sales price. Securities not listed on an exchange or the national securities market, or securities for which there were no transactions, are valued at the average of the most recent bid and asked prices, except for open short positions, where the asked price is used for valuation purposes. Bid price is used when no asked price is available. Registered investment

The Fund 17

NOTES TO FINANCIAL STATEMENTS (continued)

companies that are not traded on an exchange are valued at their net asset value.All of the preceding securities are categorized within Level 1 of the fair value hierarchy.

Fair valuing of securities may be determined with the assistance of a pricing service using calculations based on indices of domestic securities and other appropriate indicators, such as prices of relevant ADRs and financial futures. Utilizing these techniques may result in transfers between Level 1 and Level 2 of the fair value hierarchy.

When market quotations or official closing prices are not readily available, or are determined not to reflect accurately fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded (for example, a foreign exchange or market), but before the fund calculates its net asset value, the fund may value these investments at fair value as determined in accordance with the procedures approved by the fund’s Board of Directors (the “Board”). Certain factors may be considered when fair valuing investments such as: fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold, and public trading in similar securities of the issuer or comparable issuers. These securities are either categorized within Level 2 or 3 of the fair value hierarchy depending on the relevant inputs used.

For restricted securities where observable inputs are limited, assumptions about market activity and risk are used and are categorized within Level 3 of the fair value hierarchy.

Financial futures which are traded on an exchange, are valued at the last sales price on the securities exchange on which such securities are primarily traded or at the last sales price on the national securities market on each business day and are generally categorized within Level 1 of the fair value hierarchy.

18

The following is a summary of the inputs used as of December 31, 2013 in valuing the fund’s investments:

| † | See Statement of Investments for additional detailed categorizations. |

At December 31, 2013, there were no transfers between Level 1 and Level 2 of the fair value hierarchy.

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

Pursuant to a securities lending agreement with The Bank of New York Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus, the fund may lend securities to qualified institutions. It is the fund’s policy that, at origination, all loans are secured by collateral of at least 102% of the value of U.S. securities loaned and 105% of the value of foreign securities loaned. Collateral equivalent to at least 100% of the market value of securities on loan is maintained at all times. Collateral

The Fund 19

NOTES TO FINANCIAL STATEMENTS (continued)

is either in the form of cash, which can be invested in certain money market mutual funds managed by the Manager or U.S. Government and Agency securities. The fund is entitled to receive all dividends, interest and distributions on securities loaned, in addition to income earned as a result of the lending transaction. Should a borrower fail to return the securities in a timely manner, The Bank of New York Mellon is required to replace the securities for the benefit of the fund or credit the fund with the market value of the unreturned securities and is subrogated to the fund’s rights against the borrower and the collateral. During the period ended December 31, 2013, The Bank of New York Mellon earned $8,839 from lending portfolio securities, pursuant to the securities lending agreement.

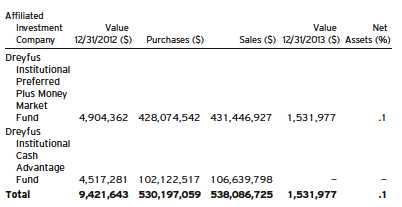

(c) Affiliated issuers: Investments in other investment companies advised by Dreyfus are defined as “affiliated” under the Act. Investments in affiliated investment companies during the period ended December 31, 2013 were as follows:

(d) Dividends to shareholders: Dividends are recorded on the ex-dividend date. Dividends from investment income-net are normally declared and paid quarterly. Dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the

20

“Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

(e) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended December 31, 2013, the fund did not have any liabilities for any uncertain tax positions.The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period ended December 31, 2013, the fund did not incur any interest or penalties.

Each tax year in the four-year period ended December 31, 2013 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At December 31, 2013, the components of accumulated earnings on a tax basis were as follows: undistributed ordinary income $6,479,987, undistributed capital gains $14,940,130 and unrealized appreciation $380,423,044.

The tax character of distributions paid to shareholders during the fiscal periods ended December 31, 2013 and December 31, 2012 were as follows: ordinary income $23,014,856 and $12,844,244, and long-term capital gains $96,828,664 and $0, respectively.

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed funds in a $265 million unsecured credit facility led by Citibank, N.A. and a $300 million unsecured credit facility provided by The Bank of New York Mellon (each, a “Facility”), each to be utilized primarily for temporary

The Fund 21

NOTES TO FINANCIAL STATEMENTS (continued)

or emergency purposes, including the financing of redemptions. Prior to October 9, 2013, the unsecured credit facility with Citibank, N.A. was $210 million. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for each Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing.

The average amount of borrowings outstanding under the Facilities during the period ended December 31, 2013 was approximately $4,700 with a related weighted average annualized interest rate of 1.13%.

NOTE 3—Management Fee and Other Transactions with Affiliates:

(a) Pursuant to a management agreement (the “Agreement”) with the Manager, the management fee is payable monthly, based on the following annual percentages of the value of the fund’s average daily net assets: .65% of the first $1.5 billion; .625% of the next $500 million; .60% of the next $500 million; and .55% over $2.5 billion.The effective management fee rate during the period ended December 31, 2013 was .65%.

The Agreement also provides for an expense reimbursement from the Manager should the fund’s aggregate expenses, exclusive of taxes and brokerage commissions, exceed 1% of the value of the fund’s average daily net assets for any full fiscal year. For the period ended December 31, 2013, there was no reduction in expenses pursuant to the Agreement.

(b) The fund has arrangements with the transfer agent and the custodian whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset transfer agency and custody fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

The fund compensates DreyfusTransfer, Inc., a wholly-owned subsidiary of the Manager, under a transfer agency agreement for providing transfer agency and cash management services for the fund. The majority of transfer agency fees are comprised of amounts paid on a per account basis, while cash management fees are related to fund subscriptions and redemptions. During the period ended December 31, 2013, the fund

22

was charged $467,655 for transfer agency services and $26,240 for cash management services.These fees are included in Shareholder servicing costs in the Statement of Operations. Cash management fees were partially offset by earnings credits of $2,738.

The fund compensates The Bank of NewYork Mellon under a custody agreement for providing custodial services for the fund.These fees are determined based on net assets, geographic region and transaction activity. During the period ended December 31, 2013, the fund was charged $70,301 pursuant to the custody agreement.

The fund compensated The Bank of New York Mellon under a cash management agreement that was in effect until September 30, 2013 for performing certain cash management services related to fund subscriptions and redemptions. During the period ended December 31, 2013, the fund was charged $9,116 pursuant to the cash management agreement, which is included in Shareholder servicing costs in the Statement of Operations.These fees were partially offset by earnings credits of $12.

During the period ended December 31, 2013, the fund was charged $9,093 for services performed by the Chief Compliance Officer and his staff.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $786,914, custodian fees $38,174, Chief Compliance Officer fees $2,299 and transfer agency fees $67,750.

(c) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales of investment securities, excluding short-term securities and financial futures, during the period ended December 31, 2013, amounted to $1,009,799,675 and $871,528,167, respectively.

The Fund 23

NOTES TO FINANCIAL STATEMENTS (continued)

Derivatives: A derivative is a financial instrument whose performance is derived from the performance of another asset. Each type of derivative instrument that was held by the fund during the period ended December 31, 2013 is discussed below.

Financial Futures: In the normal course of pursuing its investment objective, the fund is exposed to market risk, including equity price risk as a result of changes in value of underlying financial instruments.The fund invests in financial futures in order to manage its exposure to or protect against changes in the market. A financial futures contract represents a commitment for the future purchase or a sale of an asset at a specified date. Upon entering into such contracts, these investments require initial margin deposits with a counterparty, which consist of cash or cash equivalents.The amount of these deposits is determined by the exchange or Board of Trade on which the contract is traded and is subject to change.Accordingly, variation margin payments are received or made to reflect daily unrealized gains or losses which are recorded in the Statement of Operations.When the contracts are closed, the fund recognizes a realized gain or loss which is reflected in the Statement of Operations.There is minimal counterparty credit risk to the fund with financial futures since they are exchange traded, and the exchange guarantees the financial futures against default. At December 31, 2013, there were no financial futures outstanding.

The following summarizes the average market value of derivatives outstanding during the period ended December 31, 2013:

At December 31, 2013, the cost of investments for federal income tax purposes was $1,096,786,986; accordingly, accumulated net unrealized appreciation on investments was $380,423,044, consisting of $382,244,075 gross unrealized appreciation and $1,821,031 gross unrealized depreciation.

24

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

Shareholders and Board of Directors

The Dreyfus Fund Incorporated

We have audited the accompanying statement of assets and liabilities of The Dreyfus Fund Incorporated, including the statement of investments, as of December 31, 2013, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended.These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement.We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2013 by correspondence with the custodian and others. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of The Dreyfus Fund Incorporated at December 31, 2013, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with U.S. generally accepted accounting principles.

New York, New York

February 27, 2014

The Fund 25

IMPORTANT TAX INFORMATION (Unaudited)

In accordance with federal tax law, the fund hereby reports 60.92% of the ordinary dividends paid during the fiscal year ended December 31, 2013 as qualifying for the corporate dividends received deduction. For the fiscal year ended December 31, 2013, certain dividends paid by the fund may be subject to a maximum tax rate of 15%, as provided for by the Jobs and Growth Tax Relief Reconciliation Act of 2003. Of the distributions paid during the fiscal year, $19,367,350 represents the maximum amount that may be considered qualified dividend income. Shareholders will receive notification in early 2014 of the percentage applicable to the preparation of their 2013 income tax returns. Also, the fund hereby reports $.0601 per share as a long-term capital gain distribution paid on March 28, 2013 and the fund also reports $.1081 per share as a short-term capital gain distribution and $.7789 per share as a long-term capital gain distribution paid on December 23, 2013.

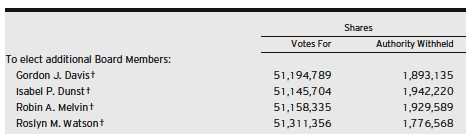

PROXY RESULTS (Unaudited)

The fund held a special meeting of shareholders on December 6, 2013.The proposal considered at the meeting, and the results, are as follows:

| † Each of the above Board Members were duly elected by shareholders at the fund’s December 6, 2013 shareholder |

| meeting. Gordon J. Davis was an existing Board Member previously having been elected by the fund’s Board. In |

| addition, Joseph S. DiMartino,Whitney I. Gerard, Nathan Leventhal and Benaree Pratt Wiley continue as Board |

| Members of the fund. |

26

INFORMATION ABOUT THE RENEWAL OF THE

FUND’S MANAGEMENT AGREEMENT (Unaudited)

At a meeting of the fund’s Board of Directors held on July 17-18, 2013, the Board considered the renewal of the fund’s Management Agreement pursuant to which Dreyfus provides the fund with investment advisory and administrative services (the “Agreement”). The Board members, a majority of whom are not “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from Dreyfus representatives. In considering the renewal of the Agreement, the Board considered all factors that it believed to be relevant, including those discussed below.The Board did not identify any one factor as dispositive, and each Board member may have attributed different weights to the factors considered.

Analysis of Nature, Extent, and Quality of Services Provided to the Fund.The Board considered information provided to them at the meeting and in previous presentations from Dreyfus representatives regarding the nature, extent, and quality of the services provided to funds in the Dreyfus fund complex. Dreyfus provided the number of open accounts in the fund, the fund’s asset size and the allocation of fund assets among distribution channels. Dreyfus also had previously provided information regarding the diverse intermediary relationships and distribution channels of funds in the Dreyfus fund complex (such as retail direct or intermediary, in which intermediaries typically are paid by the fund and/or Dreyfus) and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each intermediary or distribution channel, as applicable to the fund.

The Board also considered research support available to, and portfolio management capabilities of, the fund’s portfolio management personnel and that Dreyfus also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements.The Board also considered Dreyfus’ extensive administrative, accounting, and compliance infrastructures. The Board also considered portfolio management’s brokerage policies and practices (including policies and practices regarding soft dollars) and the standards applied in seeking best execution.

The Fund 27

INFORMATION ABOUT THE RENEWAL OF THE FUND’S

MANAGEMENT AGREEMENT (Unaudited) (continued)

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio. The Board reviewed reports prepared by Lipper, Inc. (“Lipper”), an independent provider of investment company data, which included information comparing (1) the fund’s performance with the performance of a group of comparable funds (the “Performance Group”) and with a broader group of funds (the “Performance Universe”), all for various periods ended May 31, 2013, and (2) the fund’s actual and contractual management fees and total expenses with those of a group of comparable funds (the “Expense Group”) and with a broader group of funds (the “Expense Universe”), the information for which was derived in part from fund financial statements available to Lipper as of the date of its analysis. Dreyfus previously had furnished the Board with a description of the methodology Lipper used to select the Performance Group and Performance Universe and the Expense Group and Expense Universe.

Dreyfus representatives stated that the usefulness of performance comparisons may be affected by a number of factors, including different investment limitations that may be applicable to the fund and comparison funds.The Board discussed the results of the comparisons and noted that the fund’s total return performance was generally below the Performance Group and Performance Universe medians. Dreyfus also provided a comparison of the fund’s calendar year total returns to the returns of the fund’s benchmark index and noted that the fund’s performance was above the index performance in five of the ten years shown. Dreyfus representatives noted that the fund’s longer-term Performance Group and Performance Universe comparisons were adversely impacted by a very difficult short-term period in the third quarter of 2011 for the fund’s investment approach; they noted that the fund outperformed its benchmark in calendar year 2012 and that its absolute performance and its performance relative to the Performance Group and Performance Universe for the one-year period had improved.

The Board also reviewed the range of actual and contractual management fees and total expenses of the Expense Group and Expense Universe funds and discussed the results of the comparisons.The Board

28

noted that the fund’s contractual management fee was slightly above the Expense Group median, the fund’s actual management fee was slightly above the Expense Group median and below the Expense Universe median and the fund’s total expenses were below the Expense Group and Expense Universe medians.

Dreyfus representatives reviewed with the Board the management or investment advisory fees (1) paid by funds advised or administered by Dreyfus that are in the same Lipper category as the fund and (2) paid to Dreyfus or the Dreyfus-affiliated primary employer of the fund’s primary portfolio manager(s) for advising any separate accounts and/or other types of client portfolios that are considered to have similar investment strategies and policies as the fund (the “Similar Clients”), and explained the nature of the Similar Clients.They discussed differences in fees paid and the relationship of the fees paid in light of any differences in the services provided and other relevant factors. The Board considered the relevance of the fee information provided for the Similar Clients to evaluate the appropriateness and reasonableness of the fund’s management fee.

Analysis of Profitability and Economies of Scale. Dreyfus representatives reviewed the expenses allocated and profit received by Dreyfus and the resulting profitability percentage for managing the fund and the aggregate profitability percentage to Dreyfus of managing the funds in the Dreyfus fund complex, and the method used to determine the expenses and profit. The Board concluded that the profitability results were not unreasonable, given the services rendered and service levels provided by Dreyfus. The Board also had been provided with information prepared by an independent consulting firm regarding Dreyfus’ approach to allocating costs to, and determining the profitability of, individual funds and the entire Dreyfus fund complex.The consulting firm also had analyzed where any economies of scale might emerge in connection with the management of a fund.

The Fund 29

INFORMATION ABOUT THE RENEWAL OF THE FUND’S

MANAGEMENT AGREEMENT (Unaudited) (continued)

The Board considered on the advice of its counsel the profitability analysis (1) as part of its evaluation of whether the fees under the Agreement bear a reasonable relationship to the mix of services provided by Dreyfus, including the nature, extent and quality of such services, and (2) in light of the relevant circumstances for the fund and the extent to which economies of scale would be realized if the fund grows and whether fee levels reflect these economies of scale for the benefit of fund shareholders. Dreyfus representatives also noted that, as a result of shared and allocated costs among funds in the Dreyfus fund complex, the extent of economies of scale could depend substantially on the level of assets in the complex as a whole, so that increases and decreases in complex-wide assets can affect potential economies of scale in a manner that is disproportionate to, or even in the opposite direction from, changes in the fund’s asset level.The Board also considered potential benefits to Dreyfus from acting as investment adviser and noted the soft dollar arrangements in effect for trading the fund’s investments.

At the conclusion of these discussions, the Board agreed that it had been furnished with sufficient information to make an informed business decision with respect to the renewal of the Agreement. Based on the discussions and considerations as described above, the Board concluded and determined as follows.

• The Board concluded that the nature, extent and quality of the services provided by Dreyfus are adequate and appropriate.

• The Board was concerned about the fund’s relative performance and agreed to closely monitor performance.

• The Board concluded that the fee paid to Dreyfus was reasonable in light of the considerations described above.

• The Board determined that the economies of scale which may accrue to Dreyfus and its affiliates in connection with the management of the fund had been adequately considered by Dreyfus in connection with the fee rate charged to the fund pursuant to the Agreement and that, to the extent in the future it were determined that material economies of scale had not been shared with the fund, the Board would seek to have those economies of scale shared with the fund.

30

In evaluating the Agreement, the Board considered these conclusions and determinations and also relied on its previous knowledge, gained through meetings and other interactions with Dreyfus and its affiliates, of the fund and the services provided to the fund by Dreyfus. The Board also relied on information received on a routine and regular basis throughout the year relating to the operations of the fund and the investment management and other services provided under the Agreement, including information on the investment performance of the fund in comparison to similar mutual funds and benchmark performance indices; general market outlook as applicable to the fund; and compliance reports. In addition, the Board’s consideration of the contractual fee arrangements for this fund had the benefit of a number of years of reviews of prior or similar agreements during which lengthy discussions took place between the Board and Dreyfus representatives. Certain aspects of the arrangements may receive greater scrutiny in some years than in others, and the Board’s conclusions may be based, in part, on their consideration of the same or similar arrangements in prior years.The Board determined that renewal of the Agreement was in the best interests of the fund and its shareholders.

The Fund 31

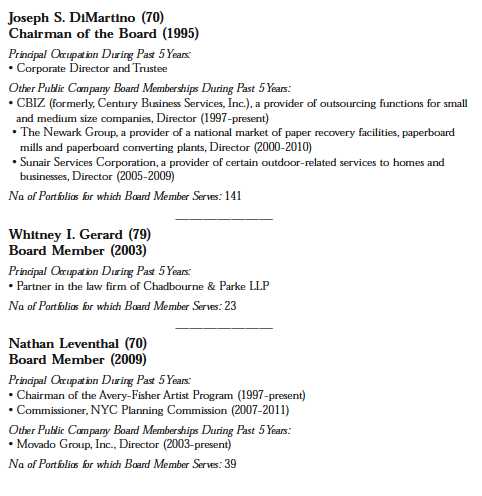

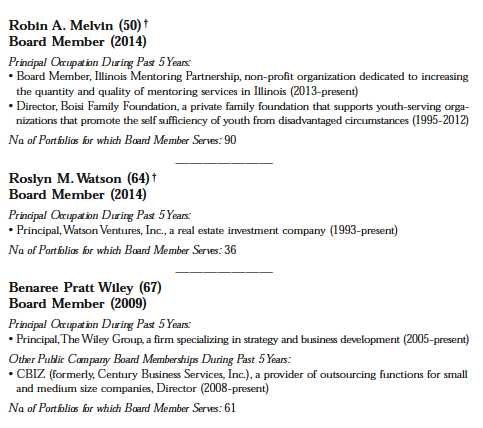

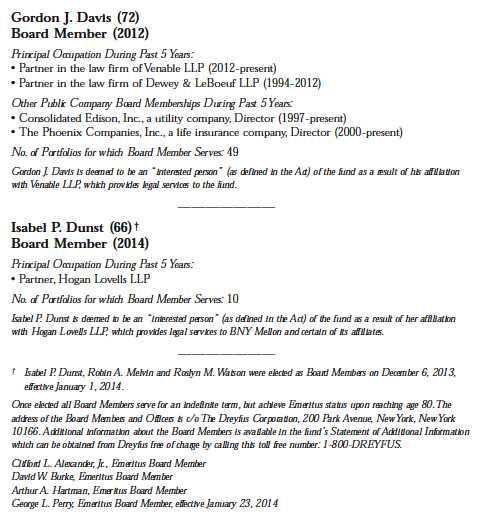

BOARD MEMBERS INFORMATION (Unaudited)

INDEPENDENT BOARD MEMBERS

32

The Fund 33

BOARD MEMBERS INFORMATION (Unaudited) (continued)

INTERESTED BOARD MEMBERS

34

OFFICERS OF THE FUND (Unaudited)

The Fund 35

OFFICERS OF THE FUND (Unaudited) (continued)

36

Item 2. Code of Ethics.

The Registrant has adopted a code of ethics that applies to the Registrant's principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. There have been no amendments to, or waivers in connection with, the Code of Ethics during the period covered by this Report.

Item 3. Audit Committee Financial Expert.

The Registrant's Board has determined that Joseph S. DiMartino, a member of the Audit Committee of the Board, is an audit committee financial expert as defined by the Securities and Exchange Commission (the "SEC"). Joseph S. DiMartino is "independent" as defined by the SEC for purposes of audit committee financial expert determinations.

Item 4. Principal Accountant Fees and Services.

(a) Audit Fees. The aggregate fees billed for each of the last two fiscal years (the "Reporting Periods") for professional services rendered by the Registrant's principal accountant (the "Auditor") for the audit of the Registrant's annual financial statements or services that are normally provided by the Auditor in connection with the statutory and regulatory filings or engagements for the Reporting Periods, were $30,857 in 2012 and $31,594 in 2013.

(b) Audit-Related Fees. The aggregate fees billed in the Reporting Periods for assurance and related services by the Auditor that are reasonably related to the performance of the audit of the Registrant's financial statements and are not reported under paragraph (a) of this Item 4 were $23,570 in 2012 and $6,000 in 2013. These services consisted of the following: (i) agreed upon procedures related to compliance with Internal Revenue Code section 817(h), (ii) security counts required by Rule 17f-2 under the Investment Company Act of 1940, as amended, (iii) advisory services as to the accounting or disclosure treatment of Registrant transactions or events and (iv) advisory services to the accounting or disclosure treatment of the actual or potential impact to the Registrant of final or proposed rules, standards or interpretations by the Securities and Exchange Commission, the Financial Accounting Standards Boards or other regulatory or standard-setting bodies.

The aggregate fees billed in the Reporting Periods for non-audit assurance and related services by the Auditor to the Registrant's investment adviser (not including any sub-investment adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by or under common control with the investment adviser that provides ongoing services to the Registrant ("Service Affiliates"), that were reasonably related to the performance of the annual audit of the Service Affiliate, which required pre-approval by the Audit Committee were $0 in 2012 and $0 in 2013.

(c) Tax Fees. The aggregate fees billed in the Reporting Periods for professional services rendered by the Auditor for tax compliance, tax advice, and tax planning ("Tax Services") were $3,334 in 2012 and $3,841 in 2013. These services consisted of: (i) review or preparation of U.S. federal, state, local and excise tax returns; (ii) U.S. federal, state and local tax planning, advice and assistance regarding statutory, regulatory or administrative developments; (iii) tax advice regarding tax qualification matters and/or treatment of various financial instruments held or proposed to be acquired or held, and (iv) determination of Passive Foreign Investment Companies. The aggregate fees billed in the Reporting Periods for Tax Services by the Auditor to Service Affiliates, which required pre-approval by the Audit Committee were $0 in 2012 and $0 in 2013.

(d) All Other Fees. The aggregate fees billed in the Reporting Periods for products and services provided by the Auditor, other than the services reported in paragraphs (a) through (c) of this Item, were $2,980 in 2012 and $2,943 in 2013. [These services consisted of a review of the Registrant's anti-money laundering program].

The aggregate fees billed in the Reporting Periods for Non-Audit Services by the Auditor to Service Affiliates, other than the services reported in paragraphs (b) through (c) of this Item, which required pre-approval by the Audit Committee, were $200,000 in 2012 and $0 in 2013.

(e)(1) Audit Committee Pre-Approval Policies and Procedures. The Registrant's Audit Committee has established policies and procedures (the "Policy") for pre-approval (within specified fee limits) of the Auditor's engagements for non-audit services to the Registrant and Service Affiliates without specific case-by-case consideration. The pre-approved services in the Policy can include pre-approved audit services, pre-approved audit-related services, pre-approved tax services and pre-approved all other services. Pre-approval considerations include whether the proposed services are compatible with maintaining the Auditor's independence. Pre-approvals pursuant to the Policy are considered annually.

(e)(2) Note: None of the services described in paragraphs (b) through (d) of this Item 4 were approved by the Audit Committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) None of the hours expended on the principal accountant's engagement to audit the registrant's financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal account's full-time, permanent employees.

Non-Audit Fees. The aggregate non-audit fees billed by the Auditor for services rendered to the Registrant, and rendered to Service Affiliates, for the Reporting Periods were $49,204,697 in 2012 and $50,384,343 in 2013.

Auditor Independence. The Registrant's Audit Committee has considered whether the provision of non-audit services that were rendered to Service Affiliates, which were not pre-approved (not requiring pre-approval), is compatible with maintaining the Auditor's independence.

Item 5. Audit Committee of Listed Registrants.

Not applicable. [CLOSED-END FUNDS ONLY]

Item 6. Investments.

(a) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable. [CLOSED-END FUNDS ONLY]

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable. [CLOSED-END FUNDS ONLY, beginning with reports for periods ended on and after December 31, 2005]

Item 9. Purchases of Equity Securities by Closed-End Management Investment Companies and Affiliated Purchasers.

Not applicable. [CLOSED-END FUNDS ONLY]

Item 10. Submission of Matters to a Vote of Security Holders.

There have been no material changes to the procedures applicable to Item 10.

Item 11. Controls and Procedures.

(a) The Registrant's principal executive and principal financial officers have concluded, based on their evaluation of the Registrant's disclosure controls and procedures as of a date within 90 days of the filing date of this report, that the Registrant's disclosure controls and procedures are reasonably designed to ensure that information required to be disclosed by the Registrant on Form N-CSR is recorded, processed, summarized and reported within the required time periods and that information required to be disclosed by the Registrant in the reports that it files or submits on Form N-CSR is accumulated and communicated to the Registrant's management, including its principal executive and principal financial officers, as appropriate to allow timely decisions regarding required disclosure.

(b) There were no changes to the Registrant's internal control over financial reporting that occurred during the second fiscal quarter of the period covered by this report that have materially affected, or are reasonably likely to materially affect, the Registrant's internal control over financial reporting.

Item 12. Exhibits.

(a)(1) Code of ethics referred to in Item 2.

(a)(2) Certifications of principal executive and principal financial officers as required by Rule 30a-2(a) under the Investment Company Act of 1940.

(a)(3) Not applicable.

(b) Certification of principal executive and principal financial officers as required by Rule 30a-2(b) under the Investment Company Act of 1940.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the Registrant has duly caused this Report to be signed on its behalf by the undersigned, thereunto duly authorized.

The Dreyfus Fund Incorporated

By: /s/ Bradley J. Skapyak | |

Bradley J. Skapyak President

| |

Date: | February 21, 2014 |

| |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this Report has been signed below by the following persons on behalf of the Registrant and in the capacities and on the dates indicated. | |

| |

By: /s/ Bradley J. Skapyak | |

Bradley J. Skapyak President

| |

Date: | February 21, 2014 |

| |

By: /s/ James Windels | |

James Windels Treasurer

| |

Date: | February 21, 2014 |

| |

EXHIBIT INDEX

(a)(1) Code of ethics referred to in Item 2.

(a)(2) Certifications of principal executive and principal financial officers as required by Rule 30a-2(a) under the Investment Company Act of 1940. (EX-99.CERT)

(b) Certification of principal executive and principal financial officers as required by Rule 30a-2(b) under the Investment Company Act of 1940. (EX-99.906CERT)