UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from __________ to __________

Commission File Number 1-8174

DUCOMMUN INCORPORATED

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 95-0693330 |

(State or other jurisdiction of incorporation or organization) | | I.R.S. Employer Identification No. |

| | |

| 23301 Wilmington Avenue, Carson, California | | 90745-6209 |

| (Address of principal executive offices) | | (Zip code) |

Registrant’s telephone number, including area code: (310) 513-7280

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

| Common Stock, $.01 par value | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting and nonvoting common equity held by nonaffiliates compared by reference to the price of which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter ended June 28, 2008 was approximately $244 million.

The number of shares of common stock outstanding on January 31, 2009 was 10,511,586.

DOCUMENTS INCORPORATED BY REFERENCE

The following documents are incorporated by reference:

(a) Proxy Statement for the 2009 Annual Meeting of Shareholders (the “2009 Proxy Statement”), incorporated partially in Part III hereof.

FORWARD-LOOKING STATEMENTS AND RISK FACTORS

Certain statements in the Form 10-K and documents incorporated by reference contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Any such forward-looking statements involve risks and uncertainties. The Company’s future financial results could differ materially from those anticipated due to the Company’s dependence on conditions in the airline industry, the level of new commercial aircraft orders, production rates for Boeing commercial aircraft, the C-17 aircraft and Apache helicopter rotor blade programs, the level of defense spending, competitive pricing pressures, manufacturing inefficiencies, start-up costs and possible overruns on new contracts, technology and product development risks and uncertainties, product performance, risks associated with acquisitions and dispositions of businesses by the Company, increasing consolidation of customers and suppliers in the aerospace industry, possible goodwill impairment, availability of raw materials and components from suppliers, credit market conditions and other factors beyond the Company’s control. See the “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Risk Factors,” and other matters discussed in this Form 10-K.

PART I

GENERAL

Ducommun Incorporated (“Ducommun” or the “Company”), is the successor to a business founded in California in 1849, first incorporated in California in 1907, and reincorporated in Delaware in 1970. Ducommun, through its subsidiaries, designs, engineers and manufactures aerostructure and electromechanical components and subassemblies, and provides engineering, technical and program management services principally for the aerospace industry. These components, assemblies and services are provided principally for domestic and foreign commercial and military aircraft, helicopter, missile and related programs as well as space programs.

Domestic commercial aircraft programs include the Boeing 737NG, 747, 767, 777 and 787. Foreign commercial aircraft programs include the Airbus Industrie A330 and A340 aircraft, Bombardier business and regional jets, and the Embraer 145 and 170/190. Major military programs include the Boeing C-17, F-15 and F-18 and Lockheed Martin F-16 and F-22 aircraft, and various aircraft and shipboard electronics upgrade programs. Commercial and military helicopter programs include helicopters manufactured by Boeing (principally the Apache and Chinook helicopters), Sikorsky, Bell, Augusta and Carson. The Company also supports various unmanned space launch vehicle and satellite programs.

On December 23, 2008, the Company acquired DynaBil Industries, Inc. (“DynaBil”), a privately-owned company based in Coxsackie, New York for $45,986,000 (net of cash acquired and excluding acquisition costs). The purchase price for DynaBil remains subject to adjustment based on a closing balance sheet. DynaBil is a leading provider of titanium and aluminum structural components and assemblies for commercial and military aerospace applications. The acquisition was funded from internally generated cash, notes to the sellers, and borrowings of approximately $10,500,000 under the Company’s credit agreement.

On January 6, 2006, the Company acquired Miltec Corporation (“Miltec”), a privately-owned company based in Huntsville, Alabama for $46,811,000 (net of cash, including assumed indebtedness and excluding acquisition costs). Miltec provides engineering, technical and program management services (including design, development, integration and test of prototype products) principally for aerospace and military markets. The acquisition was funded from internally generated cash, notes to the sellers, and borrowings of approximately $24,000,000 under the Company’s credit agreement. On May 10, 2006, the Company acquired WiseWave Technologies, Inc. (“WiseWave”), a privately-owned company based in Torrance, California for $6,827,000 (net of cash, including assumed indebtedness and excluding acquisition costs). WiseWave manufactures microwave and millimeterwave products for both aerospace and non-aerospace applications. The acquisition was funded from notes to the sellers, and borrowings of approximately $5,100,000 under the Company’s credit agreement. On September 1, 2006, the Company acquired CMP Display Systems, Inc. (“CMP”), a privately-owned company based in Newbury Park, California for $13,804,000 (net of cash acquired and excluding acquisition costs).

2

CMP manufactures incandescent, electroluminescent and LED edge lit panels and assemblies for the aerospace and defense industries. The acquisition was funded from notes to the sellers, and borrowings of approximately $10,800,000 under the Company’s credit agreement. The cost of the acquisitions was allocated on the basis of the estimated fair value of the assets acquired and liabilities assumed. The operating results for the acquisitions have been included in the consolidated statements of income since the date of the acquisitions.

PRODUCTS AND SERVICES

Ducommun operates in two business segments: Ducommun AeroStructures, Inc. (“DAS”), engineers and manufactures aerospace structural components and subassemblies, and Ducommun Technologies, Inc. (“DTI”), designs, engineers and manufactures electromechanical components and subassemblies, and provides engineering, technical and program management services (including design, development, integration and test of prototype products) principally for the aerospace and military markets. DAS provides aluminum stretch-forming, titanium and aluminum hot-forming, machining, composite lay-up, metal bonding, and chemical milling services principally for domestic and foreign commercial and military aircraft, helicopter and space programs. DTI designs and manufactures illuminated push button switches and panels, microwave and millimeterwave switches and filters, fractional horsepower motors and resolvers, and mechanical and electromechanical subassemblies, and provides engineering, technical and program management services. Components and assemblies are provided principally for domestic and foreign commercial and military aircraft, helicopter and space programs as well as selected nonaerospace applications. Engineering, technical and program management services are provided principally for advanced weapons and missile defense systems.

Business Segment Information

The Company supplies products and services to the aerospace industry. The Company’s subsidiaries are organized into two strategic businesses (DAS and DTI), each of which is a reportable operating segment. The accounting policies of the Company and its two segments are the same.

Ducommun AeroStructures, Inc.

Stretch-Forming, Hot-Forming and Machining

DAS supplies the aerospace industry with engineering and manufacturing of complex components using stretch-forming and hot-forming processes and computer-controlled machining. Stretch-forming is a process for manufacturing large, complex structural shapes primarily from aluminum sheet metal extrusions. DAS has some of the largest and most sophisticated stretch-forming presses in the United States. Hot-forming is a metal working process conducted at high temperature for manufacturing close-tolerance titanium components. DAS designs and manufactures the tooling required for the production of parts in both forming processes. Certain components manufactured by DAS are machined with precision milling equipment, including three 5-axis gantry profile milling machines and seven 5-axis numerically-controlled routers to provide computer-controlled machining and inspection of complex parts up to 100 feet long.

3

Composites and Metal Bonding

DAS engineers and manufactures metal, fiberglass and carbon composite aerostructures. DAS produces helicopter main and tail rotor blades, and adhesive bonded assemblies, including spoilers, winglets, and fuselage structural panels for aircraft.

Chemical Milling

DAS is a major supplier of close tolerance chemical milling services for the aerospace industry. Chemical milling removes material in specific patterns to reduce weight in areas where full material thickness is not required. This sophisticated etching process enables DAS to produce lightweight, high-strength designs that would be impractical to produce by conventional means. DAS offers production-scale chemical milling on aluminum, titanium, steel, nickel-base and super alloys. Jet engine components, wing leading edges and fuselage skins are examples of products that require chemical milling.

Ducommun Technologies, Inc.

Switches and Related Components

DTI develops, designs and manufactures illuminated switches, switch assemblies, keyboard panels, and edge lit panels, used in many military aircraft, helicopter, commercial aircraft and spacecraft programs. DTI manufactures switches and panels where high reliability is a prerequisite. DTI also develops, designs and manufactures microwave and millimeterwave switches, filters, and other components used principally on commercial and military aircraft and satellites. In addition, DTI develops, designs and manufactures high precision actuators, stepper motors, fractional horsepower motors and resolvers principally for space applications, and microwave and millimeterwave products for certain non-aerospace applications.

Mechanical and Electromechanical Subassemblies

DTI is a leading manufacturer of mechanical and electromechanical subassemblies for the defense electronics and commercial aircraft markets. DTI has a fully integrated manufacturing capability, including manufacturing engineering, fabrication, machining, assembly, electronic integration and related processes. DTI’s products include sophisticated radar enclosures, gyroscopes and indicators, aircraft avionics racks, and shipboard communications and control enclosures.

Engineering, Technical and Program Management Services

DTI (through its Miltec subsidiary) is a leading provider of missile and aerospace systems design, development, integration and testing. Engineering, technical and program management services are provided principally for advanced weapons systems and missile defense primarily for United States defense, space and homeland security programs.

4

SALES AND MARKETING

Military components manufactured by the Company are employed in many of the country’s front-line fighters, bombers, helicopters and support aircraft, as well as sea-based applications. Engineering, technical and program management services are provided principally for United States defense, space and homeland security programs. The Company’s defense business is diversified among a number of military manufacturers and programs. Sales related to military programs were approximately 59% of total sales in 2008, 60% of total sales in 2007 and 66% of total sales in 2006. In the space sector, the Company continues to support various unmanned launch vehicle and satellite programs. Sales related to space programs were approximately 2% of total sales in 2008, 3% of total sales in 2007 and 2% of total sales in 2006.

A major portion of sales is derived from United States government defense programs and space programs, subjecting the Company to various laws and regulations that are more restrictive than those applicable to the private sector. These defense and space programs could be adversely affected by reductions in defense spending and other government budgetary pressures which would result in reductions, delays or stretch-outs of existing and future programs.Additionally, the Company’s contracts may be subject to reductions or modifications in the event of changes in government requirements. Although the Company’s fixed-price contracts generally permit it to realize increased profits if costs are less than projected, the Company bears the risk that increased or unexpected costs may reduce profits or cause losses on the contracts. The accuracy and appropriateness of certain costs and expenses used to substantiate the Company’s direct and indirect costs for the United States government are subject to extensive regulation and audit by the Defense Contract Audit Agency, an arm of the Department of Defense. In addition, many of the Company’s contracts covering defense and space programs are subject to termination at the convenience of the customer (as well as for default). In the event of termination for convenience, the customer generally is required to pay the costs incurred by the Company and certain other fees through the date of termination.

The Company’s commercial business is represented on many of today’s major commercial aircraft. Sales related to commercial business were approximately 39% of total sales in 2008, 37% of total sales in 2007 and 32% of total sales in 2006. The Company’s commercial sales depend substantially on aircraft manufacturers’ production rates, which in turn depend upon deliveries of new aircraft. Deliveries of new aircraft by aircraft manufacturers are dependent on the financial capacity of the airlines and leasing companies to purchase the aircraft. Sales of commercial aircraft could be affected as a result of changes in new aircraft orders, or the cancellation or deferral by airlines of purchases of ordered aircraft. The Company’s sales for commercial aircraft programs also could be affected by changes in its customers’ inventory levels and changes in its customers’ aircraft production build rates.

5

MAJOR CUSTOMERS

The Company had substantial sales to Boeing, the United States government and Raytheon. During 2008, sales to Boeing were $130,783,000, or approximately 32% of total sales; sales to the United States government were $33,335,000, or approximately 8% of total sales; and sales to Raytheon were $33,248,000, or approximately 8% of total sales. Sales to Boeing, the United States government and Raytheon are diversified over a number of different commercial, military and space programs.

INFORMATION ABOUT FOREIGN AND DOMESTIC OPERATIONS AND EXPORT SALES

In 2008, 2007 and 2006, sales to foreign customers worldwide were $32,850,000 $27,707,000 and $24,879,000, respectively. The Company has manufacturing facilities in Thailand and Mexico. The amounts of revenues, profitability and identifiable assets attributable to foreign sales activity were not material when compared with the revenue, profitability and identifiable assets attributed to United States domestic operations during 2008, 2007 and 2006. The Company had no sales to a foreign country greater than 4% of total sales in 2008, 2007 and 2006. The Company is not subject to any significant foreign currency risks since all sales are made in United States dollars.

RESEARCH AND DEVELOPMENT

The Company performs concurrent engineering with its customers and product development activities under Company-funded programs and under contracts with others. Concurrent engineering and product development activities are performed for commercial, military and space applications. The Company also performs high technology systems engineering and analysis, principally under customer-funded contracts, with a focus on sensors system simulation, engineering and integration.

RAW MATERIALS AND COMPONENTS

Raw materials and components used in the manufacture of the Company’s products, including aluminum, steel and carbon fibers, generally are available from a number of vendors and are generally in adequate supply. However, the Company, from time to time, has experienced increases in lead times for, and a deterioration in availability of, aluminum, titanium and certain other materials. Moreover, certain components, supplies and raw materials for the Company’s operations are purchased from single sources. In such instances, the Company strives to develop alternative sources and design modifications to minimize the potential for business interruptions.

COMPETITION

The aerospace industry is highly competitive, and the Company’s products and services are affected by varying degrees of competition. The Company competes worldwide with domestic and international companies in most markets it services, some of which are

6

substantially larger and have greater financial, sales, technical and personnel resources. Larger competitors offering a wider array of products and services than those offered by the Company can have a competitive advantage by offering potential customers bundled products and services that the Company cannot match. The Company’s ability to compete depends principally on the quality of its goods and services, competitive pricing, product performance, design and engineering capabilities, new product innovation and the ability to solve specific customer problems.

PATENTS AND LICENSES

The Company has several patents, but it does not believe that its operations are dependent on any single patent or group of patents. In general, the Company relies on technical superiority, continual product improvement, exclusive product features, superior lead time, on-time delivery performance, quality and customer relationships to maintain its competitive advantage.

BACKLOG

Backlog is subject to delivery delays or program cancellations, which are beyond the Company’s control. As of December 31, 2008, backlog believed to be firm was approximately $475,800,000, compared to $353,225,000 at December 31, 2007. The 2008 backlog includes $41,411,000 for backlog for DynaBil. Approximately $236,000,000 of total backlog is expected to be delivered during 2009. The backlog at December 31, 2008 included the following programs:

| | | |

| | | Backlog

(In thousands) |

737NG | | $ | 57,507 |

Sikorsky Helicopters | | | 53,343 |

Apache Helicopter | | | 50,311 |

F-18 | | | 42,342 |

C-17 | | | 29,528 |

Chinook Helicopter | | | 26,038 |

Carson Helicopter | | | 25,710 |

777 | | | 22,299 |

| | | |

| | $ | 307,078 |

| | | |

Trends in the Company’s overall level of backlog, however, may not be indicative of trends in future sales because the Company’s backlog is affected by timing differences in the placement of customer orders and because the Company’s backlog tends to be concentrated in several programs to a greater extent than the Company’s sales. Beginning in January 2009, the production rate and the Company’s sales for the Apache helicopter program are expected to be reduced by approximately one-half from the rate in 2008. Current program backlog will be shipped over an extended delivery schedule.

7

ENVIRONMENTAL MATTERS

The Company’s business, operations and facilities are subject to numerous stringent federal, state and local environmental laws and regulations issued by government agencies, including the Environmental Protection Agency (“EPA”). Among other matters, these regulatory authorities impose requirements that regulate the emission, discharge, generation, management, transportation and disposal of hazardous materials, pollutants and contaminants. These regulations govern public and private response actions to hazardous or regulated substances that may be or have been released to the environment, and they require the Company to obtain and maintain licenses and permits in connection with its operations. The Company may also be required to investigate and remediate the effects of the release or disposal of materials at sites associated with past and present operations. Additionally, this extensive regulatory framework imposes significant compliance burdens and risks on the Company. The Company anticipates that capital expenditures will continue to be required for the foreseeable future to upgrade and maintain its environmental compliance efforts. The Company does not expect to spend a material amount on capital expenditures for environmental compliance during 2009.

The DAS chemical milling business uses various acid and alkaline solutions in the chemical milling process, resulting in potential environmental hazards. Despite existing waste recovery systems and continuing capital expenditures for waste reduction and management, at least for the immediate future, this business will remain dependent on the availability and cost of remote hazardous waste disposal sites or other alternative methods of disposal.

DAS has been directed by California environmental agencies to investigate and take corrective action for ground water contamination at its facilities located in El Mirage and Monrovia, California. Based on currently available information, the Company has established a reserve for its estimated liability for such investigation and corrective action in the approximate amount of $3,114,000. DAS also faces liability as a potentially responsible party for hazardous waste disposed at two landfills located in Casmalia and West Covina, California. DAS and other companies and government entities have entered into consent decrees with respect to each landfill with the United States Environmental Protection Agency and/or California environmental agencies under which certain investigation, remediation and maintenance activities are being performed. Based upon currently available information, the Company has established a reserve for its estimated liability in connection with the landfills in the approximate amount of $1,588,000. The Company’s ultimate liability in connection with these matters will depend upon a number of factors, including changes in existing laws and regulations, the design and cost of construction, operation and maintenance activities, and the allocation of liability among potentially responsible parties.

In the normal course of business, Ducommun and its subsidiaries are defendants in certain other litigation, claims and inquiries, including matters relating to environmental laws. In addition, the Company makes various commitments and incurs contingent liabilities. While it is not feasible to predict the outcome of these matters, the Company does not presently expect that any sum it may be required to pay in connection with these matters would have a material adverse effect on its consolidated financial position, results of operations or cash flows.

8

EMPLOYEES

At December 31, 2008 the Company employed 2,048 persons. The Company’s DAS subsidiary is a party to a collective bargaining agreement with labor unions at its Monrovia, California facility which covered 321 full-time hourly employees, which expires July 1, 2012. If the unionized workers were to engage in a strike or other work stoppage, if DAS is unable to negotiate acceptable collective bargaining agreements with the unions, or if other employees were to become unionized, the Company could experience a significant disruption of the Company’s operations and higher ongoing labor costs and possible loss of customer contracts, which could have an adverse effect on its business and results of operations. The Company has not experienced any material labor-related work stoppage and considers its relations with its employees to be good.

AVAILABLE INFORMATION

The Company’s Internet website address iswww.ducommun.com. The Company makes available through its Internet website its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after filing with the Securities and Exchange Commission.

The Company’s business, financial condition, results of operations and cash flows may be affected by known and unknown risks, uncertainties and other factors. Any of these risks, uncertainties and other factors could cause the Company’s future financial results to differ materially from recent financial results or from currently anticipated future financial results. In addition to those noted elsewhere in this report, the Company is subject to the following risks and uncertainties:

Aerospace Markets Are Cyclical

The aerospace markets in which the Company sells its products are cyclical and have experienced periodic declines. The Company’s sales are, therefore, unpredictable and tend to fluctuate based on a number of factors, including economic conditions and developments affecting the aerospace industry and the customers served. Many of the world’s economies have entered into recession and new commercial aircraft production currently is beginning to decline. Any downturn in commercial aircraft production could have a negative impact on the Company’s business, financial condition and operating results.

Military and Space-Related Products Are Dependent Upon Government Spending

The Company estimates that in 2008 approximately 61% of its sales were derived from military and space markets. These military and space markets are largely dependent upon government spending, particularly by the United States government. Changes in the nature or levels of spending for military and space could improve or negatively impact the Company’s prospects in its military and space markets.

9

The Company Is Dependent on Boeing Commercial Aircraft, the C-17 Aircraft and Apache Helicopter Programs

The Company estimates that in 2008 approximately 15% of its sales were for Boeing commercial aircraft, 9% of its sales were for the C-17 aircraft, and 13% of its sales were for the Apache helicopter. Beginning in January 2009, the production rate and the Company’s sales for the Apache helicopter program are expected to be reduced by approximately one-half from the rate in 2008. The Company’s sales for Boeing commercial aircraft and the C-17 aircraft are principally for new aircraft production; and the Company’s sales for the Apache helicopter are principally for replacement rotor blades. Any significant change in production rates for Boeing commercial aircraft, the C-17 aircraft and the replacement rate for the Apache helicopter blades would have a material effect on the Company’s results of operations and cash flows. In addition, there is no guarantee that the Company’s current significant customers will continue to buy products from the Company at current levels. The loss of a key customer could have a material adverse effect on the Company.

Deterioration in Credit Markets Could Adversely Impact the Company

The recent deterioration in credit markets could adversely impact the Company. The Company depends upon cash flow from operations and its revolving credit facility to provide liquidity. The Company’s credit agreement currently matures on April 7, 2010. The Company intends to enter into a new credit agreement with a group of banks during the first half of 2009, but there can be no assurance that a new credit facility will be available on terms that are acceptable to the Company and any such credit facility is likely to result in an increase in the Company’s cost of borrowings. Because of the Company’s relatively low leverage, the Company does not expect any short-term liquidity issues. However, the availability of credit on acceptable terms is necessary to support the Company’s growth and acquisition strategy.

The Company Is Experiencing Competitive Pricing Pressures

The aerospace industry is highly competitive and competitive pressures may adversely affect the Company. The Company competes worldwide with a number of domestic and international companies that are larger than it in terms of resources and market share. The Company is experiencing competitive pricing pressures in both its DAS and DTI businesses. These competitive pricing pressures have had, and are expected to continue to have, an adverse effect on the Company’s business, financial condition and operating results.

The Company Faces Risks of Cost Overruns and Losses on Fixed-Price Contracts

The Company sells many of its products under firm, fixed-price contracts providing for a fixed price for the products regardless of the production costs incurred by the Company. As a result, manufacturing inefficiencies, start-up costs and other factors may result in cost overruns and losses on contracts. The cost of producing products also may be adversely affected by increases in the cost of labor, materials, outside processing, overhead and other factors. In many cases, the Company makes multiyear firm, fixed-price commitments to its customers, without assurance that the Company’s anticipated production costs will be achieved.

10

Risks Associated With Foreign Operations Could Adversely Impact the Company

The Company has facilities in Thailand and Mexico. Doing business in foreign countries is also subject to various risks, including political instability, local economic conditions, foreign currency fluctuations, foreign government regulatory requirements, trade tariffs, and the potentially limited availability of skilled labor in proximity to the Company’s facilities.

The Company’s Products and Processes Are Subject to Risks from Changes in Technology

The Company’s products and processes are subject to risks of obsolescence as a result of changes in technology. To address this risk, the Company invests in product design and development, and for capital expenditures. There can be no guarantee that the Company’s product design and development efforts will be successful, or that the amounts of money required to be invested for product design and development and capital expenditures will not increase materially in the future.

The Company Faces Risks Associated with Acquisitions and Dispositions of Businesses

A key element of the Company’s long-term strategy has been growth through acquisitions. The Company is continuously reviewing and actively pursuing acquisitions, including acquisitions outside of its current aerospace markets. Acquisitions may require the Company to incur additional indebtedness, resulting in increased leverage. Any significant acquisition may result in a material weakening of the Company’s financial position and a material increase in the Company’s cost of borrowings. Acquisitions also may require the Company to issue additional equity, resulting in dilution to existing stockholders. This additional financing for acquisitions and capital expenditures may not be available on terms acceptable or favorable to the Company. Acquired businesses may not achieve anticipated results, and could result in a material adverse effect on the Company’s financial condition, results of operations and cash flows. The Company also periodically reviews its existing businesses to determine if they are consistent with the Company’s strategy. The Company has sold, and may sell in the future, business units and product lines, which may result in either a gain or loss on disposition.

The Company’s acquisition strategy exposes it to risks, including the risk that the Company may not be able to successfully integrate acquired businesses. The Company’s ability to grow by acquisition is dependent upon, among other factors, the availability of suitable acquisition candidates. Growth by acquisition involves risks that could have a material adverse effect on the Company’s business, financial condition and operating results, including difficulties in integrating the operations and personnel of acquired companies, the potential amortization of acquired intangible assets, the potential impairment of goodwill and the potential loss of key customers or employees of acquired companies. The Company may not be able to consummate acquisitions on satisfactory terms or, if any acquisitions are consummated, to satisfactorily integrate these acquired businesses.

11

Goodwill Could Be Impaired in the Future

In the fourth quarter of 2008, the Company recorded a non-cash charge of $13,064,000 at DTI (relating to its Miltec reporting unit) for the impairment of goodwill. The test as of December 31, 2008 indicated the book value of Miltec exceeded the fair value of the business. The impairment charge driven by adverse equity market conditions that caused a decrease in current market multiples and the Company’s stock price as of December 31, 2008 compared with the test performed as of December 31, 2007. The charge reduced goodwill recorded in connection with the acquisition of Miltec and does not impact the company’s normal business operations.

In assessing the recoverability of the Company’s goodwill at December 31, 2008, management was required to make certain critical estimates and assumptions. These estimates and assumptions included that during the next several years the Company will make improvements in manufacturing efficiency, achieve reductions in operating costs, and obtain increases in sales and backlog. Due to many variables inherent in the estimation of a business’s fair value and the relative size of the Company’s recorded goodwill, differences in estimates and assumptions may have a material effect on the results of the Company’s impairment analysis. If any of these or other estimates and assumptions are not realized in the future, or if market multiples decline further the Company may be required to record an additional impairment charge for the goodwill. The goodwill of the Company was $114,002,000 at December 31, 2008.

Significant Consolidation in the Aerospace Industry Could Adversely Affect the Company’s Business and Financial Results

The aerospace industry is experiencing significant consolidation, including the Company’s customers, competitors and suppliers. Consolidation among the Company’s customers may result in delays in the award of new contracts and losses of existing business. Consolidation among the Company’s competitors may result in larger competitors with greater resources and market share, which could adversely affect the Company’s ability to compete successfully. Consolidation among the Company’s suppliers may result in fewer sources of supply and increased cost to the Company.

The Company’s Failure to Meet Quality or Delivery Expectations of Customers Could Adversely Affect the Company’s Business and Financial Results

The Company’s customers have increased, and are expected to increase further in the future, their expectations with respect to the on-time delivery and quality of the Company’s products. In some cases, the Company does not presently satisfy these customer expectations, particularly with respect to on-time delivery. If the Company fails to meet the quality or delivery expectations of its customers, this failure could lead to the loss of one or more significant customers of the Company.

12

The Company’s Manufacturing Operations May Be Adversely Affected by the Availability of Raw Materials and Components from Suppliers

In some cases, the Company’s customers supply raw materials and components to the Company. In other cases, the Company’s customers designate specific suppliers from which the Company is directed to purchase raw materials and components. As a result, the Company may have limited control over the selection of suppliers and the timing of receipt and cost of raw materials and components from suppliers. The failure of customers and suppliers to deliver on a timely basis raw materials and components to the Company may adversely affect the Company’s results of operations and cash flows. In addition, the Company, from time to time, has experienced increases in lead times for, and deteriorations in the availability of, aluminum, titanium and certain other materials. These problems with raw material availability could have an adverse effect on the Company’s results of operations in the future.

Environmental Liabilities Could Adversely Affect the Company’s Financial Results

The Company is subject to various environmental laws and regulations. The Company’s DAS subsidiary has been directed by government environmental agencies to investigate and take corrective action for groundwater contamination at two of its facilities. DAS is also a potentially responsible party at certain sites at which it previously disposed of hazardous wastes. There can be no assurance that future developments, lawsuits and administrative actions, and liabilities relating to environmental matters will not have a material adverse effect on the Company’s results of operations or cash flows.

The DAS chemical milling business uses various acid and alkaline solutions in the chemical milling process, resulting in potential environmental hazards. Despite existing waste recovery systems and continuing capital expenditures for waste reduction and management, at least for the immediate future, this business will remain dependent on the availability and cost of remote hazardous waste disposal sites or other alternative methods of disposal.

Product Liability Claims in Excess of Insurance Could Adversely Affect the Company’s Financial Results and Financial Condition

The Company faces potential liability for personal injury or death as a result of the failure of products designed or manufactured by the Company. Although the Company maintains product liability insurance, any material product liability not covered by insurance could have a material adverse effect on the Company’s financial condition, results of operations and cash flows.

Damage or Destruction of the Company’s Facilities Caused by Earthquake or Other Causes Could Adversely Affect the Company’s Financial Results and Financial Condition

Although the Company maintains standard property casualty insurance covering its properties, the Company does not carry any earthquake insurance because of the cost of such insurance. Most of the Company’s properties are located in Southern California, an area subject to frequent and sometimes severe earthquake activity. Even if covered by insurance, any

13

significant damage or destruction of the Company’s facilities could result in the inability to meet customer delivery schedules and may result in the loss of customers and significant additional costs to the Company. As a result, any significant damage or destruction of the Company’s properties could have a material adverse effect on the Company’s business, financial condition or results of operations.

Terrorist Attacks May Adversely Impact the Company’s Operations

There can be no assurance that the current world political and military tensions, or the United States military actions, will not lead to acts of terrorism and civil disturbances in the United States or elsewhere. These attacks may strike directly at the physical facilities of the Company, its suppliers or its customers. Such attacks could have an adverse impact on the Company’s domestic and international sales, supply chain, production capabilities, insurance premiums or ability to purchase insurance, thereby adversely affecting the Company’s financial position, results of operations and cash flows. In addition, the consequences of terrorist attacks and armed conflicts are unpredictable, and their long-term effects upon the Company are uncertain.

The Company Is Dependent on Its Ability to Attract and Retain Key Personnel

The Company’s success depends in part upon its ability to attract and retain key engineering, technical and managerial personnel. The Company faces competition for management, engineering and technical personnel from other companies and organizations. Therefore, the Company may not be able to retain its existing management and other key personnel, or be able to fill new management, engineering and technical positions created as a result of expansion or turnover of existing personnel. The loss of members of the Company’s senior management group, or key engineering and technical personnel, could have a material adverse effect on the Company’s business.

Stock-Based Compensation Expense Could Change

Determining the appropriate fair value model and calculating the fair value of stock-based compensation requires the input of highly subjective assumptions, including the expected life of the stock-based compensation awards and stock price volatility. The assumptions used in calculating the fair value of stock-based compensation awards represent management’s best estimates, but these estimates involve inherent uncertainties and the application of management’s judgment. As a result, if factors change or if the Company was to use different assumptions, stock-based compensation expense could be materially different in the future. In addition, the Company is required to estimate the expected forfeiture rate and only recognize expense for those shares expected to vest. If the actual forfeiture rate is materially different from the estimated forfeiture rate, the stock-based compensation expense could be significantly different from what has been recorded in the current period.

14

Effective Income Tax Rate Could Change

The Company’s effective income tax rate for 2008, 2007 and 2006, was approximately 23%, 28% and 21%, respectively, compared to the statutory federal income tax rate of 35% and state income tax rates ranging from 6% to 9%, for each of the years. The Company’s effective tax rate was lower than the statutory rates in recent years primarily due to the benefit of research and development tax credits (which currently extends through 2009), the reduction of tax reserves and the deduction for qualified domestic production activities. The effective tax rate for the Company could be significantly higher in the future than it has been in recent years due to changes in the Company’s level or sources of income, changes in the Company’s spending, eligibility for research and development tax credits, and changes in tax laws.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

Not applicable.

15

The Company occupies approximately 21 facilities with a total office and manufacturing area of over 1,458,000 square feet, including both owned and leased properties. At December 31, 2008, facilities which were in excess of 50,000 square feet each were occupied as follows:

| | | | | | |

Location | | Segment | | Square

Feet | | Expiration

of Lease |

Carson, California | | Ducommun AeroStructures | | 286,000 | | Owned |

Monrovia, California | | Ducommun AeroStructures | | 274,000 | | Owned |

Parsons, Kansas | | Ducommun AeroStructures | | 120,000 | | Owned |

Carson, California | | Ducommun Technologies | | 117,000 | | 2011 |

Phoenix, Arizona | | Ducommun Technologies | | 100,000 | | 2012 |

Orange, California | | Ducommun AeroStructures | | 76,000 | | Owned |

El Mirage, California | | Ducommun AeroStructures | | 74,000 | | Owned |

Iuka, Mississippi | | Ducommun Technologies | | 66,000 | | 2013 |

Carson, California | | Ducommun AeroStructures | | 65,000 | | 2009 |

Huntsville, Alabama | | Ducommun Technologies | | 52,000 | | 2010 |

The Company’s facilities are, for the most part, fully utilized, although excess capacity exists from time to time based on product mix and demand. Management believes that these properties are in good condition and suitable for their present use.

Although the Company maintains standard property casualty insurance covering its properties, the Company does not carry any earthquake insurance because of the cost of such insurance. Most of the Company’s properties are located in Southern California, an area subject to frequent and sometimes severe earthquake activity.

The Company is a defendant in a lawsuit entitledUnited States of America ex rel Taylor Smith, Jeannine Prewitt and James Ailes v. The Boeing Company and Ducommun Inc., filed in the United States District Court for the District of Kansas. The lawsuit isquitam action brought against The Boeing Company (“Boeing”) and Ducommun on behalf of the United States of America for violations of the United States False Claims Act. The lawsuit alleges that Ducommun sold unapproved parts to the Boeing Commercial Airplanes-Wichita Division which were installed by Boeing in 32 aircraft ultimately sold to the United States government. The lawsuit seeks damages, civil penalties and other relief from the defendants for presenting or causing to be presented false claims for payment to the United States government. Although the amount of alleged damages are not specified, the lawsuit seeks damages in an amount equal to three times the amount of damages the United States government sustained because of the defendants’ actions, plus a civil penalty of $10,000 for each false claim made on or before September 28, 1999, and $11,000 for each false claim made on or after September 28, 1999, together with attorneys’ fees and costs. The Company intends to defend itself vigorously against the lawsuit. The Company, at this time, is unable to estimate what, if any, liability it may have in connection with the lawsuit.

16

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

None.

17

PART II

| ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The common stock of the Company (DCO) is listed on the New York Stock Exchange. On December 31, 2008, the Company had approximately 338 holders of record of common stock. The Company paid $1,586,000 of dividends in 2008. The Company paid dividends of $0.075 per common share in the third and fourth quarters of 2008. No dividends were paid during 2007. The following table sets forth the high and low sales prices per share for the Company’s common stock as reported on the New York Stock Exchange for the fiscal periods indicated.

| | | | | | | | | | | | |

| | | 2008 | | 2007 |

| | | High | | Low | | High | | Low |

First Quarter | | $ | 36.84 | | $ | 24.72 | | $ | 26.70 | | $ | 21.19 |

Second Quarter | | | 33.78 | | | 23.52 | | | 32.80 | | | 23.22 |

Third Quarter | | | 29.76 | | | 20.84 | | | 33.00 | | | 23.19 |

Fourth Quarter | | | 23.88 | | | 13.58 | | | 42.70 | | | 31.12 |

18

Equity Compensation Plan Information

The following table provides information about the Company’s compensation plans under which equity securities are authorized for issuance.

| | | | | | | |

Plan category | | Number of securities to

be issued upon exercise

of outstanding options,

warrants and rights

(a) | | Weighted-average

exercise price of

outstanding options,

warrants and rights

(b) | | Number of securities

remaining available for

future issuance under

equity compensation

plans (excluding

securities reflected in

column (a))

(c)(2) |

Equity compensation plans approved by security holders(1) | | 806,500 | | $ | 16.296 | | 344,375 |

Equity compensation plans not approved by security holders | | 0 | | | 0 | | 0 |

| | | | | | | |

Total | | 806,500 | | $ | 16.296 | | 344,375 |

| | | | | | | |

| (1) | The number of securities to be issued consists of 681,500 for stock options, 85,000 for restricted stock units and 40,000 for performance stock units at target. The weighted average exercise price applies only to the stock options. |

| (2) | Awards are not restricted to any specified form or structure and may include, without limitation, sales or bonuses of stock, restricted stock, stock options, reload stock options, stock purchase warrants, other rights to acquire stock, securities convertible into or redeemable for stock, stock appreciation rights, limited stock appreciation rights, phantom stock, dividend equivalents, performance units or performance shares, and an award may consist of one such security or benefit, or two or more of them in tandem or in the alternative. |

19

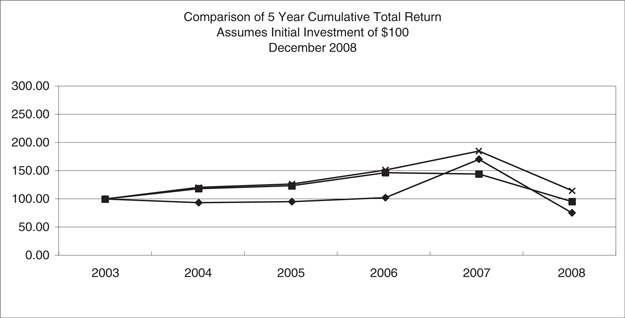

Performance Graph

The following graph compares the yearly percentage change in the Company’s cumulative total shareholder return with the cumulative total return of the Russell 2000 Index and the Spade Defense Index for the periods indicated, assuming the reinvestment of any dividends. The graph is not necessarily indicative of future price performance.

| | | | | | | | | | | | | | |

| | | | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 | | 2008 |

Ducommun Inc.  | | | | 100.00 | | 93.29 | | 95.57 | | 102.37 | | 170.46 | | 76.25 |

Russell 2000 Index  | | | | 100.00 | | 118.34 | | 123.74 | | 146.43 | | 144.17 | | 95.44 |

Spade Defense Index  | | | | 100.00 | | 120.47 | | 126.85 | | 151.37 | | 184.93 | | 114.60 |

20

Issuer Purchases of Equity Securities

The following table provides information about Company purchases of equity securities that are registered by the Company pursuant to Section 12 of the Exchange Act during the quarter ended December 31, 2008.

| | | | | | | | | | |

Period | | Total

Number of

Shares (or

Units)

Purchased | | Average

Price Paid

Per Share

(or Unit) | | Total Number of

Shares (or

Units) Purchased

as Part of

Publicly

Announced Plans

or Programs | | Maximum

Number (or

Approximate Dollar

Value) of Shares (or

Units) that May Yet

Be Purchased Under

the Plans or

Programs (1) |

Month beginning September 28, 2008 and ending October 25, 2008 | | 0 | | $ | 0.00 | | 0 | | $ | 4,704,000 |

Month beginning October 26, 2008 and ending November 22, 2008 | | 600 | | $ | 14.96 | | 600 | | $ | 4,694,992 |

Month beginning November 23, 2008 and ending December 31, 2008 | | 68,400 | | $ | 14.29 | | 68,400 | | $ | 3,714,294 |

| | | | | | | | | | |

Total | | 69,000 | | $ | 14.30 | | 69,000 | | $ | 3,714,294 |

| | | | | | | | | | |

| (1) | The Company repurchased 69,000 of its common shares during 2008 and did not repurchase any of its common shares in 2007 and 2006, in the open market. At December 31, 2008, $3,714,294 remained available to repurchase common stock of the Company under stock repurchase programs previously approved by the Board of Directors. |

21

| ITEM 6. | SELECTED FINANCIAL DATA |

| | | | | | | | | | | | | | | | | | | | |

Year Ended December 31, | | 2008(a)(b) | | | 2007 | | | 2006(c) | | | 2005 | | | 2004 | |

| (In thousands, except per share amounts) | | | | | | | | | | | | | | | |

Net Sales | | $ | 403,803 | | | $ | 367,297 | | | $ | 319,021 | | | $ | 249,696 | | | $ | 224,876 | |

| | | | | | | | | | | | | | | | | | | | |

Gross Profit as a Percentage of Sales | | | 20.3 | % | | | 20.6 | % | | | 19.6 | % | | | 20.7 | % | | | 19.4 | % |

| | | | | | | | | | | | | | | | | | | | |

Income from Continuing Operations Before Taxes | | | 17,049 | | | | 27,255 | | | | 18,088 | | | | 21,120 | | | | 14,465 | |

Income Tax Expense | | | (3,937 | ) | | | (7,634 | ) | | | (3,791 | ) | | | (5,127 | ) | | | (3,293 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net Income | | $ | 13,112 | | | $ | 19,621 | | | $ | 14,297 | | | $ | 15,993 | | | $ | 11,172 | |

| | | | | | | | | | | | | | | | | | | | |

Earnings Per Share: | | | | | | | | | | | | | | | | | | | | |

Basic earnings per share | | $ | 1.24 | | | $ | 1.89 | | | $ | 1.40 | | | $ | 1.59 | | | $ | 1.12 | |

Diluted earnings per share | | | 1.23 | | | | 1.88 | | | | 1.39 | | | | 1.57 | | | | 1.10 | |

Working Capital | | $ | 69,672 | | | $ | 77,703 | | | $ | 55,355 | | | $ | 64,312 | | | $ | 45,387 | |

Total Assets | | | 366,186 | | | | 332,476 | | | | 297,033 | | | | 227,969 | | | | 204,553 | |

Long-Term Debt, Including Current Portion | | | 30,719 | | | | 25,751 | | | | 30,436 | | | | — | | | | 1,200 | |

Total Shareholders’ Equity | | | 224,446 | | | | 214,051 | | | | 187,025 | | | | 167,851 | | | | 151,491 | |

| (a) | The results for 2008 include a pre-tax non-cash goodwill impairment charge of $13,064,000, resulting from annual impairment testing required by SFAS 142. There was no goodwill impairment in 2007, 2006, 2005 or 2004. |

| (b) | In December 2008 the Company acquired DynaBil, which is now a part of DAS. This transaction was accounted for as a purchase business combination. |

| (c) | In January, May and September 2006 the Company acquired Miltec, WiseWave and CMP, respectively, which are now part of DTI. These transactions were accounted for as purchase business combinations. |

22

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Overview

Ducommun Incorporated (“Ducommun” or the “Company”), through its subsidiaries designs, engineers and manufactures aerostructure and electromechanical components and subassemblies, and provides engineering, technical and program management services principally for the aerospace industry. These components, assemblies and services are provided principally for domestic and foreign commercial and military aircraft, helicopter, missile and related programs as well as space programs.

Domestic commercial aircraft programs include the Boeing 737NG, 747, 767, 777 and 787. Foreign commercial aircraft programs include the Airbus Industrie A330 and A340 aircraft, Bombardier business and regional jets, and the Embraer 145 and 170/190. Major military programs include the Boeing C-17, F-15 and F-18 and Lockheed Martin F-16 and F-22 aircraft, and various aircraft and shipboard electronics upgrade programs. Commercial and military helicopter programs include helicopters manufactured by Boeing (principally the Apache and Chinook helicopters), Sikorsky, Bell, Augusta and Carson. The Company also supports various unmanned space launch vehicle and satellite programs.

In the fourth quarter of 2008, the Company recorded a non-cash charge of $13,064,000 at DTI (relating to its Miltec reporting unit) for the impairment of goodwill. In accordance with SFAS No. 142 –Goodwill and Other Intangible Assets,the Company performed its required annual impairment test for goodwill using a discounted cash flow analysis supported by comparative market multiples to determine the fair values of its businesses versus their book values. The test as of December 31, 2008 indicated the book value of Miltec exceeded the fair value of the business. The impairment charge driven by adverse equity market conditions that caused a decrease in current market multiples and the Company’s stock price as of December 31, 2008 compared with the test performed as of December 31, 2007. The charge reduced goodwill recorded in connection with the acquisition of Miltec and does not impact the company’s normal business operations. The principal factors used in the discounted cash flow analysis requiring judgment are the projected results of operations, weighted average cost of capital (“WACC”), and terminal value assumptions. The WACC takes into account the relative weights of each component of the Company’s consolidated capital structure (equity and debt) and represents the expected cost of new capital adjusted as appropriate to consider risk profiles associated with growth projection risks. The terminal value assumptions are applied to the final year of discounted cash flow model. Due to many variables inherent in the estimation of a business’s fair value and the relative size of the Company’s recorded goodwill, differences in assumptions may have a material effect on the results of the Company’s impairment analysis. Prior to recording the goodwill impairment charge at Miltec, the Company tested the purchased intangible assets and other long-lived assets at the business as required by SFAS No. 144 –Accounting for the Impairment or Disposal of Long-Lived Assets, and the carrying value of these assets were determined not to be impaired.

23

The fourth quarter of 2008 was also negatively impacted by the strike of Boeing by the International Association of Machinists and Aerospace Workers and by an increase in allowance for doubtful accounts due to a customer’s bankruptcy.

On December 23, 2008, the Company acquired DynaBil Industries, Inc. (“DynaBil”), DynaBil is a leading provider of titanium and aluminum structural components and assemblies for commercial and military aerospace applications. The operating results for the acquisitions have been included in the consolidated statements of income since the date of the acquisitions. In December 2006, the Company shut down the Ducommun Technologies Fort Defiance, Arizona facility (which employed approximately 46 people at the closure date), and transferred a portion of the business to the Ducommun Technologies Phoenix, Arizona facility. On September 1, 2006, the Company acquired CMP Display Systems, Inc. (“CMP”). CMP manufactures incandescent, electroluminescent and LED edge lit panels and assemblies for the aerospace and defense industries. On May 10, 2006, the Company acquired WiseWave Technologies, Inc. (“WiseWave”). WiseWave manufactures microwave and millimeterwave products for both aerospace and non-aerospace applications. On January 6, 2006, the Company acquired Miltec Corporation (“Miltec”). Miltec provides engineering, technical and program management services, including the design, development, integration and test of prototype products. Engineering, technical and program management services are provided principally for advanced weapons systems and missile defense.

Sales, gross profit as a percentage of sales, selling, general and administrative expense as a percentage of sales, the effective tax rate and the diluted earnings per share in 2008 and 2007, respectively, were as follows:

| | | | | | | | | | | | |

| | | 2008 | | | 2007 | | | 2006 | |

Net Sales (in $000’s) | | $ | 403,803 | | | $ | 367,297 | | | $ | 319,021 | |

Gross Profit % of Sales | | | 20.3 | % | | | 20.6 | % | | | 19.6 | % |

SG&A Expense % of Sales | | | 12.5 | % | | | 12.6 | % | | | 13.1 | % |

Effective Tax Rate | | | 23.1 | % | | | 28.0 | % | | | 21.0 | % |

Diluted Earnings Per Share | | $ | 1.23 | | | $ | 1.88 | | | $ | 1.39 | |

The Company manufactures components and assemblies principally for domestic and foreign commercial and military aircraft, helicopter and space programs. The Company’s Miltec subsidiary provides engineering, technical and program management services almost entirely for United States defense, space and homeland security programs. The Company’s mix of military, commercial and space business in 2008, 2007 and 2006, respectively, was approximately as follows:

| | | | | | | | | |

| | | 2008 | | | 2007 | | | 2006 | |

Military | | 59 | % | | 60 | % | | 66 | % |

Commercial | | 39 | % | | 37 | % | | 32 | % |

Space | | 2 | % | | 3 | % | | 2 | % |

| | | | | | | | | |

Total | | 100 | % | | 100 | % | | 100 | % |

| | | | | | | | | |

24

The Company is dependent on Boeing commercial aircraft, the C-17 aircraft and the Apache helicopter programs. Sales to these programs, as a percentage of total sales, for 2008, 2007 and 2006, respectively, were approximately as follows:

| | | | | | | | | |

| | | 2008 | | | 2007 | | | 2006 | |

Boeing Commercial Aircraft | | 15 | % | | 18 | % | | 14 | % |

Boeing C-17 Aircraft | | 9 | % | | 10 | % | | 10 | % |

Boeing Apache Helicopter | | 13 | % | | 15 | % | | 18 | % |

All Others | | 63 | % | | 57 | % | | 58 | % |

| | | | | | | | | |

Total | | 100 | % | | 100 | % | | 100 | % |

| | | | | | | | | |

Net income for 2008 was lower than 2007. The decline in net income in 2008 was driven by non-cash goodwill impairment at Ducommun Technologies, Inc. (“DTI”), (relating to its Miltec reporting unit) of $13,064,000 and an increase in allowance for doubtful accounts, at Ducommun AeroStructures, Inc. (“DAS”) due to a customer’s bankruptcy. Net income was also affected by lower operating performance at DTI operating segment and a higher effective tax rate in 2008, partially offset by an improvement in operating performance at DAS and a decrease in interest expense due to lower debt and lower interest rates in 2008.

Critical Accounting Policies

Critical accounting policies are those accounting policies that can have a significant impact on the presentation of our financial condition and results of operations, and that require the use of subjective estimates based upon past experience and management’s judgment. Because of the uncertainty inherent in such estimates, actual results may differ from these estimates. Below are those policies applied in preparing our financial statements that management believes are the most dependent on the application of estimates and assumptions. For additional accounting policies, see Note 1 of “Notes to Consolidated Financial Statements.”

Revenue Recognition

The Company recognizes revenue when persuasive evidence of an arrangement exists, the price is fixed or determinable, collection is reasonably assured and delivery of products has occurred or services have been rendered. Revenue from products sold under long-term contracts is recognized by the Company on the same basis as other sale transactions. The Company recognizes revenue on the sale of services (including prototype products) based on the type of contract: time and materials, cost-plus reimbursement and firm-fixed price. Revenue is recognized (i) on time and materials contracts as time is spent at hourly rates, which

25

are negotiated with customers, plus the cost of any allowable materials and out-of-pocket expenses, (ii) on cost-plus reimbursement contracts based on direct and indirect costs incurred plus a negotiated profit calculated as a percentage of cost, a fixed amount or a performance-based award fee, and (iii) on fixed-price service contracts on the percentage-of-completion method measured by the percentage of costs incurred to estimated total costs.

Provision for Estimated Losses on Contracts

The Company records provisions for estimated losses on contracts in the period in which such losses are identified. The provisions for estimated losses on contracts require management to make certain estimates and assumptions, including those with respect to the future revenue under a contract and the future cost to complete the contract. Management’s estimate of the future cost to complete a contract may include assumptions as to improvements in manufacturing efficiency and reductions in operating and material costs. If any of these or other assumptions and estimates do not materialize in the future, the Company may be required to record additional provisions for estimated losses on contracts.

Goodwill

The Company’s business acquisitions have resulted in goodwill. In assessing the recoverability of the Company’s goodwill, management must make assumptions regarding estimated future cash flows, comparable company analyses, discount rates and other factors to determine the fair value of the respective assets. If actual results do not meet these estimates, if these estimates or their related assumptions change in the future, or if adverse equity market conditions cause a decrease in current market multiples and the Company’s stock price the Company may be required to record additional impairment charges for these assets. In the event that a goodwill impairment charge is required, it could adversely affect the operating results and financial position of the Company.

Other Intangible Assets

The Company amortizes purchased other intangible assets with finite lives using the straight-line method over the estimated economic lives of the assets, ranging from one to fourteen years. The value of other intangibles acquired through business combinations has been estimated using present value techniques which involve estimates of future cash flows. Actual results could vary, potentially resulting in impairment charges.

Accounting for Stock-Based Compensation

The Company uses a Black-Scholes valuation model in determining the stock-based compensation expense for options, net of an estimated forfeiture rate, on a straight-line basis over the requisite service period of the award. The Company has two award populations, one with an option vesting term of four years and the other with an option vesting term of one year. The Company estimated the forfeiture rate based on its historic experience.

26

For performance and restricted stock units the Company calculates compensation expense, net of an estimated forfeiture rate, on a straight line basis over the requisite service/performance period of the awards. The performance stock units vest based on a three-year cumulative performance cycle. The Company has two restricted stock units, one restricted stock unit vests at the end of five years and the other restricted stock unit vests equally over a three year period ending in 2011. The Company estimated the forfeiture rate based on its historic experience.

Inventories

Inventories are stated at the lower of cost or market, cost being determined on a first-in, first-out basis. Inventoried costs include raw materials, outside processing, direct labor and allocated overhead, adjusted for any abnormal amounts of idle facility expense, freight, handling costs, and wasted materials (spoilage) incurred, but do not include any selling, general and administrative expense. Costs under long-term contracts are accumulated into, and removed from, inventory on the same basis as other contracts. The Company assesses the inventory carrying value and reduces it, if necessary, to its net realizable value based on customer orders on hand, and internal demand forecasts using management’s best estimates given information currently available. The Company’s customer demand can fluctuate significantly caused by factors beyond the control of the Company. The Company maintains an allowance for potentially excess and obsolete inventories and inventories that are carried at costs that are higher than their estimated net realizable values. If market conditions are less favorable than those projected by management, such as an unanticipated decline in demand and not meeting expectations, inventory write-downs may be required.

Acquisitions

On December 23, 2008, the Company acquired DynaBil Industries, Inc. (“DynaBil”), a privately-owned company based in Coxsackie, New York for $45,986,000 (net of cash acquired and excluding acquisition costs). The purchase price for DynaBil remains subject to adjustment based on a closing balance sheet. DynaBil is a leading provider of titanium and aluminum structural components and assemblies for commercial and military aerospace applications. The acquisition was funded from internally generated cash, notes to the sellers, and borrowings of approximately $10,500,000 under the Company’s credit agreement. The operating results for this acquisition have been included in the consolidated statements of income since the date of the acquisition. The consolidated financial statements reflect preliminary estimates of the fair value of the assets acquired and liabilities assumed and the related allocation of the purchase price for DynaBil. The principal estimates of fair value have been determined using expected net present value techniques utilizing a 15% discount rate. Customer relationships are valued assuming an annual attrition rate of 3%. Management does not expect adjustments to these estimates, if any, to have a material effect on the Company’s consolidated financial position or results of operations.

On September 1, 2006, the Company acquired CMP, a privately-owned company based in Newbury Park, California for $13,804,000 (net of cash acquired and excluding acquisition costs). CMP manufactures incandescent, electroluminescent and LED edge lit panels and assemblies for

27

the aerospace and defense industries. The cost of the acquisition was allocated on the basis of the estimated fair value of the assets acquired and liabilities assumed. The acquisition broadens the Company’s lighted human machine interface product line. The acquisition was funded from notes to the sellers, and borrowings of approximately $10,800,000 under the Company’s credit agreement. The operating results for this acquisition have been included in the consolidated statements of income since the date of the acquisition.

On May 10, 2006, the Company acquired WiseWave, a privately-owned company based in Torrance, California for $6,827,000 (net of cash, including assumed indebtedness and excluding acquisition costs). WiseWave manufactures microwave and millimeterwave products for both aerospace and non-aerospace applications. The acquisition broadens the Company’s microwave product line and adds millimeterwave products to its offerings. The cost of the acquisition was allocated on the basis of the estimated fair value of the assets acquired and liabilities assumed. The acquisition was funded from notes to the sellers, and borrowings of approximately $5,100,000 under the Company’s credit agreement. The operating results for this acquisition have been included in the consolidated statements of income since the date of the acquisition.

On January 6, 2006, the Company acquired Miltec, a privately-owned company based in Huntsville, Alabama for $46,811,000 (net of cash, including assumed indebtedness and excluding acquisition costs). Miltec provides engineering, technical and program management services (including design, development, integration and test of prototype products) principally for aerospace and military markets. The acquisition provided the Company a platform business with leading-edge technology in a large and growing market with substantial design engineering capability. The cost of the acquisition was allocated on the basis of the estimated fair value of the assets acquired and liabilities assumed. The acquisition was funded from internally generated cash, notes to the sellers, and borrowings of approximately $24,000,000 under the Company’s credit agreement. The operating results for this acquisition have been included in the consolidated statements of income since the date of the acquisition.

Results of Operations

2008 Compared to 2007

Net sales in 2008 were $403,803,000, compared to net sales of $367,297,000 for 2007. Net sales in 2008 increased 10% from 2007 primarily due to increases in both military and commercial sales. The Company’s mix of business in 2008 was approximately 59% military, 39% commercial, and 2% space, compared to 60% military, 37% commercial, and 3% space in 2007. Foreign sales were approximately 8% of total sales in both 2008 and 2007. The Company did not have sales to any foreign country greater than 4% of total sales in 2008 or 2007.

The Company had substantial sales, through both of its business segments, to Boeing, the United States government, and Raytheon. During 2008 and 2007, sales to Boeing, the United States government, and Raytheon were as follows:

| | | | | | |

December 31, | | 2008 | | 2007 |

| (In thousands) | | | | |

Boeing | | $ | 130,783 | | $ | 126,484 |

United States government | | | 33,335 | | | 32,622 |

Raytheon | | | 33,248 | | | 30,007 |

| | | | | | |

Total | | $ | 197,366 | | $ | 189,113 |

| | | | | | |

28

At December 31, 2008, trade receivables from Boeing, the United States government and Raytheon were $5,816,000, $1,076,000 and $2,341,000, respectively. The sales and receivables relating to Boeing, the United States government and Raytheon are diversified over a number of different commercial, military and space programs.

Military components manufactured by the Company are employed in many of the country’s front-line fighters, bombers, helicopters and support aircraft, as well as sea-based applications. Engineering, technical and program management services are provided principally for United States defense, space and homeland security programs. The Company’s defense business is diversified among military manufacturers and programs. Sales related to military programs were approximately $238,309,000, or 59% of total sales in 2008, compared to $219,248,000, or 60% of total sales in 2007. The increase in military sales in 2008 resulted principally from an $8,224,000 increase in sales to the Chinook program and a $3,790,000 increase in sales to the Blackhawk program at DAS, a $5,404,000 increase in sales to the Phalanx program at DTI and a net increase in all other military programs at DAS and DTI, partially offset by a $3,121,000 reduction in sales to the F-18 program at DAS. The Apache helicopter program accounted for approximately $52,480,000 in sales in 2008, compared to $53,681,000 in sales in 2007. The C-17 program accounted for approximately $36,714,000 in sales in 2008 compared to $35,535,000 in sales in 2007. The F-18 program accounted for approximately $17,542,000 in sales in 2008, compared to $20,663,000 in sales in 2007. The F-15 program accounted for approximately $9,940,000 in sales in 2008, compared to $8,798,000 in sales in 2007.

The Company’s commercial business is represented on many of today’s major commercial aircraft. Sales related to commercial business were approximately $156,689,000, or 39% of total sales in 2008, compared to $137,864,000, or 37% of total sales in 2007. During 2008, commercial sales were higher, principally because of a $16,379,000 increase in commercial aftermarket sales at DAS and DTI, a $5,582,000 increase in sales to the Carson helicopter program, partially offset by a decrease in all other commercial sales at DAS and DTI. Sales to the Boeing 737NG program accounted for approximately $38,259,000 in sales in 2008, compared to $39,558,000 in sales in 2007. The Boeing 777 program accounted for approximately $10,400,000 in sales in 2008, compared to $11,796,000 in sales in 2007. The Company estimates that the strike of Boeing by the International Association of Machinists and Aerospace Workers, which began in the third quarter of 2008 and ended in the fourth quarter of 2008, reduced the Company’s sales in 2008 by approximately $7,479,000.

In the space sector, the Company produces components for a variety of unmanned launch vehicles and satellite programs and provides engineering services. Sales related to space programs were approximately $8,805,000, or 2% in 2008, compared to $10,185,000, or 3% of total sales in 2007. The decrease in sales for space programs resulted principally from a decrease in engineering services at DTI.

29

Backlog is subject to delivery delays or program cancellations, which are beyond the Company’s control. As of December 31, 2008, backlog believed to be firm was approximately $475,800,000, compared to $353,225,000 at December 31, 2007. The 2008 backlog includes $41,411,000 for backlog for DynaBil. Approximately $236,000,000 of total backlog is expected to be delivered during 2009. The backlog at December 31, 2008 included the following programs:

| | | |

| | | Backlog

(In thousands) |

737NG | | $ | 57,507 |

Sikorsky Helicopters | | | 53,343 |

Apache Helicopter | | | 50,311 |

F-18 | | | 42,342 |

C-17 | | | 29,528 |

Chinook Helicopter | | | 26,038 |

Carson Helicopter | | | 25,710 |

777 | | | 22,299 |

| | | |

| | $ | 307,078 |

| | | |