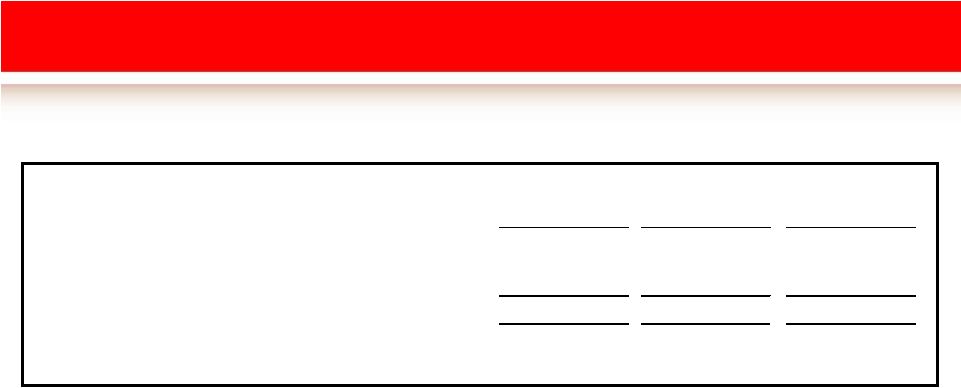

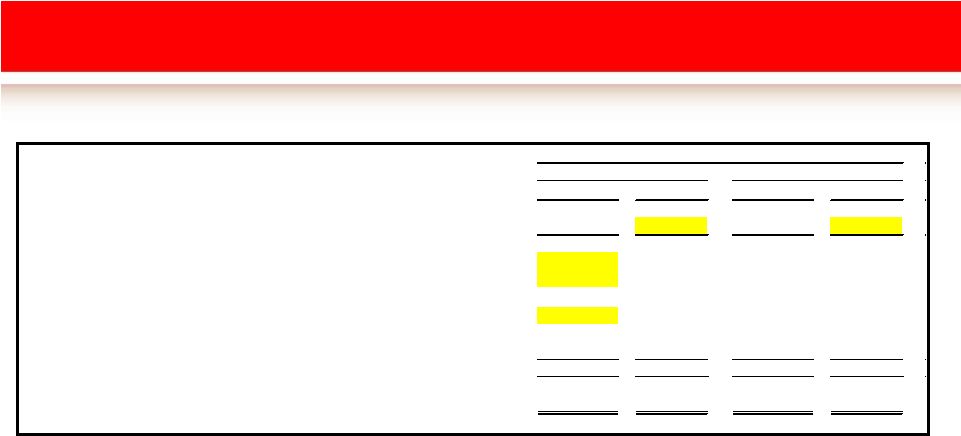

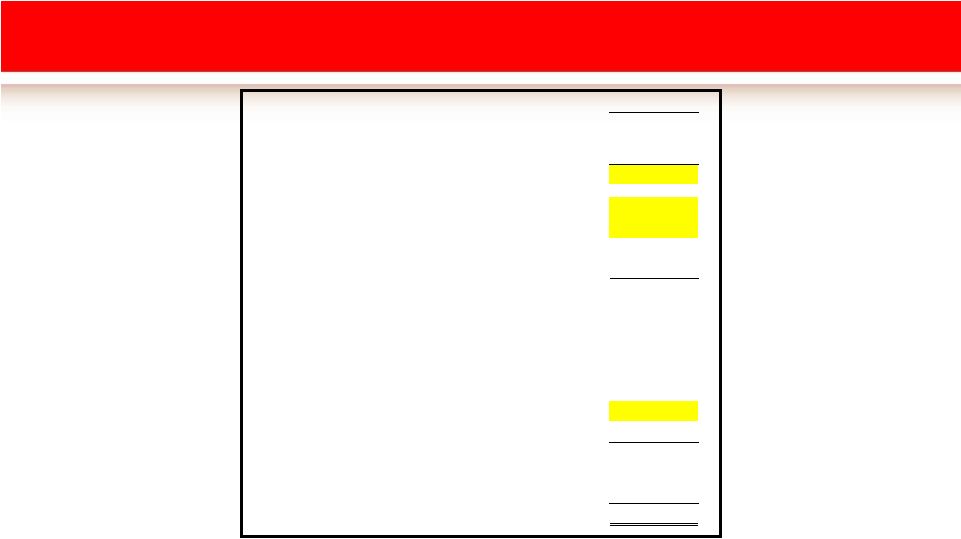

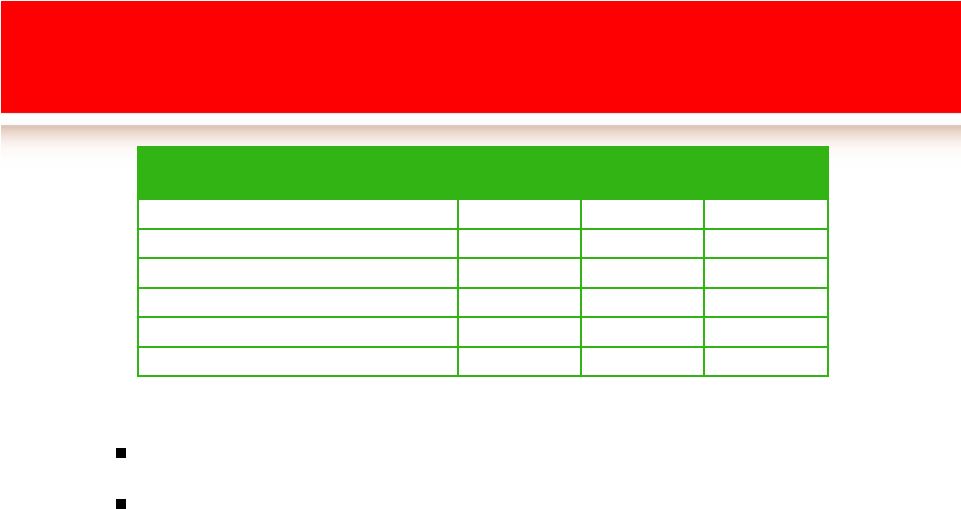

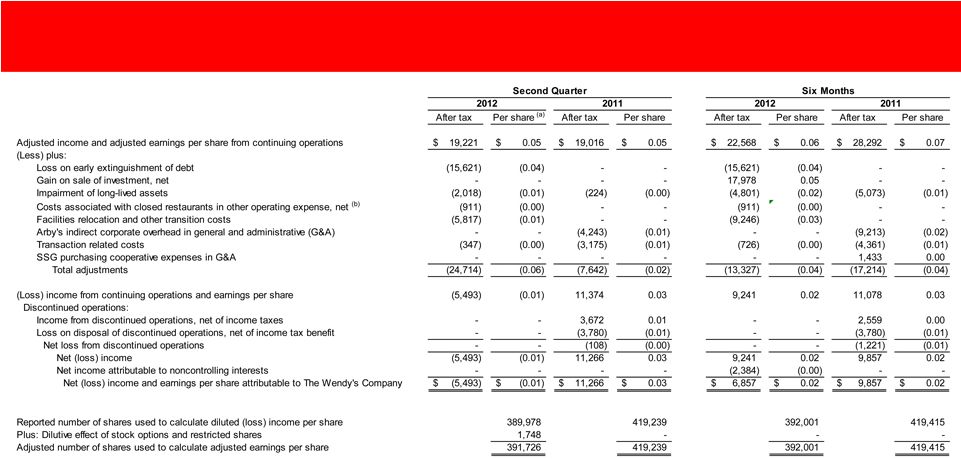

(In Thousands) (Unaudited) 2012 2011 2012 2011 Adjusted EBITDA from continuing operations 89,073 $ 89,415 $ 152,954 $ 163,140 $ (Less) plus: Depreciation and amortization (35,947) (29,842) (68,258) (60,156) Impairment of long-lived assets (3,270) (365) (7,781) (8,262) (1,477) - (1,477) - Facilities relocation and other transition costs (9,426) - (14,957) - Transaction related costs (562) (5,039) (1,174) (6,923) - (6,735) - (14,623) SSG purchasing cooperative expense reversal in G&A - - - 2,275 Operating profit 38,391 47,434 59,307 75,451 Interest expense (28,002) (28,089) (56,237) (57,531) Loss on early extinguishment of debt (25,195) - (25,195) - Gain on sale of investment, net - - 27,407 - Other income, net 640 337 2,164 590 (14,166) 19,682 7,446 18,510 Benefit from (provision for) income taxes 8,673 (8,308) 1,795 (7,432) (Loss) income from continuing operations (5,493) 11,374 9,241 11,078 Discontinued operations: Income from discontinued operations, net of income taxes - 3,672 - 2,559 Loss on disposal of discontinued operations, net of income tax benefit - (3,780) - (3,780) Net loss from discontinued operations - (108) - (1,221) Net (loss) income (5,493) 11,266 9,241 9,857 Net income attributable to noncontrolling interests - - (2,384) - (5,493) $ 11,266 $ 6,857 $ 9,857 $ Net (loss) income attributable to The Wendy's Company Arby's indirect corporate overhead in general and administrative (G&A) Costs associated with closed restaurants in other operating expense, net (a) (Loss) income from continuing operations before income taxes and noncontrolling interests Second Quarter Six Months Reconciliation of Adjusted EBITDA from Continuing Operations to Net (Loss) Income Attributable to The Wendy’s Company (a) Excludes non-cash items included in impairment of long-lived assets 61 |