Exhibit 13.1

2 0 1 4 A N N U A L R E P O R T growing shareholder value

Sensient Technologies Corporation is a leading global developer, manufacturer and marketer of advanced color, flavor and fragrance systems. Sensient uses state-ofthe-art technologies at facilities around the world to develop and manufacture customized food and beverage systems Pharmaceutical colors, coatings and excipients; cosmetic color and ingredient systems; household and industrial product formulations; digital inks; and other specialty colors and chemicals. Financial Highlights in thousands except per share Years ended December 31, 2014 2013 % Change % Change Local CurrencyResults from Continuing Operations Revenue $1,447,821 $1,462,126 (1%) 0% Operating Income from Continuing Operations 130,665 173,780 (25%) (24%) Net Earnings from Continuing Operations 81,771 114,298 (28%) (27%) Diluted Earnings per Share from Continuing Operations 1.67 2.29 (27%) (26%) Adjusted Results from Continuing Operations* Adjusted Operating Income* 221,215 205,515 8% 9% Adjusted Net Earnings* 147,307 136,257 8% 9% Adjusted Diluted Earning per Share* 3.02 2.73 11% 12% Cash Flow Activity Cash Flows from Operating Activities 189,188 153,553 23% Capital Expenditures 79,398 104,246 (24%) Free Cash Flow 109,790 49,307 123% Total Debt 466,899 355,174 31% Dividends per share 0.98 0.91 8%* These are non-GAAP financial measures. Please see page 15 of this report (reference to Non-GAAP Financial Measures in MD&A section) for a reconciliation of these measures to GAAP and a discussion of why the Company is presenting this information.

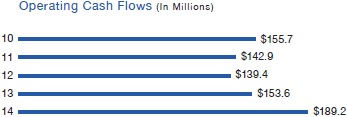

Letter to shareholders “ Our strategy is working. We are delivering operating profit growth, improved margins and strong cash flows. In addition, we have taken numerous significant actions that demonstrate our ongoing commitment to provide sustainable, long‐term value to our shareholders.” Paul Manning President and Chief Executive Officer Performance and Progress Sensient’s 2014 earnings per share increased 11% over last year’s performance to $3.02 per share. Operating margin increased 120 basis points to 15.3%, as each of our operating groups delivered higher margins this year. Overall, we had a very positive year that exceeded our performance objectives. Operating cash flow was also strong in 2014, increasing 23% to $189 million, and free cash flow more than doubled to $110 million. Return on invested capital also improved 50 basis points to 10.2%. We will continue to improve returns by delivering solid earnings growth, rationalizing our production assets, reducing our working capital levels and optimizing our capital allocation strategy. Revenue was stable in local currency terms, as we deliberately rationalized non‐strategic and low‐margin business. We began these efforts in 2010 in the Color Group and effectively concluded them in the first half of 2014. Revenue rationalization was more significant in the Flavors & Fragrances Group during 2014, and these actions will continue to impact the Group’s revenue growth in 2015. Consolidated revenue grew by 2.5% in local currency, excluding the impact of the rationalized business. Color Group – Another Strong Year The Color Group had another strong year in 2014, producing local currency revenue growth of 4%, and profit growth of 7%. The Color Group’s operating margins improved to 22.6%, an increase of 80 basis points over 2013. The Color Group’s 2014 performance was driven by its technical capabilities, innovation and market reach, and these strengths will continue to drive new growth. Sensient continues to build on our leadership in colors for foods and beverages. We stand out from competitors because of our unique ability to provide a full spectrum of both synthetic and natural color solutions. In 2014, our proprietary natural blue and brown color systems increased sales as manufacturers increasingly seek to extend their clean‐label offerings. The Color Group’s cosmetics business also performed well in 2014, and we expect sustainable growth moving forward. In 2015, we will 1

2 0 1 4 N E T I N C O M E MILLION $147 2 2 0 1 4 C A S H F L O W MILLION $189 open a new Center of Excellence just outside Paris, where we can showcase our capabilities in cosmetics and work closely with manufacturers from around the world. This new facility will enable us to strengthen ties with customers, accelerate product development and increase sales. In 2014, our industrial ink business performed especially well, and we see significant opportunities for growth in this segment. Our proprietary line of aqueous colors for digital printing is environmentally friendly and provides tremendous advantages, including brighter colors and faster printing speeds, to manufacturers of clothing, textiles and other products. The Color Group’s performance in the last five years serves as a model for the entire Company. When I joined Sensient in 2009, the Color Group’s annual revenue was $375 million, operating income was just under $59 million and the operating margin was 15.7%. During the last five years, the Group’s businesses have delivered strong growth and expanded operating margins by focusing on product development and sales coverage, improving the product mix to emphasize value‐added solutions and reducing costs. From 2009 to 2014, Color Group revenue increased 35%, while eliminating $50 million in low-margin business, operating profit has nearly doubled and our operating margin increased by 690 basis points to 22.6%. Flavors & Fragrances Group – Change and Progress In 2013, we began implementing a series of strategic initiatives in the Flavors & Fragrances Group to match the success of the Color Group. We instituted processes used by the Color Group to foster new product development and strengthened our sales and technical teams. We also realigned our commercial and technical activities around industry segments that better serve our customers. In 2014, we began to eliminate non‐strategic product lines and products that do not generate adequate margins. We will continue to evaluate our product offerings with the goal of utilizing our unique ingredients within higher‐margin, value‐added flavor and fragrance systems that are differentiated from the competition. We are also streamlining production to improve plant utilization and lower costs. These strategic changes and restructuring efforts will temper our revenue growth in 2015 for the Flavors & Fragrances Group. We do expect to see improvement in both gross margins and operating margins next year. The Group remains on track to achieve operating margins in the high‐teens and consistent operating profit growth. Sensient’s new state‐of‐the‐art Flavors & Fragrances Group headquarters, located just outside Chicago, underscores our commitment to product development and customer engagement. At the new headquarters, we can better showcase our broad product portfolio, develop new solutions and collaborate with customers. Overall, the Flavors & Fragrances Group is on track. While the Group’s operating profit did not grow, we saw significant improvement in the gross profit margin, which increased by 130 basis points. Operating margins also improved, even with our investment in sales and technical personnel. Several of the Group’s businesses performed very well and achieved double‐digit profit growth in 2014. Highlights include new wins with yogurt products; a growing beverage flavors business; and improved profitability and margin growth for our natural ingredients business. 2

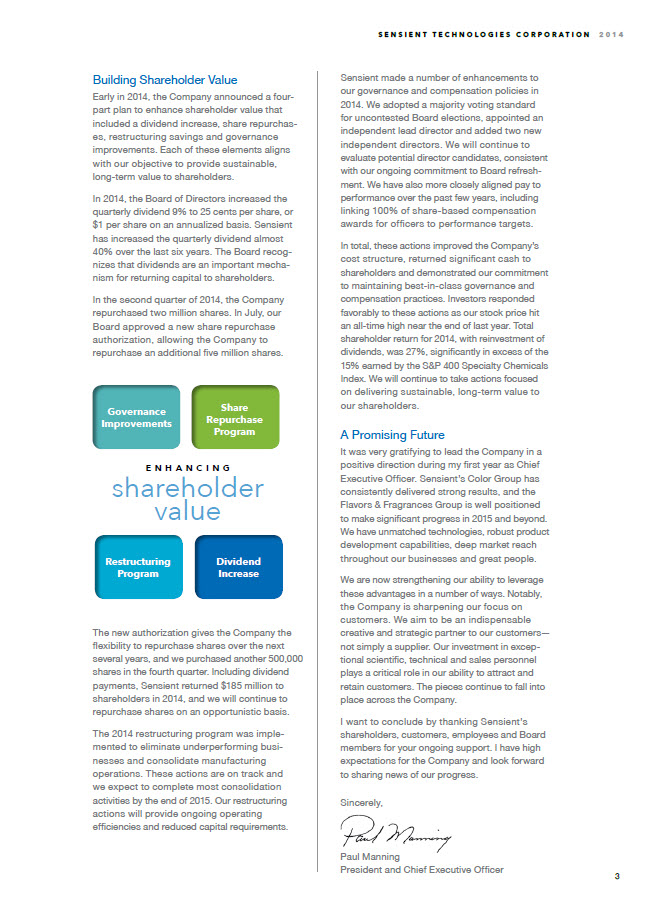

S E N S I E N T T E C H N O L O G I E S C O R P O R AT I O N 2 0 1 4 Building Shareholder Value Early in 2014, the Company announced a fourpart plan to enhance shareholder value that included a dividend increase, share repurchases, restructuring savings and governance improvements. Each of these elements aligns with our objective to provide sustainable, long-term value to shareholders. In 2014, the Board of Directors increased the quarterly dividend 9% to 25 cents per share, or $1 per share on an annualized basis. Sensient has increased the quarterly dividend almost 40% over the last six years. The Board recognizes that dividends are an important mechanism for returning capital to shareholders. In the second quarter of 2014, the Company repurchased two million shares. In July, our Board approved a new share repurchase authorization, allowing the Company to repurchase an additional five million shares. The new authorization gives the Company the flexibility to repurchase shares over the next several years, and we purchased another 500,000 shares in the fourth quarter. Including dividend payments, Sensient returned $185 million to shareholders in 2014, and we will continue to repurchase shares on an opportunistic basis. The 2014 restructuring program was implemented to eliminate underperforming businesses and consolidate manufacturing operations. These actions are on track and we expect to complete most consolidation activities by the end of 2015. Our restructuring actions will provide ongoing operating efficiencies and reduced capital requirements. Sensient made a number of enhancements to our governance and compensation policies in 2014. We adopted a majority voting standard for uncontested Board elections, appointed an independent lead director and added two new independent directors. We will continue to evaluate potential director candidates, consistent with our ongoing commitment to Board refreshment. We have also more closely aligned pay to performance over the past few years, including linking 100% of share-based compensation awards for officers to performance targets. In total, these actions improved the Company’s cost structure, returned significant cash to shareholders and demonstrated our commitment to maintaining best‐in‐class governance and compensation practices. Investors responded favorably to these actions as our stock price hit an all‐time high near the end of last year. Total shareholder return for 2014, with reinvestment of dividends, was 27%, significantly in excess of the 15% earned by the S&P 400 Specialty Chemicals Index. We will continue to take actions focused on delivering sustainable, long‐term value to our shareholders. A Promising Future It was very gratifying to lead the Company in a positive direction during my first year as Chief Executive Officer. Sensient’s Color Group has consistently delivered strong results, and the Flavors & Fragrances Group is well positioned to make significant progress in 2015 and beyond. We have unmatched technologies, robust product development capabilities, deep market reach throughout our businesses and great people. We are now strengthening our ability to leverage these advantages in a number of ways. Notably, the Company is sharpening our focus on customers. We aim to be an indispensable creative and strategic partner to our customers— not simply a supplier. Our investment in exceptional scientific, technical and sales personnel plays a critical role in our ability to attract and retain customers. The pieces continue to fall into place across the Company. I want to conclude by thanking Sensient’s shareholders, customers, employees and Board members for your ongoing support. I have high expectations for the Company and look forward to sharing news of our progress. Sincerely, Paul Manning President and Chief Executive Officer

RATEGIC Initiatives Sensient’s long-term strategy positions the Company for increased profitability and sustainable growth. The components of our strategy enable us to succeed in growing markets and deliver value to shareholders. E M P H A S I S O N Sensient is accelerating our shift to a product portfolio of complex, technology-driven systems that cannot be easily duplicated by our competitors. Our specialty systems bring unique attributes to our customers’ end products, which drives success in highly competitive consumer segments. Our products stand apart in the marketplace, enabling us to attract new projects, retain customers for the long term and achieve higher margins. We continue to exit low-margin, non-strategic businesses that do not offer growth opportunities or strong value to our customers. E N H A N C E D C A P I T A L A L L O C AT I O N The Company continues to improve capital allocation by reinvesting in projects with the highest return on invested capital, while maintaining investment-grade debt levels. We are also delivering shareholder value with a substantial dividend and stock buyback program.

I N D U S T R Y- L E A D I N G Personnel Sensient continually seeks out personnel with creative initiative, competitive energy and a commitment to serving customers and advancing the Company’s standing in the marketplace. We recruit top-level scientists, technicians and sales professionals with deep industry experience. Our personnel provide insight and expertise valued by our customers. O P T I M I Z E D M A N U FA C T U R I N G A C O M M I T M E N T TO O R G A N I C G R O W T H A N D I N N O V AT I O N Sensient is expanding our business by strengthening our engagement with customers at all stages of product development and manufacturing. We are also driving organic growth through our steadfast commitment to innovation and new product development.

COLOR Group Sensient’s Color Group is the leading global developer of high-performance colors and specialty ingredients for major consumer product segments. Through a robust R&D program, we advance the science of color and provide ongoing innovations that enable our customers to excel in highly competitive markets. We focus on developing unique products that deliver value to our customers. MARKETS WE SERV E % O F R E V E N U E G E N E R A T E D 59% 22% 14% Food and Beverage Colors Cosmetic Ingredients Specialty Inks

S E N S I E N T T E C H N O L O G I E S C O R P O R AT I O N 2 0 1 4 2014 RESULTS S A L E S R E V E N U E 4% 1% O P E R AT I N G I N C O M E A S E N S E O F P E R S P E C T I V E Pharmaceutical Excipients Technical Colors Sensient’s Color Group has made significant progress over the last five years. We have eliminated non-strategic, low-margin operations to sharpen our focus on innovative, high-margin product lines. Since 2009, even while eliminating $50 million in low-margin revenue, overall Group revenues have increased by 35% and operating income has nearly doubled.

OLOR Group I N N OVAT I V E C O LOR S O LU T I O N S LARGEST PORTFOLIO Sensient partners with our customers to help them recognize consumer trends and benefit from the latest color innovations. We offer the broadest spectrum of natural and synthetic color systems for food and non-food markets available in the industry. A REVOLUTIONARY CHANGE IN DIGITAL PRINTING Sensient’s high-performance aqueous color systems for digital printing are enabling clothing, textile and other industrial manufacturers to make significant production and logistics changes that greatly improve their businesses. With Sensient technology, our customers can create a versatile selection of products using rapid, short-run printing that reduces cost and minimizes environmental impacts.

S E N S I E N T T E C H N O L O G I E S C O R P O R AT I O N 2 0 1 4 Sensient’s comprehensive approach to supply chain management enables our customers to maintain efficient operations and protect the value of their brands. Our emphasis on product safety through sourcing, manufacturing and testing provides peace of mind to our customers G L O B A L I N N O V AT I O N GLO CAL L O C A L A P P L I C AT I O N While Sensient’s R&D centers develop technologies with global scope, our regional service labs work closely with customers to formulate applications for local markets. The Company’s best-in-class technical, regulatory and sales services strengthen our ties to customers. S U P P LY C H A I N S A F E T Y it’s only N AT U R A L CLEAN-LABEL FOOD AND BEVERAGE Consumers are increasingly seeking naturally sourced products but still want vibrant, colorful products. Sensient is making significant progress in closing the gap between natural and synthetic colors. Our proprietary natural blue greatly expands the range of natural colors available across all food and beverage categories.

Group Sensient’s Flavors & Fragrances Group is a leading provider of specialty systems for manufacturers of foods, beverages and household products. We combine proprietary technologies, scientific expertise and consumer insight to create unique solutions that enable our customers to excel in competitive markets. We will achieve higher margins and sustainable growth by emphasizing value-added, technology-based flavor and fragrance systems. MARKETS WE SERV E % O F R E V E N U E G E N E R A T E D 27% 27% 20% 10% Natural Ingredients Sweet Savory Fragrance

S E N S I E N T T E C H N O L O G I E S C O R P O R AT I O N 2 0 1 4 2014 RESULTS S A L E S R E V E N U E 9% 7% Beverage BioNutrient A S T R O N G E R D I R E C T I O N In 2013, Sensient changed the strategic direction of the Flavors & Fragrances Group to drive operating profit growth. We began to shift our product mix to higher-margin, value-added products; added new management talent; and focused on cost reduction. We realigned our business units around customer-focused segments and relocated the Group’s global headquarters to the Chicago area. In 2014, we started the process of consolidating manufacturing facilities, which will provide substantial, ongoing cost savings. The Group’s gross profit margins improved by 130 basis points in 2014, and we expect continued improvement in operating margins during the next few years.

FRAGRANCES Group Natural Extracts D E L I V E R I N G T H E TA S T E O F NAT U R E Sensient uses proprietary extraction technologies to develop vibrant, authentic taste profiles from botanical sources. The resulting natural extracts can be combined to create an infinite variety of flavors, enabling our customers to manufacture unique products that stand out in the marketplace. Sensient’s raw-material sourcing helps ensure quality control, product safety and traceability. As a result, manufacturers can enhance their marketing by labeling finished products with specific provenance declarations. health & wellness Drawing on Sensient’s unique flavor portfolio, food and beverage manufacturers are able to meet the growing consumer demand for products with reduced sugar, sodium and fat. Our flavor technologies enable caloric -reduction, while enhancing taste, masking offnotes and adding nutritional value. We will continue to increase sales and strengthen our leadership in the expanding health and wellness segment.

S E N S I E N T T E C H N O L O G I E S C O R P O R AT I O N 2 0 1 4 less fat less sodium less sugar A proprietary, all-natural line of flavormasking technologies, Smoothenol 2G™ eliminates off-notes and aftertastes associated with a new generation of natural, clean-label food and beverage products. This complete flavor-masking toolkit is unmatched in the industry. M O R E More Appealing SMOOTHENOL 2G™ NATURAL MASKING TECHNOLOGY More Choices PURE VARIETALS TRUE-TO-TYPE NATURAL FLAVORS Today’s consumers are increasingly seeking fruit varietals as part of a healthy and flavorful diet. To enable our customers to capitalize on this trend, we introduced Pure Varietals, which bring distinct true-to-type fruit flavors to foods and beverages. This product line includes several fruit varieties, notably ten apple, six peach and six cherry flavors.

FRAGRANCES Group 14 THE VALUE OF CONSUMER INSIGHT A P O S I T I V E R E ACTION Simple Apple Complete Apple Pie Sensient combines exclusive ingredients and reaction flavor technologies to develop more complex flavor profiles that appeal to consumers. These sophisticated systems result in authentic tastes that mirror entire dishes; for instance, not apple, but apple pie—complete with fruit, spice, sweetness and crust. Sensient consumer researchers shape product development and provide valuable insight to our customers. Through our proprietary predictive process, we identify consumer trends and emerging flavor preferences that drive new business development across all of our market segments. In 2014, our consumer insight research led to numerous product introductions including spirits, sauces and frozen desserts.

Sensient Technologies Corporation 2014

Management’s Discussion & Analysis of Operations & Financial Condition

OVERVIEW

Sensient Technologies Corporation (the “Company”) reported earnings per share from continuing operations of $1.67, which included $90.6 million, or $1.34 per share, of restructuring and other costs. As a part of its plan to enhance shareholder value, the Company implemented a restructuring plan (2014 Restructuring Plan), to eliminate underperforming operations, consolidate manufacturing facilities and improve efficiencies within the Company. The 2014 Restructuring Plan is anticipated to cost between $120 million and $130 million and reduce annual operating costs by approximately $30 million per year. Earnings per share from continuing operations were $2.29 in 2013, which includes restructuring costs of $31.7 million or $0.44 per share.

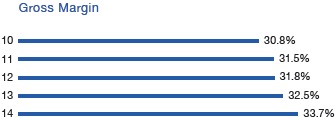

The Company’s adjusted 2014 earnings per share from continuing operations, adjusted to eliminate the impact of restructuring and other costs, increased 10.6% to $3.02 per share from $2.73 per share in 2013. Consolidated gross margin increased 130 basis points in 2014 to 33.9% and consolidated operating margin increased 120 basis points in 2014 to 15.3%, both before restructuring costs. The gross margin and operating margin improvements were driven by the Company’s focus on selling higher margin products and lower costs.

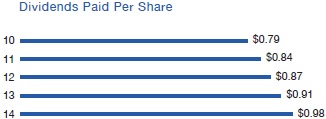

Cash flows from operating activities were very strong, increasing 23.2% in 2014 to $189.2 million from $153.6 million in 2013. The Company used its strong cash flows and debt capacity to repurchase 2.5 million shares of Company stock during the year. In addition, the Company increased its quarterly dividend 9% to 25 cents per share, or $1.00 per share on an annualized basis.

Additional information on the results is included below.

NON-GAAP FINANCIAL MEASURES

The table below reconciles certain reported results for years ended December 31, 2014 and 2013, to those results before the impact of the restructuring costs, which are non-GAAP financial measures. The Company has included non-GAAP financial measures to remove the costs related to the restructuring activities and other costs and provide investors with a view of operating performance excluding those costs. These non-GAAP financial measures are utilized by management in comparing the Company’s operating performance on a consistent basis. The Company believes that these financial measures are appropriate to enhance an overall understanding of the Company’s underlying operating performance trends compared to historical and prospective periods. The Company also believes that these measures should not be considered in isolation from, or as a substitute for, financial information calculated in accordance with GAAP.

| | | Twelve Months Ended December 31, | | | | |

| | | 2014 | | | 2013 | | | % Change | |

| Operating Income from continuing operations (GAAP) | | $ | 130,665 | | | $ | 173,780 | | | | (24.8 | %) |

| Restructuring - Cost of products sold | | | 1,914 | | | | 1,840 | | | | | |

| Restructuring & other - Selling and administrative | | | 88,636 | | | | 29,895 | | | | | |

| Adjusted operating income | | $ | 221,215 | | | $ | 205,515 | | | | 7.6 | % |

| Net Earnings from continuing operations (GAAP) | | $ | 81,771 | | | $ | 114,298 | | | | (28.5 | %) |

| Restructuring & other, before tax | | | 90,550 | | | | 31,735 | | | | | |

| Tax impact of restructuring & other | | | (25,014 | ) | | | (9,776 | ) | | | | |

| Adjusted net earnings | | $ | 147,307 | | | $ | 136,257 | | | | 8.1 | % |

| Diluted EPS from continuing operations (GAAP) | | $ | 1.67 | | | $ | 2.29 | | | | (27.1 | %) |

| Restructuring & other, net of tax | | | 1.34 | | | | 0.44 | | | | | |

| Adjusted diluted EPS | | $ | 3.02 | | | $ | 2.73 | | | | 10.6 | % |

RESTRUCTURING ACTIVITIES

In 2014, the Company announced that it was initiating its 2014 Restructuring Plan to eliminate underperforming operations, consolidate manufacturing facilities and improve efficiencies within the Company. The Company expects this plan to cost between $120 million and $130 million, and upon completion is anticipated to reduce annual operating costs by approximately $30 million per year. Incremental savings will be achieved over the next few years and the full benefit is expected to be achieved after 2016. Based on this plan, the Company determined that certain long-lived assets associated with the underperforming operations were impaired. The Company reduced the carrying amounts of these assets to their aggregate respective fair values of approximately $35 million, which were determined based on independent market values for these assets. Certain machinery and equipment has also been identified to be disposed of at the time of the facility closures and the associated depreciation for these assets has been accelerated. In addition, certain intangible assets and inventory were determined to be impaired and were written down. Employee separation and other restructuring costs were also incurred during 2014. The Company will reduce headcount by approximately 300 positions at impacted facilities primarily in the Flavors & Fragrance Group, related to direct and indirect labor at manufacturing sites. As of December 31, 2014, approximately 100 employees have been terminated. The Company recorded $101.5 million of restructuring and other costs in 2014, in accordance with GAAP and based on an internal review of the affected facilities and consultation with legal and other advisors. The Company expects to incur approximately $21 million to $31 million of additional restructuring costs by the end of 2016.

In connection with the 2014 Restructuring Plan, the Company approved a plan to dispose of a business within the Color segment. Production ceased in 2014 and the business met the criteria to be reported as a discontinued operation. The pre-tax loss from discontinued operations, which includes restructuring costs, was $11.5 million for 2014.

In 2013, the Company successfully completed its 2013 restructuring program related to relocating the Flavors & Fragrances Group headquarters to Chicago, and generating operating efficiencies across all segments of the Company by consolidating multiple facilities throughout Europe and North America. The Company recorded total costs of $31.7 million in 2013 related to the 2013 restructuring program, which included employee separation costs of $18.1 million, long-lived asset impairment of $4.2 million, gain on asset sale of $3.0 million, inventory write-down of $1.8 million, and other costs of $10.7 million. The other costs mainly consisted of decommissioning costs, professional service costs, personnel (other than employee separations) and moving related costs. The plan resulted in the reduction of global headcount of approximately 280 employees performing various functions. Management estimates that operating costs were reduced by approximately $12 million and $7 million as of December 31, 2014 and 2013, respectively.

RESULTS OF CONTINUING OPERATIONS

2014 vs. 2013

Sensient’s revenue was approximately $1.4 billion in 2014 and $1.5 billion in 2013. Sensient continues to shift to value added and technology driven products in each of our Groups, while actively rationalizing non-strategic and low margin business. Removing the impact of our rationalization efforts, our consolidated revenue increased 1.5% in 2014. Foreign currency translation did not have a material impact on consolidated revenue in 2014. Additional information on group results can be found in the Segment Information section.

The Company’s gross margin was 33.7% in 2014 and 32.5% in 2013. Included in the cost of sales are $1.9 million and $1.8 million of restructuring costs for 2014 and 2013, respectively, which reduced gross profit. Before these restructuring costs, gross margin increased 130 basis points to 33.9% in 2014 from 32.6% in 2013, primarily due to an increase in selling prices.

Selling and administrative expense as a percent of revenue was 24.7% in 2014 and 20.6% in 2013. Restructuring costs of $88.6 million and $30.0 million for 2014 and 2013, respectively, were included in selling and administrative expense. Before these restructuring costs, selling and administrative expense as a percent of revenue was 18.6% in both 2014 and 2013.

Operating income was $130.7 million in 2014 and $173.8 million in 2013. Before the restructuring costs, operating income increased 7.6% to $221.2 million in 2014 from $205.5 million in 2013 and consolidated operating margin increased 120 basis points to 15.3%. Additional information on group results can be found in the Segment Information section.

Interest expense was $16.1 million in both 2014 and 2013. The decrease in average interest rates offset the higher average outstanding debt balance.

The effective income tax rate was 28.6% in 2014 and 27.5% in 2013. The effective tax rates for both 2014 and 2013 were reduced by discrete items, including the favorable resolution of prior years’ tax matters and restructuring costs. In total, the discrete items and the impact of restructuring costs had no impact on the effective tax rate for 2014 and reduced the effective tax rate by 2.0% in 2013.

| | | 2014 | | | 2013 | |

| Rate before restructuring and discrete items | | | 28.6 | % | | | 29.5 | % |

| Restructuring impact | | | 0.8 | % | | | (0.3 | %) |

| Discrete items | | | (0.8 | %) | | | (1.7 | %) |

| Reported effective tax rate | | | 28.6 | % | | | 27.5 | % |

The effective tax rate for 2015 is expected to be between 29.5% and 30.5% prior to the recording of any discrete items and restructuring costs.

SEGMENT INFORMATION

The Company determines its operating segments based on information utilized by the chief operating decision maker to allocate resources and assess performance. Group performance is evaluated on operating income of the respective business units before restructuring charges which are reported in the Corporate & Other segment.

The Company’s reportable segments consist of the Flavors & Fragrances Group and Color Group. The results of two additional operating segments, the Asia Pacific Group and Flavors Central & South America, are reported in the Corporate & Other segment. Beginning in 2014, the results of operations for the Company’s fragrances business in Asia Pacific, previously reported in the Corporate & Other segment, are reported in the Flavors & Fragrances segment, and the results of operations for the Company’s pharmaceutical flavors business, previously reported in the Flavors & Fragrances segment, are reported in the Color segment with the pharmaceutical colors business. The Color segment results have been restated to remove the impact of a discontinued operation. The prior year results have been restated as a result of these changes.

Flavors & Fragrances Revenue for the Flavors & Fragrances Group was $847.0 million in 2014 and $876.5 million in 2013. The decrease in revenue was primarily due to lower revenue in North America ($23.3 million) and the unfavorable impact of exchange rates ($5.5 million). The lower revenue in North America was primarily related to lower natural ingredient volumes. In local currency, revenue decreased 2.7%.

Gross margin increased 130 basis points to 26.6% in 2014 from 25.3% in 2013. The increase was primarily due to the impact of higher selling prices.

Operating income for the Flavors & Fragrances Group was $119.1 million in 2014 and $120.3 million in 2013. The decrease was primarily due to the impact of unfavorable exchange rates ($0.9 million). Higher profit in North America ($1.1 million) and Mexico ($0.4 million) was offset by lower profit in Europe ($1.8 million). The higher profit in North America was due to higher selling prices, and savings associated with the restructuring program. The lower profit in Europe was primarily due to higher employee costs. In local currency, operating income decreased 0.3%. Operating margin for the Flavors & Fragrances Group increased 40 basis points to 14.1% in 2014 from 13.7% in 2013, primarily due to the Group’s focus on higher margin, value-added products.

Color Revenue for the Color Group increased 2.6% in 2014 to $508.1 million from $495.1 million in 2013. The increase in revenue was primarily due to higher sales of non-food colors ($11.8 million) and food and beverage colors ($6.5 million) partially offset by the unfavorable impact of exchange rates ($5.3 million). The higher sales of non-food colors were primarily due to higher volumes, and the higher sales of food and beverage colors were due to higher selling prices. In local currency, revenue increased 3.7%.

Gross margin for the Color Group increased 80 basis points to 41.7% in 2014 from 40.9% in 2013. The increase was primarily due to the impact of higher selling prices and the higher volumes.

Operating income for the Color Group increased 6.5% to $114.9 million in 2014 from $107.9 million in 2013. The increase was primarily due to non-food colors ($5.5 million) and food and beverage colors ($2.3 million) partially offset by the unfavorable impact of exchange rates ($0.8 million). The higher profit for non-food colors was primarily due to the higher volumes and favorable product mix. The higher profit for food and beverage colors was primarily due to higher selling prices. Operating margin for the Color Group increased 80 basis points to 22.6% in 2014 from 21.8% in 2013. In local currency, operating income increased 7.3%.

Corporate & Other The Corporate & Other segment includes the Asia Pacific Group and certain flavors businesses in Central and South America, combined with the corporate office expenses.

Revenue for the Corporate & Other segment was $146.7 million in 2014 and $145.2 million in 2013. The increase was primarily due to higher volumes and selling prices in the Asia Pacific Group offset by the unfavorable impact of exchange rates ($4.5 million). In local currency, revenue increased 4.2%.

The Corporate & Other segment reported operating losses of $103.3 million in 2014 and $54.4 million in 2013. Before the impact of restructuring costs, the Corporate & Other segment reported operating losses of $12.8 million and $22.6 million in 2014 and 2013, respectively. The improvement on results before the impact of restructuring costs was primarily due to lower corporate expenses and higher profit in the Asia Pacific Group. The lower corporate expenses were due to lower employee related compensation.

RESULTS OF CONTINUING OPERATIONS

2013 vs. 2012

Sensient’s revenue was approximately $1.5 billion in both 2013 and 2012. Revenue in the Flavors & Fragrances Group was $876.5 million in 2013 and $870.0 million in 2012. Color Group revenue was $495.1 million in 2013 and $500.7 million in 2012. Corporate & Other revenue, which includes the Company’s operations in the Asia Pacific region and certain flavor operations in Central and South America, was $145.2 million in 2013 and $139.6 million in 2012. Foreign currency translation did not have a material impact on consolidated revenue in 2013. Additional information on group results can be found in the Segment Information section.

The Company’s gross margin was 32.5% in 2013, an increase of 70 basis points from 31.8% in 2012. The 2013 gross margin before the impact of restructuring costs was 32.6%. The impact of increased selling prices and favorable product mix more than offset higher manufacturing costs in 2013.

Selling and administrative expense as a percent of revenue was 20.6% in 2013 compared to 18.6% in 2012. The increase in selling and administrative expenses during 2013 was attributable to the Company’s restructuring costs recorded in the year. Selling and administrative expense as a percent of revenue before the impact of restructuring costs in 2013 was 18.6%.

Operating income was $173.8 million in 2013 compared to $192.9 million in 2012. Before the $31.7 million of total restructuring costs, operating income for 2013 was $205.5 million, an increase of 6.6% from the prior year. Additional information on group results can be found in the Segment Information section.

Interest expense decreased 4.5% to $16.1 million in 2013 from $16.9 million in 2012. The decrease was due to lower average interest rates partially offset by higher average outstanding debt balances.

The effective income tax rate was 27.5% in 2013 and 28.9% in 2012. The effective tax rates for both 2013 and 2012 were reduced by discrete items, including the favorable resolution of prior years’ tax matters. In addition, the 2013 rate was impacted by restructuring costs. In total, these discrete items and the impact of restructuring costs reduced the effective tax rate for 2013 and 2012 by 2.0% and 2.2%, respectively.

| | | 2013 | | | 2012 | |

| Rate before restructuring and discrete items | | | 29.5 | % | | | 31.1 | % |

| Restructuring impact | | | (0.3 | %) | | | — | |

| Discrete items | | | (1.7 | %) | | | (2.2 | %) |

| Reported effective tax rate | | | 27.5 | % | | | 28.9 | % |

SEGMENT INFORMATION

Flavors & Fragrances Revenue for the Flavors & Fragrances Group was $876.5 million in 2013 and $870.0 million in 2012. The Group reported higher selling prices ($15.4 million) and the favorable impact of foreign currency translation ($4.5 million), partially reduced by lower volumes ($13.4 million). Higher selling prices were reported in both natural ingredients and traditional flavors. The lower volumes were driven by natural ingredients in North America partially offset by higher volumes in traditional flavors.

Gross margins were 25.3% of revenue in both 2013 and 2012. The impact of higher selling prices offset an increase in manufacturing costs.

The Flavors & Fragrances Group operating income was $120.3 million in 2013 and $120.8 million in 2012. The decrease in operating income was primarily related to operations in Europe and other locations ($5.2 million), partially offset by higher operating income in North America ($4.8 million). The lower profit in Europe was driven by higher employee costs related to selling and technical personnel and other costs, partially offset by the impact of higher volume. The higher profit in North America was primarily due to higher selling prices, partially offset by the impact of lower volumes and higher raw material costs. Operating income as a percent of revenue was 13.7% in 2013 and 13.9% in 2012, primarily for the reasons discussed above.

Color The Color Group revenue was $495.1 million in 2013 and $500.7 million in 2012. The decrease in revenue was primarily driven by lower sales of non-food colors ($9.1 million), partially offset by higher sales of food and beverage colors ($3.7 million). The lower sales of non-food colors were driven by lower volumes of OEM inkjet products as a result of the termination of a supply agreement by a major customer in early 2013. The Group has been replacing non-strategic products such as these with higher margin, value-added products.

Gross margin for the Color Group increased 220 basis points to 40.9% in 2013 from 38.7% in 2012. Higher selling prices, favorable product mix and favorable raw material costs were the primary reasons for the improved margins. The 2013 results reflect the Group’s strategy to focus on higher margin products and eliminate non-strategic business.

Color Group operating income in 2013 increased 6.7% to $107.9 million from $101.1 million in 2012. The increase in operating income was primarily attributable to food and beverage colors ($3.9 million) and non-food colors ($3.0 million). The higher operating income from food and beverage colors was primarily due to the impact of favorable volumes and raw material costs. The increase in operating income for non-food colors was primarily due to favorable product mix and raw material costs. Operating income as a percent of revenue increased 160 basis points to 21.8% in 2013 from 20.2% in 2012, primarily due to the reasons described above.

Corporate & Other The Corporate & Other segment includes the Asia Pacific region, and certain of the Company’s flavor businesses in Central and South America, combined with corporate expenses.

Revenue for the Corporate & Other segment was $145.2 million and $139.6 million in 2013 and 2012, respectively. The increase was primarily related to higher volumes in Asia Pacific.

The Corporate & Other segment reported operating losses of $54.4 million and $29.0 million in 2013 and 2012, respectively. Before the impact of restructuring costs, the Corporate & Other segment reported operating losses of $22.6 million in 2013. The improvement in results before the impact of restructuring costs was primarily due to profit on higher volumes and favorable product mix in Asia Pacific and lower corporate expenses.

LIQUIDITY AND FINANCIAL POSITION

The Company’s financial position remains strong, enabling it to meet cash requirements for operations, acquisitions, capital expansion programs, dividend payments to shareholders and share repurchases. The Company intends to fund working capital requirements, principal and interest payments, acquisitions and other liabilities with cash provided by operations, to the extent available, and short-term and long-term borrowings under new and existing credit facilities.

The Company’s ratio of debt to total capital was 30.8% at December 31, 2014, compared to 22.2% at December 31, 2013. The increase in 2014 was primarily due to the increase in debt to fund share repurchases.

Net cash provided by operating activities was $189.2 million in 2014, $153.6 million in 2013 and $139.4 million in 2012. Operating cash flow provided the primary source of funds for operating needs, capital expenditures, shareholder dividends and some share repurchases. The increase in net cash provided by operating activities in 2014 was primarily due to higher earnings and working capital reductions in the second half of 2014. The increase in cash from operating activities in 2013 was primarily due to a lower use of working capital partially offset by lower earnings as a result of the 2013 restructuring program.

Net cash used in investing activities was $79.1 million in 2014, $98.2 million in 2013 and $102.7 million in 2012. Capital expenditures were $79.4 million in 2014, $104.2 million in 2013 and $103.8 million in 2012.

Net cash used in financing activities was $98.6 million in 2014, $48.2 million in 2013 and $48.8 million in 2012. The Company had a net increase in debt of $85.8 million in 2014 and a net decrease in debt of $3.7 million in 2013 and a net increase of $15.9 million in 2012. In 2014, Sensient purchased $137.2 million of Company stock which settled before December 31, 2014.

The Company has paid uninterrupted quarterly cash dividends since commencing public trading in its stock in 1962. In the first quarter of 2014, the Company announced an increase in its quarterly dividend from 23 cents per share to 25 cents per share. Dividends paid per share were 98 cents in 2014, 91 cents in 2013 and 87 cents in 2012. Total dividends paid were $47.9 million, $45.5 million and $43.4 million in 2014, 2013 and 2012, respectively.

The impact of inflation on both the Company’s financial position and its results of operations has been minimal and is not expected to significantly affect 2015 results.

ISSUER PURCHASES OF EQUITY SECURITIES

Sensient purchased 2.5 million shares of Company stock in 2014 for a total cost of $138.3 million and 0.6 million shares of Company stock in 2012 for a total cost of $23.2 million. There were no purchases of Company stock in 2013. In July 2014, the Board approved a new share repurchase program under which the Company is authorized to repurchase an additional five million shares of Company stock in addition to amounts remaining from prior Board authorizations. As of December 31, 2014, 4.9 million shares were available to be repurchased under existing authorizations. The Company’s share repurchase program has no expiration date.

CRITICAL ACCOUNTING POLICIES

In preparing the financial statements in accordance with accounting principles generally accepted in the U.S., management is required to make estimates and assumptions that have an impact on the asset, liability, revenue and expense amounts reported. These estimates can also affect supplemental information disclosures of the Company, including information about contingencies, risk and financial condition. The Company believes, given current facts and circumstances, that its estimates and assumptions are reasonable, adhere to accounting principles generally accepted in the U.S. and are consistently applied. Inherent in the nature of an estimate or assumption is the fact that actual results may differ from estimates and estimates may vary as new facts and circumstances arise. The Company makes routine estimates and judgments in determining the net realizable value of accounts receivable, inventories, property, plant and equipment, and prepaid expenses. Management believes the Company’s most critical accounting estimates and assumptions are in the following areas:

Revenue Recognition The Company recognizes revenue (net of estimated discounts, allowances and returns) when title passes, the customer is obligated to pay the Company and the Company has no remaining obligations. Such recognition typically corresponds with the shipment of goods.

Goodwill Valuation The Company reviews the carrying value of goodwill annually utilizing several valuation methodologies, including a discounted cash flow model. The Company completed its annual goodwill impairment test under Accounting Standards Codification (ASC) 350, Intangibles – Goodwill and Other, in the third quarter of 2014. In conducting its annual test for impairment, the Company estimates the fair value for each of its reporting units and compares each of these values to the net book value of each reporting unit. Fair value is estimated using both a discounted cash flow analysis and an analysis of comparable company market values. If the fair value of a reporting unit exceeds its net book value, no impairment exists. The Company has three reporting units that had goodwill recorded and were tested for impairment. The Flavors & Fragrances reporting unit and the Asia Pacific reporting unit had fair values that were over 100% above their respective net book values. The fair value of the Color reporting unit had a fair value that was over 90% above its net book value. Changes in estimates of future cash flows caused by items such as unforeseen events or changes in market conditions could negatively affect the reporting units’ fair value and result in an impairment charge.

Income Taxes The Company estimates its income tax expense in each of the taxing jurisdictions in which it operates. The Company is subject to a tax audit in each of these jurisdictions, which could result in changes to the estimated tax expense. The amount of these changes would vary by jurisdiction and would be recorded when probable and estimable. These changes could impact the Company’s financial statements. Management has recorded valuation allowances to reduce the Company’s deferred tax assets to the amount that is more likely than not to be realized. Examples of deferred tax assets include deductions, net operating losses and tax credits that the Company believes will reduce its future tax payments. In assessing the future realization of these assets, management has considered future taxable income and ongoing tax planning strategies. An adjustment to the recorded valuation allowance as a result of changes in facts or circumstances could result in a significant change in the Company’s tax expense. The Company does not provide for deferred taxes on unremitted earnings of foreign subsidiaries which are considered to be invested indefinitely.

Commitments and Contingencies The Company is subject to litigation and other legal proceedings arising in the ordinary course of its businesses or arising under provisions related to the protection of the environment. Estimating liabilities and costs associated with these matters requires the judgment of management, who rely in part on information from Company legal counsel. When it is probable that the Company has incurred a liability associated with claims or pending or threatened litigation matters and the Company’s exposure is reasonably estimable, the Company records a charge against earnings. The Company recognizes related insurance reimbursement when receipt is deemed probable. The Company’s estimate of liabilities and related insurance recoveries may change as further facts and circumstances become known.

MARKET RISK FACTORS

The Company is exposed to market risks, including changes in interest rates, currency exchange rates and commodity prices. To manage the volatility relating to these exposures on a consolidated basis, the Company nets the exposures to take advantage of natural offsets. The Company also enters into various derivative transactions for some of the remaining exposures pursuant to the Company’s policies covering hedging practices. The financial impacts of these hedging instruments are offset by corresponding changes in the underlying exposures being hedged.

The Company does not hold or issue derivative financial instruments for trading purposes. Note 1 and Note 4 to the Consolidated Financial Statements include a discussion of the Company’s accounting policies for financial instruments.

A key part of the Company’s strategy is to expand into new geographic markets. Because the Company manufactures and sells its products throughout the world, it is exposed to movements in foreign currency exchange rates. The major foreign currency exposures involve the markets in Western Europe, Mexico and Canada. The primary purpose of the Company’s foreign currency hedging activities is to protect against the volatility associated with foreign currency sales, purchases of materials, and other assets and liabilities created during the normal course of business. The Company generally utilizes foreign exchange contracts with durations of less than 12 months that may or may not be designated as cash flow hedges under ASC 815, Derivatives and Hedging. The net fair value of these instruments, based on dealer quotes, was a liability of $0.1 million at December 31, 2014, and an asset of $0.2 million at December 31, 2013. At December 31, 2014, the potential gain or loss in the fair value of the Company’s outstanding foreign exchange contracts, assuming a hypothetical 10% fluctuation in the currencies of such contracts, would be approximately $1.5 million. However, any change in the value of the contracts, real or hypothetical, would be significantly offset by a corresponding change in the value of the underlying hedged items. In addition, this hypothetical calculation assumes that each exchange rate would change in the same direction relative to the U.S. dollar.

The Company has certain debt denominated in Swiss Francs and Euros. These non-derivative debt instruments act as partial hedges of the Company’s Swiss Franc and Euro net asset positions. The potential increase or decrease in the annual U.S. dollar interest expense of the Company’s outstanding foreign currency-denominated debt, assuming a hypothetical 10% fluctuation in the currencies of such debt, would be approximately $0.2 million at December 31, 2014. However, any change in interest expense from fluctuations in currency, real or hypothetical, would be significantly offset by a corresponding change in the value of the foreign income before interest. In addition, this hypothetical calculation assumes that each exchange rate would change in the same direction relative to the U.S. dollar.

The Company manages its debt structure and interest rate risk through the use of fixed rate and floating rate debt and through the use of derivatives. The Company’s primary exposure is to interest rates in the U.S. and Western Europe. At December 31, 2014, the potential increase or decrease in annual interest expense, assuming a hypothetical 10% fluctuation in interest rates of floating rate debt, would be approximately $0.3 million.

The Company is the purchaser of certain commodities, such as corn, sugar, soybean meal and fruits. The Company generally purchases these commodities based upon market prices that are established with the vendor as part of the purchase process. In general, the Company does not use commodity financial instruments to hedge commodity prices due to a high correlation between the commodity cost and the ultimate selling price of the Company’s products. On occasion, the Company may enter into non-cancelable forward purchase contracts, as deemed appropriate, to reduce the effect of price fluctuations on future manufacturing requirements.

CONTRACTUAL OBLIGATIONS

The Company is subject to certain contractual obligations, including long-term debt, operating leases, manufacturing purchases and pension benefit obligations. The Company has unrecognized tax benefits of $13.9 million as of December 31, 2014. However, the Company cannot make a reasonably reliable estimate of the period of potential cash settlement of the liabilities and, therefore, has not included unrecognized tax benefits in the following table of significant contractual obligations as of December 31, 2014.

PAYMENTS DUE BY PERIOD

| (in thousands) | | Total | | | 1 year | | | 2-3 years | | | 4-5 years | | | > 5 years | |

| Long-term debt | | $ | 451,011 | | | $ | 18,384 | | | $ | 142,870 | | | $ | 168,487 | | | $ | 121,270 | |

| Interest payments on long-term debt | | | 53,143 | | | | 13,731 | | | | 22,331 | | | | 12,920 | | | | 4,161 | |

| Operating lease obligations | | | 19,479 | | | | 7,657 | | | | 6,803 | | | | 3,201 | | | | 1,818 | |

| Manufacturing purchase commitments | | | 50,064 | | | | 48,846 | | | | 1,218 | | | | — | | | | — | |

| Pension funding obligations | | | 44,217 | | | | 9,722 | | | | 10,016 | | | | 7,021 | | | | 17,458 | |

| Total contractual obligations | | $ | 617,914 | | | $ | 98,340 | | | $ | 183,238 | | | $ | 191,629 | | | $ | 144,707 | |

NEW PRONOUNCEMENTS

On January 1, 2014, the Company adopted Accounting Standards Update (ASU) No. 2013-11, Income Taxes (Topic 740), Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists, which requires companies to change the balance sheet presentation of certain unrecognized tax benefits and deferred tax assets. The adoption of this ASU had no material impact on the Company’s balance sheet presentation, financial condition or results of operations.

On April 10, 2014, the Financial Accounting Standards Board (“FASB”) issued ASU No. 2014-08, Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity, which amends the definition of a discontinued operation in ASC 205-20, “Discontinued Operations” and requires companies to provide additional disclosures for disposal transactions. Under the revised standard, a discontinued operation represents a strategic shift that has or will have a major impact on an entity’s operations or financial results. ASU 2014-08 is required to be applied prospectively to all disposals that occur in annual periods beginning on or after December 15, 2014, with early adoption permitted. The Company will prospectively apply this guidance in 2015.

On May 28, 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers. The requirements of the new standard are effective for interim and annual periods beginning after December 15, 2016, with early adoption not permitted. The Company is currently evaluating the expected impact of this new standard.

OFF-BALANCE SHEET ARRANGEMENTS

The Company had no off-balance sheet arrangements as of December 31, 2014.

FORWARD-LOOKING STATEMENTS

This document contains forward-looking statements that reflect management’s current assumptions and estimates of future economic circumstances, industry conditions, Company performance and financial results. Forward-looking statements include statements in the future tense, statements referring to any period after December 31, 2014, and statements including the terms “expect,” “believe,” “anticipate” and other similar terms that express expectations as to future events or conditions. The Private Securities Litigation Reform Act of 1995 provides a safe harbor for such forward-looking statements. Such forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors that could cause actual events to differ materially from those expressed in those statements. A variety of factors could cause the Company’s actual results and experience to differ materially from the anticipated results. These factors and assumptions include the pace and nature of new product introductions by the Company’s customers; the Company’s ability to successfully implement its growth strategies; the outcome of the Company’s various productivity-improvement and cost-reduction efforts or other restructuring or relocation activities; changes in costs and availability of raw materials and energy; industry and economic factors related to the Company’s domestic and international business; competition from other suppliers of colors, flavors and fragrances; growth or contraction in markets for products in which the Company competes; terminations and other changes in customer relationships; industry acceptance of price increases; currency exchange rate fluctuations; cost and availability of credit; and the matters discussed above including the critical accounting policies described therein. The Company does not undertake to publicly update or revise its forward-looking statements even if experience or future changes make it clear that any projected results expressed or implied therein will not be realized.

Consolidated Statements of Earnings

| (in thousands except per share amounts) Years ended December 31, | | 2014 | | | 2013 | | | 2012 | |

| Revenue | | $ | 1,447,821 | | | $ | 1,462,126 | | | $ | 1,453,555 | |

| Cost of products sold | | | 959,311 | | | | 987,080 | | | | 990,911 | |

| Selling and administrative expenses | | | 357,845 | | | | 301,266 | | | | 269,765 | |

| Operating Income | | | 130,665 | | | | 173,780 | | | | 192,879 | |

| Interest expense | | | 16,067 | | | | 16,147 | | | | 16,901 | |

| Earnings Before Income Taxes | | | 114,598 | | | | 157,633 | | | | 175,978 | |

| Income taxes | | | 32,827 | | | | 43,335 | | | | 50,896 | |

| Earnings from Continuing Operations | | | 81,771 | | | | 114,298 | | | | 125,082 | |

| Loss from discontinued operations, net of tax | | | (8,125 | ) | | | (1,003 | ) | | | (1,174 | ) |

| Net Earnings | | $ | 73,646 | | | $ | 113,295 | | | $ | 123,908 | |

| Earnings per common share: | | | | | | | | | | | | |

| Basic: | | | | | | | | | | | | |

| Continuing operations | | $ | 1.69 | | | $ | 2.30 | | | $ | 2.52 | |

| Discontinued operations | | | (0.17 | ) | | | (0.02 | ) | | | (0.02 | ) |

| Earnings per common share | | $ | 1.52 | | | $ | 2.28 | | | $ | 2.50 | |

| Diluted: | | | | | | | | | | | | |

| Continuing operations | | $ | 1.67 | | | $ | 2.29 | | | $ | 2.51 | |

| Discontinued operations | | | (0.17 | ) | | | (0.02 | ) | | | (0.02 | ) |

| Earnings per common share | | $ | 1.51 | | | $ | 2.27 | | | $ | 2.49 | |

| Weighted average number of common shares outstanding: | | | | | | | | | | | | |

| Basic | | | 48,525 | | | | 49,755 | | | | 49,596 | |

| Diluted | | | 48,819 | | | | 49,934 | | | | 49,822 | |

See notes to consolidated financial statements.

Consolidated Statements of Comprehensive Income

| (in thousands) Years ended December 31, | | 2014 | | | 2013 | | | 2012 | |

| Net earnings | | $ | 73,646 | | | $ | 113,295 | | | $ | 123,908 | |

| Cash flow hedges adjustment, net of tax of $153, $50 and $136, respectively | | | 423 | | | | (134 | ) | | | (350 | ) |

| Pension adjustment, net of tax of $226, $3,675 and $1,040, respectively | | | 1,598 | | | | 5,294 | | | | (2,216 | ) |

| Tax effect on losses previously recorded in other comprehensive income | | | — | | | | — | | | | 16,836 | |

| Foreign currency translation on net investment hedges | | | 12,677 | | | | (4,020 | ) | | | (1,251 | ) |

| Tax effect of current year activity on net investment hedges | | | (4,947 | ) | | | 1,810 | | | | — | |

| Foreign currency translation on long term intercompany loans | | | (8,325 | ) | | | 5,781 | | | | (1,540 | ) |

| Other foreign currency translation | | | (92,556 | ) | | | 1,856 | | | | 22,984 | |

| Total Comprehensive (Loss) Income | | $ | (17,484 | ) | | $ | 123,882 | | | $ | 158,371 | |

See notes to consolidated financial statements.

Consolidated Balance Sheets

| (in thousands except share and per share amounts) December 31, | | 2014 | | | 2013 | |

| Assets | | | | | | |

| Current Assets: | | | | | | |

| Cash and cash equivalents | | $ | 20,329 | | | $ | 19,836 | |

| Trade accounts receivable, less allowance for losses of $3,838 and $4,327, respectively | | | 228,907 | | | | 233,751 | |

| Inventories | | | 449,409 | | | | 474,452 | |

| Prepaid expenses and other current assets | | | 37,713 | | | | 38,079 | |

| Deferred income taxes | | | 21,735 | | | | 23,707 | |

| Assets held for sale | | | 1,296 | | | | — | |

| Total current assets | | | 759,389 | | | | 789,825 | |

| Other assets | | | 77,376 | | | | 47,786 | |

| Intangible assets – at cost, less accumulated amortization of $14,390 and $15,634, respectively | | | 8,760 | | | | 10,546 | |

| Goodwill | | | 424,114 | | | | 457,269 | |

| Property, Plant and Equipment: | | | | | | | | |

| Land | | | 42,868 | | | | 56,343 | |

| Buildings | | | 295,381 | | | | 374,388 | |

| Machinery and equipment | | | 723,631 | | | | 751,267 | |

| Construction in progress | | | 54,579 | | | | 55,236 | |

| | | | 1,116,459 | | | | 1,237,234 | |

| Less accumulated depreciation | | | (620,892 | ) | | | (671,926 | ) |

| | | | 495,567 | | | | 565,308 | |

| Total assets | | $ | 1,765,206 | | | $ | 1,870,734 | |

| Liabilities and Shareholders’ Equity | | | | | | | | |

| Current Liabilities: | | | | | | | | |

| Trade accounts payable | | $ | 99,033 | | | $ | 99,117 | |

| Accrued salaries, wages and withholdings from employees | | | 30,010 | | | | 32,669 | |

| Other accrued expenses | | | 76,383 | | | | 78,579 | |

| Income taxes | | | 3,591 | | | | 5,478 | |

| Short-term borrowings | | | 15,888 | | | | 7,050 | |

| Total current liabilities | | | 224,905 | | | | 222,893 | |

| Deferred income taxes | | | — | | | | 19,956 | |

| Other liabilities | | | 17,372 | | | | 8,539 | |

| Accrued employee and retiree benefits | | | 24,983 | | | | 28,538 | |

| Long-term debt | | | 451,011 | | | | 348,124 | |

| Shareholders’ Equity: | | | | | | | | |

| Common stock, par value $0.10 a share, authorized 100,000,000 shares; issued 53,954,874 shares | | | 5,396 | | | | 5,396 | |

| Additional paid-in capital | | | 110,969 | | | | 105,119 | |

| Earnings reinvested in the business | | | 1,243,627 | | | | 1,217,874 | |

| Treasury stock, 6,529,891 and 4,105,827 shares, respectively, at cost | | | (227,929 | ) | | | (91,707 | ) |

| Accumulated other comprehensive (loss) income | | | (85,128 | ) | | | 6,002 | |

| | | | 1,046,935 | | | | 1,242,684 | |

| Total liabilities and shareholders’ equity | | $ | 1,765,206 | | | $ | 1,870,734 | |

See notes to consolidated financial statements.

Consolidated Statements of Cash Flows

| (in thousands) Years ended December 31, | | 2014 | | | 2013 | | | 2012 | |

| Cash Flows from Operating Activities | | | | | | | | | |

| Net earnings | | $ | 73,646 | | | $ | 113,295 | | | $ | 123,908 | |

| Adjustments to arrive at net cash provided by operating activities: | | | | | | | | | | | | |

| Depreciation and amortization | | | 51,456 | | | | 52,016 | | | | 48,352 | |

| Share-based compensation | | | 6,265 | | | | 8,430 | | | | 10,086 | |

| Loss (gain) on assets | | | 70,745 | | | | 695 | | | | (869 | ) |

| Deferred income taxes | | | (16,780 | ) | | | (6,178 | ) | | | 2,916 | |

| Changes in operating assets and liabilities: | | | | | | | | | | | | |

| Trade accounts receivable | | | (10,582 | ) | | | 3,466 | | | | (15,158 | ) |

| Inventories | | | 64 | | | | (30,217 | ) | | | (23,125 | ) |

| Prepaid expenses and other assets | | | 6,479 | | | | 616 | | | | (9,405 | ) |

| Accounts payable and other accrued expenses | | | 6,745 | | | | 3,606 | | | | 225 | |

| Accrued salaries, wages and withholdings from employees | | | (365 | ) | | | 5,384 | | | | (1,209 | ) |

| Income taxes | | | 7,047 | | | | (100 | ) | | | (1,689 | ) |

| Other liabilities | | | (5,532 | ) | | | 2,540 | | | | 5,334 | |

| Net cash provided by operating activities | | | 189,188 | | | | 153,553 | | | | 139,366 | |

| Cash Flows from Investing Activities | | | | | | | | | | | | |

| Acquisition of property, plant and equipment | | | (79,398 | ) | | | (104,246 | ) | | | (103,806 | ) |

| Proceeds from sale of assets | | | 1,029 | | | | 6,225 | | | | 1,364 | |

| Other investing activities | | | (780 | ) | | | (208 | ) | | | (242 | ) |

| Net cash used in investing activities | | | (79,149 | ) | | | (98,229 | ) | | | (102,684 | ) |

| Cash Flows from Financing Activities | | | | | | | | | | | | |

| Proceeds from additional borrowings | | | 213,985 | | | | 194,973 | | | | 73,903 | |

| Debt payments | | | (128,186 | ) | | | (198,686 | ) | | | (58,052 | ) |

| Purchase of treasury stock | | | (137,192 | ) | | | — | | | | (23,154 | ) |

| Dividends paid | | | (47,893 | ) | | | (45,513 | ) | | | (43,426 | ) |

| Proceeds from options exercised and other equity transactions | | | 733 | | | | 1,007 | | | | 1,957 | |

| Net cash used in financing activities | | | (98,553 | ) | | | (48,219 | ) | | | (48,772 | ) |

| Effect of exchange rate changes on cash and cash equivalents | | | (10,993 | ) | | | (2,331 | ) | | | 4,297 | |

| Net increase (decrease) in cash and cash equivalents | | | 493 | | | | 4,774 | | | | (7,793 | ) |

| Cash and cash equivalents at beginning of year | | | 19,836 | | | | 15,062 | | | | 22,855 | |

| Cash and cash equivalents at end of year | | $ | 20,329 | | | $ | 19,836 | | | $ | 15,062 | |

| Cash paid during the year for: | | | | | | | | | | | | |

| Interest | | $ | 16,158 | | | $ | 16,168 | | | $ | 16,897 | |

| Income taxes | | | 42,335 | | | | 47,436 | | | | 53,492 | |

| Capitalized interest | | | 1,449 | | | | 1,875 | | | | 1,601 | |

See notes to consolidated financial statements.

Consolidated Statements of Shareholders’ Equity

| | | | | | | | | | | | Treasury Stock | | | | |

| (in thousands except share and per share amounts) | | Common Stock | | | Additional Paid-in Capital | | | Earnings Reinvested in the Business | | | Shares | | | Amount | | | Accumulated Other Comprehensive Income (Loss) | |

| Balances at December 31, 2011 | | $ | 5,396 | | | $ | 94,187 | | | $ | 1,069,610 | | | | 4,038,011 | | | $ | (80,935 | ) | | $ | (39,048 | ) |

| Net earnings | | | | | | | | | | | 123,908 | | | | | | | | | | | | | |

| Other comprehensive income | | | | | | | | | | | | | | | | | | | | | | | 34,463 | |

| Cash dividends paid – $0.87 per share | | | | | | | | | | | (43,426 | ) | | | | | | | | | | | | |

| Share-based compensation | | | | | | | 10,086 | | | | | | | | | | | | | | | | | |

| Stock options exercised | | | | | | | 52 | | | | | | | | (66,579 | ) | | | 1,438 | | | | | |

| Non-vested stock issued upon vesting | | | | | | | (6,999 | ) | | | | | | | (313,812 | ) | | | 6,999 | | | | | |

| Benefit plans | | | | | | | 388 | | | | | | | | (22,925 | ) | | | 480 | | | | | |

| Purchase of treasury stock | | | | | | | | | | | | | | | 626,251 | | | | (23,154 | ) | | | | |

| Other | | | | | | | 539 | | | | | | | | 3,875 | | | | (86 | ) | | | | |

| Balances at December 31, 2012 | | | 5,396 | | | | 98,253 | | | | 1,150, 092 | | | | 4,264,821 | | | | (95,258 | ) | | | (4,585 | ) |

| Net earnings | | | | | | | | | | | 113,295 | | | | | | | | | | | | | |

| Other comprehensive income | | | | | | | | | | | | | | | | | | | | | | | 10,587 | |

| Cash dividends paid – $0.91 per share | | | | | | | | | | | (45,513 | ) | | | | | | | | | | | | |

| Share-based compensation | | | | | | | 8,430 | | | | | | | | | | | | | | | | | |

| Stock options exercised | | | | | | | (63 | ) | | | | | | | (47,584 | ) | | | 1,063 | | | | | |

| Non-vested stock issued upon vesting | | | | | | | (2,113 | ) | | | | | | | (94,600 | ) | | | 2,113 | | | | | |

| Benefit plans | | | | | | | 385 | | | | | | | | (26,635 | ) | | | 595 | | | | | |

| Other | | | | | | | 227 | | | | | | | | 9,825 | | | | (220 | ) | | | | |

| Balances at December 31, 2013 | | | 5,396 | | | | 105,119 | | | | 1,217, 874 | | | | 4,105,827 | | | | (91,707 | ) | | | 6,002 | |

| Net earnings | | | | | | | | | | | 73,646 | | | | | | | | | | | | | |

| Other comprehensive income | | | | | | | | | | | | | | | | | | | | | | | (91,130 | ) |

| Cash dividends paid – $0.98 per share | | | | | | | | | | | (47,893 | ) | | | | | | | | | | | | |

| Share-based compensation | | | | | | | 6,265 | | | | | | | | | | | | | | | | | |

| Stock options exercised | | | | | | | (161 | ) | | | | | | | (27,001 | ) | | | 753 | | | | | |

| Non-vested stock issued upon vesting | | | | | | | (1,206 | ) | | | | | | | (40,300 | ) | | | 1,206 | | | | | |

| Benefit plans | | | | | | | 510 | | | | | | | | (18,185 | ) | | | 406 | | | | | |

| Purchase of treasury stock | | | | | | | | | | | | | | | 2,500,000 | | | | (138,288 | ) | | | | |

| Other | | | | | | | 442 | | | | | | | | 9,550 | | | | (299 | ) | | | | |

| Balances at December 31, 2014 | | $ | 5,396 | | | $ | 110,969 | | | $ | 1,243,627 | | | | 6,529,891 | | | $ | (227,929 | ) | | $ | (85,128 | ) |

See notes to consolidated financial statements.

Notes to Consolidated Financial Statements

Years ended December 31, 2014, 2013 and 2012

1.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of Operations Sensient Technologies Corporation, together with its subsidiaries (the “Company”), is a leading global manufacturer and marketer of colors, flavors and fragrances. The Company uses advanced technologies at facilities around the world to develop specialty food and beverage systems, cosmetic and pharmaceutical systems, specialty inks and colors, and other specialty and fine chemicals. The Company’s reportable segments consist of the Flavors & Fragrances and Color Groups, which are managed on a products and services basis. The Asia Pacific Group and certain of the Company’s flavor businesses in Central and South America (Flavors Central & South America), which are managed on a geographic basis, are included in Corporate & Other.

Principles of Consolidation and Basis of Presentation The consolidated financial statements include the accounts of the Company and have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). All significant intercompany accounts and transactions have been eliminated in consolidation.

The results of operations for one of the Company’s business units within the Color Group have been reported as a discontinued operation for all periods presented. The corresponding assets have been reclassified in accordance with the authoritative literature on assets held for sale as of December 31, 2014. See Note 12, Discontinued Operations, for further information regarding discontinued operations.

Use of Estimates The preparation of the consolidated financial statements requires the use of management’s estimates and assumptions that affect reported amounts of assets, liabilities, revenue and expenses during the reporting period and the disclosure of contingent assets and liabilities at the date of the financial statements. Actual results could differ from those estimates.

Revenue Recognition The Company recognizes revenue (net of estimated discounts, allowances and returns) when title to goods passes, the customer is obligated to pay the Company and the Company has no remaining obligations. Such recognition typically corresponds with the shipment of goods.

Cost of Products Sold Cost of products sold includes materials, labor and overhead expenses incurred in the manufacture of our products. Cost of products sold also includes charges for obsolete and slow moving inventories, as well as costs for quality control, purchasing and receiving costs, inspection costs, warehousing costs, internal transfer costs, other costs of our internal distribution network and costs incurred for shipping and handling. The Company records fees billed to customers for shipping and handling as revenue.

Selling and Administrative Expenses Selling and administrative expenses primarily include the salaries and related costs for executive, finance, accounting, human resources, information technology, research and development and legal personnel as well as salaries and related costs of salespersons and commissions paid to external sales agents.

Cash Equivalents The Company considers all highly liquid investments with maturities of three months or less at the date of acquisition as cash equivalents.

Accounts Receivable Receivables are recorded at their face amount, less an allowance for doubtful accounts. The allowance for doubtful accounts is based on customer-specific analysis and general matters such as current assessments of past due balances and economic conditions. Specific accounts are written off against the allowance for doubtful accounts when it is deemed that the receivable is no longer collectible.

Inventories Inventories are stated at the lower of cost or market. Market is determined on the basis of estimated realizable values. Cost is determined using the first-in, first-out (“FIFO”) method with the exception of certain locations of the Flavors & Fragrances Group where cost is determined using a weighted average method. Inventories include finished and in-process products totaling $308.7 million and $317.1 million at December 31, 2014 and 2013, respectively, and raw materials and supplies of $140.7 million and $157.4 million at December 31, 2014 and 2013, respectively.

Property, Plant and Equipment Property, plant and equipment are recorded at cost reduced by accumulated depreciation. Depreciation is provided over the estimated useful life of the related asset using the straight-line method for financial reporting. The estimated useful lives for buildings and leasehold improvements range from 5 to 40 years. Machinery and equipment have estimated useful lives ranging from 3 to 20 years. Interest costs on significant projects constructed or developed for the Company’s own use are capitalized as part of the asset.

Goodwill and Other Intangible Assets The carrying value of goodwill is evaluated for impairment on an annual basis or more frequently when an indicator of impairment occurs. The impairment assessment includes comparing the carrying amount of net assets, including goodwill, of each reporting unit to its respective fair value as of the date of the assessment. Fair value was estimated based upon an evaluation of the reporting unit’s estimated future discounted cash flow as well as the public trading and private transaction valuation multiples for comparable companies. Such determination of fair value yielded no impairment in 2014, 2013 or 2012.

The cost of intangible assets with determinable useful lives is amortized on a straight-line basis to reflect the pattern of economic benefits consumed, ranging from 5 to 20 years. These assets include technological know-how, customer relationships, patents, trademarks and non-compete agreements, among others.

Impairment of Long-lived Assets The Company reviews long-lived assets for impairment whenever events or changes in business circumstances indicate that the carrying amount of the assets may not be fully recoverable. The Company performs undiscounted cash flow analyses to determine if potential impairment exists. If impairment is determined to exist, any related impairment loss is calculated based on the difference between fair value and carrying value. Impairment losses were recorded as a result of the Company’s 2014 Restructuring Plan and 2013 restructuring plan. See Note 11, Restructuring Charges, for additional information.

Financial Instruments The Company may use derivative financial instruments for the purpose of hedging currency and interest rate exposures which exist as part of ongoing business operations. As a policy, the Company does not engage in speculative or leveraged transactions, nor does the Company hold or issue financial instruments for trading purposes.

Hedge effectiveness is determined by how closely the changes in the fair value of the hedging instrument offset the changes in the fair value or cash flows of the hedged item. Hedge accounting is permitted only if the hedging relationship is expected to be highly effective at the inception of the transaction and on an ongoing basis. Any ineffective portions are recognized in earnings immediately.

Interest Rate Hedging The Company is exposed to interest rate risk through its corporate borrowing activities. The objective of the Company’s interest rate risk management activities is to manage the levels of the Company’s fixed and floating interest rate exposure to be consistent with the Company’s preferred mix. The interest rate risk management program may include entering into interest rate swaps, which qualify as fair value hedges, when there is a desire to modify the Company’s exposure to interest rates. Gains or losses on fair value hedges are recognized in earnings, net of gains and losses on the fair value of the hedged instruments.