Resource Center: 1-800-232-6643 Exhibit 99.1

Contact: Pete Bakel

202-752-2034

Date: May 5, 2016

Fannie Mae Reports Net Income of $1.1 Billion and Comprehensive Income of $936 Million for First Quarter 2016

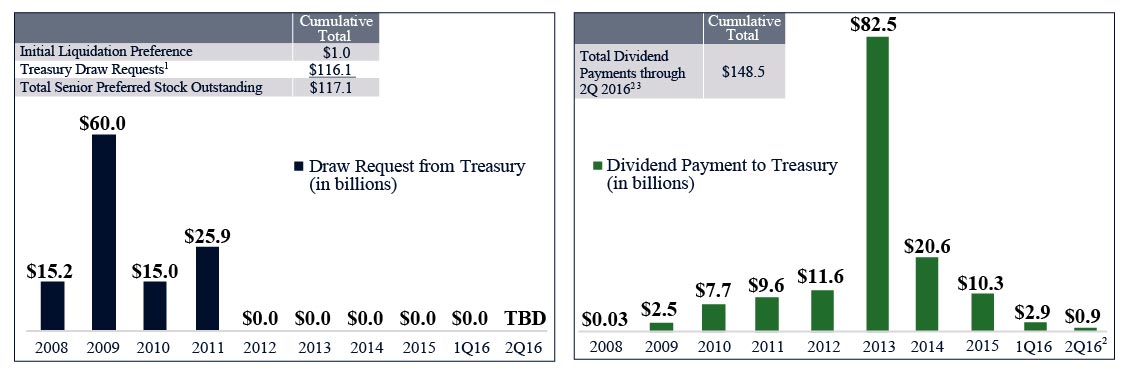

| • | Fannie Mae expects to pay $919 million in dividends to Treasury in June 2016. With the expected June dividend payment, the company will have paid a total of $148.5 billion in dividends to Treasury. Dividend payments do not reduce prior Treasury draws, which total $116.1 billion since 2008. |

| • | Fannie Mae provided approximately $115 billion in liquidity to the mortgage market in the first quarter of 2016, enabling families to buy, refinance, or rent homes. |

| • | Fannie Mae helped distressed families retain their homes or avoid foreclosure through approximately 27,000 workout solutions in the first quarter of 2016. |

| • | Fannie Mae continued to increase the role of private capital in the mortgage market and reduce taxpayer risk through its Connecticut Avenue SecuritiesTM (CAS), Credit Insurance Risk TransferTM (CIRTTM), and other types of risk-sharing transactions. Through the first quarter of 2016, Fannie Mae had transferred a significant portion of the mortgage credit risk on over $590 billion in unpaid principal balance of mortgage loans pursuant to these transactions. |

WASHINGTON, DC — Fannie Mae (FNMA/OTC) reported net income of $1.1 billion and comprehensive income of $936 million for the first quarter of 2016. The company reported a positive net worth of $2.1 billion as of March 31, 2016, which the company expects will result in its paying Treasury a $919 million dividend in June 2016.

“We continue to run our business well while supporting the improving housing market,” said Timothy J. Mayopoulos, president and chief executive officer. “The changes we have made to the company have put us in a stronger position to fulfill our responsibility to deliver safe, affordable mortgage financing for our customers, in all markets at all times. We will continue to execute on behalf of our partners, drive further improvements to housing finance and our company, and serve those who house America.”

First Quarter 2016 Results — Fannie Mae’s net income of $1.1 billion and comprehensive income of $936 million for the first quarter of 2016 compares to net income of $2.5 billion and comprehensive income of $2.3 billion for the fourth quarter of 2015. The decrease in net income was due primarily to:

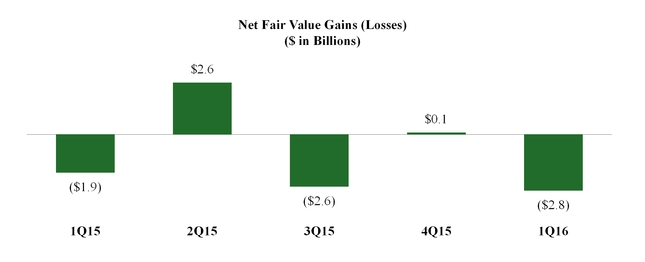

| • | Fair value losses in the first quarter of 2016 driven by decreases in longer-term interest rates negatively impacting the value of the company’s risk management derivatives, partially offset by credit-related income for the quarter. |

| First Quarter 2016 Results | 1 | |

SUMMARY OF FIRST QUARTER 2016 RESULTS

| (Dollars in millions) | 1Q16 | 4Q15 | Variance | 1Q16 | 1Q15 | Variance | ||||||||||||||||||

| Net interest income | $ | 4,769 | $ | 5,077 | $ | (308 | ) | $ | 4,769 | $ | 5,067 | $ | (298 | ) | ||||||||||

| Fee and other income | 203 | 225 | (22 | ) | 203 | 308 | (105 | ) | ||||||||||||||||

| Net revenues | 4,972 | 5,302 | (330 | ) | 4,972 | 5,375 | (403 | ) | ||||||||||||||||

| Investment gains, net | 69 | 181 | (112 | ) | 69 | 342 | (273 | ) | ||||||||||||||||

| Fair value gains (losses), net | (2,813 | ) | 135 | (2,948 | ) | (2,813 | ) | (1,919 | ) | (894 | ) | |||||||||||||

| Administrative expenses | (688 | ) | (686 | ) | (2 | ) | (688 | ) | (723 | ) | 35 | |||||||||||||

| Credit-related income (expense) | ||||||||||||||||||||||||

| Benefit (provision) for credit losses | 1,184 | (255 | ) | 1,439 | 1,184 | 533 | 651 | |||||||||||||||||

| Foreclosed property expense | (334 | ) | (477 | ) | 143 | (334 | ) | (473 | ) | 139 | ||||||||||||||

| Total credit-related income (expense) | 850 | (732 | ) | 1,582 | 850 | 60 | 790 | |||||||||||||||||

| Temporary Payroll Tax Cut Continuation Act of 2011 (“TCCA”) fees | (440 | ) | (429 | ) | (11 | ) | (440 | ) | (382 | ) | (58 | ) | ||||||||||||

| Other income (expenses), net | (264 | ) | (201 | ) | (63 | ) | (264 | ) | 5 | (269 | ) | |||||||||||||

| Income before federal income taxes | 1,686 | 3,570 | (1,884 | ) | 1,686 | 2,758 | (1,072 | ) | ||||||||||||||||

| Provision for federal income taxes | (550 | ) | (1,103 | ) | 553 | (550 | ) | (870 | ) | 320 | ||||||||||||||

| Net income | 1,136 | 2,467 | (1,331 | ) | 1,136 | 1,888 | (752 | ) | ||||||||||||||||

| Less: Net income attributable to noncontrolling interest | — | (1 | ) | 1 | — | — | — | |||||||||||||||||

| Net income attributable to Fannie Mae | $ | 1,136 | $ | 2,466 | $ | (1,330 | ) | $ | 1,136 | $ | 1,888 | $ | (752 | ) | ||||||||||

| Total comprehensive income attributable to Fannie Mae | $ | 936 | $ | 2,260 | $ | (1,324 | ) | $ | 936 | $ | 1,796 | $ | (860 | ) | ||||||||||

| Dividends distributed or available for distribution to senior preferred stockholder | $ | (919 | ) | $ | (2,859 | ) | $ | 1,940 | $ | (919 | ) | $ | (1,796 | ) | $ | 877 | ||||||||

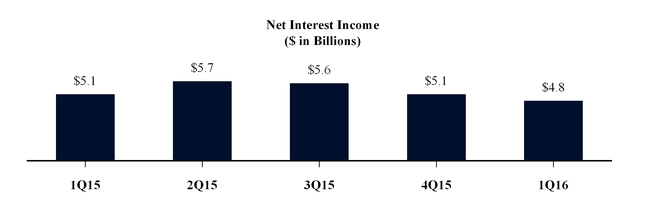

Net revenues, which consist of net interest income and fee and other income, were $5.0 billion for the first quarter of 2016, compared with $5.3 billion for the fourth quarter of 2015.

Net interest income, which includes guaranty fee revenue, was $4.8 billion for the first quarter of 2016 compared with $5.1 billion for the fourth quarter of 2015. Net interest income for the first quarter of 2016 was driven by guaranty fee revenue and interest income earned on mortgage assets in the company’s retained mortgage portfolio.

In recent years, an increasing portion of Fannie Mae’s net interest income has been derived from guaranty fees rather than from the company’s retained mortgage portfolio assets. This is a result of both the impact of guaranty fee increases implemented in 2012 and the reduction of the company’s retained mortgage portfolio. Approximately two-thirds of the company’s net interest income in the first quarter of 2016 was derived from its guaranty business. The company expects that guaranty fees will continue to account for an increasing portion of its net interest income.

| First Quarter 2016 Results | 2 | |

Net fair value losses were $2.8 billion in the first quarter of 2016, compared with gains of $135 million in the fourth quarter of 2015. Fair value losses for the first quarter of 2016 were due primarily to decreases in longer-term interest rates negatively impacting the value of the company’s risk management derivatives. The estimated fair value of the company’s financial instruments may fluctuate substantially from period to period because of changes in interest rates, the yield curve, mortgage and credit spreads, implied volatility, and activity related to these financial instruments.

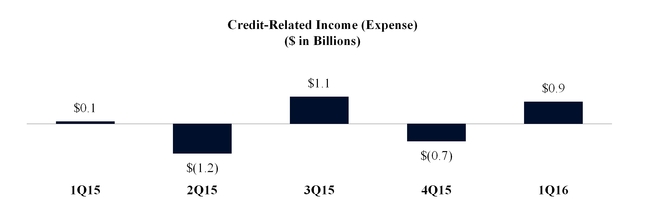

Credit-related income, which consists of a benefit for credit losses and foreclosed property expense, was $850 million in the first quarter of 2016, compared with credit-related expense of $732 million in the fourth quarter of 2015. Credit-related income in the first quarter of 2016 was due to a benefit for credit losses for the quarter attributable primarily to a decline in actual and projected mortgage interest rates. In addition, an increase in home prices, including higher distressed property valuations, also contributed to the benefit for credit losses.

| First Quarter 2016 Results | 3 | |

VARIABILITY OF FINANCIAL RESULTS

Fannie Mae expects to remain profitable on an annual basis for the foreseeable future; however, certain factors, such as changes in interest rates or home prices, could result in significant volatility in our financial results from quarter to quarter or year to year. Fannie Mae’s future financial results also will be affected by a number of other factors, including: the company’s guaranty fee rates; the volume of single-family mortgage originations in the future; the size, composition, and quality of its retained mortgage portfolio and guaranty book of business; and economic and housing market conditions. Although Fannie Mae expects to remain profitable on an annual basis for the foreseeable future, due to the company’s expectation of continued declining capital and the potential for significant volatility in its financial results, the company could experience a net worth deficit in a future quarter, particularly as the company’s capital reserve amount approaches or reaches zero. The company’s expectations for its future financial results do not take into account the impact on its business of potential future legislative or regulatory changes, which could have a material impact on the company’s financial results, particularly the enactment of housing finance reform legislation. For additional information on factors that affect the company’s financial results, please refer to “Executive Summary” in the company’s quarterly report on Form 10-Q for the quarter ended March 31, 2016 (the “First Quarter 2016 Form 10-Q”).

SUMMARY OF FIRST QUARTER 2016 BUSINESS SEGMENT RESULTS

The business groups running Fannie Mae’s three reporting segments consist of its Single-Family business, its Multifamily business, and its Capital Markets group. These business groups engage in complementary business activities in pursuing Fannie Mae’s vision to be America’s most valued housing partner and to provide liquidity, access to credit and affordability in all U.S. housing markets at all times, while effectively managing and reducing risk to Fannie Mae’s business, taxpayers, and the housing finance system. In support of this vision, Fannie Mae is focused on: advancing a sustainable and reliable business model that reduces risk to the housing finance system and taxpayers; providing reliable, large-scale access to affordable mortgage credit for qualified borrowers and helping struggling homeowners; and serving customer needs and improving the company’s business efficiency.

| First Quarter 2016 Results | 4 | |

| (Dollars in millions) | 1Q16 | 4Q15 | Variance | 1Q16 | 1Q15 | Variance | ||||||||||||||||||

| Single-Family Segment: | ||||||||||||||||||||||||

| Guaranty fee income | $ | 3,222 | $ | 3,199 | $ | 23 | $ | 3,222 | $ | 3,040 | $ | 182 | ||||||||||||

| Credit-related income (expense) | 828 | (819 | ) | 1,647 | 828 | (7 | ) | 835 | ||||||||||||||||

| TCCA fees | (440 | ) | (429 | ) | (11 | ) | (440 | ) | (382 | ) | (58 | ) | ||||||||||||

| Other | (587 | ) | (564 | ) | (23 | ) | (587 | ) | (539 | ) | (48 | ) | ||||||||||||

| Income before federal income taxes | 3,023 | 1,387 | 1,636 | 3,023 | 2,112 | 911 | ||||||||||||||||||

| Provision for federal income taxes | (643 | ) | (451 | ) | (192 | ) | (643 | ) | (581 | ) | (62 | ) | ||||||||||||

| Net income | $ | 2,380 | $ | 936 | $ | 1,444 | $ | 2,380 | $ | 1,531 | $ | 849 | ||||||||||||

| Multifamily Segment: | ||||||||||||||||||||||||

| Guaranty fee income | $ | 385 | $ | 375 | $ | 10 | $ | 385 | $ | 340 | $ | 45 | ||||||||||||

| Credit-related income | 22 | 87 | (65 | ) | 22 | 67 | (45 | ) | ||||||||||||||||

| Other | (36 | ) | (9 | ) | (27 | ) | (36 | ) | 146 | (182 | ) | |||||||||||||

| Income before federal income taxes | 371 | 453 | (82 | ) | 371 | 553 | (182 | ) | ||||||||||||||||

| Provision for federal income taxes | (38 | ) | (119 | ) | 81 | (38 | ) | (70 | ) | 32 | ||||||||||||||

| Net income | $ | 333 | $ | 334 | $ | (1 | ) | $ | 333 | $ | 483 | $ | (150 | ) | ||||||||||

| Capital Markets Segment: | ||||||||||||||||||||||||

| Net interest income | $ | 1,092 | $ | 1,312 | $ | (220 | ) | $ | 1,092 | $ | 1,602 | $ | (510 | ) | ||||||||||

| Investment gains, net | 1,415 | 860 | 555 | 1,415 | 1,509 | (94 | ) | |||||||||||||||||

| Fair value gains (losses), net | (2,803 | ) | 63 | (2,866 | ) | (2,803 | ) | (1,970 | ) | (833 | ) | |||||||||||||

| Other | (299 | ) | (444 | ) | 145 | (299 | ) | (323 | ) | 24 | ||||||||||||||

| Income (loss) before federal income taxes | (595 | ) | 1,791 | (2,386 | ) | (595 | ) | 818 | (1,413 | ) | ||||||||||||||

| Benefit (provision) for federal income taxes | 131 | (533 | ) | 664 | 131 | (219 | ) | 350 | ||||||||||||||||

| Net income (loss) | $ | (464 | ) | $ | 1,258 | $ | (1,722 | ) | $ | (464 | ) | $ | 599 | $ | (1,063 | ) | ||||||||

Single-Family Business

| • | Single-Family net income was $2.4 billion in the first quarter of 2016, compared with $936 million in the fourth quarter of 2015. Net income in the first quarter of 2016 was driven primarily by guaranty fee income and credit-related income. |

| • | Single-Family guaranty fee income was $3.2 billion for both the first quarter of 2016 and the fourth quarter of 2015. Guaranty fee income in the first quarter of 2016 was driven primarily by loans with higher guaranty fees becoming a larger part of the company’s Single-Family guaranty book of business due primarily to the cumulative impact of guaranty fee price increases implemented in 2012. |

| • | Single-Family credit-related income was $828 million in the first quarter of 2016, compared with credit-related expense of $819 million in the fourth quarter of 2015. Credit-related income in the first quarter of 2016 was due to a benefit for credit losses for the quarter attributable primarily to a decline in actual and projected mortgage interest rates. In addition, an increase in home prices, including higher distressed property valuations, also contributed to the benefit for credit losses. |

| • | The Single-Family guaranty book of business was $2.82 trillion as of March 31, 2016, compared with $2.83 trillion as of December 31, 2015. |

| First Quarter 2016 Results | 5 | |

Multifamily Business

| • | Multifamily net income was $333 million in the first quarter of 2016, compared with $334 million in the fourth quarter of 2015. Net income in the first quarter of 2016 was driven primarily by guaranty fee income. |

| • | Multifamily guaranty fee income was $385 million for the first quarter of 2016, compared with $375 million for the fourth quarter of 2015. The increase in guaranty fee income in the first quarter of 2016 was driven primarily by loans with higher guaranty fees becoming a larger part of the company’s Multifamily guaranty book of business, while loans with lower guaranty fees continue to liquidate. |

| • | The Multifamily guaranty book of business was $220.7 billion as of March 31, 2016, compared with $213.4 billion as of December 31, 2015. |

Capital Markets

| • | Capital Markets had a net loss of $464 million in the first quarter of 2016, compared with net income of $1.3 billion in the fourth quarter of 2015. Capital Markets’ net loss in the first quarter of 2016 was driven primarily by net fair value losses, partially offset by net investment gains and net interest income. |

| • | Capital Markets net fair value losses were $2.8 billion in the first quarter of 2016, compared with net fair value gains of $63 million in the fourth quarter of 2015. Net fair value losses for the first quarter of 2016 were due primarily to fair value losses on risk management derivatives driven by decreases in longer-term interest rates during the quarter. |

| • | Capital Markets net investment gains were $1.4 billion in the first quarter of 2016, compared with $860 million in the fourth quarter of 2015. Net investment gains for the first quarter of 2016 were due primarily to gains on sales of Fannie Mae MBS designated as available-for-sale securities in the first quarter of 2016. |

| • | Capital Markets net interest income was $1.1 billion for the first quarter of 2016, compared with $1.3 billion for the fourth quarter of 2015. Net interest income was driven primarily by interest income earned on mortgage assets in the company’s retained mortgage portfolio. |

| • | Capital Markets retained mortgage portfolio balance decreased to $332.6 billion as of March 31, 2016, compared with $345.1 billion as of December 31, 2015, resulting from purchases of $58.9 billion and sales and liquidations of $71.3 billion during the first quarter of 2016. |

BUILDING A SUSTAINABLE HOUSING FINANCE SYSTEM

In addition to continuing to provide liquidity and support to the mortgage market, Fannie Mae has invested significant resources toward helping to maintain a safer and sustainable housing finance system for today and build a safer and sustainable housing finance system for the future. The company is pursuing the strategic goals identified by its conservator, the Federal Housing Finance Agency (“FHFA”). These strategic goals are: maintain, in a safe and sound manner, credit availability and foreclosure prevention activities for new and refinanced mortgages to foster liquid, efficient, competitive, and resilient national housing finance markets; reduce taxpayer risk through increasing the role of private capital in the mortgage market; and build a new single-family infrastructure for use by Fannie Mae and Freddie Mac and adaptable for use by other participants in the secondary market in the future.

| First Quarter 2016 Results | 6 | |

ABOUT FANNIE MAE’S CONSERVATORSHIP

Fannie Mae has operated under the conservatorship of FHFA since September 6, 2008. Fannie Mae has not received funds from Treasury since the first quarter of 2012. The funding the company has received under its senior preferred stock purchase agreement with Treasury has provided the company with the capital and liquidity needed to fulfill its mission of providing liquidity and support to the nation’s housing finance markets and to avoid a trigger of mandatory receivership under the Federal Housing Finance Regulatory Reform Act of 2008. For periods through March 31, 2016, Fannie Mae has requested cumulative draws totaling $116.1 billion and paid $147.6 billion in dividends to Treasury. Under the senior preferred stock purchase agreement, the payment of dividends does not offset prior draws. As a result, Treasury maintains a liquidation preference of $117.1 billion on the company’s senior preferred stock.

Treasury Draws and Dividend Payments

(1) | Treasury draw requests are shown in the period for which requested and do not include the initial $1.0 billion liquidation preference of Fannie Mae’s senior preferred stock, for which Fannie Mae did not receive any cash proceeds. The payment of dividends does not offset prior Treasury draws. |

(2) | Fannie Mae expects to pay a dividend for the second quarter of 2016 calculated based on the company’s net worth of $2.1 billion as of March 31, 2016 less a capital reserve amount of $1.2 billion. |

(3) | Amounts may not sum due to rounding. |

In August 2012, the terms governing the company’s dividend obligations on the senior preferred stock were amended. The amended senior preferred stock purchase agreement does not allow the company to build a capital reserve. Beginning in 2013, the required senior preferred stock dividends each quarter equal the amount, if any, by which the company’s net worth as of the end of the immediately preceding fiscal quarter exceeds an applicable capital reserve amount. The capital reserve amount is $1.2 billion for each quarter of 2016 and will be reduced by $600 million each year until it reaches zero in 2018.

The amount of remaining funding available to Fannie Mae under the senior preferred stock purchase agreement with Treasury is currently $117.6 billion. If the company were to draw additional funds from Treasury under the agreement in a future period, the amount of remaining funding under the agreement would be reduced by the amount of the company’s draw. Dividend payments Fannie Mae makes to Treasury do not restore or increase the amount of funding available to the company under the agreement.

Fannie Mae is not permitted to redeem the senior preferred stock prior to the termination of Treasury’s funding commitment under the senior preferred stock purchase agreement. The limited circumstances under which Treasury’s funding commitment will terminate are described in “Business—Conservatorship and Treasury Agreements” in the company’s 2015 Form 10-K.

| First Quarter 2016 Results | 7 | |

CREDIT RISK TRANSFER TRANSACTIONS

In late 2013, Fannie Mae began entering into credit risk transfer transactions with the goal of transferring, to the extent economically sensible, a portion of the mortgage credit risk on some of the recently acquired loans in its single-family book of business in order to reduce the economic risk to the company and to taxpayers of future borrower defaults. Fannie Mae’s primary method of achieving this goal has been through the issuance of its Connecticut Avenue SecuritiesTM (CAS) and its Credit Insurance Risk TransferTM (CIRTTM) transactions.

These transactions transfer a portion of the mortgage credit risk associated with losses on specified reference pools of single-family mortgage loans to investors in CAS or to panels of reinsurers or insurers in CIRT transactions. Approximately 18 percent of the loans in the company’s single-family conventional guaranty book of business as of March 31, 2016, measured by unpaid principal balance, were included in a reference pool for a CAS or CIRT transaction. The company also has executed other types of risk-sharing transactions in addition to its CAS and CIRT transactions. In the aggregate, Fannie Mae’s credit risk transfer transactions completed through March 31, 2016 transferred a significant portion of the mortgage credit risk on single-family mortgages with an unpaid principal balance of over $590 billion. The mezzanine risk positions we sell in a CAS transaction and the insurance layer we obtain in a CIRT transaction typically exceed our estimated stress losses for the associated reference pool of loans.

The loans Fannie Mae has included in its single-family credit risk transfer transactions have been limited to specified categories of loans it has acquired in recent years. Loan categories the company has targeted for credit risk transfer transactions generally consist of fixed-rate 30-year single-family conventional loans that meet certain credit performance characteristics, are non-Refi Plus and have LTV ratios between 60 percent and 97 percent. These targeted loan categories constituted about half of the company’s loan acquisitions for the twelve months ended November 2014, and over 95 percent of the loans in these categories that the company acquired in the twelve months ended November 2014 were included in a subsequent credit risk transfer transaction. Loans are included in reference pools for credit risk transfer transactions on a lagged basis; typically, about one year after the company initially acquired the loans. The portion of Fannie Mae’s single-family loan acquisitions it includes in credit risk transfer transactions can vary from period to period based on market conditions and other factors.

These transactions increase the role of private capital in the mortgage market and reduce the risk to Fannie Mae’s business, taxpayers, and the housing finance system. The company intends to continue to engage in credit risk transfer transactions on an ongoing basis, subject to market conditions. Over time, the company expects that a larger portion of its single-family conventional guaranty book of business will be covered by credit risk transfer transactions.

CREDIT QUALITY

While continuing to make it possible for families to buy, refinance, or rent homes, Fannie Mae has maintained responsible credit standards. Since 2009, Fannie Mae has seen the effect of the actions it took, beginning in 2008, to significantly strengthen its underwriting and eligibility standards to promote sustainable homeownership and stability in the housing market. Fannie Mae actively monitors the credit risk profile and credit performance of the company’s single-family loan acquisitions, in conjunction with housing market and economic conditions, to determine if its pricing, eligibility, and underwriting criteria accurately reflects the risk associated with loans the company acquires or guarantees. Single-family conventional loans acquired by Fannie Mae in the first quarter of 2016 had a weighted average borrower FICO credit score at origination of 746 and a weighted average original loan-to-value ratio of 75 percent.

| First Quarter 2016 Results | 8 | |

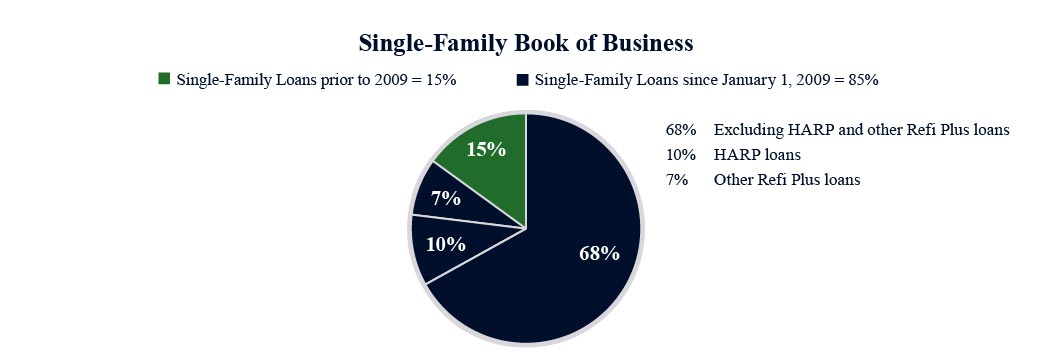

Fannie Mae’s single-family conventional guaranty book of business as of March 31, 2016 consisted of single-family loans acquired prior to 2009; non-Refi PlusTM loans acquired beginning in 2009; loans acquired through the Administration’s Home Affordable Refinance Program® (“HARP®”); and other loans acquired pursuant to the company’s Refi Plus initiative, excluding HARP loans. The company’s Refi Plus initiative, which started in April 2009 and includes HARP, provides expanded refinance opportunities for eligible Fannie Mae borrowers, and may involve the refinance of existing Fannie Mae loans with high loan-to-value ratios, including loans with loan-to-value ratios in excess of 100 percent.

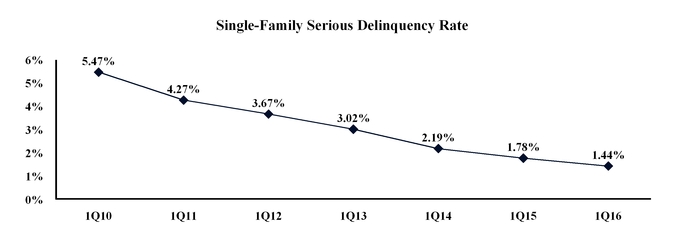

The single-family serious delinquency rate for Fannie Mae’s book of business has decreased for 24 consecutive quarters since the first quarter of 2010 and was 1.44 percent as of March 31, 2016, compared with 5.47 percent as of March 31, 2010. This decrease is primarily the result of home retention solutions, foreclosure alternatives and completed foreclosures, improved loan payment performance, and the company’s acquisition of loans with stronger credit profiles since the beginning of 2009. The company’s single-family serious delinquency rate and the period of time that loans remain seriously delinquent continue to be negatively impacted by the length of time required to complete a foreclosure in some states. Longer foreclosure timelines result in these loans remaining in the company’s book of business for a longer time, which has caused the company’s serious delinquency rate to decrease more slowly in the last few years than it would have if the pace of foreclosures had been faster. The slow pace of foreclosures in certain areas of the country has negatively affected the company’s single-family serious delinquency rates, foreclosure timelines, and financial results, and may continue to do so. Other factors such as the pace of loan modifications, the timing and volume of future nonperforming loan sales the company makes, servicer performance, changes in home prices, unemployment levels, and other macroeconomic conditions also influence serious delinquency rates.

| First Quarter 2016 Results | 9 | |

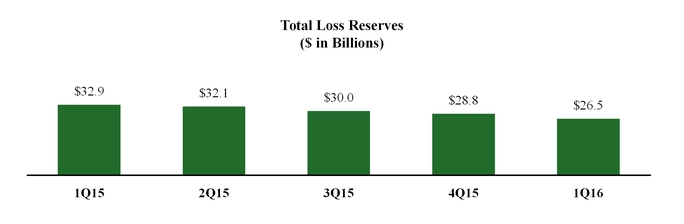

Total loss reserves, which reflect the company’s estimate of the probable losses the company has incurred in its guaranty book of business, including concessions it granted borrowers upon modification of their loans, decreased to $26.5 billion as of March 31, 2016 from $28.8 billion as of December 31, 2015. The decrease in the company’s total loss reserves for the first quarter of 2016 was primarily driven by decreasing mortgage interest rates and mortgage loan liquidations. The company’s loss reserves have declined substantially from their peak and are expected to decline further.

PROVIDING LIQUIDITY AND SUPPORT TO THE MARKET

Liquidity

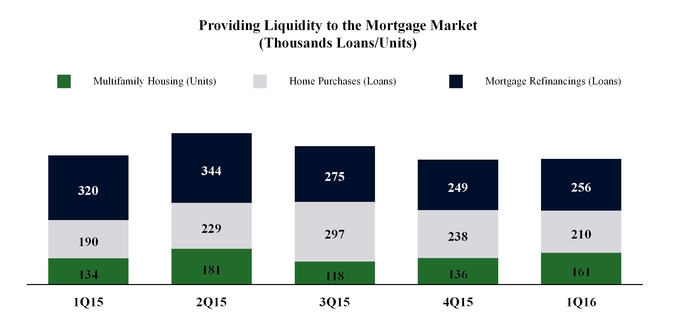

Fannie Mae provided approximately $115 billion in liquidity to the mortgage market in the first quarter of 2016, through its purchases of loans and guarantees of loans and securities, which resulted in approximately:

| • | 210,000 home purchases |

| • | 256,000 mortgage refinancings |

| • | 161,000 units of multifamily housing |

| First Quarter 2016 Results | 10 | |

The company was one of the largest issuers of single-family mortgage-related securities in the secondary market in the first quarter of 2016, with an estimated market share of new single-family mortgage-related securities issuances of 37 percent, compared with 36 percent in the fourth quarter of 2015 and 40 percent in the first quarter of 2015.

Fannie Mae also remained a continuous source of liquidity in the multifamily market in the first quarter of 2016. As of December 31, 2015 (the latest date for which information is available), the company owned or guaranteed approximately 18 percent of the outstanding debt on multifamily properties.

Refinancing Initiatives

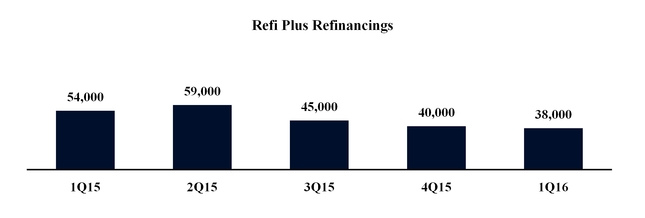

Through the company’s Refi Plus initiative, which offers refinancing flexibility to eligible Fannie Mae borrowers and includes HARP, the company acquired approximately 38,000 loans in the first quarter of 2016. Refinancings delivered to Fannie Mae through Refi Plus in the first quarter of 2016 reduced borrowers’ monthly mortgage payments by an average of $192. The company expects the volume of refinancings under HARP to continue to decline, due to a decrease in the population of borrowers with loans that have high LTV ratios who are willing to refinance and would benefit from refinancing.

| First Quarter 2016 Results | 11 | |

Home Retention Solutions and Foreclosure Alternatives

To reduce the credit losses Fannie Mae ultimately incurs on its book of business, the company has been focusing its efforts on several strategies, including reducing defaults by offering home retention solutions, such as loan modifications.

| For the Three Months Ended March 31, | |||||||||||||

| 2016 | 2015 | ||||||||||||

| Unpaid Principal Balance | Number of Loans | Unpaid Principal Balance | Number of Loans | ||||||||||

| (Dollars in millions) | |||||||||||||

| Home retention solutions: | |||||||||||||

| Modifications | $ | 3,451 | 20,899 | $ | 4,415 | 26,700 | |||||||

| Repayment plans and forbearances completed | 175 | 1,296 | 257 | 1,868 | |||||||||

| Total home retention solutions | 3,626 | 22,195 | 4,672 | 28,568 | |||||||||

| Foreclosure alternatives: | |||||||||||||

| Short sales | 611 | 2,995 | 758 | 3,689 | |||||||||

| Deeds-in-lieu of foreclosure | 265 | 1,745 | 304 | 1,968 | |||||||||

| Total foreclosure alternatives | 876 | 4,740 | 1,062 | 5,657 | |||||||||

| Total loan workouts | $ | 4,502 | 26,935 | $ | 5,734 | 34,225 | |||||||

| Loan workouts as a percentage of single-family guaranty book of business | 0.64 | % | 0.62 | % | 0.81 | % | 0.79 | % | |||||

Fannie Mae views foreclosure as a last resort. For homeowners and communities in need, the company offers alternatives to foreclosure. In dealing with homeowners in distress, the company first seeks home retention solutions, which enable borrowers to stay in their homes, before turning to foreclosure alternatives.

| • | Fannie Mae provided approximately 27,000 loan workouts during the first quarter of 2016 enabling borrowers to avoid foreclosure. |

| • | Fannie Mae completed approximately 21,000 loan modifications during the first quarter of 2016. |

| First Quarter 2016 Results | 12 | |

FORECLOSURES AND REO

When there is no viable home retention solution or foreclosure alternative that can be applied, the company seeks to move to foreclosure expeditiously in an effort to minimize prolonged delinquencies that can hurt local home values and destabilize communities.

| For the Three Months Ended March 31, | |||||||

| 2016 | 2015 | ||||||

| Single-family foreclosed properties (number of properties): | |||||||

| Beginning of period inventory of single-family foreclosed properties (REO) | 57,253 | 87,063 | |||||

| Total properties acquired through foreclosure | 16,367 | 24,316 | |||||

| Dispositions of REO | (21,331 | ) | (32,060 | ) | |||

| End of period inventory of single-family foreclosed properties (REO) | 52,289 | 79,319 | |||||

| Carrying value of single-family foreclosed properties (dollars in millions) | $ | 5,963 | $ | 8,915 | |||

| Single-family foreclosure rate | 0.38 | % | 0.56 | % | |||

| • | Fannie Mae acquired 16,367 single-family REO properties, primarily through foreclosure, in the first quarter of 2016, compared with 16,750 in the fourth quarter of 2015. |

| • | As of March 31, 2016, the company’s inventory of single-family REO properties was 52,289, compared with 57,253 as of December 31, 2015. The carrying value of the company’s single-family REO was $6.0 billion as of March 31, 2016. |

| • | The company’s single-family foreclosure rate was 0.38 percent for the three months ended March 31, 2016. This reflects the annualized total number of single-family properties acquired through foreclosure or deeds-in-lieu of foreclosure as a percentage of the total number of loans in Fannie Mae’s single-family guaranty book of business. |

Fannie Mae’s financial statements for the first quarter of 2016 are available in the accompanying Annex; however, investors and interested parties should read the company’s First Quarter 2016 Form 10-Q, which was filed today with the Securities and Exchange Commission and is available on Fannie Mae’s website, www.fanniemae.com. The company provides further discussion of its financial results and condition, credit performance, and other matters in its First Quarter 2016 Form 10-Q. Additional information about the company’s credit performance, the characteristics of its guaranty book of business, its foreclosure-prevention efforts, and other measures is contained in the “2016 First Quarter Credit Supplement” at www.fanniemae.com.

# # #

In this release, the company has presented a number of estimates, forecasts, expectations, and other forward-looking statements, including statements regarding: its future dividend payments to Treasury; the impact of and future plans with respect to the company’s credit risk transfer transactions; the sources of its future net interest income; the company’s future profitability; the factors that will affect the company’s future financial results; the factors that will affect the company’s future single-family serious delinquency rates; the future volume of its HARP refinancings; the future fair value of the company’s financial instruments; the company’s future loss reserves; and the impact of the company’s actions to reduce credit losses. These estimates, forecasts, expectations, and statements are forward-looking statements based on the company’s current assumptions regarding numerous factors, including future interest rates and home prices, the future performance of its loans and the future guaranty fee rates applicable to the loans the company acquires. Actual results, and future projections, could be materially different from what is set forth in the forward-looking statements as a result of: home price changes; interest rate changes, including negative interest rates; changes in unemployment rates; other macroeconomic and housing market variables; the company’s future serious delinquency rates; the company’s future guaranty fee pricing and the impact of that pricing on the company’s guaranty fee revenues and competitive environment; government policy; credit availability; changes in borrower behavior, including increases in the number of underwater borrowers who strategically default on their mortgage loans; the volume of loans it modifies; the effectiveness of its loss mitigation strategies; significant changes in modification and foreclosure activity; the volume and pace of future nonperforming loan sales

| First Quarter 2016 Results | 13 | |

and their impact on the company’s results and serious delinquency rates; the effectiveness of its management of its real estate owned inventory and pursuit of contractual remedies; changes in the fair value of its assets and liabilities; future legislative or regulatory requirements or changes that have a significant impact on the company’s business, such as the enactment of housing finance reform legislation; future updates to the company’s models relating to loss reserves, including the assumptions used by these models; changes in generally accepted accounting principles; changes to the company’s accounting policies; whether the company’s counterparties meet their obligations in full; effects from activities the company takes to support the mortgage market and help borrowers; the company’s future objectives and activities in support of those objectives, including actions the company may take to reach additional underserved creditworthy borrowers; actions the company may be required to take by FHFA, in its role as the company’s conservator or as its regulator, such as changes in the type of business the company does or the implementation of a single GSE security; limitations on the company’s business imposed by FHFA, in its role as the company’s conservator or as its regulator; the conservatorship and its effect on the company’s business; the investment by Treasury and its effect on the company’s business; the uncertainty of the company’s future; challenges the company faces in retaining and hiring qualified employees; the deteriorated credit performance of many loans in the company’s guaranty book of business; a decrease in the company’s credit ratings; defaults by one or more institutional counterparties; resolution or settlement agreements the company may enter into with its counterparties; operational control weaknesses; changes in the fiscal and monetary policies of the Federal Reserve, including any change in the Federal Reserve’s policy toward the reinvestment of principal payments of mortgage-backed securities or any future sales of such securities; changes in the structure and regulation of the financial services industry; the company’s ability to access the debt markets; disruptions in the housing, credit, and stock markets; government investigations and litigation; the company’s reliance on and the performance of the company’s servicers; conditions in the foreclosure environment; global political risks; natural disasters, environmental disasters, terrorist attacks, pandemics, or other major disruptive events; information security breaches; and many other factors, including those discussed in the “Risk Factors” section of and elsewhere in the company’s annual report on Form 10-K for the year ended December 31, 2015 and the company’s quarterly report on Form 10-Q for the quarter ended March 31, 2016, and elsewhere in this release.

Fannie Mae provides Web site addresses in its news releases solely for readers’ information. Other content or information appearing on these Web sites is not part of this release.

Fannie Mae enables people to buy, refinance, or rent homes.

Visit us at www.fanniemae.com/progress

Follow us on Twitter: http://twitter.com/FannieMae

| First Quarter 2016 Results | 14 | |

ANNEX

FANNIE MAE

(In conservatorship)

Condensed Consolidated Balance Sheets — (Unaudited)

(Dollars in millions, except share amounts)

| As of | |||||||||||

| March 31, | December 31, | ||||||||||

| 2016 | 2015 | ||||||||||

| ASSETS | |||||||||||

| Cash and cash equivalents | $ | 18,916 | $ | 14,674 | |||||||

| Restricted cash (includes $29,302 and $25,865, respectively, related to consolidated trusts) | 33,873 | 30,879 | |||||||||

| Federal funds sold and securities purchased under agreements to resell or similar arrangements | 17,550 | 27,350 | |||||||||

| Investments in securities: | |||||||||||

| Trading, at fair value (includes $1,200 and $135, respectively, pledged as collateral) | 40,000 | 39,908 | |||||||||

| Available-for-sale, at fair value (includes $80 and $285, respectively, related to consolidated trusts) | 16,983 | 20,230 | |||||||||

| Total investments in securities | 56,983 | 60,138 | |||||||||

| Mortgage loans: | |||||||||||

| Loans held for sale, at lower of cost or fair value | 4,639 | 5,361 | |||||||||

| Loans held for investment, at amortized cost: | |||||||||||

| Of Fannie Mae | 228,687 | 233,054 | |||||||||

| Of consolidated trusts | 2,817,440 | 2,809,180 | |||||||||

| Total loans held for investment (includes $13,714 and $14,075, respectively, at fair value) | 3,046,127 | 3,042,234 | |||||||||

| Allowance for loan losses | (25,819 | ) | (27,951 | ) | |||||||

| Total loans held for investment, net of allowance | 3,020,308 | 3,014,283 | |||||||||

| Total mortgage loans | 3,024,947 | 3,019,644 | |||||||||

| Deferred tax assets, net | 37,048 | 37,187 | |||||||||

| Accrued interest receivable (includes $7,246 and $6,974, respectively, related to consolidated trusts) | 7,978 | 7,726 | |||||||||

| Acquired property, net | 6,188 | 6,766 | |||||||||

| Other assets | 18,218 | 17,553 | |||||||||

| Total assets | $ | 3,221,701 | $ | 3,221,917 | |||||||

| LIABILITIES AND EQUITY | |||||||||||

| Liabilities: | |||||||||||

| Accrued interest payable (includes $8,212 and $8,194, respectively, related to consolidated trusts) | $ | 9,909 | $ | 9,794 | |||||||

| Debt: | |||||||||||

| Of Fannie Mae (includes $10,901 and $11,133, respectively, at fair value) | 370,819 | 386,135 | |||||||||

| Of consolidated trusts (includes $28,563 and $23,609, respectively, at fair value) | 2,828,951 | 2,811,536 | |||||||||

| Other liabilities (includes $408 and $448, respectively, related to consolidated trusts) | 9,903 | 10,393 | |||||||||

| Total liabilities | 3,219,582 | 3,217,858 | |||||||||

| Commitments and contingencies | — | — | |||||||||

| Fannie Mae stockholders’ equity: | |||||||||||

| Senior preferred stock, 1,000,000 shares issued and outstanding | 117,149 | 117,149 | |||||||||

| Preferred stock, 700,000,000 shares are authorized—555,374,922 shares issued and outstanding | 19,130 | 19,130 | |||||||||

| Common stock, no par value, no maximum authorization—1,308,762,703 shares issued and 1,158,082,750 shares outstanding | 687 | 687 | |||||||||

| Accumulated deficit | (128,665 | ) | (126,942 | ) | |||||||

| Accumulated other comprehensive income | 1,207 | 1,407 | |||||||||

| Treasury stock, at cost, 150,679,953 shares | (7,401 | ) | (7,401 | ) | |||||||

| Total Fannie Mae stockholders’ equity | 2,107 | 4,030 | |||||||||

| Noncontrolling interest | 12 | 29 | |||||||||

| Total equity | 2,119 | 4,059 | |||||||||

| Total liabilities and equity | $ | 3,221,701 | $ | 3,221,917 | |||||||

See Notes to Condensed Consolidated Financial Statements in the First Quarter 2016 Form 10-Q

| First Quarter 2016 Results | 15 | |

FANNIE MAE

(In conservatorship)

Condensed Consolidated Statements of Operations and Comprehensive Income — (Unaudited)

(Dollars and shares in millions, except per share amounts)

| For the Three Months | ||||||||||

| Ended March 31, | ||||||||||

| 2016 | 2015 | |||||||||

| Interest income: | ||||||||||

| Trading securities | $ | 120 | $ | 115 | ||||||

| Available-for-sale securities | 203 | 376 | ||||||||

| Mortgage loans (includes $24,626 and $24,622, respectively, related to consolidated trusts) | 26,961 | 27,044 | ||||||||

| Other | 48 | 33 | ||||||||

| Total interest income | 27,332 | 27,568 | ||||||||

| Interest expense: | ||||||||||

| Short-term debt | 51 | 29 | ||||||||

| Long-term debt (includes $20,658 and $20,515, respectively, related to consolidated trusts) | 22,512 | 22,472 | ||||||||

| Total interest expense | 22,563 | 22,501 | ||||||||

| Net interest income | 4,769 | 5,067 | ||||||||

| Benefit for credit losses | 1,184 | 533 | ||||||||

| Net interest income after benefit for credit losses | 5,953 | 5,600 | ||||||||

| Investment gains, net | 69 | 342 | ||||||||

| Fair value losses, net | (2,813 | ) | (1,919 | ) | ||||||

| Fee and other income | 203 | 308 | ||||||||

| Non-interest loss | (2,541 | ) | (1,269 | ) | ||||||

| Administrative expenses: | ||||||||||

| Salaries and employee benefits | 364 | 351 | ||||||||

| Professional services | 215 | 271 | ||||||||

| Occupancy expenses | 45 | 43 | ||||||||

| Other administrative expenses | 64 | 58 | ||||||||

| Total administrative expenses | 688 | 723 | ||||||||

| Foreclosed property expense | 334 | 473 | ||||||||

| Temporary Payroll Tax Cut Continuation Act of 2011 (“TCCA”) fees | 440 | 382 | ||||||||

| Other expenses (income), net | 264 | (5 | ) | |||||||

| Total expenses | 1,726 | 1,573 | ||||||||

| Income before federal income taxes | 1,686 | 2,758 | ||||||||

| Provision for federal income taxes | (550 | ) | (870 | ) | ||||||

| Net income | 1,136 | 1,888 | ||||||||

| Other comprehensive loss: | ||||||||||

| Changes in unrealized gains on available-for-sale securities, net of reclassification adjustments and taxes | (198 | ) | (91 | ) | ||||||

| Other | (2 | ) | (1 | ) | ||||||

| Total other comprehensive loss | (200 | ) | (92 | ) | ||||||

| Total comprehensive income attributable to Fannie Mae | $ | 936 | $ | 1,796 | ||||||

| Net income attributable to Fannie Mae | 1,136 | 1,888 | ||||||||

| Dividends distributed or available for distribution to senior preferred stockholder | (919 | ) | (1,796 | ) | ||||||

| Net income attributable to common stockholders | $ | 217 | $ | 92 | ||||||

| Earnings per share: | ||||||||||

| Basic | $ | 0.04 | $ | 0.02 | ||||||

| Diluted | 0.04 | 0.02 | ||||||||

| Weighted-average common shares outstanding: | ||||||||||

| Basic | 5,762 | 5,762 | ||||||||

| Diluted | 5,893 | 5,893 | ||||||||

See Notes to Condensed Consolidated Financial Statements in the First Quarter 2016 Form 10-Q

| First Quarter 2016 Results | 16 | |

FANNIE MAE

(In conservatorship)

Condensed Consolidated Statements of Cash Flows— (Unaudited)

(Dollars in millions)

| For the Three Months Ended March 31, | |||||||

| 2016 | 2015 | ||||||

| Net cash used in operating activities | $ | (3,111 | ) | $ | (1,249 | ) | |

| Cash flows provided by investing activities: | |||||||

| Proceeds from maturities and paydowns of trading securities held for investment | 975 | 296 | |||||

| Proceeds from sales of trading securities held for investment | 792 | 483 | |||||

| Proceeds from maturities and paydowns of available-for-sale securities | 883 | 1,232 | |||||

| Proceeds from sales of available-for-sale securities | 3,802 | 2,171 | |||||

| Purchases of loans held for investment | (39,935 | ) | (44,460 | ) | |||

| Proceeds from repayments of loans acquired as held for investment of Fannie Mae | 5,026 | 5,348 | |||||

| Proceeds from sales of loans acquired as held for investment of Fannie Mae | 849 | — | |||||

| Proceeds from repayments and sales of loans acquired as held for investment of consolidated trusts | 104,669 | 124,849 | |||||

| Net change in restricted cash | (2,994 | ) | (8,897 | ) | |||

| Advances to lenders | (25,635 | ) | (30,804 | ) | |||

| Proceeds from disposition of acquired property and preforeclosure sales | 4,129 | 5,490 | |||||

| Net change in federal funds sold and securities purchased under agreements to resell or similar arrangements | 9,800 | 10,720 | |||||

| Other, net | (545 | ) | 154 | ||||

| Net cash provided by investing activities | 61,816 | 66,582 | |||||

| Cash flows used in financing activities: | |||||||

| Proceeds from issuance of debt of Fannie Mae | 180,322 | 114,467 | |||||

| Payments to redeem debt of Fannie Mae | (196,016 | ) | (126,608 | ) | |||

| Proceeds from issuance of debt of consolidated trusts | 71,723 | 68,943 | |||||

| Payments to redeem debt of consolidated trusts | (107,575 | ) | (118,409 | ) | |||

| Payments of cash dividends on senior preferred stock to Treasury | (2,859 | ) | (1,920 | ) | |||

| Other, net | (58 | ) | 31 | ||||

| Net cash used in financing activities | (54,463 | ) | (63,496 | ) | |||

| Net increase in cash and cash equivalents | 4,242 | 1,837 | |||||

| Cash and cash equivalents at beginning of period | 14,674 | 22,023 | |||||

| Cash and cash equivalents at end of period | $ | 18,916 | $ | 23,860 | |||

| Cash paid during the period for: | |||||||

| Interest | $ | 26,013 | $ | 26,235 | |||

| Income taxes | 360 | — | |||||

See Notes to Condensed Consolidated Financial Statements in the First Quarter 2016 Form 10-Q

| First Quarter 2016 Results | 17 | |