October 24, 2006 to Acquire Exhibit 99.2 |

2 Forward Looking Statements Any statements set forth in the news release that are not entirely historical and factual in nature are forward-looking statements. For instance, all statements of belief and all statements about plans or expectations are forward-looking statements. Forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified. Potential risks and uncertainties regarding the acquisition of PowerDsine include, but are not limited to, the inability to close the acquisition transaction referred to in this press release for failure to obtain Israeli court approval, regulatory approval, shareholder approval, or any other reason, uncertainty as to the future profitability, if any, from the acquisition transaction referred to in this press release, and adverse impacts on the PoE markets or the speed of growth of the PoE market. The potential risks and uncertainties also include, but are not limited to, such factors as changes in generally accepted accounting principles, the difficulties regarding the making of estimates and projections, the hiring and retention of qualified personnel in a competitive labor market, acquiring, managing and integrating new operations, businesses or assets, closing or disposing of operations or assets, or possible difficulties in transferring work from one plant to another, rapidly changing technology and product obsolescence, difficulties predicting the timing and amount of plant closure costs, the potential inability to realize cost savings or productivity gains and to improve capacity utilization, potential cost increases, weakness or competitive pricing environment of the marketplace, uncertain demand for and acceptance of the company's products, adverse impacts on analog / mixed-signal markets, results of in-process or planned development or marketing and promotional campaigns, changes in demand for products, difficulties foreseeing future demand, effects of limited visibility of future sales, potential non-realization of expected orders or non-realization of backlog, product returns, product liability, and other potential unexpected business and economic conditions or adverse changes in current or expected industry conditions, business disruptions, epidemics, disasters, wars or potential future effects of the tragic events of September 11, 2001, variations in customer order preferences, fluctuations in market prices of the company's common stock and potential unavailability of additional capital on favorable terms, difficulties in implementing company strategies, dealing with environmental or other regulatory matters or litigation, or any matters involving litigation, contingent liabilities or other claims, difficulties and costs imposed by law, including under the Sarbanes-Oxley Act of 2002, difficulties in determining the scope of, and procuring and maintaining, adequate insurance coverage, difficulties, and costs, of protecting patents and other proprietary rights, work stoppages, labor issues, inventory obsolescence and, difficulties regarding customer qualification of products, manufacturing facilities and processes, and other difficulties managing consolidation or growth, including in the maintenance of internal controls, the implementation of information systems, and the training of personnel. In addition to these factors and any other factors mentioned elsewhere in this news release, the reader should refer as well to the factors, uncertainties or risks identified in the company's most recent Form 10-K and subsequent Form 10-Q reports filed by Microsemi with the SEC. Additional risk factors shall be identified from time to time in Microsemi's future filings. Microsemi does not undertake to supplement or correct any information in this release that is or becomes incorrect. If we use any non-GAAP financial measure (as defined by the SEC in Regulation G), you will find a presentation of the most directly comparable GAAP financial measure and a reconciliation of the differences between each non-GAAP financial measure used and the most directly comparable GAAP financial measure. |

3 Agenda • Transaction Overview • Overview of Microsemi • Overview of PowerDsine • Transaction Rationale |

4 Transaction Overview Consideration per Share • $8.25 in cash and 0.1498 Microsemi shares • $11.00 per share as of October 23, 2006 • 18.5% premium over PowerDsine’s closing price • 79.0 million shares outstanding post-transaction • 96% Microsemi shareholders • 4% PowerDsine shareholders Pro Forma Ownership Sources of Cash • Existing Microsemi cash on hand of $154 million plus positive cash flow prior to closing • PowerDsine cash on hand of $77 million • No external financing required or planned Anticipated Close • Calendar Q1 2007 (Microsemi’s Fiscal Q2 2007) Transaction Value • $245 million • $168 million net of cash acquired |

5 PowerDsine Snapshot • Pioneer and market leader in Power-over-Ethernet (PoE) solutions • Leading technology contributor to current and next-gen PoE standards • Successful competitor versus large-cap incumbents • Talented team of analog / mixed signal engineers • System-level power management expertise • Leveraging design expertise to penetrate other high-growth markets • Top-tier, single-source customer relationships • Strong IP portfolio including 16 PoE related patents and 91 patents pending • 139 employees (94 engineers); Global presence; Headquartered in Israel |

6 Strategic Rationale • Expand and further diversify commercial analog / mixed signal portfolio • Bolster presence in communications market via leading PoE supplier • Add mixed signal team in geography rich with silicon design talent • Leverage combined company’s high voltage process capabilities • Complement existing power management / handling expertise • Realize revenue and cost synergies to drive earnings upside • Neutral to slightly dilutive for the first twelve months after closing and accretive thereafter |

7 Key Figures (1) Based on First Call Consensus calendar year estimates as of October 20, 2006. ($ in millions) Microsemi PowerDsine Pro Forma 2007 First Call Consensus (1) Revenue $450.0 $47.0 $497.0 06 - 07 Revenue Growth 15.5% 32.9% 17.0% |

Microsemi Overview |

9 Well Diversified Company HIGH-RELIABILITY PRODUCTS HIGH PERFORMANCE ANALOG/ MIXED SIGNAL • Displays • Wireless • Storage • Notebooks / LCD TV • Displays • Wireless • Storage • Notebooks / LCD TV • Implantable Medical/MRI • Defense/Aero • Satellite • Operational Efficiencies • Profitable • Predictable • Operational Efficiencies • Profitable • Predictable • Fabless • High Margin • High Growth • System Engineered • Fabless • High Margin • High Growth • System Engineered |

10 Diverse End Markets Industrial / Industrial / Semi Cap Semi Cap Notebooks / Notebooks / LCD TV / Auto LCD TV / Auto Defense Defense Medical Medical 14% 14% Mobile/ Mobile/ Connectivity Connectivity 8% 8% 10% 10% 14% 14% Commercial Air / Commercial Air / Satellite Satellite 22% 22% 32% 32% *Represents approximate percent of sales for entire quarter ended 6/30/06, including PPG |

11 Top 100 customers ~ 70% Sales, none > 10% North America 71%, Europe 13%, Asia 16% OEM 58%, Distributors 42% *Represents approximate percent of sales for entire quarter ended 6/30/06, including PPG Solid Customer Base Industrial / Industrial / Semi Cap Semi Cap Notebooks / Notebooks / LCD TV / Auto LCD TV / Auto Defense Defense Medical Medical Mobile/ Mobile/ Connectivity Connectivity Commercial Air / Commercial Air / Satellite Satellite |

12 Fiscal Q4 Update (September 22, 2006) • On September 22, 2006, Microsemi updated its guidance for fiscal Q4 • Microsemi has scheduled its earnings call for November 16, 2006 after the market close • $0.25 - $0.27 per share Non-GAAP EPS • Flat to 2% q/q growth • 33% to 36% y/y growth Revenue Guidance (9/22/06) Metric |

PowerDsine Overview |

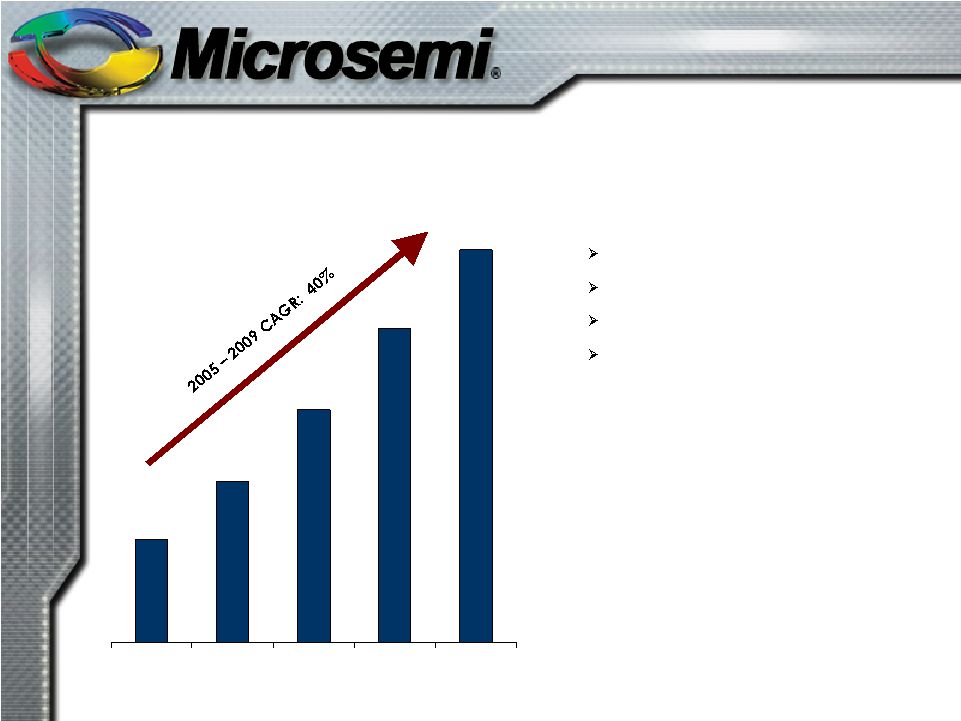

14 27.8 43.5 62.8 84.9 105.9 2005 2006 2007 2008 2009 PoE Switch Market (millions of ports) (1) (1) Source: Gartner Dataquest, November 2005. PowerDsine: Growing PoE Opportunity • PoE market is being driven by emerging high growth applications VoIP WLAN WiMAX Advanced security • PowerDsine first to sell PoE ICs commercially • PowerDsine sells to nearly every Ethernet switch vendor • New applications for PoE using the 802.3at high power standard such as laptops will drive future growth |

15 PowerDsine: Strong Technical Foundation Analog / Mixed Signal SoC Integration Power Management Software / Embedded Controller Comms / Networking Systems Expertise |

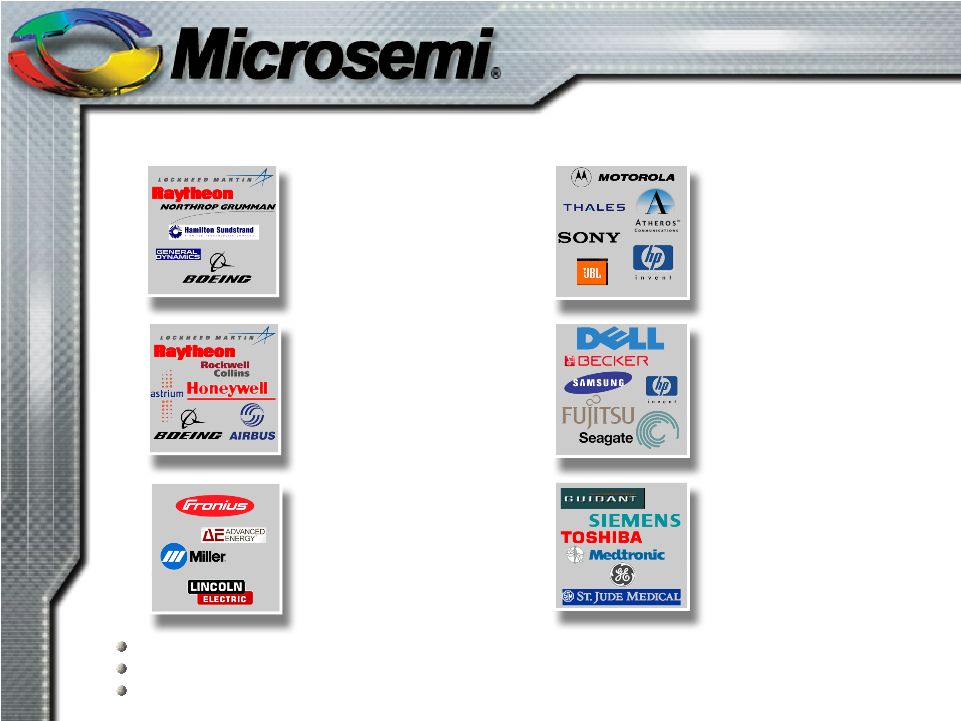

16 PowerDsine: Top-Tier Customers • Unique single-source provider of mission critical function for customers |

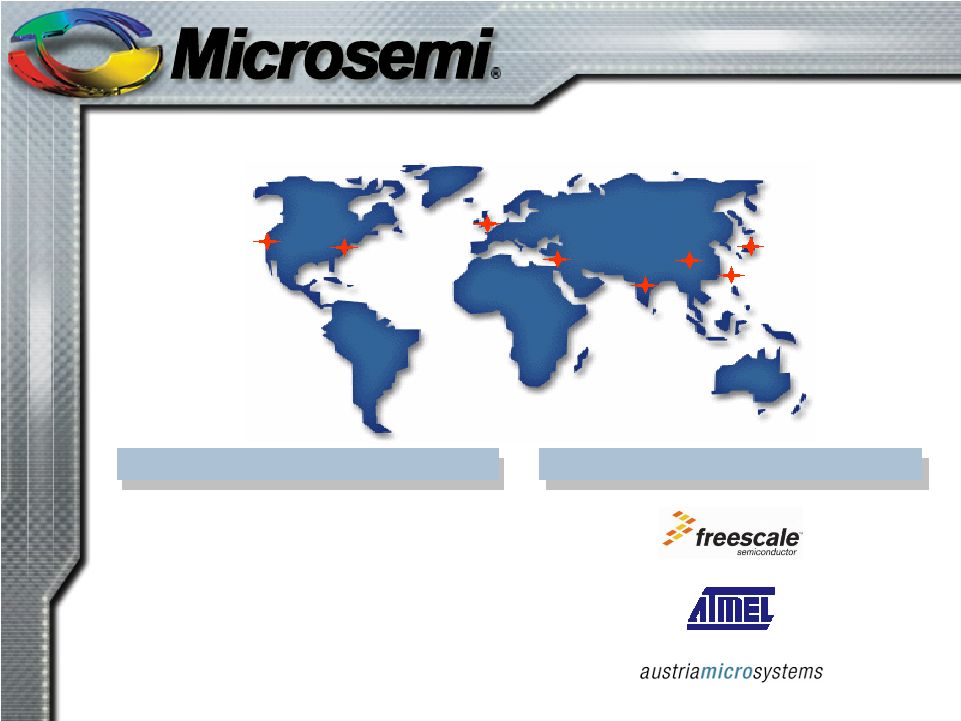

17 PowerDsine: Global Fabless Operation PowerDsine Locations Hod Hasharon, Israel (Headquarters, R&D and sales) China (Sales and tech support) India (Sales) Japan (Sales and tech support) Taiwan (Marketing, sales, and tech support) United Kingdom (Sales) United States (Marketing, R&D, sales, and tech support) PowerDsine Foundry Partners |

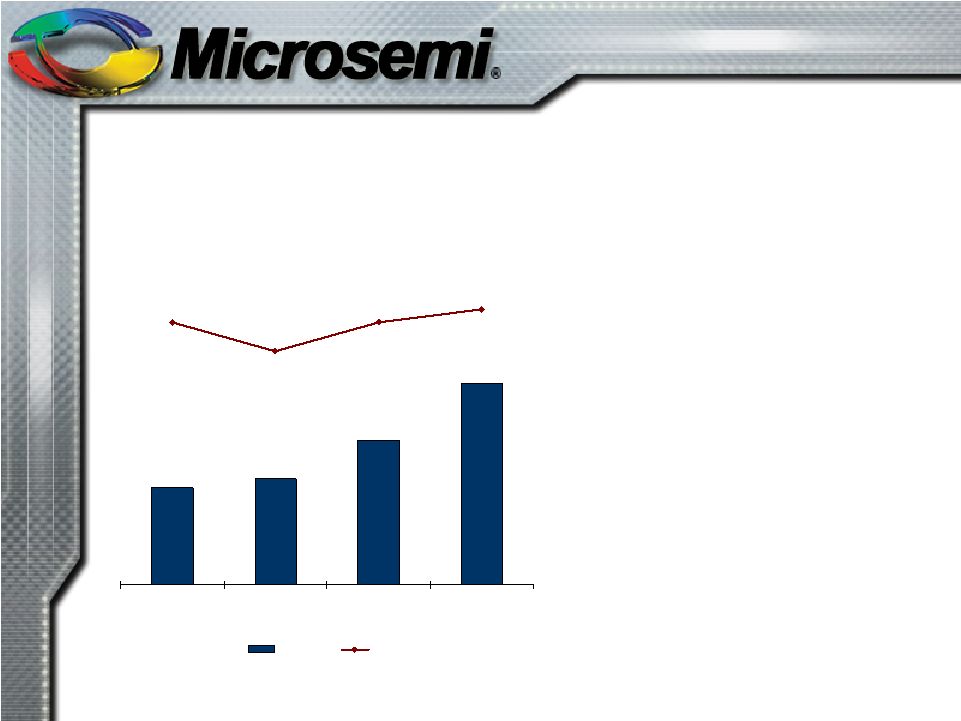

18 $7.2 $7.4 $8.3 $9.6 52.5% 52.0% 51.9% 50.6% Q405 Q106 Q206 Q306 Revenue Gross Margin PowerDsine: Positive Financial Momentum Quarterly Revenue and Gross Margins (1) (unaudited, in millions) Three Months ended 9/30/06 (2) (unaudited, in millions, except per share data) (1) Unaudited gross margins are pro forma to exclude non-cash stock-based compensation expenses. (2) Unaudited pro forma financial data excludes non-cash stock-based compensation expenses totaling $1.1 million. Revenue $9.6 Gross Profit $5.0 Gross Margin 52.5% Operating Expenses $5.6 Operating Profit ($0.3) Non-GAAP Net Income $0.6 Non-GAAP EPS $0.03 Balance Sheet Data as of 9/30/06 (unaudited, in millions) Cash & Equivalents $76.7 Debt $0.0 |

Transaction Rationale |

20 Strengthen Microsemi Offerings New Technologies New Customer Opportunities New End Markets •Networking / comms •VoIP phones / networked security / WLAN APs •3COM •Alcatel •Avaya •D-Link •Extreme •Fujitsu •HP •Huawei •Linksys •PoE •Power management •Power SoCs •NetGear •Nortel •Samsung •Software •High voltage process •Multi-disciplinary analog / mixed signal capabilities •138 engineers / 10,000 population ~ 2x U.S. •Semiconductors are major focus for the area •2,700 technology companies New Talent Pool: Israel |

21 Drive EPS Accretion Through Synergies • Cross-sell existing Microsemi and PowerDsine customers • Improve PowerDsine ability to drive sales penetration of large accounts • Accelerate commercialization of “new market” power management SoCs • Leverage combined power management capabilities / expertise • Extend system controller capabilities to new applications and markets • Increase PowerDsine volume buying power with suppliers • Eliminate duplicate public company costs • Improve operating margins |

Appendix |

23 Non-GAAP to GAAP Reconciliation – Page 18 Quarter Ended Reconciliation to GAAP 12/31/05 3/31/06 6/30/06 9/30/06 Non-GAAP Gross Profit 3.8 3.7 4.3 5.0 Stock-Based Compensation - COGS (0.0) (0.1) (0.1) (0.1) GAAP Gross Profit 3.7 3.7 4.2 4.9 Non-GAAP Operating Expenses 5.6 Stock-Based Compensation - R&D 0.3 Stock-Based Compensation - S&M 0.2 Stock-Based Compensation - G&A 0.5 GAAP Operating Expenses 6.6 Non-GAAP Income from Operations (0.3) Stock-Based Compensation - COGS (0.1) Stock-Based Compensation - R&D (0.3) Stock-Based Compensation - S&M (0.2) Stock-Based Compensation - G&A (0.5) GAAP Income from Operations (1.4) Non-GAAP Net Income 0.6 Stock-Based Compensation - COGS (0.1) Stock-Based Compensation - R&D (0.3) Stock-Based Compensation - S&M (0.2) Stock-Based Compensation - G&A (0.5) GAAP Net-Income (0.6) GAAP Net Income per Share ($0.03) |