EXHIBIT 99.2

Management’s Discussion and Analysis for the fiscal year ended December 31, 2005, dated March 1, 2006

MANAGEMENT’S DISCUSSION AND ANALYSIS

March 1, 2006

This Management’s Discussion and Analysis (MD&A) contains forward-looking statements. These statements are based on certain estimates and assumptions and involve risks and uncertainties. Actual results may differ materially. See page 58 for additional information.

This MD&A should be read in conjunction with Suncor’s audited consolidated financial statements and the accompanying notes. All financial information is reported in Canadian dollars (Cdn$) and in accordance with Canadian generally accepted accounting principles (GAAP) unless noted otherwise. The financial measures cash flow from operations, return on capital employed (ROCE) and cash and total operating costs per barrel referred to in this MD&A are not prescribed by GAAP and are outlined and reconciled in Non GAAP Financial Measures on page 56.

Certain prior year amounts have been reclassified to enable comparison with the current year’s presentation.

Base operations refers to Oil Sands mining and upgrading operations.

Barrels of oil equivalent (boe) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet (mcf) of natural gas : one barrel of crude oil is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

References to “we,” “our,” “us,” “Suncor” or “the company” mean Suncor Energy Inc., its subsidiaries, partnerships and joint venture investments, unless the context otherwise requires.

The tables and charts in this document form an integral part of this MD&A.

Additional information about Suncor filed with Canadian securities commissions and the United States Securities and Exchange Commission (SEC), including periodic quarterly and annual reports and the Annual Information Form (AIF) filed with the SEC under cover of Form 40-F, is available on-line at www.sedar.com, www.sec.gov and our website www.suncor.com.

In order to provide shareholders with full disclosure relating to potential future capital expenditures, we have provided cost estimates for projects that, in many cases, are still in the early stages of development. These costs are preliminary estimates only. The actual amounts are expected to differ and these differences may be material. For a further discussion of our significant capital projects and the range of cost estimates associated with an “on-budget” project, refer to note 1 under “Significant Capital Project Update” on page 26.

17

SUNCOR OVERVIEW AND STRATEGIC PRIORITIES

Suncor Energy Inc. is an integrated energy company headquartered in Calgary, Alberta. We operate four businesses:

• Oil Sands, located near Fort McMurray, Alberta, produces bitumen recovered from oil sands through mining and in-situ technology and upgrades it into refinery feedstock, diesel fuel and byproducts.

• Natural Gas (NG) produces natural gas in Western Canada, providing revenues and serving as a price hedge against the company’s internal natural gas consumption in our oil sands and downstream operations.

• Energy Marketing and Refining – Canada (EM&R) operates a 70,000 barrel per day (bpd) capacity refinery in Sarnia, Ontario and markets refined petroleum products to customers primarily in Ontario and Quebec. EM&R also manages our company-wide energy marketing and trading activities and sales of all Oil Sands and NG production. Financial results relating to the sales of Oil Sands and NG production are reported in those business segments.

• Refining and Marketing – U.S.A. (R&M) operates 90,000 bpd of refining capacity in Commerce City, Colorado as well as related pipeline assets. R&M markets refined petroleum products to customers throughout Colorado.

Suncor’s strategic priorities are:

Operational:

• Developing our oil sands resource base through mining and in-situ technology and supplementing Suncor bitumen production with third party supply.

• Expanding Oil Sands mine, in-situ, extraction and upgrading facilities to increase crude oil production.

• Integrating Oil Sands production into the North American energy market through Suncor’s refineries and the refineries of other customers to reduce vulnerability to supply and demand imbalances.

• Managing environmental and social performance to earn continued stakeholder support for our ongoing operations and growth plans.

• Maintaining a strong focus on worker, contractor and community safety.

• Pursuing new technology applications to increase production and reduce costs and environmental impacts.

Financial:

• Controlling costs through a strong focus on operational excellence, economies of scale and improved management of engineering, procurement and construction of major projects.

• Reducing risk associated with natural gas price volatility by producing natural gas volumes that offset purchases for internal consumption.

• Maintaining a strong balance sheet by controlling debt and closely managing capital cost outlays.

• Targeting opportunities that have the potential to support a minimum 15% return on capital employed (ROCE) assuming a US$35 West Texas Intermediate (WTI) crude oil price and a Cdn$/US$ exchange rate of $0.80.

18

2005 Overview

• In September we completed rebuilding portions of our Oil Sands plant that were damaged by fire on January 4, 2005. The recovery and planned maintenance work was completed on schedule and the plant was running at full capacity by the end of September.

• In October, we successfully commissioned an expansion of our Oil Sands facilities that increased production capacity to 260,000 bpd from the previous capacity of 225,000 bpd. The project was completed on schedule and on budget. Work to further expand Oil Sands production capacity to 350,000 bpd in 2008 also progressed during the year and is on schedule and on budget.

• Construction of the second stage of our Firebag in-situ operation was completed on schedule and on budget. Commercial operations are expected to commence in the first quarter of 2006.

• In 2005, we produced 190 million cubic feet per day (mmcf/d) of natural gas from our conventional upstream operations compared to 200 mmcf/d in 2004. The decline was primarily due to weather related drilling delays and unplanned maintenance. Production remained in excess of volumes purchased for use in our Oil Sands and downstream operations.

• On May 31, 2005, we acquired the Colorado Refining Company from Valero Energy Corp., which included a 30,000 bpd refinery located adjacent to our existing refinery in Commerce City, Colorado. This combined operation is now the largest refining complex in the U.S. Rocky Mountain region.

• Construction continued on modifications to our Sarnia and Commerce City refineries to meet low-sulphur fuels regulations that will take effect in 2006.

• Maintaining a strong balance sheet remains a priority. Despite the impact of costs associated with the fire recovery, and an increase in capital spending to $2.8 billion (excluding the cost of the fire rebuild and capitalized interest), net debt (including cash and cash equivalents) at December 31, 2005 was $2.9 billion (1.2 times cash flow from operations), compared to $2.2 billion (1.1 times cash flow from operations) at December 31, 2004.

• Our company-wide ROCE (excluding major projects in progress) was 20.9% compared to 19% in 2004.

19

SELECTED FINANCIAL INFORMATION

Annual Financial Data

Year ended December 31 ($ millions except per share data) |

| 2005 |

| 2004 |

| 2003 |

|

|

|

|

|

|

|

|

|

Revenues |

| 11 086 |

| 8 665 |

| 6 611 |

|

Net earnings |

| 1 245 |

| 1 088 |

| 1 087 |

|

Total assets |

| 15 351 |

| 11 841 |

| 10 540 |

|

Long-term debt |

| 3 007 |

| 2 217 |

| 2 934 |

|

Dividends on common shares |

| 102 |

| 97 |

| 81 |

|

Net earnings attributable to common shareholders per share – basic |

| 2.73 |

| 2.40 |

| 2.42 |

|

Net earnings attributable to common shareholders per share – diluted |

| 2.67 |

| 2.36 |

| 2.26 |

|

Cash dividends per share |

| 0.24 |

| 0.23 |

| 0.1925 |

|

Outstanding Share Data

As at December 31, 2005 (thousands) |

|

|

|

|

|

|

|

|

|

|

|

Number of common shares |

| 457 665 |

|

Number of common share options |

| 19 203 |

|

Number of common share options – exercisable |

| 9 361 |

|

Quarterly Financial Data

|

| 2005 |

| 2004 |

| ||||||||||||

|

| Quarter ended |

| Quarter ended |

| ||||||||||||

($ millions except per share) |

| Dec. 31 |

| Sept. 30 |

| June 30 |

| Mar. 31 |

| Dec. 31 |

| Sept. 30 |

| June 30 |

| Mar. 31 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenues |

| 3 503 |

| 3 142 |

| 2 380 |

| 2 061 |

| 2 321 |

| 2 326 |

| 2 212 |

| 1 806 |

|

Net earnings |

| 694 |

| 341 |

| 112 |

| 98 |

| 333 |

| 337 |

| 202 |

| 216 |

|

Net earnings attributable to common shareholders per share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

| 1.52 |

| 0.75 |

| 0.24 |

| 0.22 |

| 0.73 |

| 0.74 |

| 0.45 |

| 0.48 |

|

Diluted |

| 1.48 |

| 0.73 |

| 0.24 |

| 0.21 |

| 0.72 |

| 0.73 |

| 0.43 |

| 0.46 |

|

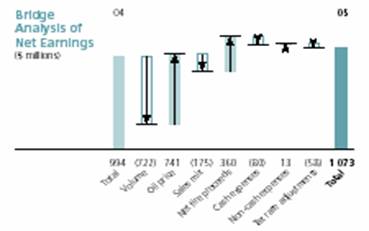

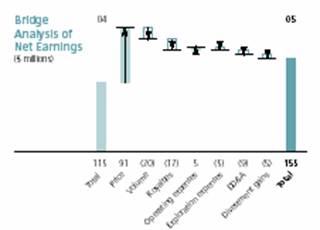

Net Earnings (1)

Year ended December 31,

($ millions)

|

| 05 |

| 04 |

| 03 |

| |

|

|

|

|

|

|

|

| |

| Oil Sands |

| 1 073 |

| 994 |

| 887 |

|

| Natural Gas |

| 155 |

| 115 |

| 120 |

|

| Energy Marketing and Refining – Canada |

| 41 |

| 80 |

| 53 |

|

| Refining and Marketing – U.S.A.(3) |

| 142 |

| 34 |

| 18 |

|

Capital Employed(1) (2)

Year ended December 31,

($ millions)

|

| 05 |

| 04 |

| 03 |

| |

|

|

|

|

|

|

|

| |

| Oil Sands |

| 4 633 |

| 4 169 |

| 4 050 |

|

| Natural Gas |

| 563 |

| 448 |

| 400 |

|

| Energy Marketing and Refining – Canada |

| 486 |

| 512 |

| 551 |

|

| Refining and Marketing – U.S.A.(3) |

| 327 |

| 232 |

| 270 |

|

Cash Flow from Operations(1)

Year ended December 31,

($ millions)

|

| 05 |

| 04 |

| 03 |

| |

|

|

|

|

|

|

|

| |

| Oil Sands |

| 1 895 |

| 1 752 |

| 1 803 |

|

| Natural Gas |

| 412 |

| 319 |

| 298 |

|

| Energy Marketing and Refining – Canada |

| 152 |

| 188 |

| 164 |

|

| Refining and Marketing – U.S.A.(3) |

| 247 |

| 59 |

| 34 |

|

(1) Excludes Corporate and Eliminations segment.

(2) Excludes major projects in progress.

(3) Refining and Marketing – U.S.A. 2003 data reflects five months of operations since acquisition on August 1, 2003. Data for 2005 includes results of the former Colorado Refining Company, acquired May 31, 2005.

20

Fluctuations in quarterly net earnings for 2005 and 2004 were due to a number of factors:

• The January 2005 fire at Oil Sands significantly reduced crude oil production to approximately 122,000 bpd for the first nine months of 2005.

• U.S. dollar denominated crude oil and natural gas prices were higher on average in 2005 compared to 2004. WTI averaged US$56.55 per barrel (bbl) in 2005 compared to US$41.40/bbl in 2004, and Henry Hub natural gas prices averaged US$8.55/mcf in 2005, compared to US$6.20/mcf in 2004.

• Cash operating costs fluctuated due to variations in Oil Sands production levels, the timing and amount of maintenance activities, and the price and volume of natural gas used for energy in Oil Sands operations.

• Commodity and refined product prices fluctuated as a result of global and regional supply and demand, as well as seasonal demand variations. In our downstream operations, seasonal fluctuations were reflected in higher demand for vehicle fuels and asphalt in summer and heating fuels in winter. Prices were also affected by decreased market supply as a result of hurricane activity in the Gulf of Mexico during the summer of 2005.

• Realized commodity prices were unfavourably impacted in 2005 and 2004 by increases in the Canadian dollar compared to the U.S. dollar, which reduced the Canadian dollar revenues earned. The stronger Canadian dollar also resulted in net foreign exchange gains on U.S. dollar denominated debt in 2005 and 2004. The higher appreciation of the Canadian dollar compared to the U.S. dollar in 2004 over 2005 resulted in higher foreign exchange gains in 2004 compared to 2005.

• A 1% reduction in the Province of Alberta’s corporate tax rates in the first quarter of 2004 increased 2004 net earnings by $53 million.

• The timing and amount of insurance receipts related to the fire at Oil Sands in January 2005.

Consolidated Financial Analysis

This analysis provides an overview of our consolidated financial results for 2005 compared to 2004. For a detailed analysis, see the various business segment analyses.

Net Earnings

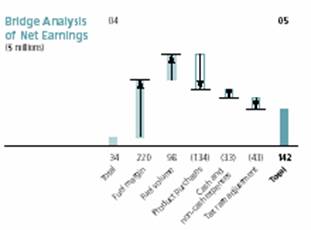

Our net earnings were $1.245 billion in 2005, compared with $1.088 billion in 2004 (2003 – $1.087 billion). The increase was primarily due to higher U.S. dollar benchmark crude oil and natural gas prices, the receipt of insurance payments related to the January 2005 fire at our oil sands facility and lower hedging losses. These positive impacts were partially offset by lower Oil Sands and Natural Gas production, higher maintenance expenses, higher energy costs in our Oil Sands and downstream operations, and the impact of a stronger Canadian dollar.

Net Earnings Components (1)

Year ended December 31 ($ millions, after-tax) |

| 2005 |

| 2004 |

| 2003 |

|

|

|

|

|

|

|

|

|

Net earnings before the following items: |

| 1 114 |

| 1 242 |

| 1 021 |

|

Firebag in-situ start-up costs (2) |

| (4 | ) | (14 | ) | — |

|

Oil Sands fire accrued insurance proceeds (2) |

| 360 |

| — |

| — |

|

Oil Sands Alberta Crown royalties |

| (256 | ) | (261 | ) | (21 | ) |

Impact of income tax rate reductions on opening net future income tax liabilities |

| — |

| 53 |

| (89 | ) |

Unrealized foreign exchange gains on U.S. dollar denominated long-term debt |

| 31 |

| 68 |

| 176 |

|

Net earnings as reported |

| 1 245 |

| 1 088 |

| 1 087 |

|

(1) This table highlights some of the factors impacting Suncor’s after-tax net earnings. For comparability purposes, readers should rely on the reported net earnings that are prepared and presented in the consolidated financial statements and notes in accordance with Canadian GAAP.

(2) Before deduction of Alberta Crown royalties.

21

Industry Indicators

(Average for the year unless otherwise noted) |

| 2005 |

| 2004 |

| 2003 |

|

|

|

|

|

|

|

|

|

West Texas Intermediate (WTI) crude oil US$/barrel at Cushing |

| 56.55 |

| 41.40 |

| 31.05 |

|

Canadian 0.3% par crude oil Cdn$/barrel at Edmonton |

| 69.00 |

| 52.55 |

| 43.55 |

|

Light/heavy crude oil differential US$/barrel WTI at Cushing less Lloydminster Blend at Hardisty |

| 20.90 |

| 13.55 |

| 8.65 |

|

Natural gas US$/thousand cubic feet (mcf) at Henry Hub |

| 8.55 |

| 6.20 |

| 5.45 |

|

Natural gas (Alberta spot) Cdn$/mcf at AECO |

| 8.50 |

| 6.80 |

| 6.70 |

|

New York Harbour 3-2-1 crack US$/barrel (1) |

| 9.50 |

| 6.90 |

| 5.30 |

|

Ontario refined product demand percentage change over prior year (2) |

| 0.2 |

| 4.3 |

| 2.5 |

|

Colorado light product demand percentage change over prior year (3) |

| 3.3 |

| 7.2 |

| (2.2 | ) |

Exchange rate: Cdn$/US$ |

| 0.83 |

| 0.77 |

| 0.72 |

|

(1) New York Harbour 3-2-1 crack is an industry indicator measuring the margin on a barrel of oil for gasoline and distillate. It is calculated by taking two times the New York Harbour gasoline margin plus one times the New York Harbour distillate margin and dividing by three.

(2) Figures for 2003 and 2004 are based on published government data. The figure for 2005 is an internal estimate based on preliminary government data.

(3) Figures for 2003 and 2004 are based on public reporting by state and government agencies. The 2005 figure is based on consensus estimates by third party consultants.

Revenues were $11.1 billion in 2005, compared with $8.7 billion in 2004 (2003 – $6.6 billion). The increase was primarily due to the following:

• Average commodity prices were higher in 2005 than in 2004. A 37% increase in average U.S. dollar WTI benchmark prices increased the selling price of Oil Sands crude oil production. Offsetting this increase, average light/heavy crude oil differentials compared to the WTI benchmark index widened by approximately 54%. As a result, the net price we received on certain sour crude oil and bitumen sales did not increase by as much as the increase in WTI.

• Refined product wholesale and retail prices in both EM&R and R&M were higher due to higher crude oil and refined product prices. In addition, a 47% increase in refined product sales volumes in R&M due to the acquisition of the Colorado Refining Company in the second quarter of 2005 had a positive impact on revenue.

• Lower strategic crude oil hedging losses increased revenues by $85 million. During 2005, we sold a portion of our crude oil production at fixed prices that were lower than prevailing market prices. During 2005 we sold 36,000 bpd at a fixed price of US$23/bbl compared to 79,000 bpd in 2004 at a fixed price range of US$21/bbl to US$24/bbl. Pretax hedging losses in 2005 were $535 million compared to $620 million in 2004.

• The recognition of $572 million pretax in net insurance proceeds related to the January 2005 fire at our Oil Sands operations.

Partially offsetting these increases were the following:

• An 8% increase in the average Cdn$/US$ exchange rate resulted in lower realizations on our crude oil sales basket and our natural gas sales. Because crude oil and natural gas are primarily sold based on U.S. dollar benchmark prices, a narrowing of the exchange rate difference produced a corresponding reduction in the Canadian dollar value of our products.

• In 2005, Oil Sands sales volumes averaged 165,300 bpd, compared with 226,300 bpd in 2004 (2003 – 218,300 bpd). Decreased crude oil production as a result of the fire, and an inventory build in the fourth quarter resulted in lower sales volumes. Oil Sands sales in 2005 included 16,600 bpd of bitumen from Firebag in-situ operations (2004 – 8,400 bpd; 2003 – 6,400 bpd).

• Natural gas production averaged 190 mmcf/d in 2005 compared to 200 mmcf/d in 2004. Lower production was the result of weather related drilling delays that impacted the western Canadian industry, as well as unplanned maintenance.

Overall, higher prices, net of the impact of the higher Cdn$/US$ exchange rate, increased total revenues by approximately $2.2 billion and lower hedging losses increased revenues by approximately $85 million. These impacts were partially offset by lower sales volumes that decreased revenues by approximately $800 million.

Purchases of crude oil and crude oil products were $4.2 billion in 2005 compared with $2.9 billion in 2004 (2003 – $1.7 billion). The increase was primarily due to the following:

• Higher benchmark crude oil prices. This factor had the largest impact on product purchases for EM&R and R&M as WTI increased 37% over the prior year.

22

• Increased purchases of crude oil feedstock to utilize the additional refining capacity acquired by R&M in the second quarter of 2005. The acquisition increased our Commerce City refining capacity from 60,000 bpd to 90,000 bpd.

• Purchased volumes of crude oil and refined products decreased in EM&R. In 2004, larger amounts of refined products were purchased to meet customer demand during the maintenance shutdown that occurred in the second quarter.

• In 2004, the repurchase of crude oil originally sold to a Variable Interest Entity (VIE) in 1999 increased purchases at Oil Sands by approximately $55 million. There was no similar transaction in 2005.

Operating, selling and general expenses were $2.1 billion in 2005 compared with $1.8 billion in 2004 (2003 – $1.5 billion). The primary reasons for the increase were:

• Higher operating expenses primarily due to higher energy costs in our Oil Sands and downstream operations.

• Increased maintenance related costs at Oil Sands, primarily to ensure reliability of the upgrader that was not damaged by the fire.

• Higher stock-based compensation expenses caused by increases in our share price.

• Incremental operating costs associated with the acquisition of the Colorado Refining Company in 2005.

Transportation and other expenses were $152 million in 2005 compared to $132 million in 2004 (2003 – $135 million). In 2004, mark-to-market gains on inventory-related derivatives of $13 million in Oil Sands reduced transportation and other costs. Despite decreased production in our Oil Sands operations, transportation costs, excluding the mark-to-market gain from 2004, have remained relatively constant due to the “ship-or-pay” nature of the contracts with our shippers. Consistent with 2004, Oil Sands pipeline tolls continued to be reduced by initial shipper toll adjustments. These toll reductions are currently expected to continue until at least 2007.

Depreciation, depletion and amortization (DD&A) was $720 million in 2005, consistent with 2004 (2003 – $622 million). DD&A at Oil Sands decreased by $23 million due to lower overburden amortization as a result of lower production, partially offset by higher maintenance shutdown and catalyst amortization, and depletion incurred in in-situ operations. NG DD&A increased by $15 million, reflecting an increased proved asset base and higher amortization related to unproven lands.

Royalty expenses were $555 million in 2005 compared with $531 million in 2004 (2003 – $139 million). The increase in 2005 was primarily related to increased natural gas royalties due to higher price realizations, partially offset by lower natural gas volumes. For a discussion of Oil Sands Crown royalties, see page 27.

Taxes other than income taxes were $529 million in 2005 compared to $540 million in 2004 (2003 – $466 million). The decrease was primarily due to lower sales volumes subject to fuel excise taxes (FET) in our Oil Sands and EM&R operations, partially offset by higher sales volumes subject to FET in our R&M operations.

Financing income was $15 million in 2005 compared with expenses of $24 million in 2004 (2003 – income of $74 million). The decrease in expenses was primarily due to higher amounts of capitalized interest, lower effective interest rates and the effects of foreign exchange on U.S. dollar operating accounts, partially offset by a $45 million decrease in foreign exchange gains on our U.S. dollar denominated long-term debt. Interest expense, net of capitalized interest, was $32 million in 2005 compared to $95 million in 2004. Interest expense, net of capitalized interest, decreased primarily due to more capital projects meeting the criteria for interest capitalization.

Income tax expense was $742 million in 2005 (37% effective tax rate), compared to $530 million in 2004 (33% effective tax rate) (2003 – $718 million – 40% effective tax rate). Income tax expense in both 2004 and 2003 included the effects of adjustments to opening future income tax balances due to changes in tax rates that reduced tax expense by $53 million in 2004 and increased tax expense by $89 million in 2003. Excluding these adjustments, income tax expense in 2004 was $583 million (36% effective tax rate) and $629 million in 2003 (35% effective tax rate).

Corporate Expenses

After-tax corporate expenses were $166 million in 2005 compared to $135 million in 2004 (2003 – $9 million). The increase was due to higher stock-based compensation expenses and higher insurance related costs, partially offset by lower financing costs as discussed previously. Corporate had a net cash deficiency of $122 million in 2005, compared with $343 million in 2004 (2003 – $280 million). The reduced deficiency was primarily due to changes in working capital.

23

Consolidated Cash Flow from Operations

Cash flow from operations was $2.476 billion in 2005 compared to $2.013 billion in 2004 (2003 – $2.040 billion). The increase in cash flow from operations was primarily due to the same factors that impacted earnings, with the exception of foreign exchange gains on our U.S. dollar denominated long-term debt and future income taxes, both of which are non-cash items.

Total dividends paid during 2005 were $0.24 per share, compared with $0.23 per share in 2004. Suncor’s Board of Directors periodically reviews the dividend policy, taking into consideration the company’s capital spending profile, financial position, financing requirements, cash flow and other relevant factors. In the second quarter of 2004, the Board approved an increase in the quarterly dividend to $0.06 per share, from $0.05 per share.

Dividends

Total dividends paid during 2005 were $0.24 per share, compared with $0.23 per share in 2004. Suncor's Board of Directors periodically reviews the dividend policy, taking into consideration the company's capital spending profile, financial position, financing requirements, cash flow and other relevant factors. In the second quarter of 2004, the Board approved an increase in the quarterly dividend to $0.06 per share, from $0.05 per share.

Oil Sands Fire

On January 4, 2005, a fire at our Oil Sands operations damaged Upgrader 2, reducing production from base operations to approximately 122,000 bpd for the first nine months of the year. Repairs and scheduled maintenance were completed in September 2005, at which time operations returned to full production capacity.

We expect our property loss and business interruption (BI) insurance policies to significantly mitigate the financial impact of the fire. During 2005, we received $115 million (US$95 million) from our property loss policy and $594 million (US$500 million) in proceeds from our BI insurance policies, including $175 million (US$150 million) received in January and February 2006. The company is currently negotiating a final settlement with its business interruption insurers. Any subsequent proceeds will be recorded when unconditionally received or receivable.

For royalty purposes, BI proceeds are treated in the same manner as the revenues they replace and, accordingly, attract Alberta Crown royalties. For further discussion about Oil Sands Crown royalties, see page 27.

In the fourth quarter of 2005, we renewed our property and BI insurance programs. All of our policy limits and deductibles remain unchanged except as noted. We carry primary and excess property loss and BI coverage with a combined limit up to US$1.150 billion, net of deductible amounts. The primary property loss policy of US$250 million has a deductible of US$10 million per incident and the primary BI policy of US$200 million has a deductible per incident of the greater of US$50 million gross earnings lost (as defined in the insurance policy) or 30 days from the incident.

The excess coverage of US$700 million can be used for either property loss or BI coverage for our Oil Sands operations. For BI purposes, this excess coverage is available commencing on the later of full utilization of the primary BI coverage or 90 days from the date of the incident. Effective January 1, 2006, the excess coverage has a ceiling of US$40/bbl WTI for purposes of determining the amount of BI losses.

Liquidity and Capital Resources

At December 31, 2005, our capital resources consisted primarily of cash flow from operations and available lines of credit. Our level of earnings and cash flow from operations depends on many factors, including commodity prices, production levels, downstream margins and Cdn$/US$ exchange rates. In 2005, cash flow from operations was negatively impacted by the fire at Oil Sands.

At December 31, 2005, our net debt (short and long-term debt less cash and cash equivalents) was approximately $2.9 billion compared to $2.2 billion at December 31, 2004. Approximately $710 million of the increase in total net debt in 2005 was the result of capital spending exceeding cash from operating activities.

In 2005, we entered into a new $600 million credit facility agreement with a one year term and also renewed $200 million of our available credit and term loan facilities. Our undrawn lines of credit at December 31, 2005 were approximately $1.3 billion. Suncor’s current long-term senior debt ratings are A- by Standard & Poor’s, A(low) by Dominion Bond Rating Service and A3 by Moody’s Investors Service. All debt ratings have a stable outlook.

Interest expense on debt continues to be influenced by the composition of our debt portfolio, and we are benefiting from short-term floating interest rates continuing at low levels. To manage fixed versus floating rate exposure, we have entered into interest rate swaps with investment grade counterparties, resulting in the swapping of $600 million of fixed rate debt to variable rate borrowings.

Management of debt levels continues to be a priority given our growth plans. We believe a phased approach to existing and future growth projects should assist us in our efforts to maintain our ability to manage project costs and debt levels.

24

We believe we have the capital resources to fund our 2006 capital spending program of $3.5 billion and to meet current working capital requirements. If additional capital is required, we believe adequate additional financing is available at commercial terms and rates.

We anticipate our growth plan will be largely financed from internal cash flow, which is dependent on commodity prices, production levels and other factors, as well as debt.

After 2006, to support our growth strategy and sustain operations, we are projecting an annual capital spending program of approximately $3.5 billion. Actual spending is subject to change due to such factors as internal and external approvals and capital availability. Refer to the discussion under Risk Factors Affecting Performance on page 29 for additional factors that can have an impact on our ability to generate funds to support investing activities.

Aggregate Contractual Obligations

|

| Payments Due by Period |

| ||||||||

($ millions) |

| Total |

| 2006 |

| 2007-08 |

| 2009-10 |

| Later Years |

|

|

|

|

|

|

|

|

|

|

|

|

|

Fixed-term debt, commercial paper (1) |

| 2 977 |

| 910 |

| 401 |

| — |

| 1 666 |

|

Capital leases |

| 30 |

| 1 |

| 2 |

| 2 |

| 25 |

|

Interest payments on fixed-term debt, commercial paper and capital leases (1) |

| 2 429 |

| 157 |

| 241 |

| 223 |

| 1 808 |

|

Employee future benefits (2) |

| 457 |

| 33 |

| 74 |

| 84 |

| 266 |

|

Asset retirement obligations (3) |

| 1 221 |

| 54 |

| 101 |

| 72 |

| 994 |

|

Non-cancellable capital spending commitments (4) |

| 240 |

| 240 |

| — |

| — |

| — |

|

Operating lease agreements, pipeline capacity and energy services commitments (5) |

| 5 408 |

| 258 |

| 507 |

| 529 |

| 4 114 |

|

Total |

| 12 762 |

| 1 653 |

| 1 326 |

| 910 |

| 8 873 |

|

In addition to the enforceable and legally binding obligations quantified in the above table, we have other obligations for goods and services and raw materials entered into in the normal course of business, which may be terminated on short notice. Commodity purchase obligations for which an active, highly liquid market exists and which are expected to be re-sold shortly after purchase, are one example of excluded items.

(1) Includes $2,066 million of U.S. and Canadian dollar denominated debt that is redeemable at our option. Maturities range from 2007 to 2034. Interest rates vary from 5.95% to 7.15%. We entered into various interest rate swap transactions maturing in 2007 and 2011 that resulted in an average effective interest rate in 2005 ranging from 4.0% to 4.6% on $600 million of our medium term notes. Approximately $890 million of commercial paper with an effective interest rate of 3.2% was issued and outstanding at December 31, 2005.

(2) Represents the undiscounted expected funding by the company to its pension plans as well as benefit payments to retirees for other post-employment benefits.

(3) Represents the undiscounted amount of legal obligations associated with site restoration on the retirement of assets with determinable lives.

(4) Non-cancellable capital commitments related to capital projects totalled approximately $240 million at the end of 2005. In addition to capital projects, we spend maintenance capital to sustain our current operations. In 2006, we anticipate spending approximately $700 million at our Oil Sands operations towards sustaining capital.

(5) Includes transportation service agreements for pipeline capacity, including tankage for the shipment of crude oil from Fort McMurray to Hardisty, Alberta, as well as energy services agreements to obtain a portion of the power and steam generated by a cogeneration facility owned by a major energy company. Non-cancellable operating leases are for service stations, office space and other property and equipment.

We are subject to financial and operating covenants related to our public market and bank debt. Failure to meet the terms of one or more of these covenants may constitute an Event of Default as defined in the respective debt agreements, potentially resulting in accelerated repayment of one or more of the debt obligations.

In addition, a very limited number of our commodity purchase agreements, off-balance sheet arrangements and derivative financial instrument agreements contain provisions linked to debt ratings that may result in settlement of the outstanding transactions should our debt ratings fall below investment grade status.

At December 31, 2005, we were in compliance with all covenants and our debt ratings were investment grade with a stable outlook. For more information, see page 24.

25

Significant Capital Project Update

We spent $2.8 billion ($3.2 billion including the cost of the fire rebuild and capitalized interest) on capital investing activities in 2005 compared to $1.825 billion in 2004. A summary of the progress on our significant projects under construction is provided below. All projects listed below have received Board of Directors approval.

|

| Cost |

| Spent |

| Total Spent |

|

|

|

|

| Estimate |

| in 2005 |

| to Date |

|

|

|

Description |

| ($ millions) (1) |

| ($ millions) |

| ($ millions) |

| Status(1) |

|

|

|

|

|

|

|

|

|

|

|

Oil Sands |

|

|

|

|

|

|

|

|

|

Millennium vacuum unit |

| 425 |

| 60 |

| 450 |

| Project was completed on budget and on schedule. (2) |

|

|

|

|

|

|

|

|

|

|

|

Firebag Stage 2 |

| 515 |

| 140 |

| 540 |

| Project was completed on budget and on schedule, commissioning is underway. (2) |

|

|

|

|

|

|

|

|

|

|

|

Coker Unit (3) |

| 2 100 |

| 530 |

| 930 |

| Project is on schedule and on budget. |

|

|

|

|

|

|

|

|

|

|

|

Firebag Cogeneration and expansion |

| 400 |

| 95 |

| 120 |

| Project is on schedule and on budget. |

|

|

|

|

|

|

|

|

|

|

|

EM&R |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Diesel desulphurization and oil sands integration |

| 800 |

| 295 |

| 475 |

| Project is on schedule and on budget. |

|

|

|

|

|

|

|

|

|

|

|

R&M |

|

|

|

|

|

|

|

|

|

Diesel desulphurization |

| 465 | ) | 285 | ) | 420 | ) | Project cost estimate has been revised from $360 (US$300). |

|

(1) Estimating and budgeting for major capital projects is a process that involves uncertainties and that evolves in stages, each with progressively more refined data and a correspondingly narrower range of uncertainty. At very early stages, when broad engineering design specifications are developed, the level of uncertainty can result in price ranges with -30%/+50% (or similar) levels of uncertainty. As project engineering progresses, vendor bids are studied, goods and materials ordered and we move closer to the build stage, the level of uncertainty narrows. Generally, when projects receive final approval from our Board of Directors, our cost estimates have a range of uncertainty that has narrowed to the -10%/+10% or similar range. The projects noted in the above table have cost estimates within this range of uncertainty. These ranges establish an expected high and low capital cost estimate for a project. When we say that a project is “on budget”, we mean that we still expect the final project capital cost to fall within the current range of uncertainty for the project. Even at this stage, the uncertainties in the estimating process and the impact of future events, can and will cause actual results to differ, in some cases materially, from our estimates.

(2) Total project cost is subject to change until all accounts are final.

(3) Excludes costs associated with bitumen feed.

Variable Interest Entities and Guarantees and Off-balance Sheet Arrangements

At December 31, 2005, we had off-balance sheet arrangements with Variable Interest Entities (VIEs), and indemnification agreements with other third parties, as described below.

We have a securitization program in place to sell, on a revolving, fully serviced and limited recourse basis, up to $340 million of accounts receivable having a maturity of 45 days or less, to a third party. The third party is a multiple party securitization vehicle that provides funding for numerous asset pools. As at December 31, 2005, $340 million (2004 – $170 million) in outstanding accounts receivable had been sold under the program. Under the recourse provisions, we provide indemnification against credit losses for certain counterparties, for which indemnification did not exceed $58 million in 2005. A contingent liability has not been recorded for this indemnification as we believe we have no significant exposure to credit losses. Proceeds received from new securitizations and proceeds from collections reinvested in securitizations on a revolving basis for the year ended December 31, 2005, were $170 million and approximately $2,220 million, respectively. We recorded an after-tax loss of approximately $4 million on the securitization program in 2005 (2004 – $2 million; 2003 – $3 million).

In 1999, we entered into an equipment sale and leaseback arrangement with a VIE for proceeds of $30 million. The VIE’s sole asset is the equipment sold to it and leased back by Suncor. The VIE was consolidated effective January 1, 2005. The initial lease term covers a period of seven years. We have provided a residual value guarantee on the equipment of up to $7 million should we elect not to repurchase the equipment at the end of the lease term. Had we elected to terminate the lease at December 31, 2005, the total cost would have been $21 million (2004 – $25 million). Annualized equipment lease payments in 2005 were $5 million (2004 – $6 million; 2003 – $4 million).

26

We have agreed to indemnify holders of the 7.15% fixed-term U.S. dollar notes, the 5.95% fixed-term U.S. dollar notes and our credit facility lenders for added costs related to taxes, assessments or other government charges or conditions, including any required withholding amounts. Similar indemnity terms apply to the receivables securitization program, and certain facility and equipment leases.

There is no limit to the maximum amount payable under the indemnification agreements described above. We are unable to determine the maximum potential amount payable as government regulations and legislation are subject to change without notice. Under these agreements, we have the option to redeem or terminate these contracts if additional costs are incurred.

Outlook

During 2006, management will focus on the following operational priorities:

• Increase annual average Oil Sands production to 260,000 bpd at an average cash operating cost of $16.00 to $16.75 per barrel, assuming a natural gas price of US$6.75/mcf at Henry Hub.

• Increase natural gas production to an average of 205 to 210 mmcf/d. We will continue to focus on deep gas prospects.

• Advance plans for increased bitumen supply. Achieve full capacity operations from Firebag Stage 1 and a steady ramp up of production from Firebag Stage 2. On the mining side, we anticipate substantial completion of engineering for the new Steepbank mine extension and extraction facilities.

• Advance plans for increased upgrader capacity. Significant progress to take Suncor to 350,000 bpd in 2008 is anticipated with major progress on construction and vessel delivery. A regulatory hearing regarding our plans for increasing production to half a million barrels per day is anticipated, while engineering for that expansion progresses to the design specification stage.

• Advancing downstream integration plans. In 2006, we expect to complete modifications to the Commerce City and Sarnia refineries to allow low sulphur fuel production. The Commerce City refinery will undergo a major maintenance shutdown to support operational reliability and to tie in equipment that will enable it to process 10,000 to 15,000 bpd of Oil Sands sour crude blends. The Sarnia refinery will also undergo a major maintenance shutdown to support operational reliability.

• Focus on company-wide efficiency. To more seamlessly integrate operations and improve efficiency and productivity, we expect to complete the implementation of a company-wide enterprise resource planning (ERP) information and management system.

Oil Sands Crown Royalties and Cash Income Taxes

Under the current Province of Alberta oil sands royalty regime, Alberta Crown royalties for oil sands projects are payable at the rate of 25% of the difference between a project’s annual gross revenues net of related transportation costs (R), less allowable costs including allowable capital expenditures (the R-C Royalty), subject to a minimum royalty, currently at 1% of R. The Alberta government has classified Suncor’s current Oil Sands operations as two distinct “projects” for royalty purposes: Suncor’s base oil sands mining and associated upgrading operations with royalties based on upgraded product values, and the current Firebag in-situ project with royalties based on bitumen values under the government’s generic bitumen-based royalty regime for oil sands projects. Pursuant to an agreement we concluded with the Government of Alberta during the third quarter of 2005, we settled the terms and conditions of our option to transition our base operations in 2009 to the generic bitumen-based royalty regime. This option was initially granted by the government in 1997, but was subject to finalizing certain terms of transition. Should we elect to move our base operations to the bitumen-based royalty in 2009, assuming no change to the current regime, we would expect to pay a royalty in respect of our base operations of 25% of R-C, with “R” based on bitumen rather than upgraded product values, and “C” excluding substantially all of the upgrading costs. We have until late 2008 to decide if we will exercise this option.

In July 2004, we issued a statement of claim against the Crown, seeking, among other things, to overturn the government’s decision on the royalty treatment of our Firebag in-situ operations. In February 2006, we advised the Government of Alberta that we had elected not to proceed with our claim relating to the royalty treatment of Firebag.

Assuming anticipated levels of operating expenses and capital expenditures for each project remain relatively constant, and there are no changes to the current Government of Alberta oil sands royalty regime or the government’s application of the applicable rules, and no other unanticipated events occur, we believe future variability in Oil Sands royalty expense will primarily be a function of changes in annual Oil Sands revenue. On that basis, we would generally expect Alberta Crown royalty expense for Oil Sands, to range as set forth in the following chart.

27

If prices rise, we would expect the percentage to increase somewhat. For years after 2008, this percentage range may decline as anticipated new in-situ production attracts royalties based on bitumen values at 1% until project payout and if we elect to exercise the bitumen royalty option referred to in the previous paragraph.

Anticipated Royalty Expense Based on Certain Assumptions

For the Period from 2006-2013

Crown Royalty Expense (based on percentage of total Oil Sands revenue) % |

|

|

|

|

|

2006-08 |

| 10-12 |

| 12-14 |

|

2009-13 (1) |

| 5-7 |

| 6-8 |

|

WTI Price/bbl US$ |

| 40 |

| 50 |

|

Natural gas price per mcf at Henry Hub US$ |

| 6.50 |

| 7.50 |

|

|

|

|

|

|

|

Light/heavy oil differential of WTI at Cushing less Maya at the U.S. Gulf Coast US$ |

| 9.50 |

| 10.50 |

|

Cdn$/US$ exchange rate |

| 0.80 |

| 0.85 |

|

(1) Assuming we exercise our option to transition our base operations in 2009 to the generic bitumen-based royalty regime.

Based on these same economic assumptions and our current capital spending plans, and assuming continuation of the current economic circumstances including no change to the current Alberta Crown royalty regime for oil sands, we would expect the 25%

R-C royalty to apply to our existing Oil Sands base operations in future years and the 1% minimum royalty to apply to the Firebag project until the next decade.

Alberta Crown royalties are highly sensitive to, among other factors, changes in crude oil and natural gas pricing, production volumes, foreign exchange rates, and capital and operating costs for each oil sands project. In addition, all aspects of the current Alberta oil sands royalty regime, including royalty rates and the royalty base, are subject to alteration by the Government of Alberta. Accordingly, in light of these uncertainties and the potential for unanticipated events to occur, we strongly caution that it is impossible to predict even a range of annualized royalty expense as a percentage of revenues or the impact royalties may have on our financial results, and actual differences may be material. For example, our Alberta oil sands Crown royalty expense in 2006 and future years may be significantly impacted by the amount of outstanding business interruption insurance proceeds we receive, and the timing of the receipts. Therefore, the forward-looking information in the preceding paragraphs and table should not be taken as an estimate, forecast or prediction of future events or circumstances.

The timing of when the Oil Sands operations will be fully cash taxable is highly dependent on crude oil commodity prices and capital invested. Using the assumptions outlined in the table above, we anticipate that our Oil Sands and NG operations will be partially cash taxable commencing in 2007. These operations will continue to be partially cash taxable until the next decade, at which point they are expected to become fully cash taxable. In any particular year, our Oil Sands and NG operations may be subject to some cash income tax due to the sensitivity to crude oil and natural gas commodity price volatility and the timing of recognition of capital expenditures for income tax purposes.

The information in the preceding paragraphs under Oil Sands Crown Royalties and Cash Income Taxes incorporates operating and capital cost assumptions included in our current budget and long-range plan, and is not an estimate, forecast or prediction of actual future events or circumstances.

Climate Change

Our effort to reduce greenhouse gas emissions is reflected in our pursuit of greater internal energy efficiency; investment in renewable energy including wind power; carbon capture research and development; and emissions offsets.

We continue to consult with governments about the impact of the Kyoto Protocol and we plan to continue to actively manage our greenhouse gas emissions. We currently estimate that in 2010 the impact of the Kyoto Protocol on Oil Sands cash operating costs would be an increase of about $0.20 to $0.27 per barrel. This estimate assumes a reduction obligation of 15% from 2010 business-as-usual energy intensity (1) and that the maximum price for carbon credits would, as the Government of Canada indicated in 2002, be capped at $15 per tonne of carbon dioxide equivalent until 2012. Based on these assumptions, we do not currently anticipate that the cost implications of federal and provincial climate change plans will have a material impact on our business or future growth plans.

The ultimate impact of Canada’s implementation of the Kyoto Protocol, however, remains subject to numerous risks, uncertainties and unknowns. These include the outcome of discussions between the federal and provincial governments, the form, impact and effectiveness of implementing legislation, the ultimate allocation of reduction obligations among economic sectors, and other details of Canada’s implementation plan, as well as international developments. In addition, the Government of Canada has not indicated what, if any, limitations will be placed on the price of carbon

(1) Reflects the level of greenhouse gas emissions that would have occurred in the absence of energy efficiency and process improvements after 2000.

28

credits after 2012. It is not possible to predict how these and other Kyoto Protocol-related issues will ultimately be resolved.

Risk Factors Affecting Performance

Our financial and operational performance is potentially affected by a number of factors including, but not limited to, commodity prices and exchange rates, environmental regulations, stakeholder support for growth plans, extreme winter weather, regional labour issues and other issues discussed within Risk Factors for each of our business segments. A more detailed discussion of risk factors is presented in our most recent Annual Information Form/Form 40-F, filed with securities regulatory authorities.

Commodity Prices, Refined Product Margins and Exchange Rates

Our future financial performance remains closely linked to hydrocarbon commodity prices, which can be influenced by many factors including global and regional supply and demand, seasonality, worldwide political events and weather. These factors, among others, can result in a high degree of price volatility. For example, from 2003 to 2005 the monthly average price for benchmark WTI crude oil ranged from a low of US$28.10/bbl to a high of US$65.55/bbl. During the same three-year period, the natural gas Henry Hub benchmark monthly average price ranged from a low of US$4.49/mcf to a high of US$14.07/mcf. We believe commodity price volatility will continue.

Crude oil and natural gas prices are based on U.S. dollar benchmarks that result in our realized prices being influenced by the Cdn$/US$ currency exchange rate, thereby creating an element of uncertainty. Should the Canadian dollar strengthen compared to the U.S. dollar, the negative effect on net earnings would be partially offset by foreign exchange gains on our U.S. dollar denominated debt. The opposite would occur should the Canadian dollar weaken compared to the U.S. dollar. Cash flow from operations is not impacted by the effects of currency fluctuations on our U.S. dollar denominated debt.

Changes to the Cdn$/US$ exchange rate relationship can create significant volatility in foreign exchange gains or losses. On the outstanding US$1 billion in debt at the end of 2005, a $0.01 change in the Cdn$/US$ exchange rate would change earnings by approximately $11 million after-tax.

During 2005, the strengthening of the Canadian dollar against the U.S. dollar resulted in a $31 million after-tax foreign exchange gain on our U.S. dollar denominated debt.

Our U.S. capital projects are expected to be partially funded from Canadian operations. A weaker Canadian dollar would result in a higher funding requirement for these projects.

Sensitivity Analysis (1)

|

|

|

|

|

| Approximate Change in |

| |||

|

|

|

|

|

| Cash Flow from |

| After-tax |

| |

|

| 2005 |

|

|

| Operations |

| Earnings |

| |

|

| Average |

| Change |

| ($ millions) |

| ($ millions) |

| |

|

|

|

|

|

|

|

|

|

| |

Oil Sands |

|

|

|

|

|

|

|

|

| |

Price of crude oil ($/barrel) (2) |

| $ | 53.81 |

| US$1.00 |

| 39 |

| 25 |

|

Sweet/sour differential ($/barrel) |

| $ | 14.55 |

| US$1.00 |

| 25 |

| 16 |

|

Sales (bpd) |

| 165 300 |

| 1 000 |

| 12 |

| 8 |

| |

Natural Gas |

|

|

|

|

|

|

|

|

| |

Price of natural gas ($/mcf) (2) |

| $ | 8.57 |

| 0.10 |

| 5 |

| 3 |

|

Production of natural gas (mmcf/d) |

| 190 |

| 10 |

| 21 |

| 10 |

| |

Energy Marketing and Refining – Canada |

|

|

|

|

|

|

|

|

| |

Refining/wholesale margin (cpl) (2) |

| 7.6 |

| 0.1 |

| 5 |

| 3 |

| |

Refining and Marketing – U.S.A. |

|

|

|

|

|

|

|

|

| |

Refining/wholesale margin (cpl) |

| 9.0 |

| 0.1 |

| 5 |

| 3 |

| |

Consolidated |

|

|

|

|

|

|

|

|

| |

Exchange rate: Cdn$/US |

| $ | 0.83 |

| 0.01 |

| 33 |

| 9 |

|

(1) The sensitivity analysis shows the main factors affecting Suncor’s annual cash flow from operations and earnings based on actual 2005 operations. The table illustrates the potential financial impact of these factors applied to Suncor’s 2005 results. A change in any one factor could compound or offset other factors.

(2) Includes the impact of hedging activities.

29

Derivative Financial Instruments

We periodically enter into commodity-based derivative financial instruments such as forwards, futures, swaps and options to hedge against the potential adverse impact of changing market prices due to variations in underlying commodity indices. We also periodically enter into derivative financial instrument contracts such as interest rate swaps and foreign currency contracts as part of our risk management strategy to manage exposure to interest rate and foreign exchange fluctuations.

We also use energy derivatives, including physical and financial swaps, forwards and options to gain market information and to earn trading revenues. These trading activities are accounted for at fair value in our consolidated financial statements.

Derivative contracts accounted for as hedges are not recognized in the Consolidated Balance Sheets. Realized and unrealized gains or losses on these contracts, including realized gains and losses on derivative hedging contracts settled prior to maturity, are recognized in earnings and cash flows when the related sales revenues, costs, interest expense and cash flows are recognized.

Gains or losses resulting from changes in the fair value of derivative contracts that do not qualify for hedge accounting are recognized in earnings and cash flows when those changes occur.

Commodity Hedging Activities Our crude oil hedging program has been the subject of periodic management reviews to determine the continued need for hedging in light of our tolerance for exposure to market volatility as well as the need for stable cash flow to finance future growth. In the first quarter of 2004, the Board of Directors suspended the strategic crude oil hedging program. Crude oil hedges in place at the time fixed the price on 36,000 bpd of crude oil at an average price of US$23/bbl for 2005 (79,000 bpd at an average price of US$21 to US$24/bbl in 2004). These contracts expired on December 31, 2005.

To provide an element of stability to future earnings and cash flow, we resumed our strategic crude oil hedging program in the third quarter of 2005, receiving Board approval to permit us to fix a price or range of prices for a percentage of our total production of crude for specified periods of time. At December 31, 2005 we had entered into US$ WTI agreements covering 7,000 bpd of crude oil beginning January 1, 2006 and ending December 31, 2007. Prices for these barrels are fixed within a range of US$50/bbl to an average of approximately US$93/bbl WTI. We have continued to enter into crude oil hedges during the first quarter of 2006. As at March 1, 2006, crude oil hedges totalling 50,000 bpd of production were outstanding for the remainder of 2006 and 2007. Prices for these barrels are fixed within a range of US$50/bbl to an average of US$91.70/bbl. We intend to consider additional costless collars of up to 30% of our crude oil production if strategic opportunities are available.

On settlement of swap agreements, our hedging contracts result in cash receipts or payments for the difference between the derivative contract and market rates for the applicable volumes hedged during the contract term. For collars, if market rates are within the range of the hedged contract prices, the option contracts making up the collar will expire with no exchange of cash. Such cash receipts or payments offset corresponding decreases or increases in our sales revenues or crude oil purchase costs. For accounting purposes, amounts received or paid on settlement are recorded as part of the related hedged sales or purchase transactions in the Consolidated Statements of Earnings. In 2005, crude oil hedging decreased our net earnings by $337 million compared to a decrease of $397 million in 2004 (2003 – decrease of $155 million).

Crude oil hedge contracts outstanding at December 31, 2005 were as follows:

|

|

|

| Average |

| Revenue |

|

|

|

|

| Quantity |

| Price |

| Hedged |

| Hedge |

|

|

| (bpd) |

| (US$ /bbl)(a) |

| (Cdn$ millions)(b) |

| Period (c) |

|

|

|

|

|

|

|

|

|

|

|

Costless collars |

| 7 000 |

| 50.00 – 92.57 |

| 149 – 276 |

| 2006 |

|

Costless collars |

| 7 000 |

| 50.00 – 92.57 |

| 149 – 276 |

| 2007 |

|

(a) Average price of crude oil costless collars is WTI per barrel at Cushing, Oklahoma.

(b) The revenue hedged is translated to Cdn$ at the year-end exchange rate and is subject to change as the Cdn$/US$ exchange rate fluctuates during the hedge period.

(c) Original hedge term is for the full year.

30

Financial Hedging Activities We periodically enter into interest rate swap contracts as part of our strategy to manage exposure to interest rates. The interest rate swap contracts involve an exchange of floating rate and fixed rate interest payments between ourselves and investment grade counterparties. The differentials on the exchange of periodic interest payments are recognized as an adjustment to interest expense.

We have entered into various interest rate swap transactions at December 31, 2005. The swap transactions result in an average effective interest rate that is different from the stated interest rate of the related underlying long-term debt instruments.

|

| Principal Swapped |

| Swap |

| 2005 Effective |

|

Description of swap transaction |

| ($ millions) |

| Maturity |

| Interest Rate |

|

|

|

|

|

|

|

|

|

Swap of 6.70% Medium Term Notes to floating rates |

| 200 |

| 2011 |

| 4.0 | % |

Swap of 6.80% Medium Term Notes to floating rates |

| 250 |

| 2007 |

| 4.6 | % |

Swap of 6.10% Medium Term Notes to floating rates |

| 150 |

| 2007 |

| 4.0 | % |

In 2005, these interest rate swap transactions reduced pretax financing expense by $14 million compared to a pretax reduction of $17 million in 2004 (2003 – $12 million pretax).

At December 31, 2005, we had also hedged a portion of our euro exposure created by the anticipated purchase of equipment for a total of $31 million euros in 2006 and 2007.

Fair Value of Strategic Derivative Hedging Instruments

The fair value of derivative hedging instruments is the estimated amount, based on broker quotes and internal valuation models that we would receive (pay) to terminate the contracts. Such amounts, which also represent the unrecognized and unrecorded gain (loss) on the contracts, were as follows at December 31:

($ millions) |

| 2005 |

| 2004 |

|

|

|

|

|

|

|

Revenue hedge swaps and collars |

| (4 | ) | (305 | ) |

Margin hedge swaps |

| 1 |

| 5 |

|

Interest rate swaps and foreign currency forwards |

| 22 |

| 36 |

|

|

| 19 |

| (264 | ) |

We also use derivative instruments to hedge risks specific to individual transactions. The estimated fair value of these instruments was $5 million at December 31, 2005, compared to $9 million at December 31, 2004.

Energy Trading Activities Energy trading activities focus on the commodities we produce. In addition to financial derivatives used for hedging activities, we also use energy derivatives to gain market information and earn trading revenues. These energy trading activities are accounted for using the mark-to-market method, and as such, physical and financial energy contracts are recorded at fair value at each balance sheet date. During 2005, we recorded a net pretax gain of $5 million compared to a pretax gain of $11 million in 2004 (2003 – pretax loss of $3 million) related to the settlement and revaluation of financial energy trading contracts. In 2005, the settlement of physical trading activities resulted in a net pretax gain of $15 million compared to a net pretax gain of $12 million in 2004 (2003 – $2 million net pretax gain). These gains were included as energy marketing and trading activities in the Consolidated Statements of Earnings. Net of related general and administrative costs, the combination of these activities resulted in 2005 net after-tax earnings of $11 million compared to net after-tax earnings of $12 million in 2004 (2003 – $2 million after-tax loss).

The fair value of unsettled financial energy trading assets and liabilities at December 31 was as follows:

($ millions) |

| 2005 |

| 2004 |

|

|

|

|

|

|

|

Energy trading assets |

| 82 |

| 26 |

|

Energy trading liabilities |

| 70 |

| 9 |

|

Net energy trading assets |

| 12 |

| 17 |

|

The valuation of the above contracts was based on actively quoted prices and internal valuation models.

Counterparty Credit Risk We may be exposed to certain losses in the event that the counterparties to derivative financial instruments are unable to meet the terms of the contracts. Our exposure is limited to those counterparties holding derivative contracts with net positive fair values at the reporting date. We minimize this risk by entering into agreements primarily with investment grade counterparties. Risk is also minimized through regular management review of the potential exposure to and credit ratings of such counterparties.

31

At December 31, the company had exposure to credit risk with counterparties as follows:

($ millions) |

| 2005 |

| 2004 |

|

Derivative contracts not accounted for as hedges |

| 82 |

| 7 |

|

Unrecognized derivative contracts accounted for as hedges |

| 30 |

| 21 |

|

Total |

| 112 |

| 28 |

|

Environmental Regulations

Environmental laws affect nearly all aspects of our operations, imposing certain standards and controls on activities relating to oil and gas mining, in-situ and conventional exploration, development and production. Environmental laws also affect refining, distribution and marketing of petroleum products and petrochemicals and require companies engaged in those activities to obtain necessary permits to operate. Environmental assessments and approvals are required before initiating most new projects or undertaking significant changes to existing operations.

In addition to these specifically known requirements, we expect that changes to environmental laws could impose further requirements on companies operating in the energy industry. Some of the issues include the possible cumulative impacts of oil sands development in the Athabasca region; the need to reduce or stabilize various emissions; issues relating to global climate change, including the uncertainties and risks associated with Canada’s implementation of the Kyoto Protocol, and uncertainties associated with predicting emission intensity levels from our future production; and other potential impacts of government regulation in areas such as land reclamation and restoration, water quality and usage, and reformulated fuels to support lower vehicle emissions. Changes in environmental laws could have an adverse effect on us in terms of product demand, product formulation and quality, methods of production, and distribution and operating costs. The complexity of these issues makes it difficult to predict their future impact.

We anticipate capital expenditures and operating expenses could increase in the future as a result of the implementation of new and increasingly stringent environmental regulations.

Regulatory Approvals

Before proceeding with most major projects, we must obtain regulatory approvals. The regulatory approval process can involve stakeholder consultation, environmental impact assessments and public hearings, among other factors. Failure to obtain regulatory approvals, or failure to obtain them on a timely basis, could result in delays, abandonment, or restructuring of projects and increased costs, all of which could negatively impact future earnings and cash flow.

Critical Accounting Estimates

Critical accounting estimates are defined as estimates that are important to the portrayal of our financial position and operations, and require management to make judgments based on underlying assumptions about future events and their effects. These underlying assumptions are based on historical experience and other factors that management believes to be reasonable under the circumstances, and are subject to change as new events occur, as more industry experience is acquired, as additional information is obtained and as our operating environment changes. Critical accounting estimates are reviewed annually by the Audit Committee of the Board of Directors. We believe the following are the most critical accounting estimates used in the preparation of our consolidated financial statements.

Property, Plant and Equipment

We account for our Oil Sands in-situ and NG exploration and production activities using the “successful efforts” method. This policy was selected over the alternative of the full-cost method because we believe it provides more timely accounting of the success or failure of exploration and production activities.

The application of the successful efforts method of accounting requires management to determine the proper classification of activities designated as developmental or exploratory, which then determines the appropriate accounting treatment of the costs incurred. The results from a drilling program can take considerable time to analyze and the determination that commercial reserves have been discovered requires both judgment and industry experience. Where it is determined that exploratory drilling will not result in commercial production, the exploratory dry hole costs are written off and reported as part of Oil Sands and NG exploration expenses in the Consolidated Statements of Earnings. Dry hole expense can fluctuate from year to year due to such factors as the level of exploratory spending, the level of risk sharing with third parties participating in the exploratory drilling and the degree of risk in drilling in particular areas.

Properties that are assumed to be productive may, over a period of time, actually deliver oil and gas in quantities different than originally estimated because of changes in reservoir performance and/or adjustments in reserves. Such changes may require a test for the potential impairment of capitalized properties based on estimates of future cash

32

flow from the properties. Estimates of future cash flows are subject to significant management judgment concerning oil and gas prices, production quantities and operating costs. Where management assesses that a property is fully or partially impaired, the book value of the property is reduced to fair value and either completely removed (“written off”) or partially removed (“written down”) in our records and reported as part of Oil Sands and NG DD&A expenses in the Consolidated Statements of Earnings.

Our plant and equipment are depreciated on a straight-line basis over the estimated useful life of the assets. The straight-line basis reflects asset usage as a function of time rather than production levels. For example, the useful life of plant and equipment at our Oil Sands base operations and our Firebag operations are not based on recorded reserves as we have access to other undeveloped properties, and bitumen feedstock from third parties, as well as the ability to provide processing services for other producers’ bitumen. Firebag and NG property costs are depleted on a unit of production (UOP) basis. UOP amortization is used where that method better matches the asset utilization with the production associated with the asset. In each case, the expense is shown on the DD&A line in both the Consolidated Statements of Earnings and in the Schedules of Segmented Earnings.

We determine useful life based on prior experience with similar assets and, as necessary, in consultation with others who have expertise with the assets in question. However, the actual useful life of the assets may differ from our original estimate due to factors such as technological obsolescence, regulatory requirements and maintenance activity. As the majority of assets are depreciated on a straight-line basis, a 10% reduction in the useful life of plant and equipment would increase annual DD&A by approximately 10%. This impact would be reflected in all of our business segments with the majority of the impact being in Oil Sands.

Negative revisions in NG reserves estimates will result in an increase in depletion expenses.

We also continuously look at ways to further utilize technological advancements and opportunities for future growth. The classification of research and development costs as either capital or expense is dependent upon specific criteria, including production feasibility, available resources and management commitment.

Overburden

As part of the process of mining oil sands, it is necessary to remove surface material such as muskeg, glacial deposits and sand. This surface material is referred to as overburden, removal of which precedes mining of the oil sands deposits.

Accordingly, the quantity of overburden removed in a given period may not bear any relationship to the quantity of oil sands mined in the period, and as such the cash outlays can be different than the amount amortized. In 2005, the overburden amortization charge was $178 million (2004 – $225 million; 2003 – $208 million) compared with actual cash overburden spending of $287 million (2004 – $222 million; 2003 – $175 million). Oil Sands overburden amortization is reported as part of DD&A in the Consolidated Statements of Earnings. Deferred overburden costs are reported as part of “deferred charges and other” in the Consolidated Balance Sheets.

To ensure that each tonne of oil sands mined is allocated a proportionate share of overburden removal costs, we use the deferral method of accounting for overburden removal costs whereby all such costs are initially set up as a deferred charge.

To allocate the deferred overburden charges, a life of mine approach is used for each mine pit, relating the removal of all overburden (on a volume basis) to the mining of all of the oil sands ore on leases where there is regulatory approval (on a tonnage basis). By adopting this approach, an overburden “stripping ratio” is calculated that relates overburden removal costs to all proved and probable oil sands ore reserves. Over time, through a combination of increased mine areas, additional drilling activity and operational experience, we have seen our stripping ratios vary, which can increase or decrease the overburden amortization costs charged to the earnings statement. In 2005, the stripping ratio decreased by approximately 10% due to new operational information and mine plan changes. The effects of the decreased stripping ratio were offset by higher per unit overburden removal costs. The $135 million increase in the amount of overburden deferred in 2005 compared to 2004 is therefore primarily due to increased overburden volumes moved (see page 43).

Our existing policy of accounting for overburden may be revised in 2006. Refer to “Recently Issued Canadian Accounting Standards” on page 39.

Asset Retirement Obligations (ARO)

We are required to recognize a liability for the future retirement obligations associated with our property, plant and equipment. An ARO is only recognized to the extent there is a legal obligation associated with the retirement of a tangible long-lived asset that we are required to settle as a result of an existing or enacted law, statute, ordinance, written or oral contract, or by legal construction of a contract under the doctrine of promissory estoppel. The ARO is based on estimated costs, taking into account the anticipated method and extent of restoration consistent

33

with legal requirements, technological advances and the possible use of the site. Since these estimates are specific to the sites involved, there are many individual assumptions underlying our total ARO amount. These individual assumptions can be subject to change based on experience.

The ARO is measured at fair value and discounted to present value using a credit-adjusted risk-free discount rate of 5.6% (2004 – 6%). The ARO accretes over time until we settle the obligation, the effect of which is included in a separate line in the Consolidated Statements of Earnings entitled “Accretion of asset retirement obligations”. Payments to settle the obligations occur on an ongoing basis and will continue over the lives of the operating assets, which can exceed 35 years. The discount rate is adjusted as appropriate, to reflect long-term changes in market rates and outlook.

An ARO is not recognized for assets with an indeterminate useful life because the amount cannot be reasonably estimated. An ARO for these assets will be recorded in the first period in which the lives of the assets are determinable.