Exhibit 13

financial discussion

OVERVIEW FOR 2003

This Financial Discussion should be read in conjunction with the information on Forward-Looking Statements and Risk Factors found at the end of the Financial Discussion.

Despite being faced with continuing challenges from the global economic environment, we delivered a very strong financial performance in 2003. Our ability to leverage our wide range of offerings resulted in double-digit earnings per share growth, strong operating cash flow, a healthy return on investment and an improved balance sheet for 2003. We continue to successfully implement our Circle the Customer – Circle the Globe growth strategy to generate strong financial results.

Several important items impacted our financial results in 2003.

Operating Performance

• We continued to find new markets in which to grow our business. Strong sales growth in Kay resulted from servicing the developing fast-casual restaurant market segment and food retail business. Professional Products introduced the first solid-based product offering for surgical instrument cleaning in the acute care market segment. Our International locations continue to expand the successful Pest Elimination business to new geographies.

• We made appropriate decisions to improve the profitability of certain business units. We have exited low-margin accounts within Professional Products, Textile Care and areas in Europe. This has negatively impacted sales growth in 2003.

• We continued to invest in future growth during 2003. This included investing in our sales-and-service force and in acquiring such businesses as Adams Healthcare. We also made investments to improve the service efficiency of GCS Service. While GCS Service had lower sales and an operating loss in 2003, we have better positioned the business for the long term.

• Our sales associates grew our business by gaining new independent and chain accounts, as well as growing business at existing customers.

• We faced competition in our markets and we countered with our innovative product offerings and our superior customer service.

Financial Performance

• Operating cash flow in 2003 continued to be very strong and allowed us to make acquisitions, pay down $108 million of debt, reacquire over $227 million of our common stock and make $75 million in additional voluntary contributions to our U.S. pension plan.

• Currency translation had a positive impact on our financial results in 2003, adding approximately $12 million to net income.

• An improvement in our annual effective income tax rate from 39.8 percent in 2002 to 38.1 percent in 2003 added approximately $7 million to net income. The acquisition of our former European joint venture business at the end of fiscal year 2001 has allowed us to have a more tax efficient structure.

The combination of all of these factors helped us exceed all three of our long-term financial objectives in 2003. These objectives are (i) 15 percent growth in diluted income per common share, (ii) 20 percent return on beginning shareholders’ equity and (iii) an investment grade or “A” rated balance sheet. Specifically, here is what we accomplished:

• Diluted net income per share was $1.06 for 2003, up 33 percent from $0.80 in 2002. Included in 2003 net income is a gain of $11.1 million, or $6.7 million net of tax, from the sale of an equity investment. For 2002, net income includes (i) a transitional impairment charge of $4.0 million after tax ($0.02 per diluted share) from the adoption of Statement of Financial Accounting Standards (SFAS) No. 142, (ii) a one-time gain of $3.5 million after tax from benefit plan changes, (iii) special charges of $32.4 million after-tax related to restructuring activities and the integration of our European operations and (iv) a gain of $1.9 million after tax ($0.01 per diluted share) from discontinued operations. These items are of a non-recurring nature and are not necessarily indicative of future operating results.

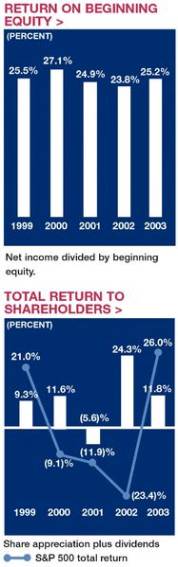

• Return on beginning shareholders’ equity was 25 percent for 2003 compared with 24 percent in 2002. The items discussed above affected the return for 2002. Adjusting for these items, return on beginning shareholders’ equity was 27 percent. This was the twelfth consecutive year we exceeded our long-term financial objective of a 20 percent return on beginning shareholders’ equity.

• We maintained our debt rating within the “A” categories of the major rating agencies during 2003.

• As a result of our continued strong financial performance and related stock price increases, on June 6, 2003, we paid a two-for-one stock split in the form of a 100 percent stock dividend to shareholders of record on May 23, 2003. All per share, shares outstanding and market price data have been adjusted to reflect the stock split.

2004 Expectations

• We expect to acquire additional businesses which fit with our Circle the Customer – Circle the Globe growth strategy.

• We remain concerned about the possible adverse impact of global terrorism, unforeseen hostilities and public health epidemics on the sensitive travel and tourism industries.

• We expect currency translation to have a favorable impact on 2004 but to a lesser extent than we experienced in 2003.

20

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

In May 2002, the Securities & Exchange Commission (SEC) issued a proposed rule: Disclosure in Management’s Discussion and Analysis about the Application of Critical Accounting Policies. Although the SEC has not issued a final rule yet, the following discussion has been prepared on the basis of the guidelines in the SEC rule proposal. If adopted as proposed, the rule would require disclosures connected with “estimates a company makes in applying its accounting policies.” However, such discussion would be limited to “critical accounting estimates,” or those that management believes meet two criteria in the proposal: “First, the accounting estimate must require a company to make assumptions about matters that are highly uncertain at the time the accounting estimate is made. Second, different estimates that the company reasonably could have used for the accounting estimate in the current period, or changes in the accounting estimate that are reasonably likely to occur from period to period, must have a material impact on the presentation of the company’s financial condition, changes in financial condition or results of operations.” Besides estimates that meet the “critical” estimate criteria, the company makes many other accounting estimates in preparing its financial statements and related disclosures. All estimates, whether or not deemed critical, affect reported amounts of assets, liabilities, revenues and expenses as well as disclosures of contingent assets and liabilities. Estimates are based on experience and other information available prior to the issuance of the financial statements. Materially different results can occur as circumstances change and additional information becomes known, even from estimates not deemed “critical” under the SEC rule proposal.

Revenue Recognition

We recognize revenue as services are performed or on product sales at the time title transfers to the customer. We record estimated reductions to revenue for customer programs and incentive offerings including pricing arrangements, promotions and other volume-based incentives at the time of sale. If market conditions were to decline, we may increase customer incentive offerings, which could reduce sales and gross profit margins at the time the incentive is offered.

Valuation Allowances and Accrued Liabilities

We estimate sales returns and allowances by analyzing historical returns and credits, and apply these trend rates to the most recent 12 months’ sales data to calculate estimated reserves for future credits. We estimate the allowance for doubtful accounts by analyzing accounts receivable balances by age, applying historical trend rates to the most recent 12 months’ sales, less actual write-offs to date. In addition, our estimates also include separately providing for 100 percent of specific customer balances when it is deemed probable that the balance is uncollectible. Actual results could differ from these estimates under different assumptions.

Estimates used to record liabilities related to pending litigation and environmental claims are based on our best estimate of probable future costs. We record the amounts that represent the points in the range of estimates that we believe are most probable or the minimum amounts when no amount within the range is a better estimate than any other amount. Potential insurance reimbursements are not anticipated in our accruals for environmental liabilities. While the final resolution of litigation and environmental contingencies could result in amounts different than current accruals, and therefore have an impact on our consolidated financial results in a future reporting period, we believe the ultimate outcome will not have a significant effect on our consolidated results of operations, financial position or cash flows.

Actuarially Determined Liabilities

The measurement of our pension and postretirement benefit obligations are dependent on a variety of assumptions determined by management and used by our actuaries. These assumptions affect the amount and timing of future contributions and expenses.

The assumptions used in developing the required estimates include discount rate, projected salary and health care cost increases, expected return or earnings on assets, retirement rates and mortality rates. The discount rate assumption is based on the investment yields available at year-end on corporate long-term bonds rated AA. Projected salary and health care cost increases are based on our long-term actual experience, the near-term outlook and assumed inflation. The expected return on plan assets reflects asset allocations, investment strategies and the views of investment managers over a long-term perspective. Retirement and mortality rates are based primarily on actual plan experience. The effects of actual results differing from our assumptions are accumulated and amortized over future periods and, therefore, generally affect our recognized expense in future periods. For 2003, our discount rates and projected salary increases used to determine our pension and postretirement obligations were lower than in 2002, while our expected return on plan assets remained unchanged.

We are self-insured in North America for most workers compensation, general liability and automotive liability losses, subject to per occurrence and aggregate annual liability limitations. We are insured for losses in excess of these limitations. We are also self-insured for health care claims for eligible participating employees, subject to certain deductibles and limitations. We determine our liabilities for claims incurred but not reported on an actuarial basis. A change in these assumptions would cause reported results to differ.

Income Taxes

Judgment is required to determine the annual effective income tax rate, deferred tax assets and liabilities and any valuation allowances recorded against net deferred tax assets. Our effective income tax rate is based on annual income, statutory tax rates and tax planning opportunities available in the various jurisdictions in which we operate. We establish liabilities or reserves when we believe that certain positions are likely to be challenged by authorities and we may not succeed, despite our belief that our tax return positions are fully supportable. We adjust these reserves in light of changing facts and circumstances, such as the progress of a tax audit. Our annual effective income tax rate includes the impact of reserve provisions and changes to reserves that we consider appropriate. This annual rate is then applied to our quarterly operating results. In the event that there is a significant one-time item recognized in our operating results, the tax attributable to that item would be separately calculated and recorded in the same period as the one-time item.

Tax regulations require items to be included in our tax returns at different times than the items are reflected in our financial statements. As a result, the effective income tax rate reflected in our financial statements differs from that reported in our tax returns. Some of these differences are permanent, such as expenses that are not deductible on our tax return, and some are temporary differences, such as depreciation expense. Temporary differences create deferred tax assets and liabilities. Deferred tax assets generally represent items that can be used as a

21

tax deduction or credit in our tax return in future years for which we have already recorded the tax benefit in our income statement. We establish valuation allowances for our deferred tax assets when the amount of expected future taxable income is not likely to support the utilization of the deduction or credit. Deferred tax liabilities generally represent items for which we have already taken a deduction in our tax return, but have not yet recognized that tax benefit in our financial statements. We have not recognized any deferred tax liabilities on undistributed international earnings because if those earnings were remitted to the United States, we believe any applicable income taxes would be substantially offset by available foreign tax credits.

A number of years may elapse before a particular tax matter, for which we have established a reserve, is audited and finally resolved. The number of tax years with open tax audits varies depending on the tax jurisdiction. In the United States, the Internal Revenue Service is currently examining our tax returns for 1999 through 2001. While it is often difficult to predict the final outcome or the timing of resolution of any particular tax matter, we believe that our reserves reflect the probable outcome of known tax contingencies. Unfavorable settlement of any particular issue would require the use of cash. Favorable resolution could result in reduced income tax expense reported in the financial statements in the future. Our tax reserves are generally presented in the balance sheet within other non-current liabilities.

Long-Lived and Intangible Assets

We periodically review our long-lived and intangible assets for impairment and assess whether significant events or changes in business circumstances indicate that the carrying value of the assets may not be recoverable. This could occur when the carrying amount of an asset exceeds the anticipated future undiscounted cash flows expected to result from the use of the asset and its eventual disposition. The amount of the impairment loss to be recorded, if any, is calculated as the excess of the asset’s carrying value over its estimated fair value. We also periodically reassess the estimated remaining useful lives of our long-lived assets. Changes to estimated useful lives would impact the amount of depreciation and amortization expense recorded in earnings. We have experienced no significant changes in the carrying value of our long-lived assets.

Statement of Financial Accounting Standards (SFAS) No. 142, Goodwill and Other Intangible Assets, requires that goodwill and certain intangible assets be assessed for impairment using fair value measurement techniques. Specifically, goodwill impairment is determined using a two-step process. Both the first step of determining the fair value of a reporting unit and the second step of determining the fair value of individual assets and liabilities of a reporting unit (including unrecognized intangible assets) are judgmental in nature and often involve the use of significant estimates and assumptions. Estimates of fair value are primarily determined using discounted cash flows, market comparisons and recent transactions. These valuation methodologies use significant estimates and assumptions, which include projected future cash flows (including timing), discount rate reflecting the risk inherent in future cash flows, perpetual growth rate, and determination of appropriate market comparables. Of the total goodwill included in our consolidated balance sheet, 15 percent is recorded in our U.S. Cleaning & Sanitizing reportable segment, 6 percent in our U.S. Other Services segment and 79 percent in our International Cleaning & Sanitizing segment.

In 2002, SFAS No. 142 became effective and as a result, we ceased to amortize goodwill in 2002. We were required to perform an initial impairment review of our goodwill at the beginning of 2002 under the guidelines of SFAS No. 142. The result of testing goodwill for impairment was a non-cash charge of $4.0 million after-tax ($0.02 per share). All of the impairment charge related to our Africa/Export operations due to the difficult economic environment in that region. We have continued to review our goodwill for impairment on an annual basis for all reporting units, including businesses reporting losses such as GCS Service, under the guidelines of SFAS No. 142.

Functional Currencies

In preparing the consolidated financial statements, we are required to translate the financial statements of our foreign subsidiaries from the currency in which they keep their accounting records, generally the local currency, into United States dollars. Assets and liabilities of these operations are translated at the exchange rates in effect at each fiscal year end. The translation adjustments related to assets and liabilities that arise from the use of differing exchange rates from period to period are included in accumulated other comprehensive income (loss) in shareholders’ equity. Income statement accounts are translated at the average rates of exchange prevailing during the year. We evaluate our International operations based on fixed rates of exchange; however, the different exchange rates from period to period impact the amount of reported income from our consolidated operations.

OPERATING RESULTS

Consolidated

(thousands, except per share) |

| 2003 |

| 2002 |

| 2001 |

| |||

|

|

|

|

|

|

|

| |||

Net sales |

| $ | 3,761,819 |

| $ | 3,403,585 |

| $ | 2,320,710 |

|

Operating income |

| $ | 482,658 |

| $ | 395,866 |

| $ | 318,179 |

|

Income |

|

|

|

|

|

|

| |||

Continuing operations before change in accounting |

| $ | 277,348 |

| $ | 211,890 |

| $ | 188,170 |

|

Change in accounting |

|

|

| (4,002 | ) |

|

| |||

Discontinued operations |

|

|

| 1,882 |

|

|

| |||

Net income |

| $ | 277,348 |

| $ | 209,770 |

| $ | 188,170 |

|

|

|

|

|

|

|

|

| |||

Diluted income per common share |

|

|

|

|

|

|

| |||

Continuing operations before change in accounting |

| $ | 1.06 |

| $ | 0.81 |

| $ | 0.72 |

|

Change in accounting |

|

|

| (0.02 | ) |

|

| |||

Discontinued operations |

|

|

| 0.01 |

|

|

| |||

Net income |

| $ | 1.06 |

| $ | 0.80 |

| $ | 0.72 |

|

Our consolidated net sales reached $3.8 billion for 2003, an increase of 11 percent over net sales of $3.4 billion in 2002. Excluding acquisitions and divestitures, consolidated net sales increased 10 percent. Changes in currency translation positively impacted the consolidated sales growth rate by 6 percentage points, primarily due to the strength of the euro against the U.S. dollar. Sales also benefited from aggressive new account sales, new products and selling more to existing customers.

22

|

| 2003 |

| 2002 |

| 2001 |

|

|

|

|

|

|

|

|

|

Gross profit as a percent of net sales |

| 50.9 | % | 50.4 | % | 51.7 | % |

Selling, general & administrative expenses as a percent of net sales |

| 38.1 | % | 37.7 | % | 38.0 | % |

Our consolidated gross profit margin in 2003 increased over 2002. In 2002, cost of sales included $9.0 million of restructuring costs. If these costs were excluded, the gross profit margin for 2002 would have been 50.7 percent. The increase in the margin for 2003 also benefited from business mix and cost reduction actions, partially offset by poor results in GCS Service during 2003.

Selling, general and administrative expenses for 2003 increased as a percentage of sales over 2002. The increase in the 2003 expense ratio is primarily due to an increase in sales-and-service investments, rising insurance costs, increased headcount and health care costs and startup expenses related to legal entity restructuring, partially offset by cost savings initiatives.

In the first quarter of 2002, we approved plans to undertake restructuring cost-saving actions. Restructuring savings were approximately $31 million and $16 million in 2003 and 2002, respectively. Most of these savings were reinvested in the business.

(thousands) |

| 2003 |

| 2002 |

| 2001 |

| |||

|

|

|

|

|

|

|

| |||

Operating income |

| $ | 482,658 |

| $ | 395,866 |

| $ | 318,179 |

|

Operating income as a percent of net sales |

| 12.8 | % | 11.6 | % | 13.7 | % | |||

Operating income for 2003 increased 22 percent over 2002. Excluding special charges in 2002 of $46 million, operating income in 2003 increased 9 percent over 2002. Adjusting for special charges, operating income in 2002 would have been 13.0 percent of net sales. The decline in 2003 operating income margins from this level reflects increased headcount and benefit costs and investments in the sales force partially offset by favorable sales volume increases and cost reduction initiatives.

Our net income was $277 million in 2003 as compared to $210 million in 2002, an increase of 32 percent. Net income in 2003 included a gain on the sale of an equity investment of $6.7 million after tax and a reduction in previously recorded restructuring expenses of $0.8 million after tax, offset by a write-off of $1.7 million of goodwill related to an international business sold in 2003. Net income in 2002 included a gain from discontinued operations of $1.9 million after tax, offset by special charges of $28.9 million after tax and a SFAS No. 142 transitional impairment charge of $4.0 million after tax. These items are of a non-recurring nature and are not necessarily indicative of future operating results. If these items are excluded from both 2003 and 2002, net income increased 13 percent for 2003. This improvement in net income reflected good fixed-rate operating income growth in our International segment, particularly in Europe. Currency translation also positively impacted net income by approximately $12 million due primarily to the strength of the euro against the U.S. dollar. The comparison of net income also benefited from a lower effective income tax rate in 2003 which was the result of cost savings initiatives, a lower overall international rate and improved international mix. Excluding the items of a non-recurring nature previously mentioned, net income for 2003 was 7.2 percent of net sales, up slightly from 7.1 percent in 2002.

2002 compared with 2001

Our consolidated net sales reached $3.4 billion for 2002, an increase of 47 percent over net sales of $2.3 billion in 2001. Business acquisitions, primarily the acquisition of the European joint venture, contributed to the overall sales growth for 2002. Excluding acquisitions, primarily the European joint venture, consolidated net sales increased 4 percent in 2002. Sales growth was experienced in most of our divisions. Changes in currency translation negatively impacted the consolidated sales growth rate by approximately 1 percentage point for 2002. Sales results reflected aggressive selling efforts, the benefits of investments in sales force training and productivity tools and new products, which were partially offset by the poor economic environment.

Our consolidated gross profit margin in 2002 decreased from 2001. Cost of sales included restructuring costs of $9.0 million for the year ended December 31, 2002. Excluding these restructuring charges, the gross profit margin would have been 50.7 percent for 2002. The gross profit margin was also negatively affected by the acquisition and consolidation of the European joint venture. The gross profit margin for 2001 on a pro forma basis (reflecting the European joint venture on a consolidated basis) was 50.2 percent. Our gross profit margin benefited from product mix improvements and cost reduction actions.

Selling, general and administrative expenses as a percent of sales for 2002 decreased when compared to 2001. The selling, general and administrative expense ratio on a pro forma basis (reflecting the consolidation of our European joint venture and the elimination of goodwill amortization) for 2001 was 37.5 percent. The increase in 2002 over the prior year pro forma expense ratio is partially due to stronger sales, which resulted in higher commissions and incentive-based compensation. This increase was partially offset by tight cost controls and savings related to restructuring activities in 2002.

During the first quarter of 2002, management approved various restructuring and other cost-saving actions, including costs to integrate our European operations, to streamline and improve our global operations. These actions resulted in pre-tax charges of approximately $51.8 million ($32.4 million after tax) in 2002. These charges were partially offset by a curtailment gain of $5.8 million ($3.5 million after tax) attributable to certain benefit plan changes. The restructuring included (i) a reduction of our global workforce during 2002, (ii) the closing of several facilities, (iii) the discontinuance of selected product lines and (iv) other actions. The expected cost savings related to restructuring activities began in 2002. Restructuring savings were approximately $16 million ($10 million after tax) in 2002. We have reinvested most of these savings in our business. Further details related to these restructuring expenses are included in Note 3 of the notes to consolidated financial statements.

Operating income for 2002 increased by 24 percent over 2001. Excluding special charges of $46 million, operating income for 2002 was 13.0 percent of net sales. This compared to 2001 pro forma operating income (reflecting the consolidation of our European joint venture and elimination of goodwill amortization) of $404 million, or 12.7 percent of net sales. This comparison of operating income margins reflects tight cost controls, savings from cost reduction initiatives and the sale of new products.

In addition to continuing operations, a legal issue related to the disposal of a business in 1992 was resolved during 2002, resulting in

23

the recognition of a gain from discontinued operations of approximately $1.9 million (net of income tax benefit of $1.1 million) or $0.01 per diluted share.

Our net income for 2002 was $210 million. Net income included restructuring charges of $32.4 million after tax, a curtailment gain of $3.5 million after tax, a gain from discontinued operations of $1.9 million after tax and a SFAS No. 142 transitional impairment charge of $4.0 million after tax. Excluding these items, our net income for 2002 increased 28 percent over net income of $188 million in 2001. This improvement reflected good operating income growth in most of our divisions, the additional operating income generated by the acquisition of the European joint venture and the elimination of goodwill amortization. This was partially offset by higher net interest expense due to increased borrowings primarily to finance our acquisition of the European joint venture. Currency translation benefited diluted net income by $0.01 per share for 2002. As a percentage of net sales, net income for 2002 was 6.2 percent. Excluding the items of a nonrecurring nature previously mentioned, net income for 2002 was 7.1 percent of net sales, down from 8.1 percent in 2001 due to the addition of the European joint venture.

OPERATING SEGMENT PERFORMANCE

Our operating segments have similar products and services and we are organized to manage our operations geographically. Our operating segments have been aggregated into three reportable segments: United States Cleaning & Sanitizing, United States Other Services, and International Cleaning & Sanitizing. We evaluate the performance of our International operations based on fixed management rates of currency exchange. Therefore, International sales and operating income totals, as well as the International financial information included in this financial discussion, are based on translation into U.S. dollars at the fixed currency exchange rates used by management for 2003. All other accounting policies of the reportable segments are consistent with accounting principles generally accepted in the United States of America and the accounting policies of the company described in Note 2 of the notes to consolidated financial statements. Additional information about our reportable segments is included in Note 16 of the notes to consolidated financial statements.

Sales by Operating Segment

(thousands) |

| 2003 |

| 2002 |

| 2001 |

| |||

|

|

|

|

|

|

|

| |||

Net sales |

|

|

|

|

|

|

| |||

United States |

|

|

|

|

|

|

| |||

Cleaning & Sanitizing |

| $ | 1,694,323 |

| $ | 1,615,171 |

| $ | 1,548,882 |

|

Other Services |

| 320,444 |

| 308,329 |

| 273,020 |

| |||

Total United States |

| 2,014,767 |

| 1,923,500 |

| 1,821,902 |

| |||

International Cleaning & Sanitizing |

| 1,560,557 |

| 1,497,935 |

| 474,089 |

| |||

Total |

| 3,575,324 |

| 3,421,435 |

| 2,295,991 |

| |||

Effect of foreign currency translation |

| 186,495 |

| (17,850 | ) | 24,719 |

| |||

Consolidated |

| $ | 3,761,819 |

| $ | 3,403,585 |

| $ | 2,320,710 |

|

The following chart presents the comparative percentage change in net sales for each of our operating segments for 2003 and 2002 (excluding Europe in 2002). European operations have been excluded in the percent change for 2002 since they were consolidated for the first time in 2002, making the percentage comparison not meaningful.

Sales Growth Information

|

| Percent Change from Prior Year |

| ||

|

| 2003 |

| 2002 |

|

|

|

|

|

|

|

Net sales |

|

|

|

|

|

United States Cleaning & Sanitizing |

|

|

|

|

|

Institutional |

| 5 | % | 6 | % |

Kay |

| 12 |

| 9 |

|

Textile Care |

| (10 | ) | 3 |

|

Professional Products |

| 9 |

| (4 | ) |

Water Care Services |

| 4 |

| (3 | ) |

Vehicle Care |

| 4 |

| 3 |

|

Food & Beverage |

| 3 |

| 1 |

|

Total United States Cleaning & Sanitizing |

| 5 | % | 4 | % |

United States Other Services |

|

|

|

|

|

Pest Elimination |

| 11 | % | 7 | % |

GCS Service |

| (7 | ) | 19 |

|

Total United States Other Services |

| 4 | % | 13 | % |

Total United States |

| 5 | % | 6 | % |

International Cleaning & Sanitizing |

|

|

|

|

|

Europe |

| 4 | % | — | % |

Asia Pacific |

| 3 |

| 2 |

|

Latin America |

| 7 |

| 9 |

|

Canada |

| 4 |

| 8 |

|

Other |

| 21 |

| 25 |

|

Total International Cleaning & Sanitizing (excluding Europe in 2002) |

| 4 | % | 7 | % |

Consolidated (excluding Europe in 2002) |

| 11 | % | 5 | % |

Sales of our United States Cleaning & Sanitizing operations were $1.7 billion in 2003 and increased 5 percent over net sales of $1.6 billion in 2002. Business acquisitions had no effect on the growth in sales for 2003. Sales benefited from good growth in our Kay and Professional Products operations, which were partially offset by lower sales in Textile Care. The increase in our Institutional division reflected its continued efforts to generate new accounts, the successful introduction of new products and improved customer service. Trends in the foodservice, hospitality and healthcare industries were challenging in early 2003 but showed signs of improvement late in the year. Kay's sales increase reflects solid growth in its food retail services business and to quickservice restaurants as well as through the introduction of new products and programs. Textile Care sales decreased, particularly to distributors, due

24

to soft industry demand and strong competition within the industry. Textile Care is focusing on improving its service and reestablishing its relationships with distributors in an effort to increase sales growth. Textile Care is also continuing to take a selective approach to new customers to ensure they meet our profit guidelines. Sales of Professional Products increased due to strong gains in the healthcare market offsetting the continuing phase-out of the specialty business. Our introduction of the first solid-based product offering to the acute care market in the second quarter of 2003 helped drive the sales growth in the healthcare market. Professional Products’ janitorial sales were also positively impacted in 2003 by a long-term supply agreement that began in December 2002. Effective January 2004, our Professional Products division was reorganized to better serve janitorial and healthcare customers by splitting the Professional Products division into two divisions, Professional Products and Healthcare. Our Food & Beverage sales were driven by improved retention and corporate account growth in the dairy, soft drink, meat and poultry and food markets. This increase was partially offset by a decrease in agricultural sales due to overall market weakness. Water Care Services had good growth in sales to the food and beverage, hospitality, healthcare and commercial accounts due to solid gains in new customer accounts. Vehicle Care sales were again driven by new business with major oil companies and successful new product introductions.

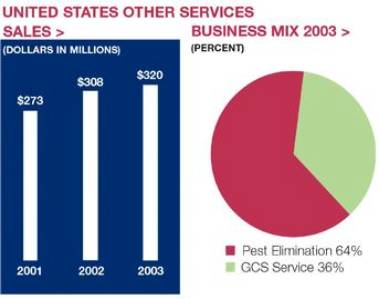

Sales of our United States Other Services operations increased 4 percent to $320 million in 2003, from $308 million in 2002. Business acquisitions had no effect on the growth in sales for 2003. Pest Elimination’s sales in 2003 reflected strong growth in both contract sales, due to the addition of new large accounts, and non-contract services, due to the aggressive efforts of the sales force. GCS Service sales decreased in 2003 due to service interruptions caused by the restructuring of field operations and the transition to a new centralized administration center, which began operation in 2003. In an effort to increase sales going forward, GCS Service implemented productivity improvement measures in the fourth quarter of 2003.

Management rate sales for our International Cleaning & Sanitizing segment were $1.6 billion for 2003, an increase of 4 percent over sales in 2002. Excluding the effects of acquisitions and divestitures, sales increased 3 percent. Sales in Europe, excluding the effects of acquisitions and divestitures, increased 2 percent. Successful new housekeeping and Ecotemp programs were partially offset by a weak European economy and strong competition. We are focusing on expanding our Pest Elimination business in Europe through acquisitions such as the Terminix operations in the United Kingdom, which was purchased in December 2002, and Nigiko with operations in France, acquired in January 2004. We expect to leverage the success of this business in the United States to become a global provider of pest elimination services. The increase in Asia Pacific was driven by Japan, New Zealand and Northeast Asia. In Japan, sales to chain restaurants and resort hotel customers improved and New Zealand is showing strong growth in its pest elimination services business. In Northeast Asia, Korea's growth was propelled by strong Institutional sales while China experienced excellent growth in its Food & Beverage sales. Good growth in these areas was partially offset by a sales decline in Australia due to soft Food & Beverage and Water Care business. Sales in Latin America, excluding acquisitions, grew 6 percent in 2003 and most Latin America countries experienced good growth except Venezuela, where a country-wide strike at the beginning of 2003 resulted in virtually no sales for the first two fiscal months of 2003. Mexico, the Caribbean and Central America all had double-digit sales growth in 2003. Growth in Latin America is being fueled by good growth in food retail programs, a demand for improved sanitation and expansion of pest elimination services. Sales in Canada increased due to continued focus on obtaining new customers and selling additional solutions to existing customers, partially offset by the impact of the Severe Acute Respiratory Syndrome (SARS) outbreak in Canada.

25

Operating Income by Operating Segment

(thousands) |

| 2003 |

| 2002 |

| 2001 |

| |||

|

|

|

|

|

|

|

| |||

Operating income |

|

|

|

|

|

|

| |||

United States |

|

|

|

|

|

|

| |||

Cleaning & Sanitizing |

| $ | 285,212 |

| $ | 271,838 |

| $ | 246,936 |

|

Other Services |

| 21,031 |

| 33,051 |

| 29,338 |

| |||

Total United States |

| 306,243 |

| 304,889 |

| 276,274 |

| |||

International Cleaning & Sanitizing |

| 159,866 |

| 138,373 |

| 44,575 |

| |||

Total |

| 466,109 |

| 443,262 |

| 320,849 |

| |||

Corporate |

| (4,834 | ) | (46,008 | ) | (4,938 | ) | |||

Effect of foreign currency translation |

| 21,383 |

| (1,388 | ) | 2,268 |

| |||

Consolidated |

| $ | 482,658 |

| $ | 395,866 |

| $ | 318,179 |

|

|

|

|

|

|

|

|

| |||

Operating income as a percent of net sales |

|

|

|

|

|

|

| |||

United States |

|

|

|

|

|

|

| |||

Cleaning & Sanitizing |

| 16.8 | % | 16.8 | % | 15.9 | % | |||

Other Services |

| 6.6 |

| 10.7 |

| 10.7 |

| |||

Total |

| 15.2 |

| 15.9 |

| 15.2 |

| |||

International Cleaning & Sanitizing |

| 10.2 |

| 9.2 |

| 9.4 |

| |||

Consolidated |

| 12.8 | % | 11.6 | % | 13.7 | % | |||

Operating income of our United States Cleaning & Sanitizing operations increased 5 percent in 2003. Operating income as a percent of sales remained the same in 2003 as 2002 due to the investments in developing the sales force and higher operating costs being offset by cost savings initiatives. We added 100 sales-and-service associates to our United States Cleaning & Sanitizing operations during 2003.

Operating income of United States Other Services operations decreased 36 percent. As a percentage of net sales, operating income decreased significantly as well. Pest Elimination had strong operating income growth, while GCS Service results reflected an operating loss. Strong growth in both contract and non-contract services, coupled with tight expense control, has helped fuel Pest Elimination’s growth. GCS Service results reflected an operating loss due to a decrease in sales resulting from operational issues encountered with a transition to a centralized administration center and the related costs invested in this initiative. This lost revenue adversely impacted operating income due to the relatively fixed nature of GCS Service’s expenses. During 2003, we added 95 sales-and-service associates to our United States Other Services operations.

Operating income of our International Cleaning & Sanitizing operations rose 16 percent in 2003 at management rates. Excluding the effects of acquisitions and divestitures, operating income increased 13 percent. Our international operating income margin also increased in 2003 over 2002. Operating income as a percent of net sales excluding acquisitions and divestitures was 10.7 in 2003 versus 9.7 in 2002. This result was due to good operating income growth and margin improvement in our European, Asia Pacific and Canadian businesses. Operating income growth was also good in Latin America. The primary reason for these significant improvements was due to the successful introduction of new products and programs as well as careful cost management. We added 80 sales-and-service associates to our International Cleaning & Sanitizing operations during 2003.

Operating income margins of our International operations are less than those realized for our U.S. operations. The lower International margins are due to (i) higher costs of importing raw materials and finished goods, (ii) the additional costs caused by the difference in scale of International operations where many operating locations are smaller in size and (iii) the additional cost of operating in numerous and diverse foreign jurisdictions. Proportionately larger investments in sales, technical support and administrative personnel are also necessary in order to facilitate the growth of our International operations.

2002 compared with 2001

Sales of our United States Cleaning & Sanitizing operations were $1.6 billion in 2002 and increased 4 percent over net sales of $1.5 billion in 2001. Business acquisitions had no effect on the growth in sales for 2002. Sales benefited from good growth in sales of U.S. Institutional and Kay operations. U.S. Institutional operations sales growth during 2002 reflected good growth driven primarily by the non-travel portion of the business. Trends in sales to the travel-related business also showed improvement over the course of 2002. Sales of Kay’s U.S. operations increased over 2001 with strong growth in both its food retail business and sales to the quickservice market. Textile Care sales increased from 2001 due to increased sales to existing customers as well as sales to new customers. Professional Products sales decreased in 2002 due to both a decline in the core sales of the Janitorial market and a decrease in the non-core specialty business reflecting a planned restructuring of the JaniSource business. Professional Products’ sales, however, were positively impacted at the end of 2002 due to a long-term supply agreement that became effective in December 2002. Water Care Services sales decreased from 2001 due to customer cost cutting and consolidations. Water Care also continued to exit non-core markets. Vehicle Care sales growth for 2002 was primarily due to new business with major oil companies as well as new product introductions. Food & Beverage sales increased slightly from 2001 with good growth in sales to the dairy, beverage and meat & poultry markets which were partially offset by weak agricultural sales.

Sales of United States Other Services operations increased 13 percent to $308 million in 2002, from $273 million in 2001. Excluding the effects of business acquisitions, sales increased 4 percent for 2002. Pest Elimination’s sales in 2002 included strong growth in non-contract services, and were partially offset by a slowdown in the growth of contract services. GCS Service sales growth increased over 2001, reflecting the continued expansion of its operations through acquisitions and a focus on integrating past acquisitions. Excluding the effects of businesses acquired, GCS Service sales decreased 1 percent for 2002. The results reflected the division’s focus on standardizing operating procedures and the impact of the hospitality slowdown on the GCS business. United States Other Services also includes modest sales from the addition of EcoSure operations in January 2002.

Management rate-based sales of our International Cleaning & Sanitizing operations reached $1.5 billion for 2002, an increase of 216 percent over sales of $0.5 billion in 2001. International Cleaning & Sanitizing includes European sales of $1.0 billion for 2002. Prior to 2002, we included the results of our former European joint venture operations in our financial statements using the equity method of accounting. Excluding Europe’s sales, International Cleaning & Sanitizing sales growth was 7 percent for 2002. Excluding all business acquisitions and divestitures, sales also increased 7 percent in 2002. European sales, although not consolidated prior to 2002, increased 8 percent over 2001 due to good growth in sales to the food and beverage markets and European acquisitions. For the Asia Pacific region, Japan, New Zealand

26

and China showed good sales growth for the year while Australia’s sales declined due to the sale of its Hygiene Services business. Asia Pacific’s sales increased 3 percent in 2002, excluding business acquisitions and divestitures. The increase in Asia Pacific sales was primarily from the institutional and food and beverage markets. Latin America sales increased 7 percent in 2002, excluding business acquisitions, with good growth in all countries except Venezuela due to the economic impact of the devaluation of its currency. Sales in Canada increased over the prior year due to good growth in sales to the institutional market.

Operating income of our United States Cleaning & Sanitizing operations was $272 million in 2002, an increase of 10 percent from operating income of $247 million in 2001. As a percentage of net sales, operating income increased from 15.9 percent in 2001 to 16.8 percent in 2002. The improvement in reported operating income margins reflected tight cost controls, savings from cost reduction initiatives, the sale of new products and the impact of adopting SFAS No. 142. Operating income in 2001 does not reflect the effect of SFAS No. 142, and thus includes amortization expenses related to goodwill of $10.6 million. If the provisions of SFAS No. 142 had been applied retroactively to January 1, 2001, operating income for our United States Cleaning & Sanitizing operations would have increased 6 percent and the operating income margin for our U.S. Cleaning & Sanitizing operations would have been 16.6 percent for 2001. We added 105 sales-and-service associates to our United States Cleaning & Sanitizing operations during 2002.

Operating income of our United States Other Services operations increased 13 percent to $33 million in 2002. The operating income margin for United States Other Services was 10.7 percent for both 2002 and 2001. Operating income in 2001 does not reflect the effect of SFAS No. 142 and includes $1.9 million of amortization expense related to goodwill. Excluding acquisitions and the effects of SFAS No. 142, operating income increased 3 percent over 2001. Excluding acquisitions and including the pro forma effects of SFAS No. 142 on 2001, the operating income margin for United States Other Services was 11.4 percent for both 2002 and 2001. Pest Elimination had strong operating income growth due to increased productivity and cost controls. Operating income for GCS Service declined due to investments in the division’s infrastructure and systems. During 2002, we added 75 sales-and-service associates to our United States Other Services operations.

Operating income of our International Cleaning & Sanitizing operations rose 210 percent to $138 million in 2002 from operating income of $45 million in 2001. The International operating income margin decreased from 9.4 percent in 2001 to 9.2 percent in 2002. Operating income in 2001 does not reflect the effect of SFAS No. 142 and includes $5.3 million of amortization expense related to goodwill. Excluding acquisitions and including the pro forma effects of SFAS No. 142 on 2001, operating income increased 15 percent over 2001. Excluding acquisitions (primarily Europe) and including the pro forma effects on SFAS No. 142 on 2001, the operating income margin for International increased to 10.3 percent of net sales from 9.6 percent in 2001. Significant operating income growth and margin improvement from Asia Pacific, Latin America and Canada contributed to the increase. We added 510 sales-and-service associates to our International Cleaning & Sanitizing operations, including Europe, during 2002.

Henkel-Ecolab

Prior to November 30, 2001, we operated cleaning and sanitizing businesses in Europe through a 50 percent economic interest in the Henkel-Ecolab joint venture. On November 30, 2001, we purchased from Henkel KGaA the remaining 50 percent interest of Henkel-Ecolab that we did not already own. Additional details related to this purchase are included in Note 5 of the notes to consolidated financial statements.

We consolidated Henkel-Ecolab’s operations effective with the November 30,2001 acquisition date and the end of Henkel-Ecolab’s fiscal year for 2001. Because we consolidate our International operations on the basis of their November 30 fiscal year ends, Henkel-Ecolab’s balance sheet was consolidated with our balance sheet as of year-end 2001. The income statement for the European operations was consolidated with our operations beginning in 2002.

Corporate

Our corporate operating expenses totaled $4.8 million in 2003, compared with $46.0 million in 2002 and $4.9 million in 2001.

Corporate operating expense in 2003 included a write-off of $1.7 million of goodwill related to an International business sold in 2003, $1.4 million of income for reductions in restructuring accruals and $4.5 million of expense for postretirement death benefits for retired executives. In 2002, the amount in corporate operating expense included restructuring and merger integration costs of $51.8 million, which were partially offset by a curtailment gain of $5.8 million related to benefit plan changes. Prior to 2002, corporate operating expense included overhead costs directly related to the European joint venture. In 2002 and 2003, these expenses were included in our International Cleaning & Sanitizing operating segment.

Interest and Income Taxes

Net interest expense for 2003 was $45 million, an increase of 3 percent over net interest expense of $44 million in 2002. The increase was primarily due to our euro-denominated debt and the strength of the euro against the U.S. dollar partially offset by lower debt levels.

Net interest expense of $44 million for 2002 increased 54 percent over net interest expense of $28 million in 2001. This increase was primarily due to higher debt levels incurred at year-end 2001 to finance the acquisition of the remaining 50 percent interest of our European joint venture which we did not already own.

Our effective income tax rate was 38.1 percent for 2003, compared with effective income tax rates of 39.8 percent and 40.5 percent in 2002 and 2001, respectively. Excluding the effects of the gain on the sale of an equity investment and the effect of special charges, the effective income tax rate was 38.0 percent for 2003. Excluding the effects of special charges in 2002, the estimated annual effective income tax rate was 39.5 percent. The reduction in the 2003 effective income tax rate was primarily due to a lower overall international rate and favorable international mix, as well as the tax savings opportunities that were available after the company’s acquisition of its European operations at the end of fiscal year 2001. The decrease in 2002 from prior years was principally due to the adoption of SFAS No. 142 at the beginning of 2002, which eliminated the amortization of goodwill and related income tax effects. Overall effective rates on International operations were higher in 2002 than in prior years, principally due to the addition of the European joint venture. This was partially offset by lower state income tax rates in 2002.

27

FINANCIAL POSITION

Our debt continued to be rated within the “A” categories by the major rating agencies during 2003. Significant changes in our financial position during 2003 and 2002 included the following:

• Total assets reached $3.2 billion at December 31, 2003, an increase of 13 percent over total assets of $2.9 billion at year-end 2002. Approximately $290 million of this increase was related to the strengthening of foreign currencies, primarily the euro. For example, 87 percent of the increase in accounts receivable was related to currency. The increase in goodwill in 2003 over 2002 was almost entirely related to currency. Other assets also increased significantly in 2003 due to a $75 million contribution to fund our U.S. pension plan.

In the liability section of the balance sheet, short-term debt was down significantly due to strong operating cash flow, which allowed us to pay down approximately $94 million of our short-term debt. Income taxes payable increased in 2003 over 2002 due to higher current income tax expense for 2003 as compared to 2002 and lower income tax payments made during the year compared to the prior year. Long-term debt also increased in 2003 due to currency as a large portion of our debt is denominated in euros.

During 2002 total assets increased to $2.9 billion from $2.5 billion at year-end 2001. Accounts receivable increased 8 percent over year end 2001, primarily due to the effect of business acquisitions during 2002, as well as due to the effect of exchange rates. Other assets also increased significantly from year-end 2001 due to payments totaling approximately $125 million to fund our U.S. pension plan during 2002. Other current liabilities increased from year-end 2001 primarily due to an increase in restructuring accruals and due to the effect of exchange rates.

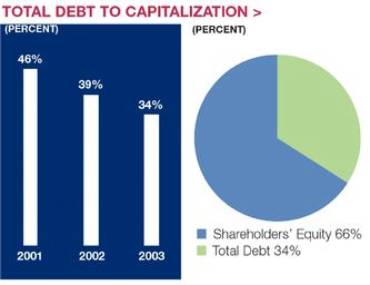

• Total debt was $675 million at December 31, 2003 and decreased from total debt of $700 million at year-end 2002. This decrease in total debt during 2003 was principally due to debt repayments made during the year, which were partially offset by the increase in debt due to the strengthening of foreign currencies, primarily the euro, during 2003. As of December 31,2003 the ratio of total debt to capitalization was 34 percent, down from 39 percent at year-end 2002 and 46 percent at year-end 2001. The lower debt to capitalization rate in 2003 and 2002 was due to debt repayments made during those years and increasing shareholders’ equity levels.

CASH FLOWS

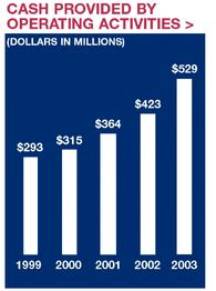

Cash provided by operating activities reached a new record high of $529 million for 2003, an increase from $423 million in 2002 and $364 million in 2001. The operating cash flow for 2003 increased over 2002 due to higher sales in 2003 and a lower contribution to the pension plan compared to 2002. Operating cash flows for 2003 were also higher than 2002 due to reduced payments on restructuring liabilities and lower estimated tax payments due to tax benefits on options exercised during 2003. The increase in operating cash flows for 2002 over 2001 reflected the additional cash flows from businesses acquired, primarily the European joint venture, as well as the improvement in accounts receivable and days sales outstanding. Historically, we have had strong operating cash flows and we anticipate this will continue. We expect to continue to use this cash flow to acquire new businesses, repurchase our common stock, invest in merchandising equipment and other capital assets and pay down debt.

Cash flows used for investing activities included capital expenditures of $212 million in 2003, $213 million in 2002 and $158 million in 2001. Worldwide additions of merchandising equipment, primarily cleaning and sanitizing product dispensers, accounted for approximately 70 percent of each year’s capital expenditures. Merchandising equipment is depreciated over 3 to 7 year lives. Cash used for businesses acquired included Adams Healthcare in 2003, Terminix Ltd. and Kleencare Hygiene in 2002 and Henkel-Ecolab in 2001.

Financing cash flow activity included cash used to reacquire shares and pay dividends and cash provided and used through our debt arrangements. Share repurchases totaled $227 million in 2003, $9 million in 2002 and $32 million in 2001. These repurchases were funded with operating cash flows and cash from the exercise of employee stock options. In October 2003, we announced a new authorization to repurchase up to 10 million additional shares of Ecolab common stock for the purpose of offsetting the dilutive effect of shares issued for stock option exercises and incentives and general corporate purposes.

In 2003, we increased our annual dividend rate for the twelfth consecutive year. We have paid dividends on our common stock for 67 consecutive years. Cash dividends declared per share of common stock, by quarter, for each of the last three years were as follows:

|

| First |

| Second |

| Third |

| Fourth |

| Year |

| |||||

|

|

|

|

|

|

|

|

|

|

|

| |||||

2003 |

| $ | 0.0725 |

| $ | 0.0725 |

| $ | 0.0725 |

| $ | 0.0800 |

| $ | 0.2975 |

|

2002 |

| 0.0675 |

| 0.0675 |

| 0.0675 |

| 0.0725 |

| 0.2750 |

| |||||

2001 |

| 0.0650 |

| 0.0650 |

| 0.0650 |

| 0.0675 |

| 0.2625 |

| |||||

28

LIQUIDITY AND CAPITAL RESOURCES

We currently expect to fund all of the requirements which are reasonably foreseeable for 2004, including new program investments, scheduled debt repayments, dividend payments, possible acquisitions and share repurchases from operating activities, cash reserves and short-term borrowings. In the event of a significant acquisition, funding may occur through additional long-term borrowings. Cash provided by operating activities reached an all time high of $529 million in 2003. While cash flows could be negatively affected by a decrease in revenues, we do not believe that our revenues are highly susceptible, over the short run, to rapid changes in technology within our industry. We have a $450 million U.S. commercial paper program and a 200 million Australian dollar commercial paper program. In June 2003, we established a $200 million European commercial paper program to provide a source of funding for our European and other international acquisitions and working capital requirements. All three programs are rated A-1 by Standard & Poor’s and P-1 by Moody’s. To support our commercial paper programs and other general business funding needs, we maintain a $275 million multi-year committed credit agreement which expires in December 2005 and a $175 million 364 day credit facility which expires in October 2004. We can draw directly on both credit facilities on a revolving credit basis. As of December 31, 2003, approximately $36 million of these credit facilities were committed to support outstanding commercial paper, leaving $414 million available for other uses. In January 2004, we issued 85 million euro (approximately $109 million at the date of the transaction) of commercial paper primarily to finance acquisitions subsequent to year-end. In addition, we have other committed and uncommitted credit lines of approximately $200 million with major international banks and financial institutions to support our general funding needs. Additional details on our credit facilities are included in Note 7 of the notes to consolidated financial statements.

During 2003, we voluntarily contributed $75 million to our U.S. pension plan. In making this contribution, we considered the normal growth in accrued plan benefits, the impact of lower year-end discount rates on the plan liability, our intent to improve the projected benefit obligation funding ratio and the 29 percent actual asset return on our pension plan in 2003. Our contributions to the pension plan did not have a material effect on our consolidated results of operations, financial condition or liquidity. We do not expect expense for our U.S. pension plan to increase significantly for 2004.

As described further in Note 5 of the consolidated financial statements, Henkel KGaA owns 28.2 percent of our common stock outstanding at December 31, 2003. In a December 2003 filing, Henkel reported that it may sell a portion or all of its holdings of Ecolab common stock and/or its holdings of common stock of The Clorox Company, or a combination of both, in connection with refinancing their pending acquisition of The Dial Corporation. Any dispositions by Henkel of any shares of Ecolab common stock would be done in accordance with the stockholder’s agreement between Henkel and Ecolab, including our right of first refusal, and applicable law.

We do not have relationships with unconsolidated entities or financial partnerships, such as entities often referred to as “structured finance” or “special purposes entities”, which are sometimes established for the purpose of facilitating off-balance sheet financial arrangements or other contractually narrow or limited purposes. As such, we are not exposed to any financing, liquidity, market or credit risk that could arise if we had engaged in such relationships.

A schedule of our obligations under various long-term debt agreements and operating leases with noncancelable terms in excess of one year are summarized in the following table:

(thousands) |

| Payments due by Period |

| |||||||||||||

Contractual obligations |

| Total |

| Less |

| 1-3 |

| 3-5 |

| More |

| |||||

Long-term debt |

| $ | 608,394 |

| $ | 3,953 |

| $ | 82,135 |

| $ | 367,021 |

| $ | 155,285 |

|

Operating leases |

| 138,525 |

| 35,726 |

| 51,136 |

| 29,392 |

| 22,271 |

| |||||

Total contractual cash obligations |

| $ | 746,919 |

| $ | 39,679 |

| $ | 133,271 |

| $ | 396,413 |

| $ | 177,556 |

|

We lease sales and administrative office facilities, distribution center facilities, computers and other equipment under longer-term operating leases. Vehicle leases are generally shorter in duration. The U.S. vehicle leases have guaranteed residual value requirements that have historically been satisfied by the proceeds on the sale of the vehicles. No amounts have been recorded for these guarantees in the table above as we believe that the potential recovery of value from the vehicles when sold will be greater than the residual value guarantee.

We do not have significant unconditional purchase obligations, or significant other commercial commitments, such as commitments under lines of credit, standby letters of credit, guarantees, standby repurchase obligations or other commercial commitments.

We are in compliance with all covenants and other requirements of our credit agreements and indentures. Additionally, we do not have any rating triggers that would accelerate the maturity dates of our debt.

A downgrade in our credit rating could limit or preclude our ability to issue commercial paper under our current programs. A credit rating downgrade could also adversely affect our ability to renew existing, or negotiate new credit facilities in the future and could increase the cost of these facilities. Should this occur, we could seek additional sources of funding, including issuing term notes or bonds. In addition, we have the ability at our option to draw upon our $450 million committed credit facilities prior to their termination.

MARKET RISK

We enter into contractual arrangements (derivatives) in the ordinary course of business to manage foreign currency exposure and interest rate risks. We do not enter into derivatives for trading purposes. Our use of derivatives is subject to internal policies that provide guidelines for control, counterparty risk and ongoing monitoring and reporting and is designed to reduce the volatility associated with movements in foreign exchange and interest rates on our income statement.

We enter into forward contracts, swaps and foreign currency options to hedge certain intercompany financial arrangements, and to hedge against the effect of exchange rate fluctuations on transactions related to cash flows and net investments denominated in currencies other than U.S. dollars. At December 31, 2003, we had approximately $239 million of foreign currency forward exchange contracts with face amounts denominated primarily in euros.

We manage interest expense using a mix of fixed and floating rate debt. To help manage borrowing costs, we may enter into interest rate swap agreements. Under these arrangements, we agree to exchange, at specified intervals, the difference between fixed and floating interest amounts calculated by reference to an agreed-upon notional principal amount. At year-end 2003, we had an interest rate swap that converts approximately euro 78 million (approximately $94 million U.S. dollars) of our Euronote debt from a fixed interest rate to a floating or variable

29

interest rate. This swap agreement is effective until February 2007. We also have an interest rate swap agreement on 50 million Australian dollars (approximately $36 million U.S. dollars) of Australian floating rate debt. This agreement is effective through November 2004 and has a fixed annual pay rate of approximately 6 percent. In September 2003, we entered into an interest rate swap agreement that converts $30 million of the 7.19% senior notes from a fixed interest rate to a floating or variable interest rate. This agreement is effective until January 2006.

Based on a sensitivity analysis (assuming a 10 percent adverse change in market rates) of our foreign exchange and interest rate derivatives and other financial instruments, changes in exchange rates or interest rates would not materially affect our financial position and liquidity. The effect on our results of operations would be substantially offset by the impact of the hedged items.

SUBSEQUENT EVENTS

In January 2004, we acquired Nigiko, a Paris-based provider of commercial pest elimination services throughout France. Nigiko pest elimination has annual sales of approximately $55 million. These operations will become part of our International Cleaning & Sanitizing operations in 2004.

In February 2004, we acquired Daydots International, a Texas-based provider of food safety products. Daydots has annual sales of approximately $22 million. These operations will become part of our U.S. Cleaning & Sanitizing operations in 2004.

FORWARD-LOOKING STATEMENTS AND RISK FACTORS

This financial discussion and other portions of this Annual Report to Shareholders contain various “Forward-Looking Statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These include expectations concerning business progress and expansion, business acquisitions, currency translation, cash flows, debt repayments, susceptibility to changes in technology, global economic conditions and liquidity requirements. These statements, which represent our expectations or beliefs concerning various future events, are based on current expectations. Therefore, they involve a number of risks and uncertainties that could cause actual results to differ materially from those of such Forward-Looking Statements. These risks and uncertainties include the vitality of the foodservice, hospitality and travel industries; restraints on pricing flexibility due to competitive factors and customer and vendor consolidations; changes in oil or raw material prices or unavailability of adequate and reasonably priced raw materials; the occurrence of capacity constraints or the loss of a key supplier; the effect of future acquisitions or divestitures or other corporate transactions; our ability to achieve plans for past acquisitions; the costs and effects of complying with: (i) laws and regulations relating to the environment and to the manufacture, storage, distribution, efficacy and labeling of our products and (ii) changes in tax, fiscal, governmental and other regulatory policies; economic factors such as the worldwide economy, interest rates and currency movements, including, in particular, our exposure to foreign currency risk; the occurrence of (a) litigation or claims, (b) the loss or insolvency of a major customer or distributor, (c) war, (d) natural or manmade disasters (including acts of terrorism or hostilities which impact our markets) and, (e) severe weather conditions or public health epidemics affecting the foodservice, hospitality and travel industries; loss of, or changes in, executive management; our ability to continue product introductions and technological innovations; and other uncertainties or risks reported from time-to-time in our reports to the Securities and Exchange Commission. In addition, we note that our stock price can be affected by fluctuations in quarterly earnings. There can be no assurances that our earnings levels will meet investors’ expectations. We undertake no duty to update our Forward-Looking Statements.

30

consolidated statement of income

Year ended December 31 (thousands, except per share) |

| 2003 |

| 2002 |

| 2001 |

| |||

|

|

|

|

|

|

|

| |||

Net sales |

| $ | 3,761,819 |

| $ | 3,403,585 |

| $ | 2,320,710 |

|

Operating expenses |

|

|

|

|

|

|

| |||

Cost of sales (including special charges (income) of ($76) in 2003, $8,977 in 2002 and ($566) in 2001) |

| 1,845,202 |

| 1,687,597 |

| 1,120,254 |

| |||

Selling, general and administrative expenses |

| 1,433,551 |

| 1,283,091 |

| 881,453 |

| |||

Special charges |

| 408 |

| 37,031 |

| 824 |

| |||

Operating income |

| 482,658 |

| 395,866 |

| 318,179 |

| |||

Gain on sale of equity investment |

| 11,105 |

|

|

|

|

| |||

Interest expense, net |

| 45,345 |

| 43,895 |

| 28,434 |

| |||

Income from continuing operations before income taxes and equity in earnings of Henkel-Ecolab |

| 448,418 |

| 351,971 |

| 289,745 |

| |||

Provision for income taxes |

| 171,070 |

| 140,081 |

| 117,408 |

| |||

Equity in earnings of Henkel-Ecolab |

|

|

|

|

| 15,833 |

| |||

Income from continuing operations before cumulative effect of change in accounting |

| 277,348 |

| 211,890 |

| 188,170 |

| |||

Cumulative effect of change in accounting |

|

|

| (4,002 | ) |

|

| |||

Gain from discontinued operations |

|

|

| 1,882 |

|

|

| |||

Net income |

| $ | 277,348 |

| $ | 209,770 |

| $ | 188,170 |

|

|

|

|

|

|

|

|

| |||

Basic income per common share |

|

|

|

|

|

|

| |||

Income from continuing operations before change in accounting |

| $ | 1.07 |

| $ | 0.82 |

| $ | 0.74 |

|

Change in accounting |

|

|

| (0.02 | ) |

|

| |||

Gain from discontinued operations |

|

|

| 0.01 |

|

|

| |||

Net income |

| $ | 1.07 |

| $ | 0.81 |

| $ | 0.74 |

|

Diluted income per common share |

|

|

|

|

|

|

| |||

Income from continuing operations before change in accounting |

| $ | 1.06 |

| $ | 0.81 |

| $ | 0.72 |

|

Change in accounting |

|

|

| (0.02 | ) |

|

| |||

Gain from discontinued operations |

|

|

| 0.01 |

|

|

| |||

Net income |

| $ | 1.06 |

| $ | 0.80 |

| $ | 0.72 |

|

|

|

|

|

|

|

|

| |||

Weighted-average common shares outstanding |

|

|

|

|

|

|

| |||

Basic |

| 259,454 |

| 258,147 |

| 254,832 |

| |||

Diluted |

| 262,737 |

| 261,574 |

| 259,855 |

| |||

The accompanying notes are an integral part of the consolidated financial statements.

31

consolidated balance sheet

December 31 (thousands, except per share) |

| 2003 |

| 2002 |

| 2001 |

| |||

|

|

|

|

|

|

|

| |||

ASSETS |

|

|

|

|

|

|

| |||

Current assets |

|

|

|

|

|

|

| |||

Cash and cash equivalents |

| $ | 85,626 |

| $ | 49,205 |

| $ | 41,793 |

|

Accounts receivable, net |

| 626,002 |

| 553,154 |

| 514,074 |

| |||

Inventories |

| 309,959 |

| 291,506 |

| 279,785 |

| |||

Deferred income taxes |

| 75,820 |

| 71,147 |

| 53,781 |

| |||

Other current assets |

| 52,933 |

| 50,925 |

| 40,150 |

| |||

Total current assets |

| 1,150,340 |

| 1,015,937 |

| 929,583 |

| |||

Property, plant and equipment, net |

| 736,797 |

| 680,265 |

| 644,323 |

| |||

Goodwill, net |

| 797,211 |

| 695,700 |

| 596,925 |

| |||

Other intangible assets, net |

| 203,859 |

| 188,670 |

| 178,951 |

| |||

Other assets, net |

| 340,711 |

| 285,335 |

| 175,218 |

| |||

Total assets |

| $ | 3,228,918 |

| $ | 2,865,907 |

| $ | 2,525,000 |

|

|

|

|

|

|

|

|

| |||

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

| |||

Current liabilities |

|

|

|

|

|

|

| |||

Short-term debt |

| $ | 70,203 |

| $ | 160,099 |

| $ | 233,393 |

|

Accounts payable |

| 212,287 |

| 205,665 |

| 199,772 |

| |||

Compensation and benefits |

| 190,386 |

| 184,239 |

| 132,720 |

| |||

Income taxes |

| 59,829 |

| 12,632 |

| 18,887 |

| |||

Other current liabilities |

| 319,237 |

| 291,193 |

| 243,180 |

| |||

Total current liabilities |

| 851,942 |

| 853,828 |

| 827,952 |

| |||

Long-term debt |

| 604,441 |

| 539,743 |

| 512,280 |

| |||

Postretirement health care and pension benefits |

| 249,906 |

| 207,596 |

| 183,281 |

| |||

Other liabilities |

| 227,203 |

| 164,989 |

| 121,135 |

| |||

Shareholders’ equity (common stock, par value $1.00 per share; shares outstanding: 2003 – 257,417; 2002 – 129,940 and 2001 – 127,900) |

| 1,295,426 |

| 1,099,751 |

| 880,352 |

| |||

Total liabilities and shareholders’ equity |

| $ | 3,228,918 |

| $ | 2,865,907 |

| $ | 2,525,000 |

|

The accompanying notes are an integral part of the consolidated financial statements.

32

consolidated statement of cash flows

Year ended December 31 (thousands) |

| 2003 |

| 2002 |

| 2001 |

| |||

|

|

|

|

|

|

|

| |||

OPERATING ACTIVITIES |

|

|

|

|

|

|

| |||

Net income |

| $ | 277,348 |

| $ | 209,770 |

| $ | 188,170 |

|

Cumulative effect of change in accounting |

|

|

| 4,002 |

|

|

| |||

Gain from discontinued operations |

|

|

| (1,882 | ) |

|

| |||

Income from continuing operations |

| 277,348 |

| 211,890 |

| 188,170 |

| |||

Adjustments to reconcile income from continuing operations to cash provided by operating activities: |

|

|

|

|

|

|

| |||

Depreciation |

| 201,512 |

| 194,840 |

| 128,020 |

| |||

Amortization |

| 28,144 |

| 28,588 |

| 34,970 |

| |||

Deferred income taxes |

| 42,455 |

| 49,923 |

| (2,950 | ) | |||

Gain on sale of equity investment |

| (11,105 | ) |

|

|

|

| |||

Equity in earnings of Henkel-Ecolab |

|

|

|

|

| (15,833 | ) | |||

Henkel-Ecolab royalties and dividends |

|

|

|

|

| 23,928 |

| |||

Special charges – asset disposals |

| 1,684 |

| 6,180 |

| (566 | ) | |||

Other, net |

| 1,837 |

| 1,835 |

| (1,373 | ) | |||

Changes in operating assets and liabilities: |

|

|

|

|

|

|

| |||

Accounts receivable |

| (5,547 | ) | 78 |

| 20,570 |

| |||

Inventories |

| (2,902 | ) | (3,567 | ) | (8,014 | ) | |||

Other assets |

| (39,224 | ) | (141,926 | ) | (26,049 | ) | |||

Accounts payable |

| (13,329 | ) | (8,860 | ) | (7,451 | ) | |||

Other liabilities |

| 48,326 |

| 84,345 |

| 31,059 |

| |||

Cash provided by operating activities |

| 529,199 |

| 423,326 |

| 364,481 |

| |||

|

|

|

|

|

|

|

| |||

INVESTING ACTIVITIES |

|

|

|

|

|

|

| |||

Capital expenditures |

| (212,035 | ) | (212,757 | ) | (157,937 | ) | |||

Property disposals |

| 8,502 |

| 6,788 |

| 3,027 |

| |||

Capitalized software expenditures |

| (8,951 | ) | (4,490 | ) |

|

| |||