Exhibit 13

Financial Discussion

OVERVIEW FOR 2005

This Financial Discussion should be read in conjunction with the information on Forward-Looking Statements and Risk Factors found at the end of the Financial Discussion.

We delivered a strong financial performance in 2005, despite being faced with significant increases in our raw material costs as well as continued challenges from the European economic environment. We achieved another year of double-digit income growth, record net sales of $4.5 billion and record cash flow from operating activities of $590 million.

Effective October 1, 2005, we elected to early-adopt the provisions of Statement of Financial Accounting Standards No. 123 (Revised 2004), Share-Based Payment (“SFAS No. 123R”), the new accounting standard for expensing stock options. As part of the transition to the new standard, all prior period financial statements have been restated to recognize share-based compensation expense historically reported in the notes to our consolidated financial statements.

In the fourth quarter of 2005 we also completed the repatriation of $223 million of foreign earnings into the United States pursuant to the provisions of the American Jobs Creation Act of 2004 (“AJCA”). The AJCA provided us with the opportunity to tax efficiently repatriate foreign earnings for qualifying investments specified in our reinvestment plan. As a result of the repatriation, we recorded a tax charge of $3.1 million in the fourth quarter of 2005.

OPERATING HIGHLIGHTS

• We effectively managed rising raw material costs as well as lackluster European economies.

• We continued our disciplined acquisition strategy with the acquisition of Midland Research Laboratories, a $16 million U.S. provider of water treatment products, and two small international businesses in Ireland and Thailand.

• We expanded our MarketGuard program globally to give food retailers worldwide access to effective food safety, pest elimination and floor care solutions to achieve high standards of cleanliness and sanitation in their operations.

• We introduced our 360º of Protection program for food service and hospitality customers, which provides a customized program to address the full spectrum of cleaning and sanitizing needs.

• We unveiled full cycle solutions for commercial laundries, designed specifically to meet laundry challenges and reduce total operating costs through a combination of chemistry, service, engineering, technology and water care solutions.

• We continued to invest in our sales-and-service force, adding associates to our sales team and making investments in their training and field technology tools.

FINANCIAL PERFORMANCE

• Consolidated net sales reached an all-time high of $4.5 billion for 2005, an increase of 8 percent over net sales of $4.2 billion in 2004. Excluding acquisitions and divestitures, consolidated net sales increased 7 percent.

• Our operating income for 2005 was $542 million and increased 11 percent over 2004. Excluding acquisitions and divestitures, operating income increased 10 percent.

• Diluted net income per share was $1.23 for 2005, up 13 percent over diluted net income per share of $1.09 in 2004. The dilutive per share amounts for both 2005 and 2004 include a charge of $0.10 per share for share-based compensation expense under the provisions of SFAS No. 123R.

• We achieved record cash flow from operating activities of $590 million in 2005, which helped us fund investments in business operations, make business acquisitions and reacquire $213 million of our common stock. It also allowed us to make additional voluntary contributions of $38 million to our United States pension plan and contributions of $27 million to various international pension plans.

• We increased our annual dividend rate for the fourteenth consecutive year. The dividend was increased 14 percent in December 2005 to an annual rate of $0.40 per common share. The increase reflects our earnings progress, strong financial position and our commitment to providing superior shareholder returns.

• Our return on beginning shareholders’ equity was 20 percent in 2005, including the expense associated with employee stock options, the fourteenth consecutive year in which we achieved our long-term financial objective of a 20 percent return on beginning shareholders’ equity.

• Currency translation continued to have an impact on our financial results, adding approximately $5 million to net income in 2005 following an $11 million benefit in 2004.

• A reduction in our annual effective income tax rate from 36.4 percent in 2004 to 35.9 percent in 2005 added approximately $3 million to net income. The reduction in the 2005 effective income tax rate was primarily due to the benefits of a lower overall international rate, favorable international mix and tax planning efforts, partially offset by the tax charge related to repatriated foreign earnings under AJCA.

• We continued our long-standing debt rating within the “A” categories of the major rating agencies during 2005.

2006 EXPECTATIONS

• We plan to continue to leverage our Circle the Customer - Circle the Globe strategy through cross-selling and cross-marketing of our many divisional products and service solutions, as well as introducing new, innovative products.

• We anticipate higher raw material and freight costs will continue to impact our operating income and present a challenge in 2006.

• We will continue to make appropriate pricing decisions to reflect the value provided by our products and services and protect operating margins.

• We expect to use our strong cash flow to make strategic business acquisitions which complement our growth strategy.

• We expect currency translation to have a negative impact in 2006.

• We will work to further reduce costs by reviewing and streamlining our business operations.

21

• We plan to make further investments in our sales-and-service force by continuing to add talented people and invest in their training and field technology tools.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Our consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United States of America (U.S. GAAP). We have adopted various accounting policies to prepare the consolidated financial statements in accordance with U.S. GAAP. Our most significant accounting policies are disclosed in Note 2 of the notes to the consolidated financial statements.

Preparation of our consolidated financial statements, in conformity with U.S. GAAP, requires us to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Estimates are considered to be critical if they meet both of the following criteria: (1) the estimate requires assumptions to be made about matters that are highly uncertain at the time the accounting estimate is made, and (2) different estimates that the company reasonably could have used for the accounting estimate in the current period, or changes in the accounting estimate that are reasonably likely to occur from period to period, must have a material impact on the presentation of the company’s financial condition, changes in financial condition or results of operations.

Besides estimates that meet the “critical” estimate criteria, we make many other accounting estimates in preparing our financial statements and related disclosures. All estimates, whether or not deemed critical, affect reported amounts of assets, liabilities, revenues and expenses as well as disclosures of contingent assets and liabilities. Estimates are based on experience and other information available prior to the issuance of the financial statements. Materially different results can occur as circumstances change and additional information becomes known, even from estimates not deemed critical. Our critical accounting estimates include the following:

SHARE-BASED COMPENSATION

Effective October 1, 2005 we early-adopted SFAS No. 123R under the modified retrospective application method.

SFAS No. 123R requires us to measure compensation expense for share-based awards at fair value at the date of grant and recognize compensation expense over the service period for awards expected to vest. As part of the transition to the new standard, all prior period financial statements have been restated to recognize share-based compensation expense historically reported in the notes to the consolidated financial statements. We did not make any modifications to outstanding stock options in anticipation of adopting the new standard.

In the fourth quarter of 2005 we began using a lattice-based binomial model for valuing new stock option grants. We believe this model considers appropriate probabilities of option exercise and post-vesting termination which are more consistent with actual and projected experience, and therefore support more accurate valuation of a stock option. Upon the adoption of SFAS No. 123R we also began using the non-substantive vesting method for new grants to retirement eligible employees and started using a forfeiture estimate in the amount of compensation expense being recognized. This change from our historical practice of recognizing forfeitures as they occur did not result in the recognition of any cumulative adjustment to income.

Determining the fair value of share-based awards at the grant date requires judgment, including estimating expected volatility, exercise and post-vesting termination behavior, expected dividends and risk-free rates of return. Additionally, the expense that is recorded is dependent on the amount of share-based awards expected to be forfeited. If actual results differ significantly from these estimates, share-based compensation expense and our results of operations could be impacted. For additional information on the impact of the adoption of SFAS No. 123R, see Note 2. For additional information on our stock incentive and option plans, including significant assumptions used in determining fair value, see Note 9.

REVENUE RECOGNITION

We recognize revenue as services are performed or on product sales at the time title to the product and risk of loss transfers to the customer. Our sales policies do not provide for general rights of return and do not contain customer acceptance clauses. We record estimated reductions to revenue for customer programs and incentive offerings including pricing arrangements, promotions and other volume-based incentives at the time the sale is recorded. Depending on market conditions, we may increase customer incentive offerings, which could reduce sales and gross profit margins at the time the incentive is offered.

VALUATION ALLOWANCES AND ACCRUED LIABILITIES

We estimate sales returns and allowances by analyzing historical returns and credits, and apply these trend rates to the most recent 12 months’ sales data to calculate estimated reserves for future credits. We estimate the allowance for doubtful accounts by analyzing accounts receivable balances by age, applying historical write-off trend rates to the most recent 12 months’ sales, less actual write-offs to date. In addition, our estimates also include separately providing for 100 percent of specific customer balances when it is deemed probable that the balance is uncollectible. Actual results could differ from these estimates under different assumptions.

Estimates used to record liabilities related to pending litigation and environmental claims are based on our best estimate of probable future costs. We record the amounts that represent the points in the range of estimates that we believe are most probable or the minimum amounts when no amount within the range is a better estimate than any other amount. Potential insurance reimbursements are not anticipated in our accruals for environmental liabilities. While the final resolution of litigation and environmental contingencies could result in amounts different than current accruals, and therefore have an impact on our consolidated financial results in a future reporting period, we believe the ultimate outcome will not have a significant effect on our consolidated results of operations, financial position or cash flows.

ACTUARIALLY DETERMINED LIABILITIES

The measurement of our pension and postretirement benefit obligations are dependent on a variety of assumptions determined by management and used by our actuaries. These assumptions affect the amount and timing of future contributions and expenses.

The assumptions used in developing the required estimates include, among others, discount rate, projected salary and health care cost increases and expected return or earnings on assets. Beginning in 2005, the discount rate assumption for the U.S. Plans is determined by considering the average of bond yield curves constructed from a large population of high-quality, non-callable, corporate bond issues with maturity dates of six months to thirty years. Bond issues in the population are rated no less than Aa by Moody’s Investor Services or AA by Standard & Poors. A single equivalent discount rate reflects the matching of the plan liability cash flows to the yield curve. Prior to 2005, the discount rate assumption was based on the investment yields available at year-end on corporate long-term bonds rated AA. Projected salary and health care cost increases are based on our long-term actual experience, the near-term outlook and assumed inflation. The expected return on plan assets reflects asset allocations, investment strategies and the views of investment managers over a long-term perspective. The effects of actual results differing from our assumptions, as well as changes in assumptions, are reflected in the unrecognized actuarial loss and amortized over future periods and, therefore, generally affect our recognized expense in future periods.

22

Our unrecognized actuarial loss, on our U.S. pension plan has grown to $230 million over the last five years due primarily to the lowering of the discount rate during that period. Significant differences in actual experience or significant changes in assumptions may materially affect pension and other post-retirement obligations.

In determining our U.S. pension and postretirement obligations for 2005, our discount rates decreased from 5.75 percent at year-end 2004 to 5.57 percent while our projected salary increase was unchanged at 4.3 percent. Our expected return on plan assets used for determining 2005 expense decreased from 9.00 percent to 8.75 percent.

The effect on 2006 expense of a decrease in discount rate or expected return on assets assumption as of December 31, 2005 is shown below assuming no changes in benefit levels and no amortization of gains or losses for our major plans:

| | Effect on U.S. Pension Plan | |

| | | | Decline in | | Higher | |

(dollars in millions) | | Assumption | | Funded | | 2006 | |

Assumption | | Change | | Status | | Expense | |

| | | | | | | |

Discount rate | | -0.25 | pts | $ | 31.4 | | $ | 4.3 | |

Expected return on assets | | -0.25 | pts | N/A | | $ | 1.8 | |

| | | | | | | | | |

| | Effect on U.S. Postretirement

Health Care Benefits Plan | |

| | | | Decline in | | Higher | |

(dollars in millions) | | Assumption | | Funded | | 2006 | |

Assumption | | Change | | Status | | Expense | |

| | | | | | | |

Discount rate | | -0.25 | pts | $ | 5.0 | | $ | 0.8 | |

Expected return on assets | | -0.25 | pts | N/A | | $ | 0.1 | |

| | | | | | | | | |

See Note 14 of the notes to the consolidated financial statements for further discussion concerning our accounting policies, estimates, funded status, planned contributions and overall financial positions of our pension and post-retirement plan obligations.

We are self-insured in North America for most workers compensation, general liability and automotive liability losses, subject to per occurrence and aggregate annual liability limitations. We are insured for losses in excess of these limitations. We have recorded both a liability and an offsetting receivable for amounts in excess of these limitations. We are also self-insured for health care claims for eligible participating employees, subject to certain deductibles and limitations. We determine our liabilities for claims incurred but not reported on an actuarial basis. A change in these assumptions would cause reported results to differ.

INCOME TAXES

Judgment is required to determine the annual effective income tax rate, deferred tax assets and liabilities and any valuation allowances recorded against net deferred tax assets. Our effective income tax rate is based on annual income, statutory tax rates and tax planning opportunities available in the various jurisdictions in which we operate. We establish liabilities or reserves when we believe that certain positions are likely to be challenged by authorities and we may not succeed, despite our belief that our tax return positions are fully supportable. We adjust these reserves in light of changing facts and circumstances. Our annual effective income tax rate includes the impact of reserve provisions and changes to reserves that we consider appropriate. During interim periods, this annual rate is then applied to our year-to-date operating results. In the event that there is a significant one-time item recognized in our interim operating results, the tax attributable to that item would be separately calculated and recorded in the same period as the one-time item.

Tax regulations require items to be included in our tax returns at different times than the items are reflected in our financial statements. As a result, the effective income tax rate reflected in our financial statements differs from that reported in our tax returns. Some of these differences are permanent, such as expenses that are not deductible on our tax return, and some are temporary differences, such as depreciation expense. Temporary differences create deferred tax assets and liabilities. Deferred tax assets generally represent items that can be used as a tax deduction or credit in our tax return in future years for which we have already recorded the tax benefit in our income statement. We establish valuation allowances for our deferred tax assets when the amount of expected future taxable income is not likely to support the utilization of the deduction or credit. Deferred tax liabilities generally represent items for which we have already taken a deduction in our tax return, but have not yet recognized that tax benefit in our financial statements. Undistributed earnings of foreign subsidiaries are considered to have been reinvested indefinitely or available for distribution with foreign tax credits available to offset the amount of applicable income tax and foreign withholding taxes that might be payable on earnings. It is impractical to determine the amount of incremental taxes that might arise if all undistributed earnings were distributed.

A number of years may elapse before a particular tax matter, for which we have established a reserve, is audited and finally resolved. The number of tax years with open tax audits varies depending on the tax jurisdiction. In the United States, during 2004, the Internal Revenue Service completed their field work examination of our tax returns for 1999 through 2001. We expect the final resolution for these returns in 2006. While it is often difficult to predict the final outcome or the timing of resolution of any tax matter, we believe that our reserves reflect the probable outcome of known tax contingencies. Unfavorable settlement of any particular issue would require the use of cash. Favorable resolution could result in reduced income tax expense reported in the financial statements in the future. Our tax reserves are generally presented in the balance sheet within other non-current liabilities.

LONG-LIVED AND INTANGIBLE ASSETS

We periodically review our long-lived and intangible assets for impairment and assess whether significant events or changes in business circumstances indicate that the carrying value of the assets may not be recoverable. This could occur when the carrying amount of an asset exceeds the anticipated future undiscounted cash flows expected to result from the use of the asset and its eventual disposition. The amount of the impairment loss to be recorded, if any, is calculated as the excess of the asset’s carrying value over its estimated fair value. We also periodically reassess the estimated remaining useful lives of our long-lived assets. Changes to estimated useful lives would impact the amount of depreciation and amortization expense recorded in earnings. We have experienced no significant changes in the carrying value or estimated remaining useful lives of our long-lived assets.

We review our goodwill for impairment on an annual basis for all reporting units, including businesses reporting losses such as GCS Service. If circumstances change significantly within a reporting unit, we would test for impairment in addition to the annual test.

Goodwill and certain intangible assets are assessed for impairment using fair value measurement techniques. Specifically, goodwill impairment is determined using a two-step process. Both the first step of determining the fair value of a reporting unit and the second step of determining the fair value of individual assets and liabilities of a reporting unit (including unrecognized intangible assets) are judgmental in nature and often involve the use of significant estimates and assumptions. Estimates of fair value are primarily determined using discounted cash flows, market comparisons and recent transactions. These valuation methodologies use significant estimates and assumptions, which include projected future cash flows (including timing), discount rate reflecting the risk inherent in future cash flows, perpetual growth rate, and determination of appropriate market comparables. No impairments were recorded in 2005, 2004 or 2003 as a result of

23

the tests performed. Of the total goodwill included in our consolidated balance sheet, 20 percent is recorded in our United States Cleaning & Sanitizing reportable segment, 5 percent in our United States Other Services segment and 75 percent in our International segment.

FUNCTIONAL CURRENCIES

In preparing the consolidated financial statements, we are required to translate the financial statements of our foreign subsidiaries from thecurrency in which they keep their accounting records, generally the local currency, into United States dollars. Assets and liabilities of these operations are translated at the exchange rates in effect at each fiscal year end. The translation adjustments related to assets and liabilities that arise from the use of differing exchange rates from period to period are included in accumulated other comprehensive income (loss) in shareholders’ equity. Income statement accounts are translated at the average rates of exchange prevailing during the year. We evaluate our International operations based on fixed rates of exchange; however, the different exchange rates from period to period impact the amount of reported income from our consolidated operations.

OPERATING RESULTS

CONSOLIDATED

(thousands, except per share) | | 2005 | | 2004 | | 2003 | |

| | | | | | | |

Net sales | | $ | 4,534,832 | | $ | 4,184,933 | | $ | 3,761,819 | |

Operating income | | 542,420 | | 489,890 | | 455,009 | |

Net income | | 319,481 | | 282,693 | | 260,590 | |

Diluted net income per common share | | $ | 1.23 | | $ | 1.09 | | $ | 0.99 | |

Our consolidated net sales for 2005 increased 8 percent to $4.5 billion compared to $4.2 billion in 2004. Excluding acquisitions and divestitures, consolidated net sales increased 7 percent. Changes in currency translation positively impacted the consolidated sales growth rate by 1 percentage point. Sales benefited from new account gains, new product and service offerings and investments in the sales-and-service force.

| | 2005 | | 2004 | | 2003 | |

Gross profit as a percent of net sales | | 50.4 | % | 51.4 | % | 50.9 | % |

Selling, general & administrative expenses as a percent of net sales | | 38.4 | % | 39.6 | % | 38.8 | % |

Our consolidated gross profit margin for 2005 decreased from 2004. The decrease was primarily driven by higher delivered product costs, partially offset by selling price increases and cost savings programs.

Selling, general and administrative expenses as a percentage of sales improved for 2005 compared to 2004. The improvement in the 2005 expense ratio is primarily due to selling price increases, sales leverage and cost savings programs partially offset by investments in the sales-and-service force and research and development.

(thousands) | | 2005 | | 2004 | | 2003 | |

Operating income | | $ | 542,420 | | $ | 489,890 | | $ | 455,009 | |

Operating income as a percent of net sales | | 12.0 | % | 11.7 | % | 12.1 | % |

| | | | | | | | | | |

Operating income for 2005 increased 11 percent over 2004. As a percent of sales, operating income also increased from 2004. The increase in operating income in 2005 is due to sales volume and selling price increases, cost reduction initiatives and lower share-based compensation expense, partially offset by higher delivered product costs as well as investments in the sales-and-service force, research and development and technology. Operating income also benefited from significant operating improvement at GCS Service in 2005.

Our net income was $319 million in 2005, an increase of 13 percent as compared to $283 million in 2004. Net income in both years included items of a non-recurring nature that are not necessarily indicative of future operating results. Net income in 2005 included a tax charge of $3.1 million related to the repatriation of foreign earnings under the AJCA. Net income in 2004 included benefits from a reduction in previously recorded restructuring expenses of $0.6 million after tax and a gain on the sale of a small international business of $0.2 million after tax. Income tax expense and net income in 2004 also included a tax benefit of $1.9 million related to prior years. These benefits were more than offset by a charge of $1.6 million for in-process research and development as part of the acquisition of Alcide Corporation and a charge of $2.4 million after tax related to the disposal of a grease management product line. Excluding these items from both years, net income increased 14 percent for 2005. This increase in net income reflects improved operating income growth by most of our business units in the face of a challenging raw material cost environment. Currency translation positively impacted net income growth in 2005 by approximately $5 million. Our 2005 net income also benefited when compared to 2004 due to a lower overall effective income tax rate which was the result of a lower international rate, international mix and tax planning efforts. Excluding the items of a non-recurring nature previously mentioned, net income was 7 percent of net sales for both 2005 and 2004.

2004 COMPARED WITH 2003

Our consolidated net sales reached $4.2 billion for 2004, an increase of 11 percent over net sales of $3.8 billion in 2003. Excluding acquisitions and divestitures, consolidated net sales increased 9 percent. Changes in currency translation positively impacted the consolidated sales growth rate by 4.5 percentage points, primarily due to the strength of the euro against the U.S. dollar. Sales also benefited from aggressive new account sales, new product and service offerings and providing more solutions for existing customers.

Our consolidated gross profit margin for 2004 increased over 2003. The increase is principally due to the benefits of cost savings initiatives, acquisitions and favorable raw material prices, especially in Europe.

Selling, general and administrative expenses for 2004 increased as a percentage of sales over 2003. The increase in the 2004 expense ratio is primarily due to investments in the sales-and-service force, information technology, research and development, acquisitions and higher compensation costs due to the issuance of stock options under a reload feature and the acceleration of vesting associated with executive retirements.

Operating income for 2004 increased 8 percent over 2003. Operating income as a percent of sales decreased slightly from 2003. The increase in operating income in 2004 is due to favorable sales volume increases and cost reduction initiatives, partially offset by investments in technology, research and development and the sales-and-service force as well as higher compensation costs.

Our net income was $283 million in 2004 as compared to $261 million in 2003, an increase of 8 percent. Net income in both years included items of a non-recurring nature that are not necessarily indicative of future operating results. Net income in 2004 included benefits from a reduction in previously recorded restructuring expenses of $0.6 million after tax and a gain on the sale of a small international business of $0.2 million after tax. Income tax expense and net income in 2004 also included a tax benefit of $1.9 million related to prior years. These benefits were more than offset by a charge of $1.6 million for in-process research and development as part of the acquisition of Alcide Corporation and a charge of $2.4 million after tax related to the disposal of a grease management product line. Net income in 2003 included a gain on the sale of an equity investment of $6.7 million after tax and a reduction in previously recorded restructuring expenses of $0.8 million after tax, partially

24

offset by a write-off of $1.7 million of goodwill related to an international business sold in 2003. If these items are excluded from both 2004 and 2003, net income increased 12 percent for 2004. This net income improvement reflects improving operating income growth across most of our divisions. Our 2004 net income also benefited when compared to 2003 due to a lower effective income tax rate which was the result of a lower international rate, tax savings efforts and the favorable tax benefit related to prior years that was recorded in 2004. Excluding the items of a non-recurring nature previously mentioned, net income was 7 percent of net sales for both 2004 and 2003.

OPERATING SEGMENT PERFORMANCE

Our operating segments have similar products and services and we are organized to manage our operations geographically. Our operating segments have been aggregated into three reportable segments: United States Cleaning & Sanitizing, United States Other Services and International. We evaluate the performance of our International operations based on fixed management rates of currency exchange. Therefore, International sales and operating income totals, as well as the International financial information included in this financial discussion, are based on translation into U.S. dollars at the fixed currency exchange rates used by management for 2005. All other accounting policies of the reportable segments are consistent with U.S. GAAP and the accounting policies of the company described in Note 2 of the notes to consolidated financial statements. Additional information about our reportable segments is included in Note 15 of the notes to consolidated financial statements.

SALES BY OPERATING SEGMENT

(thousands) | | 2005 | | 2004 | | 2003 | |

Net sales | | | | | | | |

United States | | | | | | | |

Cleaning & Sanitizing | | $ | 1,952,220 | | $ | 1,796,355 | | $ | 1,694,323 | |

Other Services | | 375,234 | | 339,305 | | 320,444 | |

Total United States | | 2,327,454 | | 2,135,660 | | 2,014,767 | |

International | | 2,229,902 | | 2,126,840 | | 1,980,722 | |

Total | | 4,557,356 | | 4,262,500 | | 3,995,489 | |

Effect of foreign currency translation | | (22,524 | ) | (77,567 | ) | (233,670 | ) |

Consolidated | | $ | 4,534,832 | | $ | 4,184,933 | | $ | 3,761,819 | |

The following chart presents the comparative percentage change in net sales for each of our operating segments for 2005 and 2004.

SALES GROWTH INFORMATION

| | Percent Change

from Prior Year | |

| | 2005 | | 2004 | |

| | | | | |

Net sales | | | | | |

United States Cleaning & Sanitizing | | | | | |

Institutional | | 7 | % | 5 | % |

Kay | | 11 | | 16 | |

Textile Care | | 5 | | 6 | |

Professional Products | | 2 | | (15 | ) |

Healthcare | | 16 | | 6 | |

Water Care Services | | 34 | | 10 | |

Vehicle Care | | 12 | | (2 | ) |

Food & Beverage | | 9 | | 9 | |

Total United States Cleaning & Sanitizing | | 9 | % | 6 | % |

United States Other Services | | | | | |

Pest Elimination | | 12 | % | 10 | % |

GCS Service | | 8 | | (1 | ) |

Total United States Other Services | | 11 | % | 6 | % |

Total United States | | 9 | % | 6 | % |

International | | | | | |

Europe | | 3 | % | 8 | % |

Asia Pacific | | 8 | | 4 | |

Latin America | | 15 | | 13 | |

Canada | | 8 | | 4 | |

Other | | 18 | | 22 | |

Total International | | 5 | % | 7 | % |

Consolidated | | 8 | % | 11 | % |

Sales of our United States Cleaning & Sanitizing operations reached nearly $2.0 billion in 2005 and increased 9 percent over net sales of $1.8 billion in 2004. Excluding acquisitions and divestitures, sales increased 8 percent for 2005. Sales benefited from double-digit organic growth in our Kay, Healthcare and Vehicle Care divisions, along with good growth in our Institutional and Food & Beverage divisions. This sales performance reflects increased account retention and penetration through enhanced service, pricing, new product and program initiatives and aggressive new account sales efforts. Institutional results reflect sales growth in all end market segments, including travel, casual dining, healthcare, and government markets. Kay’s double-digit sales increase was led by strong gains in sales to its core quickservice customers and in its food retail services business. Textile Care sales increased this year, driven by price increases and growth at existing corporate account customers. Professional Products sales, excluding the impact of last year’s VIC acquisition, were flat in 2005 compared to 2004. Success with new floor care product introductions and growth in the corporate account and government segments was offset by a decline in sales through distributors to the janitorial market. Our Healthcare Division reported a double-digit sales increase versus last year primarily due to sales of new instrument care solids as well as waterless and antibacterial

25

skincare products. Water Care Services sales growth was primarily driven by the acquisition of Midland Research Laboratories. Excluding the acquisition of Midland, Water Care sales increased 5 percent for 2005 due to sales growth in the food and beverage market segment. Vehicle Care had a double-digit sales increase in 2005. The strong sales trend was driven by new product launches, selling price increases and customer retention. Sales also benefited from increased demand due to favorable wash conditions and weather patterns. Food & Beverage sales increased 9 percent compared to the prior year. Excluding the benefits of last year’s Alcide acquisition, Food & Beverage sales increased 5 percent for 2005 primarily due to gains in the dairy, food and soft drink markets reflecting increasing penetration of existing corporate accounts as well as new business.

Sales of our United States Other Services operations increased 11 percent to $375 million in 2005, from $339 million in 2004. Pest Elimination had double-digit sales growth in both core pest elimination contract and non-contract services, such as bird and termite work, fumigation, one-shot services and its food safety audit business. GCS Service sales grew 8 percent in 2005 as service and installed parts sales increased over last year. GCS continued to increase technician productivity and improve customer service satisfaction.

Management rate sales of our International operations were $2.2 billion in 2005, an increase of 5 percent over sales of $2.1 billion in 2004. Excluding acquisitions and divestitures, sales increased 4 percent for 2005. Sales in Europe, excluding acquisitions and divestitures, were up 2 percent from 2004. Sales continue to be affected by an overall weak European economy, particularly in the major central countries. Europe’s Institutional division had a modest sales increase in 2005 as weak trends in the janitorial distributor segment in Germany, Spain and Italy offset gains in sales to food distribution and chain accounts. Gains in Europe’s Food & Beverage, Healthcare and Pest Elimination businesses helped overcome the poor economic climate in Germany and reduced European tourism. Sales in Asia Pacific, excluding acquisitions and divestitures, increased 7 percent. The growth was primarily driven by East Asia, including continued growth in China. Sales in Japan increased modestly and Australia reported good growth versus 2004. Asia Pacific growth was driven by new corporate accounts and good results in the beverage and brewery segment. Double-digit sales growth in Latin America reflected growth in all countries over last year with Mexico, Chile and Argentina showing the strongest growth. Results were due to new account gains, growth of existing accounts and strong equipment sales. Sales in Canada increased in 2005, reflecting good results from all divisions.

OPERATING INCOME BY OPERATING SEGMENT

(thousands) | | 2005 | | 2004 | | 2003 | |

Operating income | | | | | | | |

United States | | | | | | | |

Cleaning & Sanitizing | | $ | 279,960 | | $ | 266,072 | | $ | 268,646 | |

Other Services | | 36,012 | | 20,447 | | 18,228 | |

Total United States | | 315,972 | | 286,519 | | 286,874 | |

International | | 227,864 | | 217,865 | | 207,057 | |

Total | | 543,836 | | 504,384 | | 493,931 | |

Corporate | | — | | (4,361 | ) | (4,834 | ) |

Effect of foreign currency translation | | (1,416 | ) | (10,133 | ) | (34,088 | ) |

Consolidated | | $ | 542,420 | | $ | 489,890 | | $ | 455,009 | |

Operating income as a percent of net sales | | | | | | | |

United States | | | | | | | |

Cleaning & Sanitizing | | 14.3 | % | 14.8 | % | 15.9 | % |

Other Services | | 9.6 | | 6.0 | | 5.7 | |

Total | | 13.6 | | 13.4 | | 14.2 | |

International | | 10.2 | | 10.2 | | 10.5 | |

Consolidated | | 12.0 | % | 11.7 | % | 12.1 | % |

| | | | | | | | | | | | | |

Operating income of our United States Cleaning & Sanitizing operations was $280 million in 2005, an increase of 5 percent from operating income of $266 million in 2004. As a percentage of net sales, operating income decreased from 14.8 percent in 2004 to 14.3 percent in 2005. Acquisitions and divestitures had no effect on the overall percentage increase in operating income. The increase in operating income in 2005 reflects the benefits of higher sales, increased pricing and lower share-based compensation expense being partially offset by higher delivered product costs. Operating income margins declined because the negative impact of higher delivered product costs more than offset the benefits of pricing, cost savings and sales leverage. The number of sales-and-service associates in our United States Cleaning & Sanitizing operations increased by 135 in 2005 including increases due to investment in our existing businesses and the effects of acquisitions.

Operating income of United States Other Services operations increased 76 percent to $36 million in 2005. The operating income margin for United States Other Services increased to 9.6 percent in 2005 from 6.0 percent in 2004. Pest Elimination had double-digit operating income growth and GCS Service results reflect sharp profitability improvement in 2005. The increase in operating income for Pest Elimination was driven by strong sales and leverage of sales and administrative teams, with pricing and productivity improvements offsetting cost increases. GCS Service narrowed its operating loss substantially in 2005 due to good sales growth and operational improvements. GCS Service operating income growth also benefited from a favorable comparison to 2004 which included a sales decline, increased marketing expenses and higher than expected costs resulting from centralizing the parts and administration activities. We added 105 sales-and-service associates to our United States Other Services operations in 2005.

Management rate operating income of International operations rose 5 percent to $228 million in 2005 from operating income of $218 million in 2004. The International operating income margin was 10.2 percent in both 2005 and 2004. Excluding the impact of acquisitions and divestitures occurring in 2005 and 2004, operating income increased 3 percent over 2004, and the International operating income margin remained the same at 10.2 percent for both 2005 and 2004. Sales growth, pricing initiatives, lower share-based compensation expense and cost efficiencies were partially offset by

26

higher delivered product costs, unfavorable business mix and investments. We added 390 sales-and-service associates to our International operations during 2005, reflecting investments in our core businesses and the impact of acquisitions.

Operating income margins of our International operations are generally less than those realized for our U.S. operations. The lower International margins are due to (i) the additional costs caused by the difference in scale of International operations where many operating locations are smaller in size, (ii) the additional cost of operating in numerous and diverse foreign jurisdictions and (iii) higher costs of importing raw materials and finished goods. Proportionately larger investments in sales, technical support and administrative personnel are also necessary in order to facilitate the growth of our International operations.

2004 COMPARED WITH 2003

Sales of our United States Cleaning & Sanitizing operations were $1.8 billion in 2004 and increased 6 percent over net sales of $1.7 billion in 2003. Excluding acquisitions and divestitures, sales increased 5 percent in 2004. Sales benefited from double-digit growth in our Kay Division, along with good growth in our Institutional Division. This sales performance reflects increased account retention through enhanced service, new product and program initiatives and aggressive new account sales efforts. Institutional results include sales increases in all end markets, including restaurant, lodging, healthcare, travel and government markets. Kay’s double-digit sales increase over 2003 was led by strong gains in sales to its core quickservice customers and in its food retail services business. New customers, better account penetration, new products and programs and more effective field sales coverage contributed to this sales increase. Textile Care sales increase was driven by a significant corporate account gain made early in the year and improved account retention. Professional Products sales, excluding the VIC acquisition, decreased 18 percent as sales growth in corporate accounts was more than offset by the planned phase down of the janitorial equipment distribution business and weak distributor sales. Sales in our Healthcare Division were driven by strong growth in instrument care solids and skincare products which were partially offset by the exit of a private label product line. Food & Beverage sales, excluding the benefits of the Alcide acquisition, increased 5 percent primarily due to improved retention and corporate account growth in sales to the dairy, soft drink and agri markets. Water Care Services had good sales growth in the dairy, canning, meat and food processing markets. Our Circle the Customer strategy continued to produce new account gains as our Water Care Services Division worked with our Food & Beverage and Healthcare divisions to drive its sales growth. Vehicle Care sales declined due to bad weather, the impact of higher fuel prices on customer purchase decisions and the sale of retail gas stations by major oil companies to smaller franchises, which correspondingly affects distributor sales.

Sales of our United States Other Services operations increased 6 percent to $339 million in 2004, from $320 million in 2003. Pest Elimination sales increased with good growth in both core pest elimination contract and non-contract services, such as bird work, the Stealth fly program, one-shot services and its food safety audit business. GCS Service sales decreased slightly in 2004, however, sales grew in the second half of the year as a result of an increase in direct parts revenue.

Management rate sales of our International operations reached $2.1 billion in 2004, an increase of 7 percent over sales of $2.0 billion in 2003. Excluding acquisitions and divestitures, sales increased 4 percent for 2004. Sales in Europe, excluding acquisitions and divestitures, were up 3 percent primarily due to successful new product launches, increased marketing and added sales-and-service headcount that was partially offset by the effects of a weak European economy. Europe’s Institutional division made significant improvement over its 2003 trend, and strength in its Healthcare and Textile Care businesses helped overcome Germany’s poor economic climate and reduced European tourism and beverage consumption. Sales in Asia Pacific, excluding divestitures, increased 5 percent, led by good results in East Asia and New Zealand. In Northeast Asia, China and Hong Kong led the sales increase with strong results in both Institutional and Food & Beverage. New Zealand sales increased over the prior year primarily due to growth in the Food & Beverage business. Sales in Japan and Australia were flat versus 2003. Sales growth in Latin America reflected good growth in all countries and was driven by the success in new business gains in global/regional accounts, continuing to implement the Circle the Customer growth strategy and the successful launch of new programs such as MarketGuard and LaunderCare. Sales in Canada increased, reflecting an improved hospitality industry and recovery from the impact of the Severe Acute Respiratory Syndrome (SARS) outbreak in Canada in 2003.

Operating income of our United States Cleaning & Sanitizing operations was $266 million in 2004, a decrease of 1 percent from operating income of $269 million in 2003. As a percentage of net sales, operating income decreased from 15.9 percent in 2003 to 14.8 percent in 2004. Excluding acquisitions and divestitures, operating income declined 4 percent from 2003 and the operating income margin also declined from 16.2 percent in 2003 to 14.8 percent in 2004. This decline is primarily due to investments in the sales-and-service force, research and development, information technology, higher compensation costs and higher delivered product cost. This was partially offset by favorable business mix and cost efficiency improvements. The number of sales-and service associates in our United States Cleaning & Sanitizing operations declined by 60 people in 2004, as the addition of 190 new associates was offset by a decrease of 250 people due to the divestiture of our grease management product line.

Operating income of our United States Other Services operations increased 12 percent to $20 million in 2004. The operating income margin for United States Other Services increased to 6.0 percent in 2004 from 5.7 percent in 2003. Pest Elimination had strong operating income growth, while GCS Service results reflected a slightly higher operating loss. The increase in operating income for Pest Elimination was driven by increased sales volume, lower product cost and general expense controls. GCS Service results reflected an operating loss due to a decline in sales, increased marketing expenses and higher than expected costs resulting from centralizing the parts and administration activities. During 2004, we added 15 sales-and-service associates to our United States Other Services operations. This is net of a decrease in GCS Service technicians.

Management rate operating income of International operations rose 5 percent to $218 million in 2004 from operating income of $207 million in 2003. The International operating income margin decreased from 10.5 percent in 2003 to 10.2 percent in 2004. Excluding the impact of acquisitions and divestitures occurring in 2004 and 2003, operating income increased 4 percent over 2003, and the International operating income margin was 10.0 percent in 2004 and 2003. The results were due to good operating income growth across all of our international regions. We added 640 sales-and-service associates to our International operations during 2004, reflecting our investment in our core business and the impact of acquisitions.

CORPORATE

We had no operating expenses in our corporate segment in 2005, compared with $4.4 million in 2004 and $4.8 million in 2003. In 2004, corporate operating expense included a charge of $1.6 million for in-process research and development as part of the acquisition of Alcide Corporation and a charge of $4.0 million related to the disposal of a grease management product line, which were partially offset by $0.9 million of income for reductions in restructuring accruals and a $0.3 million gain on the sale of a small international business.

27

Corporate operating expense in 2003 included a write-off of $1.7 million of goodwill related to an international business sold in 2003, $1.4 million of income for reductions in restructuring accruals and $4.5 million of expense for postretirement death benefits for retired executives.

INTEREST AND INCOME TAXES

Net interest expense decreased to $44 million in 2005. The decrease was caused by higher interest income during the year due to increased levels of cash and cash equivalents and short-term investments offset partially by a small increase in interest expense. Interest expense increased due to higher short-term debt levels during the year, partially offset by lower expense on our euro denominated debt due to a stronger U.S. dollar versus the euro.

Net interest expense for 2004 was $45 million and was flat when compared to interest expense in 2003 with a slight decrease in interest expense being offset by a similar decrease in interest income. Higher interest expense on our euro denominated debt due to the stronger euro was offset by lower interest expense on other notes payable.

Our effective income tax rate was 35.9 percent for 2005, compared with effective income tax rates of 36.4 percent and

38.1 percent in 2004 and 2003, respectively. Excluding the effects of the $3.1 million tax charge related to the repatriation of foreign earnings under the American Jobs Creation Act, the estimated annual effective income tax rate for 2005 was 35.2 percent. Excluding the effects of special charges mentioned above in the corporate section and a $1.9 million tax benefit related to prior years, the estimated annual effective income tax rate was 36.7 percent for 2004. Excluding the effects of the gain on the sale of an equity investment and the effect of special charges, the effective income tax rate was 37.9 percent for 2003. Reductions in our effective income tax rates over the last three years have primarily been due to a lower overall international rate, favorable international mix the impact of tax planning efforts.

FINANCIAL POSITION

Our debt continued to be rated within the “A” categories by the major rating agencies during 2005. Significant changes in our financial position during 2005 and 2004 included the following:

During 2005, total assets increased 2 percent to $3.8 billion from $3.7 billion at year-end 2004. Cash and cash equivalents increased to $104 million and short-term investments increased to $125 million due to continued strong operating cash flow, short-term borrowings and a decrease in cash used for businesses acquisition activity in 2005. Acquisitions added approximately

$35 million in assets to the balance sheet and our voluntary contribution to the U.S. Pension plan added $38 million to other assets. The value of non-U.S. assets on the balance sheet decreased by approximately $190 million during 2005 due to foreign currency translation as the U.S. dollar strengthened against most foreign currencies, primarily the euro which decreased in value by 11 percent.

Total liabilities increased approximately $29 million in 2005. This included an increase in total debt of $44 million due to short-term borrowings. Total liabilities also reflected a decrease due to the effects of currency translation.

Total assets reached $3.7 billion at December 31, 2004, an increase of 15 percent over total assets of $3.2 billion at year-end 2003. Acquisitions added approximately $233 million in assets to the balance sheet. Also, assets increased by approximately

$181 million related to the strengthening of foreign currencies, primarily the euro. Of the increase in accounts receivable, 53 percent is due to acquisitions and currency. The increase in goodwill is 65 percent due to acquisitions and 35 percent due to currency. The increase in other assets is primarily due to the $37 million voluntary contribution made in 2004 to fund the U.S. pension plan.

Total liabilities increased approximately $210 million in 2004. Again, acquisitions and currency accounted for a large portion of this increase, approximately 74 percent.

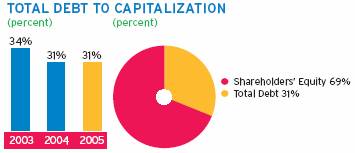

Total debt was $746 million at December 31, 2005, and increased from total debt of $702 million at year-end 2004. This increase in total debt during 2005 was primarily due to higher short-term borrowings to fund a portion of the AJCA repatriation, partially offset by a decrease in our euronotes due to the strengthening of the U.S. dollar against the euro during 2005. The ratio of total debt to capitalization was 31 percent at both year-end 2005 and 2004. The debt to capitalization ratio did not change in 2005 due to the increase in debt outstanding being offset by increasing shareholders’ equity levels.

CASH FLOWS

Cash provided by operating activities reached a record high of $590 million for 2005, an increase over $571 million in 2004 and $524 million in 2003. The increase in operating cash flow for 2005 over 2004 reflects our higher net income. Operating cash flow in 2005 benefited from sales volume and selling price increases along with improved collection of accounts receivable, as well as better inventory management and cost savings efforts. The increase in operating cash flow for 2004 over 2003 is due to increasing net income and a smaller contribution to the U.S. pension plan compared to 2003. The increase was partially offset by an increase in U.S. income tax payments in 2004 over 2003. Historically, we have had strong operating cash flows, and we anticipate this will continue. We expect to continue to use this cash flow to acquire new businesses, repurchase our common stock, pay down debt and meet our ongoing obligations and commitments.

Cash used for investing activities increased from 2004 due to $125 million of net purchases of short-term investments offset by lower acquisition activity. Cash used for investing activities included capital expenditures of $269 million in 2005, $276 million in 2004 and $212 million in 2003. Worldwide additions of merchandising equipment, primarily cleaning and sanitizing product dispensers, accounted for approximately 64 percent, 58 percent and 69 percent of each year’s capital expenditures in 2005, 2004 and 2003, respectively. Merchandising equipment is depreciated over 3 to 7 year lives. Cash used for businesses acquired included Midland Research Laboratories, Kilco Chemicals Ltd. and YSC Chemical Company in 2005, Nigiko, Daydots International, Elimco and certain business lines of VIC International in 2004, and Adams Healthcare in 2003.

Financing cash flow activity included cash used to reacquire shares of our common stock and pay dividends as well as cash provided and used through our debt arrangements. Share repurchases totaled $213 million in 2005, $165 million in 2004 and $227 million in

28

2003. These repurchases were funded with operating cash flows and cash from the exercise of employee stock options. In October 2003 we announced authorization to repurchase up to 10 million shares of Ecolab common stock. This authorization was concluded in the fourth quarter of 2005. In December 2004, we announced an authorization to repurchase up to 10 million additional shares of Ecolab common stock. As of December 31, 2005, approximately 9.8 million shares remained to be purchased under the December 2004 authorization. Shares are repurchased for the purpose of offsetting the dilutive effect of stock options and incentives and for general corporate purposes. During 2006, we expect to repurchase at least 3.5 million shares to offset the dilutive effect of stock options, based on our estimates of stock option exercises for 2006. Cash proceeds from the exercises as well as the tax benefits will provide a portion of the funding for this repurchase activity.

In 2005, we increased our annual dividend rate for the fourteenth consecutive year. We have paid dividends on our common stock for 69 consecutive years. Cash dividends declared per share of common stock, by quarter, for each of the last three years were as follows:

| | First | | Second | | Third | | Fourth | | | |

| | Quarter | | Quarter | | Quarter | | Quarter | | Year | |

| | | | | | | | | | | |

2005 | | $ | 0.0875 | | $ | 0.0875 | | $ | 0.0875 | | $ | 0.1000 | | $ | 0.3625 | |

2004 | | 0.0800 | | 0.0800 | | 0.0800 | | 0.0875 | | 0.3275 | |

2003 | | 0.0725 | | 0.0725 | | 0.0725 | | 0.0800 | | 0.2975 | |

| | | | | | | | | | | | | | | | |

LIQUIDITY AND CAPITAL RESOURCES

We currently expect to fund all of the requirements which are reasonably foreseeable for 2006, including new program investments, share repurchases, scheduled debt repayments, dividend payments, possible business acquisitions and pension contributions from operating activities, cash and short-term investment reserves and short-term borrowings. We will likely undertake long-term borrowing to refinance the euro 300 million ($355 million as of December 31, 2005) Euronotes before they mature in February 2007. In the event of a significant acquisition, funding may also occur through additional long-term borrowings. Cash provided by operating activities reached a record high of $590 million in 2005. While cash flows could be negatively affected by a decrease in revenues, we do not believe that our revenues are highly susceptible, in the short term, to rapid changes in technology within our industry. We have a $450 million U.S. commercial paper program and a $200 million European commercial paper program. Both programs are rated A-1 by Standard & Poor’s and P-1 by Moody’s. To support our commercial paper programs and other general business funding needs, we maintain a $450 million multi-year committed credit agreement which expires in August 2009 and under certain circumstances can be increased by $150 million for a total of $600 million. We can draw directly on the credit facility on a revolving credit basis. As of December 31, 2005, $88 million of this credit facility was committed to support outstanding European commercial paper, leaving $362 million available for other uses. In addition, we have other committed and uncommitted credit lines of approximately

$198 million with major international banks and financial institutions to support our general global funding needs. Additional details on our credit facilities are included in Note 6 of the notes to consolidated financial statements.

During 2005, we voluntarily contributed $38 million to our U.S. pension plan. In making this contribution, we considered the normal growth in accrued plan benefits, the impact of lower year-end discount rates on the plan liability and the tax deductibility of the contribution. Our contributions to the pension plan did not have a material effect on our consolidated results of operations, financial position or cash flows. We expect our U.S. pension plan expense to decrease to approximately $33 million in 2006 from

$35 million in 2005, primarily due to expected returns on a higher level of plan assets partially offset by a decrease in the discount rate from 5.75 percent to 5.57 percent for the 2006 expense calculation. The expected return on plan assets of 8.75 percent is consistent with 2005.

We do not have relationships with unconsolidated entities or financial partnerships, such as entities often referred to as “structured finance” or “special purposes entities”, which are sometimes established for the purpose of facilitating off-balance sheet financial arrangements or other contractually narrow or limited purposes. As such, we are not exposed to any financing, liquidity, market or credit risk that could arise if we had engaged in such relationships.

A schedule of our obligations under various notes payable, long-term debt agreements, operating leases with noncancelable terms in excess of one year, interest obligations and benefit payments are summarized in the following table:

| | Payments due by Period | | | |

(thousands) | | | | Less | | | | | | More | |

Contractual | | | | than | | 1-3 | | 3-5 | | than | |

obligations | | Total | | 1 Year | | Years | | Years | | 5 Years | |

| | | | | | | | | | | |

Notes payable | | $ | 146,725 | | $ | 146,725 | | $ | — | | $ | — | | $ | — | |

Long-term debt | | 599,576 | | 80,202 | | 362,434 | | 2,339 | | 154,601 | |

Operating leases | | 136,857 | | 41,227 | | 54,990 | | 29,781 | | 10,859 | |

Interest* | | 80,759 | | 30,958 | | 25,850 | | 21,876 | | 2,075 | |

Benefit payments** | | 569,000 | | 41,000 | | 93,000 | | 105,000 | | 330,000 | |

Total contractual cash obligations | | $ | 1,532,917 | | $ | 340,112 | | $ | 536,274 | | $ | 158,996 | | $ | 497,535 | |

* Interest on variable rate debt was calculated using the interest rate at year-end 2005.

** Benefit payments are paid out of the company’s pension and postretirement health care benefit plans.

In January 2006, we repaid our $75 million 7.19% senior notes when they became due. We expect to refinance our

euro 300 million ($355 million as of December 31, 2005) Euronotes before they become due in February 2007.

We are not required to make any contributions to our U.S. pension and postretirement health care benefit plans in 2006. However, in January 2006, we made a $45 million voluntary contribution to our U.S. pension plan. The maximum tax deductible contribution for 2006 is estimated to be approximately $50 to $60 million for our U.S. pension plan. We estimate contributions to be made to our international plans will approximate $15 to $20 million in 2006. These amounts have been excluded from the schedule of contractual obligations.

We lease sales and administrative office facilities, distribution center facilities, computers and other equipment under longer-term operating leases. Vehicle leases are generally shorter in duration. The U.S. vehicle leases have guaranteed residual value requirements that have historically been satisfied by the proceeds on the sale of the vehicles. No amounts have been recorded for these guarantees in the table above as we believe that the potential recovery of value from the vehicles when sold will be greater than the residual value guarantee.

Except for approximately $48 million of letters of credit supporting domestic and international commercial relationships and transactions, we do not have significant unconditional purchase obligations, or significant other commercial commitments, such as commitments under lines of credit, standby letters of credit, guarantees, standby repurchase obligations or other commercial commitments.

As of year-end 2005, we are in compliance with all covenants and other requirements of our credit agreements and indentures. Our $450 million multicurrency credit agreement includes a covenant regarding the ratio of the total debt to capitalization. Additionally, we do not have any rating triggers that would accelerate the maturity dates of our debt.

A downgrade in our credit rating could limit or preclude our ability to issue commercial paper under our current programs. A credit rating downgrade could also adversely affect our ability to renew existing, or negotiate new credit facilities in the future and could increase the cost

29

of these facilities. Should this occur, we could seek additional sources of funding, including issuing term notes or bonds. In addition, we have the ability at our option to draw upon our $450 million committed credit facilities prior to their termination and, under certain conditions, can increase this amount to $600 million.

MARKET RISK

We enter into contractual arrangements (derivatives) in the ordinary course of business to manage foreign currency exposure and interest rate risks. We do not enter into derivatives for trading purposes. Our use of derivatives is subject to internal policies that provide guidelines for control, counterparty risk and ongoing monitoring and reporting and is designed to reduce the volatility associated with movements in foreign exchange and interest rates on our income statement and cash flows.

We enter into forward contracts, swaps and foreign currency options to hedge certain intercompany financial arrangements, and to hedge against the effect of exchange rate fluctuations on transactions related to cash flows and net investments denominated in currencies other than U.S. dollars. As of December 31, 2005, we had approximately $395 million of foreign currency forward exchange contracts with face amounts denominated primarily in euros.

We manage interest expense using a mix of fixed and floating rate debt. To help manage borrowing costs, we may enter into interest rate swap agreements. Under these arrangements, we agree to exchange, at specified intervals, the difference between fixed and floating interest amounts calculated by reference to an agreed-upon notional principal amount. At year-end 2005, we had an interest rate swap that converts approximately euro 78 million (approximately $92 million U.S. dollars) of our Euronote debt from a fixed interest rate to a floating or variable interest rate. This swap agreement expires in February 2007. In September 2003, we entered into an interest rate swap agreement that converted $30 million of the 7.19% senior notes from a fixed interest rate to a floating or variable interest rate. This agreement expired in January 2006, when the notes reached final maturity.

Based on a sensitivity analysis (assuming a 10 percent adverse change in market rates) of our foreign exchange and interest rate derivatives and other financial instruments, changes in exchange rates or interest rates would not materially affect our financial position and liquidity. The effect on our results of operations would be substantially offset by the impact of the hedged items.

FORWARD-LOOKING STATEMENTS AND RISK FACTORS

This financial discussion and other portions of this Annual Report to Shareholders contain various “Forward-Looking Statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements include expectations concerning business progress and expansion, business acquisitions, currency translation, cash flows, debt repayments, share repurchases, susceptibility to changes in technology, global economic conditions, pension expenses and potential contributions, and liquidity requirements. These statements, which represent our expectations or beliefs concerning various future events, are based on current expectations. Therefore, they involve a number of risks and uncertainties that could cause actual results to differ materially from those of such Forward-Looking Statements. These risks and uncertainties include: the vitality of the foodservice, hospitality, travel, healthcare and food processing industries; restraints on pricing flexibility due to competitive factors, customer or vendor consolidations and existing contractual obligations; changes in oil or raw material prices or unavailability of adequate and reasonably priced raw materials or substitutes therefore; the occurrence of capacity constraints or the loss of a key supplier or the inability to obtain or renew supply agreements on favorable terms; the effect of future acquisitions or divestitures or other corporate transactions; our ability to achieve plans for past acquisitions; the costs and effects of complying with: (i) laws and regulations relating to the environment and to the manufacture, storage, distribution, efficacy and labeling of our products, and (ii) changes in tax, fiscal, governmental and other regulatory policies; economic factors such as the worldwide economy, interest rates and currency movements, including, in particular, our exposure to foreign currency risk; the occurrence of (a) litigation or claims, (b) the loss or insolvency of a major customer or distributor, (c) war (including acts of terrorism or hostilities which impact our markets), (d) natural or manmade disasters, or (e) severe weather conditions or public health epidemics affecting the foodservice, hospitality and travel industries; loss of, or changes in, executive management; our ability to continue product introductions or reformulations and technological innovations; and other uncertainties or risks reported from time to time in our reports to the Securities and Exchange Commission. In addition, we note that our stock price can be affected by fluctuations in quarterly earnings. There can be no assurances that our earnings levels will meet investors’ expectations. We undertake no duty to update our Forward-Looking Statements.

30

Consolidated Statement of Income

Year ended December 31 (thousands, except per share) | | 2005 | | 2004 | | 2003 | |

| | | | | | | |

Net sales | | $ | 4,534,832 | | $ | 4,184,933 | | $ | 3,761,819 | |

| | | | | | | |

Operating expenses | | | | | | | |

Cost of sales (including special charges (income) of ($106) in 2004 and ($76) in 2003) | | 2,248,831 | | 2,033,492 | | 1,846,584 | |

Selling, general and administrative expenses | | 1,743,581 | | 1,657,084 | | 1,459,818 | |

Special charges | | | | 4,467 | | 408 | |

Operating income | | 542,420 | | 489,890 | | 455,009 | |

| | | | | | | |

Gain on sale of equity investment | | | | | | 11,105 | |

| | | | | | | |

Interest expense, net | | 44,238 | | 45,344 | | 45,345 | |

| | | | | | | |

Income before income taxes | | 498,182 | | 444,546 | | 420,769 | |

| | | | | | | |

Provision for income taxes | | 178,701 | | 161,853 | | 160,179 | |

Net income | | $ | 319,481 | | $ | 282,693 | | $ | 260,590 | |

| | | | | | | |

Net income per common share | | | | | | | |

Basic | | $ | 1.25 | | $ | 1.10 | | $ | 1.00 | |

Diluted | | $ | 1.23 | | $ | 1.09 | | $ | 0.99 | |

| | | | | | | |

Weighted-average common shares outstanding | | | | | | | |

Basic | | 255,741 | | 257,575 | | 259,454 | |

Diluted | | 260,098 | | 260,407 | | 262,737 | |

The accompanying notes are an integral part of the consolidated financial statements.

31

Consolidated Balance Sheet

December 31 (thousands, except per share) | | 2005 | | 2004 | | 2003 | |

| | | | | | | |

ASSETS | | | | | | | |

Current assets | | | | | | | |

Cash and cash equivalents | | $ | 104,378 | | $ | 71,231 | | $ | 85,626 | |

Short-term investments | | 125,063 | | | | | |

Accounts receivable, net | | 743,520 | | 738,266 | | 626,002 | |

Inventories | | 325,574 | | 338,603 | | 309,959 | |

Deferred income taxes | | 65,880 | | 76,038 | | 75,820 | |

Other current assets | | 57,251 | | 54,928 | | 52,933 | |

| | | | | | | |

Total current assets | | 1,421,666 | | 1,279,066 | | 1,150,340 | |

| | | | | | | |

Property, plant and equipment, net | | 835,503 | | 834,730 | | 736,797 | |

| | | | | | | |

Goodwill | | 937,019 | | 991,811 | | 797,211 | |

| | | | | | | |

Other intangible assets, net | | 202,936 | | 229,095 | | 203,859 | |

| | | | | | | |

Other assets, net | | 399,504 | | 381,472 | | 340,711 | |

Total assets | | $ | 3,796,628 | | $ | 3,716,174 | | $ | 3,228,918 | |

| | | | | | | |

LIABILITIES AND SHAREHOLDERS’ EQUITY | | | | | | | |

Current liabilities | | | | | | | |

Short-term debt | | $ | 226,927 | | $ | 56,132 | | $ | 70,203 | |

Accounts payable | | 277,635 | | 269,561 | | 212,287 | |

Compensation and benefits | | 214,131 | | 231,856 | | 190,386 | |

Income taxes | | 39,583 | | 22,709 | | 59,829 | |

Other current liabilities | | 361,081 | | 359,289 | | 319,237 | |

Total current liabilities | | 1,119,357 | | 939,547 | | 851,942 | |

| | | | | | | |

Long-term debt | | 519,374 | | 645,445 | | 604,441 | |

| | | | | | | |

Postretirement health care and pension benefits | | 302,048 | | 270,930 | | 249,906 | |

| | | | | | | |

Other liabilities | | 206,639 | | 262,111 | | 201,548 | |

| | | | | | | |

Shareholders’ equity (common stock, par value $1.00 per share; shares outstanding: 2005 - 254,143; 2004 - 257,542 and 2003 - 257,417) | | 1,649,210 | | 1,598,141 | | 1,321,081 | |

Total liabilities and shareholders’ equity | | $ | 3,796,628 | | $ | 3,716,174 | | $ | 3,228,918 | |

The accompanying notes are an integral part of the consolidated financial statements.

32

Consolidated Statement of Cash Flows

Year ended December 31 (thousands) | | 2005 | | 2004 | | 2003 | |

| | | | | | | |

OPERATING ACTIVITIES | | | | | | | |

Net income | | $ | 319,481 | | $ | 282,693 | | $ | 260,590 | |

Adjustments to reconcile net income to cash provided by operating activities: | | | | | | | |

Depreciation | | 222,712 | | 213,523 | | 201,512 | |

Amortization | | 34,223 | | 33,431 | | 26,591 | |

Deferred income taxes | | (13,021 | ) | 14,342 | | 36,796 | |

Share-based compensation expense | | 39,087 | | 44,660 | | 29,202 | |

Excess tax benefits from share-based payment arrangements | | (11,682 | ) | (11,556 | ) | (5,267 | ) |

Gain on sale of equity investment | | | | | | (11,105 | ) |

Disposal loss, net | | | | 3,691 | | | |

Charge for in-process research and development | | | | 1,600 | | | |

Special charges - asset disposals | | | | | | 1,684 | |

Other, net | | (882 | ) | (2,507 | ) | 1,837 | |

Changes in operating assets and liabilities: | | | | | | | |

Accounts receivable | | (44,839 | ) | (47,217 | ) | (5,547 | ) |

Inventories | | 2,553 | | (5,481 | ) | (2,902 | ) |

Other assets | | (21,853 | ) | (31,723 | ) | (39,224 | ) |

Accounts payable | | 18,987 | | 34,841 | | (13,329 | ) |

Other liabilities | | 45,370 | | 40,611 | | 43,094 | |

Cash provided by operating activities | | 590,136 | | 570,908 | | 523,932 | |

| | | | | | | |

INVESTING ACTIVITIES | | | | | | | |

Capital expenditures | | (268,783 | ) | (275,871 | ) | (212,035 | ) |

Property disposals | | 21,209 | | 18,373 | | 8,502 | |

Capitalized software expenditures | | (10,949 | ) | (9,688 | ) | (8,951 | ) |

Businesses acquired and investments in affiliates, net of cash acquired | | (26,967 | ) | (129,822 | ) | (31,726 | ) |

Sale of businesses and assets | | 1,441 | | 3,417 | | 27,130 | |

Proceeds from sales and maturities of short-term investments | | 60,625 | | | | | |

Purchases of short-term investments | | (185,688 | ) | | | | |

Cash used for investing activities | | (409,112 | ) | (393,591 | ) | (217,080 | ) |

| | | | | | | |

FINANCING ACTIVITIES | | | | | | | |

Net borrowings (repayments) of notes payable | | 96,683 | | (17,474 | ) | (94,412 | ) |

Long-term debt borrowings | | 4,664 | | 7,325 | | 5,959 | |

Long-term debt repayments | | (5,710 | ) | (6,632 | ) | (13,270 | ) |

Reacquired shares | | (213,266 | ) | (165,414 | ) | (227,145 | ) |

Cash dividends on common stock | | (89,807 | ) | (82,419 | ) | (75,413 | ) |

Exercise of employee stock options | | 49,726 | | 59,989 | | 126,615 | |

Excess tax benefits from share-based payment arrangements | | 11,682 | | 11,556 | | 5,267 | |

Other, net | | | | (800 | ) | (313 | ) |

Cash used for financing activities | | (146,028 | ) | (193,869 | ) | (272,712 | ) |

| | | | | | | |

Effect of exchange rate changes on cash | | (1,849 | ) | 2,157 | | 2,281 | |

| | | | | | | |

INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | | 33,147 | | (14,395 | ) | 36,421 | |

Cash and cash equivalents, beginning of year | | 71,231 | | 85,626 | | 49,205 | |

Cash and cash equivalents, end of year | | $ | 104,378 | | $ | 71,231 | | $ | 85,626 | |

The accompanying notes are an integral part of the consolidated financial statements.

33

Consolidated Statement of Comprehensive Income and Shareholders’ Equity

| | | | | | | | Accumulated | | | | | |

| | | | Additional | | | | Other | | | | | |

| | Common | | Paid-in | | Retained | | Comprehensive | | Treasury | | | |

(thousands) | | Stock | | Capital | | Earnings | | Income(Loss) | | Stock | | Total | |

Balance December 31, 2002 | | $ | 151,950 | | $ | 453,450 | | $ | 1,110,707 | | $ | (76,108 | ) | $ | (520,252 | ) | $ | 1,119,747 | |

| | | | | | | | | | | | | |

Net income | | | | | | 260,590 | | | | | | 260,590 | |

Foreign currency translation | | | | | | | | 90,601 | | | | 90,601 | |

Other comprehensive loss | | | | | | | | (865 | ) | | | (865 | ) |

Minimum pension liability | | | | | | | | (9,530 | ) | | | (9,530 | ) |

Comprehensive income | | | | | | | | | | | | 340,796 | |

Cash dividends declared | | | | | | (77,132 | ) | | | | | (77,132 | ) |

Stock options and awards | | 3,596 | | 161,262 | | | | | | (43 | ) | 164,815 | |

Reacquired shares | | | | | | | | | | (227,145 | ) | (227,145 | ) |

Stock dividend | | 154,738 | | (154,738 | ) | | | | | | | — | |

Balance December 31, 2003 | | 310,284 | | 459,974 | | 1,294,165 | | 4,098 | | (747,440 | ) | 1,321,081 | |

| | | | | | | | | | | | | |