UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-03055

| T. Rowe Price Tax-Exempt Money Fund, Inc. |

|

| (Exact name of registrant as specified in charter) |

| |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

| (Address of principal executive offices) |

| |

| David Oestreicher |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (410) 345-2000

Date of fiscal year end: February 29

Date of reporting period: February 29, 2016

Item 1. Report to Shareholders

| Tax-Exempt Money Fund | February 29, 2016 |

The views and opinions in this report were current as of February 29, 2016. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

REPORTS ON THE WEB

Sign up for our Email Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

Manager’s Letter

Fellow Shareholders

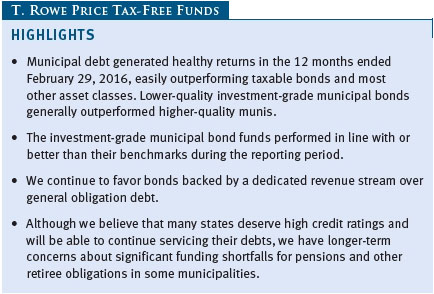

Tax-free municipal bonds strongly outperformed taxable bonds in the 12-month period ended February 29, 2016, with the Barclays Municipal Bond Index returning 3.95% versus 1.50% for the Barclays U.S. Aggregate Bond Index. In fact, munis were one of the best-performing asset classes over the last year, as global equities and other higher-risk assets fell sharply in response to China’s economic deceleration and tumbling commodity prices. Money market yields remained very low over the last year, but they increased toward the end of 2015 as the Federal Reserve raised the overnight federal funds target rate in December for the first time in nine years. Shorter-term municipal bond yields also rose in anticipation of a Fed rate hike, but intermediate- and long-term yields declined. Longer-maturity municipals outperformed shorter-maturity issues, and lower-quality investment-grade munis generally outperformed higher-quality bonds. The T. Rowe Price Tax-Free Funds mostly performed in line with or better than their benchmarks, and their longer-term relative performance remained favorable.

ECONOMY AND INTEREST RATES

The U.S. economy expanded at a relatively soft annualized rate of 1.0% in the fourth quarter of 2015, according to the most recent estimates, but the underlying trend of moderate U.S. economic growth seems to remain in place. Jobs growth was solid throughout 2015, averaging more than 200,000 per month, and the national unemployment rate fell to 4.9% in February, its lowest level in eight years. Falling domestic oil production and the strong U.S. dollar have weighed on the manufacturing sector, but weakness in the natural resources and manufacturing segments has not spilled over to the broader economy.

Although broad measures of inflation have been very low due to declining oil and other commodity prices—which is a plus for consumers and many businesses—Fed officials decided to raise short-term interest rates on December 16 because of labor market improvement and their confidence that inflation will return to 2% over the medium term. The new fed funds target rate range is 0.25% to 0.50%; the range had been 0.00% to 0.25% since December 2008. While core inflation (which excludes food and energy costs) is beginning to turn higher, we believe subsequent interest rate increases will be very gradual, as the Fed will likely watch the effects of each rate increase for several months before deciding to act again.

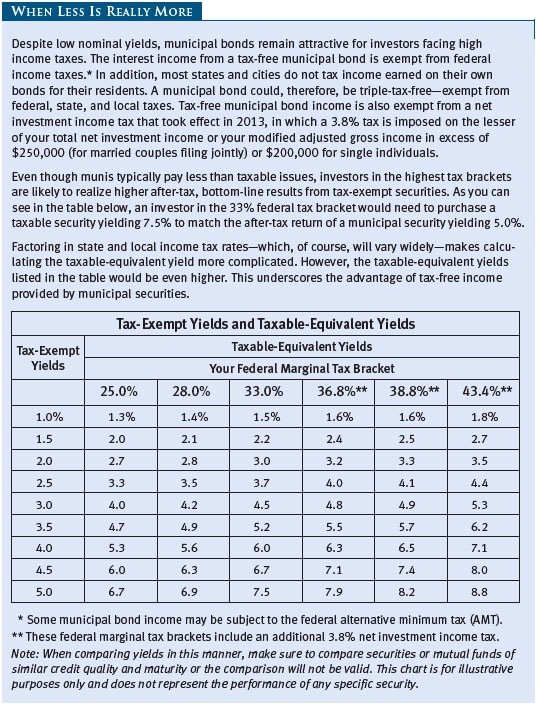

Short-term Treasury and municipal yields increased over the last year, which is not unusual in advance of Fed tightening. Intermediate-term Treasury and muni yields declined, resulting in flatter yield curves in both markets. The 30-year Treasury bond yield was virtually unchanged over the last year, whereas high-quality 30-year muni bond yields declined, resulting in price appreciation that contributed to muni outperformance. With 30-year muni yields above 30-year Treasury yields at the end of our reporting period, long-term municipal bonds remain an attractive option for longer-term, income-oriented investors.

As an illustration of their relative attractiveness, on February 29, 2016, the 2.80% yield offered by a 30-year tax-free general obligation (GO) bond rated AAA was about 107% of the 2.61% pretax yield offered by a 30-year Treasury bond. Including the 3.8% net investment income tax that took effect in 2013 as part of the Affordable Care Act, the top marginal federal tax rate currently stands at 43.4%. An investor in this tax bracket would need to invest in a taxable bond yielding about 4.95% to receive the same after-tax income as that generated by the municipal bond. (To calculate a municipal bond’s taxable-equivalent yield, divide the yield by the quantity of 1.00 minus your federal tax bracket expressed as a decimal—in this case, 1.00 – 0.434, or 0.566.)

MUNICIPAL MARKET NEWS

Total municipal bond issuance in 2015 was about $398 billion, according to The Bond Buyer, while issuance in the first two months of 2016 was roughly $55 billion. Limited supply and strong demand during the second half of the reporting period created a strong technical environment and bolstered the muni market, even in the face of the Federal Reserve’s December rate hike. While refunding debt rose significantly in the first half of our fiscal year as muni issuers took advantage of low borrowing costs to refinance older, higher-cost debt, year-over-year issuance declined throughout the second half of our reporting period. As for demand, a slow but steady pace of muni market outflows in the first half of our fiscal year reversed and turned into a strong pace of inflows in the second half. Overall, flows into municipal bond funds for the last 12 months were positive.

Generally, fundamentals for municipal issuers remain solid. The overwhelming number of issuers in the $3.7 trillion municipal bond market are acting responsibly—raising revenues, reducing expenses, balancing budgets, and taking steps to address long-term liability issues. Most state and local governments have been very cautious about adding to indebtedness since the financial crisis, and a strengthening economy has helped tax revenues rebound. Over 60% of the market, as measured by the Barclays Municipal Bond Index, is AAA or AA rated.

Although the market is overwhelmingly high quality, many states and municipalities are grappling with underfunded pensions and other post-employment benefit (OPEB) obligations. New reporting rules from the Governmental Accounting Standards Board are bringing greater transparency to state and local governments’ pension funding gaps, long-term risks that investors often overlooked in the past. We believe the market will price in higher pension risks over time, as the magnitude of unfunded liabilities becomes more conspicuous.

The Commonwealth of Puerto Rico, which experienced its first official default when it failed to make the full payment due on its Public Finance Corporation bonds at the beginning of August, remained in the headlines in the last six months. Puerto Rico defaulted on approximately $37 million of the roughly $1 billion in debt payments due on January 1, 2016. The default had little impact on the broader muni market, as Governor Alejandro García Padilla had warned that another default was coming in the absence of help from Washington. Near the end of our reporting period, the governor signed the Revitalization Act, which will allow the Puerto Rico Electric Power Authority (PREPA) to restructure nearly $9 billion of its debt. T. Rowe Price’s municipal team has long maintained that Puerto Rico’s debt burden is unsustainable and would eventually need to be restructured.

In terms of sector performance, revenue bonds outperformed state and local GOs over the last year. We continue to favor bonds backed by a dedicated revenue stream over GOs, as we consider revenue bonds to be largely insulated from the pension funding concerns facing state and local governments. Across our municipal platform, we have an overweight to the higher-yielding health care and transportation revenue-backed sectors. Among revenue bonds, transportation and water/sewer were two of the best-performing segments. Resource recovery, leasing, and housing bonds lagged the broader market but still posted positive results. High yield tobacco bonds performed extremely well, outpacing the broad muni market by a wide margin.

PORTFOLIO STRATEGY

TAX-EXEMPT MONEY FUND

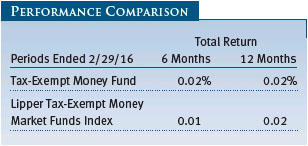

The fund returned 0.02% during the past six months and 0.02% for the fiscal year ended February 29, 2016, compared with 0.01% and 0.02%, respectively, for the Lipper Tax-Exempt Money Market Funds Index. Yields for money market investors remain near 0.00% despite the Fed’s 25-basis-point rate increase in December.

While longer-maturity (6- to 12-month) money market yields have moved somewhat higher, rates in the front end of the yield curve—where the fund must do the bulk of its investing—remain in the low single digits. Overnight and seven-day yields were unchanged at 0.01% and 0.02%, respectively. Yields on 6- to 12-month maturities moved higher by about 17 basis points over the reporting period to 0.40%.

While expectations for the future path of interest rates should influence money market yields, the dominant factor suppressing tax-exempt yields remains persistently low supply. As we have noted in previous shareholder letters, historically low interest rates have encouraged many municipal issuers to borrow for longer periods to lock in currently favorable financing costs, leading to less short-term issuance to offset maturing debt. As a result, variable rate demand note (VRDN) supply ended 2015 at $178 billion, down 21% from the prior year and 68.6% lower than the 2007 high of $565 billion. The resulting imbalance between supply and demand has led to an environment in which total municipal money market assets under management ($244 billion) now greatly exceed VRDN supply outstanding, a condition last seen in the 1980s.

Further contributing to the ongoing technical imbalance, municipalities have seen their revenues increase as a result of better economic conditions over the last couple of years, reducing their need for annual short-term borrowing. Municipalities borrowed $34.5 billion to bridge their cash needs in 2015, which was the lowest level in over 15 years and 47% below the 2010 peak of $65 billion. This is good news for municipalities but bad news for money market funds because these issuers tend to be well-known, liquid names that provide diversification and supply to money market funds starved for new issuance.

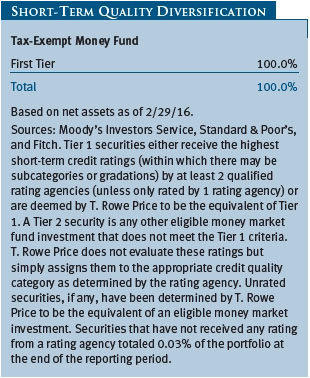

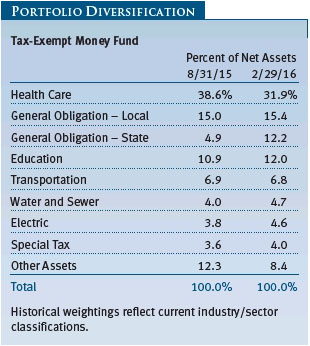

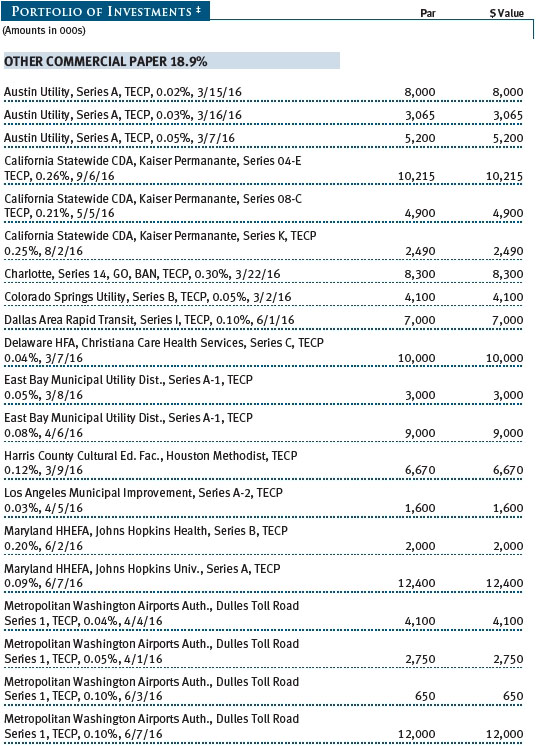

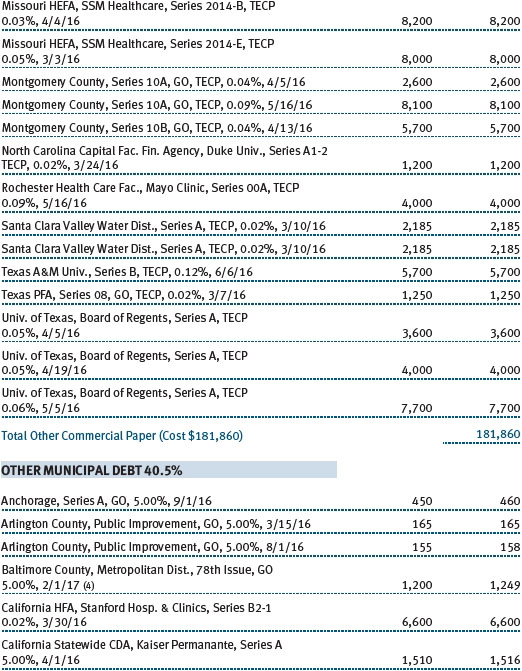

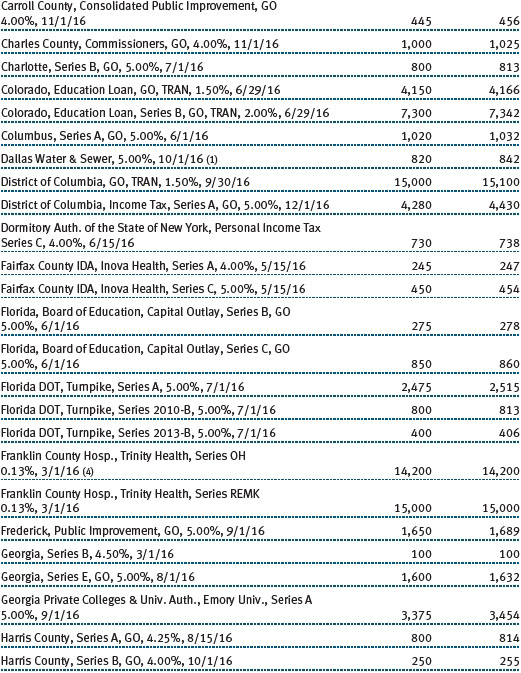

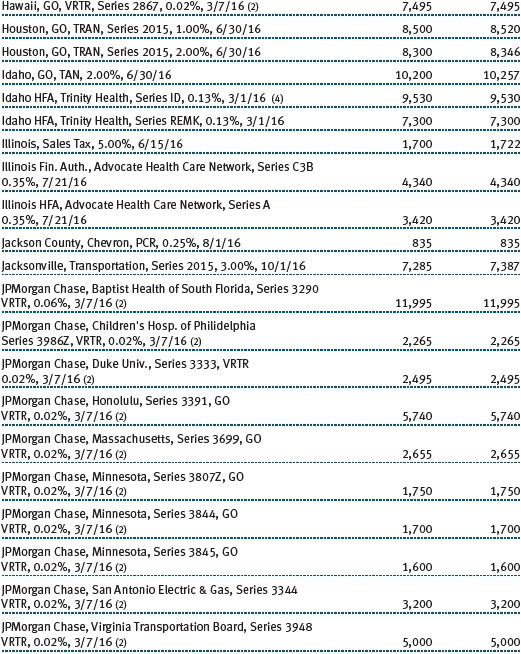

Credit quality plays a large role in the management of the fund, and the portfolio’s overall credit quality remains quite strong. As a policy, we favor only the most highly rated issuers in sectors such as hospitals and education as well as some select GO issuers. Some prominent positions in the portfolio include the State of Massachusetts, Trinity Healthcare, and the University of Texas. While the Fed raised interest rates in December, we believe that the path toward rate normalization will be long and slow. As always, we remain committed to managing a high-quality, diversified portfolio focused on liquidity and stability of principal, which we deem of utmost importance to our valued shareholders. (Please refer to the fund’s portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

As we have discussed in prior shareholder letters, the Securities and Exchange Commission (SEC) enacted rules that will change the way money funds are managed, and these changes become fully effective in October 2016. These rule changes will differentiate between types of money funds (prime versus government funds, for example) as well as classes of shareholders (individual versus institutional investors).

T. Rowe Price has been carefully considering these SEC rule changes and their implications and is crafting solutions designed to minimize the impacts on our money fund shareholders. As such, we will introduce changes to our money fund lineup in 2016. While most modifications will have little effect on the majority of shareholders, some will be more noticeable, such as changes to some funds’ investment strategies or the suitability of a given fund for certain classes of investors.

As for the Tax-Exempt Money Fund, we are not making any changes to the fund’s investment program. However, per the new SEC rules, the fund must adopt the ability—effective October 14, 2016—to implement liquidity fees or temporarily suspend redemptions (also known as “gates”) in times of severe redemption pressure on the fund. Also, because the fund will be available only to individual investors under the new rules, we will be closing the fund to new institutional accounts on July 1, 2016. Institutional investors who already have an account in the fund may continue to add to their account after July 1, 2016, but they will need to exchange into another fund or redeem their shares by September 23, 2016. We expect to provide more detailed information about these and other money fund rule-related changes within the coming months to help shareholders make informed decisions.

TAX-FREE SHORT-INTERMEDIATE FUND

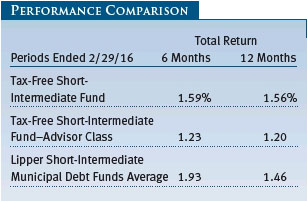

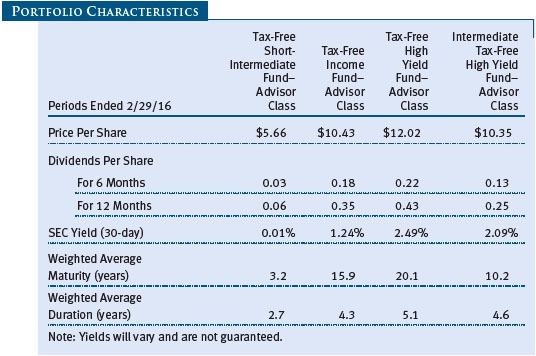

The fund returned 1.56% during the 12-month reporting period versus 1.46% for the Lipper Short-Intermediate Municipal Debt Funds Average, which measures the performance of competing funds. (Performance is also shown in the Performance Comparison table for the Advisor Class, which has a different fee structure.) Our emphasis on revenue bonds over prerefunded debt contributed to the fund’s relative outperformance. The fund’s net asset value per share was $5.67 at the end of February, up from $5.62 six months earlier. Dividends per share contributed $0.08 to the fund’s total return during the 12-month period.

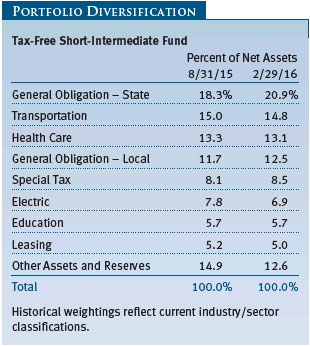

The fund’s duration shortened modestly to 2.7 years from 2.9 years over the past 12 months as we believed the market would react negatively to the Fed’s initial rate increase in December; however, the volatility in global markets and low inflation pushed off concerns about further rate hikes by the Fed. While our overall view is for higher rates eventually, it has become increasingly clear that the pace of Fed rate hikes in 2016 will be much slower than most had predicted. As for yield curve positioning, the fund’s overweight to maturities in the 7- to 10-year range contributed to relative results as longer-term municipal yields decreased over the period.

While our preference for revenue bonds over GOs remains intact as a result of our concerns about the considerable unfunded pension and OPEB liabilities that many state and local government issuers face, it has become challenging to find opportunities in revenue debt over the past couple of years in the short-to-intermediate municipal market. As a result, we increased the fund’s allocation to GOs by almost five percentage points over the 12-month period by adding exposure to states with relatively well-funded pensions, including California, Florida, Washington, and Minnesota. Our underweight to the prerefunded sector contributed to relative results over the past 12 months as the high-quality, lower-yielding sector underperformed both GOs and revenue bonds. (Please refer to the fund’s portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

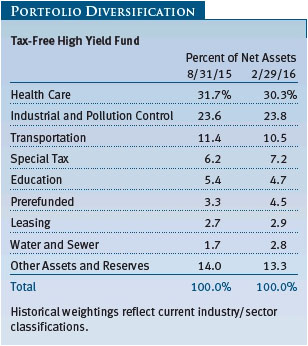

Within the revenue sector, health care and transportation remain the fund’s largest allocations and overweights relative to the index. We have been able to keep our health care allocation around 13%, as we found enough new hospital investments to replace bonds that matured during the reporting period. The fund’s allocation to transportation fell from 17.0% to 14.8%, reflecting the difficulty in sourcing revenue bonds within the short-to-intermediate maturity range. Security selection in the health care sector contributed to the fund’s relative performance, speaking to the strength of our fundamental credit research capabilities.

TAX-FREE INCOME FUND

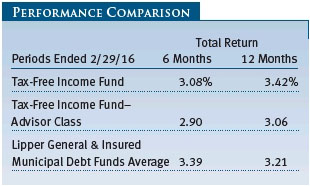

The fund returned 3.42% during the 12-month period ended February 29, 2016, versus 3.21% for the Lipper peer group average, which measures the performance of competing funds. (Performance for the Advisor Class was somewhat lower, reflecting its different fee structure.) Our emphasis on revenue bonds over GOs as well as strong security selection accounted for the fund’s relative outperformance. The fund’s net asset value per share was $10.42 at the end of February, up from $10.30 six months earlier. Dividends per share contributed $0.39 to the fund’s total return during the 12-month period.

The fund’s duration declined slightly to 4.3 years as yields moved lower over the past 12 months, and it was shorter than the duration of the Barclays Municipal Bond Index. During the second half of the reporting period, the fund’s duration shortened relative to the Lipper peer group. This positioning detracted modestly from relative returns. As for yield curve positioning, we maintained an overweight relative to the benchmark in maturities of 15 years and longer to earn the additional yield available on longer-term securities. The portfolio was underweight the 3- to 10-year segment of the yield curve as a result of our outlook for rising shorter-term rates with the Fed’s initial rate hike in December.

The fund’s weighted average maturity also decreased to 15.9 years yet remained longer than that of the benchmark, reflecting our bias toward bonds with longer maturities. This was due in part to the portfolio’s increased exposure to prerefunded securities. Persistently low rates have enabled issuers to refinance older, high-cost debt at more favorable terms, creating a larger allocation to these high-quality securities in the portfolio. This exposure represents a modest addition of liquidity within the fund, which we believe is appropriate in today’s volatile rate environment and leaves us well positioned to take advantage of the possibility of rising interest rates.

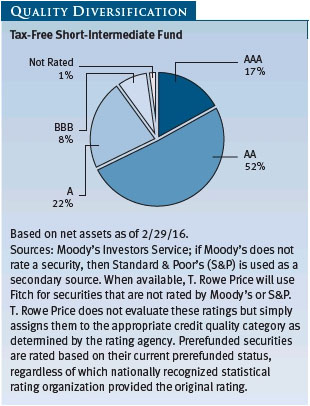

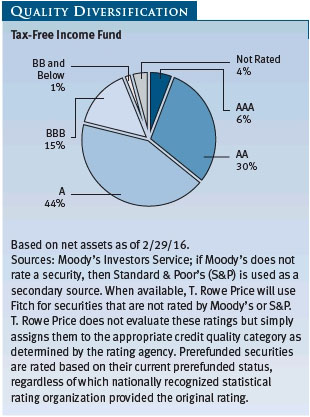

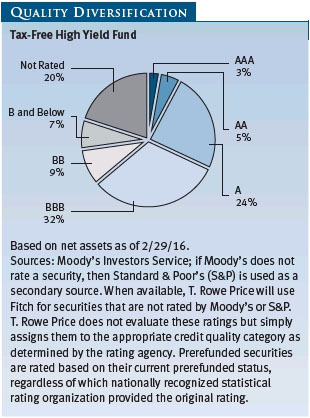

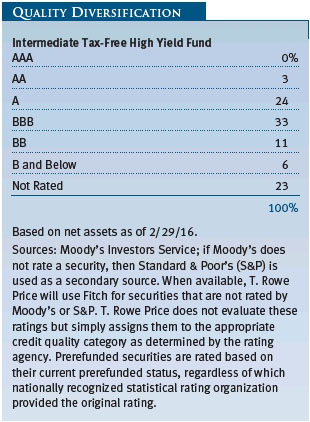

There was no significant change in the fund’s credit quality profile, as we maintained an overweight in bonds rated A and lower and an underweight in high-quality AAA and AA rated debt. Our purchases over the last 12 months were concentrated in the A and BBB rating categories, where we believe that our credit research team can find investment opportunities that offer incremental risk-adjusted yield advantages. This credit quality positioning boosted relative returns as lower-quality munis outperformed higher-quality issues.

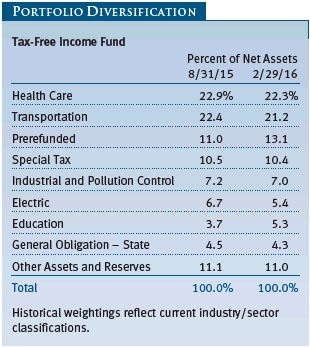

Our preference for revenue bonds over GOs remained intact as a result of our longer-term concern that many municipalities will face fiscal challenges related to unfunded pension and OPEB liabilities. During the reporting period, the revenue bonds we added to the portfolio included debt issued by New Orleans, Water & Sewer and Anne Arundel Health. Health care and transportation remain the fund’s largest sector allocations. Security selection in the health care sector made a notable contribution to the fund’s relative performance, speaking to the strength of our fundamental credit research capabilities. (Please refer to the fund’s portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

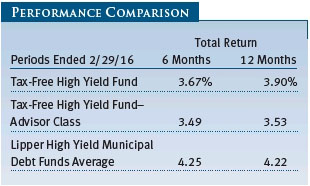

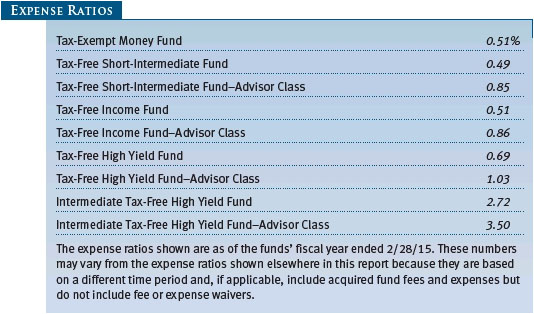

TAX-FREE HIGH YIELD FUND

The Tax-Free High Yield Fund posted a return of 3.90% for the 12-month period ended February 29, 2016, versus 4.22% for our Lipper peer group. (The result for the Advisor Class, which has a different fee structure, is also shown in the Performance Comparison table.) The fund’s net asset value per share was $12.02 at the end of February, up from $11.83 six months earlier, and dividends per share contributed $0.47 to the fund’s total return during the 12-month period.

Our conservative positioning in tobacco securitization bonds detracted from relative performance over the last 12 months as the sector sharply outperformed; however, it has significantly contributed to the fund’s longer-term track record. Cigarette shipments have recently declined at a slower rate after years of precipitous drops due to “sin” taxes and successful cessation initiatives. These shipments are a key driver of payments to states under the Master Settlement Agreement struck with tobacco companies in the late 1990s. Higher levels of disposable income resulting from sharp energy price drops have also contributed to this stabilization in domestic cigarette sales. We added some exposure to the sector over the reporting period, but we remain cautiously positioned versus many peers.

We maintained considerable exposure to industrial development and pollution control revenue bonds backed by corporations. Some holdings in this sector were hurt by the precipitous drop in energy prices over the last 12 months. We reduced our holdings of bonds backed by Marathon Oil and eliminated our exposure to CONSOL Energy debt. Tax-exempt bonds backed by steel companies also struggled throughout the period. We continue to like the diversification benefits and credit metrics of many corporate borrowers from a longer-term perspective. (Please refer to the fund’s portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

The fund benefited from its extensive holdings in the health care sector. Hospitals again posted strong financial performance, as solid reimbursement trends, healthy balance sheets, industry consolidation, and sound financial management drove further improvement in this sector’s overall credit metrics. Our holdings of Onondaga Civic Development Corporation, Saint Joseph’s Hospital Health Center bonds were upgraded sharply following the issuer’s acquisition by a higher-rated health system. We maintained an overweight position in life care revenue bonds, which are issued for continuing care retirement communities, versus many peers. The creditworthiness of well-conceived retirement communities has improved in recent years, and the demographics of an aging population bolster the longer-term prospects for the segment. Our position in Oklahoma County Financial Authority, Epworth Villa debt bounced back during the period.

We still favor essential service revenue bonds in the transportation sector. Issuers such as airports and toll roads generate steady, predictable operating cash flow for the benefit of bondholders, often with little direct competition. Two of our holdings in Indiana (Ohio River Bridges and I-69 Development Partners) outpaced the market during the reporting period as those projects moved closer to completion.

We continue to avoid GOs, as we expect risk premiums in this segment of the municipal market to move higher in response to the long-term neglect of adequate pension (and OPEB) funding for employees of many state and local governments. Most Puerto Rico-related municipal debt continued to slide over the period as the market grappled with likely defaults from many borrowers in the commonwealth. Our holdings of Puerto Rico Electric Power Authority (the commonwealth’s public energy utility) bonds gained during the period after the utility’s restructuring proposal positively surprised market participants.

Medium- and lower-quality municipals performed quite well during the 12-month period versus many other fixed income markets with credit risk. While the volatile energy market has weighed on taxable high yield investors in particular, we have limited exposure to commodity prices. Although interest rates remain low and the yield spreads between munis with different levels of credit quality remain tight by historical norms, we believe that high yield municipals still offer solid relative value for taxable investors seeking income. As always, we will continue to rely heavily on our fundamental research-driven investment process to uncover the best risk-adjusted opportunities within this market.

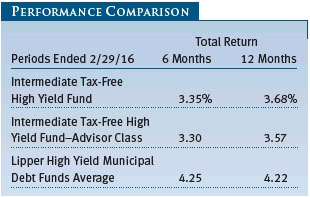

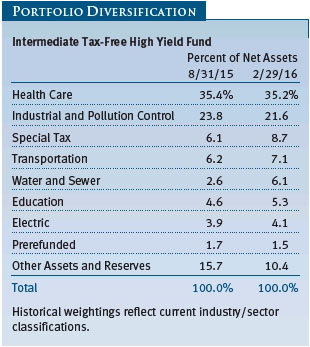

INTERMEDIATE TAX-FREE HIGH YIELD FUND

The Intermediate Tax-Free High Yield Fund generated a return of 3.68% for the 12-month period ended February 29, 2016, versus 4.22% for our Lipper peer group average. (The result for the Advisor Class, which has a different fee structure, is also shown in the Performance Comparison table.) The fund’s net asset value per share was $10.35 at the end of February, up from $10.15 six months earlier, and dividends per share contributed $0.26 to the fund’s total return during the 12-month period.

The fund’s duration is significantly shorter than the average duration of its Lipper peers as a result of our intermediate-term mandate. The fund’s Lipper peer group encompasses all tax-free high yield funds regardless of targeted duration or maturity. This weighed on the relative results of our intermediate-term portfolio as interest rates decreased over the 12-month period. We expect this outcome to reverse during periods of rising interest rates, when the limited term structure of our portfolio would buoy returns versus riskier competitors.

Our conservative positioning in tobacco securitization bonds also detracted from relative performance as the sector sharply outperformed. Cigarette shipments have recently declined at a slower rate after years of precipitous drops due to “sin” taxes and successful cessation initiatives. These shipments are a key driver of payments to states under the Master Settlement Agreement struck with tobacco companies in the late 1990s. Higher levels of disposable income resulting from sharp energy price drops have also contributed to this stabilization in domestic cigarette sales. We maintained allocations to tobacco bonds with short expected maturities from New Jersey and California, but our exposure to the sector is lighter than that of many peers. (Please refer to the fund’s portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

We continue to favor industrial development bonds issued on a tax-exempt basis by corporations. Some holdings in this sector were hurt by the precipitous drop in energy prices over the last 12 months and detracted from relative performance. We eliminated our allocation to CONSOL Energy debt as a result of its significant exposure to fuel price volatility. The vicious repricing of risk in the commodity markets over the reporting period also hurt our U.S. Steel bonds.

On the positive side, the fund benefited from its extensive holdings in the health care sector. Hospitals again posted strong financial performance, as solid reimbursement trends, healthy balance sheets, industry consolidation, and sound financial management drove further improvement in this sector’s overall credit metrics. Our holdings of Onondaga Civic Development Corporation, Saint Joseph’s Hospital Health Center bonds were upgraded sharply following the issuer’s acquisition by a higher-rated health system. We maintained an overweight position in life care revenue bonds, which are issued for continuing care retirement communities, versus many peers. The creditworthiness of well-conceived retirement communities has improved in recent years, and the demographics of an aging population bolster the longer-term prospects for the segment. Our position in bonds from The Evergreens (New Jersey) performed well during the period. In addition, the fund’s holdings of essential service water and sewer revenue bonds fared well. Bonds issued by Detroit Water & Sewer Authority improved notably, benefiting from a Moody’s rating upgrade.

We still favor essential service revenue bonds in the transportation sector. Issuers such as airports and toll roads generate steady, predictable operating cash flow for the benefit of bondholders, often with little direct competition. Two of our holdings in Indiana (Ohio River Bridges and I-69 Development Partners) outpaced the market during the reporting period as those projects moved closer to completion.

We continue to avoid GOs, as we expect risk premiums in this segment of the municipal market to move higher in response to the long-term neglect of adequate pension (and OPEB) funding for employees of many state and local governments. Most Puerto Rico-related municipal debt continued to slide over the period as the market grappled with likely defaults from many borrowers in the commonwealth. We initiated positions in insured debt from Puerto Rico Electric Power Authority (the commonwealth’s public energy utility) and insured Puerto Rico GOs, and they performed strongly. We believe that the companies insuring these bonds (including AGM, AGC, and National Re) are well capitalized and would be able to pay the principal and interest on any missed payments by the commonwealth and its agencies.

Medium- and lower-quality municipals performed quite well during the 12-month period versus many other fixed income markets with credit risk. While the volatile energy market has weighed on taxable high yield investors in particular, we have limited exposure to commodity prices. Although interest rates remain low and the yield spreads between munis with different levels of credit quality remain tight by historical norms, we believe that high yield municipals still offer solid relative value for taxable investors seeking income. As always, we will continue to rely heavily on our fundamental research-driven investment process to uncover the best risk-adjusted opportunities within this market.

OUTLOOK

We believe that the municipal bond market remains a high-quality market that offers good opportunities for long-term investors seeking tax-free income. While fundamentals are sound overall and technical support should persist, investors should expect modest returns in 2016, perhaps just earning the coupon income offset somewhat by modest declines in principal values. If the economic recovery prompts the Fed to continue raising short-term interest rates, muni bond yields are likely to rise along with Treasury yields—although not to the same extent. While higher yields typically pressure bond prices, we expect Fed rate increases to be gradual and modest. Moreover, munis should be less susceptible to rising rates than Treasuries given their attractive tax-equivalent yields and the steady demand for tax-exempt income.

While we believe that many states deserve high credit ratings and will be able to continue servicing their debts, we have longer-term concerns about significant funding shortfalls for pensions and OPEB obligations in some jurisdictions. These funding gaps stem from investment losses during the financial crisis, insufficient plan contributions over time, and unrealistic return projections. Although few large plans are at risk of insolvency in the near term, the magnitude of unfunded liabilities is becoming more conspicuous in a few states.

Ultimately, we believe T. Rowe Price’s independent credit research is our greatest strength and will remain an asset for our investors as we navigate the current market environment. As always, we focus on finding attractively valued bonds issued by municipalities with good long-term fundamentals—an investment strategy that we believe will continue to serve our investors well.

Thank you for investing with T. Rowe Price.

Respectfully submitted,

Joseph K. Lynagh

Chairman of the Investment Advisory Committee

Tax-Exempt Money Fund

Charles B. Hill

Chairman of the Investment Advisory Committee

Tax-Free Short-Intermediate Fund

Konstantine B. Mallas

Chairman of the Investment Advisory Committee

Tax-Free Income Fund

James M. Murphy

Chairman of the Investment Advisory Committee

Tax-Free High Yield Fund and Intermediate Tax-Free High Yield Fund

March 21, 2016

The committee chairmen have day-to-day responsibility for managing the portfolios and work with committee members in developing and executing the funds’ investment programs.

RISKS OF FIXED INCOME INVESTING

Since money market funds are managed to maintain a constant $1.00 share price, there should be little risk of principal loss. However, there is no assurance the fund will avoid principal losses if fund holdings default or are downgraded, or if interest rates rise sharply in an unusually short period. In addition, the fund’s yield will vary; it is not fixed for a specific period like the yield on a bank certificate of deposit. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. Although a money market fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in it. The fund’s sponsor has no legal obligation to provide financial support to the fund, and you should not expect that the sponsor will provide financial support to the fund at any time.

Bonds are subject to interest rate risk (the decline in bond prices that usually accompanies a rise in interest rates) and credit risk (the chance that any fund holding could have its credit rating downgraded or that a bond issuer will default by failing to make timely payments of interest or principal), potentially reducing the fund’s income level and share price. High yield bonds could have greater price declines than funds that invest primarily in high-quality bonds. Municipalities issuing high yield bonds are not as strong financially as those with higher credit ratings, so the bonds are usually considered speculative investments. Some income may be subject to state and local taxes and the federal alternative minimum tax.

GLOSSARY

Barclays Municipal Bond Index: An unmanaged index that tracks municipal debt instruments.

Barclays 1–5 Year Blend (1–6 Year Maturity) Index: A subindex of the Barclays Municipal Bond Index. It is a rules-based, market value-weighted index of short-term bonds engineered for the tax-exempt bond market.

Barclays 65% High-Grade/35% High-Yield Index: An index that tracks Barclays indexes of both investment-grade and below investment-grade municipal debt instruments.

Basis point: One one-hundredth of one percentage point, or 0.01%.

Credit spread: The additional yield that investors demand to hold a bond with credit risk compared with a Treasury security with a comparable maturity date.

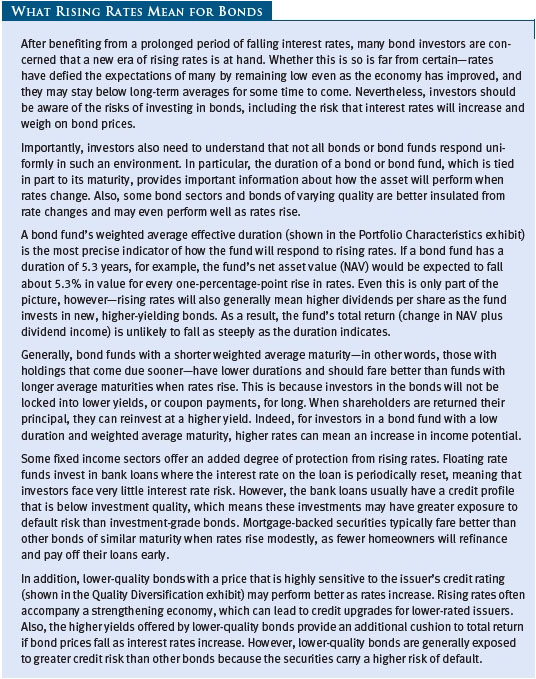

Duration: A measure of a bond fund’s sensitivity to changes in interest rates. For example, a fund with a duration of five years would fall about 5% in price in response to a one-percentage-point rise in interest rates, and vice versa.

Escrowed-to-maturity bond: A bond that has the funds necessary for repayment at maturity, or a call date, set aside in a separate or “escrow” account.

Federal funds rate: The interest rate charged on overnight loans of reserves by one financial institution to another in the United States. The Federal Reserve sets a target federal funds rate to affect the direction of interest rates.

General obligation (GO) debt: A government’s strongest pledge that obligates its full faith and credit, including, if necessary, its ability to raise taxes.

Investment grade: High-quality bonds as measured by one of the major credit rating agencies. For example, Standard & Poor’s designates the bonds in its top four categories (AAA to BBB) as investment grade.

Lipper averages: The averages of available mutual fund performance returns for specified time periods in categories defined by Lipper Inc.

Lipper indexes: Fund benchmarks that consist of a small number (10 to 30) of the largest mutual funds in a particular category as tracked by Lipper Inc.

Other post-employment benefit (OPEB) liability: Benefits paid to an employee after retirement, such as premiums for life and health insurance.

Prerefunded bond: A bond that originally may have been issued as a general obligation or revenue bond but that is now secured by an escrow fund consisting entirely of direct U.S. government obligations that are sufficient for paying the bondholders.

SEC yield (7-day simple): A method of calculating a money fund’s yield by annualizing the fund’s net investment income for the last seven days of each period divided by the fund’s net asset value at the end of the period. Yield will vary and is not guaranteed.

SEC yield (30-day): A method of calculating a fund’s yield that assumes all portfolio securities are held until maturity. Yield will vary and is not guaranteed.

Weighted average life: A measure of a fund’s credit quality risk. In general, the longer the average life, the greater the fund’s credit quality risk. The average life is the dollar-weighted average maturity of a portfolio’s individual securities without taking into account interest rate readjustment dates. Money funds must maintain a weighted average life of less than 120 days.

Weighted average maturity: A measure of a fund’s interest rate sensitivity. In general, the longer the average maturity, the greater the fund’s sensitivity to interest rate changes. The weighted average maturity may take into account the interest rate readjustment dates for certain securities. Money funds must maintain a weighted average maturity of less than 60 days.

Yield curve: A graphic depiction of the relationship between yields and maturity dates for a set of similar securities. A security with a longer maturity usually has a higher yield. If a short-term security offers a higher yield, then the curve is said to be “inverted.” If short- and long-term bonds are offering equivalent yields, then the curve is said to be “flat.”

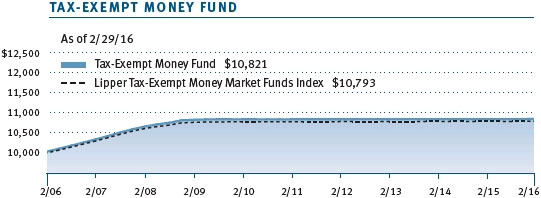

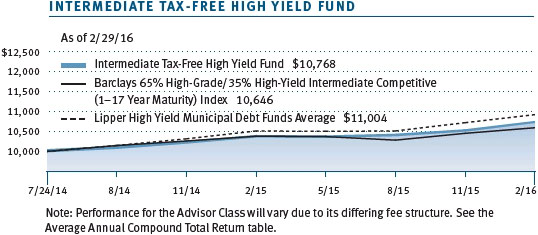

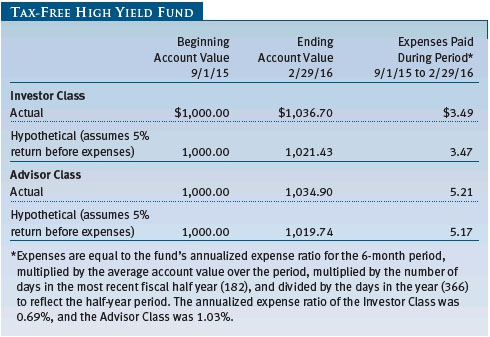

Performance and Expenses

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

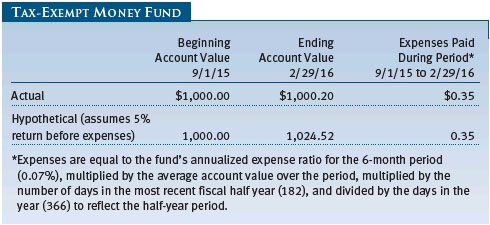

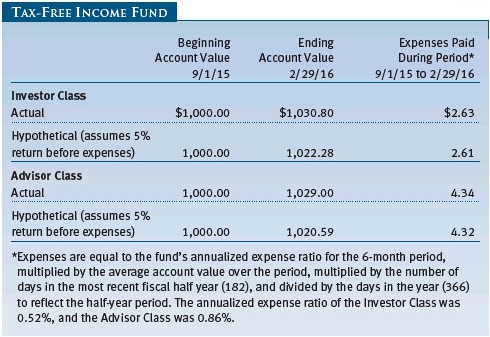

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Actual Expenses

The first line of the following table (Actual) provides information about actual account values and actual expenses. You may use the information on this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number on the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Please note that the Tax-Free Short-Intermediate Fund, Tax-Free Income Fund, Tax-Free High Yield Fund, and Intermediate Tax-Free High Yield Fund have two share classes: The original share class (Investor Class) charges no distribution and service (12b-1) fee, and the Advisor Class shares are offered only through unaffiliated brokers and other financial intermediaries and charge a 0.25% 12b-1 fee. Each share class is presented separately in the table.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (Hypothetical) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Note: T. Rowe Price charges an annual account service fee of $20, generally for accounts with less than $10,000. The fee is waived for any investor whose T. Rowe Price mutual fund accounts total $50,000 or more; accounts electing to receive electronic delivery of account statements, transaction confirmations, prospectuses, and shareholder reports; or accounts of an investor who is a T. Rowe Price Preferred Services, Personal Services, or Enhanced Personal Services client (enrollment in these programs generally requires T. Rowe Price assets of at least $100,000). This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

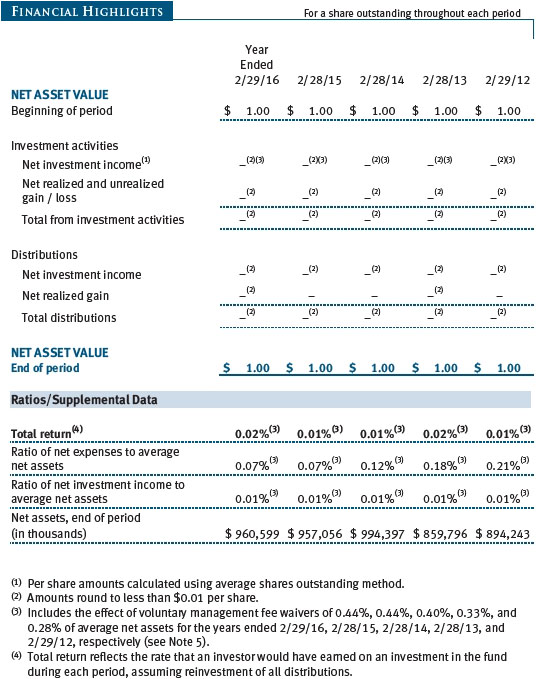

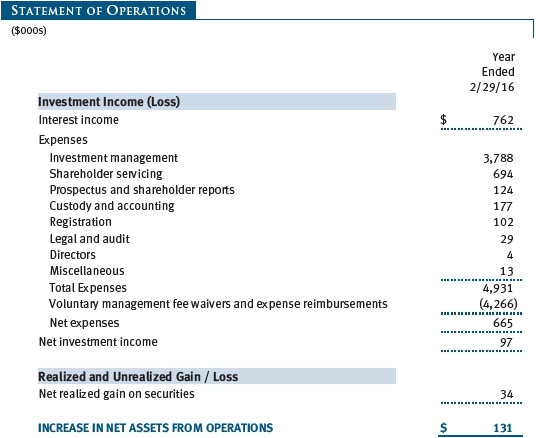

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

| Notes to Financial Statements |

T. Rowe Price Tax-Exempt Money Fund, Inc. (the fund), is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, open-end management investment company. The fund commenced operations on April 8, 1981. The fund seeks to provide preservation of capital, liquidity, and, consistent with these objectives, the highest current income exempt from federal income taxes.

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

Basis of Preparation The fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 (ASC 946). The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (GAAP), including, but not limited to, ASC 946. GAAP requires the use of estimates made by management. Management believes that estimates and valuations are appropriate; however, actual results may differ from those estimates, and the valuations reflected in the accompanying financial statements may differ from the value ultimately realized upon sale or maturity.

Investment Transactions, Investment Income, and Distributions Income and expenses are recorded on the accrual basis. Premiums and discounts on debt securities are amortized for financial reporting purposes. Income tax-related interest and penalties, if incurred, would be recorded as income tax expense. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the identified cost basis. Income distributions are declared daily and paid monthly. Distributions to shareholders are recorded on the ex-dividend date.

New Accounting Guidance In May 2015, FASB issued ASU No. 2015-07, Fair Value Measurement (Topic 820), Disclosures for Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent). The ASU removes the requirement to categorize within the fair value hierarchy all investments for which fair value is measured using the net asset value per share practical expedient and amends certain disclosure requirements for such investments. The ASU is effective for interim and annual reporting periods beginning after December 15, 2015. Adoption will have no effect on the fund’s net assets or results of operations.

NOTE 2 - VALUATION

The fund’s financial instruments are valued and its net asset value (NAV) per share is computed at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day the NYSE is open for business. The fund’s financial instruments are reported at fair value, which GAAP defines as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The T. Rowe Price Valuation Committee (the Valuation Committee) has been established by the fund’s Board of Directors (the Board) to ensure that financial instruments are appropriately priced at fair value in accordance with GAAP and the 1940 Act. Subject to oversight by the Board, the Valuation Committee develops and oversees pricing-related policies and procedures and approves all fair value determinations.

Various valuation techniques and inputs are used to determine the fair value of financial instruments. GAAP establishes the following fair value hierarchy that categorizes the inputs used to measure fair value:

Level 1 – quoted prices (unadjusted) in active markets for identical financial instruments that the fund can access at the reporting date

Level 2 – inputs other than Level 1 quoted prices that are observable, either directly or indirectly (including, but not limited to, quoted prices for similar financial instruments in active markets, quoted prices for identical or similar financial instruments in inactive markets, interest rates and yield curves, implied volatilities, and credit spreads)

Level 3 – unobservable inputs

Observable inputs are developed using market data, such as publicly available information about actual events or transactions, and reflect the assumptions market participants would use to price the financial instrument. Unobservable inputs are those for which market data are not available and are developed using the best information available about the assumptions that market participants would use to price the financial instrument. GAAP requires valuation techniques to maximize the use of relevant observable inputs and minimize the use of unobservable inputs. Input levels are not necessarily an indication of the risk or liquidity associated with financial instruments at that level but rather the degree of judgment used in determining those values. For example, securities held by a money market fund are generally high quality and liquid; however, they are reflected as Level 2 because the inputs used to determine fair value are not quoted prices in an active market.

In accordance with Rule 2a-7 under the 1940 Act, the fund values its securities at amortized cost, which approximates fair value. Securities for which amortized cost is deemed not to reflect fair value are stated at fair value as determined in good faith by the Valuation Committee. On February 29, 2016, all of the fund’s financial instruments were classified as Level 2 in the fair value hierarchy.

NOTE 3 - OTHER INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks and/or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

Restricted Securities The fund may invest in securities that are subject to legal or contractual restrictions on resale. Prompt sale of such securities at an acceptable price may be difficult and may involve substantial delays and additional costs.

When-Issued Securities The fund may enter into when-issued purchase or sale commitments, pursuant to which it agrees to purchase or sell, respectively, an authorized but not yet issued security for a fixed unit price, with payment and delivery not due until issuance of the security on a scheduled future date. When-issued securities may be new securities or securities issued through a corporate action, such as a reorganization or restructuring. Until settlement, the fund maintains liquid assets sufficient to settle its commitment to purchase a when-issued security or, in the case of a sale commitment, the fund maintains an entitlement to the security to be sold. Amounts realized on when-issued transactions are included in realized gain/loss on securities in the accompanying financial statements.

NOTE 4 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its income and gains. Distributions determined in accordance with federal income tax regulations may differ in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences.

The fund files U.S. federal, state, and local tax returns as required. The fund’s tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations, which is generally three years after the filing of the tax return but which can be extended to six years in certain circumstances. Tax returns for open years have incorporated no uncertain tax positions that require a provision for income taxes.

Reclassifications to paid-in capital relate primarily to an over-distribution of taxable income not deemed a return of capital for tax purposes. For the year ended February 29, 2016, the following reclassifications were recorded to reflect tax character (there was no impact on results of operations or net assets):

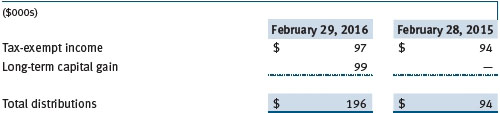

Distributions during the years ended February 29, 2016 and February 28, 2015, were characterized for tax purposes as follows:

At February 29, 2016, the tax-basis cost of investments and components of net assets were as follows:

NOTE 5 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. (Price Group). The investment management agreement between the fund and Price Associates provides for an annual investment management fee, which is computed daily and paid monthly. The fee consists of an individual fund fee, equal to 0.10% of the fund’s average daily net assets, and a group fee. The group fee rate is calculated based on the combined net assets of certain mutual funds sponsored by Price Associates (the group) applied to a graduated fee schedule, with rates ranging from 0.48% for the first $1 billion of assets to 0.275% for assets in excess of $400 billion. The fund’s group fee is determined by applying the group fee rate to the fund’s average daily net assets. At February 29, 2016, the effective annual group fee rate was 0.29%.

Price Associates may voluntarily waive all or a portion of its management fee and reimburse operating expenses to the extent necessary for the fund to maintain a zero or positive net yield (voluntary waiver). Any amounts waived/paid by Price Associates under this voluntary agreement are not subject to repayment by the fund. Price Associates may amend or terminate this voluntary arrangement at any time without prior notice. For the year ended February 29, 2016, expenses waived/repaid totaled $4,266,000.

In addition, the fund has entered into service agreements with Price Associates and a wholly owned subsidiary of Price Associates (collectively, Price). Price Associates provides certain accounting and administrative services to the fund. T. Rowe Price Services, Inc., provides shareholder and administrative services in its capacity as the fund’s transfer and dividend-disbursing agent. For the year ended February 29, 2016, expenses incurred pursuant to these service agreements were $81,000 for Price Associates and $252,000 for T. Rowe Price Services, Inc. The total amount payable at period-end pursuant to these service agreements is reflected as Due to Affiliates in the accompanying financial statements.

As of February 29, 2016, T. Rowe Price Group, Inc., or its wholly owned subsidiaries owned 3,634,591 shares of the fund, representing less than 1% of the fund’s net assets.

The fund may participate in securities purchase and sale transactions with other funds or accounts advised by Price Associates (cross trades), in accordance with procedures adopted by the fund’s Board and Securities and Exchange Commission rules, which require, among other things, that such purchase and sale cross trades be effected at the independent current market price of the security. Purchases and sales cross trades aggregated $106,230,000 and $254,870,000, respectively, with net realized gain of $0 for the year ended February 29, 2016. Generally, cross trades were executed due to the limited supply of high-quality municipal securities available in the market and the adviser’s decision to continue owning certain investments in funds or accounts advised by Price Associates.

| Report of Independent Registered Public Accounting Firm |

To the Board of Directors and Shareholders of

T. Rowe Price Tax-Exempt Money Fund, Inc.

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of the T. Rowe Price Tax-Exempt Money Fund, Inc. (the “Fund”) at February 29, 2016, the results of its operations, the changes in its net assets and the financial highlights for each of the periods indicated therein, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at February 29, 2016 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Baltimore, Maryland

April 20, 2016

| Tax Information (Unaudited) for the Tax Year Ended 2/29/16 |

We are providing this information as required by the Internal Revenue Code. The amounts shown may differ from those elsewhere in this report because of differences between tax and financial reporting requirements.

The fund’s distributions to shareholders included:

| ● | $4,000 from short-term capital gains

|

| ● | $99,000 from long-term capital gains, subject to a long-term capital gains tax rate of not greater than 20%

|

| ● | $96,000 which qualified as exempt-interest dividends |

| Information on Proxy Voting Policies, Procedures, and Records |

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information. You may request this document by calling 1-800-225-5132 or by accessing the SEC’s website, sec.gov.

The description of our proxy voting policies and procedures is also available on our website, troweprice.com. To access it, click on the words “Social Responsibility” at the top of our corporate homepage. Next, click on the words “Conducting Business Responsibly” on the left side of the page that appears. Finally, click on the words “Proxy Voting Policies” on the left side of the page that appears.

Each fund’s most recent annual proxy voting record is available on our website and through the SEC’s website. To access it through our website, follow the above directions to reach the “Conducting Business Responsibly” page. Click on the words “Proxy Voting Records” on the left side of that page, and then click on the “View Proxy Voting Records” link at the bottom of the page that appears.

| How to Obtain Quarterly Portfolio Holdings |

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available electronically on the SEC’s website (sec.gov); hard copies may be reviewed and copied at the SEC’s Public Reference Room, 100 F St. N.E., Washington, DC 20549. For more information on the Public Reference Room, call 1-800-SEC-0330.

| About the Fund’s Directors and Officers |

Your fund is overseen by a Board of Directors (Board) that meets regularly to review a wide variety of matters affecting or potentially affecting the fund, including performance, investment programs, compliance matters, advisory fees and expenses, service providers, and business and regulatory affairs. The Board elects the fund’s officers, who are listed in the final table. At least 75% of the Board’s members are independent of T. Rowe Price Associates, Inc. (T. Rowe Price), and its affiliates; “inside” or “interested” directors are employees or officers of T. Rowe Price. The business address of each director and officer is 100 East Pratt Street, Baltimore, Maryland 21202. The Statement of Additional Information includes additional information about the fund directors and is available without charge by calling a T. Rowe Price representative at 1-800-638-5660.

| Independent Directors |

| |

| Name | | |

| (Year of Birth) | | |

| Year Elected* | | |

| [Number of T. Rowe Price | | Principal Occupation(s) and Directorships of Public Companies and |

| Portfolios Overseen] | | Other Investment Companies During the Past Five Years |

| | | |

| William R. Brody, M.D. Ph.D. | | President and Trustee, Salk Institute for Biological Studies (2009 |

| (1944) | | to present); Director, BioMed Realty Trust (2013 to 2016); Director, |

| 2009 | | Novartis, Inc. (2009 to 2014); Director, IBM (2007 to present) |

| [184] | | |

| | | |

| Anthony W. Deering | | Chairman, Exeter Capital, LLC, a private investment firm (2004 to |

| (1945) | | present); Director, Brixmor Real Estate Investment Trust (2012 to |

| 1983 | | present); Director and Advisory Board Member, Deutsche Bank |

| [184] | | North America (2004 to present); Director, Under Armour (2008 |

| | to present); Director, Vornado Real Estate Investment Trust (2004 |

| | to 2012) |

| | | |

| Bruce W. Duncan | | President, Chief Executive Officer, and Director (2009 to present), |

| (1951) | | and Chairman of the Board (January 2016 to present), First Industrial |

| 2013 | | Realty Trust, an owner and operator of industrial properties; |

| [184] | | Chairman of the Board (2005 to present) and Director (1999 to |

| | present), Starwood Hotels & Resorts, a hotel and leisure company |

| | | |

| Robert J. Gerrard, Jr. | | Advisory Board Member, Pipeline Crisis/Winning Strategies, a |

| (1952) | | collaborative working to improve opportunities for young African |

| 2013 | | Americans (1997 to present) |

| [184] | | |

| | | |

| Paul F. McBride | | Advisory Board Member, Vizzia Technologies (2015 to present) |

| (1956) | | |

| 2013 | | |

| [184] | | |

| | | |

| Cecilia E. Rouse, Ph.D. | | Dean, Woodrow Wilson School (2012 to present); Professor and |

| (1963) | | Researcher, Princeton University (1992 to present); Director, MDRC, |

| 2013 | | a nonprofit education and social policy research organization (2011 |

| [184] | | to present); Member of National Academy of Education (2010 to |

| | present); Research Associate of Labor Program (2011 to present) |

| | and Board Member (2015 to present), National Bureau of Economic |

| | Research (2011 to present); Chair of Committee on the Status of |

| | Minority Groups in the Economic Profession (2012 to present) and |

| | Vice President (2015 to present), American Economic Association |

| | | |

| John G. Schreiber | | Owner/President, Centaur Capital Partners, Inc., a real estate |

| (1946) | | investment company (1991 to present); Cofounder, Partner, and |

| 1992 | | Cochairman of the Investment Committee, Blackstone Real Estate |

| [184] | | Advisors, L.P. (1992 to 2015); Director, General Growth Properties, |

| | Inc. (2010 to 2013); Director, Blackstone Mortgage Trust, a real |

| | estate financial company (2012 to 2016); Director and Chairman of |

| | the Board, Brixmor Property Group, Inc. (2013 to present); Director, |

| | Hilton Worldwide (2013 to present); Director, Hudson Pacific |

| | Properties (2014 to 2016) |

| | | |

| Mark R. Tercek | | President and Chief Executive Officer, The Nature Conservancy (2008 |

| (1957) | | to present) |

| 2009 | | |

| [184] | | |

| |

| * Each independent director serves until retirement, resignation, or election of a successor. |

| |

| Inside Directors | | |

| |

| Name | | |

| (Year of Birth) | | |

| Year Elected* | | |

| [Number of T. Rowe Price | | Principal Occupation(s) and Directorships of Public Companies and |

| Portfolios Overseen] | | Other Investment Companies During the Past Five Years |

| | | |

| Edward C. Bernard | | Director and Vice President, T. Rowe Price; Vice Chairman of the |

| (1956) | | Board, Director, and Vice President, T. Rowe Price Group, Inc.; |

| 2006 | | Chairman of the Board, Director, and President, T. Rowe Price |

| [184] | | Investment Services, Inc.; Chairman of the Board and Director, |

| | T. Rowe Price Retirement Plan Services, Inc., and T. Rowe Price |

| | Services, Inc.; Chairman of the Board, Chief Executive Officer, |

| | | Director, and President, T. Rowe Price International and T. Rowe |

| | Price Trust Company; Chairman of the Board, all funds |

| | | |

| Edward A. Wiese, CFA | | Vice President, T. Rowe Price, T. Rowe Price Group, Inc., T. Rowe |

| (1959) | | Price International, and T. Rowe Price Trust Company; Vice President, |

| 2015 | | Tax-Exempt Money Fund |

| [54] | | |

| |

| *Each inside director serves until retirement, resignation, or election of a successor. |

| Officers |

| |

| Name (Year of Birth) | | |

| Position Held With Tax-Exempt | | |

| Money Fund | | Principal Occupation(s) |

| | | |

| Austin Applegate (1974) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc.; formerly, Senior Municipal Credit |

| | Research Analyst, Barclays (to 2011) |

| | | |

| Darrell N. Braman (1963) | | Vice President, Price Hong Kong, Price |

| Vice President | | Singapore, T. Rowe Price, T. Rowe Price Group, |

| | Inc., T. Rowe Price International, T. Rowe Price |

| | Investment Services, Inc., and T. Rowe Price |

| | Services, Inc. |

| | | |

| Steven G. Brooks, CFA (1954) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| M. Helena Condez (1962) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| G. Richard Dent (1960) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Stephanie A. Gentile, CFA (1956) | | Vice President, T. Rowe Price; formerly Director, |

| Vice President | | Credit Suisse Securities (to 2014) |

| | | |

| John R. Gilner (1961) | | Chief Compliance Officer and Vice President, |

| Chief Compliance Officer | | T. Rowe Price; Vice President, T. Rowe Price |

| | Group, Inc., and T. Rowe Price Investment |

| | Services, Inc. |

| | | |

| Dominic Janssens (1965) | | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President | | Group, Inc., and T. Rowe Price Trust Company |

| | | |

| Paul J. Krug, CPA (1964) | | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President | | Group, Inc., and T. Rowe Price Trust Company |

| | | |

| Marcy M. Lash (1963) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Alan D. Levenson, Ph.D. (1958) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Patricia B. Lippert (1953) | | Assistant Vice President, T. Rowe Price and |

| Secretary | | T. Rowe Price Investment Services, Inc. |

| | | |

| Joseph K. Lynagh, CFA (1958) | | Vice President, T. Rowe Price, T. Rowe Price |

| President | | Group, Inc., and T. Rowe Price Trust Company |

| | | |

| Catherine D. Mathews (1963) | | Vice President, T. Rowe Price, T. Rowe Price |

| Treasurer and Vice President | | Group, Inc., and T. Rowe Price Trust Company |

| | | |

| Alexander S. Obaza (1981) | | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President | | Group, Inc., and T. Rowe Price Trust Company |

| | | |

| David Oestreicher (1967) | | Director, Vice President, and Secretary, T. Rowe |

| Vice President | | Price Investment Services, Inc., T. Rowe Price |

| | Retirement Plan Services, Inc., T. Rowe |

| | Price Services, Inc., and T. Rowe Price Trust |

| | Company; Chief Legal Officer, Vice President, |

| | and Secretary, T. Rowe Price Group, Inc.; Vice |

| | President and Secretary, T. Rowe Price and |

| | T. Rowe Price International; Vice President, |

| | Price Hong Kong and Price Singapore |

| | | |

| John W. Ratzesberger (1975) | | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President | | Group, Inc., and T. Rowe Price Trust Company; |

| | formerly, North American Head of Listed |

| | Derivatives Operation, Morgan Stanley |

| | (to 2013) |

| | | |

| Deborah D. Seidel (1962) | | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President | | Group, Inc., T. Rowe Price Investment Services, |

| | Inc., and T. Rowe Price Services, Inc. |

| | | |

| Chen Shao (1980) | | Vice President, T. Rowe Price |

| Assistant Vice President | | |

| | | |

| Douglas D. Spratley, CFA (1969) | | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President | | Group, Inc. |

| | | |

| Jeffrey T. Zoller (1970) | | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President | | International, and T. Rowe Price Trust Company |

| |

| Unless otherwise noted, officers have been employees of T. Rowe Price or T. Rowe Price International for at least 5 years. |

Item 2. Code of Ethics.

The registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of this code of ethics is filed as an exhibit to this Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Directors/Trustees has determined that Mr. Bruce W. Duncan qualifies as an audit committee financial expert, as defined in Item 3 of Form N-CSR. Mr. Duncan is considered independent for purposes of Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

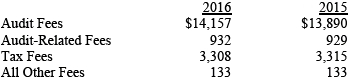

(a) – (d) Aggregate fees billed for the last two fiscal years for professional services rendered to, or on behalf of, the registrant by the registrant’s principal accountant were as follows:

Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. Audit-related fees include amounts reasonably related to the performance of the audit of the registrant’s financial statements and specifically include the issuance of a report on internal controls and, if applicable, agreed-upon procedures related to fund acquisitions. Tax fees include amounts related to services for tax compliance, tax planning, and tax advice. The nature of these services specifically includes the review of distribution calculations and the preparation of Federal, state, and excise tax returns. All other fees include the registrant’s pro-rata share of amounts for agreed-upon procedures in conjunction with service contract approvals by the registrant’s Board of Directors/Trustees.

(e)(1) The registrant’s audit committee has adopted a policy whereby audit and non-audit services performed by the registrant’s principal accountant for the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant require pre-approval in advance at regularly scheduled audit committee meetings. If such a service is required between regularly scheduled audit committee meetings, pre-approval may be authorized by one audit committee member with ratification at the next scheduled audit committee meeting. Waiver of pre-approval for audit or non-audit services requiring fees of a de minimis amount is not permitted.

(2) No services included in (b) – (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50 percent of the hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) The aggregate fees billed for the most recent fiscal year and the preceding fiscal year by the registrant’s principal accountant for non-audit services rendered to the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant were $2,554,000 and $2,042,000, respectively.

(h) All non-audit services rendered in (g) above were pre-approved by the registrant’s audit committee. Accordingly, these services were considered by the registrant’s audit committee in maintaining the principal accountant’s independence.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

(a) Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

Not applicable.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.

(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is attached.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant's principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

T. Rowe Price Tax-Exempt Money Fund, Inc.

| | By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| |

| Date April 20, 2016 | | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| | By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| |

| Date April 20, 2016 | | |

| |

| |

| By | /s/ Catherine D. Mathews |

| | Catherine D. Mathews |

| | Principal Financial Officer |

| |

| Date April 20, 2016 | | |