Nasdaq: PEBO April 12, 2007

Welcome to our …

Annual Shareholders Meeting

1

Today’s agenda

•

Updated profile of Peoples Bancorp.

•

2006 in review.

•

“Working Together”: Universal Financial Services.

•

Strategies and future outlook.

•

Q&A session.

2

Disclaimer

Please note and understand that commentary in this presentation may contain projections or other forward-looking statements regarding future events or Peoples Bancorp’s (“Peoples”) future financial performance. These statements are based on management’s current expectations. The statements in this presentation which are not historical fact are forward looking statements that involve a number of risks and uncertainties, including, but not limited to, the interest rate environment; the effect of federal and/or state banking, insurance, and tax regulations; the effect of technological changes; the effect of economic conditions; the impact of competitive products and pricing; and other risks detailed in Peoples’ Securities and Exchange Commission filings. Although management believes that the expectations in these forward-looking statements are based on reasonable assumptions within the bounds of management's knowledge of Peoples’ business and operations, it is possible that actual results may differ materially from these projections. Peoples disclaims any responsibility to update these forward-looking statements.

3

Management change

Earlier this week …

•

Chief Financial Officer and Treasurer Donald J. Landers resigned his position.

•

Carol A. Schneeberger, Executive Vice President of Operations, has been named interim CFO and Treasurer.

–

Nearly 30 years experience and active member of key financial committees at Peoples Bancorp.

–

Search for permanent CFO to begin in the near-term.

4

PEBO at a glance

Banking

Investments

Insurance

e-Banking

Assets: $1.9 billion

Associates: 580

Locations: 48

ATMs: 37

130,000 customers

5

2006

in

review

review

6

Earnings and dividend growth

All data adjusted for stock splits and dividends.

$2.01

$0.83

$29.70

$15.89

$1.47

$0.49

EPS CAGR = 6%

DPS CAGR = 11% (41 consecutive annual increases)

7

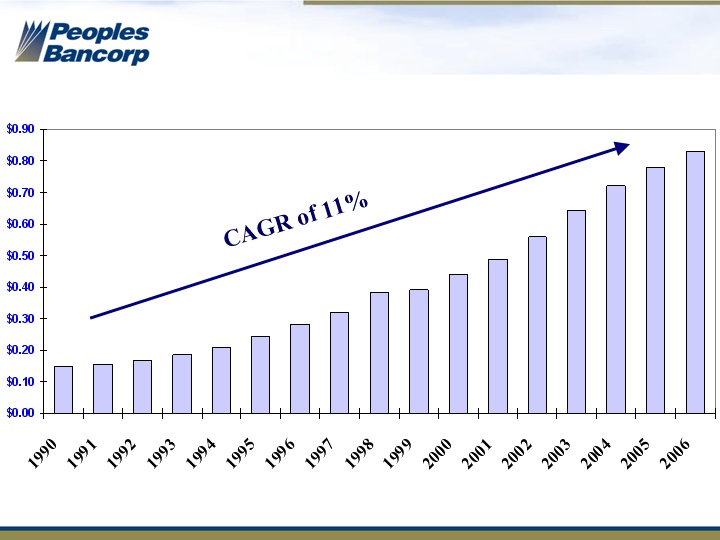

Dividends since 1990

All data adjusted for stock splits and dividends.

$0.83

$0.15

8

2006 Performance Ratios

Peoples Bancorp Inc. | Midwest Peer Median (1) | |

1 Yr EPS Growth | 3.6% | 4.7% |

Return on Assets | 1.15% | 1.01% |

Return on Equity | 11.33% | 12.56% |

Return on Tangible Equity | 18.87% | 15.71% |

Efficiency Ratio (2) | 57.51% | 62.57% |

(1) Publicly traded financial companies in Midwest US with $1 to $5 billion in assets. Source: SNL Securities.

(2) Lower number reflects better performance.

9

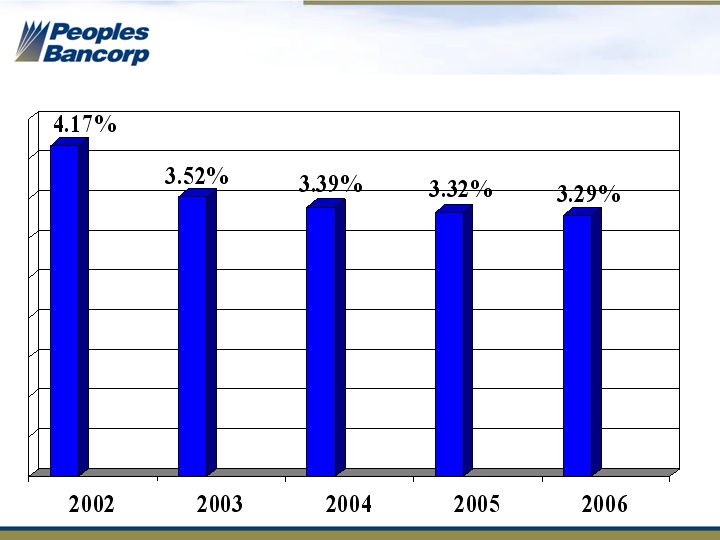

Net interest margin

10

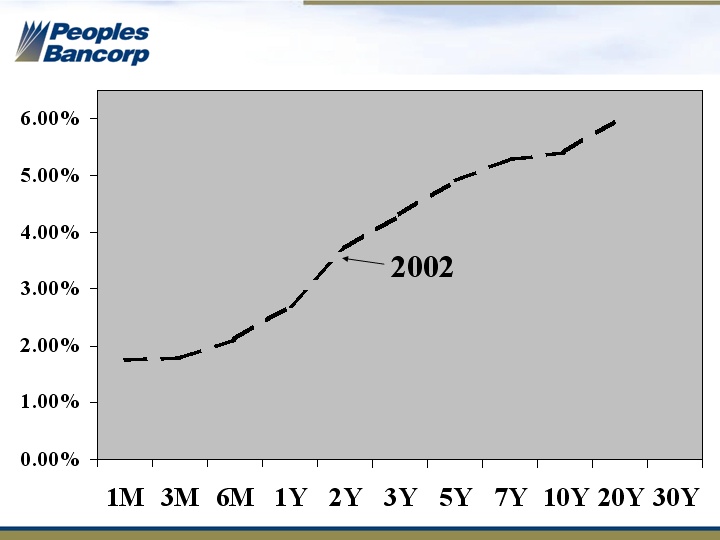

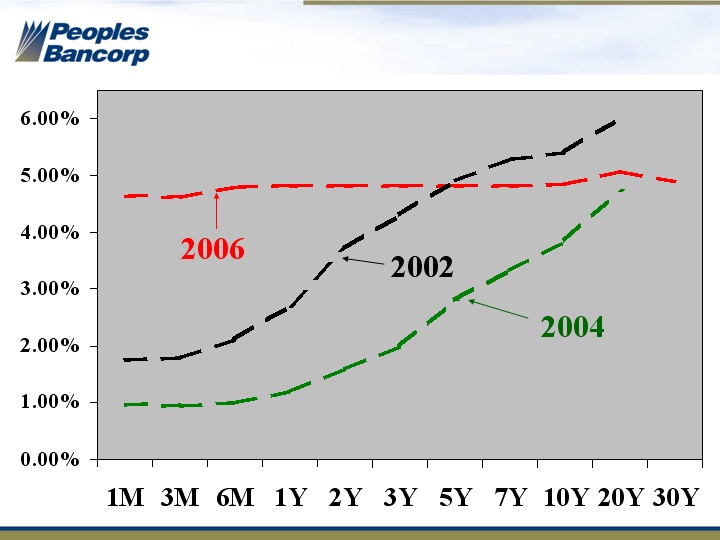

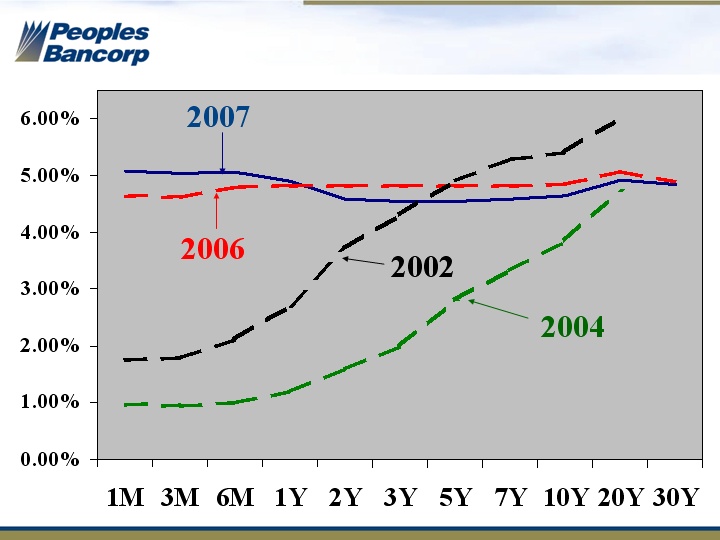

US Treasury yield curve

11

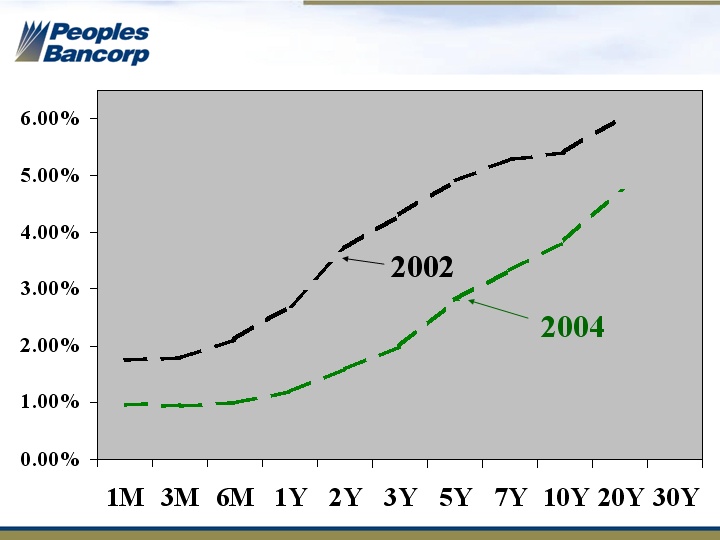

US Treasury yield curve

12

US Treasury yield curve

13

US Treasury yield curve

14

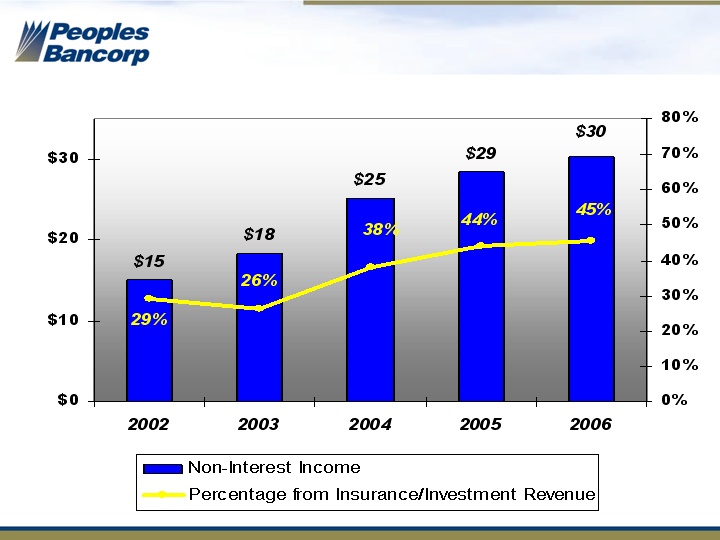

Non-interest income

($ in millions)

15

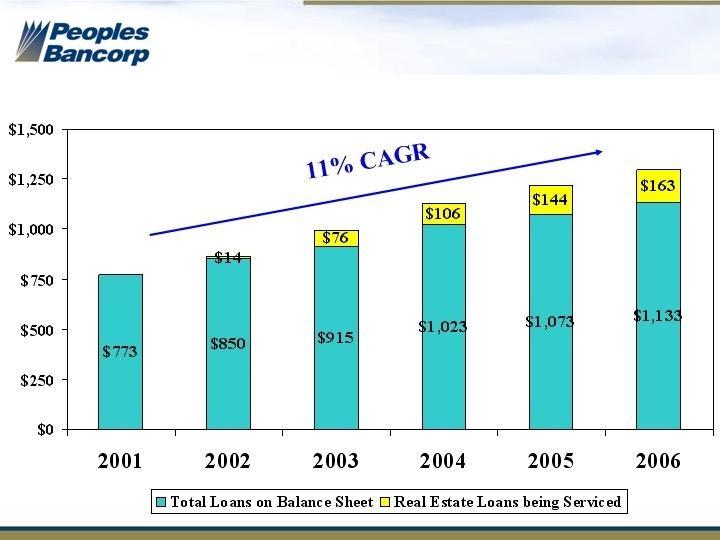

$773

(in millions)

Loan growth

(in millions)

$1,296

16

Loan quality

Peoples Bancorp Inc. 2006 | Midwest Peer Group Median 2006 | Peoples Bancorp Inc. Last 5 Year Average | |

Net Loan Chargeoffs to Average Loans | 0.29% | 0.18% | 0.24% |

Nonperforming Loans to Total Loans | 0.88% | 0.67% | 0.75% |

Allowance for Loan Losses to Total Loans | 1.28% | 1.11% | 1.44% |

17

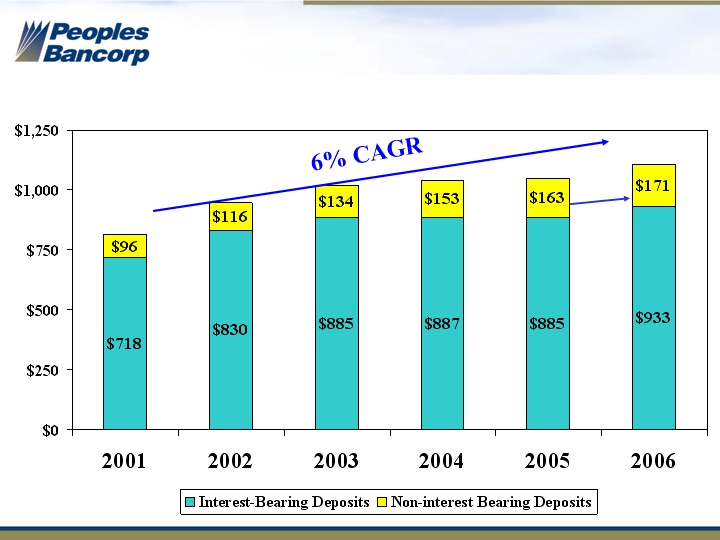

Customer deposit growth

$814

$1,104

($ in millions, excludes brokered CD’s)

+5%

18

“Freedom Force”

•

Targeted marketing campaign designed to attract new

customers.

customers.

•

13% increase in checking account sales over previous year.

“Remote Deposit Capture”

•

Technology that makes banking easier for businesses.

•

Allows us to gather deposits in areas with fewer

branches.

19

Summary Financial Data

($000) | At or For December 31, 2006 | At or For December 31, 2005 | Variance |

| Total Assets | $1,875,000 | $1,855,000 | + 1% |

| Total Loans | $1,132,000 | $1,072,000 | + 6% |

| Allowance for Loan Losses | $14,509 | $14,720 | - 1% |

| Total Deposits (1) | $1,104,000 | $1,048,000 | + 5% |

| Total Revenues | $84,342 | $81,473 | + 4% |

| Net Interest Income | $53,217 | $52,306 | + 2% |

| Non-Interest Income | $31,125 | $29,167 | + 7% |

| Provision for Loan Losses | $3,622 | $2,028 | + 79% |

| Non-Interest Expense | $51,297 | $51,342 | Flat |

| Net Income | $21,558 | $20,499 | + 5% |

(1) Excludes brokered CD’s.

20

Working

Together:

We're

We're

Better !

21

–

E-Banking capabilities

–

Full-service offices

–

Loan production office in Westerville, OH

Comprehensive

commercial and

consumer

banking

products

commercial and

consumer

banking

products

22

•

Assets under management $845 million

–

Services $735 million

•

Trusts and Estates

•

Investment Management

•

Employee Benefit Plans

–

Brokerage (Raymond James) $110 million

23

•

2006 property and casualty revenues: $7.8 million.

–

Primarily commercial lines, with some personal lines, life, and health insurance.

–

Over 40 licensed producers.

–

Opportunity for continued integration of customer relationships.

24

Our strategies and

future outlook …

25

“Take care of our customers”

•

Have size and scope to offer universal financial services.

•

Be small enough to maintain fast, friendly community minded approach.

•

Build lasting relationships with our customers.

•

Win with our people.

–

Be a good teammate.

•

To each other.

•

To our communities.

26

Community Reinvestment Act Performance Evaluation

Peoples Bancorp associates volunteered over 25,000

hours to local charities and community events

Peoples Bank Earned a CRA rating of

Outstanding

27

Our strategies

•

Focus on customers first.

•

Build lasting relationships by anticipating and meeting their needs.

•

Work together as a true team across all product lines to leverage our “universal” financial services offering.

•

Continue technology enhancements that make it easier for customers to do business with us.

•

Expand in economically vibrant markets.

28

Lancaster, OH expansion

2Q 2007

29

2006 Merger & Acquisition Activity

•

Opened de novo full-service office with ATM in Lancaster, OH

•

Acquired full-service office in Carroll, OH

•

Sold Chesterhill, OH & South Shore, KY offices.

30

-

Full Service

Office with

Drive-Thru and

ATM

Drive-Thru and

ATM

-

Expected

opening in

October 2007

October 2007

-

Will be 2nd office

in Huntington

Huntington, WV expansion

31

Some challenges

•

Flat to inverted yield curve.

–

When will it change?

•

Economic conditions.

–

If economy slows, will loan quality be OK?

•

Competition for deposits.

–

Interest rate environment and “thirst” for funding

sources at an all time high.

•

Increasing regulatory burden.

–

Now more than ever . . .

32

PEBO stock price vs. S&P 100 in last 12 months

PEBO

S&P 500

YTD PEBO – down 12.9%

YTD Midwest Peer Median – down 9.7%

33

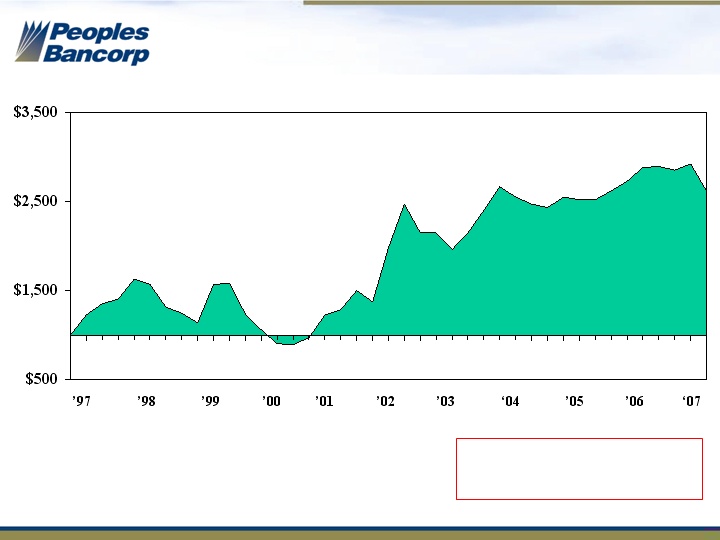

Measures PEBO investment on 3/31/1997 through 3/31/2007.

Assumes quarterly dividend reinvestment.

10.1%

Compound Average

Annual Return

$2,617

5-year CAGR = 7.7%

20-year CAGR = 14.5%

10-year total shareholder return

34

Our strengths

•

Diversified revenue streams.

–

Our product offerings make us truly a “full-service”

company ... Unique for our size.

•

Proven track record of revenue growth.

•

Core competency of growth through acquisition.

•

Consistent dividend increases.

–

41 consecutive years.

35

DISCUSSION

Mark Bradley, President and Chief Executive Officer

Thank you for your attendance and support !

36