|

Exhibit 99.1

|

Exhibit 99.1

Whatever it takes friendly UNITED A STAR ALLIANCE MEMBER

Jim Compton

Vice Chairman & Chief Revenue Officer John Rainey EVP & Chief Financial Officer

Safe Harbor Statement

Certain statements included in this release are forward - looking and thus reflect our current expectations and beliefs with respect to certain current and future events and financial performance. Such forward - looking statements are and will be subject to many risks and uncertainties relating to our operations and business environment that may cause actual results to differ materially from any future results expressed or implied in such forward - looking statements. Words such as “expects,” “will,” “plans,” “anticipates,” “indicates,” “believes,” “forecast,” “guidance,” “outlook” and similar expressions are intended to identify forward - looking statements. Additionally, forward - looking statements include statements that do not relate solely to historical facts, such as statements which identify uncertainties or trends, discuss the possible future effects of current known trends or uncertainties or which indicate that the future effects of known trends or uncertainties cannot be predicted, guaranteed or assured. All forward - looking statements in this report are based upon information available to us on the date of this report. We undertake no obligation to publicly update or revise any forward - looking statement, whether as a result of new information, future events, changed circumstances or otherwise, except as required by applicable law. Our actual results could differ materially from these forward - looking statements due to numerous factors including, without limitation, the following: our ability to comply with the terms of our various financing arrangements; the costs and availability of financing; our ability to maintain adequate liquidity; our ability to execute our operational plans; our ability to control our costs, including realizing benefits from our resource optimization efforts, cost reduction initiatives and fleet replacement programs; our ability to utilize our net operating losses; our ability to attract and retain customers; demand for transportation in the markets in which we operate; an outbreak of a disease that affects travel demand or travel behavior; demand for travel and the impact that global economic conditions have on customer travel patterns; excessive taxation and the inability to offset future taxable income; general economic conditions (including interest rates, foreign currency exchange rates, investment or credit market conditions, crude oil prices, costs of aircraft fuel and energy refining capacity in relevant markets); our ability to cost-effectively hedge against increases in the price of aircraft fuel; any potential realized or unrealized gains or losses related to fuel or currency hedging programs; the effects of any hostilities, act of war or terrorist attack; the ability of other air carriers with whom we have alliances or partnerships to provide the services contemplated by the respective arrangements with such carriers; the costs and availability of aviation and other insurance; the costs associated with security measures and practices; industry consolidation or changes in airline alliances; competitive pressures on pricing and on demand; our capacity decisions and the capacity decisions of our competitors; U.S. or foreign governmental legislation, regulation and other actions (including open skies agreements and environmental regulations); labor costs; our ability to maintain satisfactory labor relations and the results of the collective bargaining agreement process with our union groups; any disruptions to operations due to any potential actions by our by our labor groups; weather conditions; the possibility that expected merger synergies will not be realized or will not be realized within the expected time period; and other risks and uncertainties set forth under Item 1A, Risk Factors, of UAL’s Annual Report on Form 10-K, as well as other risks and uncertainties set forth from time to time in the reports we file with the SEC.

2

Committed to running a great airline and improving returns

Deliver Improve efficiency Strengthen Expand revenue reliability and quality balance sheet

3

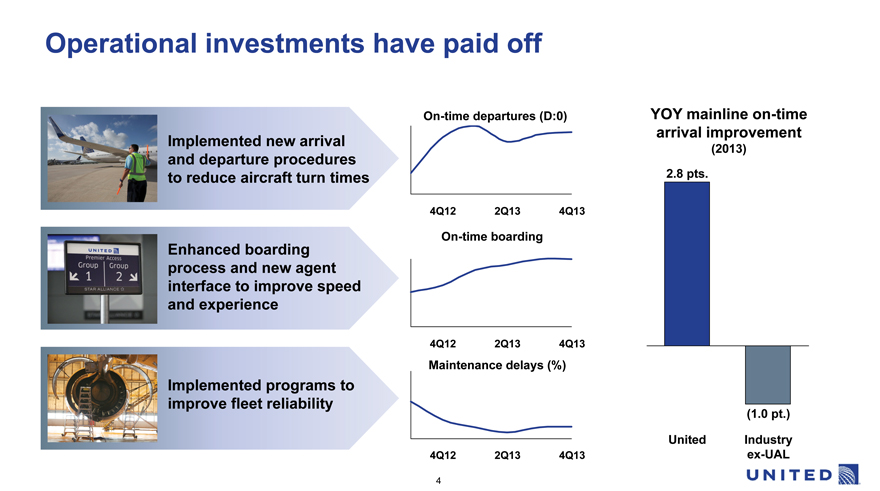

Operational investments have paid off

Implemented new arrival and departure procedures to reduce aircraft turn times

Enhanced boarding process and new agent interface to improve speed and experience

Implemented programs to improve fleet reliability

On-time departures (D:0) YOY mainline on-time arrival improvement

(2013)

2.8 pts.

4Q12 2Q13 4Q13

On-time boarding

4Q12 2Q13 4Q13

Maintenance delays (%)

(1.0 pt.)

United Industry

4Q12 2Q13 4Q13 ex-UAL

4

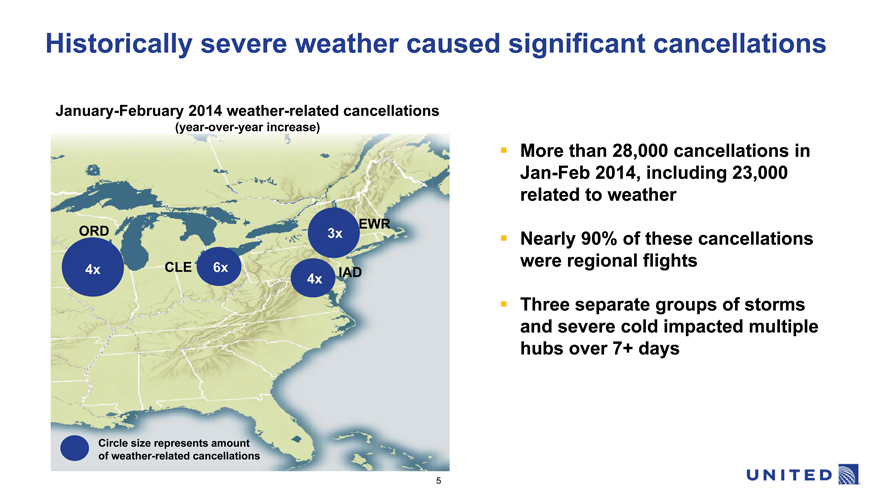

Historically severe weather caused significant cancellations

January -February 2014 weather-related cancellations

(year-over-year increase)

EWR ORD 3x

4x CLE 6x IAD

4x

Circle size represents amount of weather-related cancellations

More than 28,000 cancellations in Jan-Feb 2014, including 23,000 related to weather

Nearly 90% of these cancellations were regional flights

Three separate groups of storms and severe cold impacted multiple hubs over 7+ days

5

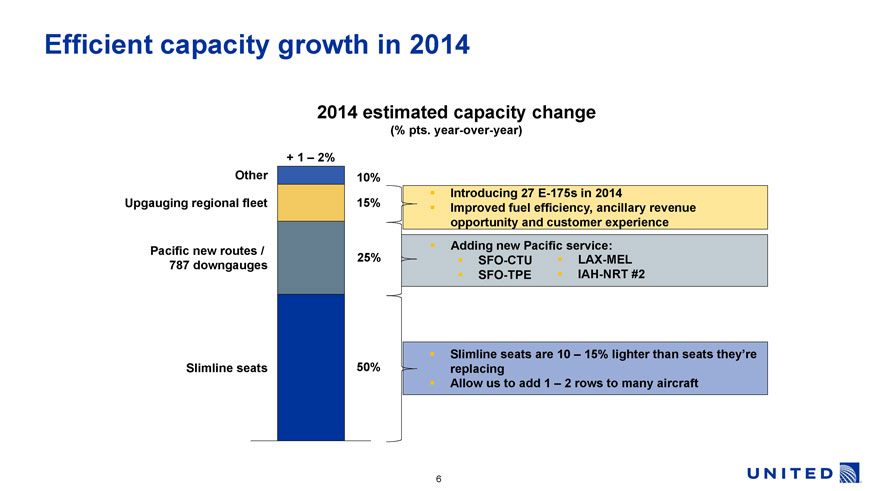

Efficient capacity growth in 2014

2014 estimated capacity change

(% pts. year-over-year)

+ 1 – 2%

Other

Upgauging regional fleet

Pacific new routes / 787 downgauges

Slimline seats

10%

15%

25%

50%

Introducing 27 E-175s in 2014

Improved fuel efficiency, ancillary revenue opportunity and customer experience

Adding new Pacific service:

SFO-CTU

SFO-TPE

LAX-MEL

IAH-NRT #2

Slimline seats are 10 – 15% lighter than seats they’re replacing

Allow us to add 1 – 2 rows to many aircraft

UNITED

6

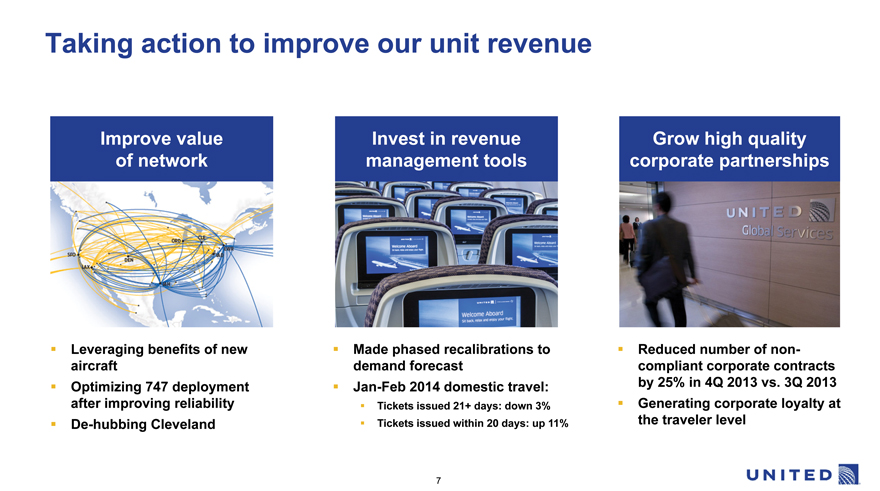

Taking action to improve our unit revenue

Improve value Invest in revenue Grow high quality of network management tools corporate partnerships

Leveraging benefits of new Made phased recalibrations to Reduced number of non- aircraft demand forecast compliant corporate contracts

Optimizing 747 deployment Jan-Feb 2014 domestic travel: by 25% in 4Q 2013 vs. 3Q 2013 after improving reliability Tickets issued 21+ days: down 3% Generating corporate loyalty at

De-hubbing Cleveland Tickets issued within 20 days: up 11% the traveler level

7

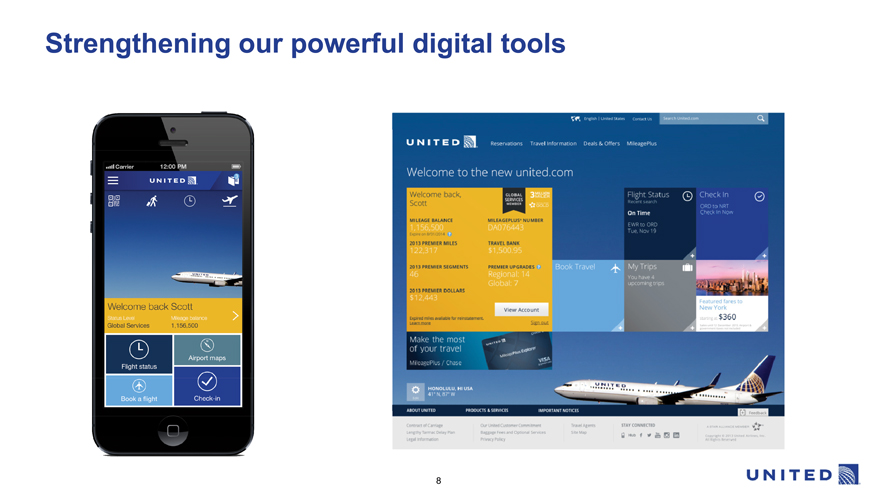

Strengthening our powerful digital tools

8

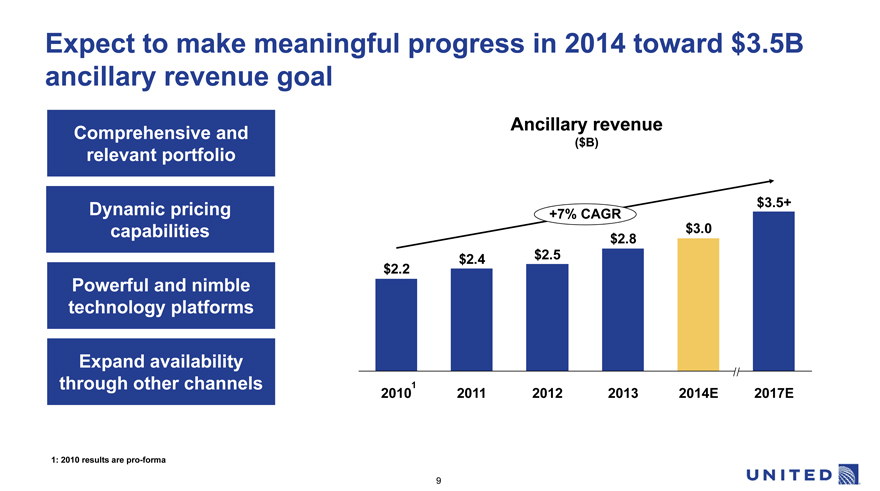

Expect to make meaningful progress in 2014 toward $3.5B ancillary revenue goal

Ancillary revenue Comprehensive and

($B)

relevant portfolio

Dynamic pricing $3.5+

+7%CAGR

capabilities $3.0

$2.8 $2.4 $2.5 $2.2

Powerful and nimble technology platforms

Expand availability through other channels 1

2010 2011 2012 2013 2014E 2017E

1: 2010 results are pro-forma

9

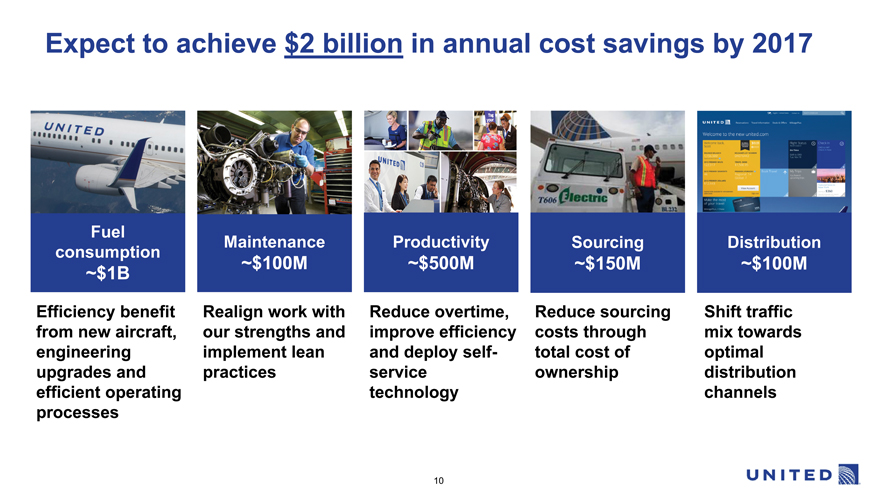

Expect to achieve $2 billion in annual cost savings by 2017

Fuel

Maintenance Productivity Sourcing Distribution consumption

~$100M ~$500M ~$150M ~$100M ~$1B

Efficiency benefit Realign work with Reduce overtime, Reduce sourcing Shift traffic from new aircraft, our strengths and improve efficiency costs through mix towards engineering implement lean and deploy self- total cost of optimal upgrades and practices service ownership distribution efficient operating technology channels processes

10

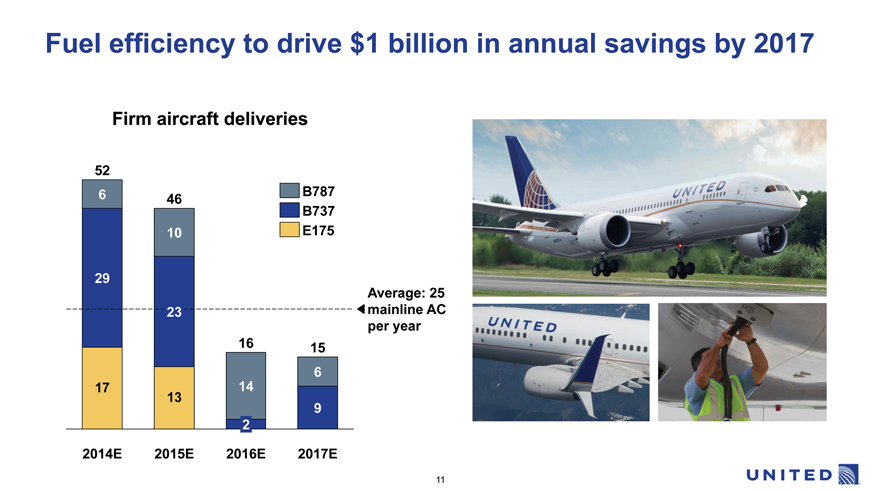

Fuel efficiency to drive $1 billion in annual savings by 2017

Firm aircraft deliveries

52

6 B787 46 B737

10 E175

29

Average: 25 23 mainline AC per year

16 15 6

17 14 13

9 2

2014E 2015E 2016E 2017E

11

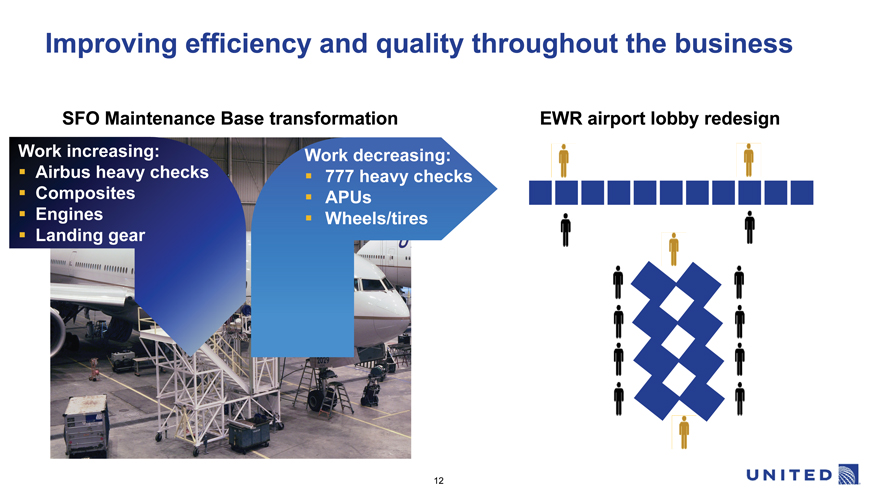

Improving efficiency and quality throughout the business

SFO Maintenance Base transformation EWR airport lobby redesign

Work increasing: Work decreasing:

Airbus heavy checks 777 heavy checks

Composites APUs

Engines Wheels/tires

Landing gear

12

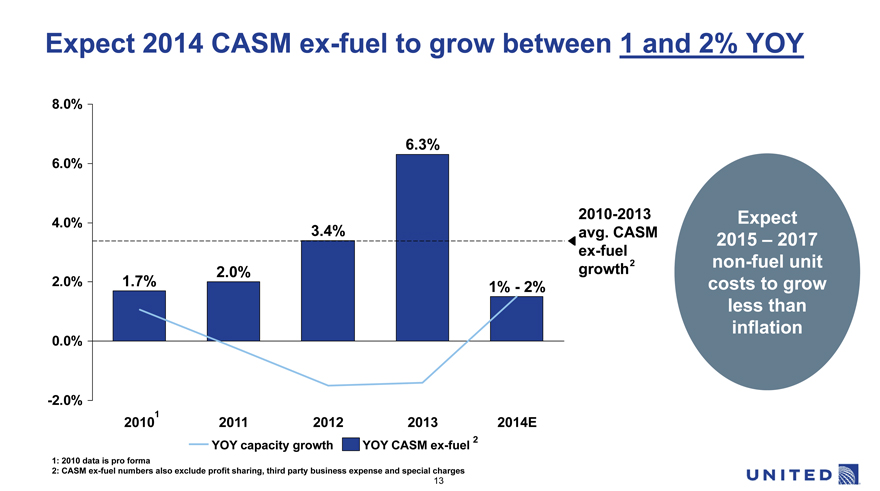

Expect 2014 CASM ex-fuel to grow between 1 and 2% YOY

8.0%

6.3%

6.0%

2010-2013 Expect

4.0%

3.4% avg. CASM

2015 – 2017

ex-fuel

growth 2 non-fuelunit

2.0%

2.0% 1.7% 1% -2% costs to grow less than 00% inflation

-2.0%

1

2010 2011 2012 2013 2014E

YOY capacity growth YOY CASM ex-fuel 2

1: 2010 data is pro forma

2: CASM ex-fuel numbers also exclude profit sharing, third party business expense and special charges

13

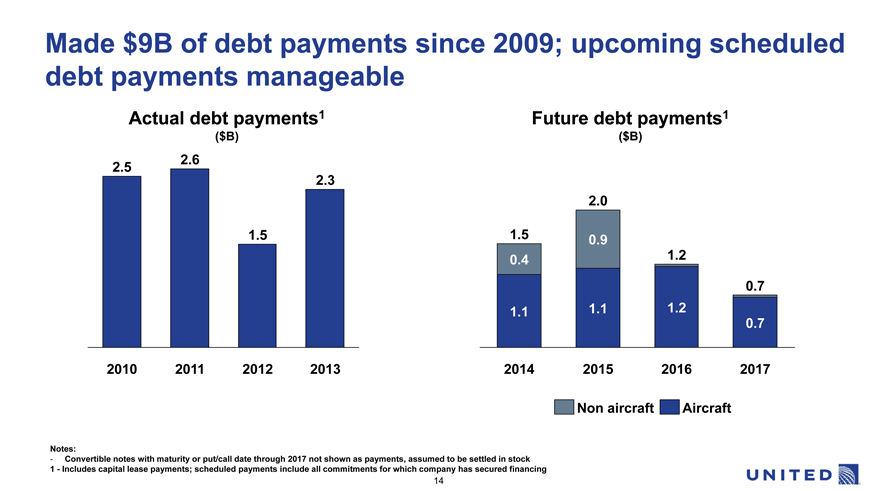

Made $9B of debt payments since 2009; upcoming scheduled debt payments manageable

Actual debt payments 1 Future debt payments 1

($B) ($B)

2.6 2.5

2.3

2.0

1.5 1.5 0.9

0.4 1.2

0.7 1.1 1.1 1.2 0.7

2010 2011 2012 2013 2014 2015 2016 2017

Non aircraft Aircraft

Notes:

- Convertible notes with maturity or put/call date through 2017 not shown as payments, assumed to be settled in stock 1-Includes capital lease payments; scheduled payments include all commitments for which company has secured financing

14

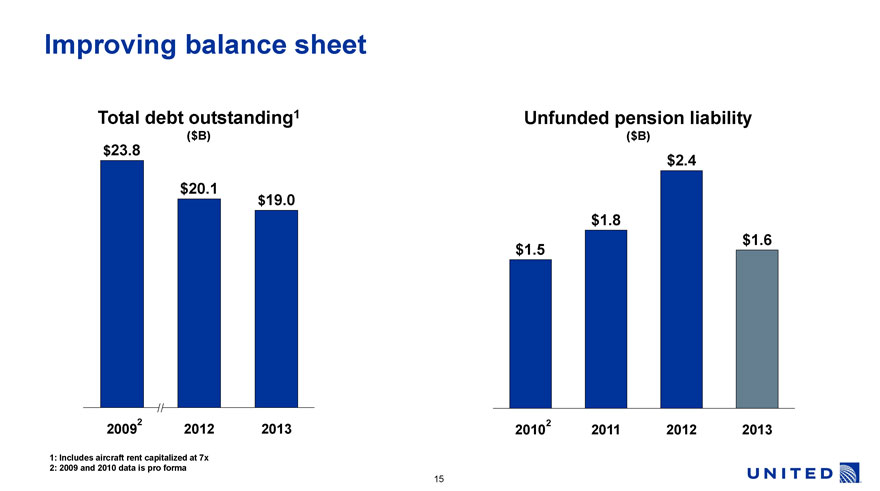

Improving balance sheet

Total debt outstanding1

($B)

$23.8

$20.1

$19.0

2009 2

2012

2013

Unfunded pension liability

($B)

$1.5

$1.8

$2.4

$1.6

2010 2

2011

2012

2013

1: Includes aircraft rent capitalized at 7x

2: 2009 and 2010 data is pro forma

UNITED

15

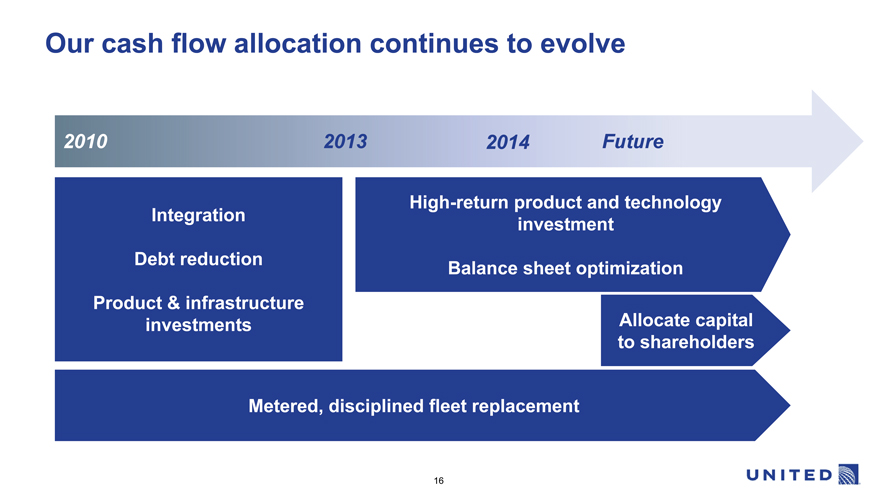

Our cash flow allocation continues to evolve

High-return product and technology Integration investment Debt reduction Balance sheet optimization Product & infrastructure investments Allocate capital to shareholders

Metered, disciplined fleet replacement

16

Improving long-term shareholder value

Generate ROIC greater than 10%

Increase earnings by 2-4x

Improve capital structure

Balance free cash flow allocation

17