QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registranto | ||

Filed by a Party other than the Registrantý | ||

Check the appropriate box: | ||

o | Preliminary Proxy Statement | |

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

o | Definitive Proxy Statement | |

o | Definitive Additional Materials | |

ý | Soliciting Material under §240.14a-12 | |

| EQT Corporation | ||||

(Name of Registrant as Specified In Its Charter) | ||||

JANA Partners LLC | ||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

Payment of Filing Fee (Check the appropriate box): | ||||

ý | No fee required. | |||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

o | Fee paid previously with preliminary materials. | |||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

(1) | Amount Previously Paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

October 2, 2017

Board of Directors (the "Board")

EQT Corporation

625 Liberty Avenue, Suite 1700

Pittsburgh, Pennsylvania 15222

Ladies & Gentlemen,

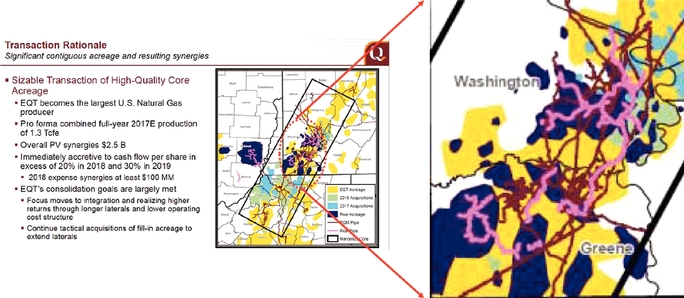

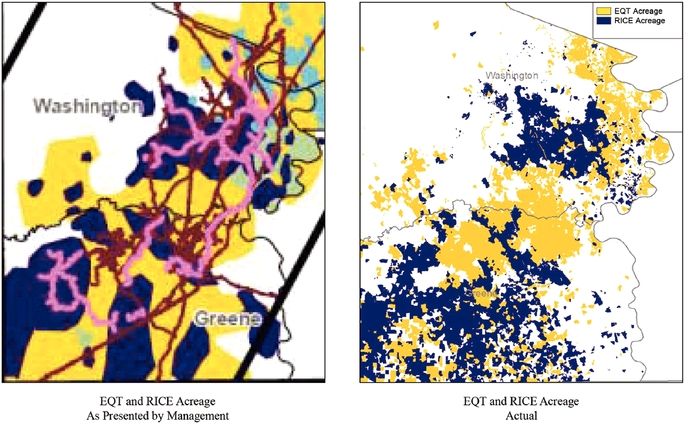

As you know, JANA Partners LLC ("we" or "us") believes that EQT Corporation ("EQT" or the "Company") shareholders should vote against the overpriced and dilutive acquisition of Rice Energy ("Rice") and that EQT should immediately commit to a separation through a spinoff of its midstream business. As set forth inExhibit A, EQT has published a map of the combined EQT/Rice land holdings that appear to show vast tracts of contiguous acreage which can be efficiently drilled by the combined company, and thus would produce the 1,200 wells with 12,000 foot laterals in Washington and Greene counties that are the linchpin of EQT's rationale for the transaction.Exhibit B, however, shows that EQT's map is blatantly deceptive. With the help of a leading petroleum engineering firm with extensive experience in the Appalachian basin and experienced industry operators, and using publicly available information, we have magnified EQT's map and it is obvious that many of the tracts which appear contiguous never actually touch. This means that for EQT to fulfill its promises with respect to longer drilling laterals, three things would need to be true:

- •

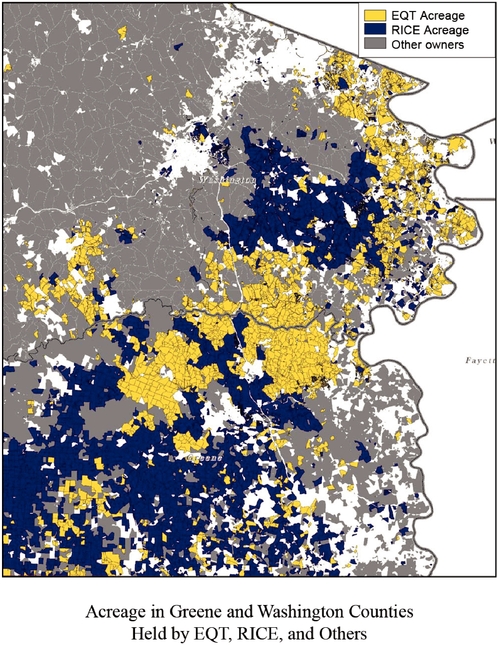

- EQT would need to have access to the hundreds of plots of land between EQT and Rice drilling areas.However, this would require an unquantified and likely very large expenditure of time and capital in addition to the $8.2 billion EQT proposes to pay for Rice, and in any event is highly unlikely given that, as shown inExhibit C, these properties are largely controlled by other operators. If these lots were readily accessible, presumably EQT or Rice would have already purchased or leased them.

- •

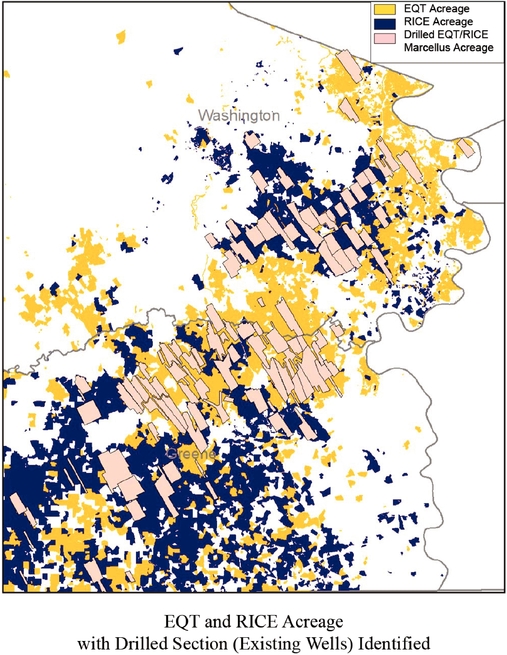

- This additional required acreage would need to be undrilled.However, our work shows that hundreds of wells have already been drilled in the adjacent acreage.

- •

- The lots already controlled by EQT and Rice that abut the additional required acreage would need to not have any wells already drilled by EQT or Rice along the abutting borders.However, Exhibit D makes clear that this is not the case.

In short, an accurate analysis of the undeveloped combined EQT and Rice acreage cannot support anything close to the 1,200 well locations that EQT management says can be drilled to 12,000 foot lateral lengths. There simply is not the real estate to support management's claims.

We are presenting our latest findings in detail because we think every Board member should see for themselves the distance between the transaction they have attempted to sell to shareholders and reality, and ask themselves whether they think they have complied with their fiduciary duty in evaluating this proposed acquisition and presenting it to shareholders. We also believe that the Board's insistence on putting the Rice transaction to a shareholder vote before announcing how it intends to address the Company's persistent sum of the parts discount, in fact even before it begins consideration of this issue, is completely inexcusable. The Board is in effect asking shareholders to overlook EQT's history of value-destroying acquisitions and foot-dragging on addressing its undervaluation and trust that the Board will make the right decision for shareholders after winning approval to acquire Rice. If it was not clear before, we think it is crystal clear now that the Board has not earned that trust.

The case for opposing the Rice acquisition, demanding immediate action to address EQT's persistent sum of the parts discount, and evaluating significant Board change at EQT is stronger than ever. Should you wish to discuss this matter further, we can be reached at (212) 455-0900.

| Sincerely, | ||

/s/ BARRY ROSENSTEIN Barry Rosenstein Managing Partner JANA Partners LLC |

Additional Information

JANA Partners LLC ("JANA") intends to file with the SEC a definitive proxy statement and an accompanying proxy card to be used to solicit proxies in connection with the upcoming special meeting of shareholders of EQT Corporation (the "Company"), including any adjournments or postponements thereof or any other meeting that may be called in lieu thereof (the "Special Meeting"). Information relating to the participant in such proxy solicitation has been included in a preliminary proxy statement filed by JANA with the SEC on September 11, 2017 and in any amendments to that preliminary proxy statement. Shareholders are advised to read the definitive proxy statement and any other documents related to the solicitation of shareholders of the Company in connection with the Special Meeting when they become available because they will contain important information, including additional information relating to JANA. These materials and other materials filed by JANA in connection with the solicitation of proxies will be available at no charge at the SEC's website at www.sec.gov. The definitive proxy statement (when available) and other relevant documents filed by JANA with the SEC will also be available, without charge, on request from JANA's proxy solicitor, Okapi Partners LLC, at (855) 208-8902 or via email at info@okapipartners.com.

Exhibit A

Exhibit B

Exhibit C

Exhibit D