UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ☐ | Definitive Proxy Statement | |

| ☐ | Definitive Additional Materials | |

| ☒ | Soliciting Material Pursuant to §240.14a-12 | |

EXXON MOBIL CORPORATION

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. | |||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ☐ | Fee paid previously with preliminary materials. | |||

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

2021 INVESTOR DAY Virtual Webcast / 03.03.212021 INVESTOR DAY Virtual Webcast / 03.03.21

CAUTIONARY STATEMENT FORWARD-LOOKING STATEMENTS. Outlooks; projections; goals; estimates; discussions of earnings, cash flow, margins, and resource potential; descriptions of strategic plans and objectives; planned capital and cash operating expense reductions and the ability to meet or exceed announced reduction objectives; plans to reduce future emissions intensity and the expected resulting absolute emissions reductions; emission profiles of future developments; carbon capture results and the impact of operational and technology efforts; future business markets like carbon capture or hydrogen; the impacts of the COVID-19 pandemic and corresponding market impacts on ExxonMobil’s businesses and results; price and market recoveries; energy market evolution; recovery and production rates; rates of return; drilling programs and improvements; asset sales; reserve and resource additions; proved reserves and other resource volumes; development plans; future distributions; asset carrying values and any increases or impairments; integration benefits; and other statements of future events or conditions in this presentation or the subsequent discussion period are forward-looking statements. Actual future results could differ materially due to a number of factors. These include global and regional changes in the demand, supply, prices, differentials or other market conditions affecting oil, gas, petroleum, petrochemicals and feedstocks; company actions to protect the health and safety of employees, vendors, customers, and communities; the ability to access short- and long-term debt markets on a timely and affordable basis; the severity, length and ultimate impact of COVID-19 and government responses on people and economies; global population and economic growth; reservoir performance and depletion rates; the outcome of exploration projects and the timely completion of development and construction projects; regional differences in product concentration and demand; war, trade agreements, shipping blockades or harassment and other political, public health or security concerns; changes in law, taxes or regulation, including environmental regulations, taxes, political sanctions and international treaties; the timely granting or freeze, suspension or revocation of government permits; the resolution of contingencies and uncertain tax positions; the impact of fiscal and commercial terms and the outcome of commercial negotiations; feasibility and timing for regulatory approval of potential investments or divestments; the actions of competitors and preferences of customers; the capture of efficiencies between business lines; unexpected technological developments; general economic conditions, including the occurrence and duration of economic recessions; unforeseen technical or operating difficulties; the ability to bring new technologies to commercial scale on a cost- competitive basis, including large-scale hydraulic fracturing projects and carbon capture projects; and other factors discussed here, in Item 1A. Risk Factors in our Form 10-K for the year ended December 31, 2020 and under the heading Factors Affecting Future Results on the Investors page of our website at www.exxonmobil.com under the heading News & Resources. The forward-looking statements and dates used in this presentation are based on management’s good faith plans and objectives as of the March 3, 2021 date of this presentation, unless otherwise stated. We assume no duty to update these statements as of any future date and neither future distribution of this material nor the continued availability of this material in archive form on our website should be deemed to constitute an update or re-affirmation of these figures as of any future date. Any future update of these figures will be provided only through a public disclosure indicating that fact. SUPPLEMENTAL INFORMATION. See the Supplemental Information included on pages 64 through 74 of this presentation for additional important information required by Regulation G for non-GAAP measures or that the company considers is useful to investors as well as definitions of terms used in the materials, including future earnings, cash flow, margins, ROCE, returns, rate of return, addressable markets, available cash from operations, operating cash flow, cash operating expenses, net cash margin, free cash, free cash flow, and resource potential. Supplemental Information also includes information on the assumptions used in these materials, including assumptions on future crude oil prices and product margins used to develop outlooks regarding future potential outcomes of current management plans. 2CAUTIONARY STATEMENT FORWARD-LOOKING STATEMENTS. Outlooks; projections; goals; estimates; discussions of earnings, cash flow, margins, and resource potential; descriptions of strategic plans and objectives; planned capital and cash operating expense reductions and the ability to meet or exceed announced reduction objectives; plans to reduce future emissions intensity and the expected resulting absolute emissions reductions; emission profiles of future developments; carbon capture results and the impact of operational and technology efforts; future business markets like carbon capture or hydrogen; the impacts of the COVID-19 pandemic and corresponding market impacts on ExxonMobil’s businesses and results; price and market recoveries; energy market evolution; recovery and production rates; rates of return; drilling programs and improvements; asset sales; reserve and resource additions; proved reserves and other resource volumes; development plans; future distributions; asset carrying values and any increases or impairments; integration benefits; and other statements of future events or conditions in this presentation or the subsequent discussion period are forward-looking statements. Actual future results could differ materially due to a number of factors. These include global and regional changes in the demand, supply, prices, differentials or other market conditions affecting oil, gas, petroleum, petrochemicals and feedstocks; company actions to protect the health and safety of employees, vendors, customers, and communities; the ability to access short- and long-term debt markets on a timely and affordable basis; the severity, length and ultimate impact of COVID-19 and government responses on people and economies; global population and economic growth; reservoir performance and depletion rates; the outcome of exploration projects and the timely completion of development and construction projects; regional differences in product concentration and demand; war, trade agreements, shipping blockades or harassment and other political, public health or security concerns; changes in law, taxes or regulation, including environmental regulations, taxes, political sanctions and international treaties; the timely granting or freeze, suspension or revocation of government permits; the resolution of contingencies and uncertain tax positions; the impact of fiscal and commercial terms and the outcome of commercial negotiations; feasibility and timing for regulatory approval of potential investments or divestments; the actions of competitors and preferences of customers; the capture of efficiencies between business lines; unexpected technological developments; general economic conditions, including the occurrence and duration of economic recessions; unforeseen technical or operating difficulties; the ability to bring new technologies to commercial scale on a cost- competitive basis, including large-scale hydraulic fracturing projects and carbon capture projects; and other factors discussed here, in Item 1A. Risk Factors in our Form 10-K for the year ended December 31, 2020 and under the heading Factors Affecting Future Results on the Investors page of our website at www.exxonmobil.com under the heading News & Resources. The forward-looking statements and dates used in this presentation are based on management’s good faith plans and objectives as of the March 3, 2021 date of this presentation, unless otherwise stated. We assume no duty to update these statements as of any future date and neither future distribution of this material nor the continued availability of this material in archive form on our website should be deemed to constitute an update or re-affirmation of these figures as of any future date. Any future update of these figures will be provided only through a public disclosure indicating that fact. SUPPLEMENTAL INFORMATION. See the Supplemental Information included on pages 64 through 74 of this presentation for additional important information required by Regulation G for non-GAAP measures or that the company considers is useful to investors as well as definitions of terms used in the materials, including future earnings, cash flow, margins, ROCE, returns, rate of return, addressable markets, available cash from operations, operating cash flow, cash operating expenses, net cash margin, free cash, free cash flow, and resource potential. Supplemental Information also includes information on the assumptions used in these materials, including assumptions on future crude oil prices and product margins used to develop outlooks regarding future potential outcomes of current management plans. 2

AGENDA • Welcome Stephen Littleton Vice President, Investor Relations and Secretary • Growing shareholder value Darren Woods Chairman of the Board and Chief Executive Officer in a lower-carbon future • Upstream Neil Chapman Senior Vice President • Downstream and Chemical Jack Williams Senior Vice President • Financial plan Andrew Swiger Senior Vice President • Closing Darren Woods Chairman of the Board and Chief Executive Officer 3AGENDA • Welcome Stephen Littleton Vice President, Investor Relations and Secretary • Growing shareholder value Darren Woods Chairman of the Board and Chief Executive Officer in a lower-carbon future • Upstream Neil Chapman Senior Vice President • Downstream and Chemical Jack Williams Senior Vice President • Financial plan Andrew Swiger Senior Vice President • Closing Darren Woods Chairman of the Board and Chief Executive Officer 3

2021 INVESTOR DAY 2021 INVESTOR DAY

2020 PERSPECTIVE Delivered on commitments in a challenging environment while preserving long-term value • Managed global operations to supply essential energy and products with best-ever safety and reliability performance • Improved cash Opex by more than 15 percent with $3 billion of structural savings versus 2019 • Reduced capital investments by more than 30 percent while maintaining advantages and project value • Achieved 2020 emission-reduction goals and established new 2025 plans consistent with the goals of the Paris Agreement • Advanced key projects and achieved operational milestones in Guyana and the Permian Basin 52020 PERSPECTIVE Delivered on commitments in a challenging environment while preserving long-term value • Managed global operations to supply essential energy and products with best-ever safety and reliability performance • Improved cash Opex by more than 15 percent with $3 billion of structural savings versus 2019 • Reduced capital investments by more than 30 percent while maintaining advantages and project value • Achieved 2020 emission-reduction goals and established new 2025 plans consistent with the goals of the Paris Agreement • Advanced key projects and achieved operational milestones in Guyana and the Permian Basin 5

GROWING LONG-TERM SHAREHOLDER VALUE Progressing actions to highgrade portfolio and improve earnings and cash flow • Committed to delivering sustainable shareholder value • Competitively advantaged assets and investments drive strong cash flow to sustain dividend, reduce debt, and invest in the future • Significant structural cost savings and flexible Capex resilient to price cycles • Focused on industry-leading safety, reliability, and environmental performance; executing plans to deliver aggressive 2025 emission reductions • Strategy leverages experience and competitive advantages to deliver value while transitioning to a lower-carbon future, consistent with the goals of the Paris Agreement See Supplemental Information for definitions. 6GROWING LONG-TERM SHAREHOLDER VALUE Progressing actions to highgrade portfolio and improve earnings and cash flow • Committed to delivering sustainable shareholder value • Competitively advantaged assets and investments drive strong cash flow to sustain dividend, reduce debt, and invest in the future • Significant structural cost savings and flexible Capex resilient to price cycles • Focused on industry-leading safety, reliability, and environmental performance; executing plans to deliver aggressive 2025 emission reductions • Strategy leverages experience and competitive advantages to deliver value while transitioning to a lower-carbon future, consistent with the goals of the Paris Agreement See Supplemental Information for definitions. 6

GROWING SHAREHOLDER VALUE IN A LOWER-CARBON FUTUREGROWING SHAREHOLDER VALUE IN A LOWER-CARBON FUTURE

IPCC EXPECTS A DIVERSE ENERGY MIX IN ACHIEVING 2°C Multiple potential pathways to 2°C lead to wide range of projections 2040 ENERGY MIX IN IPCC LOWER 2°C SCENARIOS Quadrillion BTUs (Quads) High IPCC 2040 Wind/Solar Lower 2°C energy demand Bioenergy • Substantial efficiency gains range 19% Low-carbon Wind Other needed to offset population energy Solar demand and economic growth grows 44% Low Bioenergy Coal • Significant growth in low- Other carbon energy Coal • Oil and natural gas remain Oil / Oil & Oil / 55% Natural gas Natural gas essential 48% Natural gas still integral 2019 IAv PCC era 2 g 0 e40 IEA 2019 IPCC 2040 total energy demand average estimated demand Average Source: (left) IEA World Energy Outlook 2020; (right) IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios. 8 See Supplemental Information for definitions.IPCC EXPECTS A DIVERSE ENERGY MIX IN ACHIEVING 2°C Multiple potential pathways to 2°C lead to wide range of projections 2040 ENERGY MIX IN IPCC LOWER 2°C SCENARIOS Quadrillion BTUs (Quads) High IPCC 2040 Wind/Solar Lower 2°C energy demand Bioenergy • Substantial efficiency gains range 19% Low-carbon Wind Other needed to offset population energy Solar demand and economic growth grows 44% Low Bioenergy Coal • Significant growth in low- Other carbon energy Coal • Oil and natural gas remain Oil / Oil & Oil / 55% Natural gas Natural gas essential 48% Natural gas still integral 2019 IAv PCC era 2 g 0 e40 IEA 2019 IPCC 2040 total energy demand average estimated demand Average Source: (left) IEA World Energy Outlook 2020; (right) IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios. 8 See Supplemental Information for definitions.

IPCC OIL & GAS DEMAND DRIVEN BY ECONOMIC GROWTH Hard-to-decarbonize sectors meet demands from increasing population and growing prosperity GLOBAL ENERGY DEMAND IN IPCC LOWER 2°C SCENARIOS Quads • 80% of demand for oil and natural gas Wind Fuel driven by three sectors Other 21% Solar 20% Industrial Bioenergy • Natural gas into power generation and Feed industrial furnaces Power Other 13% Generation 22% Coal 24% • Oil required as industrial feedstock for Commercial consumer goods Natural Transport gas • Oil / distillate for commercial transport Oil IPCC 2040 IPCC 2040 average estimated demand Average Source: IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios and ExxonMobil analysis. See Supplemental Information for definitions. 9 See Supplemental Information for footnotes.IPCC OIL & GAS DEMAND DRIVEN BY ECONOMIC GROWTH Hard-to-decarbonize sectors meet demands from increasing population and growing prosperity GLOBAL ENERGY DEMAND IN IPCC LOWER 2°C SCENARIOS Quads • 80% of demand for oil and natural gas Wind Fuel driven by three sectors Other 21% Solar 20% Industrial Bioenergy • Natural gas into power generation and Feed industrial furnaces Power Other 13% Generation 22% Coal 24% • Oil required as industrial feedstock for Commercial consumer goods Natural Transport gas • Oil / distillate for commercial transport Oil IPCC 2040 IPCC 2040 average estimated demand Average Source: IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios and ExxonMobil analysis. See Supplemental Information for definitions. 9 See Supplemental Information for footnotes.

REDUCING EMISSIONS REQUIRES INNOVATION Available alternatives do not fully meet sector needs POWER GENERATION TRANSPORTATION INDUSTRIAL Need: 24/7 on-demand electricity Need: rapid refueling of energy-dense fuels Need: fuel for high-temperature processes Electricity Oil and Bioenergy Gas Wind Electricity Coal Oil and Other Gas IPCC IPCC IPCC 2040 2040 2040 Nuclear Oil and Solar Other Gas renewables Coal (e.g. hydro, geo) Other Limits of Solar / wind limited in poor resource areas Temperature intensity required for heavy Battery weight and long charging time alternatives and by intermittency manufacturing Innovations • Lower-cost CCS and hydrogen• Lower-cost biofuels and hydrogen• Lower-cost CCS and hydrogen required • Battery energy-density breakthroughs• Battery energy-density breakthroughs• Less energy-intensive processes Source: IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios and ExxonMobil analysis of IPCC Fifth Assessment Report and Special Report 1.5. 10REDUCING EMISSIONS REQUIRES INNOVATION Available alternatives do not fully meet sector needs POWER GENERATION TRANSPORTATION INDUSTRIAL Need: 24/7 on-demand electricity Need: rapid refueling of energy-dense fuels Need: fuel for high-temperature processes Electricity Oil and Bioenergy Gas Wind Electricity Coal Oil and Other Gas IPCC IPCC IPCC 2040 2040 2040 Nuclear Oil and Solar Other Gas renewables Coal (e.g. hydro, geo) Other Limits of Solar / wind limited in poor resource areas Temperature intensity required for heavy Battery weight and long charging time alternatives and by intermittency manufacturing Innovations • Lower-cost CCS and hydrogen• Lower-cost biofuels and hydrogen• Lower-cost CCS and hydrogen required • Battery energy-density breakthroughs• Battery energy-density breakthroughs• Less energy-intensive processes Source: IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios and ExxonMobil analysis of IPCC Fifth Assessment Report and Special Report 1.5. 10

EXXONMOBIL INNOVATIONS TO REDUCE EMISSIONS Focused on solutions for hard-to-decarbonize sectors TODAY TOMORROW • Switching coal to natural gas POWER • Cogeneration• Fuel cells for lower-cost CCS and hydrogen GENERATION • Lubricants for wind turbines • Fuels and lubricants to improve fuel COMMERCIAL efficiency TRANSPORT • Biofuels blending and distribution• Advanced biofuels long-haul trucks, • Lightweight plastics to improve vehicle aviation, marine efficiency • New materials with lower-emission • Fuel cells for lower-cost CCS and hydrogen INDUSTRIAL footprint • Less energy-intense manufacturing steel, cement, • Energy-efficient process redesign textiles, plastics processes • Carbon capture 11EXXONMOBIL INNOVATIONS TO REDUCE EMISSIONS Focused on solutions for hard-to-decarbonize sectors TODAY TOMORROW • Switching coal to natural gas POWER • Cogeneration• Fuel cells for lower-cost CCS and hydrogen GENERATION • Lubricants for wind turbines • Fuels and lubricants to improve fuel COMMERCIAL efficiency TRANSPORT • Biofuels blending and distribution• Advanced biofuels long-haul trucks, • Lightweight plastics to improve vehicle aviation, marine efficiency • New materials with lower-emission • Fuel cells for lower-cost CCS and hydrogen INDUSTRIAL footprint • Less energy-intense manufacturing steel, cement, • Energy-efficient process redesign textiles, plastics processes • Carbon capture 11

PROVEN RECORD IN ADVANCING LOW-CARBON TECHNOLOGIES Focused on solutions aligned with competitive strengths and experience Controlled Freeze LaBarge Zone™ Gorgon expansion commercial demonstration Low Carbon Solutions LaBarge created Qatar Qatar expansion CCS Low-emission LaBarge Sleipner Venture Fuels Venture plant offshore field created created C O M M E R C I A L I Z A T I O N 1986 2000 2010 2020 R & D C O L L A B O R A T I O N S Strategic Fuel cells Direct air capture Stanford Global Climate & Georgia Algae CCS alliance Energy Project Tech biofuels process Cellulosic biodiesel U.S. DOE / National labs Energy Centers Carbon capture and storage (CCS) Stanford Low-emissions fuels Strategic Energy Alliance Low-carbon technologies 12 2014 2015 2016 2018 2018PROVEN RECORD IN ADVANCING LOW-CARBON TECHNOLOGIES Focused on solutions aligned with competitive strengths and experience Controlled Freeze LaBarge Zone™ Gorgon expansion commercial demonstration Low Carbon Solutions LaBarge created Qatar Qatar expansion CCS Low-emission LaBarge Sleipner Venture Fuels Venture plant offshore field created created C O M M E R C I A L I Z A T I O N 1986 2000 2010 2020 R & D C O L L A B O R A T I O N S Strategic Fuel cells Direct air capture Stanford Global Climate & Georgia Algae CCS alliance Energy Project Tech biofuels process Cellulosic biodiesel U.S. DOE / National labs Energy Centers Carbon capture and storage (CCS) Stanford Low-emissions fuels Strategic Energy Alliance Low-carbon technologies 12 2014 2015 2016 2018 2018

SIGNIFICANT VALUE IN GROWING MARKETS ExxonMobil well positioned to capitalize across value chains through 2040 and beyond Total Addressable Production Manufacturing Markets / Sectors 1 Market: 2040 Fuels ~$6T Transport Power gen Industrial Biofuels ~$400B Transport Hydrogen ~$1T 3 Oil and Natural gas Transport Power gen Industrial 48% of energy mix 5-7% depletion per year Chemicals ~$4T Infrastructure Goods/products CO 2 Utilization Storage Carbon to CO Carbon products 2 ~$2T Carbon 1 Grows ~35% per year Capture 2 Mitigates 15% of emissions See Supplemental Information for footnotes. 13 13SIGNIFICANT VALUE IN GROWING MARKETS ExxonMobil well positioned to capitalize across value chains through 2040 and beyond Total Addressable Production Manufacturing Markets / Sectors 1 Market: 2040 Fuels ~$6T Transport Power gen Industrial Biofuels ~$400B Transport Hydrogen ~$1T 3 Oil and Natural gas Transport Power gen Industrial 48% of energy mix 5-7% depletion per year Chemicals ~$4T Infrastructure Goods/products CO 2 Utilization Storage Carbon to CO Carbon products 2 ~$2T Carbon 1 Grows ~35% per year Capture 2 Mitigates 15% of emissions See Supplemental Information for footnotes. 13 13

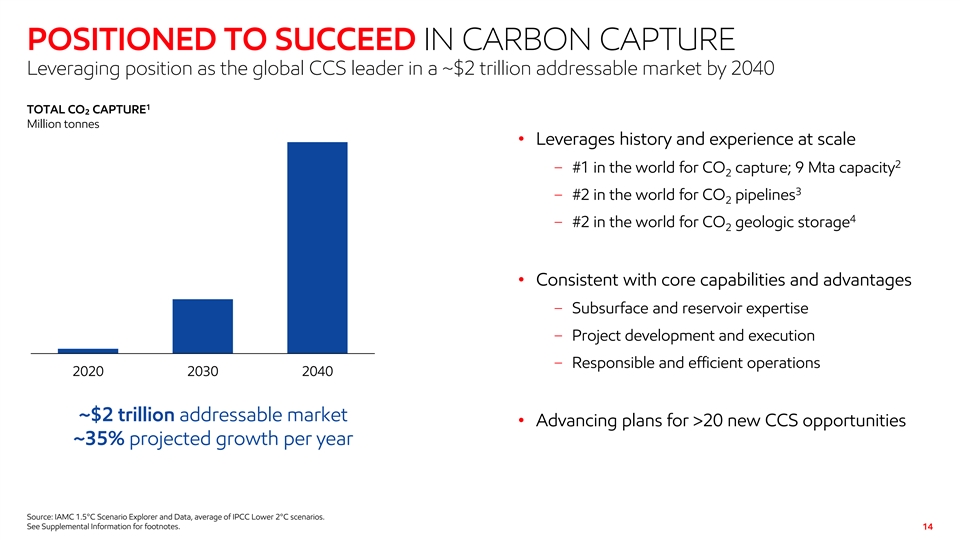

POSITIONED TO SUCCEED IN CARBON CAPTURE Leveraging position as the global CCS leader in a ~$2 trillion addressable market by 2040 1 TOTAL CO₂ CAPTURE Million tonnes • Leverages history and experience at scale 2 − #1 in the world for CO capture; 9 Mta capacity 2 3 − #2 in the world for CO pipelines 2 4 − #2 in the world for CO geologic storage 2 • Consistent with core capabilities and advantages − Subsurface and reservoir expertise − Project development and execution − Responsible and efficient operations 2020 2030 2040 ~$2 trillion addressable market • Advancing plans for >20 new CCS opportunities ~35% projected growth per year Source: IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios. See Supplemental Information for footnotes. 14POSITIONED TO SUCCEED IN CARBON CAPTURE Leveraging position as the global CCS leader in a ~$2 trillion addressable market by 2040 1 TOTAL CO₂ CAPTURE Million tonnes • Leverages history and experience at scale 2 − #1 in the world for CO capture; 9 Mta capacity 2 3 − #2 in the world for CO pipelines 2 4 − #2 in the world for CO geologic storage 2 • Consistent with core capabilities and advantages − Subsurface and reservoir expertise − Project development and execution − Responsible and efficient operations 2020 2030 2040 ~$2 trillion addressable market • Advancing plans for >20 new CCS opportunities ~35% projected growth per year Source: IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios. See Supplemental Information for footnotes. 14

IMPROVING ENVIRONMENT FOR CCS DEPLOYMENT Increasing government and market recognition of CCS importance Policy support is growing Technology for hard-to-abate sectors Offsets market >$200 billion is underfunded potential by 2040 % Billion USD per year 800 100 ◄$20 billion Buildings Africa annual Transport ◄100 $/T cost Asia Pacific Industrial 400 50 North 68% America ◄30 $/T Power cost generation Europe 19% Europe 0 0 Global emissions Climate tech 2030 2040 2011-2015 2016-2020 2017 venture funding 2013-2019 NEW CCS POLICIES INTRODUCED EMISSIONS AND VENTURE FUNDING OFFSETS MARKET Source: IEA Policies Database (as of Feb 24, 2021). Source: Emissions from ExxonMobil 2019 Outlook for Energy. Venture funding Source: ExxonMobil analysis of “The Economic Potential of Article 6 of the based on ExxonMobil analysis of IEA (2020), Energy Technology Perspectives Paris Agreement and Implementation Challenges”, IETA, University of 2020, IEA, Paris https://www.iea.org/reports/energy-technology-perspectives- Maryland and CPLC. Washington, D.C. License: Creative Commons Attribution 15 2020 and PwC The State of Climate Tech 2020. CC BY 3.0 IGO.IMPROVING ENVIRONMENT FOR CCS DEPLOYMENT Increasing government and market recognition of CCS importance Policy support is growing Technology for hard-to-abate sectors Offsets market >$200 billion is underfunded potential by 2040 % Billion USD per year 800 100 ◄$20 billion Buildings Africa annual Transport ◄100 $/T cost Asia Pacific Industrial 400 50 North 68% America ◄30 $/T Power cost generation Europe 19% Europe 0 0 Global emissions Climate tech 2030 2040 2011-2015 2016-2020 2017 venture funding 2013-2019 NEW CCS POLICIES INTRODUCED EMISSIONS AND VENTURE FUNDING OFFSETS MARKET Source: IEA Policies Database (as of Feb 24, 2021). Source: Emissions from ExxonMobil 2019 Outlook for Energy. Venture funding Source: ExxonMobil analysis of “The Economic Potential of Article 6 of the based on ExxonMobil analysis of IEA (2020), Energy Technology Perspectives Paris Agreement and Implementation Challenges”, IETA, University of 2020, IEA, Paris https://www.iea.org/reports/energy-technology-perspectives- Maryland and CPLC. Washington, D.C. License: Creative Commons Attribution 15 2020 and PwC The State of Climate Tech 2020. CC BY 3.0 IGO.

CCS MORE COST EFFECTIVE THAN OTHER TECHNOLOGIES Cost of CCS is well below many carbon reduction policies 1,2 CCS COSTS FOR MITIGATING INDUSTRIAL EMISSIONS $/tonne CO for conventional technology 2 • Two-thirds of emissions from point sources 3 U.S. EV Tax Credit (2020) 450 300 conducive to CCS IPCC Carbon Price (2040) for Lower 2°C Scenarios • Mitigates emissions at costs below policy support in California Low Carbon other sectors Fuel Credit (2020) 200 • Costs well below average carbon price projected in IPCC Lower 2°C 4 − Projected to reduce cost of 2°C by >50% 100 U.S. 45Q Tax • Potential to generate tradeable carbon offsets Credit (2026) 0 Natural gas Hydrogen Steel / iron Industrial production plant plant furnace Source: National Petroleum Council report: A Roadmap to At-Scale Deployment of Carbon Capture, Use, and Storage (2019). See Supplemental Information for footnotes and definitions. 16CCS MORE COST EFFECTIVE THAN OTHER TECHNOLOGIES Cost of CCS is well below many carbon reduction policies 1,2 CCS COSTS FOR MITIGATING INDUSTRIAL EMISSIONS $/tonne CO for conventional technology 2 • Two-thirds of emissions from point sources 3 U.S. EV Tax Credit (2020) 450 300 conducive to CCS IPCC Carbon Price (2040) for Lower 2°C Scenarios • Mitigates emissions at costs below policy support in California Low Carbon other sectors Fuel Credit (2020) 200 • Costs well below average carbon price projected in IPCC Lower 2°C 4 − Projected to reduce cost of 2°C by >50% 100 U.S. 45Q Tax • Potential to generate tradeable carbon offsets Credit (2026) 0 Natural gas Hydrogen Steel / iron Industrial production plant plant furnace Source: National Petroleum Council report: A Roadmap to At-Scale Deployment of Carbon Capture, Use, and Storage (2019). See Supplemental Information for footnotes and definitions. 16

EXXONMOBIL RESEARCH TO FURTHER REDUCE CCS COSTS Targeting one-third lower cost by 2030 COST OF CCS $/tonne CO 2 • >10 years of CCS-related R&D • R&D focused on effectiveness and efficiency improvements − Advanced materials for improved capture and concentration − Design optimized for capital efficiency • Fuel cell technology concept delivers step-change in cost − Same emissions reduction with less energy − Opportunity to co-produce hydrogen or power • Deploying technology key to experience curve and Current CCS Fuel cell Other Transport & Objective lower cost technology concept R&D storage Source: ExxonMobil analysis of potential cost reduction for large scale natural gas combined cycle power generation. 17EXXONMOBIL RESEARCH TO FURTHER REDUCE CCS COSTS Targeting one-third lower cost by 2030 COST OF CCS $/tonne CO 2 • >10 years of CCS-related R&D • R&D focused on effectiveness and efficiency improvements − Advanced materials for improved capture and concentration − Design optimized for capital efficiency • Fuel cell technology concept delivers step-change in cost − Same emissions reduction with less energy − Opportunity to co-produce hydrogen or power • Deploying technology key to experience curve and Current CCS Fuel cell Other Transport & Objective lower cost technology concept R&D storage Source: ExxonMobil analysis of potential cost reduction for large scale natural gas combined cycle power generation. 17

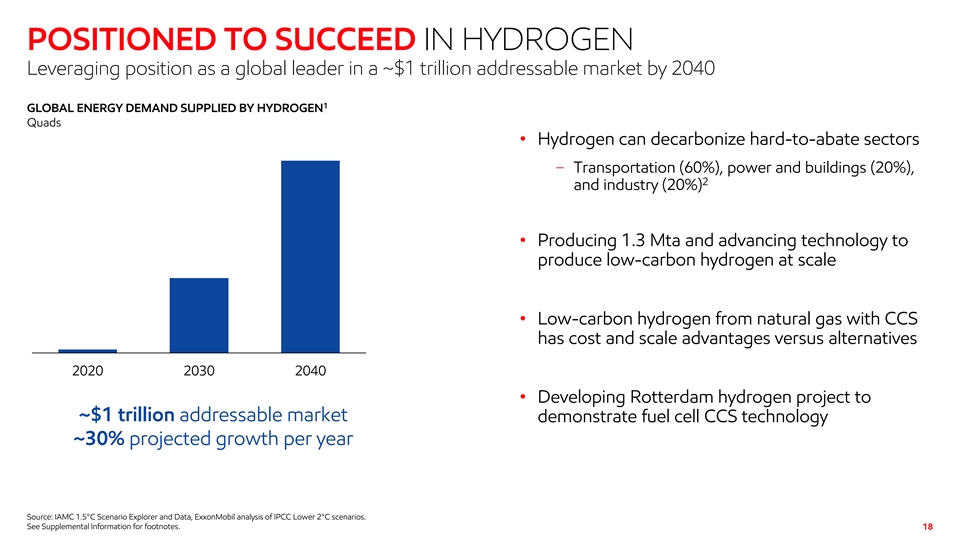

POSITIONED TO SUCCEED IN HYDROGEN Leveraging position as a global leader in a ~$1 trillion addressable market by 2040 1 GLOBAL ENERGY DEMAND SUPPLIED BY HYDROGEN Quads • Hydrogen can decarbonize hard-to-abate sectors − Transportation (60%), power and buildings (20%), 2 and industry (20%) • Producing 1.3 Mta and advancing technology to produce low-carbon hydrogen at scale • Low-carbon hydrogen from natural gas with CCS has cost and scale advantages versus alternatives 2020 2030 2040 • Developing Rotterdam hydrogen project to ~$1 trillion addressable market demonstrate fuel cell CCS technology ~30% projected growth per year Source: IAMC 1.5°C Scenario Explorer and Data, ExxonMobil analysis of IPCC Lower 2°C scenarios. See Supplemental Information for footnotes. 18POSITIONED TO SUCCEED IN HYDROGEN Leveraging position as a global leader in a ~$1 trillion addressable market by 2040 1 GLOBAL ENERGY DEMAND SUPPLIED BY HYDROGEN Quads • Hydrogen can decarbonize hard-to-abate sectors − Transportation (60%), power and buildings (20%), 2 and industry (20%) • Producing 1.3 Mta and advancing technology to produce low-carbon hydrogen at scale • Low-carbon hydrogen from natural gas with CCS has cost and scale advantages versus alternatives 2020 2030 2040 • Developing Rotterdam hydrogen project to ~$1 trillion addressable market demonstrate fuel cell CCS technology ~30% projected growth per year Source: IAMC 1.5°C Scenario Explorer and Data, ExxonMobil analysis of IPCC Lower 2°C scenarios. See Supplemental Information for footnotes. 18

REDUCING EMISSIONS CONSISTENT WITH GOALS OF PARIS Plans provide affordable and reliable energy while minimizing environmental impacts 1,2,3 EXXONMOBIL AND SOCIETY’S EMISSIONS Percent reduction versus 2016 1 Society’s emissions 0.9 Paris submissions (estimated 2016 Nationally Determined Contributions) 0% 0.8 ExxonMobil GHG emissions 0.7 -25% 0.6 0.5 -50% 0.4 0.3 -75% 0.2 0.1 Hypothetical Hypothetical 1.5°C pathway 2°C pathway Net -100% 0 zero 2016 2015 2030 2045 2060 2075 See Supplemental Information for footnotes. 19REDUCING EMISSIONS CONSISTENT WITH GOALS OF PARIS Plans provide affordable and reliable energy while minimizing environmental impacts 1,2,3 EXXONMOBIL AND SOCIETY’S EMISSIONS Percent reduction versus 2016 1 Society’s emissions 0.9 Paris submissions (estimated 2016 Nationally Determined Contributions) 0% 0.8 ExxonMobil GHG emissions 0.7 -25% 0.6 0.5 -50% 0.4 0.3 -75% 0.2 0.1 Hypothetical Hypothetical 1.5°C pathway 2°C pathway Net -100% 0 zero 2016 2015 2030 2045 2060 2075 See Supplemental Information for footnotes. 19

POSITIONED FOR A LOWER-CARBON FUTURE Leveraging capabilities and expertise to reduce emissions and deliver value Low Research, develop, Operated Announced reduction Carbon commercialize GHG emissions plans to 1 Solutions >$13 Billion -6% since 2016 2025 new business to advance lower-emission solutions: absolute emissions have absolute Upstream GHG commercial CCS CCS / hydrogen, biofuels, declined since start of the emissions to drop by ~30%, 2 3 opportunities and deploy cogeneration, and efficiency Paris Agreement methane & flaring 40-50% technologies Support the goals of Global Hydrogen Renewables in CCS leader produced operations (600MW) Paris 40% 1.3 Mta #2 All-time buyer Agreement engaging in climate-related of all CO captured, 2 developing technology to of wind / solar power policy, including carbon equivalent to planting produce low-carbon H with among Oil and Gas; top 5% 2 4 5 pricing ~2 billion trees CCS at scale across all corporates See Supplemental Information for footnotes. 20POSITIONED FOR A LOWER-CARBON FUTURE Leveraging capabilities and expertise to reduce emissions and deliver value Low Research, develop, Operated Announced reduction Carbon commercialize GHG emissions plans to 1 Solutions >$13 Billion -6% since 2016 2025 new business to advance lower-emission solutions: absolute emissions have absolute Upstream GHG commercial CCS CCS / hydrogen, biofuels, declined since start of the emissions to drop by ~30%, 2 3 opportunities and deploy cogeneration, and efficiency Paris Agreement methane & flaring 40-50% technologies Support the goals of Global Hydrogen Renewables in CCS leader produced operations (600MW) Paris 40% 1.3 Mta #2 All-time buyer Agreement engaging in climate-related of all CO captured, 2 developing technology to of wind / solar power policy, including carbon equivalent to planting produce low-carbon H with among Oil and Gas; top 5% 2 4 5 pricing ~2 billion trees CCS at scale across all corporates See Supplemental Information for footnotes. 20

OIL AND GAS INVESTMENT NEEDED TO MEET DEMAND New supply required to offset depletion GLOBAL OIL SUPPLY AND DEMAND GLOBAL ENERGY DEMAND IN IPCC LOWER 2°C SCENARIOS Mbd Quads 120 525 High demand Wind t IEA STEPS demand Solar t Bioenergy Average 350 80 demand based Other on IPCC Lower 2°C scenarios Coal New supply required Natural gas 175 40 Low demand 48% Oil Decline without investment: ~7% per year 0 - 0 IPCC 2040 2019 2040 IPCC 2040 Average average estimated demand • Oil and natural gas remain essential 1 • $12 trillion of investment needed by 2040 in 2°C Source: (left) IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios; (right) Excludes biofuels. IHS, IEA, ExxonMobil analysis of IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios. See Supplemental Information for footnotes and definitions. 21OIL AND GAS INVESTMENT NEEDED TO MEET DEMAND New supply required to offset depletion GLOBAL OIL SUPPLY AND DEMAND GLOBAL ENERGY DEMAND IN IPCC LOWER 2°C SCENARIOS Mbd Quads 120 525 High demand Wind t IEA STEPS demand Solar t Bioenergy Average 350 80 demand based Other on IPCC Lower 2°C scenarios Coal New supply required Natural gas 175 40 Low demand 48% Oil Decline without investment: ~7% per year 0 - 0 IPCC 2040 2019 2040 IPCC 2040 Average average estimated demand • Oil and natural gas remain essential 1 • $12 trillion of investment needed by 2040 in 2°C Source: (left) IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios; (right) Excludes biofuels. IHS, IEA, ExxonMobil analysis of IAMC 1.5°C Scenario Explorer and Data, average of IPCC Lower 2°C scenarios. See Supplemental Information for footnotes and definitions. 21

INDUSTRY-LEADING ASSETS AND INVESTMENT PORTFOLIO Responsibly meeting the continued demand for oil and gas Operational excellence Capital flexibility Cash Opex 1 <0.02 LTIR $6 billion ~$35 /bbl best-ever workforce safety and in structural efficiencies by year- to maintain dividend at 10-year reliability performance in 2020 average downstream and end 2023 versus 2019 2,3 chemical margins in 2025 Upstream Downstream Chemical ~90% 30% 60% growth in high-value of 2021-2025 investments have improvement in net cash margin 4 performance products by 2027 cost-of-supply ≤$35/bbl driven primarily by conversion from major projects 5 projects at advantaged sites See Supplemental Information for footnotes and definitions. 22INDUSTRY-LEADING ASSETS AND INVESTMENT PORTFOLIO Responsibly meeting the continued demand for oil and gas Operational excellence Capital flexibility Cash Opex 1 <0.02 LTIR $6 billion ~$35 /bbl best-ever workforce safety and in structural efficiencies by year- to maintain dividend at 10-year reliability performance in 2020 average downstream and end 2023 versus 2019 2,3 chemical margins in 2025 Upstream Downstream Chemical ~90% 30% 60% growth in high-value of 2021-2025 investments have improvement in net cash margin 4 performance products by 2027 cost-of-supply ≤$35/bbl driven primarily by conversion from major projects 5 projects at advantaged sites See Supplemental Information for footnotes and definitions. 22

UPSTREAMUPSTREAM

UPSTREAM STRATEGY RECONNECT 2020 update • Reduced 2020 cash Opex by 18% versus 2019 • Deferred 2020-25 investments of ~$50 billion; value deferred with delayed Strengthening portfolio implementation competitiveness 1 • ~90% of 2021-25 Upstream investments have cost-of-supply ≤$35/bbl 2 • Finalizing >$1 billion North Sea divestment; 10 assets in market • Three new Guyana discoveries; total resource ~9 Boeb Robust pipeline of future developments• Focused exploration on industry-leading basins in Guyana-Suriname and Brazil • Met 15% methane and 25% flare reduction goals Reducing emissions • Established plans to: consistent with goals of − Reduce methane intensity by 40-50% and flaring intensity by 35-45% by the Paris Agreement 3 2025 − Eliminate routine flaring in Upstream operations by 2030 See Supplemental Information for footnotes and definitions. 24UPSTREAM STRATEGY RECONNECT 2020 update • Reduced 2020 cash Opex by 18% versus 2019 • Deferred 2020-25 investments of ~$50 billion; value deferred with delayed Strengthening portfolio implementation competitiveness 1 • ~90% of 2021-25 Upstream investments have cost-of-supply ≤$35/bbl 2 • Finalizing >$1 billion North Sea divestment; 10 assets in market • Three new Guyana discoveries; total resource ~9 Boeb Robust pipeline of future developments• Focused exploration on industry-leading basins in Guyana-Suriname and Brazil • Met 15% methane and 25% flare reduction goals Reducing emissions • Established plans to: consistent with goals of − Reduce methane intensity by 40-50% and flaring intensity by 35-45% by the Paris Agreement 3 2025 − Eliminate routine flaring in Upstream operations by 2030 See Supplemental Information for footnotes and definitions. 24

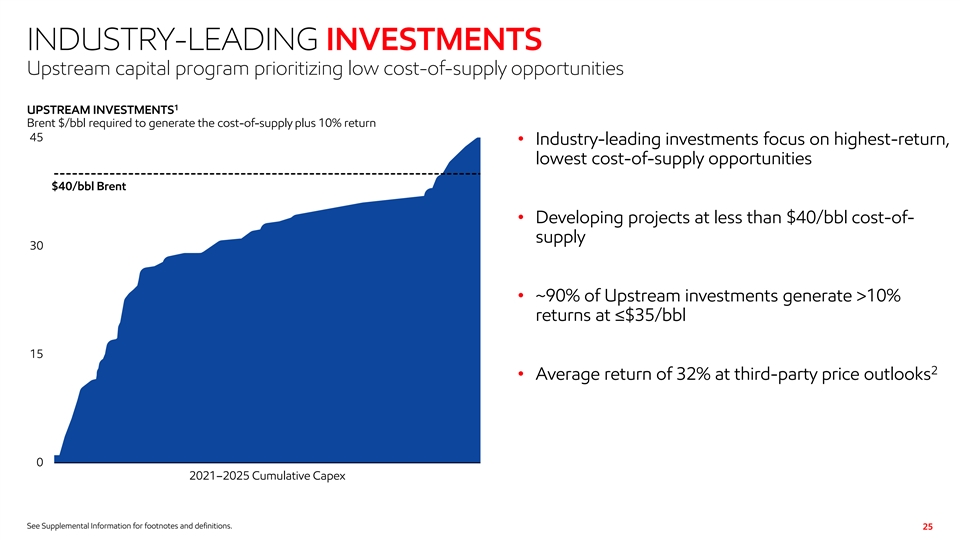

INDUSTRY-LEADING INVESTMENTS Upstream capital program prioritizing low cost-of-supply opportunities 1 UPSTREAM INVESTMENTS Brent $/bbl required to generate the cost-of-supply plus 10% return 45 • Industry-leading investments focus on highest-return, lowest cost-of-supply opportunities $40/bbl Brent • Developing projects at less than $40/bbl cost-of- supply 30 • ~90% of Upstream investments generate >10% returns at ≤$35/bbl 15 2 • Average return of 32% at third-party price outlooks 0 2021–2025 Cumulative Capex See Supplemental Information for footnotes and definitions. 25INDUSTRY-LEADING INVESTMENTS Upstream capital program prioritizing low cost-of-supply opportunities 1 UPSTREAM INVESTMENTS Brent $/bbl required to generate the cost-of-supply plus 10% return 45 • Industry-leading investments focus on highest-return, lowest cost-of-supply opportunities $40/bbl Brent • Developing projects at less than $40/bbl cost-of- supply 30 • ~90% of Upstream investments generate >10% returns at ≤$35/bbl 15 2 • Average return of 32% at third-party price outlooks 0 2021–2025 Cumulative Capex See Supplemental Information for footnotes and definitions. 25

HIGH-RETURN INVESTMENTS GUYANA Industry’s largest oil-play discovered in the past decade GHG intensity Exploration Resource Production ~80% >45% lower ~9 Boeb >750 Kbd success rate with 18 than Upstream average in including three additional by 2026 1 2025; zero routine flaring discoveries discoveries in 2020 by 2030 Cash flow High return Highly resilient Community support ~$3.5 billion >20% >10% >2,000 2,3 3 of operating cash flow in rate of return return at <$35/bbl Guyanese supporting 2 2025 developments 2 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. 26 See Supplemental Information for footnotes and definitions.HIGH-RETURN INVESTMENTS GUYANA Industry’s largest oil-play discovered in the past decade GHG intensity Exploration Resource Production ~80% >45% lower ~9 Boeb >750 Kbd success rate with 18 than Upstream average in including three additional by 2026 1 2025; zero routine flaring discoveries discoveries in 2020 by 2030 Cash flow High return Highly resilient Community support ~$3.5 billion >20% >10% >2,000 2,3 3 of operating cash flow in rate of return return at <$35/bbl Guyanese supporting 2 2025 developments 2 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. 26 See Supplemental Information for footnotes and definitions.

HIGH-RETURN INVESTMENTS GUYANA Maintaining aggressive development schedule of low cost-of-supply resource DISCOVERED RESOURCE CAPACITY Boeb Kbd 9• Liza Phase 1 achieved nameplate capacity FPSO 6 1,000 • Liza Phase 2 on schedule for start-up in 2022 Future FPSO 5 − 2H21 arrival in Guyanese waters FPSOs 6 Yellowtail • Payara FID in 2020, start-up in 2024 − Begin topside installation in 1H22 500 Yellowtail, Payara FPSO 5 & 6 3 • Sixth FPSO producing by 2027 Liza Ph 2 Liza Ph 1, • Capturing capital efficiencies through “design one, Liza Ph 2, build many” approach Liza Ph 1 and Payara 0 0 2020 2022 2024 2025 2026 2027 See Supplemental Information for definitions. 27HIGH-RETURN INVESTMENTS GUYANA Maintaining aggressive development schedule of low cost-of-supply resource DISCOVERED RESOURCE CAPACITY Boeb Kbd 9• Liza Phase 1 achieved nameplate capacity FPSO 6 1,000 • Liza Phase 2 on schedule for start-up in 2022 Future FPSO 5 − 2H21 arrival in Guyanese waters FPSOs 6 Yellowtail • Payara FID in 2020, start-up in 2024 − Begin topside installation in 1H22 500 Yellowtail, Payara FPSO 5 & 6 3 • Sixth FPSO producing by 2027 Liza Ph 2 Liza Ph 1, • Capturing capital efficiencies through “design one, Liza Ph 2, build many” approach Liza Ph 1 and Payara 0 0 2020 2022 2024 2025 2026 2027 See Supplemental Information for definitions. 27

HIGH-RETURN INVESTMENTS GUYANA Exploration success increasing value of developments ~100 MILES Stabroek Payara/Liza Mako/Uaru Yellowtail/Redtail Longtail/Turbot Haimara • Size and quality of resource enables: − Highly capital-efficient development − Extended production plateaus through facilities integration − Unmatched flexibility and optionality potential NW SE • Significant additional resource potential Penetrated reservoirs Seismic signature Pac Paco or ra a − New discoveries beneath previously identified Sta Stab broek roek Koe Koeb bi i Pay Payar ara a resource W Whi hip ptai tail l Ua Uar ru u Kaieteur Li Liza za Dee Deep p R Re ed dt tai aill Li Liza za Y Ye ellllo ow wt tai aill − Anticipate 10 exploration and appraisal wells in Ma Mak ko o 2021 including Koebi and Whiptail S Sn no oe ek k T Tr riip pllet etai aill Canje Block 59 Hammer Hammerh he ead ad U Uar aru u- -2 2 Lo Lon ng gt tai aill Stabroek Y Ye ellllo ow wt tai aill- -2 2 T Tu ur rb bo ot t Largest operated position in Guyana-Suriname T Tiillapi apia a L Long ongtai tail l 2 2 & & 3 3 Basin • Total basin potential more than 2x discovered Hai Haimar mara a resource Block 52 Pl Plu uma ma G U Y A N A • Began testing play extensions in 2020-2021 ExxonMobil interests Discoveries 2021 wells − Quality reservoirs and hydrocarbons identified in S U R I N A M E first wells in Canje, Kaieteur, and Suriname See Supplemental Information for definitions. 28HIGH-RETURN INVESTMENTS GUYANA Exploration success increasing value of developments ~100 MILES Stabroek Payara/Liza Mako/Uaru Yellowtail/Redtail Longtail/Turbot Haimara • Size and quality of resource enables: − Highly capital-efficient development − Extended production plateaus through facilities integration − Unmatched flexibility and optionality potential NW SE • Significant additional resource potential Penetrated reservoirs Seismic signature Pac Paco or ra a − New discoveries beneath previously identified Sta Stab broek roek Koe Koeb bi i Pay Payar ara a resource W Whi hip ptai tail l Ua Uar ru u Kaieteur Li Liza za Dee Deep p R Re ed dt tai aill Li Liza za Y Ye ellllo ow wt tai aill − Anticipate 10 exploration and appraisal wells in Ma Mak ko o 2021 including Koebi and Whiptail S Sn no oe ek k T Tr riip pllet etai aill Canje Block 59 Hammer Hammerh he ead ad U Uar aru u- -2 2 Lo Lon ng gt tai aill Stabroek Y Ye ellllo ow wt tai aill- -2 2 T Tu ur rb bo ot t Largest operated position in Guyana-Suriname T Tiillapi apia a L Long ongtai tail l 2 2 & & 3 3 Basin • Total basin potential more than 2x discovered Hai Haimar mara a resource Block 52 Pl Plu uma ma G U Y A N A • Began testing play extensions in 2020-2021 ExxonMobil interests Discoveries 2021 wells − Quality reservoirs and hydrocarbons identified in S U R I N A M E first wells in Canje, Kaieteur, and Suriname See Supplemental Information for definitions. 28

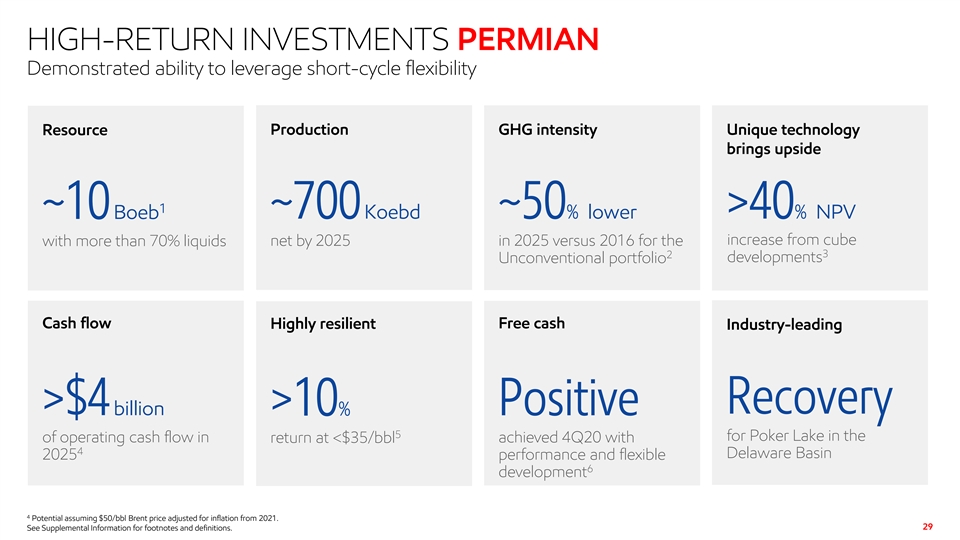

HIGH-RETURN INVESTMENTS PERMIAN Demonstrated ability to leverage short-cycle flexibility Resource Production GHG intensity Unique technology brings upside 1 ~10 Boeb ~700 Koebd ~50% lower >40% NPV increase from cube with more than 70% liquids net by 2025 in 2025 versus 2016 for the 3 2 developments Unconventional portfolio Cash flow Free cash Highly resilient Industry-leading Recovery >$4 billion Positive >10% 5 for Poker Lake in the of operating cash flow in achieved 4Q20 with return at <$35/bbl 4 Delaware Basin 2025 performance and flexible 6 development 4 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. 29 See Supplemental Information for footnotes and definitions.HIGH-RETURN INVESTMENTS PERMIAN Demonstrated ability to leverage short-cycle flexibility Resource Production GHG intensity Unique technology brings upside 1 ~10 Boeb ~700 Koebd ~50% lower >40% NPV increase from cube with more than 70% liquids net by 2025 in 2025 versus 2016 for the 3 2 developments Unconventional portfolio Cash flow Free cash Highly resilient Industry-leading Recovery >$4 billion Positive >10% 5 for Poker Lake in the of operating cash flow in achieved 4Q20 with return at <$35/bbl 4 Delaware Basin 2025 performance and flexible 6 development 4 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. 29 See Supplemental Information for footnotes and definitions.

HIGH-RETURN INVESTMENTS PERMIAN Leveraging unique competitive advantages HYDROCARBON DENSITY MAP 1 • World-class resource base of ~10 Boeb − >70% higher-margin liquids Delaware • Development plans leverage unique set of Basin competitive advantages: Midland − Large contiguous acreage position Basin ExxonMobil − Subsurface understanding acreage − Drilling and completion capability EDDY MARTIN − Demonstrated success in large-scale project execution COUNTY COUNTY • Competitive advantages are key to achieving double- MIDLAND 40 55 COUNTY miles miles digit returns at <$35/bbl − Improved capital efficiency Poker − Lower operating cost Lake − Higher resource recovery 25 miles 31 miles See Supplemental Information for footnotes and definitions. 30HIGH-RETURN INVESTMENTS PERMIAN Leveraging unique competitive advantages HYDROCARBON DENSITY MAP 1 • World-class resource base of ~10 Boeb − >70% higher-margin liquids Delaware • Development plans leverage unique set of Basin competitive advantages: Midland − Large contiguous acreage position Basin ExxonMobil − Subsurface understanding acreage − Drilling and completion capability EDDY MARTIN − Demonstrated success in large-scale project execution COUNTY COUNTY • Competitive advantages are key to achieving double- MIDLAND 40 55 COUNTY miles miles digit returns at <$35/bbl − Improved capital efficiency Poker − Lower operating cost Lake − Higher resource recovery 25 miles 31 miles See Supplemental Information for footnotes and definitions. 30

HIGH-RETURN INVESTMENTS PERMIAN Unique Poker Lake development: >2.5 Boeb net resource, >65 thousand contiguous acres POKER LAKE UNIT • Largest contiguous development in the Permian Compression and pumps − Scale is key to lower cost and capital efficiency Separation and local storage Well pads • Multi-well pad corridor design provides: − Advantaged drilling and completion costs − More efficient utilization of surface facilities Central − Lower operating and maintenance cost processing facility • Leveraging cube development to deliver 40% higher 1 net present value versus alternatives − Cube performance in line with expectations • Started up major low-cost gathering and separation facility in 2020 − Central processing facility See Supplemental Information for footnotes and definitions. 31HIGH-RETURN INVESTMENTS PERMIAN Unique Poker Lake development: >2.5 Boeb net resource, >65 thousand contiguous acres POKER LAKE UNIT • Largest contiguous development in the Permian Compression and pumps − Scale is key to lower cost and capital efficiency Separation and local storage Well pads • Multi-well pad corridor design provides: − Advantaged drilling and completion costs − More efficient utilization of surface facilities Central − Lower operating and maintenance cost processing facility • Leveraging cube development to deliver 40% higher 1 net present value versus alternatives − Cube performance in line with expectations • Started up major low-cost gathering and separation facility in 2020 − Central processing facility See Supplemental Information for footnotes and definitions. 31

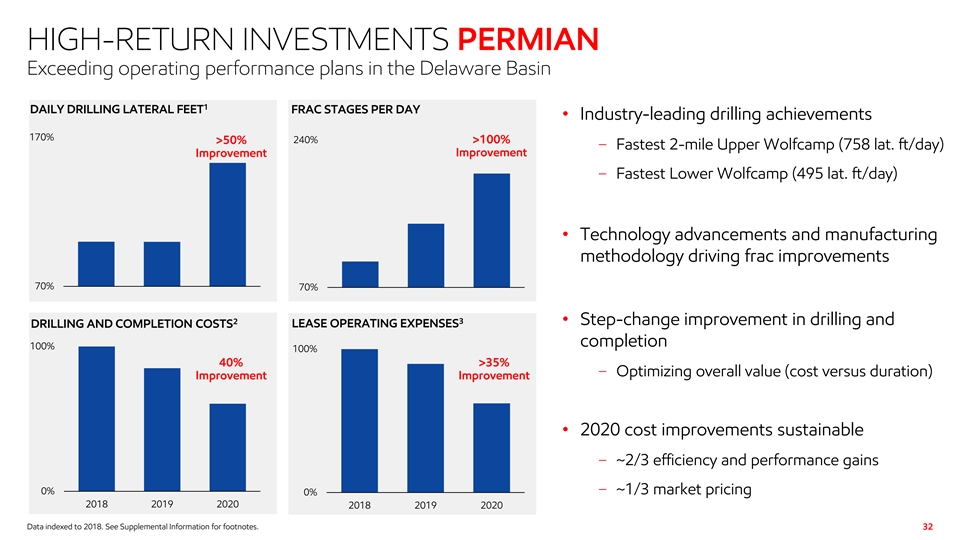

HIGH-RETURN INVESTMENTS PERMIAN Exceeding operating performance plans in the Delaware Basin 1 DAILY DRILLING LATERAL FEET FRAC STAGES PER DAY • Industry-leading drilling achievements 170% 240% >100% >50% − Fastest 2-mile Upper Wolfcamp (758 lat. ft/day) Improvement Improvement − Fastest Lower Wolfcamp (495 lat. ft/day) • Technology advancements and manufacturing methodology driving frac improvements 70% 70% 2 3 • Step-change improvement in drilling and LEASE OPERATING EXPENSES DRILLING AND COMPLETION COSTS completion 100% 100% 40% >35% − Optimizing overall value (cost versus duration) Improvement Improvement • 2020 cost improvements sustainable − ~2/3 efficiency and performance gains 0% − ~1/3 market pricing 0% 2018 2019 2020 2018 2019 2020 Data indexed to 2018. See Supplemental Information for footnotes. 32HIGH-RETURN INVESTMENTS PERMIAN Exceeding operating performance plans in the Delaware Basin 1 DAILY DRILLING LATERAL FEET FRAC STAGES PER DAY • Industry-leading drilling achievements 170% 240% >100% >50% − Fastest 2-mile Upper Wolfcamp (758 lat. ft/day) Improvement Improvement − Fastest Lower Wolfcamp (495 lat. ft/day) • Technology advancements and manufacturing methodology driving frac improvements 70% 70% 2 3 • Step-change improvement in drilling and LEASE OPERATING EXPENSES DRILLING AND COMPLETION COSTS completion 100% 100% 40% >35% − Optimizing overall value (cost versus duration) Improvement Improvement • 2020 cost improvements sustainable − ~2/3 efficiency and performance gains 0% − ~1/3 market pricing 0% 2018 2019 2020 2018 2019 2020 Data indexed to 2018. See Supplemental Information for footnotes. 32

HIGH-RETURN INVESTMENTS PERMIAN >15% increase in resource recovery versus 2018 Achieving industry-leading well performance in Poker Lake 1 DELAWARE AVERAGE WELL OIL PRODUCTION RATES (365 DAYS) DELAWARE AVERAGE WELL CUMULATIVE OIL PRODUCTION Bbl/d Kbbl 300 700 2020 2019 2018 0 0 Poker ExxonMobil 6 0 12 Lake Months Source: ExxonMobil analysis Source: Peer range - IHS Markit; ExxonMobil - ExxonMobil analysis See Supplemental Information for footnotes and definitions. 33HIGH-RETURN INVESTMENTS PERMIAN >15% increase in resource recovery versus 2018 Achieving industry-leading well performance in Poker Lake 1 DELAWARE AVERAGE WELL OIL PRODUCTION RATES (365 DAYS) DELAWARE AVERAGE WELL CUMULATIVE OIL PRODUCTION Bbl/d Kbbl 300 700 2020 2019 2018 0 0 Poker ExxonMobil 6 0 12 Lake Months Source: ExxonMobil analysis Source: Peer range - IHS Markit; ExxonMobil - ExxonMobil analysis See Supplemental Information for footnotes and definitions. 33

HIGH-RETURN INVESTMENTS PERMIAN Flexible development with options to reduce spend as market changes PRODUCTION Koebd net 800 • Pace of investment set by objective to: − Maintain positive free cash ~$60/bbl − Deliver industry-leading capital efficiency − Achieve double-digit returns at <$35/bbl Production range − Strengthen balance sheet ~$50/bbl • Prioritizing highest-quality core opportunities 400 • 2021 production outlook ~400 Koebd − 7-10 rigs, 5-7 frac crews • Longer-term outlook of ~700 Koebd by 2025 − Flexibility across state and federal acreage • Unique technology program brings significant upside 0 to current planning basis 2020 2021 2025 See Supplemental Information for definitions. 34HIGH-RETURN INVESTMENTS PERMIAN Flexible development with options to reduce spend as market changes PRODUCTION Koebd net 800 • Pace of investment set by objective to: − Maintain positive free cash ~$60/bbl − Deliver industry-leading capital efficiency − Achieve double-digit returns at <$35/bbl Production range − Strengthen balance sheet ~$50/bbl • Prioritizing highest-quality core opportunities 400 • 2021 production outlook ~400 Koebd − 7-10 rigs, 5-7 frac crews • Longer-term outlook of ~700 Koebd by 2025 − Flexibility across state and federal acreage • Unique technology program brings significant upside 0 to current planning basis 2020 2021 2025 See Supplemental Information for definitions. 34

HIGH-RETURN INVESTMENTS BRAZIL BACALHAU Expanding portfolio of low cost-of-supply deepwater developments GHG intensity Capacity Resource >65% lower 220 Kbd ~1 Boeb 1 than Upstream average in 2025 with start-up in 2024 for Phase 1 Cash flow Highly resilient High return ~$1 billion >10% >15% 2 3 2,3 of operating cash flow in 2025 return at <$35/bbl rate of return 2 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. 35 See Supplemental Information for footnotes and definitions.HIGH-RETURN INVESTMENTS BRAZIL BACALHAU Expanding portfolio of low cost-of-supply deepwater developments GHG intensity Capacity Resource >65% lower 220 Kbd ~1 Boeb 1 than Upstream average in 2025 with start-up in 2024 for Phase 1 Cash flow Highly resilient High return ~$1 billion >10% >15% 2 3 2,3 of operating cash flow in 2025 return at <$35/bbl rate of return 2 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. 35 See Supplemental Information for footnotes and definitions.

HIGH-POTENTIAL BRAZIL EXPLORATION Leading position in one of the most prolific offshore basins in the world 1 Cutthroat-1 • Second largest IOC acreage position − 2.6 million net acres S e r g i p e B a s i n − Operate more than 60% Mairare-1* B R A Z I L • Multiple prospects averaging >1 Boeb of Urissane-1* recoverable resource Naru-1* C a m p o s • Three wells drilled B a s i n Yba-1* ExxonMobil interests 2021 wells Opal-1 − Results confirm working hydrocarbon system in 2020 wells Tita-1 outer basins − Integrating results to guide future drilling Araucaria-1* • Plan to drill up to five wells in 2021; ~$200 million S a n t o s 2 B a s i n total cost *Petrobras operated See Supplemental Information for footnotes and definitions. 36HIGH-POTENTIAL BRAZIL EXPLORATION Leading position in one of the most prolific offshore basins in the world 1 Cutthroat-1 • Second largest IOC acreage position − 2.6 million net acres S e r g i p e B a s i n − Operate more than 60% Mairare-1* B R A Z I L • Multiple prospects averaging >1 Boeb of Urissane-1* recoverable resource Naru-1* C a m p o s • Three wells drilled B a s i n Yba-1* ExxonMobil interests 2021 wells Opal-1 − Results confirm working hydrocarbon system in 2020 wells Tita-1 outer basins − Integrating results to guide future drilling Araucaria-1* • Plan to drill up to five wells in 2021; ~$200 million S a n t o s 2 B a s i n total cost *Petrobras operated See Supplemental Information for footnotes and definitions. 36

RESILIENT LNG PORTFOLIO Diverse pipeline of low cost-of-supply developments Development status • Mozambique: Coral FLNG, 3.4 Mta, start-up in 2022 Growing sales GHG intensity • Mozambique: Rovuma, 15 Mta st 26 Mta in 2025 1 quartile − Capital efficient from scale of 85 TCF Area 4 resource 1 operated performance − Pursuing synergies with Area 1 ~10% net sales increase versus 2020 • Golden Pass: 16 Mta, start-up in 2024 − Capital-efficient import terminal conversion Cash flow Highly resilient − Atlantic Basin supply point providing logistics optimization and customer supply diversity ~$5 billion >10% • PNG: Papua, 5 Mta 3 of operating cash flow in return at <$5/Mbtu 2 − Capital efficient leveraging current facilities 2025; ~$4 billion in 2020 − Continuing development optimization 2 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. See Supplemental Information for footnotes and definitions. 37RESILIENT LNG PORTFOLIO Diverse pipeline of low cost-of-supply developments Development status • Mozambique: Coral FLNG, 3.4 Mta, start-up in 2022 Growing sales GHG intensity • Mozambique: Rovuma, 15 Mta st 26 Mta in 2025 1 quartile − Capital efficient from scale of 85 TCF Area 4 resource 1 operated performance − Pursuing synergies with Area 1 ~10% net sales increase versus 2020 • Golden Pass: 16 Mta, start-up in 2024 − Capital-efficient import terminal conversion Cash flow Highly resilient − Atlantic Basin supply point providing logistics optimization and customer supply diversity ~$5 billion >10% • PNG: Papua, 5 Mta 3 of operating cash flow in return at <$5/Mbtu 2 − Capital efficient leveraging current facilities 2025; ~$4 billion in 2020 − Continuing development optimization 2 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. See Supplemental Information for footnotes and definitions. 37

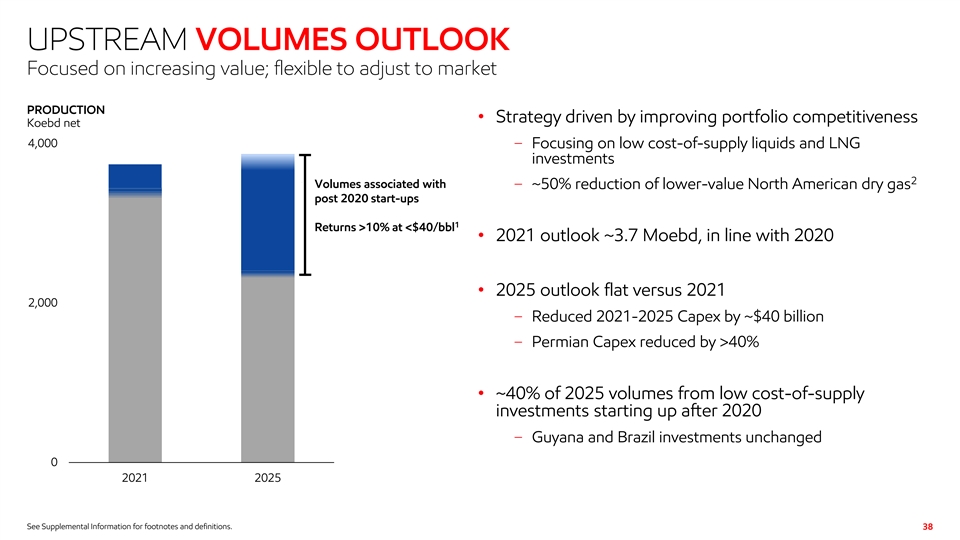

UPSTREAM VOLUMES OUTLOOK Focused on increasing value; flexible to adjust to market PRODUCTION • Strategy driven by improving portfolio competitiveness Koebd net 4,000 − Focusing on low cost-of-supply liquids and LNG investments 2 Volumes associated with − ~50% reduction of lower-value North American dry gas post 2020 start-ups 1 Returns >10% at <$40/bbl • 2021 outlook ~3.7 Moebd, in line with 2020 • 2025 outlook flat versus 2021 2,000 − Reduced 2021-2025 Capex by ~$40 billion − Permian Capex reduced by >40% • ~40% of 2025 volumes from low cost-of-supply investments starting up after 2020 − Guyana and Brazil investments unchanged 0 2021 2025 See Supplemental Information for footnotes and definitions. 38UPSTREAM VOLUMES OUTLOOK Focused on increasing value; flexible to adjust to market PRODUCTION • Strategy driven by improving portfolio competitiveness Koebd net 4,000 − Focusing on low cost-of-supply liquids and LNG investments 2 Volumes associated with − ~50% reduction of lower-value North American dry gas post 2020 start-ups 1 Returns >10% at <$40/bbl • 2021 outlook ~3.7 Moebd, in line with 2020 • 2025 outlook flat versus 2021 2,000 − Reduced 2021-2025 Capex by ~$40 billion − Permian Capex reduced by >40% • ~40% of 2025 volumes from low cost-of-supply investments starting up after 2020 − Guyana and Brazil investments unchanged 0 2021 2025 See Supplemental Information for footnotes and definitions. 38

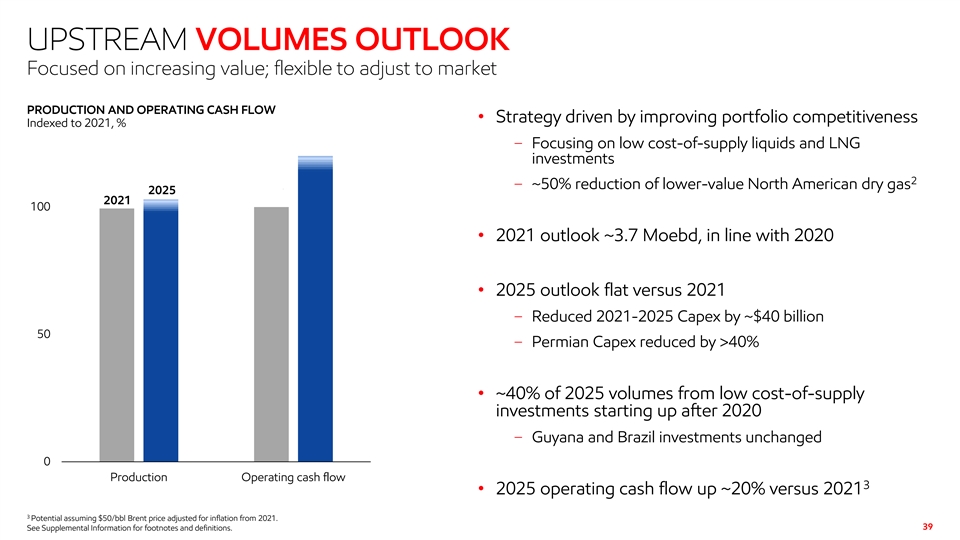

UPSTREAM VOLUMES OUTLOOK Focused on increasing value; flexible to adjust to market PRODUCTION AND OPERATING CASH FLOW • Strategy driven by improving portfolio competitiveness Indexed to 2021, % − Focusing on low cost-of-supply liquids and LNG investments 2 − ~50% reduction of lower-value North American dry gas 2025 2021 100 • 2021 outlook ~3.7 Moebd, in line with 2020 • 2025 outlook flat versus 2021 − Reduced 2021-2025 Capex by ~$40 billion 50 − Permian Capex reduced by >40% • ~40% of 2025 volumes from low cost-of-supply investments starting up after 2020 − Guyana and Brazil investments unchanged 0 Production Operating cash flow 3 • 2025 operating cash flow up ~20% versus 2021 3 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. 39 See Supplemental Information for footnotes and definitions.UPSTREAM VOLUMES OUTLOOK Focused on increasing value; flexible to adjust to market PRODUCTION AND OPERATING CASH FLOW • Strategy driven by improving portfolio competitiveness Indexed to 2021, % − Focusing on low cost-of-supply liquids and LNG investments 2 − ~50% reduction of lower-value North American dry gas 2025 2021 100 • 2021 outlook ~3.7 Moebd, in line with 2020 • 2025 outlook flat versus 2021 − Reduced 2021-2025 Capex by ~$40 billion 50 − Permian Capex reduced by >40% • ~40% of 2025 volumes from low cost-of-supply investments starting up after 2020 − Guyana and Brazil investments unchanged 0 Production Operating cash flow 3 • 2025 operating cash flow up ~20% versus 2021 3 Potential assuming $50/bbl Brent price adjusted for inflation from 2021. 39 See Supplemental Information for footnotes and definitions.

DOWNSTREAM & CHEMICALDOWNSTREAM & CHEMICAL

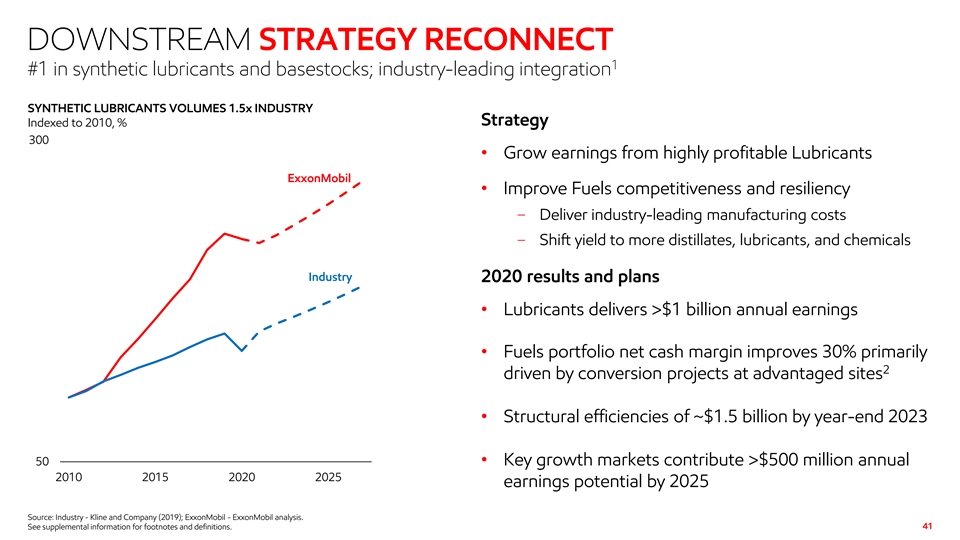

DOWNSTREAM STRATEGY RECONNECT 1 #1 in synthetic lubricants and basestocks; industry-leading integration SYNTHETIC LUBRICANTS VOLUMES 1.5x INDUSTRY Strategy Indexed to 2010, % 300 • Grow earnings from highly profitable Lubricants ExxonMobil • Improve Fuels competitiveness and resiliency − Deliver industry-leading manufacturing costs − Shift yield to more distillates, lubricants, and chemicals Industry 2020 results and plans • Lubricants delivers >$1 billion annual earnings • Fuels portfolio net cash margin improves 30% primarily 2 driven by conversion projects at advantaged sites • Structural efficiencies of ~$1.5 billion by year-end 2023 50 • Key growth markets contribute >$500 million annual 2010 2015 2020 2025 earnings potential by 2025 Source: Industry - Kline and Company (2019); ExxonMobil - ExxonMobil analysis. 41 See supplemental information for footnotes and definitions.DOWNSTREAM STRATEGY RECONNECT 1 #1 in synthetic lubricants and basestocks; industry-leading integration SYNTHETIC LUBRICANTS VOLUMES 1.5x INDUSTRY Strategy Indexed to 2010, % 300 • Grow earnings from highly profitable Lubricants ExxonMobil • Improve Fuels competitiveness and resiliency − Deliver industry-leading manufacturing costs − Shift yield to more distillates, lubricants, and chemicals Industry 2020 results and plans • Lubricants delivers >$1 billion annual earnings • Fuels portfolio net cash margin improves 30% primarily 2 driven by conversion projects at advantaged sites • Structural efficiencies of ~$1.5 billion by year-end 2023 50 • Key growth markets contribute >$500 million annual 2010 2015 2020 2025 earnings potential by 2025 Source: Industry - Kline and Company (2019); ExxonMobil - ExxonMobil analysis. 41 See supplemental information for footnotes and definitions.

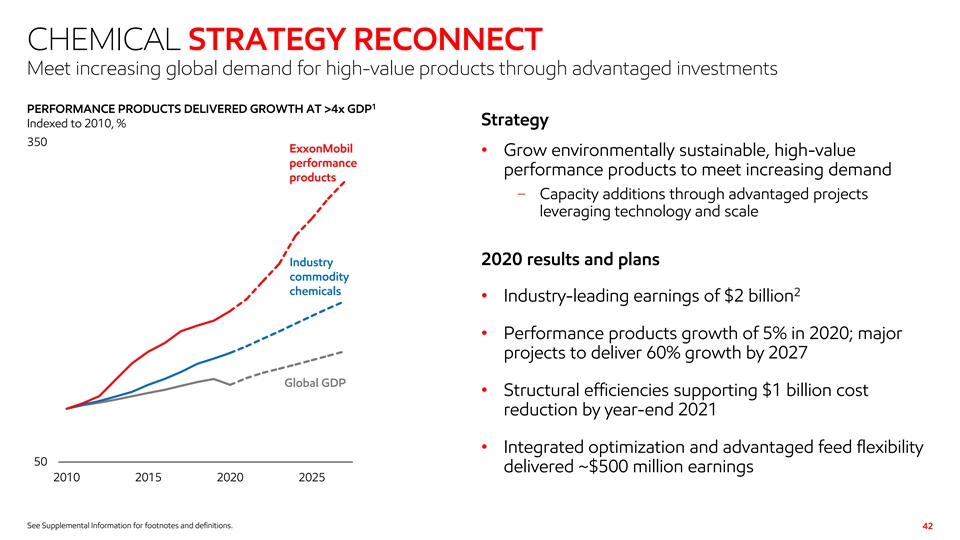

CHEMICAL STRATEGY RECONNECT Meet increasing global demand for high-value products through advantaged investments 1 PERFORMANCE PRODUCTS DELIVERED GROWTH AT >4x GDP Strategy Indexed to 2010, % 350 ExxonMobil • Grow environmentally sustainable, high-value performance performance products to meet increasing demand products − Capacity additions through advantaged projects leveraging technology and scale 2020 results and plans Industry commodity chemicals 2 • Industry-leading earnings of $2 billion • Performance products growth of 5% in 2020; major projects to deliver 60% growth by 2027 Global GDP • Structural efficiencies supporting $1 billion cost reduction by year-end 2021 • Integrated optimization and advantaged feed flexibility 50 delivered ~$500 million earnings 2010 2015 2020 2025 See Supplemental Information for footnotes and definitions. 42CHEMICAL STRATEGY RECONNECT Meet increasing global demand for high-value products through advantaged investments 1 PERFORMANCE PRODUCTS DELIVERED GROWTH AT >4x GDP Strategy Indexed to 2010, % 350 ExxonMobil • Grow environmentally sustainable, high-value performance performance products to meet increasing demand products − Capacity additions through advantaged projects leveraging technology and scale 2020 results and plans Industry commodity chemicals 2 • Industry-leading earnings of $2 billion • Performance products growth of 5% in 2020; major projects to deliver 60% growth by 2027 Global GDP • Structural efficiencies supporting $1 billion cost reduction by year-end 2021 • Integrated optimization and advantaged feed flexibility 50 delivered ~$500 million earnings 2010 2015 2020 2025 See Supplemental Information for footnotes and definitions. 42

LEADING CHEMICAL BUSINESS Diversified and resilient portfolio delivers strong earnings growth An industry leader across the cycle #1 or #2 market position in >80% of Performance product development chemical product portfolio supports rapid sales growth 4 400% Polyethylene ExxonMobil Performance market position: #1 Total market position: #1 Fluids / plasticizer Market position: #1 Vistamaxx™ Propylene-based plastomer Market position: #1 Industry 2 200% Adhesions Market position: #1 IOC Synthetics Performance Market position: #1 polypropylene Performance TPV and butyl rubber polyethylene Market position: #1 0% 0 Aromatics 2010 2015 2020 2025 2010-2019 2020 Market position: #2 average 1 2 3 MARKET POSITION ANNUAL EARNINGS, Billion USD EXXONMOBIL SALES VOLUME, Indexed to 2010 See Supplemental Information for footnotes and definitions. 43LEADING CHEMICAL BUSINESS Diversified and resilient portfolio delivers strong earnings growth An industry leader across the cycle #1 or #2 market position in >80% of Performance product development chemical product portfolio supports rapid sales growth 4 400% Polyethylene ExxonMobil Performance market position: #1 Total market position: #1 Fluids / plasticizer Market position: #1 Vistamaxx™ Propylene-based plastomer Market position: #1 Industry 2 200% Adhesions Market position: #1 IOC Synthetics Performance Market position: #1 polypropylene Performance TPV and butyl rubber polyethylene Market position: #1 0% 0 Aromatics 2010 2015 2020 2025 2010-2019 2020 Market position: #2 average 1 2 3 MARKET POSITION ANNUAL EARNINGS, Billion USD EXXONMOBIL SALES VOLUME, Indexed to 2010 See Supplemental Information for footnotes and definitions. 43

INNOVATIVE PRODUCTS PROVIDE CUSTOMER BENEFITS High-value products provide customer choices for lower emissions or improved efficiencies HIGH-VALUE PRODUCTS MEET EVOLVING CUSTOMER NEEDS Representative examples 1 PRODUCT / SECTOR POTENTIAL BENEFITS Plastic packaging 54% lower lifecycle GHG emissions impact versus alternatives Flexible film applications Exceed™ XP enables up to 30% down gauging versus conventional plastics Advanced recycling of plastic waste To produce certified circular polymers with equivalent performance of virgin plastics Polypropylene automotive application Fuel efficiency improves 6-8% for a 10% reduction in vehicle weight 2 Synergy Diesel Efficient™ Improves average fuel economy by 2% versus diesel fuel without detergent additive Synthetic motor oil Can improve fuel economy up to 2% versus conventional mineral engine oils Wind turbine gear oil Mobil SHC™ Gear 320 WT oil offers long oil drain interval with 10-year warranty 2 Synergy Diesel Efficient™ assumes a 250 gallon tank and an average of 7 miles per gallon. See Supplemental Information for footnotes and definitions. 44INNOVATIVE PRODUCTS PROVIDE CUSTOMER BENEFITS High-value products provide customer choices for lower emissions or improved efficiencies HIGH-VALUE PRODUCTS MEET EVOLVING CUSTOMER NEEDS Representative examples 1 PRODUCT / SECTOR POTENTIAL BENEFITS Plastic packaging 54% lower lifecycle GHG emissions impact versus alternatives Flexible film applications Exceed™ XP enables up to 30% down gauging versus conventional plastics Advanced recycling of plastic waste To produce certified circular polymers with equivalent performance of virgin plastics Polypropylene automotive application Fuel efficiency improves 6-8% for a 10% reduction in vehicle weight 2 Synergy Diesel Efficient™ Improves average fuel economy by 2% versus diesel fuel without detergent additive Synthetic motor oil Can improve fuel economy up to 2% versus conventional mineral engine oils Wind turbine gear oil Mobil SHC™ Gear 320 WT oil offers long oil drain interval with 10-year warranty 2 Synergy Diesel Efficient™ assumes a 250 gallon tank and an average of 7 miles per gallon. See Supplemental Information for footnotes and definitions. 44

PRODUCT MIX DELIVERS INCREASED VALUE Proprietary technology enables product mix upgrade 1 DOWNSTREAM AND CHEMICAL PRODUCT MIX UPGRADE PLANS 2027 volume change, indexed to 2017 -50% 0% 50% • Grow Chemical performance product Performance products commodity ++ volume consistent with demand Chemical Commodity • Highgrade refinery product mix +$70/bbl − Reduce fuel oil and gasoline yield Lubricants +$45/bbl • Proprietary technology enables: − Fuel oil to lubricant upgrade Diesel / Jet +$14/bbl − New innovative chemical products Feedstock Refining $/bbl Gasoline +$9/bbl Fuel oil -$11/bbl Product spreads versus average 2 refining feedstock cost $/bbl See Supplemental Information for footnotes and definitions. 45PRODUCT MIX DELIVERS INCREASED VALUE Proprietary technology enables product mix upgrade 1 DOWNSTREAM AND CHEMICAL PRODUCT MIX UPGRADE PLANS 2027 volume change, indexed to 2017 -50% 0% 50% • Grow Chemical performance product Performance products commodity ++ volume consistent with demand Chemical Commodity • Highgrade refinery product mix +$70/bbl − Reduce fuel oil and gasoline yield Lubricants +$45/bbl • Proprietary technology enables: − Fuel oil to lubricant upgrade Diesel / Jet +$14/bbl − New innovative chemical products Feedstock Refining $/bbl Gasoline +$9/bbl Fuel oil -$11/bbl Product spreads versus average 2 refining feedstock cost $/bbl See Supplemental Information for footnotes and definitions. 45

FUTURE INVESTMENTS DELIVER ROBUST RETURNS Advantaged investments focus on margin improvement and high-value product growth FUTURE MAJOR DOWNSTREAM & CHEMICAL GROWTH PROJECTS EARNINGS FROM FUTURE MAJOR GROWTH PROJECTS 1 2 DELIVER ~30% RETURN DELIVER >$2 BILLION AT 10-YEAR LOW MARGINS Billion USD 5 Refining product upgrades Connect advantaged Upstream with Permian crude venture world-class U.S. Gulf Coast assets Beaumont light crude Process advantaged Permian crude Fawley hydrofiner Capture attractive local diesel market Singapore resid upgrade Upgrade bottoms to lubes and distillates 30% 1 return Chemical high-value performance product growth Corpus Christi complex Leverage North America gas advantage China complex Enables access to key growth market Baton Rouge polypropylene Meet growing auto / durable demand Sustain performance polyethylene and Baytown expansion Vistamaxx™ growth 0 10-year 10-year low margins average margins See Supplemental Information for footnotes and definitions. 46FUTURE INVESTMENTS DELIVER ROBUST RETURNS Advantaged investments focus on margin improvement and high-value product growth FUTURE MAJOR DOWNSTREAM & CHEMICAL GROWTH PROJECTS EARNINGS FROM FUTURE MAJOR GROWTH PROJECTS 1 2 DELIVER ~30% RETURN DELIVER >$2 BILLION AT 10-YEAR LOW MARGINS Billion USD 5 Refining product upgrades Connect advantaged Upstream with Permian crude venture world-class U.S. Gulf Coast assets Beaumont light crude Process advantaged Permian crude Fawley hydrofiner Capture attractive local diesel market Singapore resid upgrade Upgrade bottoms to lubes and distillates 30% 1 return Chemical high-value performance product growth Corpus Christi complex Leverage North America gas advantage China complex Enables access to key growth market Baton Rouge polypropylene Meet growing auto / durable demand Sustain performance polyethylene and Baytown expansion Vistamaxx™ growth 0 10-year 10-year low margins average margins See Supplemental Information for footnotes and definitions. 46

DELIVERING ON STRATEGIC PRIORITIES Earnings growth through integration, cost reductions, and project portfolio Leading 2020 Structural • World-class Downstream and Chemical businesses Chemical earnings efficiencies with leading market positions • Competitive cost structure supported by industry- ~$2 billion $2.5 billion leading integration platform and nearly double 10-year combined Downstream and 1 industry-average earnings Chemical by year-end 2023 • Earnings growth driven by innovative, high-value products to meet increasing customer demand 2020 Lubricants Major growth earnings projects • Attractive major projects resilient across market cycles 3 >$1 billion >30% return industry-leading synthetic resilient across the cycle 2 lubricants positon with significant upside See Supplemental Information for footnotes and definitions. 47DELIVERING ON STRATEGIC PRIORITIES Earnings growth through integration, cost reductions, and project portfolio Leading 2020 Structural • World-class Downstream and Chemical businesses Chemical earnings efficiencies with leading market positions • Competitive cost structure supported by industry- ~$2 billion $2.5 billion leading integration platform and nearly double 10-year combined Downstream and 1 industry-average earnings Chemical by year-end 2023 • Earnings growth driven by innovative, high-value products to meet increasing customer demand 2020 Lubricants Major growth earnings projects • Attractive major projects resilient across market cycles 3 >$1 billion >30% return industry-leading synthetic resilient across the cycle 2 lubricants positon with significant upside See Supplemental Information for footnotes and definitions. 47

FINANCIAL PLAN FINANCIAL PLAN

REAFFIRMING CAPITAL ALLOCATION PHILOSOPHY Maintaining flexibility to respond as markets evolve • Long-term capital allocation priorities remain − Invest in advantaged projects to drive cash flow − Maintain balance sheet strength − Provide reliable dividend • Flexibility to efficiently respond to market developments − Driving further structural cost reductions − Advancing flexible portfolio of high-return, cost-advantaged investments • Ability to preserve strong balance sheet and maintain dividend 49REAFFIRMING CAPITAL ALLOCATION PHILOSOPHY Maintaining flexibility to respond as markets evolve • Long-term capital allocation priorities remain − Invest in advantaged projects to drive cash flow − Maintain balance sheet strength − Provide reliable dividend • Flexibility to efficiently respond to market developments − Driving further structural cost reductions − Advancing flexible portfolio of high-return, cost-advantaged investments • Ability to preserve strong balance sheet and maintain dividend 49

DRIVING STRUCTURAL COST EFFICIENCIES Achieved ~$3 billion of structural reductions in 2020; $6 billion by 2023 CASH OPEX EXCLUDING ENERGY AND PRODUCTION TAXES Billion USD • Delivered on cost reduction objectives, outperforming revised plan 44 3 • Leveraged prior reorganizations to deliver structural reductions of ~$3 billion in 2020 41 39 39 38 3+ • Additional $3 billion of structural efficiencies through 2023 for a total of $6 billion versus 2019 34 34 2019 Structural Market / 2020 Structural Market / 2023 activity activity See Supplemental Information for definitions. 50DRIVING STRUCTURAL COST EFFICIENCIES Achieved ~$3 billion of structural reductions in 2020; $6 billion by 2023 CASH OPEX EXCLUDING ENERGY AND PRODUCTION TAXES Billion USD • Delivered on cost reduction objectives, outperforming revised plan 44 3 • Leveraged prior reorganizations to deliver structural reductions of ~$3 billion in 2020 41 39 39 38 3+ • Additional $3 billion of structural efficiencies through 2023 for a total of $6 billion versus 2019 34 34 2019 Structural Market / 2020 Structural Market / 2023 activity activity See Supplemental Information for definitions. 50

MAINTAINING INVESTMENT OPTIONALITY Demonstrated ability to adjust capital spending and preserve value CAPEX 2021–2025 Billion USD • 2021-2025 capital program optimized to current $20 - $25 market outlook Guidance: $16 - $19 20 Flexible • Investment strategy prioritizes highest-return opportunities • Robust economics across price scenarios 10 Less • Flexibility to adjust investments in response to flexible market conditions in any year 0 2021 2022 - 2025 average See Supplemental Information for definitions. 51MAINTAINING INVESTMENT OPTIONALITY Demonstrated ability to adjust capital spending and preserve value CAPEX 2021–2025 Billion USD • 2021-2025 capital program optimized to current $20 - $25 market outlook Guidance: $16 - $19 20 Flexible • Investment strategy prioritizes highest-return opportunities • Robust economics across price scenarios 10 Less • Flexibility to adjust investments in response to flexible market conditions in any year 0 2021 2022 - 2025 average See Supplemental Information for definitions. 51