Strategic Update

Conference Call

September 21, 2007

1

“Statements in this presentation and conference call that set forth

expectations or predictions are based on facts and situations that

are known to us as of today, September 21, 2007.

“Actual results may differ materially, due to risks and uncertainties,

such as those described on pages 16-22 of the Form 10-K in our

2006 annual report and our other subsequent filings with the SEC.

Statements in this presentation and conference call are not

guarantees of future performance.”

Disclosure

2

2007 Update

Key Takeaways from Strategic Plan

Economic Environments

Inside the Supply Chain

Targeted Real Estate Investment

Leveraging our Financial Strength

Call Agenda

3

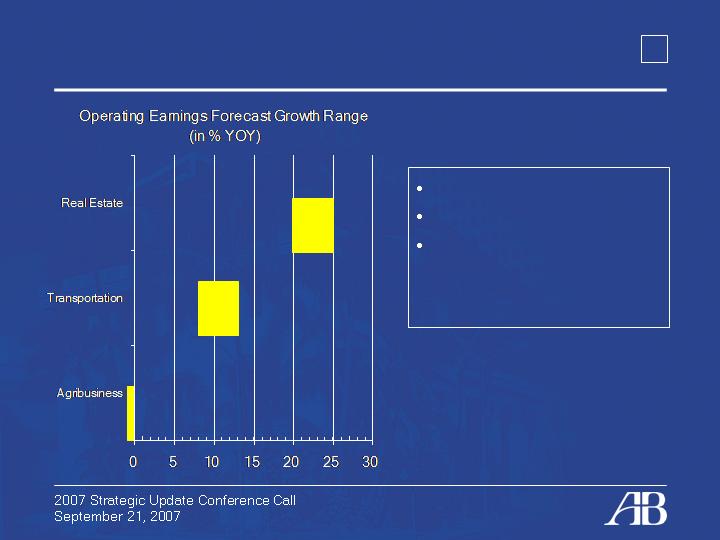

Real Estate: 20 - 25%

Transportation: 8 – 13%

3Q Earnings webcast

scheduled for 10/26

from Shanghai

2007 Business Outlook

4

2007 Update

Key Takeaways from Strategic Plan

Economic Environments

Inside the Supply Chain

Targeted Real Estate Investment

Leveraging our Financial Strength

Call Agenda

5

Strategic Plan Overview

Biennial strategic plan complete

Six-month iterative process from ground up

Solid growth prospects characterize plan

Key goal is to sustain growth in shareholder value

6

Common Strengths

Growing with what we know

Established brands and expertise are

essential to growth initiatives

Strong asset base and competitive positions

Debt capacity and projected cash flows will

again provide opportunities

Growth with a balanced risk profile

7

Key Elements of our Plan

Capitalize on investment opportunities caused by

less robust economic environments

Build on increasing international transportation

perspective and reputation

Pursuing “door-to-door” via logistics and RE

Exploring additional “port-to-port” strategies

Develop opportunities on U.S. mainland

Increase commitment to grow commercial portfolio

via land monetization

Maintain position of strength in Hawaii

8

Creating Shareholder Value

*Through September 14, 2007. ALEX vs. indices in basis points.

+130

+40

+1440

A&B vs. SPREIT

19.6

17.6

1.8

SPREIT Index

+ 320

+ 260

+ 650

A&B vs. TRAN

17.7

15.4

9.7

TRAN Index

12.8

11.6

14.9

S&P 500 (SPX)

+ 810

+ 640

+ 130

A&B vs. S&P

18.0

3 Yr

20.9

16.2

ALEX

5 Yr

1 Yr

(Total Shareholder Return %)

9

Shareholder Value Objectives

10 – 12% annual earnings growth – non-linear

Commitment to sustained dividend growth

Opportunistic share repurchases

Focused growth in higher-value segments

10

2007 Update

Key Takeaways from Strategic Plan

Economic Environments

Inside the Supply Chain

Targeted Real Estate Investment

Leveraging our Financial Strength

Call Agenda

11

Economic Environment/Opportunities

Hawaii Transportation

Economic growth plateau;

container/auto volumes flat

Continued Matson strength

and market depth

Manage costs, seek reductions

Fleet deployment efficiency

Economic Environment

Opportunities

12

Economic Environment/Opportunities

Hawaii Real Estate

Residential markets cyclically impacted

Modest to moderate impact on development pipeline

Commercial markets robust and stable

Continued supply constraint in all asset classes

Investment opportunities may accelerate

Economic Environment

Opportunities

13

Economic Environment/Opportunities

Real Estate Scenarios & Response

Modest impact on residential sales through 2008

Greater impact if prolonged to 2009 and beyond

Good environment for opportunistic investments

Little impact on short/mid-term performance

Investment environment remains challenging

III. Residential and commercial markets stable

Note: Entitlement velocity relatively independent of market cycles

II. Rise in commercial cap rates

Turnover of commercial properties sales might slow

Better environment for long-term investments

+

-

+

-

=

-

+

I. Contraction in residential markets

14

Economic Environment/Opportunities

International

Global trade prospects strong

Asian economies projected to expand by 8% in 2007, 2008

China economy strong

PRC projected to expand by 9% from 2007 - 2011

Guam outlook positive with military influx

$10B military build-up for 8K Marines

$2.6B infrastructure build-out

Economic Environment

Opportunities

Expand Asian business model

Guam infrastructure/real estate

15

Economic Environment/Opportunities

United States

MIL markets/volumes

Short-term weakness

Long-term expansion

Real Estate backbone to global trade

Supply chain outsourcing growing

Well-located logistics properties

increasingly valuable

Logistics/Real Estate links forming

Leasing portfolio

MIL offices/network

Economic Environment

Opportunities

16

2007 Update

Key Takeaways from Strategic Plan

Economic Environments

Inside the Supply Chain

Targeted Real Estate Investment

Leveraging our Financial Strength

Call Agenda

17

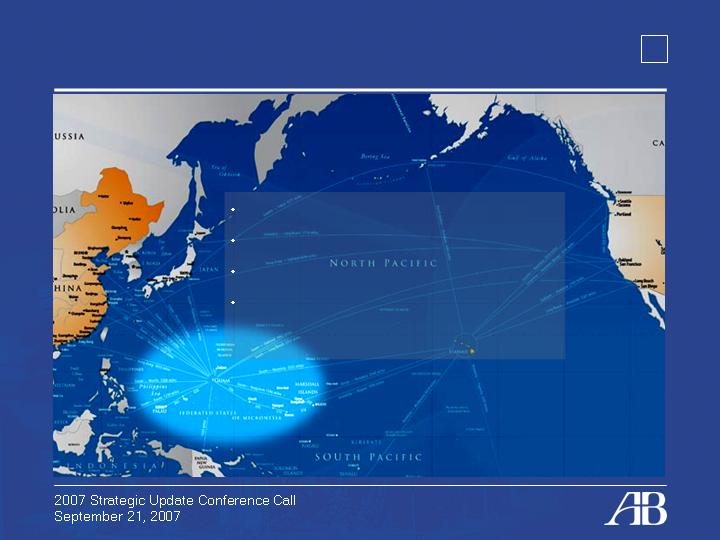

Inside the Supply Chain

Evolution versus Revolution

Value creation shifts from “port-to-port” to “door-to-door”

based on ALEX asset, market and financial strength

Port to Port

Matson Navigation

China/Asia

Port to DC

Matson

Integrated

Logistics

DC to Retail

Matson Global

United States

DC to Port

Matson

Integrated

Logistics

Factory to

Distribution Center

Matson Global

PORT

PORT

18

Inside the Supply Chain

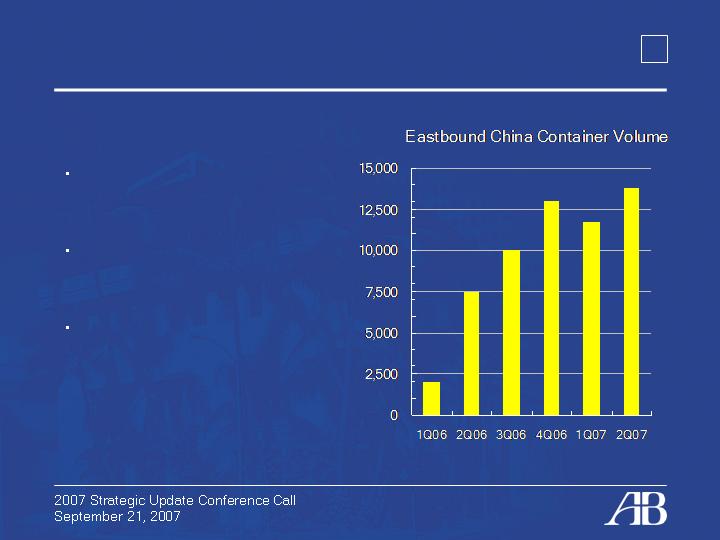

China Service – Port to Port

Reaching full capacity with

current deployment

Growing yields primary focus:

progress in 2007

Exploring other port to port

options

19

Inside the Supply Chain

Matson Integrated Logistics – Domestic Port to Door

Rail Highway Expedited Specialty Warehousing

Favorable Industry

Growth

Core Competency

(A&B Properties

Warehousing)

Acquisition Appetite

20

Inside the Supply Chain

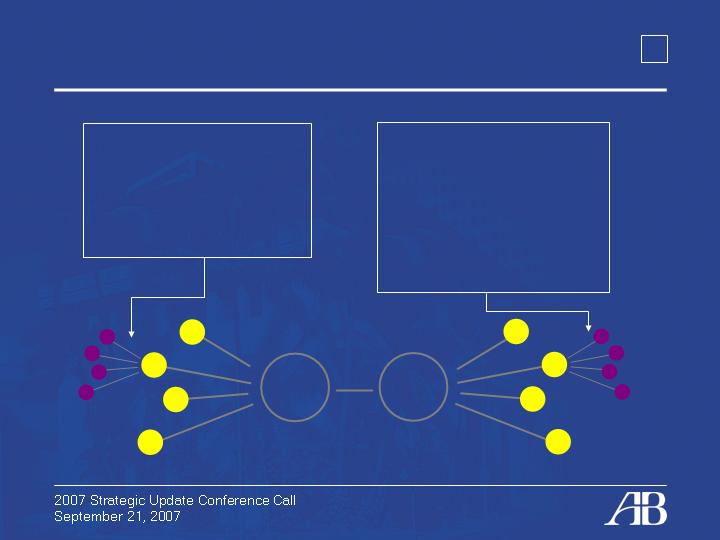

Matson Global Distribution Services – Door to Door

Asia

Warehousing

NVOCC

Freight Forwarding

Inland Transportation

United States

Guaranteed China-U.S.

Deconsolidation/Transload

Warehousing

Value Added Services

NVOCC/Freight Forwarding

Network Design

Local Distribution

21

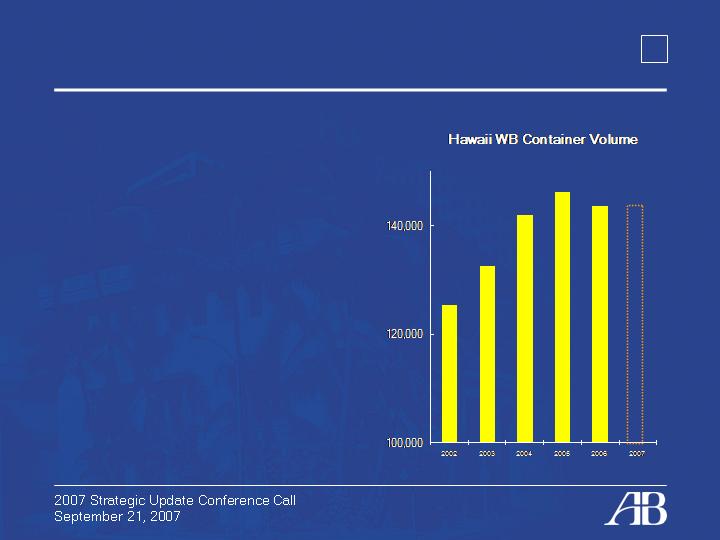

A Rising Guam Market

Military redeployment provides opportunity

Rising volume tide evidenced in 2007

Significant infrastructure requirements

Potential to grow as transshipment center

22

2007 Update

Key Takeaways from Strategic Plan

Economic Environments

Inside the Customer Supply Chain

Targeted Real Estate Investment

Leveraging our Financial Strength

Call Agenda

23

Targeted Real Estate Investments

Earn

Operate, realize value of current development

pipeline investments & leasing portfolio

Grow

Dedicated development expansion; Hawaii first,

mainland second, but increasing

Allocate

Leasing portfolio expansion from land monetization

Continued use of 1031 exchange

24

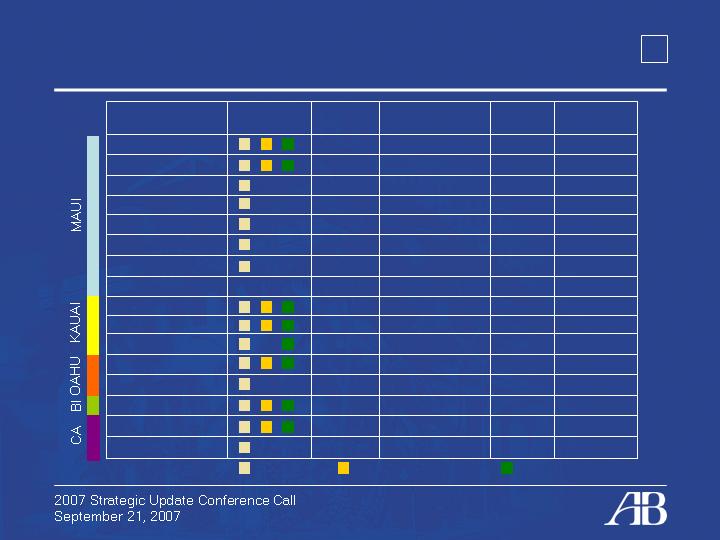

Targeted Real Estate Investments

Development Pipeline – Earn

137

31

SF/MF Homes

J.V.

Ka Milo

5

57

Commercial

J.V.

Valencia

TBD

30

Commercial

J.V.

Bakersfield

5,000

352

24

132

1,200

TBD

440R/200K s.f.

103

TBD

75

9

1C/12R

150

Total Units

325

SF Lots

A&B

Brydeswood

17

SF Homes

A&B

Port Allen

4

Condominium

A&B

Kane Street

20

Mixed Use

A&B

Kahului Town Center

180

Commercial

A&B

Maui Business Park II

1,000

3

1,000

145

13

7

11

25

Acreage

J.V.

A&B

J.V.

TBD

A&B

A&B

A&B

J.V.

Structure

Master Community

Condominium

Mixed Use

TBD

MF Homes

SF Lots

Comm/Res.

MF Homes

Asset

Class

Waiawa

Keola La'i

Kukui'ula

Additional Wailea

Wailea MF-7

Wailea MF-19

Wailea MF-11

Kai Malu at Wailea

Status

Entitled

Under construction

Sales Commenced

25

Targeted Real Estate Investments

Development Pipeline – Earn

Current diversified pipeline strength

valuable in down cycle

Diversified portfolio across geography, asset class

No direct exposure to credit market contagion

Income generation relatively secure

Free cash flow significant

26

Targeted Real Estate Investments

Project X - Grow

Hawaii projects first

Initial mainland focus in Southern California

Continue to exploit historical areas of strength:

resort and lifestyle communities

secondary, strengthening markets

Expand joint venture activities

Patience: cyclical opportunities will emerge

27

Targeted Real Estate Investments

Leasing Portfolio Reinvestment – Earn, Grow & Allocate

Strength of current model

Growing historical/prospective earnings streams

Portfolio expansion through 1031 exchanges

Concentration and asset-class focus possible

28

Targeted Real Estate Investments

Recycling Assets into Earnings Streams – Grow & Allocate

Target bulk land sales to accelerate capture of

underlying value

Reinvest proceeds to grow commercial portfolio

29

Targeted Real Estate Investments

Capital Deployment in Strategic Plan - Allocate

New Capital

Recycled Capital

1031 Exchanges

New

Investments

(Project X)

Pipeline

Development

30

Agribusiness

Sugar/coffee still best use of agricultural lands

Return to historical sugar production levels of 200K

tons annually

Triple specialty sugar capacity to 60K tons

Determine role of energy initiatives in HC&S’ future

31

2007 Update

Key Takeaways from Strategic Plan

Economic Environments

Inside the Customer Value & Supply Chain

Targeted Real Estate Investment

Leveraging our Financial Strength

Call Agenda

32

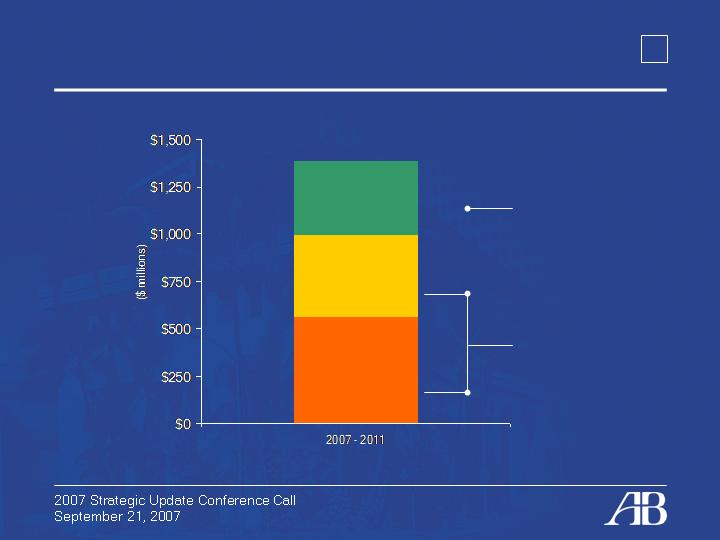

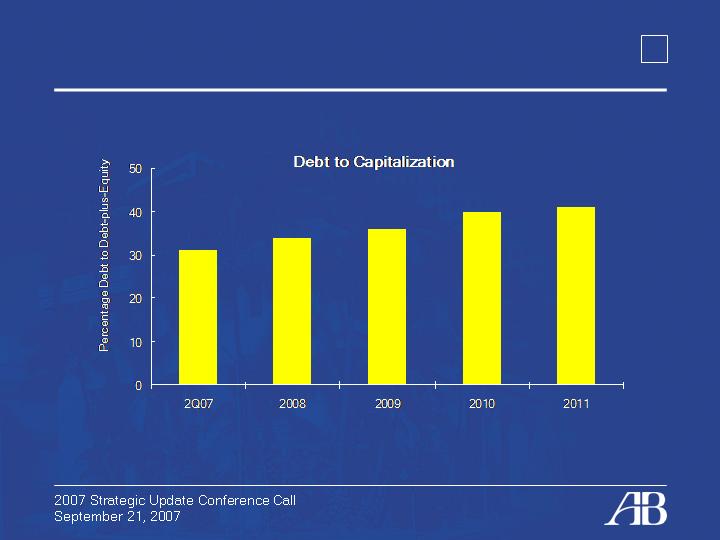

Leveraging Our Financial Strength

Projected Debt

33

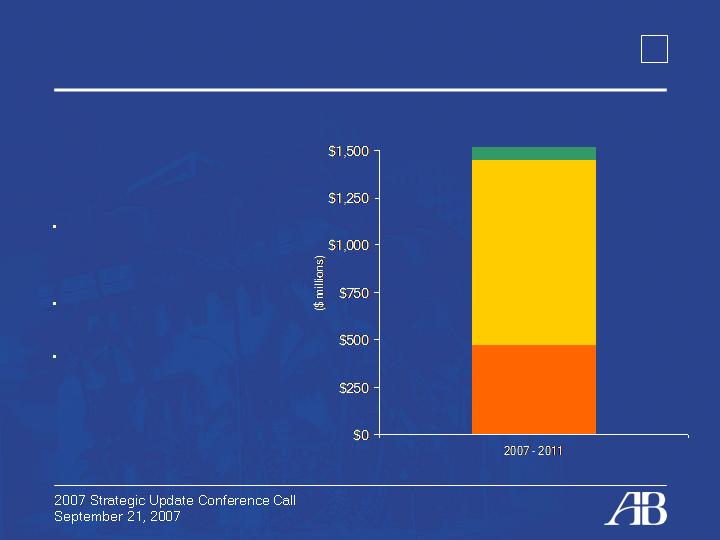

Leveraging Our Financial Strength

Capital Allocation (excluding 1031 Exchanges*)

$1.5 Billion at work:

2/3 allocated to growth

capital, mostly real

estate

Allocation for MIL

acquisitions

Matson vessel

investment cycle

mostly outside of Plan

Excludes $400MM of 1031 exchange capital

Agribusiness

Real Estate

Transportation

34

Leveraging Our Financial Strength

Free Cash Flow

Core businesses generate significant FCF above

and beyond replacement capital growth, creates

opportunities

Properties capital budget includes large amount of

“quick turn” capital. Asset base grows more slowly

as cash is recycled

35

Conclusion

We will create supply chain solutions by leveraging

and expanding our transportation and real estate

businesses

We will accelerate and intensify development

investment, land monetization and income

portfolio expansion

We will leverage our financial strength

We are committed to double digit earnings growth

36

Q&A

Questions & Answers

37