Citizens Republic Bancorp (CTZ+A) Inactive

Filed: 26 Jul 06, 12:00am

2nd Quarter 2006

Investor Presentation

July 2006

Filing pursuant to Rule 425 under the

Securities Act of 1933, as amended

Deemed filed under Rule 14a-12 under the

Securities Exchange Act of 1934, as amended

Filer: Citizens Banking Corporation

Subject Company: Republic Bancorp Inc.

Exchange Act File Number of Subject Company:

000-15734

Safe Harbor Statement

Discussions in this release that are not statements of historical fact (including statements that include terms

such as “will,” “may,” “should,” “believe,” “expect,” “anticipate,” “estimate,” “intend,” and “plan”) are forward-

looking statements that involve risks and uncertainties, and Citizens’ actual future results could materially differ

from those discussed. Factors that could cause or contribute to such differences include, without limitation,

adverse changes in Citizens’ loan and lease portfolios resulting in credit risk-related losses and expenses

(including losses due to fraud, Michigan automobile-related industry changes and shortfalls, and other economic

factors) as well as additional increases in the allowance for loan losses; fluctuations in market interest rates,

the effects on net interest income of changes in Citizens’ interest rate risk position and the potential inability to

hedge interest rate risks economically; adverse changes in economic or financial market conditions and the

economic effects of terrorist attacks and potential attacks; Citizens’ potential inability to continue to attract core

deposits; Citizens’ potential inability to continue to obtain third party financing on favorable terms; adverse

changes in competition, pricing environments or relationships with major customers; unanticipated expenses

and payments relating to litigation brought against Citizens from time to time; Citizens’ potential inability to

adequately invest in and implement products and services in response to technological changes; adverse

changes in applicable laws and regulatory requirements; the potential lack of market acceptance of Citizens’

products and services; changes in accounting and tax rules and interpretations that negatively impact results of

operations or financial position; the potential inadequacy of Citizens’ business continuity plans or data security

systems; the potential failure of Citizens’ external vendors to fulfill their contractual obligations to Citizens;

Citizens’ potential inability to integrate acquired operations, including those associated with the pending merger

with Republic Bancorp; unanticipated environmental liabilities or costs; impairment of the ability of the banking

subsidiaries to pay dividends to the holding company parent; the potential circumvention of Citizens’ controls

and procedures; Citizens’ success in managing the risks involved in the foregoing; and other risks and

uncertainties detailed from time to time in its filings with the Securities and Exchange Commission. Other

factors not currently anticipated may also materially and adversely affect Citizens’ results of operations. There

can be no assurance that future results will meet expectations. While Citizens believes that the forward-looking

statements in this release are reasonable, you should not place undue reliance on any forward-looking

statement. In addition, these statements speak only as of the date made. Citizens does not undertake, and

expressly disclaims any obligation to update or alter any statements, whether as a result of new information,

future events or otherwise, except as required by applicable law.

2

Additional Information

In connection with the proposed merger, Citizens and Republic will file a joint proxy statement/prospectus with

the Securities and Exchange Commission (“SEC”). Investors and security holders are advised to read the

joint proxy statement/prospectus when it becomes available because it will contain important

information. Investors and security holders may obtain a free copy of the joint proxy statement/prospectus

(when available) and other documents filed by Citizens and Republic with the SEC at the SEC’s website at

http://www.sec.gov. Free copies of the joint proxy statement/prospectus (when available) and each company’s

other filings with the SEC may also be obtained by accessing Citizens’ website at http://www.citizensonline.com

under the Investor Relations section or by accessing Republic’s website at http://www.republicbancorp.com under

the Investor Relations section.

Citizens and Republic and their respective directors, executive officers and other members of their management

may be soliciting proxies from their respective shareholders in favor of the merger. Information concerning

persons who may be considered participants in the solicitation of Citizens’ shareholders under the rules of the SEC

is set forth in the Proxy Statement filed by Citizens with the SEC on March 22, 2006, and information concerning

persons who may be considered participants in the solicitation of Republic’s shareholders under the rules of the

SEC is set forth in the Proxy Statement filed by Republic with the SEC on March 14, 2006. Additional information

regarding the interests of those participants and other persons who may be deemed participants in the

transaction may be obtained by reading the joint proxy statement/prospectus regarding the proposed merger

when it becomes available. You may obtain free copies of these documents as described above.

This communication shall not constitute an offer to sell or the solicitation of an offer to buy securities, nor shall

there be any sale of securities in any jurisdiction in which such solicitation or sale would be unlawful prior to the

registration or qualification under the securities laws of such jurisdiction.

3

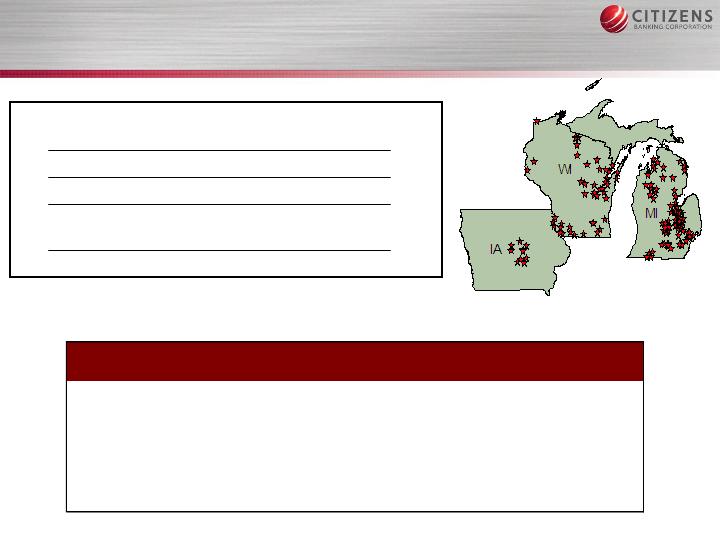

Who We Are

4

Source: SNL DataSource Deposit Market Share Analysis

182 Branch & Financial Centers

193 ATMs

2nd largest bank holding company in

Michigan

68th largest bank in the U.S.

$7.8 billion in assets

$2.6 billion in trust assets under

administration

$1.0 bil market cap as of June 30, 2006

Key

Total

Deposits

Mkt. Share

Markets

Rank

Branches

Loans

$MM

%

Flint, MI

1

21

621

$

1,536

$

37.6%

Saginaw/BC/Mid, MI

2

22

719

$

679

$

17.3%

Southeast, MI

24

15

941

$

288

$

0.4%

Jackson, MI

3

9

365

$

238

$

14.7%

Lansing, MI

6

13

212

$

310

$

5.8%

Fox Valley, WI

7

5

128

$

160

$

5.4%

Our Turnaround Strategy

Since 2002

Build a strong proven management team:

Large, community, and multiple lines of business experience

Experience in turnarounds, culture change and transformations

Hire the best with strong injection of expertise

Front line authority and capability to provide solutions

Back office - “store support” for the front line

Enhance our product array to compete at all levels

Treasury/Cash Management

Business Deposit Products (bundled services, imaging, internet)

Wealth Management

Develop a rigorous and disciplined sales management

focus with consultative selling

Leverage sales culture and process to gain “fair share”

Streamlined operating model with high touch - high service

Lightning fast response time on decisions and problem resolution

5

Our Turnaround Strategy

Since 2002

Invest into high growth markets enhancing our

footprint

Southeast Michigan

New management team and seasoned personnel in Wisconsin

Make the necessary people and process changes to

enhance our operating model

Enterprise risk management

Program management process with certified leaders

Establish “core competencies” in Balance Sheet Mgt.

Credit Quality – underwriting, monitoring, collection

Asset/Liability Management

Institutionalize cost management

6

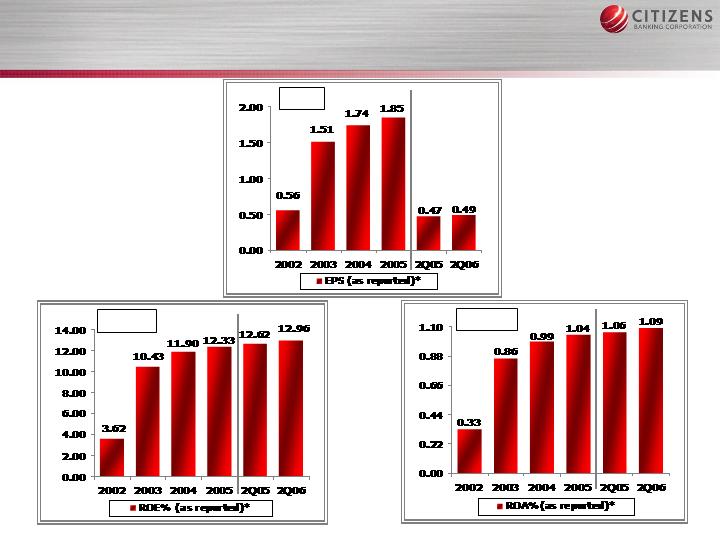

Proven Ability to Execute

* As reported includes continued and discontinued operations for 2002-2004 (see slide 25).

ROE%

EPS

ROA%

7

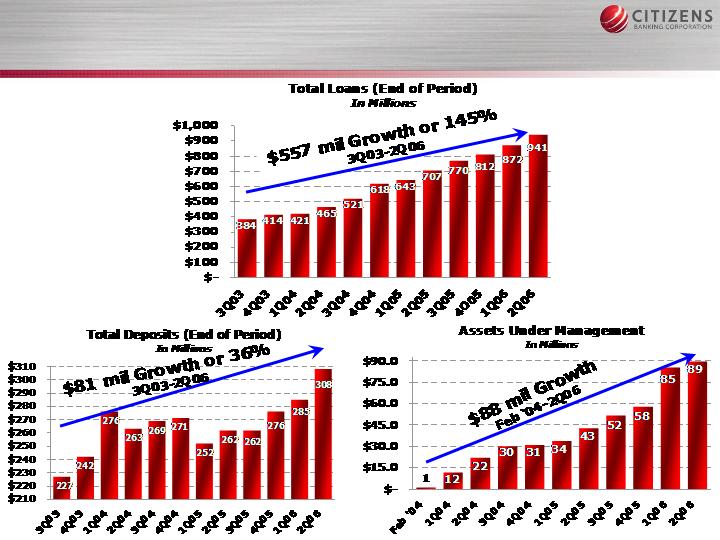

Proven Ability to Execute

Consistent Loan Growth Trends

* Restated – excludes Illinois subsidiary balances which are now treated as discontinued operations.

Total Loans (Less Mortgage & HFS)

After a Period of Rationalizing Credit

8

Proven Ability to Execute

Southeast Michigan Initiative

9

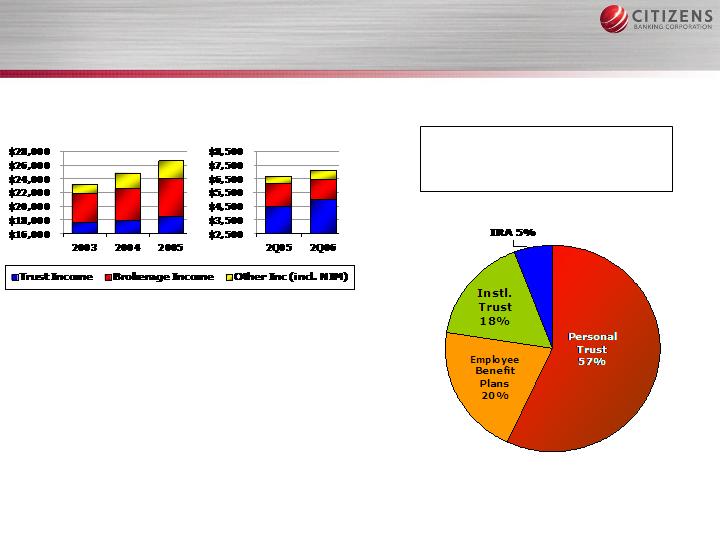

Proven Ability to Execute

Wealth Management

Annual

Quarterly

Total Revenue

Delivering growth through

objective and unbiased

investment advice utilizing an

open architecture environment

June 2006 (EOM)

Trust Assets under Administration

($2.6 Billion)

Personal Trust includes Private

Asset Management and Personal

Trust Services

10

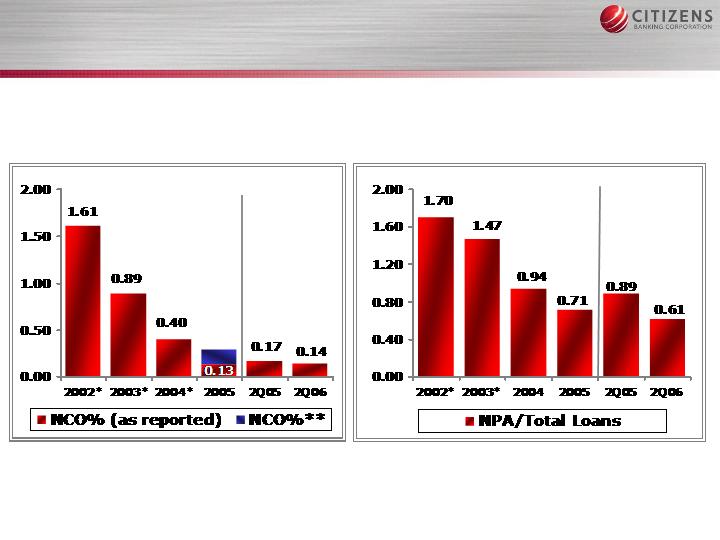

0.29**

** As reported NCO% = 13bps; Excluding the 4Q05 $9.1 mil insurance settlement NCO% = 29bps.

Proven Ability to Execute

Credit Quality

* Restated – excludes Illinois subsidiary which is now treated as discontinued operations.

Net Charge-off %

NPA %

11

Proven Ability to Execute

High Grade Consumer Underwriting

12

Our Highest Strategic Priorities

Increase the emphasis on solutions driven, low cost deposit

generation from consumers, small business,

commercial/business banking, and municipalities

Strengthen and Execute our Value Proposition in all lines of

business and markets as the best institution to bank with based

on enhanced client service and outstanding human capital

Differentiated service quality

Proactive operating model with Lightning Fast response

Increase the effectiveness of our operating model in all of our

community markets

Continue the emphasis on growing loans, total deposits, and fee

based services while increasing cross-sales within and across

lines of business

Accelerate the sales cycle in Commercial and Wealth and leverage the cross-

sell opportunities

Continue to maintain our strong commitment to balance sheet

management:

Credit Quality

Asset/Liability Management

Regulatory Compliance

13

Immediately GAAP and cash accretive to EPS for all shareholders

Financial returns improved - utilizes existing operating capacity for improved efficiency

Combines strong credit cultures

Attractive dividend yield of 4.75%

45th largest bank holding company in the United States

$2.0 billion in combined market capitalization (1)

275 branches in five states

$13.9 billion in assets, $8.6 billion in deposits and $2.6 billion in trust assets

Well positioned for further growth

The New Citizens Republic Bancorp

Company Profile

Enhanced Scale

Complementary

Business Mix

Combined sales and service culture enhances product suite and distribution channels

Broader retail, commercial banking, and commercial real estate businesses

Expanded wealth management capabilities and scale

Balanced and focused mortgage banking business

Attractive SBA, RV/Marine and asset-based lending businesses

Geographically

Diversified

Footprint

Improves existing MI footprint while expanding presence into new, attractive markets

Well positioned to compete with super regionals and community banks

Significantly increases SE Michigan presence - almost 5% of total Michigan deposits

Stable niche franchises in WI, OH, IA and IN

Key social issues decided - new executive management focused on execution

Familiar markets and businesses

In-market transaction - reasonable cost savings assumptions

Manageable

Execution Risk

Financially

Attractive

(1) Based on CBCF average closing price for 10 trading days ended 6/26/06

14

Merger Caps Turnaround Efforts

Initiated in 2002

Republic adds significant senior management depth and talent to current Citizens leadership

team

Long-term track record of consistent financial performance and shareholder value creation

Republic ranked #17 in Fortune’s 2006 “100 Best Companies to Work For” - 6 th year on list

and Working Mother magazine’s list of “100 Best Companies For Working Mothers” - 5th year

in a row

Build a Strong

Management Team

and Corporate

Culture

Enhance Product

Array to Compete

at All Levels

Adds #1 SBA bank lender based in Michigan - 11 consecutive years

Adds exceptional mortgage banking and commercial real estate capabilities and expertise

Potential to leverage Citizens’ wealth management, commercial and cash management

products across Republic’s customers and markets

Rigorous and

Disciplined Sales

Management

Focus

Republic operates a streamlined operating model emphasizing high touch and high

quality service - aligned with Citizens’ new strategy

Further leverages sales culture and processes to gain market share and growth

19% of Republic’s deposits are from Southeast Michigan

Significantly increases Southeast Michigan presence from 20 to 39 locations

Increases % of deposits in large MSAs from 54% to 64%

Republic also adds $375+ million in deposits and 14 branches in Cleveland and Akron, Ohio

Invest in High

Growth Markets/

Enhance Footprint

Establish Core

Competency in

Balance Sheet

Management

Republic maintains a lower risk credit profile - 48% of loans in residential mortgages

Republic’s historical charge-off metrics among the best in Midwest

peer group (14 bps on average over past 3 years)

Citizens Goals

Republic Impact

15

16

Top Markets — Total Deposits(1)

(in millions)

Source: SNL Financial as of 6/30/05

(2) Includes Corporate Public Funds deposit balances

(1) Does not include the impact of potential divestitures

(2)

(2)

Creates Leading Michigan Franchise with Capacity for

Additional Deposit Growth

Note: Excludes RBNC’s Indianapolis LPO

Rank 1 1 9 1 2

Deposits by State

Complementary Geographic

Footprints

Total Deposits - Michigan

Rank

Institution

Branches

Deposits

($mm)

Mkt Share

(%)

1

LaSalle Bank

263

19,098

13.7

2

Comerica

254

18,305

13.1

3

JPMorgan Chase

256

17,166

12.3

4

Fifth Third

263

12,670

9.1

5

National City

264

9,916

7.1

6

Flag

star Bancorp

108

8,151

5.9

7

Pro Forma Citizens/Republic

1

89

6,581

4.7

8

Royal Bank of Scotland

127

5,197

3.7

9

Huntington Bancshares

117

4,943

3.6

10

Chemical Financial

134

2,878

2.1

17

(2) Deposit data as of 6/30/05

(3) Loan data as of 3/31/06

Source: SNL Financial and management data

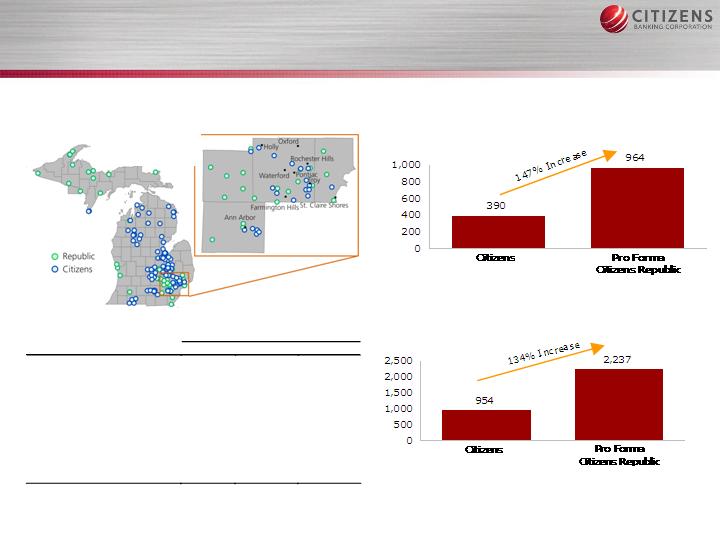

Southeast Michigan Deposits (39 Branches(1)(2))

(in millions)

Southeast Michigan Loans(1)(3)

(in millions)

Southeast Michigan Demographics

Attractive Southeast Michigan

Presence

Growth

2005

‘0

0

–

‘

05

E

‘05

–

‘10

E

Population

Southeastern MI Average

(

1

)

6.26

%

6.73

%

Michigan

3.74

4.08

National

6.15

6.26

Household Income

Southeastern MI Average

(1)

$

84,674

15.09

%

17.97

%

Michigan

Median

50,118

12.16

10.95

National

Me

dian

49,747

17.98

17.36

(1)

Selected Southeast

ern Michigan counties include:

Livingston, Macomb, Oakland

and Washtenaw

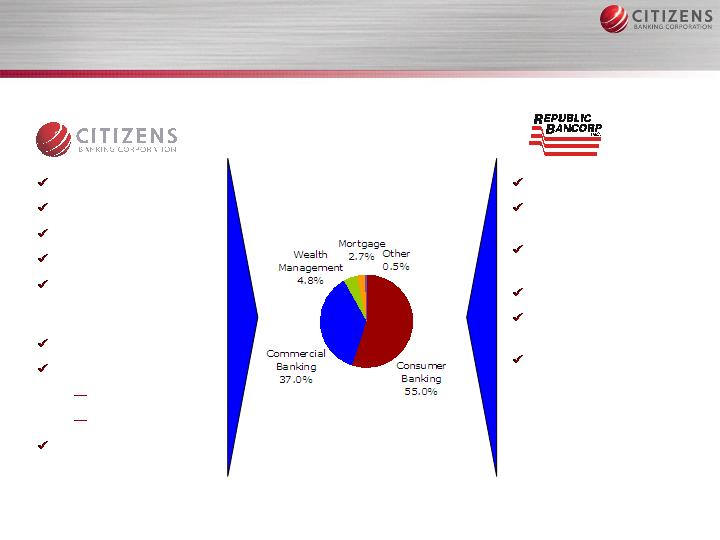

Retail Banking

Consumer

Lending

Commercial

Real Estate

SBA Lending

Mortgage

Banking

Commercial and

Residential

Construction

Lending

Complementary Business Focus and Mix

Provide Significant Potential for Revenue Enhancements

Retail Banking

Consumer Lending

Commercial Banking

Treasury/Cash Mgmt.

Rate Risk Mgmt. and

International

Services

Wealth Management

Specialty Lending

RV/Marine

Asset Based

Mortgage Banking

1Q06 Net Revenues: $142.4mm

Superior Product Suite

Source: Company filings

18

Manageable Execution Risk

Key decisions have been made

Senior leadership roles defined at announcement

Other key social issues have been agreed upon

Friendly,

in-market

Merger

Mitigating

Integration Risk

Complementary branch networks with modest branch overlap

Complementary product offerings and capabilities

Strong regional brand

Reasonable and achievable cost savings assumptions (9% of combined expenses)

Revenue enhancements have been identified but not included in the pro forma

financials

Experienced

Management

Teams

Successful acquisition integration a core competency of both management teams

Compatible service-oriented corporate cultures and strategies

Repositions balance sheet to mitigate interest rate risk, improve liquidity,

reduce reliance on wholesale funding, and improve quality of earnings

Aligns credit policies, guidelines, discipline, and processes - moving the

combined organization to Citizens’ standards and practices

Risk

Management

19

20

Pro Forma Financial Impact

Analysis (1)

2007

($mm, except per share data)

70% Phase-in

100% Phase-in

Citizens Stand Alone Net Income (2)(3)

88

88

Republic Stand Alone Net Income (2)(3)

70

70

Cost Savings (After-tax) (2)(4)

13

18

Other Adjustments (After-tax) (2)(5)

(14)

(14)

Pro Forma Net Income

157

162

Pro Forma Avg. Fully-Diluted Shares (mm)

76

76

Pro Forma GAAP EPS

2.07

2.13

Pro Forma Cash EPS

2.16

2.23

Impact to Citizens Republic

Accretion/(Dilution) to GAAP EPS (%)

0.9

4.0

Accretion/(Dilution) to Cash EPS (%)

3.3

6.3

(1)

Based on 0.515 exchange ratio for an implied transaction value of $1,048 mm and 15% cash/85%

stock consideration

(2)

Assumes 35% tax rate

(3)

Assumes 2007 GAAP EPS estimates for Citizens of $2.05 and Republic of $0.93

(4)

Assumes $28mm in pre-tax cost savings phased-in 70% in 2007 and 100% in 2008

(5)

CDI amortization, net of Republic’s existing CDI amortization, cost of financing, and funding of

,

restructuring costs (5.00% pre-tax). Includes impact of balance sheet restructuring and purchase

accounting mark-to-market adjustments

Favorable Pricing

21

Citizens/Republic

Median of Comparable

Transactions

(1)

Price/Forward Earnings (x)

15.4

(

2

)

19.9

Price/Forward Earnings with Cost Savings (x) (3)

12.

2

14.1

Price/

Book Value (x)

2.5

8

(

4

)

2.21

Price/

Tangible Book Value (x)

2.

60

(

4

)

3.04

(1)

Bank and thrift transactions between $500 million and $2.5 billion announced after 1/1/04

(2)

Based on I/B/E/S estimates

(3)

Assumes fully phased-in cost savings

(4)

Financial data as of 3/31/06

Sources of Cost Savings

Annual cost savings

already identified

$28 million or 9% of combined expense base

70% phase-in for 2007 and 100% thereafter

Anticipated $87 million pre-tax restructuring costs

22

Sources of Cost Savings/Restructuring Costs

(

1

)

Includes severance, change of controls for Republic & Citizens, and retention

(

2

)

Includes fixed asset write-offs and branding including signage & colleratal materials

(

3

)

Includes capital improvements/conversion costs, advisory fees, other balance

Sheet fees, contract costs, and restricted stock

(

$mm

)

Fully Phased-in

Annual

Cost Savings

Restructuring

Costs

Personnel

$16

$

4

0

(1)

Facilities/Branches

2

17

(2)

Systems/Other

10

30

(3)

Total (Pre-tax)

$28

$

87

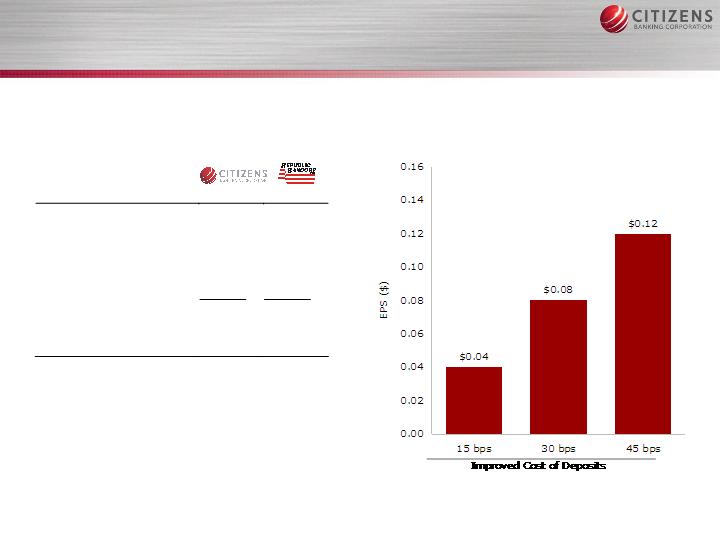

Opportunity to Improve Deposit

Mix and Costs

23

Potential EPS Benefit Related to

Change in Republic’s Deposit Mix

and Pricing

(%)

(%)

Non

-

Interest Bearing

16.3

9.0

Interest-Bearing Demand

14.8

6.0

MMDA & Savings

26.3

27.9

Time Deposits

42.6

57.1

Total

100.0

100.0

Cost of Deposits

2.28

2.8

1

Source: Company filings as of 3/31/06

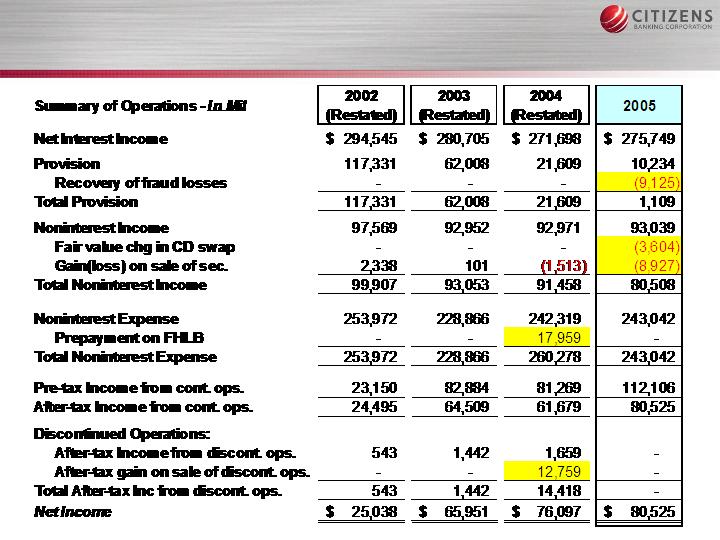

Financial Highlights

Summary Income Statement

(Full Year)

25

Summary Income Statement

(Quarterly)

26

Summary of Operations - In Mil

2Q05

1Q06

2Q06

Net Interest Income

68,779

$

67,475

$

65,990

$

Provision

1,396

3,000

1,139

Noninterest Income

23,109

22,657

23,691

Gain(loss) on sale of sec.

37

7

54

Gain on sale of Royal Oak

-

2,906

-

Total Noninterest Income

23,146

25,570

23,745

Noninterest Expense

60,990

60,122

60,065

Contribution to Charitable Trust

-

1,450

-

Total Noninterest Expense

60,990

61,572

60,065

Pre-tax Income

29,539

28,473

28,531

Net Income

20,565

$

20,756

$

20,907

$

EPS (Diluted)

$0.47

$0.48

$0.49

ROE%

12.62%

12.86%

12.96%

ROA%

1.06%

1.10%

1.09%

NIM%

3.92%

3.97%

3.84%

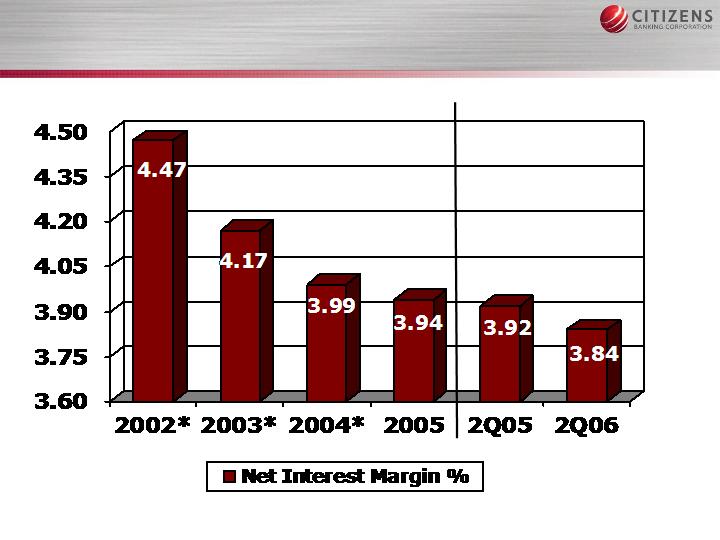

Asset/Liability Management

Continues to Provide a Strong NIM%

* Restated – excludes Illinois subsidiary which is now treated as discontinued operations.

27

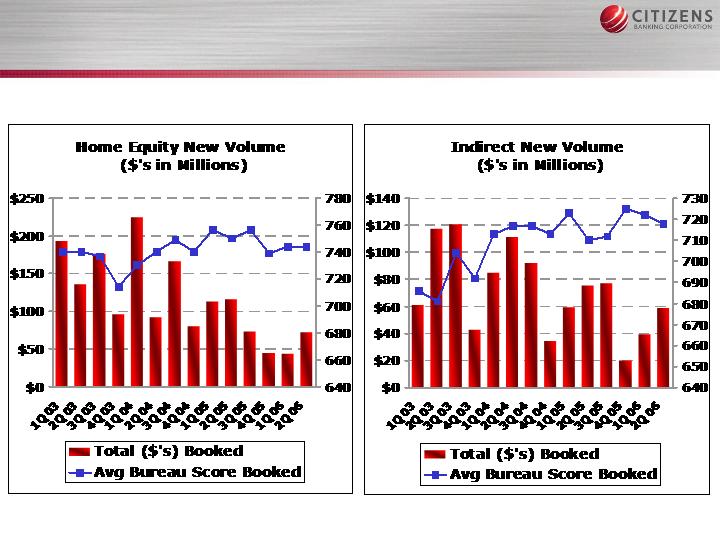

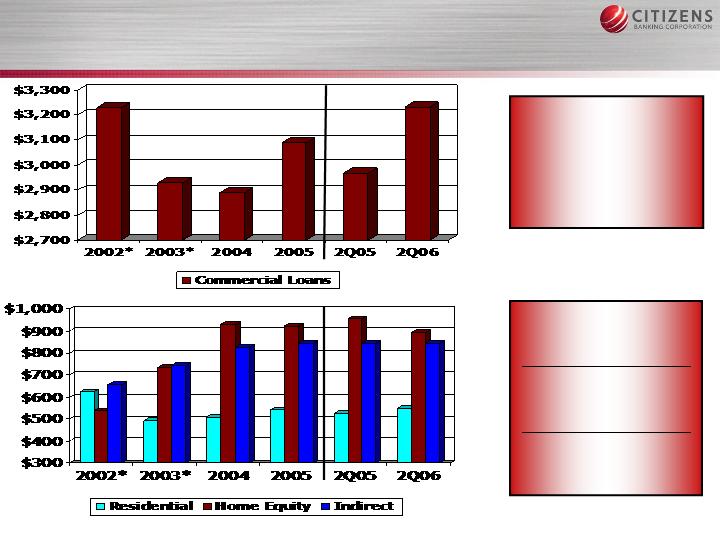

Loan Highlights During a Highly

Competitive Period (in millions – end of period)

Commercial

grew 8.9% from

2Q05 to 2Q06

(all markets

showed growth in

2005)

Home Equity has

grown 72% from

2002 to 2005

Indirect has grown

29% from

2002 to 2005

Current Economic

Cycle – Flat

Consumer Volume

* Restated – excludes Illinois subsidiary balances which are now treated as discontinued operations.

28

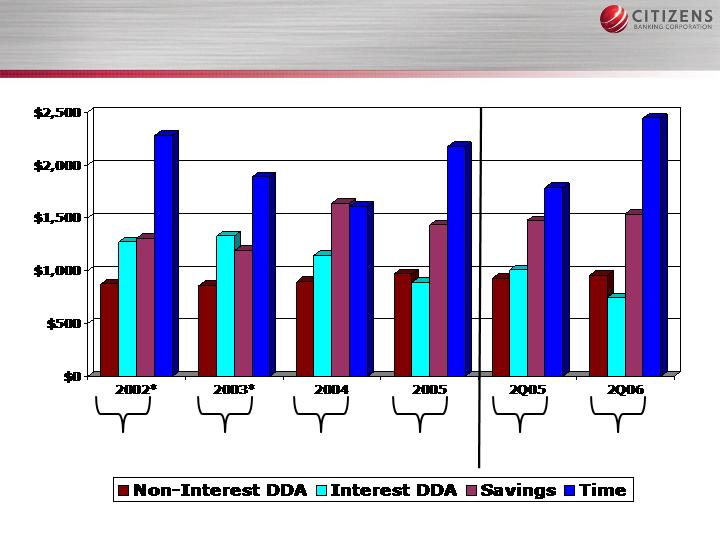

Consistent Core Funding Base

(in millions – end of period)

* Restated – excludes Illinois subsidiary balances which are now treated as discontinued operations.

Core %

60%

Core %

64%

Core %

70%

Core %

60%

Core %

57%

Core %

66%

29

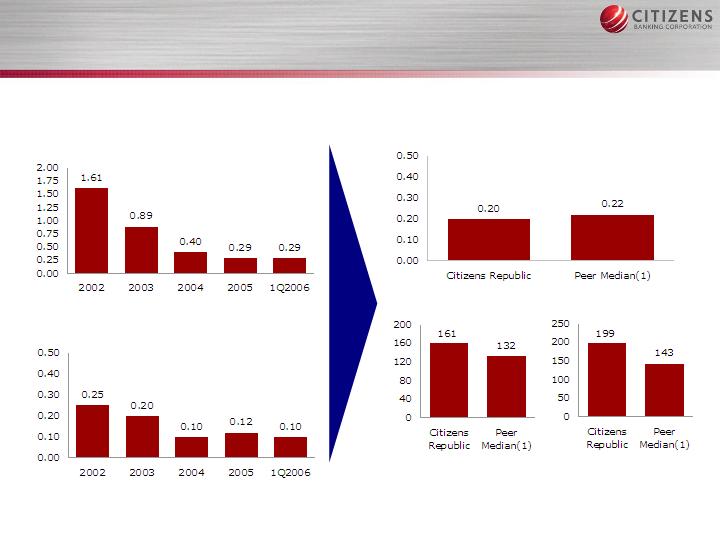

Key Credit Quality Ratios

30

* Restated – excludes Illinois subsidiary which is now treated as discontinued operations.

** As reported 2005 NCO% = 13bps; Excluding the 4Q05 $9.1 mil insurance settlement NCO% = 29bps.

2002*

2003*

2004*

2005

2Q05

2Q06

Credit Quality

LLR/NPA

118%

160%

240%

292%

245%

330%

LLR/NPL

130%

178%

285%

358%

284%

420%

NPA/Total Loans

1.70%

1.47%

0.94%

0.71%

0.89%

0.61%

NCO%

1.61%

0.89%

0.40%

0.13%

**

0.17%

0.14%

LLR%

2.01%

2.35%

2.27%

2.07%

2.17%

2.00%

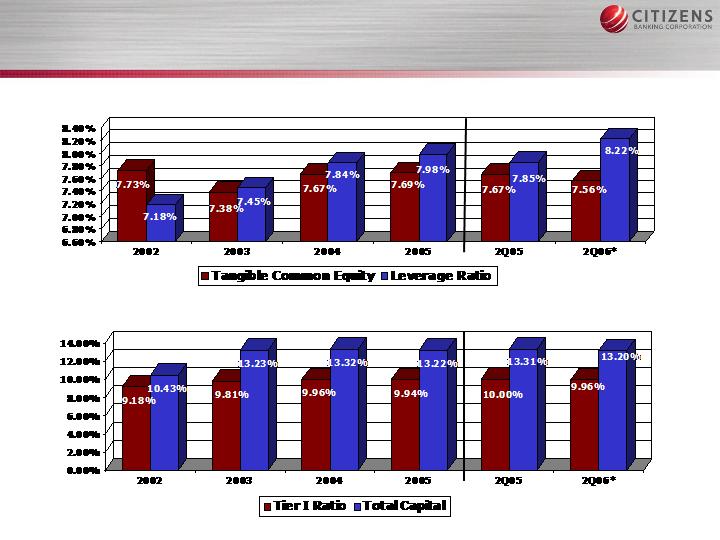

Capital Management

* Estimate

31

Strategic Rationale for the

Combination

Enhances scale and overall franchise value

Improves geographic footprint—expands presence in

attractive markets

Diversifies revenue mix through complementary lines

of business adding tremendous revenue potential

Adds management depth and talent

Manageable execution risk

GAAP and Cash EPS accretive in 2007

Creating a Leading Midwestern Franchise

32

Why Invest In Citizens?

Citizens Banking Corporation (CBCF) stock:

Proven execution ability will drive success of the

integration and business strategies

The new company will possess significantly enhanced

scale/efficiency and an improved geographic footprint

Complimentary business mix will drive more revenue

opportunities

Strong management teams committed to long-

term growth, prudent risk management, and

shareholder value

Dividend Yield of 4.75% at the end of the second

quarter, with share price upside potential

Long-term outlook for earnings growth is positive

33

Appendix

Transaction Summary

Implied Per Share Consideration(1):

$2.08 cash plus 0.4378 shares of CBCF common stock per

RBNC share

$13.86 / share (1)

Implied Transaction Price:

RBNC shareholders to elect between CBCF stock and cash,

subject to proration

Stock / Cash Election:

Flint, Michigan

Corporate Headquarters:

Chairman—Jerry Campbell (until YE 2007) when Bill Hartman

succeeds (until YE 2012)

CEO—Bill Hartman (until YE 2010) when Dana Cluckey

succeeds

President & COO—Dana Cluckey

Executive Management:

9 Citizens directors / 7 Republic directors

Board of Directors Composition:

Fourth quarter 2006

Expected Closing:

$36mm (3.5% of transaction value)

Termination Fee (mutual):

Completed

Due Diligence:

(1) Based on CBCF average closing price for 10 trading

days ended 6/26/06. Includes net options.

Approximately 85% stock / 15% cash

Fixed number of CBCF shares—approximately 33.2 million

Fixed cash amount of approximately $155 million

Consideration Mix:

Stock Component to RBNC Shareholders:

Cash Component to RBNC Shareholders:

Transaction Value at Announcement:

$1.048 billion (1)

56% Citizens / 44% Republic

Pro Forma Ownership:

Regulatory; Citizens and Republic shareholders

Approvals:

35

Strong, Experienced

Management Team

Jerry Campbell

Chairman

Charlie Christy

CFO

Tom Menacher

Merger Integration

Roy Eon

Operations/

Technology

Debra Hanses

Human

Resources

Clint Sampson

Regional Chairman –

MI Commercial

Banking

John Schwab

Chief Credit Officer

Cathy Nash

Retail Banking

Jim Schmelter

Wealth

Management

Bill Hartman

CEO

Dana Cluckey

President & COO

Randy Peterson

Regional Chairman—

Wisconsin and Iowa

Cathy Rosenthal

Corporate

General Auditor

36

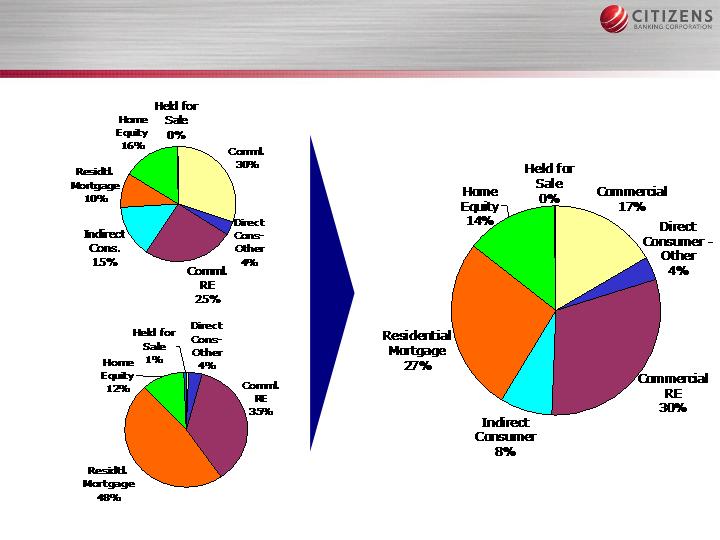

Diversified Loan Portfolio

(as of 1Q06)

Citizens

Republic

Citizens Republic

Combined

Source: Company filings and management data

37

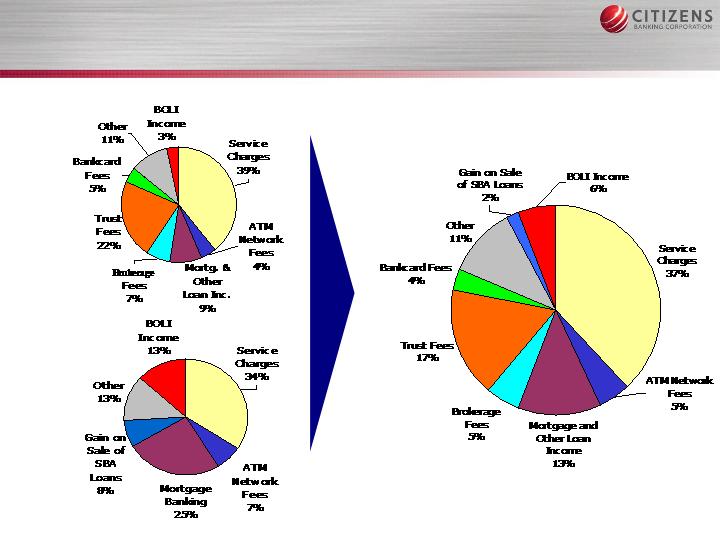

Diversified Fee Income Base

(as of 1Q06)

Citizens

Republic

Citizens Republic

Combined

Note: Citizens and combined exclude the $2.9 million

gain on the sale of Royal Oak, MI office building

Source: Company filings and management data

38

Strong Credit Quality —

Compares Favorably to Peers

Net Charge-Off/Total Loans (%)

Net Charge-Off/Total Loans (%)

Allowance/NPAs (%)

Source: Company filings and SNL Financial

(1)

Peers include FMBI, FMER, MAFB, ONB, PRK and SKYF

Allowance/NPLs (%)

Citizens

Republic

Note: 2005 excludes the 4Q05 $9.1 mil insurance settlement; 2005 as

reported NCO% = 13bps.

39

Combined Balance Sheet

40

Source: Company filings and management data

For the Period Ended

3/31/06

Estimated at Close

($mm)

Citizens

Republic

12/31/06

(1)

Assets:

Cash and Investment Securities

1,767

1,

277

2,

687

Net Loans

5,490

4,

729

9,606

Goodwill and Intangibles

65

4

7

78

Other Assets

341

23

4

6

49

Total Assets

7,

66

3

6,

244

13,7

20

Liabilities and Equity:

Deposits

5,

524

3,

084

8,

545

Borrowings

1,3

80

2,

690

3,1

62

Other Liabilities

82

6

3

29

2

Total Liabilities

6,986

5,

837

11,99

9

Capital Securities

25

–

182

Common Equity

6

52

4

0

7

1,

54

0

Total Liabilities and Equity

7,

663

6,

244

1

3,7

20

Capital Ratios:

TCE/TA

(2)

7.

72

%

6.

4

5

%

5.89

%

Tier 1

10

.

09

%

11.12

%

9.80

%

(1)

Includes purchase accounting adjustments, balance sheet restructuring and merger synergies/costs

(2)

Includes assumed divestiture levels

Loan Portfolio

More balanced loan portfolio

Loan Composition—As of 3/31/06

41

Citizens

Republic

Combined

($mm)

Total

3/31/06

% of

Total

Total

3/31/06

% of

Total

Total

3/31/06

% of

Total

Commercial

1,689

30.2

28

0.6

1,717

16.6

Commercial Real Estate

1,419

25.

4

1,727

36.4

3,146

30.5

Residential Mortgage

549

9.8

2,267

47.8

2,816

2

7.2

Home Equity

901

16.1

551

11.6

1,452

14.0

Direct Consumer

-

Other

208

3.7

174

3.6

382

3.7

Indirect Consumer

826

14.8

-

-

826

8.0

Total Loans

5,592

100.0

4,

7

47

100.0

10,

3

39

100.0

Held for Sale

13

–

25

–

38

–

Total Gross Loans

5,605

–

4,

7

72

–

10,

377

–

Yield on Loans

6.83

%

–

6.32

%

–

6.60

%

–

Source

:

Company filings

and management

data

Deposit Profile

Deposit Composition—As of 3/31/06

42

Citizens

Republic

Combined

($mm)

Total

3/31/06

% of

Total

Total

3/31/06

% of

Total

Total

3/31/06

% of

Total

Noninterest

-

Bearing

900

16.3

278

9.0

1,178

13.7

Interest

-

Bearing Demand

816

14.8

186

6.0

1,002

11.6

MMDA & Savings

1,453

26.3

859

27.9

2,312

26

.9

Time Deposits

2,355

42.6

1,761

57.1

4,116

47.8

Total Deposits

5,524

100.0

3,084

100.0

8,60

8

100.0

Cost of Total Deposits

2.28

%

–

2.8

1

%

–

2.47

%

–

Source:

Company filings

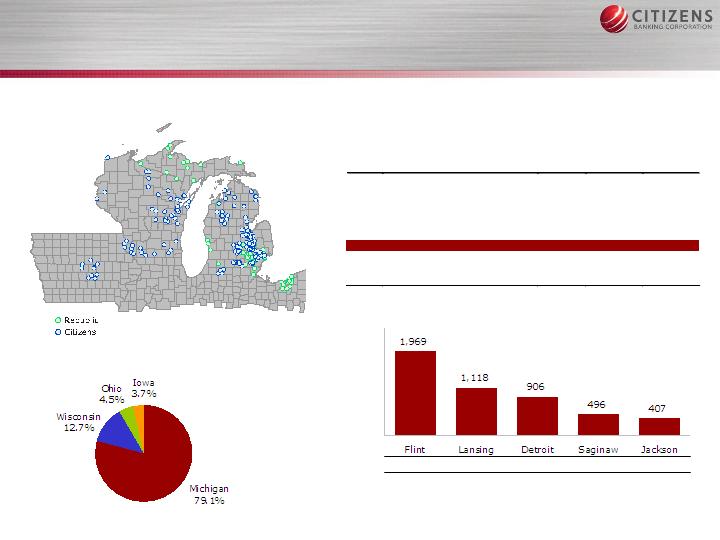

Pro Forma Market Position(1)

43

State

Branches

(No.)

Deposits

($mm)

Rank

(No.)

Cumulative %

of Franchise

Michigan

189

6,581

7

79.1

Wisconsin

54

1,057

13

91.8

Ohio

16

377

39

96.3

Iowa

11

305

33

100.0

Top 10

Markets

Flint, MI

(2

)

33

1,969

1

23.7

Lansing

-

East Lansing, MI

(2

)

18

1,118

1

37.1

Detroit

-

Warren

-

Livonia, MI

36

906

9

48.0

Saginaw

-

Saginaw Township North, MI

16

496

1

54.0

Jackson, MI

13

407

2

58.8

Cleveland

-

Elyria

-

Mentor, OH

12

342

16

62.9

Ann Arbor, MI

8

207

10

65.4

Green Bay, WI

9

174

10

67.5

Bay City, MI

5

160

4

69.5

Appleton, WI

5

160

7

71.4

(1)

Does not include the impact of potential divestitures

(2)

Includes Corporate Public Funds deposit balances

Source:

SNL Financial

as of 6/30/05