QuickLinks -- Click here to rapidly navigate through this document

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14D-9

(RULE 14d-101)

SOLICITATION/RECOMMENDATION STATEMENT

UNDER SECTION 14(d)(4) OF THE SECURITIES EXCHANGE ACT OF 1934

Advanced Neuromodulation Systems, Inc.

(Name of Subject Company)

Advanced Neuromodulation Systems, Inc.

(Name of Person Filing Statement)

Common Stock, Par Value $.05 Per Share

(Including The Associated Common Stock Purchase Rights)

(Title of Class of Securities)

801003104

(CUSIP Number of Class of Securities)

Christopher G. Chavez

President and Chief Executive Officer

Advanced Neuromodulation Systems, Inc.

6901 Preston Road

Plano, Texas 75024

(972) 309-8000

(Name, Address and Telephone Number of Person Authorized to

Receive Notice and Communications on Behalf of the Person(s) Filing Statement)

With copies to each of:

| Kenneth G. Hawari General Counsel and Executive Vice President Advanced Neuromodulation Systems, Inc. 6901 Preston Road Plano, Texas 75024-2508 (972) 309-8000 | Joseph Cialone, II Baker Botts L.L.P. One Shell Plaza 910 Louisiana Houston, TX 77002-4995 (713) 229-1234 |

- o

- Check the box if the filing relates solely to preliminary communications made before the commencement of a tender offer.

Item 1. Subject Company Information.

The name of the subject company is Advanced Neuromodulation Systems, Inc., a Texas corporation (the "Company"). The address of the principal executive offices of the Company is 6901 Preston Road, Plano, Texas 75024-2508. The telephone number of the Company at its principal executive offices is (972) 309-8000.

The title of the class of equity securities to which this Solicitation/Recommendation Statement on Schedule 14D-9 (together with the Exhibits and Annexes hereto, this "Statement") relates is the common stock, par value $.05 per share, of the Company (the "Common Stock"), including the associated common stock purchase rights (the "Rights") issued pursuant to that certain Rights Agreement, dated as of August 30, 1996, between the Company (then known as Quest Medical, Inc.), and Computershare Investor Services, L.L.C. (then known as KeyCorp Shareholder Services, Inc.), as rights agent, as amended from time to time (the "Rights Agreement").

As of October 17, 2005, 20,206,036 shares of Common Stock were outstanding.

Item 2. Identity and Background of Filing Person.

The filing person is the subject company. The Company's name, business address and business telephone number are set forth in Item 1 above.

This Statement relates to the offer by Apollo Merger Corp., a Texas corporation (the "Purchaser") and a wholly owned subsidiary of St. Jude Medical Inc., a Minnesota corporation ("St. Jude Medical"), to purchase each issued and outstanding share of Common Stock, including the attached Right (each a "Share"), for $61.25, net to the seller in cash, without interest (such price per Share, or the highest price paid in the offer, the "Offer Price"), upon the terms and subject to the conditions set forth in the Offer to Purchase, dated October 18, 2005 (as amended or supplemented from time to time, the "Offer to Purchase"), and in the related Letter of Transmittal (which, together with the Offer to Purchase, as may be amended or supplemented from time to time, constitute the "Offer"). The Offer is further described in a Tender Offer Statement on Schedule TO (as amended or supplemented from time to time, the "Schedule TO") filed by St. Jude Medical and the Purchaser with the Securities and Exchange Commission (the "Commission") on October 18, 2005. Copies of each of the Offer to Purchase and the Letter of Transmittal are attached as Exhibit (a)(1) and Exhibit (a)(2), respectively, to the Schedule TO, and each is incorporated herein by reference.

The Offer is being made pursuant to the Agreement and Plan of Merger, dated as of October 15, 2005, among St. Jude Medical, the Company and the Purchaser (the "Merger Agreement"). The Merger Agreement provides that, subject to the satisfaction or waiver of certain conditions, and in accordance with the Texas Business Corporation Act (the "TBCA"), the Purchaser will be merged with and into the Company with the Company surviving the Merger (such surviving corporation is sometimes referred to as the "Surviving Corporation" and such merger is referred to as the "Merger"). At the effective time of the Merger (the "Effective Time"), each issued and outstanding share of the common stock, par value $.01 per share, of the Purchaser will be converted into one fully paid and nonassessable share of common stock of the Surviving Corporation, all Shares that are owned by the Company as treasury stock and any Shares owned by St. Jude Medical or the Purchaser will be cancelled and retired and will cease to exist and all other issued and outstanding Shares (other than Dissenting Shares (as defined below) and Restricted Shares (as defined below) that remain subject to restrictions) will be converted into the right to receive the Offer Price, without interest (the "Per Share Price"). Shares held by shareholders who have not voted in favor of the Merger or consented thereto in writing and who have properly demanded appraisal and complied with the provisions of the TBCA relating to dissenters' rights of appraisal (the "Dissenting Shares") will not be converted into a right to receive the Per Share Price, unless such holder fails to perfect, withdraws or otherwise loses his, her or its right to appraisal.

2

As set forth in the Schedule TO, the principal executive offices of St. Jude Medical and the Purchaser are located at One Lillehei Plaza, St. Paul, Minnesota 55117. The Company is making information relating to the Offer and the Merger available on the internet at www.ans-medical.com.

Item 3. Past Contacts, Transactions, Negotiations and Agreements.

Certain contracts, agreements, arrangements or understandings between the Company or its affiliates and certain of its directors and executive officers are, except as noted below, described in the Information Statement (the "Information Statement") pursuant to Rule 14f-1 under the Securities Exchange Act of 1934, as amended (the "Exchange Act"), that is attached as Annex B to this Statement and is incorporated herein by reference. Except as described in this Statement (including in the Exhibits hereto and in Annex B hereto) or incorporated herein by reference, to the knowledge of the Company, as of the date of this Statement, there is no material agreement, arrangement or understanding or any actual or potential conflict of interest between the Company or its affiliates and (1) the Company's executive officers, directors or affiliates or (2) the Purchaser, St. Jude Medical or their respective executive officers, directors or affiliates.

Agreements with St. Jude Medical

Merger Agreement. The summary of the Merger Agreement and the description of the conditions to the Offer contained in the Introduction and Sections 11 and 15 of the Offer to Purchase, which is being mailed to shareholders together with this Statement, are incorporated herein by reference. Such summary and description are qualified in their entirety by reference to the Merger Agreement, which has been filed as Exhibit (e)(1) hereto and is incorporated herein by reference.

Confidentiality Agreement. The summary of the Confidentiality Agreement contained in Section 11 of the Offer to Purchase is incorporated herein by reference. Such summary is qualified in its entirety by reference to the Confidentiality Agreement, which has been filed as Exhibit (e)(3) hereto and is incorporated herein by reference.

Effects of the Offer and the Merger under Company Stock Plans and Agreements Between the Company and its Executive Officers

Interests of Certain Persons. Certain members of the Company's management and its Board of Directors (the "Board") may be deemed to have interests in the transactions contemplated by the Merger Agreement that are different from or in addition to their interests as Company shareholders generally. The Board was aware of these interests and considered them, among other matters, in approving the Merger Agreement and the transactions contemplated thereby. As described below, consummation of the Offer will constitute a change in control of the Company for the purposes of determining the entitlements due to the executive officers and directors of the Company in respect of certain severance and other benefits.

Stock Options. At the Effective Time of the Merger, the portion of each outstanding option to purchase shares of Common Stock issued under one of the Company's stock option plans that is vested at the Effective Time will be cancelled in exchange for a single lump sum cash payment equal to the product of (1) the excess, if any, of the Per Share Price (as defined in the Merger Agreement) over the per share exercise price of such stock option at the Effective Time and (2) the number of Shares issuable upon exercise of the vested portion of such stock option at the Effective Time, less any applicable tax or other withholdings. The portion of each outstanding option to purchase shares of Common Stock issued under one of the Company's stock option plans that is unvested at the Effective Time will be assumed by St. Jude Medical and converted into an option to purchase common stock of

3

St. Jude Medical, par value $.01 per share ("St. Jude Medical Common Stock"). Such unvested portion of any stock option so converted will continue to have (and be subject to) the same terms and conditions (including vesting schedule) as set forth in the applicable stock option plan of the Company and any individual agreement thereunder at the Effective Time, except that, as of the Effective Time:

- •

- each stock option so converted will be exercisable for that number of whole shares of St. Jude Medical Common Stock equal to the product of the number of Shares that were issuable upon exercise of such stock option at the Effective Time multiplied by the Exchange Ratio (as defined below) (rounding down to the nearest whole number of shares of St. Jude Medical Common Stock); and

- •

- the per share exercise price for the shares of St. Jude Medical Common Stock issuable upon exercise of such Company stock option so converted will be equal to the quotient determined by dividing (1) the exercise price per Share at which such Company stock option was exercisable immediately prior to the Effective Time, by (2) the Exchange Ratio, rounding up to the nearest whole cent.

For purposes of the above calculations the "Exchange Ratio" will mean a fraction, the numerator of which is a per Share price equal to the Offer Price and the denominator of which is the average closing price of a share of St. Jude Medical Common Stock on the New York Stock Exchange over the ten trading days immediately preceding (but not including) the date on which the Effective Time occurs.

The Company has entered into stock option agreements with each of its executive officers and directors and certain other employees that provide that all unvested options will immediately vest in full upon any "Sale of the Corporation." Under the terms of the stock option agreements, a "Sale of the Corporation" will occur if the Company engages in a merger, consolidation, recapitalization, reorganization or sale, lease or transfer of all or substantially all of its assets in which the shareholders immediately before the transaction hold less than 51% of the voting power of the surviving corporation after the transaction. Consummation of the Offer in accordance with its terms will result in a "Sale of the Corporation" under such agreements.

The foregoing summary is qualified in its entirety by reference to the Merger Agreement, which has been filed as Exhibit (e)(1) hereto and is incorporated herein by reference.

Restricted Stock. At the Effective Time, certain of the outstanding Shares that are subject to repurchase by the Company or otherwise subject to a risk of forfeiture or other similar condition under the Company's stock option plans or any restricted stock purchase agreement (a "Restricted Share"), and as to which such restrictions will not have been eliminated at or prior to the Effective Time, will be assumed by St. Jude Medical and converted into shares of St. Jude Medical Common Stock as described below. Restricted Shares so converted will continue to have, and be subject to, the same terms and conditions (including vesting schedule and repurchase rights) as set forth at the Effective Time, except that, as of the Effective Time, Restricted Shares so converted will thereafter be converted into that number of whole shares of St. Jude Medical Common Stock equal to the product of the number of Restricted Shares held by each such holder immediately prior to the Effective Time multiplied by the Exchange Ratio (as described above) (rounding down to the nearest whole number of shares of St. Jude Medical Common Stock). The Company will take such steps as are necessary to communicate with individual holders and legend or retain possession of certificates evidencing all Restricted Shares that are to be assumed and converted in accordance with the foregoing, so as to ensure that such shares may not be tendered for purchase in the Offer or exchanged for payment in the Merger. The Company has entered into restricted stock award agreements with each of its executive officers and directors and certain other employees that provide that the restricted stock award

4

will immediately vest and become nonforfeitable in full upon any "Sale of the Corporation." Under the terms of the stock award agreements, a "Sale of the Corporation" will occur if the Company engages in a merger, consolidation, recapitalization, reorganization or sale, lease or transfer of all or substantially all of its assets in which the shareholders immediately before the transaction hold less than 51% of the voting power of the surviving corporation after the transaction. Consummation of the Offer in accordance with its terms will result in a "Sale of the Corporation" under such agreements. The foregoing summary is qualified in its entirety by reference to the Merger Agreement, which has been filed as Exhibit (e)(1) hereto and is incorporated herein by reference.

As a result, in addition to the amounts the Company's directors and officers will receive as consideration for their Shares in the Offer and the Merger, the following directors and executive officers will receive the payments set forth below based on the options and restricted stock held by such persons:

| Director/Officer | Options | Restricted Stock | ||||

|---|---|---|---|---|---|---|

| Christopher G. Chavez | $ | 13,231,895 | $ | 1,435,394 | ||

| Scott F. Drees | $ | 6,073,105 | $ | 666,094 | ||

| Robert C. Eberhart, Ph.D. | $ | 1,374,575 | $ | 202,125 | ||

| John H. Erickson | $ | 7,217,778 | $ | 505,313 | ||

| Kenneth G. Hawari | $ | 4,964,593 | $ | 737,756 | ||

| Joseph E. Laptewicz | $ | 1,374,575 | $ | 202,125 | ||

| J. Phillip McCormick | $ | 888,338 | $ | 202,125 | ||

| F. Robert Merrill III | $ | 4,435,341 | $ | 542,369 | ||

| Hugh M. Morrison | $ | 1,868,488 | $ | 306,250 | ||

| Richard D. Nikolaev | $ | 1,309,836 | $ | 202,125 | ||

| Michael J. Torma, M.D. | $ | 860,939 | $ | 202,125 | ||

Change in Control Agreements and Severance Payments. The Company has entered into change-in-control agreements that contain severance provisions with 16 of its officers, including Christopher G. Chavez, Kenneth G. Hawari, Scott F. Drees, F. Robert Merrill, III, James P. Calhoun, John H. Erickson and Stuart B. Johnson. These agreements generally provide that if within two years from the date of a "change-in-control" (as defined below) of the Company, the employment of the executive is terminated without cause, or in the event that the executive terminates his or her employment with the Company based on a change in or diminishment of his or her responsibilities, or a reduction in salary, the executive will be entitled to severance pay as provided for in his or her agreement. Messrs. Chavez's and Hawari's agreements only require a change-in-control to trigger their right to severance compensation. The severance pay for Messrs. Chavez and Hawari would be an amount equal to 299% each of their respective annual salary and bonus compensation. The severance pay for the remaining executives would be an amount ranging from one year's salary to one and one-half times each of their respective annual salary and targeted bonus compensation. Additionally, all of the officers are entitled to a lump sum job search payment of $25,000.

For purposes of each of these agreements, a "change-in-control" generally means any of the following events: (1) the consummation of a consolidation, merger or other reorganization in which the Company is merged, consolidated or reorganized into or with another corporation or other legal person or in which shares of the Company's stock are converted into cash, securities or other property, other than a merger of the Company in which the holders of the Company's Common Stock immediately prior to the merger own more than 50% of the common stock of the surviving corporation or its ultimate parent immediately after the merger; (2) the sale of all or substantially all of the Company's assets; (3) if at any time the persons serving on the Board cease for any reason to constitute at least a

5

majority thereof; (4) the approval by the Company's shareholders of our complete liquidation or dissolution; and (5) the acquisition by any person, together with its affiliates and associates, of 50% or more of the Company's outstanding Common Stock. Additionally, the agreements provide that payments from the Company that (a) constitute "parachute payments," as defined in Section 280G of the Internal Revenue Code (the "Code"), and (b) would subject the executive to the 20% excise tax contained in Section 4999 of the Code, will be "grossed-up" by an additional payment in an amount that will cause the aggregate after-tax compensation and benefits received by the executive under the agreement to equal the aggregate after-tax compensation and benefits the executive would have received if Sections 280G and 4999 of the Code had not been enacted.

As a result of the Offer, these executives will, upon their resignation with good reason or termination without cause within two years of a change-in-control (and without regard to resignation or termination in the case of Messrs. Chavez and Hawari), be entitled to receive, upon consummation of the Offer, the payments set forth below pursuant to the terms of their agreements:

| Officer | Change of Control Payment | ||

|---|---|---|---|

| Christopher G. Chavez | $ | 1,931,125 | |

| F. Robert Merrill III | $ | 450,250 | |

| Scott F. Drees | $ | 547,000 | |

| Kenneth G. Hawari | $ | 1,177,645 | |

| James P. Calhoun | $ | 365,200 | |

| John H. Erickson | $ | 394,600 | |

| Stuwart B. Johnson | $ | 367,300 | |

In addition to the payments described above, the Company shall provide to the executive throughout his employment term group insurance benefits, retirement benefits, and other benefits substantially similar to those received by the executive immediately prior to the change of control.

Employees. The Merger Agreement provides the Surviving Corporation will provide retained employees of the Company and its subsidiaries with employee benefits no less favorable in the aggregate than benefits provided to St. Jude Medical's similarly situated employees, or those benefits provided by the Company immediately prior to the closing date of the Merger. The Merger Agreement also provides that each employee's tenure with the Company will be treated as service with St. Jude Medical and the Surviving Corporation for purposes of vesting and entitlement to benefits, including for severance benefits and vacation or other leave entitlement, unless such treatment would result in a duplication of benefits or was not recognized under the corresponding Company plan. To the extent permitted by applicable law and by the applicable St. Jude Medical benefit plan and to the extent that Company employees are covered by the St. Jude Medical's benefit plans, St. Jude Medical will cause any and all pre-existing condition (or actively at work or similar) limitations, eligibility waiting periods and evidence of insurability requirements under St. Jude Medical's benefit plans to be waived with respect to such Company employees and their eligible dependents and will provide them with credit for any co-payments, deductibles, and offsets (or similar payments) made during the plan year including the Effective Time for purposes of satisfying any applicable deductible, out-of-pocket, or similar requirements under any St. Jude Medical benefit plan. The foregoing summary is qualified in its entirety by reference to the Merger Agreement, which has been filed as Exhibit (e)(1) hereto and is incorporated herein by reference.

Indemnification; Directors' and Officers' Insurance. The Merger Agreement provides that the Surviving Corporation will indemnify and hold harmless (including advancement of expenses) the current and former directors and officers of the Company in respect of acts or omissions occurring on or prior to the Effective Time to the maximum extent permitted by applicable law or provided in the

6

articles of incorporation, bylaws and indemnity agreements of the Company in effect on the date of the Merger Agreement. The Merger Agreement further provides that St. Jude Medical and the Surviving Corporation will cause to be maintained for a period of not less than six years from and after the Effective Time the Company's current directors' and officers' insurance and indemnification policy to the extent that it provides coverage for events occurring prior to the Effective Time (the "D&O Insurance") for all persons who are directors and officers of the Company on the date of the Merger Agreement, so long as the annual premium therefor would not be in excess of two times the amount per annum the Company paid in its last full fiscal year, on terms and conditions substantially similar to the existing D&O Insurance. If the existing D&O Insurance cannot be maintained, expires or is terminated or canceled during such six-year period, St. Jude Medical and the Surviving Corporation will use reasonable efforts to cause to be obtained as much D&O Insurance as can be obtained for the remainder of such period for an annualized premium not in excess of two times the amount per annum the Company paid in its last full fiscal year, on terms and conditions substantially similar to the existing D&O Insurance. Pursuant to the Merger Agreement, in the event the Surviving Corporation is unable to satisfy its indemnification obligations in respect of the directors and officers of the Company, St. Jude Medical will be deemed to have assumed and will therefore be obligated to pay such indemnification obligations to the same extent as the Surviving Corporation, up to a maximum amount of $350,000,000.

Section 16 Matters. Prior to the Effective Time, the Company will take all such steps as may be required to cause any dispositions of Common Stock or options resulting from the Merger by each officer and director who is subject to the reporting requirements under Section 16(a) of the Exchange Act, to be exempt from liability under Rule 16b-3 promulgated under the Exchange Act.

Representation on the Board. The Merger Agreement sets forth certain agreements between the Company, St. Jude Medical and the Purchaser regarding the election or appointment of directors to the Company's Board concurrently with the purchase and payment for Shares pursuant to the Offer as a result of which St. Jude Medical or the Purchaser and their affiliates own beneficially at least a majority of the then outstanding Shares. The summary of these agreements is contained in Section 11 of the Offer to Purchase, which is being mailed to shareholders together with this Statement and filed as an exhibit to the Schedule TO, and is incorporated into this Statement by reference. Such summary is qualified in its entirety by reference to the Merger Agreement, which has been filed with the Commission by the Company and has been filed as Exhibit (e)(1) to this Statement and is incorporated in this Statement by reference.

Item 4. The Solicitation or Recommendation.

Recommendation of the Board

The Board, at a meeting held on October 14, 2005, by a unanimous vote, among other things, (1) approved in all respects the Merger Agreement and the transactions contemplated therein, including the Offer and the Merger, (2) determined that the Merger Agreement and the transactions contemplated therein, including the Offer and the Merger, are advisable and fair to and in the best interests of the Company and its shareholders, (3) approved the Offer and the Merger, upon the terms and subject to the conditions set forth in the Merger Agreement, (4) recommended that the holders of Shares accept the Offer and tender their Shares in the Offer and vote their shares of Common Stock in favor of the approval of the Merger and the Merger Agreement at any meeting of shareholders of the Company called to consider the approval of the Merger and the Merger Agreement, and (5) approved the Merger Agreement and the transactions contemplated thereby, including the Offer and the Merger, for purposes of exempting such transactions from the restrictions of Article 13.03 of the TBCA, which apply to certain business combination transactions.

7

Background of the Transaction

The Board and management have been committed to growing the Company's business organically and through the acquisition of technologies, assets or companies that could enhance the Company's competitive position in the field of neuromodulation. Accordingly, the Company's management has periodically explored and assessed, and has discussed with the Board, strategies to grow the Company's business through targeted and selective acquisitions of technologies, assets or other companies in the medical device industry that could help it achieve its strategic goals. The Board and management have also been willing to consider the possibility of business combinations involving the Company and larger health care companies, if such a combination were perceived to be in the best interest of the Company's shareholders. The increasing level of technological innovation and product development in neuromodulation devices, increasing competition, the need for greater mass and investment flexibility in developing the Company's organic opportunities for product and indication incubation and development, the continuing challenges in achieving and maintaining adequate reimbursement for the Company's products, the increasing cost and complexity of conducting Food and Drug Administration ("FDA") approved clinical trials and obtaining FDA market clearance for its products, and other developments in the medical device industry generally have been factors that the Board and management have considered in the course of conducting their analysis of the Company's strategic options.

From time to time, in the period preceding the commencement of negotiations with St. Jude Medical, other medical device companies and investment bankers contacted the Company and communicated informally with Company representatives with respect to their views regarding the neuromodulation industry, the broader medical device industry and potential strategic options and alternatives. Except as described below, none of the discussions proceeded beyond the exploratory stage and no understanding with respect to the terms of any transaction was reached.

In May 2005, Piper Jaffray & Co. ("Piper Jaffray"), the Company's financial advisor, contacted a substantial company in the medical products industry and advised it of increased strategic interest in the Company by certain other parties. This company responded that it did not have an interest in pursuing an acquisition of the Company at that time. Piper Jaffray advised the Company's management of this response.

In late May 2005, St. Jude Medical authorized Banc of America Securities LLC ("Banc of America Securities"), its financial advisor, to contact Piper Jaffray concerning a potential acquisition of the Company by St. Jude Medical. Banc of America Securities then contacted Piper Jaffray to express St. Jude Medical's interest in discussing such an acquisition.

In early June 2005, Piper Jaffray contacted the Company and informed Mr. Christopher Chavez, the Company's President and Chief Executive Officer, that St. Jude Medical was interested in meeting with Mr. Chavez regarding St. Jude Medical's interest in the Company and a potential business combination. Piper Jaffray and Banc of America Securities arranged a meeting among Mr. Daniel Starks, St. Jude Medical's Chairman, President and Chief Executive Officer, and Mr. John Heinmiller, St. Jude Medical's Executive Vice President and Chief Financial Officer, and Mr. Chavez.

On June 7 and 8, 2005, Mr. Chavez and Mr. Kenneth G. Hawari, the Company's Executive Vice President of Corporate Development and General Counsel, met with Mr. Starks and Mr. Heinmiller to discuss their respective companies' businesses, operations, strategic directions and related matters.

On June 20, 2005, Piper Jaffray spoke with Mr. Heinmiller, who indicated that St. Jude Medical was interested in continuing discussions. Piper Jaffray indicated that a confidentiality agreement would need to be put in place and stated that it would inform the Company of St. Jude Medical's interest.

8

On June 21, 2005, Mr. Starks contacted Mr. Chavez and expressed interest in continuing their discussions. Mr. Starks stated that he and Mr. Heinmiller believed that a business combination involving the Company could result in a number of important mutual benefits, including opportunities to leverage the companies' respective technologies, research and development, operations, sales and marketing organizations, and clinical and regulatory organizations. Mr. Starks indicated that St. Jude Medical's board of directors would be meeting in a regularly scheduled meeting on August 4-5, 2005, that one topic for consideration at that meeting would be St. Jude Medical's strategic opportunities for growth, and that he would like to present a possible acquisition of the Company as such an opportunity.

On July 18, 2005, Mr. Starks called Mr. Chavez and discussed St. Jude Medical's continuing interest in pursuing a business combination. Mr. Starks and Mr. Chavez continued to discuss potential advantages of a possible business combination. Mr. Chavez indicated that he was willing to continue the discussions, but that Mr. Starks would need to provide some indication of what St. Jude Medical would be willing to pay per share to acquire the Company before the Company would expend significant time or effort in further discussions. They agreed that a face-to-face meeting to discuss the Company's business and business prospects, potential transaction synergies and leverage opportunities, and valuation issues was necessary and would be scheduled after St. Jude Medical's scheduled August 4-5, 2005 board meeting, assuming St. Jude Medical's board decided to pursue those discussions.

On July 28, 2005, the Company entered into a confidentiality and standstill agreement with St. Jude Medical.

On August 8, 2005, Mr. Chavez, Mr. Hawari and Mr. Robert Merrill III, the Company's Chief Financial Officer, met with Mr. Starks and other officers of St. Jude Medical: Mr. Heinmiller, Mr. Michael Coyle (President of St. Jude Medical's Cardiac Rhythm Management Division), Mr. Joseph McCullough (President of St. Jude Medical's International Division), Mr. Michael Rousseau (President of St. Jude Medical's U.S. Division) and Mr. Kevin O'Malley (Vice President and General Counsel). Mr. Chavez provided a review of the Company's products and markets, operations, financial performance, clinical studies, growth opportunities and strategic outlook. Mr. Merrill presented the St. Jude Medical executives with a review of the potential new indications that the Company was pursuing through clinical trials and evaluation. Mr. Starks informed Mr. Chavez that he expected to call Mr. Chavez within a reasonably short period of time to indicate St. Jude Medical's interest in pursuing a business combination.

Representatives of Banc of America Securities met with Messrs. Starks, Heinmiller and O'Malley to discuss their preliminary valuation analysis of the Company. Following this meeting, St. Jude Medical authorized Banc of America Securities to contact Piper Jaffray to inform them of St. Jude Medical intent in pursuing a business combination.

On August 17, 2005, Piper Jaffray contacted Mr. Hawari and informed him that Mr. Starks planned to express an indication of interest in St. Jude Medical's acquiring the Company at a specified price per share, and invited Mr. Chavez to call Mr. Starks.

On August 18, 2005, Mr. Chavez called Mr. Starks, who indicated that St. Jude Medical was interested in pursuing discussions regarding a potential all-cash acquisition at a specified price range per share of $58.00 to $60.00. Mr. Chavez stated that he would discuss the indication of interest with the Company's Board, which was already scheduled to meet on August 31 through September 2, 2005.

9

From August 31 through September 2, 2005, the Company's Board held its regularly scheduled board meeting. Over the course of these three days, the Board was provided information regarding St. Jude Medical and its indication of interest, Piper Jaffray provided financial advice to the Board regarding the indication of interest, comparable transactions and valuations, the Board discussed the indication of interest with Baker Botts L.L.P., outside counsel to the Company, and discussed the legal and fiduciary standards applicable to the Board's discussion and consideration of the indication of interest. In addition, management presented the Board with a comprehensive situational analysis of the Company's financial results, its financial prospects, opportunities for organic growth through its incubation opportunities, competitive analysis, constraints on long-term investments by the Company, challenges in reimbursement, the cost and challenges of conducting clinical trials and obtaining FDA approvals, and other risks and opportunities presented by the neuromodulation and medical device industry generally. After numerous discussions over the course of three days, and informally afterward, the Board directed Mr. Chavez to contact St. Jude Medical and elicit St. Jude Medical's "highest and best" proposal on price per share.

On September 6, 2005, Mr. Chavez contacted Mr. Starks and indicated that the Company's Board had discussed St. Jude Medical's indication of interest over the course of its board meeting and in the days following. Mr. Chavez stated that the Board appreciated the potential merits of a business combination, but had authorized him to ask St. Jude Medical to increase its proposed price per share. Mr. Starks indicated that he would discuss the issue with his management team and respond within a week or two.

On September 15, 2005, Mr. Starks called Mr. Chavez and stated that St. Jude Medical would be willing to increase its proposed price per share to a range of $60.00 to $61.25, subject to completing its due diligence. Mr. Chavez stated that he would convene a special board meeting to consider the proposal.

On September 20, 2005, the Company Board met via telephone conference call to evaluate and consider St. Jude Medical's revised proposal. Piper Jaffray provided financial advice to the Board regarding the revised proposal and provided its views on whether other parties would have an interest in making a proposal at or above the indicated price per share. Mr. Hawari advised the Board regarding legal and fiduciary standards applicable to the Board's consideration of the revised indication of interest. The Board determined to proceed with discussions with St. Jude Medical to reach a definitive agreement and to permit St. Jude Medical to conduct due diligence on the Company. The Board also authorized management and Piper Jaffray to contact another potential acquiror, which we refer to as "Company X," that had indicated its interest in a possible acquisition of the Company on several occasions during the preceding years and had visited the Company's headquarters in Plano, Texas in January 2005 to receive a management presentation regarding the Company, its operations, products and prospects, and to evaluate the Company as a potential acquisition candidate. The Board also authorized the Company to engage advisors to assist in discussions with St. Jude Medical and Company X, and any other parties that Piper Jaffray concluded possessed the financial capability and strategic interest in combining with the Company.

Following the September 20, 2005 Board meeting, Piper Jaffray contacted a Vice President of Business Development of Company X, and indicated that a third party had presented the Company with a serious indication of interest in a business combination, and inquired whether Company X had an interest in considering making its own proposal. Piper Jaffray invited Company X to make such a proposal and outlined the timeframe within which such proposal would need to be received in order to be considered along with the first proposal. The officer stated that Company X might have such an interest and indicated that he would discuss the matter with his superiors.

10

On September 21, 2005, Mr. Chavez called a senior executive of Company X, and reiterated the information that Piper Jaffray had delivered to the Vice President of Business Development. The senior executive called by Mr. Chavez had been one of the Company X representatives who had visited the Company in January 2005. The senior executive stated that he believed Company X would have an interest in evaluating a potential acquisition of the Company and inquired about the process that would be involved. Mr. Chavez suggested that Company X consider performing its due diligence and determine whether it was interested in making a proposal. The senior executive said that either he or another Company X representative would contact Mr. Chavez within a week.

Later that day, Mr. Chavez contacted Mr. Starks and informed him that the Company Board had authorized management to pursue discussions with St. Jude Medical with a view to entering into a definitive merger agreement. The parties tentatively agreed to structure the transaction as a cash tender offer by a wholly owned subsidiary of St. Jude Medical for all of the Company's issued and outstanding shares followed by a cash-for-stock merger of that subsidiary into the Company. Mr. Chavez also informed Mr. Starks that he had contacted Company X to inform them of a third party's serious indication of interest in pursuing a business combination.

On September 23, 2005, a group of St. Jude Medical's business executives, investment bankers and attorneys met with a group of the Company's business executives, investment bankers and attorneys in Dallas, Texas at the offices of Baker Botts to discuss non-price terms of the proposed transaction, discuss a plan for St. Jude Medical's conduct of due diligence, and generally organize the process for negotiating and completing a definitive merger agreement.

On September 26, 2005, St. Jude Medical's attorneys, accountants and investment bankers commenced their formal due diligence review of the Company.

On September 27, 2005, a larger group of St. Jude Medical's business executives met with a larger group of the Company's business executives in Dallas, Texas at the offices of Baker Botts to conduct a management review of the Company, its operations, products, financial prospects and organic growth opportunities. That day and over the next several days, members of St. Jude Medical's management group conducted individual due diligence meetings with members of Company management. St. Jude Medical's attorneys, accountants and investment bankers also participated in the due diligence process.

Later on September 27, 2005, a group of Company X's key business executives met with a group of the Company's key business executives in Plano, Texas to conduct its own management review of the Company, its operations, products, financial prospects and organic growth opportunities. Company X indicated that it would be evaluating the prospect of an acquisition of the Company and asked for an opportunity to conduct business, financial and legal due diligence, which the Company stated it would be willing to facilitate.

Late on September 27, 2005, St. Jude Medical's attorneys delivered a first draft of a merger agreement to the Company and its attorneys.

During the next two weeks, both St. Jude Medical and Company X separately conducted their due diligence investigations via in-person visits to Dallas and Plano and through telephonic conference calls. During this time, senior executives of the Company held further, separate discussions with each of St. Jude Medical and Company X regarding their due diligence investigations.

On October 3, 2005, St. Jude Medical executives and attorneys met with Company executives and attorneys to negotiate the terms of a merger agreement.

On October 6, 2005, Mr. Heinmiller and Mr. O'Malley contacted Mr. Hawari to discuss open issues and a proposed timetable for St. Jude Medical's entering into a merger agreement with the Company. Later that day, Mr. Starks contacted Mr. Chavez and discussed the details of St. Jude

11

Medical's proposed timetable and plans for communicating with investors, employees, customers and other constituencies if a merger agreement were negotiated and signed by the two parties.

On October 7, 2005, the Company provided St. Jude Medical with draft disclosure schedules to the draft merger agreement then under negotiation. On the same day, the Company provided Company X with a draft merger agreement for Company X's consideration, and two days later the Company provided Company X with draft disclosure schedules. Throughout this time, Piper Jaffray kept Company X apprised of the timeframe within which a proposal would need to be received from Company X in order to be considered along with the proposal from the first party.

On October 10, 2005, executives of Company X met in Plano, Texas with members of the Company's management team to discuss the potential benefits of Company X's acquisition of the Company. Following this meeting, Piper Jaffray again invited Company X to submit an offer for the Company.

Piper Jaffray held discussions on October 12 and on the morning of October 13 with Company X during which representatives of Company X reiterated their continued interest in exploring an acquisition of the Company and indicated a range of potential offer prices for the Company's Common Stock, but noted that Company X's board of directors had not reviewed the proposed transaction or authorized representatives of Company X to make a formal proposal to acquire the Company. Company X also indicated its desire to conduct more due diligence before submitting a proposed transaction to its board of directors.

Later on October 13, 2005, the Company Board held a special meeting in Plano, Texas to review and discuss the terms of the proposed St. Jude Medical merger agreement, the status of negotiations with St. Jude Medical, the status of discussions with Company X and the results of their respective due diligence investigations. Mr. Chavez reviewed prior discussions with both St. Jude Medical and Company X, and Mr. Hawari described the chronology of events that had occurred with St. Jude Medical and Company X since the September 20, 2005 Board meeting. After full discussion of the status of discussions with Company X, the Board determined that Company X's range of potential offer prices for the Common Stock was not competitive with St. Jude Medical's firm proposal, and determined that Company X was highly unlikely to increase its range to a level that would be superior to St. Jude Medical's proposal, even after conducting additional due diligence. In addition, the Board determined that the continued uncertainty of whether Company X would submit a formal proposal did not warrant delaying further action on St. Jude Medical's firm proposal. The Board then turned its attention to the proposed transaction with St. Jude Medical. Piper Jaffray provided strategic and financial advice to the Board regarding the negotiations and the terms of the transaction and orally confirmed that it would be prepared to deliver its opinion that, subject to the assumptions made, procedures followed, matters considered and limitations on the scope of the review undertaken by Piper Jaffray, as of the date of the Board's meeting to consider the merger agreement with St. Jude Medical and the transactions contemplated thereby, the consideration set forth in the merger agreement was fair to the Company's shareholders from a financial point of view. Baker Botts discussed the tender offer structure and reviewed the material terms of the definitive merger agreement governing the transaction (including material terms that then remained subject to further negotiation) and the legal and fiduciary standards applicable to the Board's consideration of the merger agreement and the transactions contemplated by the merger agreement. After additional discussion, the Board authorized management to complete negotiations with St. Jude Medical and finalize the terms of the Merger Agreement with St. Jude Medical, adopted a bylaw amendment relating to indemnification of directors and officers, and agreed to meet again by telephone on the following day, October 14, 2005.

On October 13 and 14, 2005, the Company and St. Jude Medical continued to negotiate the terms of the draft Merger Agreement and St. Jude Medical continued its due diligence.

12

On October 14, 2005, St. Jude Medical's board of directors held a special meeting to review and discuss the terms of the proposed Merger Agreement. Members of St. Jude Medical's senior management reviewed the negotiations that had taken place with the Company, and also updated St. Jude Medical's board of directors on the due diligence review that had occurred. Representatives of Banc of America Securities were present at the meeting and prior to the meeting had provided St. Jude Medical's board of directors with a financial presentation concerning the proposed acquisition. At the conclusion of this meeting, St. Jude Medical's board of directors authorized its officers to proceed at a price of $61.25 per share.

After the close of business on October 14, 2005, Mr. O'Malley and Mr. Heinmiller contacted Mr. Hawari regarding the St. Jude Medical Board of Directors' decision. Mr. O'Malley, Mr. Heinmiller and Mr. Hawari discussed and negotiated the remaining open issues and reached agreement on such issues. Following those discussions, the Company Board held a special telephonic meeting. During this meeting, Messrs. Chavez and Hawari reviewed the negotiations that had taken place with St. Jude Medical since the previous Board meeting and recommended that the Board authorize and approve the Merger Agreement with St. Jude Medical. Piper Jaffray orally provided its financial analysis and delivered to the Board its opinion that, as of such date, and subject to the assumptions made, procedures followed, matters considered and limitations on the scope of the review undertaken by Piper Jaffray, the Offer Price proposed to be paid in the Offer and the Per Share Price proposed to be paid in the Merger, in each case as set forth in the Merger Agreement, was fair to the Company's shareholders from a financial point of view. Mr. Hawari and Baker Botts updated the Board on the resolution of the material terms of the Merger Agreement that had been unresolved as of the time of the previous Board meeting. Following further discussion, the Board voted unanimously to approve the Merger Agreement and related matters, and to recommend the Offer and the Merger to the Company's shareholders. The Board also authorized officers of the Company to finalize and execute the definitive Merger Agreement and related documents and adopted a bylaw amendment relating to filling Board vacancies.

The Company and St. Jude Medical finalized the terms of the Merger Agreement including, among other things, the per share price and the termination fee, following the Company Board meeting and into the following day, October 15, 2005. Late in the day on this date, the Company Board convened again by conference call to approve certain changes to the Company bylaw amendment adopted on October 13 relating to indemnification of directors and officers. Following this meeting, the Company, St. Jude Medical and St. Jude Medical's acquisition subsidiary executed the Merger Agreement.

On Sunday, October 16, 2005, the Company and St. Jude Medical issued a joint press release announcing the execution of the Merger Agreement.

On October 17, 2005, St. Jude Medical and the Company held a joint conference call to discuss the proposed business combination.

On October 18, 2005, St. Jude Medical's acquisition subsidiary commenced the Offer.

The portions of the background of the transaction set forth above that relate solely to St. Jude Medical's board meetings and discussions with Banc of America Securities are based on statements made by St. Jude Medical in the Offer to Purchase and have not been independently verified by the Company.

13

Reasons for the Recommendation of the Board of Directors

In approving the Offer, the Merger, the Merger Agreement and the transactions contemplated thereby and recommending that all holders of Shares accept the Offer and tender their Shares pursuant to the Offer, the Board considered a number of factors, including:

- •

- Company Operations and Financial Condition. The Board considered the current and historical financial condition and results of operations of the Company, as well as its prospects and objectives, including the risks involved in achieving those prospects and objectives, and the current and expected conditions in the medical device industry.

- •

- Piper Jaffray Fairness Opinion. The Board has received a presentation by Piper Jaffray and the written opinion of Piper Jaffray to the effect that, as of the date of the opinion and based upon and subject to the various considerations set forth in the opinion, the Offer Price to be received by the holders of Shares in the Offer and the Per Share Price to be received by holders of Shares in the Merger is fair from a financial point of view to such holders.The full text of the Piper Jaffray written opinion dated October 14, 2005, which sets forth, among other things, the assumptions made, procedures followed, matters considered and limitations on the scope of the review undertaken by Piper Jaffray in rendering its opinion, is attached as Annex A and is incorporated in its entirety herein by reference. Company shareholders are urged to, and should, carefully read the Piper Jaffray opinion in its entirety. The Piper Jaffray opinion addresses only the fairness, from a financial point of view and as of the date of the opinion, to holders of Common Stock of the Offer Price proposed to be paid in the Offer and the Per Share Price proposed to be paid in the Merger. The Piper Jaffray opinion was directed solely to the Board and was not intended to be, and does not constitute, a recommendation to any Company shareholder as to how any shareholder should vote or act on any matter relating to the proposed Offer or Merger.

- •

- Offer Price. The Board considered that the Offer Price represents a premium of approximately 30% over the closing price of the Shares on The Nasdaq National Market on October 14, 2005, and a premium of approximately 25% over the average of the closing prices of the Shares on The Nasdaq National Market for the last 30 days of trading prior to October 16, 2005, the date of the announcement of the parties' execution of the Merger Agreement.

- •

- The Merger Agreement. The Board considered the financial and other terms of the Offer, the Merger and the Merger Agreement, including the benefits of the transaction being structured as a first-step tender offer and second-step merger, which may provide the Company's shareholders with an opportunity to receive cash on an accelerated basis, and the nature of the arm's length negotiation of the Merger Agreement.

- •

- Presentations and Management View. The Board considered the presentations by, and discussion of the terms of the Merger Agreement with, the Company's senior management, Baker Botts L.L.P. and Piper Jaffray. The Board also considered the belief of the Company's senior management that, based on its review of the Company's strategic alternatives and recent discussions with a substantial third party in the medical products industry to ascertain its level of interest in engaging in a business combination transaction with the Company, and based on Piper Jaffray's experience in the industry and contact with at least one other potential acquiror who had indicated that it did not have an interest in pursuing an acquisition of the Company at the time, it was highly unlikely that any party would propose an alternative transaction that would be more favorable to the Company and its stockholders than the Offer and the Merger.

- •

- Strategic Alternatives. The Board considered potential strategic alternatives available to the Company and the viability and risks associated with each alternative, including the prospects for

14

- •

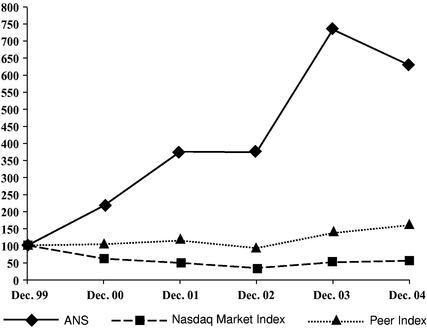

- Trading Price of the Company Common Stock. The Board considered the recent and historical stock price performance of the shares of Company Common Stock.

- •

- Minimum Tender Condition. The Board considered the fact that the Offer is conditioned on there being tendered and not validly withdrawn a majority of the outstanding shares of Company Common Stock on a "fully-diluted basis" (as defined in the Merger Agreement) and the fact that St. Jude Medical is not permitted to waive this condition without the consent of the Board.

- •

- Other Conditions to Consummation. The Board considered the likelihood that the Offer and the Merger would be consummated, including the customary nature of the conditions to the Offer and the Merger, the absence of any financing condition, the experience, reputation and financial condition of St. Jude Medical, the consents and approvals required to consummate the Offer and the Merger, including regulatory clearance under the HSR Act (as defined below) and foreign antitrust laws, and the favorable prospects for receiving such consents and approvals.

- •

- Fiduciary Out. The Board considered the fact that while the Merger Agreement prohibits the Company from soliciting proposals concerning an acquisition of the Company, the Board, in the exercise of its fiduciary duties, would be able, subject to compliance with certain requirements, to provide information to, and engage in negotiations with, a third party that makes an unsolicited superior proposal (as defined in the Merger Agreement), and that the Board would be able to terminate the Merger Agreement and accept a superior acquisition proposal upon payment to St. Jude Medical of a termination fee of $35,000,000 and subject to compliance with certain other requirements.

- •

- Availability of Dissenters' Rights. The Board considered the fact that shareholders of the Company who believe that the terms of the Offer and the Merger are unfair have the right to dissent from the Merger and demand payment of the fair value for their shares, in lieu of the consideration to be received in the Merger, in accordance with Texas law, if such shareholders do not tender their shares in the Offer, do not vote in favor of the Merger and otherwise comply with Texas law.

the Company on a stand-alone basis and the risks associated with achieving and executing upon the Company's business plan, both short-term and long-term. In particular, the Board considered the increased competition in the medical device industry and the recent entry of a competitor with significantly greater resources than the Company, and the fact that greater size, critical mass and resources are increasingly required for companies to successfully compete in this industry.

The foregoing discussion of the information and factors considered by the Board is not intended to be exhaustive, but summarizes the material factors considered. The members of the Board evaluated the Offer, the Merger and the Merger Agreement in light of their knowledge of the business, financial condition and prospects of the Company, and based upon the advice of financial and legal advisors. In view of the number and wide variety of factors, both positive and negative, considered by the Board, the Board did not find it practical to, and did not, quantify or otherwise assign relative or specific weights to the factors considered or determine that any factor was of particular importance. Rather, the Board viewed its position and recommendations as being based on the totality of the information presented to and considered by the Board. In addition, individual members of the Board may have given differing weights to different factors and may have viewed certain factors more positively or negatively than others.

15

Intent to Tender

To the best of the Company's knowledge, after reasonable inquiry, each executive officer, director, affiliate and subsidiary of the Company currently intends, subject to compliance with applicable law, including Section 16(b) of the Exchange Act, to tender all Shares held of record or beneficially owned by such person or entity to the Purchaser in the Offer, other than such Shares, if any, that any such person or entity may have an unexercised right to purchase by exercising stock options. Following the Merger, St. Jude Medical or the Surviving Corporation will pay each holder of Company stock options that were vested at the effective time of the Merger cash in an amount equal to the product of (1) the amount, if any, by which $61.25 (or the highest price paid for any Share in the Offer) exceeds the per Share exercise price of such option holder's vested options and (2) the number of Shares underlying such option holder's vested options. Company stock options that are unvested at the effective time of the Merger will be converted into St. Jude Medical stock options in the manner specified in the Merger Agreement.

Item 5. Persons/Assets Retained, Employed, Compensated or Used.

The Company engaged Piper Jaffray to act as investment banker for the Company. Pursuant to the engagement letter between the Company and Piper Jaffray, dated as of September 16, 2005, Piper Jaffray is entitled to the following fees:

- •

- an opinion fee in the amount of $500,000, which was payable at the time Piper Jaffray delivered its fairness opinion;

- •

- a cash fee, payable upon closing of the transactions contemplated by the Merger Agreement, equal to 0.9% of the aggregate transaction value (as defined in the engagement letter) up to $1.12 billion; provided that to the extent the aggregate transaction value exceeds $1.12 billion (such excess, the "Differential"), such cash fee will be increased by an amount equal to 2.5% multiplied by the Differential; and provided further that any opinion fee paid to Piper will be deducted from any cash fee payable upon the closing; and

- •

- a cash fee equal to 15% of any termination fee that the Company receives if the transactions contemplated by the Merger Agreement are not completed and the Company receives a break-up fee, topping fee or other termination or nonconsummation fee.

The Company has also agreed to indemnify Piper Jaffray and its directors, officers, agents, employees and controlling persons for certain costs, expenses and liabilities, including certain liabilities under the federal securities laws. In the ordinary course of business, Piper Jaffray may actively trade Shares and other securities of the Company, as well as securities of St. Jude Medical, for its own account and for the accounts of its customers and, accordingly, may at any time hold a long or short position in such securities.

The Company may engage a proxy solicitation or similar firm to assist in the solicitation of tenders of Shares and will pay any such firm fees at market rates.

Except as set forth above, neither the Company nor any person acting on its behalf has or currently intends to employ, retain or compensate any person to make solicitations or recommendations to the shareholders of the Company on its behalf with respect to the Offer, except that such solicitations or recommendations may be made by directors, officers or employees of the Company, for which services no additional compensation will be paid.

16

Item 6. Interest in Securities of the Subject Company.

On August 1, 2005, pursuant to a previously adopted 10b5-1 plan, John Erickson, Vice President of Research and Development, sold 1,000 Shares at a price of $49.30 per share, 200 Shares at a price of $49.28 per share, 147 Shares at a price of $49.31 per share, 100 Shares at a price of $49.28 per share, 34 Shares at a price of $49.30 per share and 19 Shares at a price of $49.32 per share.

No transactions in Shares have been effected during the past 60 days by the Company or any subsidiary of the Company or, to the knowledge of the Company, by any executive officer, director or affiliate of the Company, other than the execution and delivery of the Merger Agreement and the transactions described in the preceding paragraph.

Item 7. Purposes of the Transaction and Plans or Proposals.

Except as set forth in this Statement, the Company is not currently undertaking or engaged in any negotiations in response to the Offer that relate to (1) a tender offer for or other acquisition of the Company's securities by the Company, any subsidiary of the Company or any other person; (2) an extraordinary transaction, such as a merger, reorganization or liquidation, involving the Company or any subsidiary of the Company; (3) a purchase, sale or transfer of a material amount of assets of the Company or any subsidiary of the Company; or (4) any material change in the present dividend rate or policy, or indebtedness or capitalization of the Company.

Except as set forth in this Statement, there are no transactions, resolutions of the Board, agreements in principle, or signed contracts in response to the Offer that relate to one or more of the events referred to in the preceding paragraph.

Item 8. Additional Information.

Texas Business Corporation Act

We are subject to Part Thirteen (the "Business Combination Law") of the TBCA. In general, the Business Combination Law prevents an "affiliated shareholder" or its affiliates or associates from entering into or engaging in a "business combination" with an "issuing public corporation" during the three-year period immediately following the affiliated shareholder's acquisition of shares unless: (1) before the date the person became an affiliated shareholder, the board of directors of the issuing public corporation approved the business combination or the acquisition of shares made by the affiliated shareholder on that date; or (2) not less than six months after the date the person became an affiliated shareholder, the business combination is approved by the affirmative vote of holders of at least two-thirds of the issuing public corporation's outstanding voting shares not beneficially owned by the affiliated shareholder or its affiliates or associates.

For the purposes of the Business Combination Law, an "affiliated shareholder" is defined generally as a person who is or was within the preceding three-year period the beneficial owner of 20% or more of a corporation's outstanding voting shares. A "business combination" is defined generally to include: (1) mergers or share exchanges; (2) dispositions of assets having an aggregate value equal to 10% or more of the market value of the assets or of the outstanding common stock representing 10% or more of the earning power or net income of the corporation; (3) certain issuances or transaction by the corporation that would increase the affiliated shareholder's number of shares of the corporation; (4) certain liquidations or dissolutions; and (5) the receipt of tax, guarantee, loan or other financial benefits by an affiliated shareholder of the corporation.

An "issuing public corporation" is defined generally as a Texas corporation with 100 or more shareholders, any voting shares registered under the Exchange Act, or any voting shares qualified for trading in a national market system.

17

In accordance with the provisions of Article 13.03 of the TBCA, the Board has approved the Merger Agreement and the transactions contemplated thereby, as described in Item 4 above and, therefore, the restrictions of Part Thirteen of the TBCA are inapplicable to the Merger and the transactions contemplated by the Merger Agreement.

Dissenters' Appraisal Rights. No appraisal rights are available in connection with the Offer. Upon completion of the Offer, however, St. Jude Medical will cause the Purchaser and the Company to effect the Merger, unless it is not lawful to do so, and each holder of Shares who has not tendered such holder's Shares in the Offer and who validly exercises such holder's appraisal rights in connection with the Merger by properly complying with the requirements of Articles 5.12, 5.13 and 5.16, as applicable, of the TBCA will have the right to have the "fair value" of such holder's Shares determined by a court and paid to them in cash. Under Texas law, if shareholders are given an opportunity to vote on the merger at a shareholders' meeting, the fair value of shares for purposes of the exercise of dissenters' appraisal rights in connection with the Merger is defined as the value of the Shares as of the day immediately preceding the shareholders' meeting, excluding any appreciation or depreciation in anticipation of the Merger. Alternatively, if shareholders are not given an opportunity to vote on the Merger because the Purchaser owns at least 90% of the Shares following the tender offer, the fair value of Shares for purposes of the exercise of dissenters' appraisal rights in connection with the Merger is defined as the value of the Shares as of the day before the effective date of the Merger, excluding any appreciation or depreciation in anticipation of the Merger. This value may be determined to be more or less than or the same as the $61.25 per share cash consideration to be received either in the Offer or pursuant to the terms of the Merger.

Failure to follow the steps required by Articles 5.12, 5.13 and 5.16 of the TBCA for validly exercising dissenters' appraisal rights may result in the loss of dissenters' appraisal rights, in which event a record holder will be entitled to receive the consideration with respect to such holder's shares in accordance with the Merger. In view of the complexity of Articles 5.11, 5.12, 5.13 and 5.16 of the TBCA, if you are considering dissenting from the Merger and pursuing appraisal rights, you are urged to consult your own legal counsel.

Appraisal rights cannot be exercised at this time. The information set forth above is for informational purposes only with respect to alternatives available to shareholders if the Merger is consummated. Shareholders who will be entitled to appraisal rights in connection with the Merger will receive additional information concerning appraisal rights and the procedures to be followed in connection therewith before such shareholders have to take any action relating thereto.

Shareholders who sell shares in the Offer will not be entitled to exercise appraisal rights with respect to their Shares but, rather, will receive the Offer Price.

The foregoing summary of the rights of objecting shareholders under the TBCA does not purport to be a complete statement of the procedures to be followed by shareholders of the Company desiring to exercise any available dissenters' appraisal rights. The foregoing discussion is qualified in its entirety by Articles 5.11, 5.12, 5.13 and 5.16 of the TBCA, which are attached as Exhibit (a)(6)(ii) hereto.

Short-form Merger. Under the TBCA, if the Purchaser acquires, pursuant to the Offer or otherwise, at least 90% of the outstanding shares of the Common Stock, the Purchaser will be able to effect the Merger after consummation of the Offer without a vote of the Company's shareholders. If the Purchaser does not acquire at least 90% of the outstanding shares of Common Stock pursuant to the Offer or otherwise and a vote of the Company's shareholders is required under the TBCA, a significantly longer period of time will be required to effect the Merger.

18

Regulatory Approvals

United States. Under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended (the "HSR Act"), and the rules that have been promulgated thereunder by the Federal Trade Commission (the "FTC"), certain acquisition transactions may not be consummated unless certain information has been furnished to the Antitrust Division of the Department of Justice and the FTC and certain waiting period requirements have been satisfied. The purchase of Shares pursuant to the Offer is subject to such requirements.

Pursuant to the requirements of the HSR Act, the Purchaser has informed the Company that it expects to file a Notification and Report Form with respect to the Offer and Merger with the Antitrust Division and the FTC on or about October 19, 2005. The waiting period applicable to the purchase of Shares pursuant to the Offer is scheduled to expire at 11:59 p.m., New York City time, 15 days after such filing. Prior to such time, the Antitrust Division or the FTC may extend the waiting period by requesting additional information or documentary material relevant to the Offer from the Purchaser. If such a request is made, the waiting period will be extended until 11:59 p.m., New York City time, on the tenth day after substantial compliance by the Purchaser with such request. Thereafter, consummation of the Merger may be legally delayed only by court order. In practice, complying with a request for additional information or material can take a significant amount of time. In addition, if the Antitrust Division or the FTC raises substantive issues in connection with a proposed transaction, the parties frequently engage in negotiations with the relevant governmental agency concerning possible means of addressing those issues and may agree to delay consummation of the transaction while such negotiations continue. Expiration or termination of the applicable waiting period under the HSR Act is a condition to the Purchaser's obligation to accept for payment and pay for Shares tendered pursuant to the Offer.

The Merger will not require an additional filing under the HSR Act if the Purchaser owns 50% or more of the outstanding Shares at the time of the Merger or if the Merger occurs within one year after the HSR Act waiting period applicable to the Offer expires or is terminated.

The Antitrust Division and the FTC frequently scrutinize the legality under the antitrust laws of transactions such as the Purchaser's proposed acquisition of the Company. At any time before or after the Purchaser's acquisition of Shares pursuant to the Offer, the Antitrust Division or the FTC could take such action under the antitrust laws as it deems necessary or desirable in the public interest, including seeking to enjoin the purchase of Shares pursuant to the Offer or the consummation of the Merger or seeking the divestiture of Shares acquired by the Purchaser or the divestiture of substantial assets of the Company or its subsidiaries or St. Jude Medical or its subsidiaries. Private parties, including state Attorneys General, may also bring legal action under the antitrust laws under certain circumstances. There can be no assurance that a challenge to the Offer on antitrust grounds will not be made or, if such a challenge is made, of the result thereof.

Foreign Jurisdictions. St. Jude Medical and the Company conduct operations in a large number of other jurisdictions throughout the world, where other antitrust filings or approvals may be required or advisable in connection with the completion of the Offer and the Merger. St. Jude Medical and the Purchaser currently intend to make filings or seek approvals in certain other jurisdictions if necessary; however, St. Jude Medical and the Purchaser do not expect such filings or approvals to materially delay the completion of the Offer or the consummation of the Merger. However, it cannot be ruled out that any foreign antitrust authority might seek to require remedial undertakings as a condition to its approval.

19

Section 14(f) Information Statement

The Information Statement attached as Annex B to this Statement is being furnished in connection with the possible designation by St. Jude Medical, pursuant to the terms of the Merger Agreement, of certain persons to be elected to the Company Board other than at a meeting of the Company's shareholders.

Certain Other Matters

Second Amendment to Rights Agreement. Each Right issued pursuant to the Rights Agreement entitles the registered holder to purchase under some circumstances one share of Common Stock at a price of $133.33 a share, subject to adjustment. Generally, the Rights become exercisable 10 business days after the earlier of (1) the first public announcement that a person or group of affiliated or associated persons (an "Acquiring Person") has acquired or obtained the right to acquire beneficial ownership of 15% or more of the outstanding Common Stock or (2) the commencement of a tender offer or exchange offer, the consummation of which would result in beneficial ownership by a person or group of 20% or more of the Common Stock (the earlier of such dates being the "Distribution Date"). After any person becomes an Acquiring Person, each holder of a Right (other than the Acquiring Person) will thereafter have the right to receive that number of shares of Common Stock having a market value equal to two times the applicable purchase price of the Right. Upon the vote of the Board, the Rights may be redeemed at a price of $.01 per Right at any time prior to a person becoming an Acquiring Person.

The Company and Computershare Investor Services LLC, as rights agent under the Rights Agreement, amended the Rights Agreement as of October 14, 2005 to provide, among other things, that (1) none of St. Jude Medical, the Purchaser or any of their respective affiliates or associates will become an Acquiring Person and (2) no Distribution Date, Stock Acquisition Date, Section 11(a)(ii) Event, Section 13 Event or Triggering Event (each, as defined in the Rights Agreement) will occur, in each case solely by virtue of (A) the Offer, (B) the acquisition of Common Stock pursuant to the Offer, the Merger or the Merger Agreement, (C) the execution and delivery of the Merger Agreement or (D) the consummation of the Offer, the Merger or any of the other transactions contemplated by the Merger Agreement.

20

Item 9. Material to be Filed as Exhibits.

The following Exhibits are attached hereto:

| Exhibit Number | Description | |

|---|---|---|

(a)(1) | Letter to the shareholders of the Company, dated October 18, 2005. | |

(a)(2) | Offer to Purchase, dated October 18, 2005 | |

(a)(3) | Form of Letter of Transmittal. | |

(a)(4) | Opinion of Piper Jaffray & Co., dated as of October 14, 2005 (included as Annex A to this Statement). | |

(a)(5) | Joint Press Release issued by the Company and St. Jude Medical on October 16, 2005 (incorporated by reference to Exhibit 99.1 of the Form 8-K filed by the Company on October 17, 2005). | |

(a)(6)(i) | Part 13 of the Texas Business Corporation Act. | |

(a)(6)(ii) | Articles 5.11, 5.12, 5.13 and 5.16(E) of the Texas Business Corporation Act. | |

(e)(1) | Agreement and Plan of Merger, dated as of October 15, 2005, among St. Jude Medical, the Purchaser and the Company (incorporated by reference to Exhibit 2.1 to the Form 8-K filed by the Company on October 17, 2005). | |

(e)(2) | Information Statement of the Company, dated October 18, 2005 (included as Annex B hereto). | |

(e)(3) | Confidentiality Agreement dated July 28, 2005 between the Company and St. Jude Medical. | |

(e)(4) | Special Termination Agreement between the Company and Christopher G. Chavez, President and Chief Executive Officer, dated as of April 1, 2002. | |

(e)(5) | Special Termination Agreement between the Company and Mr. Kenneth G. Hawari, General Counsel, Executive Vice President—Corporate Development and Secretary, dated as of April 1, 2002. | |

(e)(6) | Special Termination Agreement between the Company and Mr. Scott F. Drees, Executive Vice President—Operations, dated as of May 25, 2001. | |

(e)(7) | Special Termination Agreement between the Company and Mr. F. Robert Merrill, III, Chief Financial Officer, dated as of May 25, 2001. | |

(e)(8) | Special Termination Agreement between the Company and Mr. James P. Calhoun, Vice President—Human Resources, dated as of May 25, 2001. | |

(e)(9) | Special Termination Agreement between the Company and Mr. John H. Erickson, Vice President—Research & Development, dated as of May 25, 2001. | |

(e)(10) | Special Termination Agreement between the Company and Mr. Stuart B. Johnson, Vice President—Manufacturing, dated as of May 25, 2001. | |

(e)(11) | Second Amendment to Rights Agreement, dated as of October 14, 2005. | |

(g) | Not applicable. |

21

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this Statement is true, complete and correct.

| ADVANCED NEUROMODULATION SYSTEMS, INC. | |||||

By: | /s/ KENNETH G. HAWARI | ||||

| Name: | Kenneth G. Hawari | ||||

| Title: | Executive Vice President—Corporate Development, General Counsel and Secretary | ||||

![]()

October 14, 2005

Personal and Confidential

The Board of Directors

Advanced Neuromodulation Systems, Inc.