RECAPITALIZATION PLAN

APRIL 2006

FORWARD-LOOKING STATEMENTS

Forward-Looking Statements. This document contains forward-looking statements. These statements relate to analyses and other information

that are based on forecasts of future results and estimates of amounts not yet determinable. These statements also relate to future prospects,

developments and business strategies. These forward-looking statements are identified by their use of terms and phrases such as “anticipate,”

“believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “will” and similar terms and phrases, including references to

assumptions. These forward-looking statements involve risks and uncertainties, internal and external, that may cause Engelhard’s actual future

activities and results of operations to be materially different from those suggested or described in this document. Risks and uncertainties that

could cause actual results to differ materially and negatively impact us include, but are not limited to, the following: we may not be able to

achieve and execute internal business plans; we may experience changes in market conditions that cause us to consider divesting or

restructuring operations, which could impact future earnings; our future cash flows depend upon the creation, acquisition and commercialization

of new technologies to replace obsolete technologies; we depend upon the operating success of our manufacturing facilities and do not maintain

redundant capacity; we could experience capacity constraints, and should demand for certain products increase, we could have short-term

difficulty meeting the increased demand, hindering growth opportunities; we may experience product quality deficiencies; we could experience

physical inventory losses by theft and manufacturing inefficiency, particularly with regard to precious and base metals; we are currently engaged

in various legal disputes, and unfavorable resolution of these disputes and still unidentified future legal claims could negatively impact us; we

are subject to contingencies related to actual or alleged environmental contamination to which we may be a party; we face uncertainty regarding

the outcome of the BASF offer, which may affect our stock price, future business, employee retention and recruitment, and may negatively

impact supplier and customer relationships; as a manufacturer, we are subject to end-user product liability litigation associated with our

products; we face competitive pricing or product development activities affecting demand for our products; we are dependent upon the markets

for our customers’ products as a supplier of materials to other manufacturers; the solvency and liquidity of our customers could change; we

could face fluctuations in the supply and prices of precious and base metals and fluctuations in the relationships between forward prices to spot

prices; we could face a decrease in the availability or an increase in the cost of energy, notably natural gas, rare earth compounds, substrates

and other raw materials; we are subject to recent adverse trends in benefit costs, notably pension and medical benefits; we face risks related to

higher interest rates and changes in foreign currency exchange rates; geographic expansion may not develop as anticipated; we are exposed to

overall economic conditions and could be impacted by economic downturns and inflation; and we face risks related to increased levels of

worldwide political instability, the impact of the repeal of the U.S. export sales tax incentive, government legislation and/or regulation particularly

on environmental and taxation matters, and a slowdown in the expected rate of environmental regulations and the impact of natural disasters.

1

FORWARD-LOOKING STATEMENTS (Cont’d)

For a more thorough discussion of these factors, please refer to the Appendix to this document and “Forward-Looking Statements” (excluding

the first sentence thereof), “Risk Factors” and “Key Assumptions” on pages 34, 35 and 38, respectively, of Engelhard’s 2005 Annual Report on

Form 10-K, dated March 3, 2006.

Investors are cautioned not to place undue reliance on any forward-looking statement, which speaks only as of the date made, and to recognize

that forward-looking statements are predictions of future results, which may not occur as anticipated. Actual results could differ materially from

those anticipated in the forward-looking statements and from historical results due to the risks and uncertainties described above, as well as

others that Engelhard may consider immaterial or does not anticipate at this time. The foregoing risks and uncertainties are not exclusive and

further information concerning Engelhard and its businesses, including factors that potentially could materially affect its financial results or

condition, may emerge from time to time. Investors are advised to consult any further disclosures Engelhard makes on related subjects in

Engelhard’s future periodic and current reports and other documents that Engelhard files with or furnishes to the Securities and Exchange

Commission (“SEC”).

No Offer or Solicitation. This document does not constitute an offer or invitation to purchase nor a solicitation of an offer to sell any securities

of Engelhard. The proposed self-tender offer by Engelhard described in this document has not commenced. Any offers to purchase or

solicitation of offers to sell will be made only pursuant to a tender offer statement (including an offer to purchase, a letter of transmittal and other

offer documents) filed by Engelhard (“Engelhard’s Tender Offer Statement”) with the SEC. ENGELHARD’S SHAREHOLDERS ARE ADVISED

TO READ ENGELHARD’S TENDER OFFER STATEMENT AND ANY OTHER DOCUMENTS RELATING TO THE TENDER OFFER THAT

ARE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN

IMPORTANT INFORMATION.

Additional Information and Where to Find It. Engelhard also plans to file with the SEC and mail to its shareholders a definitive Proxy

Statement on Form 14A relating to the 2006 annual meeting of shareholders and the election of directors (the “2006 Proxy Statement”) and

other important information. Engelhard and its directors and certain of its officers may be deemed, under SEC rules, to be participants in

soliciting proxies from Engelhard’s shareholders. Information regarding the names of Engelhard’s directors and executive officers and their

respective interests in Engelhard by security holdings or otherwise is set forth in Engelhard’s Proxy Statement relating to the 2005 annual

meeting of shareholders (the “2005 Proxy Statement”). Additional information regarding the interests of such and other potential participants

will be included in the 2006 Proxy Statement and other relevant documents to be filed with the SEC in connection with Engelhard’s 2006 annual

meeting of shareholders that will be filed with the SEC. INVESTORS AND SECURITY HOLDERS ARE ADVISED TO READ THE 2006 PROXY

STATEMENT AND OTHER MATERIALS FILED WITH THE SEC BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. On

January 9, 2006, BASF filed a Tender Offer Statement on Schedule TO, which has been amended (the “BASF Tender Offer Statement”). In

response to the BASF Tender Offer Statement, Engelhard has filed certain materials with the SEC, including the Schedule 14D-9 filed on

February 2, 2006, which has been amended (the “Schedule 14D-9”).

2

Investors and security holders may obtain a free copy of Engelhard’s Tender Offer Statement (when it is filed and becomes available), Schedule

14D-9, 2005 Proxy Statement, 2006 Proxy Statement (when it is filed and becomes available), BASF’s Tender Offer Statement and other

documents filed by Engelhard or BASF with the SEC at the SEC's website at http://www.sec.gov. In addition, investors and security holders

may obtain a free copy of each of the Schedule 14D-9, 2005 Proxy Statement, 2006 Proxy Statement (when it is filed and becomes available),

Engelhard’s Tender Offer Statement (when it is filed and becomes available), as well as Engelhard’s related filings with the SEC, from

Engelhard by directing a request to Engelhard Corporation, 101 Wood Avenue, Iselin, New Jersey 08830, Attention: Investor Relations or at

732-205-5000, or from MacKenzie Partners, Inc. by calling 1-800-322-2885 toll free or at 1-212-929-5500 collect or by e-mail at

Engelhard@mackenziepartners.com.

Risk Factors Related to the Recapitalization. The recapitalization presents some potential risks and disadvantages to the Company and its

continuing shareholders, including the following:

If we complete the recapitalization, our indebtedness and interest expense will increase, and the terms of our future indebtedness may be

adversely affected. As a result of the recapitalization and the related borrowings, our indebtedness will be more substantial in relation to

our shareholders’ equity. After giving pro forma effect to the recapitalization and the related borrowings at June, 2006, the Company

would have had total indebtedness of $1,800 million and shareholders’ equity of $295 million as of December 31, 2005.

Following our announcement of the recapitalization, we expect our credit ratings will be downgraded by each of the principal rating

agencies, but that we will maintain our investment grade ratings. Should the Company’s rating drop below investment grade, the

Company would experience higher capital costs and may incur difficulty in procuring metals.

Our ability to repurchase our shares in the self-tender will be subject to a number of conditions, including obtaining financing. The

commitment letter we received to provide a one year bridge facility of $1.5 billion to fund the repurchase and related costs and expenses

is subject to a number of conditions, including there being no material adverse change in the Company since December 31, 2005 and

there being no material disruption of or material adverse change in financial, banking or capital markets since April 25, 2006. In addition,

we have to amend our existing credit facilities to permit the increased level of indebtedness.

The expected benefits of the recapitalization plan rely in part on our ability to refinance our bridge facility and the terms of the financing

obtained. The expected terms used herein are based on current market conditions. The terms of any permanent financing will depend on

market conditions at the time we incur the indebtedness, and are likely to be different. In addition, a portion of the permanent financing is

expected to have a floating rate of interest, which may increase over time.

FORWARD-LOOKING STATEMENTS (Cont’d)

3

I.

Introduction

II.

Business Review and Update

III.

Financial Overview

IV.

Recapitalization Plan

V.

Concluding Remarks

Appendix

Table of Contents

4

I. Introduction

Introduction

Background

On January 3, 2006, BASF publicly announced its intention to launch a hostile offer

to acquire Engelhard at $37 per share, and on January 9, 2006, BASF filed a

Tender Offer Statement

On January 23, 2006, Engelhard’s Board announced its determination that the

BASF offer was inadequate and not in the best interests of Engelhard shareholders

Concurrently, the Board authorized Engelhard's management team and

independent advisors to explore strategic alternatives to seek to maximize

shareholder value, including the possible sale of the Company

On April 19, 2006, BASF made a proposal for $38.00 per share in response to

Engelhard’s request for an increased offer following BASF’s access to non-public

information

On April 25, 2006, the Engelhard Board unanimously determined that:

The $38.00 per share proposal was inadequate and not in the best interests of

Engelhard’s shareholders

A recapitalization of the Company represents the most attractive strategic

alternative available to Engelhard for delivering greater value to Engelhard’s

shareholders than BASF’s proposal of $38.00 per share

6

Introduction

Recapitalization Plan Overview

The recapitalization plan (“Recapitalization Plan”) consists of:

The purchase of 26 million shares (approximately 20% of Engelhard’s shares

outstanding including exercisable options) at a price of $45.00 per share

Continued execution of the Company’s business strategy, including an

incremental cost-savings initiative associated with the Recapitalization Plan

Shares to be purchased through a self-tender offer

Committed financing, subject to customary conditions, is in place from Merrill Lynch

and JPMorgan to initially fund self-tender offer; permanent financing expected to

comprise a mix of hybrid securities and floating- and fixed-rate debt

Investment grade ratings profile expected based upon rating agency feedback

The Board will increase its size at the June 2 Annual Meeting from six to nine,

giving shareholders the ability to elect a majority of the Board (without the damage

and distraction that could result from a potentially lengthy consent solicitation that

BASF has threatened) and in so doing, giving shareholders the ability to decide

whether the Recapitalization Plan or BASF's $38.00 proposal (which the Board has

found to be inadequate) serves the shareholders' best interests

7

Introduction

Recapitalization Plan Highlights

The Engelhard Board of Directors strongly believes that the Recapitalization Plan

represents the best value creation alternative and is in the best interests of Engelhard

shareholders for a number of reasons, including:

The Recapitalization Plan should deliver value superior to BASF’s $38.00 per share

proposal

Accretion to EPS and EPS growth commencing in 2007

Expected strong forward price to earnings (P/E) multiple

Provides meaningful liquidity to Engelhard shareholders at an attractive price of

$45.00 per share

Offers Engelhard shareholders the ability to participate in Engelhard’s strengthening

business prospects and realize the Company’s future growth potential through

appreciation of the market price of the stock or a future sale of the Company

Maintains investment grade credit profile

8

Introduction

Timetable

Announcement of Recapitalization Plan

Filing of Preliminary Proxy Materials

Commencement of Self-Tender Offer

Engelhard Annual Shareholders Meeting

Self-Tender Offer closes subject to satisfaction or

waiver of conditions including if BASF’s nominees

constitute a majority of the Board and the Board

determines not to proceed with Self Tender Offer

April 26, 2006

Following Annual

Meeting

________Date_________

______________________Key Event______________________

June 2, 2006

Week of May 1,

2006

9

II. Business Review and

Update

Business Update

Engelhard Business Highlights

Engelhard is one of the largest surface and materials science companies in the world

The Company has made significant investments in recent years in both organic growth initiatives and

strategic acquisitions

Investments already made in new growth initiatives alone are expected to add an additional

$100 million in operating earnings from 2005 to 2007

Engelhard has demonstrated a strong commitment to R&D

Engelhard has streamlined its business portfolio, used the proceeds to invest in higher-margin

businesses and improved the Company’s overall business mix

Over the last several years, Engelhard invested in businesses such as diesel-emission control,

energy & fuel materials, personal care & cosmetic materials and separators & polymers, and exited

low-margin and low-growth legacy precious-metal fabrication businesses

Engelhard expects to benefit from numerous global trends over the next several years which include:

Significant increase in demand projected for sophisticated emission-control technologies as more

stringent regulatory guidelines take effect globally

Worldwide growing demand for energy, energy-related materials and environmentally friendly fuels

Growing demand for personal care and cosmetic products driven by increasing affluence of a global

and aging population

High-Margin, Non-Cyclical Business Portfolio with Strong Growth Prospects

11

Business Update

Engelhard Shaping Value Proposition

Core competencies in surface and materials science

Strategic focus on technology and high-growth markets

Enabled by ingenuity

Enhanced by a passion for productivity

All leveraged by a seamlessly integrated, decentralized operating philosophy

Enterprise wide competencies focused on technologies/markets to fuel

growth through expanded, value-adding served industry market portfolio

Reduced cyclicality, increased globalization and increased cash flow

enhance value of growth from strategic context

12

13

$28

8%

$66

19%

$141

42%

$6

2%

$98

29%

$2,096

45%

$726

16%

$1,009

22%

$79

2%

$687

15%

Ventures (3)

Materials Services

Process Technologies

Environmental Technologies

Appearance and Performance Tech.

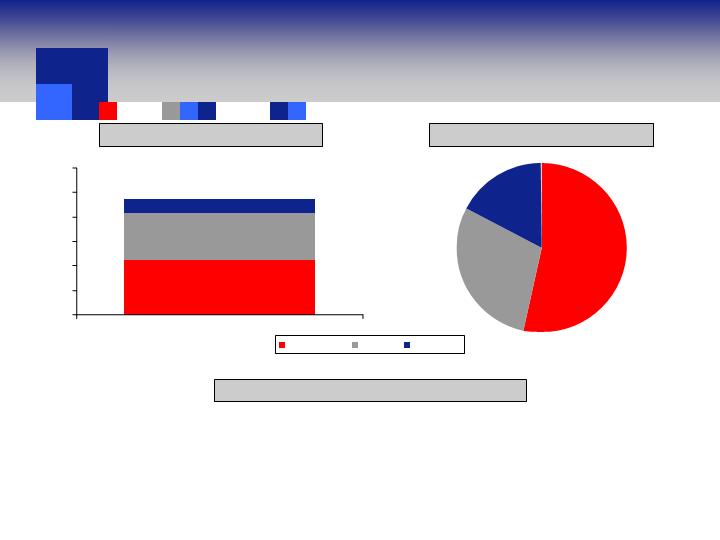

Business Update

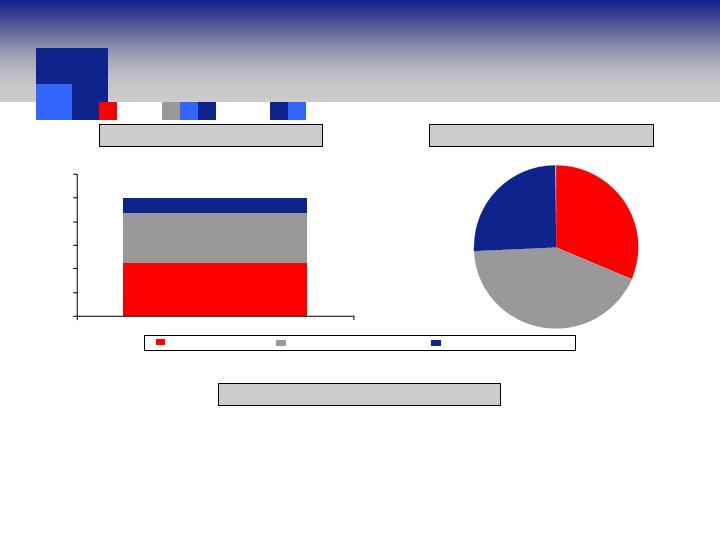

Overview of The Business Segments

Engelhard technology platforms support growth in expanding markets

2005 Sales: $4,597mm (1)

2005 Operating Earnings: $339mm (1) (2)

(1)

Reflects 2005 financial information from Engelhard’s 10-K filed March 3, 2006.

(2)

Operating earnings do not include unallocated corporate expense ($40 million).

(3)

Ventures sales includes $3 million of Corporate.

Engelhard

13%

Lyondell (1)

7%

Nova Chem

3%

Engelhard’s Operating Margin Consistent Throughout the Cycle

Note: Engelhard’s margins exclude Materials Services and Substrates.

Source: Reflects 2005 Engelhard information from Engelhard’s 10-K filed March 3, 2006. Other information based on Wall Street research.

(1) Lyondell adjusted to include proportionate share of joint ventures.

Dow

14%

Business Update

Strength Throughout The Cycle

Rohm & Haas

13%

Eastman

14%

(10.0%)

(5.0%)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

14

15

Note: As of December 30, 2005.

Source: Bloomberg. Chemical composite includes Air Products & Chemicals Inc., Ashland Inc., The Dow Chemical Co., Eastman Chemical Co., Ecolab Inc., Du Pont de Nemours &

Co., Hercules Inc., International Flavors and Fragrances Inc., Monsanto Co., PPG Industries Inc., Praxair Inc., Rohm & Haas Co. and Sigma-Aldrich Corp.

Engelhard

Chemical Composite

More stable earnings through cycles

Engelhard is at an inflection point as its successful strategic initiatives converge

Business Update

Increased Stability of Earnings

2010E

Operating

Earnings

2005

Operating

Earnings

2000

Operating

Earnings

Business Update

Improving Business Mix

Note: Includes reportable segments and Ventures. Does not include unallocated corporate ($29 million in 2000, $40 million in 2005, and $46 million in 2010) or 2000 special and other

charges ($133 million). 2005 financial information reflects Engelhard’s 10-K filed March 3, 2006. 2010E financial information based on Engelhard Management Operating Plan

developed in August, 2005.

70%

30%

90%

2%

8%

Technology Businesses

Materials Services

Ventures

92%

5%

3%

16

Environmental Technologies

Overview

Marketing Cost-Effective

Compliance

Global presence; diverse markets

& customers

Increasingly stringent

environmental regulations

Technology-driven

products and processes

Sales $1,009 $2,125

’06E - ’10E

Operating

Earnings

Growth

Note: Dollars in millions. 2010 metrics rounded to the nearest $25 million and all financial information includes pass-through

of substrates.

(1) 2010E financial information is based on Engelhard Management Operating Plan developed in August, 2005.

2005A

2010E (1)

Low teens

17

Environmental Technologies

Competitive Advantages

The following provide competitive advantages:

Surface and materials science expertise

Engine application laboratories

State-of-the-art, high-precision manufacturing technology in all major regions

Precious metals management

Business awarded to-date supports majority of projected sales

80% of 2007

70% of 2008

60% of 2009

Robust research pipeline

30-Year Track Record of Leadership & Innovation

18

US-EPA 2004

US-EPA 1998

Euro 3 2000

Euro 4 2005

Euro 5 ’08

Japan ’05

US ’07

US-EPA 2010

Note: Increasingly stringent regulations in emission standards in heavy-duty-diesel expected to drive sectional growth in catalyst technology.

(1) Worldwide Heavy-Duty-Diesel.

Emerging Market Regulations (Euro 4 Proposed)

Turkey: '08

Brazil: '09

China: '10

India: '11-'12

Environmental Technologies

Exhaust Emissions Regulations (1) Drive Growth

19

Environmental Technologies

Growth Opportunities

Increasingly stringent regulations around the world

Approximately 70% operating earnings growth in the heavy-duty-diesel market (1)

Technology leadership

Specific strengths in engine and catalyst technology

Expansion into a broad range of developing markets and geographies

Sustainable productivity gains

Engelhard’s base global auto-catalyst business expected to grow at more than a 5%

CAGR from 2005 to 2010, excluding medium- and heavy-duty-diesel

Environmental Technologies expected to be a significant driver of growth

(1) Based on Engelhard Management Operating Plan developed in August, 2005. Compounded annual growth rate from 2006-2010.

20

Note: 2010E financial information based on Engelhard Management Operating Plan developed in August, 2005.

Numbers rounded to the nearest $25mm.

(1) Automotive includes light duty diesel.

(2) Percentage numbers are 2005E-2010E CAGR of the respective market.

(3) Other includes retrofit, motorcycle, other mobile sources, stationary and Engineered Materials Systems.

Environmental Technologies

Financial Targets

$1,116

Incremental Sales from ’05 to ’10E (2)

2010E Sales Target

2010E Operating Earnings Target of $250 million

Other (3)

Heavy Duty Diesel

Automotive (1)

51%

11%

13%

$437

$565

$114

$1,375

$500

$250

$0

$500

$1,000

$1,500

$2,000

$2,500

$2,125

21

Environmental Technologies

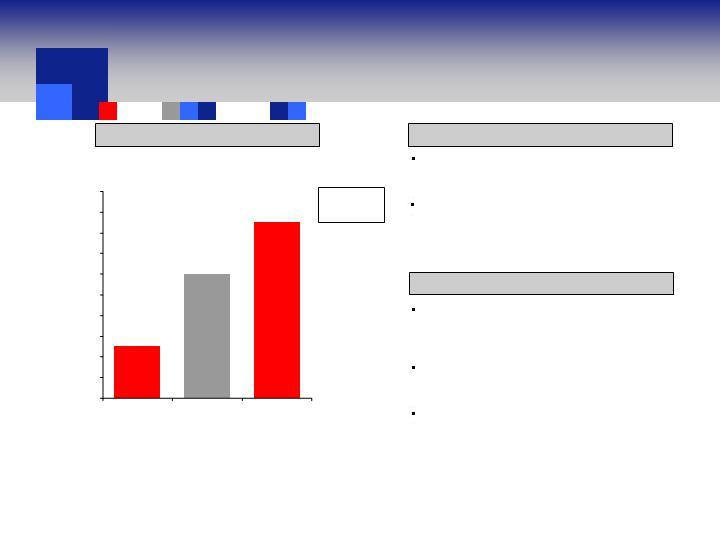

Recent Results

Sales

Selected Highlights

Operating Earnings

Double-digit sales and operating

earnings growth

Growth in auto catalysts driven by

European light-duty-diesel

Strong growth in Asia; continued

strength in joint ventures in Korea

and Japan, which are not included

in the Environmental Technologies

operating earnings

Continued productivity gains

Note: Dollars in millions. Q1 2006 financials based on April 26, 2006 Engelhard press release.

(1) Operating margin includes substrates; excluding substrates, margins were approximately flat Q106 vs. Q105.

16%

13%

Operating

Margin (1)

Q over Q

Growth: 12%

Q over Q

Growth: 35%

$238

$320

$0

$100

$200

$300

$400

Q1 2005

Q1 2006

$42

$37

$0

$10

$20

$30

$40

$50

$60

Q1 2005

Q1 2006

22

Process Technologies

Overview

Marketing Process

Productivity

Technology/market

development

More Stringent Environmental

regulations

Value pricing

Sales $687 $950

’06E - ’10E

Operating

Earnings

Growth

2005A

2010E (1)

Mid teens

Note: Dollars in millions and 2010 metrics rounded to the nearest $25 million.

(1) 2010E financial information is based on Engelhard Management Operating Plan developed in August, 2005.

23

Process Technologies

Competitive Advantages

Surface and materials science:

Distributed Matrix System (DMS) maximizes refinery gasoline yields

Controlled Particle Design (CPD) providing uniform particles and unique morphology for

Fischer-Tropsch Gas-to-Liquids (GTL) technologies

Ziegler/Natta Technology – Fourth Generation (Lynx) improving process economics

through superior activity by increasing the pounds of polypropylene produced per pound

of catalysis

Expertise across a broad diversity of manufacturing operations:

Catalytic manufacturing capabilities ranging from producing kilograms per order for the

fine chemicals market to tons per day of fluid catalytic cracking (FCC) catalyst for the

petroleum-refining market

While maintaining global, low cost positions and excellent quality

24

Process Technologies

Growth Opportunities

Process Technologies is poised to achieve double-digit operating

earnings growth in 2006 to 2010E (1)

(1) Based on Engelhard Management Operating Plan estimates developed in August, 2005.

Growth initiatives include:

Increased product offerings to previously unserved refining markets including diesel,

distillate and petrochemical feedstock markets

Continued expansion of gas-to-liquids market with Fischer-Tropsch and syngas

technology; continued leveraging of those technologies in the emerging gas economy

Expansion into previously unserved petrochemical markets based on current

commercial agreements

Increased synergies from leveraging DMS technology platform to expand refinery

catalysis

Leverage Lynx polypropylene success in polyethylene catalyst market

25

Process Technologies

Financial Targets

2010E Sales Target

$263

Incremental Sales from ’05 to ’10E (2)

Note: Above financial information based on Engelhard Management Operating Plan developed in August, 2005. Numbers rounded to the nearest $25mm.

(1) Precious Metals revenues included in Chemicals.

(2) Percentage numbers are 2005-2010E CAGR of the respective market.

Chemicals (1)

Refining

Polyolefins

8%

5%

9%

2010E Operating Earnings Target of $200 million

$450

$375

$125

$0

$200

$400

$600

$800

$1,000

$1,200

$950

$45

$78

$140

26

Process Technologies

Recent Results

Sales

Selected Highlights

Operating Earnings

Double-digit sales and operating

earnings growth and margin

expansion

Continued strong demand for

technologies for petroleum refining,

including strength in additives

Strong pricing power in chemical

process market; capacity utilization

rates approximately 90%

Note: Dollars in millions. Q1 2006 financials based on April 26, 2006 Engelhard press release.

Operating

Margin

13%

15%

Q over Q

Growth: 16%

Q over Q

Growth: 38%

$171

$148

$0

$50

$100

$150

$200

Q1 2005

Q1 2006

$26

$19

$0

$5

$10

$15

$20

$25

$30

Q1 2005

Q1 2006

27

Appearance and Performance Technologies

Overview

Enabling Marketing of

Enhanced Image &

Functionality

Develop markets

Leverage assets

Enrich product mix

Pricing and sustainable

productivity gains

Sales $726 $1,000

’06E - ’10E

Operating

Earnings

Growth

2005A

2010E (1)

Double-digit

Note: Dollars in millions and 2010 metrics rounded to the nearest $25 million.

(1) 2010E financial information is based on Engelhard Management Operating Plan developed in August, 2005.

28

Appearance and Performance Technologies

Growth Opportunities

Worldwide leadership position in personal care and cosmetics

New product development and technological focus

Globalization

Continued growth in developing markets, especially Asia-Pacific

Return of investment in Company’s personal care business gaining momentum

Focus on Japan yielding results as Engelhard anticipates growth of 30% versus 8%

market growth (1)

Significant margin improvement in minerals

Improved product mix – less dependence on paper market

Improved pricing

Appearance and Performance Technologies Is Positioned for Double-Digit Growth

(1) Based on Engelhard management guidance. Compound annual growth rate from 2006-2010.

29

Appearance and Performance Technologies

Sales and Operating Earnings Growth Drivers

Personal Care

Sales:

Asia (ex China): Market-share expansion in large, mature

Japanese and Korean markets where

predecessor businesses had low penetration

China: High organic growth on low base

NAFTA: Organic growth only, due to high penetration

Europe/Latin America: Organic growth supplemented with

share expansion where predecessor US

business had low penetration

Operating Earnings:

Better utilization of assets, particularly Long Island facility

Grow sales with little SG&A additions

Earnings from sales expansion

Effects/Colors

Sales:

Base business growth

Asia growth

New effects/colors technologies/products

Major paint customer geographic expansion

Operating Earnings:

Productivity, largely manufacturing & supply chain

Grow sales with little SG&A addition

Earnings from sales growth

Performance Minerals

Sales:

New products: Favorable inter-material substitution

Non-paper, specialty growth in diversified markets

Price increases/energy surcharges/contract improvements

Operating Earnings:

Margin recovery

Productivity, largely manufacturing & supply chain

Earnings from sales growth

Business Transformation

30

Appearance and Performance Technologies

Financial Targets

Incremental Sales from ’05 to ’10E (2)

2010E Sales Target

$274

Note: Above financial information based on Engelhard Management Operating Plan developed in August, 2005.

Numbers rounded to the nearest $25mm.

(1)

Specialty Minerals includes kaolin and attapulgite.

(2)

Percentage numbers are 2005-2010E CAGR of the respective market.

Specialty Minerals (1)

Effects Materials and Colors

Personal Care Materials

7%

18%

4%

2010E Operating Earnings Target of $175 million

$450

$425

$125

$0

$200

$400

$600

$800

$1,000

$1,200

$1,000

$71

$117

$86

31

Appearance & Performance Technologies

Recent Results

Sales

Selected Highlights

Operating Earnings

Double-digit gains in sales and operating

earnings growth

Continued positive impact of recent

acquisitions in cosmetics and

personal care

Continue to optimize mix by

successfully redirecting mid-Georgia

assets to higher margin specialty

kaolin and refining catalysts markets

Higher pricing and energy

surcharges offset higher natural gas

costs

Operating

Margin

Note: Dollars in millions. Q1 2006 financials based on April 26, 2006 Engelhard press release.

10%

11%

Q over Q

Growth: 19%

Q over Q

Growth: 19%

$206

$174

$0

$50

$100

$150

$200

$250

Q1 2005

Q1 2006

$18

$22

$0

$5

$10

$15

$20

$25

Q1 2005

Q1 2006

32

Enabling Technology

Businesses

High returns on invested

capital

Source of cash

Risk management

Enabler for catalyst sales

Sales $2,096 $2,425

2010E (1)

2005A

Note: Dollars in millions and 2010 metrics rounded to the nearest $25 million.

(1) 2010E financial information is based on Engelhard Management Operating Plan developed in August, 2005.

Materials Services

Overview

33

Materials Services

Core Strengths and Risk Management

Experienced management team with

knowledge in specific markets

Assay Services

Inventory management

Logistics and security

Precious metal-based solutions

Refining and recycling

Core Strengths

Procedures and controls are in place and

followed carefully to minimize:

Price risk

Credit risk

Errors in location, quantities, currency,

or value

Over limits

Improper transactions

Risk Management

34

Materials Services

Recent Results and Long-Term Plan

Selected Highlights

Operating Earnings

Increased volume and

improvements in recycling process

results

Strong demand for platinum and

rhodium related to pending diesel

regulations

Long-Term Plan

For planning purposes, long-term

projected operating earnings

approximate $15 million annually

This compares to $28 million for the

full year of 2005 and $17 million for

the first quarter of 2006

Our core strengths, which have driven

recent results, expected to continue to be

strategically pursued and provide

upside to the long-term plan

Note: Dollars in millions. Q1 2006 financials based on April 26, 2006 Engelhard press release.

Q over Q

Growth: 240%

$17

$12

$5

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

Q1 2005

Q4 2005

Q1 2006

35

Ventures

Overview

“Develop the white

space, expand the core”

Platform identification

Opportunity development

Funding & staffing

Start-up & incubation

Sales $76 $210

’06E - ’10E

Operating

Earnings

Growth

2005A

2010E (1)

Double-digit

Note: Dollars in millions and 2010 metrics rounded to the nearest $10 million.

(1) 2010E financial information is based on Engelhard Management Operating Plan developed in August, 2005.

36

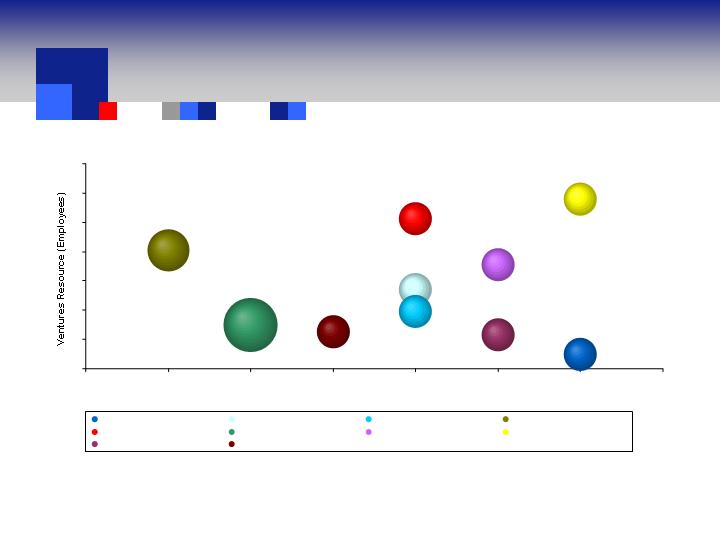

Ventures

Pipeline

Note: Proppants and Water projects are reflected in the Engelhard Management Operating Plan developed in August, 2005. Net Present Value of Proppants projects and

water projects estimated to be $80 mm and $50 mm, respectively. Financial impact of other projects in the pipeline are not reflected in the Engelhard Management Operating

Plan developed in August, 2005. This graph indicates the year in which these projects (represented by the bubbles) reach first $1 million of annual operating earnings.

30

30

30

$50

NPV

30

$80

NPV

30

30

30

30

0

1

2

3

4

5

6

7

2005

2006

2007

2008

2009

2010

2011

2012

Year of $1 million Operating Earnings

Scratch Resistant Coatings

Battery Materials

Photovoltaic Inks

Water

Aseptrol

Proppants

Fuel Cells/Portable

Fuel Cells/Hydrogen

Fuel Cells/Electrochem

Fuel Cells/Prereforming

37

Ventures

Growth Opportunities

Drive to become the leading global supplier of non-carbon separation and purification

technologies to the gas, fuel and water markets to generate $200 million in revenues in

2010

Oil and gas well stimulation materials should allow for additional earnings growth, given

supply shortages and strong exploration and production activities

Increased cost of fossil fuels expected to provide growth opportunities in alternative

energy sources including fuel cells, photovoltaics, biofuels and battery materials

Ventures systematically develops adjacent-space opportunities that leverage attractive

markets and new technologies

38

Ventures

Financial Targets

Incremental Sales from ’05 to ’10E

2010E Sales Target

$134

Note: Above financial information based on Engelhard Management Operating Plan developed August, 2005.

Numbers rounded to the nearest $10mm.

(1) Energy Materials includes Proppants and Fuel Cell.

Programs commercialized to date expected to yield $14 million in operating earnings in 2006

2010E Operating Earnings Target of $40 million

Alumina/Silica

Energy Materials (1)

Water Treatment

$140

$50

$20

$0

$50

$100

$150

$200

$250

$210

$15

$49

$70

39

Ventures

Recent Results

Sales

Selected Highlights

Operating Earnings

Ventures group expected to

contribute $14 million in operating

earnings for the full year 2006

Acquired adsorbents and catalyst

business of Almatis in 2005,

expanding the Company’s

technology portfolio to include

catalyst supports and alumina-

based adsorbents and dessicants

Obtained customer commitment for

new proppants

Operating

Margin

Note: Dollars in millions. Q1 2006 financials based on April 26, 2006 Engelhard press release.

5%

7%

Q over Q

Growth: 131%

Q over Q

Growth: 200%

$30

$13

$0

$5

$10

$15

$20

$25

$30

$35

Q1 2005

Q1 2006

$2.1

$0.7

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

Q1 2005

Q1 2006

40

III. Financial Overview – Before

Recapitalization Plan

2006 (1)

Double-digit earnings growth from technology segments

13% return on average total capital

Maintain financial capability

2006-2010E (1)

EPS CAGR of approximately 16%

Approximately 300 bps operating margin improvement between 2006-2010

Sales 8% CAGR

Average ROAC 14%-15%

(1) Based on Engelhard Management Operating Plan developed in August, 2005. Please refer to assumptions in Appendix. Forecast reflects announced regulations and plant constructions leading

to peak growth rates in 2008. Growth rates then return to low double-digit levels. Outer plan years do not include impact of new regulations, such as Off-Road HDD, or new customer plants not

yet contracted.

Financial Overview – Before Recapitalization Plan

Financial Goals

42

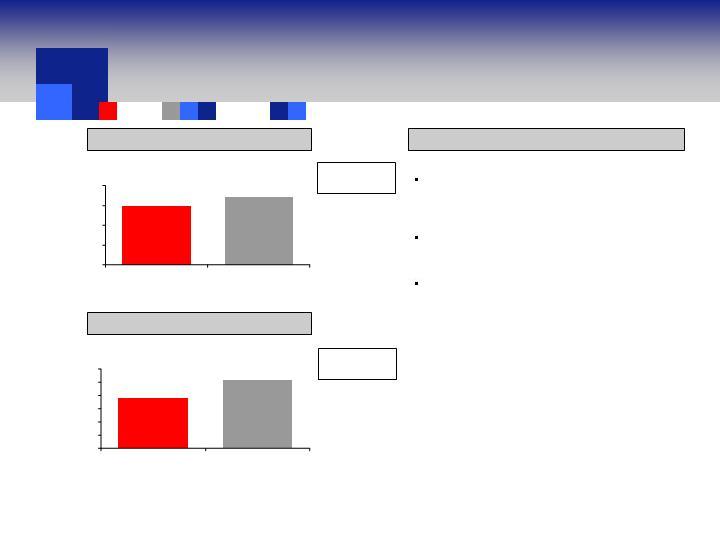

Financial Overview – Before Recapitalization Plan

Engelhard Today and in the Future

Sales Perspective

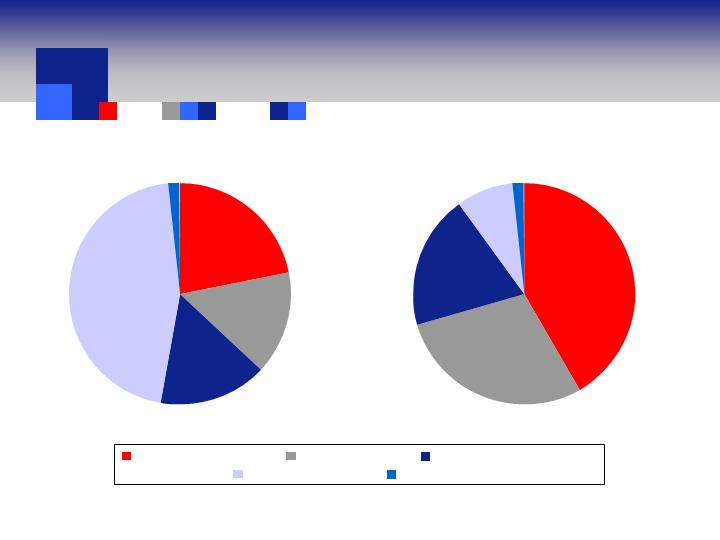

2005A Operating Earnings: $339 Million (1)(2)

2005A Sales: $4,597 Million (1)

2010E Sales: $6,710 Million

2010E Operating Earnings: $680 Million

Operating Earnings Perspective

Appearance & Performance Tech.

Environmental Technologies

Process Technologies

Materials Services

Ventures (3)

Note: 2010 financial information based on Engelhard Management Operating Plan developed in August, 2005.

(1)

Reflects 2005 financial information from Engelhard’s 10-K filed March 3, 2006.

(2)

Operating earnings do not include unallocated corporate expense ($40 million in 2005 and $46 million in 2010).

(3)

Ventures sales in 2005 include $3 million of Corporate.

15%

2%

22%

16%

45%

29%

2%

42%

19%

8%

14%

3%

32%

15%

36%

29%

6%

37%

26%

2%

43

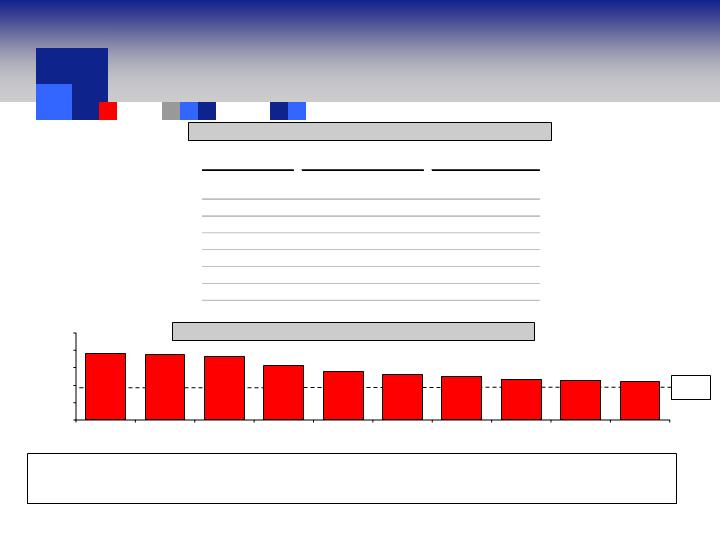

Financial Overview – Before Recapitalization Plan

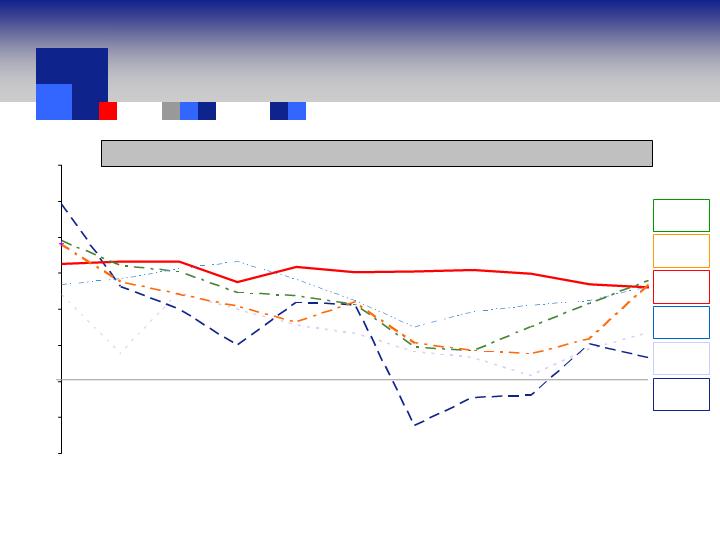

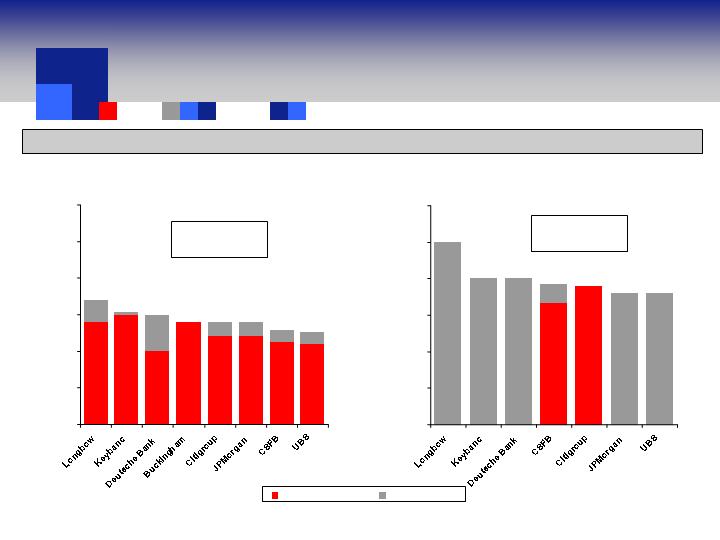

Recent Earnings Perspective

Wall Street Estimates Have Increased Versus Expectations Prior to BASF Offer

2006E

2007E

(1)

Buckingham Research suspended coverage for Engelhard in January.

(2)

No change in estimates.

$2.35

$2.25

$2.20

$2.20

$2.27

$2.14

$2.13

$2.20

(1)

As of December 31, 2005

As of April 21, 2006

$2.46

(2)

Mean as of 12/31/05: $2.39

Current Mean: $2.49

Mean as of 12/31/05: $2.13

Current Mean: $2.22

$2.10

$2.20

$2.25

$2.00

$2.20

$2.20

$2.06

$2.05

$0.08

$0.15

$0.08

$0.10

$0.10

$0.25

$0.02

$1.50

$1.75

$2.00

$2.25

$2.50

$2.75

$3.00

$2.45

$2.40

$2.40

$2.33

$2.50

$2.50

$2.75

$0.13

$1.50

$1.75

$2.00

$2.25

$2.50

$2.75

$3.00

44

IV. Recapitalization Plan

Recapitalization Plan

Overview

Self-tender offer at $45.00 per share in cash

The purchase of up to 26 million shares or approximately 20% of the shares outstanding including

exercisable options

Self-tender offer will be initially funded through a bridge facility which is to be refinanced with a mix

of hybrid securities (ICONs) and fixed and floating rate debt after closing the self tender offer

Merrill Lynch and JPMorgan have committed, subject to customary conditions, to provide

Engelhard with a $1.5 billion 364-day bridge credit facility to be used for the self-tender offer

Targeted investment grade ratings outcome

Recapitalization Plan cost savings initiative

Incremental $15 million in annual pre-tax savings

To be implemented in 2006 and fully-reflected in 2007 results

Savings primarily in SG&A, including warehousing expenses

Cash costs expected to be approximately $20 million during the second half of 2006

46

Recapitalization Plan

Financing Detail

Sources & Uses (1)

Pro Forma Capitalization (1)

Note: Dollars in Millions.

(1) Self-tender offer will initially be funded by a bridge facility.

(2) Assumes 50% equity credit from rating agencies for ICONs.

(3) EBITDA calculated as operating earnings of $299mm plus equity in earnings of affiliates of $33mm and depreciation and amortization of $132mm. EBITDA is used by financial institutions to

evaluate credit worthiness.

(4) Net of option proceeds of approximately $24.3mm.

Year Ended

Year Ended

12/31/2005

12/31/2005

Pre-Recap

Adjustment

Pro Forma

Cash

$42

6

$47

Non-Cash Current Assets

2,110

--

2,110

Other Assets

1,727

--

1,727

Total Assets

$3,879

$3,885

Non-Debt Current Liabilities

$1,468

$1,468

Existing Debt

600

--

600

Senior Notes

--

400

400

ICONs

--

800

800

Total Debt

600

1200

1,800

Other Liabilities

322

322

Equity

1,489

(1,194)

295

Total Liabilities & Equity

$3,879

$3,885

Operating Earnings

$299

$299

EBITDA

(3)

463

463

Total Interest

34

87

121

Total Debt/EBITDA

(3)

1.3x

3.0x

(2)

Total Debt to Capitalization

28.7%

66.8%

(2)

EBITDA/Interest

(3)

13.7x

3.8x

Corporate Credit Rating

A3/A-/A-

Investment Grade

Sources:

Amount

Callable Floating Senior Notes @ LIBOR + 80bps (6.140%)

$200.0

10 Year Senior Notes @ 6.405%

200.0

5 Year Call Basket C Security (ICON) @ 7.6125% - 60 Yr. Maturity

400.0

10 Year Call Basket C Security (ICON) @ 7.9675%- 60 Yr. Maturity

400.0

Total Sources

$1,200.0

Uses:

Amount

Purchase of Equity

(4)

$45.00

per share

$1,149.3

Fees & Expenses

25.0

Restructuring Costs

20.0

Incremental Cash

5.7

Total Uses

$1,200.0

47

Recapitalization Plan

Pro Forma EPS

2007 – First Full Year

Note: Interest rates based on current market conditions. Additional interest expense calculation assumes a fixed rate of 6.140% for the $200mm Callable Senior Notes debt tranche. A one percentage

point change in the LIBOR rate would have an approximate $0.01 impact on EPS in 2007. Per share values rounded to two decimals.

Assumptions

2007 Wall Street Average

$2.49

Wall Street analyst range $2.40 - $2.75

Additional Interest Expense

(0.52)

$200mm of Callable Floating Senior Notes @ LIBOR + 80bps (6.140%)

$200mm of 10 Year Senior Notes @ 6.405%

$400mm of 5 Year Basket C Security (ICON) @ 7.6125%

$400mm of 10 Year Basket C Security (ICON) @ 7.9675%

Cost-Savings Initiative

0.09

$15 mm annual pretax savings fully reflected in 2007

Reduced Shares

0.49

Repurchase of 26mm shares (~20% shares outstanding and

underlying vested options)

Pro Forma 2007 EPS

(Building from Wall Street Average)

$2.55

48

Recapitalization Plan

Market Multiples Have Generally Increased Since BASF Offer Was Made

Source: Factset. Based on Wall Street Research.

49

Du Pont

IFF

Cytec

Rohm & Haas

Albemarle

Umicore

Aldrich

Sigma-

Matthey

Johnson

Air Products

Praxair

20.0x

18.0

16.0

14.0

12.0

10.0

14.4x

14.5x

14.7x

15.0x

15.3x

15.5x

16.2x

17.2x

17.5x

17.6x

14.9x

16.6x

13.0x

13.7x

10.6x

14.2x

13.4x

14.1x

15.0x

17.6x

As of 12/30/2005

As of 4/21/2006

2007 P/E Multiple Analysis

Increase:

1.5x

11.5%

Average:

0.8x

5.7%

1.4x

10.7%

4.1x

38.6%

1.4x

9.6%

0.9x

6.3%

1.9x

14.4%

2.6x

17.6%

1.2x

8.0%

(0.4x)

(2.2%)

1.0x

5.8%

Pts.

%

50

12/30/05

7/1/05

12/31/04

7/2/04

1/2/04

7/4/03

1/3/03

60.0%

40.0%

20.0%

0.0%

(20.0%)

(40.0%)

12/30/05

7/1/05

12/31/04

7/2/04

1/2/04

7/4/03

1/3/03

20.0%

10.0%

0.0%

(10.0%)

(20.0%)

(30.0%)

(40.0%)

3-Year

Avg: (6.9%)

3-Year

Avg: 19.3%

1.0x

6.8%

4.6x

30.7%

2.7x

20.3%

-1.5x

(10.7%)

-0.2x

(1.6%)

-1.1x

(8.5%)

Umicore

Differential

at BASF

Offer

-1.6x

(11.3%)

2005 Average Differential

2004 Average Differential

2003 Average Differential

Recapitalization Plan

EC’s “Unaffected” Forward P/E Multiple Relative to Key Industry Peers over Time

JM

Differential

at BASF

Offer

-4.1x

(29.1%)

2005 Average Differential

2004 Average Differential

2003 Average Differential

Source: Factset.

Note: Johson Matthey and Umicore are the key industry peers to Engelhard.

Recapitalization Plan

Illustrative Market Value Per Share – Based on 2007 and 2010 EPS

Note: JM and Umicore are the key industry peers to Engelhard. Engelhard believes that its standalone forward P/E multiple should reflect a relationship to key industry peers more in

line with historical levels.

(1) See page 50 for derivation.

(2) Applied Johnson Matthey’s long-term projected annual EPS growth rate of 8.0% based on Wall Street research to 2007 EPS of Johnson Matthey to drive 2010 forward P/E

multiple of 13.8x. Applied Umicore’s long-term projected annual EPS growth rate of 10.1% based on Wall Street research to 2007 EPS of Umicore to drive 2010 forward P/E

multiple of 11.6x. Price as of April 21, 2006.

Based on 2010P EPS

Based on 2007P EPS

3 Year Average Discount (1)

1 Year Average Premium (1)

(3 Year Average Premium: 19.3%)

Blended Price Per

Hypothetical

Resultant

Implied Price Per

Share Assuming Pro

Engelhard

2007 P/E

Share Based on

Rata Participation in

Premium/(Discount)

Multiple

$2.55 Projected EPS

Self Tender

Engelhard Relative to

Johnson Matthey

(6.9%)

16.0

$40.87

$41.70

(JM Currently at 17.2x)

Engelhard Relative to

Umicore

6.8%

16.6

$42.24

$42.80

(Umicore Currently at 15.5x)

Blended Price Per

Hypothetical

Resultant

Implied Price Per

Share Assuming Pro

Engelhard

2010 Forward

Share Based on

Rata Participation in

Premium/(Discount)

P/E Multiple

(2)

$4.22 Projected EPS

Self Tender

Engelhard Relative to

Johnson Matthey

(6.9%)

12.8

$54.13

$52.29

(JM Currently at 13.8x)

Engelhard Relative to

Umicore

6.8%

12.4

$52.33

$50.85

(Umicore Currently at 11.6x)

51

Recapitalization Plan

Required Stock Price and ’07 P/E to Deliver Hypothetical Blended Values of $38-$45

Per Share

Based on 2007 EPS of $2.55

2007 P/E Multiple Analysis – Current Multiples (1)

LT Proj. EPS

Growth Rate (1)

10.5%

8.0%

10.0%

10.0%

10.0%

10.0%

10.1%

7.7%

9.5%

10.0%

14.2x

B/E ’07P/E

(1)

Based on Wall street research average 2007 EPS projections and stock price. Average long-term projected EPS growth rate per First Call as of April 21, 2006.

Engelhard First Call LT Proj. EPS Growth:

Engelhard Operating Plan LT Proj. EPS Growth (’05-’10):

Pro Forma for Recap:

10%

14%

14%+

17.6x

17.5x

17.2x

16.2x

15.5x

15.3x

15.0x

14.7x

14.5x

14.4x

10.0x

12.0x

14.0x

16.0x

18.0x

20.0x

Praxair

Air Products

Johnson

Matthey

Sigma-

Aldrich

Umicore

Albemarle

Rohm & Haas

Cytec

IFF

Du Pont

Hypothetical

Required

Implied

Blended Value

Stock Price

2007 P/E

38.00

36.24

14.2x

39.00

37.49

14.7x

40.00

38.74

15.2x

41.00

39.99

15.7x

42.00

41.24

16.2x

43.00

42.50

16.7x

44.00

43.75

17.2x

45.00

45.00

17.6x

52

V. Concluding Remarks

Concluding Remarks

Proxy Process and Annual Meeting Highlights

Proxy Process:

In Proxy Statement, among other things, Engelhard announces Board of Directors to expand Board by 3 seats

at the Annual Meeting

Engelhard names nominees for those intended seats

BASF will also have opportunity until close of business on May 8, 2006 to name 3 additional nominees;

Engelhard willing to consider reasonable extension to the extent BASF determines it needs a longer period of

time to name additional nominees

Engelhard Annual Meeting:

Proxies tabulated – shareholders supporting Engelhard can submit proxies for Engelhard’s 5 director nominees

(two Class 1 directors whose terms expire plus Engelhard nominees to fill 3 vacancies to be created)

Shareholders preferring BASF Offer can submit proxies in support of BASF’s nominees

Self Tender Offer:

Would close post-shareholder meeting unless:

BASF’s nominees constitute a majority of the Board and a majority of the Board determines not to proceed

with self tender offer

Engelhard recommends acceptance of an amended Tender Offer that BASF may choose to make

Engelhard approves a transaction that it determines is a superior alternative to the Recapitalization Plan

Other customary closing conditions (including financing) are not satisfied or waived

Shareholder Choice: Recapitalization Plan or BASF Offer

54

Concluding Remarks

Recapitalization Plan Highlights and Board Recommendation

The Recapitalization Plan should deliver value superior to BASF’s $38.00 per share proposal

Accretion to EPS and EPS growth commencing in 2007

Expected strong forward price to earnings (P/E) multiple

Provides meaningful liquidity to Engelhard shareholders at an attractive price of $45.00 per share

Offers Engelhard shareholders the ability to participate in Engelhard’s strengthening business

prospects and realize the Company’s future growth potential through appreciation of the market

price of the stock or a future sale of the Company

Maintains investment grade credit profile

The Board unanimously recommends that shareholders:

Vote for the five Engelhard director nominees

Tender into the Company’s $45 per share tender offer

55

Appendix

Environmental Technologies

Light Duty Vehicles

• Light duty vehicle builds will grow globally at 2% over the plan period, from 62 million vehicles in 2005 to 68 million by 2010, driven primarily by increasing living

standards in emerging markets.

• N. America with strictest regulation and largest engines averages almost three catalysts per vehicle. Europe, with increasing penetration rates of catalyzed

soot filters (CSF) will increase to slightly over two catalysts per vehicle. Tightening regulatory standards in developing countries will bring the average in these

regions up to one catalyst per vehicle.

• Increasingly strict regulatory standards and fluctuating precious metal pricing will require more advanced technology with related value pricing.

• Net effect of the above is that the global market for light duty emission control catalysts will grow at a 5% CAGR, from $1.5B in 2005 to $1.9B by 2010. Of the

$1.9B in 2010, $1.4B relates to gasoline with the remaining $0.5B relating to light-duty diesel, primarily in Europe.

• Gasoline:

1. Global segment will grow from 103M catalysts in 2005 to 115M by 2010, a 2.2% CAGR, with an average catalyst manufacturing charge of $12/catalyst.

2. N. America and Europe will show minimal growth with Japan and Korea flat. Most of the growth will come from emerging markets, led by China.

3. Stricter regulations will be adopted in the emerging markets over the plan period. China and India will begin Euro 3 this year and Euro 4 by 2008-10. Brazil

will adopt a US Tier 2 program in 2009. Russia will begin to implement Euro 2 this year and Euro 3 by 2008.

• Light-duty Diesel:

1. Europe, which accounts for 75% of the market, will grow from 9.4M vehicles in 2005 to almost 12M by 2010, a 5% CAGR. A large percentage of the

remaining 25% is produced in Japan and Korea for export into Europe.

2. The biggest driver for this growth is the diesel penetration rate growing from 46% this year to 50% by 2010.

3. The catalyst market for light-duty diesels in Europe is currently forecasted to be almost $400M by the end of 2010. The largest growth opportunity is the

accelerated adoption rate of CSF’s.

4. Euro 4, which began phasing in 2004 (2005 new platforms) has not been filter (CSF) forcing. However, several European countries became aware that

ambient air quality standards were being exceeded in urban areas, primarily due to particulate matter. Driving restrictions on unfiltered vehicles were

discussed as a possible solution which prompted OEM’s to “voluntarily” install filters.

5. Awareness of particulate matter has forced the EU to accelerate the adoption of Euro 5 for light-duty diesel (now projected for 2009). Euro 5 reduces

particulate emissions by 80% vs. Euro 4 and will be filter forcing for a majority of diesel vehicles.

6. Grow Engelhard’s market share in Europe from 24% to 35% by 2008.

Note: Based on Engelhard Management Operating Plan estimates developed August, 2005.

Appendix

Financial Assumptions

Key Assumptions

57

Environmental Technologies (Cont’d)

Heavy-Duty Diesel (HDD)

• HDD engine demand will increase only 1% per year, from 1.6M engines in 2005 to 1.7M engines in 2010 in the U.S., Europe and Japan.

• However, tightening regulations will increase the catalyst market from 1.4M units in 2005 to 5M units in 2010.

• Market Revenues (ex-PGM/ex-substrate) are projected to grow from $100M in 2005 to $330M-$370M in 2010.

• For On-Road, US 2007 & 2010, Euro 4 & 5 and Japan 2005 & 2009 are “On Track” for implementation.

• Successful fleet testing of US07 emission systems in 2006.

• Non-vanadium SCR will be required in US, Europe and Japan.

• European tax incentive programs will drive early adoption of CSF’s.

• New off-road regulations begin in 2008 and are not included in sales or earnings estimates.

Stationary Source

• The Food Service market will grow from $3M in 2005 to $10M in 2010 driven by pending charbroiler regulations (2007). Addresses fine particulate control and health and safety

benefits for ventless ovens.

• Successful development of differentiated mercury sorbent technology for coal-fired power plants assumed for 2008-2010.

Temperature Sensing

• Market will grow from $225M in 2005 to $300M in 2010, a CAGR of 6%.

• Engelhard will improve on its 8% market share through three growth strategies:

1. Accelerate optical thermometry commercialization by penetrating new markets.

2. Continue Asia geographic expansion.

3. Add wafer thermocouple technology to complete Engelhard temperature measurement portfolio.

Note: Based on Engelhard Management Operating Plan estimates developed August, 2005.

Appendix

Financial Assumptions

Key Assumptions

58

Appendix

Financial Assumptions

Key Assumptions

Process Technologies

Chemicals

• Gas Economy catalyst market forecast to approximate $350M in 2006 with a CAGR of 15%.

• Additional Gas Economy catalyst growth from:

1. Planned expansion from current “gas-to-liquids” (GTL) customer.

2. Leveraging Fischer-Tropsch catalyst technology to other major GTL players.

3. Leverage our syngas position from Nanjing acquisition.

• Successful entry into unserved petrochemical markets, including ethane based styrene, ethane based acetic acid, propane based acrylic acid and propane based propylene

oxide, based on current commercial agreements.

• Growth rates for catalyst markets for oleochemicals, petrochemicals and fine chemicals range from 2% to 10%.

Petroleum Refining

• FCC additives growth approximating 22%:

1. Underlying market growth of 10%.

2. Additional growth from the expansion into environmental and gasoline conversion additive technologies to meet increasing global demands of propylene and petrochemical

feedstocks and regulatory compliance.

• Entry into new refining market areas by leveraging Engelhard technology through prospective licensing agreements, including hydrocracking, deep catalytic cracking and

reforming.

• FCC market growth only projected at 2% with additional income from productivity gains.

• Natural gas price used was $7.25 per MMBTU. Adverse variances are expected to be substantially covered by surcharges and other pricing actions.

Polyolefins

• Polypropylene growth approximating 26%:

1. Assumed growth of 7% in proprietary catalyst representing underlying market growth of 5-6% and remaining growth through differentiation and acceleration of our technology

development into the packaging and film markets.

2. Growth in volume from new licenses.

• Continuation of entry into polyethylene market.

Note: Based on Engelhard Management Operating Plan estimates developed August, 2005.

59

Appendix

Financial Assumptions

Key Assumptions

Appearance and Performance Technologies

Personal Care Materials

• 7% growth per year in delivery systems for personal care through 2009. In the case of commodity vitamins (30% of market) where Engelhard does not participate, the rate is 5%.

For more specialized actives, such as unique extracts from plants, the growth rate is closer to 10%.

• Additional sales/earnings from expanding the product offerings globally from the acquisitions made in the U.S. and France in 2004 and 2005.

• Additional earnings from optimizing synergies in technology, manufacturing and sales as Engelhard continues to integrate the two acquisitions.

Effects

• Market for effect pigments in cosmetics and personal care will grow at 7% per year. The market growth rate for industrial applications will be 4-5%. Growth in the automotive

market will be lower.

• Expanding Engelhard’s innovation track into new programs beyond mica and borosilicate glass, bismuth and film by focusing R&D on technology platforms and away from line

extensions will add $15M to sales.

• Cost reductions will add $10M to earnings by 2010.

• Faster innovation and an applications lab in China will work to counter Chinese competition, as well as pay attention to costs.

Kaolin

• Recover $10M in sales and $4M in earnings from strikes in Finland and Canada.

• $20M in sales in 2010 from Décor Growth Program (decorative laminate paper market with substitution for TiO2).

• Crop Protectants (Surround) will add $32M of sales and $10M of earnings by 2010.

• Cost reduction initiatives will add $12M in earnings.

• Natural gas price used was $7.25 per MMBTU. Adverse variances are expected to be substantially covered by surcharges and other pricing actions.

Note: Based on Engelhard Management Operating Plan estimates developed August, 2005.

60

Appendix

Financial Assumptions

Key Assumptions

Ventures

Alumina business acquired in 2005 accounts for $12M of 2010 operating earnings with modest growth rates.

• Frac Sand accounts for $9M of 2010 operating earnings and depends mostly on continued demand from the energy sector.

• Aseptrol/Water Treatment are slated to generate $7M of operating earnings related to health requirements.

• Nothing included in sales and earnings for Ceramic Proppants and Battery Materials programs.

Corporate

• Share buy-back programs, enabled by operating cash flows, will offset the dilutive impact of equity-based awards under employee benefit plans. Diluted shares outstanding for

Operating Plan period are 122 million.

Share buy-back programs, enabled by operating cash flows, will offset the dilutive impact of equity-based awards under employee benefit plans. Diluted shares outstanding post-

recapitalization plan are 101 million.

• The average effective tax rate for the Operating Plan period on a standalone basis is 24%, with the 2010 period at 25%.

The average effective tax rate post-recapitalization is 25% with the 2010 period at 26%.

• Equity earnings from the Company’s equity method joint ventures, which primarily serve the Japanese and Korean automotive catalyst markets, have conservatively been held

constant throughout the plan period, despite a 25% CAGR over the past three years.

Note: Based on Engelhard Management Operating Plan estimates developed August, 2005, except post-recapitalization items as noted.

61