FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Dated February 2, 2022

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

Aktiebolaget Svensk Exportkredit

Swedish Export Credit Corporation

(Translation of Registrant’s Name into English)

Klarabergsviadukten

61-63

SE-101 23 Stockholm

Sweden

(Address of Principal Executive Offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

| Form 20-F x | Form 40-F ¨ |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): N/A

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): N/A

Indicate by check mark whether by furnishing the information contained in this Form, the registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

| Yes ¨ | No x |

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): N/A

Incorporation by Reference

This Report on Form 6-K, including the exhibits hereto, is hereby incorporated by reference, in its entirety, into the registration statement on Form F-3 (File No. 333-249829) of Aktiebolaget Svensk Exportkredit (publ) (“SEK”).

This Report comprises the following:

| 1. | Registrant’s report for the fourth quarter of 2021. |

| 2. | Table of unaudited consolidated capitalization of the Registrant (attached as Exhibit 99.2 hereto). |

1

AB Svensk Exportkredit

Swedish Export Credit Corporation

Year-end Report 2021

January-December 2021

2

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this Report to be signed on its behalf by the undersigned, thereunto duly authorized.

Dated: February 2, 2022

| AB Svensk Exportkredit | ||

| (Swedish Export Credit Corporation) | ||

| By: | /s/ Magnus Montan | |

| Magnus Montan, Chief Executive Officer | ||

3

| AB Svensk Exportkredit Swedish Export Credit Corporation |

January-December 2021

(Compared to the period January-December 2020)

| Net interest income Skr 1,907 million (2020: Skr 1,946 million) |

| Operating profit Skr 1,305 million (2020: Skr 1,238 million) |

| Net profit Skr 1,034 million (2020: Skr 968 million) |

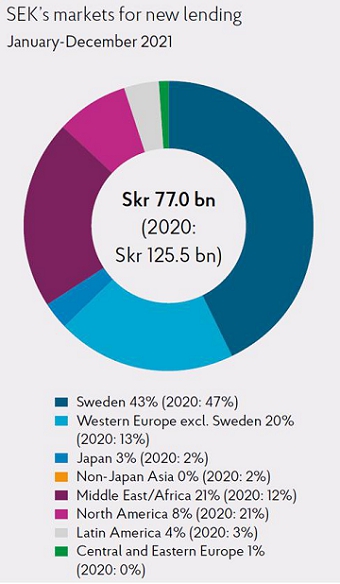

| New lending Skr 77.0 billion (2020: Skr 125.5 billion) |

| Volume of green bonds issued Skr 6.1 billion (2020: 5.1 billion) |

| Basic and diluted earnings per share Skr 259 (2020: Skr 243) |

| After-tax return on equity 5.1 percent (2020: 4.9 percent) |

Fourth quarter of 2021

(Compared to the fourth quarter of 2020)

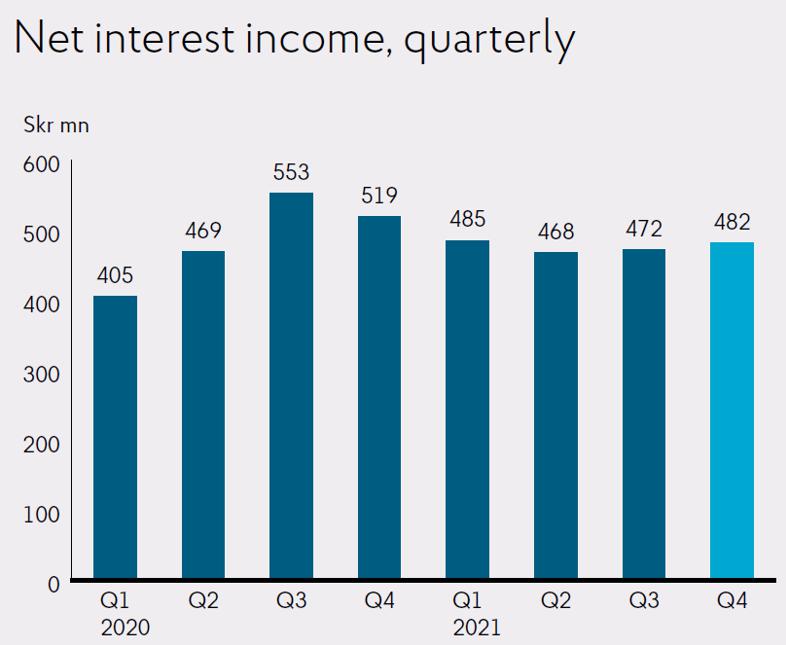

| | Net interest income Skr 482 million (4Q20: Skr 519 million) |

| | Operating profit Skr 300 million (4Q20: Skr 436 million) |

| | Net profit Skr 236 million (4Q20: Skr 341 million) |

| | New lending Skr 26.6 billion (4Q20: Skr 18.6 billion) |

| | Volume of green bonds issued Skr - billion (4Q20: 1.6 billion) |

| | Basic and diluted earnings per share Skr 59 (4Q20: Skr 86) |

| | After-tax return on equity 4.6 percent (4Q20: 6.9 percent) |

Equity and balances

(Compared to December 31, 2020)

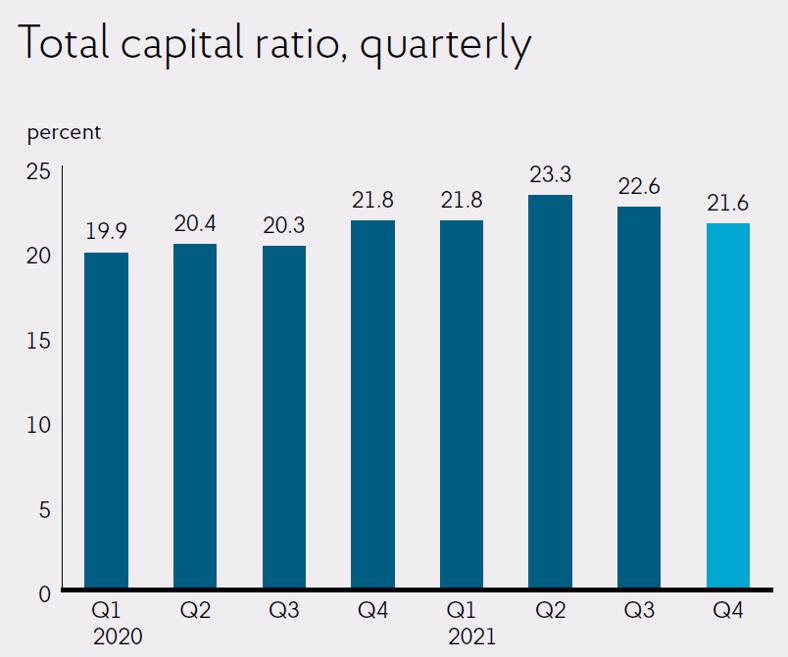

| | Total capital ratio 21.6 percent (year-end 2020: 21.8 percent) |

| | Total assets Skr 333.6 billion (year-end 2020: Skr 335.4 billion) |

| | Loans, outstanding and undisbursed Skr 291.1 billion (year-end 2020: Skr 288.9 billion) |

| | Proposed ordinary dividend Skr 414 million (year-end 2020: Skr 290 million) |

| Year-end Report 2021 | Page 2 of 29 |

Increased client activity in the fourth quarter

In the fourth quarter, SEK has noted increased demand for financing of major transition projects in Sweden and internationally, particularly within energy, infrastructure, hospitals and water treatment. The need for transition projects in developing countries is substantial, particularly when it comes to projects with a social impact.

In the fourth quarter, SEK closed its first transaction within the framework of social loans, an export credit of EUR 186 million, with SEK financing the renovation and new build of two specialist hospitals in Ghana. Several Swedish companies are supplying products and expertise for the project. The hospitals are expected to provide high-quality specialist care that will improve the lives of a great number of people in the communities they serve. Conducting business in developing countries with complex regulatory environments can be challenging, but SEK is working intensely to support projects in the region.

In the fourth quarter, net interest income increased compared with the preceding quarter. Client activity increased and we reached a new lending volume of Skr 27 billion compared with Skr 12 billion in the preceding quarter. Return on equity amounted to 4.6 percent, a decline compared with the preceding quarter, which was the result of higher costs for adapting to regulations and higher provisions for expected credit losses compared with the third quarter.

During the quarter, we have continued efforts to review SEK’s strategic direction and to prepare our business plan for 2022–2024. We will strive to increase our income base and grow in terms of the number of clients and total outstanding client exposures. We will also look to deepen relationships and broaden the scope of business with existing clients and create new business opportunities through partnerships and collaboration. We will efficiently create more value for more exporters.

SEK has implemented organizational changes with the aim of working more strategically and advancing our position in the area of sustainability. For example, SEK resolved to establish a new function, Sustainability, the manager of which is part of the executive management team. Our aim is for sustainable finance to become an equally natural part of SEK’s brand as international financing is today. Another new function is Strategy, Business Development and Communication, which is responsible for the company’s strategic business development.

For the full-year, we recorded a somewhat lower net interest income, Skr 1,907 million compared with SEK 1,946 million for last year. We reached a new lending volume of Skr 77 billion compared with Skr 125 billion. This decline compared with the previous year is attributable to the extraordinarily high levels of lending in 2020, when many companies secured their financing needs in the early stages of the COVID-19 pandemic, to help strengthen their liquidity position. Since provisions for expected credit losses were lower than the preceding year, we recorded a higher net profit for the full year, Skr 1,034 million compared with Skr 968 million for last year.

During the almost two years that have passed since the beginning of the COVID-19 pandemic, SEK has supported our clients’ increased financing requirements, while retaining a strong financial position. Our capitalization exceeds the requirements of the Finansinspektionen (the Swedish FSA) as well as the company’s capital target, and we have continually maintained high liquidity while retaining a match funded balance sheet.

Magnus Montan

Chief Executive Officer

| Year-end Report 2021 | Page 3 of 29 |

Increasing demand for working capital and export credits

SEK recorded a relatively strong fourth quarter with company lending amounting to Skr 26.6 billion (2020: Skr 18.6 billion). Demand for financing has been positively impacted by a favorable economic trend, generally higher acquisition activity, and strong demand for export and project credits.

Following limited demand for working capital from Swedish exporters during the first half of the year, lending increased during the second half of the year. Working capital for the fourth quarter amounted to Skr 8.5 billion (4Q20: Skr 6.5 billion), which is higher compared with the same period in the previous year.

Export credits and Trade Finance also performed well in the final quarter of the year. The company has financed Skr 9.2 billion in export credits to, for example Turkey, Zambia, Burkina Faso and Ghana.

Some transactions have been delayed due to component shortages and delivery disruptions. The spread of the COVID-19 pandemic has also limited opportunities to meet clients and business partners. Despite this, the number of clients has increased by 11 percent in 2021.

In 2021, SEK prepared two new offerings in sustainable finance: a social loan and a sustainability-linked loan. One example of a sustainability-linked transaction in the fourth quarter was the lending of EUR 55 million in working capital to the industrial group Axel Johnson International, which develops and acquires technology companies in strategic niche markets. The loan is related to Axel Johnson International’s sustainability target that aims to increase its share of renewable electricity as well as energy-efficiency enhancements in own operations and internal transportation. If the target is achieved, a lower interest rate will apply for the borrower.

| SEK’s new lending | ||

| Skr bn | Jan-Dec 2021 | Jan-Dec 2020 |

| Lending to Swedish exporters1 | 25.1 | 62.2 |

| Lending to exporters’ customers2 | 51.9 | 63.3 |

| Total | 77.0 | 125.5 |

| CIRR loans as percentage of new lending | 15% | 15% |

| 1 | Of which Skr 2.6 billion (year-end 2020: Skr 1.1 billion) had not been disbursed at period end. |

| 2 | Of which Skr 18.6 billion (year-end 2020: Skr 17.9 billion) had not been disbursed at period end. |

| Year-end Report 2021 | Page 4 of 29 |

|

Borrowing volume back to pre-pandemic level

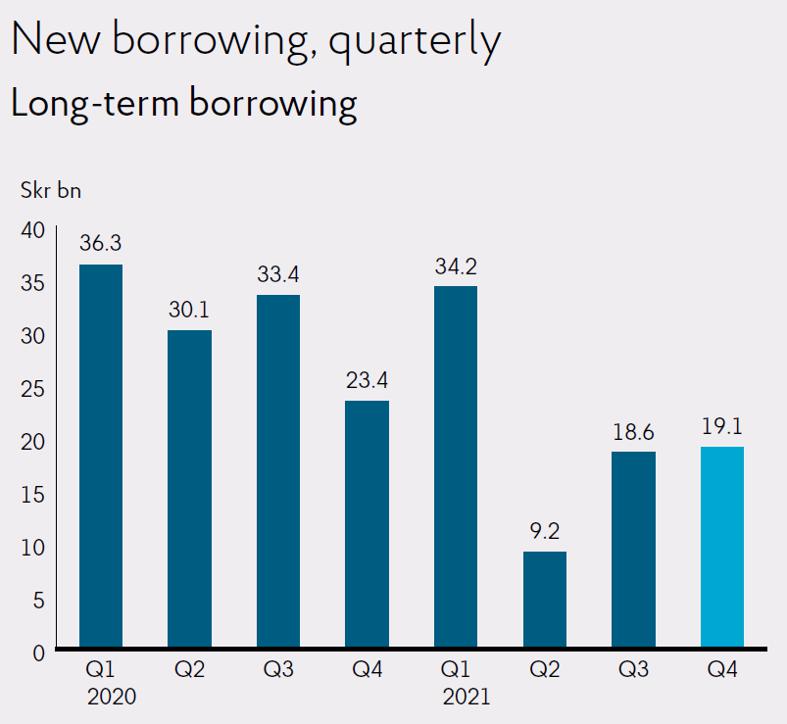

After a substantial increase in borrowing requirements in 2020 due to increased customer demand largely driven by the COVID-19 pandemic, SEK’s need to raise long-term financing normalized in 2021. Over the course of the year, SEK raised borrowings corresponding to Skr 81.1 billion with maturities of at least one year, compared with Skr 123.2 billion in 2020. The borrowing volume in the fourth quarter of 2021 was Skr 19.1 billion.

In the fourth quarter, SEK conducted a public offering of a USD 1.25 billion two-year fixed rate bond. Similar to SEK’s previous benchmark notes offerings, the bond was marketed and priced against SOFR (Secured Overnight Financing Rate) instead of LIBOR, in accordance with the standard that is being developed in the market. As part of the efforts to adopt to SOFR and replacing LIBOR, SEK also issued a new global bond tranche of USD 350 million of its USD 700 million bond with a SOFR-based floating interest rate, which increased its value outstanding to USD 1.05 billion.

The volume of new structured debt in 2021 remained at the same level as 2020, but increased as a share of total new borrowing from 13 percent in 2020 to 20 percent in 2021.

In furtherance of SEK’s commitment to sustainability, the company issued Skr 6.1 billion in green bonds during 2021.

SEK continues to have high liquidity for new lending and is well prepared to meet the future financing needs of the Swedish export industry.

| SEK’s borrowing | ||

| Skr bn | Jan-Dec 2021 | Jan-Dec 2020 |

| New long-term borrowing | 81.1 | 123.2 |

| Volume of green bonds issued during the period | 6.1 | 5.1 |

| Outstanding senior debt | 295.0 | 287.5 |

| Repurchase and redemption of own debt | 1.5 | 3.0 |

| Year-end Report 2021 | Page 5 of 29 |

January-December 2021

Operating profit amounted to Skr 1,305 million (2020: Skr 1,238 million). Net profit amounted to Skr 1,034 million (2020: Skr 968 million). The higher net profit compared with the previous year is mainly explained by lower provisions for expected credit losses. The lower provisions are partly attributable to the decrease of the reserve for expected credit losses that had been increased in connection with the COVID-19 pandemic.

Net interest income

Net interest income amounted to Skr 1,907 million (2020: Skr 1,946 million), a decrease of 2 percent compared to the previous year. The record high lending in 2020 has continued to have a positive impact on the company’s net interest income, albeit now decreasing. SEK has noted a stabilization of net interest income at a somewhat lower level. This is due in part to the fact that some short-term working capital financing that was raised at relatively high interest rates at the start of the COVID-19 pandemic has matured.

The table below shows average interest-bearing assets and liabilities.

| Skr bn, average | Jan-Dec 2021 | Jan-Dec 2020 | Change |

| Total loans | 234.5 | 224.6 | 4% |

| Liquidity investments | 63.5 | 61.4 | 3% |

| Interest-bearing assets | 314.2 | 305.5 | 3% |

| Interest-bearing liabilities | 291.2 | 280.2 | 4% |

Net results of financial transactions

Net results of financial transactions amounted to Skr 56 million (2020: Skr 83 million) mainly due to early loan redemptions and unrealized value changes in derivatives. Although the volatility in the fixed income market was relatively high during the period, the company’s risk hedging strategies have worked well and the volatility in the company’s net results of financial transactions has been kept low.

Operating expenses

Operating expenses amounted to Skr -670 million (2020: Skr -596 million), an increase of 12 percent compared to the previous year. The increase in operating expenses is mainly due to write-downs of intangible assets, but also increased costs for regulatory compliance adaption of operations. No provision was made for the individual variable remuneration program (2020: Skr 8 million).

Net credit losses

Net credit losses amounted to Skr 41 million (2020: Skr -153 million). Net credit losses were primarily attributable to decreased provisions for expected credit losses for exposures in stage 1 and stage 2, partly offset by increased provisions for expected credit losses for exposures in stage 3. The decrease in provisions for stage 1 and stage 2 was largely attributable to a gradual decrease of the reserve for expected credit losses that had been increased in connection with the COVID-19 pandemic. In 2021, SEK incurred losses of Skr 52 million

on exposures as to which provisions had already largely been taken.

SEK’s IFRS 9 model is based on GDP growth projections estimating the impact on the probability of default. SEK’s management believes the model underestimates the probability of default within the asset portfolio, see Note 4. Although the recovery has been faster than expected, SEK has made an overall adjustment accordingly.

Loss allowances as of December 31, 2021, amounted to Skr -164 million compared to Skr -249 million as of December 31, 2020, of which exposures in stage 3 amounted to Skr -48 million (year-end 2020: Skr -46 million).

The provision ratio amounted to 0.06 percent (year-end 2020: 0.08 percent).

Taxes

Tax costs amounted to Skr -271 million (2020: Skr -270 million), and the effective tax rate amounted to 20.8 percent (2020: 21.8 percent).

Other comprehensive income (OCI)

Other comprehensive income before tax amounted to Skr 0 million (2020: Skr 19 million). The outcome is explained by a positive result related to the revaluation of defined benefit plans, which was affected by a higher discount rate, and offset by a negative result from changes in own credit risk.

October-December 2021

Operating profit for the fourth quarter amounted to Skr 300 million (4Q20: Skr 436 million). Net profit amounted to Skr 236 million (4Q20: Skr 341 million). The decrease in profit compared to the same period in the previous year was partly attributable to lower net interest income and lower net results of financial transactions, but also to higher operating expenses.

Net interest income

Net interest income amounted to Skr 482 million (4Q20: Skr 519 million), a decrease of 7 percent compared to the same period in the previous year. Even though the preceding year’s high volume of new lending had a positive effect on the company’s net interest income, SEK has noted a stabilization of net interest income in the fourth quarter at a somewhat lower level. This is due in part to the fact that some short-term working capital financing that was raised at relatively high interest rates at the start of the COVID-19 pandemic has matured.

The table below shows average interest-bearing assets and liabilities.

| Skr bn, average | Oct-Dec 2021 | Oct-Dec 2020 | Change |

| Total loans | 233.0 | 239.4 | -3% |

| Liquidity investments | 64.2 | 68.9 | -7% |

| Interest-bearing assets | 308.2 | 328.2 | -6% |

| Interest-bearing liabilities | 291.2 | 306.3 | -5% |

| Year-end Report 2021 | Page 6 of 29 |

Net results of financial transactions

Net results of financial transactions amounted to Skr 41 million (4Q20: Skr 87 million) mainly due to unrealized value changes in derivatives. Volatility in the fixed income market was relatively high during the period, but the company’s risk hedging strategies have worked well and the volatility in the company’s net results of financial transactions has been kept low.

Operating expenses

Operating expenses amounted to Skr -208 million (4Q20: Skr -163 million), an increase of 28 percent compared to the same period in the previous year. The increase is partly explained by the write-downs of intangible assets during the fourth quarter. The costs associated with regulatory compliance have also increased during the period compared to the same period in the previous year.

All provisions made for the individual variable remuneration program during the year were released during the fourth quarter, since no such remuneration will be paid out for 2021 (4Q20: Skr 2 million).

Net credit losses

Net credit losses amounted to Skr -9 million (4Q20: Skr 7 million). Net credit losses were primarily attributable to established losses on exposures in stage 3 that had not been fully reserved, but also to increased provisions for expected credit losses for exposures in stage 1.

SEK’s IFRS 9 model is based on GDP growth projections estimating the impact on the probability of default. SEK’s management believes the model underestimates the probability of default within the asset portfolio, see Note 4. SEK has made an overall adjustment accordingly.

Taxes

Tax costs amounted to Skr -64 million (4Q20: Skr -95 million), and the effective tax rate amounted to 21.3 percent (4Q20: 21.8 percent).

Other comprehensive income (OCI)

Other comprehensive income before tax amounted to Skr -10 million (4Q20: Skr 25 million) due to a negative result from the revaluation of defined benefit plans. This result was partly offset by positive results related to changes in own credit risk.

Statement of Financial Position

Total assets and liquidity investments

Total assets decreased by 1 percent compared to the end of 2020.

| Skr bn | December 31, 2021 | December 31, 2020 | Change |

| Total assets | 333.6 | 335.4 | -1% |

| Liquidity investments | 67.9 | 59.2 | 15% |

| Total loans | 237.2 | 231.7 | 2% |

| of which loans in the CIRR-system | 87.9 | 69.2 | 27% |

SEK’s total net exposures, after risk mitigation, amounted to Skr 372.5 billion as of December 31, 2021 (year-end 2020: Skr 359.5 billion). Credit exposures have increased to financial institutions, which is mainly due to the increase in liquidity investments.

Liabilities and equity

As of December 31, 2021, the aggregate volume of available funds and shareholders’ equity exceeded the aggregate volume of loans outstanding and loans committed at all maturities. SEK considers all of its outstanding commitments to be covered through maturity.

SEK has a credit facility in place with the Swedish National Debt Office of up to Skr 200 billion, of which Skr 10 billion was utilized as of December 31, 2021. The Skr 10 billion draw was made in March of 2020, at the start of the COVID-19 pandemic, to ensure coverage of the increased demand from clients that arose. The credit facility can be utilized when the Swedish export industry’s demand for financing is particularly high.

Capital adequacy

As of December 31, 2021, SEK’s total own funds amounted to Skr 19.9 billion (year-end 2020: Skr 19.5 billion). The total capital ratio was 21.6 percent (year-end 2020: 21.8 percent), representing a margin of 5.9 percentage points above SEK’s estimate of Finansinspektionen’s (the Swedish FSA) requirement of 15.7 percent as of December 31, 2021. The corresponding Common Equity Tier 1 capital estimated requirement was 10.6 percent. Given that SEK’s own funds are comprised solely of Common Equity Tier 1 capital, this total capital ratio represents a margin of 11.0 percentage points above the requirement. Overall, SEK is strongly capitalized and has healthy liquidity.

The leverage ratio has improved compared to the end of 2020, primarily as the result of the Capital Requirements Regulation (CRRII) (EU Regulation 2019/876) that entered into force on June 28, 2021. The regulation has introduced changes to the bases of calculation for the ratio in which certain exposures are no longer included.

The liquidity coverage ratio (LCR) is in line with the liquidity at the end of 2020. The LCR ratio varies during the year due to the volatility of inflows and outflows, and is a normal aspect of SEK’s business.

| Percent | December 31, 2021 | December 31, 2020 |

| Common Equity Tier 1 capital ratio | 21.6 | 21.8 |

| Tier 1 capital ratio | 21.6 | 21.8 |

| Total capital ratio | 21.6 | 21.8 |

| Leverage ratio1 | 9.3 | 5.8 |

| Liquidity coverage ratio (LCR) | 463 | 447 |

| Net stable funding ratio (NSFR) | 139 | 135 |

| 1 | In the second quarter of 2021, SEK changed its methodology for calculating the Leverage ratio to comply with new regulatory requirements (CRRII). Comparative figures have not been recalculated. |

| Year-end Report 2021 | Page 7 of 29 |

Rating

| Skr | Foreign currency | |

| Moody’s | Aa1/Stable | Aa1/Stable |

| Standard & Poor’s | AA+/Stable | AA+/Stable |

Dividend

The Board of Directors has resolved to propose the payment of a dividend of Skr 414 million (2020: Skr 290 million) at the company’s annual general meeting, corresponding to 40 percent of the year’s profit, which is in line with the company’s dividend policy of 20-40 percent.

Other events

At SEK’s annual general meeting on March 24, 2021, Lennart Jacobsen was elected as a new member of the Board of Directors of SEK (the “Board”). After ten years of service, Ulla Nilsson and Cecilia Ardström stepped down from their respective positions as members of the Board. A resolution passed at the annual general meeting to adopt the income statement and balance sheet in the Annual and Sustainability Report 2020, and to appropriate distributable funds pursuant to the Board’s proposal. Resolutions were also passed at the annual general meeting relating to the company’s financial goals. The profitability target was changed from 6 percent to 5 percent return on equity after tax. The change was the result of lower central bank policy rates. Furthermore, the dividend policy was changed from the previous 30 percent dividend to a 20-40 percent dividend range of the year’s profit with the aim of increasing the company’s flexibility with respect to capitalization. The company’s capital target was left unchanged.

Catrin Fransson stepped down as CEO of SEK on July 15, 2021, at her own request. On May 3, 2021, Magnus Montan was appointed as the new CEO of SEK, and assumed his new office on July 16, 2021.

In 2021, SEK implemented a number of organizational changes to meet customer requirements more efficiently. The Large Corporates and Mid Corporates functions have been replaced by the Customer Relations and Structured Finance functions, and the new Strategy, Business Development and Communication function was created. SEK also resolved to establish a new function, Sustainability, the manager of which is to be part of the executive management team.

In the fourth quarter of 2021, SEK moved to a new office at Fleminggatan in Stockholm.

Risk factors and the macro environment

Various risks arise as part of SEK’s operations, primarily credit risks, but also market, liquidity, re-financing, operational and sustainability

risks. For a more detailed description of these risks, refer to the separate risk report Capital Adequacy and Risk Management Report Pillar 3 2020 and Note 29 to the annual financial statements included in SEK’s 2020 Annual Report on Form 20-F, as well as the “Risk Factors” section in SEK’s 2020 Annual Report on Form 20-F.

According to Statistics Sweden, the annualized rate of Swedish GDP growth was 4.7 percent in the third quarter of 2021 and the unemployment rate was 8.3 percent as of November 2021. The consumer price index rose 3.3 percent on an annualized basis in November 2021 and the repo rate remained unchanged at zero percent.

Energy shortages, a rising inflation outlook and disrupted supply chain logistics have dominated the news in the fourth quarter. Following the positive outlook regarding the impact of the COVID-19 pandemic in the third quarter, perhaps particularly in Europe and the US, the spread of infection increased during the second half of the fourth quarter. About 75 percent of the adult population of the western world is now vaccinated, which is why the effect on society is not as extreme as before. Vaccination rates have not reached the same levels in other parts of the world – despite the apparent increased vaccination rates by the end of 2021 – leaving those parts of the world more vulnerable. However, closures of societal functions are less widespread than during previous waves of high COVID-infection rates, which is why the impact on real economies has been limited.

Overall, there have been strong macro-economic indicators in the fourth quarter in the form of strong stock markets and rising long-term interest rates, higher inflation expectations, and expected constraints from the central banks. The US central bank, the Federal Reserve, is indicating up to three interest-rate hikes in 2022, a considerable U-turn in only a few months.

The substantial adverse effect that the COVID-19 pandemic had on Swedish exports during the first half of 2020 has largely been reversed. The challenges that the export industry faced in the fourth quarter have concerned material shortages and logistics problems rather than limitations directly related to the current restrictions due to COVID-19. Industry order intake in Sweden declined by 0.9 percent between October and November, and Business Sweden’s Export Managers’ Index rose 1.5 points to 67.6 in the fourth quarter of 2021 compared with 66.1 for the preceding quarter.

The strong state of Sweden’s public finances, with low public debt, has allowed the use of fiscal stimuli. The Swedish state has implemented special measures to promote Swedish exports during the COVID-19 pandemic, and SEK’s role of securing financing for the Swedish export industry has become even clearer in the form of the expansion of the credit facility with the Swedish National Debt Office from Skr 125 billion to Skr 200 billion in June 2020. Since the more critical phase of the COVID-19 pandemic appears to be behind us, and economic growth is favorable, the credit facility has been revised to Skr 175 billion from January 2022.

| Year-end Report 2021 | Page 8 of 29 |

Financial targets

| Profitability target | A return on equity after tax of at least 5 percent. |

| Dividend policy | Payment of an ordinary dividend of 20-40 percent of the profit for the year. |

| Capital target | SEK’s total capital ratio is to exceed the Swedish FSA’s requirement by 2 to 4 percentage points and SEK’s Common Equity Tier 1 capital ratio is to exceed the Swedish FSA’s requirement by at least 4 percentage points. Currently, the capital targets mean that the total capital ratio should amount to 17.7-19.7 percent and the Common Equity Tier 1 capital ratio should amount to 14.6 percent, based on SEK’s estimation of the Swedish FSA’s requirements as of December 31, 2021. |

Key performance indicators (unaudited)

| Skr mn (if not otherwise indicated) | Oct-Dec 2021 | Jul-Sep 2021 | Oct-Dec 2020 | Jan-Dec 2021 | Jan-Dec 2020 |

| New lending | 26,565 | 12,356 | 18,574 | 76,988 | 125,470 |

| of which to Swedish exporters | 8,520 | 5,871 | 6,494 | 25,075 | 62,148 |

| of which to exporters’ customers | 18,045 | 6,485 | 12,080 | 51,913 | 63,322 |

| CIRR-loans as a percentage of new lending | 10% | 0% | 8% | 15% | 15% |

| Loans, outstanding and undisbursed | 291,095 | 279,598 | 288,891 | 291,095 | 288,891 |

| New long-term borrowings | 19,100 | 18,563 | 23,372 | 81,103 | 123,156 |

| Volume of green bonds issued during the period | - | 2,100 | 1,600 | 6,100 | 5,100 |

| Outstanding senior debt | 295,000 | 287,423 | 287,462 | 295,000 | 287,462 |

| After-tax return on equity | 4.6% | 6.3% | 6.9% | 5.1% | 4.9% |

| Proposed ordinary dividend | - | - | - | 414 | 290 |

| Common Equity Tier 1 capital ratio | 21.6% | 22.6% | 21.8% | 21.6% | 21.8% |

| Tier 1 capital ratio | 21.6% | 22.6% | 21.8% | 21.6% | 21.8% |

| Total capital ratio | 21.6% | 22.6% | 21.8% | 21.6% | 21.8% |

| Leverage ratio1 | 9.3% | 9.7% | 5.8% | 9.3% | 5.8% |

| Liquidity coverage ratio (LCR) | 463% | 1,399% | 447% | 463% | 447% |

| Net stable funding ratio (NSFR) | 139% | 141% | 135% | 139% | 135% |

| 1 | In the second quarter of 2021, SEK changed its methodology for calculating the Leverage ratio to comply with new regulatory requirements (CRRII). Comparative figures have not been recalculated. |

See definitions on page 30.

| Year-end Report 2021 | Page 9 of 29 |

Condensed Consolidated Statement of Comprehensive Income (unaudited)

| Skr mn | Note | Oct-Dec 2021 | Jul-Sep 2021 | Oct-Dec 2020 | Jan-Dec 2021 | Jan-Dec 2020 |

| Interest income | 703 | 678 | 737 | 2,719 | 4,108 | |

| Interest expenses | -221 | -206 | -218 | -812 | -2,162 | |

| Net interest income | 2 | 482 | 472 | 519 | 1,907 | 1,946 |

| Net fee and commission expense | -6 | -6 | -14 | -29 | -42 | |

| Net results of financial transactions | 3 | 41 | 23 | 87 | 56 | 83 |

| Other operating income | 0 | - | - | 0 | - | |

| Total operating income | 517 | 489 | 592 | 1,934 | 1,987 | |

| Personnel expenses | -96 | -76 | -95 | -359 | -347 | |

| Other administrative expenses | -66 | -49 | -56 | -231 | -198 | |

| Depreciation and impairment of non-financial assets | -46 | -11 | -12 | -80 | -51 | |

| Total operating expenses | -208 | -136 | -163 | -670 | -596 | |

| Operating profit before credit losses | 309 | 353 | 429 | 1,264 | 1,391 | |

| Net credit losses | 4 | -9 | 49 | 7 | 41 | -153 |

| Operating profit | 300 | 402 | 436 | 1,305 | 1,238 | |

| Tax expenses | -64 | -83 | -95 | -271 | -270 | |

| Net profit1 | 236 | 319 | 341 | 1,034 | 968 | |

| Other comprehensive income related to: | ||||||

| Items not to be reclassified to profit or loss | ||||||

| Own credit risk | 7 | -11 | -9 | -24 | 18 | |

| Revaluation of defined benefit plans | -17 | 6 | 34 | 24 | 1 | |

| Tax on items not to be reclassified to profit or loss | 2 | 1 | -5 | 0 | -5 | |

| Net items not to be reclassified to profit or loss | -8 | -4 | 20 | 0 | 14 | |

| Total other comprehensive income | -8 | -4 | 20 | 0 | 14 | |

| Total comprehensive income1 | 228 | 315 | 361 | 1,034 | 982 | |

| Skr | ||||||

| Basic and diluted earnings per share2 | 59 | 80 | 86 | 259 | 243 |

| 1 | The entire profit is attributable to the shareholder of the Parent Company. |

| 2 | Net profit divided by average number of shares, which amounts to 3,990,000 for each period. |

| Year-end Report 2021 | Page 10 of 29 |

Consolidated Statement of Financial Position (unaudited)

| Skr mn | Note | December 31, 2021 | December 31, 2020 |

| Assets | |||

| Cash and cash equivalents | 5 | 11,128 | 3,362 |

| Treasuries/government bonds | 5 | 10,872 | 22,266 |

| Other interest-bearing securities except loans | 5 | 45,881 | 33,551 |

| Loans in the form of interest-bearing securities | 4, 5 | 46,578 | 50,780 |

| Loans to credit institutions | 4, 5 | 20,775 | 31,315 |

| Loans to the public | 4, 5 | 180,288 | 171,562 |

| Derivatives | 5, 6 | 8,419 | 7,563 |

| Tangible and intangible assets | 331 | 145 | |

| Deferred tax asset | 11 | 15 | |

| Other assets | 7,451 | 12,853 | |

| Prepaid expenses and accrued revenues | 1,913 | 1,987 | |

| Total assets | 333,647 | 335,399 | |

| Liabilities and equity | |||

| Borrowing from credit institutions | 5 | 5,230 | 3,486 |

| Borrowing from the public | 5 | 10,000 | 10,000 |

| Debt securities issued | 5 | 279,770 | 273,976 |

| Derivatives | 5, 6 | 14,729 | 25,395 |

| Other liabilities | 1,167 | 455 | |

| Accrued expenses and prepaid revenues | 1,875 | 1,924 | |

| Provisions | 68 | 99 | |

| Total liabilities | 312,839 | 315,335 | |

| Share capital | 3,990 | 3,990 | |

| Reserves | -129 | -129 | |

| Retained earnings | 16,947 | 16,203 | |

| Total equity | 20,808 | 20,064 | |

| Total liabilities and equity | 333,647 | 335,399 |

| Year-end Report 2021 | Page 11 of 29 |

Condensed Consolidated Statement of Changes in Equity (unaudited)

| Skr mn | Equity | Share capital | Reserves | Retained earnings | |

Own credit risk | Defined benefit plans | ||||

| Opening balance of equity January 1, 2020 | 19,082 | 3,990 | -98 | -45 | 15,235 |

| Net profit Jan-Dec 2020 | 968 | 968 | |||

| Other comprehensive income Jan-Dec 2020 | 14 | 14 | 0 | ||

| Total comprehensive income Jan-Dec 2020 | 982 | - | 14 | 0 | 968 |

| Dividend | - | - | |||

| Closing balance of equity December 31, 20201 | 20,064 | 3,990 | -84 | -45 | 16,203 |

| Opening balance of equity January 1, 2021 | 20,064 | 3,990 | -84 | -45 | 16,203 |

| Net profit Jan-Dec 2021 | 1,034 | 1,034 | |||

| Other comprehensive income Jan-Dec 2021 | 0 | -18 | 18 | ||

| Total comprehensive income Jan-Dec 2021 | 1,034 | - | -18 | 18 | 1,034 |

| Dividend | -290 | -290 | |||

| Closing balance of equity December 31, 20211 | 20,808 | 3,990 | -102 | -27 | 16,947 |

| 1 | The entire equity is attributable to the shareholder of the Parent Company. |

| Year-end Report 2021 | Page 12 of 29 |

Condensed Statement of Cash Flows in the Consolidated Group (unaudited)

| Skr mn | Jan-Dec 2021 | Jan-Dec 2020 |

| Operating activities | ||

| Operating profit | 1,305 | 1,238 |

| Adjustments for non-cash items in operating profit | 69 | 140 |

| Income tax paid | -263 | -311 |

| Changes in assets and liabilities from operating activities | 19,464 | -19,055 |

| Cash flow from operating activities | 20,575 | -17,988 |

| Investing activities | ||

| Capital expenditures | -242 | -35 |

| Cash flow from investing activities | -242 | -35 |

| Financing activities | ||

| Change in senior debt | -10,958 | 29,460 |

| Derivatives, net | -1,523 | -8,651 |

| Dividend paid | -290 | - |

| Payment of lease liability | -24 | -27 |

| Cash flow from financing activities | -12,795 | 20,782 |

| Cash flow for the period | 7,538 | 2,759 |

| Cash and cash equivalents at beginning of the period | 3,362 | 1,362 |

| Cash flow for the period | 7,538 | 2,759 |

| Exchange-rate differences on cash and cash equivalents | 228 | -759 |

| Cash and cash equivalents at end of the period1 | 11,128 | 3,362 |

| 1 | Cash and cash equivalents include, in this context, cash at banks that can be immediately converted into cash and short-term deposits for which the time to maturity does not exceed three months from trade date. |

| Year-end Report 2021 | Page 13 of 29 |

Notes

| Note 1. | Accounting policies |

| Note 2. | Net interest income |

| Note 3. | Net results of financial transactions |

| Note 4. | Impairments |

| Note 5. | Financial assets and liabilities at fair value |

| Note 6. | Derivatives |

| Note 7. | CIRR-system |

| Note 8. | Pledged assets and contingent liabilities |

| Note 9. | Capital adequacy |

| Note 10. | Exposures |

| Note 11. | Transactions with related parties |

| Note 12. | Events after the reporting period |

References to “SEK” or the “Parent Company” are to AB Svensk Exportkredit. References to “Consolidated Group” are to SEK and its consolidated subsidiary. All amounts are in Skr million, unless otherwise indicated. All figures relate to the Consolidated Group, unless otherwise indicated.

Note 1. Accounting policies

This condensed year-end report is presented in accordance with International Accounting Standard (IAS) 34, Interim Financial Reporting. The Consolidated Group’s consolidated accounts have been prepared in accordance with the International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB), together with the interpretations from IFRS Interpretations Committee (IFRS IC). The IFRS standards applied by SEK are all endorsed by the European Union (EU). The accounting also follows the additional standards imposed by the Annual Accounts Act for Credit Institutions and Securities Companies (1995:1559) (ÅRKL) and the regulation and general guidelines issued by Finansinspektionen (the Swedish FSA), “Annual Reports in Credit Institutions and Securities Companies” (FFFS 2008:25). In addition to this, the supplementary accounting rules for groups (RFR 1) issued by the Swedish Financial Reporting Board have been applied. SEK also follows the state’s principles for external reporting in accordance with its State Ownership Policy and principles for state-owned enterprises.

This condensed year-end report of Aktiebolaget Svensk Exportkredit (publ) (Swedish Export Credit Corporation) (the “Parent Company”) has been prepared in accordance with the ÅRKL, and the RFR 2 recommendation, “Accounting for Legal Entities,” issued by the Swedish Financial Reporting Board, as well as the accounting regulations of the Swedish FSA (FFFS 2008:25), which means that within the framework of the ÅRKL, IFRS has been applied to the greatest extent possible. The Parent Company’s results and total assets represent most of the results and total assets of the Consolidated Group, so the Consolidated Group’s information in these notes largely reflects the condition of the Parent Company. The condensed interim report does not include all the disclosures required in the annual financial statements, and should be read in conjunction with the company’s annual financial statements as of December 31, 2020.

The accounting policies, methods of computation and presentation of the Consolidated Group are, in all material aspects, the same as those used for the 2020 annual financial statements on Form 20-F, except for the changes described below. In addition to the changes below, certain amounts reported in prior periods have been restated to conform to the current presentation. SEK analyzes and assesses the application and impact of changes in financial reporting standards that are applied within the Group. Changes that are not mentioned are either not applicable to SEK or have been determined to not have a material impact on SEK’s financial reporting.

The amendments to IFRS 9, IAS 39, IFRS 7, IFRS 4 and IFRS 16 in “Reform for new reference rates - phase 2” have been applicable since January 1, 2021. Phase 2 of the reform of the reference rates is comprised of three main areas: hedge accounting, modifications and information. The changes clarify that hedge accounting does not

have to cease just because the hedged items and hedging instruments were modified as a result of the IBOR reform. Security conditions (and associated documentation) must be changed to reflect the modifications made to the hedged item, the hedging instrument and the hedged risk. Any value adjustments resulting from the changes must be reported as hedging inefficiency. During 2021, SEK has applied the relief under IFRS 9 for changing the hedged risk in existing hedge accounting relationships with GBP LIBOR and JPY LIBOR. The reform of the reference rates further clarifies that modifications required as a direct result of the IBOR reform, when made in an economically equivalent way, should not be reported as modifications for instruments valued at accrued acquisition value. For such modifications, the effective interest rate must be adjusted in line with those modified cash flows. SEK has used the accounting relief rule for modifications for a few transactions. SEK’s exposure that is directly affected by the reference interest rate reform is mainly its lending contracts to variable interest rates, its lending and borrowing contracts at fixed interest rates that are hedged at variable interest rates and currency swaps at variable interest rates. The exposures to variable interest rates are mainly against USD LIBOR, STIBOR and EURIBOR. GBP LIBOR, CHF LIBOR and JPY LIBOR ceased on December 31, 2021. Exposures against these variable interest rates have been converted. For USD LIBOR, the most common maturities are expected to expire after June 30, 2023. SEK has lending contracts and derivative contracts maturing after June 30, 2023 in USD LIBOR with a nominal amount of USD 1,870 million and USD 19,284 million, respectively. The amendments are not expected to result in a change to SEK’s hedging conditions and no significant modification gains or modification losses are expected to be reported, and are therefore not expected to have any significant impact on SEK’s accounts, capital adequacy or large exposures when first applied.

To further improve the resilience of credit institutions within the EU, a reform package was adopted in June 2019: Regulation (EU) 2019/876 (CRRII) and Directive (EU) 2019/878 (CRDV) of the European Parliament and of the Council. On June 28, 2021, the Capital Requirements Regulation (CRRII) entered into force. This means that new requirements such as a binding leverage ratio and a binding net stable funding ratio (NSFR) are included in Note 9, Capital adequacy. The information is published in accordance with Finansinspektionen’s (the Swedish FSA) Supervisory Regulations FFFS 2014:12 and FFFS 2008:25.

There are no other IFRS or IFRS Interpretations Committee interpretations that are not yet applicable that are expected to have a material impact on SEK’s financial statements, capital adequacy or large exposure ratios.

| Year-end Report 2021 | Page 14 of 29 |

Note 2. Net interest income

| Skr mn | Oct-Dec 2021 | Jul-Sep 2021 | Oct-Dec 2020 | Jan-Dec 2021 | Jan-Dec 2020 |

| Interest income | |||||

| Loans to credit institutions | 29 | 35 | 36 | 131 | 236 |

| Loans to the public | 995 | 948 | 975 | 3,782 | 4,210 |

| Loans in the form of interest-bearing securities | 193 | 199 | 208 | 776 | 897 |

| Interest-bearing securities excluding loans in the form of interest-bearing securities | 10 | 9 | 20 | 50 | 242 |

| Derivatives | -584 | -568 | -557 | -2,239 | -1,708 |

| Administrative remuneration CIRR-system | 55 | 50 | 46 | 198 | 197 |

| Other assets | 5 | 5 | 9 | 21 | 34 |

| Total interest income1 | 703 | 678 | 737 | 2,719 | 4,108 |

| Interest expenses | |||||

| Interest expenses | -199 | -184 | -197 | -724 | -2,076 |

| Resolution fee | -22 | -22 | -21 | -88 | -86 |

| Total interest expenses | -221 | -206 | -218 | -812 | -2,162 |

| Net interest income | 482 | 472 | 519 | 1,907 | 1,946 |

| 1 | Interest income calculated using the effective interest method amounted to Skr 4,264 million during January-December 2021 (2020: Skr 4,960 million). |

Note 3. Net results of financial transactions

| Skr mn | Oct-Dec 2021 | Jul-Sep 2021 | Oct-Dec 2020 | Jan-Dec 2021 | Jan-Dec 2020 |

| Derecognition of financial instruments not measured at fair value through profit or loss | 2 | 1 | 3 | 33 | 14 |

| Financial assets or liabilities at fair value through profit or loss | 33 | 19 | 39 | 13 | -22 |

| Financial instruments under fair-value hedge accounting | 5 | 4 | 42 | 12 | 86 |

| Currency exchange-rate effects on all assets and liabilities excl. currency exchange-rate effects related to revaluation at fair value | 1 | -1 | 3 | -2 | 5 |

| Total net results of financial transactions | 41 | 23 | 87 | 56 | 83 |

| Year-end Report 2021 | Page 15 of 29 |

Note 4. Impairments

| Skr mn | Oct-Dec 2021 | Jul-Sep 2021 | Oct-Dec 2020 | Jan-Dec 2021 | Jan-Dec 2020 |

| Expected credit losses, stage 1 | -3 | 27 | 9 | 60 | -98 |

| Expected credit losses, stage 2 | 1 | 10 | -2 | 29 | -48 |

| Expected credit losses, stage 3 | -1 | 12 | 0 | -46 | -7 |

| Established losses | -42 | -7 | - | -52 | -20 |

| Reserves applied to cover established credit losses | 35 | 7 | - | 49 | 20 |

| Recovered credit losses | 1 | - | - | 1 | - |

| Net credit losses | -9 | 49 | 7 | 41 | -153 |

| Skr mn | December 31, 2021 | December 31, 2020 | |||

| Stage 1 | Stage 2 | Stage 3 | Total | Total | |

| Loans, before expected credit losses | 196,912 | 38,185 | 2,284 | 237,381 | 231,919 |

| Off balance sheet exposures, before expected credit losses | 31,577 | 28,466 | 105 | 60,148 | 62,504 |

| Total, before expected credit losses | 228,489 | 66,651 | 2,389 | 297,529 | 294,423 |

| Loss allowance, loans | -82 | -27 | -48 | -157 | -240 |

| Loss allowance, off balance sheet exposures1 | -6 | -1 | 0 | -7 | -9 |

| Total loss allowance | -88 | -28 | -48 | -164 | -249 |

| Provision ratio (in percent) | 0.04 | 0.04 | 2.01 | 0.06 | 0.08 |

| 1 Recognized under provision in Consolidated Statement of Financial Position. Off balance sheet exposures consist of guarantee commitments, committed undisbursed loans and binding offers, see Note 8. | |||||

The table above shows the book value of loans and nominal amounts for off-balance sheet exposures before expected credit losses for each stage as well as related loss allowance amounts, in order to place expected credit losses in relation to credit exposures. Overall, the credit portfolio has an extremely high credit quality and SEK

often uses risk mitigation measures, primarily through guarantees from the Swedish Export Credit Agency (EKN) and other government export credit agencies in the Organisation for Economic Co-operation and Development (OECD), which explains the low provision ratio.

Loss Allowance

| December 31, 2021 | December 31, 2020 | ||||

| Skr mn | Stage 1 | Stage 2 | Stage 3 | Total | Total |

| Opening balance January 1 | -147 | -56 | -46 | -249 | -128 |

| Increases due to origination and acquisition | -40 | 0 | -25 | -65 | -84 |

| Net remeasurement of loss allowance | 51 | 13 | -43 | 21 | -69 |

| Transfer to stage 1 | 0 | 0 | - | 0 | - |

| Transfer to stage 2 | 2 | -6 | - | -4 | - |

| Transfer to stage 3 | 0 | 2 | -21 | -19 | -9 |

| Decreases due to derecognition | 47 | 20 | 43 | 110 | 8 |

| Decrease in allowance account due to write-offs | - | - | 49 | 49 | 20 |

| Exchange-rate differences1 | -1 | -1 | -5 | -7 | 13 |

| Closing balance | -88 | -28 | -48 | -164 | -249 |

| 1 Recognized under net results of financial transactions in Statement of Comprehensive Income. | |||||

Provisions for expected credit losses (ECLs) are calculated using quantitative models based on inputs, assumptions and methods that are highly reliant on assessments. In particular, the following could heavily impact the level of provisions: the establishment of a material increase in credit risk, allowing for forward-looking macroeconomic scenarios, and the measurement of both ECLs over the next 12 months and lifetime ECLs. ECLs are based on objective assessments of what SEK expects to lose on the exposures given what was known on the reporting date and taking into account possible future events. The ECL is a probability-weighted amount that is determined by evaluating the outcome of several possible scenarios and where the data taken into consideration comprises information from previous conditions, current conditions and projections of future economic conditions. SEK’s method entails three scenarios being prepared for each probability of default curve: (i) a base scenario, (ii) a downturn scenario and (iii) an upturn scenario. The base scenario consists of

GDP forecasts from the World Bank. When calculating the ECL as of December 31, 2021, the latest available forecast was the World Bank’s forecast from June 2021. According to the World Bank’s forecast, global economic output is expected to increase by 5.6 percent in 2021 and to increase by 4.3 percent in 2022. The base scenario has been weighted at between 73 and 80 percent, and the downturn and upturn scenarios weighted equally at between 5 and 19 percent.

SEK’s IFRS 9 model is based on GDP growth projections estimating the impact on the probability of default. SEK’s management believes that the strong positive GDP growth projections may understate the probability of default of the asset portfolio. In the fourth quarter, as the IFRS 9 model is assessed to underestimate the probability of default, SEK made an overall adjustment to increase expected credit losses which was calculated pursuant to SEK’s IFRS 9 model as of December 31, 2021.

| Year-end Report 2021 | Page 16 of 29 |

Note 5. Financial assets and liabilities at fair value

| Skr mn | December 31, 2021 | ||

| Book value | Fair value | Surplus value (+)/ Deficit value (–) | |

| Cash and cash equivalents | 11,128 | 11,128 | - |

| Treasuries/governments bonds | 10,872 | 10,872 | - |

| Other interest-bearing securities except loans | 45,881 | 45,881 | - |

| Loans in the form of interest-bearing securities | 46,578 | 47,991 | 1,413 |

| Loans to credit institutions | 20,775 | 20,993 | 218 |

| Loans to the public | 180,288 | 186,436 | 6,148 |

| Derivatives | 8,419 | 8,419 | - |

| Total financial assets | 323,941 | 331,720 | 7,779 |

| Borrowing from credit institutions | 5,230 | 5,230 | - |

| Borrowing from the public | 10,000 | 10,000 | - |

| Debt securities issued | 279,770 | 280,294 | 524 |

| Derivatives | 14,729 | 14,729 | - |

| Total financial liabilities | 309,729 | 310,253 | 524 |

| Skr mn | December 31, 2020 | ||

| Book value | Fair value | Surplus value (+)/ Deficit value (–) | |

| Cash and cash equivalents | 3,362 | 3,362 | - |

| Treasuries/governments bonds | 22,266 | 22,266 | - |

| Other interest-bearing securities except loans | 33,551 | 33,551 | - |

| Loans in the form of interest-bearing securities | 50,780 | 52,091 | 1,311 |

| Loans to credit institutions | 31,315 | 31,424 | 109 |

| Loans to the public | 171,562 | 180,453 | 8,891 |

| Derivatives | 7,563 | 7,563 | - |

| Total financial assets | 320,399 | 330,710 | 10,311 |

| Borrowing from credit institutions | 3,486 | 3,486 | - |

| Borrowing from the public | 10,000 | 10,000 | - |

| Debt securities issued | 273,976 | 274,552 | 576 |

| Derivatives | 25,395 | 25,395 | - |

| Total financial liabilities | 312,857 | 313,433 | 576 |

Determination of fair value

The determination of fair value is described in the annual financial statements included in SEK’s 2020 Annual Report on Form 20-F, see Note 1 (h) (viii) Principles for determination of fair value of finan-

cial instruments and (ix) Determination of fair value of certain types of financial instruments.

| Year-end Report 2021 | Page 17 of 29 |

Financial assets in fair value hierarchy

| Skr mn | Financial assets at fair value through profit or loss | |||

| Level 1 | Level 2 | Level 3 | Total | |

| Treasuries/governments bonds | 5,638 | 5,234 | - | 10,872 |

| Other interest-bearing securities except loans | 26,549 | 19,332 | - | 45,881 |

| Derivatives | - | 7,933 | 486 | 8,419 |

| Total, December 31, 2021 | 32,187 | 32,499 | 486 | 65,172 |

| Total, December 31, 2020 | 33,582 | 28,220 | 1,578 | 63,380 |

Financial liabilities in fair value hierarchy

| Skr mn | Financial liabilities at fair value through profit or loss | |||

| Level 1 | Level 2 | Level 3 | Total | |

| Debt securities issued | - | 6,761 | 32,555 | 39,316 |

| Derivatives | - | 12,206 | 2,523 | 14,729 |

| Total, December 31, 2021 | - | 18,967 | 35,078 | 54,045 |

| Total, December 31, 2020 | - | 29,744 | 43,039 | 72,783 |

Due to an increased element of subjective assessment of the input in the valuation, a transfer of Skr -1 million for derivatives was made from level 2 to level 3 (year-end 2020: a transfer of Skr -10,649 million for debt securities issued was made from level 2 to level 3, a

transfer from level 3 to level 2 of Skr 6,534 million for debt securities issued was made and a transfer from level 3 to level 2 of net Skr -1,259 million for derivatives was made).

Financial assets and liabilities at fair value in Level 3, 2021

| Skr mn | January 1, 2021 | Purchases | Settle- ments & sales | Transfers to Level 3 | Transfers from Level 3 | Gains (+) and losses (–) through profit or loss1 | Gains (+) and losses (–) in Other com- prehensive income | Exchange- rate differences | December 31, 2021 |

| Debt securities issued | -41,198 | -10,372 | 19,337 | - | - | 196 | -36 | -482 | -32,555 |

| Derivatives, net | -263 | 5 | -599 | -1 | - | 411 | -1,590 | -2,037 | |

| Net assets and liabilities | -41,461 | -10,367 | 18,738 | -1 | - | 607 | -36 | -2,072 | -34,592 |

Financial assets and liabilities at fair value in Level 3, 2020

| Skr mn | January 1, 2020 | Purchases | Settle- ments & sales | Transfers to Level 3 | Transfers from Level 3 | Gains (+) and losses (–) through profit or loss1 | Gains (+) and losses (–) in Other com- prehensive income | Exchange- rate differences | December 31, 2020 |

| Debt securities issued | -43,752 | -10,584 | 16,285 | -10,649 | 6,534 | -1,345 | 44 | 2,269 | -41,198 |

| Derivatives, net | 22 | 7 | -400 | - | -1,259 | -1,597 | - | 2,964 | -263 |

| Net assets and liabilities | -43,730 | -10,577 | 15,885 | -10,649 | 5,275 | -2,942 | 44 | 5,233 | -41,461 |

| 1 | Gains and losses through profit or loss, including the impact of exchange-rates, is reported as net interest income and net results of financial transactions. The unrealized fair value changes for assets and liabilities, including the impact of exchange-rates, held as of December 31, 2021 amounted to a Skr 594 million gain (year-end 2020: Skr 36 million gain) and are reported as net results of financial transactions. |

Uncertainty of valuation of Level 3 instruments

As the estimation of parameters included in the models used to calculate the market value of Level 3 instruments is associated with subjectivity and uncertainty, SEK has conducted an analysis of the difference in fair value of Level 3 instruments using other established parameter values. Option models and discounted cash flows are used to value the Level 3 instruments. For the Level 3 instruments that are significantly affected by different types of correlations, which are not based on observable market data, a revaluation has been made by shifting the correlations. The correlation is expressed as a value between 1 and –1, where 0 indicates no relationship, 1 indicates a maximum positive relationship and -1 indicates a maximum negative relationship. The maximum correlation in the range of unobservable inputs can thus be from 1 to –1. In the analysis, the correlations have been adjusted by +/– 0.12, which represents the level SEK uses within its prudent valuation framework. For Level 3 instruments that are significantly affected by non-observable market data

in the form of SEK’s own creditworthiness, a revaluation has been made by shifting the credit curve. The revaluation is made by shifting the credit spreads by +/- 10 basis points, which has been assessed as a reasonable change in SEK’s credit spread. The analysis shows the impact of the non-observable market data on the market value. In addition, the market value will be affected by observable market data. The result of the analysis corresponds with SEK’s business model where issued securities are linked with a matched hedging derivative. The underlying market data is used to evaluate the issued security as well as to evaluate the fair value in the derivative. This means that a change in fair value of the issued security, excluding SEK’s own credit spread, is offset by an equally large change in fair value in the derivative.

| Year-end Report 2021 | Page 18 of 29 |

Sensitivity analysis – level 3 assets and liabilities

| Assets and liabilities | December 31, 2021 | |||||

| Skr mn | Fair Value | Unobservable input | Range of estimates for unobservable input | Valuation method | Sensitivity max | Sensitivity min |

| Equity | -892 | Correlation | 0.12 – (0.12) | Option Model | -3 | 3 |

| Interest rate | -1 | Correlation | 0.12 – (0.12) | Option Model | 0 | 0 |

| FX | -1,038 | Correlation | 0.12 – (0.12) | Option Model | -56 | 56 |

| Other | -106 | Correlation | 0.12 – (0.12) | Option Model | 0 | 0 |

| Sum derivatives, net | -2,037 | -59 | 59 | |||

| Equity | -9,283 | Correlation | 0.12 – (0.12) | Option Model | 3 | -3 |

| Credit spreads | 10BP – (10BP) | Discounted cash flow | 10 | -10 | ||

| Interest rate | -11,900 | Correlation | 0.12 – (0.12) | Option Model | 0 | 0 |

| Credit spreads | 10BP – (10BP) | Discounted cash flow | 58 | -58 | ||

| FX | -11,235 | Correlation | 0.12 – (0.12) | Option Model | 59 | -59 |

| Credit spreads | 10BP – (10BP) | Discounted cash flow | 50 | -50 | ||

| Other | -137 | Correlation | 0.12 – (0.12) | Option Model | 0 | 0 |

| Credit spreads | 10BP – (10BP) | Discounted cash flow | 1 | -1 | ||

| Sum debt securities issued | -32,555 | 181 | -181 | |||

| Total effect on total comprehensive income | 122 | -122 | ||||

| Derivatives, net, December 31, 2020 | -263 | -59 | 59 | |||

| Debt securities issued, December 31, 2020 | -41,198 | 196 | -196 | |||

| Total effect on total comprehensive income, December 31, 2020 | 137 | -137 | ||||

The sensitivity analysis shows the effect that a shift in correlations or SEK’s own credit spread has on Level 3 instruments. The table presents maximum positive and negative change in fair value when correlations or SEK’s own credit spread is shifted by +/– 0.12 and +/- 10 basis points, respectively. When determining the total maximum/minimum effect on total comprehensive income the most adverse/favorable shift is

chosen, considering the net exposure arising from the issued securities and the derivatives, for each correlation. The resulting effect related to correlation sensitivity is Skr +/- 3 million. The impact from SEK’s own credit spread amounts to Skr 119 million (year-end 2020: Skr 137 million) under a maximum scenario and Skr -119 million (year-end 2020: Skr -137 million) under a minimum scenario.

Fair value related to credit risk

Fair value originating from credit risk (- liabilities increase/ + liabilities decrease) | The period’s change in fair value originating from credit risk (+ income/ - loss) | |||

| Skr mn | December 31, 2021 | 31 December 2020 | Jan–Dec 2021 | Jan–Dec 2020 |

| CVA/DVA, net1 | -14 | -17 | 3 | -5 |

| OCA2 | -132 | -108 | -24 | 18 |

| 1 | Credit value adjustment (CVA) and Debt value adjustment (DVA) reflects how the counterparties’ credit risk as well as SEK’s own credit rating affects the fair value of derivatives. |

| 2 | Own credit adjustment (OCA) reflects how the changes in SEK’s credit rating affects the fair value of financial liabilities measured at fair value through profit and loss. |

| Year-end Report 2021 | Page 19 of 29 |

Note 6. Derivatives

Derivatives by category

| Skr mn | December 31, 2021 | December 31, 2020 | ||||

Assets Fair value | Liabilities Fair value | Nominal amounts | Assets Fair value | Liabilities Fair value | Nominal amounts | |

| Interest rate-related contracts | 3,192 | 9,464 | 361,160 | 3,846 | 11,774 | 323,664 |

| Currency-related contracts | 5,218 | 3,518 | 157,362 | 3,249 | 11,236 | 153,838 |

| Equity-related contracts | 2 | 895 | 9,801 | 457 | 620 | 15,598 |

| Contracts related to commodities, credit risk, etc. | 7 | 852 | 3,521 | 11 | 1,765 | 7,513 |

| Total derivatives | 8,419 | 14,729 | 531,844 | 7,563 | 25,395 | 500,613 |

| In accordance with SEK’s policies with regard to counterparty, interest rate, currency exchange, and other exposures, SEK uses, and is a party to, different kinds of derivative instruments, mostly various interest rate-related and currency exchange-related contracts, | primarily to hedge risk exposure inherent in financial assets and liabilities. These contracts are carried at fair value in the statements of financial position on a contract-by-contract basis. |

Note 7. CIRR-system

Pursuant to the company’s assignment as stated in its owner instruction issued by the Swedish government, SEK administers credit granting in the Swedish system for officially supported export credits (CIRR-system). SEK receives compensation from the Swedish government in the form of an administrative compensation, which is calculated based on the principal amount outstanding. The administrative compensation paid by the state to SEK is recognized in the CIRR-system as administrative remuneration to SEK. Refer to the following tables of the statement of comprehensive income and statement of financial positions for the CIRR-system, presented as reported to the owner. Interest expenses includes interest expenses for loans between SEK and the CIRR-system which reflects the borrowing cost for the CIRR-system. Interest expenses for derivatives hedging CIRR-loans are also recognized as interest | expenses, which differs from SEK’s accounting principles. Arrangement fees to SEK are recognized together with other arrangement fees as interest expenses. In addition to the CIRR-system, SEK administers the Swedish government’s previous concessionary credit program according to the same principles as the CIRR-system. No new lending is being offered under the concessionary credit program. As of December 31, 2021, concessionary loans outstanding amounted to Skr 315 million (year-end 2020: Skr 382 million) and operating profit for the program amounted to Skr -21 million (2020: Skr -28 million) for the period January-December 2021. SEK’s administrative compensation for administrating the concessionary credit program amounted to Skr 1 million (2020: Skr 1 million). |

Statement of Comprehensive Income for the CIRR-system

| Skr mn | Oct-Dec 2021 | Jul-Sep 2021 | Oct-Dec 2020 | Jan-Dec 2021 | Jan-Dec 2020 |

| Interest income | 579 | 541 | 509 | 2,105 | 2,170 |

| Interest expenses | -533 | -514 | -535 | -2,061 | -2,087 |

| Interest compensation | - | - | - | 7 | 14 |

| Exchange-rate differences | 0 | 0 | 2 | -1 | 4 |

| Profit before compensation to SEK | 46 | 27 | -24 | 50 | 101 |

| Administrative remuneration to SEK | -55 | -50 | -46 | -197 | -196 |

| Operating profit CIRR-system | -9 | -23 | -70 | -147 | -95 |

| Reimbursement to (–) / from (+) the State | 9 | 23 | 70 | 147 | 95 |

| Year-end Report 2021 | Page 20 of 29 |

Statement of Financial Position for the CIRR-system

| Skr mn | December 31, 2021 | December 31, 2020 |

| Cash and cash equivalents | 8 | 2 |

| Loans | 87,872 | 69,163 |

| Derivatives | 36 | - |

| Other assets | 7,359 | 12,528 |

| Prepaid expenses and accrued revenues | 470 | 407 |

| Total assets | 95,745 | 82,100 |

| Liabilities | 88,092 | 69,289 |

| Derivatives | 7,060 | 12,232 |

| Accrued expenses and prepaid revenues | 593 | 579 |

| Total liabilities | 95,745 | 82,100 |

| Commitments | ||

| Committed undisbursed loans | 39,084 | 51,463 |

| Binding offers | 1,510 | 1,322 |

Note 8. Pledged assets and contingent liabilities

| Skr mn | December 31, 2021 | December 31, 2020 |

| Collateral provided | ||

| Cash collateral under the security agreements for derivative contracts | 10,417 | 21,979 |

| Contingent liabilities1 | ||

| Guarantee commitments | 4,767 | 3,969 |

| Commitments1 | ||

| Committed undisbursed loans | 53,871 | 57,213 |

| Binding offers | 1,510 | 1,322 |

| 1 | For expected credit losses in guarantee commitments, committed undisbursed loans and binding offers, see Note 4. |

| Year-end Report 2021 | Page 21 of 29 |

Note 9. Capital adequacy

The capital adequacy analysis relates to the parent company AB Svensk Exportkredit. The information is disclosed according to FFFS 2014:12 and FFFS 2008:25. For further information on capital adequacy and risks, see Note 29 to the annual financial statements included in SEK’s 2020 Annual Report on Form 20-F and see SEK’s 2020 Capital Adequacy and Risk Management (Pillar 3) Report.

Capital Adequacy Analysis

| December 31, 2021 | December 31, 2020 | |

| Capital ratios | percent1 | percent1 |

| Common Equity Tier 1 capital ratio | 21.6 | 21.8 |

| Tier 1 capital ratio | 21.6 | 21.8 |

| Total capital ratio | 21.6 | 21.8 |

| 1 | Capital ratios exclusive of buffer requirements are the quotients of the relevant capital measure and the total risk exposure amount. See tables Own funds – adjusting items and Minimum capital requirements exclusive of buffer. |

| December 31, 2021 | December 31, 2020 | |||

| Total risk-based capital requirement | Skr mn | percent1 | Skr mn | percent1 |

| Capital base requirement of 8 percent2 | 7,371 | 8.0 | 7,136 | 8.0 |

| of which Tier 1 requirement of 6 percent | 5,528 | 6.0 | 5,352 | 6.0 |

| of which minimum requirement of 4.5 percent | 4,146 | 4.5 | 4,014 | 4.5 |

| Pillar 2 capital requirements3 | 3,382 | 3.7 | 3,921 | 4.4 |

| Common Equity Tier 1 capital available to meet buffer requirements4 | 9,149 | 9.9 | 12,310 | 13.8 |

| Capital buffer requirements | 2,333 | 2.5 | 2,259 | 2.5 |

| of which Capital conservation buffer | 2,303 | 2.5 | 2,230 | 2.5 |

| of which Countercyclical buffer | 30 | 0.0 | 29 | 0.0 |

| Pillar 2 guidance5 | 1,382 | 1.5 | - | - |

| Total risk-based capital requirement | 14,468 | 15.7 | 13,316 | 14.9 |

| 1 | Expressed as a percentage of total risk exposure amount. |

| 2 | The minimum requirements according to CRR (Regulation (EU) No 575/2013 of the European Parliament and of the Council of June 26, 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012) have fully come into force in Sweden without regard to the transitional period. |

| 3 | Individual Pillar 2 requirement of 3.67 percent calculated on the total risk exposure amount, according to the decision from the latest Swedish FSA Supervisory Review and Evaluation Process (”SREP”) on September 29, 2021. |

| 4 | Common Equity Tier 1 capital available to meet buffer requirement after 8 percent minimum capital requirement (SEK covers all minimum requirements with CET1 capital - i.e., 4.5 percent, 1.5 percent and 2 percent) and after the Pillar 2 requirements (3.67 percent). The Pillar 2 requirement was not deducted in the previous year’s figure. |

| 5 | The Swedish FSA notified SEK on September 29, 2021, within the latest SREP, that in addition to the capital requirements according to Regulation (EU) no 575/2013 on prudential requirements, SEK should hold additional capital (pillar 2 guidance) of 1.50 percent of the total risk-weighted exposure amount. The Pillar 2 guidance is not a binding requirement. |

| December 31, 2021 | December 31, 2020 | |

| Leverage ratio1 | Skr mn | Skr mn |

| On-balance sheet exposures | 209,889 | 297,605 |

| Off-balance sheet exposures | 5,309 | 37,162 |

| Total exposure measure2 | 215,198 | 334,767 |

| Leverage ratio3 | 9.3% | 5.8% |

| 1 | The leverage ratio reflects the full impact of IFRS 9 as no transitional rules were utilized. |

| 2 | In the second quarter of 2021, SEK changed its methodology for calculating the exposure measure in leverage ratio to comply with new regulatory requirements (CRRII), pursuant to which certain exposures are no longer included. Comparative figures have not been recalculated. |

| 3 | Defined by CRR as the quotient of the Tier 1 capital and an exposure measure. |

| December 31, 2021 | December 31, 2020 | |||

| Total Leverage ratio requirement | Skr mn | percent1 | Skr mn | percent1 |

| Capital base requirement of 3 percent | 6,456 | 3.0 | - | - |

| Pillar 2 guidance2 | 323 | 0.2 | - | - |

| Total capital requirement relating to Leverage ratio | 6,779 | 3.2 | - | - |

| 1 | Expressed as a percentage of total exposure amount. |

| 2 | The Swedish FSA has on September 29, 2021 notified SEK, within the latest SREP, that SEK may hold additional capital (pillar 2 guidance) of 0.15 percent calculated on the total Leverage ratio exposure measure. The Pillar 2 guidance is not a binding requirement. |

| Year-end Report 2021 | Page 22 of 29 |

Own funds – Adjusting items

| Skr mn | December 31, 2021 | December 31, 2020 |

| Share capital | 3,990 | 3,990 |

| Retained earnings | 15,518 | 14,856 |

| Accumulated other comprehensive income and other reserves | 323 | 292 |

| Independently reviewed profit net of any foreseeable charge or dividend | 601 | 694 |

| Common Equity Tier 1 (CET1) capital before regulatory adjustments | 20,432 | 19,832 |

| Additional value adjustments due to prudent valuation | -395 | -306 |

| Intangible assets1 | -99 | -98 |

| Gains or losses on liabilities valued at fair value resulting from changes in own credit standing | 98 | 77 |

| Negative amounts resulting from the calculation of expected loss amounts | -111 | -55 |

| Total regulatory adjustments to Common Equity Tier 1 capital | -507 | -382 |

| Total Common Equity Tier 1 capital | 19,925 | 19,450 |

| Total Own funds | 19,925 | 19,450 |

| 1 | From December 31, 2020, SEK applies the amendments to Delegated Regulation (EU) No 241/2014 regarding deduction of software assets from Common Equity Tier 1 (CET1). The amendments introduce an exemption from the deduction of intangible assets from CET1 for prudently valued software assets of which the value is not negatively affected by resolution, insolvency or liquidation of the institution. |

Minimum capital requirements exclusive of buffer

| Skr mn | December 31, 2021 | December 31, 2020 | ||||

| EAD1 | Risk exposure amount | Minimum capital requirement | EAD1 | Risk exposure amount | Minimum capital requirement | |

| Credit risk standardized method | ||||||

| Corporates | 2,990 | 2,990 | 239 | 2,238 | 2,238 | 179 |

| Exposures in default | 74 | 74 | 6 | 7 | 7 | 1 |

| Total credit risk standardized method | 3,064 | 3,064 | 245 | 2,245 | 2,245 | 180 |

| Credit risk IRB method | ||||||

| Central Governments | 196,606 | 9,673 | 774 | 192,077 | 9,684 | 775 |

| Financial institutions2 | 41,082 | 8,843 | 707 | 30,661 | 6,764 | 541 |

| Corporates3 | 115,412 | 62,988 | 5,039 | 117,415 | 63,766 | 5,101 |

| Assets without counterparty | 372 | 372 | 30 | 163 | 163 | 13 |

| Total credit risk IRB method | 353,472 | 81,876 | 6,550 | 340,316 | 80,377 | 6,430 |

| Credit valuation adjustment risk | n.a. | 2,922 | 233 | n.a. | 2,284 | 183 |

| Foreign exchange risk | n.a. | 645 | 52 | n.a. | 664 | 52 |

| Commodities risk | n.a. | 11 | 1 | n.a. | 7 | 1 |

| Operational risk | n.a. | 3,622 | 290 | n.a. | 3,625 | 290 |

| Total | 356,536 | 92,140 | 7,371 | 342,561 | 89,202 | 7,136 |

| 1 | Exposure at default (EAD) shows the size of the outstanding exposure at default. | |

| 2 | Of which counterparty risk in derivatives: EAD Skr 5,975 million (year-end 2020: Skr 5,535 million), Risk exposure amount of Skr 2,000 million (year-end 2020: Skr 1,908 million) and Capital requirement of Skr 160 million (year-end 2020: Skr 153 million). | |

| 3 | Of which related to specialized lending: EAD Skr 5,224 million (year-end 2020: 3,847 million), Risk exposure amount of Skr 3,589 million (year-end 2020: Skr 2,739 million) and Capital requirement of Skr 287 million (year-end 2020: Skr 219 million). |

Credit risk

For classification and quantification of credit risk, SEK uses the IRB approach. Specifically, SEK applies the Foundation Approach. Under the Foundation Approach, the company determines the probability of default within one year (PD) for each of its counterparties, while the remaining parameters are established in accordance with CRR. Application of the IRB approach requires the Swedish FSA’s permission and is subject to ongoing supervision. Certain exposures are, by permission from the Swedish FSA, exempted from application of the IRB approach, and, instead, the standardized approach is applied. In 2020, SEK reviewed its credit risk processes in order to comply with new regulatory requirements, EBA Guidelines EBA/GL/2016/07 and Commission Delegated Regulation (EU) 2018/171, on the definition of default. As a result, SEK established a new internal

definition of default, which was subsequently approved by the Swedish FSA and later, on January 1, 2021, implemented in the IRB approach for own funds requirements calculation. Counterparty risk exposure amounts in derivatives are calculated in accordance with the standardized approach for counterparty credit risk. SEK has been applying a new standardized approach for counterparty credit risk since June 30, 2021.

Credit valuation adjustment risk

Credit valuation adjustment risk is calculated for all over-the-counter derivative contracts, except for credit derivatives used as credit protection and transactions with a qualifying central counterparty. SEK calculates this capital requirement according to the standardized method.

| Year-end Report 2021 | Page 23 of 29 |

Foreign exchange risk

Foreign exchange risk is calculated according to the standardized approach, whereas the scenario approach is used for calculating the gamma and volatility risks.

Commodities risk

Capital requirements for commodity risk are calculated in -accordance with the simplified approach under the standardized approach. The scenario approach is used for calculating the gamma and volatility risks.

Operational risk

Capital requirement for operational risk is calculated according to the standardized approach. The company’s operations are divided into business areas as defined in the CRR. The capital requirement for each area is calculated by multiplying a factor depending on the business area by an income indicator. The factors applicable for SEK are 15 percent and 18 percent. The income indicators consist of the average operating income for the past three financial years for each business area.

Transitional rules

The capital adequacy ratios reflect the full impact of IFRS 9 as no transitional rules for IFRS 9 were utilized.

Capital buffer requirements

SEK expects to meet capital buffer requirements with Common Equity Tier 1 capital. The mandatory capital conservation buffer is 2.5 percent. The countercyclical buffer rate that is applied to exposures located in Sweden was lowered from 2.5 percent to 0 percent as of March 16, 2020. The reduction was made for preventive purposes, in order to counteract credit tightening due to the development and spread of COVID-19 and its effects on the economy. The Swedish FSA decided on September 29, 2021 to increase the countercyclical buffer rate to 1 percent. The new countercyclical buffer rate applies from September 29, 2022. As of December 31, 2021, the capital requirement related to relevant exposures in Sweden was 68 percent (year-end 2020: 70 percent) of the total relevant capital requirement regardless of location; this fraction is also the weight applied on the Swedish buffer rate when calculating SEK’s countercyclical capital buffer. The countercyclical capital buffer as of December 31, 2021 for Sweden has been dissolved due to the reduction of the countercyclical buffer value to 0 percent. Buffer rates applicable in other countries may have effects on SEK, but as most capital requirements for SEK’s relevant credit exposures are related to Sweden, the potential effect is limited. As of December 31, 2021, the contribution to SEK’s countercyclical buffer from buffer rates in other countries was 0.03 percentage points (year-end 2020: 0.03 percentage points). SEK has not been classified as a systemically important institution by any financial regulatory authority. The capital buffer requirements for systemically important institutions that came into force January 1, 2016, therefore do not apply to SEK.

Pillar 2 guidance

The Pillar 2 guidance refers to what the Swedish FSA believes to be an appropriate level of the institution’s own funds. The difference between the believed appropriate level of own funds and the minimum capital requirement, the Pillar 2 capital requirement and the combined capital buffer requirement will be calculated, decided and established by the Swedish FSA in the form of a non-binding recommendation (so-called pillar 2 guidance). The Pillar 2 guidance covers both the risk-based capital requirement and the leverage ratio requirement, and replaces the previous capital planning buffer.

Internally assessed economic capital

| Skr mn | December 31, 2021 | December 31, 2020 |