UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-02105

Fidelity Salem Street Trust

(Exact name of registrant as specified in charter)

245 Summer St., Boston, MA 02210

(Address of principal executive offices) (Zip code)

Margaret Carey, Secretary

245 Summer St.

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code:

617-563-7000

| |

Date of fiscal year end: | August 31 |

|

|

Date of reporting period: | February 29, 2024 |

Item 1.

Reports to Stockholders

Fidelity® Series Government Money Market Fund

Semi-Annual Report

February 29, 2024

Contents

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-544-8544 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2024 FMR LLC. All rights reserved.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT. Forms N-PORT are available on the SEC's web site at http://www.sec.gov. A fund's Forms N-PORT may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.institutional.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED •MAY LOSE VALUE •NO BANK GUARANTEE

Neither the Fund nor Fidelity Distributors Corporation is a bank.

| Current 7-Day Yields |

| | | |

| Fidelity® Series Government Money Market Fund | 5.38% | |

| | | |

Yield refers to the income paid by the Fund over a given period. Yield for money market funds is usually for seven-day periods, as it is here, though it is expressed as an annual percentage rate. Past performance is no guarantee of future results. Yield will vary and it's possible to lose money investing in the Fund. | |

| Effective Maturity Diversification (% of Fund's Investments) |

| Days |

| 1 - 7 | 66.0 | |

| 8 - 30 | 8.1 | |

| 31 - 60 | 11.3 | |

| 61 - 90 | 6.7 | |

| 91 - 180 | 4.0 | |

| > 180 | 3.9 | |

| Effective maturity is determined in accordance with the requirements of Rule 2a-7 under the Investment Company Act of 1940. |

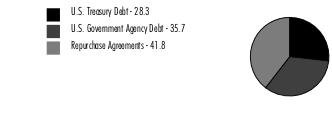

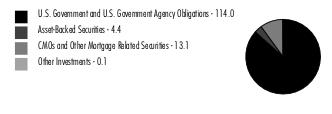

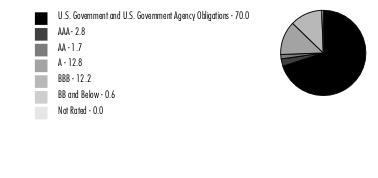

Asset Allocation (% of Fund's net assets) |

|

Net Other Assets (Liabilities) - (5.8)% |

|

Showing Percentage of Net Assets

| U.S. Treasury Debt - 28.3% |

| | | Yield (%)(a) | Principal Amount (b) | Value ($) |

| U.S. Treasury Obligations - 28.3% | | | | |

| U.S. Treasury Bills | | | | |

| 3/5/24 to 8/29/24 | | 5.18 to 5.45 | 793,800,000 | 788,373,862 |

| U.S. Treasury Notes | | | | |

| 4/30/24 to 1/15/25 (c) | | 4.88 to 5.47 | 65,000,000 | 64,900,721 |

| | | | | |

| TOTAL U.S. TREASURY DEBT (Cost $853,274,583) | | | | 853,274,583 |

| | | | | |

| U.S. Government Agency Debt - 35.7% |

| | | Yield (%)(a) | Principal Amount (b) | Value ($) |

| Federal Agencies - 35.7% | | | | |

| Federal Farm Credit Bank | | | | |

| 3/13/24 to 1/30/26 (c)(d) | | 5.33 to 5.51 | 182,727,000 | 182,730,568 |

| Federal Home Loan Bank | | | | |

| 3/6/24 to 1/2/26 (c) | | 4.79 to 5.54 | 892,804,623 | 892,163,445 |

| | | | | |

| TOTAL U.S. GOVERNMENT AGENCY DEBT (Cost $1,074,894,013) | | | | 1,074,894,013 |

| | | | | |

| U.S. Government Agency Repurchase Agreement - 16.4% |

| | | Maturity Amount ($) | Value ($) |

| In a joint trading account at 5.31% dated 2/29/24 due 3/1/24 (Collateralized by (U.S. Government Obligations)) # | | 235,232,685 | 235,198,000 |

| With: | | | |

| ABN AMRO Bank NV at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Government Obligations valued at $5,100,752, 3.00% - 6.50%, 7/1/51 - 2/1/54) | | 5,000,738 | 5,000,000 |

| Bank of America NA at 5.41%, dated 1/5/24 due 5/6/24 (Collateralized by U.S. Government Obligations valued at $3,085,752, 3.50%, 7/1/42) | | 3,055,002 | 3,000,000 |

| BMO Harris Bank NA at 5.34%, dated 2/1/24 due 3/7/24 (Collateralized by U.S. Government Obligations valued at $4,097,551, 3.50%, 8/20/47) | | 4,035,600 | 4,000,000 |

| BNP Paribas, SA at: | | | |

5.32%, dated 1/17/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $5,145,744, 0.00% - 5.55%, 12/31/24 - 2/15/54) | | 5,067,239 | 5,000,000 |

5.33%, dated: | | | |

| 1/10/24 due 3/7/24 (Collateralized by U.S. Government Obligations valued at $5,139,745, 0.00% - 7.00%, 7/31/24 - 10/1/53) | | 5,045,157 | 5,000,000 |

| 1/11/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $8,300,870, 0.00% - 6.50%, 1/15/31 - 2/1/54) | | 8,071,067 | 8,000,000 |

5.4%, dated: | | | |

| 12/1/23 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $13,475,201, 0.00% - 6.50%, 8/15/27 - 8/1/53) | | 13,177,450 | 13,000,000 |

| 12/13/23 due 3/13/24 (Collateralized by U.S. Treasury Obligations valued at $6,252,634, 0.00% - 7.00%, 2/20/26 - 2/15/51) | | 6,081,900 | 6,000,000 |

| BNY Mellon Capital Markets Corp. at 5.35%, dated 2/1/24 due 3/21/24 (Collateralized by U.S. Treasury Obligations valued at $9,219,640, 0.00% - 5.50%, 4/16/24 - 2/1/54) | | 9,065,538 | 9,000,000 |

| BofA Securities, Inc. at: | | | |

5.34%, dated 2/1/24 due 3/7/24 (Collateralized by U.S. Government Obligations valued at $5,121,939, 4.00% - 6.50%, 2/1/46 - 1/1/54) | | 5,044,500 | 5,000,000 |

5.36%, dated 1/25/24 due 4/25/24 (Collateralized by U.S. Government Obligations valued at $3,076,402, 2.50% - 6.50%, 7/20/36 - 10/20/53) | | 3,040,647 | 3,000,000 |

5.37%, dated 1/26/24 due 4/26/24 (Collateralized by U.S. Government Obligations valued at $3,075,976, 4.50% - 6.00%, 9/1/43 - 8/1/53) (c)(d)(e) | | 3,040,723 | 3,000,000 |

5.38%, dated: | | | |

| 1/2/24 due 4/2/24 (Collateralized by U.S. Government Obligations valued at $23,667,054, 2.50% - 5.00%, 2/1/26 - 5/1/53) (c)(d)(e) | | 23,312,787 | 23,000,000 |

| 1/18/24 due 4/18/24 (Collateralized by Mortgage Loan Obligations valued at $10,265,547, 4.39% - 5.39%, 12/1/28 - 1/1/31) (c)(d)(e) | | 10,135,994 | 10,000,000 |

| CIBC Bank U.S.A. at 5.32%, dated 2/13/24 due 3/7/24 (Collateralized by U.S. Government Obligations valued at $11,248,187, 2.00% - 6.50%, 4/1/33 - 4/1/59) | | 11,047,141 | 11,000,000 |

| Citigroup Global Capital Markets, Inc. at 5.34%, dated 2/1/24 due 3/4/24 (Collateralized by U.S. Government Obligations valued at $8,196,717, 4.00% - 6.00%, 9/27/24 - 3/1/53) | | 8,037,973 | 8,000,000 |

| FICC State Street GC (Gov. Repo) at 5.32%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Government Obligations valued at $7,446,277, 1.50% - 6.50%, 10/31/30 - 8/1/53) | | 7,001,034 | 7,000,000 |

| Goldman Sachs & Co. at 5.32%, dated 2/26/24 due 3/4/24 (Collateralized by U.S. Treasury Obligations valued at $10,206,100, 0.75%, 5/31/26) | | 10,010,344 | 10,000,000 |

| ING Financial Markets LLC at 5.36%, dated: | | | |

2/1/24 due 3/21/24 (Collateralized by U.S. Government Obligations valued at $8,195,233, 6.00%, 9/1/53) | | 8,058,364 | 8,000,000 |

2/2/24 due 3/22/24 (Collateralized by U.S. Government Obligations valued at $4,097,009, 6.00%, 9/1/53) | | 4,029,182 | 4,000,000 |

| Mitsubishi UFJ Securities (U.S.A.), Inc. at 5.36%, dated 2/1/24 due 4/22/24 (Collateralized by U.S. Government Obligations valued at $23,561,295, 2.00% - 6.50%, 5/1/25 - 4/1/53) | | 23,277,380 | 23,000,000 |

| MUFG Securities (Canada), Ltd. at 5.36%, dated 2/1/24 due 4/22/24 (Collateralized by U.S. Treasury Obligations valued at $5,154,350, 0.38% - 6.00%, 7/15/25 - 6/1/53) | | 5,060,300 | 5,000,000 |

| RBC Financial Group at 5.34%, dated 2/1/24 due 3/7/24 (Collateralized by U.S. Government Obligations valued at $55,354,956, 0.63% - 8.00%, 1/15/26 - 3/1/54) | | 54,392,490 | 54,000,000 |

| TD Securities (U.S.A.) at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Government Obligations valued at $6,120,903, 2.50%, 5/20/51) | | 6,000,885 | 6,000,000 |

| Wells Fargo Securities, LLC at: | | | |

5.4%, dated 1/16/24 due 3/15/24 (Collateralized by U.S. Government Obligations valued at $7,188,196, 5.00%, 10/1/52) | | 7,061,950 | 7,000,000 |

5.43%, dated 12/19/23 due 3/21/24 (Collateralized by U.S. Government Obligations valued at $13,406,004, 5.50%, 2/1/54) | | 13,182,358 | 13,000,000 |

| TOTAL U.S. GOVERNMENT AGENCY REPURCHASE AGREEMENT (Cost $493,198,000) | | | 493,198,000 |

| | | | |

| U.S. Treasury Repurchase Agreement - 25.4% |

| | | Maturity Amount ($) | Value ($) |

| With: | | | |

| ABN AMRO Bank NV at 5.3%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $6,120,949, 0.38% - 0.75%, 9/30/27 - 1/31/28) | | 6,000,883 | 6,000,000 |

| Barclays Bank PLC at: | | | |

5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $21,423,175, 3.13%, 8/15/25) | | 21,003,098 | 21,000,000 |

5.33%, dated 2/2/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $16,387,656, 3.13%, 8/15/25) | | 16,113,707 | 16,000,000 |

| BNP Paribas, SA at: | | | |

5.32%, dated: | | | |

| 1/8/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $7,196,007, 1.13% - 5.36%, 7/31/24 - 8/15/53) | | 7,062,067 | 7,000,000 |

| 1/9/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $7,194,937, 1.13% - 4.13%, 7/31/27 - 8/15/53) | | 7,064,136 | 7,000,000 |

| 1/10/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $19,527,195, 1.38% - 4.75%, 7/31/29 - 11/15/53) | | 19,171,274 | 19,000,000 |

| 1/11/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $7,192,803, 0.00% - 5.45%, 4/4/24 - 8/15/52) | | 7,062,067 | 7,000,000 |

5.35%, dated 2/14/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $33,740,064, 0.63% - 5.36%, 7/31/24 - 2/15/54) (c)(d)(e) | | 33,593,404 | 33,000,000 |

5.39%, dated 12/1/23 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $6,203,400, 1.13% - 5.50%, 7/31/25 - 11/15/53) | | 6,081,748 | 6,000,000 |

| BofA Securities, Inc. at: | | | |

5.33%, dated 2/5/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $2,047,582, 2.75% - 3.88%, 8/15/33 - 8/15/42) | | 2,026,946 | 2,000,000 |

5.34%, dated 1/16/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $2,053,659, 2.75% - 3.88%, 8/15/33 - 8/15/42) (c)(d)(e) | | 2,019,283 | 2,000,000 |

5.35%, dated 1/25/24 due 4/25/24 (Collateralized by U.S. Treasury Obligations valued at $3,076,379, 2.75% - 3.88%, 8/15/33 - 8/15/42) (c)(d)(e) | | 3,040,571 | 3,000,000 |

| CIBC Bank U.S.A. at: | | | |

5.31%, dated 2/15/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $2,044,570, 3.25% - 3.88%, 5/15/42 - 2/15/43) | | 2,010,325 | 2,000,000 |

5.32%, dated: | | | |

| 1/30/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $2,049,386, 0.88% - 4.38%, 9/15/25 - 8/15/53) | | 2,015,073 | 2,000,000 |

| 2/2/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $3,072,838, 0.38% - 4.13%, 12/31/25 - 8/15/53) | | 3,021,280 | 3,000,000 |

5.33%, dated 1/29/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $5,125,355, 1.13% - 4.13%, 2/15/26 - 8/15/53) | | 5,042,936 | 5,000,000 |

| Federal Reserve Bank of New York at 5.3%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $90,013,280, 0.25% - 2.38%, 5/15/24 - 2/15/32) | | 90,013,250 | 90,000,000 |

| FICC ACAFB Repo Program at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $3,101,114, 2.88%, 5/15/52) | | 3,000,443 | 3,000,000 |

| Ficc Nomura Gc Repo (GOV REPO) at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $15,302,331, 0.00%, 10/31/24) | | 15,002,213 | 15,000,000 |

| Fixed Income Clearing Corp. - BNP at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $19,382,879, 1.13% - 5.57%, 7/31/24 - 11/15/53) | | 19,002,803 | 19,000,000 |

| Fixed Income Clearing Corp. - BNYM at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $109,140,013, 0.75%, 3/31/26) | | 107,015,783 | 107,000,000 |

| Fixed Income Clearing Corp. - SSB at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $76,518,450, 3.50%, 1/31/28) | | 75,011,063 | 75,000,000 |

| Fixed Income Clearing Corp.- Morgan Stanley & CO LLC at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $4,081,350, 3.50%, 4/30/28) | | 4,000,590 | 4,000,000 |

| Goldman Sachs & Co. at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $5,100,757, 1.25%, 9/30/28) | | 5,000,738 | 5,000,000 |

| ING Financial Markets LLC at: | | | |

5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $1,023,425, 4.00%, 2/28/30) | | 1,000,148 | 1,000,000 |

5.35%, dated: | | | |

| 1/31/24 due 3/21/24: | | | |

| (Collateralized by U.S. Treasury Obligations valued at $3,073,671, 1.13% - 3.88%, 4/30/25 - 8/15/43) | | 3,022,292 | 3,000,000 |

| (Collateralized by U.S. Treasury Obligations valued at $3,073,668, 0.50% - 4.13%, 10/31/27 - 8/15/42) | | 3,022,292 | 3,000,000 |

| 2/1/24 due 3/21/24: | | | |

| (Collateralized by U.S. Treasury Obligations valued at $3,073,243, 1.38% - 4.25%, 5/15/25 - 2/28/29) | | 3,021,846 | 3,000,000 |

| (Collateralized by U.S. Treasury Obligations valued at $3,073,198, 0.25% - 4.38%, 7/31/25 - 8/15/43) | | 3,021,846 | 3,000,000 |

| J.P. Morgan Securities, LLC at 5.33%, dated: | | | |

2/6/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $20,472,488, 0.00% - 5.38%, 8/8/24 - 2/15/31) (c)(d)(e) | | 20,130,289 | 20,000,000 |

2/8/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $12,279,861, 1.75% - 7.63%, 12/31/24 - 12/31/28) (c)(d)(e) | | 12,074,620 | 12,000,000 |

| Lloyds Bank Corp. Markets PLC at: | | | |

5.33%, dated 3/1/24 due 3/8/24 (Collateralized by U.S. Treasury Obligations valued at $2,039,139, 4.38%, 12/15/26) | | 2,002,073 | 2,000,000 |

5.39%, dated 1/5/24 due 3/5/24 (Collateralized by U.S. Treasury Obligations valued at $2,060,014, 1.38% - 4.63%, 9/15/26 - 10/31/28) | | 2,017,967 | 2,000,000 |

| Lloyds Bank PLC at 5.49%, dated 12/20/23 due 3/20/24 (Collateralized by U.S. Treasury Obligations valued at $4,123,786, 0.38% - 2.50%, 1/31/25 - 2/15/27) | | 4,055,510 | 4,000,000 |

| Mitsubishi UFJ Securities (U.S.A.), Inc. at 5.34%, dated 2/1/24 due 4/22/24 (Collateralized by U.S. Treasury Obligations valued at $6,146,327, 0.00% - 4.63%, 4/2/24 - 8/15/50) | | 6,072,090 | 6,000,000 |

| Mizuho Bank, Ltd. at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $7,188,802, 1.63%, 5/15/31) | | 7,001,033 | 7,000,000 |

| MUFG Securities (Canada), Ltd. at: | | | |

5.33%, dated 2/1/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $2,049,498, 1.75% - 4.38%, 8/15/26 - 11/15/51) | | 2,014,509 | 2,000,000 |

5.34%, dated 2/1/24 due 4/22/24 (Collateralized by U.S. Treasury Obligations valued at $4,097,580, 1.13% - 6.00%, 2/28/25 - 11/15/51) | | 4,048,060 | 4,000,000 |

| MUFG Securities EMEA PLC at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $8,164,019, 3.50%, 2/15/33) | | 8,001,180 | 8,000,000 |

| Natixis SA at: | | | |

5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $1,020,203, 0.75% - 5.50%, 1/31/26 - 6/30/30) | | 1,000,148 | 1,000,000 |

5.33%, dated 2/1/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $9,219,436, 0.00% - 4.38%, 5/23/24 - 2/15/49) | | 9,065,293 | 9,000,000 |

| NatWest Markets Securities, Inc. at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $1,020,187, 2.88%, 5/15/43) | | 1,000,148 | 1,000,000 |

| RBC Dominion Securities at 5.33%, dated 2/1/24 due 3/7/24 (Collateralized by U.S. Treasury Obligations valued at $5,122,089, 1.75% - 4.75%, 6/15/26 - 2/15/54) | | 5,036,274 | 5,000,000 |

| SMBC Nikko Securities America, Inc. at 5.31%, dated 2/29/24 due 3/1/24 (Collateralized by U.S. Treasury Obligations valued at $216,271,943, 0.00% - 7.50%, 5/30/24 - 8/15/43) | | 212,031,270 | 212,000,000 |

| TOTAL U.S. TREASURY REPURCHASE AGREEMENT (Cost $767,000,000) | | | 767,000,000 |

| | | | |

| TOTAL INVESTMENT IN SECURITIES - 105.8% (Cost $3,188,366,596) | 3,188,366,596 |

NET OTHER ASSETS (LIABILITIES) - (5.8)% | (175,634,581) |

| NET ASSETS - 100.0% | 3,012,732,015 |

| | |

The date shown for securities represents the date when principal payments must be paid, taking into account any call options exercised by the issuer and any permissible maturity shortening features other than interest rate resets.

Legend

| (a) | Yield represents either the annualized yield at the date of purchase, or the stated coupon rate, or, for floating and adjustable rate securities, the rate at period end. |

| (b) | Amount is stated in United States dollars unless otherwise noted. |

| (c) | Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end. |

| (d) | Coupon is indexed to a floating interest rate which may be multiplied by a specified factor and/or subject to caps or floors. |

| (e) | The maturity amount is based on the rate at period end. |

Investment Valuation

All investments are categorized as Level 2 under the Fair Value Hierarchy. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in these securities. For more information on valuation inputs, refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

| Other Information |

| # Additional information on each counterparty to the repurchase agreement is as follows: |

| Repurchase Agreement / Counterparty | Value ($) | |

| $235,198,000 due 3/01/24 at 5.31% | | |

| BNY Mellon Capital Markets LLC | 4,092,000 | |

| Bank of America, N.A. | 11,789,000 | |

| Bank of Nova Scotia | 3,538,000 | |

| BofA Securities, Inc. | 206,000 | |

| Citigroup Global Markets, Inc. | 10,845,000 | |

| Credit Agricole CIB New York Branch | 21,075,000 | |

| HSBC Securities (USA), Inc. | 16,215,000 | |

| ING Financial Markets LLC | 3,734,000 | |

| JP Morgan Securities LLC | 14,363,000 | |

| Mitsubishi UFJ Securities Holdings Ltd | 7,531,000 | |

| Mizuho Securities USA, Inc. | 4,911,000 | |

| Nomura Securities International | 16,356,000 | |

| RBC Dominion Securities, Inc. | 42,596,000 | |

| Royal Bank of Canada | 2,362,000 | |

| Sumitomo Mitsui Banking Corp. | 59,622,000 | |

| Sumitomo Mitsui Banking Corp. NY | 7,087,000 | |

| Wells Fargo Bank National Asso | 2,326,000 | |

| Wells Fargo Securities LLC | 6,550,000 | |

| | 235,198,000 | |

| Statement of Assets and Liabilities |

| | | | February 29, 2024 (Unaudited) |

| | | | | |

| Assets | | | | |

Investment in securities, at value (including repurchase agreements of $1,260,198,000) - See accompanying schedule Unaffiliated issuers (cost $3,188,366,596): | | | $ | 3,188,366,596 |

| Cash | | | | 28,000,480 |

| Receivable for fund shares sold | | | | 32,710,821 |

| Interest receivable | | | | 10,855,282 |

Total assets | | | | 3,259,933,179 |

| Liabilities | | | | |

| Payable for investments purchased | $ | 2,000,000 | | |

| Payable for fund shares redeemed | | 245,184,214 | | |

| Other payables and accrued expenses | | 16,950 | | |

| Total Liabilities | | | | 247,201,164 |

| Net Assets | | | $ | 3,012,732,015 |

| Net Assets consist of: | | | | |

| Paid in capital | | | $ | 3,012,703,198 |

| Total accumulated earnings (loss) | | | | 28,817 |

| Net Assets | | | $ | 3,012,732,015 |

Net Asset Value, offering price and redemption price per share ($3,012,732,015 ÷ 3,012,712,252 shares) | | | $ | 1.00 |

| Statement of Operations |

| | | | Six months ended February 29, 2024 (Unaudited) |

| Investment Income | | | | |

| Interest | | | $ | 126,141,511 |

| Expenses | | | | |

| Custodian fees and expenses | $ | 29,989 | | |

| Independent trustees' fees and expenses | | 7,877 | | |

| Miscellaneous | | 2 | | |

| Total Expenses | | | | 37,868 |

| Net Investment income (loss) | | | | 126,103,643 |

| Realized and Unrealized Gain (Loss) | | | | |

| Net realized gain (loss) on: | | | | |

| Investment Securities: | | | | |

| Unaffiliated issuers | | 13,072 | | |

| Total net realized gain (loss) | | | | 13,072 |

| Net increase in net assets resulting from operations | | | $ | 126,116,715 |

| Statement of Changes in Net Assets |

| |

| | Six months ended February 29, 2024 (Unaudited) | | Year ended August 31, 2023 |

| Increase (Decrease) in Net Assets | | | | |

| Operations | | | | |

| Net investment income (loss) | $ | 126,103,643 | $ | 187,036,655 |

| Net realized gain (loss) | | 13,072 | | (77,719) |

Net increase in net assets resulting from operations | | 126,116,715 | | 186,958,936 |

| Distributions to shareholders | | (126,102,075) | | (187,148,956) |

| | | | | |

| Share transactions | | | | |

| Proceeds from sales of shares | | 910,688,862 | | 5,147,361,735 |

| Reinvestment of distributions | | 126,058,743 | | 185,138,909 |

| Cost of shares redeemed | | (3,074,680,998) | | (2,654,426,557) |

| | | | | |

Net increase (decrease) in net assets and shares resulting from share transactions | | (2,037,933,393) | | 2,678,074,087 |

| Total increase (decrease) in net assets | | (2,037,918,753) | | 2,677,884,067 |

| | | | | |

| Net Assets | | | | |

| Beginning of period | | 5,050,650,768 | | 2,372,766,701 |

| End of period | $ | 3,012,732,015 | $ | 5,050,650,768 |

| | | | | |

| Other Information | | | | |

| Shares | | | | |

| Sold | | 910,688,862 | | 5,147,361,735 |

| Issued in reinvestment of distributions | | 126,058,743 | | 185,138,909 |

| Redeemed | | (3,074,680,998) | | (2,654,426,557) |

| Net increase (decrease) | | (2,037,933,393) | | 2,678,074,087 |

| | | | | |

Financial Highlights

| Fidelity® Series Government Money Market Fund |

| |

| | Six months ended (Unaudited) February 29, 2024 | | Years ended August 31, 2023 | | 2022 | | 2021 | | 2020 | | 2019 |

Selected Per-Share Data | | | | | | | | | | | | |

| Net asset value, beginning of period | $ | 1.00 | $ | 1.00 | $ | 1.00 | $ | 1.00 | $ | 1.00 | $ | 1.00 |

| Income from Investment Operations | | | | | | | | | | | | |

Net investment income (loss) A | | .027 | | .046 | | .003 | | .001 | | .010 | | .024 |

| Net realized and unrealized gain (loss) | | - B | | (.002) | | .002 | | - B | | .001 | | - B |

| Total from investment operations | | .027 | | .044 | | .005 | | .001 | | .011 | | .024 |

| Distributions from net investment income | | (.027) | | (.044) | | (.005) | | (.001) | | (.011) | | (.024) |

| Total distributions | | (.027) | | (.044) | | (.005) | | (.001) | | (.011) | | (.024) |

| Net asset value, end of period | $ | 1.00 | $ | 1.00 | $ | 1.00 | $ | 1.00 | $ | 1.00 | $ | 1.00 |

Total Return C,D | | 2.73% | | 4.54% | | .53% | | .10% | | 1.08% | | 2.38% |

Ratios to Average Net Assets A,E,F | | | | | | | | | | | | |

Expenses before reductions G | | -% H,I | | -% | | -% | | -% | | -% | | -% |

Expenses net of fee waivers, if any G | | -% H,I | | -% | | -% | | -% | | -% | | -% |

Expenses net of all reductions G | | -% H,I | | -% | | -% | | -% | | -% | | -% |

| Net investment income (loss) | | 5.42% H,I | | 4.59% | | .31% | | .10% | | .98% | | 2.35% |

| Supplemental Data | | | | | | | | | | | | |

| Net assets, end of period (000 omitted) | $ | 3,012,732 | $ | 5,050,651 | $ | 2,372,767 | $ | 9,692,737 | $ | 9,500,272 | $ | 6,572,472 |

ANet investment income (loss) is affected by the timing of the declaration of dividends by any underlying mutual funds or exchange-traded funds (ETFs). Net investment income (loss) of any mutual funds or ETFs is not included in the Fund's net investment income (loss) ratio.

BAmount represents less than $.0005 per share.

CTotal returns for periods of less than one year are not annualized.

DTotal returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

EFees and expenses of any underlying mutual funds or exchange-traded funds (ETFs) are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of these expenses.

FExpense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed, waived, or reduced through arrangements with the investment adviser, brokerage services, or other offset arrangements, if applicable, and do not represent the amount paid by the class during periods when reimbursements, waivers or reductions occur.

GAmount represents less than .005%.

HProxy expenses are not annualized.

IAnnualized.

For the period ended February 29, 2024

1. Organization.

Fidelity Series Government Money Market Fund (the Fund) is a fund of Fidelity Salem Street Trust (the Trust) and is authorized to issue an unlimited number of shares. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust. Shares are offered only to certain other Fidelity funds, Fidelity managed 529 plans, and Fidelity managed collective investment trusts.

2. Significant Accounting Policies.

The Fund is an investment company and applies the accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 Financial Services - Investment Companies. The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The Fund's Schedule of Investments lists any underlying mutual funds or exchange-traded funds (ETFs) but does not include the underlying holdings of these funds. The following summarizes the significant accounting policies of the Fund:

Investment Valuation. The Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

Level 1 - unadjusted quoted prices in active markets for identical investments

Level 2 - other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, etc.)

Level 3 - unobservable inputs (including the Fund's own assumptions based on the best information available)

As permitted by compliance with certain conditions under Rule 2a-7 of the 1940 Act, securities are valued at amortized cost, which approximates fair value. The amortized cost of an instrument is determined by valuing it at its original cost and thereafter amortizing any discount or premium from its face value at a constant rate until maturity. Securities held by a money market fund are generally high quality and liquid; however, they are reflected as Level 2 because the inputs used to determine fair value are not quoted prices in an active market.

Investment Transactions and Income. The net asset value per share for processing shareholder transactions is calculated as of the close of business of the New York Stock Exchange (NYSE), normally 4:00 p.m. Eastern time. Security transactions are accounted for as of trade date. Gains and losses on securities sold are determined on the basis of identified cost. Interest income is accrued as earned and includes coupon interest and amortization of premium and accretion of discount on debt securities as applicable.

Expenses. Expenses directly attributable to a fund are charged to that fund. Expenses attributable to more than one fund are allocated among the respective funds on the basis of relative net assets or other appropriate methods. Expenses included in the accompanying financial statements reflect the expenses of that fund and do not include any expenses associated with any underlying mutual funds or exchange-traded funds. Although not included in a fund's expenses, a fund indirectly bears its proportionate share of these expenses through the net asset value of each underlying mutual fund or exchange-traded fund. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

Income Tax Information and Distributions to Shareholders. Each year, the Fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code, including distributing substantially all of its taxable income and realized gains. As a result, no provision for U.S. Federal income taxes is required. The Fund files a U.S. federal tax return, in addition to state and local tax returns as required. The Fund's federal income tax returns are subject to examination by the Internal Revenue Service (IRS) for a period of three fiscal years after they are filed. State and local tax returns may be subject to examination for an additional fiscal year depending on the jurisdiction.

Distributions are declared and recorded daily and paid monthly from net investment income. Distributions from realized gains, if any, are declared and recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

Capital accounts within the financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Capital accounts are not adjusted for temporary book-tax differences which will reverse in a subsequent period.

Book-tax differences are primarily due to capital loss carryforwards and losses deferred due to wash sales.

As of period end, the cost and unrealized appreciation (depreciation) in securities for federal income tax purposes were as follows:

| Gross unrealized appreciation | $- |

| Gross unrealized depreciation | - |

| Net unrealized appreciation (depreciation) | $- |

| Tax cost | $3,188,366,596 |

Capital loss carryforwards are only available to offset future capital gains of the Fund to the extent provided by regulations and may be limited. The capital loss carryforward information presented below, including any applicable limitation, is estimated as of prior fiscal period end and is subject to adjustment.

Short-term | $- |

Long-term | (80,258) |

| Total capital loss carryforward | $(80,258) |

Repurchase Agreements. Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, funds and other registered investment companies having management contracts with Fidelity Management and Research Company LLC, or its affiliates are permitted to transfer uninvested cash balances into joint trading accounts which are then invested in repurchase agreements. Funds may also invest directly with institutions in repurchase agreements. Repurchase agreements may be collateralized by cash or government securities. Upon settlement date, collateral is held in segregated accounts with custodian banks and may be obtained in the event of a default of the counterparty. The collateral balance is monitored on a daily basis to ensure it is at least equal to the principal amount of the repurchase agreement (including accrued interest). In the event of a default by the counterparty, realization of the collateral proceeds could be delayed, during which time the value of the collateral may decline.

3. Fees and Other Transactions with Affiliates.

Management Fee. Fidelity Management & Research Company LLC (the investment adviser) and its affiliates provide the Fund with investment management related services for which the Fund does not pay a management fee. Under the management contract, the investment adviser or an affiliate pays all ordinary operating expenses of the Fund, except custody fees, fees and expenses of the independent Trustees, and certain miscellaneous expenses such as proxy and shareholder meeting expenses.

Interfund Trades. Funds may purchase from or sell securities to other Fidelity Funds under procedures adopted by the Board. The procedures have been designed to ensure these interfund trades are executed in accordance with Rule 17a-7 of the 1940 Act. During the period, there were no interfund trades.

Subsequent Event - Sub-Advisory Arrangements. Effective March 1, 2024, the Fund's sub-advisory agreements with FMR Investment Management (UK) Limited, Fidelity Management & Research (Hong Kong) Limited, and Fidelity Management & Research (Japan) Limited will be amended to provide that the investment adviser will pay each sub-adviser monthly fees equal to 110% of the sub-adviser's costs for providing sub-advisory services.

4. Other.

A fund's organizational documents provide former and current trustees and officers with a limited indemnification against liabilities arising in connection with the performance of their duties to the fund. In the normal course of business, a fund may also enter into contracts that provide general indemnifications. A fund's maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against a fund. The risk of material loss from such claims is considered remote.

At the end of the period, mutual funds and accounts managed by the investment adviser or its affiliates were the owners of record of all of the outstanding shares of the Fund.

5. Risk and Uncertainties.

Many factors affect a fund's performance. Developments that disrupt global economies and financial markets, such as pandemics, epidemics, outbreaks of infectious diseases, war, terrorism, and environmental disasters, may significantly affect a fund's investment performance. The effects of these developments to a fund will be impacted by the types of securities in which a fund invests, the financial condition, industry, economic sector, and geographic location of an issuer, and a fund's level of investment in the securities of that issuer. Significant concentrations in security types, issuers, industries, sectors, and geographic locations may magnify the factors that affect a fund's performance.

As a shareholder, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments or redemption proceeds, as applicable and (2) ongoing costs, which generally include management fees, distribution and/or service (12b-1) fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in a fund and to compare these costs with the ongoing costs of investing in other mutual funds.

| The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (September 1, 2023 to February 29, 2024). |

Actual Expenses

The first line of the accompanying table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line for a class/Fund under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. If any fund is a shareholder of any underlying mutual funds or exchange-traded funds (ETFs) (the Underlying Funds), such fund indirectly bears its proportional share of the expenses of the Underlying Funds in addition to the direct expenses incurred presented in the table. These fees and expenses are not included in the annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. If any fund is a shareholder of any Underlying Funds, such fund indirectly bears its proportional share of the expenses of the Underlying Funds in addition to the direct expenses as presented in the table. These fees and expenses are not included in the annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | Annualized Expense Ratio- A | | Beginning Account Value September 1, 2023 | | Ending Account Value February 29, 2024 | | Expenses Paid During Period- C September 1, 2023 to February 29, 2024 |

| | | | | | | | | | |

| Fidelity® Series Government Money Market Fund | | | | -%-D | | | | | | |

| Actual | | | | | | $ 1,000 | | $ 1,027.30 | | $-E |

Hypothetical-B | | | | | | $ 1,000 | | $ 1,024.86 | | $-E |

| |

A Annualized expense ratio reflects expenses net of applicable fee waivers.

B 5% return per year before expenses

C Expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 182/ 366 (to reflect the one-half year period). The fees and expenses of any Underlying Funds are not included in each annualized expense ratio.

D Amount represents less than .005%.

E Amount represents less than $.005.

Board Approval of Investment Advisory Contracts and Management Fees

Fidelity Series Government Money Market Fund

Each year, the Board of Trustees, including the Independent Trustees (together, the Board), considers the renewal of the fund's management contract with Fidelity Management & Research Company LLC (FMR) and the sub-advisory agreements (together, the Advisory Contracts) for the fund. FMR and the sub-advisers are referred to herein as the Investment Advisers. The Board, assisted by the advice of fund counsel and Independent Trustees' counsel, requests and considers a broad range of information relevant to the renewal of the Advisory Contracts throughout the year.

The Board meets regularly and, at each of its meetings, covers an extensive agenda of topics and materials and considers factors that are relevant to its annual consideration of the renewal of the fund's Advisory Contracts, including the services and support provided to the fund and its shareholders. The Board's Operations Committee, of which all the Independent Trustees are members, meets regularly throughout the year and requests, receives and considers, among other matters, information related to the annual consideration of the renewal of the fund's Advisory Contracts before making its recommendation to the Board. The Board also meets as needed to review matters specifically related to the Board's annual consideration of the renewal of the Advisory Contracts. Members of the Board may also meet from time to time with trustees of other Fidelity funds through joint ad hoc committees to discuss certain matters relevant to all of the Fidelity funds.

At its September 2023 meeting, the Board unanimously determined to renew the fund's Advisory Contracts. In considering whether to renew the Advisory Contracts for the fund, the Board considered all factors it believed relevant and reached a determination, with the assistance of fund counsel and Independent Trustees' counsel and through the exercise of its business judgment, that the renewal of the Advisory Contracts was in the best interests of the fund and its shareholders and the fact that no fee is payable under the management contract was fair and reasonable in light of all of the surrounding circumstances.

Nature, Extent, and Quality of Services Provided. The Board considered staffing as it relates to the fund, including the backgrounds and experience of investment personnel of the Investment Advisers, and also considered the Investment Advisers' implementation of the fund's investment program. The Independent Trustees also had discussions with senior management of Fidelity's investment operations and investment groups. The Board considered the structure of the investment personnel compensation program and whether this structure provides appropriate incentives to act in the best interests of the fund.

Resources Dedicated to Investment Management and Support Services. The Board reviewed the general qualifications and capabilities of Fidelity's investment staff, including its size, education, experience, and resources, as well as Fidelity's approach to recruiting, training, managing, and compensating investment personnel. The Board noted the resources devoted to Fidelity's global investment organization, and that Fidelity's analysts have extensive resources, tools and capabilities that allow them to conduct quantitative and fundamental analysis, as well as credit analysis of issuers, counterparties and guarantors. Further, the Board considered that Fidelity's investment professionals have sufficient access to global information and data so as to provide competitive investment results over time, and that those professionals also have access to sophisticated tools that permit them to assess portfolio construction and risk and performance attribution characteristics continuously, as well as to transmit new information and research conclusions rapidly around the world. Additionally, in its deliberations, the Board considered Fidelity's trading, risk management, compliance, cybersecurity, and technology and operations capabilities and resources, which are integral parts of the investment management process.

Administrative Services. The Board considered (i) the nature, extent, quality, and cost of advisory and administrative services performed by the Investment Advisers and their affiliates under the Advisory Contracts and under separate agreements covering transfer agency and pricing and bookkeeping; (ii) the nature and extent of Fidelity's supervision of third party service providers, principally custodians, subcustodians, and pricing vendors; and (iii) the resources devoted by Fidelity to, and the record of compliance with, the fund's compliance policies and procedures.

Investment Performance. The Board reviewed the fund's absolute investment performance, as well as the fund's relative investment performance. In this regard, the Board noted that the fund is designed to offer an investment option for other investment companies, collective investment trusts, and 529 plans managed by Fidelity and ultimately to enhance the performance of those investment companies, collective investment trusts, and 529 plans.

Based on its review, the Board concluded that the nature, extent, and quality of services provided to the fund under the Advisory Contracts should continue to benefit the shareholders of the fund.

Competitiveness of Management Fee and Total Expense Ratio. The Board considered that the fund does not pay FMR a management fee for investment advisory services, but that FMR receives fees for providing services to funds, collective investment trusts, and 529 plans that invest in the fund. The Board also noted that FMR or an affiliate undertakes to pay all operating expenses of the fund, except transfer agent fees, 12b-1 fees, Independent Trustee fees and expenses, custodian fees and expenses, proxy and shareholder meeting expenses, interest, taxes, and extraordinary expenses (such as litigation expenses). The Board further noted that the fund pays its non-operating expenses, including brokerage commissions and fees and expenses associated with the fund's securities lending program, if applicable.

The Board further considered that FMR has contractually agreed to reimburse the fund to the extent that total operating expenses, with certain exceptions, as a percentage of its average net assets, exceed 0.003% through December 31, 2025.

Based on its review, the Board considered that the fund does not pay a management fee and concluded that the fund's total expense ratio was reasonable in light of the services that the fund and its shareholders receive and the other factors considered.

Costs of the Services and Profitability. The Board considered the level of Fidelity's profits in respect of all the Fidelity funds.

A public accounting firm has been engaged annually by the Board as part of the Board's assessment of Fidelity's profitability analysis. The engagement includes the review and assessment of the methodologies used by Fidelity in determining the revenues and expenses attributable to Fidelity's fund business, and completion of agreed-upon procedures in respect of the mathematical accuracy of certain fund profitability information and its conformity to established allocation methodologies. After considering the reports issued under the engagement and information provided by Fidelity, the Board concluded that while other allocation methods may also be reasonable, Fidelity's profitability methodologies are reasonable in all material respects.

The Board also reviewed Fidelity's non-fund businesses and potential indirect benefits such businesses may have received as a result of their association with Fidelity's fund business (i.e., fall-out benefits) as well as cases where Fidelity's affiliates may benefit from the funds' business. The Board considered areas where potential indirect benefits to the Fidelity funds from their relationships with Fidelity may exist. The Board's consideration of these matters was informed by the findings of a joint ad hoc committee created by it and the boards of other Fidelity funds to evaluate potential fall-out benefits.

The Board concluded that the costs of the services provided by and the profits realized by Fidelity in connection with the operation of the fund were not relevant to the renewal of the Advisory Contracts because the fund pays no advisory fees and FMR or an affiliate bears all expenses of the fund, with limited exceptions.

Economies of Scale. The Board concluded that because the fund pays no advisory fees and FMR or an affiliate bears all expenses of the fund with certain limited exceptions, the realization of economies of scale was not a material factor in the Board's decision to renew the fund's Advisory Contracts.

Additional Information Requested by the Board. In order to develop fully the factual basis for consideration of the Fidelity funds' advisory contracts, the Board requested and received additional information on certain topics, including: (i) Fidelity's fund profitability methodology, profitability trends for certain funds, the allocation of various costs to different funds, and the impact of certain factors on fund profitability results; (ii) portfolio manager changes that have occurred during the past year and Fidelity's views regarding portfolio manager investment in the Fidelity funds that they manage; (iii) hiring, training, and retaining personnel; (iv) the arrangements with and compensation paid to certain fund sub-advisers and the treatment of such compensation within Fidelity's fund profitability methodology; (v) the terms of the funds' various management fee structures, including the basic group fee and the terms of Fidelity's voluntary expense limitation arrangements; (vi) Fidelity's transfer agent, pricing and bookkeeping fees, expense and service structures for different funds and classes relative to competitive trends and market conditions; (vii) the impact on fund profitability of recent industry trends, such as the growth in passively managed funds and the changes in flows for different types of funds; (viii) the types of management fee and total expense comparisons provided, and the challenges and limitations associated with such information; (ix) explanations regarding the relative total expense ratios and management fees of certain funds and classes, total expense and management fee competitive trends, and methodologies for total expense and management fee competitive comparisons; (x) information concerning expense limitations applicable to certain funds; and (xi) matters related to money market funds, exchange-traded funds, and target date funds.

Conclusion. Based on its evaluation of all of the conclusions noted above, and after considering all factors it believed relevant, the Board, including the Independent Trustees, concluded that the advisory and sub-advisory fee arrangements are fair and reasonable in light of all of the surrounding circumstances and that the fund's Advisory Contracts should be renewed through September 30, 2024.

Board Approval of Investment Advisory Contracts

Fidelity Series Government Money Market Fund

At its January 2024 meeting, the Board of Trustees, including the Independent Trustees (together, the Board), approved amended and restated sub-advisory agreements (the Sub-Advisory Contracts) for the fund, including the fund's sub-advisory agreements with FMR Investment Management (UK) Limited (FMR UK), Fidelity Management & Research (Hong Kong) Limited (FMR H.K.), and Fidelity Management & Research (Japan) Limited (FMR Japan). The Sub-Advisory Contracts will be effective March 1, 2024. The Board will consider the annual renewal of the fund's Sub-Advisory Contracts in September 2024, following its review of additional materials provided by FMR.

The Board considered the Sub-Advisory Contracts, which changed the arrangements for fees paid by FMR to the sub-advisers under the agreements. The Board noted that the agreements with FMR UK, FMR H.K., and FMR Japan were amended to provide that FMR will compensate each sub-adviser at a fee equal to 110% of the sub-adviser's costs incurred in providing services under the agreement. The Board considered that, under the Sub-Advisory Contracts, FMR, and not the fund, will continue to pay the sub-advisory fees to each applicable sub-adviser, and that the management fee paid by the fund under the management contract with FMR will remain unchanged.

The Board considered that the approval of the fund's Sub-Advisory Contracts will not result in any changes in the investment process or strategies employed in the management of the fund's assets or the day-to-day management of the fund or the persons primarily responsible for such management. Further, the Board considered that the Sub-Advisory Contracts would not change the obligations and services of FMR and its affiliates on behalf of the fund, and, in particular, there would be no change in the nature and level of services provided to the fund by FMR and its affiliates.

In connection with its consideration of future renewals of the fund's advisory contracts, the Board will consider: (i) the nature, extent and quality of services provided to the funds, including shareholder and administrative services and investment performance; (ii) the competitiveness of the management fee and total expenses for the fund; (iii) the costs of the services and profitability, including the revenues earned and the expenses incurred in conducting the business of developing, marketing, distributing, managing, administering, and servicing the fund and its shareholders, to the extent applicable; and (iv) whether there have been economies of scale in respect of the Fidelity funds, whether the Fidelity funds (including the fund) have appropriately benefited from any such economies of scale, and whether there is the potential for realization of any further economies.

Based on its evaluation of all of the conclusions noted above, and after considering all factors it believed relevant, the Board concluded that the fund's management fee structure is fair and reasonable, and that the fund's Sub-Advisory Contracts should be approved.

| A special meeting of shareholders was held on October 18, 2023. The results of votes taken among shareholders on the proposal before them are reported below. Each vote reported represents one dollar of net asset value held on the record date for the meeting. |

| Proposal 1 |

| To elect a Board of Trustees. |

| | # of Votes | % of Votes |

| Abigail P. Johnson |

| Affirmative | 378,729,502,260.01 | 97.58 |

| Withheld | 9,407,876,478.96 | 2.42 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Jennifer Toolin McAuliffe |

| Affirmative | 378,454,868,010.95 | 97.51 |

| Withheld | 9,682,510,728.02 | 2.49 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Christine J. Thompson |

| Affirmative | 378,837,121,274.52 | 97.60 |

| Withheld | 9,300,257,464.45 | 2.40 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Elizabeth S. Acton |

| Affirmative | 378,262,110,794.85 | 97.46 |

| Withheld | 9,875,267,944.12 | 2.54 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Laura M. Bishop |

| Affirmative | 380,482,113,171.06 | 98.03 |

| Withheld | 7,655,265,567.91 | 1.97 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Ann E. Dunwoody |

| Affirmative | 380,016,034,008.12 | 97.91 |

| Withheld | 8,121,344,730.85 | 2.09 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| John Engler |

| Affirmative | 379,432,488,394.20 | 97.76 |

| Withheld | 8,704,890,344.77 | 2.24 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Robert F. Gartland |

| Affirmative | 378,741,819,600.60 | 97.58 |

| Withheld | 9,395,559,138.37 | 2.42 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Robert W. Helm |

| Affirmative | 380,389,324,755.07 | 98.00 |

| Withheld | 7,748,053,983.90 | 2.00 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Arthur E. Johnson |

| Affirmative | 378,427,694,151.67 | 97.50 |

| Withheld | 9,709,684,587.30 | 2.50 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Michael E. Kenneally |

| Affirmative | 377,842,228,145.18 | 97.35 |

| Withheld | 10,295,150,593.79 | 2.65 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Mark A. Murray |

| Affirmative | 380,158,432,703.37 | 97.94 |

| Withheld | 7,978,946,035.60 | 2.06 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| Carol J. Zierhoffer |

| Affirmative | 380,522,113,360.24 | 98.04 |

| Withheld | 7,615,265,378.73 | 1.96 |

| TOTAL | 388,137,378,738.97 | 100.00 |

| | | |

| Proposal 1 reflects trust wide proposal and voting results. |

1.9878696.107

GVM-SANN-0424

Fidelity® Investment Grade Bond Fund

Semi-Annual Report

February 29, 2024

Includes Fidelity and Fidelity Advisor share classes

Contents

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-544-8544 if you're an individual investing directly with Fidelity, call 1-800-835-5092 if you're a plan sponsor or participant with Fidelity as your recordkeeper or call 1-877-208-0098 on institutional accounts or if you're an advisor or invest through one to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2024 FMR LLC. All rights reserved.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT. Forms N-PORT are available on the SEC's web site at http://www.sec.gov. A fund's Forms N-PORT may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.institutional.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED •MAY LOSE VALUE •NO BANK GUARANTEE

Neither the Fund nor Fidelity Distributors Corporation is a bank.

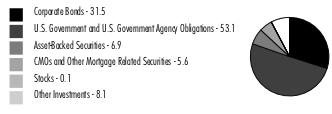

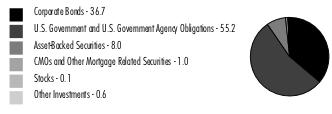

The information in the following tables is based on the combined Investments of the Fund and its pro-rata share of investments in Fidelity's Central Funds, other than the Money Market Central Funds.

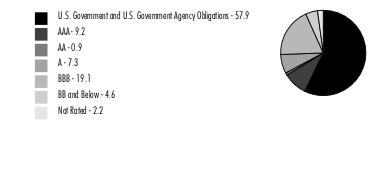

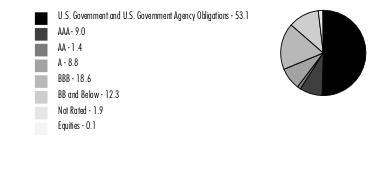

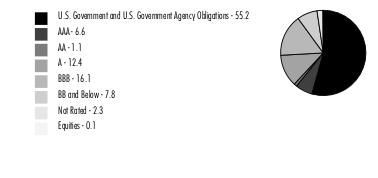

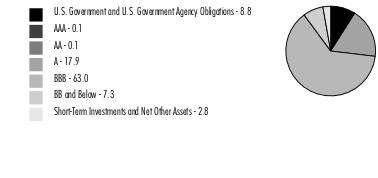

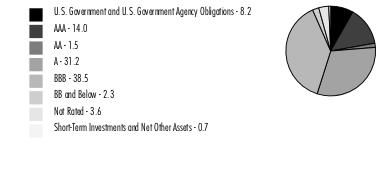

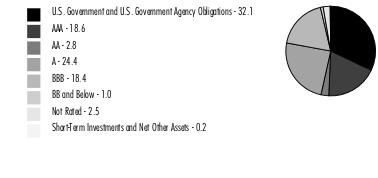

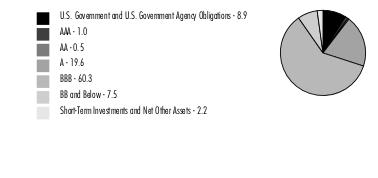

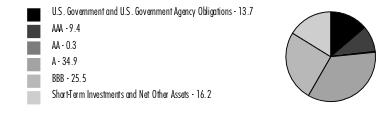

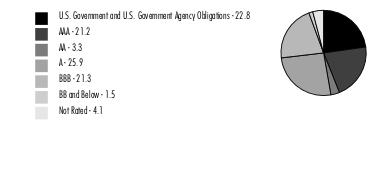

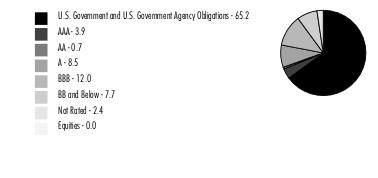

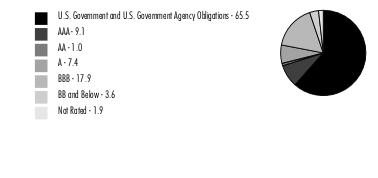

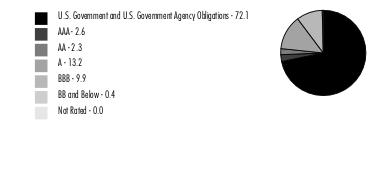

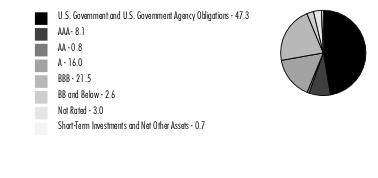

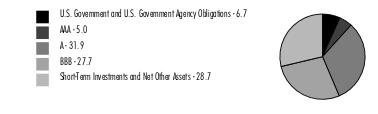

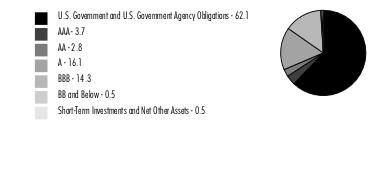

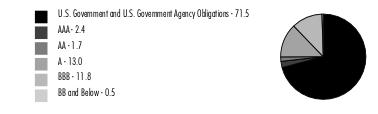

Quality Diversification (% of Fund's net assets) |

|

Short-Term Investments and Net Other Assets (Liabilities) - (1.2)% |

| |

| We have used ratings from Moody's Investors Service, Inc. Where Moody's® ratings are not available, we have used S&P® ratings. All ratings are as of the date indicated and do not reflect subsequent changes. |

Securities rated BB or below were rated investment grade at the time of acquisition.

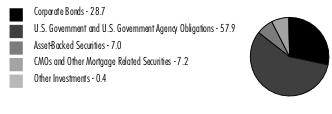

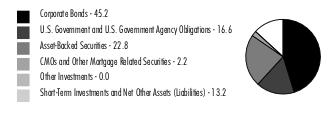

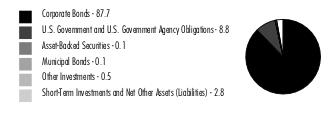

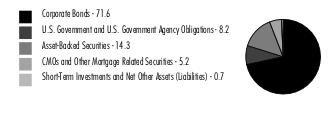

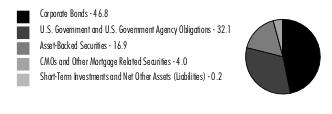

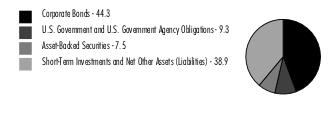

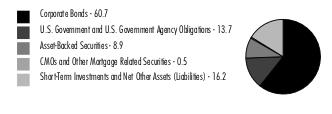

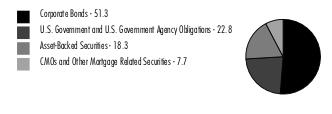

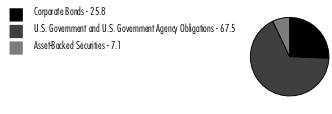

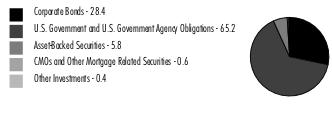

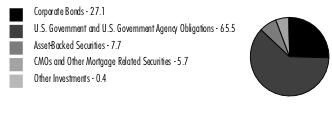

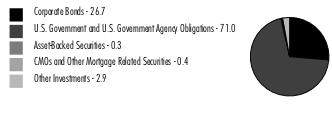

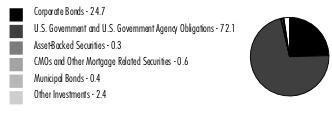

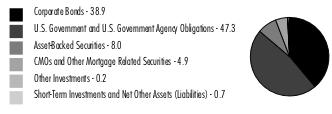

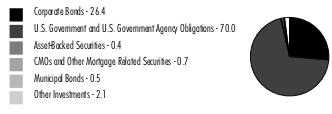

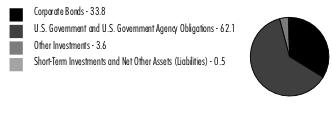

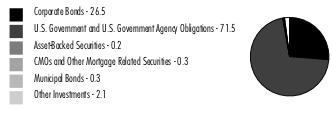

Asset Allocation (% of Fund's net assets) |

|

Short-Term Investments and Net Other Assets (Liabilities) - (1.2)% |

Written options - (0.3)% |

Futures and Swaps - (0.7)% |

Percentages in the above tables are adjusted for the effect of TBA Sale Commitments. |

|

An unaudited holdings listing for the Fund, which presents direct holdings as well as the pro-rata share of any securities and other investments held indirectly through its investment in underlying non-money market Fidelity Central Funds, is available at fidelity.com and/or institutional. fidelity.com, as applicable.

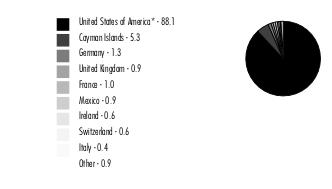

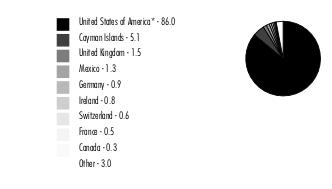

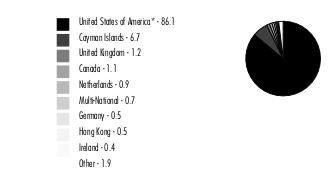

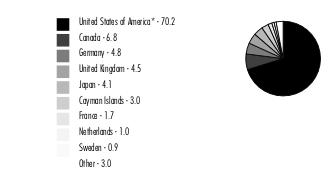

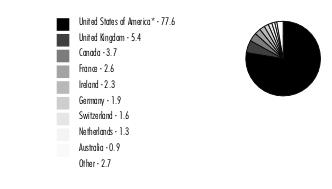

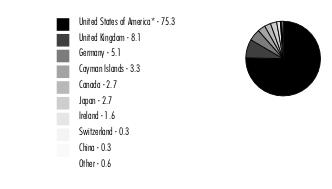

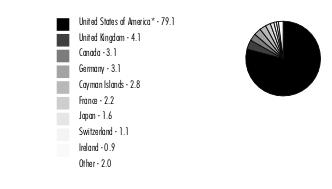

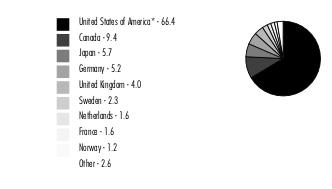

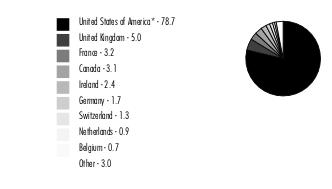

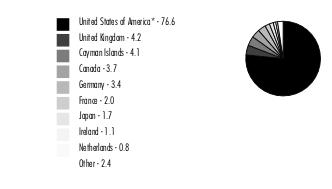

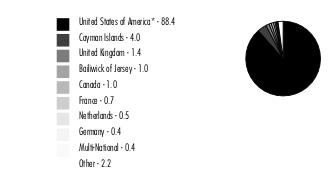

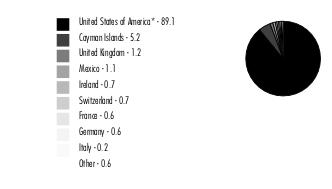

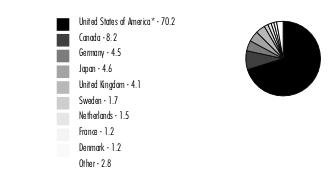

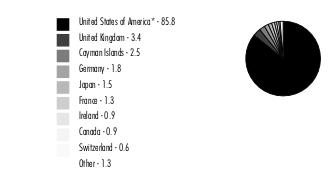

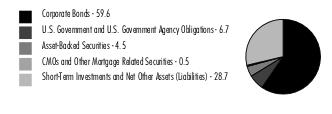

Geographic Diversification (% of Fund's net assets) |

|

* Includes Short-Term investments and Net Other Assets (Liabilities). Percentages are adjusted for the effect of derivatives, if applicable. |

| |

Showing Percentage of Net Assets

| Nonconvertible Bonds - 27.3% |

| | | Principal Amount (a) (000s) | Value ($) (000s) |

| COMMUNICATION SERVICES - 2.5% | | | |

| Diversified Telecommunication Services - 0.6% | | | |

| AT&T, Inc.: | | | |

| 2.55% 12/1/33 | | 1,806 | 1,424 |

| 4.3% 2/15/30 | | 34,036 | 32,460 |

| Verizon Communications, Inc.: | | | |

| 2.987% 10/30/56 | | 869 | 540 |

| 4.5% 8/10/33 | | 3,429 | 3,236 |

| 4.862% 8/21/46 | | 14,251 | 13,062 |

| | | | 50,722 |

| Media - 1.6% | | | |

| Charter Communications Operating LLC/Charter Communications Operating Capital Corp.: | | | |

| 2.8% 4/1/31 | | 25,400 | 20,526 |

| 3.7% 4/1/51 | | 15,400 | 9,348 |

| 3.85% 4/1/61 | | 4,000 | 2,323 |

| 3.9% 6/1/52 | | 7,000 | 4,401 |

| 4.8% 3/1/50 | | 12,000 | 8,683 |

| 5.375% 5/1/47 | | 22,326 | 17,631 |

| 5.75% 4/1/48 | | 11,014 | 9,169 |

| 6.834% 10/23/55 | | 7,000 | 6,633 |

| Comcast Corp. 3.75% 4/1/40 | | 622 | 509 |

| Discovery Communications LLC: | | | |

| 3.625% 5/15/30 | | 4,063 | 3,571 |

| 4.65% 5/15/50 | | 10,998 | 8,340 |

| Fox Corp.: | | | |

| 5.476% 1/25/39 | | 1,366 | 1,276 |

| 5.576% 1/25/49 | | 906 | 829 |

| Time Warner Cable LLC: | | | |

| 4.5% 9/15/42 | | 544 | 398 |

| 5.5% 9/1/41 | | 966 | 796 |

| 5.875% 11/15/40 | | 7,077 | 6,104 |

| 6.55% 5/1/37 | | 3,601 | 3,392 |

| 6.75% 6/15/39 | | 6,233 | 5,881 |

| 7.3% 7/1/38 | | 2,390 | 2,383 |

| Warnermedia Holdings, Inc.: | | | |

| 3.755% 3/15/27 | | 5,285 | 5,001 |

| 4.054% 3/15/29 | | 1,832 | 1,697 |

| 4.279% 3/15/32 | | 5,334 | 4,706 |

| 5.05% 3/15/42 | | 2,865 | 2,409 |

| 5.141% 3/15/52 | | 27,262 | 22,153 |

| | | | 148,159 |

| Wireless Telecommunication Services - 0.3% | | | |

| T-Mobile U.S.A., Inc.: | | | |

| 3.75% 4/15/27 | | 6,800 | 6,518 |

| 3.875% 4/15/30 | | 20,000 | 18,564 |

| | | | 25,082 |

TOTAL COMMUNICATION SERVICES | | | 223,963 |

| CONSUMER DISCRETIONARY - 1.3% | | | |

| Automobiles - 0.0% | | | |

| General Motors Financial Co., Inc. 5.85% 4/6/30 | | 3,042 | 3,082 |

| Broadline Retail - 0.2% | | | |

| Alibaba Group Holding Ltd.: | | | |

| 2.125% 2/9/31 | | 3,090 | 2,551 |

| 2.7% 2/9/41 | | 16,100 | 11,059 |

| | | | 13,610 |

| Household Durables - 0.3% | | | |

| Lennar Corp.: | | | |

| 4.75% 11/29/27 | | 15,563 | 15,315 |

| 5% 6/15/27 | | 8,419 | 8,349 |

| Toll Brothers Finance Corp. 4.35% 2/15/28 | | 2,908 | 2,795 |

| | | | 26,459 |

| Specialty Retail - 0.4% | | | |

| AutoNation, Inc. 4.75% 6/1/30 | | 909 | 865 |

| AutoZone, Inc. 4% 4/15/30 | | 21,631 | 20,360 |

| Lowe's Companies, Inc.: | | | |

| 3.75% 4/1/32 | | 2,515 | 2,285 |

| 4.25% 4/1/52 | | 10,263 | 8,246 |

| 4.45% 4/1/62 | | 10,550 | 8,423 |

| | | | 40,179 |

| Textiles, Apparel & Luxury Goods - 0.4% | | | |

| Tapestry, Inc.: | | | |

| 3.05% 3/15/32 | | 20,094 | 16,282 |

| 7% 11/27/26 | | 3,083 | 3,166 |

| 7.05% 11/27/25 | | 1,143 | 1,164 |

| 7.35% 11/27/28 | | 4,784 | 5,004 |

| 7.7% 11/27/30 | | 4,784 | 5,073 |

| 7.85% 11/27/33 | | 4,784 | 5,175 |

| | | | 35,864 |

TOTAL CONSUMER DISCRETIONARY | | | 119,194 |

| CONSUMER STAPLES - 1.1% | | | |

| Beverages - 0.1% | | | |

| Anheuser-Busch InBev Finance, Inc. 4.7% 2/1/36 | | 1,032 | 988 |

| Anheuser-Busch InBev Worldwide, Inc. 5.8% 1/23/59 (Reg. S) | | 8,567 | 9,094 |

| | | | 10,082 |

| Food Products - 1.0% | | | |

| JBS U.S.A. Lux SA/JBS Food Co./JBS U.S.A. Finance, Inc.: | | | |

| 2.5% 1/15/27 | | 14,165 | 12,996 |

| 3% 5/15/32 | | 14,250 | 11,409 |

| 3.625% 1/15/32 | | 1,330 | 1,118 |

| 5.125% 2/1/28 | | 4,285 | 4,198 |

| 5.5% 1/15/30 | | 39,620 | 38,615 |

| 5.75% 4/1/33 | | 8,830 | 8,563 |

| Kraft Heinz Foods Co. 7.125% 8/1/39 (b) | | 5,618 | 6,394 |

| | | | 83,293 |

TOTAL CONSUMER STAPLES | | | 93,375 |

| ENERGY - 2.4% | | | |

| Oil, Gas & Consumable Fuels - 2.4% | | | |

| Columbia Pipelines Operating Co. LLC: | | | |

| 5.927% 8/15/30 (b) | | 1,258 | 1,281 |

| 6.036% 11/15/33 (b) | | 3,393 | 3,484 |

| 6.497% 8/15/43 (b) | | 1,014 | 1,073 |

| 6.544% 11/15/53 (b) | | 1,826 | 1,945 |

| 6.714% 8/15/63 (b) | | 1,093 | 1,184 |

| DCP Midstream Operating LP 5.6% 4/1/44 | | 1,707 | 1,626 |

| Energy Transfer LP: | | | |

| 3.75% 5/15/30 | | 2,274 | 2,074 |

| 4.95% 6/15/28 | | 2,591 | 2,552 |

| 5% 5/15/50 | | 18,683 | 16,106 |

| 5.25% 4/15/29 | | 1,549 | 1,543 |

| 5.4% 10/1/47 | | 1,426 | 1,293 |

| 5.8% 6/15/38 | | 1,445 | 1,429 |

| 6% 6/15/48 | | 1,441 | 1,412 |

| 6.125% 12/15/45 | | 400 | 397 |

| 6.25% 4/15/49 | | 1,064 | 1,074 |

| Hess Corp.: | | | |

| 5.6% 2/15/41 | | 22,554 | 22,711 |

| 7.125% 3/15/33 | | 839 | 941 |

| 7.3% 8/15/31 | | 1,023 | 1,151 |

| 7.875% 10/1/29 | | 2,921 | 3,273 |

| Kinder Morgan, Inc. 3.6% 2/15/51 | | 18,000 | 12,354 |

| MPLX LP: | | | |

| 4.8% 2/15/29 | | 816 | 799 |

| 4.95% 9/1/32 | | 7,989 | 7,652 |

| 5.5% 2/15/49 | | 2,450 | 2,294 |

| Occidental Petroleum Corp.: | | | |

| 6.45% 9/15/36 | | 2,750 | 2,895 |

| 6.6% 3/15/46 | | 3,032 | 3,221 |

| 7.5% 5/1/31 | | 3,937 | 4,348 |

| Ovintiv, Inc.: | | | |

| 5.15% 11/15/41 | | 2,000 | 1,704 |

| 8.125% 9/15/30 | | 3,357 | 3,762 |

| Petroleos Mexicanos: | | | |

| 5.95% 1/28/31 | | 2,610 | 2,026 |

| 6.49% 1/23/27 | | 1,757 | 1,642 |

| 6.5% 3/13/27 | | 5,805 | 5,414 |

| 6.75% 9/21/47 | | 14,189 | 9,010 |

| 6.84% 1/23/30 | | 5,979 | 5,111 |

| 6.95% 1/28/60 | | 4,247 | 2,694 |

| 7.69% 1/23/50 | | 70,161 | 48,330 |

| Plains All American Pipeline LP/PAA Finance Corp. 3.55% 12/15/29 | | 1,242 | 1,127 |

| Sabine Pass Liquefaction LLC 4.5% 5/15/30 | | 9,286 | 8,886 |

| The Williams Companies, Inc.: | | | |

| 3.5% 11/15/30 | | 9,960 | 8,988 |

| 4.65% 8/15/32 | | 8,326 | 7,921 |

| 5.3% 8/15/52 | | 1,888 | 1,767 |

| Western Gas Partners LP: | | | |

| 4.65% 7/1/26 | | 1,129 | 1,105 |

| 4.75% 8/15/28 | | 781 | 754 |

| 5.25% 2/1/50 | | 7,720 | 6,830 |

| | | | 217,183 |

| FINANCIALS - 12.9% | | | |

| Banks - 7.3% | | | |

| Bank of America Corp.: | | | |

| 1.922% 10/24/31 (c) | | 20,000 | 16,139 |

| 2.299% 7/21/32 (c) | | 25,000 | 20,235 |

| 2.884% 10/22/30 (c) | | 50,000 | 44,033 |

| 4.183% 11/25/27 | | 4,363 | 4,218 |

| 4.25% 10/22/26 | | 23,937 | 23,421 |

| 5.015% 7/22/33 (c) | | 13,700 | 13,354 |

| Barclays PLC: | | | |

| 2.852% 5/7/26 (c) | | 9,444 | 9,130 |

| 4.375% 1/12/26 | | 2,821 | 2,764 |

| 4.836% 5/9/28 | | 3,683 | 3,549 |

| 5.088% 6/20/30 (c) | | 11,424 | 10,822 |

| 5.2% 5/12/26 | | 26,475 | 26,178 |

| BNP Paribas SA 2.219% 6/9/26 (b)(c) | | 9,008 | 8,623 |

| BPCE SA 4.875% 4/1/26 (b) | | 4,662 | 4,559 |

| Citigroup, Inc.: | | | |

| 2.976% 11/5/30 (c) | | 50,000 | 44,065 |

| 4.075% 4/23/29 (c) | | 16,389 | 15,642 |

| 4.125% 7/25/28 | | 4,363 | 4,150 |

| 4.3% 11/20/26 | | 1,115 | 1,086 |

| 4.412% 3/31/31 (c) | | 21,454 | 20,266 |

| 4.45% 9/29/27 | | 55,258 | 53,526 |

| 4.6% 3/9/26 | | 5,613 | 5,521 |

| 5.3% 5/6/44 | | 6,000 | 5,730 |

| Citizens Financial Group, Inc. 2.638% 9/30/32 | | 4,614 | 3,503 |

| Commonwealth Bank of Australia 3.61% 9/12/34 (b)(c) | | 2,250 | 2,002 |

| HSBC Holdings PLC: | | | |

| 4.25% 3/14/24 | | 905 | 904 |

| 4.95% 3/31/30 | | 1,541 | 1,509 |

| 5.25% 3/14/44 | | 656 | 625 |

| Intesa Sanpaolo SpA: | | | |

| 5.017% 6/26/24 (b) | | 836 | 831 |

| 5.71% 1/15/26 (b) | | 37,209 | 36,869 |

| JPMorgan Chase & Co.: | | | |

| 2.956% 5/13/31 (c) | | 5,034 | 4,372 |

| 4.493% 3/24/31 (c) | | 17,000 | 16,328 |

| 5.717% 9/14/33 (c) | | 65,747 | 66,571 |

| NatWest Group PLC: | | | |

| 3.073% 5/22/28 (c) | | 5,536 | 5,137 |

| 4.8% 4/5/26 | | 12,145 | 11,995 |

| 5.125% 5/28/24 | | 13,736 | 13,690 |

| Rabobank Nederland 4.375% 8/4/25 | | 3,024 | 2,966 |

| Societe Generale: | | | |

| 1.038% 6/18/25 (b)(c) | | 50,000 | 49,222 |

| 1.488% 12/14/26 (b)(c) | | 13,930 | 12,847 |

| 4.25% 4/14/25 (b) | | 4,491 | 4,394 |

| Wells Fargo & Co.: | | | |

| 3.196% 6/17/27 (c) | | 40,441 | 38,504 |

| 3.526% 3/24/28 (c) | | 11,202 | 10,621 |

| 4.3% 7/22/27 | | 16,184 | 15,711 |

| 4.478% 4/4/31 (c) | | 15,500 | 14,739 |

| Westpac Banking Corp. 4.11% 7/24/34 (c) | | 3,103 | 2,834 |

| | | | 653,185 |

| Capital Markets - 2.6% | | | |

| Ares Capital Corp.: | | | |

| 3.25% 7/15/25 | | 42,008 | 40,349 |

| 3.875% 1/15/26 | | 16,340 | 15,676 |

| Athene Global Funding: | | | |

| 5.339% 1/15/27 (b) | | 12,500 | 12,431 |

| 5.583% 1/9/29 (b) | | 6,252 | 6,229 |

| Blackstone Private Credit Fund 7.05% 9/29/25 | | 10,049 | 10,181 |

| Deutsche Bank AG 4.5% 4/1/25 | | 8,603 | 8,438 |

| Deutsche Bank AG New York Branch: | | | |

| 3.729% 1/14/32 (c) | | 8,509 | 6,970 |

| 4.1% 1/13/26 | | 5,262 | 5,133 |

| Goldman Sachs Group, Inc.: | | | |

| 2.383% 7/21/32 (c) | | 12,267 | 9,983 |

| 4.25% 10/21/25 | | 7,670 | 7,534 |

| 6.75% 10/1/37 | | 24,081 | 26,175 |

| Morgan Stanley: | | | |

| 3.622% 4/1/31 (c) | | 35,865 | 32,582 |

| 5% 11/24/25 | | 2,037 | 2,025 |

| UBS Group AG: | | | |

| 1.494% 8/10/27 (b)(c) | | 7,599 | 6,884 |

| 2.593% 9/11/25 (b)(c) | | 9,092 | 8,936 |

| 3.75% 3/26/25 | | 6,137 | 6,010 |

| 4.194% 4/1/31 (b)(c) | | 30,399 | 27,958 |

| | | | 233,494 |

| Consumer Finance - 1.9% | | | |

| AerCap Ireland Capital Ltd./AerCap Global Aviation Trust: | | | |

| 1.75% 1/30/26 | | 10,220 | 9,495 |

| 2.45% 10/29/26 | | 5,268 | 4,859 |

| 3% 10/29/28 | | 5,518 | 4,958 |

| 3.3% 1/30/32 | | 5,903 | 4,992 |

| 4.45% 4/3/26 | | 2,472 | 2,422 |

| 6.5% 7/15/25 | | 4,349 | 4,390 |

| Ally Financial, Inc.: | | | |

| 4.625% 3/30/25 | | 2,237 | 2,212 |

| 5.8% 5/1/25 | | 19,772 | 19,741 |

| 7.1% 11/15/27 | | 9,050 | 9,423 |

| 8% 11/1/31 | | 3,172 | 3,482 |

| Capital One Financial Corp.: | | | |

| 3.65% 5/11/27 | | 15,715 | 14,968 |

| 3.8% 1/31/28 | | 6,614 | 6,255 |

| 4.985% 7/24/26 (c) | | 8,087 | 8,013 |

| 5.247% 7/26/30 (c) | | 10,430 | 10,170 |

| 7.624% 10/30/31 (c) | | 7,729 | 8,458 |

| Discover Financial Services: | | | |

| 3.95% 11/6/24 | | 1,184 | 1,169 |

| 4.1% 2/9/27 | | 8,206 | 7,870 |

| 4.5% 1/30/26 | | 3,562 | 3,505 |

| 6.7% 11/29/32 | | 1,995 | 2,088 |

| Ford Motor Credit Co. LLC: | | | |

| 4.063% 11/1/24 | | 18,137 | 17,887 |

| 5.584% 3/18/24 | | 4,908 | 4,907 |

| Synchrony Financial: | | | |

| 3.95% 12/1/27 | | 5,215 | 4,831 |

| 4.25% 8/15/24 | | 7,369 | 7,301 |

| 4.375% 3/19/24 | | 5,520 | 5,516 |

| 5.15% 3/19/29 | | 6,486 | 6,187 |

| | | | 175,099 |

| Financial Services - 0.5% | | | |

| Brixmor Operating Partnership LP: | | | |

| 4.05% 7/1/30 | | 6,803 | 6,260 |

| 4.125% 6/15/26 | | 3,253 | 3,135 |

| 4.125% 5/15/29 | | 12,222 | 11,428 |

| Corebridge Financial, Inc.: | | | |

| 3.9% 4/5/32 | | 4,093 | 3,602 |

| 4.35% 4/5/42 | | 931 | 768 |

| 4.4% 4/5/52 | | 2,754 | 2,210 |

| Jackson Financial, Inc.: | | | |

| 3.125% 11/23/31 | | 955 | 790 |

| 5.17% 6/8/27 | | 3,740 | 3,716 |

| 5.67% 6/8/32 | | 4,017 | 4,003 |

| Pine Street Trust I 4.572% 2/15/29 (b) | | 4,516 | 4,270 |

| Pine Street Trust II 5.568% 2/15/49 (b) | | 4,529 | 4,174 |

| | | | 44,356 |

| Insurance - 0.6% | | | |

| Five Corners Funding Trust II 2.85% 5/15/30 (b) | | 13,114 | 11,368 |

| Liberty Mutual Group, Inc. 3.95% 5/15/60 (b) | | 10,260 | 7,341 |

| Lincoln National Corp. 3.4% 1/15/31 | | 9,415 | 8,239 |

| Pacific LifeCorp 5.125% 1/30/43 (b) | | 1,657 | 1,540 |

| Pricoa Global Funding I 5.375% 5/15/45 (c) | | 1,988 | 1,957 |

| Prudential Financial, Inc.: | | | |

| 3.935% 12/7/49 | | 2,764 | 2,169 |

| 6% 9/1/52 (c) | | 14,201 | 14,163 |

| Swiss Re Finance Luxembourg SA 5% 4/2/49 (b)(c) | | 600 | 582 |

| Unum Group: | | | |

| 4% 6/15/29 | | 3,614 | 3,380 |

| 5.75% 8/15/42 | | 1,024 | 994 |

| | | | 51,733 |

TOTAL FINANCIALS | | | 1,157,867 |

| HEALTH CARE - 2.1% | | | |

| Biotechnology - 0.2% | | | |

| Amgen, Inc.: | | | |

| 5.25% 3/2/33 | | 4,736 | 4,723 |

| 5.6% 3/2/43 | | 4,499 | 4,504 |

| 5.65% 3/2/53 | | 2,236 | 2,235 |

| 5.75% 3/2/63 | | 4,076 | 4,076 |

| | | | 15,538 |

| Health Care Providers & Services - 0.7% | | | |

| Centene Corp.: | | | |

| 2.45% 7/15/28 | | 12,745 | 11,233 |

| 2.625% 8/1/31 | | 5,945 | 4,865 |

| 3.375% 2/15/30 | | 5,110 | 4,508 |

| 4.25% 12/15/27 | | 5,450 | 5,184 |

| 4.625% 12/15/29 | | 8,470 | 8,017 |

| HCA Holdings, Inc.: | | | |

| 3.5% 9/1/30 | | 3,895 | 3,480 |

| 3.625% 3/15/32 | | 1,074 | 938 |

| 5.625% 9/1/28 | | 4,885 | 4,923 |

| 5.875% 2/1/29 | | 3,803 | 3,871 |

| Sabra Health Care LP 3.2% 12/1/31 | | 12,177 | 9,873 |

| Toledo Hospital 5.325% 11/15/28 | | 1,513 | 1,413 |

| Universal Health Services, Inc. 2.65% 10/15/30 | | 10,442 | 8,718 |

| | | | 67,023 |

| Pharmaceuticals - 1.2% | | | |

| Bayer U.S. Finance II LLC: | | | |

| 4.25% 12/15/25 (b) | | 43,242 | 42,044 |

| 4.375% 12/15/28 (b) | | 58,400 | 54,400 |

| Elanco Animal Health, Inc. 6.65% 8/28/28 (c) | | 905 | 912 |

| Utah Acquisition Sub, Inc. 3.95% 6/15/26 | | 1,304 | 1,259 |

| Viatris, Inc.: | | | |

| 2.7% 6/22/30 | | 6,115 | 5,150 |

| 3.85% 6/22/40 | | 2,664 | 1,958 |

| 4% 6/22/50 | | 3,018 | 2,060 |

| | | | 107,783 |

TOTAL HEALTH CARE | | | 190,344 |

| INDUSTRIALS - 0.9% | | | |

| Aerospace & Defense - 0.3% | | | |

| BAE Systems PLC 3.4% 4/15/30 (b) | | 2,547 | 2,307 |

| The Boeing Co.: | | | |

| 5.15% 5/1/30 | | 14,840 | 14,592 |

| 5.805% 5/1/50 | | 4,840 | 4,665 |

| 5.93% 5/1/60 | | 4,840 | 4,634 |

| | | | 26,198 |

| Building Products - 0.0% | | | |

| Carrier Global Corp.: | | | |

| 5.9% 3/15/34 | | 922 | 956 |

| 6.2% 3/15/54 | | 956 | 1,043 |

| | | | 1,999 |

| Trading Companies & Distributors - 0.3% | | | |

| Air Lease Corp.: | | | |

| 3.375% 7/1/25 | | 7,888 | 7,662 |

| 3.75% 6/1/26 | | 15,000 | 14,451 |

| | | | 22,113 |

| Transportation Infrastructure - 0.3% | | | |

| Avolon Holdings Funding Ltd.: | | | |

| 3.25% 2/15/27 (b) | | 7,484 | 6,915 |

| 3.95% 7/1/24 (b) | | 5,580 | 5,538 |

| 4.375% 5/1/26 (b) | | 4,949 | 4,775 |

| 6.375% 5/4/28 (b) | | 7,943 | 8,060 |

| | | | 25,288 |

TOTAL INDUSTRIALS | | | 75,598 |

| INFORMATION TECHNOLOGY - 0.8% | | | |

| Electronic Equipment, Instruments & Components - 0.0% | | | |

| Dell International LLC/EMC Corp. 6.2% 7/15/30 | | 2,284 | 2,390 |

| Semiconductors & Semiconductor Equipment - 0.6% | | | |

| Broadcom, Inc.: | | | |

| 1.95% 2/15/28 (b) | | 2,435 | 2,162 |

| 2.45% 2/15/31 (b) | | 20,716 | 17,306 |

| 2.6% 2/15/33 (b) | | 20,716 | 16,651 |

| 3.187% 11/15/36 (b) | | 5,647 | 4,427 |

| 3.5% 2/15/41 (b) | | 16,728 | 12,792 |

| | | | 53,338 |

| Software - 0.2% | | | |

| Oracle Corp.: | | | |

| 2.95% 4/1/30 | | 6,400 | 5,676 |

| 3.6% 4/1/50 | | 6,370 | 4,485 |

| 3.85% 4/1/60 | | 6,400 | 4,454 |

| | | | 14,615 |

TOTAL INFORMATION TECHNOLOGY | | | 70,343 |

| MATERIALS - 0.1% | | | |

| Chemicals - 0.1% | | | |

| Celanese U.S. Holdings LLC: | | | |

| 6.35% 11/15/28 | | 4,423 | 4,549 |

| 6.55% 11/15/30 | | 4,484 | 4,662 |

| 6.7% 11/15/33 | | 2,619 | 2,751 |

| | | | 11,962 |

| REAL ESTATE - 2.4% | | | |

| Equity Real Estate Investment Trusts (REITs) - 2.0% | | | |

| Alexandria Real Estate Equities, Inc.: | | | |

| 2% 5/18/32 | | 6,718 | 5,194 |

| 4.9% 12/15/30 | | 4,519 | 4,400 |

| American Homes 4 Rent LP: | | | |

| 2.375% 7/15/31 | | 977 | 787 |

| 3.375% 7/15/51 | | 1,510 | 995 |

| 3.625% 4/15/32 | | 3,763 | 3,283 |

| 4.3% 4/15/52 | | 2,608 | 2,024 |

| Boston Properties, Inc.: | | | |

| 3.25% 1/30/31 | | 4,526 | 3,814 |

| 4.5% 12/1/28 | | 2,824 | 2,668 |

| Corporate Office Properties LP: | | | |

| 2% 1/15/29 | | 747 | 619 |

| 2.25% 3/15/26 | | 2,339 | 2,187 |

| 2.75% 4/15/31 | | 2,202 | 1,777 |

| Healthcare Realty Holdings LP: | | | |

| 3.1% 2/15/30 | | 1,129 | 972 |

| 3.5% 8/1/26 | | 1,176 | 1,119 |

| Hudson Pacific Properties LP 4.65% 4/1/29 | | 6,288 | 5,237 |

| Invitation Homes Operating Partnership LP 4.15% 4/15/32 | | 5,643 | 5,090 |