Exhibit 99.1

May 2005

Safe Harbor Statement Under the

Private Securities Litigation Reform Act of 1995

The presentation relating to this material may contain forward-looking statements. Forward-looking statements made by or on behalf of Gallagher are subject to risks and uncertainties, including but not limited to the following: Gallagher’s commission revenues are highly dependent on premiums charged by insurers, which are subject to fluctuation; lower interest rates reduce Gallagher’s income earned on invested funds; the alternative insurance market continues to grow which could unfavorably impact commission and favorably impact fee revenue, though not necessarily to the same extent; Gallagher’s revenues vary significantly from period to period as a result of the timing of policy inception dates and the net effect of new and lost business production; the insurance brokerage industry is subject to a great deal of uncertainty due to investigations into its business practices by various governmental authorities and related private litigation; the general level of economic activity can have a substantial impact on Gallagher’s renewal business; Gallagher’s operating results, returns on investments and financial position may be adversely impacted by exposure to various market risks such as interest rate, equity pricing, foreign exchange rates and the competitive environment or the outcome of litigation concerning Gallagher’s Syn/Coal production; Gallagher’s revenues and net earnings may be subject to reduction due to the elimination of contingent commission arrangements in 2005 and related developments in the insurance industry; and Gallagher’s effective income tax rate may be subject to increase as a result of changes in income tax laws or unfavorable interpretations of such laws or developments resulting in the loss or unavailability of Syn/Coal credits. Gallagher’s ability to grow has been enhanced through acquisitions, which may or may not be available on acceptable terms in the future and which, if consummated, may or may not be advantageous to Gallagher. Accordingly, actual results may differ materially from those set forth in the forward-looking statements.

2

Non-GAAP Financial Measures

Regulation G Disclosure

This presentation includes certain non-GAAP financial measures as defined under rules promulgated by the U.S. Securities and Exchange Commission (the “SEC”). As required by SEC rules, we have provided reconciliations of those measures to the most directly comparable GAAP measures, which are available on our investor relations web-site at www.ajg.com.

3

Arthur J. Gallagher & Co.

World’s fourth-largest insurance brokerage and risk management services firm Public since 1984 Market capitalization of $2.7 billion Shares outstanding of 93.2 million Dividend yield of 3.9 52-week range – $28.06—$33.96 Traded NYSE as “AJG”

As of 3/31/05, unless otherwise indicated

4

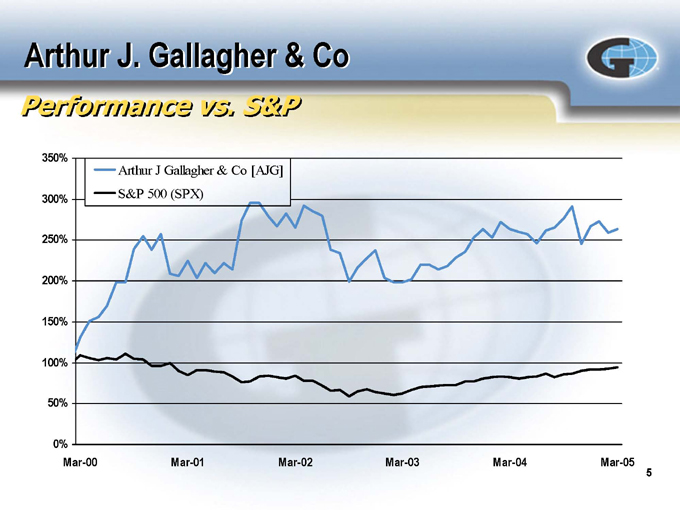

Arthur J. Gallagher & Co

Performance vs. S&P

350% 300% 250% 200% 150% 100% 50% 0%

Arthur J Gallagher & Co [AJG]

S&P 500 (SPX)

Mar-00 Mar-01 Mar-02 Mar-03 Mar-04 Mar-05

5

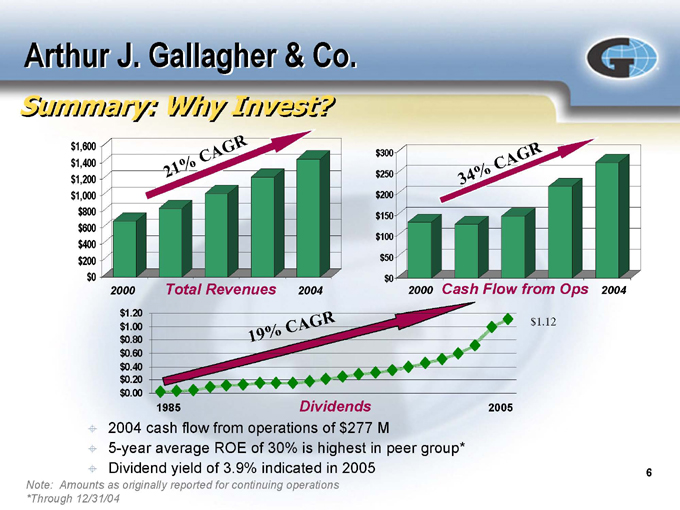

Arthur J. Gallagher & Co.

Summary: Why Invest?

$1,600 $1,400 $1,200 $1,000 $800 $600 $400 $200 $0

21%

CAGR

2000

Total Revenues

2004 $300 $250 $200 $150 $100 $50 $0

34%

CAGR

2000

Cash Flow from Ops

2004 $1.20 $1.00 $0.80 $0.60 $0.40 $0.20 $0.00

19%

CAGR

1985

Dividends

2005 $1.12

2004 cash flow from operations of $277 M

5-year average ROE of 30% is highest in peer group* Dividend yield of 3.9% indicated in 2005

Note: Amounts as originally reported for continuing operations *Through 12/31/04

6

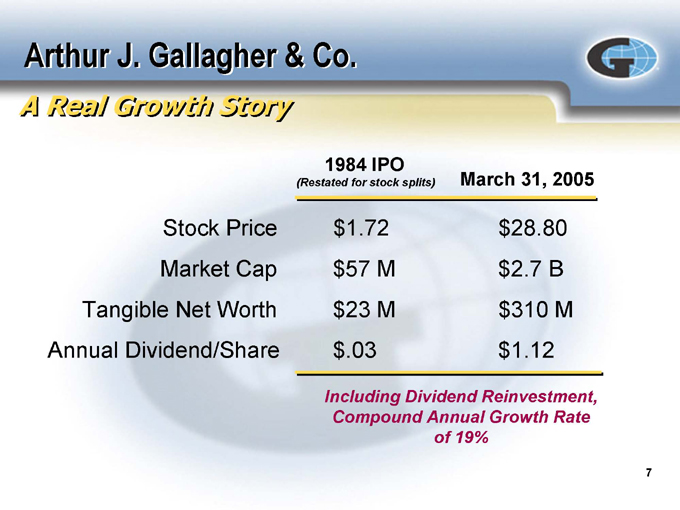

Arthur J. Gallagher & Co.

A Real Growth Story

1984 IPO

(Restated for stock splits) March 31, 2005

Stock Price $1.72 $28.80

Market Cap $57 M $2.7 B

Tangible Net Worth $23 M $310 M

Annual Dividend/Share $.03 $1.12

Including Dividend Reinvestment, Compound Annual Growth Rate of 19%

7

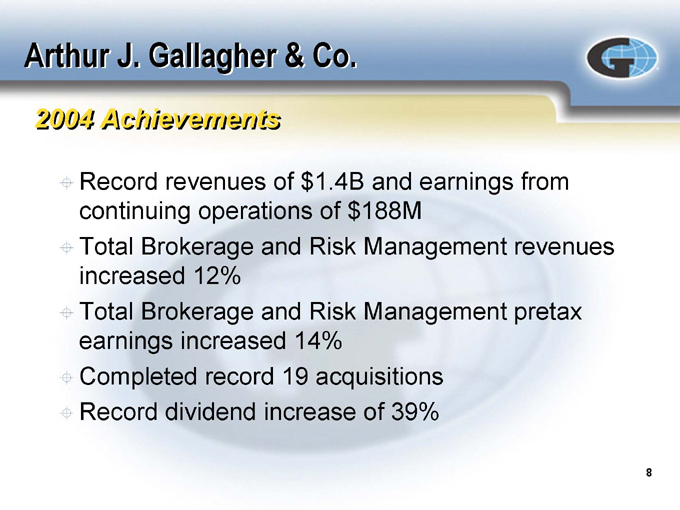

Arthur J. Gallagher & Co.

2004 Achievements

Record revenues of $1.4B and earnings from continuing operations of $188M

Total Brokerage and Risk Management revenues increased 12% Total Brokerage and Risk Management pretax earnings increased 14% Completed record 19 acquisitions Record dividend increase of 39%

8

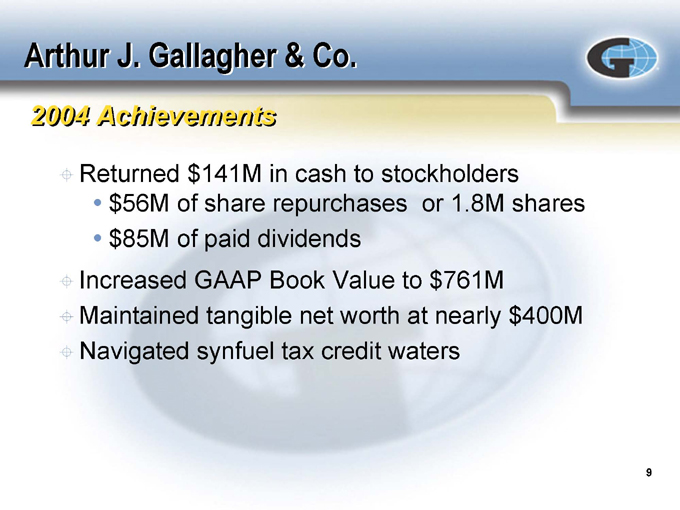

Arthur J. Gallagher & Co.

2004 Achievements

Returned $141M in cash to stockholders $56M of share repurchases or 1.8M shares $85M of paid dividends

Increased GAAP Book Value to $761M Maintained tangible net worth at nearly $400M Navigated synfuel tax credit waters

9

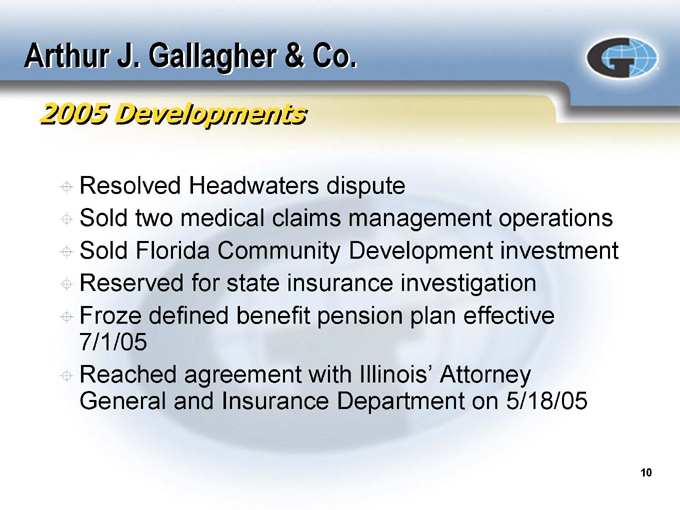

Arthur J. Gallagher & Co.

2005 Developments

Resolved Headwaters dispute

Sold two medical claims management operations Sold Florida Community Development investment Reserved for state insurance investigation Froze defined benefit pension plan effective 7/1/05 Reached agreement with Illinois’ Attorney General and Insurance Department on 5/18/05

10

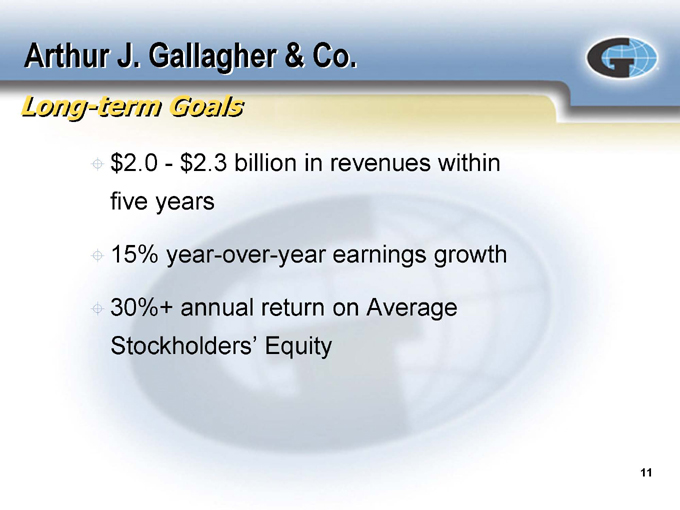

Arthur J. Gallagher & Co.

Long-term Goals $2.0—$2.3 billion in revenues within five years

15% year-over-year earnings growth

30%+ annual return on Average Stockholders’ Equity

11

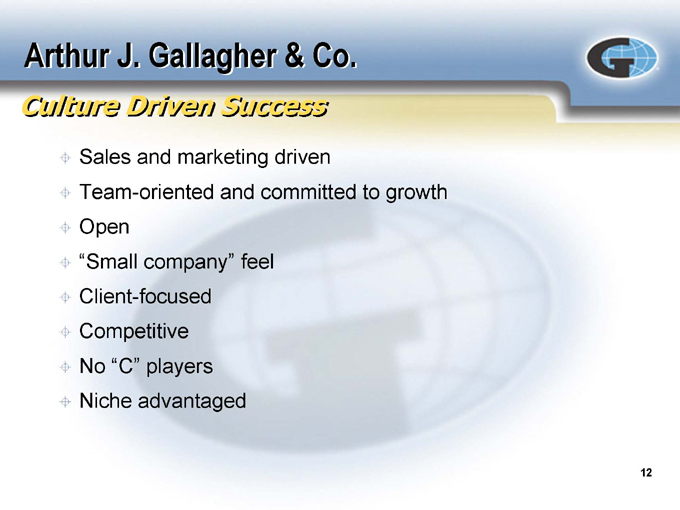

Arthur J. Gallagher & Co.

Culture Driven Success

Sales and marketing driven

Team-oriented and committed to growth Open “Small company” feel Client-focused Competitive No “C” players Niche advantaged

12

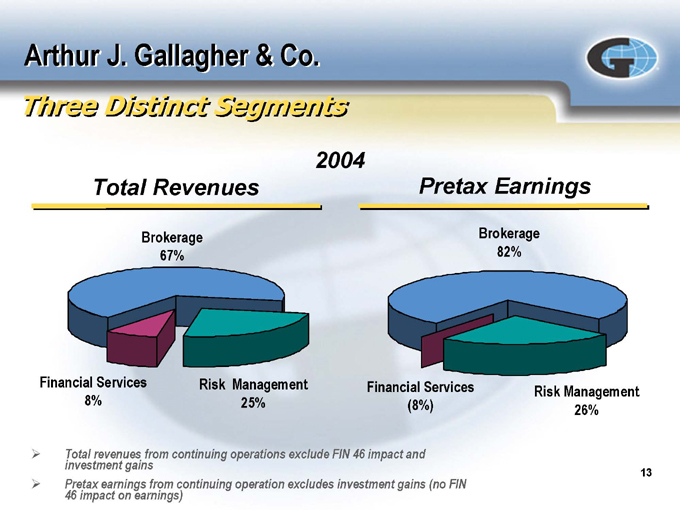

Arthur J. Gallagher & Co.

Three Distinct Segments

2004

Total Revenues

Brokerage 67%

Financial Services 8%

Risk Management 25%

Pretax Earnings

Brokerage 82%

Financial Services (8%)

Risk Management 26%

Total revenues from continuing operations exclude FIN 46 impact and investment gains

Pretax earnings from continuing operation excludes investment gains (no FIN 46 impact on earnings)

13

Brokerage Segment

Gallagher’s largest business segment Acts as intermediary – no underwriting risk Niche driven Alternative market leaders

14

Brokerage Segment

Contingent Commission Chronology

October 2004—effective 1/1/05, not entering into new volume/profit-based contingent agreements as retail broker Received subpoenas and other requests for information from state attorneys general and state regulatory authorities Q4 2004—conducted internal review with outside counsel which found no evidence of price fixing, bid rigging or improper tying arrangements Q1 2005, received $20.7M in contingent commissions on 2004 contracts Q1 2005—recorded $35M charge ($21M after tax, or $.23 per diluted share) as best estimate of amount to resolve the state insurance investigations based on costs of similar industry settlements thus far, plus an accrual for legal costs May 18, 2005 – reach agreement with Illinois’ Attorney General and Insurance Department – no lawsuit; no unlawful conduct will create $27M fund for certain retail clients which does not represent a fine or penalty will adopt certain business reforms including an agreement not to receive retail contingent commissions

Continue full cooperation with other state regulatory authorities

15

Brokerage Segment

A Strategic Consolidator

Geographic diversity; enhance or expand capabilities Approximately 140 acquisitions in this segment from 1986 through 3/31/05 The rules: financial health, similar culture Gallagher is merger partner of choice

16

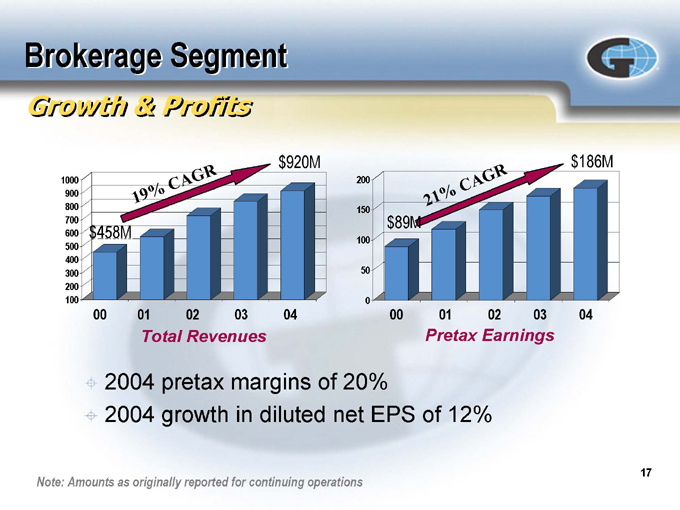

Brokerage Segment

Growth & Profits

1000 900 800 700 600 500 400 300 200 100 $458M

19%

CAGR

$920M

00 01 02 03 04

Total Revenues

200 150 100 50 0 $89M

21%

CAGR

$186M

00 01 02 03 04

Pretax Earnings

2004 pretax margins of 20%

2004 growth in diluted net EPS of 12%

Note: Amounts as originally reported for continuing operations

17

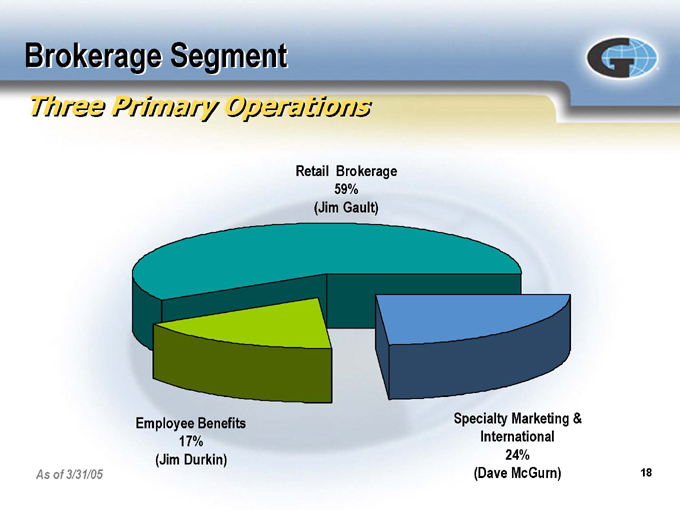

Brokerage Segment

Three Primary Operations

Retail Brokerage 59% (Jim Gault)

Employee Benefits 17% (Jim Durkin)

Specialty Marketing & International 24% (Dave McGurn)

As of 3/31/05

18

Retail Brokerage Offices

19

Retail Brokerage

Niches

Agribusiness Aviation Captives Construction Construction Project Solutions Energy Global Risk Management Healthcare Higher Education Management Liability Marine

Mergers & Acquisitions Personal Insurance Public Entity Real Estate

General Commercial Habitational Hospitality Shopping Centers

Religious/Nonprofit Restaurant Scholastic K-12 Transportation Worldwide Risk Services

20

Retail Brokerage

High Growth & Profit Potential

Niches – number and size Acquisitions and hiring Alternative market

Captives Rent-a-captives Deductible plans Self-insurance

21

Specialty Marketing & International

Offices, Joint Ventures & Alliances

Specialty Marketing & International

Capabilities

Wholesale Brokerage International P&C Brokerage Programs/Program Administration Reinsurance Brokerage Captives/Rent-a-Captives CoverageFirst.com

23

Employee Benefits Offices

24

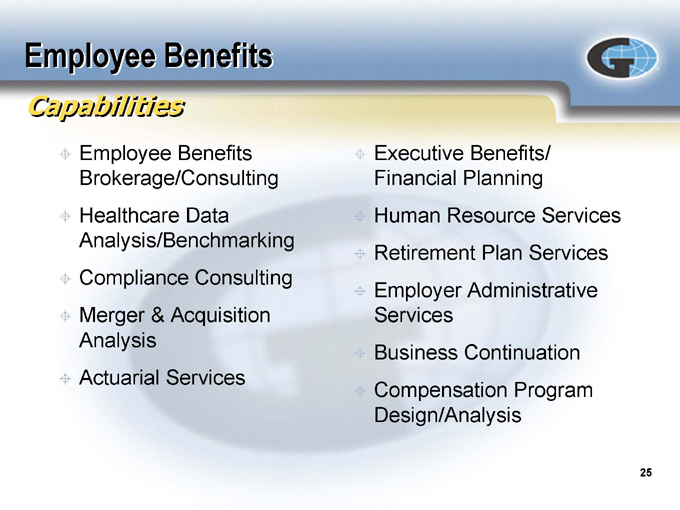

Employee Benefits

Capabilities

Employee Benefits Brokerage/Consulting Healthcare Data Analysis/Benchmarking Compliance Consulting Merger & Acquisition Analysis Actuarial Services

Executive Benefits/ Financial Planning Human Resource Services Retirement Plan Services Employer Administrative Services Business Continuation Compensation Program Design/Analysis

25

Employee Benefits

High Growth & Profit Potential

Niche marketing

Cross-selling opportunities with Retail Brokerage Merger and acquisition opportunities Assisting clients/prospects with four top priorities

Controlling health and welfare costs Providing better retirement tools/information Benefits communication and administration Compliance with federal and state regulations

26

Risk Management Segment

Gallagher’s Property/Casualty Claims Management Operation “Gallagher Bassett” – Rich McKenna World’s largest multiline, third-party administrator (Business Insurance magazine) Revenue growth is all organic Fee revenues are primarily generated based on number of claims Significant barriers to entry into this business – high retention levels

27

Risk Management Segment

Growth & Profits

350 300 250 200 150 100 50 0

16%

CAGR

$203M $346M

2000 2004

Total Revenues

60 50 40 30 20 10 0

24%

CAGR

$28M $58M

2000 2004

Pretax Earnings

2004 pretax margin of 17%

2004 growth in diluted net EPS of 47%

Note: Amounts as originally reported for continuing operations

28

Gallagher Bassett Offices

29

Risk Management Segment

Expertise

Real-time Claims Reporting Recoveries (subrogation, salvage, etc.) Appraisal Services Litigation Management Information Management

Managed Care Services Loss Control Services Safety Programs Settlement Management Education and Training

30

Risk Management Segment

High Growth & Profit Potential

Fortune 1000 companies

Outsourcing of insurance co. claims departments Captives Program business Expanding global capabilities Enhancements in systems/processes related to:

Electronic data storage Security Claims regulatory changes

Access to information via the Internet Employer communication/plan administration

31

Financial Services Segment $889 Million of Cash & Investments*

Investments Allocated to Financial Services Segment

($171 M)

Cash Allocated to Risk Management Segment

($140 M)

Cash Allocated to Brokerage Segment

($578 M)

* As of March 31, 2005 – Cash & investments net of related investment borrowings

32

Financial Services Segment

Net Assets Under Management and Financial Guarantees $400 $350 $300 $250

$200 $150 $362 $187

2002 2005

Net Asset Classes 3/31/05 $70 $60 $50 $40 $30 $20 $10 $0

Tax Adv. Asset Mgmt. Real Estate Other

Low Income Housing $16M Alternative Energy $61M Asset Alliance $47M Real Estate, incl HO $23M Bermuda Insurance $27M VC, Airplanes & Other $13M $ In millions

33

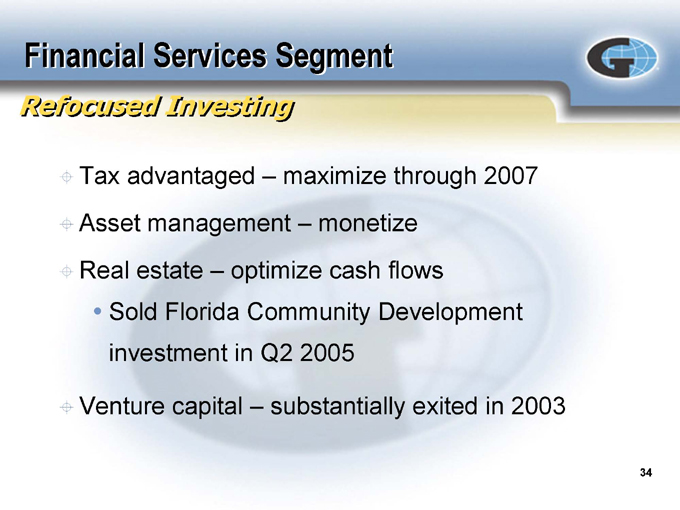

Financial Services Segment

Refocused Investing

Tax advantaged – maximize through 2007 Asset management – monetize Real estate – optimize cash flows

Sold Florida Community Development investment in Q2 2005

Venture capital – substantially exited in 2003

34

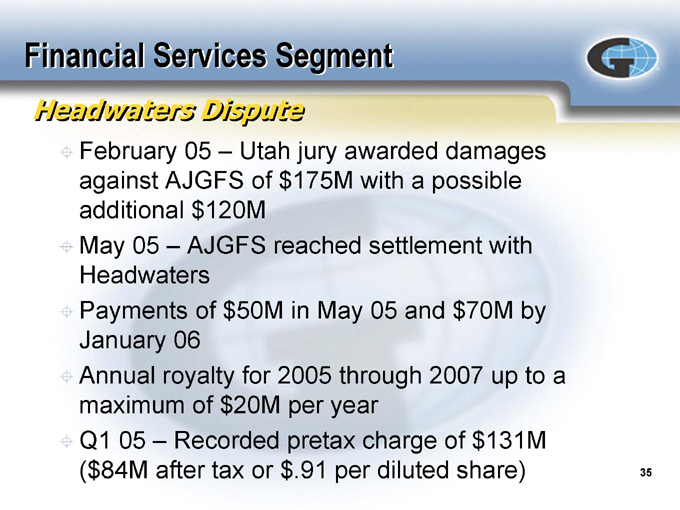

Financial Services Segment

Headwaters Dispute

February 05 – Utah jury awarded damages against AJGFS of $175M with a possible additional $120M

May 05 – AJGFS reached settlement with Headwaters Payments of $50M in May 05 and $70M by January 06 Annual royalty for 2005 through 2007 up to a maximum of $20M per year Q1 05 – Recorded pretax charge of $131M

($84M after tax or $.91 per diluted share)

35

Arthur J. Gallagher & Co.

Why Invest?

36

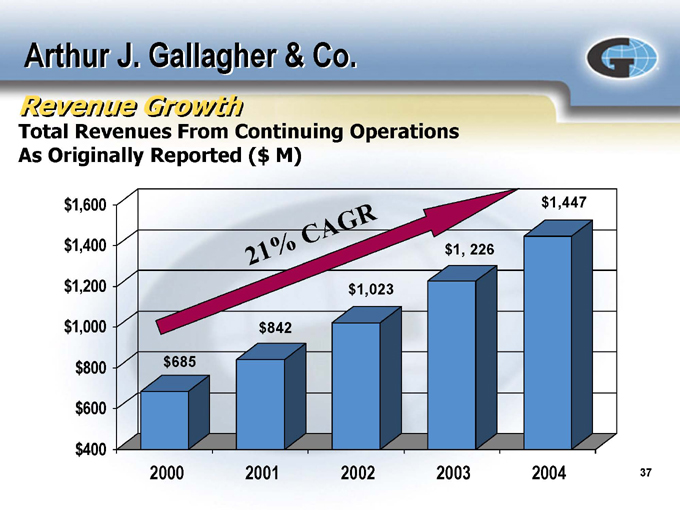

Arthur J. Gallagher & Co.

Revenue Growth

Total Revenues From Continuing Operations As Originally Reported ($ M) $1,600 $1,400 $1,200 $1,000 $800 $600 $400

21%

CAGR

$685 $842 $1,023 $1, 226 $1,447

2000 2001 2002 2003 2004

37

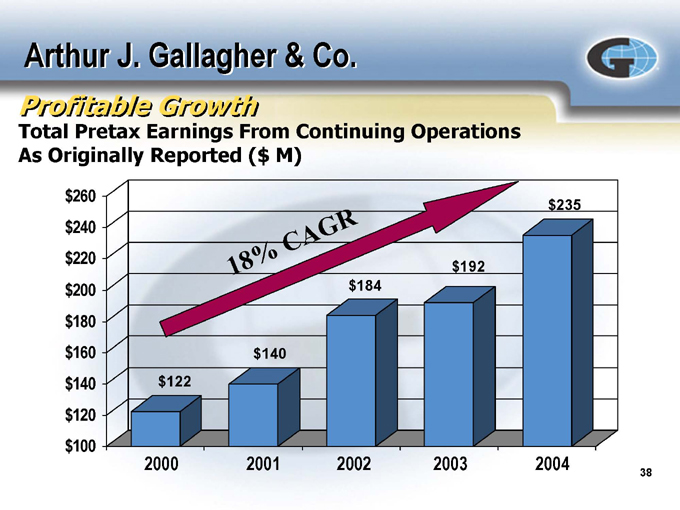

Arthur J. Gallagher & Co.

Profitable Growth

Total Pretax Earnings From Continuing Operations As Originally Reported ($ M) $260 $240 $220 $200 $180 $160 $140 $120 $100

18%

CAGR

$122 $140 $184 $192 $235

2000 2001 2002 2003 2004

38

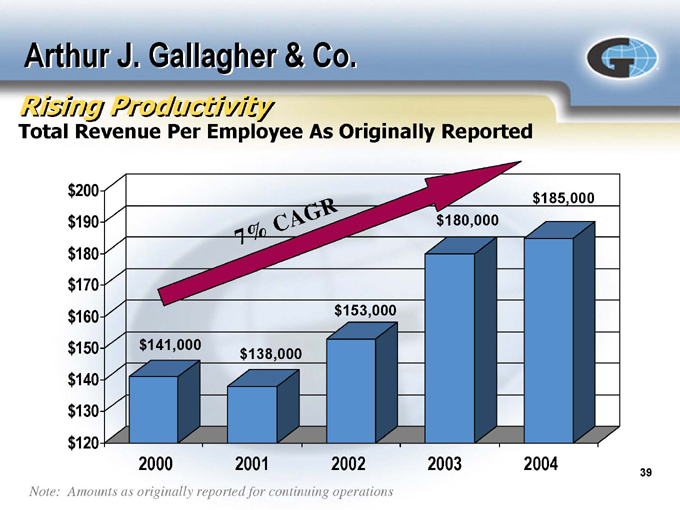

Arthur J. Gallagher & Co.

Rising Productivity

Total Revenue Per Employee As Originally Reported $200 $190 $180 $170 $160 $150 $140 $130 $120

7%

CAGR

$141,000 $138,000 $153,000 $180,000 $185,000

2000 2001 2002 2003 2004

Note: Amounts as originally reported for continuing operations

39

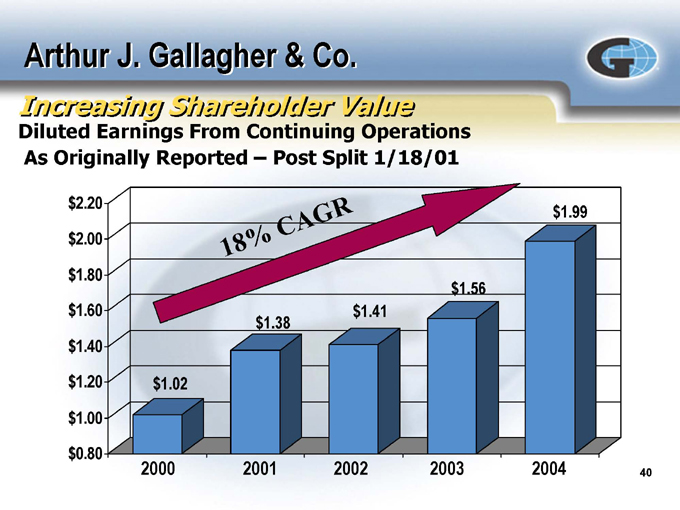

Arthur J. Gallagher & Co.

Increasing Shareholder Value

Diluted Earnings From Continuing Operations As Originally Reported – Post Split 1/18/01 $2.20 $2.00

$1.80 $1.60

$1.40 $1.20

$1.00 $0.80

18%

CAGR

$1.02 $1.38 $1.41 $1.56 $1.99

2000 2001 2002 2003 2004

40

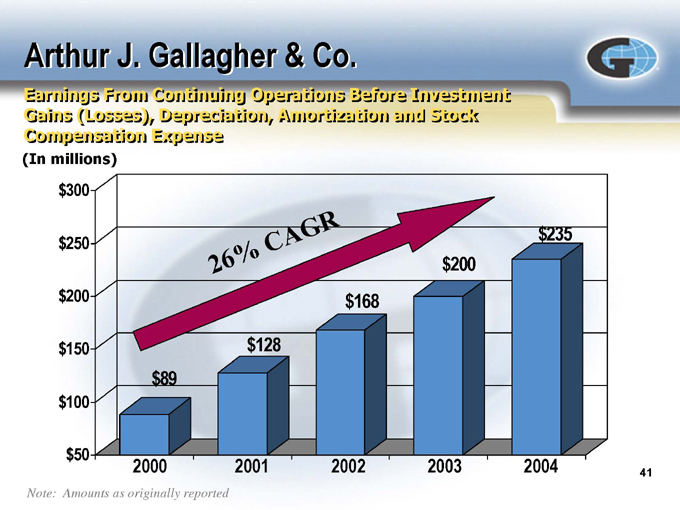

Arthur J. Gallagher & Co.

Earnings From Continuing Operations Before Investment Gains (Losses), Depreciation, Amortization and Stock Compensation Expense

(In millions) $300 $250 $200 $150 $100 $50

26%

CAGR

$89 $128 $168 $200 $235

2000 2001 2002 2003 2004

Note: Amounts as originally reported

41

Arthur J. Gallagher & Co.

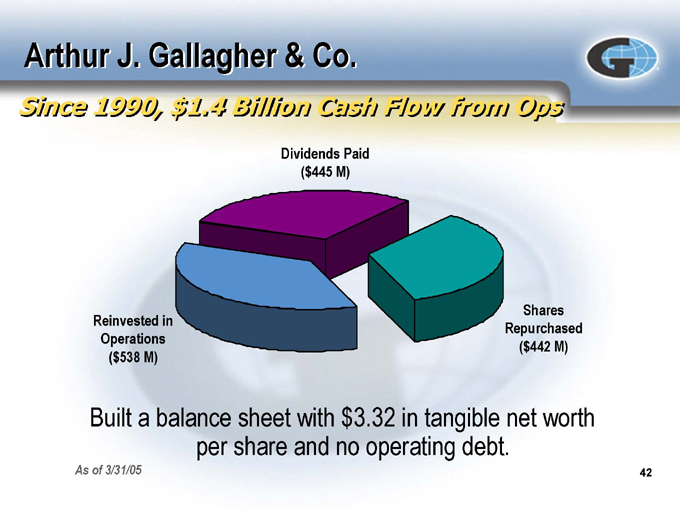

Since 1990, $1.4 Billion Cash Flow from Ops

Dividends Paid

($445 M)

Reinvested in Operations

($538 M)

Shares Repurchased

($442 M)

Built a balance sheet with $3.32 in tangible net worth per share and no operating debt.

As of 3/31/05

42

Arthur J. Gallagher & Co.

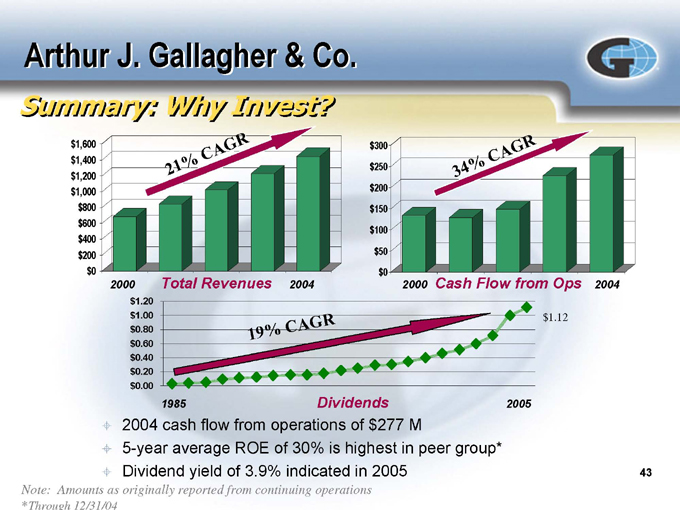

Summary: Why Invest?

$1,600 $1,400 $1,200 $1,000 $800 $600 $400 $200 $0

21%

CAGR

2000

Total Revenues

2004 $300 $250 $200 $150 $100 $50 $0

34%

CAGR

2000

Cash Flow from Ops

2004 $1.20 $1.00 $0.80 $0.60 $0.40 $0.20 $0.00

19%

CAGR

$1.12

1985

Dividends

2005

2004 cash flow from operations of $277 M

5-year average ROE of 30% is highest in peer group* Dividend yield of 3.9% indicated in 2005

Note: Amounts as originally reported from continuing operations

* Through 12/31/04

43

Culture Driven Success

The Gallagher Way

Shared values at Gallagher are the rock foundation of the Company and our Culture. What is a Shared Value? These are the concepts that the vast majority of movers and shakers in the Company passionately adhere to. What are some of Gallagher’s Shared Values?

1. We are a Sales and Marketing Company dedicated to providing excellence in Risk Management Services to our clients.

2. We support one another. We believe in one another. We acknowledge and respect the ability of one another.

3. We push for professional excellence.

4. We can all improve and learn from one another.

5. There are no second class citizens -everyone is important and everybody’s job is important.

6. We’re an open society.

7. Empathy for the other person is not a weakness.

8. Suspicion breeds more suspicion. To trust and be trusted is vital.

9. Leaders need followers. How leaders treat followers has a direct impact on the effectiveness of the leader.

10. Interpersonal business relationships should be built. 11. We all need one another. We are all cogs in a wheel. 12. No department or person is an island.

13. Professional courtesy is expected.

14. Never ask someone to do something you wouldn’t do yourself.

15. I consider myself support for our Sales & Marketing. We can’t make things happen without each other.

We are a team.

16. Loyalty and respect are earned -not dictated. 17. Fear is a turn-off.

18. People skills are very important at Gallagher. 20. We run to problems -not away from them.

21. We adhere to the highest standards or moral and ethical behavior.

22. People work harder and are more effective when they’re turned on -not turned off. 23. We are a warm, close Company. This is a strength -not a weakness.

24. We must continue building a professional Company -together -as a team.

25. Shared values can be altered with circumstances -but carefully and with tact and consideration for one another’s needs.

When accepted Shared Values are changed or challenged, the emotional impact and negative feelings can damage the Company.

44