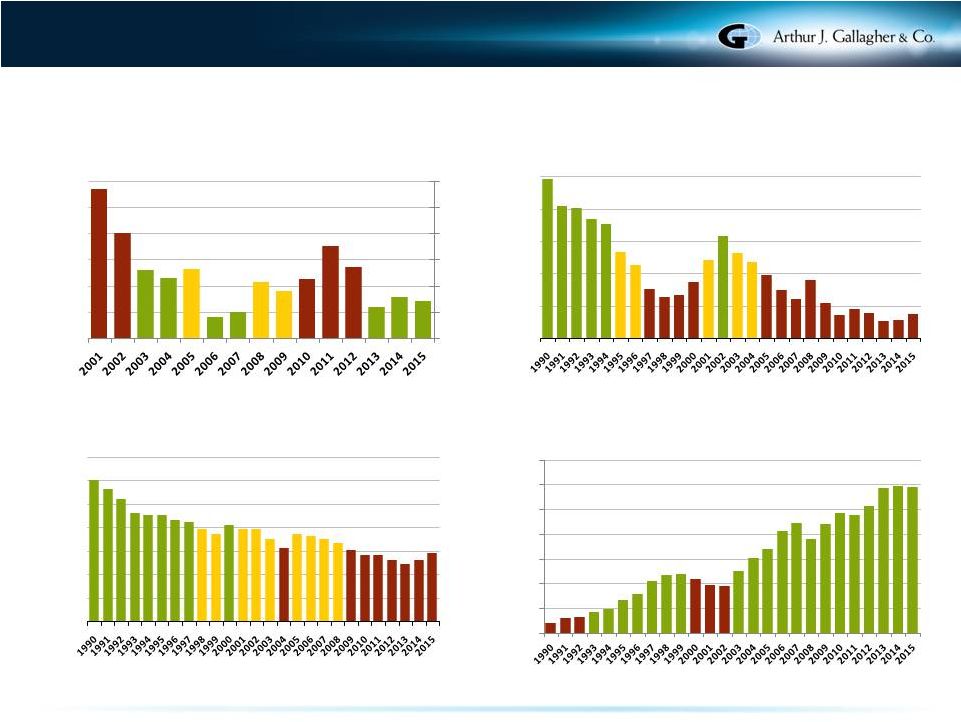

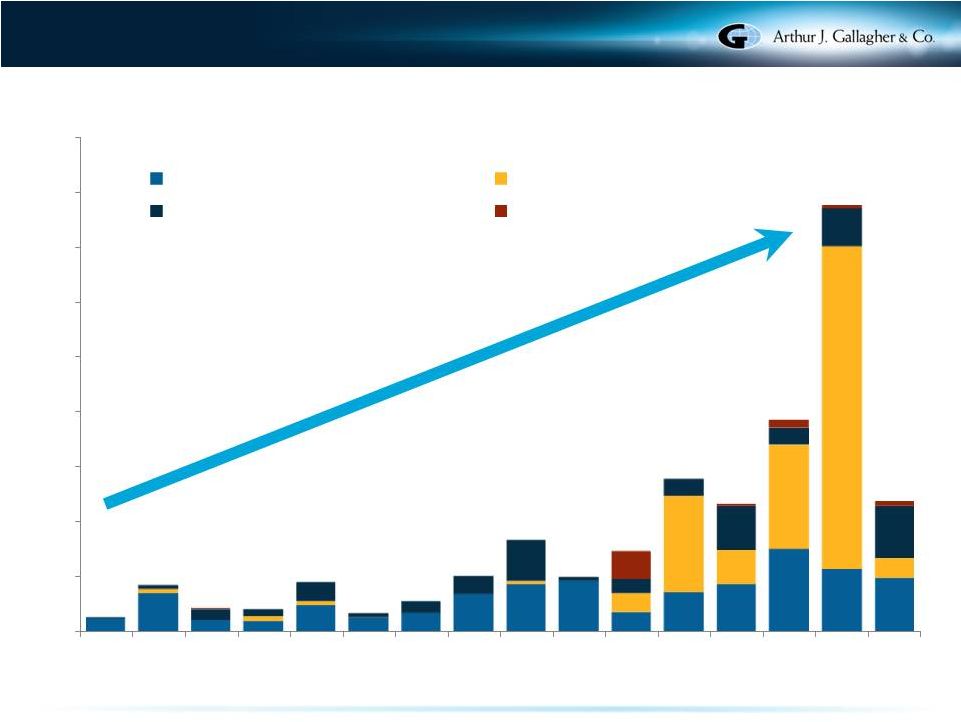

8 Information Regarding Non-GAAP Measures This presentation includes references to Adjusted EBITDAC, Adjusted EBITDAC margin, Adjusted Revenues, Adjusted Operating Expense Ratio and Organic Growth, which are measures not in accordance with, or an alternative to, the GAAP information provided herein. Earnings Measures - Gallagher believes that each of Adjusted EBITDAC and Adjusted EBITDAC margin, as defined below, provides a meaningful representation of its operating performance and improves the comparability of Gallagher’s results between periods by eliminating the impact of certain items that have a high degree of variability. Adjusted EBITDAC is defined as earnings from continuing operations before interest, income taxes, depreciation, amortization and the change in estimated acquisition earnout payables (EBITDAC), further adjusted to exclude gains realized from sales of books of business, acquisition integration costs, earnout related compensation charges, workforce related charges, lease termination related charges, client run-off/bankruptcy impact, South Australia and claim portfolio transfer ramp up fees/costs, acquisition related adjustments and the period-over-period impact of foreign currency translation, as applicable. Adjusted EBITDAC margin is defined as Adjusted EBITDAC divided by Adjusted Revenues (defined below). The most directly comparable GAAP measure for these non-GAAP earnings measures is net earnings. For the Brokerage Segment, the Risk Management Segment, and the two segments on a combined basis, net earnings was $139 million, $35 million and $174 million, respectively, in 2011, $156 million, $43 million and $199 million, respectively, in 2012, $205 million, $48 million and $253 million, respectively, in 2013, $264 million, $42 million and $306 million, respectively, in 2014 and $268 million, $57 million and $325 million, respectively, in 2015. Revenue and Expense Measures - Gallagher believes that Adjusted Revenues and Adjusted Operating Expense Ratio, each as defined below, provides stockholders and other interested persons with useful information that will assist such persons in analyzing Gallagher’s operating results as they develop a future outlook for Gallagher. Gallagher believes that Organic Growth provides a comparable measurement of revenue growth that is associated with the revenue sources that will be continuing in 2016 and beyond. Gallagher has historically viewed organic revenue growth as an important indicator when assessing and evaluating the performance of its Brokerage and Risk Management segments. Gallagher also believes that using this measure allows financial statement users to measure, analyze and compare the growth from its Brokerage and Risk Management segments in a meaningful and consistent manner. Adjusted Revenues is defined as revenues, adjusted to exclude gains realized from sales of books of business, New Zealand earthquake claims administration fees, South Australia ramp up fees and the impact of client bankruptcy. Adjusted Operating Expense Ratio is defined as operating expense, adjusted to eliminate lease termination and abandonment charges, acquisition related adjustments and integration costs, costs related to New Zealand earthquake claims administration, South Australia and claim portfolio transfer ramp up costs, and the impact of foreign currency translation, as applicable, divided by Adjusted Revenues. Organic Growth is defined as organic change in commission and fee revenues (including supplemental and contingent commissions), and excludes the first twelve months of net commission and fee revenues generated from acquisitions accounted for as purchases and the net commission and fee revenues related to operations disposed of in each year presented. These commissions and fees are excluded from organic revenues in order to help interested persons analyze the revenue growth associated with the operations that were a part of Gallagher in both the current and prior year. In addition, change in organic growth excludes the period-over-period impact of foreign currency translation. The amounts excluded with respect to foreign currency translation are calculated by applying 2015 foreign exchange rates to the same periods in 2014. The most directly comparable GAAP measure for Adjusted Revenues and Organic Growth is reported revenues. For the Brokerage Segment, reported revenues were $533 million, $679 million, $783 million, $863 million, $946 million, $1,007 million, $1,114 million, $1,188 million, $1,276 million, $1,329 million, $1,544 million, $1,812 million, $2,126 million, $2,896 million, and $3,324 million in 2001, 2002, 2003, 2004, 2005, 2006, 2007, 2008, 2009, 2010, 2011, 2012, 2013, 2014 and 2015, respectively. For the Risk Management Segment, reported revenues were $682.3 million and $727.1 million in 2014 and 2015, respectively. The most directly comparable GAAP measure for Adjusted Operating Expense Ratio is reported operating expense, which was $247 million and $638 million in 2008 and 2015, respectively, for the Brokerage Segment and $126 million and $181 million in 2008 and 2015, respectively, for the Risk Management Segment. Reconciliations – For other reconciliations, please see the appendix at the back of this presentation and the examples set forth in "Reconciliation of Non-GAAP Measures and supplemental quarterly financial data " on Gallagher's Web site at ajg.com/IR. |