Exhibit 99(c)(2)

Confidential

Presentation to

The Board of Directors of

Prab, Inc.

December 30, 2003

The information contained herein is of a confidential nature and is intended for the

exclusive use of the persons or firm to whom it is furnished by us. Reproduction,

publication, or dissemination of portions hereof may not be made without prior

approval of Lincoln Partners LLC.

Table of Contents |

• | Background of the Proposed Transaction |

|

|

• | Scope of Analysis |

|

|

• | Business Overview |

|

|

• | Industry Impressions |

|

|

• | Valuation and Financial Analysis |

|

|

• | Summary Conclusions |

|

|

• | Appendix |

| 2 | [lp graphic] |

|

Background of the

Proposed Transaction

| 3 | [lp graphic] |

Background |

• | Prab, Inc., ("Prab" or the "Company") which operates under two divisions, Prab Conveyors and Hapman Conveyors, designs and manufactures conveyors, metal scrap reclamation systems and bulk material handling equipment and systems which it sells to die casting, metal stamping, general metal working, and other industries. For the fiscal year ended October 31, 2003, Prab posted unaudited sales and adjusted earnings before interest, taxes, depreciation and amortization ("EBITDA") of $13.9 million and $782 thousand respectively. |

|

|

• | On July 23, 2003, the Board of Directors of Prab (the "Board") was informed by members of management ("Management") that a group within management desired to take the Company private. |

|

|

• | Management proposed forming an acquisition company ("Kalamazoo Acquisition Corp." or "KAC") to purchase all of the outstanding shares held by the independent shareholders at a price of $2.00 per share in a going private transaction. This bid represented a 22.5% premium over the 30 day average trading price of Prab's stock ($1.63) prior to announcement of the offer. |

Note: 2003 EBITDA adjusted to exclude $162,515 of expenses (incremental legal, advisory and Special Committee fees, etc.) related to this going private transaction

| 4 | [lp graphic] |

Background |

• | After receiving management's offer for Prab, the Board formed a Special Committee ("Committee") of the independent directors to review and negotiate the merger proposal. Members of the Committee included William G. Blunt, James H. Haas and John W. Garside. Fred Schroeder was later added to the Committee. |

|

|

• | On July 28, 2003, the Company received a merger proposal from Stevens Financial Group, LLC ("Stevens") which offered shareholders a price of $2.20 per share. This bid represented a 34.9% premium to Prab's stock price. |

|

|

• | On August 18, 2003, the Company received a merger proposal from Inter-Source Acquisition, Inc. ("Inter-Source") which offered shareholders a price of $2.25 per share representing a 38.1% premium to Prab's stock price. |

|

|

• | On August 22, 2003, the Company issued a press release announcing the Inter-Source proposal. In addition, the press release noted that the Committee had hired Varnum, Riddering, Schmidt & Howlett LLP ("Varnum") to serve as independent legal counsel to the Special Committee and Lincoln Partners to assist the Committee in considering its strategic alternatives. |

| 5 | [lp graphic] |

Background |

• | As the Company received unsolicited bids, it issued a series of 8-K filings announcing the bids and indicating that Prab was considering its strategic alternatives. In addition, various articles regarding a potential transaction appeared in the local press. |

|

|

• | Subsequently, five additional groups expressed an interest in acquiring Prab. Together, all eight bidders, after executing the appropriate confidentiality agreements, received supplemental information regarding the Company and were directed to provide revised proposals by September 12, 2003. |

|

|

• | On September 12, 2003, two of the eight bidders submitted bids to acquire Prab. KAC submitted a revised bid of $2.30/share and Stevens submitted a bid that included a range of $2.20 - $2.45/share. |

|

|

• | Three strategic bidders (Flexicon Corporation, Inter-Source, Inc. and Quality Products) declined to bid for Prab after receiving supplemental information about the Company. These bidders noted concern regarding employment agreements covering Gary Herder and Ned Thompson, pension liabilities and environmental matters, among others, as their reasons for declining. |

| 6 | [lp graphic] |

Background |

• | Two financial bidders (Argonne Capital Group and Platinum Technology) exited the bidding process at this time. These bidders were not provided any further information regarding Prab. |

|

|

• | On September 17, 2003 the Special Committee initiated a review of the employment agreements in order to determine if they could be modified to attract more strategic interest in Prab and, in turn, further maximize shareholder value. The bidding process was placed on hold until a review of the agreements was completed. |

|

|

• | During this period, two additional strategic bidders (National Bulk Equipment, Inc. and Schenck AccuRate) expressed an interest in Prab, executed non-disclosure agreements and received supplemental information about the Company. Also, a new financial bidder, Siegler Corporation ("Siegler") entered the process. |

|

|

• | Two strategic bidders expressed an interest in acquiring the Hapman division only. The Special Committee considered a sale of Hapman only, but determined that given the small size of Prab, Inc., the difficulty in separating the two intertwined businesses, and the loss of overhead coverage upon a sale of Hapman, a sale of the entire company was more strategically viable for the shareholders. |

| 7 | [lp graphic] |

Background |

• | On November 5, the Special Committee convened via conference call to discuss changes to the employment agreements with Herder and Thompson. Several significant changes had been negotiated. As a result, the severance liability was significantly reduced from $1.5 million to $649,241. |

|

|

• | Revised employment agreements were distributed to the bidders. The bidders were instructed to provide bids, or reaffirm earlier bids, by November 14th. |

|

|

• | On November 14th, three bidders submitted proposals for Prab. KAC reaffirmed its bid of $2.30/share. Stevens reaffirmed its bid of $2.20 - $2.45/share. Siegler submitted a bid for $2.30 - $2.40/share. |

|

|

• | Stevens and Siegler were invited to attend management presentations on-site at Prab. They were also provided with copies of Prab's Agreement and Plan of Merger (the "Merger Agreement"). All three bidders were instructed to provide final bids, along with marked copies of the Merger Agreement, by December 10th. |

| 8 | [lp graphic] |

Background |

• | Siegler subsequently declined to visit Prab and pursue a transaction. Stevens visited the Company, but did not ultimately provide a written bid for Prab following its visit. They verbally indicated that, if they were to provide a written bid, it would be for less than $2.20/share. |

|

|

• | On December 9th, KAC submitted a letter of intent to acquire Prab for $2.40/share. KAC's offer included commitment letters from three different banks willing to provide the necessary senior debt financing. In addition, KAC provided a marked version of the Merger Agreement with only one comment. KAC requested that the time period for maintaining directors' and officer's liability insurance be reduced from six to three years. |

|

|

• | KAC's final offer represents a 47% premium to Prab's 30-day average trading price prior to KAC's initial offer and a 20% increase from their initial $2.00/share offer for Prab. |

|

|

• | KAC's offer equates to a total enterprise value of $3.7 million for Prab. |

| 9 | [lp graphic] |

Background |

• | A summary of the bidders is shown in the table below: |

Company | Type | Initial Indication | Final Offer |

Argonne Capital Group | Financial | Declined | N/A |

Flexicon Corp. | Strategic | Declined | N/A |

Inter-Source, Inc. | Strategic | $2.25/share | Declined |

KAC | Strategic | $2.00 | $2.40 |

Magnum Systems, Inc. | Strategic | Declined | N/A |

National Bulk Equipment, Inc. | Strategic | Declined | N/A |

Platinum Equity, LLC | Financial | Declined | N/A |

Quality Products, Inc. | Strategic | Declined | N/A |

Schenck AccuRate | Strategic | Declined | N/A |

Siegler Corp. | Financial | $2.30 - $2.40 | Declined |

Stevens Financial Group LLC | Financial | $2.20 - $2.45 | Declined |

| 10 | [lp graphic] |

|

Scope of Analysis

| 11 | [lp graphic] |

Scope of Analysis |

The Board of Directors of Prab has engaged Lincoln Partners LLC ("Lincoln Partners") to provide independent financial advisory services to the Board of Directors in connection with the Proposed Transaction. Lincoln Partners has specifically been asked to render an opinion as to whether the price and terms of the Proposed Transaction are fair to Prab from a financial point of view. Lincoln Partners was not retained or asked to advise in the negotiations with the group of potential acquirers.

Lincoln Partners' analysis was based on:

• | Review of Prab's Form 10-KSB and Form 10-KSB/A (if applicable) for the fiscal years ended October 31, 1998 - 2002; |

|

|

• | Review of Prab's Form 10-QSB for the quarterly periods ended April 30, 2003 and July 30, 2003; |

|

|

• | Review of Prab's unaudited, internal financial statements for the year ended October 31, 2003; |

|

|

• | Review of financial projections for the year ended October 31, 2004 prepared by the Company's management; |

| 12 | [lp graphic] |

Scope of Analysis |

• | Review of KAC's Letter of Intent dated December 9, 2003; |

|

|

• | Discussions with Gary A. Herder, Chairman of the Board, President and Chief Executive Officer of Prab; Robert W. Klinge, Chief Financial Officer of Prab; Eric V. Brown, Jr., Secretary and Director; and Ned Thompson, Vice President of Operations, regarding Prab's business and financial historical performance, future prospects, the Company's competitive position and industry trends; |

|

|

• | Analysis of public information with respect to certain other companies in lines of businesses we believe to be comparable to Prab, in whole or in part. This includes an examination of current public market prices and resulting valuation statistics and a review of change-of-control transactions for companies deemed comparable to Prab; and |

|

|

• | Review of certain other relevant, publicly available information, including economic, industry and investment information. |

| 13 | [lp graphic] |

Scope of Analysis |

• | Lincoln Partners has relied on information provided by Prab and other public sources without independent verification thereof. |

|

|

• | Lincoln Partners has not conducted an independent appraisal of any of the assets or liabilities of Prab, nor have we made any physical inspection of the properties or assets of Prab. |

|

|

• | In connection with our engagement, Lincoln Partners was not requested to, and Lincoln Partners did not, solicit third party indications of interests for all or part of Prab. Lincoln Partners was not requested to consider, and our opinion does not address, the relative merits of the Proposed Transaction as compared to any alternative business strategies that may exist for Prab or the effect of any other transaction in which Prab might engage. |

| 14 | [lp graphic] |

|

Business Overview

| 15 | [lp graphic] |

Business Overview |

• | Prab, Inc. is engaged in the manufacturing of metal scrap reclamation systems, bulk material handling equipment and conveyor equipment for a variety of industrial markets. For the fiscal year ended October 31, 2003, Prab posted net sales of $13.9 million and adjusted EBITDA of $782 thousand. |

|

|

• | Prab operates in two segments: Prab Conveyors and Hapman Conveyors. The Prab Conveyor segment primarily manufactures metal scrap handling conveyors and complete processing systems. |

|

|

• | The Hapman division, acquired in 1972, designs, engineers and manufactures equipment to facilitate the movement of powders and bulk solids. Hapman serves the pharmaceutical, chemical, food, plastics, mining and waste water treatment industries. |

Note: 2003 EBITDA adjusted to exclude $162,515 of expenses (incremental legal, advisory and Special Committee fees, etc.) related to this going private transaction

| 16 | [lp graphic] |

Business Overview |

• | Prab's scrap metal reclamation systems are priced from $50,000 to $1,500,000. As a result of the high price of larger systems, the Company's sales from year-to-year fluctuate due to the timing of large system orders. |

|

|

• | Prab's sales are well-diversified, with the top customer representing less than 11% of fiscal 2002 sales. The Company's sales are not dependent on one or a few major customers. |

|

|

• | Prab has been selling its metal reclamation systems for many years. As a result, the Company has a large installed base from which are generated significant parts sales. For fiscal 2002, sales of parts represented 23% of sales. |

| 17 | [lp graphic] |

Business Overview |

• | Prab operates from a 72,000 square foot building located in Kalamazoo, Michigan. The facility is owned by the Company. The facility is presently under-utilized with only a first shift operation. Management believes its financial projections can be met without requiring expansion of existing manufacturing capacity. |

|

|

• | As of December 31, 2002, Prab employed 83 people, 81 of which were employed full-time. 36 of the employees are covered by a collective bargaining agreement that expires November 1, 2005. |

| 18 | [lp graphic] |

Business Overview |

• | The following table details Prab's historical operating results from fiscal year 1998 to 2003: |

FYE October 31, |

| 1998 |

| 1999 |

| 2000 |

| 2001 |

| 2002 |

| 2003(1,2) |

|

Sales |

| $ 18,237 |

| $ 15,317 |

| $ 15,687 |

| $ 14,847 |

| $ 12,942 |

| $ 13,898 |

|

Growth |

|

|

| -16.0% |

| 2.4% |

| -5.4% |

| -12.8% |

| 7.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Profit |

| 7,060 |

| 6,060 |

| 5,360 |

| 5,893 |

| 4,656 |

| 5,428 |

|

Gross Margin |

| 38.7% |

| 39.6% |

| 34.2% |

| 39.7% |

| 36.0% |

| 39.1% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income |

| 1,651 |

| 894 |

| 176 |

| 832 |

| 264 |

| 610 |

|

Operating Income Margin |

| 9.1% |

| 5.8% |

| 1.1% |

| 5.6% |

| 2.0% |

| 4.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation and Amortization |

| 184 |

| 210 |

| 206 |

| 201 |

| 196 |

| 172 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EBITDA |

| 1,835 |

| 1,105 |

| 382 |

| 1,033 |

| 460 |

| 782 |

|

EBITDA Margin |

| 10.1% |

| 7.2% |

| 2.4% |

| 7.0% |

| 3.6% |

| 5.6% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital Expenditures |

| 223 |

| 136 |

| 163 |

| 99 |

| 118 |

| 181 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Backlog (a) |

| 3,174 |

| 2,084 |

| 3,984 |

| 2,995 |

| 2,899 |

| 2,693 |

|

Growth |

|

|

| -34.3% |

| 91.2% |

| -24.8% |

| -3.2% |

| -7.1% |

|

(1) Unaudited results provided by management.

(2) $162,515 of going private costs incurred by FY 2003 (incremental legal, advisory and Special Committee fees, etc.) excluded from SG&A.

Source: 10K Fillings for the fiscal years ended October 31(1998-2002), Internal statements for FY 2003.

| 19 | [lp graphic] |

Business Overview |

• | A summary of Prab's balance sheet is provided below: |

Prab, Inc. |

|

|

|

|

|

In 000s |

|

|

|

|

|

|

|

|

|

|

|

Cash | 1,556 |

| Accounts Payable | 993 |

|

Accounts Receivable | 2,239 |

| Customer Deposits | 426 |

|

Inventory | 1,442 |

| Accrued Payroll | 368 |

|

Prepaid Expense | 164 |

| Accrued Commissions | 269 |

|

Deferred Income Taxes | 316 |

| Other | 296 |

|

PP&E, net | 797 |

| Def. Compensation | 24 |

|

Other | 163 |

| Accrued Pension Costs | 441 |

|

Total Assets | $6,677 |

| Shareholders' Equity | 3,862 |

|

|

|

|

| $6,677 |

|

| 20 | [lp graphic] |

|

Industry Impressions

| 21 | [lp graphic] |

Industry Impressions |

Introduction to the Material Handling industry

• | The Material Handling Equipment Manufacturing (MHEM) industry generally includes the following types of products: | |

| - | Conveyors and conveying equipment |

| - | Overhead traveling cranes, hoists and monorail systems |

| - | Industrial truck, tractors, trailers and stacker machinery |

| - | Other material handling equipment |

|

| |

• | The MHEM serves as a good proxy for the industry, representing over $20 billion or approximately 30% to 35% of total U.S. Material Handling consumption. | |

|

| |

• | Demand is driven primarily by macroeconomic factors such as industrial production, capital spending, and housing starts, among others. | |

Source: MHIA, September 2003.

| 22 | [lp graphic] |

Industry Impressions |

Economic outlook

• | A recent survey of 30 professional economists suggests a generally positive outlook for the remainder of 2003 and into 2004(1): | |

| - | After a slow first half, real GDP growth reached an upwardly revised 8.2% in Q3 2003 and should expand by 4.0% in 2004 |

| - | The unemployment rate is expected to fall to 6.1% to 5.8% by the end of 2004 |

| - | Wage growth, forecast to be 3.3% this year and 3.5% next year, should support continued consumer spending |

| - | Continued low (albeit rising) mortgage rates should allow housing to maintain its place as a leading sector in 2003 before tapering off in 2004 |

| - | Deflation is not expected to occur during the forecast horizon |

| - | Corporate profits are projected to grow 8.4% in 2003 and 10.9% in 2004 |

|

| |

• | Middle East turmoil, global terrorism and SARS (and other flu-like epidemics) were considered to pose the greatest risks to the economy. | |

(1) National Association of Business Economists survey of 30 members taken September 2003, as reported by MHIA.

| 23 | [lp graphic] |

Industry Impressions |

• | Annualized new orders and shipments peaked at $20.4 billion in Q1 2001, and have declined steadily since as poor corporate profits and excess capacity have significantly reduced business investment. |

|

|

• | New orders reached a cyclical trough and stabilized in the second and third quarters of 2002. New orders for Q2 2003 declined 3.1% compared to Q2 2002. |

Material Handling Equipment Manufacturing (1992 - 2003)

Source: MHIA, September 2003.

| 24 | [lp graphic] |

Industry Impressions |

• | MHEM has moved into the "decelerating decline," which indicates a tempered forecast for the full year 2003. |

Industrial Sector by Phase of Cycle - June 2003

Source: MHIA and Manufacturers Alliance - MAPI, September 2003.

| 25 | [lp graphic] |

Industry Impressions |

Leading indicators

• | The Material Handling Industry of America (MHIA) believes that six economic factors help predict the cyclicality of the industry and tend to lead by 9 to 21 months: | |

| - | The Institute for Supply Management Index leads by 9 months |

| - | The FRB Industrial Production Index leads by 12 months |

| - | The FRB Capacity Utilization Index leads by 9 to 12 months |

| - | The Consumer Confidence Index leads by 15 months |

| - | The Housing Starts Index leads by 21 months |

| - | The NABE Capital Index leads by 12 months |

|

| |

• | Therefore, some 9 to 21 months after these series bottom out, it is considered likely that MHEM will do the same. | |

|

| |

• | The following three slides illustrate trends in the six leading indicators and the implied trend for the MHEM industry. | |

Note: FRB: Federal Reserve Board; NABE: National Association of Business Economists.

| 26 | [lp graphic] |

Industry Impressions |

Leading indicators

Annual Rate of Change

Institute for Supply Management Index

FRB Industrial Production Index

Source: MHIA, September 2003.

Note: FRB: Federal Reserve Board.

| 27 | [lp graphic] |

Industry Impressions |

Leading indicators

Annual Rate of Change

FRB Capacity Utilization Index

Consumer Confidence Index

Source: MHIA, September 2003.

Note: FRB: Federal Reserve Board.

| 28 | [lp graphic] |

Industry Impressions |

Leading indicators

Annual Rate of Change

Housing Starts Index

NABE Capital Index

Source: MHIA, September 2003.

Note: NABE: National Association of Business Economists.

| 29 | [lp graphic] |

Industry Impressions |

MHEM market forecast

• | 2004 Growth Forecasts: | |

| - | New Orders up 6.5% - 7.5% |

| - | Shipments up 6.0% - 6.5% |

| - | Consumption up 6.0% - 6.5% |

|

| |

• | Forecasts indicate that: | |

| - | The MHEM series will most likely show a "dip" in Q4 2003 and will then follow leading indicators into the next cyclical phase of "accelerating growth" resuming normal expansion for the remainder of 2004 and into 2005 |

|

|

|

| - | Volumes for 2003 are expected to be typical of levels for the period 1995 through 1999 |

Market Forecast for MHEM

Source: MHIA, September 2003.

| 30 | [lp graphic] |

Industry Impressions |

Conclusions

• | Near-term U.S. economic outlook is positive. | |

|

| |

• | The Material Handling Equipment Manufacturing industry is believed to be rebounding from a cyclical downturn that began in Q1 2001: | |

| - | Leading indicators are positive |

| - | Growth expected to recover in Q1 2004, vaulting the industry into the "accelerated growth" category |

|

| |

• | Positive outlook in material handling economic sector activity could create optimism for strategic acquirers: | |

| - | Merger activity has the potential to accelerate |

| - | Increased potential for premium valuations |

| 31 | [lp graphic] |

|

Valuation and Financial Analysis

| 32 | [lp graphic] |

Valuation and Financial Analysis |

• | In order to value Prab, we performed several generally accepted financial, analytical and comparative analyses, the results of which were considered as a whole. This analysis included: | |

|

|

|

| - | Comparable Company Analysis("Comparable Analysis"), in which the performance and market valuation of public companies comparable to the Company are analyzed. |

|

|

|

| - | Comparable Transaction Analysis("Transaction Analysis"), in which publicly available information on comparable change-of-control sales of businesses deemed similar to the Company are analyzed. |

|

|

|

| - | Discounted Cash Flow Analysis ("DCF"), in which the Company's projected free cash flows are discounted back to the present time at a rate appropriate for their risk. A DCF was prepared based on projections of the Company's cash flows. |

| 33 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis

Lincoln Partners reviewed publicly-traded companies and M&A transactions and selected two categories of comparables/targets that reflect the following characteristics of Prab:

• | Conveyor equipment companies - The publicly-traded companies fitting this description sell capital equipment products similar to those produced by Prab. | |

|

| |

• | Other material handling companies- Lincoln Partners selected a group of companies that, like Prab, sell other types of material handling equipment. | |

|

| |

| Other Considerations | |

|

| |

• | Company size: | |

| - | Enterprise value < $500 million |

| - | Sales between $15 million and $500 million |

|

| |

• | M&A transaction timing - within the past three years | |

Note: One transaction, from beyond three years, was included and considered relevant because the acquirer is a public comparable and the target is a strong fit relative to Prab.

| 34 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis

• | Lincoln Partners' initial discussions with management yielded no publicly-traded direct competitors. Management described the U.S. conveyor industry as highly fragmented with few large public companies and numerous privately held organizations. |

|

|

• | Management mentioned a direct competitor, Mayfran International, Inc., which is a subsidiary of a large industrial conglomerate, Tomkins plc. Tomkins was excluded because of Mayfran's size relative to the parent (less than 2% of 2002 sales). |

|

|

• | Lincoln Partners identified several publicly-traded European conveyor manufacturers, but excluded these and focused on U.S. companies more comparable to Prab in terms of geographic markets served, size and other similar operating characteristics. |

| 35 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis

• | After an extensive search, we selected five U.S. conveyor equipment and material handling companies:Cascade Corp.,Columbus McKinnon, Inc.,Key Technology, Inc.,Paragon Technologies, Inc., andQuipp, Inc.as comparable companies for Prab. | |

|

| |

• | In addition to evaluating these five companies quantitatively, we also assessed them as "comparable" to Prab based on the following characteristics: | |

|

| |

| - | Concentration in the materials handling industry |

| - | Percentage of sales from manufacturing |

| - | Cyclical end markets |

| - | Similar size characteristics |

| - | Similar profitability levels |

|

| |

• | The following slides present a quantitative and qualitative analysis of the comparable companies selected. | |

| 36 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis

• | The following table details the LTM operating results of the comparable companies and Prab, Inc. |

| Last Twelve Months | ||||||||||||||

|

|

|

|

| EBITDA |

|

|

| Free Cash |

| CapEx as % | ||||

Cascade Corp. | $ | 284.7 |

| $ | 45.2 |

| 15.9% |

| $ | 13.8 |

| $ | 31.4 |

| 30.6% |

Columbus McKinnon Corp. |

| 439.4 |

|

| 45.6 |

| 10.4% |

|

| 4.9 |

|

| 40.7 |

| 10.7% |

Key Technology, Inc. |

| 82.6 |

|

| 13.2 |

| 16.0% |

|

| 0.5 |

|

| 12.7 |

| 4.0% |

Paragon Technologies, Inc. |

| 36.8 |

|

| 1.0 |

| 2.6% |

|

| 0.2 |

|

| 0.7 |

| 23.2% |

Quipp, Inc. |

| 17.3 |

|

| 0.1 |

| 0.8% |

|

| 0.2 |

|

| (0.0 | ) | 131.2% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mean |

| 172.2 |

|

| 21.0 |

| 9.1% |

|

| 3.9 |

|

| 17.1 |

| 39.9% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Prab | $ | 13.9 |

| $ | 0.8 |

| 5.6% |

| $ | 0.2 |

| $ | 0.6 |

| 23.1% |

Note: Prab's LTM EBITDA adjusted for expenses (detailed in the DCF section) related to this going private transaction.

| 37 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis

• | The following table details the valuation multiples for this group: |

|

|

|

|

|

|

| Firm Value/LTM | |||||

| Market |

|

|

|

|

|

|

|

| |||

Cascade Corp. | $ | 268.7 |

| $ | 22.1 |

| $ | 290.9 |

| 6.4x |

| 1.4x |

Columbus McKinnon Corp. |

| 105.8 |

|

| 290.5 |

|

| 396.2 |

| 8.7x |

| 1.1x |

Key Technology, Inc. |

| 68.6 |

|

| (0.2 | ) |

| 68.3 |

| 5.2x |

| 2.3x |

Paragon Technologies, Inc. |

| 41.8 |

|

| (5.7 | ) |

| 36.0 |

| nmf |

| 2.2x |

Quipp, Inc. |

| 17.4 |

|

| (3.5 | ) |

| 14.0 |

| nmf |

| 1.8x |

|

|

|

|

|

|

|

|

|

|

|

|

|

Mean |

|

|

|

|

|

|

|

|

| 6.8x |

| 1.8x |

| 38 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis | Sales | EBITDA | Firm Value |

| $284.7 | $45.2 | $290.9 |

Cascade Corp. |

| ||

• | Cascade Corp. ("CC") manufactures material handling load engagement devices, hose reels, side shifters and related replacement parts, primarily for the truck lift industry. |

|

|

• | The company is in the same industry as Prab, but is impacted by different end markets (primarily construction and agricultural). CC's financial performance (and to an extent, end markets) has stabilized and the company has been rewarded by a steadily increasing equity market value (58% increase YTD). |

|

|

• | CC is of larger scale than Prab ($280MM in sales) and has significantly higher profitability (16.6% EBITDA margins) on an LTM basis. |

|

|

• | Overall, we would expect CC to trade at a higher multiple than Prab due to its larger size and more attractive profit margins. |

| 39 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis | Sales | EBITDA | Firm Value |

| $439.4 | $45.6 | $396.2 |

Columbus McKinnon Corp. |

| ||

• | Columbus McKinnon Corp. ("CMC") manufactures a wide range of material handling products including hoists, cranes, chains, conveyors, material handling systems, lift tables and parts. |

|

|

• | The company is much larger than Prab, with over $400 million in annual sales. CMC has grown primarily through acquisition. The company has acquired 14 companies since 1994. |

|

|

• | CMC's EBITDA margins are significantly higher than Prab. The company's EBITDA/Sales margin (on an LTM basis) was 10.4% compared to 5.6% for Prab. |

|

|

• | Overall, we would expect CMC to trade at a higher multiple than Prab due to its larger size, steady financial performance and more attractive profit margins. |

| 40 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis | Sales | EBITDA | Firm Value |

| $82.6 | $13.2 | $68.3 |

Key Technology, Inc. |

| ||

• | Key Technology, Inc. ("Key") designs and manufactures process automation systems that integrate optical inspection equipment, sorters, conveying equipment, scanners and detection systems. These systems appear to be more complex and involve a greater element of technology than Prab's products. As such, they may command greater margins. |

|

|

• | The company primarily serves the food, pharmaceutical, and tobacco industries - all of which tend to be non-cyclical. Thus, even through the economic recession, Key's sales and profitability have increased. |

|

|

• | Key's EBITDA/sales margin on an LTM basis is significantly higher than Prab's (16.0% versus 5.6%). |

|

|

• | Overall, based on Key's more complex products, attractive end markets and higher profitability, we would expect the company to trade at a higher multiple than Prab. |

| 41 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis | Sales | EBITDA | Firm Value |

| $36.8 | $1.0 | $36.0 |

Paragon Technologies, Inc. |

| ||

• | Paragon Technologies, Inc. ("PT") is a specialized systems integrator supplying branded, automated material handling systems to manufacturing, assembly, order selection and distribution operations. The company also manufactures branded, conveyor products. |

|

|

• | Although PT is involved in the material handling industry, as the company's name implies, a significant portion of PT's business involves systems integration (39%) rather than manufacturing (61%). Thus, we would expect PT's business model, in the long term, to generate higher margins than Prab. |

|

|

• | With annual sales under $40 million, PT is comparable in size to Prab. |

|

|

• | In contrast to Prab, PT's profitability has improved on an LTM basis compared to 2002 results. Thus, we would expect PT to trade at a higher multiple than Prab. |

| 42 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis | Sales | EBITDA | Firm Value |

| $17.3 | $0.1 | $14.0 |

Quipp, Inc. |

| ||

• | Quipp, Inc. ("Quipp") manufactures post-press material handling equipment to newspaper publishers, with newspaper conveyor systems comprising a majority of sales. |

|

|

• | Quipp's primary end market, newspaper publishing, is highly cyclical and has experienced a prolonged downturn. Similar to Prab, Quipp sells its products as part of integrated systems and individual units. |

|

|

• | Although Quipp's current size and LTM profitability levels are very similar to Prab's, the company, in the recent past (2000), has demonstrated an ability to generate significantly greater earnings than Prab. In FY 2000, the company posted sales and EBITDA of $35.4 million and $7.2 million, respectively. |

|

|

• | Given Quipp's historical earnings levels, which have been substantially higher than Prab's we would expect Quipp to trade higher than Prab. |

| 43 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis

• | For a variety of reasons, each company specific, we would expect all of the companies in our comparable group to trade higher than Prab. |

|

|

• | We evaluated the comparable company group based on valuation multiples of earnings and book value to determine a comparable valuation range for Prab. We used the bottom quartile of ranges for both techniques and applied this range to Prab. |

|

|

• | The range of Total Enterprise Value/Book Value multiples for our comparable group was 1.1x - 2.3x. Because we would expect Prab to trade at the lower end of the range, we determined Prab's value using the bottom quartile of the sample group or 1.1x - 1.4x book value. |

|

|

• | The range of Total Enterprise Value/EBITDA multiples was 5.2x - 8.7x. Again, we used the bottom quartile of the sample group or 5.2x - 6.1x for Prab. |

| 44 | [lp graphic] |

Valuation and Financial Analysis |

Comparable company analysis

• | Applying these value ranges to Prab yields the following dollar ranges: |

| Book Value(1) | $3,478 |

|

|

|

|

|

|

|

| Comparable Company Multiple Range | 1.1 |

| 1.4 |

| Total Enterprise Value | $3,825 |

| $4,869 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Trailing 12-month EBITDA(2) | $782 |

|

|

|

|

|

|

|

| Comparable Company Multiple Range | 5.2 |

| 6.1 |

| Total Enterprise Value | $4,067 |

| $4,771 |

(1) Book Value has been adjusted down by the difference between the net pension termination liability ($825,000) and Prab's Accrued Pension Cost ($441,000) or by $384,000.

(2) EBITDA adjusted to exclude $162,515 of expenses (incremental legal, advisory and Special Committee fees, etc.) related to this going private transaction

| 45 | [lp graphic] |

Valuation and Financial Analysis |

Comparable transaction analysis

• | We analyzed seven transactions that occurred in the materials handling industry. |

|

|

• | The transactions were selected based on the following factors: |

| - | A majority of the companies' operations were dedicated to manufacturing materials handling equipment; |

|

|

|

| - | From a size standpoint, all the transactions were less than $275 million in purchase price; and |

|

|

|

| - | The transactions occurred within the last four years. Although we had hoped to used a shorter historical time period, due to the limited number of transactions, we extended our search in order to include a larger sample size. |

| 46 | [lp graphic] |

Valuation and Financial Analysis |

Comparable transactions analysis

• | The following table summarizes the transactions that were examined. |

($ in millions) |

|

|

|

|

|

|

| Transaction Value/LTM | |||

|

|

|

| Transaction |

| EBITDA |

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

Conveying Systems |

|

|

|

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

|

|

|

Aug-02 |

| Grove Worldwide | Manitowoc Company, |

|

|

|

|

|

|

|

|

Nov-00 |

| Blue Giant | TBM Holdings, Inc. |

| 11 |

| 3.8% |

| 6.3x |

| 1.6x |

May-00 |

| Lee Engineering Co., | TBM Holdings, Inc. |

|

|

|

|

|

|

|

|

Feb-00 |

| Long Reach Holdings, | TBM Holdings, Inc. |

|

|

|

|

|

|

|

|

Sep-99 |

| Ermanco, Inc. | Paragon Technologies |

| 23 |

| 12.6% |

| 5.8x |

| 5.3x |

|

| Conveyor Company A | Financial Sponsor |

| <$125 |

| 28.8% |

| 5.1x |

| nmf |

|

| Conveyor Company B | Financial Sponsor |

| <$125 |

| 21.5% |

| 7.1x |

| 5.2x |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Mean |

|

|

| 12.3% |

| 6.5x |

| 2.5x |

|

|

|

|

|

|

|

|

|

|

|

|

(1) Unable to accurately calculate Lee Engineering standalone EBITDA due to high levels of corporate expenses allocated.

Note: Conveyor Company A and Conveyor Company B represent proprietary transactions where Lincoln Partners acted as a sell side advisor. For confidentiality reasons, specific details of these transactions have not been disclosed.

| 47 | [lp graphic] |

Valuation and Financial Analysis |

Comparable transactions analysis

• | Descriptions of the target companies are provided below: |

| - | Grove Worldwide:Manufacturer of material handling equipment, including mobile hydraulic cranes and aerial work platforms. The company's products are used in the construction and general industrial markets, among others. |

|

|

|

| - | Blue Giant Equipment Corp.:Manufactures loading dock equipment, dock safety products, dock lifts, scissor lifts and industrial pallet trucks and stackers. |

|

|

|

| - | Lee Engineering Co., Inc.:Manufactures material handling equipment including pallet stackers, scissor lifts and dock lifts under the Presto Lifts and Regal brand names. |

|

|

|

| - | Long Reach Holdings, Inc.:Manufactures lift truck attachments and material handling equipment. |

|

|

|

| - | Ermanco, Inc.:Manufacturer, designer and installer of complete conveying systems for a variety of manufacturing and warehousing applications. |

|

|

|

| - | Conveyor Company A:Manufacturer of material handling systems or products. |

|

|

|

| - | Conveyor Company B: Manufacturer of material handling systems or products. |

| 48 | [lp graphic] |

Valuation and Financial Analysis |

Comparable transactions analysis

• | The range of implied valuation multiples for the comparable transactions we analyzed varied significantly. Reasons for such variation included: |

- | Differences in the future growth expectations for the respective target companies; | |

|

| |

| - | Differences in profitability (such as EBITDA margin) of the target acquisition; |

|

|

|

| - | Differences in the strategic rationale for the respective transactions, from the perspective of both the buyers and the sellers; and |

|

|

|

| - | Differences in the magnitude, as well as the form, of synergistic opportunities between the buyers and sellers (i.e., cost savings and new revenue opportunities). |

|

|

|

| - | Differences in how the acquiring company valued the company (i.e., on a cash flow or book value basis). |

| 49 | [lp graphic] |

Valuation and Financial Analysis |

Comparable transactions analysis

• | These transaction multiples are based on LTM financial data for the target as of the acquisition date. |

|

|

• | Although these acquisitions may have been priced based on potential cost savings or incremental revenue growth, we were unable to adjust the EBITDA figures for these factors since more detailed information was not available. |

|

|

• | As a result, these multiples may be overstated as the LTM EBITDA used may not reflect the incremental operating income obtained. |

| 50 | [lp graphic] |

Valuation and Financial Analysis |

Comparable transactions analysis

• | We evaluated the comparable transactions based on valuation multiples of earnings and book value to determine a valuation range for Prab. The range of Total Enterprise Value/EBITDA multiples was 5.1x - 8.0x, which we applied to Prab. |

|

|

• | Three of the transactions involved target companies that demonstrated strong financial performance and profitability (as shown by their EBITDA margins). We believe these companies were sold primarily based on their earnings rather than book values. |

|

|

• | In contrast, four transactions involved companies that, like Prab, suffered from lackluster earnings performance as reflected in their low, and in two instances negative, EBITDA margins. These four transactions were Grove Worldwide, Blue Giant, Lee Engineering/Presto Lifts and Long Reach Holdings, Inc. As a benchmark, we believe these four companies represent a more relevant comparison of book value for Prab. |

| 51 | [lp graphic] |

Valuation and Financial Analysis |

Comparable transactions analysis

• | The range of Total Enterprise Value/Book Value for the four companies was 1.0.x - 1.6x, which we applied to Prab. |

|

|

• | A summary of our value ranges for Prab based on our comparable transaction analysis is as follows: |

| Book Value(1) | $3,478 |

|

|

|

|

|

|

|

| Comparable Company Multiple Range | 1.0 |

| 1.6 |

| Total Enterprise Value | $3,478 |

| $5,564 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Trailing 12-month EBITDA(2) | $782 |

|

|

|

|

|

|

|

| Comparable Company Multiple Range | 5.1 |

| 8.0 |

| Total Enterprise Value | $3,988 |

| $6,256 |

(1) Adjusted to reflect unbooked pension liability.

(2) EBITDA adjusted to exclude $162,515 of expenses (incremental legal, advisory and Special Committee fees, etc.) related to this going private transaction

| 52 | [lp graphic] |

Valuation and Financial Analysis |

Discounted cash flow analysis ("DCF")

• | Prab's future cash flows were projected for a five year period and discounted to the present at an appropriate cost of capital. |

|

|

• | The Company's terminal value was calculated in 2008 using the Gordon Growth perpetuity formula. |

|

|

• | Due to the nature of Prab's business which can involve a single order of significant dollar value, year-to-year results can easily be skewed by only a few orders. Therefore, we calculated a five year average of Prab's earnings to use as the basis of our DCF analysis. |

| 53 | [lp graphic] |

Valuation and Financial Analysis |

DCF - Base Year Calculation

• | A summary of 1999-2003 historical results is provided below: |

Historical Income Statements

per 10K Filings, Management

(Dollars in thousands)

FYE October 31 | 1999 |

| 2000 |

| 2001 |

| 2002 |

| 2003(1,3) |

|

Sales | 15,317 |

| 15,687 |

| 14,847 |

| 12,942 |

| 13,898 |

|

COGS | (9,257 | ) | (10,327 | ) | (8,954 | ) | (8,286 | ) | (8,470 | ) |

Gross Profit | 6,060 |

| 5,360 |

| 5,893 |

| 4,656 |

| 5,428 |

|

Gross Margin | 39.6% |

| 34.2% |

| 39.7% |

| 36.0% |

| 39.1% |

|

|

|

|

|

|

|

|

|

|

|

|

SG&A | (5,166 | ) | (5,184 | ) | (5,061 | ) | (4,392 | ) | (4,818 | ) |

Add Back: Pension Expense (Income) | (14 | ) | (20 | ) | 17 |

| 48 |

| 0 |

|

SG&A | (5,180 | ) | (5,204 | ) | (5,045 | ) | (4,344 | ) | (4,818 | ) |

Operating Income | 881 |

| 156 |

| 848 |

| 312 |

| 610 |

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation | 210 |

| 206 |

| 201 |

| 196 |

| 172 |

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted EBITDA | 1,091 |

| 362 |

| 1,049 |

| 508 |

| 782 |

|

|

|

|

|

|

|

|

|

|

|

|

Capital Expenditures | (136 | ) | (163 | ) | (99 | ) | (118 | ) | (181 | ) |

| Average |

| Add |

| Base Year |

|

Sales | 14,538 |

|

|

| 14,538 |

|

COGS | (9,059 | ) |

|

| (9,059 | ) |

Gross Profit | 5,479 |

|

|

| 5,479 |

|

Gross Margin | 37.7% |

|

|

| 37.7% |

|

|

|

|

|

|

|

|

SG&A | (4,924 | ) |

|

| (4,924 | ) |

Add Back: Pension Expense (Income) | 6 |

|

|

| 6 |

|

SG&A | (4,918 | ) | 64 |

| (4,854 | ) |

Operating Income | 561 |

| 64 |

| 625 |

|

|

|

|

|

|

|

|

Depreciation | 197 |

|

|

| 197 |

|

|

|

|

|

|

|

|

Adjusted EBITDA | 758 |

| 64 |

| 822 |

|

|

|

|

|

|

|

|

Capital Expenditures | (140 | ) |

|

| (140 | ) |

(1) | 2003 unaudited year end financials provided by management. |

(2) | Includes $63,830 of public company expenses provided by management (assumes maintaining board). |

(3) | $162,515 of going private costs incurred in FY 2003 (incremental legal fees, advisory, Special Committee, etc.) excluded from SG&A |

| 54 | [lp graphic] |

Valuation and Financial Analysis |

DCF - Assumptions

• | As shown in the previous slide, the base year was calculated using operating results from 1999-2003. Important to note, the base year EBITDA ($822 thousand) used in the DCF, based on 5-year average operating results, was significantly higher than the 2004 forecast provided by management ($427 thousand). |

|

|

• | Sales are projected to grow at 3% annually, which is in line with overall U.S. economic growth projections. Because the base year already incorporates an average of five historic years, we believe only minimal growth from the base average is warranted. |

|

|

• | Depreciation decreases gradually to equal capital expenditures in the last forecasted year. |

|

|

• | EBITDA margins remain constant from base year level. |

|

|

• | Earnings are taxed at the Company's tax rate of 40%. |

| 55 | [lp graphic] |

Valuation and Financial Analysis |

DCF - Assumptions

• | We made two adjustments to the 5-year EBITDA average to calculate our base year: |

Pension Liability

| • | Several bidders voiced concern regarding Prab's defined benefit plan which is underfunded, creating a liability on the Company's balance sheet. Because this liability is not ever-green and, at some point, must be paid, we deducted it from the DCF. |

|

|

|

| • | We added the 5-year average pension expense from EBITDA and deducted the net pension termination liability from our DCF analysis. |

Costs of a Public Company

| • | As a public Company, Prab incurs some annual expenses that would be eliminated under private ownership. These nominal expenses were added back to the 5-year average EBITDA calculation. |

| 56 | [lp graphic] |

Valuation and Financial Analysis |

DCF - Assumptions

• | The working capital base year was calculated using the twelve month average from fiscal 2003. |

|

|

• | Working capital grows at the rate of sales growth. |

|

|

• | Capital expenditures remain constant at the five year average. |

| 57 | [lp graphic] |

Valuation and Financial Analysis |

DCF -Summary of projected operating results

• | A summary of projected operating results is provided below: |

(Dollars in thousands) |

|

|

|

|

|

|

|

|

| |||||

|

|

|

|

|

|

|

|

|

| |||||

| 2004F |

| 2005F |

| 2006F |

| 2007F |

| 2008F | |||||

Sales | $ | 14,974 |

| $ | 15,424 |

| $ | 15,886 |

| $ | 16,363 |

| $ | 16,854 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EBITDA | $ | 854 |

| $ | 894 |

| $ | 906 |

| $ | 946 |

| $ | 961 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales Growth |

| 3.0% |

|

| 3.0% |

|

| 3.0% |

|

| 3.0% |

|

| 3.0% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EBITDA Margin |

| 5.7% |

|

| 5.8% |

|

| 5.7% |

|

| 5.8% |

|

| 5.7% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Working Capital | $ | 1,543 |

| $ | 1,589 |

| $ | 1,637 |

| $ | 1,686 |

| $ | 1,737 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital Expenditures | $ | 140 |

| $ | 140 |

| $ | 140 |

| $ | 140 |

| $ | 140 |

| 58 | [lp graphic] |

Valuation and Financial Analysis |

DCF - Assumptions

• | The weighted average cost of capital ("WACC") depends on the Company's capital structure (i.e. the amount of senior, subordinated debt and equity). |

|

|

• | This capital structure does not reflect the Company's current leverage as we assumed that the amount of debt will increase to a sustainable level consistent with other players in the industry. |

|

|

• | We calculated three different WACCs using three slightly different capital structures. |

|

|

• | The WACC takes into account the tax deductibility of debt. |

|

|

• | Based on our WACC analysis, our discount rates for the Company ranged from 13.0% to 14.0%. |

|

|

• | We assumed a terminal growth rate of 1% to reflect the mature industry and limited above average growth potential. |

| 59 | [lp graphic] |

Valuation and Financial Analysis |

DCF - Results

• | As shown by the chart below, the Company's firm value ranges from $3.0 million to $3.3 million depending on the discount rate used in our analysis. |

| Discount |

| Firm Values |

|

|

|

|

|

|

| 14.0% |

| $ 3,043 |

|

|

|

|

|

|

| 13.5% |

| $ 3,174 |

|

|

|

|

|

|

| 13.0% |

| $ 3,315 |

|

| 60 | [lp graphic] |

|

Summary Conclusions

| 61 | [lp graphic] |

Summary Conclusions |

Implied firm values

| (Dollars in thousands) |

| Implied Firm |

| ||

|

|

|

|

|

|

|

| Discounted Cash Flow |

| $ 3,043 | - | $ 3,315 |

|

|

|

|

|

|

|

|

| Comparable Transactions: |

|

|

|

|

|

| Multiple of: |

|

|

|

|

|

| EBITDA |

| $ 3,988 |

| $ 6,256 |

|

|

|

|

|

|

|

|

| Book Value |

| $ 3,478 |

| $ 5,564 |

|

|

|

|

|

|

|

|

| Comparable Companies: |

|

|

|

|

|

| Multiple of: |

|

|

|

|

|

| EBITDA |

| $ 4,067 |

| $ 4,771 |

|

|

|

|

|

|

|

|

| Book Value |

| $ 3,825 |

| $ 4,869 |

|

| 62 | [lp graphic] |

Summary Conclusions |

Per share analysis

(Dollars in thousands, except per share values) | Comparable Companies |

| Comparable Transactions |

| Discounted | |||||||||

| Book Value |

| EBITDA |

| Book Value |

| EBITDA |

| Cash Flow | |||||

Implied Value (high end of range) | $ | 4,869 |

| $ | 4,771 |

| $ | 5,564 |

| $ | 6,256 |

| $ | 3,315 |

Add: Exercise of Options(2) |

| 248 |

|

| 248 |

|

| 248 |

|

| 248 |

|

| 248 |

Add: Look-Back Value(3) |

| 255 |

|

| 255 |

|

| 255 |

|

| 255 |

|

| 255 |

Adjusted Shareholders Equity | $ | 5,372 |

| $ | 5,274 |

| $ | 6,068 |

| $ | 6,760 |

| $ | 3,819 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares Outstanding(1) |

| 1,418.610 |

|

| 1,418.610 |

|

| 1,418.610 |

|

| 1,418.610 |

|

| 1,418.610 |

Add: Exercise of Options |

| 191.000 |

|

| 191.000 |

|

| 191.000 |

|

| 191.000 |

|

| 191.000 |

Add: Look-Back Shares |

| 150.049 |

|

| 150.049 |

|

| 150.049 |

|

| 150.049 |

|

| 150.049 |

Shares Outstanding Fully Diluted |

| 1,759.659 |

|

| 1,759.659 |

|

| 1,759.659 |

|

| 1,759.659 |

|

| 1,759.659 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

High value per share | $ | 3.05 |

| $ | 3.00 |

| $ | 3.45 |

| $ | 3.84 |

| $ | 2.17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Implied Value (low end of range) | $ | 3,825 |

| $ | 4,067 |

| $ | 3,478 |

| $ | 3,988 |

| $ | 3,043 |

Add: Exercise of Options(2) |

| 248 |

|

| 248 |

|

| 248 |

|

| 248 |

|

| 248 |

Add: Look-Back Value(3) |

| 255 |

|

| 255 |

|

| 255 |

|

| 255 |

|

| 255 |

Adjusted Shareholders Equity | $ | 4,329 |

| $ | 4,570 |

| $ | 3,981 |

| $ | 4,492 |

| $ | 3,547 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares Outstanding(1) |

| 1,418.610 |

|

| 1,418.610 |

|

| 1,418.610 |

|

| 1,418.610 |

|

| 1,418.610 |

Add: Exercise of Options |

| 191.000 |

|

| 191.000 |

|

| 191.000 |

|

| 191.000 |

|

| 191.000 |

Add: Look-Back Shares |

| 150.049 |

|

| 150.049 |

|

| 150.049 |

|

| 150.049 |

|

| 150.049 |

Shares Outstanding Fully Diluted |

| 1,759.659 |

|

| 1,759.659 |

|

| 1,759.659 |

|

| 1,759.659 |

|

| 1,759.659 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Low value per share | $ | 2.46 |

| $ | 2.60 |

| $ | 2.26 |

| $ | 2.55 |

| $ | 2.02 |

(1) Source: Prab, Inc.'s Form10Q for the quarterly period ended July 31, 2003.

(2) Source: Management; approximately 105,000 stock options have been granted since the latest 10-K filing for the yearly period ended October 31, 2002 for a total of 191,000 with a weighted average exercise price of $1.30.

(3) In May 2003, the Company made an agreement to repurchase 150,049 shares that contains "Look-Back-Event" and "Look-Back-Value" provisions for a period of twelve months that entitles the shareholders the right to additional payment for value above $1.70.

| 63 | [lp graphic] |

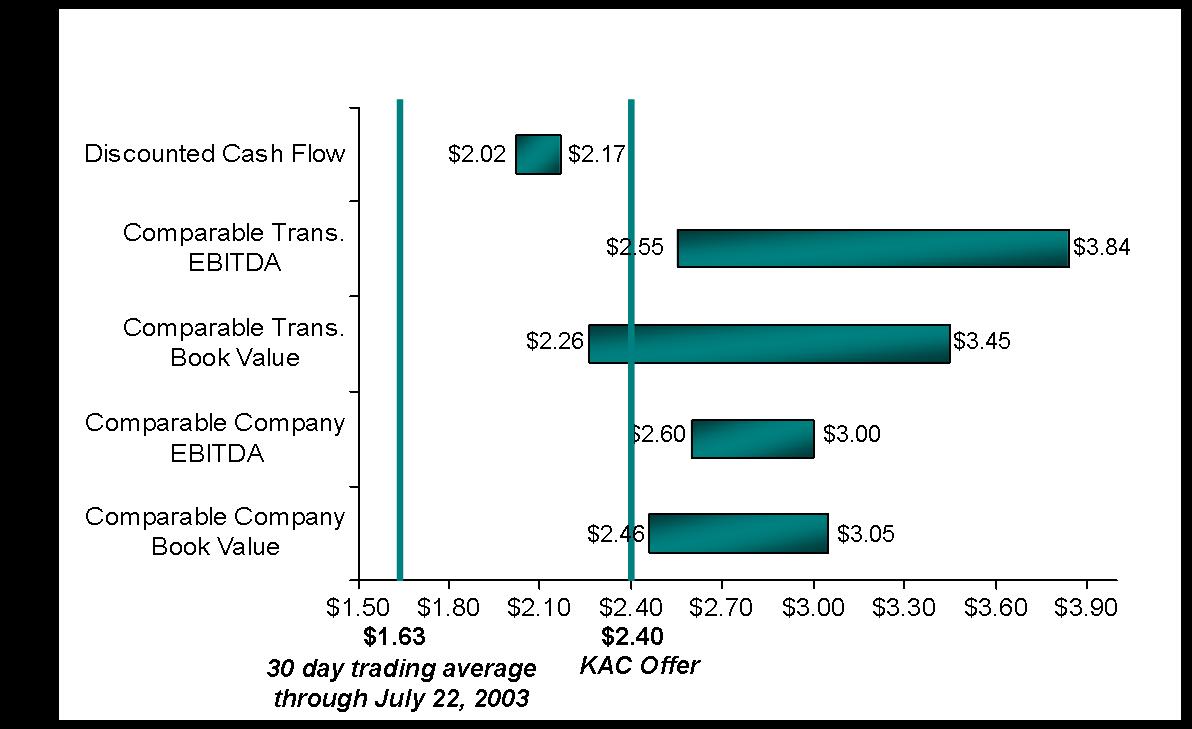

Summary Conclusions |

Lincoln Partners' summary value per share

| 64 | [lp graphic] |

Summary Conclusions |

Other considerations

• | In addition to the three analytical methods used to arrive at our opinion, Lincoln Partners considered the percent premium offered : |

| - | The 5-year average premium (1998-2002) offered for transactions with a purchase price of $25 million or less is 44.8%. |

|

|

|

| - | Applying a 44.8% premium to the 30 day average trading price would imply a $2.36/share. |

|

|

|

| - | KAC's bid of $2.40/share or $3.7 million represents a premium of 47% over the 30 day average trading price prior to KAC's initial bid for Prab. |

|

|

|

| - | KAC's bid exceeds the average premium offered on similarly-sized transactions. |

Source: Mergerstat Review.

Note: Five year average premium excludes negative premiums.

| 65 | [lp graphic] |

Summary Conclusions |

Other considerations

• | Lincoln Partners also considered the following factors: |

| - | Size: With a total enterprise value less than $5.0 million, Prab's valuation would be significantly discounted for size. Based on our experience as investment bankers, it is unlikely that a company of this size with similar business characteristics would sell for more than 5.0x EBITDA or $3.9 million. |

|

|

|

| - | Lack of Interested Bidders: Prab was "in play" for over four months, during which eleven interested parties emerged. However, the Special Committee eventually received only one final, written offer for the Company. |

|

|

|

| - | Final Price Relative to Initial Offer: KAC's final offer of $2.40/share or $3.7 million represents a 20% increase over their initial bid of $2.00/share. |

| 66 | [lp graphic] |

Summary Conclusions |

Based upon and subject to the foregoing, our experience as investment bankers, our analysis as demonstrated in this document and other factors we deemed relevant, we are of the opinion that, as of the date hereof, the price and terms for the proposed sale of Prab, Inc. to Kalamazoo Acquisition Corporation for a price and under terms specified in the Letter of Intent dated December 9, 2003 are fair to the shareholders of Prab from a financial point of view.

| 67 | [lp graphic] |

|

Appendix

| 68 | [lp graphic] |