Fifth Third Bank | All Rights Reserved Annual Meeting of Fifth Third Shareholders April 15, 2008 Kevin Kabat, President & CEO Exhibit 99.1 |

2 Fifth Third Bank | All Rights Reserved Agenda Difficult economic environment Credit mitigation Comparative outperformance Operating strengths Building a better tomorrow |

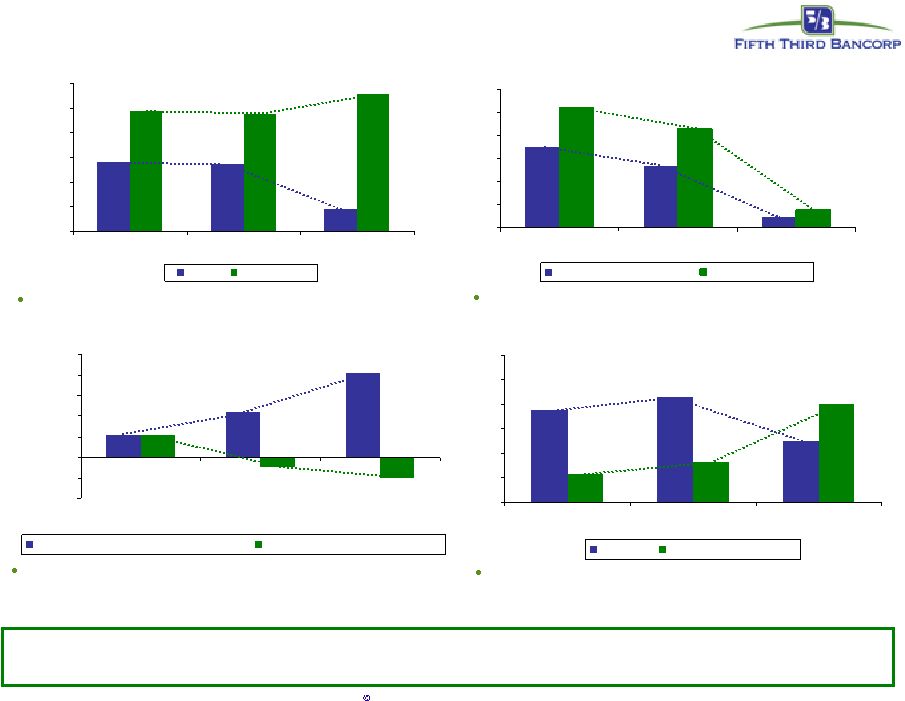

3 Fifth Third Bank | All Rights Reserved 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 10 Yr. Avg. Last 6 Mos. 2008 F Fed Funds Spreads (Bank Sub Debt) Difficult environment Unemployment is expected to approach 6% in 2008 with Detroit approaching 9%. Current banking environment has severely deteriorated. 2008 looks to be the banking industry’s worst year in the past two decades. While the Fed is aggressively reducing rates to bolster these markets, credit spreads continue to widen. Foreclosures will more than double 2007’s elevated levels and housing depreciation will significantly impact losses on foreclosures. Retail sales and consumer spending levels effect continued talk of recession. A prolonged recession will increase loss assumptions for 2009 and beyond. 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 10 Yr. Avg. Last 6 Mos. 2008 F GDP Unemployment Labor market 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 10 Yr. Avg. Last 6 Mos. 2008 F Consumer Spending (Annual) Retail Sales (Annual) Retail and consumer spending -20.00% -10.00% 0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 10 Yr. Avg. Last 6 Mos. 2008 F Growth in Foreclosures as % of Total Loans Housing Price Appreciation (Annual) Housing market Interest rate market |

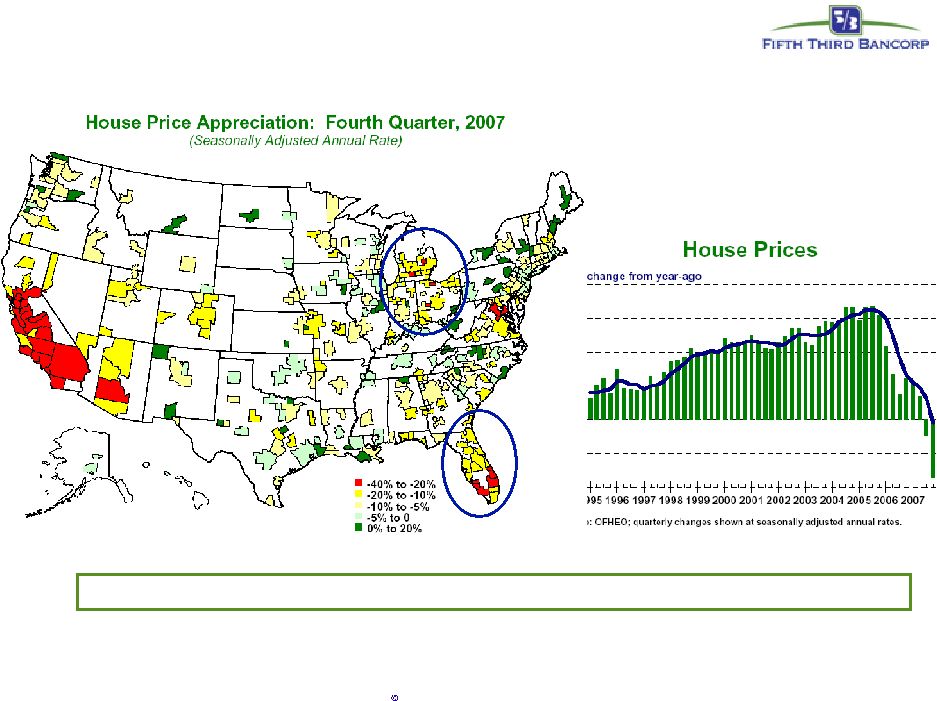

4 Fifth Third Bank | All Rights Reserved Difficult environment Housing prices have declined significantly in many parts of our footprint Map from Global Insight/National City Corporation |

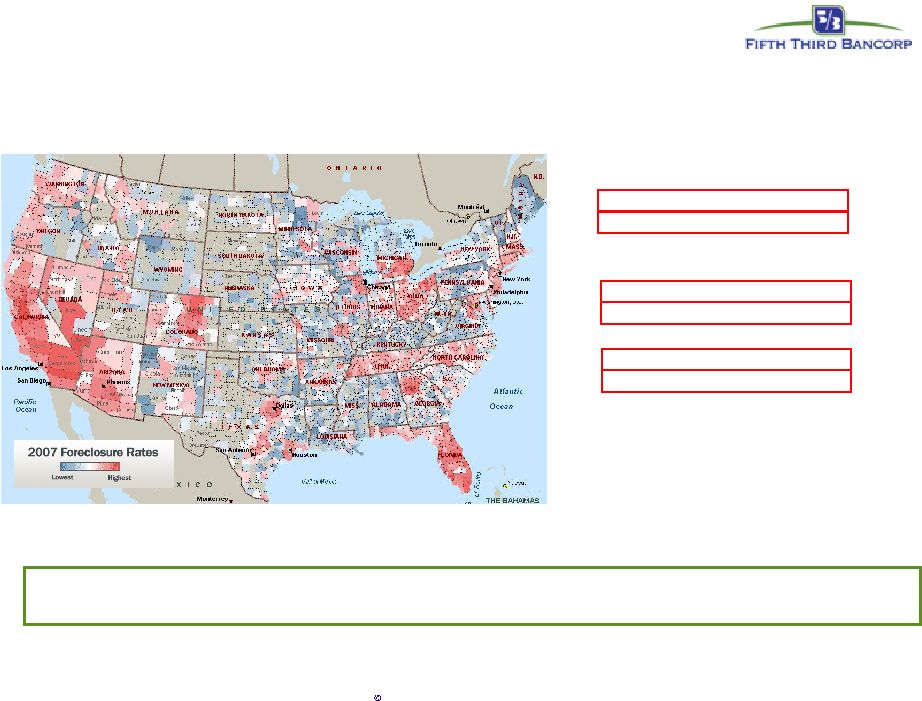

5 Fifth Third Bank | All Rights Reserved Difficult environment Our footprint has experienced very high foreclosure rates during 2007, most notably in Florida, Michigan, and Ohio Source: Realty Trac 2007 foreclosure rates 1 Nevada 3.38 2 Florida 2.00 3 Michigan 1.95 4 California 1.92 5 Colorado 1.92 6 Ohio 1.80 7 Georgia 1.57 8 Arizona 1.52 9 Illinois 1.25 10 Indiana 1.03 Foreclosure rates by state |

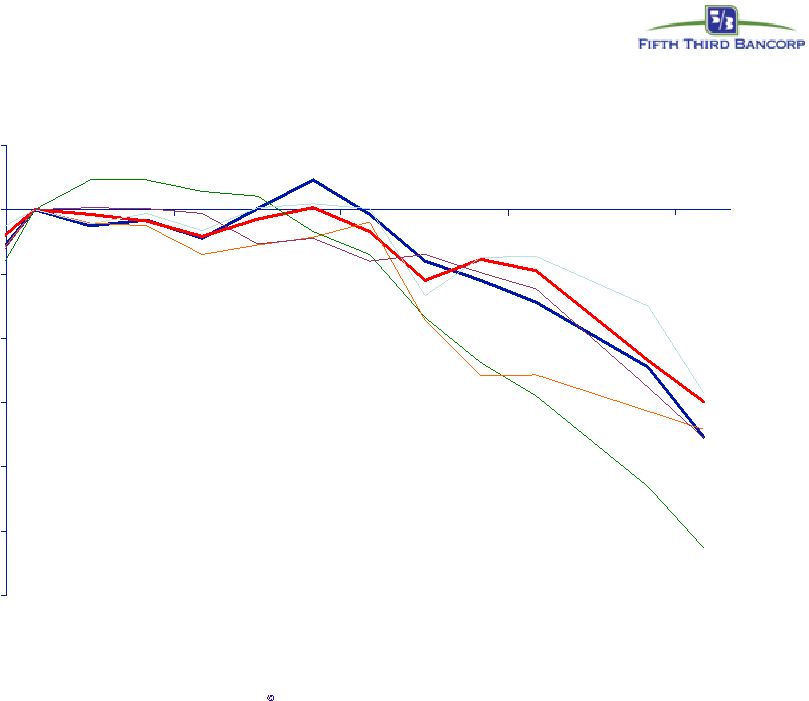

6 Fifth Third Bank | All Rights Reserved 2007 total return (change in price plus dividends) -60.00% -50.00% -40.00% -30.00% -20.00% -10.00% 0.00% 10.00% 12/06 03/07 06/07 09/07 12/07 FITB: -35% MI: -29% NCC: -53% HBAN: -34% KEY: -36% S&P banks: - 30% |

7 Fifth Third Bank | All Rights Reserved Credit containment Fifth Third has consistently maintained conservative underwriting standards throughout all credit cycles. Geographic and economic issues have required aggressive management action Eliminated all brokered HELOC production Suspended all new developer lending Significantly tightened underwriting limits and exception authorities Centralized all credit approvals Major expansion of commercial and consumer workout teams Aggressive write downs in stressed geographies Significant addition to reserve levels Direct executive management oversight of every major credit decision Fifth Third has moved aggressively to stay ahead of emerging credit issues |

8 Fifth Third Bank | All Rights Reserved Credit containment Fifth Third has developed and implemented targeted strategies to help our customers who are experiencing financial difficulties. Options include: — Refinancing – saleable or on balance sheet — Rate reductions, term extensions and loss mitigations Loss mitigation strategies have been enhanced as follows: — Payment affordability – expanded payment reduction options including: – Rate reductions – Interest and fees waivers – Principal balance reductions (temporary or permanent) – Suspension of penalty interest assessed after delinquency grace period. |

9 Fifth Third Bank | All Rights Reserved 133% 58.6% 10.0% 6% 6% 1% 1% Midwest peers (3) 2007 In line Outperformed Outperformed Outperformed Outperformed Outperformed Outperformed 2007 performance vs. peers 134% 56.4% 14.3% 9% 7% 5% 3% FITB 2007 142% NPA growth 58.7% 10.0% Operating efficiency ratio (1) Operating ROE (1) 3% Operating fee growth (1) 5% 2% Average loan growth NII growth 1% Average core deposit growth Large bank peers (2) 2007 (1) Excludes certain previously reported one-time charges from fee growth, efficiency ratio, and ROE . Reported fee growth was 23%, reported efficiency ratio was 60.2%, reported ROE was 11.2%. (2) Large bank peer average consists of BBT, CMA, HBAN, KEY, MTB, MI, NCC, PNC, RF, STI, USB, WB, WM, WFC and ZION; for peer deposit, loan, NPA, and fee comparisons, excludes HBAN, NCC, PNC, RF, WB and WFC due to significant impact of acquisitions. (3) Midwest peer average consists of HBAN, KEY, MI, CMA, NCC and USB, except where outlined above. Source: SNL and company reports Peer performance summary Continue to outperform on key value drivers; credit challenging |

10 Fifth Third Bank | All Rights Reserved (CAGR: 2007 vs. 2003: per share) 1 Excludes certain previously reported one-time charges from fee growth, efficiency ratio, and ROE: reported efficiency ratio was 60.2%, reported ROE was 11.2%. 2 Median of large bank peers; median revenue growth of seven processing companies (CEN, DST, PAYX, ADS, FISV, GPN, TSS); 3 Average of large Midwest peers (NCC, HBAN, MI, KEY, CMA, USB). Source: SNL Financial; data shown per share to adjust for effect of acquisitions. Strong underlying performance 10.0% 10.0% 14.3% Operating ROE (1) 58.6% 58.7% 56.4% Operating efficiency ratio (1) 17% 19% 22% Credit card loan growth N/A 14% 16% Processing fee growth (1) 4% 6% 9% Core deposit growth 8% 9% 13% Loan growth Midwest Peers 3 Peer Group 2 Fifth Third |

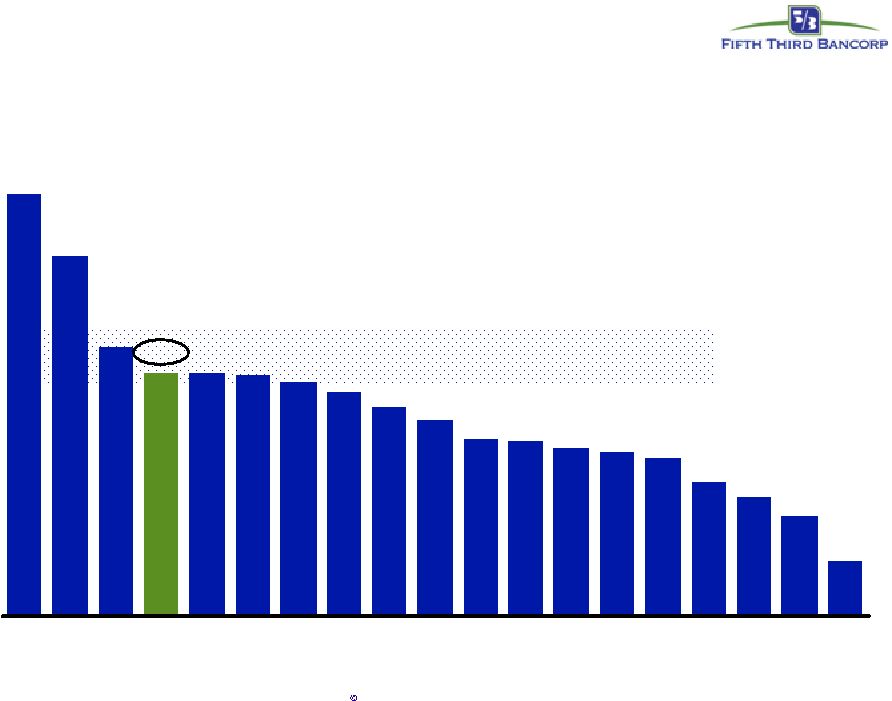

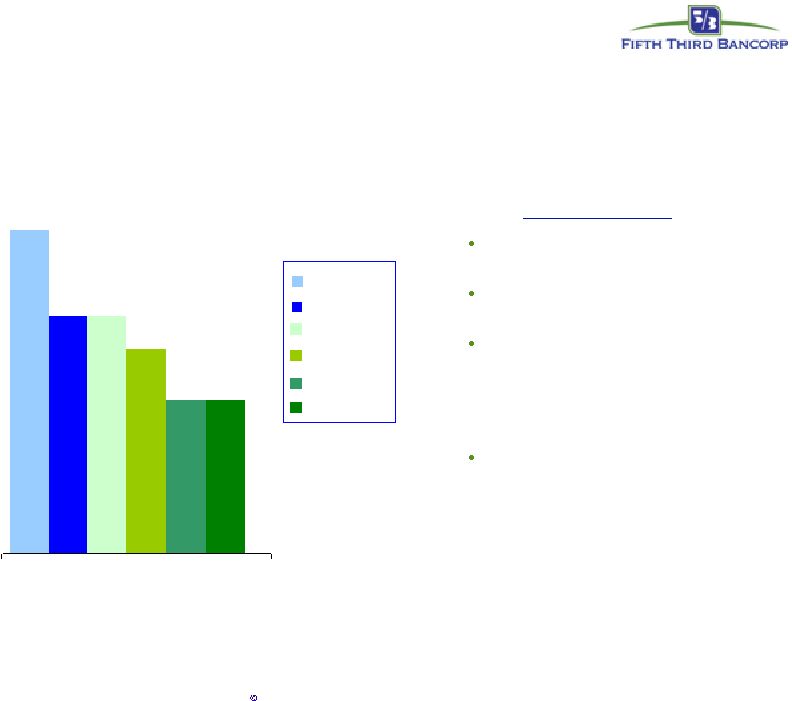

11 Fifth Third Bank | All Rights Reserved 9.01% 7.99% 6.03% 6.02% 5.99% 5.88% 5.70% 5.47% 5.27% 4.95% 4.90% 4.81% 4.74% 4.61% 4.22% 3.98% 3.65% 2.93% 6.46% MI CMA KEY FITB WFC STI RF ZION BBT NCC MTB JPM HBAN USB PNC WM WB BAC C Strong tangible capital position Peer group: U.S. banks sharing similar geography or debt ratings. Source: SNL Target : 6-6.5% Tangible common equity as % of tangible assets |

12 Fifth Third Bank | All Rights Reserved Fifth Third differentiators Integrated affiliate delivery model Aggressive sales culture Operational efficiency Streamlined decision making Integrated payments platform (FTPS) Acquisition integration Customer satisfaction |

13 Fifth Third Bank | All Rights Reserved University of Michigan – ACSI survey Surveyed customers of large U.S. banks 2007 Citigroup Fifth Third Wachovia Wells Chase B of A 69 74 72 74 79 *Fifth Third Bank engaged the American Customer Satisfaction Index (ACSI) in custom research projects surveying Fifth Third Bank customers in the 4th quarter of 2007. In the surveys, ACSI used the same statistical methodology as the independently measured banks, Wachovia, Bank of America, Chase, Wells Fargo, and Citigroup 2007 key actions Financial center service optimization initiative launched Added KDI component to new incentive compensation plan Implemented a consistent process and support tools for handling customers problems at the financial centers and call center Created a central escalation team to manage problems that cannot be resolved immediately 69 |

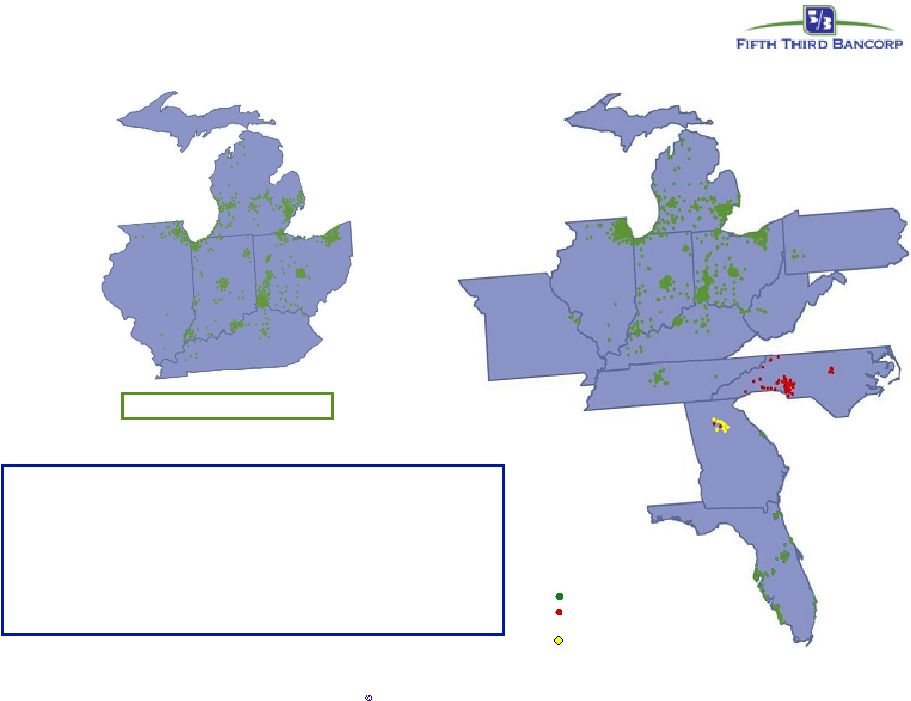

14 Fifth Third Bank | All Rights Reserved Cincinnati Florence Louisville Lexington Nashville Atlanta Augusta Orlando Tampa Naples Raleigh Charlotte Huntington Pittsburgh Cleveland Columbus Toledo Detroit Grand Rapids Traverse City Chicago Evansville Jacksonville Indianapolis Fifth Third’s current footprint First Charter (subject to regulatory approval) First Horizon branches (pending) St. Louis Today* Cincinnati Florence Louisville Lexington Cleveland Columbus Toledo Detroit Grand Rapids Traverse City Chicago Evansville Indianapolis Geographic diversification First quarter 2004 15 branches in Florida 12 6 # of states with branches 1,296 960 Banking centers $79B $55B Deposits $116B $94B Assets Today* 1Q04 * Pro forma as of 12/31/07 for pending acquisitions |

15 Fifth Third Bank | All Rights Reserved Fifth Third: building a better tomorrow Consistently outperform the U.S. banking industry Deliver growth in excess of industry Enhance the customer experience Increase employee engagement Institutionalize enterprise operational excellence |

16 Fifth Third Bank | All Rights Reserved Cautionary statement This report may contain forward-looking statements about Fifth Third Bancorp and/or the company as combined acquired entities within the meaning of Sections 27A of the Securities Act of 1933, as amended, and Rule 175 promulgated thereunder, and 21E of the Securities Exchange Act of 1934, as amended, and Rule 3b-6 promulgated thereunder, that involve inherent risks and uncertainties. This report may contain certain forward-looking statements with respect to the financial condition, results of operations, plans, objectives, future performance and business of Fifth Third Bancorp and/or the combined company including statements preceded by, followed by or that include the words or phrases such as “believes,” “expects,” “anticipates,” “plans,” “trend,” “objective,” “continue,” “remain” or similar expressions or future or conditional verbs such as “will,” “would,” “should,” “could,” “might,” “can,” “may” or similar expressions. There are a number of important factors that could cause future results to differ materially from historical performance and these forward-looking statements. Factors that might cause such a difference include, but are not limited to: (1) general economic conditions and weakening in the economy, specifically the real estate market, either national or in the states in which Fifth Third, one or more acquired entities and/or the combined company do business, are less favorable than expected; (2) deteriorating credit quality; (3) political developments, wars or other hostilities may disrupt or increase volatility in securities markets or other economic conditions; (4) changes in the interest rate environment reduce interest margins; (5) prepayment speeds, loan origination and sale volumes, charge-offs and loan loss provisions; (6) our ability to maintain required capital levels and adequate sources of funding and liquidity; (7) changes and trends in capital markets; (8) competitive pressures among depository institutions increase significantly; (9) effects of critical accounting policies and judgments; (10) changes in accounting policies or procedures as may be required by the Financial Accounting Standards Board or other regulatory agencies; (11) legislative or regulatory changes or actions, or significant litigation, adversely affect Fifth Third, one or more acquired entities and/or the combined company or the businesses in which Fifth Third, one or more acquired entities and/or the combined company are engaged; (12) ability to maintain favorable ratings from rating agencies; (13) fluctuation of Fifth Third’s stock price; (14) ability to attract and retain key personnel; (15) ability to receive dividends from its subsidiaries; (16) potentially dilutive effect of future acquisitions on current shareholders' ownership of Fifth Third; (17) effects of accounting or financial results of one or more acquired entity; (18) difficulties in combining the operations of acquired entities; (19) ability to secure confidential information through the use of computer systems and telecommunications network; and (20) the impact of reputational risk created by these developments on such matters as business generation and retention, funding and liquidity. Additional information concerning factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements is available in the Bancorp's Annual Report on Form 10-K for the year ended December 31, 2007, filed with the United States Securities and Exchange Commission (SEC). Copies of this filing are available at no cost on the SEC's Web site at www.sec.gov or on the Fifth Third’s Web site at www.53.com. Fifth Third undertakes no obligation to release revisions to these forward-looking statements or reflect events or circumstances after the date of this report. |

Fifth Third Bank | All Rights Reserved Annual Meeting of Fifth Third Shareholders April 15, 2008 |