© Fifth Third Bank | All Rights Reserved Citi 2010 Financial Services Conference Kevin T. Kabat Chairman, President & Chief Executive Officer March 11, 2010 Please refer to earnings release dated January 21, 2010 and 10-K dated February 26, 2010 for further information, including full results reported on a U.S. GAAP basis Exhibit 99.1 |

2 © Fifth Third Bank | All Rights Reserved 4Q09 in review Prudent management of credit position • Net charge-offs declined 6% • Early and late stage delinquencies declined significantly from 3Q09 • NPAs, excluding loans held-for-sale, increased 1% from the previous quarter • Reserve position remains strong, at 4.88% of loans and 127% of nonperforming loans • Realized credit losses have been significantly below SCAP scenarios Strong capital levels • Tangible common equity ratio of 6.5% • Tier 1 common ratio of 7.0% • Tier 1 capital ratio of 13.3% • Exceeded $1.1 billion SCAP capital commitment by 80% Continued core business momentum • Net loss of $98 million vs. 3Q09 net loss of $97 million (3Q included Visa benefit of $206 million after-tax) – Pre-tax net loss of $210 million, vs. 3Q09 pre-tax $420 million loss excluding Visa benefit – Currently expect further improvement in 1Q10 • Net interest margin of 3.55%, up 12 bps sequentially • Average core deposits up 11%, wholesale funding down 44% year-over-year • Extended $19 billion of new and renewed credit |

|

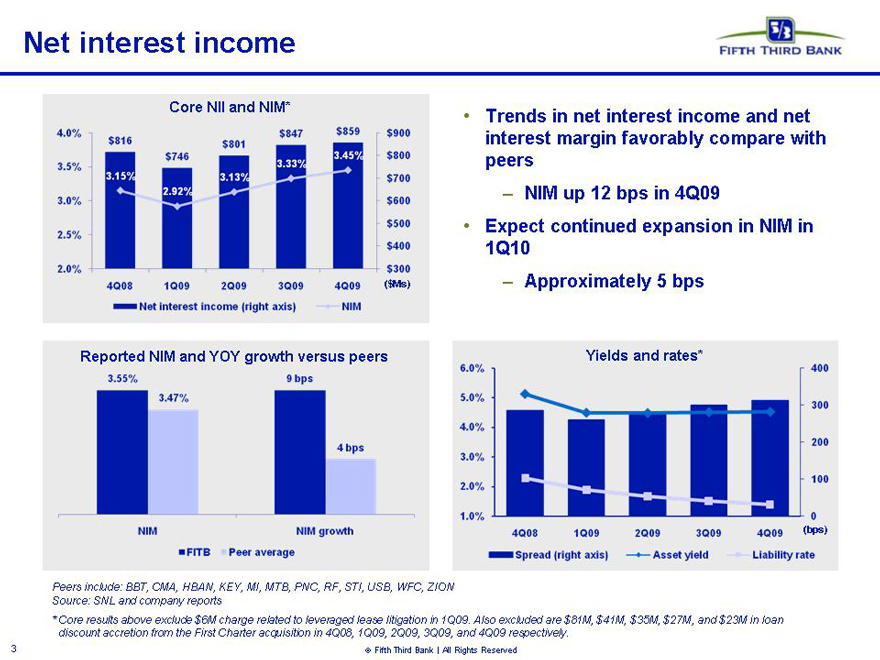

Net interest income

Core NII and NIM*

4.0% 3.5% 3.0% 2.5% 2.0%

$816 $746 $801 $847 $859

3.15% 2.92% 3.13% 3.33% 3.45%

$900 $800 $700 $600 $500 $400 $300 ($Ms)

4Q08 1Q09 2Q09 3Q09 4Q09

Net interest income (right axis) NIM

• Trends in net interest income and net interest margin favorably compare with peers

– NIM up 12 bps in 4Q09

• Expect continued expansion in NIM in 1Q10

– Approximately 5 bps

Reported NIM and YOY growth versus peers

3.55% 3.47% 9bps 4bps

NIM NIM growth

FITB Peer average

Yields and rates*

6.0% 5.0% 4.0% 3.0% 2.0% 1.0%

4Q08 1Q09 2Q09 3Q09 4Q09

400 300 200 100 0 (bps)

Spread (right axis) Asset yield Liability rate

Peers include: BBT, CMA, HBAN, KEY, MI, MTB, PNC, RF, STI, USB, WFC, ZION

Source: SNL and company reports

* Core results above exclude $6M charge related to leveraged lease litigation in 1Q09. Also excluded are $81M, $41M, $35M, $27M, and $23M in loan discount accretion from the First Charter acquisition in 4Q08, 1Q09, 2Q09, 3Q09, and 4Q09 respectively.

©Fifth Third Bank | All Rights Reserved

3 |

|

|

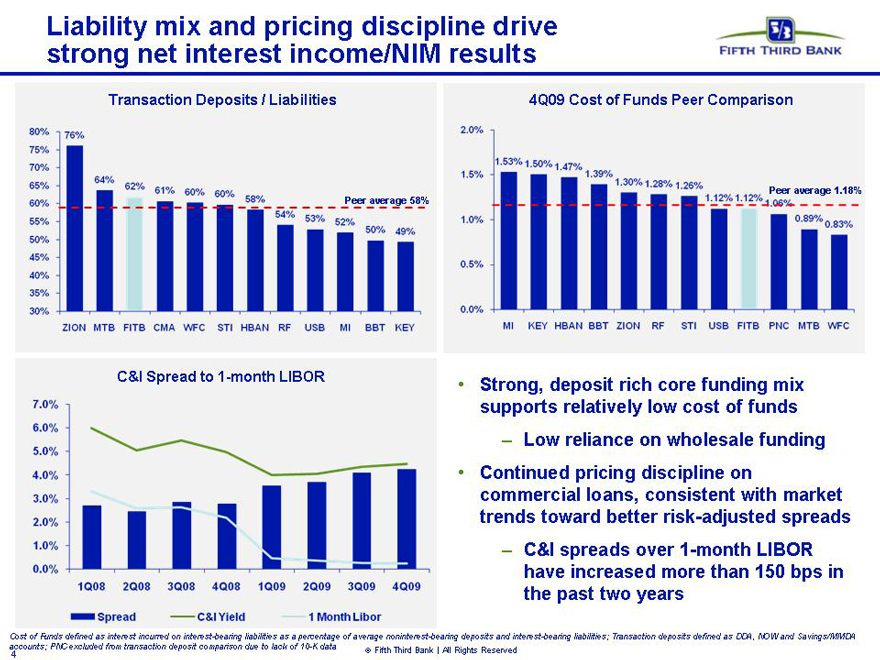

Liability mix and pricing discipline drive strong net interest income/NIM results

Transaction Deposits / Liabilities

80% 75% 70% 65% 60% 55% 50% 45% 40% 35% 30%

76% 64% 62% 61% 60% 58% 54% 53% 52% 50% 49%

Peer average 58%

ZION MTB FITB CMA WFC STI HBAN RF USB MI BBT KEY

4Q09 Cost of Funds Peer Comparison

2.0% 1.5% 1.0% 0.5% 0.0%

1.53% 1.50% 1.47% 1.39% 1.30% 1.28% 1.26% 1.12% 1.12% 1.06% 0.89% 0.83%

Peer average 1.18%

MI KEY HBAN BBT ZION RF STI USB FITB PNC MTB WFC

C&I Spread to 1-month LIBOR

7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0%

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

Spread C&I Yield 1 Month Libor

• Strong, deposit rich core funding mix supports relatively low cost of funds

– Low reliance on wholesale funding

• Continued pricing discipline on commercial loans, consistent with market trends toward better risk-adjusted spreads

– C&I spreads over 1-month LIBOR have increased more than 150 bps in the past two years

Cost of Funds defined as interest incurred on interest-bearing liabilities as a percentage of average noninterest-bearing deposits and interest-bearing liabilities; Transaction deposits defined as DDA, NOW and Savings/MMDA accounts; PNC excluded from transaction deposit comparison due to lack of 10-K data

© Fifth Third Bank | All Rights Reserved

4 |

|

|

Balance sheet:

Continued growth in core funding

Average loan growth ($B)

86 84 82 80 78

33 34 33 33 32

53 50 49 47 46

4Q08 1Q09 2Q09 3Q09 4Q09

Commercial Loan Consumer Loans

Average core deposit growth ($B)

+11%

64 67 69 70 72

15 16 16 17 16

21 21 21 21 22

28 30 32 32 34

4Q08 1Q09 2Q09 3Q09 4Q09

Demand/IBT Savings/MMDA Consumer CD/Core foreign

Average wholesale funding ($B)

(44%)

40 35 31 26 22

13 13 11 10 10

13 10 8 6 4

14 12 12 10 8

4Q08 1Q09 2Q09 3Q09 4Q09

LT debt ST borrowings Non-core deposits

Extended nearly $75B of new and renewed credit in 2009

• CRE loans down 4% sequentially and 17% year-over-year

– Reduced exposure to homebuilder/developer and other non-owner occupied loans; sale or transfer to held-for-sale of $1.3B in 4Q08

– New homebuilder/developer, non-owner occupied CRE suspended 2008

• C&I loans down 6% sequentially and 15% from 4Q08 largely due to lower line utilization and soft demand

• Strong mortgage originations - $2.0B in residential mortgage loans held-for-sale warehouse (not carried in loans held-for investment)

• Core deposit to loan ratio of 93%, up from 75% in 4Q08

• Everyday Great Rates strategy continues to drive core deposit growth

– DDAs up 6% sequentially and 24% from the previous year

– Commercial core deposits up 12% sequentially and 28% from the previous year

– Retail core deposits were flat sequentially and up 6% from the previous year

• Reduced wholesale funding by $3.8 billion sequentially and $17.5 billion from the previous year

– Non-core deposits down 19% sequentially and 39% from the previous year

– Short term borrowings down 39% sequentially and 73% from the previous year

– Long-term debt up 3% sequentially and down 21% from the previous year

• Portion of excess core funding invested in agency mortgage-backed securities (balance sheet hedges added to mitigate interest rate risk)

©Fifth Third Bank | All Rights Reserved

5 |

|

6 © Fifth Third Bank | All Rights Reserved Deposit share momentum • Continued focus on customer satisfaction and building full relationships has given strong momentum to the retail network • Fifth Third grew deposits in 15 of 16 affiliate markets in 2009 – Modest attrition in North Carolina acquisition market • Fifth Third grew deposit market share in 75% of affiliate markets in 2009 Affiliate 5/3 Deposit (08-09) 5/3 Market Share Name Deposit ($) (%) Share 2009 2008 Chicago 788,601 9.8% 4.0% 3.8% Northeastern Ohio 606,708 17.0% 4.2% 3.8% South Florida 579,342 21.1% 3.1% 2.8% Eastern Michigan 418,525 11.9% 5.4% 5.0% Central Florida 338,091 28.9% 3.0% 2.5% Tampa 334,080 24.5% 3.5% 3.1% Central Ohio 213,971 5.6% 11.1% 11.2% Cincinnati 212,656 2.2% 21.5% 21.9% Southern Indiana 195,169 8.6% 4.1% 4.0% Louisville 194,593 13.0% 8.9% 8.2% Northwestern Ohio 177,122 7.5% 16.2% 15.4% Western Michigan 149,252 2.1% 18.4% 18.4% Tennessee 142,615 12.8% 3.5% 3.3% Central Indiana 139,354 4.7% 8.4% 8.3% Central Kentucky 2,608 0.3% 8.1% 8.7% North Carolina (113,631) -4.4% 4.8% 5.3% Source: FDIC, SNL Financial; branches included are full service retail / brick and mortar; data excludes headquarters branches with over $250 million in deposits. |

7 Fee income and expenses – core trends* 556 620 645 605 629 650 659 653 623 578 $0 $100 $200 $300 $400 $500 $600 $700 4Q08 1Q09 2Q09 3Q09 4Q09 Core Fee Income Excluding the Effect from Credit Core fee income ($M) Core expenses ($M) 998 913 912 939 945 892 826 866 839 890 $0 $200 $400 $600 $800 $1,000 $1,200 4Q08 1Q09 2Q09 3Q09 4Q09 Core Noninterest Expense Excluding the Effect from Credit • Strong mortgage banking results continued in 4Q09, resulting in $4.4B of originations and $132M in net revenue • Investment advisory revenue up 4% from the previous quarter driven by higher market values • Card and processing revenue increased 3% sequentially and 9% from the previous year (excluding divested EPP revenue) • Corporate banking revenue up 15% sequentially driven by growth in institutional sales, interest rate derivative sales revenue, and business lending fees • Equity income from the FTPS JV was $8M in the fourth quarter versus $7M the previous quarter • Credit related cost affected fee income by $30M in 4Q09 compared with $45M the previous quarter • Declines in core expenses driven by broad-based, disciplined expense control • Core efficiency ratio of 62.5% in 4Q09, an improvement from 63.5% in 3Q09 and 68.7% in 4Q08 • Credit related costs affected non-interest expenses by $55M in 4Q09 compared with $100M the previous quarter • Total credit losses on mortgage repurchases ~$65M in 2009 (~$20M in 4Q09) * Refer to slide 6 for itemized effects of non-core fees and expenses © Fifth Third Bank | All Rights Reserved |

|

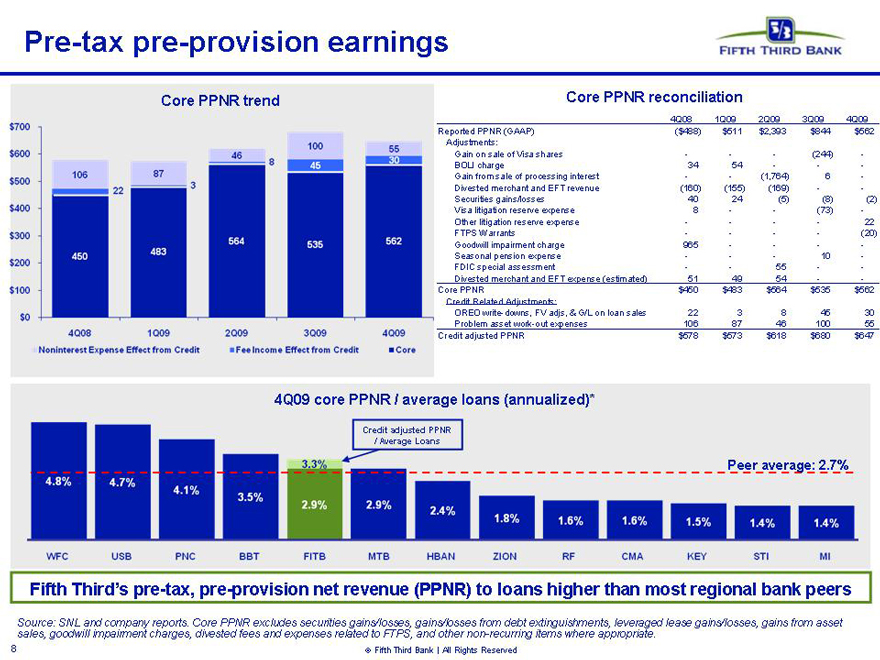

Pre-tax pre-provision earnings

Core PPNR trend

$700

$600

$500

$400

$300

$200

$100

$0

106 87 46 100 55

22 3 8 45 30

450 483 564 535 562

4Q08 1Q09 2Q09 3Q09 4Q09

Noninterest Expense Effect from Credit

Fee Income Effect from Credit

Core

4Q09 core PPNR / average loans (annualized)*

Credit adjusted PPNR

/ Average Loans

Peer average: 2.7%

3.3%

4.8% 4.7% 4.1% 3.5% 2.9% 2.9% 2.4% 1.8% 1.6% 1.6% 1.5% 1.4% 1.4%

WFC

USB

PNC

BBT

FITB

MTB

HBAN

ZION

RF

CMA

KEY

STI

MI

Fifth Third’s pre-tax, pre-provision net revenue (PPNR) to loans higher than most regional bank peers

Source: sales, goodwill SNL and impairment company charges, reports. Core divested PPNR fees excludes and expenses securities related gains/losses, to FTPS, gains/losses and other from non-recurring debt extinguishments, items where appropriate. leveraged lease gains/losses, gains from asset

© Fifth Third Bank | All Rights Reserved

8 |

|

9 © Fifth Third Bank | All Rights Reserved Portfolio performance drivers Performance largely driven by No participation in exotic mortgages Discontinued or suspended lending * Residential construction-related consumer mortgages intended to be held in portfolio until permanent financing complete. Jumbo mortgage originations currently being held due to market conditions. Geography • Florida and Michigan most stressed • Remaining Midwest and Southeast performance reflect economic trends Products • Homebuilder/developer charge-offs $110 million in 4Q09 – Total charge-off ratio 3.6% (3.1% ex-HBs) – Commercial charge-off ratio 4.1% (3.2% ex- HBs) • Brokered home equity charge-offs 7.0% in 4Q09 – Direct home equity portfolio 1.9% 4Q09 NCO Ratios Coml Cons Total FL/MI 8.4% 5.3% 7.1% Other 2.5% 2.1% 2.3% • Subprime • Option ARMs Discontinued in 2007 • Brokered home equity ($2.9B down to $1.9B) Suspended in 2008 • Homebuilder/residential development ($3.3B down to $1.6B) • Other non-owner occupied commercial RE excluding homebuilder/developer ($9.2B down to $8.0B) Saleability • All mortgages originated for intended sale* Total 4.1% 3.0% 3.6% |

|

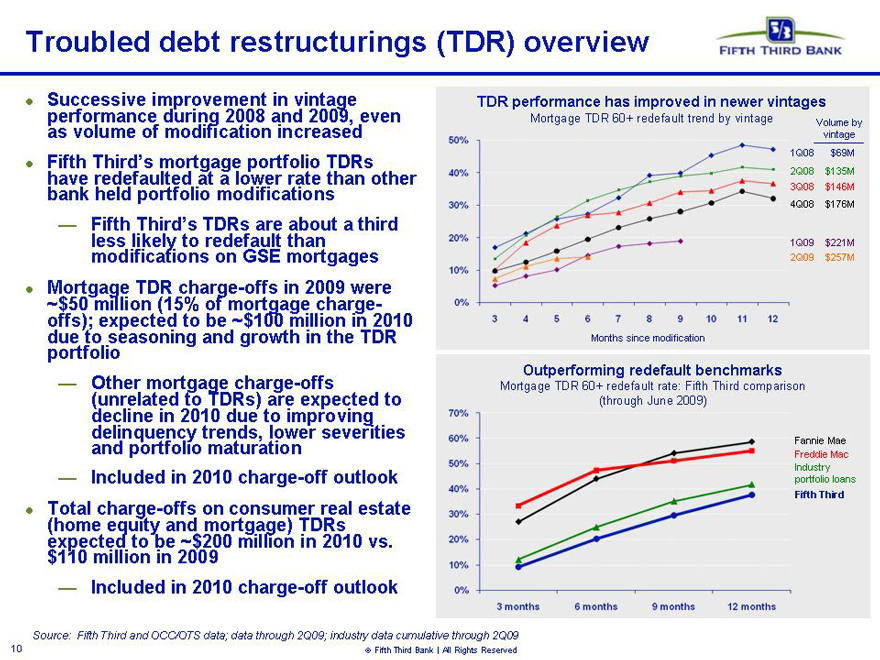

Troubled debt restructurings (TDR) overview

Successive improvement in vintage performance during 2008 and 2009, even as volume of modification increased

Fifth Third’s mortgage portfolio TDRs have redefaulted at a lower rate than other bank held portfolio modifications

Fifth Third’s TDRs are about a third less likely to redefault than modifications on GSE mortgages

Mortgage TDR charge-offs in 2009 were ~$50 million (15% of mortgage charge-offs); expected to be ~$100 million in 2010 due to seasoning and growth in the TDR portfolio

Other mortgage charge-offs (unrelated to TDRs) are expected to decline in 2010 due to improving delinquency trends, lower severities and portfolio maturation

Included in 2010 charge-off outlook

Total charge-offs on consumer real estate (home equity and mortgage) TDRs expected to be ~$200 million in 2010 vs. $110 million in 2009

Included in 2010 charge-off outlook

TDR performance has improved in newer vintages

Mortgage TDR 60+ redefault trend by vintage

50%

40%

30%

20%

10%

0%

3 |

| 4 5 6 7 8 9 10 11 12 |

Volume by

vintage

1Q08 $69M

2Q08 $135M

3Q08 $146M

4Q08 $176M

1Q09 $221M

2Q09 $257M

Months since modification

Outperforming redefault benchmarks

Mortgage TDR 60+ redefault rate: Fifth Third comparison (through June 2009)

Fannie Mae Freddie Mac Industry portfolio loans

Fifth Third

70%

60%

50%

40%

30%

20%

10%

0%

3 |

| months |

6 |

| months |

9 months

12 months

Source: Fifth Third and OCC/OTS data; data through 2Q09; industry data cumulative through 2Q09

Fifth Third Bank | All Rights Reserved

10

|

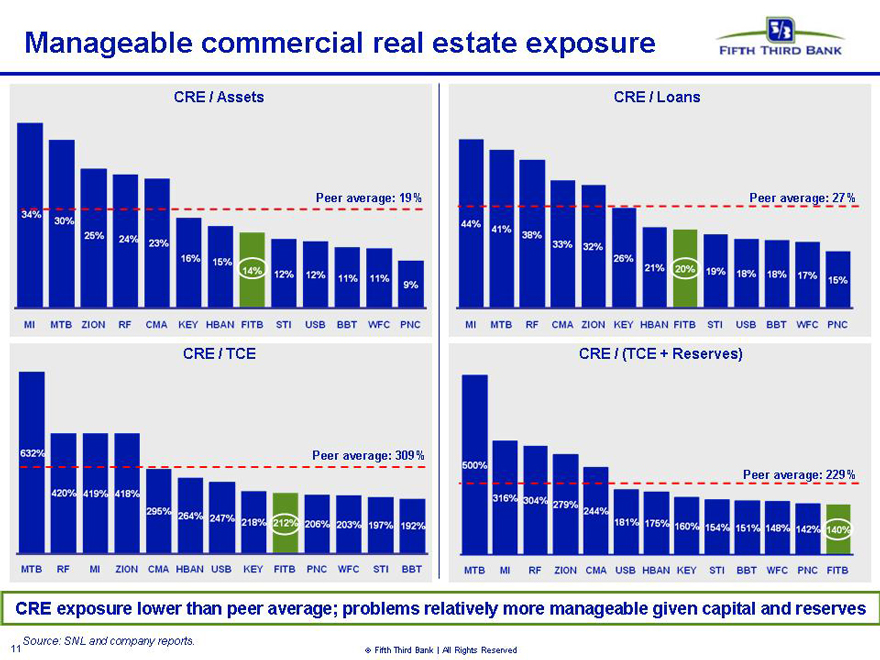

Manageable commercial real estate exposure

CRE / Assets

Peer average: 19%

34% 30% 25% 24% 23% 16% 15% 14% 12% 12% 11% 11% 9%

MI MTB ZION RF CMA KEY HBAN FITB STI USB BBT WFC PNC

CRE / Loans

Peer average: 27%

44% 41% 38% 33% 32% 26% 21% 20% 19% 18% 18% 17% 15%

MI MTB RF CMA ZION KEY HBAN FITB STI USB BBT WFC PNC

CRE / TCE

Peer average: 309%

632% 420% 419% 148% 295% 264% 247% 218% 212% 206% 203% 197% 192%

MTB RF MI ZION CMA HBAN USB KEY FITB PNC WFC STI BBT

CRE / (TCE + Reserves)

Peer average: 229%

500% 316% 304% 249% 244% 181% 175% 160% 154% 151% 148% 142% 140%

MTB MI RF ZION CMA USB HBAN KEY STI BBT WFC PNC FITB

CRE exposure lower than peer average; problems relatively more manageable given capital and reserves

Source: SNL and company reports.

©Fifth Third Bank | All Rights Reserved

11

|

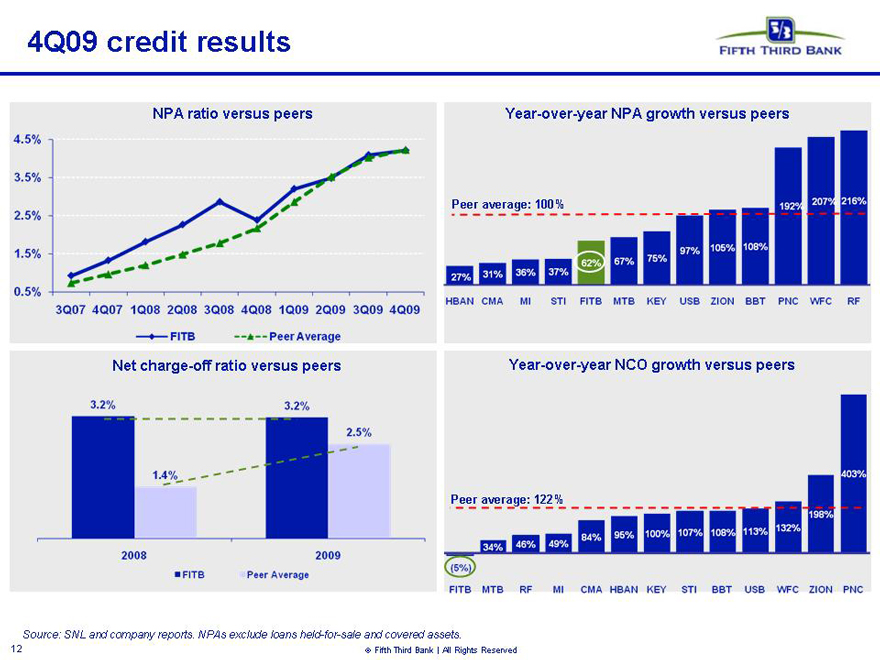

4Q09 credit results

NPA ratio versus peers

4.5%

3.5%

2.5%

1.5%

0.5%

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

FITB

Peer Average

Year-over-year NPA growth versus peers

Peer average: 100%

27% 31% 36% 37% 62% 67% 75% 97% 105% 108% 192% 207% 216%

HBAN CMA MI STI FITB MTB KEY USB ZION BBT PNC WFC RF

Net charge-off ratio versus peers

3.2% 3.2%

1.4% 2.5%

2008 2009

FITB

Peer Average

Year-over-year NCO growth versus peers

Peer average: 122%

5% 34% 46% 49% 84% 95% 100% 107% 108% 113% 132% 198% 403%

FITB MTB RF MI CMA HBAN KEY STI BBT USB WFC ZION PNC

Source: SNL and company reports. NPAs exclude loans held-for-sale and covered assets.

©Fifth Third Bank | All Rights Reserved

12

|

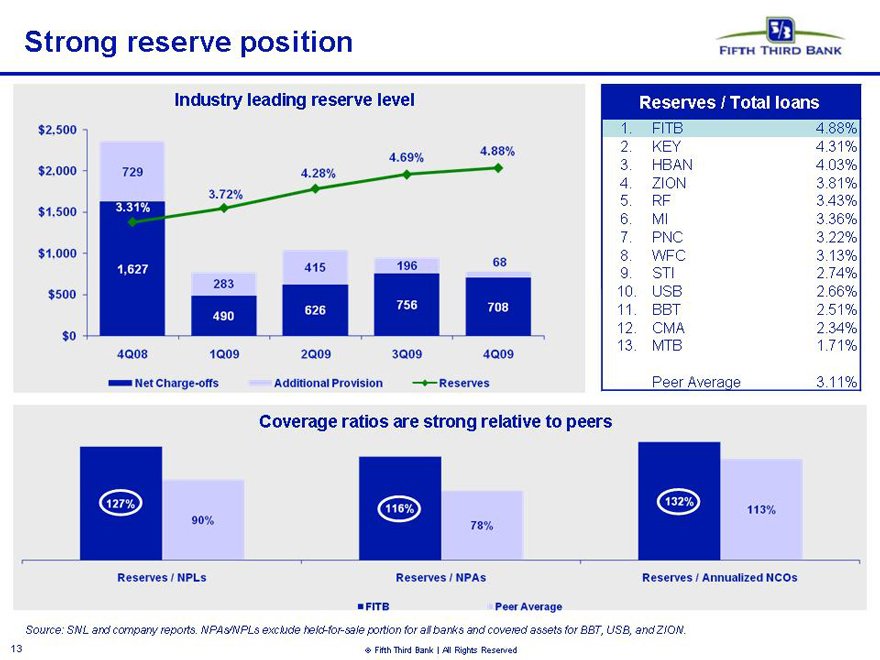

Strong reserve position

Industry leading reserve level

$2,500 $2,000 $1,500 $1,000 $500 $0

4Q08 1Q09 2Q09 3Q09 4Q09

Reserves / Total loans

1. FITB 4.88%

2. KEY 4.31%

3. HBAN 4.03%

4. ZION 3.81%

5. RF 3.43%

6. MI 3.36%

7. PNC 3.22%

8. WFC 3.13%

9. STI 2.74%

10. USB 2.66%

11. BBT 2.51%

12. CMA 2.34%

13. MTB 1.71%

Peer Average 3.11%

Coverage ratios are strong relative to peers

127% 90% 116% 78% 132% 113%

Reserves/NPLs Reserves/NPAs Reserves/Annualized NCOs

FITB Peer Average

Source: SNL and company reports. NPAs/NPLs exclude held-for-sale portion for all banks and covered assets for BBT, USB, and ZION.

©Fifth Third Bank | All Rights Reserved

13

14 © Fifth Third Bank | All Rights Reserved Updated stress testing - process overview Similar process to that used in 2008 and SCAP processes; updated for actual performance and current economic expectations Base and Stress case scenarios key economic assumptions (Moody’s Economy.com “Base” and “Longer Recession and Weaker Recovery Case”) Commercial — 33 geographic/industry sectors analyzed and regressed against economic and performance drivers — Migration trends from criticized to nonaccrual and charge-off evaluated by region and industry Consumer — Portfolios subdivided into appropriate categories (i.e. liquidating vs. non- liquidating home equity) — Results derived using combination of regression models, loss curves and roll rates, and applied economic factors – Mortgage and home equity key correlation: HPI – Credit card key correlation: unemployment – Other consumer key correlations: unemployment and GDP Economic Assumptions* 2010 2011 2010 2011 Peak Unemployment 10.4% 9.6% 11.5% 12.2% GDP 2.3% 4.7% 0.8% 4.7% Avg. change in quarterly HPI (1.8%) (0.2%) (2.7%) (1.8%) Base Adverse * Moody’s Economy.com; as of year-end 2009 |

15 © Fifth Third Bank | All Rights Reserved Updated credit loss expectations vs. SCAP scenarios Realized credit losses have been significantly below SCAP submissions, which is expected to continue * Red SCAP line represents more adverse scenario as adjusted by supervisors for additional assumed two-year losses. Supervisory estimates of total two-year losses under more adverse scenario were not allocated by period. Estimate allocates total two-year supervisory losses using the allocation under Fifth Third’s submission. ** Source for assumptions: Moody’s Economy.com. Assumptions as of year-end 2009. Fifth Third’s realized credit losses have been significantly below its SCAP submitted baseline and more adverse scenarios – In SCAP submissions, we incorporated significant conservatism, given then- prevailing negative economic and industry trends and extreme uncertainty in potential loss outcomes at the time – Economic and credit market conditions have been much better than potential downside expectations in Spring 2009, benefitting results vs. SCAP scenarios Base and stress scenarios reflect Moody’s Base Case and Moody’s Longer Recession and Weaker Recovery Case (as of December 2009)** Our current expectation is for 2010 losses to be lower than 2009 |

16 © Fifth Third Bank | All Rights Reserved Strong capital position Source: SNL and company reports. (TCE + reserves) / Loans Tangible common equity ratio Peer average: 6.2% Peer average: 12.0% Strong capital ratios relative to peers, particularly considering reserve levels Tier 1 common ratio Peer average: 7.1% Peer average w/ TARP: 11.2% Peer average w/o TARP: 8.9% Tier 1 capital ratio (with and without TARP) 8.6% 11.1% 10.5% 11.5% 11.5% 12.0% 12.5% 13.0% 12.8% 13.3% |

|

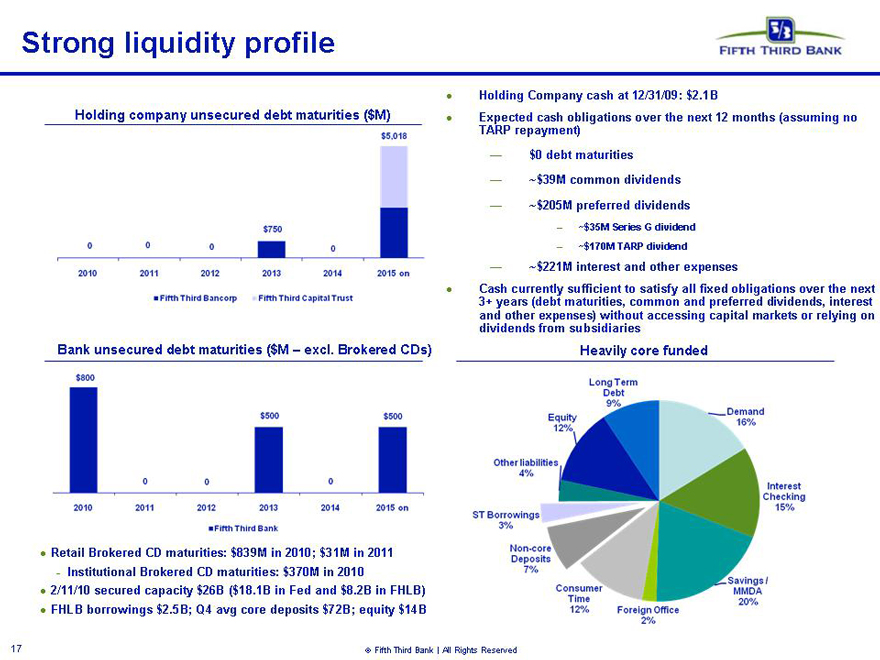

Strong liquidity profile

Holding company unsecured debt maturities ($M)

$5, 018

0 0 0 $750 0

2010 2011 2012 2013 2014 2015 on

Fifth Third Bancorp

Fifth Third Capital Trust

Bank unsecured debt maturities ($M – excl. Brokered CDs)

$800 $500 $500

0 0 0

2010 2011 2012 2013 2014 2015 on

Holding Company cash at 12/31/09: $2.1B Expected cash obligations over the next 12 months (assuming no TARP repayment)

— $0 debt maturities

— ~$39M common dividends

— ~$205M preferred dividends

– ~$35M Series G dividend

– ~$170M TARP dividend

— ~$221M interest and other expenses Cash currently sufficient to satisfy all fixed obligations over the next 3+ years (debt maturities, common and preferred dividends, interest and other expenses) without accessing capital markets or relying on dividends from subsidiaries

Heavily core funded

Long Term Debt 9%

Equity 12%

Demand 16%

Other liabilities 4%

Interest Checking 15%

ST Borrowings 3%

Non-core Deposits 7%

Consumer Time 12%

Foreign Office 2%

Savings / MMDA 20%

Retail Brokered CD maturities: $839M in 2010; $31M in 2011

Institutional Brokered CD maturities: $370M in 2010

2/11/10 secured capacity $26B ($18.1B in Fed and $8.2B in FHLB)

FHLB borrowings $2.5B; Q4 avg core deposits $72B; equity $14B

© Fifth Third Bank | All Rights Reserved

17

18 © Fifth Third Bank | All Rights Reserved Peer performance summary Continue to outperform on key value drivers FITB 4Q09 Large bank peers (1) 4Q09 Midwest peers (2) 4Q09 SEQ performance vs. peers Net interest margin / (bps) 3.55% (+12) 3.47% (+11) 3.19% (+16) Outperformed Operating fee growth^ 4% -1% 2% Outperformed Core pre-tax pre-provision earnings^ / loans 2.9% 2.7% 2.3% Outperformed Operating efficiency ratio^ 63% 65% 67% Outperformed Average core deposits growth* 3% 2% 2% Outperformed Average loan growth* -3% -3% -4% In line NPA ratio** / (bps) 4.21% (+12) 4.23% (+21) 4.07% (-5) In line Net charge-off ratio / (bps) 3.62% (-13) 2.94% (+19) 3.76% (+52) In line Large bank peer average consists of BBT, CMA, HBAN, KEY, MTB, MI, PNC, RF, STI, USB, WFC, and ZION, unless otherwise noted. Midwest peer average consists of CMA, HBAN, KEY, MI, and USB, unless otherwise noted. * Average loan and average core deposit growth excludes BBT and USB due to impact from acquisitions. Average loans include only loans held-for- investment. ^ Operating fee growth, core pre-tax pre-provision earnings, and operating efficiency ratio exclude the following items where appropriate: securities gains/losses, gains/losses from debt extinguishments, leveraged lease gains/losses, gains from asset sales, goodwill impairment charges, and other non- recurring items where appropriate. ** NPAs exclude loans held-for-sale and covered assets. Source: SNL and company reports. (1) (2) |

19 © Fifth Third Bank | All Rights Reserved 2010 developments Fifth Third response Macro themes • Sluggish loan demand • Deposits to grow but expect some diminution as later liquidity drawn down by deposits to support expansion in spending • Additional consumer regulation • Higher interest rates later in 2010 • TARP repayment • Leverage existing customer relationships at the local level to offer our full portfolio of products and services across all of our lines of business • Invest in sales force expansion initiatives to increase resources and branch hours while maintaining focus on a near-term return to profitability • Reorient fee structure of products and services to offer a clearer and higher value proposition to our clients and create more sustainable, consistent growth • Maintain excess liquidity, neutral to modest asset sensitive positioning • Remain committed to repayment in a manner that is in the best interest of all constituents, including shareholders © Fifth Third Bank | All Rights Reserved 19 |

20 © Fifth Third Bank | All Rights Reserved Summary Fifth Third continues to execute on its strategic initiatives and is focused on being well-positioned for the turn of the cycle. • Dedicated to serving the needs of families and businesses for more than 150 years • Businesses creating new and profitable opportunities to enhance value • Trends in NII and NIM favorably compare with peers • Ongoing expense control • Continued shift back toward core funding Core franchise remains strong • Strong reserve coverage of problem loans • Aggressive management has mitigated areas of highest risk • Significantly enhanced SAG and workout resources, while continuing prudent lending practices • Some positive signs in 2H09 results, though challenges will continue Aggressive management of credit issues • Successfully completed June 2008 capital plan and SCAP capital actions • Actions exceeded SCAP Tier 1 common equity commitment by 80% • Current capital levels able to withstand significant additional economic deterioration as demonstrated by the SCAP assessment Robust capital levels |

21 © Fifth Third Bank | All Rights Reserved Cautionary statement This report may contain statements that we believe are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Rule 175 promulgated thereunder, and Section 21E of the Securities Exchange Act of 1934, as amended, and Rule 3b-6 promulgated thereunder. These statements relate to our financial condition, results of operations, plans, objectives, future performance or business. They usually can be identified by the use of forward-looking language such as “will likely result,” “may,” “are expected to,” “is anticipated,” “estimate,” “forecast,” “projected,” “intends to,” or may include other similar words or phrases such as “believes,” “plans,” “trend,” “objective,” “continue,” “remain,” or similar expressions, or future or conditional verbs such as “will,” “would,” “should,” “could,” “might,” “can,” or similar verbs. You should not place undue reliance on these statements, as they are subject to risks and uncertainties, including but not limited to the risk factors set forth in our most recent Annual Report on Form 10-K and our most recent quarterly report on Form 10-Q. When considering these forward-looking statements, you should keep in mind these risks and uncertainties, as well as any cautionary statements we may make. Moreover, you should treat these statements as speaking only as of the date they are made and based only on information then actually known to us. There are a number of important factors that could cause future results to differ materially from historical performance and these forward- looking statements. Factors that might cause such a difference include, but are not limited to: (1) general economic conditions and weakening in the economy, specifically the real estate market, either nationally or in the states in which Fifth Third, one or more acquired entities and/or the combined company do business, are less favorable than expected; (2) deteriorating credit quality; (3) political developments, wars or other hostilities may disrupt or increase volatility in securities markets or other economic conditions; (4) changes in the interest rate environment reduce interest margins; (5) prepayment speeds, loan origination and sale volumes, charge-offs and loan loss provisions; (6) Fifth Third’s ability to maintain required capital levels and adequate sources of funding and liquidity; (7) maintaining capital requirements may limit Fifth Third’s operations and potential growth; (8) changes and trends in capital markets; (9) problems encountered by larger or similar financial institutions may adversely affect the banking industry and/or Fifth Third (10) competitive pressures among depository institutions increase significantly; (11) effects of critical accounting policies and judgments; (12) changes in accounting policies or procedures as may be required by the Financial Accounting Standards Board (FASB) or other regulatory agencies; (13) legislative or regulatory changes or actions, or significant litigation, adversely affect Fifth Third, one or more acquired entities and/or the combined company or the businesses in which Fifth Third, one or more acquired entities and/or the combined company are engaged; (14) ability to maintain favorable ratings from rating agencies; (15) fluctuation of Fifth Third’s stock price; (16) ability to attract and retain key personnel; (17) ability to receive dividends from its subsidiaries; (18) potentially dilutive effect of future acquisitions on current shareholders’ ownership of Fifth Third; (19) effects of accounting or financial results of one or more acquired entities; (20) difficulties in separating Fifth Third Processing Solutions from Fifth Third; (21) loss of income from any sale or potential sale of businesses that could have an adverse effect on Fifth Third’s earnings and future growth;(22) ability to secure confidential information through the use of computer systems and telecommunications networks; and (23) the impact of reputational risk created by these developments on such matters as business generation and retention, funding and liquidity. You should refer to our periodic and current reports filed with the Securities and Exchange Commission, or “SEC,” for further information on other factors, which could cause actual results to be significantly different from those expressed or implied by these forward-looking statements. |