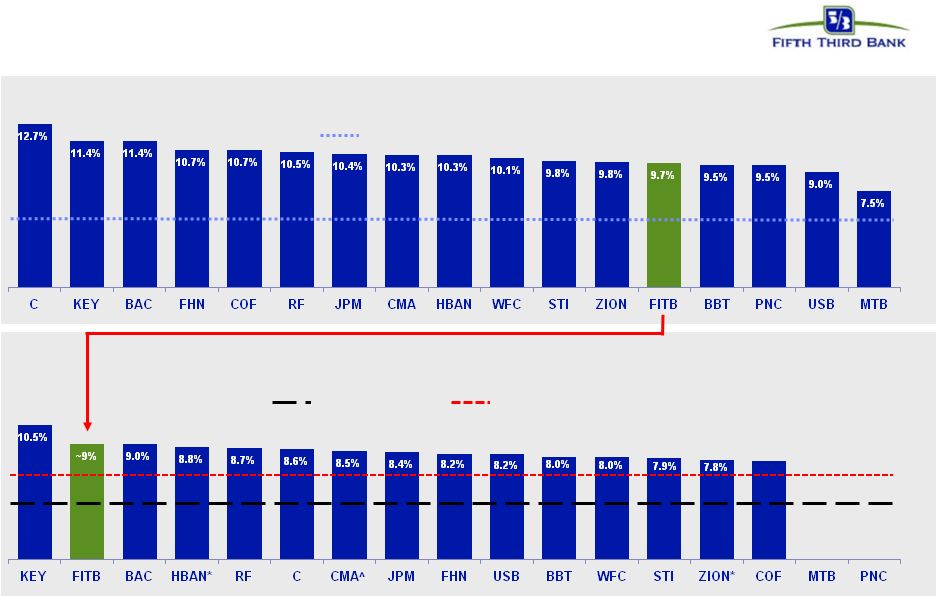

23 Fifth Third Bank | All Rights Reserved Regulation G Non-GAAP reconciliation Fifth Third Bancorp and Subsidiaries Regulation G Non-GAAP Reconcilation $ and shares in millions (unaudited) September June March December September 2012 2012 2012 2011 2011 Income before income taxes (U.S. GAAP) $503 $565 $603 $418 $530 Add: Provision expense (U.S. GAAP) 65 71 91 55 87 Pre-provision net revenue (a) 568 636 694 473 617 Net income available to common shareholders (U.S. GAAP) 354 376 421 305 373 Add: Intangible amortization, net of tax 2 2 3 3 3 Tangible net income available to common shareholders 356 378 424 308 376 Tangible net income available to common shareholders (annualized) (b) 1,416 1,520 1,705 1,222 1,492 Average Bancorp shareholders' equity (U.S. GAAP) 13,887 13,628 13,366 13,147 12,841 Less: Average preferred stock (398) (398) (398) (398) (398) Average goodwill (2,417) (2,417) (2,417) (2,417) (2,417) Average intangible assets (31) (34) (38) (42) (47) Average tangible common equity (c) 11,041 10,779 10,513 10,290 9,979 Total Bancorp shareholders' equity (U.S. GAAP) 13,718 13,773 13,560 13,201 13,029 Less: Preferred stock (398) (398) (398) (398) (398) Goodwill (2,417) (2,417) (2,417) (2,417) (2,417) Intangible assets (30) (33) (36) (40) (45) Tangible common equity, including unrealized gains / losses (d) 10,873 10,925 10,709 10,346 10,169 Less: Accumulated other comprehensive income / loss (468) (454) (468) (470) (542) Tangible common equity, excluding unrealized gains / losses (e) 10,405 10,471 10,241 9,876 9,627 Total assets (U.S. GAAP) 117,483 117,543 116,747 116,967 114,905 Less: Goodwill (2,417) (2,417) (2,417) (2,417) (2,417) Intangible assets (30) (33) (36) (40) (45) Tangible assets, including unrealized gains / losses (f) 115,036 115,093 114,294 114,510 112,443 Less: Accumulated other comprehensive income / loss, before tax (720) (698) (720) (723) (834) Tangible assets, excluding unrealized gains / losses (g) 114,316 114,395 113,574 113,787 111,609 Common shares outstanding (h) 897 919 920 920 920 Net charge-offs (i) 156 181 220 239 262 Ratios: Return on average tangible common equity (b) / (c) 12.8% 14.1% 16.2% 11.9% 15.0% Tangible common equity (excluding unrealized gains/losses) (e) / (g) 9.10% 9.15% 9.02% 8.68% 8.63% Tangible common equity (including unrealized gains/losses) (d) / (f) 9.45% 9.49% 9.37% 9.04% 9.04% Tangible book value per share (d) / (h) 12.12 11.89 11.64 11.25 11.05 Pre-provision net revenue / net charge-offs (a) / (i) 364% 351% 315% 198% 235% For the Three Months Ended |