Use these links to rapidly review the document

TABLE OF CONTENTS

United States Securities and Exchange Commission

Washington, DC 20549

FORM 10-K

| (Mark One) | |

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007 |

or |

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to |

Commission file number:0-10653

UNITED STATIONERS INC.

(Exact Name of Registrant as Specified in its Charter)

Delaware

(State or Other Jurisdiction of

Incorporation or Organization) | | 36-3141189

(I.R.S. Employer Identification No.) |

One Parkway North Boulevard

Suite 100

Deerfield, Illinois 60015-2559

(847) 627-7000

(Address, Including Zip Code and Telephone Number, Including Area Code, of Registrant's

Principal Executive Offices) |

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $0.10 par value per share

(Title of Class) | | Name of Exchange on which registered:

NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer ý | | Accelerated filer o | | Non-accelerated filer o | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes o No ý

The aggregate market value of the common stock of United Stationers Inc. held by non-affiliates as of June 30, 2007 was approximately $1.9 billion.

On February 26, 2008, United Stationers Inc. had 23,376,977 shares of common stock outstanding.

Documents Incorporated by Reference:

Certain portions of United Stationers Inc.'s definitive Proxy Statement relating to its 2008 Annual Meeting of Stockholders, to be filed within 120 days after the end of United Stationers Inc.'s fiscal year, are incorporated by reference into Part III.

UNITED STATIONERS INC.

FORM 10-K

For The Year Ended December 31, 2007

TABLE OF CONTENTS

PART I

ITEM 1. BUSINESS.

General

United Stationers Inc. is North America's largest broad line wholesale distributor of business products, with consolidated net sales of approximately $4.6 billion. United stocks a broad and deep line of over 100,000 products and offers thousands more in the following categories: technology products, traditional business products, office furniture, janitorial and breakroom supplies, and industrial supplies. The company's network of 70 distribution centers allows it to ship these items to approximately 30,000 reseller customers, reaching more than 90% of the U.S. and major cities in Mexico on an overnight basis.

Except where otherwise noted, the terms "United" and "the Company" refer to United Stationers Inc. and its consolidated subsidiaries. The parent holding company, United Stationers Inc. (USI), was incorporated in 1981 in Delaware. USI's only direct wholly owned subsidiary—and its principal operating company—is United Stationers Supply Co. (USSC), incorporated in 1922 in Illinois.

Products

United stocks over 100,000 stockkeeping units ("SKUs") in these categories:

Technology Products. The Company is a leading wholesale distributor of computer supplies and peripherals in North America. It stocks more than 11,000 items, including imaging supplies, data storage, digital cameras, computer accessories and computer hardware items such as printers and other peripherals. United provides these products to value-added computer resellers, office products dealers, drug stores, grocery chains and e-commerce merchants. Technology products generated over 37% of the Company's 2007 consolidated net sales.

Traditional Office Products. The Company is one of the largest national wholesale distributors of a broad range of office supplies. It carries approximately 22,000 brand-name and private label products, such as filing and record keeping products, business machines, presentation products, writing instruments, paper products, organizers, calendars and general office accessories. These products contributed almost 30% of net sales during the year.

Janitorial and Breakroom Supplies. United is a leading wholesaler of janitorial and breakroom supplies throughout the U.S. The Company holds over 7,000 items in these lines: janitorial and breakroom supplies, foodservice consumables (such as disposable tableware), safety and security items, and paper and packaging supplies. This product category provided nearly 20% of the latest year's net sales primarily from Lagasse, Inc. (Lagasse), a wholly owned subsidiary of USSC, and is the fastest growing category of the business.

Office Furniture. United is one of the largest office furniture wholesaler distributors in North America. It stocks over 5,000 products from more than 60 of the industry's leading manufacturers including, desks, filing and storage solutions, seating and systems furniture, along with a variety of products for niche markets such as education, government, healthcare and professional services. Innovative marketing programs and related services help drive this business across multiple customer channels. This product category represented approximately 12% of net sales for the year.

Industrial Supplies. With the acquisition of ORS Nasco Holding, Inc. (ORS Nasco) completed on December 21, 2007, the Company now stocks approximately 60,000 items including hand and power tools, safety and security supplies, janitorial equipment and supplies, other various industrial MRO (maintenance, repair and operations) items and oil field and welding supplies. This product category accounted for less than 1% of the Company's net sales in 2007 as the acquisition was not completed until late December. The Company offers many more items in these product lines within the industrial supplies category.

The remaining 1% of the Company's consolidated net sales came from freight and advertising revenue.

1

United offers private brand products within each of its product categories to help resellers provide quality value-priced items to their customers. These include Innovera™ technology products, Universal® office products, Windsoft® paper products, UniSan® janitorial and sanitation products, and Alera™ office furniture. ORS Nasco offers private label brand products in the welding, industrial, safety and oil field pipeline categories under its own brand offering, Anchor Brand™. During 2007, private brand products accounted for almost 13% of United's net sales.

Customers

United serves a diverse group of approximately 30,000 customers. They include independent office products dealers; contract stationers; office products superstores; computer products resellers; office furniture dealers; mass merchandisers; mail order companies; sanitary supply, paper and foodservice distributors; drug and grocery store chains; e-commerce merchants; oil field, welding supply and industrial/MRO distributors; and other independent distributors. No single customer accounted for more than 8% of 2007 consolidated net sales.

Independent resellers accounted for approximately 80% of consolidated net sales. The Company provides these customers with specialized services designed to help them market their products and services while improving operating efficiencies and reducing costs.

Marketing and Customer Support

United's customers can purchase most of the products the Company distributes at similar prices from many other sources. As a matter of fact, many reseller customers purchase their products from more than one source, frequently using "first call" and "second call" distributors. A "first call" distributor typically is a reseller's primary wholesaler and has the first opportunity to fill an order. If the "first call" distributor cannot meet the demand, or do so on a timely basis, the reseller will contact its "second call" distributor.

United's marketing and logistic capabilities differentiate the company from its competitors by providing an unmatched level of value-added services to resellers:

- •

- A broad line of products for one-stop shopping;

- •

- Comprehensive printed product catalogs for easy shopping and reference guides;

- •

- A new digital catalog and search capabilities to power e-commerce web sites;

- •

- Extensive promotional materials and marketing programs to increase sales;

- •

- High levels of products in stock, with an average line fill rate better than 97% in 2007;

- •

- Efficient order processing, resulting in a 99.5% order accuracy rate for the year;

- •

- High-quality customer service from several state-of-the-art customer care centers;

- •

- National distribution capabilities that enable same-day or overnight delivery to more than 90% of the U.S. and major cities in Mexico, providing a 99% on-time delivery rate in 2007;

- •

- Training programs designed to help resellers improve their operations;

- •

- End-consumer research to help resellers better understand their market.

United's marketing programs emphasize two other major strategies. First, the Company produces product content that is used to populate an extensive array of print and electronic catalogs for commercial dealers, contract stationers and retail dealers. The printed catalogs usually are customized with each reseller's name, then sold to the resellers who, in turn, distribute them to their customers. The Company markets its broad product offering primarily through a General Line catalog. This is available in both print and electronic versions, produced twice a year, and can include various selling prices (rather than the manufacturer's suggested retail price). In addition, the Company typically produces a number of promotional catalogs each quarter. United also develops separate quarterly flyers covering most of its product categories, including its private brand lines that offer a large selection of popular commodity

2

products. Since catalogs and electronic content provide product exposure to end consumers and generate demand, United tries to maximize their distribution on behalf of its suppliers and customers.

Second, United provides its resellers with a variety of dealer support and marketing services. These programs are designed to help resellers differentiate themselves by making it easier for customers to buy from them, and often allow resellers to reach customers they had not traditionally served.

Resellers can place orders with the Company through the Internet, by phone, fax and e-mail and through a variety of electronic order entry systems. Electronic order entry systems allow resellers to forward their customers' orders directly to United, resulting in the delivery of pre-sold products to the reseller. In 2007, United received approximately 85% of its orders electronically.

Distribution

The Company uses a network of 70 distribution centers to provide over 100,000 items to its approximately 30,000 reseller customers. This network, combined with the Company's depth and breadth of inventory in technology products, traditional office products, office furniture, janitorial and breakroom supplies, and industrial supplies, enables the Company to ship products on an overnight basis to more than 90% of the U.S. and major cities in Mexico. United's domestic operations generated $4.5 billion of its $4.6 billion in 2007 consolidated net sales, with its international operations contributing another $0.1 billion to 2007 net sales.

Regional distribution centers are supplemented with 27 local distribution points across the U.S., which serve as re-distribution points for orders filled at the regional centers. United has a dedicated fleet of approximately 600 trucks, most of which are under contract to the Company. This enables United to make direct deliveries to resellers from regional distribution centers and local distribution points.

United's inventory locator system allows it to provide resellers with timely delivery of the products they order. If a reseller asks for an item that is out of stock at the nearest distribution center, the system has the capability to automatically search for the product at other facilities within the shuttle network. When the item is found, the alternate location coordinates shipping with the primary facility. For most resellers, the result is a single on-time delivery of all items. This system gives United added inventory support while minimizing working capital requirements. As a result, the Company can provide higher service levels to its reseller customers, reduce back orders, and minimize time spent searching for substitute merchandise. These factors contribute to a high order fill rate and efficient levels of inventory. To meet its delivery commitments and to maintain high order fill rates, United carries a significant amount of inventory, which contributes to its overall working capital requirements.

The "Wrap and Label" program is another important service for resellers. It gives resellers the option to receive individually packaged orders ready to be delivered to their end consumers. For example, when a reseller places orders for several individual consumers, United can pick and pack the items separately, placing a label on each package with the consumer's name, ready for delivery to the end consumer by the reseller. Resellers appreciate the "Wrap and Label" program because it eliminates the need to break down bulk shipments and repackage orders before delivering them to consumers.

United also offers a drop ship service directly to the end consumer. Shipping labels reflect the reseller's name and complete consumer delivery address. This value added service provides same-day shipping to the end consumer with the reseller avoiding the cost of rehandling. The bulk of the 40,000 cartons shipped per day are handled by a large package delivery company and leading provider of specialized transportation and logistics services. United's proprietary order routing system ensures optimal order fill rate with a next- to second- day delivery commitment. United ships nearly 25% of its daily order volume directly to the end consumer.

In addition to providing value-adding programs for resellers, United also remains committed to reducing its operating costs. Its "War on Waste" (WOW2) program is meeting the goal of removing $100 million in costs over five years through a combination of new and continuing activities. These include the 2006 Workforce Reduction Program to lower the Company's cost structure. In addition, WOW2 includes

3

process improvement and work simplification activities that will help increase efficiency throughout the business and improve customer satisfaction.

Purchasing and Merchandising

As the largest broad line wholesale business products distributor in North America, United leverages its broad product selection as a key merchandising strategy. The Company orders products from over 1,000 manufacturers. This purchasing volume means United receives substantial supplier allowances and can realize significant economies of scale in its logistics and distribution activities. In 2007, United's largest supplier was Hewlett-Packard Company, which represented approximately 20% of its total purchases.

The Company's Merchandising Department is responsible for selecting merchandise and for managing the entire supplier relationship. Product selection is based on three factors: end-consumer acceptance; anticipated demand for the product; and the manufacturer's total service, price and product quality. As part of its effort to create an integrated supplier approach, United introduced the "Preferred Supplier Program" several years ago. In exchange for working closely with United to reduce overall supply chain costs, participating suppliers' products are treated as preferred brands in the Company's marketing efforts.

Competition

There is only one other nationwide broad line office products competitor in North America. United and this firm compete on the basis of breadth of product lines, availability of products, speed of delivery to resellers, order fill rates, net pricing to resellers, and the quality of marketing and other value-added services.

United competes with other national, regional and specialty wholesalers of office products, office furniture, technology products, janitorial and breakroom supplies and industrial supplies. Its competition also includes local and regional office products wholesalers and furniture, janitorial and breakroom supplies distributors, which typically offer more limited product lines. The Company also competes with other wholesale distributors in the industrial supplies market. In addition, United competes with various national distributors of computer consumables. In most cases, competition is based primarily upon net pricing, minimum order quantity, speed of delivery, and value-added marketing and logistics services.

The Company also competes with manufacturers who often sell their products directly to resellers and may offer lower prices. United believes that it provides an attractive alternative to manufacturer direct purchases by offering a combination of value-added services, including 1) Wrap and Label capabilities, 2) marketing and catalog programs, 3) same-day and next-day delivery, 4) a broad line of business products from multiple manufacturers on a "one-stop shop" basis, and 5) lower minimum order quantities.

Seasonality

United's sales generally are relatively steady throughout the year. However, sales also reflect seasonal buying patterns for consumers of office products. In particular, the Company's sales of office products usually are higher than average during January, when many businesses begin operating under new annual budgets and release previously deferred purchase orders. Janitorial and breakroom supplies sales are somewhat higher in the summer months.

Employees

As of February 26, 2008, United employed approximately 6,100 people.

Management believes it has good relations with its associates. Approximately 660 of the shipping, warehouse and maintenance associates at certain of the Company's Baltimore, Los Angeles and New Jersey facilities are covered by collective bargaining agreements. In 2006, United successfully renegotiated the bargaining agreement with associates in the Baltimore facility. The bargaining

4

agreement in the New Jersey facility is scheduled to expire in 2008. The bargaining agreement for the Los Angeles facility has expired and the union is working on a day-to-day contract. A new bargaining agreement is expected to be finalized in 2008 after union elections are complete. The Company has not experienced any work stoppages during the past five years.

Availability of the Company's Reports

The Company's principal Web site address iswww.unitedstationers.com. This site provides United's Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K—as well as amendments and exhibits to those reports filed or furnished under Section 13(a) or 15(d) of the Securities Exchange Act of 1934 (the "Exchange Act") for free as soon as reasonably practicable after they are electronically filed with, or furnished to, the Securities and Exchange Commission (SEC). In addition, copies of these filings (excluding exhibits) may be requested at no cost by contacting the Investor Relations Department:

United Stationers Inc.

Attn: Investor Relations Department

One Parkway North Boulevard

Suite 100

Deerfield, IL 60015-2559

Telephone: (847) 627-7000

E-mail:IR@ussco.com

ITEM 1A. RISK FACTORS.

Any of the risks described below could have a material adverse effect on the Company's business, financial condition or results of operations. These risks are not the only risks facing United; the Company's business operations could also be materially adversely affected by risks and uncertainties that are not presently known to United or that United currently deems immaterial.

United may not achieve its cost-reduction and margin enhancement goals.

United has set goals to improve its profitability over time by reducing expenses and growing sales to existing and new customers. There can be no assurance that United will achieve its enhanced profitability goals. Factors that could have a significant effect on the Company's efforts to achieve these goals include the following:

- •

- Inability to achieve the Company's annual "War on Waste" (WOW2) initiatives to reduce expenses and improve productivity and quality;

- •

- Impact on gross margin from competitive pricing pressures;

- •

- Failure to maintain or improve the Company's sales mix between lower margin and higher margin products;

- •

- Inability to pass along cost increases from United's suppliers to its customers;

- •

- Failure to increase sales of United's private brand products; and

- •

- Failure of customers to adopt the Company's product pricing and marketing programs.

The loss of a significant customer could significantly reduce United's revenues and profitability.

United's top five customers accounted for approximately 26% of the Company's 2007 net sales. The loss of one or more key customers, changes in the sales mix or sales volume to key customers or a significant downturn in the business or financial condition of any of them could significantly reduce United's sales and profitability.

United relies on independent dealers for a significant percentage of its net sales.

Sales to independent office product dealers accounted for a significant portion of United's 2007 net sales. Independent dealers compete with national retailers that have substantially greater financial

5

resources and technical and marketing capabilities. Over the years, several of the Company's independent dealer customers have been acquired by national retailers. If United's customer base of independent dealers declines, the Company's business and results of operations may be adversely affected.

United operates in a competitive environment.

The Company operates in a competitive environment. Competition is based largely upon service capabilities and price, as the Company's competitors are wholesalers that offer the same or similar products that the Company offers to the same customers or potential customers. United also faces competition from some of its own suppliers, which sell their products directly to United's customers. The Company's financial condition and results of operations depend on its ability to compete effectively on price, product selection and availability, marketing support, logistics and other ancillary services.

United's operating results depend on the strength of the general economy.

The customers that United serves are affected by changes in economic conditions outside the Company's control, including national, regional and local slowdowns in general economic activity and job markets. Demand for the products and services the Company offers, particularly in office products, is affected by the number of white collar and other workers employed by the businesses United's customers serve. An interruption of growth in these markets or a reduction of white collar and other jobs may adversely affect the Company's operating results. Any future general economic downturn, together with the negative effect this has on the number of white collar workers employed, may adversely affect United's business, financial condition and results of operations.

The loss of key suppliers or supply chain disruptions could decrease United's revenues and profitability.

United believes its ability to offer a combination of well-known brand name products as well as competitively priced private brand products is an important factor in attracting and retaining customers. The Company's ability to offer a wide range of products is dependent on obtaining adequate product supply from manufacturers or other suppliers. United's agreements with its suppliers are generally terminable by either party on limited notice. The loss of, or a substantial decrease in the availability of products from key suppliers at competitive prices could cause the Company's revenues and profitability to decrease. In addition, supply interruptions could arise due to transportation disruptions, labor disputes or other factors beyond United's control. Disruptions in United's supply chain could result in a decrease in revenues and profitability.

United's reliance on supplier allowances and promotional incentives could impact profitability.

Supplier allowances and promotional incentives which are often based on volume contribute significantly to United's profitability. If United does not comply with suppliers' terms and conditions, or does not make requisite purchases to achieve certain volume hurdles, United may not earn certain allowances and promotional incentives. In addition, if United's suppliers reduce or otherwise alter their allowances or promotional incentives, United's profit margin for the sale of the products it purchases from those suppliers may be harmed. The loss or diminution of supplier allowances and promotional support could have an adverse effect on the Company's results of operation.

United must manage inventory effectively in order to maximize supplier allowances while minimizing excess and obsolete inventory.

United's profitability depends heavily on supplier allowances, which United earns based on the volume of merchandise it purchases. To maximize supplier allowances and minimize excess and obsolete inventory, United must project end-consumer demand for over 100,000 SKUs in stock. If United underestimates demand for a particular manufacturer's products, the Company will lose sales, reduce customer satisfaction, and earn a lower level of allowances from that manufacturer. If United overestimates demand, it may have to liquidate excess or obsolete inventory at a loss.

6

United is focusing on increasing its sales of private brand products. These products can present unique inventory challenges. United sources many of its private brand products overseas, resulting in longer order-lead times than for comparable products sourced domestically. These longer lead-times make it more difficult to forecast demand accurately and will naturally require larger inventory investments to support high service levels. In addition, United generally does not have the right to return excess inventory of private brand products to the manufacturers.

The need to replace legacy systems with new information technology systems better equipped to support the Company's business could disrupt United's business and result in increased costs and decreased revenues.

The Company relies on information technology in all aspects of its business, including managing and replenishing inventory, filling and shipping customer orders and coordinating sales and marketing activities. Many of the Company's software applications are legacy systems, including order entry, order processing, pricing, billing, returns and credits, financial, and inventory receiving and control. The Company is building and implementing new applications to replace some of the legacy systems and to provide new services to customers. Interruptions in the proper functioning of the Company's information systems or delays in implementing new systems could disrupt United's business and result in increased costs and decreased revenue. A significant disruption or failure of the Company's existing information technology systems or in its development and implementation of new systems could put it at a competitive disadvantage and could adversely affect its results of operations.

United may not be successful in identifying, consummating and integrating future acquisitions.

Historically, part of United's growth and expansion into new product categories or markets has come from targeted acquisitions. Going forward, United may not be able to identify attractive acquisition candidates or complete the acquisition of any identified candidates at favorable prices and upon advantageous terms and conditions. Furthermore, competition for attractive acquisition candidates may limit the number of acquisition candidates or increase the overall costs of making acquisitions. Acquisitions involve significant risks and uncertainties, including difficulties integrating acquired business systems and personnel with United's business; the potential loss of key employees, customers or suppliers; the assumption of liabilities and exposure to unforeseen liabilities of acquired companies; the difficulties in achieving target synergies; and the diversion of management attention and resources from existing operations. Difficulties in identifying, completing or integrating acquisitions could impede United's revenues and profitability.

The Company relies heavily on its key executives and the loss of one or more of these individuals could harm the Company's ability to carry out its business strategy.

United's ability to implement its business strategy depends largely on the efforts, skills, abilities and judgment of the Company's executive management team. United's success also depends to a significant degree on its ability to recruit and retain sales and marketing, operations and other senior managers. The Company may not be successful in attracting and retaining these employees, which may in turn have an adverse effect on the Company's results of operations and financial condition.

United's financial condition and results of operation depend on the availability of financing sources to meet its business needs.

The Company depends on various external financing sources to fund its operating, investing, and financing activities. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—General" included below under Item 7. One of the Company's external financing sources is a receivables securitization program that is dependent on a back-up liquidity facility which must be renewed annually. The Company's other primary external financing sources terminate or mature in four to six years. If the Company is unable to obtain or renew its financing sources on commercially reasonable terms, its business and financial condition could be materially adversely affected.

7

Unexpected events could disrupt normal business operations, which might result in increased costs and decreased revenues.

Unexpected events, such as hurricanes, fire, war, terrorism, and other natural or man-made disruptions, may increase the cost of doing business or otherwise impact United's financial performance. In addition, damage to or loss of use of significant aspects of the Company's infrastructure due to such events could have an adverse affect on the Company's operating results and financial condition.

ITEM 1B. UNRESOLVED COMMENT LETTERS.

None.

ITEM 2. PROPERTIES.

The Company considers its properties to be suitable with adequate capacity for their intended uses. The Company evaluates its properties on an ongoing basis to improve efficiency and customer service and leverage potential economies of scale. Substantially all owned facilities are subject to liens under USSC's debt agreements (see the information under the caption "Liquidity and Capital Resources" included below under Item 7). As of December 31, 2007, these properties consisted of the following:

Offices. The Company owns approximately 49,000 square feet of office space in Orchard Park, New York and a 136,000 square foot facility in Des Plaines, Illinois. The Des Plaines, Illinois location previously housed the Company's corporate headquarters. During 2006, the Company relocated its corporate headquarters from Des Plaines, Illinois to Deerfield, Illinois. As a result, the Company entered into an 11-year commercial lease for approximately 205,000 square feet of office space. In addition, the Company leases approximately 22,000 square feet of office space in Harahan, Louisiana. On March 9, 2007, the Company entered into a contract to sell its former corporate headquarters in Des Plaines, Illinois. The contract expires on March 5, 2008. The Buyer has informed the Company that it has not been able to secure financing to close the deal and has requested a contract extension of at least nine months.

Distribution Centers. The Company utilizes 70 distribution centers totaling approximately 12.6 million square feet of warehouse space. Of the 12.6 million square feet of distribution center space, 2.4 million square feet is owned and 10.2 million square feet is leased. The Company expects to open a new facility in Orlando, Florida during the second quarter of 2008. This new facility will help improve overall customer service and maximize efficiencies.

ITEM 3. LEGAL PROCEEDINGS.

The Company is involved in legal proceedings arising in the ordinary course of or incidental to its business. The Company is not involved in any legal proceedings that it believes will result, individually or in the aggregate, in a material adverse effect upon its financial condition or results of operations.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS.

No matters were submitted to a vote of security holders during the fourth quarter of 2007.

8

EXECUTIVE OFFICERS OF THE REGISTRANT (as of February 20, 2008)

The executive officers of the Company are as follows:

Name, Age and

Position with the Company

| | Business Experience

|

|---|

Richard W. Gochnauer

58, President and Chief Executive Officer | | Richard W. Gochnauer became the Company's President and Chief Executive Officer in December 2002, after joining the Company as its Chief Operating Officer and as a Director in July 2002. From 1994 until he joined the Company, Mr. Gochnauer held the positions of Vice Chairman and President, International, and President and Chief Operating Officer of Golden State Foods, a privately-held food company that manufactures and distributes food and paper products. |

S. David Bent

47, Senior Vice President and

Chief Information Officer |

|

S. David Bent joined the Company as its Senior Vice President and Chief Information Officer in May 2003. From August 2000 until such time, Mr. Bent served as the Corporate Vice President and Chief Information Officer of Acterna Corporation, a multi-national telecommunications test equipment and services company, and also served as General Manager of its Software Division from October 2002. Previously, he spent 18 years with the Ford Motor Company. During his Ford tenure, Mr. Bent most recently served during 1999 and 2000 as the Chief Information Officer of Visteon Automotive Systems, a tier one automotive supplier, and from 1998 through 1999 as its Director, Enterprise Processes and Systems. |

Ronald C. Berg

48, Senior Vice President, Inventory Management |

|

Ronald C. Berg has been the Company's Senior Vice President, Inventory Management, since May 2006. From May 2005 to May 2006 he served as Senior Vice President, Business Transformation. He previously served as Senior Vice President, Inventory Management and Facility Support from October, 2001 until May 2005. He also served as the Company's Vice President, Inventory Management, since 1997, and as a Director, Inventory Management, since 1994. He began his career with the Company in 1987 as an Inventory Rebuyer, and spent several years thereafter in various product and furniture or general inventory management positions. Prior to joining the Company, Mr. Berg managed Solar Cine Products, Inc., a family-owned, photographic equipment business. |

Eric A. Blanchard

51, Senior Vice President, General Counsel and Secretary |

|

Eric A. Blanchard has served as the Company's Senior Vice President, General Counsel and Secretary since January 2006. From November 2002 until December 2005 he served as the Vice President, General Counsel and Secretary at Tennant Company. Previously Mr. Blanchard was with Dean Foods Company where he held the positions of Chief Operating Officer, Dairy Division from January 2002 to October 2002, Vice President and President, Dairy Division from 1999 to 2002 and General Counsel and Secretary from 1988 to 1999. |

9

Patrick T. Collins

47, Senior Vice President, Sales |

|

Patrick T. Collins joined the Company in October 2004 as Senior Vice President, Sales. Prior to joining the Company, Mr. Collins was employed by Ingram Micro, a global technology distribution company, from January 2000 through August 2004, in various senior sales and marketing roles, serving most recently as its Senior Group Vice President of Sales and Marketing. In that capacity, Mr. Collins had operating responsibility for sales, marketing, purchasing and supplier relations for Ingram Micro's North American division. Prior to joining Ingram Micro in early 2000, Mr. Collins was with the Frito-Lay division of PepsiCo, Inc., a global food and beverage consumer products company, for nearly 15 years, where he held various accounting, planning, sales and general management positions. |

Timothy P. Connolly

44, Senior Vice President, Operations |

|

Timothy P. Connolly has served as Senior Vice President, Operations since December 2006. From February 2006 to such time, Mr. Connolly was Vice President, Field Operations Support and Facility Engineering at the Field Support Center. He joined the Company in August 2003 as Region Vice President Operations, Midwest. Before joining the Company, Mr. Connolly was the Regional Vice President, Midwest Region for Cardinal Health where he directed operations, sales, human resources, finance and customer service for one of Cardinal's largest pharmaceutical distribution centers. |

James K. Fahey

57, Senior Vice President, Merchandising |

|

James K. Fahey is the Company's Senior Vice President, Merchandising, with responsibility for category management and merchandising, global sourcing, and supplier revenue management. From September 1992 until he assumed that position in October 1998, Mr. Fahey served as Vice President, Merchandising of the Company. Prior to that time, he served as the Company's Director of Merchandising. Before he joined the Company in 1991, Mr. Fahey had an extensive career in both retail and consumer direct-response marketing. |

Mark J. Hampton

54, Senior Vice President, Marketing |

|

Mark J. Hampton is the Company's Senior Vice President, Marketing, with responsibility for marketing, pricing and advertising activities. He previously served as Senior Vice President, Marketing and Field Support Services, from late 2001 until early 2003, Senior Vice President, Marketing, and President and Chief Operating Officer of The Order People Company, during 2001 and Senior Vice President, Marketing, from October 2000. Mr. Hampton began his career with the Company in 1980 and left the Company to work in the office products dealer community in 1991. Upon his return to the Company in 1992, he served as Midwest Regional Vice President, Vice President and General Manager of the Company's MicroUnited division and, from 1994, Vice President, Marketing. Mr. Hampton will be leaving the Company at the end of February, 2008. |

10

Jeffrey G. Howard

52, Senior Vice President, National Accounts and Channel Management |

|

Jeffrey G. Howard has served as the Company's Senior Vice President, National Accounts and Channel Management, since October 2004. From early 2003 until such time, he was Senior Vice President, National Accounts and New Business Development. Mr. Howard previously held the positions of Senior Vice President, Sales and Customer Support Services from October 2001, Senior Vice President, National Accounts, from late 2000 and Vice President, National Accounts, from 1994. He joined the Company in 1990 as General Manager of its Los Angeles distribution center, and was promoted to Western Region Vice President in 1992. Mr. Howard began his career in the office products industry in 1973 with Boorum & Pease Company, which was acquired by Esselte Pendaflex in 1985. |

Robert J. Kelderhouse

52, Vice President, Treasurer |

|

Robert J. Kelderhouse is expected to be elected and approved as Vice President, Treasurer of the Company at the Board of Directors meeting on March 4, 2008. Mr. Kelderhouse joined the company as a full time employee in February, 2008 and has served in a consulting capacity since November, 2007. Prior to joining the Company, Mr. Kelderhouse spent six years with R.R. Donnelley & Sons Company and one of its acquired companies, Wallace Computer Services, Inc. He served as Senior Vice President and Treasurer of R.R. Donnelley from February, 2004 through March, 2006 and as Vice President and Treasurer of Wallace Computer Services, Inc. from May, 1999 through May, 2003. Prior to joining Wallace, Mr. Kelderhouse held numerous financial and treasury management positions throughout a sixteen year career at Heller International Corporation, a global commercial finance company. His last position at Heller was as Senior Vice President, Finance and Capital Markets for the Sales Finance Group. |

Kenneth M. Nickel

40, Vice President, Controller and Chief Accounting Officer |

|

Kenneth M. Nickel has been the Company's Vice President, Controller and Chief Accounting Officer since February 2007. Prior to that, Mr. Nickel served as the Company's Vice President and Controller from November 2002 to February 2007, as its Vice President and Field Support Center Controller from November 2001 to October 2002 and as its Vice President and Assistant Controller from April 2001 to October 2001. Mr. Nickel has been with the Company since November 1989 and has held progressively more responsible accounting positions within the Company's Finance department. |

11

P. Cody Phipps

46, President, United Stationers Supply |

|

P. Cody Phipps has served as the Company's President, United Stationers Supply since October 2006. He joined the Company in August 2003 as its Senior Vice President, Operations. Prior to joining the Company, Mr. Phipps was a partner at McKinsey & Company, Inc., a global management consulting firm. During his tenure at McKinsey from and after 1990, he became a leader in the firm's North American Operations Effectiveness Practice and co-founded and led its Service Strategy and Operations Initiative, which focused on driving significant operational improvements in complex service and logistics environments. Prior to joining McKinsey, Mr. Phipps worked as a consultant with The Information Consulting Group, a systems consulting firm, and as an IBM account marketing representative. |

Victoria J. Reich

50, Senior Vice President and Chief Financial Officer |

|

Victoria J. Reich joined the Company in June 2007 as its Senior Vice President and Chief Financial Officer. Prior to joining the Company, Ms. Reich spent ten years with Brunswick Corporation where she most recently was President of Brunswick European Group from August 2003 until June 2006. She served as Brunswick's Senior Vice President and Chief Financial Officer from 2000 to 2003 and as Vice President and Controller from 1996 until 2000. Before joining Brunswick, Ms. Reich spent 17 years at General Electric Company where she held various financial management positions. |

William K. Scheller

54, Senior Vice President and President, ORS Nasco, Inc. |

|

William K. Scheller joined the Company in December 2007 as its Senior Vice President and President of ORS Nasco, Inc., a wholly owned subsidiary of USSC. USSC completed the acquisition of ORS Nasco in December 2007. Mr. Scheller joined ORS Nasco as President and CEO in September 1998. Mr. Scheller previously served as Director of Distribution / Logistics for Patterson Dental Company (PDCO) for eight years, where his responsibilities included warehouse operations, transportation, inventory control, supplier negotiations and procurement. Before PDCO, he held numerous positions throughout his 12 years at Pillsbury Company. |

Stephen A. Schultz

41, Senior Vice President and President, Lagasse, Inc. |

|

Stephen A. Schultz is the President of Lagasse, Inc., a wholly owned subsidiary of USSC, a position he has held since August 2001. In October 2003, he assumed the additional position of Senior Vice President, Category Management-Janitorial/Sanitation, of the Company. Mr. Schultz joined Lagasse in early 1999 as Vice President, Marketing and Business Development, and became a Senior Vice President of Lagasse in late 2000. Before joining Lagasse, he served for nearly 10 years in various executive sales and marketing roles for Hospital Specialty Company, a manufacturer and distributor of hygiene products for the institutional janitorial and sanitation industry. |

Executive officers are elected by the Board of Directors. Except as required by individual employment agreements between executive officers and the Company, there exists no arrangement or understanding between any executive officer and any other person pursuant to which such executive officer was elected. Each executive officer serves until his or her successor is appointed and qualified or until his or her earlier removal or resignation.

12

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Common Stock Information

USI's common stock is quoted through the NASDAQ Global Select Market ("NASDAQ") under the symbol USTR. The following table shows the high and low closing sale prices per share for USI's common stock as reported by NASDAQ:

| | High

| | Low

|

|---|

| 2007 | | | | | | |

| First Quarter | | $ | 60.21 | | $ | 46.15 |

| Second Quarter | | | 68.20 | | | 59.52 |

| Third Quarter | | | 70.82 | | | 52.36 |

| Fourth Quarter | | | 60.47 | | | 45.79 |

2006 |

|

|

|

|

|

|

| First Quarter | | $ | 53.10 | | $ | 48.22 |

| Second Quarter | | | 56.01 | | | 44.77 |

| Third Quarter | | | 51.00 | | | 44.95 |

| Fourth Quarter | | | 49.07 | | | 45.58 |

On February 26, 2008, the closing sale price of Company's common stock as reported by NASDAQ was $52.91 per share. On February 26, 2008, there were approximately 806 holders of record of common stock. A greater number of holders of USI common stock are "street name" or beneficial holders, whose shares are held of record by banks, brokers and other financial institutions.

13

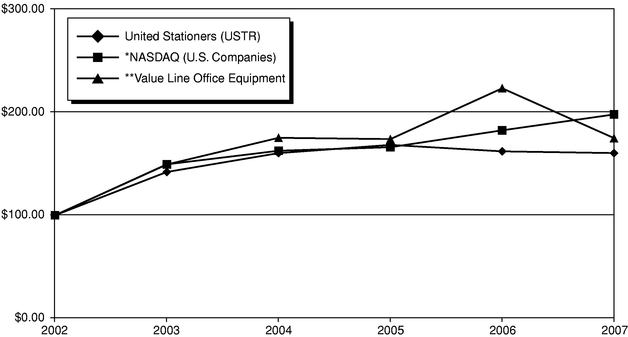

Stock Performance Graph

The following graph compares the performance of the Company's common stock over a five-year period with the cumulative total returns of (1) The NASDAQ Stock Market Index (U.S. companies), and (2) a group of companies included within Value Line's Office Equipment Industry Index. The graph assumes $100 was invested on December 31, 2002 in the Company's common stock and in each of the indices and assumes reinvestment of all dividends (if any) at the date of payment. The following stock price performance graph is presented pursuant to SEC rules and is not meant to be an indication of future performance.

| | 2002

| | 2003

| | 2004

| | 2005

| | 2006

| | 2007

|

|---|

| United Stationers (USTR) | | $ | 100.00 | | $ | 142.08 | | $ | 160.42 | | $ | 168.40 | | $ | 162.12 | | $ | 160.45 |

| *NASDAQ (U.S. Companies) | | $ | 100.00 | | $ | 149.52 | | $ | 162.72 | | $ | 166.17 | | $ | 182.58 | | $ | 197.99 |

| **Value Line Office Equipment | | $ | 100.00 | | $ | 149.32 | | $ | 175.29 | | $ | 174.03 | | $ | 223.44 | | $ | 175.02 |

Common Stock Repurchases

As of December 31, 2007, the Company had $68.4 million under share repurchase authorizations from its Board of Directors. During 2007, the Company repurchased 6,561,416 shares of common stock at an aggregate cost of $383.3 million.

Purchases may be made from time to time in the open market or in privately negotiated transactions. Depending on market and business conditions and other factors, the Company may continue or suspend purchasing its common stock at any time without notice.

Acquired shares are included in the issued shares of the Company and treasury stock, but are not included in average shares outstanding when calculating earnings per share data.

14

The following table summarizes purchases of the Company's common stock during the fourth quarter of 2007:

Period

| | Total

Number of

Shares

Purchased

| | Average

Price

Paid Per

Share

| | Total

Number of

Shares

Purchased

as Part of

Publicly

Announced

Plans or

Programs(1)

| | Approximate

Dollar Value

of Shares that

May Yet Be

Purchased

Under the

Plans or

Programs

|

|---|

| 10/1/2007—10/31/2007 | | 740,893 | | $ | 56.74 | | 740,893 | | $ | 107,973,448 |

| 11/1/2007—11/30/2007 | | 680,493 | | | 57.92 | | 680,493 | | | 68,562,236 |

| 12/1/2007—12/31/2007 | | 4,060 | | | 48.96 | | 4,060 | | | 68,363,454 |

| | |

| | | | |

| | | |

| | Total | | 1,425,446 | | $ | 57.28 | | 1,425,446 | | | |

- (1)

- All share purchases were executed under share repurchase authorizations given by the Company's Board of Directors and made under a 10b-5 plan.

Dividends

The Company's policy has been to reinvest earnings to enhance its financial flexibility and to fund future growth. Accordingly, USI has not paid cash dividends and has no plans to declare cash dividends on its common stock at this time. Furthermore, as a holding company, USI's ability to pay cash dividends in the future depends upon the receipt of dividends or other payments from its operating subsidiary, USSC. The Company's debt agreements impose limited restrictions on the payment of dividends. For further information on the Company's debt agreements, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources" in Item 7, and Note 9 to the Consolidated Financial Statements included in Item 8 of this Annual Report.

Securities Authorized for Issuance under Equity Compensation Plans

The information required by Item 201(d) of Regulation S-K (Securities Authorized for Issuance under Equity Compensation Plans) is included in Item 12 of this Annual Report.

ITEM 6. SELECTED FINANCIAL DATA.

The selected consolidated financial data of the Company for the years ended December 31, 2003 through 2007 have been derived from the Consolidated Financial Statements of the Company, which have been audited by Ernst & Young LLP, an independent registered public accounting firm. See Note 1 to the Consolidated Financial Statements. The adoption of new accounting pronouncements, changes in certain accounting policies, reclassifications of discontinued operations and certain other reclassifications are reflected in the financial information presented below. The selected consolidated financial data below should be read in conjunction with, and is qualified in its entirety by, Management's Discussion and Analysis of Financial Condition and Results of Operations and the Consolidated

15

Financial Statements of the Company included in Items 7 and 8, respectively, of this Annual Report. Except for per share data, all amounts presented are in thousands:

| | Years Ended December 31,(9)

| |

|---|

| | 2007

| | 2006(1)

| | 2005

| | 2004(2)

| | 2003

| |

|---|

| Income Statement Data: | | | | | | | | | | | | | | | | |

| Net sales | | $ | 4,646,399 | | $ | 4,546,914 | | $ | 4,279,089 | | $ | 3,838,701 | | $ | 3,652,413 | |

| Cost of goods sold | | | 3,939,684 | | | 3,792,833 | | | 3,637,065 | | | 3,254,169 | | | 3,105,635 | |

| | |

| |

| |

| |

| |

| |

| | Gross profit | | | 706,715 | | | 754,081 | | | 642,024 | | | 584,532 | | | 546,778 | |

| Operating expenses: | | | | | | | | | | | | | | | | |

| | Warehousing, marketing and administrative expenses | | | 502,810 | | | 516,234 | | | 471,193 | | | 422,595 | | | 406,446 | |

| | Restructuring and other charges (reversal), net(3) | | | 1,378 | | | 1,941 | | | (1,331 | ) | | — | | | — | |

| | |

| |

| |

| |

| |

| |

| Total operating expenses | | | 504,188 | | | 518,175 | | | 469,862 | | | 422,595 | | | 406,446 | |

| | |

| |

| |

| |

| |

| |

| Operating Income | | | 202,527 | | | 235,906 | | | 172,162 | | | 161,937 | | | 140,332 | |

| Interest expense | | | (13,109 | ) | | (8,276 | ) | | (3,050 | ) | | (3,324 | ) | | (6,816 | ) |

| Interest income | | | 1,197 | | | 970 | | | 342 | | | 362 | | | 262 | |

| Loss on early retirement of debt(4) | | | — | | | — | | | — | | | — | | | (6,693 | ) |

| Other expense, net(5) | | | (14,595 | ) | | (12,786 | ) | | (7,035 | ) | | (3,488 | ) | | (4,826 | ) |

| | |

| |

| |

| |

| |

| |

| Income from continuing operations before income taxes and cumulative effect of a change in accounting principle | | | 176,020 | | | 215,814 | | | 162,419 | | | 155,487 | | | 122,259 | |

| Income tax expense | | | 68,825 | | | 80,510 | | | 60,949 | | | 57,523 | | | 46,480 | |

| | |

| |

| |

| |

| |

| |

| Income from continuing operations before cumulative effect of a change in accounting principle | | | 107,195 | | | 135,304 | | | 101,470 | | | 97,964 | | | 75,779 | |

| (Loss) income from discontinued operations, net of tax | | | — | | | (3,091 | ) | | (3,969 | ) | | (7,993 | ) | | 3,331 | |

| | |

| |

| |

| |

| |

| |

| Income before cumulative effect of a change in accounting principle | | | 107,195 | | | 132,213 | | | 97,501 | | | 89,971 | | | 79,110 | |

| Cumulative effect of a change in accounting principle(6) | | | — | | | — | | | — | | | — | | | (6,108 | ) |

| | |

| |

| |

| |

| |

| |

| Net income | | $ | 107,195 | | $ | 132,213 | | $ | 97,501 | | $ | 89,971 | | $ | 73,002 | |

| | |

| |

| |

| |

| |

| |

| Net income per share—basic: | | | | | | | | | | | | | | | | |

| | Income from continuing operations before cumulative effect of a change in accounting principle | | $ | 3.92 | | $ | 4.37 | | $ | 3.08 | | $ | 2.93 | | $ | 2.29 | |

| | (Loss) income from discontinued operations, net of tax | | | — | | | (0.10 | ) | | (0.12 | ) | | (0.24 | ) | | 0.10 | |

| | Cumulative effect of a change in accounting principle | | | — | | | — | | | — | | | — | | | (0.19 | ) |

| | |

| |

| |

| |

| |

| |

| | Net income per common share—basic | | $ | 3.92 | | $ | 4.27 | | $ | 2.96 | | $ | 2.69 | | $ | 2.20 | |

| | |

| |

| |

| |

| |

| |

| Net income per share—diluted: | | | | | | | | | | | | | | | | |

| | Income from continuing operations before cumulative effect of a change in accounting principle | | $ | 3.83 | | $ | 4.31 | | $ | 3.02 | | $ | 2.88 | | $ | 2.27 | |

| | (Loss) income from discontinued operations, net of tax | | | — | | | (0.10 | ) | | (0.12 | ) | | (0.23 | ) | | 0.10 | |

| | Cumulative effect of a change in accounting principle | | | — | | | — | | | — | | | — | | | (0.19 | ) |

| | |

| |

| |

| |

| |

| |

| | Net income per common share—diluted | | $ | 3.83 | | $ | 4.21 | | $ | 2.90 | | $ | 2.65 | | $ | 2.18 | |

| | |

| |

| |

| |

| |

| |

| Cash dividends declared per share | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | |

Balance Sheet Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Working capital(7) | | $ | 543,258 | | $ | 551,556 | | $ | 421,005 | | $ | 545,552 | | $ | 498,523 | |

| Total assets(7) | | | 1,765,555 | | | 1,560,355 | | | 1,550,545 | | | 1,419,756 | | | 1,305,357 | |

| Total debt(8) | | | 451,000 | | | 117,300 | | | 21,000 | | | 18,000 | | | 17,324 | |

| Total stockholders' equity | | | 574,254 | | | 800,940 | | | 768,512 | | | 737,071 | | | 677,460 | |

Statement of Cash Flows Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net cash provided by operating activities | | $ | 218,054 | | $ | 13,994 | | $ | 236,067 | | $ | 50,701 | | $ | 171,015 | |

| Net cash used in investing activities | | | (197,898 | ) | | (18,624 | ) | | (171,748 | ) | | (13,378 | ) | | (14,279 | ) |

| Net cash (used in) provided by financing activities | | | (13,188 | ) | | 2,198 | | | (62,680 | ) | | (32,032 | ) | | (164,416 | ) |

Other Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Pro forma amounts assuming the accounting change for EITF Issue No. 02-16:(6) | | | | | | | | | | | | | | | | |

| Net income | | $ | 107,195 | | $ | 132,213 | | $ | 97,501 | | $ | 89,971 | | $ | 79,110 | |

| Earnings per share: | | | | | | | | | | | | | | | | |

| | Basic | | $ | 3.92 | | $ | 4.27 | | $ | 2.96 | | $ | 2.69 | | $ | 2.39 | |

| | Diluted | | $ | 3.83 | | $ | 4.21 | | $ | 2.90 | | $ | 2.65 | | $ | 2.37 | |

- (1)

- In 2006, the Company recorded $60.6 million, or $1.21 per diluted share in non-recurring favorable benefits from the Company's product content syndication program and certain marketing program changes.

16

- (2)

- During 2004, the Company recorded a pre-tax write-off of approximately $13.2 million in supplier allowances, customer rebates and trade receivables, inventory and other items associated with the Company's Canadian Division.

- (3)

- Reflects restructuring and other charges in the following years:2007—$1.4 million charge for the 2006 Workforce Reduction Program. 2006—$6.0 million charge for the 2006 Workforce Reduction Program, partially offset by a $4.1 million reversal of previously established restructuring reserves.2005—$1.3 million reversal of previously established restructuring reserves. See Note 5 to the Consolidated Financial Statements included in Item 8 of this Annual Report.

- (4)

- During 2003, the Company redeemed its 8.375% Senior Subordinated Notes and replaced its then existing credit agreement with a new Five-Year Revolving Credit Agreement. As a result, the Company recorded a loss on early retirement of debt totaling $6.7 million, of which $5.9 million was associated with the redemption of the 8.375% Senior Subordinated Notes and $0.8 million related to the write-off of deferred financing costs associated with replacing the prior credit agreement.

- (5)

- Primarily represents the loss on the sale of certain trade accounts receivable through the Company's Receivables Securitization Program. For further information on the Company's Receivables Securitization Program, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Off-Balance Sheet Arrangements—Receivables Securitization Program" under Item 7 of this Annual Report.

- (6)

- Effective January 1, 2003, the Company adopted EITF Issue No. 02-16. As a result, during the first quarter of 2003 the Company recorded a non-cash, cumulative after-tax charge of $6.1 million, or $0.19 per diluted share, related to the capitalization into inventory of a portion of fixed promotional allowances received from vendors for participation in the Company's advertising publications.

- (7)

- In accordance with Generally Accepted Accounting Principles ("GAAP"), total assets exclude $248.0 million in 2007, $225.0 million in 2006 and 2005, $118.5 million in 2004 and $150.0 million in 2003 of certain trade accounts receivable sold through the Company's Receivables Securitization Program. For further information on the Company's Receivables Securitization Program, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Off-Balance Sheet Arrangements—Receivables Securitization Program" under Item 7 of this Annual Report.

- (8)

- Total debt includes current maturities.

- (9)

- Certain prior period amounts have been reclassified to conform to the current presentation. Such reclassifications were limited to Balance Sheet and Cash Flow Statement presentation and did not impact the Statements of Income. Specifically, the Company reclassified capitalized software costs from "Other Assets" to "Property, Plant and Equipment" beginning in the first quarter of 2006, with prior periods updated to conform to this presentation. For the years ended December 31, 2005, 2004 and 2003, $17.0 million, $3.7 million and $3.3 million, respectively, in operating cash outflows were reclassified as cash outflows from investing activities. The reclassification of capitalized software also resulted in a reclassification from "Other Assets" to "Property, Plant and Equipment" for 2005 of $17.0 million. Additionally, the Company reclassified certain offsets to "Accrued Liabilities" related to merchandise return reserves to "Inventory". This reclassification began in the fourth quarter of 2007, with prior periods updated to conform to this presentation. For the years ended December 31, 2006, 2005, 2004 and 2003, $7.0 million, $8.3 million, $6.6 million and $5.9 million, respectively, were reclassified to "Inventory" out of "Accrued Liabilities" with corresponding changes made to the Statement of Cash Flows within "Cash Flows From Operating Activities".

FORWARD LOOKING INFORMATION

This Annual Report on Form 10-K contains "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Exchange Act. Forward-looking statements often contain words such as "expects," "anticipates," "estimates," "intends," "plans," "believes," "seeks," "will," "is likely," "scheduled," "positioned to," "continue," "forecast," "predicting," "projection," "potential" or similar expressions. Forward-looking statements include references to goals, plans, strategies, objectives, projected costs or savings, anticipated future performance, results or events and other statements that are not strictly historical in nature. These forward-looking statements are based on management's current expectations, forecasts and assumptions. This means they involve a number of risks and uncertainties that could cause actual results to differ materially from those expressed or implied here. These risks and uncertainties include, without limitation, those set forth above under the heading "Risk Factors."

Readers should not place undue reliance on forward-looking statements contained in this Annual Report on Form 10-K. The forward-looking information herein is given as of this date only, and the Company undertakes no obligation to revise or update it.

17

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

The following discussion should be read in conjunction with both the information at the end of Item 6 of this Annual Report on Form 10-K appearing under the caption, "Forward Looking Information," and the Company's Consolidated Financial Statements and related notes contained in Item 8 of this Annual Report.

Overview and Recent Results

The Company is North America's largest broad line wholesale distributor of business products, with 2007 net sales of $4.6 billion. The Company sells its products through a national distribution network of 70 distribution centers to approximately 30,000 resellers, who in turn sell directly to end consumers.

Organic sales year-to-date through February 26, 2008, were up approximately 1.6% compared with the same period last year. Including incremental sales related to ORS Nasco, year-to-date 2008 revenues were up approximately 7.4%.

Key Company and Industry Trends

The following is a summary of selected trends, events or uncertainties that the Company believes may have a significant impact on its future performance.

- •

- While the macroeconomic environment that supports business-related spending remains uncertain, efforts are being made by the Company to manage all aspects of the business including a disciplined focus on cost control and working capital efficiency improvement.

- •

- On December 21, 2007, the Company completed the acquisition of ORS Nasco, a pure wholesale distributor of industrial supplies. ORS Nasco annual sales for 2007 were nearly $285 million; this acquisition provides United with a new growth platform beginning in 2008. The purchase price, net of cash acquired, was approximately $180 million.

- •

- Management will continue to focus on its six key value drivers, which it believes will help the Company reach important milestones: deliver profitable sales growth, drive out waste, grow private brands, optimize assets, leverage the potential of the ORS Nasco and Sweet Paper acquisitions and enhance the Company's marketing capabilities. Specifically, as part of the effort to drive out waste, several project teams have been engaged in identifying key areas of the business where Six Sigma and lean management tools are being used to reduce costs.

- •

- Total Company sales for 2007 grew 2.2% to $4.6 billion. Adjusted for one more sales day in 2007, sales were up 1.8% over 2006. Continued strong growth was seen in janitorial and breakroom supplies with solid growth in traditional office products. These improvements were partially offset by declines in the technology and furniture categories. The 2007 results include ORS Nasco effective with the acquisition date of December 21, 2007. The acquisition did not have a material impact on the overall sales growth rate for the year.

- •

- Gross margin as a percent of sales for 2007 was 15.2% versus 16.6% in 2006. Gross margin in 2006 benefited from $60.6 million of non-recurring gains related to the Company's product content syndication program and certain marketing program changes. Excluding these non-recurring items, gross margin for 2006 was 15.3%, or 4 basis points (bps) higher than 2007.

- •

- Cash flow increased in 2007 compared with 2006 reflecting working capital improvements made during 2007.

- •

- Significant progress was also made in optimizing the Company's assets over the past year as the Company continues to improve working capital efficiency and works toward achieving its optimal

18

capital structure. In July 2007, the Company amended and restated its Five-Year Revolving Credit Agreement (July 2007 Credit Agreement) that, among other things, provided an additional $100 million in capacity. In October 2007, the Company entered into the 2007 Master Note Purchase Agreement under which it issued and sold $135 million of floating rate senior secured notes in a private placement. In December 2007, the Company also entered into an Amendment to its July 2007 Credit Agreement that provided for a Term Loan of $200 million in addition to the existing Revolving Credit Facility.

- •

- During the fourth quarter of 2007, the Company entered into two interest rate swap transactions to mitigate its floating rate risk on $335 million of London Interbank Offered Rate (LIBOR) based debt. These swap transactions effectively fix the interest rates at 4.674% and 4.075% for $135 million and $200 million of the Company's LIBOR based debt, respectively. These cash flow hedges are being accounted for under the principles outlined in the Financial Accounting Standards Board ("FASB") Statement of Financial Standards ("SFAS") No. 133,Accounting for Derivative Instruments and Hedging Activities ("SFAS No. 133"). See Note 20 of the Consolidated Financial Statements for more detail on the accounting for these transactions.

- •

- During 2007, the Company acquired approximately 6.6 million shares of common stock for $383 million under its publicly announced share repurchase programs. An additional $67.5 million or approximately 1.2 million shares were repurchased in 2008 through February 26, 2008. As of February 26, 2008, the Company had approximately $0.9 million remaining under its August 2007 Board share repurchase authorization. The Company anticipates that the Board of Directors will continue to consider share repurchases throughout 2008.

- •

- During 2007, the Company continued development of its technology enabled marketing capabilities. The Company published its new content and introduced its electronic catalog demonstrating its enhanced content and search capabilities. The Company is working with industry software providers to embed its electronic catalog content into their e-commerce solutions which will enhance the end-consumers' shopping experience and give our reseller customer a competitive advantage. SAP is continuing to invest in their SAP Hosted Solution for Business Products Resellers (the "Solution") which is aimed at providing independent dealers with an enhanced shopping experience for their customers to effectively run their businesses. While the roll-out process of this technology platform has been slowed to more fully develop the functionality and capabilities of the system, SAP anticipates being able to roll out enhanced products for dealers in late 2008.

Acquisition of ORS Nasco Holding, Inc.

On December 21, 2007, the Company's subsidiary, USSC, completed the purchase of 100% of the outstanding shares of ORS Nasco Holding, Inc. (ORS Nasco) from an affiliate of Brazos Private Equity Partners, LLC of Dallas, Texas, and other shareholders. This acquisition was completed with the payment of the base purchase price of $175 million plus estimated working capital adjustments, a pre-closing tax benefit payment and other adjusting items. In total, the preliminary purchase price was $180.6 million, including $0.5 million in transaction costs and net of cash acquired subject to finalizing working capital adjustments. The acquisition will allow the Company to diversify its product offering and provides an entry into the wholesale industrial supplies market. The purchase price was financed through the addition of a $200 million Term Loan under the accordion feature of USSC's existing credit agreement. The purchase price is also subject to certain post-closing adjustments. The Company's Consolidated Financial Statements include ORS Nasco's results of operations from December 22, 2007 and are not deemed material for purposes of providing pro forma financial information. The transaction is expected to be accretive to United's earnings beginning in 2008.

19

ORS Nasco is a pure wholesale distributor of industrial supplies, with annual sales in 2007 of approximately $285 million. The company sells exclusively to independent distributors, stocking approximately 60,000 items and offering thousands of additional premium branded and private label products from approximately 500 manufacturers. ORS Nasco sells to approximately 7,000 independent distributors in multiple channels, including industrial, MRO (maintenance, repair and operations), safety, construction, welding, and oil field services. It serves a very diverse customer base through eight distribution centers strategically located across the United States, and is headquartered in Muskogee, Oklahoma.

The acquisition was accounted for under the purchase method of accounting in accordance with Financial Accounting Standards No. 141, Business Combinations, with the excess purchase price over the fair market value of the assets acquired and liabilities assumed allocated to goodwill. Based on a preliminary purchase price allocation, the preliminary purchase price of $180.6 million, net of cash received, has resulted in goodwill and intangible assets of $89.7 million and $44.6 million, respectively. Neither the goodwill nor the intangible assets are expected to generate a tax deduction. The intangible assets purchased include unamortizable intangibles of $12.3 million that have indefinite lives while the remaining $32.3 million in intangible assets acquired is amortizable. The weighted average useful life of intangibles is expected to be approximately 14 years. The Company recorded amortization for these intangibles from December 22, 2007 through year end. Subsequent adjustments may be made to the purchase price allocation based on, among other things, post-closing purchase price adjustments and finalizing the valuation of tangible and intangible assets.

Critical Accounting Policies, Judgments and Estimates

The Company's significant accounting policies are more fully described in Note 2 of the Consolidated Financial Statements. As described in Note 2, the preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions about future events that affect the amounts reported in the financial statements and accompanying notes. Future events and their effects cannot be determined with absolute certainty. Therefore, the determination of estimates requires the exercise of judgment. Actual results may differ from those estimates. The Company believes that such differences would have to vary significantly from historical trends to have a material impact on the Company's financial results.

The Company's critical accounting policies are most significant to the Company's financial condition and results of operations and require especially difficult, subjective or complex judgments or estimates by management. In most cases, critical accounting policies require management to make estimates on matters that are uncertain at the time the estimate is made. The basis for the estimates is historical experience, terms of existing contracts, observance of industry trends, information provided by customers or vendors, and information available from other outside sources, as appropriate. These critical accounting policies include the following:

Supplier allowances (fixed and variable) are common practice in the business products industry and have a significant impact on the Company's overall gross margin. Gross margin is determined by, among other items, file margin (determined by reference to invoiced price), as reduced by estimated customer discounts and rebates as discussed below, and increased by estimated supplier allowances and promotional incentives. These allowances and incentives are estimated on an ongoing basis and the potential variation between the actual amount of these margin contribution elements and the Company's estimates of them could be material to its financial results. Reported results include management's current estimate of such allowances and incentives.

20

In 2007, approximately 15% of the Company's estimated annual supplier allowances and incentives were fixed, based on supplier participation in various Company advertising and marketing publications. Fixed allowances and incentives are taken to income through lower cost of goods sold as inventory is sold.

The remaining 85% of the Company's estimated supplier allowances and incentives in 2007 were variable, based on the volume and mix of the Company's product purchases from suppliers. These variable allowances are recorded based on the Company's annual inventory purchase volumes and product mix and are included in the Company's financial statements as a reduction to cost of goods sold, thereby reflecting the net inventory purchase cost. Supplier allowances and incentives attributable to unsold inventory are carried as a component of net inventory cost. The potential amount of variable supplier allowances often differs based on purchase volumes by supplier and product category. As a result, lower Company sales volume (which reduce inventory purchase requirements) and product sales mix changes (primarily because higher-margin products often benefit from higher supplier allowance rates) can make it difficult to reach supplier allowance growth hurdles.

Fixed supplier allowances traditionally represented 40% to 45% of the Company's total annual supplier allowances, compared to the 15% referenced above. This ratio has declined significantly as the Company's 2007 supplier contracts eliminated the majority of the historical fixed component and replaced it with a variable allowance based on product purchases. The Company transitioned to a calendar year program with its 2006 Supplier Allowance Program for product content syndication. This change altered the year-over-year timing on recognizing related income, which resulted in a non-recurring positive impact to gross margin of $41.6 million during 2006.