| | |

| | Exhibit IX |

| | |

| | Financial Report 2013 |

Contents

Report of the Board of Directors 2013

In 2013, the global economy continued its protracted post-crisis transition. The largest advanced economies gradually strengthened, while emerging economies slowed down. The anticipation of more restrictive monetary policy in the U.S. pushed long-term government bond yields higher. Corporate bond spreads in Northern Europe generally tightened, while short- to medium-term bank lending was readily available.

During the year, the overall economic growth in the Nordic–Baltic region remained weak, with only a few of the smaller economies growing by more than 2%. While faring better than the rest of Europe, real capital investment stagnated and remains well below 2008 levels.

Despite the stagnant investment climate, the Bank signed loan agreements for a total of EUR 1,810 million (2012: EUR 2,366 million) and disbursed EUR 1,922 million (2012: EUR 2,355 million). Moreover, half of these loans are to new borrowers, which broadens NIB’s client base and reduces concentration in the loan portfolio.

NIB raised EUR 4.1 billion in new funding during 2013.

Despite somewhat lower lending volumes, the Bank’s profit for the period increased to EUR 217 million (2012: EUR 209 million). Impairment charges decreased compared to the previous year and the average margin for the loan portfolio increased.

Mission fulfilment

In 2013, the Board of Directors, chaired by Rolandas Kriščiūnas, streamlined NIB’s mission. According to the new wording, “NIB finances projects that improve the competitiveness and environment of the Nordic and Baltic countries”. In the same context, a vision of “a prosperous and sustainable Nordic–Baltic region” was introduced.

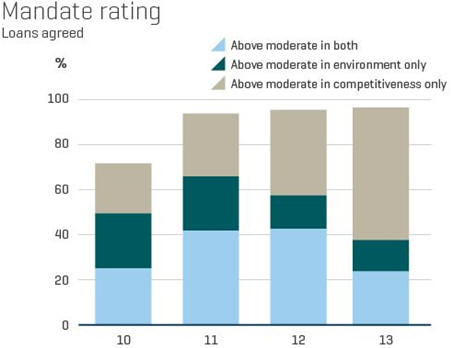

NIB finances specific investment projects that fulfil the Bank’s mission. This is secured by reviewing all projects from the sustainability perspective, by doing a so called mandate rating. In 2013, the proportion of loans achieving “good” or “excellent” mandate fulfilment was 98%.

Projects with a high competitiveness impact included infrastructure investments, such as public transport, roads, ports, transmission lines, healthcare development and municipal infrastructure. In addition, support for R&D continues to have a strong focus, given that innovation is the key driver of improvements in productivity and long-term growth in today’s knowledge-based economies.

A number of loan programmes have also been extended to financial intermediaries, including leasing companies, with the specific target of strengthening the potential of smaller businesses to invest and expand their economic activities. These programmes will continue to be an important way for NIB to support the growth of the companies that account for job creation and value added in its member countries.

During the year, the Bank started developing a special initiative to broaden its outreach to the SME sector in its member countries in cooperation with local banks.

NIB defines loans to projects with significant direct or indirect positive environmental impacts as environmental loans, regardless of the industrial sector in which they occur. In 2013, a total volume of EUR 713 million was agreed for projects with an environmental mission fulfilment of “good” or “excellent”, which is equivalent to 39% of total agreed volume.

Many projects had a strong focus on climate change mitigation and on helping our member countries’ transition towards a resource-efficient, low-carbon economy. NIB estimates that its projects agreed in 2013 will help reduce CO2 emissions by 370,000 tonnes annually.

The majority of NIB’s financing was directed at reducing greenhouse gas emissions by investing in renewable energy generation or improving energy efficiency. NIB was involved in eight hydropower projects aimed at increasing efficiency by upgrading existing plants. NIB-financed energy projects will add over 1 TWh annually to renewable energy generation.

NIB’s environmental lending also included several projects increasing the resource efficiency of transport systems (e.g. rail and public transport infrastructure projects in Sweden, Lithuania and Latvia).

Lending activities

In 2013, NIB’s lending activities developed well. The Bank signed 43 loan agreements with a combined total of EUR 1,810 million. Half of these loans are to new borrowers, which broadens NIB’s client base and reduces concentration in the loan portfolio. Lending developments in terms of business sectors are displayed in the table.

Disbursements of loans totalled EUR 1,922 million, compared to EUR 2,355 million during 2012. The lower outcome was the result of some coinciding factors. Continued low growth in the major part of the member area held back investments. At the same time, liquidity in general improved in the financial markets, with increasing amounts of capital being made available in the Nordic–Baltic region. This also affected the loan portfolio through larger than average early redemptions of loans, partly due to successful refinancing arrangements. Lending activities, however, increased notably towards the end of the year.

Lending

| | | | | | | | |

| (In EUR million unless otherwise specified) | | 2013 | | | 2012 | |

Energy and environment | | | 302 | | | | 525 | |

Infrastructure and telecom | | | 474 | | | | 744 | |

Industries and services | | | 805 | | | | 899 | |

Financial institutions and SMEs | | | 230 | | | | 198 | |

Loans agreed, total | | | 1,810 | | | | 2,366 | |

Member countries | | | 1,760 | | | | 1,880 | |

Non-member countries | | | 50 | | | | 487 | |

Loans disbursed, total | | | 1,922 | | | | 2,355 | |

Member countries | | | 1,670 | | | | 1,979 | |

Non-member countries | | | 251 | | | | 376 | |

Number of loan agreements, total | | | 43 | | | | 42 | |

Member countries | | | 42 | | | | 33 | |

Non-member countries | | | 1 | | | | 9 | |

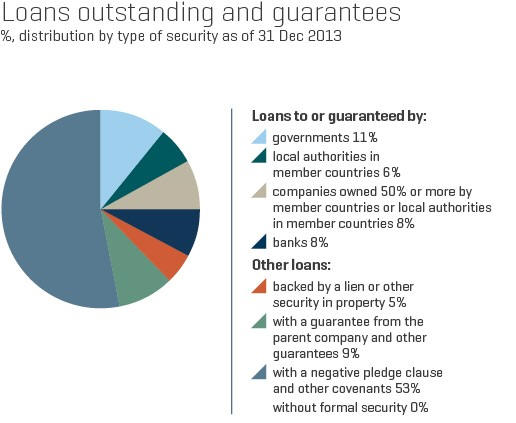

Loans outstanding and guarantees | | | 14,667 | | | | 15,131 | |

Member countries | | | 12,035 | | | | 12,241 | |

Non-member countries | | | 2,669 | | | | 2,930 | |

Repayments and prepayments | | | 1,819 | | | | 1,503 | |

Collective impairements | | | -37 | | | | -40 | |

Treasury activities

During 2013, NIB raised EUR 4.1 billion through 42 funding transactions. At year-end, outstanding debt totalled EUR 18,421 million in 19 currencies. In February 2013, the Bank issued its largest ever single funding transaction through a three-year, USD 2 billion global benchmark transaction.

NIB’s investor distribution continued to be diversified, with global investors supporting NIB’s funding programme. Asia remains the most important region and made up 38% of all investors in 2013. Investors based in Europe and the Americas make up 30% and 11% respectively, while the Australia and New Zealand region increased and represents 13% of the investor base in 2013.

The Bank issued two NIB Environmental Bonds during 2013. One issue targeted Swedish investors and one was directed at Japanese retail investors. The proceeds were used for financing environmental projects in Sweden and Denmark.

The Bank’s liquidity remained strong during 2013, with 23% invested in money market instruments and 77% invested in highly rated floating and fixed-income securities. Of this liquidity, 83% is invested in line with the Basel III liquidity criteria (being defined as High Quality Liquid Assets).

It is the Bank’s target to ensure a sufficient level of liquidity to be able to continue disbursing new loans and fulfil all payment obligations for one year forward without necessitating additional funding. This target was also reached in 2013.

Financial activities

| | | | | | | | | | | | |

| (In EUR million) | | 2013 | | | 2012 | | | 2011 | |

| New debt issues | | | 4,080 | | | | 4,355 | | | | 2,887 | |

| Debts evidenced by certificates at year-end | | | 18,421 | | | | 20,332 | | | | 18,433 | |

| Number of borrowing transactions | | | 42 | | | | 28 | | | | 43 | |

| Number of borrowing currencies | | | 12 | | | | 8 | | | | 11 | |

Risk management

The Bank’s overall risk position remained solid in 2013, based on sustained high asset quality and a sound capitalisation level. Despite continued weakness in the economic environment and some counterparties facing difficulties, the overall quality of the loan portfolio remained high.

In total, 83% of the lending exposure was in the investment grade categories (risk classes 1–10), which was almost unchanged compared to year-end 2012. The exposure in the weakest risk classes (17–20) increased to 1.2% of total lending (compared to 0.5% the year before) due to the downgrading of a few borrowers.

Non-performing loans and loans for which specific impairments have been made decreased to EUR 66 million net after impairment (2012: EUR 80 million), representing 0.4% of the total lending exposure.

The Bank maintains a well-balanced loan portfolio, taking into consideration its mission. There were no material changes in the geographical and sectoral distribution of the loan portfolio in 2013. At year-end, the member countries accounted for 80% (2012: 77%) of the total lending exposure, followed by Central and Eastern Europe with 9% and Asia with 7%.

The decline in the treasury exposure mainly stemmed from a decrease in the swap exposure and related lower volumes of cash collateral placed.

As in the previous year, the credit quality of the Treasury portfolio was strong, with 99% of the exposure in the investment-grade categories (risk classes 1–10). The geographical distribution of the Treasury portfolio was weighted towards Germany and France, together accounting for 41% of the exposure (2012: 32%). Of the Treasury exposure, 32% was to the member countries, compared to 39% the year before.

The Bank continues to put emphasis on strengthening its risk management in order to keep up with evolving market standards. During 2013, resources were devoted to identifying and addressing gaps in such standards, and measures were taken to further enhance the monitoring of the Bank’s market risk. Furthermore, credit risk management is being streamlined by integrating credit analysis, monitoring and reporting into a common platform.

Compliance

In 2013, the Board approved a Non-Compliant Jurisdiction Policy aimed at strengthening the Bank’s due diligence on anti-money laundering and terrorist financing and tax evasion. The Board of Directors was presented in 2013 with investigation reports on two customer cases of alleged fraud and corruption. The relevant national authorities have been informed accordingly.

Financial results

Despite the unfavourable investment climate, NIB managed to improve its financial results. NIB recorded a solid profit of EUR 217 million, compared with a profit of EUR 209 million in 2012.

Net interest income decreased somewhat in 2013. This was driven by lower interest income from treasury activities due to the low-yield interest rate environment. Partly offsetting this was the increased average margin for the loan portfolio.

Impairment charges in 2013 decreased and were EUR 15 million, compared with EUR 56 million last year. Individually assessed impairments were in line with last year. Collectively assessed impairments decreased, with a positive impact on the result of EUR 3 million.

Costs including depreciation in 2013 were 2% higher than in 2012, and total expenses amounted to EUR 39 million (2012: EUR 38 million). The cost/income ratio remained low and was 14%. The average number of employees was 183 (2012: 180). The increase was due to a strengthening of the control environment of the Bank.

The Bank’s total assets decreased to EUR 23 billion as of 31 December 2013 (2012: EUR 26 billion). The equity ratio, calculated as equity over total assets, has consequently increased to 12%. The total amount of loans outstanding decreased to EUR 14.7 billion (2012: EUR 15.1 billion).

NIB issued EUR 4.1 billion of long-term debt during the year. Total debt outstanding as of the end of 2013 amounted to EUR 18.4 billion (2012: EUR 20.3 billion). Changes in currency exchange rates reduced the size of the Bank’s balance sheet, particularly total debt outstanding and the related swap transactions.

The Bank’s AAA/Aaa credit rating was affirmed with stable outlook by S&P on 5 December 2013 and by Moody’s on 28 June 2013. NIB maintains strong balance sheet, high asset quality and strong ownership support.

Key figures

| | | | | | | | | | | | |

| (in EUR million) | | 2013 | | | 2012 | | | 2011 | |

Net interest income | | | 244 | | | | 252 | | | | 228 | |

Profit/loss on financial operations | | | 20 | | | | 43 | | | | 8 | |

Loan impairments | | | 15 | | | | 56 | | | | 12 | |

Profit/loss | | | 217 | | | | 209 | | | | 194 | |

Equity | | | 2,831 | | | | 2,666 | | | | 2,456 | |

Total assets | | | 23,490 | �� | | | 25,983 | | | | 23,802 | |

Solvency ratio (equity/total assets %) | | | 12.1% | | | | 10.3% | | | | 10.3% | |

Cost/income ratio | | | 14.3% | | | | 12.5% | | | | 15.2% | |

Dividend

The Board of Directors proposes to the Board of Governors that EUR 55 million be paid as dividends to the Bank’s member countries for the year 2013.

Outlook

While most of the year 2013 was dominated by the slowdown in economic activity and weak investment climate, activity picked up towards year-end. Consistent with underlying macroeconomic fundamentals, this suggests an improving trend in capital investment in the Nordic–Baltic region and somewhat stronger demand for loans heading into 2014.

Banks will still focus on building and protecting capital rather than extending new credit. These developments— together with the stricter Basel requirements—continue to highlight NIB’s value in flexible long-term lending. However, headwinds remain in both the global and regional economies, which are expected to prevent activity from picking up more substantially.

Proposal by the Board of Directors to the Board of Governors

The Board of Directors’ proposal with regard to the allocation of profit for the year 2013 takes into account the need to keep the Bank’s ratio of equity to risk weighted assets at a secure level, which is a prerequisite for maintaining the Bank’s high creditworthiness.

In accordance with section 11 of the Statutes of the Bank, the profit for 2013 of EUR 217,210,128.68 is to be allocated as follows:

| • | | EUR 162,210,128.68 is transferred to the General Credit Risk Fund as a part of equity; |

| • | | no transfer is made to the Special Credit Risk Fund for Project Investment Loans; |

| • | | no transfer is made to the Statutory Reserve - the Statutory Reserve amounts to EUR 686,325,305.70 or 11.2% of the Bank’s authorised capital stock as of 31 December 2013; and |

| • | | EUR 55,000,000.00 is made available for distribution as dividends to the Bank’s member countries. |

More information can be found in the statement of comprehensive income, statement of financial position, changes in equity and cash flow statement, as well as in the notes to the financial statements.

Helsinki, 6 March 2014

| | | | |

Rolandas Kriščiūnas | | Līga Kļaviņa on behalf of Kaspars Āboliņš | | Pentti Pikkarainen |

| | |

Silje Gamstøbakk | | Jesper Olesen | | Sven Hegelund |

Þorsteinn Þorsteinsson | | Henrik Normann President and CEO | | Madis Üürike |

Statement of comprehensive income

1 January – 31 December

| | | | | | | | | | | | |

| EUR 1,000 | | Note | | | 2013 | | | 2012 | |

| Interest income | | | | | | | 404,179 | | | | 494,064 | |

Interest expense | | | | | | | -159,975 | | | | -242,370 | |

| Net interest income | | | (1), (2), (22) | | | | 244,204 | | | | 251,693 | |

| | | |

Commission income and fees received | | | (3) | | | | 10,199 | | | | 10,620 | |

| Commission expense and fees paid | | | | | | | -2,454 | | | | -2,223 | |

| Net profit/loss on financial operations | | | (4) | | | | 19,840 | | | | 43,288 | |

| Foreign exchange gains and losses | | | | | | | -384 | | | | -221 | |

| Operating income | | | | | | | 271,404 | | | | 303,157 | |

| | | |

Expenses General administrative expenses | | | (5), (22) | | | | 35,217 | | | | 34,291 | |

| Depreciation | | | (9), (10) | | | | 3,592 | | | | 3,611 | |

| Impairment of loans | | | (6), (8) | | | | 15,385 | | | | 56,050 | |

| Total expenses | | | | | | | 54,194 | | | | 93,951 | |

| | | | | | | | | | | | | |

| PROFIT/LOSS FOR THE YEAR | | | | | 217,210 | | | 209,205 | |

| | | | | | | | | | |

Total comprehensive income | | | | | | | 217,210 | | | | 209,205 | |

The Nordic Investment Bank’s accounts are kept in euro.

Statement of financial position at 31 December

| | | | | | | | | | | | | | | | |

| EUR 1,000 | | | | | Note | | | 2013 | | | 2012 | |

ASSETS | | | | | | | (1), (18), (19), (20), (21) | | | | | | | | | |

Cash and cash equivalents | | | | | | | (17), (23) | | | | 1,757,616 | | | | 2,817,189 | |

Financial placements | | | | | | | (17) | | | | | | | | | |

Placements with credit institutions | | | | | | | | | | | 5,741 | | | | 4,191 | |

Debt securities | | | | | | | (7) | | | | 5,343,419 | | | | 5,248,858 | |

Other | | | | | | | | | | | 24,247 | | | | 22,059 | |

| | | | | | | | | | | | 5,373,407 | | | | 5,275,108 | |

Loans outstanding | | | | | | | (8), (17) | | | | 14,666,747 | | | | 15,130,669 | |

| Intangible assets | | | | | | | (9) | | | | 5,111 | | | | 4,446 | |

| Tangible assets, property and equipment | | | | | | | (9) | | | | 29,640 | | | | 29,856 | |

Other assets | | | | | | | (11), (17) | | | | | | | | | |

Derivatives | | | | | | | | | | | 1,308,990 | | | | 2,347,873 | |

Other assets | | | | | | | (22) | | | | 30,279 | | | | 25,895 | |

| | | | | | | | | | | | 1,339,269 | | | | 2,373,768 | |

Payments to the Bank’s reserves, receivable | | | | | | | | | | | - | | | | - | |

| Accrued interest and fees receivable | | | | | | | | | | | 318,151 | | | | 351,875 | |

| TOTAL ASSETS | | | | | | | | | | | 23,489,941 | | | | 25,982,911 | |

| | | | |

LIABILITIES AND EQUITY | | | | | | | (1), (18), (19), (20), (21) | | | | | | | | | |

| Liabilities | | | | | | | | | | | | | | | | |

| Amounts owed to credit institutions | | | | | | | (17), (22) | | | | | | | | | |

Short-term amounts owed to credit institutions | | | | | | | (16), (23) | | | | 372,402 | | | | 1,593,338 | |

Long-term amounts owed to credit institutions | | | | | | | | | | | - | | | | 15,222 | |

| | | | | | | | | | | | 372,402 | | | | 1,608,560 | |

Debts evidenced by certificates | | | | | | | (12), (17) | | | | | | | | | |

Debt securities issued | | | | | | | | | | | 18,346,651 | | | | 20,254,987 | |

Other debt | | | | | | | | | | | 73,906 | | | | 77,144 | |

| | | | | | | | | | | | 18,420,557 | | | | 20,332,131 | |

| Other liabilities | | | | | | | (13), (17) | | | | | | | | | |

Derivatives | | | | | | | | | | | 1,615,146 | | | | 1,102,707 | |

Other liabilities | | | | | | | | | | | 8,094 | | | | 9,397 | |

| | | | | | | | | | | | 1,623,240 | | | | 1,112,104 | |

Accrued interest and fees payable | | | | | | | | | | | 242,855 | | | | 264,439 | |

| Total liabilities | | | | | | | | | | | 20,659,054 | | | | 23,317,234 | |

Equity | | | | | | | | | | | | | | | | |

Authorised and subscribed capital | | | 6,141,903 | | | | | | | | | | | | | |

of which callable capital | | | -5,723,302 | | | | | | | | | | | | | |

Paid-in capital | | | 418,602 | | | | (14) | | | | 418,602 | | | | 418,602 | |

| Reserve funds | | | | | | | (15) | | | | | | | | | |

Statutory Reserve | | | | | | | | | | | 686,325 | | | | 686,325 | |

General Credit Risk Fund | | | | | | | | | | | 1,112,831 | | | | 955,626 | |

Special Credit Risk Fund PIL | | | | | | | | | | | 395,919 | | | | 395,919 | |

Payments to the Bank’s reserves, receivable | | | | | | | | | | | - | | | | - | |

| Profit/loss for the year | | | | | | | | | | | 217,210 | | | | 209,205 | |

| Total equity | | | | | | | | | | | 2,830,887 | | | | 2,665,677 | |

TOTAL LIABILITIES AND EQUITY | | | | | | | | | | | 23,489,941 | | | | 25,982,911 | |

Collateral and commitments | | | | | | | (16) | | | | | | | | | |

The Nordic Investment Bank’s accounts are kept in euro.

Changes in equity

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| EUR 1,000 | | Paid-in

capital | | | Statutory

Reserve | | | General

Credit

Risk Fund | | | Special

Credit

Risk

Fund

PIL | | | Payments

to the

Bank’s

Statutory

Reserve

and

credit

risk funds | | | Appropriation

to dividend

payment | | | Other value

adjustments | | | Profit/

Loss for

the year | | | Total | |

| EQUITY AT 31 DECEMBER 2011 | | | 418,602 | | | | 683,685 | | | | 761,589 | | | | 395,919 | | | | 2,640 | | | | 0 | | | | 0 | | | | 194,037 | | | | 2,456,472 | |

| Appropriations between reserve funds | | | | | | | | | | | 194,037 | | | | | | | | | | | | | | | | | | | | -194,037 | | | | 0 | |

| Paid-in capital | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 0 | |

| Called in authorised and subscribed capital | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 0 | |

| Payments to the Bank’s Statutory Reserve and credit risk funds, receivable | | | | | | | 2,640 | | | | | | | | | | | | -2,640 | | | | | | | | | | | | | | | | 0 | |

| Comprehensive income for the year | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 209,205 | | | | 209,205 | |

| EQUITY AT 31 DECEMBER 2012 | | 418,602 | | | 686,325 | | | 955,625 | | | 395,919 | | | 0 | | | 0 | | | 0 | | | 209,205 | | | 2,665,677 | |

| Appropriations between reserve funds | | | | | | | | | | | 157,205 | | | | | | | | | | | | 52,000 | | | | | | | | -209,205 | | | | 0 | |

| Paid-in capital | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 0 | |

| Called in authorised and subscribed capital | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 0 | |

| Payments to the Bank’s Statutory Reserve and credit risk funds, receivable | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 0 | |

| Dividend payment | | | | | | | | | | | | | | | | | | | | | | | -52,000 | | | | | | | | | | | | -52,000 | |

| Comprehensive income for the year | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 217,210 | | | | 217,210 | |

| EQUITY AT 31 DECEMBER 2013 | | | 418,602 | | | | 686,325 | | | | 1,112,831 | | | | 395,919 | | | | 0 | | | | 0 | | | | 0 | | | | 217,210 | | | | 2,830,887 | |

| | | | | | | | |

| Proposed appropriation of the year’s profit/loss | | 2013 | | | 2012 | |

Appropriation to Statutory Reserve | | | - | | | | - | |

Appropriations to credit risk reserve funds | | | | | | | | |

General Credit Risk Fund | | | 162,210 | | | | 157,205 | |

Special Credit Risk Fund PIL | | | - | | | | - | |

Appropriation to dividend payment | | | 55,000 | | | | 52,000 | |

Profit/loss for the year | | | 217,210 | | | | 209,205 | |

The Nordic Investment Bank’s accounts are kept in euro.

Cash flow statement 1 January – 31 December

| | | | | | | | | | |

| EUR 1,000 | | Note | | Jan–Dec

2013 | | | Jan–Dec

2012 | |

Cash flows from operating activities | | | | | | | | | | |

Profit/loss from operating activities | | | | | 217,210 | | | | 209,205 | |

| | | |

Adjustments: | | | | | | | | | | |

Unrealised gains/losses of financial assets held at fair value | | | | | -13,500 | | | | -44,717 | |

Depreciation and write-down in value of tangible and intangible assets | | | | | 3,592 | | | | 3,611 | |

Change in accrued interest and fees (assets) | | | | | 33,724 | | | | 11,812 | |

Change in accrued interest and fees (liabilities) | | | | | -21,584 | | | | -14,939 | |

Impairment of loans | | | | | 15,385 | | | | 56,050 | |

Adjustment to hedge accounting | | | | | -2,294 | | | | 1,381 | |

Other adjustments to the year’s profit | | | | | -1,820 | | | | -2,523 | |

Adjustments, total | | | | | 13,503 | | | | 10,675 | |

| | | |

Lending | | | | | | | | | | |

Disbursements of loans | | | | | -1,921,755 | | | | -2,354,787 | |

Repayments of loans | | | | | 1,818,766 | | | | 1,502,789 | |

Capitalisations, redenominations, index adjustments, etc. | | | | | -686 | | | | 245 | |

Transfer of loans to claims in other assets | | | | | - | | | | 2,854 | |

Exchange rate adjustments | | | | | 414,332 | | | | -85,199 | |

Lending, total | | | | | 310,656 | | | | -934,098 | |

| | | |

Cash flows from operating activities, total | | | | | 541,369 | | | | -714,218 | |

| | | |

Cash flows from investing activities | | | | | | | | | | |

Placements and debt securities | | | | | | | | | | |

Purchase of debt securities | | | | | -2,437,468 | | | | -2,893,778 | |

Sold and matured debt securities | | | | | 2,310,584 | | | | 2,046,894 | |

Placements with credit institutions | | | | | -1,550 | | | | -674 | |

Other financial placements | | | | | 1,222 | | | | -3,463 | |

Exchange rate adjustments, etc. | | | | | 27,783 | | | | 4,074 | |

Placements and debt securities, total | | | | | -99,429 | | | | -846,947 | |

| | | |

Other items | | | | | | | | | | |

Acquisition of intangible assets | | | | | -2,440 | | | | -1,727 | |

Acquisition of tangible assets | | | | | -1,602 | | | | -820 | |

Change in other assets | | | | | 172 | | | | 13,587 | |

Other items, total | | | | | -3,870 | | | | 11,040 | |

| | | |

Cash flows from investing activities, total | | | | | -103,300 | | | | -835,907 | |

| | | |

Cash flows from financing activities | | | | | | | | | | |

Debts evidenced by certificates | | | | | | | | | | |

Issues of new debt | | | | | 4,079,958 | | | | 4,355,019 | |

Redemptions | | | | | -3,776,926 | | | | -2,435,918 | |

Exchange rate adjustments | | | | | -1,608,276 | | | | -312,663 | |

Debts evidenced by certificates, total | | | | | -1,305,244 | | | | 1,606,438 | |

| | | |

Other items | | | | | | | | | | |

Long-term placements from credit institutions | | | | | -15,222 | | | | -86,444 | |

Change in swap receivables | | | | | 638,041 | | | | 262,337 | |

Change in swap payables | | | | | 459,022 | | | | 70,114 | |

Change in other liabilities | | | | | -1,304 | | | | -545 | |

Dividend paid | | | | | -52,000 | | | | - | |

Paid-in capital and reserves | | | | | - | | | | 2,640 | |

Other items, total | | | | | 1,028,537 | | | | 248,102 | |

| | | |

Cash flows from financing activities, total | | | | | -276,706 | | | | 1,854,540 | |

| | | | | | | | | | | | |

| | | |

CHANGE IN CASH AND CASH EQUIVALENTS, NET | | | (23) | | | | 161,363 | | | | 304,414 | |

| | | |

Opening balance for cash and cash equivalents, net | | | | | | | 1,223,851 | | | | 919,437 | |

Closing balance for cash and cash equivalents, net | | | | | | | 1,385,213 | | | | 1,223,851 | |

| | | |

Additional information to the statement of cash flows | | | | | | | | | | | | |

Interest income received | | | | | | | 437,903 | | | | 505,876 | |

Interest expense paid | | | | | | | -181,559 | | | | -257,309 | |

The cash flow statement has been prepared using the indirect method and cash flow items cannot be directly concluded from the statements of financial positions.

Notes to the financial statements

ACCOUNTING POLICIES

General operating principles

The operations of the Nordic Investment Bank (hereinafter called the Bank or NIB) are governed by an agreement (hereinafter called the Agreement) among the governments of Denmark, Estonia, Finland, Iceland, Latvia, Lithuania, Norway and Sweden (hereinafter called the member countries), and the Statutes adopted in conjunction with that agreement. NIB is an international financial institution that operates in accordance with sound banking principles. NIB finances private and public projects which have high priority with the member countries and the borrowers. NIB finances projects both within and outside the member countries, and offers its clients long-term loans and guarantees on competitive market terms.

NIB acquires the funds to finance its lending by borrowing on international capital markets.

The authorised capital stock of the Bank is subscribed by the member countries. Any increase or decrease in the authorised capital stock shall be decided by the Board of Governors, upon a proposal of the Board of Directors of the Bank.

In the member countries, the Bank is exempt from payment restrictions and credit policy measures, and has the legal status of an international legal person, with full legal capacity. The Agreement concerning NIB contains provisions regarding immunities and privileges accorded to the Bank, e.g. the exemption of the Bank’s assets and income from taxation.

The headquarters of the Bank are located at Fabianinkatu 34 in Helsinki, Finland.

Significant accounting policies

Basis for preparing the financial statements

The Bank’s financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB). The Bank’s accounts are kept in euro. With the exceptions noted below, they are based on historical cost.

Significant accounting judgements and estimates

As part of the process of preparing the financial statements in conformity with IFRS, the Bank’s management is required to make certain judgements, estimates and assumptions that have an effect on the Bank’s profits, its financial position and other information presented in the Annual Report. These estimates are based on available information and the judgements made by the Bank’s management. Actual outcomes may deviate from the assessments made, and such deviations may at times be substantial.

The Bank uses various valuation models and techniques to estimate fair values of assets and liabilities. There are significant uncertainties related to these estimates, in particular when they involve modelling complex financial instruments, such as derivative instruments used for hedging activities related to both borrowing and lending. The estimates are highly dependent on market data, such as the level of interest rates, currency rates and other factors. The uncertainties related to these estimates are reflected mainly in the statement of financial position. NIB

undertakes continuous development in order to improve the basis for the fair value estimates, with regard to both modelling and market data. Changes in estimates resulting from refinements in assumptions and methodologies are reflected in the period in which the enhancements are first applied.

Judgements and estimates are also associated with impairment testing of loans and claims.

Recognition and derecognition of financial instruments

Financial instruments are recognised in the statement of financial position on a settlement date basis.

A financial asset is derecognised when the contractual rights to the cash flows from the financial asset expire.

A financial liability is removed from the statement of financial position when the obligation specified in the contract is discharged, cancelled or expires.

Foreign currency translation

Monetary assets and liabilities denominated in foreign currencies are recognised in the accounts at the exchange rate prevailing on the closing date. Non-monetary assets and liabilities are recognised in the accounts at the euro rate prevailing on the transaction date. Income and expenses recognised in currencies other than the euro are converted on a daily basis to the euro, in accordance with the euro exchange rate prevailing on that day.

Realised and unrealised exchange rate gains and losses are recognised in the statement of comprehensive income.

The Bank uses the official exchange rates published for the euro by the European Central Bank. See Note 24.

Basis for measurement

The financial statements have been prepared on the historical cost basis, except for the following material items in the statement of financial position.

After the adaptation of IFRS 9 in 2011, the Bank classifies its financial assets into the following categories: those measured at amortised cost, and those measured at fair value. This classification depends on both the contractual characteristics of the assets and the business model adopted for their management.

Financial assets at amortised cost

An investment is classified at “amortised cost” only if both of the following criteria are met: the objective of the Bank’s business model is to hold the assets in order to collect the contractual cash flows and the contractual terms of the financial assets must give rise on specified dates to cash flows that are only payments of principal and interest on the principal amount outstanding.

Financial assets at fair value

If either of the two criteria above is not met, the asset cannot be classified in the amortised cost category and must be classified at fair value.

Recognised financial assets and financial liabilities designated as hedged items in qualifying fair value hedge relationships are adjusted for changes in fair value attributable to the risk being hedged.

Cash and cash equivalents

Cash and cash equivalents comprise monetary assets and placements with original maturities of six months or less, calculated from the date the acquisition and placements were made.

Cash and cash equivalents in the cash flow statement refers to the net amount of monetary assets, placements and liabilities with original maturities of six months or less, calculated from the time the transaction was entered into.

Financial placements

Items recognised as financial placements in the statement of financial position include placements with credit institutions and placements in debt securities, for example, bonds and other debt certificates, as well as certain placements in instruments with equity features. The placements are initially recognised on the settlement date. Their subsequent accounting treatment depends on both the Bank’s business model for managing the placements and their contractual cash flow characteristics.

Lending

The Bank may grant loans and provide guarantees under its Ordinary Lending or under special lending facilities. The special lending facilities, which carry member country guarantees, consist of Project Investment Loans (PIL) and Environmental Investment Loans (MIL).

Ordinary Lending includes loans and guarantees within and outside the member countries. The Bank’s Ordinary Lending ceiling corresponds to 250% of its authorised capital and accumulated general reserves and amounts to EUR 20,258 million following the allocations of the year’s profit in accordance with the Board of Directors’ proposal.

Project Investment Loans are granted for financing creditworthy projects in the emerging markets of Africa, Asia, Europe and Eurasia, Latin America and the Middle East. The Bank’s Statutes permit loans to be granted and guarantees to be issued under the PIL facility up to an amount corresponding to EUR 4,000 million. The member countries guarantee the PIL loans up to a total amount of EUR 1,800 million. The Bank, however, will assume 100% of any losses incurred under an individual PIL loan, up to the amount available at any given time in the Special Credit Risk Fund for PIL. Only thereafter would the Bank be able to call the member countries’ guarantees according to the following principle: the member countries guarantee 90% of each loan under the PIL facility up to a total amount of EUR 1,800 million. Payment under the member countries’ guarantees would take place at the request of the Board of Directors, as provided for under an agreement between the Bank and each individual member country.

The Bank is authorised to grant special Environmental Investment Loans up to the amount of EUR 300 million, for the financing of environmental projects in the areas adjacent to the member countries. The Bank’s member countries guarantee 100% of the MIL facility.

The Bank’s lending transactions are recognised in the statement of financial position at the time the funds are transferred to the borrower. Loans are recognised initially at historical cost, which corresponds to the fair value of the transferred funds, including transaction costs. Loans outstanding are carried at amortised cost. If the loans are hedged against changes in fair value by using derivative instruments, they are recognised in the statement of financial position at fair value, with value changes recognised in the statement of comprehensive income. Changes in fair value are mainly caused by changes in market interest rates.

Impairment of loans and receivables

Impairment of individually assessed loans

The Bank reviews its problem loans and receivables on each reporting date to assess whether an allowance for impairment should be recorded in the statement of comprehensive income. In particular, judgement by management is required in estimating the amount and timing of future cash flows when determining the level of allowance required. Such estimates are based on assumptions about a number of factors and actual results may differ, resulting in future changes to the allowance.

Receivables are carried at their estimated recoverable amount. Where the collectability of identified loans is in doubt, specific impairment losses are recognised in the statement of comprehensive income. Impairment is defined as the difference between the carrying value of the asset and the net present value of expected future cash flows, determined using the instrument’s original effective interest rate where applicable. If the carrying amount of the loan is higher than the net present value of the estimated future cash flows, including the fair value of the collaterals, the loan is impaired.

For issued guarantees, the impairment is recognised when it is both probable that the guarantee will need to be settled and the settlement amount can be reliably estimated.

In the event that payments in respect of an ordinary loan are more than 90 days overdue, all of the borrower’s loans are deemed to be non-performing and consequently the need for impairment is assessed and recognised.

In the event that payments in respect of a PIL loan to a government or guaranteed by a government are more than 180 days overdue, all of the borrower’s loans are deemed to be non-performing.

Whenever payments in respect of a PIL loan that is not to a government or guaranteed by a government are more than 90 days overdue, all of the borrower’s loans are deemed to be non-performing. Impairment losses are then recognised in respect of the part of the outstanding loan principal, interest, and fees that correspond to the Bank’s own risk for this loan facility at any given point in time.

Whenever payments in respect of a MIL loan that is not to a government or guaranteed by a government are more than 90 days overdue, or payments in respect of a MIL loan to a government or guaranteed by a government are more than 180 days overdue, all of the borrower’s loans are deemed to be non-performing. Due to the Bank’s member countries’ guarantees, no impairment losses are recognised for MIL loans.

Impairment of collectively assessed loans

Loans that are not individually impaired will be transferred to a group of loans with similar risk characteristics for a collective impairment test.

The Bank assesses the need to make a collective impairment test on exposures which, although not specifically identified as requiring a specific allowance, have a greater risk of default than when originally granted. This collective impairment test is based on any deterioration in the internal rating of the groups of loans or investments from the time they were granted or acquired. These internal ratings take into consideration factors such as any deterioration in counterparty risk, the value of collaterals or securities received, and the outlook for the sector, as well as identified structural weaknesses or deterioration in cash flows.

The process includes management’s judgement based on the current macroeconomic environment and the current view of the expected economic outlook. In the Bank’s view, the assumptions and estimates made represent an appropriate level of conservatism and are reflective of the predicted economic conditions, the Bank’s portfolio

characteristics and their correlation with losses incurred based on historical loss experience. The impairment remains related to the group of loans until the losses have been identified on an individual basis.

Intangible assets

Intangible assets mainly consist of investments in software, software licences and ongoing investments in new ICT systems. The investments are carried at historical cost, and are amortised over the assessed useful life of the assets, which is estimated to be between three and five years. The amortisations are made on a straight-line basis.

Tangible assets

Tangible assets in the statement of financial position include land, buildings, office equipment, and other tangible assets owned by the Bank. The assets are recognised at historical cost, less any accumulated depreciation based on their assessed useful life. No depreciations are made for land. The Bank’s office building in Helsinki is depreciated on a straight-line basis over a 40-year period. The Bank’s other buildings are depreciated over a 30-year period. The depreciation period for office equipment and other tangible assets is determined by assessing the individual item. The depreciation period is usually three to five years. The depreciations are calculated on a straight-line basis.

Write-downs and impairment of intangible and tangible assets

The Bank’s assets are reviewed annually for impairment. If there is any objective evidence of impairment, the impairment loss is determined based on the recoverable amount of the assets.

Borrowing

The Bank’s borrowing transactions are recognised in the statement of financial position at the time the funds are transferred to the Bank. The borrowing transactions are recognised initially at a cost that comprises the fair value of the funds transferred, less transaction costs. The Bank uses derivative instruments to hedge the fair value of virtually all its borrowing transactions. In these instances, the borrowing transaction is subsequently recognised in the statement of financial position at fair value, with any changes in value recognised in the statement of comprehensive income.

Securities delivered under repurchase agreements are not derecognised from the statement of financial position. Cash received under repurchase agreements is recognised in the statement of financial position as “Amounts owed to credit institutions”.

Derivative instruments and hedge accounting

The Bank’s derivative instruments are initially recognised on a trade-date basis at fair value in the statement of financial position as “Other assets” or “Other liabilities”.

During the time the Bank holds a derivative instrument, any changes in the fair value of such an instrument are recognised in the statement of comprehensive income, or directly in “Equity” as part of the item “Other value adjustments”, depending on the purpose for which the instruments were acquired. The value changes of derivative instruments that were not acquired for hedging purposes are recognised in the statement of comprehensive income. The accounting treatment for derivative instruments that were acquired for hedging purposes depends on whether the hedging operation was in respect of cash flow or fair value.

At the time the IAS 39 standard concerning hedge accounting was adopted, the Bank had a portfolio of floating rate assets which had been converted to fixed rates using derivative contracts (swaps). This portfolio was designated as a cash flow hedge, but this specific type of hedging is no longer used for new transactions. In general, the Bank does not have an ongoing programme for entering into cash flow hedging, although it may choose to do so at any given point in time.

When hedging future cash flows, the change in fair value of the effective portion of the hedging instrument is recognised directly in “Equity” as part of the item “Other value adjustments” until the maturity of the instrument. At maturity, the amount accumulated in “Equity” is included in the statement of comprehensive income in the same period or periods during which the hedged item affects the statement of comprehensive income.

In order to protect NIB from market risks that arise as an inherent part of its borrowing and lending activities, the Bank enters into swap transactions. The net effect of the swap hedging is to convert the borrowing and lending transactions to floating rates. This hedging activity is an integral part of the Bank’s business process and is a fair value hedge.

When hedging the fair value of a financial asset or liability, the derivative instrument’s change in fair value is recognised in the statement of comprehensive income together with the hedged item’s change in fair value in “Net profit on financial operations”.

Sometimes a derivative may be a component of a hybrid financial instrument that includes both the derivative and a host contract. Such embedded derivative instruments are part of a structured financing transaction that is hedged against changes in fair value by means of matching swap contracts. In such cases, both the hedged borrowing transaction and the hedging derivative instrument are recognised at fair value with changes in fair value in the statement of comprehensive income.

The hedge accounting is based on a clearly documented relationship between the item hedged and the hedging instrument. When there is a high (negative) correlation between the hedging instrument on the one hand and the value change of the hedged item or the cash flows generated by the hedged item on the other, the hedge is regarded as effective. The hedging relationship is documented at the time the hedge transaction is entered into, and the effectiveness of the hedge is assessed continuously.

Determination of fair value

The fair value of financial instruments, including derivative instruments that are traded in a liquid market, is the bid or offered closing price at balance sheet date. Many of NIB’s financial instruments are not traded in a liquid market, such as the Bank’s borrowing transactions with embedded derivative instruments. These are measured at fair value using different valuation models and techniques. This process involves determining future expected cash flows, which can then be discounted to the balance sheet date. The estimation of future cash flows for these instruments is subject to assumptions on market data, and in some cases, in particular where options are involved, even on the behaviour of the Bank’s counterparties. The fair value estimate may therefore be subject to variations and may not be realisable in the market. Under different market assumptions, the values could also differ substantially.

The Bank measures fair values using the following fair value hierarchy that reflects the significance of the inputs used in making the measurements:

Level 1: Quoted market prices (unadjusted) in an active market for identical instruments.

Level 2: Valuation techniques based on observable inputs, either directly (i.e. as prices) or indirectly (i.e. derived from prices). This category includes instruments valued using: quoted market prices in active markets for similar instruments; quoted prices for identical or similar instruments in markets that are considered less than active; or other valuation techniques where all significant inputs are directly or indirectly observable from market data.

Level 3: Valuation techniques using significant unobservable inputs. This category includes all instruments where the valuation technique includes inputs not based on observable data and where the unobservable inputs have a significant effect on the instrument’s valuation. This category includes instruments that are valued based on quoted

prices for similar instruments where significant unobservable adjustments or assumptions are required to reflect differences between the instruments.

See Note 17 for further details.

Equity

As of 31 December 2013, the Bank’s authorised and subscribed capital is EUR 6,141.9 million, of which the paid-in portion is EUR 418.6 million. Payment of the subscribed, non-paid-in portion of the authorised capital, that is, the callable capital, will take place at the request of the Bank’s Board of Directors to the extent that the Board deems it necessary for the fulfilment of the Bank’s debt obligations.

The Bank’s reserves have been built up by means of appropriations from the profits of previous accounting periods, and consist of the Statutory Reserve, as well as the General Credit Risk Fund and the Special Credit Risk Fund for PIL.

The Bank’s profits, after allocation to appropriate credit risk funds, are transferred to the Statutory Reserve until it amounts to 10% of NIB’s subscribed authorised capital. Thereafter, the Board of Governors, upon a proposal by the Bank’s Board of Directors, decides upon the allocation of the profits between the reserve fund and dividends on the subscribed capital.

The General Credit Risk Fund is designed to cover unidentified exceptional risks in the Bank’s operations. Allocations to the Special Credit Risk Fund for PIL are made primarily to cover the Bank’s own risk in respect of credit losses on PIL loans.

Interest

The Bank’s net interest income includes accrued interest on loans, debt securities, placements and accruals of the premium or discount value of financial instruments. Net interest income also includes interest expenses on debts, swap fees and borrowing costs.

Fees and commissions

Fees collected when disbursing loans are recognised as income at the time of the disbursement, which means that fees and commissions are recognised as income at the same time as the costs are incurred. Commitment fees are charged on loans that are agreed but not yet disbursed, and are accrued in the statement of comprehensive income over the commitment period.

Annually recurrent costs arising as a result of the Bank’s borrowing, investment and payment transactions are recognised under the item “Commission expense and fees paid”.

Financial transactions

The Bank recognises in “Net profit on financial operations” both realised and unrealised gains and losses on debt securities and other financial instruments. Adjustments for hedge accounting are included.

Administrative expenses

The Bank provides services to its related parties, the Nordic Development Fund (NDF) and the Nordic Environment Finance Corporation (NEFCO). Payments received by the Bank for providing services at cost to these organisations are recognised as a reduction in the Bank’s administrative expenses. NIB receives a host country reimbursement from the Finnish Government equal to the tax withheld from the salaries of NIB’s employees. This payment reduces the Bank’s administrative expenses, as shown in Note 5.

Leasing agreements

Leasing agreements are classified as operating leases if the rewards and risks incident to ownership of the leased asset, in all major respects, lie with the lessor. Lease payments under operating leases are recognised on a straight- line basis over the lease term. The Bank’s rental agreements are classified as operating leases.

Employee pensions and insurance

The Bank is responsible for arranging pension security for its employees. In accordance with the Host Country Agreement between the Bank and the Finnish Government and as part of the Bank’s pension arrangements, the Bank has decided to apply the Finnish state pension system. Contributions to this pension system, which are paid into the Finnish State Pension Fund, are calculated as a percentage of salaries. The Finnish Ministry of Finance determines the basis for the contributions and establishes the actual percentage of the contributions according to a proposal from the local government pensions institution Keva. See Note 5.

NIB also provides its permanent employees with a supplementary pension insurance scheme arranged by a private pension insurance company. This is group pension insurance based on a defined contribution plan. The Bank’s pension liability is completely covered.

In addition to the applicable local social security systems, NIB has taken out, for example, comprehensive accident, life, medical and disability insurance policies for its employees in the form of group insurance.

Segment information

Segment information and currency distribution in the notes are presented in nominal amounts. The adjustment to hedge accounting is presented as a separate item (except for Note 1, the primary reporting segment).

Reclassifications

Following the amendment to IAS 39 issued in October 2008, permitting the reclassification of financial assets in certain restricted circumstances, the Bank decided to reclassify EUR 715 million of its trading portfolio assets into the held-to-maturity portfolio. This amendment has been applied retrospectively to commence on 1 September 2008. The reclassification has resulted in the cessation of fair value accounting for those assets previously designated as held for trading. The fair values of the assets at the date of reclassification became their new amortised cost, and those assets will subsequently be accounted for on that measurement basis. The reclassified cost will be amortised over the instrument’s expected remaining lifetime through interest income using the effective interest method. See Note 7.

Some other minor reclassifications have been made. The comparative figures have been adjusted accordingly.

INTERNATIONAL FINANCIAL REPORTING STANDARDS AND INTERPRETATIONS

New and amended standards applied in the financial year 2013

Since 1 January 2013, NIB has applied the following new and amended standards that have come into effect. These had no significant impact on the financial statements for the financial year 2013.

| • | | Amendments to IAS 1 Presentation of Financial Statements: The major change is the requirement to group items of other comprehensive income as to whether or not they will be reclassified subsequently to profit or loss when specific conditions are met. The amendments have not had an impact on the presentation of NIB’s other comprehensive income. |

| • | | IFRS 10 Consolidated Financial Statements and subsequent amendments: IFRS 10 builds on existing principles by identifying the concept of control as the determining factor when deciding whether an entity should be incorporated within the consolidated financial statements. The standard also provides additional guidance to assist in the determination of control where this is difficult to assess. The new standard has not had an impact on NIB’s financial statements. |

| • | | IFRS 11 Joint Arrangements and subsequent amendments: In the accounting of joint arrangements, IFRS 11 focuses on the rights and obligations of the arrangement rather than its legal form. There are two types of joint arrangements: joint operations and joint ventures. In future, jointly controlled entities are to be accounted for using only one method, the equity method, and the other alternative of proportional consolidation is no longer allowed. The new standard has not had an impact on NIB’s financial statements. |

| • | | IFRS 12 Disclosures of Interest in other Entities and subsequent amendments. IFRS 12 includes the disclosure requirements for all forms of interests in other entities, including associates, joint arrangements, structured entities and other off-balance sheet vehicles. The new standard has not had an impact on NIB’s financial statements. |

| • | | IFRS 13 Fair Value Measurement: IFRS 13 establishes a single source for all fair value measurements and disclosure requirements for use across IFRSs. The new standard also provides a precise definition of fair value. IFRS 13 does not extend the use of fair value accounting, but it provides guidance on how to measure fair value under IFRSs when fair value is required or permitted. The impact has not been significant. |

| • | | Annual Improvements to IFRSs 2009-2011 (May 2012): The annual improvements process provides a mechanism for minor and non-urgent amendments to IFRSs to be grouped together and issued in one annual package. These amendments cover five standards in total. Their impact has not been significant. |

| • | | Amendments to IFRS 7 Financial Instruments: Disclosures: The amendments clarify disclosure requirements for financial assets and liabilities that are offset in the statement of financial position or subject to master netting arrangements or similar agreements. The amended standard has not had a significant impact on NIB’s financial statements. |

Adoption of new and amended standards and interpretations applicable in future financial years

NIB has not yet adopted the following new and amended standards and interpretations already issued by the IASB. NIB will adopt them as of the effective date or, if the date is other than the first day of the financial year, from the beginning of the subsequent financial year.

| • | | Amendments to IAS 32 Financial Instruments: Presentation (effective for financial years beginning on or after 1 January 2014): The amendments provide clarifications on the application of presentation requirements for offsetting financial assets and financial liabilities on the statement of financial position and give more related application guidance. The amendments are not assessed to have a significant impact on NIB’s financial statements. |

| • | | Amendments to IAS 36 Impairment of Assets (effective for financial years beginning on or after 1 January 2014): The objective of the amendments is to clarify that the scope of the disclosures of information about the recoverable amount of assets, where that amount is based on fair value less costs of disposal, is limited to impaired assets. The amended standard is not assessed to have a significant impact on NIB’s financial statements. |

| • | | Amendments to IAS 39 Financial Instruments: Recognition and Measurement (effective for financial years beginning on or after 1 January 2014): The amendments made to IAS 39 provide an exception to the requirement to discontinue hedge accounting in certain circumstances where a derivative which has been designated as a hedging instrument is novated from one counterparty to a central counterparty as a consequence of laws or regulations. The amendments are not assessed to have an impact on NIB’s financial statements. |

| • | | Annual Improvements to IFRSs (2011-2013 cycle and 2010-2012 cycle, December 2013) (effective for financial years beginning on or after 1 July 2014): The annual improvements process provides a mechanism for minor and non-urgent amendments to IFRSs to be grouped together and issued in one annual package. These amendments cover in total four (2011-2013 cycle) and seven (2010-2012 cycle) standards. Their impacts vary standard by standard but are not significant. |

IFRS 9 Financial Instruments 2013: Introduces new requirements for hedge accounting that align hedge accounting more closely with risk management. The requirements also establish a more principle-based approach to hedge accounting. Amendments dealing with general hedge accounting were issued in November 2013. The unfinished part of IFRS 9, impairment of financial assets, is still a work in progress. Furthermore, the IASB is also considering limited amendments regarding the classification and measurement of financial assets. The macro hedge phase has been taken apart from the IFRS 9 project as a separate project. As the IFRS 9 project is incomplete, the impacts of the standard on the financial statement cannot yet be assessed.

RISK MANAGEMENT

The Bank assumes a conservative approach to risk-taking. Its constituent documents require that loans be made in accordance with sound banking principles, that adequate security be obtained for the loans and that the Bank protect itself against the risk of exchange rate losses. The Bank’s risk tolerance is defined by a set of policies, guidelines and limits taking into account the objective of maintaining strong credit quality, stable earnings and a level of capital required to maintain the AAA/Aaa rating.

The main risks—credit risk, market risk, liquidity risk and operational risk—are managed carefully with risk management closely integrated into the Bank’s business processes. As an international financial institution, the Bank is not subject to national or international banking regulations. However, the Bank’s risk management systems and processes are reviewed on an ongoing basis and adapted to changing conditions with the aim to comply in substance with what the Bank identifies as the relevant market standards and best practices, including the recommendations of the Basel Committee on Banking Supervision.

Key risk responsibilities

The Board of Directors lays down the general framework for the Bank’s risk management by approving its financial policies and guidelines, including maximum limits for exposure to the main types of risk. Credit approval is primarily the responsibility of the Board of Directors. The Board annually grants authorisation to the Bank to raise funds in the capital markets based on its estimated funding requirements.

The President is responsible for managing the risk profile of the Bank within the framework set by the Board of Directors, and for ensuring that the Bank’s aggregate risk is consistent with its financial resources. The Board of Directors has delegated some credit approval authority to the President for execution in the Credit Committee.

To assist and advise the President, the following committees have been established:

The Executive Committee consists of the President and senior officers, whose appointment to the committee has been confirmed by the Board of Directors. The committee is the forum for addressing policy and management issues, including following up the financial results, business plan and strategy of the Bank. The committee meets approximately twice a month.

The Credit Committee consists of the President and senior officers appointed by the Board of Directors. The committee is responsible for preparing and making decisions on credit matters related to the lending operations and for decisions on treasury counterparties. Among other things, the committee reviews all credit proposals before they are submitted to the Board of Directors for approval. The committee meets weekly.

The Finance Committee consists of the President, the Head of Treasury and the Head of Risk and Finance. The committee is responsible for preparing and making decisions on matters related to the treasury operations. The committee makes recommendations, and where appropriate, decisions in the area of market, counterparty and liquidity risk exposure, monitors the Bank’s borrowing activities and has oversight of treasury risk reporting to the Board of Directors. The committee meets monthly.

The Asset and Liability Committee (ALCO) consists of the members of the Executive Committee and the Chief Risk Officer. Together with the Executive Committee, it has the overall responsibility for the Bank’s risk management. ALCO’s duties include monitoring the Bank’s balance sheet development and capital adequacy, setting targets and limits for risk to be managed at the bank level, reviewing liquidity risk management and funding structure, as well as monitoring performance against the agreed risk appetite. The committee meets approximately six times a year.

In the day-to-day management of risks, the Bank has established a segregation of duties between units that enter into business transactions with customers or otherwise expose the Bank to risk on the one hand, and units in charge of risk assessment, risk measurement and control on the other hand. The business units, Lending and Treasury, are responsible for the day-to-day management of all risks assumed through their operations and for ensuring that an adequate return is achieved for the risks taken. These duties are carried out in accordance with guidelines, instructions and limits set for their respective activities.

Risk and Finance, Credit and Analysis, Legal and Compliance and Internal Audit are independent from the departments carrying out the Bank’s business activities.

Risk and Finance has the overall responsibility for measuring, monitoring and reporting on risks across risk types and organisational units. The unit is responsible for the Bank’s risk models and tools, the day-to-day monitoring of market and operational risks and the assessment of risk related to new instruments. The Head of Risk and Finance reports to the President.

Credit and Analysis is responsible for assessing and monitoring credit risk in the Bank’s lending and treasury operations and for overseeing that credit proposals are in compliance with established limits and policies. The unit also manages transactions requiring particular attention due to restructuring work-out and recovery processing. The Head of Credit and Analysis reports to the President.

The Legal department carries the responsibility for minimising and mitigating legal risks in the Bank’s activities. The General Counsel reports to the President.

The Compliance function assists the Bank in identifying, assessing, monitoring and reporting on compliance risk in matters relating to the institution, its operations and to the personal conduct of staff members. The Chief Compliance Officer reports to the President, with full and unlimited access to the Chairman of the Board of Directors and the Chairman of the Control Committee.

Internal Audit provides an independent evaluation of the controls, risk management and governance processes. The Head of Internal Audit reports to the Board of Directors and the Control Committee.

The Control Committee is the Bank’s supervisory body. It ensures that the operations of the Bank are conducted in accordance with the Statutes. The committee is responsible for the audit of the Bank and submits its annual audit report to the Board of Governors.

Credit risk

Credit risk is the Bank’s main financial risk. Credit risk is the risk that the Bank’s borrowers and other counterparties fail to fulfil their contractual obligations and that any collateral held does not cover the Bank’s claims. Following from NIB’s mandate and financial structure, most of the credit risk stems from lending operations. The Bank is also exposed to credit risk in its treasury activities, where credit risk derives from the financial assets, such as fixed-income securities and interbank deposits, that the Bank uses for investing its liquidity, and from derivative instruments used for managing currency and interest rate risks and other market risks related to structured funding transactions.

Credit risk management

Credit risk policies and guidelines

The Bank’s credit policy sets the basic criteria for acceptable credit risks, including the minimum credit quality levels for borrowers and guarantors in lending operations, and identifies risk areas that require special attention. The credit enhancement policy requires that the Bank’s position in a transaction should rank at least equal to that of other senior lenders. The credit enhancement guidelines specify the types of security and contractual undertakings that the Bank deems acceptable to mitigate credit risk. Through a set of key clauses for the loan documentation, the Bank strives to ensure that it will receive early warning if the credit quality of a borrower deteriorates or if an event occurs that could have an adverse effect on a borrower’s ability to repay the loan. The portfolio policy aims to ensure adequate diversification of credit risk across counterparties, countries and industry sectors. Based on the policies set by the Board of Directors, specific guidelines and instructions have been implemented as a basis for the business and control processes and procedures.

Credit risk assessment

Credit risk assessment is an important part of the credit process. Credit and Analysis independently assesses the creditworthiness of borrowers and treasury counterparties. The assessment is qualitative and quantitative and based on internal rating methodologies supported by scoring models. The assessment results in a risk rating denoting the probability of default of the counterparty.

The credit enhancement in a transaction is assessed separately and a loss-given-default (LGD) is determined for the transaction as an estimate of the portion of the Bank’s claim that would not be recoverable if the counterparty defaults. The combination of the probability of default of the counterparty and the LGD quantifies the expected loss for the transaction. The Bank applies a rating scale ranging from 1 to 20, with class 1 representing the lowest probability of default and expected loss. In addition, the rating scale includes a class D for non-performing transactions or transactions for which specific impairment provisions have been made. The rating scale is mapped to the ratings of Standard & Poor’s and Moody’s such that classes 1 to 10 correspond to the external rating equivalent of investment grade (AAA to BBB- and Aaa to Baa3, respectively).

Credit risk limits

The primary source of credit risk is the individual counterparty, and the secondary source is the potential default correlation of groups of counterparties and sectors. Exposure limits are set at both counterparty and portfolio levels. Counterparty limits are determined based on the probability of default and expected loss. To reduce risk concentration, the Bank applies portfolio-level limits for large counterparty exposure as well as for sector and country exposures. The limits are scaled to the Bank’s equity, the counterparty’s equity, the size of the total credit exposure and the Bank’s economic capital. As a general principle, the Bank limits the maximum amount granted as loan or guarantee for a single project to 50% of the total project cost.

Credit risk monitoring

The Bank works continuously to review the quality of its credit exposures. Strong emphasis is put on regularly monitoring the creditworthiness of the counterparties in the Bank’s lending and treasury operations. The monitoring frequency is determined based on, among other things, the ratings and the size and type of exposure. Generally, intensified follow-up applies to counterparties with internal ratings below the level eligible for new exposure or other defined levels. When serious deterioration of a counterparty’s debt repayment capacity and/or financial standing is identified, the counterparty is transferred to the watch list and placed under close monitoring with regular reporting to the Board of Directors.

Compliance with existing limits is monitored regularly, for treasury counterparties limit compliance is monitored on a daily basis.

Portfolio-level measurement and monitoring of credit risk is carried out within the Bank’s economic capital framework. Economic capital is the Bank’s estimate of the capital required to cover unexpected losses deriving from credit risk, market risk and operational risk. As the Bank is not subject to regulatory capital requirements, the economic capital is used for internal monitoring to ensure that the Bank has sufficient capital to fulfil its commitments. The portfolio approach provides a more comprehensive assessment of the Bank’s aggregate credit risk as it captures the impact of concentration and diversification in the Bank’s operations. A report on the Bank’s economic capital and risk profile is submitted to the Board of Directors every four months. The report includes an analysis of the capital required, the aggregate credit risk exposure, credit risk concentrations, changes in the risk profile and exposure against portfolio risk limits with any breaches of limits explained.

Derivatives

The Bank uses derivatives as part of its funding strategy in order to match the interest rate and currency characteristics of the funds raised with those of loans granted and to reduce funding costs. In liquidity management, derivatives are used to mitigate interest rate risk. Derivatives are transacted under normal counterparty limits.

As a rule, NIB enters into International Swaps and Derivatives Association (ISDA) contracts with swap counterparties. This allows the netting of the obligations arising under all of the derivative contracts covered by the ISDA agreement in case of insolvency and, thus, results in one single net claim on, or payable to, the counterparty. Netting is applied for the measurement of the Bank’s credit exposure only in cases when it is deemed to be legally enforceable in the relevant jurisdiction and against a counterparty. The gross total market value of swaps at year-end 2013 amounted to EUR 1,480 million, compared to a market value of EUR 651 million after applying netting (year-end 2012: EUR 2,568 million and EUR 1,951 million, respectively).

The credit risk on swaps is further mitigated through credit support agreements with the Bank’s major swap counterparties. Under these agreements, swap exposures exceeding agreed thresholds are collateralised by cash or high-quality government securities. Both the swap portfolio with individual counterparties and the collateral received are regularly monitored and valued, with a subsequent call for additional collateral or release. The Bank largely uses unilateral credit support agreements under which the Bank does not have to post collateral. At year-end 2013, the Bank held EUR 601 million (2012: EUR 1,783 million) in gross collateral received, of which EUR 283 million (2012: EUR 1,464 million) was in cash and EUR 318 million (2012: EUR 319 million) in securities (Note 16, Collateral and Commitments).

Credit risk reserves, impairment methodology

The Bank maintains two credit risk funds within its equity, in addition to the Statutory Reserve. The General Credit Risk Fund is available to cover unexpected losses arising from the Bank’s lending and other business activities. At year-end 2013 the fund amounted to EUR 1,113 million before allocation of the profit for the year. The Statutes require that the Bank maintains the Special Credit Risk Fund for the Project Investment Loan (PIL) facility to cover the Bank’s own risk on such loans before resorting to the member countries’ guarantees that support the facility. At year-end 2013, the fund amounted to EUR 396 million.

At least every four months the Bank reviews the possible need for impairment provisions on weak exposures. The assessment is carried out both at the level of the individual counterparty and collectively for groups of counterparties.

At the counterparty level, a specific impairment provision is recognised if there is objective evidence that the counterparty’s capacity to fulfil its obligations has deteriorated to the extent that full repayment is unlikely when taking into consideration any collateral received. Collective impairment provisions are determined on a portfolio basis for exposures with similar credit risk characteristics as reflected in their risk ratings. The process includes management’s judgement based on the current macroeconomic environment and the current view of the expected economic outlook. In the Bank’s view, the assumptions and estimates made represent an appropriate level of conservatism and are reflective of the predicted economic conditions, the Bank’s portfolio characteristics and their correlation with losses incurred based on historical loss experience. In the assessment of sovereign exposures, the Bank takes into account its preferred creditor status. The Bank’s principles for impairment provisioning are described in more detail in the section Significant accounting policies.

Credit risk exposure

Tables 1 to 3 below provide an overview of the Bank’s aggregate credit risk exposure at year-end 2013 distributed according to expected loss (EL) before collective impairment. Aggregate credit exposure comprises lending and treasury exposure. Lending exposure includes loans outstanding and loans agreed but not yet disbursed, without taking into account any collateral or other credit enhancement. Regarding the treasury exposure, capital market investments are included at nominal value, while derivatives are included at market value net of collateral held when credit support agreements are in place, and at market value with an add-on for potential future exposure when not under credit support agreement. The exposure to collateralised placements is calculated as a fixed percentage of the market value of the collateral held.

TABLE 1. Credit risk exposure by internal rating (in EUR million)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Risk class (EL) | | S&P

equivalent | | Lending | | | 31.12.2013 Treasury | | | Total | | | Lending | | | 31.12.2012 Treasury | | | Total | |

1–2 | | AAA/AA+ | | | 2,417 | | | | 3,577 | | | | 5,994 | | | | 2,277 | | | | 4,966 | | | | 7,243 | |

3–4 | | AA/AA- | | | 831 | | | | 1,605 | | | | 2,436 | | | | 1,014 | | | | 1,455 | | | | 2,469 | |

5–6 | | A+/A | | | 1,307 | | | | 853 | | | | 2,160 | | | | 1,147 | | | | 1,044 | | | | 2,191 | |

7–8 | | A-/BBB+ | | | 4,398 | | | | 86 | | | | 4,484 | | | | 5,112 | | | | 207 | | | | 5,319 | |

9–10 | | BBB/BBB- | | | 4,099 | | | | 24 | | | | 4,123 | | | | 3,912 | | | | 85 | | | | 3,997 | |