Exhibit 13.1

2007 ANNUAL REPORT

2007 Annual Report

Table of Contents

Letter to Stockholders | 2 |

| |

5-Year Performance Comparison | 3 |

| |

Financial Highlights | 4 |

| |

Management’s Discussion | 6-17 |

| |

Consolidated Balance Sheets | 19 |

| |

Consolidated Statements of Income | 20 |

| |

Consolidated Statements of Cash Flows | 21 |

| |

Consolidated Statements of Changes in Stockholders’ Equity | 22 |

| |

Notes to Consolidated Financial Statements | 23-50 |

| |

Report of Independent Auditors | 51-52 |

| |

Corporate Information | 53 |

| |

Bancorp and Subsidiaries Consolidating Balance Sheet | 54 |

| |

Bancorp Directors | 55 |

| |

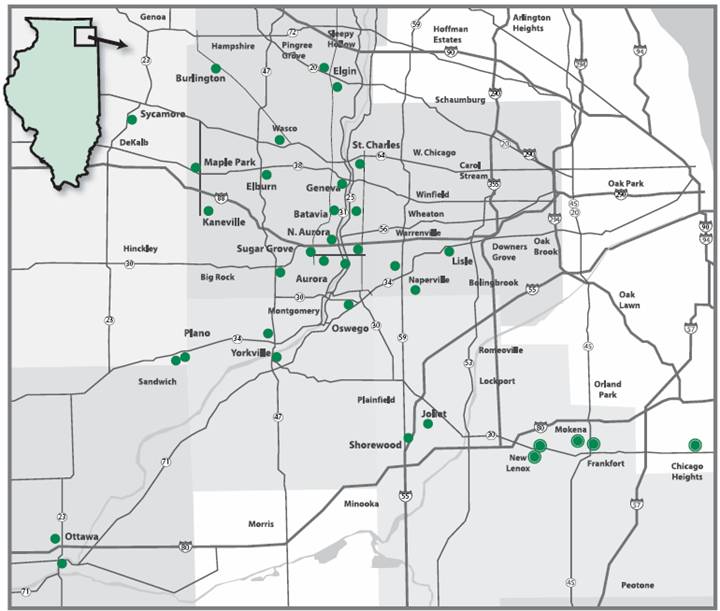

Old Second Locations Map | 56 |

1

2007 Year End Letter to Stockholders

The year 2007 was a challenging year for the entire banking industry.

Despite the difficult economic climate, Old Second Bancorp, Inc., had a number of very positive results, especially when compared to others in the banking industry. Net income was $24.0 million, up slightly from the prior year’s income of $23.7 million, Earnings per share were $1.89 compared to $1.75 in 2006, an 8% increase, and our return on equity was 16.13% versus 15.29% in 2006.

Real estate markets and the economy were soft and slowed considerably in the second half of 2007. Despite these demanding market conditions, our net charge-offs were only 0.03% of loans, or $546,000, which compares very favorably to the rest of the industry.

We recognized a slow down in margin growth and earnings early in 2007 and undertook a number of cost saving initiatives that helped to improve the bottom line. These initiatives included headcount reductions of 8.5%, the elimination of our separate charters, merging of the mortgage company into the bank, closing three branches, centralizing operations and implementing other improvements that led to efficiencies.

Also, as part of capital management, we issued $25 million in trust preferred securities and used the proceeds to buy back our stock.

On November 5, 2007, the company entered into an agreement to acquire HeritageBanc, Inc. On February 8, 2008, we closed this acquisition and now have expanded our footprint into Will and Southern Cook counties. These new areas provide us with great growth opportunities and give us branches in the majority of top growth markets in northern Illinois. With this acquisition, we now have 35 branches and over $3 billion in assets. We also continue to have the #1 market share in Kane and Kendall counties and have expanded our presence in the Elgin and Joliet/Plainfield markets.

One of the brighter areas in 2007 was our wealth management group, which had assets grow to $1.2 billion while our revenue generated by that group grew from $8.3 million to $9.6 million, or an increase of $1.3 million (+ 16%) over the prior year.

We continue to grow our commercial lending group and have made some good additions to that area with a stronger emphasis on commercial and industrial lending.

On the retail side, our emphasis on sales and service helped us to attain 6,638 new checking accounts and increase our banking households to 56,300. Our “right-size” strategy of offering the best of what large banks offer with the quality and service offered by smaller banks continues to be very effective and I believe is what makes us the “bank of choice” in all of our major markets.

We expect economic and market conditions to continue to be a challenge in 2008. Real estate markets will likely stay soft and may not improve until later in 2008 and competition in our markets will remain very intense.

2

However, I remain optimistic about our performance relative to our peers. We believe that the strong demographics in our markets should allow us to experience growth levels above most other areas and should allow us to rebound faster than these other areas.

Our employees continue to be our #1 asset and strength. I am very encouraged by their efforts and attitudes and would like to especially thank them, especially in these trying times.

I would also like to thank our Directors for their guidance, our stockholders for their belief in us and our customers for their continued dedication.

| | |

|

William B. Skoglund Chairman |

5-Year Performance Comparison

Date | | Old Second

Bancorp | | NASDAQ

Bank Index | | S&P 500 | |

December 2002 | | $ | 100.00 | | $ | 100.00 | | $ | 100.00 | |

December 2003 | | $ | 136.31 | | $ | 133.01 | | $ | 128.63 | |

December 2004 | | $ | 178.49 | | $ | 151.12 | | $ | 142.59 | |

December 2005 | | $ | 174.09 | | $ | 148.22 | | $ | 149.58 | |

December 2006 | | $ | 169.87 | | $ | 168.65 | | $ | 173.15 | |

December 2007 | | $ | 158.62 | | $ | 135.14 | | $ | 182.64 | |

3

Old Second Bancorp, Inc. and Subsidiaries

Financial Highlights

(In thousands, except share data)

| | 2007 | | 2006 | | 2005 | | 2004 | | 2003 | |

Balance sheet items at year-end | | | | | | | | | | | |

Total assets | | $ | 2,658,576 | | $ | 2,459,140 | | $ | 2,367,830 | | $ | 2,105,019 | | $ | 1,839,689 | |

Loans, gross | | 1,891,110 | | 1,763,912 | | 1,704,382 | | 1,509,076 | | 1,319,538 | |

Deposits | | 2,113,618 | | 2,062,693 | | 1,935,278 | | 1,798,849 | | 1,524,634 | |

Securities sold under agreement to repurchase | | 53,222 | | 38,218 | | 57,625 | | 45,242 | | 47,848 | |

Federal funds purchased | | 165,100 | | 54,000 | | 170,000 | | 49,000 | | 102,700 | |

Other short-term borrowings | | 82,873 | | 73,090 | | 1,825 | | 26,786 | | 3,346 | |

Junior subordinated debentures | | 57,399 | | 31,625 | | 31,625 | | 31,625 | | 31,625 | |

Note payable | | 18,610 | | 16,425 | | 3,200 | | 2,700 | | 500 | |

Stockholders’ equity before other comprehensive income (loss) | | 147,918 | | 161,100 | | 156,824 | | 134,664 | | 113,989 | |

Stockholders’ equity | | 149,889 | | 158,555 | | 152,262 | | 134,988 | | 116,994 | |

| | | | | | | | | | | |

Results of operations for the year ended | | | | | | | | | | | |

Net interest and dividend income | | $ | 68,598 | | $ | 71,199 | | $ | 73,999 | | $ | 68,359 | | $ | 62,376 | |

Provision for loan losses | | 1,188 | | 1,244 | | 353 | | (2,900 | ) | 3,251 | |

Net income | | 23,972 | | 23,656 | | 27,683 | | 26,287 | | 22,108 | |

| | | | | | | | | | | |

Per share data | | | | | | | | | | | |

Basic earnings | | $ | 1.92 | | $ | 1.77 | | $ | 2.05 | | $ | 1.96 | | $ | 1.57 | |

Diluted earnings | | 1.89 | | 1.75 | | 2.03 | | 1.94 | | 1.56 | |

Dividends declared | | 0.59 | | 0.55 | | 0.51 | | 0.46 | | 0.40 | |

Stockholders’ equity as of December 31 | | 12.34 | | 12.08 | | 11.26 | | 10.06 | | 8.74 | |

| | | | | | | | | | | |

Weighted average diluted shares outstanding | | 12,655,306 | | 13,526,603 | | 13,661,024 | | 13,535,881 | | 14,198,908 | |

Weighted average basic shares outstanding | | 12,508,551 | | 13,367,062 | | 13,486,598 | | 13,413,263 | | 14,096,244 | |

Shares outstanding at year-end | | 12,149,296 | | 13,127,292 | | 13,520,073 | | 13,424,346 | | 13,387,480 | |

Note: On June 15, 2004, the board of directors declared a 2-for-1 stock split effected in the form of a stock dividend payable on July 28, 2004 to stockholders of record on July 16, 2004. All references to the number of common shares and per share amounts have been restated as appropriate to reflect the effect of the stock splits for all periods presented.

4

Old Second Bancorp, Inc.

and Subsidiaries

Management’s Discussion

and Analysis of Financial Condition

and Results of Operations

5

Old Second Bancorp, Inc. and Subsidiaries

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Overview

The following discussion provides additional information regarding the Company’s operations for the twelve-month periods ending December 31, 2007, 2006, and 2005, and financial condition at December 31, 2007 and 2006. This discussion should be read in conjunction with “Selected Consolidated Financial Data” and the Company’s consolidated financial statements and the accompanying notes thereto included or incorporated by reference elsewhere in this document.

Old Second Bancorp, Inc. is a financial services company with its main headquarters located in Aurora, Illinois. The consolidated financial statements include Old Second Bancorp, Inc. and its wholly-owned subsidiaries, which are together referred to as the “Company”:

· Old Second National Bank (“the Bank”).

· Old Second Financial, Inc., which provides insurance agency services.

· Old Second Capital Trust I, which was formed for the exclusive purpose of issuing trust preferred securities in an offering that was completed in July 2003. Old Second Capital Trust I is an unconsolidated subsidiary of the Company. See Notes A and J to the consolidated financial statements for further discussion.

· Old Second Capital Trust II, which was formed for the exclusive purpose of issuing trust preferred securities in an offering that was completed in April 2007. Old Second Capital Trust II is also an unconsolidated subsidiary of the Company and additional information is available in the notes cited above.

· Old Second Affordable Housing Fund, L.L.C., which was formed for the purpose of providing down payment assistance for home ownership to qualified individuals.

· Old Second Management, LLC (“OSM”), which was formed for the purpose of providing a possible future source of capital as well as providing certain tax advantages. Old Second Bank owns 100% of the common stock of OSM. Old Second Realty, LLC (“OSR”) is a Delaware real estate investment trust and 100% of the common stock of OSR is owned by OSM. As of January 2, 2007, there were various minority holders of preferred stock in OSR.

· Old Second Acquisition, Inc., which was formed as part of the November 5, 2007 Agreement and Plan of Merger between the Company, Old Second Acquisition, Inc., a wholly-owned subsidiary of the Company, and HeritageBanc, Inc. (“Heritage”). The parties consummated the merger on February 8, 2008, at which time, Old Second Acquisition, Inc. was merged with and into Heritage with Heritage as the surviving corporation as a wholly-owned subsidiary of the Company. Additionally, the parties merged Heritage Bank, a wholly- owned subsidiary of Heritage, with and into Old Second National Bank, with Old Second National Bank as the surviving bank. After the completion of the merger transaction, Heritage was dissolved and is no longer an existing subsidiary.

Inter-company transactions and balances are eliminated in consolidation. The results discussed in this document do not include any operations of Heritage as that transaction closed in 2008.

The Company provides financial services through its thirty- five banking locations located in Cook, Kane, Kendall, DeKalb, DuPage, LaSalle and Will counties in Illinois. One new location was opened on the western edge of Elgin in May 2007. With the February 2008 Heritage acquisition, the Company expanded its franchise into southwestern Cook County and the desirable, higher growth markets of the south Chicago suburbs by adding six additional banking locations. This allowed the Company to fill in its footprint surrounding the Chicago metropolitan area. With the application of relationship focused banking strategies, the Company expects to provide the new client base with wealth management services, and expanded mortgage, treasury and retail services that Old Second Bank is able to offer in addition to traditional loan and deposit products. The Company paid consideration of $43.0 million in cash and 1,563,636 shares of the Company’s stock valued at $27.50 per share to consummate the acquisition on February 8, 2008. The final terms of the credit facilities established with LaSalle Bank to complete the acquisition are detailed in Note J. Additional organizational changes that occurred during 2007 are also detailed in Note A.

Our primary deposit products are checking, NOW, money market, savings, and certificate of deposit accounts, and the Company’s primary lending products are commercial mortgages, construction lending, commercial and industrial loans, residential mortgages and installment loans. Major portions of the Company’s loans are secured by various forms of collateral including real estate, business assets, and consumer property while borrower cash flow is the primary source of repayment. The Bank also engages in trust operations.

The Company recorded net income of $24.0 million or $1.89 diluted earnings per share in 2007, which compares with

6

earnings of $23.7 million or $1.75 per diluted share in 2006, and $27.7 million, or $2.03 per diluted share in 2005. Basic earnings per share were $1.92 in 2007, $1.77 in 2006, and $2.05 in 2005. In 2007, balance sheet growth in earning assets, an increase in noninterest income, a reduction in provision for income taxes, and a decrease in advertising and other expenses combined to offset a lower net interest margin and increased personnel and occupancy costs. Earnings also improved in 2007 due to reduced expense from nonrecurring 2006 categories such as loss on settlement of pension obligation, and amortization of core deposit intangible assets, net of a $1.0 million adjustment, which reduced interest expense from short-term borrowings. The May 2007 repurchase of 973,251 shares of common stock reduced the shares outstanding, which also increased earnings per share. The provision for loan losses for 2007 substantially equaled the 2006 expense of $1.2 million with no fourth quarter addition recorded in either period.

Net interest income declined $2.6 million (3.7%) to $68.6 million in 2007, compared to a decrease of $2.8 million (3.8%) to $71.2 million in 2006. Even though there was an increase in earning assets in both years, the growth in earning assets in 2007 continued to be offset by a lower net interest margin. Average earning assets grew $136.6 million or 6.2% in 2007. Despite that growth, the net interest margin (tax equivalent basis) was 3.05% in 2007 and 3.34% in 2006. Year-end total assets were $2.66 billion as of December 31, 2007, an increase of $199.4 million (8.1%) from $2.46 billion as of December 31, 2006. Average assets were $2.52 billion, $2.38 billion, and $2.24 billion in 2007, 2006, and 2005, respectively.

Application of critical accounting policies

The Company’s consolidated financial statements are prepared in accordance with United States generally accepted accounting principles and follow general practices within the banking industry. Application of these principles requires management to make estimates, assumptions, and judgments that affect the amounts reported in the consolidated financial statements and accompanying notes. These estimates, assumptions, and judgments are based on information available as of the date of the consolidated financial statements. Future changes in information may affect these estimates, assumptions, and judgments; which, in turn, may affect amounts reported in the consolidated financial statements.

All significant accounting policies are presented in Note A to the consolidated financial statements. These policies, along with the disclosures presented in the other financial statement notes and in this discussion, provide information on how significant assets and liabilities are valued in the financial statements and on how those values are determined.

Management has determined that the Company’s accounting policies with respect to the allowance for loan losses is the accounting area requiring subjective or complex judgments that is most important to the Company’s financial position and results of operations, and therefore, is the Company’s only critical accounting policy. The allowance for loan losses represents management’s estimate of probable credit losses inherent in the loan portfolio. Determining the amount of the allowance for loan losses is considered a critical accounting estimate because it requires significant judgment and the use of estimates related to the amount and timing of expected future cash flows on impaired loans, estimated losses on pools of homogeneous loans based on historical loss experience, and consideration of current economic trends and conditions, all of which may be susceptible to significant change. The loan portfolio also represents the largest asset type on the consolidated balance sheet. The allowance for loan losses is a valuation allowance for credit losses, increased by the provision for loan losses and decreased by charge-offs less recoveries. Management estimates the allowance balance required using an assessment of various risk factors including, but not limited to, past loan loss experience, known and inherent risks in the portfolio, information about specific borrower situations and estimated collateral values, volume trends in delinquencies and nonaccruals, economic conditions, and other factors. Allocations of the allowance may be made for specific loans, but the entire allowance is available for losses inherent in the loan portfolio. A loan is considered impaired when it is probable that not all contractual principal or interest due will be received according to the original terms of the loan agreement. Management defines the measured value of an impaired loan based upon the present value of the future cash flows, discounted at the loan’s original effective interest rate, or the fair value of underlying collateral, if the loan is collateral dependent. Impaired loans at December 31, 2007 and 2006 were $25.8 million and $9.2 million respectively. In addition, a discussion of the factors driving changes in the amount of the allowance for loan losses is included in the Provision for Loan Losses section that follows.

Results of operations

Net interest income

Net interest income is the difference between interest income earned on earning assets and interest expense paid on interest bearing liabilities. As such, net interest income is affected by changes in the volume and yields on earning assets and the volume and rates paid on interest bearing liabilities. Net interest margin is the ratio of tax-equivalent net interest income to average earning assets. Decreases in net interest income during this period were primarily the result of the increase in the cost of funds exceeding the increase in the yield on earning assets. Even though the average tax- equivalent yield on earning assets increased 22 basis points from 6.45% in 2006, to 6.67% in 2007, the cost of funds on interest bearing liabilities increased 54 basis points from 3.62%, to 4.16% in the same period. The average net interest margin (tax equivalent) was 3.05%, 3.34%, and 3.64% in 2007, 2006, and 2005, respectively.

Net interest income was $68.6 million in 2007, $71.2 million in 2006, and $74.0 million in 2005. Average earning assets

7

were $2.36 billion in 2007, an increase of $136.6 million, or 6.2%, from $2.22 billion in 2006. Average earning assets were $2.11 billion in 2005. Average portfolio loans increased $76.9 million, or 4.4%, from $1.75 billion in 2006 to $1.83 billion in 2007. During 2006, average portfolio loans increased $130.8 million, or 8.1%, from $1.62 billion in 2005, to $1.75 billion in 2006. Average interest bearing liabilities were $2.09 billion in 2007, an increase of $140.7 million, or 7.2%, in 2006. Average interest bearing liabilities were $1.95 billion in 2006, an increase of $127.7 million, or 7.0%, from $1.82 billion in 2005. In 2006, management recorded an adjustment to interest expense on other short-term borrowings of $961,000 due to a reduction in estimate for accrued interest payable. Approximately $528,000 of this reduction related to 2006.

Changes in deposit funding composition also continued to have the effect of increasing interest costs and lowering the net interest margin in 2007. The average balances of lower- cost sources of funds such as interest-bearing transaction accounts and savings accounts declined $8.7 million, or 3.3%, and $12.1 million, or 10.6%, respectively, from December 31, 2006 to December 31, 2007. At the same time, noninterest-bearing deposits increased by a nominal amount while higher-cost sources of funds such as money market and time deposits increased $84.0 million, or 20.2% and $38.3 million, or 4.0%, respectively. Non-deposit funding costs also increased significantly in 2007 primarily due to the increase in average balances that occurred across all borrowing categories with the largest increase in the overnight borrowing category of federal funds purchased.

Given the Company’s mix of negatively gapped interest earning assets and interest bearing liabilities at December 31, 2006, the net interest margin was susceptible to a decrease in 2007, which exhibited a generally static rate environment during most of the year. The first half of year 2007 was also characterized by an inverted yield curve whereby shorter-term rates were higher than longer-term rates. The Federal Open Market Committee (“FOMC”) began to decrease the target for the Federal Funds rate by announcing a 50 basis points reduction on September 18, which was followed by two successive 25 basis point decreases on October 31 and December 11, 2007. These decreases lowered the target rate from 5.25% at January 1, 2007 to 4.25% at December 31, 2007. In 2007, the Bank’s prime rate decreased in correlation with the Federal Funds rate, moving from 8.25% on January 1, 2007 to 7.25% as of December 31, 2007. Increasing interest costs associated with generating continued deposit growth and other sources of funds in 2007 contributed to a decline in the net interest margin. Since the Company continued to be liability sensitive at December 31, 2007, it was generally positioned to benefit from interest rate decreases including the recent announcements of 75 and 50 basis points cuts on January 22 and 31, 2008 respectively. The Company’s liability sensitive position was somewhat reduced however, with the February 8, 2008 acquisition of Heritage.

Provision for loan losses

The Company recorded a $1.2 million provision for loan losses in both 2007 and 2006 with no provision in the fourth quarter of either year. The provision for loan losses was $353,000 in 2005. Provisions for loan losses are made to provide for probable and estimable losses inherent in the loan portfolio. Nonperforming loans increased to $6.0 million at December 31, 2007 from $2.2 million at December 31, 2006 and were $6.6 million at December 31, 2005. The increase in nonperforming loans in 2007 was primarily due to the addition of four real estate construction loans and one adjustable rate mortgage loan that were added in the fourth quarter, and a residential home equity loan that was added in the third quarter. The advance ratios of balances outstanding to the estimated collateral value for the fourth quarter loan additions are sufficient under the Company’s established credit review policies. The Company is in a first lien position on the home equity loan. All five of the nonperforming loan relationships identified in the fourth quarter were placed on nonaccrual status. Even with the current developments in the loan portfolio, management determined that no additional provision was required in the fourth quarter of 2007. In large part, this is because management had observed slower real estate building and development activity in the Company’s market areas during 2006. Even though the Company’s borrowers generally continued to meet their obligations during 2006, management believed that the general risk in this sector was greater than before, and increased the provision for loan losses despite a decrease in nonperforming loans. Management acted upon its growing concern with the general commercial real estate market, as well as the large concentration of commercial real estate loans held by the Company and increased its qualitative risk factors for this sector starting in 2006.

The ratio of the allowance for loan losses to nonperforming loans was 281.95% as of December 31, 2007, compared with 731.06% as of December 31, 2006 and 232.36% at December 31, 2005. Nonperforming loans are defined as non-accrual loans, restructured loans, and loans past due ninety days or more and still accruing interest. Net charge-offs in 2007, 2006 and 2005 were $546,000, $380,000, and $519,000, respectively. When compared with total loans, net charge-offs as a percentage of total average loans were 0.03%, 0.02%, and 0.03% in 2007, 2006, and 2005. The loan portfolio continues to represent the largest asset on the Consolidated Balance Sheets. When measured as a percentage of loans outstanding, the allowance for loan losses was 0.89% as of December 31, 2007 and 0.92% at December 31, 2006.

The allowance for loan losses consists of three components: (i) specific allocations established for losses resulting from an analysis developed through reviews of individual loans for which the recorded investment in the loan exceeds the measured value of the loan; (ii) reserves based on historical loss experience for each loan category; and (iii) reserves based on general current economic conditions as well as specific economic and other factors believed to be relevant to the Company’s loan portfolio. Management evaluates the

8

sufficiency of the allowance for loan loss based on the combined total of each of these components. The components of the allowance for loan losses represent an estimation done pursuant to Statement of Accounting Standard (“SFAS”) 5, Accounting for Contingencies, and SFAS 114, Accounting by Creditors for Impairment of a Loan; and SFAS 118 which amends several provisions of SFAS 114.

Specific allocations

Management reviews on a quarterly basis certain loans on nonaccrual, loans over 90 days past due, troubled debt restructurings or any loans considered doubtful or loss. The individual loan officers analyze these loans with the results reported to the Loan Review Committee on a Credit Management Report. From that report, management determines the amount of specific allocations by reviewing, on a credit-by credit basis, all loans considered impaired under SFAS 114 as amended by SFAS 118 as well as all problem and watch loans. SFAS 114 defines impaired loans as loans where, based on current information and events, it is probable that a creditor may be unable to collect all amounts due according to the original contractual terms of the loan agreement.

A problem loan is defined by the Company’s loan policy as “A credit that is inadequately protected by the current sound worth and paying capacity of the borrower or of the collateral pledged, if any. Loans so classified have a well-defined weakness that jeopardizes the liquidation of the debt. These loans are characterized by the distinct possibility that the Bank will sustain some loss if the deficiencies are not corrected. Loss potential, while existing in the aggregate amount of substandard loans, does not have to exist in individual loans classified”.

Specific allocations are discussed at the quarterly watch list meeting. The Vice President of Loan Review chairs this meeting. The committee consists of the Company’s President, Regional Senior Vice Presidents, the Executive Vice President of Credit & Chief Risk Officer, and other senior lenders who are members of the loan committee.

As of December 31, 2007, the Company had eighteen nonaccrual loans totaling $5.3 million with a specific allocation of $136,000 for those loans. The Company has no specific allocations for restructured or past due loans included in the allowance. As of December 31, 2006, the Company had fourteen nonaccrual loans totaling $1.6 million with a specific allocation of $133,000 for those loans. As of December 31, 2005, the Company had eleven nonaccrual loans totaling $3.8 million with an allocation of $476,000 for those loans. Impaired loans at December 31, 2007, 2006, and 2005 were $25.8 million, $9.2 million, and $8.5 million, respectively. The 2007 increase in impaired loans was primarily due to the third quarter addition of one commercial real estate borrowing relationship that has a specific allocation of approximately $763,000.

Historical reserves and management allocations

The component of the allowance for loan losses based on historical loan loss experience is determined using historical charge-off data for the last five years, with more weight placed on the most recent years. This calculation is done quarterly. Management considers a variety of factors to determine the appropriate level of allowance for inherent loan losses including but not limited to, past loan loss experience, known and inherent risks in the portfolio, information about specific borrower situations and estimated collateral values, volume trends in delinquencies and nonaccruals, economic conditions, and other factors. Allocations of the allowance may be made for specific loans, but the entire allowance is available for losses inherent in the loan portfolio. Beginning in 2006, the large concentration of commercial real estate loans held by the Company and management’s observation of slower building and development activity in the commercial real estate sector were specific considerations in determining the factors used to estimate the allowance for loan loss. All factors are considered on a quarterly basis and are adjusted when appropriate. In addition, various regulatory agencies, as an integral part of their examination process, periodically review the Company’s allowance for loan losses. Such agencies may require the Company to make additional provisions to the allowance based on their judgments about information available to them at the time of their examination.

The general component of the allowance recognizes probable inherent, but undetected, losses in the loan portfolio. Regardless of how management analyzes customer performance, ratings migration, economic conditions and interest rate risk, management believes there are additional potential risks that are unaccounted for in the process of making loans. This is due to several factors including, but not limited to:

· Timing delays in receiving information regarding a customer’s financial condition;

· Changes in individual business climates;

· The judgmental nature of individual loan evaluations and collateral assessments; and

· The open interpretation of economic trends.

The analysis of these factors involves a high degree of judgment by management. Because of the imprecision surrounding these factors, the bank estimates a range of inherent losses and maintains a general allowance that is not allocated to a specific category.

Historically, the Company has had minimal credit losses. The current allowance is weighted heavily toward the real estate portfolio due to its size in relation to the other portions of our portfolio. Starting in 2006, the Company made some reallocations in our reserves based on the review of the portfolio, the current economic conditions and the credit quality of the portfolio. While there can be no assurance that the allowance for loan losses will be adequate to cover all

9

losses, management believed that the allowance for loan losses was adequate at December 31, 2007.

Noninterest income

Noninterest income was $31.9 million for the year 2007, an increase of $3.1 million, or 11.0%, as compared to 2006. The increase in noninterest income in 2007 was primarily the result of increased income from trust department and mortgage banking operations. Noninterest income was $28.7 million in 2006 compared to $28.1 million in 2005.

Trust income was $8.7 million in the year 2007, an increase of $1.1 million, or 14.1%, from 2006 due principally to increased volume in estate administration activity coupled with an increase in assets under management. Assets under management were $1.1 billion, $1.0 billion, and $959.5 million at December 31, 2007, 2006, and 2005, respectively. Trust income increased to $7.6 million in 2006, an increase of $951,000, or 14.3%, from $6.6 million in 2005. Trust income has increased generally over all three periods due to greater volumes in both assets under management and estate administration activities. Assets under management increased in large part because of successful new business development activities.

Service charges on deposits were $8.6 million in 2007, an increase of $224,000, or 2.7%, from $8.3 million in 2006, primarily due to increased volumes from overdraft protection service fees. Service charges on deposits were $8.3 million in 2005. Mortgage banking income, including net gain on sales of mortgage loans, secondary market fees, and servicing income was $5.6 million in 2007, an increase of $751,000, or 15.5%, from $4.9 million in 2006. The largest increase in income from mortgage operations was in net gain on sales of mortgage loans, which resulted largely from a significant revision to secondary market execution processes. Mortgage banking income is largely volume-driven and mortgage activity is susceptible to changes in interest rates and general economic conditions. Mortgage-related noninterest income, principally gains on sales of mortgage loans, totaled $6.7 million in 2005. Loans sold were $232.4 million in 2007, $288.8 million in 2006, and $396.7 million in 2005. Originations in 2007 decreased as the decline in mortgage rates, which would typically spur an increase in refinancing activity, did not begin until late in 2007. Similarly, the decrease in originations in 2006 was primarily the result of rising mortgage rates during the first half of 2006, which decreased demand for mortgages.

Gains on sales of securities in 2007 were $674,000, an increase of $256,000, or 61.2%, as compared with $418,000 for 2006. There was a $14,000 loss recorded in 2005. Bank owned life insurance (“BOLI”) income decreased $41,000, or 2.0%, from $2.1 million to $2.0 million in 2007, due in large part to the decreasing interest rates available on the underlying insurance investments. BOLI income was $985,000 in 2005, but the Company purchased $20.0 million of BOLI during the fourth quarter of 2005, which substantially increased income in this category in 2006.

Interchange income from debit card usage was $2.0 million in 2007, an increase of $226,000, or 12.7%, from $1.8 million in 2006. The Company continued to increase the number of cards outstanding in 2007 because of successful cross-selling and other marketing efforts, and as customers continued to show a preference for this form of payment. Debit card interchange income was $1.5 million in 2005. Other income increased $661,000, or 18.1%, to $4.3 million in 2007, from $3.7 million in 2006. The comparative improvement in 2007 performance was primarily due to increased levels of fee income from processing of merchant credit card sales combined with annuity sales, mutual fund and letter of credit fees. Other income decreased to $3.7 million in 2006 from $4.0 million in 2005, principally due to a decrease in letter of credit fees in 2006.

Noninterest expense

Noninterest expense was $66.5 million during 2007, an increase of $1.3 million, or 2.1%, from $65.1 million in the prior year. Noninterest expense totaled $60.5 million in 2005. The efficiency ratio was 64.1%, 63.3%, and 57.6% for December 31, 2007, 2006, and 2005, respectively. This ratio measures noninterest expense as a percentage of the sum of net tax-equivalent interest income plus noninterest income. Because a financial institution’s largest noninterest expense is generally the cost of salary and benefits, management of this cost has a significant impact on efficiency. In 2007, salaries and benefits were $38.1 million compared to $35.9 million in 2006, an increase of $2.2 million or 6.2%. The increase in expense was primarily due to increases in bonus expense and profit sharing accruals as well as increases in mortgage and brokerage commissions coupled with increases in stock compensation and health insurance costs. The Company generally experiences increases in this category due to annual increases in salary and other compensation coupled with rising health care costs, but an evaluation of 2007 events is also required to understand current year fluctuations. The full time equivalent employee (“FTE”) figure decreased from 582 at December 31, 2006 to 541 at December 31, 2007. The FTE tally was smaller at December 31, 2007 primarily because of the 8.5% reduction in available positions that was announced April 13, 2007. Despite a reduction in workforce, there were overall increases in salaries and benefits as the Company shifted toward a performance based pay structure by placing emphasis upon commissions and bonus remuneration. The Company expects that the move away from the defined benefit pension plan that was settled in 2006 to the enhanced 401K and profit sharing structure will provide further opportunity to align individual performance with Company goals.

For 2006, salaries and benefits were $35.9 million compared to $35.6 million in 2005, and the nominal increase of $233,000 or 0.7% was due in large part to a decrease in accrued management bonus expense in 2006. The full time equivalent employee count increased from 548 at December 31, 2005 to 582 at December 31, 2006, primarily due to the increased staffing requirements at the five new banking locations opened in 2006.

10

Occupancy expenses were $5.4 million in 2007, $4.6 million in 2006, and $3.7 million in 2005. Furniture and equipment expenses were $6.4 million in 2007, $5.3 million in 2006, and $5.1 million in 2005. In 2007, net occupancy and furniture and equipment expenses increased $1.9 million, or 19.7%, from 2006. That increase was primarily attributable to the combined effect of the Company’s expansion and development into new markets, network and system integration costs from the bank charter consolidation, and third and fourth quarter 2007 recognition of accelerated leasehold depreciation and other associated impaired asset expense. The latter items resulted primarily from the July 2007 closing of three leased branches that had market overlap with existing locations. The bulk of future savings from these closures will begin in the first quarter of 2008 as two of the leases have now terminated. The expiration dates changed to December 31, 2007 and February 23, 2008 as the Company negotiated an accelerated exit from an original expiry date of March 31, 2009 at one of the closed locations while maintaining automated teller machine services at that site. The Company opened five new retail locations in 2006 and a new location on the western edge of Elgin in May 2007 and began the process of relocating a loan production office late in 2007 that will be completed in the first quarter of 2008. In 2006, net occupancy and furniture and equipment expense increased $1.1 million, or 12.5% from 2005. As mentioned previously, the Company expanded its market presence in 2006, which also increased the related facility expenses and was the primary cause of this increase.

Significant decreases in advertising expense were realized in 2007 in comparison to both 2006 and 2005. Other expense also decreased $525,000, or 3.4%, from $15.5 million in 2006 to $15.0 million in 2007, as the Company continued to emphasize cost control and review procedures. Lower expense levels were recorded in several categories, with some of the largest reductions in other employee related expenditures such as recruitment and travel as well as decreased audit fees. Other expenses had increased $1.5 million, or 10.8%, from $14.0 million in 2005, to $15.5 million in 2006. The increases in 2006 were primarily due to costs associated with the amortization and valuation of mortgage servicing rights, increased audit and compliance including ongoing compliance with Sarbanes-Oxley mandates, loan production related expenditures, rising costs associated with automatic teller machine operations and new employee recruitment fees.

Income taxes

The Company’s provisions for Federal and State of Illinois income taxes were $8.8 million, $9.9 million, and $13.6 million during the years ended December 31, 2007, 2006, and 2005. The effective income tax rates for these years were 26.9%, 29.4%, and 33.0%. Increased levels of tax-exempt income from securities helped to reduce income tax expense when comparing 2007 to 2006. In addition to the increased volume of tax-exempt assets, the average tax-equivalent yield on tax-exempt securities held by the Company increased from 5.47% as of December 31, 2006 to 5.98% or 51 basis points as of December 31, 2007. The reduction in effective tax rate in the latter two years was primarily attributable, however, to the formation of a real estate investment trust (REIT) in the fourth quarter of 2006. The REIT holds certain commercial real estate loans, and other real estate loans that were previously held by our main bank subsidiary. In addition to income tax benefits, which lowered the effective tax rate, the REIT ownership structure also provides the Company with an alternate vehicle for raising future capital as desired. A late 2007 change to Illinois tax law related to the deductibility of REIT dividends will eliminate the recognition of a substantial portion of the tax benefits related to this ownership structure beginning January 1, 2009.

Financial condition

Total assets were $2.66 billion as of December 31, 2007, an increase of $199.4 million, or 8.1%, from $2.46 billion as of December 31, 2006. The most significant growth in assets was in loans, which were $1.89 billion as of December 31, 2007, an increase of $127.2 million, or 7.2%, from $1.76 billion as of December 31, 2006. Total deposits increased $50.9 million, or 2.5%, during 2007. The largest increase in funding, however, was in federal funds purchased which grew $111.1 million, or 205.7%, to $165.1 million at December 31, 2007. Junior subordinated debentures also increased to $57.4 million, an increase of $25.8 million, or 81.5%, from $31.6 million at December 31, 2006.

Investments

Securities available for sale increased $88.0 million during 2007, from $472.9 million as of December 31, 2006, to $560.9 million as of December 31, 2007. At December 31, 2007, U.S. government agency securities and mortgage-backed agency securities were $210.6 million and $96.9 million respectively. The Company decreased its position in agency securities by $56.6 million, or 21.2%, as of December 31, 2007 while it simultaneously increased mortgage-backed agency securities by $77.3 million, or 394.2%. U.S. government agency securities comprised 37.5% of the portfolio as of December 31, 2007, and 56.5% of the portfolio as of December 31, 2006 whereas the mortgage-backed agency securities represented 17.3% and 4.1% of the investment portfolio as of the same dates. As of December 31, 2007, the Company held $73.9 million in collateralized mortgage obligations versus $26.7 million a year earlier. Mortgage-backed agency securities and collateralized mortgage obligations generally offered a higher rate of return during 2007. At December 31, 2007, state and political subdivision securities were $159.8 million, an increase of $10.1 million, or 6.8%, from $149.6 million a year earlier. State and political subdivision securities comprised 28.5% of the portfolio as of December 31, 2007, compared to 31.6% of the portfolio as of December 31, 2006. The net unrealized gains in the portfolio were $3.3 million at December 31, 2007 as compared to net unrealized losses of $4.2 million as of December 31, 2006, primarily due to changes in interest rates.

11

Loans

Total loans were $1.89 billion as of December 31, 2007, an increase of $127.2 million, or 7.2%, from $1.76 billion as of December 31, 2006. The largest increase was in residential real estate loans, which rose $47.3 million, or 8.1%, since December 31, 2006. Commercial real estate and construction and development loans increased $28.8 million and $24.4 million, respectively, since December 31, 2006. The loan portfolio generally reflects the economic profile of the communities in which the Company operates. Because the Company is located in markets with open areas for growth, real estate lending (including commercial, residential, and construction) comprises a significant portion of the portfolio. These categories comprised 88.1% of the portfolio as of December 31, 2007 compared to 88.7% of the portfolio as of December 31, 2006. The commercial and industrial loan sector also increased $21.5 million, or 12.2%, to $197.1 million at December 31, 2007, from $175.6 million at December 31, 2006. At the same time, installment loans increased $5.0 million, or 21.5%, to $28.4 million from $23.3 at December 31, 2006. The 2007 loan growth was substantially from within the Company’s market area including a nominal amount of participations purchased. The Company does not have any material direct exposure to sub prime loan products, as it has focused real estate lending on commercial real estate and construction and development loans, as well as on traditional loan products to residential borrowers.

The provision for loan losses was $1.2 million in both 2007 and 2006, respectively. As discussed in the Provision for Loan Losses section above, management identified a growing concern with the commercial real estate market generally, and the large concentration of commercial real estate loans held by the Company starting in 2006. These factors contributed to the increase in the provision for 2006 compared to 2005, in spite of the decline in nonperforming loans.

One measure of the adequacy of the allowance for loan losses is the ratio of the allowance to total loans. The allowance for loan losses as a percentage of total loans was 0.89% as of December 31, 2007, compared to 0.92% as of December 31, 2006. In management’s judgment, an adequate allowance for estimated losses has been established; however, there can be no assurance that losses will not exceed the estimated amounts in the future.

Management, along with many other financial institutions, remains cautious about the current economic environment and outlook. Furthermore, a sustained slowdown in the real estate market could adversely affect consumer confidence and collateral values. These events adversely affect cash flows generally for both commercial and individual borrowers, and as a result, the Company could experience increases in problem assets, delinquencies, and losses on loans in future periods.

Sources of funds

One of the Company’s primary sources of funds is customer deposits. Total deposits increased $50.9 million, or 2.5%, during 2007 to $2.11 billion as of December 31, 2007. Noninterest-bearing deposits decreased $9.1 million, or 3.2%, while NOW and savings deposits decreased $10.2 million, or 4.0%, and $7.8 million, or 7.5%, respectively. At the same time, money market accounts increased $59.5 million, or 13.3%. In 2007, time deposits increased $18.6 million, or 1.9%. The 2007 growth in money market accounts resulted from depositor preference for liquidity and check accessibility not offered in a traditional savings account and particularly as time deposit rates decreased in the fourth quarter. The balances in all borrowing categories increased with the largest increase in federal funds purchased and junior subordinated debentures. The former category increased to fund investment and loan portfolio growth, whereas the $25.8 subordinated debenture issuance served to provide the primary source of financing for the common stock tender offer that was completed in May 2007. The changes in deposit composition combined with increases in other borrowed funds as well as a generally higher cost of funds during most of 2007 adversely affected the net interest margin.

The Company also utilizes securities sold under repurchase agreements as a source of funds. These repurchase agreements, which are typically of short-term duration, were $53.2 million at December 31, 2007, which was an increase of $15.0 million, or 39.3%. As mentioned previously, the largest increase in funding was in the overnight federal funds purchased category, which grew to $165.1 million at December 31, 2007. The federal funds market is an efficient source of funds that generally reprices immediately in a declining rate environment. Other short-term borrowings increased by $9.8 million, or 13.4% to $82.9 million from $73.1 million. The note payable balance outstanding increased $2.2 million, or 13.3% to $18.6 million as of December 31, 2007 compared to $16.4 million as of December 31, 2006. A primary purpose of this note was to fund repurchases of the Company’s stock in 2006 whereas the 2007 increase related primarily to operating needs. Repurchased shares can be reissued from treasury stock as a future capital source or to fulfill employee related stock compensation plans, the interim repurchase of shares also enhanced return on equity and both the book value and earnings per share. Junior subordinated debentures increased $25.8 million, or 81.5%, to $57.4 million at December 31, 2007. The Company issued the new subordinated debenture in return for the aggregate net proceeds of a trust-preferred offering that occurred in April 2007. Those proceeds provided the primary source of financing for the common stock tender offer that was subsequently completed in May 2007. The Company is currently maintaining liquid assets and delivering consistent growth in core funding to provide funding for loan growth. Additional information on the final terms of the credit facilities that were established with LaSalle Bank to fund the February 8, 2008 acquisition of Heritage are detailed in Note J.

12

Capital

Total stockholders’ equity decreased $8.7 million, or 5.5%, to $149.9 million during 2007, from $158.6 million as of December 31, 2006. Net income of $24.0 million, reduced by dividends of $7.3 million, increased retained earnings to $209.9 million as of December 31, 2007. In the same year, a $4.5 million change to a net unrealized securities gain position from a $2.5 million net unrealized securities loss position at December 31, 2006 also increased stockholders’ equity. In 2006 retained earnings increased by net income of $23.7 million, less dividends of $7.3 million. During 2006, a $2.0 million decrease in unrealized net securities losses increased stockholders’ equity.

The Company repurchased 1,038,251 shares in 2007, resulting in an increase in treasury stock to 4,545,479 shares as of December 31, 2007. The repurchase of these shares increased treasury stock by $31.2 million, or 49.2%, to $94.8 million at December 31, 2007, from $63.5 million at December 31, 2006. While treasury stock decreased stockholders equity, it also increased earnings per share by reducing the number of shares outstanding. Return on average equity was 16.13%, 15.29%, and 19.11% in 2007, 2006, and 2005, respectively.

The exercise of stock options, related tax benefit, and stock-based compensation expense contributed $1.4 million to stockholders’ equity in 2007, and $1.1 million to stockholders’ equity in 2006.

The Company completed a sale of $31.6 million of cumulative trust preferred securities by its subsidiary, Old Second Capital Trust I (Nasdaq: OSBCP) in 2003. The trust preferred securities remain outstanding for a 30-year term, but subject to regulatory approval, they can be called in whole or in part at the Company’s discretion after an initial five-year period. Dividends are payable quarterly at an annual rate of 7.80% and are included in interest expense in the consolidated financial statements. The Company issued an additional $25.0 million of cumulative trust preferred securities through a private placement completed by its new unconsolidated subsidiary, Old Second Capital Trust II (“the Trust”) in April 2007. These trust preferred securities also mature in 30 years, but subject to the aforementioned regulatory approval, can be called in whole or in part on a quarterly basis commencing June 15, 2017. The quarterly cash distributions on the securities are fixed at 6.766% through June 15, 2017 and float at 150 basis points over the British Bankers Association three-month LIBOR rate thereafter. Trust preferred proceeds of $30.8 million and $49.3 million are held by outside investors and qualified as Tier 1 regulatory capital as of December 31, 2006 and 2007, respectively. An additional $6.5 million of Trust preferred proceeds qualified as Tier 2 regulatory capital as of December 31, 2007.

Bank regulatory agencies have adopted capital standards by which all banks and bank holding companies are evaluated. The Bank was also categorized as well capitalized as of both December 31, 2007 and 2006. Additional information regarding capital levels and minimum required levels can be found in Note R to the financial statements. Additional information related to the amount and form of consideration paid to consummate the February 8, 2008 acquisition of Heritage is outlined in Note X.

Quantitative and qualitative disclosure about market risk

Liquidity and market risk

Liquidity is the Company’s ability to fund operations, to meet depositor withdrawals, to provide for customer’s credit needs, and to meet maturing obligations and existing commitments. The liquidity of the Company principally depends on cash flows from operating activities, investment in and maturity of assets, changes in balances of deposits and borrowings, and its ability to borrow funds.

Net cash inflows from operations were $13.9 million during 2007. Net cash outflows from investing activities were $214.6 million in 2007, primarily as a result of $127.7 million in net principal disbursed on loans. Net cash outflows relating to securities available for sale were $79.4 million as a result of cash inflows of $214.3 million for the maturity and sale of securities available for sale, offset by cash outflows of $293.6 million for the purchases of securities available for sale. Net cash inflows from financing activities were $176.9 million in 2007, which included a net increase in deposits of $50.9 million and increases in securities sold under agreement to purchase, federal funds purchased, and proceeds from subordinated debentures of $15.0 million, $111.1 million and $25.8 million respectively. As mentioned previously the 2007 net increase of $2.2 million in note payable and $25.8 million of debenture proceeds were used primarily to repurchase the Company’s treasury shares.

Management of investing and financing activities along with market conditions determine the level and the stability of net interest cash flows. Management’s policy is to mitigate the impact of changes in market interest rates to the extent possible, so that balance sheet growth is the principal determinant of growth in net interest cash flows.

Net cash inflows from operations were $38.2 million during 2006. Net cash outflows from investing activities were $71.7 million in 2006, primarily as a result of $59.9 million in net principal disbursed on loans. Net cash outflows relating to securities available for sale were $1.2 million as a result of cash inflows of $169.1 million for the maturity and sale of securities available for sale, offset by cash outflows of $170.3 million for the purchases of securities available for sale. Net cash inflows from financing activities were $57.0 million in 2006, which included a net increase in deposits of $127.4 million and decreases in short-term borrowings, which includes federal funds purchased, and repurchase agreements sold of $44.7 million and $19.4 million respectively. The proceeds of $13.2 million from the note payable were used primarily to repurchase the Company’s treasury shares.

13

Net cash inflows from operations were $31.1 million during 2005. Net cash outflows from investing activities were $264.2 million in 2005, as a result of $196.1 million in net principal disbursed on loans. Net cash outflows relating to securities available for sale were $36.1 million as a result of cash inflows of $158.4 million for the maturity and sale of securities available for sale, offset by cash outflows of $194.5 million for the purchases of securities available for sale. Net cash inflows from financing activities were $239.5 million in 2005, which included a net increase in deposits of $136.4 million and an increase in short-term borrowings and federal funds and securities sold under repurchase agreements of $108.4 million.

Interest rate risk

The impact of movements in general market interest rates on a financial institution’s financial condition, including capital adequacy, earnings, and liquidity, is known as interest rate risk. Interest rate risk is the Company’s primary market risk. As a financial institution, accepting and managing this risk is an inherent aspect of the Company’s business. However, safe and sound management of interest rate risk requires that it be maintained at prudent levels.

The Company seeks to achieve consistent growth in net interest income and net income while managing volatility that arises from shifts in interest rates. The Bank’s Asset and Liability Management Committee (“ALCO”) oversees financial risk management by developing programs to measure and manage interest rate risks within authorized limits set by the Bank’s Board of Directors. ALCO also approves the Bank’s asset/liability management policies, oversees the formulation and implementation of strategies to improve balance sheet positioning and earnings, and reviews the Bank’s interest rate sensitivity position. Management uses net interest income simulation modeling tools to analyze and capture near-term and longer-term interest rate exposures.

The Company analyzes interest rate risk by examining the extent to which assets and liabilities are interest rate sensitive. The interest sensitivity gap is defined as the difference between the amount of interest earning assets maturing or repricing within a specific time period and the amount of interest-bearing liabilities maturing or repricing within that time period. A gap is considered positive when the amount of interest sensitive assets exceeds the amount of interest sensitive liabilities. A gap is considered negative when the amount of interest sensitive liabilities exceeds the amount of interest sensitive assets. During a period of rising interest rates, a negative gap would tend to result in a decrease in net interest income while a positive gap would tend to increase net interest income. The Company’s policy is to manage the balance sheet such that fluctuations in the net interest margin are minimized regardless of the level of interest rates.

The table on page 15 illustrates expected maturities and does not necessarily indicate the future impact of general interest rate movements on the Company’s net interest income because the repricing of certain assets and liabilities is discretionary and is subject to competitive and other pressures. As a result, assets and liabilities indicated as repricing within the same period may in fact reprice at different times and at different rate levels. Assets and liabilities are reported in the earliest time frame in which maturity or repricing may occur. Although securities available for sale are reported in the earliest period in which maturity or repricing may occur, these securities may be sold in response to changes in interest rates or liquidity needs.

The Company is also exposed to interest rate risk on loans held for sale and rate lock commitments as discussed in Note S.

Effects of inflation

In management’s opinion, changes in interest rates affect the financial condition of a financial institution to a far greater degree than changes in the inflation rate. While interest rates are greatly influenced by changes in the inflation rate, they do not change at the same rate or in the same magnitude as the inflation rate. Rather, interest rate volatility is based on changes in the expected rate of inflation, as well as on changes in monetary and fiscal policies. A financial institution’s ability to be relatively unaffected by changes in interest rates is a good indicator of its capability to perform in today’s volatile economic environment. The Company seeks to insulate itself from interest rate volatility by ensuring that rate sensitive assets and rate sensitive liabilities respond to changes in interest rates in a similar time frame and to a similar degree.

14

Expected Maturity of Interest-Earning Assets and Interest-Bearing Liabilities at December 31:

| | Expected Maturity Dates | |

| | 1 Year | | 2 Years | | 3 Years | | 4 Years | | 5 Years | | Thereafter | | Total | |

2007 Interest-earning Assets | | | | | | | | | | | | | | | |

Deposits with financial institutions | | $ | 403 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 403 | |

Average interest rate | | 3.54 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 3.54 | % |

Federal funds sold | | $ | 2,370 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 2,370 | |

Average interest rate | | 3.65 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 3.65 | % |

Securities (including FHLB/FRB stock) | | $ | 73,611 | | $ | 23,094 | | $ | 29,558 | | $ | 23,154 | | $ | 22,264 | | $ | 398,125 | | $ | 569,806 | |

Average interest rate | | 3.60 | % | 4.37 | % | 4.72 | % | 4.72 | % | 4.84 | % | 4.88 | % | 4.67 | % |

Fixed rate loans (including loans held for sale) | | $ | 174,078 | | $ | 112,190 | | $ | 200,723 | | $ | 154,861 | | $ | 219,906 | | $ | 178,201 | | $ | 1,039,959 | |

Average interest rate | | 6.49 | % | 6.21 | % | 6.29 | % | 6.99 | % | 6.96 | % | 6.67 | % | 6.67 | % |

Adjustable rate loans | | $ | 326,539 | | $ | 82,920 | | $ | 17,616 | | $ | 4,318 | | $ | 36,098 | | $ | 400,337 | | $ | 867,828 | |

Average interest rate | | 7.58 | % | 7.33 | % | 7.33 | % | 7.26 | % | 7.09 | % | 6.36 | % | 6.97 | % |

Total | | $ | 577,001 | | $ | 218,204 | | $ | 247,897 | | $ | 182,333 | | $ | 278,268 | | $ | 976,663 | | $ | 2,480,366 | |

| | | | | | | | | | | | | | | |

Interest-bearing Liabilities | | | | | | | | | | | | | | | |

Interest-bearing deposits | | $ | 1,505,178 | | $ | 38,848 | | $ | 26,588 | | $ | 10,918 | | $ | 6,540 | | $ | 253,997 | | $ | 1,842,069 | |

Average interest rate | | 4.27 | % | 4.36 | % | 4.48 | % | 4.96 | % | 4.66 | % | 1.38 | % | 3.88 | % |

Federal funds purchased | | $ | 165,100 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 165,100 | |

Average interest rate | | 4.09 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 4.09 | % |

Short-term borrowings | | $ | 136,095 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 136,095 | |

Average interest rate | | 3.60 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 3.60 | % |

Note payable | | $ | 18,610 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 18,610 | |

Average interest rate | | 6.14 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 6.14 | % |

Junior subordinated debentures | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 57,399 | | $ | 57,399 | |

Average interest rate | | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 7.34 | % | 7.34 | % |

Total | | $ | 1,824,983 | | $ | 38,848 | | $ | 26,588 | | $ | 10,918 | | $ | 6,540 | | $ | 311,396 | | $ | 2,219,273 | |

Period gap | | $ | (1,247,982 | ) | $ | 179,356 | | $ | 221,309 | | $ | 171,415 | | $ | 271,728 | | $ | 665,267 | | $ | 261,093 | |

Cumulative gap | | (1,247,982 | ) | (1,068,626 | ) | (847,317 | ) | (675,902 | ) | (404,174 | ) | 261,093 | | | |

| | | | | | | | | | | | | | | |

2006 Interest-earning Assets | | | | | | | | | | | | | | | |

Deposits with financial institutions | | $ | 5,493 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 5,493 | |

Average interest rate | | 5.08 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 5.08 | % |

Federal funds sold | | $ | 2,305 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 2,305 | |

Average interest rate | | 5.13 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 5.13 | % |

Securities (including FHLB/FRB stock) | | $ | 71,069 | | $ | 78,281 | | $ | 22,679 | | $ | 37,005 | | $ | 15,070 | | $ | 257,576 | | $ | 481,680 | |

Average interest rate | | 3.61 | % | 3.81 | % | 4.36 | % | 4.53 | % | 4.37 | % | 4.47 | % | 4.23 | % |

Fixed rate loans (including loans held for sale) | | $ | 123,697 | | $ | 139,001 | | $ | 118,012 | | $ | 216,625 | | $ | 163,927 | | $ | 125,577 | | $ | 886,839 | |

Average interest rate | | 7.06 | % | 6.11 | % | 6.08 | % | 6.21 | % | 7.01 | % | 6.46 | % | 6.48 | % |

Adjustable rate loans | | $ | 357,478 | | $ | 68,338 | | $ | 20,381 | | $ | 6,946 | | $ | 5,457 | | $ | 432,851 | | $ | 891,451 | |

Average interest rate | | 8.52 | % | 8.07 | % | 7.94 | % | 8.10 | % | 8.14 | % | 6.48 | % | 7.48 | % |

Total | | $ | 560,042 | | $ | 285,620 | | $ | 161,072 | | $ | 260,576 | | $ | 184,454 | | $ | 816,004 | | $ | 2,267,768 | |

| | | | | | | | | | | | | | | |

Interest-bearing Liabilities | | | | | | | | | | | | | | | |

Interest-bearing deposits | | $ | 1,267,640 | | $ | 180,957 | | $ | 28,554 | | $ | 24,173 | | $ | 10,602 | | $ | 270,137 | | $ | 1,782,063 | |

Average interest rate | | 4.17 | % | 4.60 | % | 4.53 | % | 4.60 | % | 4.96 | % | 1.47 | % | 3.82 | % |

Federal funds purchased | | $ | 54,000 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 54,000 | |

Average interest rate | | 5.30 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 5.30 | % |

Short-term borrowings | | $ | 111,308 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 111,308 | |

Average interest rate | | 5.06 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 5.06 | % |

Note payable | | $ | 16,425 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 16,425 | |

Average interest rate | | 6.50 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 6.50 | % |

Junior subordinated debentures | | $ | — | | $ | 31,625 | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 31,625 | |

Average interest rate | | 0.00 | % | 7.80 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 7.80 | % |

Total | | $ | 1,449,373 | | $ | 212,582 | | $ | 28,554 | | $ | 24,173 | | $ | 10,602 | | $ | 270,137 | | $ | 1,995,421 | |

Period gap | | $ | (889,331 | ) | $ | 73,038 | | $ | 132,518 | | $ | 236,403 | | $ | 173,852 | | $ | 545,867 | | $ | 272,347 | |

Cumulative gap | | (889,331 | ) | (816,293 | ) | (683,775 | ) | (447,372 | ) | (273,520 | ) | 272,347 | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

15

Off-balance sheet arrangements

Contractual Obligations, Commitments, Contingent Liabilities, and Off-Balance Sheet Arrangements

The Company has various financial obligations that may require future cash payments. The following table presents, as of December 31, 2007, significant fixed and determinable contractual obligations to third parties by payment date.

| | Within

One Year | | One to

Three Years | | Three to

Five Years | | Over

Five Years | | Total | |

Deposits without a stated maturity | | $ | 1,120,914 | | $ | — | | $ | — | | $ | — | | $ | 1,120,914 | |

Certificates of deposit | | 909,810 | | 65,435 | | 17,459 | | — | | 992,704 | |

Securities sold under repurchase agreements | | 53,222 | | — | | — | | — | | 53,222 | |

Federal funds purchased | | 165,100 | | — | | — | | — | | 165,100 | |

Other short-term borrowings | | 82,873 | | — | | — | | — | | 82,873 | |

Junior subordinated debentures | | — | | — | | — | | 57,399 | | 57,399 | |

Note payable | | 18,610 | | — | | — | | — | | 18,610 | |

Purchase obligations | | 2,518 | | 1,553 | | 19 | | 1 | | 4,091 | |

Operating leases | | 584 | | 355 | | 114 | | — | | 1,053 | |

Nonqualified voluntary deferred compensation | | 123 | | 862 | | 556 | | 681 | | 2,222 | |

Total | | $ | 2,353,754 | | $ | 68,205 | | $ | 18,148 | | $ | 58,081 | | $ | 2,498,188 | |

Purchase obligations represent obligations under agreements to purchase goods or services that are enforceable and legally binding on the Company and that specify all significant terms, including: fixed or minimum quantities to be purchased; fixed, minimum or variable price provisions; and the approximate timing of the transaction. The purchase obligation amounts presented above primarily relate to certain contractual payments for services provided for information technology, capital expenditures, and the outsourcing of certain operational activities.

Commitments: The following table details the amounts and expected maturities of significant commitments to extend credit as of December 31, 2007:

| | Within

One Year | | One to

Three Years | | Three to

Five Years | | Over

Five Years | | Total | |

Commitment to extend credit: | | | | | | | | | | | |

Commercial secured by real estate | | $ | 71,416 | | $ | 20,218 | | $ | 14,242 | | $ | 4,608 | | $ | 110,484 | |

Revolving open end residential | | 2,127 | | 1,992 | | 17,097 | | 109,043 | | 130,259 | |

Other | | 108,905 | | 4,308 | | 379 | | 1,199 | | 114,791 | |

Financial standby letters of credit | | 18,012 | | 1,267 | | — | | — | | 19,279 | |

Performance standby letters of credit | | 24,917 | | 3,539 | | 710 | | — | | 29,166 | |

Commercial letters of credit | | 1,236 | | — | | 11,307 | | — | | 12,543 | |

Total | | $ | 226,613 | | $ | 31,324 | | $ | 43,735 | | $ | 114,850 | | $ | 416,522 | |

Controls and procedures

The Chief Executive Officer and Chief Financial Officer have evaluated the effectiveness of the design and operation of the Company’s disclosure controls and procedures, as defined in Rule 13a-15(e) promulgated under the Securities and Exchange Act of 1934, as amended, as of December 31, 2007. Based on that evaluation, the Chief Executive Officer and Chief Financial Officer concluded that as of December 31, 2007 the Company’s disclosure controls and procedures are effective to ensure that information required to be disclosed by the Company is appropriately recorded, processed, summarized and reported.

Special note concerning forward-looking statements

This document (including information incorporated by reference) contains, and future oral and written statements of the Company and its management may contain, forward-looking statements, within the meaning of such term in the Private Securities Litigation Reform Act of 1995, with respect to the financial condition, results of operations, plans, objectives, future performance and business of the Company. Forward-looking statements, which may be based upon beliefs, expectations and assumptions of the Company’s management and on information currently available to

16

management, are generally identifiable by the use of words such as “believe,” “expect,” “anticipate,” “plan,” “intend,” “estimate,” “may,” “will,” “would,” “could,” “should” or other similar expressions. Additionally, all statements in this document, including forward-looking statements, speak only as of the date they are made, and the Company undertakes no obligation to update any statement in light of new information or future events.

The Company’s ability to predict results or the actual effect of future plans or strategies is inherently uncertain. Factors that could have a material adverse effect on the operations and future prospects of the Company and its subsidiaries include, but are not limited to, those set forth under item 1.A “Risk Factors” of the Form 10-K and as set forth below:

· The strength of the United States economy in general and the strength of the local economies in which the Company conducts its operations which may be less favorable than expected and may result in, among other things, a deterioration in the credit quality and value of the Company’s assets.

· Credit risks and the risks from concentrations (by geographic area and by industry) within the Company’s loan portfolio.

· The economic impact of past and any future terrorists attacks, acts of war or threats thereof and the response of the United States to any such threats and attacks.

· The effects of, and changes in, federal, state and local laws, regulations and policies affecting banking, securities, insurance and monetary and financial matters.

· The effects of changes in interest rates (including the effects of changes in the rate of prepayments of the Company’s assets) and the policies of the Board of Governors of the Federal Reserve System.

· The ability of the Company to compete with other financial institutions as effectively as the Company currently intends due to increases in competitive pressures in the financial services sector.

· The inability of the Company to obtain new customers and to retain existing customers.

· The timely development and acceptance of products and services, including products and services offered through alternative delivery channels such as the Internet.

· Technological changes implemented by the Company and by other parties, including third party vendors, which may be more difficult or more expensive than anticipated or which may have unforeseen consequences to the Company and its customers.

· The ability of the Company to develop and maintain secure and reliable electronic systems.

· The ability of the Company to retain key executives and employees and the difficulty that the Company may experience in replacing key executives and employees in an effective manner.

· Consumer spending and saving habits which may change in a manner that affects the Company’s business adversely.

· Business combinations and the integration of acquired businesses, which may be more difficult or expensive than expected.

· The costs, effects and outcomes of existing or future litigation.

· Changes in accounting policies and practices, as may be adopted by state and federal regulatory agencies and the Financial Accounting Standards Board, the Public Company Accounting Oversight Board, and the Securities and Exchange Commission.

· If our Real Estate Investment Trust (REIT) affiliate fails to qualify as a REIT, we may be subject to a higher consolidated effective tax rate. Old Second National Bank holds certain commercial real estate loans, residential real estate loans and other loans, and mortgage-backed investment securities in a real estate investment trust through its wholly owned subsidiary Old Second Management, LLC which is domiciled in Delaware. Qualification as a REIT involves application of specific provisions of the Internal Revenue Code relating to various asset, income, and investment tests. If the REIT fails to meet any of the required provisions for REITs, or there are changes in tax laws or interpretation thereof, it could no longer qualify as a REIT and the resulting tax consequences would increase our effective tax rate or cause us to have a tax liability for prior years. As noted previously, a late 2007 change to Illinois tax law related to the deductibility of REIT dividends will eliminate the recognition of a large portion of the tax benefits related to this ownership structure beginning January 1, 2009.

· The ability of the Company to manage the risks associated with the foregoing as well as anticipated.

These risks and uncertainties should be considered in evaluating forward-looking statements and undue reliance should not be placed on such statements.

17

Old Second Bancorp, Inc.

and Subsidiaries

Consolidated Statements

& Notes to Consolidated

Financial Statements

18

Old Second Bancorp, Inc. and Subsidiaries

Consolidated Balance Sheets

December 31, 2007 and 2006

(In thousands, except share data)

| | 2007 | | 2006 | |

Assets | | | | | |

Cash and due from banks | | $ | 60,804 | | $ | 80,727 | |

Interest bearing deposits with financial institutions | | 403 | | 5,493 | |

Federal funds sold | | 2,370 | | 2,305 | |

Short-term securities available for sale | | 1,162 | | — | |

Cash and cash equivalents | | 64,739 | | 88,525 | |

Securities available for sale | | 559,697 | | 472,897 | |

Federal Home Loan Bank and Federal Reserve Bank stock | | 8,947 | | 8,783 | |

Loans held for sale | | 16,677 | | 14,378 | |

Loans | | 1,891,110 | | 1,763,912 | |

Less: allowance for loan losses | | 16,835 | | 16,193 | |

Net loans | | 1,874,275 | | 1,747,719 | |

Premises and equipment, net | | 49,698 | | 48,404 | |

Other real estate owned | | — | | 48 | |

Mortgage servicing rights, net | | 2,482 | | 2,882 | |

Goodwill, net | | 2,130 | | 2,130 | |

Bank owned life insurance (BOLI) | | 47,936 | | 45,861 | |

Accrued interest and other assets | | 31,995 | | 27,513 | |

Total assets | | $ | 2,658,576 | | $ | 2,459,140 | |

| | | | | |

Liabilities | | | | | |

Deposits: | | | | | |

Noninterest bearing demand | | $ | 271,549 | | $ | 280,630 | |

Interest bearing: | | | | | |

Savings, NOW, and money market | | 849,365 | | 807,949 | |

Time | | 992,704 | | 974,114 | |

Total deposits | | 2,113,618 | | 2,062,693 | |

Securities sold under repurchase agreements | | 53,222 | | 38,218 | |

Federal funds purchased | | 165,100 | | 54,000 | |

Other short-term borrowings | | 82,873 | | 73,090 | |

Junior subordinated debentures | | 57,399 | | 31,625 | |

Note payable | | 18,610 | | 16,425 | |

Accrued interest and other liabilities | | 17,865 | | 24,534 | |

Total liabilities | | 2,508,687 | | 2,300,585 | |

| | | | | |

Stockholders’ Equity | | | | | |

Preferred stock, $1.00 par value; authorized 300,000 shares; none issued | | — | | — | |

Common stock, $1.00 par value; authorized 20,000,000 shares; issued 16,694,775 in 2007 and 16,634,520 in 2006, outstanding 12,149,296 in 2007 and 13,127,292 in 2006 | | 16,695 | | 16,635 | |

Additional paid-in capital | | 16,114 | | 14,814 | |

Retained earnings | | 209,867 | | 193,170 | |

Accumulated other comprehensive income (loss) | | 1,971 | | (2,545 | ) |

Treasury stock, at cost, 4,545,479 in 2007 and 3,507,228 shares in 2006 | | (94,758 | ) | (63,519 | ) |

Total stockholders’ equity | | 149,889 | | 158,555 | |