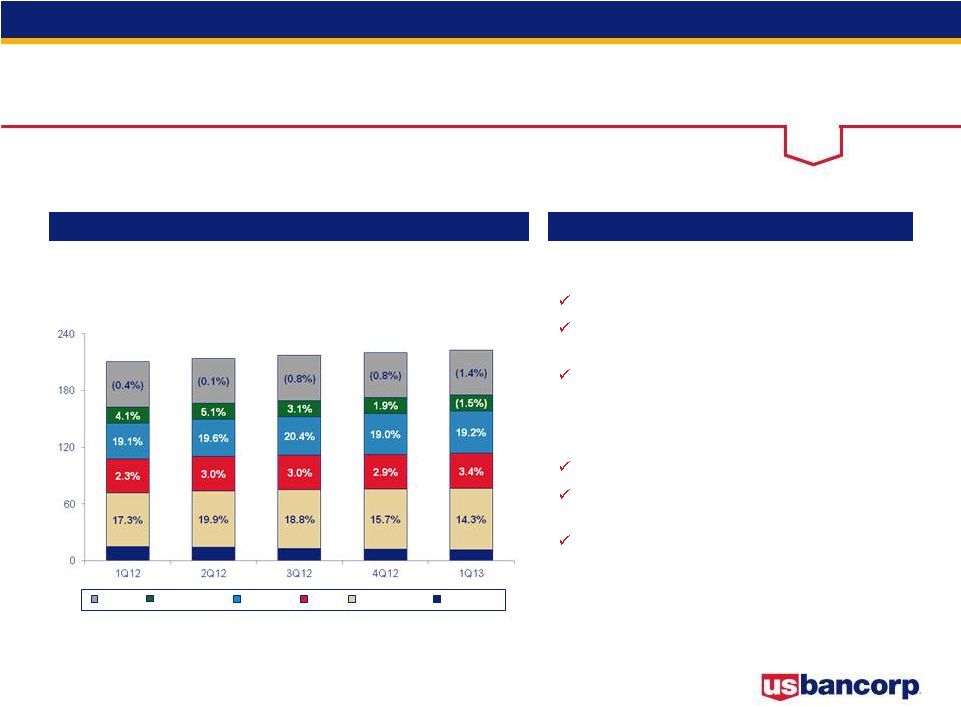

29 1Q13 Earnings Conference Call Non-GAAP Financial Measures $ in millions 1Q13 4Q12 3Q12 2Q12 1Q12 Total equity 40,847 $ 40,267 $ 39,825 $ 38,874 $ 36,914 $ Preferred stock (4,769) (4,769) (4,769) (4,769) (3,694) Noncontrolling interests (1,316) (1,269) (1,164) (1,082) (1,014) Goodwill (net of deferred tax liability) (8,333) (8,351) (8,194) (8,205) (8,233) Intangible assets (exclude mortgage servicing rights) (963) (1,006) (980) (1,118) (1,182) Tangible common equity (a) 25,466 24,872 24,718 23,700 22,791 Tier 1 capital, determined in accordance with prescribed regulatory requirements using Basel I definition 31,774 31,203 30,766 30,044 29,976 Trust preferred securities - - - - (1,800) Preferred stock (4,769) (4,769) (4,769) (4,769) (3,694) Noncontrolling interests, less preferred stock not eligible for Tier I capital (684) (685) (685) (685) (686) Tier 1 common equity using Basel I definition (b) 26,321 25,749 25,312 24,590 23,796 Tangible common equity (as calculated above) 22,791 Adjustments¹ 434 Tier 1 common equity using Basel III proposals published prior to June 2012 (c) 23,225 Tangible common equity (as calculated above) 25,466 24,872 24,718 23,700 81 126 157 153 Tier 1 common equity approximated using proposed rules for the Basel III standardized approach released June 2012 (d) 25,547 24,998 24,875 23,853 Total assets 355,447 353,855 352,253 353,136 340,762 Goodwill (net of deferred tax liability) (8,333) (8,351) (8,194) (8,205) (8,233) Intangible assets (exclude mortgage servicing rights) (963) (1,006) (980) (1,118) (1,182) Tangible assets (e) 346,151 344,498 343,079 343,813 331,347 Risk-weighted assets, determined in accordance with prescribed regulatory requirements using Basel I definition (f) 289,672 287,611 282,033 279,972 274,847 Risk-weighted assets using Basel III proposals published prior to June 2012 (g) - - - - 277,856 Risk-weighted assets, determined in accordance with prescribed regulatory requirements using Basel I definition 289,672 287,611 282,033 279,972 21,021 21,233 22,167 23,240 Risk-weighted assets approximated using proposed rules for the Basel III standardized approach released June 2012 (h) 310,693 308,844 304,200 303,212 Ratios Tangible common equity to tangible assets (a)/(e) 7.4% 7.2% 7.2% 6.9% 6.9% Tangible common equity to risk-weighted assets using Basel I definition (a)/(f) 8.8% 8.6% 8.8% 8.5% 8.3% Tier 1 common equity to risk-weighted assets using Basel I definition (b)/(f) 9.1% 9.0% 9.0% 8.8% 8.7% Tier 1 common equity to risk-weighted assets using Basel III proposals published prior to June 2012 (c)/(g) - - - - 8.4% Tier 1 common equity to risk-weighted assets approximated using proposed rules for the 8.2% 8.1% 8.2% 7.9% - 1Q13 risk-weighted assets are preliminary data, subject to change prior to filings with applicable regulatory agencies 1 Principally net losses on cash flow hedges included in accumulated other comprehensive income 2 Includes net losses on cash flow hedges included in accumulated other comprehensive income, unrealized losses on securities transferred from available-for-sale to held-to-maturity included in accumulated other comprehensive income and disallowed mortgage servicing rights 3 Includes higher risk-weighting for residential mortgages, unfunded loan commitments, investment securities and purchased mortgage servicing rights, and other adjustments Basel III standardized approach released June 2012 (d)/(h) Adjustments² Adjustments³ |