Exhibit 99.1 December 6, 2023 Goldman Sachs U.S. Financial Services Conference 2023 Andy Cecere Chairman, President and Chief Executive Officer John Stern Senior Executive Vice President and Chief Financial Officer 1 U.S. Bank | Confidential

Forward-looking statements The following information appears in accordance with the Private Securities Litigation Reform Act of 1995: This presentation contains forward-looking statements about U.S. Bancorp. Statements that are not historical or current facts, including statements about beliefs and expectations, are forward-looking statements and are based on the information available to, and assumptions and estimates made by, management as of the date hereof. These forward-looking statements cover, among other things, future economic conditions and the anticipated future revenue, expenses, financial condition, asset quality, capital and liquidity levels, plans, prospects and operations of U.S. Bancorp. Forward-looking statements often use words such as “anticipates,” “targets,” “expects,” “hopes,” “estimates,” “projects,” “forecasts,” “intends,” “plans,” “goals,” “believes,” “continue” and other similar expressions or future or conditional verbs such as “will,” “may,” “might,” “should,” “would” and “could.” Forward-looking statements involve inherent risks and uncertainties that could cause actual results to differ materially from those set forth in forward-looking statements, including the following risks and uncertainties: deterioration in general business and economic conditions or turbulence in domestic or global financial markets, which could adversely affect U.S. Bancorp’s revenues and the values of its assets and liabilities, reduce the availability of funding to certain financial institutions, lead to a tightening of credit, and increase stock price volatility; turmoil and volatility in the financial services industry, including failures or rumors of failures of other depository institutions, which could affect the ability of depository institutions, including U.S. Bank National Association, to attract and retain depositors, and could affect the ability of financial services providers, including U.S. Bancorp, to borrow or raise capital; increases in Federal Deposit Insurance Corporation (“FDIC”) assessments due to bank failures; actions taken by governmental agencies to stabilize the financial system and the effectiveness of such actions; changes to regulatory capital, liquidity and resolution-related requirements applicable to large banking organizations in response to recent developments affecting the banking sector; changes to statutes, regulations, or regulatory policies or practices, including capital and liquidity requirements, and the enforcement and interpretation of such laws and regulations, and U.S. Bancorp’s ability to address or satisfy those requirements and other requirements or conditions imposed by regulatory entities; changes in interest rates; increases in unemployment rates; deterioration in the credit quality of its loan portfolios or in the value of the collateral securing those loans; risks related to originating and selling mortgages, including repurchase and indemnity demands, and related to U.S. Bancorp’s role as a loan servicer; impacts of current, pending or future litigation and governmental proceedings; increased competition from both banks and non-banks; effects of climate change and related physical and transition risks; changes in customer behavior and preferences and the ability to implement technological changes to respond to customer needs and meet competitive demands; breaches in data security; failures or disruptions in or breaches of U.S. Bancorp’s operational, technology or security systems or infrastructure, or those of third parties; failures to safeguard personal information; impacts of pandemics, including the COVID-19 pandemic, natural disasters, terrorist activities, civil unrest, international hostilities and geopolitical events; impacts of supply chain disruptions, rising inflation, slower growth or a recession; failure to execute on strategic or operational plans; effects of mergers and acquisitions and related integration; effects of critical accounting policies and judgments; effects of changes in or interpretations of tax laws and regulations; management’s ability to effectively manage credit risk, market risk, operational risk, compliance risk, strategic risk, interest rate risk, liquidity risk and reputation risk; and the risks and uncertainties more fully discussed in the section entitled “Risk Factors” of U.S. Bancorp’s Form 10-K for the year ended December 31, 2022, and subsequent filings with the Securities and Exchange Commission. In addition, U.S. Bancorp’s acquisition of MUFG Union Bank presents risks and uncertainties, including, among others: the risk that the cost savings, any revenue synergies and other anticipated benefits of the acquisition may not be realized or may take longer than anticipated to be realized; and the possibility that the combination of MUFG Union Bank with U.S. Bancorp, including the integration of MUFG Union Bank, may be more costly or difficult to complete than anticipated or have unanticipated adverse results. In addition, factors other than these risks also could adversely affect U.S. Bancorp’s results, and the reader should not consider these risks to be a complete set of all potential risks or uncertainties. Readers are cautioned not to place undue reliance on any forward-looking statements. Forward-looking statements speak only as of the date hereof, and U.S. Bancorp undertakes no obligation to update them in light of new information or future events. This presentation includes non-GAAP financial measures to describe U.S. Bancorp’s performance. The calculations of these measures are provided in the Appendix. These disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. 2 U.S. Bancorp

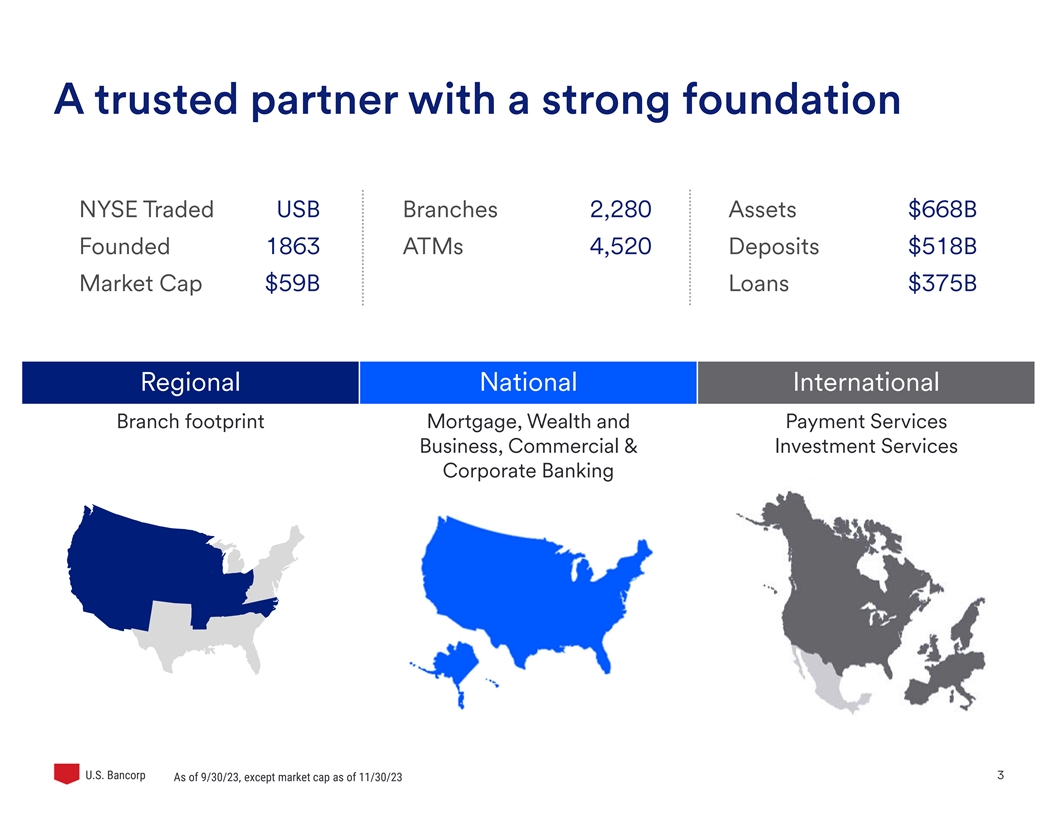

A trusted partner with a strong foundation NYSE Traded USB Branches 2,280 Assets $668B Founded 1863 ATMs 4,520 Deposits $518B Market Cap $59B Loans $375B Regional National International Branch footprint Mortgage, Wealth and Payment Services Business, Commercial & Investment Services Corporate Banking 3 U.S. Bancorp As of 9/30/23, except market cap as of 11/30/23

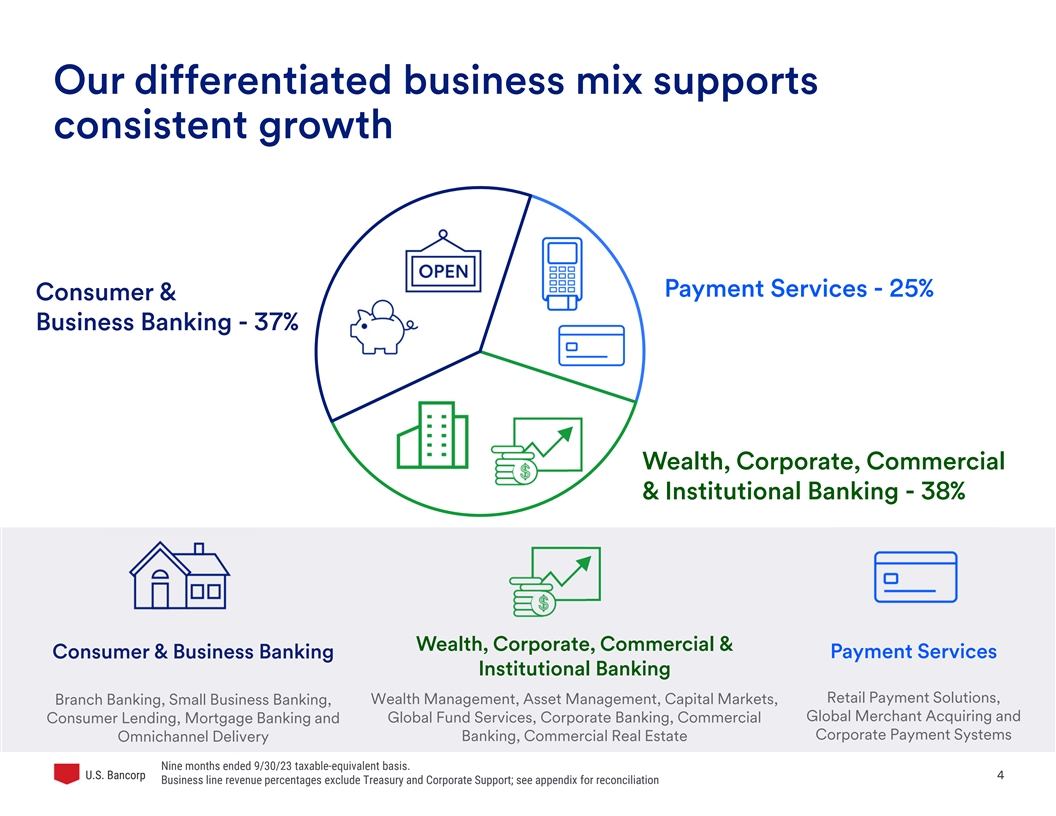

Our differentiated business mix supports consistent growth Payment Services - 25% Consumer & Business Banking - 37% Wealth, Corporate, Commercial & Institutional Banking - 38% Wealth, Corporate, Commercial & Consumer & Business Banking Payment Services Institutional Banking Retail Payment Solutions, Wealth Management, Asset Management, Capital Markets, Branch Banking, Small Business Banking, Global Merchant Acquiring and Global Fund Services, Corporate Banking, Commercial Consumer Lending, Mortgage Banking and Corporate Payment Systems Omnichannel Delivery Banking, Commercial Real Estate Nine months ended 9/30/23 taxable-equivalent basis. 4 U.S. Bancorp Business line revenue percentages exclude Treasury and Corporate Support; see appendix for reconciliation

Enhancing Our Strength and Stability Successful Accelerated Category II Conversion of Capital Commitment Union Bank Build Relief National banking franchise with increased scale, broader reach and meaningful growth opportunities 5 U.S. Bancorp

Union Bank Acquisition… One Year Later What we’ve accomplished: Meaningful growth opportunities: Providing a more holistic product and service offering state of the art digital tools to Union Bank’s loyal customers Successful Conversion ü ~1m ~190k >50k Consumer Business Banking Commercial & 1 Accounts Clients HNW Households ~600k in digital enrollments ü mobile banking, digital mortgage, Consumer Banking card and auto merchant, real-time payments, Business Banking commercial card Achieved $900M run rate ü the spectrum of investment Wealth Management cost synergies management, trust, financial planning Treasury Management, capital Commercial Banking markets, credit Improved scale and market share with significant revenue growth opportunities 1 6 U.S. Bancorp High Net Worth Clients

Capital Efficient Growth Continued focus on high-margin / high-growth business and deepening our most profitable client relationships 1,2 Pre-acquisition CET1 ratio Our Strategy Impact of • Deepen client relationships and Union Bank acquisition leverage full-bank capabilities 1.6% • Reduce lending activity in capital intensive, low return businesses 9.7% 9.7% • Align incentives to promote cross- business area growth to optimize 8.4% 7% CET1 Ratio Regulatory returns Minimum Binding Capital Constraint • Continued implementation of balance sheet optimization initiatives with low- 3Q22 4Q22 3Q23 to-neutral earnings impact 130bps of accretion in 3 quarters Enhanced earnings power drives expected capital generation of ~20-25bps per quarter 1 Ratios calculated in accordance with transitional regulatory requirements related to the current expected credit losses methodology 7 U.S. Bancorp 2 Common equity tier 1 capital to risk-weighted assets, reflecting Basel III standardized with 5 year current expected credit losses (CECL) transition

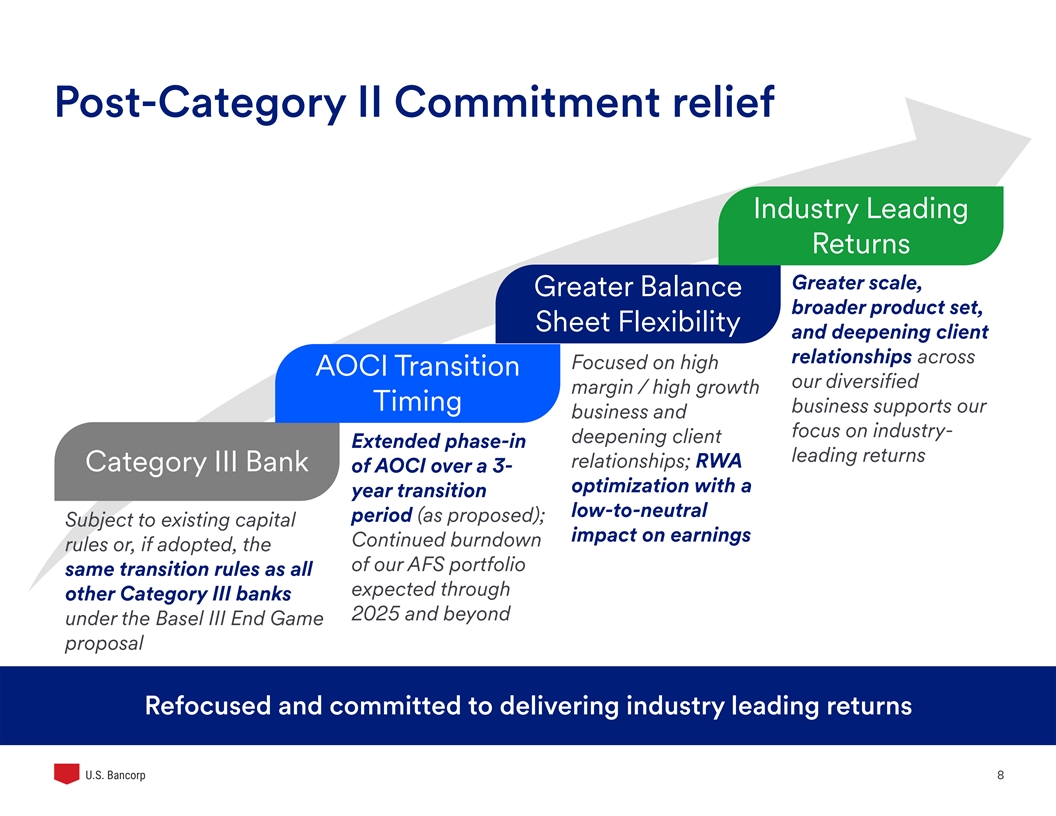

Post-Category II Commitment relief Industry Leading Returns Greater scale, Greater Balance broader product set, Sheet Flexibility and deepening client relationships across Focused on high AOCI Transition our diversified margin / high growth Timing business supports our business and focus on industry- deepening client Extended phase-in leading returns relationships; RWA Category III Bank of AOCI over a 3- optimization with a year transition low-to-neutral period (as proposed); Subject to existing capital impact on earnings Continued burndown rules or, if adopted, the of our AFS portfolio same transition rules as all expected through other Category III banks 2025 and beyond under the Basel III End Game proposal Refocused and committed to delivering industry leading returns 8 U.S. Bancorp

Well-Positioned for 2024 and Beyond Realization of Revenue Growth Opportunities with Union Bank Prudent Expense Management Focus on Industry Leading Returns 9 U.S. Bancorp

U.S. Bancorp

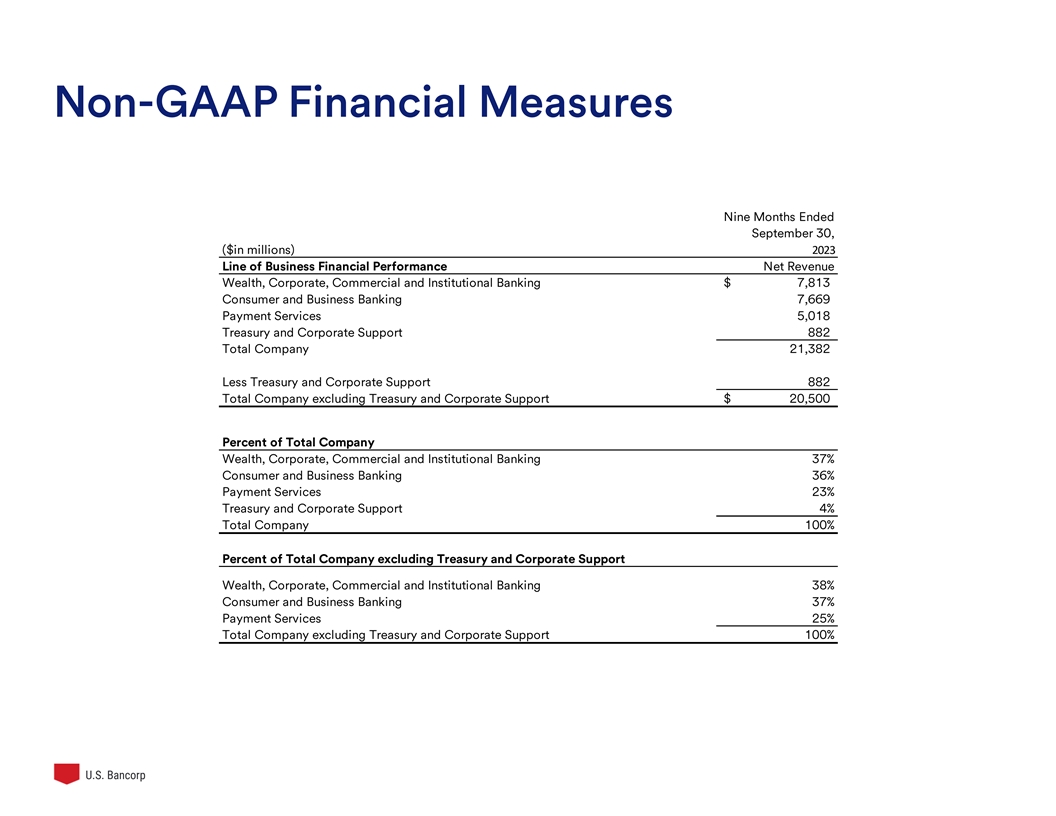

Non-GAAP Financial Measures Nine Months Ended September 30, ($in millions) 2023 Line of Business Financial Performance Net Revenue Wealth, Corporate, Commercial and Institutional Banking $ 7,813 Consumer and Business Banking 7,669 Payment Services 5,018 Treasury and Corporate Support 882 Total Company 21,382 Less Treasury and Corporate Support 882 Total Company excluding Treasury and Corporate Support $ 20,500 Percent of Total Company Wealth, Corporate, Commercial and Institutional Banking 37% Consumer and Business Banking 36% Payment Services 23% Treasury and Corporate Support 4% Total Company 100% Percent of Total Company excluding Treasury and Corporate Support Wealth, Corporate, Commercial and Institutional Banking 38% Consumer and Business Banking 37% Payment Services 25% Total Company excluding Treasury and Corporate Support 100% U.S. Bancorp