Citigroup 2012 Financial Services Conference March 8, 2012 Exhibit 99 |

2 This presentation contains forward looking statements within the meaning of the Private Securities Litigation Reform Act giving the Company's expectations or predictions of future financial or business performance or conditions. Forward-looking statements are typically identified by words such as "believe," "expect," "anticipate," "intend," "target," "estimate," "continue," "positions," "prospects" or "potential," by future conditional verbs such as "will," "would," "should," "could" or "may," or by variations of such words or by similar expressions. These forward-looking statements are subject to numerous assumptions, risks and uncertainties which change over time. Forward-looking statements speak only as of the date they are made and we assume no duty to update forward-looking statements. In addition to factors previously disclosed in our SEC reports and those identified elsewhere in this presentation, the following factors among others, could cause actual results to differ materially from forward-looking statements or historical performance: changes in asset quality and credit risk; the inability to sustain revenue and earnings growth; changes in interest rates and capital markets; inflation; customer acceptance of M&T products and services; customer borrowing, repayment, investment and deposit practices; customer disintermediation; the introduction, withdrawal, success and timing of business initiatives; competitive conditions; the inability to realize cost savings or revenues or to implement integration plans and other consequences associated with mergers, acquisitions and divestitures; economic conditions; and the impact, extent and timing of technological changes, capital management activities, and other actions of the Federal Reserve Board and legislative and regulatory actions and reforms, including those associated with the Dodd-Frank Wall Street Reform and Consumer Protection Act. Annualized, pro forma, projected and estimated numbers are used for illustrative purpose only, are not forecasts and may not reflect actual results. Disclaimer |

3 Today’s Agenda Who is M&T Bank? 2011 Highlights Consistent, conservative operating philosophy Wilmington Trust Outlook |

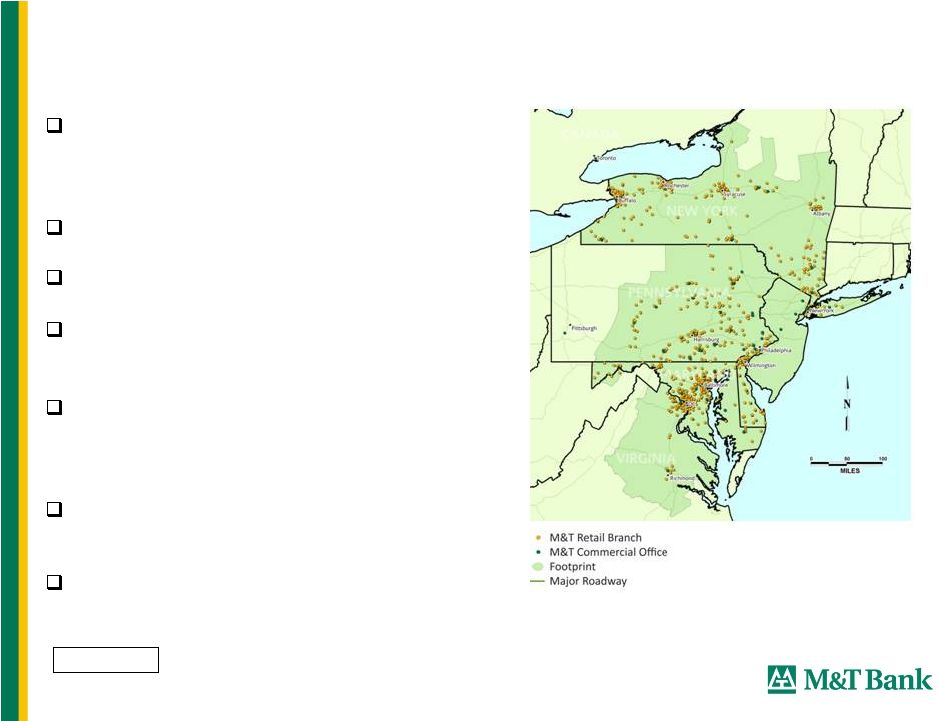

4 Top 20 US-based full-service commercial bank holding company by assets and Top 15 by market cap Founded in 1856 $78 billion total assets 776 domestic branches and more than 2,000 ATMs 15,666 employees located in New York, Maryland, Pennsylvania, Washington, D.C., Virginia, West Virginia and Delaware Over 2 million consumer/retail household customers Approximately 220,000 commercial customers M&T Bank Corporate Profile As of 12/31/11 |

5 Most honored bank in 2011 Greenwich Excellence Awards for Small Business Banking: 12 national awards and 2 regional awards Highest number of awards among all 750 banks rated by business customers Received the highest possible Community Reinvestment Act (CRA) rating on every exam since 1982 M&T Charitable Foundation has contributed over $147 million to not-for-profit organizations in its communities over the past 10 years Contributed $40 million to M&T Charitable Foundation in 2011 More than 3,000 M&T employees volunteer with 5,100 different not-for-profit organizations Strong long-term returns for shareholders Recognition from Customers, Communities & Shareholders |

6 Strong Presence In Our Communities We lend in the markets where we live and work to people and enterprises whom we know #1 Small Business Lender in:** Baltimore Binghamton Buffalo Philadelphia Rochester Syracuse Washington, DC Wilmington Ranked 6 th Nationally Ranked 3 rd in Eastern U.S. #1 lead bank market share among middle market clients in:* Baltimore Binghamton Buffalo Harrisburg Northern Pennsylvania Rochester Syracuse State of Maryland overall State of Delaware overall * Independent market research ** Small Business Administration #1 or #2 deposit market share in 8 of top 10 communities: #2 in Baltimore #1 in Binghamton #1 in Buffalo #2 in Harrisburg #2 in Rochester #1 in Syracuse #1 State of Delaware / Wilmington City #1 in York |

7 Summary of Full Year 2011 Results 12% increase in diluted GAAP & Net Operating EPS Net operating return on tangible common equity of 17.96% Increased tangible book value per common share by 14% No secondary equity offering Consummated Wilmington Trust merger in May Expansion into new markets, encompassed by the Wilmington Trust Diversification into a wider array of trust and fiduciary businesses, Completed integration of core banking systems at end of 3Q franchise |

8 Executed on 2011 Capital Plan Retired $330 million of WT’s TARP preferred stock from US Treasury Redeemed additional $370 million of M&T’s TARP preferred stock Issued $500 million of 6.875% perpetual preferred stock to bolster Tier 1 capital Unchanged $2.80 per share dividend Built capital ratios while absorbing WT and supporting loan growth Tier 1 common capital ratio up 35bp to 6.86% at year-end 2011 Tangible common equity ratio up 21bp to 6.40% at year end 2011. |

9 Strong credit through crisis Focused on returns Consistent capital generation (1) The Efficiency Ratio and Pre-tax, Pre-provision Earnings are non-GAAP financial measures. A reconciliation of GAAP to non-GAAP financial measures is available in the appendix. The Efficiency Ratio reflects non-interest expense (excluding amortization expense associated with intangible assets and merger-related expenses) as a percentage of fully taxable equivalent net interest income and non-interest revenues (excluding gains or losses from securities transactions and merger-related gains). (2) Excludes merger-related gains and expenses and amortization expense associated with intangible assets. (1) Key Ratios 2006 2007 2008 2009 2010 2011 Net Interest Margin 3.70% 3.60% 3.38% 3.49% 3.84% 3.73% Efficiency Ratio - Tangible (1) 51.51% 52.77% 54.35% 56.50% 53.71% 60.43% Pre-tax, Pre-provision Earnings ($MM) 1,312 1,156 1,152 1,123 1,461 1,495 Allowance to Loans (As At) 1.51% 1.58% 1.61% 1.69% 1.74% 1.51% Net Charge-Offs to Loans 0.16% 0.26% 0.78% 1.01% 0.67% 0.47% Net Operating Return on Tangible Assets (2) 1.67% 1.27% 0.97% 0.71% 1.17% 1.26% Tangible Common Equity (2) 29.55% 22.58% 19.63% 13.42% 18.95% 17.96% Common Equity to Assets - Tangible 5.84% 5.01% 4.59% 5.13% 6.19% 6.40% Tier 1 Common Capital Ratio 6.42% 5.62% 6.08% 5.66% 6.51% 6.86% Tier 1 Capital Ratio 7.74% 6.84% 8.83% 8.59% 9.47% 9.67% Total Capital Ratio 11.78% 11.18% 12.83% 12.30% 13.08% 13.26% Leverage Ratio 7.20% 6.59% 8.35% 8.43% 9.33% 9.28% TBV per Share 28.57 27.98 25.94 28.27 33.26 37.79 Superior pre-credit earnings |

10 Consistent, Conservative Operating Philosophy Focus on return, not volume Solid underwriting Efficient provider of basic banking services Prudent capital allocation Disciplined approach to acquisitions Acquirer of choice - superior returns for our partners Management, employees & Board own or control >20% of M&T stock Owner-operators |

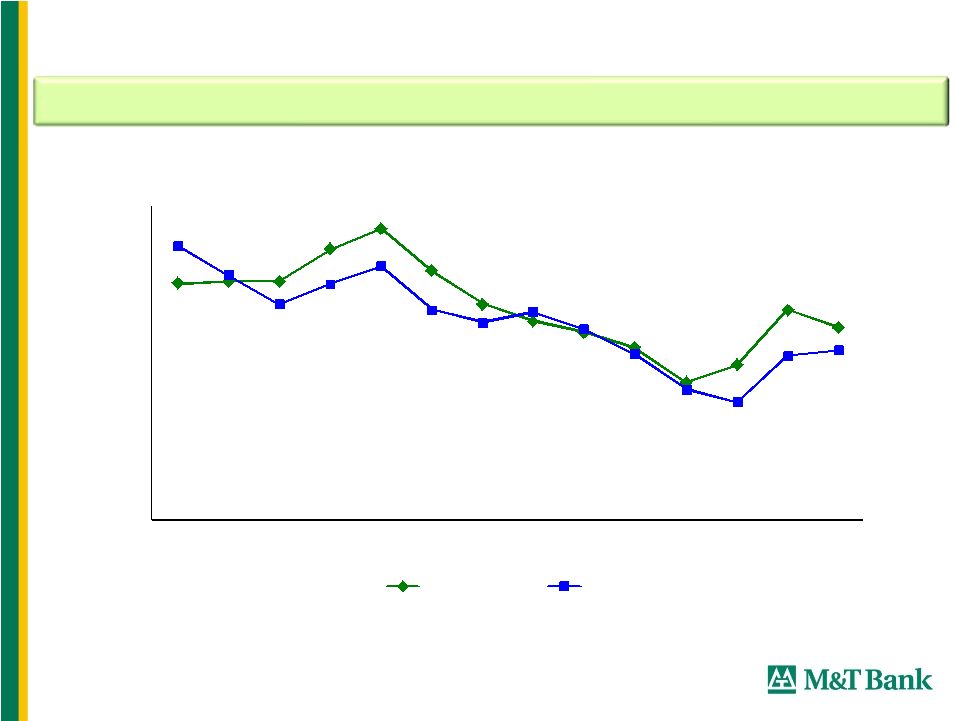

11 4.01 3.73 4.25 3.58 2.5 3.0 3.5 4.0 4.5 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 MTB Peer Median Disciplined margin management Note: Taxable Equivalent net interest margin used for M&T and for peer banks when available. Net Interest Margin M&T focuses on returns and relationships rather than volumes |

12 Notes: 1) Source: Industry data was obtained from the 1/6/2012 H8 prepared by the Federal Reserve. 2) Loan growth at Domestically Chartered Commercial Banks, adjusted to exclude the March 31, 2010 impact of FAS 167 balance sheet consolidation and September 2008 addition of Washington Mutual. 3) Industry Commercial loans include both “C&I and Other Loans” and “Commercial Real Estate Loans” as outlined in the H8 report. 4) The 1Q11 decline in industry loans is unadjusted for Citigroup’s sale of $26 billion in consumer loans to Sallie Mae. 5) MTB loan growth acquisition adjusted for Partners and First Horizon (Dec-07), Provident (Jun-09), Bradford (Sep-09), K Bank (Dec-10), and Wilmington Trust (Jun-11) Linked Quarter Loan Growth M&T has outperformed the industry through the credit cycle Total Industry MTB Commercial Loans 2.1% 2.5% Res. Real Estate Loans 1.8% 10.3% Consumer Loans 1.3% -0.6% Total Loans & Leases 1.8% 2.9% 4Q11 Linked Qtr Loan Growth Domestic Unnualized 4.1% 3.9% 1.1% 0.0% 2.8% -0.3% -2.6% -0.8% -3.2% 0.0% -3.3% -0.9% -1.4% 0.5% -2.5% 0.5% 1.3% 1.8% 2.4% 4.0% 2.6% -0.3% -0.9% 0.6% -0.2% -0.4% -1.5% -0.5% -0.9% -0.7% -0.5% 2.1% 0.2% 0.4% -0.2% 2.9% -4.0% -3.0% -2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Domestically Chartered Commercial Banks MTB |

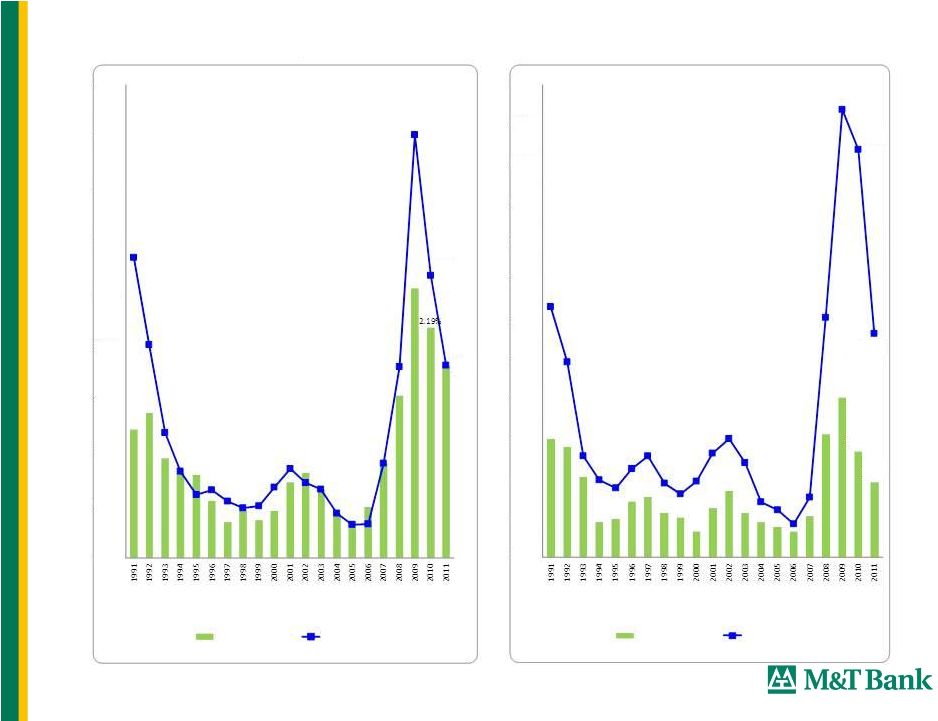

13 Historical Credit Cycle: 1991 - 2011 Source: SNL Interactive. Regulatory and GAAP filings * Top 25 publicly traded banks in each year. 0.67% 0.47% 2.59% 1.42% 0.00% 0.25% 0.50% 0.75% 1.00% 1.25% 1.50% 1.75% 2.00% 2.25% 2.50% 2.75% 3.00% NCOs / Average Loans MTB Top 25 Median* 1.83% 2.68% 1.83% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% 4.50% Nonaccrual Loans / Total Loans MTB Top 25 Median* |

14 17.5% 15.7% 11.1% 10.4% 9.4% 9.1% 8.0% 7.7% 7.0% 6.1% 5.1% 3.1% Median 8.5% 0% 5% 10% 15% 20% Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 MTB Total Loans 9.3% 9.1% 8.7% 8.5% 7.5% 7.1% 4.8% 4.1% 4.0% 3.8% 2.8% 0.6% Median 5.9% 0% 3% 6% 9% 12% Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 MTB Comm. Real Estate 36.5% 33.2% 29.9% 26.4% 21.3% 20.8% 19.8% 16.6% 15.7% 15.3% 10.2% 8.0% Median 20.3% 0% 10% 20% 30% 40% Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 MTB Construction 15.7% 11.0% 8.9% 8.5% 7.7% 6.7% 6.1% 5.0% 4.9% 4.5% 3.4% 2.9% Median 6.4% 0% 5% 9% 14% 18% Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 MTB Commercial & Industrial 12.0% 11.2% 9.8% 8.7% 8.2% 5.5% 5.0% 4.7% 4.7% 4.4% 3.9% 2.7% Median 5.2% 0% 3% 6% 9% 12% 15% Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 MTB Peer 9 Peer 10 Peer 11 Residential Mortgage 26.4% 14.3% 9.8% 9.1% 7.3% 5.3% 5.2% 5.2% 4.5% 3.3% 3.3% 1.8% Median 5.3% 0% 6% 12% 18% 24% 30% Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 MTB HELOC Loss Experience Through Financial Crisis 3Q07 – 4Q11* * Represents cumulative net credit losses from 3Q07 through 4Q11 as percentage of average loans over that period |

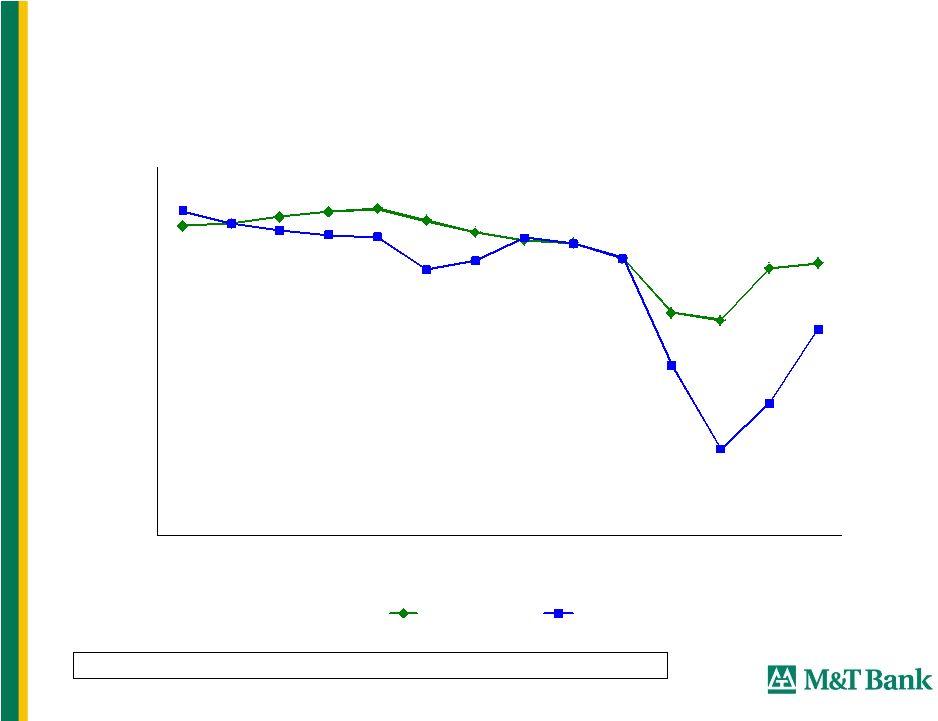

15 3.78% 3.32% 3.96% 2.52% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% 4.50% '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 MTB Peer Median Balancing risk and rewards in lending Risk-Adjusted Net Interest Margin* 1998-2011 *Reflects FTE Net Interest Income less Net Charge-offs as percentage of average earning assets |

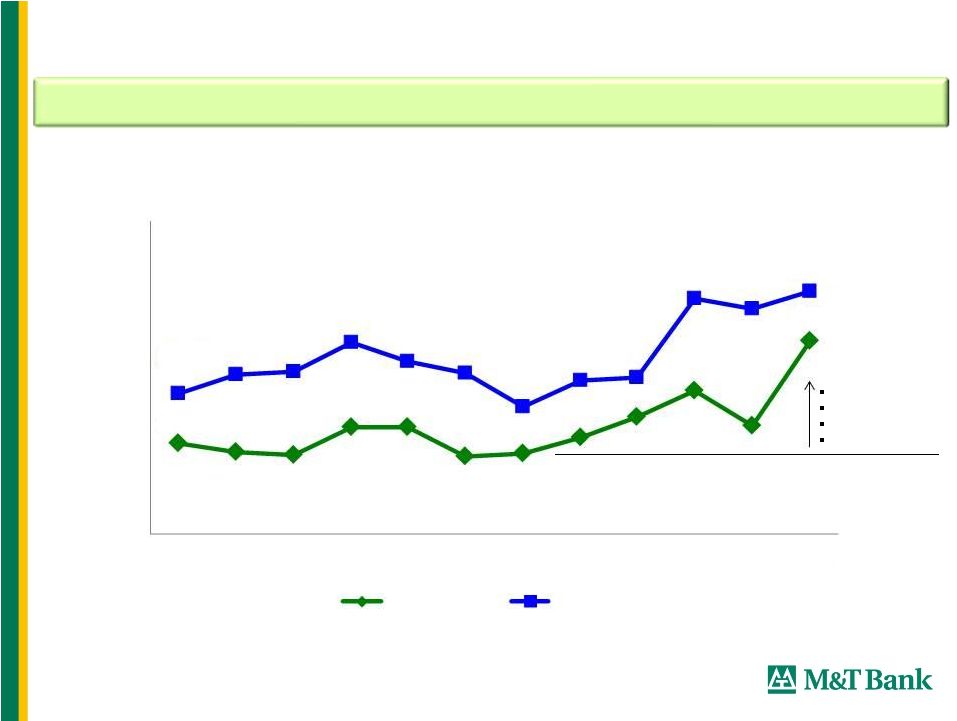

16 Efficiency Ratio M&T’s philosophy relies on efficiently delivering banking services 2011 results influenced by Wilmington Trust and noteworthy 4Q items Wilmington Trust FDIC Fee Regulation Credit Cycle 52.25% 60.43% 56.28% 64.33% 45% 50% 55% 60% 65% 70% '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 MTB Peer Median Efficiency Ratio reflects non-interest expense (excluding amortization expense associated with intangible assets, merger-related expenses and other non-recurring expenses) as a percentage of fully taxable equivalent net interest income and non-interest revenues (excluding gains from securities transactions and merger-related gains). The Efficiency Ratio is a non-GAAP measure. See Appendix for a reconciliation to GAAP measures. |

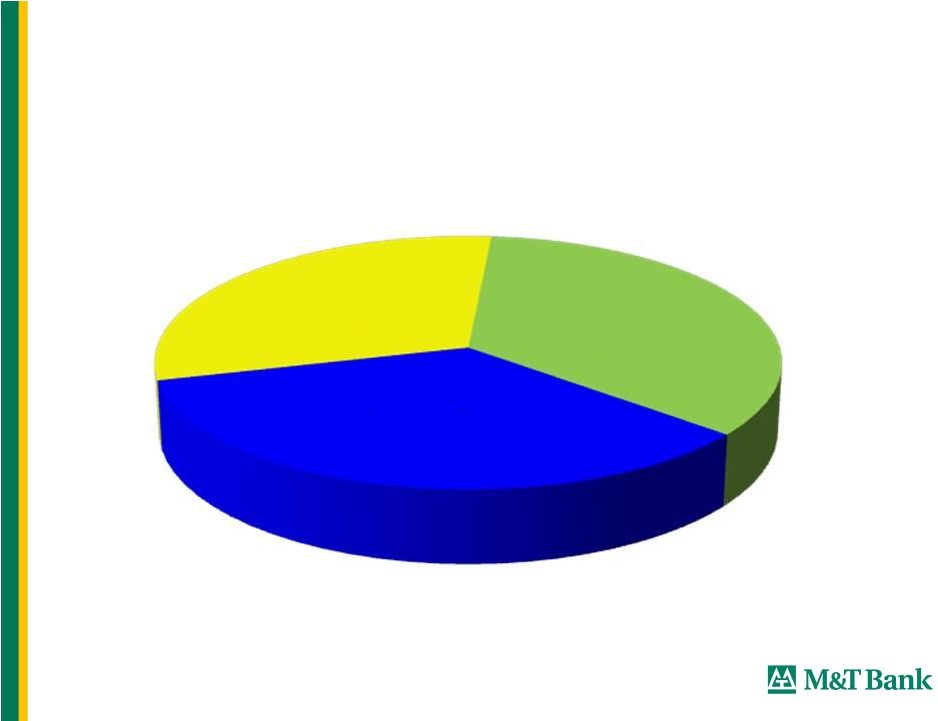

17 Prudent Capital Allocation Cumulative Capital Retained, Dividends and Share Repurchases 1983 – 2011 Share Repurchases 34% Dividends 31% Capital Retained 35% |

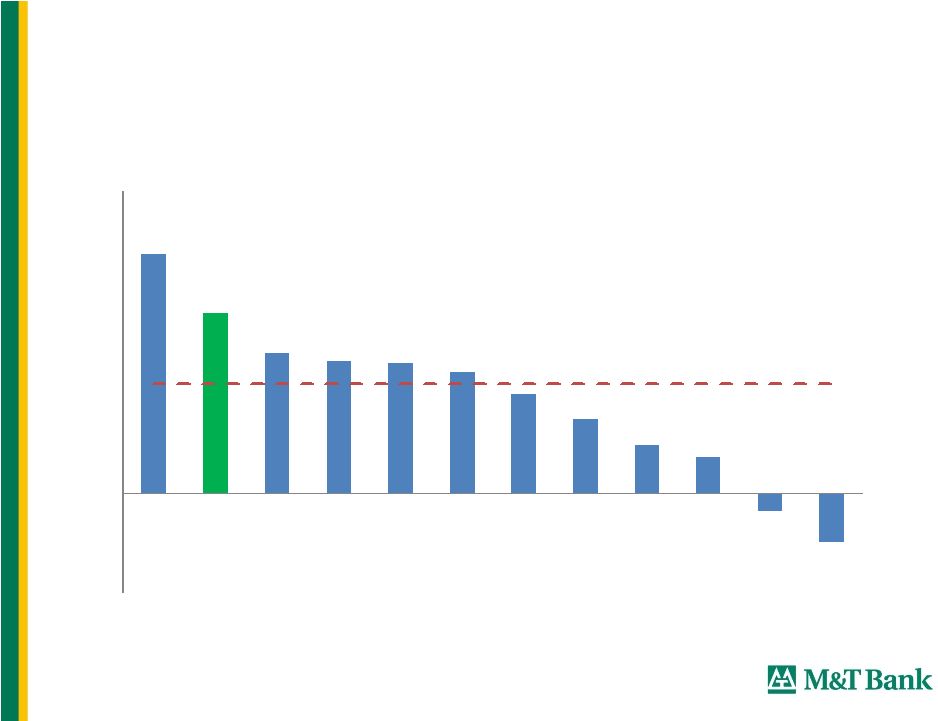

18 23.8% 18.0% 14.0% 13.2% 13.0% 12.0% 10.0% 7.4% 4.7% 3.6% -1.7% -4.9% -10% 0% 10% 20% 30% Peer 1 MTB Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 Peer Median 10.9% Net Operating Return on Tangible Common Equity – FY-2011 Note: Excludes amortization of intangibles and goodwill impairment, merger-related items, and other nonrecurring items as noted by SNL. |

Acquistion MTB Total Return BKX Total Return Outperformance Wilmington Trust 9.0% 1.9% 7.2% Provident 63.6% 9.4% 54.2% Allfirst 30.4% -17.1% 47.5% Keystone 169.2% -20.4% 189.6% Total Returns to Date Since Acquisition Announcement* M&T’s Acquisitions vs. Bank Deals > than $1B since 2000: Deal Value / Tangible Common Equity The M&T strategy: Value accrues to seller over time (1) Deal Value at Announcement and Tangible Common Equity at Most Recent Quarter before Announcement (2) Although Provident and Wilmington were both less than $1.0 billion in Deal Value, they have been included for reference (2) Source: SNL Financial, SNL Total Return for MTB, Bloomberg - BKX Total Return * Return calculated from first closing price post-announcement [Wilmington: 11/1/2010, Provident: 12/19/2008, Allfirst: 9/26/2002, Keystone: 5/17/2000] through 3/5 /12 19 |

20 Overview of Wilmington Trust Acquisition, May 2011 M&T consummated Wilmington Trust merger May 2011 o Completed integration of core banking systems at end of 3 Quarter 2011 Compelling partnership: o Wilmington’s #1 market share in Delaware combined with M&T’s leading Mid-Atlantic commercial bank presence provides top-tier scale o M&T’s ability to leverage and grow the established value of the Wilmington Trust brand in trust, wealth management and corporate services o Increased fee income diversifies revenue and enhances M&T’s ROE o Shared values for community banking creates added returns for communities rd |

21 WT merger targets announced at acquisition – 11/1/10: High single-digit 2012 GAAP EPS accretion Low double-digit 2012 net operating EPS accretion Merger synergies about 15% of WT expense base - $80 million annualized by end of 2012 Merger-related expenses likely won’t exceed $100 million excl. purchase accounting & Capex 2012 EPS impact consistent with original targets $13 million of merger synergies realized in 4Q11 On track to realize full annual run-rate by 4Q12 following Trust systems integration $84 million merger-related expenses incurred through y/e 2011 Up to $10 million remaining merger-related expenses in 1H12 Update on Wilmington Trust merger Update at Investor Conference - September 2011 First Quarter 2012 status: |

22 Wilmington Trust is comprised of 2 Complementary Businesses Corporate Client Services (CCS) 2011 post–acquisition fee revenues - $119 million Four discrete business groups Corporate Trust / Capital Markets Retirement & Institutional Services M&T Insurance Agency Investment Management Wealth Advisory Services (WAS) 2011 post-acquisition fee revenues - $87 million Two distinct customer segments: Opportunities typically arise through referrals from lawyers, accountants, record keepers, investment bankers, financial advisors and consultants. Provide administrative and/or fiduciary solutions to corporations, governments & large institutions for complex transactions and legal structures. M&T’s middle market customer base includes some 8,500 commercial clients; we believe expanding Commercial/Wealth relationships will be a strong generator of new business. Wealth creators - entrepreneurs and privately held business owners that need both traditional commercial loan and deposit services for their business plus fiduciary and investment services for personal wealth Multigenerational wealth “family offices” with complex fiduciary, investment and private banking needs. |

23 One-time NIM expansion from 4Q11’s 3.60% as excess liquidity held at Fed over 2H11 has been deployed or withdrawn For FY2012, expect NIM slightly lower than FY2011’s 3.73% NIM outlook combined w/ mid-single digit loan growth implies growth in NII Remain cautious with our outlook for credit Expect continued, slow, steady improvement Focused on expenses Reminder: Seasonal expense surge in 1Q due to equity compensation grants Outlook Consistent with Remarks on January earnings call |

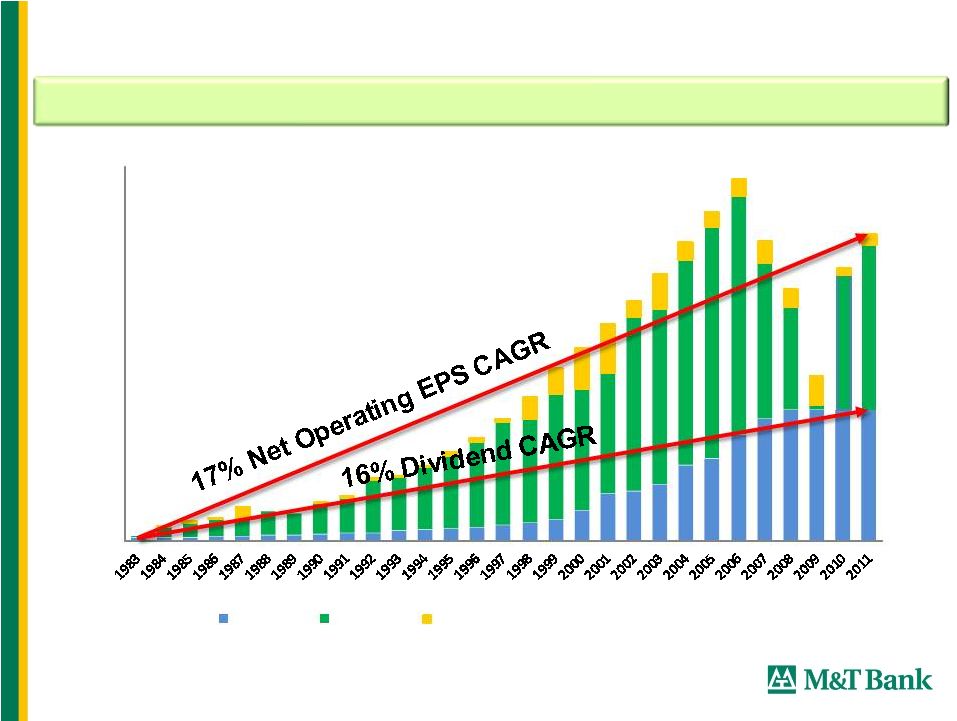

24 Earnings & Dividend Growth: 1983 - 2011 Note: Data prior to 1998 does not include provisions of SFAS No. 123 and No. 148 stock option expensing. M&T maintained its dividend and experienced no losses through the recent crisis Net Operating Income and Net Operating EPS are non-GAAP financial measures. Refer to the Appendix for a reconciliation between these measures and GAAP 2.80 2.80 5.84 6.55 $0.00 $1.00 $2.00 $3.00 $4.00 $5.00 $6.00 $7.00 $8.00 Dividends GAAP EPS Impact of Amortization and Merger-related expenses |

25 Strong Long-term Returns to Shareholders Highest annual stock price appreciation among top 100 banks since 1983 19.3% annual total return since 1980 Highest total return among top 50 banks since 2000 19 highest return among top 50 banks in 2011 th |

Citigroup 2012 Financial Services Conference March 8, 2012 |

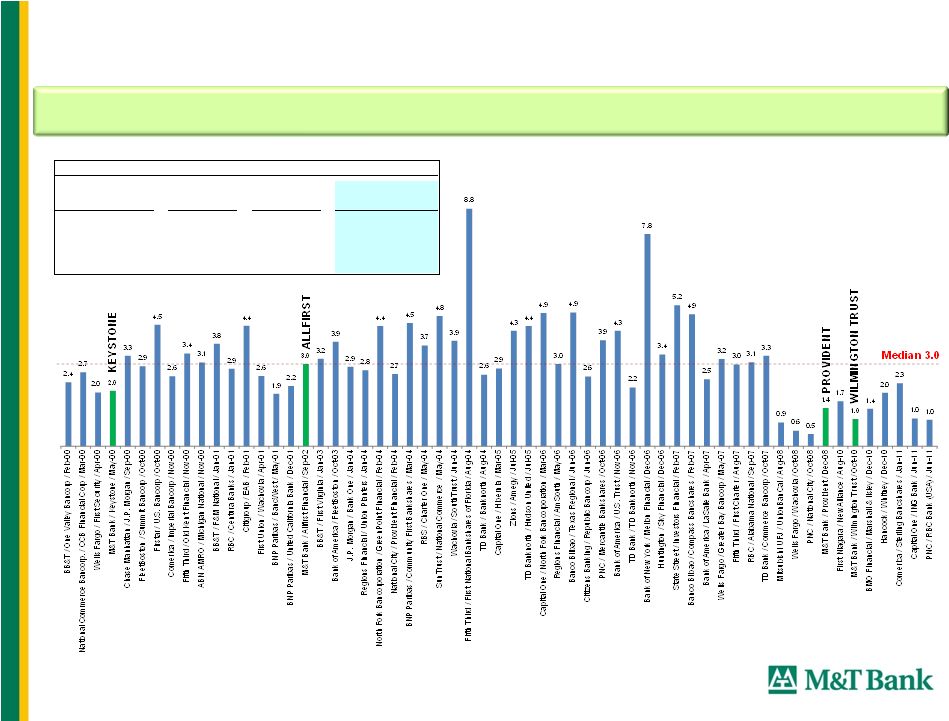

27 1 1983 Stock Prices Source: Compustat and/or SNL M&T Bank Corporation… a solid investment Stock Closing Price at Return 2/29/2012 3/31/1983 CAGR Rank Company Name Ticker ($) ($) 1 (%) 1 M&T Bank Corporation MTB 81.62 1.34 15.3 2 State Street Corporation STT 42.23 1.06 13.6 3 U.S. Bancorp USB 29.40 0.92 12.7 4 Northern Trust Corporation NTRS 44.41 1.51 12.4 5 Wells Fargo & Company WFC 31.29 1.18 12.0 23 — — 2.8 Median — — 7.6 MTB Price @ Median Growth Rate 11.09 1.34 7.6 Of the largest 100 banks operating in 1983, only 23 remain today Among the remaining, M&T ranks 1 st in stock price growth |

28 19.3% Annual rate of return since 1980* – 22 nd best return of the entire universe of over 700 U.S. based stocks that have traded publicly since 1980 $3,418 invested in M&T in 1980 would be worth $1 million today *CAGR calculated assuming reinvestment of dividends through February 29, 2012. M&T Bank Corporation… a solid investment Rank Company Name Industry Annual Return 1 Eaton Vance Corp. Financials 25.1 2 Limited Brands Inc. Consumer Discretionary 23.3 3 Gap Inc. Consumer Discretionary 22.8 4 Progressive Corp. Financials 22.8 5 TJX Cos. Consumer Discretionary 22.6 6 Stryker Corp. Health Care 22.2 7 Wal-Mart Stores Inc. Consumer Staples 21.8 8 Hasbro Inc. Consumer Discretionary 21.6 9 Mylan Inc. Health Care 21.6 10 Precision Castparts Corp. Industrials 21.4 11 Leucadia National Corp. Financials 20.9 12 Raven Industries Inc. Industrials 20.9 13 Valspar Corp. Materials 20.7 14 State Street Corp. Financials 20.3 15 HollyFrontier Corp. Energy 20.3 16 Danaher Corp. Industrials 20.3 17 Berkshire Hathaway Inc. Cl A Financials 20.2 18 Robert Half International Inc. Industrials 19.8 19 Forest Laboratories Inc. Health Care 19.8 20 Family Dollar Stores Inc. Consumer Discretionary 19.4 21 Graco Inc. Industrials 19.4 22 M&T Bank Corp. Financials 19.3 |

29 Total Returns to Shareholders (1) Largest 50 banks by market capitalization as of January 1, 2000 (1) Total Return To Shareholder from 12/31/1999 to 12/31/2011, as sourced from Barclays Capital and SNL Financial. |

30 Appendix |

31 2011 Peer Group - Largest 12 Regional Banks BB&T Corporation M&T Bank Corporation Capital One Financial Corporation PNC Financial Services Group, Inc. Comerica Incorporated Regions Financial Corporation Fifth Third Bancorp Synovus Financial Corp. SunTrust Banks, Inc. Huntington Bancshares Incorporated Zions Bancorporation KeyCorp |

32 Reconciliation of GAAP and Non-GAAP Measures Net Income 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 $'s in millions Net income $268.2 $353.1 $456.7 $573.9 $722.5 $782.2 $839.2 $654.3 $555.9 $379.9 $736.2 $859.5 Intangible amortization* 56.1 99.4 32.5 47.8 46.1 34.7 38.5 40.5 40.5 39.0 35.3 37.6 Merger-related items* 16.4 4.8 - 39.2 - - 3.0 9.1 2.2 36.5 (16.3) (12.8) Net operating income $340.7 $457.3 $489.2 $660.9 $768.6 $816.9 $880.7 $703.8 $598.6 $455.4 $755.2 $884.3 Pre-Tax, Pre-Provision Income GAAP Pre-tax Income $422.3 $551.6 $675.9 $850.7 $1,066.5 $1,170.9 $1,231.6 $963.5 $739.8 $519.3 $1,092.8 $1,224.6 Provision for credit losses 38.0 103.5 122.0 131.0 95.0 88.0 80.0 192.0 412.0 604.0 368.0 270.0 Pre-Tax, Pre-Provision Income $460.3 $655.1 $797.9 $981.7 $1,161.5 $1,258.9 $1,311.6 $1,155.5 $1,151.8 $1,123.3 $1,460.8 $1,494.6 Earnings Per Share Diluted earnings per share $3.24 $3.58 $4.78 $4.95 $6.00 $6.73 $7.37 $5.95 $5.01 $2.89 $5.69 $6.35 Intangible amortization* 0.67 1.00 0.34 0.41 0.38 0.30 0.33 0.37 0.36 0.34 0.29 0.30 Merger-related items* 0.20 0.05 - 0.34 - - 0.03 0.08 0.02 0.31 (0.14) (0.10) Diluted net operating earnings per share $4.11 $4.63 $5.12 $5.70 $6.38 $7.03 $7.73 $6.40 $5.39 $3.54 $5.84 $6.55 Efficiency Ratio $'s in millions Non-interest expenses $718.6 $980.6 $961.6 $1,448.2 $1,516.0 $1,485.1 $1,551.7 $1,627.7 $1,727.0 $1,980.6 $1,914.8 $2,478.1 less: intangible amortization 69.6 121.7 51.5 78.2 75.4 56.8 63.0 66.5 66.6 64.3 58.1 61.6 less: merger-related expenses 26.0 8.0 - 60.4 - - 5.0 14.9 3.5 89.2 0.8 83.7 Non-interest operating expenses $623.0 $850.9 $910.1 $1,309.6 $1,440.6 $1,428.3 $1,483.7 $1,546.3 $1,656.8 $1,827.2 $1,856.0 $2,332.8 Tax equivalent revenues $1,189.4 $1,653.3 $1,773.6 $2,446.2 $2,694.9 $2,761.3 $2,883.1 $2,804.1 $2,900.6 $3,125.7 $3,399.6 $3,998.6 less: gain/(loss) on sale of securities (3.1) 1.9 (0.6) 2.5 2.9 1.2 2.6 1.2 34.4 1.2 2.8 150.2 less: net OTTI losses recognized - - - - - (29.4) - (127.3) (182.2) (138.3) (86.3) (77.0) less: merger-related gains - - - - - - - - - 29.1 27.5 64.9 Denominator for efficiency ratio $1,192.5 $1,651.4 $1,774.2 $2,443.7 $2,692.0 $2,789.5 $2,880.5 $2,930.2 $3,048.4 $3,233.7 $3,455.6 $3,860.5 Net operating efficiency ratio 52.3% 51.5% 51.3% 53.6% 53.5% 51.2% 51.5% 52.8% 54.4% 56.5% 53.7% 60.4% *Net of tax |

33 Reconciliation of GAAP and Non-GAAP Measures Average Assets 2006 2007 2008 2009 2010 2011 $'s in millions Average assets 55,839 $ 58,545 $ 65,132 $ 67,472 $ 68,380 $ 73,977 $ Goodwill (2,908) (2,933) (3,193) (3,393) (3,525) (3,525) Core deposit and other intangible assets (191) (221) (214) (191) (153) (168) Deferred taxes 38 24 30 33 29 43 Average tangible assets 52,778 $ 55,415 $ 61,755 $ 63,921 $ 64,731 $ 70,327 $ Average Common Equity $'s in millions Average common equity 6,041 $ 6,247 $ 6,423 $ 6,616 $ 7,367 $ 8,207 $ Goodwill (2,908) (2,933) (3,193) (3,393) (3,525) (3,525) Core deposit and other intangible assets (191) (221) (214) (191) (153) (168) Deferred taxes 38 24 30 33 29 43 Average tangible common equity 2,980 $ 3,117 $ 3,046 $ 3,065 $ 3,718 $ 4,557 $ |