Allegheny Energy

Edison Electric Institute

Financial Conference

November 5-8, 2006

Forward-Looking Statements

In addition to historical information, this presentation contains a number of "forward-looking

statements" as defined in the Private Securities Litigation Reform Act of 1995. Words such as

anticipate, expect, project, intend, plan, believe and words and terms of similar substance used in

connection with any discussion of future plans, actions or events identify forward-looking statements.

These include statements with respect to: regulation and the status of retail generation service supply

competition in states served by Allegheny Energy's delivery business, Allegheny Power; the closing of

various agreements; financing plans; demand for energy and the cost and availability of raw materials,

including coal; provider-of-last resort and power supply contracts; results of litigation; results of

operations; internal controls and procedures; capital expenditures; status and condition of plants and

equipment; regulatory matters; and accounting issues. Forward-looking statements involve estimates,

expectations, and projections and, as a result, are subject to risks and uncertainties. There can be no

assurance that actual results will not materially differ from expectations. Actual results have varied

materially and unpredictably from past expectations. Factors that could cause actual results to differ

materially include, among others, the following: changes in the price of power and fuel for electric

generation; general economic and business conditions; changes in access to capital; complications or

other factors that render it difficult or impossible to obtain necessary lender consents or regulatory

authorizations on a timely basis; environmental regulations; the results of regulatory proceedings,

including proceedings related to rates; changes in industry capacity, development, and other activities

by Allegheny's competitors; changes in the weather and other natural phenomena; changes in the

underlying inputs and assumptions, including market conditions used to estimate the fair values of

commodity contracts; changes in laws and regulations applicable to Allegheny, its markets or its

activities; the loss of any significant customers and suppliers; dependence on other electric

transmission and gas transportation systems and their constraints on availability; changes in PJM,

including changes to participants rules and tariffs; the effect of accounting policies issued periodically

by accounting standard-setting bodies; and the continuing effects of global instability, terrorism and

war. Additional risks and uncertainties are identified and discussed in Allegheny Energy's reports and

registration statements filed with the Securities and Exchange Commission. These forward-looking

statements speak only as of the date of this document. Allegheny Energy undertakes no obligation to

update its forward-looking statements to reflect events or circumstances after

the date of this document.

2

Non-GAAP Financial Measures

This presentation includes non-GAAP financial measures as defined in the

Securities and Exchange Commission’s Regulation G. Where noted, the

presentation shows certain financial information on an “as adjusted” basis, to

exclude the effect of certain items as described herein. By presenting “as adjusted”

results, management intends to provide investors with a better understanding of

the core results and underlying trends from which to consider past performance

and prospects for the future.

Users of this financial information should consider the types of events and

transactions for which adjustments have been made. “As adjusted” information

should not be considered in isolation or viewed as a substitute for, or superior to,

net income or other data prepared in accordance with GAAP as measures of our

operating performance or liquidity. In addition, the “as adjusted” information is not

necessarily comparable to similarly titled measures provided by other companies.

Pursuant to the requirements of Regulation G, we have attached a table that

reconciles the non-GAAP financial measures in this presentation to the most

directly comparable GAAP measures. The table is also available at

www.alleghenyenergy.com.

3

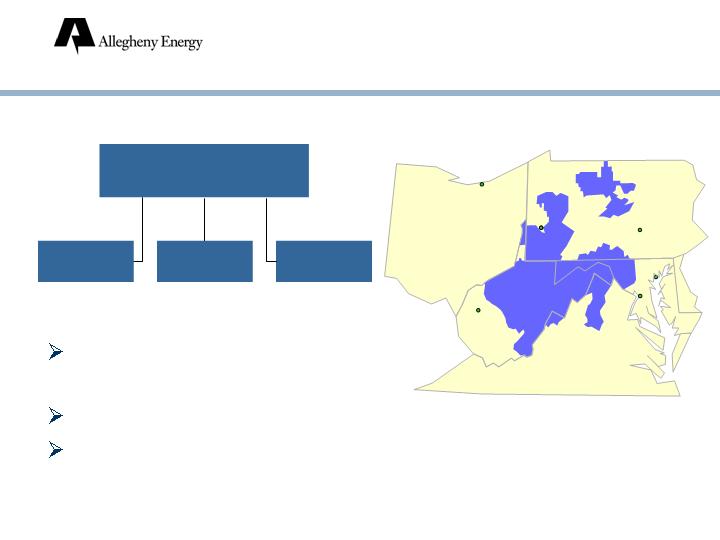

Allegheny Energy

Allegheny

Energy

Generation

Coal-fired, PJM

48.1 million MWH*

Delivery

1.6 million customers,

PA-MD-WV-VA

* 12 months ended December 31, 2005

4

Earnings Growth Drivers

Increase generation rates

Improve plant availability

Control O&M expense

Complete West Virginia rate case

Expand transmission system

Other growth catalysts

5

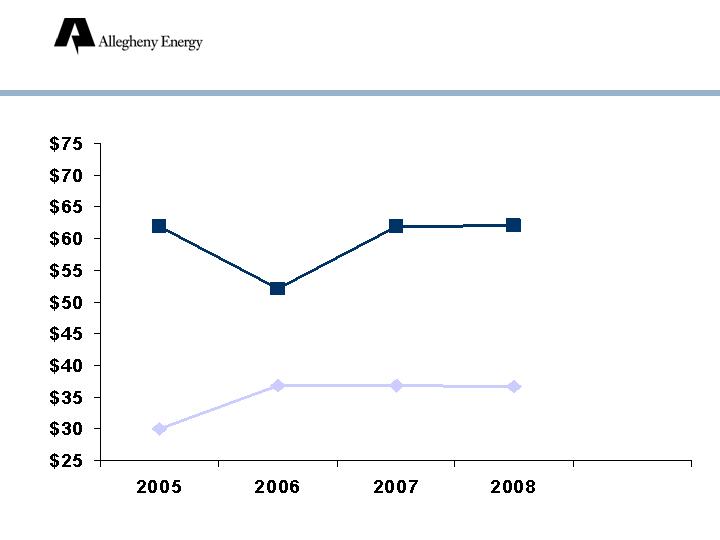

Pennsylvania POLR Rate

$ per MWH

Cumulative Increase in

Pre-Tax Operating Income

$ millions; estimates

Growth Driver:

Increase Generation Rates

6

Growth Driver:

Increase Generation Rates

July January

2007 2009

State Virginia Maryland

MWH transitioning 1.0 - 3.2 million* 3.5 million

to market-based rates

Increase in pre-tax income $20-60 million* $60 million

* annualized

7

2008

Goal

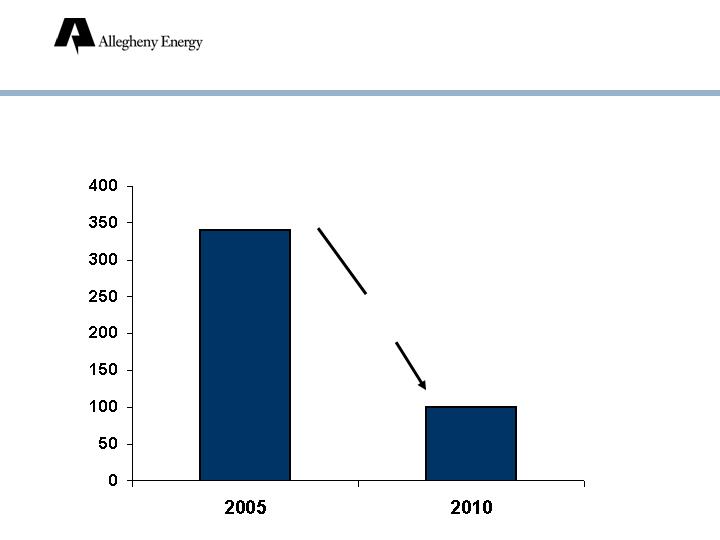

Supercritical Coal Units

Each 1% improvement provides benefit >$10 million

2006

Est.

Growth Driver:

Improve Plant Availability

2007

Goal

8

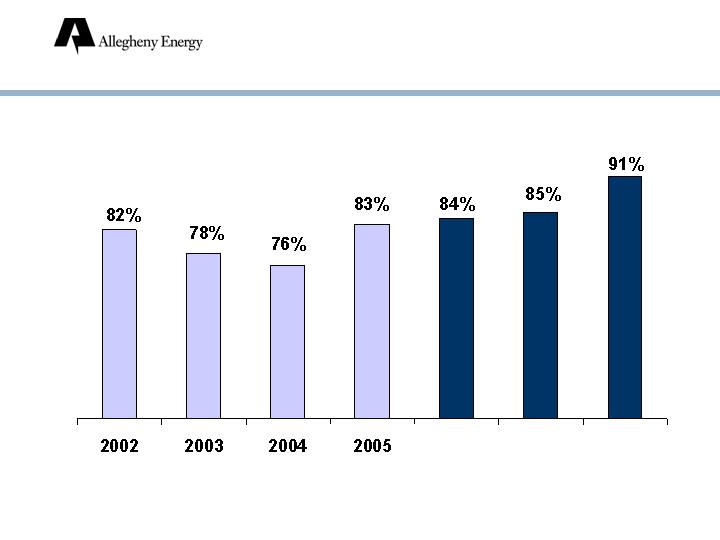

Achieve 91% Availability

Outage Factor

(supercritical units)

22%

24%

17%

16%

15%

9%

Reduce planned

outages

Reduce unplanned

outages

18%

9

2005

Ft. Martin 2

COMPLETED

PLANNED

Harrison 1

Harrison 3

Hatfield 1

Hatfield 3

Pleasants 2

Ft. Martin 1

Hatfield 2

Harrison 2

Pleasants 1

2006

2007

Improving Availability:

Conducting Extended Planned Outages

10

Unplanned Outage Factor

Units Which Completed Extended Outages

Planned Outages: Results

Pre-outage Post-outage

* Including transformer failure: Harrison 1 = 10%, average = 6%. Post-outage average is time weighted.

11

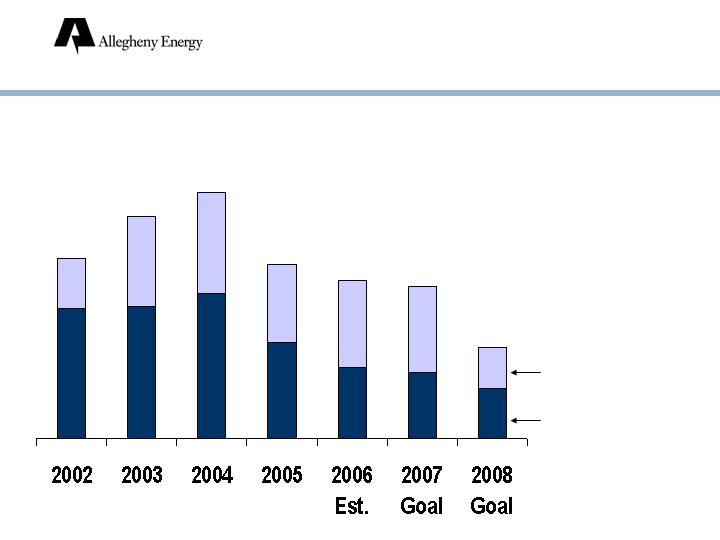

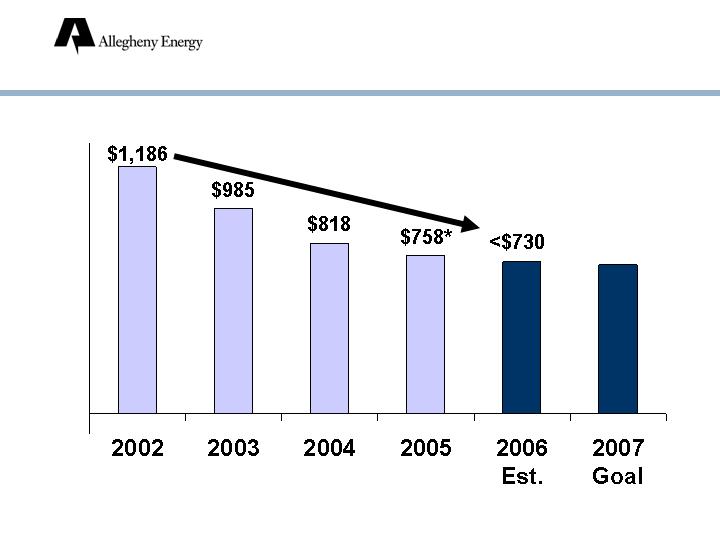

$700-730

Growth Driver:

Control O&M Expense

* 2005 = $775 after adjustment

($ millions)

12

Requested $100 million net increase

Fuel, purchased power: $126 million increase

Base rates: $26 million decrease

10% net increase (residential)

Requested reinstatement of fuel cost adjustment

Proposed ROE: 11.75%

Probable effective date: late May 2007

Growth Driver:

West Virginia Rate Case

13

Growth Driver:

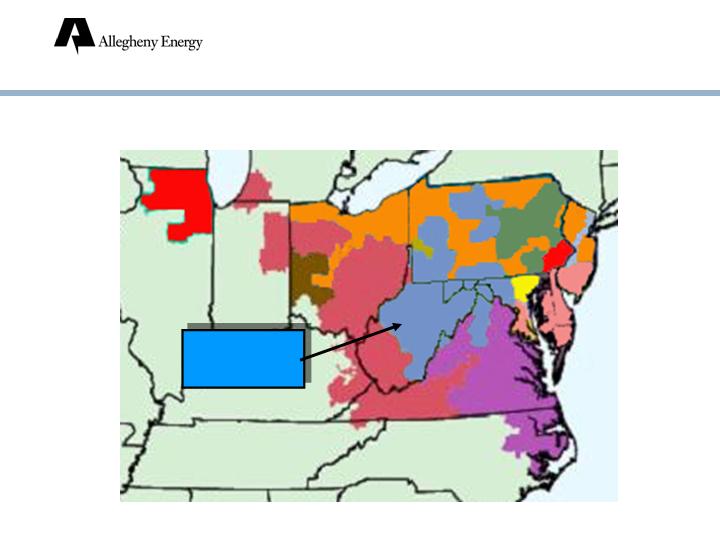

Expand Transmission System

Allegheny

Energy

Located In the Heart of PJM

14

Growth Driver:

Expand Transmission System

2007: enhance near-term reliability

Cost: $70 million

By 2011: construct ~210-mile line

Cost: over $850 million (preliminary estimate)

FERC approved incentive rate treatment,

including return during construction

Separate legal entity to own, construct

85% of costs recovered from other PJM

utilities

15

Approved Transmission Line

16

Potential for Additional

Transmission Investment

Most projects under

consideration pass

through Allegheny’s

service area

PJM to select best

solutions in early

2007

Under Consideration by PJM

for 2012-2021 Plan

17

Other Growth Catalysts

Projected PJM

Reserve Margin

Increasing marginal heat rate

Gas will more frequently impact PJM energy prices

Improving capacity values

16% PJM Target

18

Provides advance price signal for capacity needs

3-year forward auction market

Potentially significant benefits to Allegheny as POLR

contracts expire

FERC decision requested by late December 2006

Other Growth Catalysts

Proposed PJM Regional Pricing Model

19

Improve

Environmental Performance

By 2010:

One of the cleanest coal fleets in the U.S.

2009

$500 – 550

Ft. Martin Scrubbers

2009

~$650

Hatfield Scrubbers

2008

$110

Pleasants Bypass

IN

SERVICE

ESTIMATED

COST

($ Millions)

20

Improve

Environmental Performance

SO2 Emissions

(thousands of tons)

70%

reduction

21

Improving financial results

Reduced debt

Improving credit statistics

Contracting generation and coal

2007 earnings growth drivers

Financial Review

22

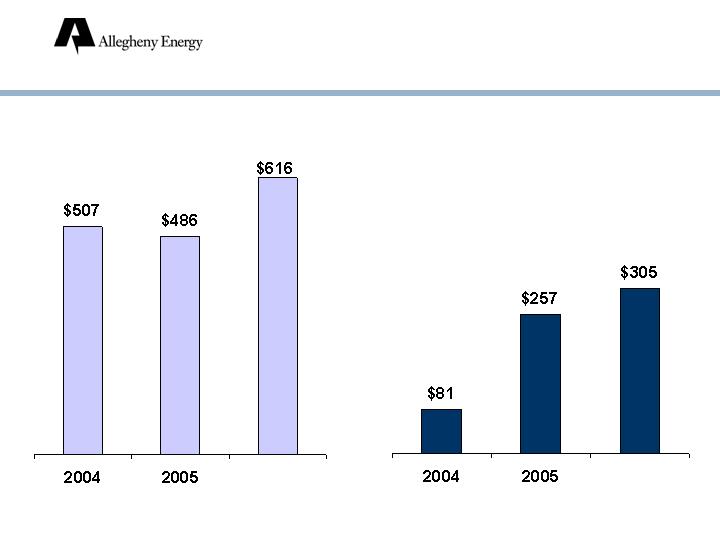

Improving Financial Results

Earnings per Share

2003

2005

2004

2006

9 mos.

($2.80)

($0.37)

($1.83)

$0.47

$0.40

$0.94

$1.51

$1.46

As Reported

As Adjusted

23

Cash Flow

($ millions)

Cash from Operations

as reported

Free Cash Flow

(adjusted cash from operations

net of capital expenditures)

2006

9 mos.

2006

9 mos.

24

Debt Outstanding

($ billions)

* $3.6 billion after $300 million maturity on October 1, 2006

25

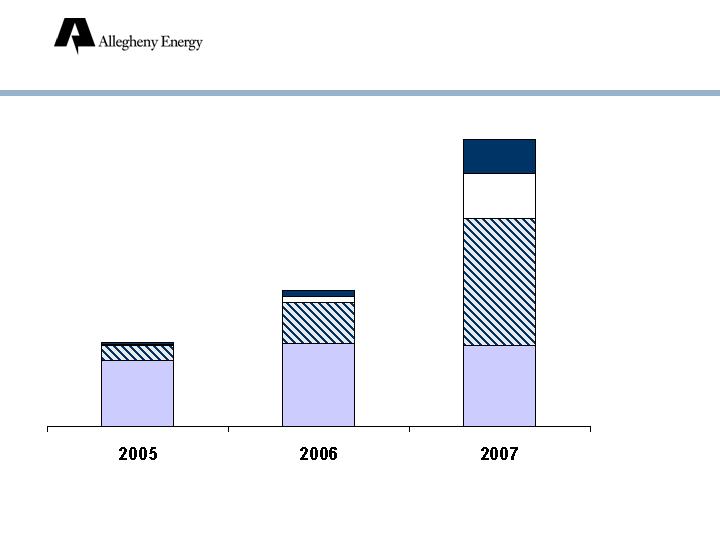

Capital Expenditures

($ millions)

$307

~$1,000

~$500

Environmental –

other

Environmental –

securitized

All other

Transmission

26

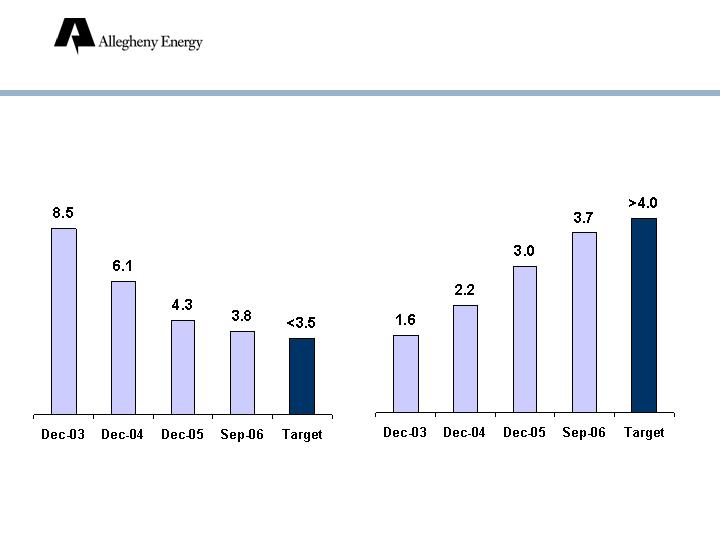

Debt/EBITDA*

EBITDA/Interest*

* Based on adjusted EBITDA and adjusted interest for 12-month periods. Excludes

securitized debt and interest.

Credit Statistics:

Targets Remain Unchanged

27

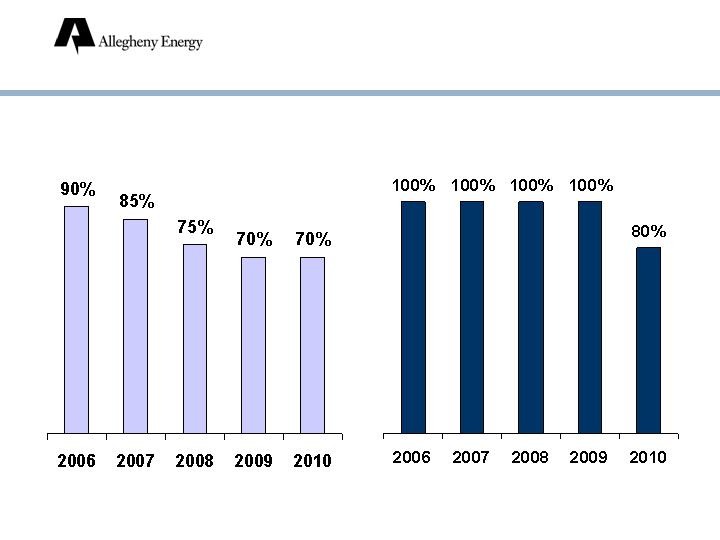

Contracting Generation

and Coal

Generation Under Contract

% of Total Projected Output

Coal Under Contract

% of Fixed-Price Commitments*

* Excludes West Virginia

28

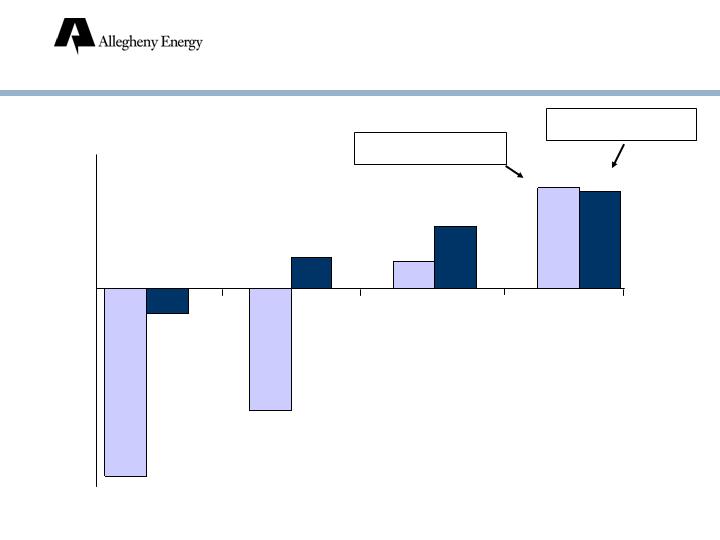

2007 Earnings Growth:

Key Drivers

*2007 vs. 2006 as adjusted

positive/negative

Other factors

10

Interest expense

(30)

Higher SO2 allowance costs

(45)

Higher coal prices

--

O&M expense

10

Plant availability

positive/negative

Market prices

10

Maryland customer credit

20

Virginia rates

60

West Virginia rate case

$50

Pennsylvania generation rates

CONTRIBUTION TO PRE-TAX INCOME*

($ millions; estimates)

29

Supplemental Information

30

Earnings (Loss) Per Share

0.56

0.65

Q3

0.22

0.18

Q2

$0.68

$0.67

2006: Q1

0.94

0.40

Year

0.02

0.02

Q4

0.45

0.21

Q3

0.08

(0.12)

Q2

$0.39

$0.29

2005: Q1

0.47

(1.83)

Year

0.22

0.48

Q4

0.37

(2.40)

Q3

(0.21)

(0.31)

Q2

$(0.03)

$0.25

2004: Q1

(0.37)

(2.80)

Year

(0.14)

(0.11)

Q4

0.11

(0.40)

Q3

$(0.23)

(1.82)

Q2

$(0.32)

$(0.46)

2003: Q1

As Adjusted

As Reported

31

EBITDA

286.3

286.3

Q3

193.6

193.6

Q2

$322.1

$322.1

2006: Q1

890.2

888.6

Year

162.1

162.1

Q4

274.2

254.7

Q3

192.7

210.6

Q2

$261.3

$261.3

2005: Q1

762.5

914.0

Year

221.8

312.7

Q4

243.2

243.2

Q3

122.0

110.3

Q2

$175.5

$247.8

2004: Q1

634.9

156.8

Year

185.6

197.4

Q4

225.3

117.3

Q3

150.1

(203.5)

Q2

$92.9

$77.6

2003: Q1

As Adjusted

As Reported

$ millions

Reported

32

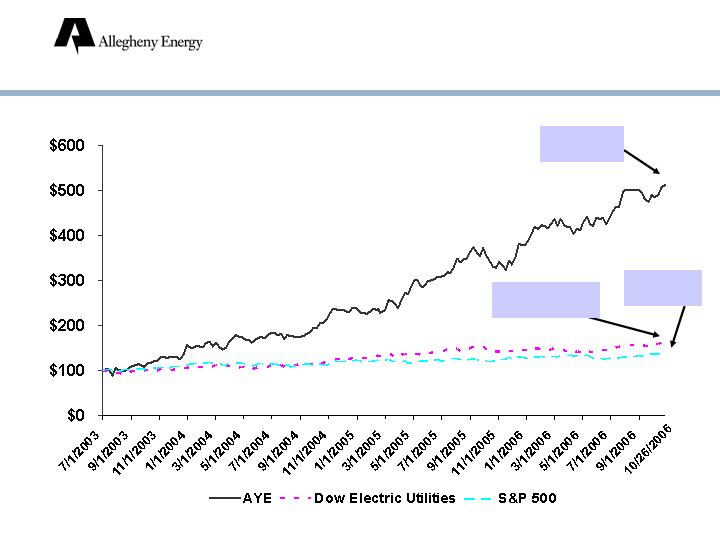

Stock Price Performance

$100 Invested on July 1, 2003

AYE: $512

Dow Electrics:

$164

S&P: $141

The Road to Growth

33

Enhance Operating Performance

Financial

Performance

Engaged

Employees

Environmental

Stewardship

Shareholder

Value

Operational

Excellence

VISION:

“To Be a Top Performing Utility by

Year-End 2007”

Customer

Satisfaction

34

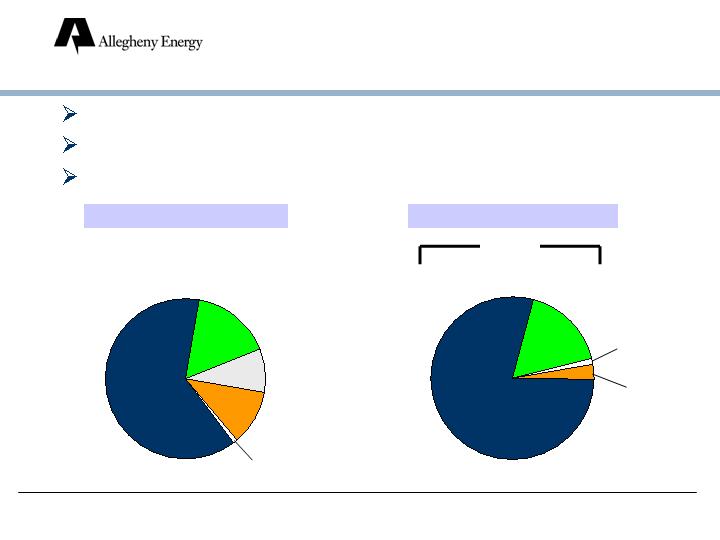

Generation and Marketing:

Overview

Capacity*

* Excludes Gleason peaking unit (held for sale). Output for year ended December 31, 2005.

Capacity: over 9,600 MW*

Primarily base load coal-fired plants

Located in PJM (13 states)

MWH Output*

Hydro

11%

Gas

9%

Supercritical

Coal

63%

Other Coal

16%

Oil

1%

Supercritical

Coal

79%

Gas

1%

Hydro

3%

Other Coal

17%

Coal

96%

35

Low-Cost Generation Fleet

Allegheny has an advantaged dispatch in PJM

PJM Dispatch Cost (Ozone Season): $/MWh

Allegheny Supercritical Coal Units

Dispatch Cost

Allegheny – Other Units

Assumptions: natural gas delivered at approximately $8.00/mmBTU; coal at approximately $2.75/mmBTU; SO 2

at $670/ton; NOx at $1,750/ton.

36

World’s largest competitive power market

Over 51 million people

700 million MWH of energy annually

163,500 MW of capacity

Nation’s most liquid spot power market

Model for FERC’s proposed Standard Market

Design

Provides transactional flexibility: contracts not

required

Generation and Marketing:

PJM -- An Attractive Market

37

Growth Driver:

Transition to Market-Based Rates

Market: Current*

POLR: Maryland

Generation Rates

$ per MWH

* As of October 9, 2006

38

Improving Performance,

Reducing Spending

O&M and Capital*

Unplanned outage

factor

High

Performance

Under-investment

Re-investment

Reduce

spending

* Special maintenance O&M and capital for supercritical coal units. Excludes environmental spending.

Goal

39

Exposure to

SO2 Allowance Market

SO2 Emissions

in Excess of Allowances

(tons; estimated as of October 2006)

* Approximately 75% of 2007 and 2008 short position is at Monongahela

Power

2006 -0-

2007 40,000*

2008 40,000 - 80,000*

40

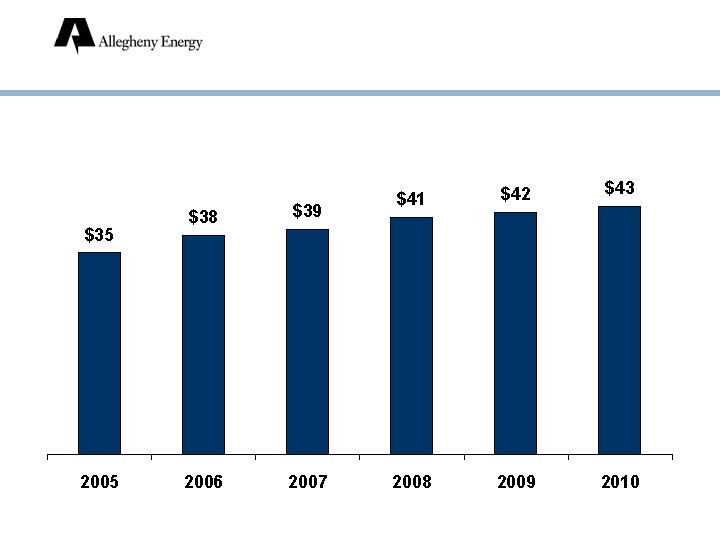

Coal:

Average Delivered Cost/Ton

Existing Contracts Only

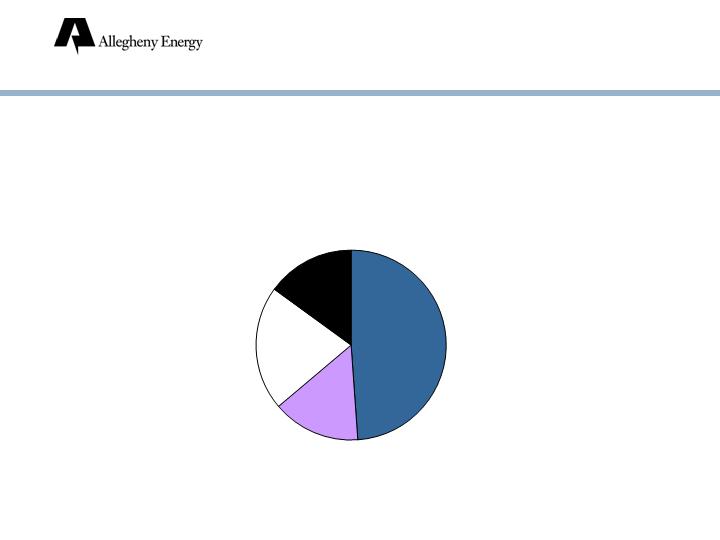

41

Only 15% of Coal

Delivered by Rail

Note: Some barge coal originates on short line railroads.

Rail

15%

Barge

49%

Conveyor

15%

Truck

21%

Coal Delivery Methods

2006

42

Delivery and Services:

Overview

In 4 states (PA, WV, MD,

VA)

1.6 million electric customers

Load growth: 2.0% compounded

annually (1995-2005; retail)

Allegheny Power

West Penn

Power

Monongahela

Power

Potomac

Edison

VIRGINIA

CHARLESTON

OHIO

HARRISBURG

MARYLAND

KENTUCKY

PENNSYLVANIA

CLEVELAND

BALTIMORE

PITTSBURGH

WASHINGTON, DC

WEST

VIRGINIA

43

Delivery and Services:

Retail Revenue Mix, 2005

By State

By Customer Class

Residential

43%

Industrial

31%

Commercial

25%

Other

1%

44

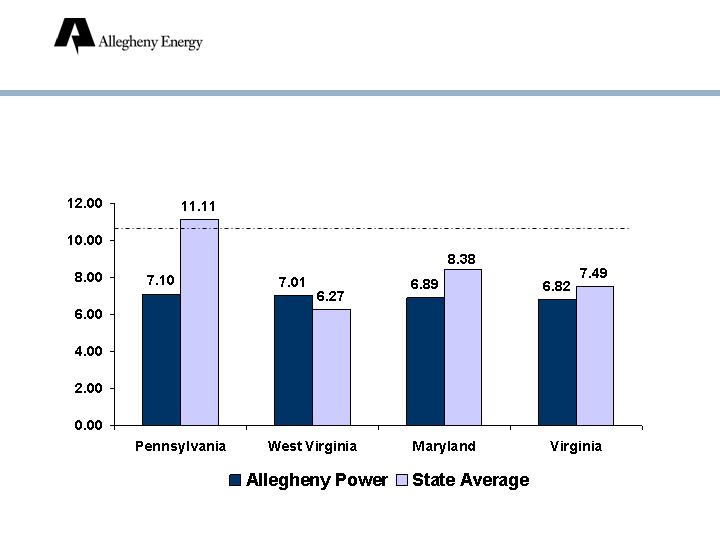

Delivery and Services:

Competitive Rates

National

Average =

10.62 ¢/kWh

Residential Rates

¢/kWh as of January 1, 2006

45

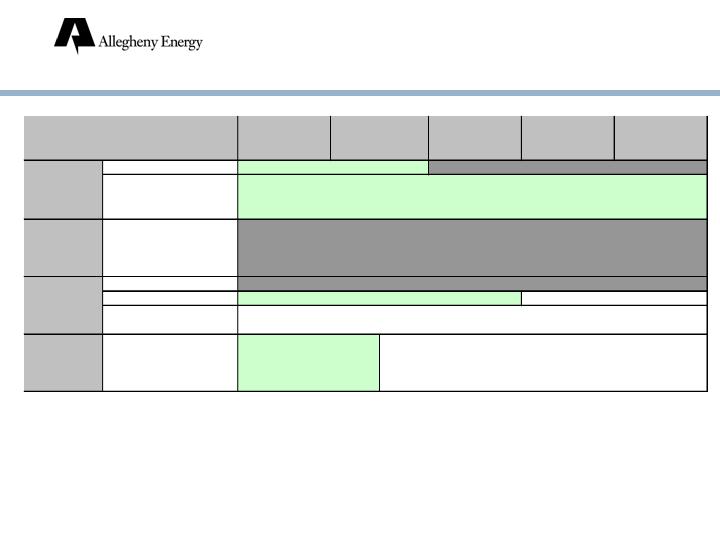

1 Generation rate caps include rate increases in each year, 2006-2010.

2 One-time T&D increase can be requested through 2007. After 2007, can

request recovery of purchased power and annual incremental T&D

reliability and environmental costs, and one additional T&D cost

increase.

Regulatory Timeline

46

2006

2008

2009

2010

T&D

Generation

T&D

Gen. - Res.

Through 2007

2

Gen. - Com. & Ind.

T&D

and

Generation

Regulated

Capped through 2008

Market-based

Market-based

Regulated

Distribution capped through 2007

Increases through 2010

1

2007

Through 2010

2

State

WV

T&D

and

Generation

Regulated

PA

MD

VA