UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

FOR ANNUAL AND TRANSITION REPORTS PURSUANT TO SECTIONS 13 OR

15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

| | x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) of the SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2006 |

OR

| | ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) of the SECURITIES EXCHANGE ACT OF 1934 |

| | | | |

Commission File Number | | Registrant; State of Incorporation; Address; and Telephone Number | | I.R.S. Employer Identification Number |

1-267 | | ALLEGHENY ENERGY, INC. | | 13-5531602 |

| | (A Maryland Corporation) | | |

| | 800 Cabin Hill Drive | | |

| | Greensburg, Pennsylvania 15601 | | |

| | Telephone (724) 837-3000 | | |

| | |

1-5164 | | MONONGAHELA POWER COMPANY | | 13-5229392 |

| | (An Ohio Corporation) | | |

| | 1310 Fairmont Avenue | | |

| | Fairmont, West Virginia 26554 | | |

| | Telephone (304) 366-3000 | | |

| | |

0-14688 | | ALLEGHENY GENERATING COMPANY | | 13-3079675 |

| | (A Virginia Corporation) | | |

| | 800 Cabin Hill Drive | | |

| | Greensburg, Pennsylvania 15601 | | |

| | Telephone (724) 837-3000 | | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| | | | | | |

Allegheny Energy, Inc. | | Yes | x | | No | ¨ |

Monongahela Power Company | | Yes | ¨ | | No | x |

Allegheny Generating Company | | Yes | ¨ | | No | x |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| | | |

Allegheny Energy, Inc. | | ¨ | |

Monongahela Power Company | | ¨ | |

Allegheny Generating Company | | ¨ | |

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) have been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrants’ knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer (as defined in Rule 12b-2 of the Act).

| | | | | | |

| | | Large accelerated filer | | Accelerated filer | | Non-accelerated filer |

Allegheny Energy, Inc. | | x | | ¨ | | ¨ |

Monongahela Power Company | | ¨ | | ¨ | | x |

Allegheny Generating Company | | ¨ | | ¨ | | x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

| | | | | | |

Allegheny Energy, Inc. | | Yes | ¨ | | No | x |

Monongahela Power Company | | Yes | ¨ | | No | x |

Allegheny Generating Company | | Yes | ¨ | | No | x |

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

Registrant | | Title of each class | | Name of each exchange on which registered |

Allegheny Energy, Inc. | | Common Stock,

$1.25 par value | | New York Stock Exchange

Chicago Stock Exchange |

| | |

Monongahela Power Company | | Cumulative Preferred Stock,

$100 par value:

4.40%

4.50%, Series C | | American Stock Exchange

American Stock Exchange |

|

Securities registered pursuant to Section 12(g) of the Act: |

| | |

Allegheny Generating Company | | Common Stock,

$1.00 par value | | None |

| | | | |

| | | Aggregate market value of voting and non-voting common equity held by nonaffiliates of the registrants at June 30, 2006 | | Number of shares of common stock of the registrants outstanding at February 20, 2007 |

Allegheny Energy, Inc. | | $6,095,989,273 | | 164,445,354 ($1.25 par value) |

Monongahela Power Company | | None (a) | | 5,891,000 ($50 par value) |

Allegheny Generating Company | | None (b) | | 1,000 ($1.00 par value) |

| (a) | All outstanding common stock is held by Allegheny Energy, Inc. |

| (b) | All outstanding common stock is held by Allegheny Generating Company’s parent companies, Monongahela Power Company and Allegheny Energy Supply Company, LLC. |

Documents Incorporated by Reference

Portions of the Allegheny Energy, Inc. definitive Proxy Statement for its 2007 Annual Meeting of Stockholders are incorporated by reference to Part III of this Annual Report on Form 10-K.

GLOSSARY

| I. | The following abbreviations and terms are used in this report to identify Allegheny Energy, Inc. and its subsidiaries: |

| | |

ACC | | Allegheny Communications Connect, Inc., a subsidiary of Allegheny Ventures |

AE | | Allegheny Energy, Inc., a diversified utility holding company |

AESC | | Allegheny Energy Service Corporation, a subsidiary of AE |

AE Solutions | | Allegheny Energy Solutions, Inc., a subsidiary of Allegheny Ventures |

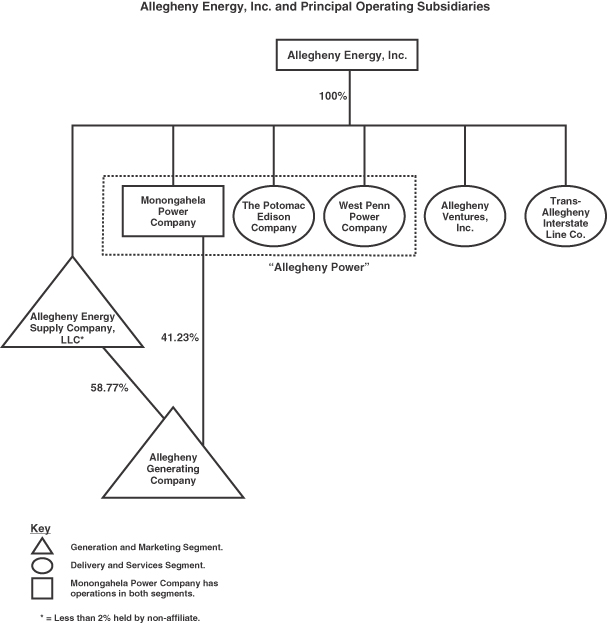

AE Supply | | Allegheny Energy Supply Company, LLC, an unregulated generation subsidiary of AE |

AGC | | Allegheny Generating Company, an unregulated generation subsidiary of AE Supply and Monongahela |

Allegheny | | Allegheny Energy, Inc., together with its consolidated subsidiaries |

Allegheny Ventures | | Allegheny Ventures, Inc., a nonutility, unregulated subsidiary of AE |

Distribution Companies | | Collectively, Monongahela, Potomac Edison and West Penn, which do business as Allegheny Power |

Green Valley Hydro | | Green Valley Hydro, LLC, a subsidiary of AE |

Monongahela | | Monongahela Power Company, a regulated subsidiary of AE |

Potomac Edison | | The Potomac Edison Company, a regulated subsidiary of AE |

Registrants | | Collectively, AE, Monongahela and AGC |

TrAIL Company | | Trans-Allegheny Interstate Line Company |

West Penn | | West Penn Power Company, a regulated subsidiary of AE |

| II. | The following abbreviations and acronyms are used in this report to identify entities and terms relevant to Allegheny’s business and operations: |

| | |

BTU | | British Thermal Unit |

CDD | | Cooling Degree-Days |

CDWR | | California Department of Water Resources |

Clean Air Act | | Clean Air Act of 1970 |

DOE | | United States Department of Energy |

EPA | | United States Environmental Protection Agency |

Energy Policy Act | | Energy Policy Act of 2005 |

Exchange Act | | Securities Exchange Act of 1934, as amended |

FERC | | Federal Energy Regulatory Commission, an independent commission within the DOE |

FPA | | Federal Power Act |

GAAP | | Generally accepted accounting principles used in the United States of America |

HDD | | Heating Degree-Days |

KW | | Kilowatt, which is equal to 1,000 watts |

kWh | | Kilowatt-hour, which is a unit of electric energy equivalent to one KW operating for one hour |

Maryland PSC | | Maryland Public Service Commission |

MW | | Megawatt, which is equal to 1,000,000 watts |

MWh | | Megawatt-hour, which is a unit of electric energy equivalent to one MW operating for one hour |

NSR | | The New Source Performance Review Standards, or “New Source Review,” applicable to facilities deemed “new” sources of emissions by the EPA |

OVEC | | Ohio Valley Electric Corporation |

Pennsylvania PUC | | Pennsylvania Public Utility Commission |

PJM | | PJM Interconnection, L.L.C., a regional transmission organization |

PLR | | Provider-of-last-resort |

PURPA | | Public Utility Regulatory Policies Act of 1978 |

RTO | | Regional Transmission Organization |

SEC | | Securities and Exchange Commission |

SOS | | Standard Offer Service |

T&D | | Transmission and distribution |

Virginia SCC | | Virginia State Corporate Commission |

West Virginia PSC | | Public Service Commission of West Virginia |

CONTENTS

THIS COMBINED FORM 10-K IS SEPARATELY FILED BY ALLEGHENY ENERGY, INC., MONONGAHELA POWER COMPANY AND ALLEGHENY GENERATING COMPANY. INFORMATION CONTAINED HEREIN RELATING TO ANY INDIVIDUAL REGISTRANT IS FILED BY THE REGISTRANT ON ITS OWN BEHALF. NONE OF THE REGISTRANTS MAKES ANY REPRESENTATION AS TO INFORMATION RELATING TO THE OTHER REGISTRANTS.

PART I

ITEM 1. BUSINESS

OVERVIEW

Allegheny is an integrated energy business that owns and operates electric generation facilities and delivers electric services to customers in Pennsylvania, West Virginia, Maryland and Virginia. AE, Allegheny’s parent holding company, was incorporated in Maryland in 1925. Allegheny operates its business primarily through AE’s various directly and indirectly owned subsidiaries.

Allegheny has two business segments:

| | • | | The Delivery and Services segment includes Allegheny’s electric T&D operations. |

| | • | | The Generation and Marketing segment includes Allegheny’s power generation operations. |

The Delivery and Services Segment

The principal companies and operations in AE’s Delivery and Services segment include the following:

| | • | | The Distribution Companies include Monongahela (excluding its West Virginia generation assets), Potomac Edison and West Penn. Each of the Distribution Companies is a public utility company and does business under the trade name Allegheny Power. Allegheny Power’s principal business is the operation of electric public utility systems. |

| | • | | Monongahela was incorporated in Ohio in 1924. It conducts an electric T&D business that serves approximately 375,000 customers in northern West Virginia in a service area of approximately 12,400 square miles with a population of approximately 776,000. Monongahela’s Delivery and Services segment had operating revenues of $674.9 million and sold 10,351 million kWhs of electricity to retail customers in 2006. Monongahela also owns generation assets, which are included in the Generation and Marketing Segment. See “The Generation and Marketing Segment” below. Monongahela conducted electric T&D operations in Ohio and natural gas T&D operations in West Virginia until it sold the assets related to these operations on December 31, 2005 and September 30, 2005, respectively. Monongahela agreed to sell power at a fixed price to Columbus Southern Power Company (“Columbus Southern”), the purchaser of its electric T&D operations in Ohio, to serve Monongahela’s former Ohio customers until May 31, 2007. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Asset Sales” below. |

| | • | | Potomac Edison was incorporated in Maryland in 1923 and was also incorporated in Virginia in 1974. It operates an electric T&D system in portions of West Virginia, Maryland and Virginia. Potomac Edison serves approximately 466,600 customers in a service area of about 7,300 square miles with a population of approximately 1.02 million. Potomac Edison had total operating revenues of $856.0 million and sold 12,902 million kWhs of electricity to retail customers in 2006. |

| | • | | West Penn was incorporated in Pennsylvania in 1916. It operates an electric T&D system in southwestern, south-central and northern Pennsylvania. West Penn serves approximately 707,000 |

6

| | customers in a service area of about 9,900 square miles with a population of approximately 1.5 million. West Penn had total operating revenues of $1,210.5 million and sold 19,926 million kWhs of electricity to retail customers in 2006. |

In April 2002, the Distribution Companies transferred functional control over their transmission systems to PJM. See “The Distribution Companies’ Obligations and the PJM Market” below.

| | • | | TrAIL Company was incorporated in Maryland and Virginia in 2006 following PJM’s approval of a regional transmission expansion plan designed to maintain the reliability of the transmission grid in the Mid-Atlantic region. The transmission expansion plan includes a new, 240-mile 500 kV transmission line, 210 miles of which is to be located in the Distribution Companies’ PJM zone. PJM designated Allegheny to construct the portion of the line that will be located in the Distribution Companies’ PJM zone. TrAIL Company was formed in connection with the management and financing of transmission expansion projects, including this project (the “TrAIL Project”), and will own and operate the new transmission line. |

| | • | | Allegheny Ventures is a nonutility, unregulated subsidiary of AE that was incorporated in Delaware in 1994. Allegheny Ventures engages in telecommunications and unregulated energy-related projects. Allegheny Ventures has two principal wholly-owned subsidiaries, ACC and AE Solutions. Both ACC and AE Solutions are Delaware corporations. ACC develops fiber-optic projects, including fiber and data services. AE Solutions manages energy-related projects. Allegheny Ventures had total operating revenues of $6.6 million in 2006. |

During 2006, the Delivery and Services segment had operating revenues of $2,717.7 million and net income of $179.4 million. As of December 31, 2006, the Delivery and Services segment held $4.1 billion of identifiable assets. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 9, “Business Segments,” to the Consolidated Financial Statements.

The Generation and Marketing Segment

The principal companies and operations in AE’s Generation and Marketing segment include the following:

| | • | | AE Supply is a Delaware limited liability company formed in 1999. AE Supply owns, operates and manages electric generation facilities. AE Supply also purchases and sells energy and energy-related commodities. As of December 31, 2006, AE Supply owned or contractually controlled approximately 7,535 MWs of generation capacity. Effective as of January 1, 2007, AE Supply and Monongahela completed an intra-company transfer of assets (the “Asset Swap”) that realigned generation ownership and contractual arrangements within the Allegheny system. As discussed in greater detail under the heading “Electric Facilities” below, the purpose of the Asset Swap was to enable the securitization financing of a majority of the costs associated with the installation of flue gas desulfurization units and related pollution control equipment (“Scrubbers”) at Monongahela’s Fort Martin generation facility. Immediately following the Asset Swap, AE Supply owned or contractually controlled 6,876 MWs of generation capacity. See “Electric Facilities” below. |

AE Supply markets its electric generation capacity to various customers and markets. Currently, the majority of the Generation and Marketing segment’s normal operating capacity is committed to supplying the PLR and other obligations of the Distribution Companies. AE Supply had total operating revenues of $1,492.9 million in 2006.

| | • | | Monongahela’s West Virginia generation assets are included in the Generation and Marketing segment. As of December 31, 2006, Monongahela owned or contractually controlled 2,135 MWs of generation capacity. Immediately following the Asset Swap, Monongahela owned or contractually controlled 2,794 MWs of generation capacity. See “Electric Facilities” below. |

Monongahela’s generation capacity supplies Monongahela’s Delivery and Services segment. In addition, in connection with the Asset Swap, AE Supply assigned to Monongahela its obligation to

7

supply generation to meet Potomac Edison’s load obligations in West Virginia. Monongahela’s Generation and Marketing segment had operating revenues of $401.1 million in 2006.

| | • | | AGC was incorporated in Virginia in 1981. As of December 31, 2006, AGC was owned approximately 77% by AE Supply and approximately 23% by Monongahela. As a result of the Asset Swap, AGC currently is owned approximately 59% by AE Supply and approximately 41% by Monongahela. AGC’s sole asset is a 40% undivided interest in the Bath County, Virginia pumped-storage hydroelectric generation facility and its connecting transmission facilities. All of AGC’s revenues are derived from sales of its 1,035 MW share of generation capacity from the Bath County generation facility to AE Supply and Monongahela. AGC had total operating revenues of $65.3 million in 2006. See “Electric Facilities” below. |

AE Supply is contractually obligated to provide Potomac Edison and West Penn with the power that they need to meet a majority of their PLR obligations.Monongahela is contractually obligated to provide Potomac Edison with the power that it needs to meet its load obligations in West Virginia. To facilitate the economic dispatch of generation, AE Supply and Monongahela sell power into the PJM market and purchase power from the PJM market to meet their obligations under these contracts. See “The Distribution Companies’ Obligations and the PJM Market” and “Fuel, Power and Resource Supply” below.

During 2006, the Generation and Marketing segment had operating revenues of $1,834.4 million and net income of $139.9 million. As of December 31, 2006, the Generation and Marketing segment held $4.1 billion of identifiable assets. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 9, “Business Segments,” to the Consolidated Financial Statements.

Intersegment Services

AESC was incorporated in Maryland in 1963 as a service company for AE. AESC employs substantially all of the employees who provide services to AE, AE Supply, AGC, the Distribution Companies, Allegheny Ventures, TrAIL Company and their respective subsidiaries. These companies reimburse AESC at cost for services provided to them by AESC’s employees. AESC had 4,362 employees as of December 31, 2006.

The Distribution Companies’ Obligations and the PJM Market

Allegheny’s business has been significantly influenced by state and federal deregulation initiatives, including the implementation of retail choice and plans to transition from cost-based to market-based rates, as well as by the development of wholesale electricity markets and RTOs, particularly PJM.

Each of the states in Allegheny’s service territory other than West Virginia has, to some extent, deregulated its electric utility industry. Pennsylvania, Maryland and Virginia have instituted retail customer choice and are transitioning to market-based, rather than cost-based pricing for generation, although recent legislation under consideration in Virginia proposes some degree of re-regulation. In West Virginia, the rates charged to retail customers are regulated by the West Virginia PSC and are determined through traditional, cost-based, regulated utility rate-making.

West Penn has PLR obligations to its customers in Pennsylvania. Potomac Edison has PLR obligations to its customers in Virginia and its residential customers in Maryland. As “providers of last resort,” West Penn and Potomac Edison must supply power to certain retail customers who have not chosen alternative suppliers (or have chosen to return to Allegheny service) at rates that are capped at various levels during the applicable transition period. The transition periods vary across Allegheny’s service area and across customer class:

| | • | | Potomac Edison. In Maryland, the transition period for residential customers ends on December 31, 2008. The transition period for commercial and industrial customers ended on December 31, 2004. The generation rates that Potomac Edison charges residential customers in Maryland are capped through |

8

| | December 31, 2008, while the T&D rate caps for all customers expired on December 31, 2004. A statewide settlement approved by the Maryland PSC in 2003 extends Potomac Edison’s obligation to provide residential “standard offer service” (“SOS”) at market prices beyond the expiration of the transition periods. In December 2006, Potomac Edison proposed a rate stabilization and transition plan for its residential customers in Maryland that is intended to gradually transition customers from capped generation rates to generation rates based on market prices, while at the same time preserving for customers the benefit of previous rate caps. In Virginia, the transition period ends on December 31, 2010. See “Regulatory Framework Affecting Allegheny” below. |

| | • | | West Penn. In Pennsylvania, the transition period ends on December 31, 2010. As part of a May 2005 order approving a settlement, the Pennsylvania PUC extended Pennsylvania’s generation rate caps from 2008 to 2010. The settlement approved by the Pennsylvania PUC also extended distribution rate caps from 2005 to 2007, with an additional rate cap in place for 2009 at the rate in effect on January 1, 2009, and provided for increases in generation rates in 2007, 2009 and 2010, in addition to previously-approved increases for 2006 and 2008. Rate caps on transmission services expired on December 31, 2005. See “Regulatory Framework Affecting Allegheny” below. |

These transition periods could be altered by legislative, judicial or, in some cases, regulatory actions. See “Regulatory Framework Affecting Allegheny” below.

Potomac Edison and West Penn have contracts with AE Supply under which AE Supply provides Potomac Edison and West Penn with the majority of the power necessary to meet their PLR obligations. Additionally, Potomac Edison has a contract with Monongahela under which Monongahela provides Potomac Edison with the power necessary to meet its load obligations in West Virginia.

All of Allegheny’s generation facilities are located within the PJM market, and all of the power that the Generation and Marketing segment generates is sold into the PJM market. To facilitate the economic dispatch of generation, AE Supply and Monongahela sell the power that they generate into the PJM market and purchase from the PJM market the power necessary to meet their obligations to supply power.

In connection with the sale of its electric T&D operations in Ohio, Monongahela agreed to sell power at a fixed price to Columbus Southern to serve Monongahela’s former Ohio customers through May 2007. Monongahela purchases the power required to meet this obligation from the PJM market.

As an RTO, PJM coordinates the movement of electricity over the transmission grid in all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia. In April 2002, the Distribution Companies transferred functional control over their transmission systems to PJM.

For a more detailed discussion, see “Fuel, Power and Resource Supply,” “Regulatory Framework Affecting Allegheny” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview” below.

Initiatives and Achievements

Allegheny’s long-term strategy is to focus on its core generation and T&D businesses. Allegheny’s management believes that this emphasis is enabling Allegheny to take advantage of its regional presence, operational expertise and knowledge of its markets to grow earnings and add shareholder value.

Significant initiatives and recent achievements include:

| | • | | Pursuing Transmission Expansion. In June 2006, PJM approved a regional transmission expansion plan designed to maintain the reliability of the transmission grid in the Mid-Atlantic region that includes |

9

| | a new, 240-mile extra high-voltage transmission line extending from southwestern Pennsylvania, through West Virginia to northern Virginia, 210 miles of which is to be located in the Distribution Companies’ PJM zone. The line is designed to alleviate future reliability concerns and increase the west to east transmission capability of the PJM transmission system. PJM designated Allegheny to construct the portion of the line that will be located in the Distribution Companies’ PJM zone. Additionally, FERC approved four incentive rate treatments, which are intended to promote the construction of transmission facilities, for the transmission line, and PJM has requested that the DOE designate the project as a National Interest Electric Transmission Corridor. Allegheny currently is in the process of siting the transmission line and will seek requisite permits and regulatory approvals. PJM is considering additional transmission expansion initiatives, a number of which, as contemplated, would pass through Allegheny’s service territory. |

| | • | | Managing Environmental Compliance and Risks. Allegheny is working to effectively manage its environmental compliance efforts to ensure continuing compliance with applicable federal and state regulations while controlling its compliance costs, reducing emissions levels and minimizing its risk exposure. |

Among other initiatives, AE Supply and Monongahela are currently blending lower-sulfur Powder River Basin (“PRB”) coal at several generation facilities and are working to implement the financing and construction of Scrubbers at the Hatfield’s Ferry generation facility in Pennsylvania and the Fort Martin generation facility in West Virginia, as well as other pollution control projects at other facilities. In 2006, Monongahela and Potomac Edison received approval from the West Virginia PSC to finance the majority of the cost of constructing Scrubbers at the Fort Martin generation facility through the securitization of a customer charge. Effective January 1, 2007, Allegheny completed the Asset Swap, an intra-company transfer of assets that realigned generation ownership and contractual arrangements within the Allegheny system in a manner that will facilitate the proposed securitization and the construction of the Fort Martin Scrubbers. In July 2006, AE Supply entered into construction contracts in connection with its plans to install Scrubbers at its Hatfield’s Ferry generation facility. See “Environmental Matters” and “Electric Facilities” below.

| | • | | Managing Transition to Market-based Rates. In 2005, Allegheny successfully implemented a plan to transition Pennsylvania customers to generation rates based on market prices through increases in applicable rate caps in 2007, 2009 and 2010 and a two-year extension of the applicable transition period. Together with previously approved rate cap increases for 2006 and 2008, these increases will gradually move generation rates in Pennsylvania closer to market prices. |

Allegheny is actively working to effectively manage a similar transition in Maryland. In December 2006, Allegheny filed a proposal with the Maryland PSC to transition residential customers from capped generation rates to generation rates based on market prices beginning in 2007 and ending in 2010. Under the proposed plan, residential customers would pay a distribution surcharge beginning on March 31, 2007. The proposed plan, including the application of the surcharge, would result in an overall rate increase of approximately 15% annually from 2007 to 2010. With the expiration of the residential generation rate caps and the move to generation rates based on market prices on January 1, 2009, the surcharge would convert to a credit on customers’ bills. Funds collected through the surcharge during 2007 and 2008, plus interest, would be returned to customers as a credit on their electric bills, thereby reducing the effect of the rate cap expiration. The credit would continue, with adjustments, to maintain rate stability until December 31, 2010. Following public hearings, Allegheny filed an alternate proposal that would, among other things, provide customers with the ability to opt out of the surcharge. See “Regulatory Framework Affecting Allegheny” and “Fuel, Power and Resource Supply” below.

| | • | | Maximizing Generation Value. Allegheny is working to maximize the value of the power that it generates by ensuring full recovery of its costs and a reasonable return through the traditional rate-making process for its regulated utilities, as well as through the transition to market prices for AE Supply and its subsidiaries. |

10

For example, in July 2006, Monongahela and Potomac Edison filed a request with the West Virginia PSC to increase their West Virginia retail rates by approximately $100 million annually. If approved by the West Virginia PSC, this proposal would result in, among other things, a $126 million increase in rates related to fuel and purchased power costs, including reinstatement of a fuel cost recovery clause, and a $26 million decrease in base rates. See “Risks Relating to Regulation” below.

As discussed above, in April 2005, Allegheny obtained approval from the Pennsylvania PUC for increases in applicable rate caps in 2007, 2009 and 2010 in connection with a two-year extension of the period during which Pennsylvania customers will transition to market prices. In addition, AE Supply won the contracts to serve the PLR customer load in Pennsylvania in 2009 and 2010 and entered into contracts to provide power to Potomac Edison to serve commercial, industrial and municipal customer loads in Maryland.

| | • | | Maximizing Operational Efficiency. Allegheny is working to maximize the availability and operational efficiency of its physical assets, particularly its supercritical generation facilities (those that utilize steam pressure in excess of 3,200 pounds per square inch). In 2007, Allegheny expects to complete a program, which it began in 2005, of planned extended maintenance outages at each of its 10 supercritical generating units, targeted at improving availability at those units. The units for which this planned maintenance has been completed already demonstrate improved performance. |

Allegheny also is seeking to optimize operations and maintenance costs for its other generation facilities, T&D assets and related corporate functions, to reduce costs and to pursue other productivity improvements necessary to build a high performance organization.

For example, in January 2007, Allegheny successfully implemented an enterprise resource planning system as part of its program to improve its processes and technology. As part of the same initiative, Allegheny entered into an agreement in 2005 to outsource many of its information technology functions.

Additionally, Allegheny has entered into various coal supply contracts in an effort to ensure a consistent supply of coal at predictable prices, and currently has contracts in place for the delivery of approximately 96% of its expected coal needs for 2007. See “Fuel, Power and Resource Supply” below.

| | • | | Achieving and Maintaining High Customer Satisfaction. Allegheny continues to see high levels of satisfaction among its customers. For example, a leading independent survey firm ranked Allegheny first in customer satisfaction for residential customers in the eastern United States, as well as first among commercial and industrial customers in the northeast. |

| | • | | Substantially Reducing and Proactively Managing Debt. Between December 1, 2003 and December 31, 2006, Allegheny restructured much of its debt and reduced debt by approximately $2.425 billion. This restructuring effort included debt reductions of approximately $918 million in 2005 and $517 million in 2006. |

Through these restructuring efforts, Allegheny secured more favorable terms and conditions with respect to much of its debt, including reduced interest rates. The resulting reductions in interest expense, coupled with the reductions in debt and general improvements in Allegheny’s financial condition, have led to multiple upgrades in Allegheny’s credit ratings. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Changes in Credit Ratings” below and Note 4, “Capitalization,” to the Consolidated Financial Statements.

| | • | | Improving Liquidity. Allegheny has improved its liquidity through prudent cash management, opportunistic sales of non-core assets, cutting costs and expenses, extending debt maturities and other financing strategies. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources” below and Note 4, “Capitalization,” to the Consolidated Financial Statements. |

| | • | | Disposing of Non-Core Assets. Allegheny has reoriented its business to focus on its core businesses and assets. With the 2006 sale of its Gleason generation facility for approximately $23 million and of a |

11

| | related receivable for approximately $27 million, Allegheny completed its initiative to sell its significant non-core assets. Since 2004, Allegheny has completed a number of other significant sales of non-core assets, including: |

| | • | | the September 2005 sale by Monongahela of its West Virginia natural gas T&D business for cash proceeds of approximately $161 million and the assumption by the purchaser of approximately $87 million of debt; |

| | • | | the August 2005 sale by AE Supply of its Wheatland generation facility for approximately $100 million; |

| | • | | the December 2004 sale by AE Supply of its Lincoln generation facility and an accompanying tolling agreement for approximately $175 million; and |

| | • | | the December 2004 sale by AE of a 9% interest in OVEC (AE continues to hold a 3.5% interest in OVEC) for $102 million in cash, of which approximately $96 million was received at the closing of the transaction and approximately $6 million was released from escrow and received in 2006, upon the satisfaction of certain conditions. |

In addition, in December 2005, Monongahela sold its electric T&D operations in Ohio for net cash proceeds of approximately $52 million.

See “Management’s Discussion and Analysis of Financial Condition and Results of Operations— Liquidity and Capital Resources—Asset Sales” below and Note 7, “Discontinued Operations,” to the Consolidated Financial Statements.

Management’s priorities for 2007 include continued focus on improving operations, managing the transition to market-based rates and expanding Allegheny’s transmission system.

12

Where You Can Find More Information

AE, Monongahela and AGC file or furnish Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements (for AE) and other information with or to the SEC. You may read and copy any document that the Registrants file with the SEC at the SEC’s public reference room at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. These SEC filings are also available to the public from the SEC’s website athttp://www.sec.gov.

The Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements, statements of changes in beneficial ownership and other SEC filings, and any amendments to those reports, that AE, Monongahela and AGC file with or furnish to the SEC under the Exchange Act are made available free of charge on AE’s website athttp://www.alleghenyenergy.com as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. Audited annual financial statements for AE Supply, Potomac Edison and West Penn, none of which are reporting companies under the Exchange Act, also will be available on AE’s website. AE’s website and the information contained therein are not incorporated into this report.

13

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

In addition to historical information, this report contains a number of forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. Words such as anticipate, expect, project, intend, plan, believe and words and terms of similar substance used in connection with any discussion of future plans, actions or events identify forward-looking statements. These include statements with respect to:

| | • | | rate regulation and the status of retail generation service supply competition in states served by the Distribution Companies; |

| | • | | demand for energy and the cost and availability of raw materials, including coal; |

| | • | | PLR and power supply contracts; |

| | • | | internal controls and procedures; |

| | • | | status and condition of plants and equipment; |

| | • | | changes in technology and their effects on the competitiveness of Allegheny’s generation facilities; |

| | • | | work stoppages by Allegheny’s unionized employees; |

| | • | | capacity purchase commitments; and |

Forward-looking statements involve estimates, expectations and projections and, as a result, are subject to risks and uncertainties. There can be no assurance that actual results will not differ materially from expectations. Actual results have varied materially and unpredictably from past expectations. Factors that could cause actual results to differ materially include, among others, the following:

| | • | | plant performance and unplanned outages; |

| | • | | volatility and changes in the price of power, coal, natural gas and other energy-related commodities; |

| | • | | general economic and business conditions; |

| | • | | changes in access to capital markets; |

| | • | | complications or other factors that make it difficult or impossible to obtain necessary lender consents or regulatory authorizations on a timely basis; |

| | • | | environmental regulations; |

| | • | | the results of regulatory proceedings, including proceedings related to rates; |

| | • | | changes in industry capacity, development and other activities by Allegheny’s competitors; |

| | • | | changes in the weather and other natural phenomena; |

| | • | | changes in the underlying inputs and assumptions, including market conditions, used to estimate the fair values of commodity contracts; |

| | • | | changes in customer switching behavior and their resulting effects on existing and future PLR load requirements; |

| | • | | changes in laws and regulations applicable to Allegheny, its markets or its activities; |

14

| | • | | the loss of any significant customers or suppliers; |

| | • | | dependence on other electric transmission and gas transportation systems and their constraints on availability; |

| | • | | inflationary and interest rate trends; |

| | • | | the implementation of Allegheny’s outsourcing initiative or new enterprise resource planning system; |

| | • | | the possibility of adverse consequences arising from governmental audits of Allegheny’s tax returns; |

| | • | | changes in market rules, including changes to PJM’s participant rules and tariffs; |

| | • | | the effect of accounting pronouncements issued periodically by accounting standard-setting bodies and accounting issues facing Allegheny; and |

| | • | | the continuing effects of global instability, terrorism and war. |

15

ALLEGHENY’S SALES AND REVENUES

Generation and Marketing

The Generation and Marketing segment had operating revenues of $1,834.4 million and $1,703.3 million in 2006 and 2005, respectively. For more information regarding the Generation and Marketing segment’s operating revenues, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” below and Note 9, “Business Segments,” to the Consolidated Financial Statements.

Delivery and Services

The Delivery and Services segment sold 43,179 million and 48,275 million kWhs of electricity to retail customers in 2006 and 2005, respectively. The Delivery and Services segment had operating revenues of $2,717.7 million and $2,845.5 million in 2006 and 2005, respectively. These revenues included revenue from electric sales and unregulated services. There were $1,430.6 million and $1,510.9 million of intersegment sales and revenues between the Generation and Marketing segment and the Delivery and Services segment in 2006 and 2005, respectively, which were eliminated for Allegheny’s consolidated results of operations. The following table describes the segment’s revenues from electric sales:

| | | | | | |

Revenues (in millions): | | 2006 | | 2005 |

Retail electric: | | | | | | |

Generation | | $ | 1,688.0 | | $ | 1,783.9 |

Transmission | | | 160.3 | | | 176.0 |

Distribution | | | 682.8 | | | 711.0 |

| | | | | | |

Subtotal retail | | $ | 2,531.1 | | $ | 2,670.9 |

| | | | | | |

Transmission services and bulk power | | | 150.7 | | | 115.9 |

Other affiliated and nonaffiliated energy services | | | 35.9 | | | 58.7 |

| | | | | | |

Total Delivery and Services revenues | | $ | 2,717.7 | | $ | 2,845.5 |

| | | | | | |

Allegheny had operating revenues from discontinued operations of $218.5 million for the year ended December 31, 2005. These revenues primarily related to its natural gas T&D business in West Virginia, which was sold on September 30, 2005. Allegheny did not have any operating revenues from discontinued operations in 2006. For more information regarding the Delivery and Services segment’s revenues, see “Management’s Discussion and Analysis of Financial Condition and Operating Results” below and Note 9, “Business Segments,” to the Consolidated Financial Statements.

16

CAPITAL EXPENDITURES

Actual capital expenditures for 2006 and projected capital expenditures for 2007 and 2008 are shown in the following tables. The projected amounts and timing are subject to continuing review and adjustment, and actual capital expenditures may vary from these estimates.

Allegheny Consolidated Totals

| | | | | | | | | |

| | | Actual | | Projected |

(In millions) | | 2006 | | 2007 | | 2008 |

Transmission and distribution facilities: | | | | | | | | | |

Transmission expansion (a) | | | 3 | | | 90 | | | 240 |

Other transmission and distribution facilities | | | 197 | | | 215 | | | 215 |

Environmental: | | | | | | | | | |

Fort Martin Scrubbers (b) | | | 9 | | | 150 | | | 260 |

Hatfield Scrubbers (c) | | | 64 | | | 390 | | | 285 |

Other | | | 65 | | | 75 | | | 75 |

Other generation facilities | | | 71 | | | 90 | | | 40 |

Other capital expenditures | | | 38 | | | 20 | | | 5 |

| | | | | | | | | |

Total capital expenditures | | $ | 447 | | $ | 1,030 | | $ | 1,120 |

| | | | | | | | | |

AFUDC and capitalized interest included above | | $ | 12 | | $ | 30 | | $ | 50 |

| | | | | | | | | |

Monongahela

| | | | | | | | | |

| | | Actual | | Projected |

(In millions) | | 2006 | | 2007 | | 2008 |

Transmission and distribution facilities | | $ | 50 | | $ | 55 | | $ | 60 |

Environmental: | | | | | | | | | |

Fort Martin Scrubbers (b) | | | 9 | | | 150 | | | 260 |

Other | | | 14 | | | 20 | | | 15 |

Other generation facilities | | | 15 | | | 30 | | | 20 |

Other capital expenditures | | | 3 | | | 5 | | | — |

| | | | | | | | | |

Total capital expenditures | | $ | 91 | | $ | 260 | | $ | 355 |

| | | | | | | | | |

AFUDC and capitalized interest included above | | $ | 2 | | $ | 5 | | $ | 5 |

| | | | | | | | | |

AGC

| | | | | | | | | |

| | | Actual | | Projected |

(In millions) | | 2006 | | 2007 | | 2008 |

Generation facilities and other | | $ | 4 | | $ | 7 | | $ | 5 |

| | | | | | | | | |

| (a) | Includes construction of the TrAIL Project, which has a target completion date of 2011 and estimated total cost of approximately $820 million, as well as other transmission projects requested by PJM. |

| (b) | Construction of Scrubbers at the Fort Martin generation facility is expected to be completed during 2009 at an estimated total cost of approximately $550 million, excluding AFUDC of $5 million. Allegheny plans to fund $450 million of these costs through securitization of an environmental control surcharge to be collected from the West Virginia customers of Monongahela and Potomac Edison. |

| (c) | Construction of Scrubbers at the Hatfield’s Ferry generating facility is expected to be completed during 2009 at an estimated total cost of approximately $725 million, excluding capitalized interest of $60 million. |

17

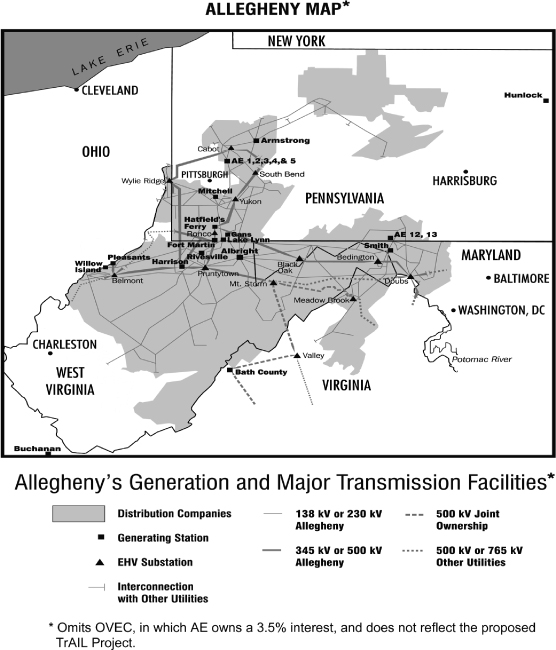

ELECTRIC FACILITIES

Generation Capacity

All of Allegheny’s owned or controlled generation capacity is part of the Generation and Marketing segment. Allegheny’s owned and controlled capacity as of January 1, 2007 was 9,670 MWs, of which 7,604 MWs (78.6%) were coal-fired, 891 MWs (9.2%) were natural gas-fired, 1,093 MWs (11.3%) were pumped-storage and hydroelectric and 82 MWs (0.8%) were oil-fired. The Distribution Companies are obligated to purchase 479 MWs of power through state utility commission-approved arrangements pursuant to PURPA. This PURPA capacity is part of the Delivery and Services segment, except that, effective January 1, 2007, the PURPA capacity for which Monongahela contracts is part of the Generation and Marketing segment. Allegheny’s generation capacity is more fully described in the tables titled “Nominal Maximum Operational Generation Capacity” and “PURPA Capacity” below.

2006 Capacity Acquisitions and Dispositions

Allegheny Energy Supply Hunlock Creek, LLC (“AE Hunlock”), a wholly owned subsidiary of AE, previously owned a 50% interest in Hunlock Creek Energy Ventures (“HCEV”), which owned and operated a 48 MW coal-fired generation facility and a 44 MW gas-fired combustion turbine generation facility located on real property in Hunlock Township, Luzerne County, Pennsylvania. UGI Hunlock Development Company (“UGI”) also owned a 50% interest in HCEV. UGI held a put option under which it could require AE Supply to purchase UGI’s 50% interest in either the coal-fired facility, the gas-fired facility, or both for a 90-day period beginning on January 24, 2006. AE, AE Hunlock, and AE Supply entered into an agreement dated March 1, 2006 with UGI, UGI Development Company (“UGI Development”), and HCEV under which HCEV distributed the coal-fired facility to UGI and AE Hunlock purchased UGI’s 50% interest in HCEV, thereby effectively obtaining the gas-fired facility. HCEV was dissolved, and the assets and liabilities of HCEV, including the gas-fired facility, were contributed to AE Supply. See Note 24, “HCEV Partnership Interest,” to the Consolidated Financial Statements.

In December 2006, AE Supply sold its Gleason generation facility, a 526 MW natural gas-fired peaking facility located in Gleason, Tennessee. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Asset Sales” below and Note 7, “Discontinued Operations” to the Consolidated Financial Statements.

Asset Swap and Proposed Securitization

In May 2005, the state of West Virginia adopted legislation permitting securitization financing for the construction of certain types of pollution control equipment at facilities owned by public utilities that are regulated by the West Virginia PSC, subject to the satisfaction of certain criteria. Effective January 1, 2007, AE Supply and Monongahela completed the Asset Swap, an intra-company transfer of assets that realigned generation ownership and contractual arrangements within the Allegheny system in order to, among other things, allow Monongahela to own 100% of the Fort Martin generation facility in West Virginia and, along with Potomac Edison, to finance the construction of Scrubbers at its Fort Martin generation facility through the securitization of a charge that Monongahela and Potomac Edison will impose on their retail customers in West Virginia.

As a result of the Asset Swap, Monongahela also owns 100% of the Albright, Rivesville and Willow Island generation facilities in West Virginia. In addition, Monongahela is contractually entitled to a greater proportion of the generation (189 additional MWs) from the Bath County, Virginia generation facility. Also as a result of the Asset Swap, AE Supply owns 100% of the Hatfield’s Ferry generation facility in Pennsylvania, which prior to the Asset Swap was jointly owned by AE Supply and Monongahela, and has a greater ownership interest in the Harrison and Pleasants generation facilities in West Virginia, for an additional 13 MWs and 176 MWs, respectively. AE Supply also has contractual rights to a greater amount of generation from OVEC. In addition, AE Supply assigned to Monongahela the obligation to supply the generation to meet Potomac Edison’s load obligations in West Virginia.

18

In 2006, the West Virginia PSC issued an Order that, as amended, authorizes Allegheny to securitize up to $450 million in construction costs associated with the construction of Scrubbers at the Fort Martin generation facility, plus $16.5 million in upfront financing costs and certain other costs. See “Regulatory Framework Affecting Allegheny” below and Note 26, “Subsequent Event—Asset Swap,” to the Consolidated Financial Statements.

The table below shows the nominal maximum operational generation capacity owned or controlled by Allegheny, as of January 1, 2007. This generation is included in the Generation and Marketing segment. Effective January 1, 2007, Allegheny completed the Asset Swap, which realigned generation ownership and contractual arrangements within the Allegheny system and which is reflected in the table below.

Nominal Maximum Operational Generation Capacity (MW)

| | | | | | | | | | |

| | | Units | | Project Total | | Regulated | | Unregulated | | Service Commencement Dates (a) |

Stations | | | | Monongahela | | AE Supply and Other | |

Coal Fired-Supercritical (Steam): | | | | | | | | | | |

Harrison (Haywood, WV) | | 3 | | 1,972 | | 405 | | 1,567 | | 1972-74 |

Hatfield’s Ferry (Masontown, PA) | | 3 | | 1,710 | | | | 1,710 | | 1969-71 |

Pleasants (Willow Island, WV) | | 2 | | 1,300 | | 100 | | 1,200 | | 1979-80 |

Fort Martin (Maidsville, WV) | | 2 | | 1,107 | | 1,107 | | | | 1967-68 |

| | | | | |

Coal Fired-Other (Steam): | | | | | | | | | | |

Armstrong (Adrian, PA) | | 2 | | 356 | | | | 356 | | 1958-59 |

Albright (Albright, WV) | | 3 | | 292 | | 292 | | | | 1952-54 |

Mitchell (Courtney, PA) | | 1 | | 288 | | | | 288 | | 1963 |

Ohio Valley Electric Corp. (Chelsea, OH) (Madison, IN) (b) | | 11 | | 78 | | 78 | | | | |

Willow Island (Willow Island, WV) | | 2 | | 243 | | 243 | | | | 1949-60 |

Rivesville (Rivesville, WV) | | 2 | | 142 | | 142 | | | | 1943-51 |

R. Paul Smith (Williamsport, MD) | | 2 | | 116 | | | | 116 | | 1947-58 |

| | | | | |

Pumped-Storage and Hydro: | | | | | | | | | | |

Bath County (Warm Springs, VA) (c) | | 6 | | 1,035 | | 427 | | 608 | | 1985; 2001 |

Lake Lynn (Lake Lynn, PA) (d) | | 4 | | 52 | | | | 52 | | 1926 |

Green Valley Hydro (e) | | 21 | | 6 | | | | 6 | | Various |

| | | | | |

Gas-Fired: | | | | | | | | | | |

AE Nos. 3, 4 & 5 (Springdale, PA) | | 3 | | 540 | | | | 540 | | 2003 |

AE Nos. 1 & 2 (Springdale, PA) | | 2 | | 88 | | | | 88 | | 1999 |

AE Nos. 8 & 9 (Gans, PA) | | 2 | | 88 | | | | 88 | | 2000 |

AE Nos. 12 & 13 (Chambersburg, PA) | | 2 | | 88 | | | | 88 | | 2001 |

Buchanan (Oakwood, VA) (f) | | 2 | | 43 | | | | 43 | | 2002 |

Hunlock CT (Hunlock Creek, PA) | | 1 | | 44 | | | | 44 | | 2000 |

| | | | | |

Oil-Fired (Steam): | | | | | | | | | | |

Mitchell (Courtney, PA) | | 1 | | 82 | | | | 82 | | 1949 |

| | | | | | | | | | |

Total Capacity | | | | 9,670 | | 2,794 | | 6,876 | | |

| | | | | | | | | | |

| (a) | When more than one year is listed as a commencement date for a particular generation facility, the dates refer to the years in which operations commenced for the different units at that generation facility. |

| (b) | This figure represents capacity entitlement through AE’s ownership of OVEC shares. AE holds a 3.5% equity stake in, and is a sponsoring company of, OVEC. OVEC supplies power to its sponsoring companies under an intercompany power agreement. Currently, as a result of AE’s equity interest, Monongahela is |

19

| | entitled to 3.5% of OVEC generation, a portion (66 MWs) of which it has agreed to sell to AE Supply at cost in connection with the Asset Swap. Monongahela will transfer to AE Supply its rights to OVEC generation at such time as AE Supply’s long-term unsecured non-credit enhanced indebtedness has a Standard & Poor’s credit rating of at least BBB- and a Moody’s Investor Services, Inc. credit rating of at least Baa3. |

| (c) | This figure represents capacity entitlement through ownership of AGC. |

| (d) | AE Supply has a license for Lake Lynn through 2024. |

| (e) | Green Valley Hydro’s license for hydroelectric facilities Dam No. 4 and Dam No. 5, located in West Virginia and Maryland will expire November 30, 2024. Potomac Edison has licenses through 2024 for the Shenandoah, Warren, Luray and Newport projects located in Virginia. |

| (f) | Buchanan Energy Company of Virginia, LLC, a subsidiary of AE Supply (“Buchanan”), is part-owner of Buchanan Generation LLC (“Buchanan Generation”). CNX Gas Corporation and Buchanan have equal ownership interests in Buchanan Generation. AE Supply operates and dispatches 100% of Buchanan Generation’s 86 MWs. |

PURPA Capacity

The following table shows additional generation capacity available to the Distribution Companies through state utility commission-approved arrangements pursuant to PURPA. PURPA requires electric utility companies, such as the Distribution Companies, to interconnect with, provide back-up electric service to and purchase electric capacity and energy from qualifying small power production and cogeneration facilities. The amounts shown in this table are included in the Delivery and Services segment, except that, effective January 1, 2007, the PURPA generation for which Monongahela contracts is part of the Generation and Marketing segment.

| | | | | | | | | | |

PURPA Stations | | Project Total | | Monongahela | | Potomac Edison | | West Penn | | PURPA Contract Termination Date |

Coal-Fired: Steam | | | | | | | | | | |

AES Warrior Run (Cumberland, MD) (a) | | 180 | | | | 180 | | | | 02/10/2030 |

AES Beaver Valley (Monaca, PA) | | 125 | | | | | | 125 | | 12/31/2016 |

Grant Town (Grant Town, WV) | | 80 | | 80 | | | | | | 05/28/2036 |

West Virginia University (Morgantown, WV) | | 50 | | 50 | | | | | | 04/17/2027 |

| | | | | |

Hydro: | | | | | | | | | | |

Hannibal Lock and Dam (New Martinsville, WV) | | 31 | | 31 | | | | | | 06/01/2034 |

Allegheny Lock and Dam 6 (Freeport, PA) | | 7 | | | | | | 7 | | 06/30/2034 |

Allegheny Lock and Dam 5 (Freeport, PA) | | 6 | | | | | | 6 | | 09/30/2034 |

| | | | | | | | | | |

Total PURPA Capacity | | 479 | | 161 | | 180 | | 138 | | |

| | | | | | | | | | |

| (a) | As required under the terms of a Maryland restructuring settlement, Potomac Edison began to offer the 180 MW output of the AES Warrior Run project to the wholesale market beginning July 1, 2000 and will continue to do so for the term of the AES Warrior Run contract, which ends on February 10, 2030. Revenue received from the sale reduces the AES Warrior Run surcharge paid by Maryland customers. As of January 1, 2005, AES Warrior Run output is being sold to a non-affiliated third party. |

The Energy Policy Act amended PURPA. Among other things, the amendments provide that electric utilities are no longer required to enter into any new contractual obligation to purchase energy from a qualifying facility if FERC finds that the facility has non-discriminatory access to a functioning wholesale market and open-access transmission. See “Regulatory Framework Affecting Allegheny” below.

20

The following table sets forth the existing miles of T&D lines and the number of substations of the Distribution Companies and AGC as of December 31, 2006:

| | | | | | | | | | |

| | | Underground | | Above- Ground | | Total Miles | | Total Miles Consisting of 500-Kilovolt (kV) Lines | | Number of Transmission and Distribution

Substations |

Monongahela | | 758 | | 22,312 | | 23,070 | | 246 | | 343 |

Potomac Edison | | 4,983 | | 18,098 | | 23,081 | | 178 | | 188 |

West Penn | | 2,782 | | 24,198 | | 26,980 | | 276 | | 595 |

AGC (a) | | 0 | | 87 | | 87 | | 87 | | 1 |

| | | | | | | | | | |

Total | | 8,523 | | 64,695 | | 73,218 | | 787 | | 1,127 |

| | | | | | | | | | |

| (a) | Total Bath County transmission lines, of which AGC owns an undivided 40% interest and Virginia Electric and Power Company owns the remainder. |

The Distribution Companies’ transmission network has 12 extra-high-voltage (345 kV and above) and 36 lower-voltage interconnections with neighboring utility systems.

21

22

FUEL, POWER AND RESOURCE SUPPLY

Generation and Marketing Segment

Coal Supply

Allegheny consumed approximately 19 million tons of coal in 2006 at an average price of $37.95 per ton delivered. Allegheny purchased this coal primarily from mines in Pennsylvania, West Virginia and Ohio. However, Allegheny also purchases coal from other regions. During 2005, Allegheny initiated the blending of coal from the Powder River Basin, or “PRB” coal, with eastern bituminous coal at several generation facilities. The Powder River Basin is a major coal producing area in northeastern Wyoming and southeastern Montana. Allegheny currently intends to continue to blend PRB coal at several generation facilities.

Historically, Allegheny has purchased coal from a limited number of suppliers. Of Allegheny’s coal purchases in 2006, 66% came from subsidiaries of two companies, the larger of which represented 44% of the total tons purchased. As of February 20, 2007, Allegheny had contracts in place for the delivery of approximately 96% of the coal that Allegheny expects to consume in 2007, at an average price of approximately $40 per ton delivered. Various industry and operational factors, including increased costs, transportation constraints, safety issues and operational difficulties, may have negative effects on coal supplier performance.

In December 2005, Allegheny signed a coal lease and sales agreement with an affiliate of Alliance Resource Partners, L.P. to permit, develop and mine Allegheny’s coal reserve in Washington County, Pennsylvania. Alliance is evaluating the feasibility of mining the reserve and will seek the necessary permits and other governmental approvals to mine the reserve. If the reserve is developed, it is expected to produce high BTU, “scrubber-quality” coal suitable for use in Allegheny’s power plants with sulfur dioxide (“SO2”) emission controls, and Allegheny has agreed to purchase up to two million tons annually of the mine’s output. Allegheny also will receive estimated royalty payments of $5 million to $10 million per year on coal that is mined and sold from the reserve, depending upon production levels and coal prices, after the mine reaches full commercial operation.

Natural Gas Supply

AE Supply purchases natural gas to supply its natural gas-fired generation facilities. In 2006, AE Supply purchased its natural gas requirements principally in the spot market. One of AE Supply’s subsidiaries has a long-term natural gas agreement in place with a supplier. The natural gas provided under this agreement is used at the Buchanan generation facility.

Natural Gas Transportation Contracts

Dominion Transmission Transportation Contract. AE Supply has a long-term agreement with Dominion Transmission, Inc. for the transportation of natural gas under a tariff approved by FERC. This agreement provides for the transportation of 95,000 decatherms of natural gas per day through May 31, 2013, from the Oakford, Pennsylvania interconnection to AE Supply’s combined cycle plant in Springdale, Pennsylvania.

Equitable Gas Transportation Contract. AE Supply has a long-term agreement with Equitable Gas Company, a division of Equitable Resources, Inc., for the transportation of natural gas under a tariff approved by the Pennsylvania PUC. This agreement provides for transportation of 90,000 decatherms of natural gas per day until December 31, 2012 from Greene County, Pennsylvania to the Hatfield’s Ferry generation facility in Masontown, Pennsylvania. This transportation agreement was purchased for anticipated natural gas reburn opportunities at Hatfield’s Ferry. Natural gas reburn reduces NOx emissions at a generation facility by using natural gas instead of coal for a portion of the generation facility’s anticipated fuel requirements.

El Paso Transportation Contract. AE Supply had a long-term agreement with El Paso Natural Gas Company for the transportation of natural gas under tariffs approved by FERC. This agreement provided for the

23

transportation of gas from western Texas and northern New Mexico to the southern California border and was purchased for anticipated natural gas deliveries to a combined-cycle generation project that was contemplated in La Paz, Arizona. This project has been cancelled. In August 2003, AE Supply permanently turned back to the pipeline approximately 85% of its capacity obligation under this contract. In November 2004, AE Supply entered into a release for the balance of this capacity. This contract expired as of October 1, 2006.

Kern River Transportation Contract. AE Supply has a long-term agreement with Kern River Gas Transmission Company for the transportation of natural gas under a tariff approved by FERC. This agreement provides for the transportation of 45,122 decatherms of natural gas per day through April 30, 2018 from Opal, Wyoming to southern California. This transportation agreement was purchased for anticipated natural gas deliveries into southern California and at the Las Vegas Cogeneration II combined-cycle generation facility in Las Vegas, Nevada, in which Allegheny’s participation was terminated in 2003. AE Supply has entered into long-term capacity releases for the full contract volume through October 30, 2008.

The Delivery and Services Segment

Electric Power

Allegheny reorganized its corporate structure in response to electric utility deregulation within its service area between 1999 and 2001. The Distribution Companies, with the exception of Monongahela and its West Virginia generation assets, do not produce their own power. Potomac Edison transferred all of its generation assets to AE Supply in 2000. West Penn transferred all of its generation assets to AE Supply in 1999. Monongahela transferred the portion of its generation assets dedicated to its previously-owned Ohio service territory to AE Supply in 2001. The Asset Swap realigned ownership of certain generation facilities between Monongahela and AE Supply, effective as of January 1, 2007. See “Electric Facilities” above.

Each of the states in Allegheny’s service territory other than West Virginia has, to some extent, deregulated its electric utility industry. Pennsylvania, Maryland and Virginia have instituted retail customer choice and are transitioning to market-based, rather than cost-based pricing, although recent legislation under consideration in Virginia proposes some degree of re-regulation. West Penn has PLR obligations to its customers in Pennsylvania. Potomac Edison has PLR obligations to its customers in Virginia and its residential customers in Maryland.

As “providers of last resort,” West Penn and Potomac Edison must supply power (i.e., generation services) to certain retail customers who have not chosen alternative suppliers (or have chosen to return to Allegheny service) at rates that are capped at various levels during the applicable transition period. West Penn and Potomac Edison provide T&D services to customers in their service areas regardless of electricity generation supplier. See “The Distribution Companies’ Obligations and the PJM Market” above and “Regulatory Framework Affecting Allegheny” below.

A significant portion of the power necessary to meet the PLR obligations of West Penn and Potomac Edison is purchased from AE Supply. AE Supply is contractually obligated to provide power to West Penn and Potomac Edison during the relevant state deregulation transition periods under the terms of power sales agreements. These power sales agreements include both fixed price and market-based pricing components. These pricing components may not fully reflect the cost of supplying this power. As a result, AE Supply currently absorbs a portion of the risk of fuel price increases and increased costs of environmental compliance. Prior to January 1, 2007, AE Supply also sold power to Potomac Edison to serve customers in Potomac Edison’s West Virginia service territory. In connection with the Asset Swap, Monongahela assumed the obligation to supply power to Potomac Edison to meet its West Virginia load obligations. A portion of Allegheny’s PLR obligations is satisfied by PURPA contract purchases.

When existing power sales agreements terminate, Potomac Edison and West Penn will be unable to rely on the previously dedicated supply of power at specified contract prices to meet their respective power supply requirements. The arrangements to serve the applicable PLR obligations following the expiration of these

24

agreements have been partially determined in Maryland but are still under development in Pennsylvania and Virginia and in Maryland, with respect to residential customers. AE Supply’s and Monongahela’s existing power sales agreements with West Penn and Potomac Edison will expire as set forth in the chart below.

| | | | |

Distribution Company | | State | | Expiration Date of Power Sale Agreement(a) |

Potomac Edison | | Maryland | | December 31, 2008 |

Potomac Edison | | Virginia | | June 30, 2007 |

Potomac Edison | | West Virginia | | January 1, 2027 |

West Penn | | Pennsylvania | | December 31, 2010 |

| (a) | The power sales agreements reflected on the table are with AE Supply, except for Potomac Edison’s agreement with Monongahela to serve Potomac Edison’s West Virginia load obligations. |

To facilitate the economic dispatch of its generation, Monongahela sells the power that it generates from its West Virginia jurisdictional assets into the PJM market and purchases from the PJM market the power necessary to meet its West Virginia jurisdictional customer load and contractual obligations to provide power.

25

REGULATORY FRAMEWORK AFFECTING ALLEGHENY

The interstate transmission services and wholesale power sales of the Distribution Companies, AE Supply and AGC are regulated by FERC under the FPA. The Distribution Companies’ local distribution service and sales at the retail level are subject to state regulation. The statutory and regulatory framework affecting these companies has evolved significantly over the past decade, and these changes have exposed the companies to significant new risks and opportunities. In addition, Allegheny’s communications subsidiary, ACC, is subject, to a limited extent, to the jurisdiction of the Federal Communications Commission and state regulatory commissions. Allegheny is subject to numerous other local, state and federal laws, regulations and rules. See “Risk Factors” below.

Federal Regulation and Rate Matters

FERC, Competition and RTOs

FERC is an independent agency within the DOE that regulates the U.S. electric utility industry.

FERC Authority Under the Federal Power Act

FERC regulates the transmission and wholesale sales of electricity under the authority of the FPA. Under the FPA, as amended by the Energy Policy Act, FERC regulates:

| | • | | the rates, terms and conditions of wholesale power sales and transmission services offered by public utilities; |

| | • | | the development, operation and maintenance of hydroelectricity projects; |

| | • | | the interconnection of transmission systems with other electric systems, including generation facilities; |

| | • | | the disposition of public utility property and the merger, acquisition and consolidation of public utility systems; |

| | • | | the issuance of certain securities and assumption of certain liabilities by public utilities; |

| | • | | the system of accounts and methods of depreciation used by public utilities; |

| | • | | the reliability of the transmission grid; |

| | • | | the siting of certain transmission facilities; |

| | • | | the allocation of transmission rights; |

| | • | | the types of incentives available to encourage new transmission investment; |

| | • | | the transparency of power sales prices and market manipulation; |

| | • | | the relationship between holding companies and their public utility affiliates, including cost allocations, affiliate transactions and communications, and the availability of books and records; and |

| | • | | the holding of interlocking positions by directors and officers of public utilities. |

In addition, FERC has the authority under the FPA to resolve complaints initiated on its own motion or by others as well as to conduct investigations. FERC also has the authority to enforce the FPA through the imposition of penalties.

The FPA gives FERC exclusive rate-making jurisdiction over wholesale sales and transmission of electricity in interstate commerce. Entities, such as the Distribution Companies, AE Supply and AGC, that sell electricity at wholesale or own transmission facilities are considered “public utilities” subject to FERC jurisdiction. Public utilities must obtain FERC acceptance for filing of their wholesale rate schedules. Rates for wholesale sales of

26

electricity are determined on a cost-basis, or, if the seller demonstrates that it does not have market power, FERC may grant market-based rate authority, which allows transactions to be priced based on prevailing market conditions. Rates for transmission facilities are determined on a cost basis.

Competition and RTOs

Over the past decade, FERC has taken a number of steps to foster increased competition within the electric industry. Among other things, FERC requires public utilities that own transmission facilities to offer non-discriminatory, open-access transmission services. In addition, FERC has imposed standards of conduct governing communications between employees conducting transmission functions and employees engaged in wholesale power sale activities. These standards of conduct are intended to prevent transmission-owning utilities from giving their power marketing businesses preferential access to the transmission system and transmission information. FERC also has taken steps to encourage utilities to participate in RTOs, such as PJM, by transferring functional control over their transmission assets to RTOs.

Following FERC’s initiative to promote competition, a number of states, including Pennsylvania, Maryland and Virginia, adopted retail access legislation, which permitted utilities to transfer their generation assets to affiliated companies or third parties. Similar to many other utilities, the Distribution Companies restructured their businesses in Pennsylvania, Maryland and Virginia between 1996 and 2001 to comply with retail restructuring requirements in those states by, among other things, transferring generation assets serving customers in those states to AE Supply.

However, this trend toward restructuring and increased competition for retail markets has slowed in response to events over the past several years. Market-based competition within the wholesale markets is now continuing with greater FERC oversight, and some states have moved away from electricity choice at the retail level by delaying the implementation of retail competition (as in Virginia) or rejecting it outright (as in West Virginia). Delays, discontinuations or reversals of electricity marketing restructurings in states in which Allegheny operates could have a material adverse effect on its results of operation and financial condition.

All of Allegheny’s generation assets and power supply obligations are located within the PJM market, and PJM maintains functional control over the Distribution Companies’ transmission facilities. Changes in the PJM tariff, operating agreement, policies and/or market rules could adversely affect Allegheny’s financial results. These matters include changes involving: the terms, conditions and pricing of transmission services; construction of transmission enhancements; auction of long-term financial transmission rights and the allocation mechanism for the auction revenues; changes in the locational marginal pricing mechanism; changes in transmission congestion patterns due to the implementation of PJM’s regional transmission expansion planning protocol or other required transmission system upgrades; generation retirement rules and reliability pricing issues.

FERC actions with respect to the transmission rate design within PJM may impact the Distribution Companies. Beginning in July 2003, FERC issued a series of orders related to transmission rate design for the PJM and Midwest Independent Transmission System Operator regions. Specifically, FERC ordered the elimination of multiple and additive (i.e., “pancaked”) rates and called for the implementation of a long-term rate design for these regions. In November 2004, FERC rejected long-term regional rate proposals from the Distribution Companies and others. FERC concluded that neither the rate design proposals, nor the existing PJM rate design, had been shown to be just and reasonable. However, FERC ordered the continuation of the existing PJM rate design and the implementation of a transition charge for these regions through March 31, 2006 through filings made by transmission owners in both regions. In February 2005, FERC accepted these transition charges, effective December 1, 2004, subject to an evidentiary hearing. FERC’s February 2005 order remains subject to multiple rehearing requests and, potentially, appellate review. Allegheny cannot predict the outcome of these proceedings or whether they will have a material impact on its business or financial position.

During the now-expired transition period, the Distribution Companies were both payers and payees of transition charges. These charges resulted in the payment by the Distribution Companies of $13.7 million, and

27

payments to the Distribution Companies of $4.8 million, for the 16-month period ended March 31, 2006. Following the evidentiary hearing, on August 10, 2006, an administrative law judge issued an initial decision that generally found fault with the methodologies used to develop the transition charges. That decision is now subject to review by FERC. The order that will be issued by FERC on review of the initial decision may require the Distribution Companies to refund some portion of the amounts received from these transition charges or entitle the Distribution Companies to receive additional revenue from these charges. In addition, the Distribution Companies may be required to pay additional amounts as a result of increases in the transition charges previously billed to them, or they may receive refunds of transition charges previously billed. Allegheny cannot predict the outcome of these proceedings. The Distribution Companies have entered into nine partial settlements with regard to the transition charges, and may enter into additional settlements in the future. FERC has approved two of these settlements, and approval is pending for the remaining partial settlements.

In a May 2005 order, FERC again determined that the existing PJM rate design may not be just and reasonable. On September 30, 2005, the Distribution Companies, together with another PJM transmission owner, filed a proposed rate design with FERC to replace the existing rate design within PJM, effective April 1, 2006. Two other PJM transmission owners also filed a separate proposed rate design. A hearing was held in April 2006 to determine whether the rate design is unjust and unreasonable and whether it should be replaced by either of the proposed rate designs. An initial decision was issued on July 13, 2006 by an administrative law judge, finding that the existing PJM rate design for existing transmission facilities is not just and reasonable. The administrative law judge found that the rate design for existing transmission facilities proposed by Allegheny is just and reasonable, but ruled that the rate design proposed by FERC staff is also just and reasonable, is superior and should be made effective as of April 1, 2006. The initial decision also found that the Distribution Companies’ proposal for rate recovery for new transmission facilities had not demonstrated that the existing rate recovery mechanism for such facilities is unjust and unreasonable but adopted the Distribution Companies’ position that the implementation of a new rate design does not necessitate a change in the allocation of auction revenue rights and financial transmission rights. The initial decision will not become effective until acted upon by FERC, which may accept, modify or reject the initial decision.