Exhibit 99.1

FOURTH QUARTER 2008

FINANCIAL SUPPLEMENT

If you need further information, please contact:

Dave Miller, Investor Relations

901-523-4162

dwmiller@firsthorizon.com

| TABLE OF CONTENTS | |||||||||||

| Page | |||||||||||

| First Horizon National Corporation Segment Structure | 3 | ||||||||||

| Performance Highlights | 4 | ||||||||||

| Charges for Restructuring, Repositioning, & Efficiency Initiatives | 6 | ||||||||||

| Consolidated Results | |||||||||||

| Income Statement | |||||||||||

| Summary Income Statement | 7 | ||||||||||

| Income Statement | 8 | ||||||||||

| Other Income and Other Expense | 9 | ||||||||||

| Balance Sheet | |||||||||||

| Period End Balance Sheet | 10 | ||||||||||

| Average and Period End Loans | 11 | ||||||||||

| Average Balance Sheet | 12 | ||||||||||

| Average Balance Sheet: Income & Expense | 13 | ||||||||||

| Average Balance Sheet: Yields & Rates | 14 | ||||||||||

| Mortgage Servicing Rights | 15 | ||||||||||

| Business Segment Detail | |||||||||||

| Segment Highlights | 16 | ||||||||||

| Regional Banking | 17 | ||||||||||

| Capital Markets | 18 | ||||||||||

| National Specialty Lending | 19 | ||||||||||

| Mortgage Banking | 20 | ||||||||||

| Mortgage Banking: Servicing | 21 | ||||||||||

| Corporate | 22 | ||||||||||

| Capital Highlights | 23 | ||||||||||

| Asset Quality | |||||||||||

| Asset Quality: Consolidated | 24 | ||||||||||

| Analysis of FAS 114 Loans, ORE, & NPL Rollforward | 26 | ||||||||||

| Asset Quality: Regional Banking | 27 | ||||||||||

| Asset Quality: National Specialty Lending | 28 | ||||||||||

| Asset Quality: Mortgage Banking & Capital Markets | 29 | ||||||||||

| Asset Quality Highlights: Key Portfolios - Commercial | 30 | ||||||||||

| Asset Quality Highlights: Key Portfolios - Consumer | 31 | ||||||||||

| Asset Quality Process | 32 | ||||||||||

| Glossary of Terms | 33 | ||||||||||

| Other Information | |||||||||||

This financial supplement contains forward-looking statements involving significant risks and uncertainties. A number of important factors could cause actual results to differ materially from those in the forward-looking information. Those factors include general economic and financial market conditions, including expectations of and actual timing and amount of interest rate movements including the slope of the yield curve, competition, customer and investor responses to these conditions, ability to execute business plans, geopolitical developments, recent and future legislative and regulatory developments, natural disasters, and items mentioned in this financial supplement and in FHN's most recent press release, as well as critical accounting estimates and other factors described in FHN’s recent filings with the SEC. FHN disclaims any obligation to update any such factors or to publicly announce the result of any revisions to any of the forward-looking statements included herein or therein to reflect future events or developments. | |||||||||||

| FIRST HORIZON NATIONAL CORPORATION SEGMENT STRUCTURE | ||||||||||

| Regional Banking | ||||

| -Traditional banking services for consumers and business | ||||

| -Activities include lending and deposit taking, investments, insurance, financial planning, trust services, asset management, | ||||

| cash management, and health savings accounts | ||||

| -Primarily southeastern US footprint, with approximately 200 financial centers in Tennessee and nearby markets | ||||

| -First Tennessee banking franchise and middle market lending are key businesses | ||||

| -First Horizon Banks included for periods prior to divestiture | ||||

| Capital Markets | ||||

| -Fixed income sales, trading, and strategies for institutional clients in U.S. and abroad | ||||

| -Other capital markets products include: | ||||

| -Equity research, portfolio advisory, derivatives, and loan trading | ||||

| -Correspondent banking provides credit, depository, and other banking related services to other financial institutions | ||||

| National Specialty Lending | ||||

| -Wind-down portfolio that includes lending activities such as consumer lending and construction lending outside Regional Banking footprint | ||||

| -Construction lending includes national home builder, one-time close, and commercial real estate portfolios | ||||

| -In January 2008, FHN announced the discontinuation of national home builder and commercial real estate | ||||

| lending through its First Horizon Construction Lending offices | ||||

| -Consumer lending consists mainly of national retail-originated home equity loans and lines | ||||

| Mortgage Banking | ||||

| -Primarily consists of first lien mortgage originations and servicing | ||||

| -In a transaction that closed on August 31, 2008, First Horizon National Corp sold its mortgage servicing platform | ||||

| and origination offices outside Tennessee to MetLife Bank, N.A. | ||||

| Corporate | ||||

| -Includes executive management, enterprise-wide risk management, corporate finance, | ||||

| corporate communications, and legal functions | ||||

| -Also includes funding function for the corporation and any impact from balance sheet positioning | ||||

3

| PERFORMANCE HIGHLIGHTS | |||||||||

| Summary of Fourth Quarter 2008 Significant Items (in millions) | |||||||||

| Segment | Item | Income Statement | Pre-Tax | Comments | |||||

| National Specialty Lending | MSR Valuation Adjustment | Noninterest income: Revenue from loan sales and securitizations | $(5.1) | Reduction in valuation of MSR related to prior consumer loan sales primarily due to interest rate changes. | |||||

| Mortgage Banking | Reinsurance Reserve | Noninterest expense: Other | $(16.5) | Increase in reserves for PMI reinsurance contracts due to increasing mortgage defaults. | |||||

| Servicing Sale Obligation | Noninterest income: Mortgage Banking | $(6.5) | Recognition of liability for minimum servicing fee guarantee on prior servicing sales. | ||||||

| Corporate | Reduction of Visa Contingent Liability | Noninterest expense: Other | $11.0 | Reversal of proportionate share of escrow funding by Visa for certain Visa litigation matters for which FHN has a contingent guarantee. | |||||

| Venture Capital Investment Dividends | Net interest income | $3.6 | Dividends received as part of wind down of venture capital investments. | ||||||

| Sales of Venture Capital Investments | Securities Gains/(Losses) | $1.3 | Gains from marks to sales price for venture capital investments. | ||||||

| Restructuring, Repositioning & Efficiency Initiatives | Noninterest expense: Various | $(10.2) | Expenses from contract terminations, severance, and office closures. Detailed further on page 6. | ||||||

| Restructuring, Repositioning & Efficiency Initiatives | Noninterest income: Various | $(.1) | True up from Mortgage divestiture & repurchase reserves from First Horizon Bank branch sales. Detailed further on page 6. | ||||||

| (Fourth Quarter 2008 vs. Third Quarter 2008) | ||||

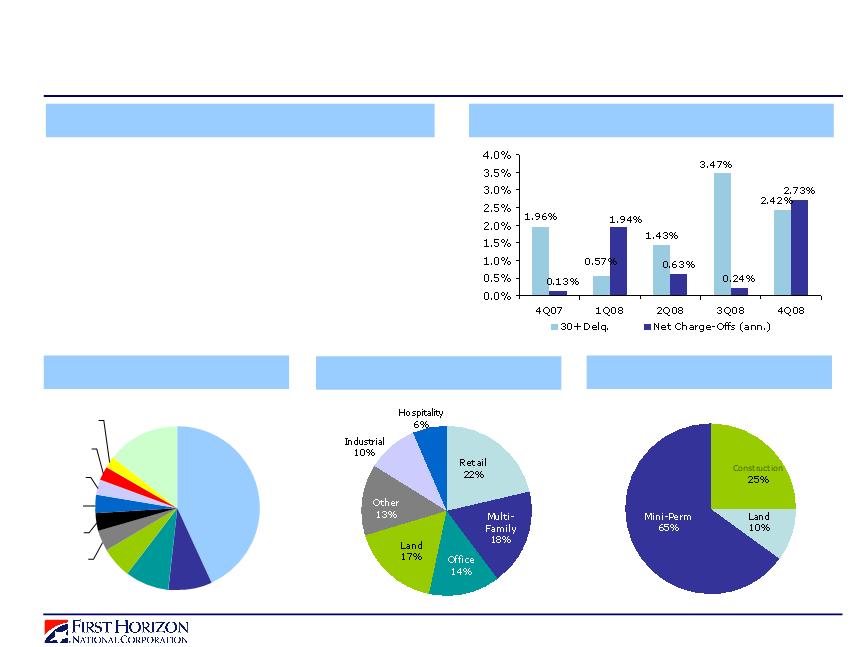

| Asset Quality | ||||

| - Provision decreased to $280.0 million in the fourth quarter compared to $340.0 million in third quarter 2008 | ||||

| - Portfolio deterioration in fourth quarter due to declining economic conditions | ||||

| - Continuing commercial portfolio deterioration | ||||

| - Residential CRE seeing downward trend in provisioning as credits are further along in credit cycle | ||||

| - Income CRE and C&I experiencing negative grade migration | ||||

| - Improved delinquency trends | ||||

| - Consumer portfolios experiencing continued stress | ||||

| - Home equity delinquencies increased | ||||

| - OTC provisioning limited due to third quarter efforts to identify inherent losses | ||||

| - Permanent mortgage portfolio experiencing increased loss severities | ||||

| - Net charge-offs were 361 annualized basis points of average loans driven by residential CRE, C&I, home equity and OTC portfolios | ||||

| - Net charge-offs of $191.2 million in fourth quarter compared to $154.7 million in prior quarter | ||||

| - Charging off almost all impaired commercial loan balances down to most likely estimate of collateral value net of costs to sell | ||||

| - NPAs increased to 538 basis points from 463 basis points reflecting portfolio deterioration from current economic conditions | ||||

| - Total NPAs increased to $1.2 billion from $1.0 billion primarily from deterioration in national construction portfolios | ||||

| - Allowance as a percentage of loans ratio increased to 399 basis points from 352 basis points in prior quarter | ||||

| Capital | ||||

| - Continued quarterly dividend payable in common stock | ||||

| - Received $866.5 million of funds from Capital Purchase Program | ||||

| - Considered part of Tier I Capital | ||||

| - Current ratios also continue to benefit from balance sheet contraction (estimated based on period end balances) | ||||

| - 7.3% for tangible common equity to tangible assets | ||||

| - 14.9% for Tier I | ||||

| - 20.1% for Total Capital | ||||

4

| PERFORMANCE HIGHLIGHTS (continued) | |||||

| (Fourth Quarter 2008 vs. Third Quarter 2008) | |||||

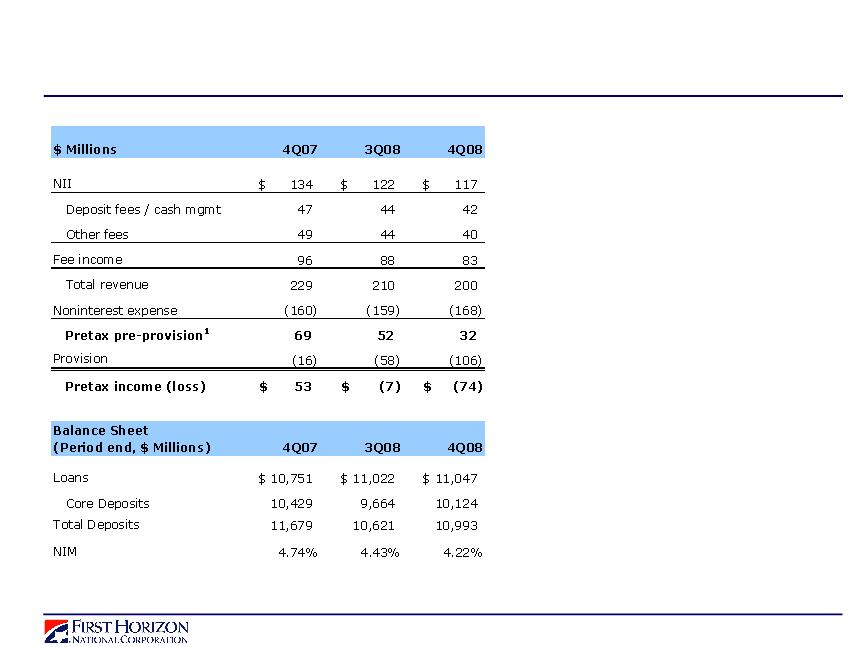

| Regional Banking | |||||

| - Net interest margin decreased to 4.22% compared to 4.43% in third quarter | |||||

| - Reflects competition for deposit accounts and increase in nonaccrual loans | |||||

| - Noninterest income declined to $82.6 million from $87.9 million | |||||

| - Reduced deposit and wealth management fees in fourth quarter due to weak economic conditions | |||||

| - Provision expense in third and fourth quarters primarily reflects deterioration in commercial loans | |||||

| - Noninterest expense increased to $167.8 million compared to $158.6 million in prior quarter | |||||

| - Primarily from higher personnel, infrastructure and credit-related costs | |||||

| Capital Markets | |||||

| - Fixed income revenues were $156.5 million in fourth quarter compared to $80.1 million in prior quarter | |||||

| - Increase due to Federal Reserve rate reductions in fourth quarter creating a steeper yield curve | |||||

| - Also benefited from market volatility | |||||

| - Other product revenues were $20.8 million in fourth quarter compared to $18.4 million in third quarter | |||||

| - Provision expense decreased to $8.1 million from $38.5 million | |||||

| - Current stress in financial system continuing to impact correspondent banking loans | |||||

| - Increase in noninterest expense resulted from higher production levels | |||||

| National Specialty Lending | |||||

| - Sequential decline in net interest income as loan portfolios continue to wind down | |||||

| - Net interest margin decreased to 1.85% compared to 2.14% in third quarter | |||||

| - Primarily results from an increase in nonaccrual loans | |||||

| - Provision for loan losses continues to reflect deterioration within national construction and consumer lending portfolios | |||||

| - Noninterest income decreased sequentially | |||||

| - $5.1 million reduction in value of MSR primarily due to interest rate changes | |||||

| - Charge of $2.3 million recognized in fourth quarter for repurchase reserves | |||||

| - $1.7 million charge recognized in third quarter | |||||

| - Noninterest expense decreased primarily due to the effects of winding down operations | |||||

| Mortgage Banking | |||||

| - Decreased origination income due to completion of MetLife transaction in August | |||||

| - Net effect of adopting new accounting standards negatively affected pre-tax earnings by negligible amount | |||||

| - $14.4 million negative effect on third quarter 2008 | |||||

| - Third quarter adjustment of $15.5 million to reflect revised cash flow expectations related to mortgage origination activities | |||||

| - Hedging results positively impacted earnings by $64.6 million vs. $50.8 million in third quarter | |||||

| - Falling rates and a steeper yield curve combined with positive convexity in the portfolio to benefit the hedge position | |||||

| - Servicing runoff decreased to $9.9 million for fourth quarter from $20.1 million in prior quarter | |||||

| - Consistent with decline in servicing portfolio | |||||

| - Other income declined due to completion of MetLife transaction | |||||

| - $6.5 million charge recognized in fourth quarter related to servicing fee guarantees on prior servicing sales | |||||

| - Net interest income declines consistent with decrease in warehouse | |||||

| - Provision of $22.0 million in fourth quarter due to deterioration in permanent mortgage portfolio | |||||

| - $2.9 million of provision in prior quarter | |||||

| - Noninterest expense declined to $39.5 million in fourth quarter compared to $89.0 million in prior quarter | |||||

| - Due to sale of national mortgage offices and servicing platform at the end of August | |||||

| - Fourth quarter includes $16.5 million of expense for PMI reinsurance liability due to increased mortgage defaults | |||||

| - Provision for foreclosure losses of $1.8 million in fourth quarter | |||||

| - $3.4 million in third quarter | |||||

| Taxes | |||||

| - Approximate $8 million positive quarterly effect from permanent tax credits | |||||

| Corporate Segment | |||||

| - Net charges of $10.3 million recognized for restructuring, repositioning and efficiency initiatives (detail on next page) | |||||

| - Fourth quarter included $10.2 million of expenses | |||||

| - Primarily for contract terminations, severance and office closures | |||||

| - $0.1 million of net charges related to Mortgage and First Horizon Bank branch sales presented in (Losses)/Gains on Divestitures | |||||

| - Prior quarter included $33.9 million of net charges for these initiatives | |||||

| - $11.0 million of expense reductions recognized in fourth quarter related to contingent liability for Visa litigation matters | |||||

| - Represents FHN's proportionate share of Visa's escrow funding in fourth quarter | |||||

| - $11.0 million of expense recognized in third quarter to increase contingent liability | |||||

| - $3.6 million of dividends received from venture capital investments included in interest income | |||||

| - $1.3 million of securities gains from marks to sales price for venture capital investments | |||||

| - Fourth quarter includes $2.3 million of gains on repurchase of $35.0 million of debt | |||||

| - Prior quarter included $18.9 million of gains on repurchase of $91.7 million of debt | |||||

5

CHARGES FOR RESTRUCTURING, REPOSITIONING, & EFFICIENCY INITIATIVES | ||||||||||||||||||||

| Unaudited | ||||||||||||||||||||

| By Income Statement Impact (Thousands, rounded) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | |||||||||||||||

| Noninterest income | ||||||||||||||||||||

| Mortgage banking | $ | - | $ | (700 | ) | $ | (9,300 | ) | $ | (2,700 | ) | $ | (6,400 | ) | ||||||

| Gains/(Losses) on divestitures | (100 | ) | (17,500 | ) | (400 | ) | (1,000 | ) | 15,700 | |||||||||||

| Noninterest expense | ||||||||||||||||||||

| Employee compensation, incentives, and benefits | 600 | 10,700 | 5,700 | 7,400 | 8,400 | |||||||||||||||

| Occupancy | (200 | ) | 3,900 | 3,400 | 1,000 | 5,500 | ||||||||||||||

| Operations services | - | - | - | - | 400 | |||||||||||||||

| Equipment rentals, depreciation, and maintenance | - | 100 | 4,200 | - | 500 | |||||||||||||||

| All other expense | 9,800 | 1,000 | 3,000 | 9,200 | 21,100 | |||||||||||||||

| Total (loss) before income taxes | $ | (10,300 | ) | $ | (33,900 | ) | $ | (26,000 | ) | $ | (21,300 | ) | $ | (26,600 | ) | |||||

6

| CONSOLIDATED SUMMARY RESULTS | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Income Statement Highlights | ||||||||||||||||||||||||||||

| Net interest income | $ | 204,948 | $ | 223,147 | $ | 238,895 | $ | 228,092 | $ | 225,987 | (8 | )% | (9 | )% | ||||||||||||||

| Noninterest income | 336,672 | 305,383 | 400,018 | 383,130 | 103,429 | 10 | % | 226 | % | |||||||||||||||||||

| Securities gains/(losses), net | 1,346 | (210 | ) | (972 | ) | 65,946 | (10,442 | ) | NM | NM | ||||||||||||||||||

| Total revenue | 542,966 | 528,320 | 637,941 | 677,168 | 318,974 | 3 | % | 70 | % | |||||||||||||||||||

| Noninterest expense | 349,658 | 402,274 | 465,843 | 438,277 | 561,559 | (13 | )% | (38 | )% | |||||||||||||||||||

| Provision | 280,000 | 340,000 | 220,000 | 240,000 | 156,519 | (18 | )% | 79 | % | |||||||||||||||||||

| Pre-tax income/(loss) | (86,692 | ) | (213,954 | ) | (47,902 | ) | (1,109 | ) | (399,104 | ) | 59 | % | 78 | % | ||||||||||||||

| Benefit for income taxes | (30,988 | ) | (88,859 | ) | (28,821 | ) | (8,146 | ) | (146,342 | ) | 65 | % | 79 | % | ||||||||||||||

| Income/(loss) from continuing operations | (55,704 | ) | (125,095 | ) | (19,081 | ) | 7,037 | (252,762 | ) | 55 | % | 78 | % | |||||||||||||||

Income from discontinued operations, net of tax | - | - | - | 883 | 4,137 | - | (100 | )% | ||||||||||||||||||||

| Net income/(loss) | $ | (55,704 | ) | $ | (125,095 | ) | $ | (19,081 | ) | $ | 7,920 | $ | (248,625 | ) | 55 | % | 78 | % | ||||||||||

| Preferred stock dividends | - | - | - | - | - | - | - | |||||||||||||||||||||

| Income/(loss) available to common shareholders | $ | (55,704 | ) | $ | (125,095 | ) | $ | (19,081 | ) | $ | 7,920 | $ | (248,625 | ) | 55 | % | 78 | % | ||||||||||

| Common Stock Data | ||||||||||||||||||||||||||||

| Diluted EPS from continuing operations (a) | $ | (.27 | ) | $ | (.61 | ) | $ | (.11 | ) | $ | .05 | $ | (1.91 | ) | 56 | % | 86 | % | ||||||||||

| Diluted EPS (a) | (.27 | ) | (.61 | ) | (.11 | ) | .06 | (1.88 | ) | 56 | % | 86 | % | |||||||||||||||

| Diluted shares (a) | 204,882 | 204,880 | 180,186 | 132,938 | 132,336 | * | 55 | % | ||||||||||||||||||||

| Period-end shares outstanding (a) | 205,819 | 205,837 | 205,994 | 133,639 | 133,218 | * | 54 | % | ||||||||||||||||||||

| Dividends declared per share (b) | NM (c) | NM (d) | $ | .19 | (e) | $ | .19 | (e) | $ | .43 | (e) | NM | NM | |||||||||||||||

| Balance Sheet Highlights (Period End) | ||||||||||||||||||||||||||||

| Total loans, net of unearned income | $ | 21,278,190 | $ | 21,601,898 | $ | 22,225,232 | $ | 21,932,020 | $ | 22,103,516 | (1 | )% | (4 | )% | ||||||||||||||

| Total loans held for sale-divestiture | - | - | - | 207,672 | 289,878 | - | (100 | )% | ||||||||||||||||||||

| Total deposits | 14,241,814 | 13,778,235 | 15,093,947 | 16,188,542 | 17,032,285 | 3 | % | (16 | )% | |||||||||||||||||||

| Total deposits-divestiture | - | - | 296,632 | 118,720 | 230,418 | - | (100 | )% | ||||||||||||||||||||

| Total assets | 31,021,980 | 32,804,376 | 35,549,961 | 37,267,945 | 37,015,461 | (5 | )% | (16 | )% | |||||||||||||||||||

| Total assets-divestiture | - | - | 395,628 | 216,431 | 305,734 | - | (100 | )% | ||||||||||||||||||||

| Total liabilities | 27,447,348 | 29,931,458 | 32,557,238 | 34,860,441 | 34,584,588 | (8 | )% | (21 | )% | |||||||||||||||||||

| Total liabilities-divestiture | - | - | 298,098 | 120,590 | 232,343 | - | (100 | )% | ||||||||||||||||||||

| Total shareholders' equity | 3,279,467 | 2,577,641 | 2,697,446 | 2,112,227 | 2,135,596 | 27 | % | 54 | % | |||||||||||||||||||

| Key Ratios & Other | ||||||||||||||||||||||||||||

| Return on average assets | (.71 | )% | (1.49 | )% | (.21 | )% | .09 | % | (2.65 | )% | ||||||||||||||||||

| Return on average equity (f) | (7.14 | )% | (18.30 | )% | (3.02 | )% | 1.47 | % | (42.52 | )% | ||||||||||||||||||

| Net interest margin | 2.96 | % | 3.01 | % | 3.01 | % | 2.81 | % | 2.77 | % | ||||||||||||||||||

| Efficiency ratio | 64.4 | % | 76.1 | % | 73.0 | % | 64.7 | % | 176.1 | % | ||||||||||||||||||

| Book value per common share | $ | 12.13 | $ | 12.52 | $ | 13.09 | $ | 15.81 | $ | 16.03 | ||||||||||||||||||

| Tangible book value per common share | $ | 10.98 | $ | 11.36 | $ | 11.92 | $ | 13.98 | $ | 14.16 | ||||||||||||||||||

| FTE employees | 6,095 | 6,195 | 9,386 | 9,711 | 10,174 | (2 | )% | (40 | )% | |||||||||||||||||||

| NM - Not meaningful | |

| * Amount is less than one percent. | |

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| (a) | Shares restated for October 1, 2008 and January 1, 2009 stock dividends. |

| (b) | Third and fourth quarter 2008 dividend declared paid in shares. |

| (c) | Stock dividend rate of 1.837% per share. |

| (d) | Stock dividend rate of 3.0615% per share. |

| (e) | Cash dividends per share restated for October 1, 2008, and January 1, 2009, stock dividends. |

| (f) | Ratio includes preferred stock related to the CPP. |

7

| CONSOLIDATED INCOME STATEMENT | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Interest income | $ | 331,554 | $ | 383,243 | $ | 415,485 | $ | 476,443 | $ | 545,136 | (13 | )% | (39 | )% | ||||||||||||||

| Less interest expense | 126,606 | 160,096 | 176,590 | 248,351 | 319,149 | (21 | )% | (60 | )% | |||||||||||||||||||

| Net interest income | 204,948 | 223,147 | 238,895 | 228,092 | 225,987 | (8 | )% | (9 | )% | |||||||||||||||||||

| Provision for loan losses | 280,000 | 340,000 | 220,000 | 240,000 | 156,519 | (18 | )% | 79 | % | |||||||||||||||||||

| Net interest income/(loss) after | ||||||||||||||||||||||||||||

| provision for loan losses | (75,052 | ) | (116,853 | ) | 18,895 | (11,908 | ) | 69,468 | 36 | % | (208 | )% | ||||||||||||||||

| Noninterest income: | ||||||||||||||||||||||||||||

| Capital markets | 174,671 | 95,954 | 122,338 | 131,457 | 98,482 | 82 | % | 77 | % | |||||||||||||||||||

| Deposit transactions | ||||||||||||||||||||||||||||

| and cash management | 43,882 | 45,802 | 46,797 | 42,553 | 47,971 | (4 | )% | (9 | )% | |||||||||||||||||||

| Mortgage banking (a) (b) (c) | 80,087 | 106,817 | 172,418 | 158,712 | (113,965 | ) | (25 | )% | 170 | % | ||||||||||||||||||

| Trust services and investment | ||||||||||||||||||||||||||||

| management | 7,675 | 8,154 | 8,883 | 9,109 | 10,097 | (6 | )% | (24 | )% | |||||||||||||||||||

| Insurance commissions | 6,806 | 7,332 | 6,822 | 8,144 | 7,529 | (7 | )% | (10 | )% | |||||||||||||||||||

| Revenue from loan sales and securitizations (d) | (782 | ) | 3,238 | (6,984 | ) | (4,097 | ) | (171 | ) | (124 | )% | (357 | )% | |||||||||||||||

| Securities gains/(losses), net | 1,346 | (210 | ) | (972 | ) | 65,946 | (10,442 | ) | NM | NM | ||||||||||||||||||

| Gains/(losses) on divestitures (e) | (106 | ) | (17,489 | ) | (429 | ) | (995 | ) | 15,695 | 99 | % | (101 | )% | |||||||||||||||

| Other | 24,439 | 55,575 | 50,173 | 38,247 | 37,791 | (56 | )% | (35 | )% | |||||||||||||||||||

| Total noninterest income | 338,018 | 305,173 | 399,046 | 449,076 | 92,987 | 11 | % | 264 | % | |||||||||||||||||||

| Adjusted gross income after | ||||||||||||||||||||||||||||

| provision for loan losses | 262,966 | 188,320 | 417,941 | 437,168 | 162,455 | 40 | % | 62 | % | |||||||||||||||||||

| Noninterest expense: | ||||||||||||||||||||||||||||

| Employee compensation, | ||||||||||||||||||||||||||||

| incentives and benefits (c) (e) | 180,871 | 215,498 | 277,078 | 287,470 | 226,905 | (16 | )% | (20 | )% | |||||||||||||||||||

| Occupancy (e) | 19,149 | 27,210 | 30,018 | 28,591 | 34,209 | (30 | )% | (44 | )% | |||||||||||||||||||

| Operations services | 19,345 | 20,041 | 19,124 | 18,964 | 20,148 | (3 | )% | (4 | )% | |||||||||||||||||||

| Equipment rentals, depreciation | ||||||||||||||||||||||||||||

| and maintenance | 11,454 | 12,336 | 18,268 | 15,011 | 16,252 | (7 | )% | (30 | )% | |||||||||||||||||||

| Legal and professional fees | 17,711 | 16,955 | 14,030 | 15,022 | 17,629 | 4 | % | * | ||||||||||||||||||||

| Communications and courier | 7,754 | 9,628 | 11,477 | 11,004 | 10,664 | (19 | )% | (27 | )% | |||||||||||||||||||

| Amortization of intangible assets | 1,805 | 1,802 | 2,182 | 2,440 | 2,864 | * | (37 | )% | ||||||||||||||||||||

| Goodwill impairment | - | - | - | - | 71,074 | NM | NM | |||||||||||||||||||||

| Other (c) (e) (f) (g) | 91,569 | 98,804 | 93,666 | 59,775 | 161,814 | (7 | )% | (43 | )% | |||||||||||||||||||

| Total noninterest expense | 349,658 | 402,274 | 465,843 | 438,277 | 561,559 | (13 | )% | (38 | )% | |||||||||||||||||||

| Pretax (loss) | (86,692 | ) | (213,954 | ) | (47,902 | ) | (1,109 | ) | (399,104 | ) | 59 | % | 78 | % | ||||||||||||||

| Benefit for income taxes | (30,988 | ) | (88,859 | ) | (28,821 | ) | (8,146 | ) | (146,342 | ) | 65 | % | 79 | % | ||||||||||||||

| Income/(loss) from continuing operations | $ | (55,704 | ) | $ | (125,095 | ) | $ | (19,081 | ) | $ | 7,037 | $ | (252,762 | ) | 55 | % | 78 | % | ||||||||||

| Income from discontinued operations, | ||||||||||||||||||||||||||||

| net of tax | - | - | - | 883 | 4,137 | NM | NM | |||||||||||||||||||||

| Net income/(loss) | $ | (55,704 | ) | $ | (125,095 | ) | $ | (19,081 | ) | $ | 7,920 | $ | (248,625 | ) | 55 | % | 78 | % | ||||||||||

| Preferred stock dividends | - | - | - | - | - | NM | NM | |||||||||||||||||||||

| Income/(loss) available to common shareholders | $ | (55,704 | ) | $ | (125,095 | ) | $ | (19,081 | ) | $ | 7,920 | $ | (248,625 | ) | 55 | % | 78 | % | ||||||||||

| NM - Not meaningful | |

| * Amount is less than one percent. | |

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| 4Q08 Key Impacts | |

| (a) | Includes recognition of liability for minimum servicing fee guarantee related to prior servicing sales. |

| (b) | Includes effects of electing fair value for mortgage warehouse loans. |

| (c) | Includes effect of adopting new accounting standards. |

| (d) | Includes MSR valuation adjustment related to prior consumer loan sales. |

| (e) | Includes a portion of net charges for $10.3 million, see Restructuring, Repositioning & Efficiency Initiatives page for further details. |

| (f) | Includes increase in reinsurance reserves for PMI reinsurance contracts. |

| (g) | Includes reversal of expense related to Visa litigation matters for which FHN is contingently liable. |

8

| OTHER INCOME AND OTHER EXPENSE | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Other Income | ||||||||||||||||||||||||||||

| Brokerage management fees and | ||||||||||||||||||||||||||||

| commissions | $ | 7,307 | $ | 7,824 | $ | 8,690 | $ | 8,413 | $ | 8,747 | (7 | )% | (16 | )% | ||||||||||||||

| Bank owned life insurance | 5,107 | 6,731 | 6,343 | 6,962 | 6,697 | (24 | )% | (24 | )% | |||||||||||||||||||

| Bankcard income | 5,226 | 5,587 | 5,728 | 5,540 | 6,221 | (6 | )% | (16 | )% | |||||||||||||||||||

| Other service charges | 3,002 | 3,043 | 3,189 | 3,396 | 3,357 | (1 | )% | (11 | )% | |||||||||||||||||||

| Remittance processing | 3,160 | 3,314 | 3,206 | 3,273 | 3,450 | (5 | )% | (8 | )% | |||||||||||||||||||

| Reinsurance fees | 2,624 | 2,830 | 3,320 | 3,145 | 2,794 | (7 | )% | (6 | )% | |||||||||||||||||||

| ATM interchange fees | 2,485 | 2,263 | 2,238 | 2,238 | 2,224 | 10 | % | 12 | % | |||||||||||||||||||

| Deferred compensation | (12,531 | ) | (5,145 | ) | 1,325 | (6,550 | ) | (1,667 | ) | 144 | % | 652 | % | |||||||||||||||

| Letter of credit | 1,322 | 1,603 | 1,274 | 1,458 | 1,759 | (18 | )% | (25 | )% | |||||||||||||||||||

| Electronic banking fees | 1,492 | 1,535 | 1,572 | 1,618 | 1,636 | (3 | )% | (9 | )% | |||||||||||||||||||

| Check clearing fees | 538 | 838 | 887 | 862 | 1,125 | (36 | )% | (52 | )% | |||||||||||||||||||

| Federal flood certifications | - | 863 | 1,259 | 1,523 | 1,084 | (100 | )% | (100 | )% | |||||||||||||||||||

| Other | 4,707 | 24,289 | 11,142 | 6,369 | 364 | (81 | )% | NM | ||||||||||||||||||||

| Total | $ | 24,439 | $ | 55,575 | $ | 50,173 | $ | 38,247 | $ | 37,791 | (56 | )% | (35 | )% | ||||||||||||||

| Other Expense | ||||||||||||||||||||||||||||

| Computer software (a) | 7,151 | 7,162 | 8,120 | 7,956 | 26,185 | * | (73 | )% | ||||||||||||||||||||

| Advertising and public relations (a) | 7,366 | 9,142 | 7,179 | 9,327 | 10,297 | (19 | )% | (28 | )% | |||||||||||||||||||

| Travel and entertainment (a) | 3,314 | 3,358 | 5,672 | 5,027 | 5,829 | (1 | )% | (43 | )% | |||||||||||||||||||

| Low income housing expense | 4,289 | 5,064 | 4,815 | 4,566 | 6,605 | (15 | )% | (35 | )% | |||||||||||||||||||

| Contract employment (a) | 11,569 | 9,033 | 7,359 | 5,584 | 5,202 | NM | NM | |||||||||||||||||||||

| Distributions on preferred stock | ||||||||||||||||||||||||||||

| of subsidiary | 4,209 | 2,875 | 2,844 | 4,061 | 4,679 | 46 | % | (10 | )% | |||||||||||||||||||

| Foreclosed real estate | 10,941 | 4,979 | 10,720 | 6,362 | 8,871 | 120 | % | 23 | % | |||||||||||||||||||

| Supplies (a) | 2,053 | 2,725 | 2,942 | 3,020 | 3,496 | (25 | )% | (41 | )% | |||||||||||||||||||

| Loan closing costs | 3,129 | 10,314 | 11,718 | 13,060 | 1,279 | (70 | )% | 145 | % | |||||||||||||||||||

| Customer relations | 1,897 | 2,727 | 2,544 | 1,707 | 2,834 | (30 | )% | (33 | )% | |||||||||||||||||||

| Other insurance and taxes | 2,305 | 749 | 2,036 | 1,758 | 2,684 | 208 | % | (14 | )% | |||||||||||||||||||

| Employee training and dues | 1,771 | 1,485 | 1,632 | 1,398 | 1,183 | 19 | % | 50 | % | |||||||||||||||||||

| Fed services fees | 1,526 | 1,975 | 1,941 | 1,611 | 1,463 | (23 | )% | 4 | % | |||||||||||||||||||

| Complimentary check expense | 1,065 | 1,259 | 1,154 | 1,298 | 1,206 | (15 | )% | (12 | )% | |||||||||||||||||||

| Loan insurance expense | 1,482 | 1,477 | 1,198 | 1,113 | 1,073 | * | 38 | % | ||||||||||||||||||||

| Bank examination costs | 514 | 1,523 | 1,054 | 1,053 | 1,142 | (66 | )% | (55 | )% | |||||||||||||||||||

| Deposit insurance premium | 4,288 | 4,146 | 3,403 | 2,827 | 1,223 | 3 | % | 251 | % | |||||||||||||||||||

| Other (a) (b) (c) | 22,700 | 28,811 | 17,335 | (11,953 | ) | 76,563 | (21 | )% | (70 | )% | ||||||||||||||||||

| Total | $ | 91,569 | $ | 98,804 | $ | 93,666 | $ | 59,775 | $ | 161,814 | (7 | )% | (43 | )% | ||||||||||||||

| NM - Not meaningful | |

| * Amount is less than one percent. | |

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| 4Q08 Key Impacts | |

| (a) | Includes a portion of net charges for $9.8 million, see Restructuring, Repositioning & Efficiency Initiatives page for further details. |

| (b) | Includes increase in reinsurance reserves for PMI reinsurance contracts. |

| (c) | Includes reversal of expense related to Visa litigation matters for which FHN is contingently liable. |

9

| CONSOLIDATED PERIOD-END BALANCE SHEET | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||

| Investment securities | $ | 3,125,153 | $ | 2,840,739 | $ | 2,896,928 | $ | 3,034,798 | $ | 3,032,791 | 10 | % | 3 | % | ||||||||||||||

| Loans held for sale | 566,654 | 718,029 | 2,554,030 | 3,616,018 | 3,461,712 | (21 | )% | (84 | )% | |||||||||||||||||||

| Loans held for sale-divestiture (a) | - | - | - | 207,672 | 289,878 | NM | NM | |||||||||||||||||||||

| Loans, net of unearned income | 21,278,190 | 21,601,898 | 22,225,232 | 21,932,020 | 22,103,516 | (1 | )% | (4 | )% | |||||||||||||||||||

| Federal funds sold and securities | ||||||||||||||||||||||||||||

| purchased under agreements to resell | 772,357 | 921,295 | 1,166,982 | 898,615 | 1,089,495 | (16 | )% | (29 | )% | |||||||||||||||||||

| Interest bearing cash | 207,792 | 37,546 | 39,829 | 46,382 | 39,422 | 453 | % | 427 | % | |||||||||||||||||||

| Trading securities | 945,766 | 1,561,024 | 1,473,815 | 1,553,053 | 1,768,763 | (39 | )% | (47 | )% | |||||||||||||||||||

| Trading securities-divestiture (a) | - | - | 89,239 | - | - | NM | NM | |||||||||||||||||||||

| Total earning assets | 26,895,912 | 27,680,531 | 30,446,055 | 31,288,558 | 31,785,577 | (3 | )% | (15 | )% | |||||||||||||||||||

| Cash and due from banks | 552,423 | 815,935 | 838,376 | 851,875 | 1,170,220 | (32 | )% | (53 | )% | |||||||||||||||||||

| Capital markets receivables | 1,178,932 | 1,651,547 | 994,571 | 1,680,057 | 524,419 | (29 | )% | 125 | % | |||||||||||||||||||

| Mortgage servicing rights, net | 376,844 | 798,491 | 903,634 | 895,923 | 1,159,820 | (53 | )% | (68 | )% | |||||||||||||||||||

| Mortgage servicing rights, net-divestiture (a) | - | - | 235,761 | - | - | NM | NM | |||||||||||||||||||||

| Goodwill | 192,408 | 192,408 | 192,408 | 192,408 | 192,408 | NM | NM | |||||||||||||||||||||

| Other intangible assets, net | 45,081 | 46,887 | 48,615 | 52,017 | 56,907 | (4 | )% | (21 | )% | |||||||||||||||||||

| Premises and equipment, net | 333,931 | 336,078 | 344,410 | 382,488 | 399,305 | * | (16 | )% | ||||||||||||||||||||

| Real estate acquired by foreclosure (b) | 125,538 | 151,461 | 141,857 | 106,018 | 103,982 | (17 | )% | 21 | % | |||||||||||||||||||

| Allowance for loan losses | (849,210 | ) | (760,456 | ) | (575,149 | ) | (483,203 | ) | (342,341 | ) | 12 | % | 148 | % | ||||||||||||||

| Other assets | 2,170,121 | 1,891,494 | 1,908,795 | 2,293,045 | 1,949,308 | 15 | % | 11 | % | |||||||||||||||||||

| Other assets-divestiture (a) | - | - | 70,628 | 8,759 | 15,856 | NM | NM | |||||||||||||||||||||

| Total assets | $ | 31,021,980 | $ | 32,804,376 | $ | 35,549,961 | $ | 37,267,945 | $ | 37,015,461 | (5 | )% | (16 | )% | ||||||||||||||

| Liabilities and Shareholders' Equity | ||||||||||||||||||||||||||||

| Deposits | ||||||||||||||||||||||||||||

| Savings | $ | 4,824,939 | $ | 4,350,832 | $ | 4,041,352 | $ | 4,217,215 | $ | 3,872,684 | 11 | % | 25 | % | ||||||||||||||

| Other interest-bearing deposits | 1,783,362 | 1,638,731 | 1,880,678 | 1,986,556 | 1,946,933 | 9 | % | (8 | )% | |||||||||||||||||||

| Time deposits | 2,294,644 | 2,510,344 | 2,468,521 | 2,648,339 | 2,826,301 | (9 | )% | (19 | )% | |||||||||||||||||||

| Interest bearing deposits-divestiture (a) | - | - | - | 99,370 | 189,051 | NM | NM | |||||||||||||||||||||

| Total interest-bearing core deposits | 8,902,945 | 8,499,907 | 8,390,551 | 8,951,480 | 8,834,969 | 5 | % | * | ||||||||||||||||||||

| Noninterest-bearing deposits | 3,956,633 | 3,808,239 | 4,453,332 | 4,995,696 | 5,026,417 | 4 | % | (21 | )% | |||||||||||||||||||

| Noninterest-bearing deposits-divestiture (a) | - | - | 296,632 | 18,197 | 28,750 | NM | NM | |||||||||||||||||||||

| Total core deposits | 12,859,578 | 12,308,146 | 13,140,515 | 13,965,373 | 13,890,136 | 4 | % | (7 | )% | |||||||||||||||||||

| Certificates of deposit $100,000 and more | 1,382,236 | 1,470,089 | 1,953,432 | 2,222,016 | 3,129,532 | (6 | )% | (56 | )% | |||||||||||||||||||

| Certificates of deposit $100,000 and more-divestiture (a) | - | - | - | 1,153 | 12,617 | NM | NM | |||||||||||||||||||||

| Total deposits | 14,241,814 | 13,778,235 | 15,093,947 | 16,188,542 | 17,032,285 | 3 | % | (16 | )% | |||||||||||||||||||

| Federal funds purchased and securities | ||||||||||||||||||||||||||||

| sold under agreements to repurchase | 1,751,079 | 1,890,681 | 2,620,014 | 3,678,217 | 4,829,597 | (7 | )% | (64 | )% | |||||||||||||||||||

| Federal funds purchased and securities | ||||||||||||||||||||||||||||

| sold under agreements to repurchase-divestiture (a) | - | - | - | 11,572 | 20,999 | NM | NM | |||||||||||||||||||||

| Trading liabilities | 359,502 | 380,896 | 464,225 | 531,259 | 556,144 | (6 | )% | (35 | )% | |||||||||||||||||||

| Other short term borrowings and commercial paper (c) | 4,279,689 | 6,149,073 | 5,998,810 | 4,753,582 | 3,422,995 | (30 | )% | 25 | % | |||||||||||||||||||

| Term borrowings | 4,022,297 | 4,545,791 | 5,783,407 | 6,060,795 | 6,027,967 | (12 | )% | (33 | )% | |||||||||||||||||||

| Other collateralized borrowings | 745,363 | 749,797 | 767,010 | 809,273 | 800,450 | * | (7 | )% | ||||||||||||||||||||

| Total long-term debt | 4,767,660 | 5,295,588 | 6,550,417 | 6,870,068 | 6,828,417 | (10 | )% | (30 | )% | |||||||||||||||||||

| Capital markets payables | 1,115,428 | 1,645,118 | 868,883 | 1,688,870 | 586,358 | (32 | )% | 90 | % | |||||||||||||||||||

| Other liabilities | 932,176 | 785,061 | 959,476 | 1,136,461 | 1,305,868 | 19 | % | (29 | )% | |||||||||||||||||||

| Other liabilities-divestiture (a) | - | - | 1,466 | 1,870 | 1,925 | NM | NM | |||||||||||||||||||||

| Total liabilities | 27,447,348 | 29,924,652 | 32,557,238 | 34,860,441 | 34,584,588 | (8 | )% | (21 | )% | |||||||||||||||||||

| Preferred stock of subsidiary | 295,165 | 295,277 | 295,277 | 295,277 | 295,277 | * | * | |||||||||||||||||||||

| Shareholders' Equity | ||||||||||||||||||||||||||||

| Preferred stock capital surplus - (CPP) | 782,680 | - | - | - | - | NM | NM | |||||||||||||||||||||

| Common stock | 128,302 | 125,996 | 122,345 | 79,242 | 78,979 | 2 | % | 62 | % | |||||||||||||||||||

| Capital surplus | 1,048,602 | 1,016,498 | 980,428 | 362,823 | 361,826 | 3 | % | 190 | % | |||||||||||||||||||

| Capital surplus common stock warrants - (CPP) | 83,860 | - | - | - | - | NM | NM | |||||||||||||||||||||

| Undivided profits | 1,387,854 | 1,489,990 | 1,646,272 | 1,704,559 | 1,742,892 | (7 | )% | (20 | )% | |||||||||||||||||||

| Accumulated other comprehensive loss, net | (151,831 | ) | (48,037 | ) | (51,599 | ) | (34,397 | ) | (48,101 | ) | (216 | )% | (216 | )% | ||||||||||||||

| Total shareholders' equity | 3,279,467 | 2,584,447 | 2,697,446 | 2,112,227 | 2,135,596 | 27 | % | 54 | % | |||||||||||||||||||

| Total liabilities and shareholders' equity | $ | 31,021,980 | $ | 32,804,376 | $ | 35,549,961 | $ | 37,267,945 | $ | 37,015,461 | (5 | )% | (16 | )% | ||||||||||||||

| NM - Not meaningful | |

| * Amount is less than one percent. | |

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| (a) | Second quarter 2008 associated with the sale of certain mortgage operations, prior periods associated with the sale of First Horizon Bank branches. |

| (b) | Fourth quarter 2008 includes $21.2 million of foreclosed assets related to government insured mortgages. |

| (c) | Fourth quarter 2008 includes $4.0 billion of FRB Term Auction Facility borrowings. |

10

| CONSOLIDATED AVERAGE AND PERIOD-END LOANS | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Average Loans (Net) | ||||||||||||||||||||||||||||

| Commercial | ||||||||||||||||||||||||||||

| Commercial, financial and industrial | $ | 7,516,557 | $ | 7,530,724 | $ | 7,212,907 | $ | 7,121,890 | $ | 6,957,498 | * | 8 | % | |||||||||||||||

| Real estate commercial (a) | 1,479,582 | 1,497,773 | 1,401,267 | 1,347,377 | 1,301,866 | (1 | )% | 14 | % | |||||||||||||||||||

| Real estate construction (b) | 1,917,647 | 2,162,817 | 2,481,680 | 2,713,253 | 2,825,210 | (11 | )% | (32 | )% | |||||||||||||||||||

| Total commercial loans | 10,913,786 | 11,191,314 | 11,095,854 | 11,182,520 | 11,084,574 | (2 | )% | (2 | )% | |||||||||||||||||||

| Retail | ||||||||||||||||||||||||||||

| Real estate residential (c) | 8,172,174 | 8,166,295 | 7,878,845 | 7,774,415 | 7,605,345 | * | 7 | % | ||||||||||||||||||||

| Real estate construction (d) | 1,087,752 | 1,350,092 | 1,666,007 | 1,909,061 | 2,096,561 | (19 | )% | (48 | )% | |||||||||||||||||||

| Other retail | 137,185 | 138,848 | 138,242 | 141,961 | 144,116 | (1 | )% | (5 | )% | |||||||||||||||||||

| Credit card receivables | 190,189 | 193,517 | 193,850 | 195,081 | 201,153 | (2 | )% | (5 | )% | |||||||||||||||||||

| Real estate loans pledged against | ||||||||||||||||||||||||||||

| other collateralized borrowings (e) | 716,925 | 721,760 | 735,828 | 755,071 | 779,013 | (1 | )% | (8 | )% | |||||||||||||||||||

| Total retail loans | 10,304,225 | 10,570,512 | 10,612,772 | 10,775,589 | 10,826,188 | (3 | )% | (5 | )% | |||||||||||||||||||

| Total loans, net of unearned income | $ | 21,218,011 | $ | 21,761,826 | $ | 21,708,626 | $ | 21,958,109 | $ | 21,910,762 | (2 | )% | (3 | )% | ||||||||||||||

| Period-End Loans (Net) | ||||||||||||||||||||||||||||

| Commercial | ||||||||||||||||||||||||||||

| Commercial, financial and industrial | $ | 7,863,727 | $ | 7,642,684 | $ | 7,717,110 | $ | 7,238,630 | $ | 7,140,087 | 3 | % | 10 | % | ||||||||||||||

| Real estate commercial (a) | 1,454,040 | 1,492,323 | 1,463,726 | 1,345,526 | 1,294,922 | (3 | )% | 12 | % | |||||||||||||||||||

| Real estate construction (b) | 1,778,140 | 2,020,455 | 2,271,533 | 2,602,968 | 2,753,475 | (12 | )% | (35 | )% | |||||||||||||||||||

| Total commercial loans | 11,095,907 | 11,155,462 | 11,452,369 | 11,187,124 | 11,188,484 | (1 | )% | (1 | )% | |||||||||||||||||||

| Retail | ||||||||||||||||||||||||||||

| Real estate residential (c) | 8,161,435 | 8,192,926 | 8,196,622 | 7,858,109 | 7,791,885 | * | 5 | % | ||||||||||||||||||||

| Real estate construction (d) | 980,798 | 1,201,911 | 1,513,845 | 1,814,863 | 2,008,289 | (18 | )% | (51 | )% | |||||||||||||||||||

| Other retail | 135,779 | 139,441 | 138,970 | 138,253 | 144,019 | (3 | )% | (6 | )% | |||||||||||||||||||

| Credit card receivables | 189,554 | 194,966 | 195,703 | 191,119 | 204,812 | (3 | )% | (7 | )% | |||||||||||||||||||

| Real estate loans pledged against | ||||||||||||||||||||||||||||

| other collateralized borrowings (e) | 714,717 | 717,192 | 727,723 | 742,552 | 766,027 | * | (7 | )% | ||||||||||||||||||||

| Total retail loans | 10,182,283 | 10,446,436 | 10,772,863 | 10,744,896 | 10,915,032 | (3 | )% | (7 | )% | |||||||||||||||||||

| Total loans, net of unearned income | $ | 21,278,190 | $ | 21,601,898 | $ | 22,225,232 | $ | 21,932,020 | $ | 22,103,516 | (1 | )% | (4 | )% | ||||||||||||||

| * Amount is less than one percent. | |

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| (a) | Includes nonconstruction income property loans. |

| (b) | Includes home builder, condominium, and income property construction loans. |

| (c) | Includes home equity loans, home equity lines of credit and permanent mortgages. |

| (d) | Includes one-time close product. |

| (e) | Includes on balance sheet securitizations of home equity loans. |

11

| CONSOLIDATED AVERAGE BALANCE SHEET | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||||

| Earning assets: | ||||||||||||||||||||||||||||

| Loans, net of unearned income (a) | $ | 21,218,011 | $ | 21,761,826 | $ | 21,708,626 | $ | 21,958,109 | $ | 21,910,762 | (2 | )% | (3 | )% | ||||||||||||||

| Loans held for sale | 650,844 | 1,950,831 | 3,606,621 | 3,728,008 | 3,337,237 | (67 | )% | (80 | )% | |||||||||||||||||||

| Loans held for sale-divestiture (b) | - | - | 195,175 | 248,751 | 467,424 | NM | NM | |||||||||||||||||||||

| Investment securities: | ||||||||||||||||||||||||||||

| U.S. Treasuries | 48,415 | 47,843 | 47,123 | 43,305 | 36,062 | 1 | % | 34 | % | |||||||||||||||||||

| U.S. government agencies | 2,576,587 | 2,524,895 | 2,649,651 | 2,725,948 | 2,787,078 | 2 | % | (8 | )% | |||||||||||||||||||

| States and municipalities | 75,084 | 31,682 | 31,347 | 12,847 | 1,740 | 137 | % | NM | ||||||||||||||||||||

| Other | 282,639 | 268,939 | 257,907 | 232,472 | 230,808 | 5 | % | 22 | % | |||||||||||||||||||

| Total investment securities | 2,982,725 | 2,873,359 | 2,986,028 | 3,014,572 | 3,055,688 | 4 | % | (2 | )% | |||||||||||||||||||

| Capital markets securities inventory | 1,135,270 | 1,355,501 | 1,630,501 | 1,961,964 | 1,934,055 | (16 | )% | (41 | )% | |||||||||||||||||||

| Mortgage banking trading securities | 242,930 | 304,278 | 387,469 | 405,579 | 527,453 | (20 | )% | (54 | )% | |||||||||||||||||||

| Mortgage banking trading securities-divestiture (b) | - | 62,131 | 981 | - | - | NM | NM | |||||||||||||||||||||

| Other earning assets: | ||||||||||||||||||||||||||||

| Federal funds sold and securities | ||||||||||||||||||||||||||||

| purchased under agreements to resell | 911,387 | 1,213,510 | 1,275,548 | 1,304,707 | 1,237,957 | (25 | )% | (26 | )% | |||||||||||||||||||

| Interest bearing cash | 546,732 | 39,666 | 36,573 | 46,093 | 28,968 | NM | NM | |||||||||||||||||||||

| Total other earning assets | 1,458,119 | 1,253,176 | 1,312,121 | 1,350,800 | 1,266,925 | 16 | % | 15 | % | |||||||||||||||||||

| Total earning assets | 27,687,899 | 29,561,102 | 31,827,522 | 32,667,783 | 32,499,544 | (6 | )% | (15 | )% | |||||||||||||||||||

| Allowance for loan losses | (741,076 | ) | (619,977 | ) | (529,124 | ) | (359,600 | ) | (246,916 | ) | 20 | % | 200 | % | ||||||||||||||

| Cash and due from banks | 495,500 | 638,467 | 697,013 | 786,693 | 846,793 | (22 | )% | (41 | )% | |||||||||||||||||||

| Capital markets receivables | 432,614 | 196,285 | 251,667 | 297,908 | 182,358 | 120 | % | 137 | % | |||||||||||||||||||

| Premises and equipment, net | 334,642 | 339,575 | 373,403 | 390,291 | 407,212 | (1 | )% | (18 | )% | |||||||||||||||||||

| Other assets | 2,839,665 | 3,219,952 | 3,517,017 | 3,367,729 | 3,540,575 | (12 | )% | (20 | )% | |||||||||||||||||||

| Other assets-divestiture (b) | - | 46,091 | 8,603 | 11,581 | 20,868 | NM | NM | |||||||||||||||||||||

| Total assets | $ | 31,049,244 | $ | 33,381,495 | $ | 36,146,101 | $ | 37,162,385 | $ | 37,250,434 | (7 | )% | (17 | )% | ||||||||||||||

| Liabilities and shareholders' equity: | ||||||||||||||||||||||||||||

| Interest-bearing liabilities: | ||||||||||||||||||||||||||||

| Interest-bearing deposits: | ||||||||||||||||||||||||||||

| Interest bearing deposits-divestiture (b) | $ | - | $ | - | $ | 30,695 | $ | 127,352 | $ | 292,615 | NM | NM | ||||||||||||||||

| Other interest-bearing deposits | 1,615,764 | 1,724,504 | 1,911,341 | 1,922,506 | 1,685,749 | (6 | )% | (4 | )% | |||||||||||||||||||

| Savings | 4,741,073 | 4,002,907 | 4,180,739 | 4,134,308 | 3,749,222 | 18 | % | 26 | % | |||||||||||||||||||

| Time deposits | 2,461,921 | 2,422,189 | 2,530,300 | 2,763,335 | 2,850,719 | 2 | % | (14 | )% | |||||||||||||||||||

| Total interest-bearing core deposits | 8,818,758 | 8,149,600 | 8,653,075 | 8,947,501 | 8,578,305 | 8 | % | 3 | % | |||||||||||||||||||

| Certificates of deposit $100,000 and more | 1,491,297 | 1,839,651 | 2,022,972 | 2,696,781 | 4,464,070 | (19 | )% | (67 | )% | |||||||||||||||||||

| Certificates of deposit $100,000 and more-divestiture (b) | - | - | 279 | 4,770 | 30,499 | NM | NM | |||||||||||||||||||||

| Federal funds purchased and securities | ||||||||||||||||||||||||||||

| sold under agreements to repurchase | 2,021,033 | 2,593,485 | 3,810,955 | 5,236,736 | 4,936,968 | (22 | )% | (59 | )% | |||||||||||||||||||

| Federal funds purchased and securities | ||||||||||||||||||||||||||||

| sold under agreements to repurchase-divestiture (b) | - | - | 3,102 | 16,171 | 33,370 | NM | NM | |||||||||||||||||||||

| Capital markets trading liabilities | 488,102 | 708,875 | 768,565 | 846,369 | 812,969 | (31 | )% | (40 | )% | |||||||||||||||||||

| Other short-term borrowings and commercial paper (c) | 5,096,108 | 6,083,691 | 5,513,454 | 3,850,704 | 2,651,882 | (16 | )% | 92 | % | |||||||||||||||||||

| Long term debt: | ||||||||||||||||||||||||||||

| Term borrowings | 4,266,510 | 5,193,319 | 5,886,694 | 6,013,433 | 5,981,215 | (18 | )% | (29 | )% | |||||||||||||||||||

| Other collateralized borrowings | 747,824 | 756,999 | 792,388 | 790,811 | 813,075 | (1 | )% | (8 | )% | |||||||||||||||||||

| Total long-term debt | 5,014,334 | 5,950,318 | 6,679,082 | 6,804,244 | 6,794,290 | (16 | )% | (26 | )% | |||||||||||||||||||

| Total interest-bearing liabilities | 22,929,632 | 25,325,620 | 27,451,484 | 28,403,276 | 28,302,353 | (9 | )% | (19 | )% | |||||||||||||||||||

| Noninterest-bearing deposits | 3,652,161 | 4,031,157 | 4,619,333 | 4,743,479 | 4,838,363 | (9 | )% | (25 | )% | |||||||||||||||||||

| Other noninterest-bearing deposits-divestiture (b) | - | 3,038 | 8,902 | 21,327 | 54,928 | NM | NM | |||||||||||||||||||||

| Capital markets payables | 374,368 | 178,289 | 232,282 | 292,846 | 173,351 | 110 | % | 116 | % | |||||||||||||||||||

| Other liabilities | 692,759 | 827,244 | 995,931 | 1,234,695 | 1,262,345 | (16 | )% | (45 | )% | |||||||||||||||||||

| Other liabilities-divestiture (b) | - | 1,397 | 1,022 | 2,335 | 3,885 | NM | NM | |||||||||||||||||||||

| Preferred stock of subsidiary | 295,165 | 295,277 | 295,277 | 295,277 | 295,277 | * | * | |||||||||||||||||||||

| Shareholders' equity | 3,105,159 | 2,719,473 | 2,541,870 | 2,169,150 | 2,319,932 | 14 | % | 34 | % | |||||||||||||||||||

| Total liabilities and shareholders' equity | $ | 31,049,244 | $ | 33,381,495 | $ | 36,146,101 | $ | 37,162,385 | $ | 37,250,434 | (7 | )% | (17 | )% | ||||||||||||||

| NM - Not meaningful | |

| * Amount is less than one percent. | |

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| (a) | Includes loans on nonaccrual status. |

| (b) | Third and second quarters 2008 associated with the sale of certain mortgage operations, prior periods associated with the sale of First Horizon Bank branches. |

| (c) | In fourth quarter 2008, FRB Term Auction Facility borrowings averaged $3.1 billion and FHLB borrowings averaged $1.7 billion. |

12

| CONSOLIDATED AVERAGE BALANCE SHEET: INCOME & EXPENSE | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||||

| Earning assets: | ||||||||||||||||||||||||||||

| Loans, net of unearned income (a) | $ | 254,946 | $ | 281,777 | $ | 285,539 | $ | 331,803 | $ | 385,027 | (10 | )% | (34 | )% | ||||||||||||||

| Loans held for sale | 9,821 | 29,078 | 54,217 | 58,438 | 62,249 | (66 | )% | (84 | )% | |||||||||||||||||||

| Investment securities: | ||||||||||||||||||||||||||||

| U.S. Treasuries | 233 | 250 | 249 | 340 | 434 | (7 | )% | (46 | )% | |||||||||||||||||||

| U.S. government agencies | 36,565 | 34,886 | 36,573 | 37,954 | 39,027 | 5 | % | (6 | )% | |||||||||||||||||||

| States and municipalities | 944 | 372 | 324 | 220 | 4 | 154 | % | NM | ||||||||||||||||||||

| Other | 6,080 | 3,336 | 2,159 | 2,290 | 2,904 | 82 | % | 109 | % | |||||||||||||||||||

| Total investment securities | 43,822 | 38,844 | 39,305 | 40,804 | 42,369 | 13 | % | 3 | % | |||||||||||||||||||

| Capital markets securities inventory | 12,790 | 15,898 | 18,131 | 22,652 | 25,261 | (20 | )% | (49 | )% | |||||||||||||||||||

| Mortgage banking trading securities | 8,253 | 11,781 | 12,120 | 13,363 | 16,436 | (30 | )% | (50 | )% | |||||||||||||||||||

| Other earning assets: | ||||||||||||||||||||||||||||

| Federal funds sold and securities | ||||||||||||||||||||||||||||

| purchased under agreements to resell | 1,493 | 5,944 | 6,266 | 9,341 | 13,485 | (75 | )% | (89 | )% | |||||||||||||||||||

| Interest bearing cash | 850 | 253 | 189 | 357 | 450 | 236 | % | 89 | % | |||||||||||||||||||

| Total other earning assets | 2,343 | 6,197 | 6,455 | 9,698 | 13,935 | (62 | )% | (83 | )% | |||||||||||||||||||

| Total earning assets/interest income | $ | 331,975 | $ | 383,575 | $ | 415,767 | $ | 476,758 | $ | 545,277 | (13 | )% | (39 | )% | ||||||||||||||

| Liabilities and shareholders' equity: | ||||||||||||||||||||||||||||

| Interest-bearing liabilities: | ||||||||||||||||||||||||||||

| Interest-bearing deposits: | ||||||||||||||||||||||||||||

| Other interest-bearing deposits | $ | 1,552 | $ | 2,849 | $ | 3,556 | $ | 5,906 | $ | 5,976 | (46 | )% | (74 | )% | ||||||||||||||

| Savings | 18,666 | 17,005 | 18,362 | 25,888 | 30,864 | 10 | % | (40 | )% | |||||||||||||||||||

| Time deposits | 21,739 | 22,443 | 25,540 | 31,502 | 35,234 | (3 | )% | (38 | )% | |||||||||||||||||||

| Total interest-bearing core deposits | 41,957 | 42,297 | 47,458 | 63,296 | 72,074 | (1 | )% | (42 | )% | |||||||||||||||||||

| Certificates of deposit $100,000 and more | 12,680 | 15,184 | 17,361 | 31,069 | 59,851 | (16 | )% | (79 | )% | |||||||||||||||||||

| Federal funds purchased and securities | ||||||||||||||||||||||||||||

| sold under agreements to repurchase | 2,738 | 10,696 | 17,834 | 38,521 | 52,635 | (74 | )% | (95 | )% | |||||||||||||||||||

| Capital markets trading liabilities | 5,876 | 8,304 | 9,400 | 9,615 | 10,588 | (29 | )% | (45 | )% | |||||||||||||||||||

| Other short-term borrowings and commercial paper | 20,164 | 36,496 | 31,591 | 31,527 | 30,229 | (45 | )% | (33 | )% | |||||||||||||||||||

| Long term debt: | ||||||||||||||||||||||||||||

| Term borrowings | 38,062 | 41,598 | 47,129 | 66,303 | 82,870 | (9 | )% | (54 | )% | |||||||||||||||||||

| Other collateralized borrowings | 5,129 | 5,521 | 5,817 | 8,020 | 10,902 | (7 | )% | (53 | )% | |||||||||||||||||||

| Total long-term debt | 43,191 | 47,119 | 52,946 | 74,323 | 93,772 | (8 | )% | (54 | )% | |||||||||||||||||||

| Total interest-bearing liabilities/interest expense | $ | 126,606 | $ | 160,096 | $ | 176,590 | $ | 248,351 | $ | 319,149 | (21 | )% | (60 | )% | ||||||||||||||

| Net interest income-tax equivalent basis | $ | 205,369 | $ | 223,479 | $ | 239,177 | $ | 228,407 | $ | 226,128 | (8 | )% | (9 | )% | ||||||||||||||

| Fully taxable equivalent adjustment | (421 | ) | (332 | ) | (282 | ) | (315 | ) | (141 | ) | (27 | )% | (199 | )% | ||||||||||||||

| Net interest income | $ | 204,948 | $ | 223,147 | $ | 238,895 | $ | 228,092 | $ | 225,987 | (8 | )% | (9 | )% | ||||||||||||||

| NM - Not meaningful | |

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| Income amounts are adjusted to a fully taxable equivalent. Earning assets income is expressed net of unearned income. | |

| (a) | Includes loans on nonaccrual status. |

13

| CONSOLIDATED AVERAGE BALANCE SHEET: YIELDS & RATES | ||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | |||||||||||||||

| Assets: | ||||||||||||||||||||

| Earning assets: | ||||||||||||||||||||

| Loans, net of unearned income (a) | 4.78 | % | 5.16 | % | 5.29 | % | 6.07 | % | 6.98 | % | ||||||||||

| Loans held for sale | 6.04 | 5.96 | 5.70 | 5.88 | 6.54 | |||||||||||||||

| Investment securities: | ||||||||||||||||||||

| U.S. Treasuries | 1.92 | 2.08 | 2.13 | 3.15 | 4.77 | |||||||||||||||

| U.S. government agencies | 5.68 | 5.53 | 5.52 | 5.57 | 5.60 | |||||||||||||||

| States and municipalities | 5.03 | 4.70 | 4.14 | 6.87 | .82 | |||||||||||||||

| Other | 8.60 | 4.96 | 3.35 | 3.94 | 5.03 | |||||||||||||||

| Total investment securities | 5.88 | 5.41 | 5.27 | 5.41 | 5.55 | |||||||||||||||

| Capital markets securities inventory | 4.51 | 4.69 | 4.45 | 4.62 | 5.22 | |||||||||||||||

| Mortgage banking trading securities | 13.59 | 12.86 | 12.48 | 13.18 | 12.46 | |||||||||||||||

| Other earning assets: | ||||||||||||||||||||

| Federal funds sold and securities | ||||||||||||||||||||

| purchased under agreements to resell | .65 | 1.95 | 1.98 | 2.88 | 4.32 | |||||||||||||||

| Interest bearing cash | .62 | 2.54 | 2.08 | 3.11 | 6.17 | |||||||||||||||

| Total other earning assets | .64 | 1.97 | 1.98 | 2.89 | 4.36 | |||||||||||||||

| Total earning assets/interest income | 4.78 | % | 5.17 | % | 5.24 | % | 5.86 | % | 6.67 | % | ||||||||||

| Liabilities and shareholders' equity: | ||||||||||||||||||||

| Interest-bearing liabilities: | ||||||||||||||||||||

| Interest-bearing deposits: | ||||||||||||||||||||

| Other interest-bearing deposits | .38 | % | .66 | % | .74 | % | 1.19 | % | 1.33 | % | ||||||||||

| Savings | 1.57 | 1.69 | 1.76 | 2.50 | 3.19 | |||||||||||||||

| Time deposits | 3.51 | 3.69 | 4.06 | 4.55 | 4.73 | |||||||||||||||

| Total interest-bearing core deposits | 1.89 | 2.06 | 2.21 | 2.85 | 3.33 | |||||||||||||||

| Certificates of deposit $100,000 and more | 3.38 | 3.28 | 3.45 | 4.63 | 5.28 | |||||||||||||||

| Federal funds purchased and securities | ||||||||||||||||||||

| sold under agreements to repurchase | .54 | 1.64 | 1.88 | 2.95 | 4.20 | |||||||||||||||

| Capital markets trading liabilities | 4.79 | 4.66 | 4.92 | 4.57 | 5.17 | |||||||||||||||

| Other short-term borrowings and commercial paper | 1.57 | 2.39 | 2.30 | 3.29 | 4.52 | |||||||||||||||

| Long term debt: | ||||||||||||||||||||

| Term borrowings | 3.57 | 3.21 | 3.20 | 4.41 | 5.55 | |||||||||||||||

| Other collateralized borrowings | 2.74 | 2.92 | 2.94 | 4.06 | 5.36 | |||||||||||||||

| Total long-term debt | 3.45 | 3.17 | 3.17 | 4.37 | 5.52 | |||||||||||||||

| Total interest-bearing liabilities/interest expense | 2.20 | % | 2.52 | % | 2.58 | % | 3.51 | % | 4.49 | % | ||||||||||

| Net interest spread | 2.58 | % | 2.65 | % | 2.66 | % | 2.35 | % | 2.18 | % | ||||||||||

| Effect of interest-free sources used to fund | ||||||||||||||||||||

| earning assets | .38 | .36 | .35 | .46 | .59 | |||||||||||||||

| Net interest margin | 2.96 | % | 3.01 | % | 3.01 | % | 2.81 | % | 2.77 | % | ||||||||||

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| Yields are adjusted to a fully taxable equivalent. | |

| Earning assets yields are expressed net of unearned income. | |

| Rates are expressed net of unamortized debenture cost for long-term debt. | |

| Net interest margin is computed using total net interest income. | |

| (a) | Includes loans on nonaccrual status. |

14

| MORTGAGE SERVICING RIGHTS | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| First Liens | ||||||||||||||||||||||||||||

| Fair value beginning balance | $ | 770,635 | $ | 1,111,204 | $ | 865,855 | $ | 1,122,415 | $ | 1,429,245 | (31 | )% | (46 | )% | ||||||||||||||

| Addition of mortgage servicing rights | 1,073 | 61,501 | 100,305 | 78,871 | 67,300 | |||||||||||||||||||||||

| Reductions due to loan payments | (10,771 | ) | (22,179 | ) | (38,598 | ) | (37,448 | ) | (40,930 | ) | ||||||||||||||||||

| Reductions due to sale | (52,006 | ) | (317,640 | ) | (72,271 | ) | (43,842 | ) | (96,502 | ) | ||||||||||||||||||

| Changes in fair value due to: | ||||||||||||||||||||||||||||

| Changes in valuation model inputs | ||||||||||||||||||||||||||||

| or assumptions (a) | (354,558 | ) | (63,061 | ) | 255,890 | (254,076 | ) | (236,695 | ) | |||||||||||||||||||

| Other changes in fair value | 21 | 810 | 23 | (65 | ) | (3 | ) | |||||||||||||||||||||

| Fair value ending balance | $ | 354,394 | $ | 770,635 | $ | 1,111,204 | $ | 865,855 | $ | 1,122,415 | (54 | )% | (68 | )% | ||||||||||||||

| Second Liens | ||||||||||||||||||||||||||||

| Fair value beginning balance | $ | 17,513 | $ | 18,138 | $ | 20,126 | $ | 25,832 | $ | 28,747 | (3 | )% | (39 | )% | ||||||||||||||

| Addition of mortgage servicing rights | - | - | - | - | - | |||||||||||||||||||||||

| Reductions due to loan payments | (1,517 | ) | (614 | ) | (1,737 | ) | (2,617 | ) | (2,097 | ) | ||||||||||||||||||

| Changes in fair value due to: | ||||||||||||||||||||||||||||

| Changes in valuation model inputs | ||||||||||||||||||||||||||||

| or assumptions (a) | (2,438 | ) | (14 | ) | (254 | ) | (3,089 | ) | (834 | ) | ||||||||||||||||||

| Other changes in fair value | - | 3 | 3 | - | 16 | |||||||||||||||||||||||

| Fair value ending balance | $ | 13,558 | $ | 17,513 | $ | 18,138 | $ | 20,126 | $ | 25,832 | (23 | )% | (48 | )% | ||||||||||||||

| HELOC | ||||||||||||||||||||||||||||

| Fair value beginning balance | $ | 10,343 | $ | 10,053 | $ | 9,942 | $ | 11,573 | $ | 12,597 | 3 | % | (18 | )% | ||||||||||||||

| Addition of mortgage servicing rights | 43 | 43 | 215 | 887 | 174 | |||||||||||||||||||||||

| Reductions due to loan payments | (432 | ) | (483 | ) | (491 | ) | (707 | ) | (736 | ) | ||||||||||||||||||

| Changes in fair value due to: | ||||||||||||||||||||||||||||

| Changes in valuation model inputs | ||||||||||||||||||||||||||||

| or assumptions (a) | (1,401 | ) | - | (230 | ) | (1,935 | ) | (462 | ) | |||||||||||||||||||

| Other changes in fair value | 339 | 730 | 617 | 124 | - | |||||||||||||||||||||||

| Fair value ending balance | $ | 8,892 | $ | 10,343 | $ | 10,053 | $ | 9,942 | $ | 11,573 | (14 | )% | (23 | )% | ||||||||||||||

| Total Consolidated | ||||||||||||||||||||||||||||

| Fair value beginning balance | $ | 798,491 | $ | 1,139,395 | $ | 895,923 | $ | 1,159,820 | $ | 1,470,589 | (30 | )% | (46 | )% | ||||||||||||||

| Addition of mortgage servicing rights | 1,116 | 61,544 | 100,520 | 79,758 | 67,474 | |||||||||||||||||||||||

| Reductions due to loan payments | (12,720 | ) | (23,276 | ) | (40,826 | ) | (40,772 | ) | (43,763 | ) | ||||||||||||||||||

| Reductions due to sale | (52,006 | ) | (317,640 | ) | (72,271 | ) | (43,842 | ) | (96,502 | ) | ||||||||||||||||||

| Changes in fair value due to: | ||||||||||||||||||||||||||||

| Changes in valuation model inputs | ||||||||||||||||||||||||||||

| or assumptions (a) | (358,397 | ) | (63,075 | ) | 255,406 | (259,100 | ) | (237,991 | ) | |||||||||||||||||||

| Other changes in fair value | 360 | 1,543 | 643 | 59 | 13 | |||||||||||||||||||||||

| Fair value ending balance | $ | 376,844 | $ | 798,491 | $ | 1,139,395 | $ | 895,923 | $ | 1,159,820 | (53 | )% | (68 | )% | ||||||||||||||

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| (a) | Principally reflects changes in discount rates and prepayment speed assumptions, mostly due to changes in interest rates. |

15

| BUSINESS SEGMENT HIGHLIGHTS | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Regional Banking | ||||||||||||||||||||||||||||

| Total revenues (a) | $ | 199,974 | $ | 210,298 | $ | 212,920 | $ | 207,636 | $ | 229,125 | (5 | )% | (13 | )% | ||||||||||||||

| Provision for loan losses | 105,825 | 58,201 | 89,477 | 75,264 | 15,831 | 82 | % | 568 | % | |||||||||||||||||||

| Noninterest expenses | 167,828 | 158,628 | 150,294 | 150,523 | 159,882 | 6 | % | 5 | % | |||||||||||||||||||

| Pre-tax income/(loss) | (73,679 | ) | (6,531 | ) | (26,851 | ) | (18,151 | ) | 53,412 | NM | (238 | )% | ||||||||||||||||

| Provision/(benefit) for income taxes | (27,511 | ) | (11,670 | ) | (19,838 | ) | (13,541 | ) | 27,026 | (136 | )% | (202 | )% | |||||||||||||||

| Net income/(loss) from continuing operations | (46,168 | ) | 5,139 | (7,013 | ) | (4,610 | ) | 26,386 | NM | (275 | )% | |||||||||||||||||

| Income from discontinued operations, net of tax | - | - | - | 883 | 4,137 | NM | NM | |||||||||||||||||||||

| Net income/(loss) | $ | (46,168 | ) | $ | 5,139 | $ | (7,013 | ) | $ | (3,727 | ) | $ | 30,523 | NM | (251 | )% | ||||||||||||

| National Specialty Lending | ||||||||||||||||||||||||||||

| Total revenues (a) | $ | 36,332 | $ | 49,424 | $ | 39,052 | $ | 55,040 | $ | 54,321 | (26 | )% | (33 | )% | ||||||||||||||

| Provision for loan losses | 144,049 | 240,470 | 108,000 | 149,483 | 139,398 | (40 | )% | 3 | % | |||||||||||||||||||

| Noninterest expenses | 21,873 | 23,487 | 26,675 | 25,146 | 31,067 | (7 | )% | (30 | )% | |||||||||||||||||||

| Pre-tax (loss) | (129,590 | ) | (214,533 | ) | (95,623 | ) | (119,589 | ) | (116,144 | ) | 40 | % | (12 | )% | ||||||||||||||

| Benefit for income taxes | (48,830 | ) | (79,488 | ) | (33,528 | ) | (46,359 | ) | (43,859 | ) | 39 | % | (11 | )% | ||||||||||||||

| Net (loss) | $ | (80,760 | ) | $ | (135,045 | ) | $ | (62,095 | ) | $ | (73,230 | ) | $ | (72,285 | ) | 40 | % | (12 | )% | |||||||||

| Mortgage Banking | ||||||||||||||||||||||||||||

| Total revenues (a) | $ | 96,967 | $ | 138,337 | $ | 222,297 | $ | 198,066 | $ | (79,826 | ) | (30 | )% | 221 | % | |||||||||||||

| Provision for loan losses | 22,018 | 2,878 | 4,001 | 222 | 46 | NM | NM | |||||||||||||||||||||

| Noninterest expenses | 39,503 | 89,040 | 149,062 | 147,543 | 174,203 | (56 | )% | (77 | )% | |||||||||||||||||||

| Pre-tax income/(loss) | 35,446 | 46,419 | 69,234 | 50,301 | (254,075 | ) | (24 | )% | 114 | % | ||||||||||||||||||

| Provision/(benefit) for income taxes | 12,941 | 16,645 | 22,960 | 18,129 | (99,185 | ) | (22 | )% | 113 | % | ||||||||||||||||||

| Net income/(loss) | $ | 22,505 | $ | 29,774 | $ | 46,274 | $ | 32,172 | $ | (154,890 | ) | (24 | )% | 115 | % | |||||||||||||

| Capital Markets | ||||||||||||||||||||||||||||

| Total revenues (a) | $ | 197,471 | $ | 117,527 | $ | 143,150 | $ | 153,579 | $ | 119,191 | 68 | % | 66 | % | ||||||||||||||

| Provision for loan losses | 8,108 | 38,451 | 18,522 | 15,031 | 1,244 | (79 | )% | 552 | % | |||||||||||||||||||

| Noninterest expenses | 114,955 | 87,674 | 100,559 | 115,728 | 87,042 | 31 | % | 32 | % | |||||||||||||||||||

| Pre-tax income/(loss) | 74,408 | (8,598 | ) | 24,069 | 22,820 | 30,905 | NM | 141 | % | |||||||||||||||||||

| Provision/(benefit) for income taxes | 27,910 | (3,375 | ) | 8,960 | 8,437 | 11,572 | NM | 141 | % | |||||||||||||||||||

| Net income/(loss) | $ | 46,498 | $ | (5,223 | ) | $ | 15,109 | $ | 14,383 | $ | 19,333 | NM | 141 | % | ||||||||||||||

| Corporate | ||||||||||||||||||||||||||||

| Total revenues (a) | $ | 12,222 | $ | 12,734 | $ | 20,522 | $ | 62,847 | $ | (3,837 | ) | (4 | )% | 419 | % | |||||||||||||

| Provision for loan losses | - | - | - | - | - | NM | NM | |||||||||||||||||||||

| Noninterest expenses | 5,499 | 43,445 | 39,253 | (663 | ) | 109,365 | (87 | )% | (95 | )% | ||||||||||||||||||

| Pre-tax income/(loss) | 6,723 | (30,711 | ) | (18,731 | ) | 63,510 | (113,202 | ) | 122 | % | 106 | % | ||||||||||||||||

| Provision/(benefit) for income taxes | 4,502 | (10,970 | ) | (7,375 | ) | 25,188 | (41,896 | ) | 141 | % | 111 | % | ||||||||||||||||

| Net income/(loss) | $ | 2,221 | $ | (19,741 | ) | $ | (11,356 | ) | $ | 38,322 | $ | (71,306 | ) | 111 | % | 103 | % | |||||||||||

| Total Consolidated | ||||||||||||||||||||||||||||

| Total revenues (a) | $ | 542,966 | $ | 528,320 | $ | 637,941 | $ | 677,168 | $ | 318,974 | 3 | % | 70 | % | ||||||||||||||

| Provision for loan losses | 280,000 | 340,000 | 220,000 | 240,000 | 156,519 | (18 | )% | 79 | % | |||||||||||||||||||

| Noninterest expenses | 349,658 | 402,274 | 465,843 | 438,277 | 561,559 | (13 | )% | (38 | )% | |||||||||||||||||||

| Pre-tax income/(loss) | (86,692 | ) | (213,954 | ) | (47,902 | ) | (1,109 | ) | (399,104 | ) | 59 | % | 78 | % | ||||||||||||||

| Benefit for income taxes | (30,988 | ) | (88,859 | ) | (28,821 | ) | (8,146 | ) | (146,342 | ) | 65 | % | 79 | % | ||||||||||||||

| Net income/(loss) from continuing operations | (55,704 | ) | (125,095 | ) | (19,081 | ) | 7,037 | (252,762 | ) | 55 | % | 78 | % | |||||||||||||||

| Income from discontinued operations, net of tax | - | - | - | 883 | 4,137 | NM | NM | |||||||||||||||||||||

| Net income/(loss) | $ | (55,704 | ) | $ | (125,095 | ) | $ | (19,081 | ) | $ | 7,920 | $ | (248,625 | ) | 55 | % | 78 | % | ||||||||||

| NM - Not meaningful | |

| Certain previously reported amounts have been reclassified to agree with current presentation. | |

| (a) | Includes noninterest income and net interest income/(expense). |

16

| REGIONAL BANKING | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Income Statement | ||||||||||||||||||||||||||||

| Net interest income | $ | 117,356 | $ | 122,379 | $ | 120,384 | $ | 120,565 | $ | 133,613 | (4 | )% | (12 | )% | ||||||||||||||

| Noninterest income | 82,618 | 87,919 | 92,536 | 87,071 | 95,511 | (6 | )% | (13 | )% | |||||||||||||||||||

| Securities gains/(losses), net | - | - | - | - | 1 | NM | NM | |||||||||||||||||||||

| Total revenue | 199,974 | 210,298 | 212,920 | 207,636 | 229,125 | (5 | )% | (13 | )% | |||||||||||||||||||

| Total noninterest expense | 167,828 | 158,628 | 150,294 | 150,523 | 159,882 | 6 | % | 5 | % | |||||||||||||||||||

| Provision | 105,825 | 58,201 | 89,477 | 75,264 | 15,831 | 82 | % | 568 | % | |||||||||||||||||||

| Pretax income/(loss) | $ | (73,679 | ) | $ | (6,531 | ) | $ | (26,851 | ) | $ | (18,151 | ) | $ | 53,412 | NM | NM | ||||||||||||

| Efficiency ratio | 83.92 | % | 75.43 | % | 70.59 | % | 72.49 | % | 69.78 | % | ||||||||||||||||||

| Balance Sheet (millions) | ||||||||||||||||||||||||||||

| Average loans | $ | 10,898 | $ | 10,915 | $ | 10,801 | $ | 10,705 | $ | 10,667 | * | 2 | % | |||||||||||||||

| Other earning assets | 163 | 65 | 242 | 339 | 525 | 151 | % | (69 | )% | |||||||||||||||||||

| Total earning assets | 11,061 | 10,980 | 11,043 | 11,044 | 11,192 | 1 | % | (1 | )% | |||||||||||||||||||

| Core deposits | 9,753 | 9,564 | 9,970 | 10,059 | 9,854 | 2 | % | (1 | )% | |||||||||||||||||||

| Other deposits | 978 | 976 | 1,053 | 1,160 | 1,369 | * | (29 | )% | ||||||||||||||||||||

| Deposits - divestiture | - | - | 37 | 153 | 378 | NM | (100 | )% | ||||||||||||||||||||

| Total deposits | 10,731 | 10,540 | 11,060 | 11,372 | 11,601 | 2 | % | (7 | )% | |||||||||||||||||||

| Total period end deposits | 10,993 | 10,621 | 11,035 | 11,370 | 11,679 | 4 | % | (6 | )% | |||||||||||||||||||

| Total period end assets | $ | 11,999 | $ | 12,301 | $ | 12,234 | $ | 12,172 | $ | 12,674 | (2 | )% | (5 | )% | ||||||||||||||

| Net interest margin | 4.22 | % | 4.43 | % | 4.38 | % | 4.39 | % | 4.74 | % | ||||||||||||||||||

| Noninterest Income Detail | ||||||||||||||||||||||||||||

| Deposit transactions & cash mgmt | $ | 42,388 | $ | 44,470 | $ | 45,404 | $ | 41,230 | $ | 46,648 | (5 | )% | (9 | )% | ||||||||||||||

| Insurance commissions | 7,027 | 7,160 | 7,033 | 7,854 | 7,485 | (2 | )% | (6 | )% | |||||||||||||||||||

| Trust services & investment mgmt | 7,697 | 8,192 | 8,915 | 9,147 | 10,137 | (6 | )% | (24 | )% | |||||||||||||||||||

| Bankcard Income | 4,416 | 4,706 | 4,752 | 4,491 | 5,035 | (6 | )% | (12 | )% | |||||||||||||||||||

| Other service charges | 3,500 | 3,556 | 3,780 | 4,037 | 4,152 | (2 | )% | (16 | )% | |||||||||||||||||||

| Miscellaneous revenue | 17,590 | 19,835 | 22,652 | 20,312 | 22,054 | (11 | )% | (20 | )% | |||||||||||||||||||

| Total noninterest income | $ | 82,618 | $ | 87,919 | $ | 92,536 | $ | 87,071 | $ | 95,511 | (6 | )% | (13 | )% | ||||||||||||||

| Key Statistics | ||||||||||||||||||||||||||||

| Locations | ||||||||||||||||||||||||||||

| Financial Centers | 202 | 200 | 198 | 206 | 216 | 1 | % | (6 | )% | |||||||||||||||||||

| First Tennessee | 202 | 200 | 198 | 197 | 197 | 1 | % | 3 | % | |||||||||||||||||||

| First Horizon Bank | - | - | - | 9 | 19 | NM | (100 | )% | ||||||||||||||||||||

| Trust Assets | ||||||||||||||||||||||||||||

| Total assets (millions) | $ | 9,606 | $ | 11,015 | $ | 11,291 | $ | 11,681 | $ | 12,300 | (13 | )% | (22 | )% | ||||||||||||||

| Total managed assets (millions) | 4,664 | 5,089 | 5,373 | 5,641 | 5,880 | (8 | )% | (21 | )% | |||||||||||||||||||

| NM - Not meaningful |

| * Amount is less than one percent. |

| Certain previously reported amounts have been reclassified to agree with current presentation. |

17

| CAPITAL MARKETS | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Income Statement | ||||||||||||||||||||||||||||

| Net interest income | ||||||||||||||||||||||||||||

| Correspondent Banking | $ | 12,337 | $ | 11,841 | $ | 12,399 | $ | 12,808 | $ | 11,437 | 4 | % | 8 | % | ||||||||||||||

| Capital Markets | 7,829 | 7,151 | 6,094 | 6,841 | 4,389 | 9 | % | 78 | % | |||||||||||||||||||

| Total net interest income | 20,166 | 18,992 | 18,493 | 19,649 | 15,826 | 6 | % | 27 | % | |||||||||||||||||||

| Noninterest income: | ||||||||||||||||||||||||||||

| Fixed income | 156,522 | 80,104 | 105,002 | 152,208 | 77,126 | 95 | % | 103 | % | |||||||||||||||||||

| Other | 20,783 | 18,431 | 19,655 | (18,278 | ) | 26,239 | 13 | % | (21 | )% | ||||||||||||||||||

| Total noninterest income | 177,305 | 98,535 | 124,657 | 133,930 | 103,365 | 80 | % | 72 | % | |||||||||||||||||||

| Total revenue | 197,471 | 117,527 | 143,150 | 153,579 | 119,191 | 68 | % | 66 | % | |||||||||||||||||||

| Noninterest expense | 114,955 | 87,674 | 100,559 | 115,728 | 87,042 | 31 | % | 32 | % | |||||||||||||||||||

| Provision | 8,108 | 38,451 | 18,522 | 15,031 | 1,244 | (79 | )% | 552 | % | |||||||||||||||||||

| Pretax income/(loss) | $ | 74,408 | $ | (8,598 | ) | $ | 24,069 | $ | 22,820 | $ | 30,905 | NM | 141 | % | ||||||||||||||

| Efficiency ratio | 58.21 | % | 74.60 | % | 70.25 | % | 75.35 | % | 73.03 | % | ||||||||||||||||||

| Balance Sheet (millions) | ||||||||||||||||||||||||||||

| Trading inventory | $ | 1,135 | $ | 1,356 | $ | 1,631 | $ | 1,962 | $ | 1,934 | (16 | )% | (41 | )% | ||||||||||||||

| Average Loans (a) | 1,719 | 1,759 | 1,491 | 1,465 | 1,402 | (2 | )% | 23 | % | |||||||||||||||||||

| Other earning assets | 981 | 1,275 | 1,656 | 1,728 | 1,708 | (23 | )% | (43 | )% | |||||||||||||||||||

| Total earning assets | 3,835 | 4,390 | 4,778 | 5,155 | 5,044 | (13 | )% | (24 | )% | |||||||||||||||||||

| Total period end assets | $ | 5,055 | $ | 5,968 | $ | 5,602 | $ | 6,154 | $ | 5,265 | (15 | )% | (4 | )% | ||||||||||||||

| Net interest margin: | ||||||||||||||||||||||||||||

| Correspondent Banking | 3.46 | % | 2.97 | % | 3.06 | % | 3.28 | % | 3.01 | % | ||||||||||||||||||

| Capital Markets | 1.29 | % | 1.01 | % | .78 | % | .77 | % | .49 | % | ||||||||||||||||||

| Total Capital Markets | 2.09 | % | 1.72 | % | 1.56 | % | 1.53 | % | 1.24 | % | ||||||||||||||||||

| NM - Not meaningful |

| * Amount is less than one percent. |

| Certain previously reported amounts have been reclassified to agree with current presentation. |

| (a) Includes trust preferred warehouse loans moved from loans held for sale to loans held to maturity in 2Q08. |

18

| NATIONAL SPECIALTY LENDING | ||||||||||||||||||||||||||||

| Quarterly, Unaudited | ||||||||||||||||||||||||||||

| 4Q08 Change vs. | ||||||||||||||||||||||||||||

| (Thousands) | 4Q08 | 3Q08 | 2Q08 | 1Q08 | 4Q07 | 3Q08 | 4Q07 | |||||||||||||||||||||

| Income Statement | ||||||||||||||||||||||||||||

| Net interest income | $ | 36,841 | $ | 45,243 | $ | 53,555 | $ | 54,389 | $ | 58,698 | (19 | )% | (37 | )% | ||||||||||||||

| Noninterest income | (509 | ) | 4,181 | (14,503 | ) | 651 | (4,377 | ) | (112 | )% | 88 | % | ||||||||||||||||

| Total revenue | 36,332 | 49,424 | 39,052 | 55,040 | 54,321 | (26 | )% | (33 | )% | |||||||||||||||||||

| Total noninterest expense | 21,873 | 23,487 | 26,675 | 25,146 | 31,067 | (7 | )% | (30 | )% | |||||||||||||||||||

| Provision | 144,049 | 240,470 | 108,000 | 149,483 | 139,398 | (40 | )% | 3 | % | |||||||||||||||||||

| Pretax (loss) | $ | (129,590 | ) | $ | (214,533 | ) | $ | (95,623 | ) | $ | (119,589 | ) | $ | (116,144 | ) | 40 | % | (12 | )% | |||||||||