Exhibit 99.1

FMC Corporation

West Coast Marketing Trip

March 23rd – 25th, 2004

William G. Walter Chairman, President and CEO

Disclaimer

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995

These slides and the accompanying presentation contain “forward-looking statements” that represent management’s best judgment as of the date hereof based on information currently available. Actual results of the Company may differ materially from those contained in the forward-looking statements.

Additional information concerning factors that may cause results to differ materially from those in the forward-looking statements is contained in the Company’s periodic reports filed under the Securities Exchange Act of 1934, as amended.

The Company undertakes no obligation to update or revise these forward-looking statements to reflect new events or uncertainties.

1

Use of Non-GAAP Terms

These slides contain certain “non-GAAP financial terms” which are defined below and on FMC’s Investor Relations web site (http://ir.fmc.com) in the Glossary of Financial Terms section. In addition, in the Conference Calls and Presentations section of the web site, we have provided reconciliations of non-GAAP terms to the closest GAAP term. Lastly, these slides contain references to segment financial items which are presented in detail in Note 19 of FMC’s 2003 Form 10-K.

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) is the sum of Income (loss) from continuing operations before income taxes and cumulative effect of change in accounting principle and Depreciation and Amortization.

EBITDA Margin is the quotient of EBITDA (defined above) and Revenue.

ROIC (Return on Invested Capital) is the sum of Earnings from continuing operations before restructuring and other charges (gains) and after-tax Interest expense divided by the sum of Short-term debt, Current portion of long-term debt, Long-term debt and Total shareholders’ equity.

2

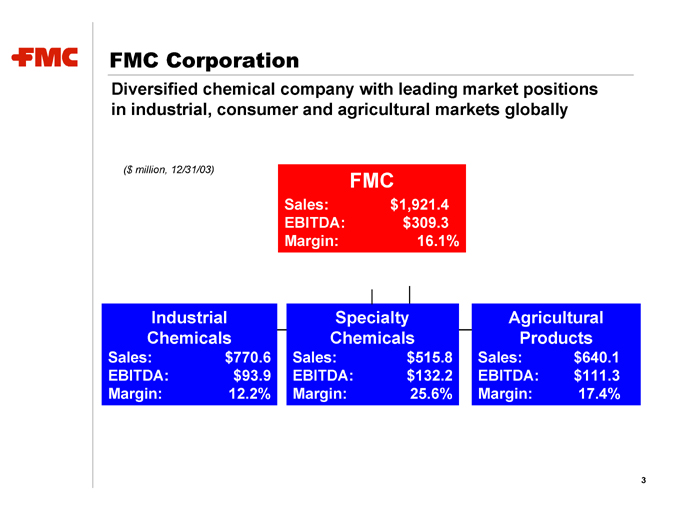

FMC Corporation

Diversified chemical company with leading market positions in industrial, consumer and agricultural markets globally

($ million, 12/31/03)

FMC

Sales: $1,921.4

EBITDA: $ 309.3

Margin: 16.1%

Industrial Specialty Agricultural

Chemicals Chemicals Products

Sales: $770.6 Sales: $515.8 Sales: $640.1

EBITDA: $93.9 EBITDA: $132.2 EBITDA: $111.3

Margin: 12.2% Margin: 25.6% Margin: 17.4%

3

FMC Strengths

Leading market positions

Global presence

Diversified business mix and high-quality customer base

Diversified and integrated cost structure

Focused R&D and strong applications expertise

Proven management with extensive industry experience

4

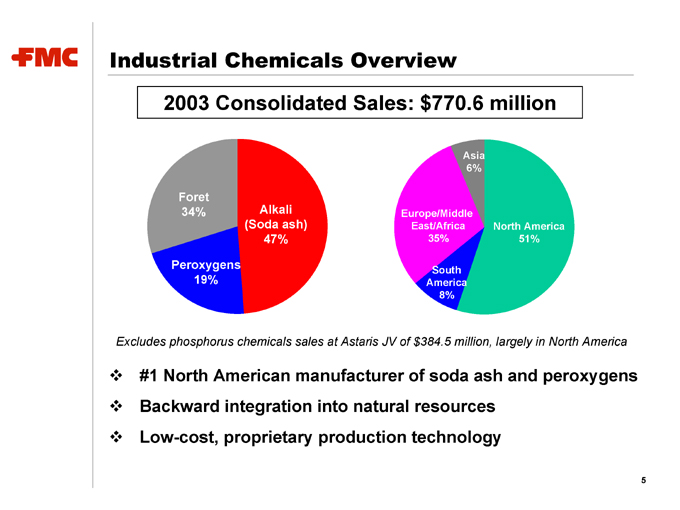

Industrial Chemicals Overview

2003 Consolidated Sales: $770.6 million

Alkali (Soda ash) 47%

Peroxygens 19%

Foret 34%

North America 51%

South America 8%

Europe/Middle East/Africa 35%

Asia 6%

Excludes phosphorus chemicals sales at Astaris JV of $384.5 million, largely in North America

#1 North American manufacturer of soda ash and peroxygens

Backward integration into natural resources

Low-cost, proprietary production technology

5

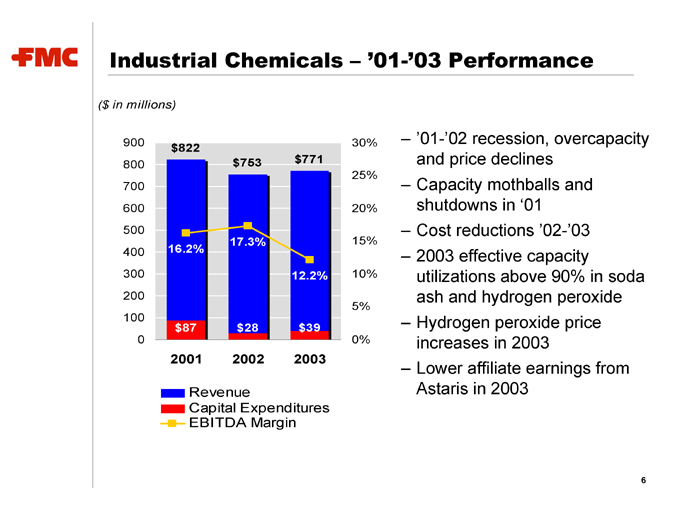

Industrial Chemicals – ‘01-’03 Performance

($ in millions)

$822 16.2% $87 2001

$753 17.3% $28 2002

$771 12.2% $39 2003

Revenue

Capital Expenditures

EBITDA Margin

– ‘01-’02 recession, overcapacity and price declines

– Capacity mothballs and shutdowns in ‘01

– Cost reductions ‘02-’03

– 2003 effective capacity utilizations above 90% in soda ash and hydrogen peroxide

– Hydrogen peroxide price increases in 2003

– Lower affiliate earnings from Astaris in 2003

6

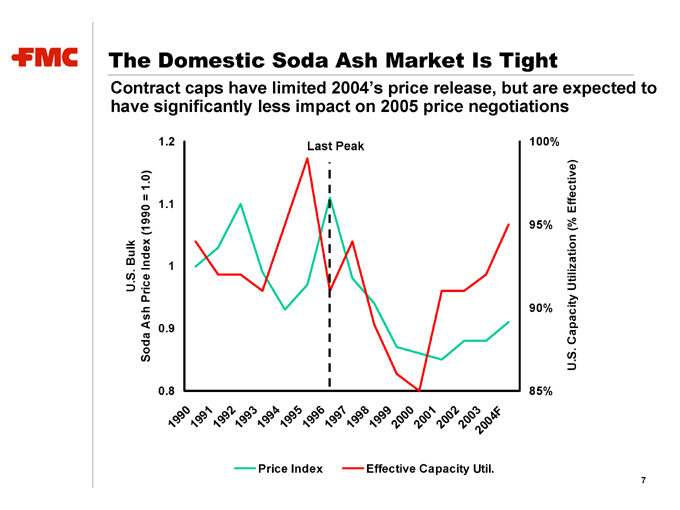

The Domestic Soda Ash Market Is Tight

Contract caps have limited 2004’s price release, but are expected to have significantly less impact on 2005 price negotiations

Last Peak

Price Index

Effective Capacity Util.

7

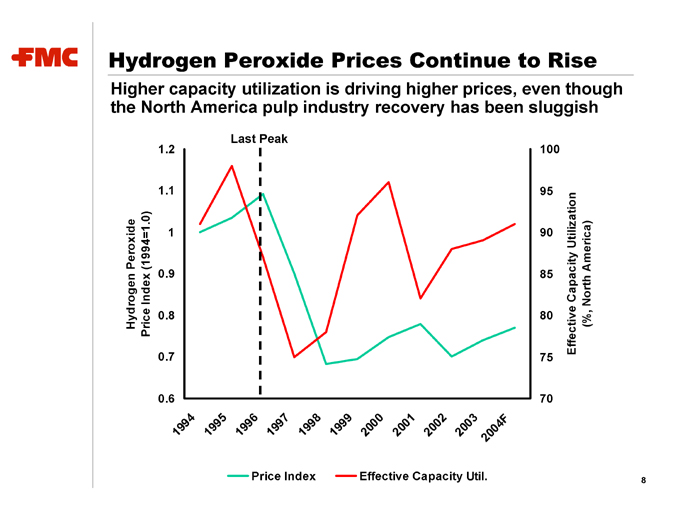

Hydrogen Peroxide Prices Continue to Rise

Higher capacity utilization is driving higher prices, even though the North America pulp industry recovery has been sluggish

Last Peak

Price Index

Effective Capacity Util.

8

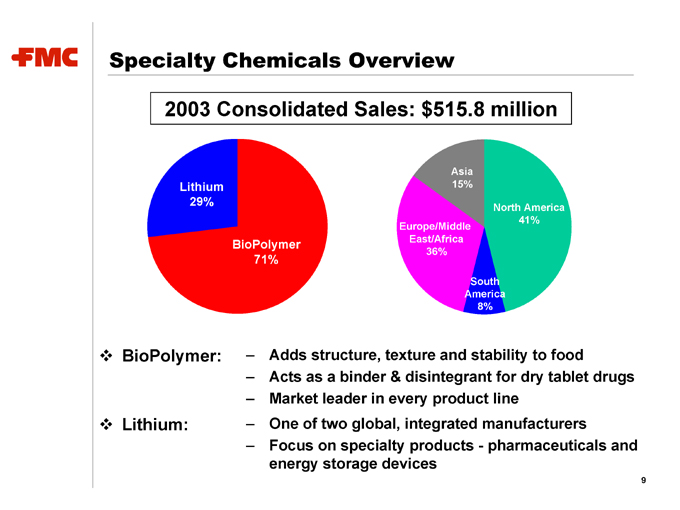

Specialty Chemicals Overview

2003 Consolidated Sales: $515.8 million

BioPolymer 71%

Lithium 29%

North America 41%

South America 8%

Europe/Middle East/Africa 36%

Asia 15%

BioPolymer: – Adds structure, texture and stability to food

– Acts as a binder & disintegrant for dry tablet drugs

– Market leader in every product line

Lithium: – One of two global, integrated manufacturers

– Focus on specialty products—pharmaceuticals and energy storage devices

9

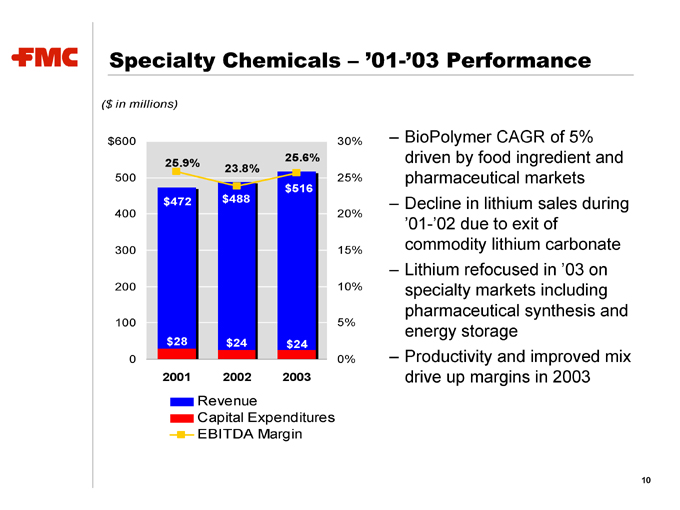

Specialty Chemicals – ‘01-’03 Performance

($ in millions)

25.9% $472 $28 2001

23.8% $488 $24 2002

25.6% $516 $24 2003

Revenue

Capital Expenditures

EBITDA Margin

– BioPolymer CAGR of 5% driven by food ingredient and pharmaceutical markets

– Decline in lithium sales during ‘01-’02 due to exit of commodity lithium carbonate

– Lithium refocused in ‘03 on specialty markets including pharmaceutical synthesis and energy storage

– Productivity and improved mix drive up margins in 2003

10

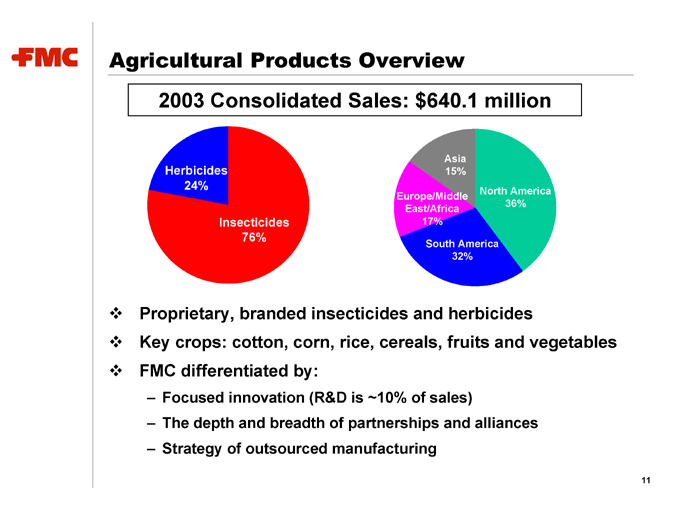

Agricultural Products Overview

2003 Consolidated Sales: $640.1 million

Insecticides 76%

Herbicides 24%

North America 36%

South America 32%

Europe/Middle East/Africa 17%

Asia 15%

Proprietary, branded insecticides and herbicides

Key crops: cotton, corn, rice, cereals, fruits and vegetables

FMC differentiated by:

– Focused innovation (R&D is ~10% of sales)

– The depth and breadth of partnerships and alliances

– Strategy of outsourced manufacturing

11

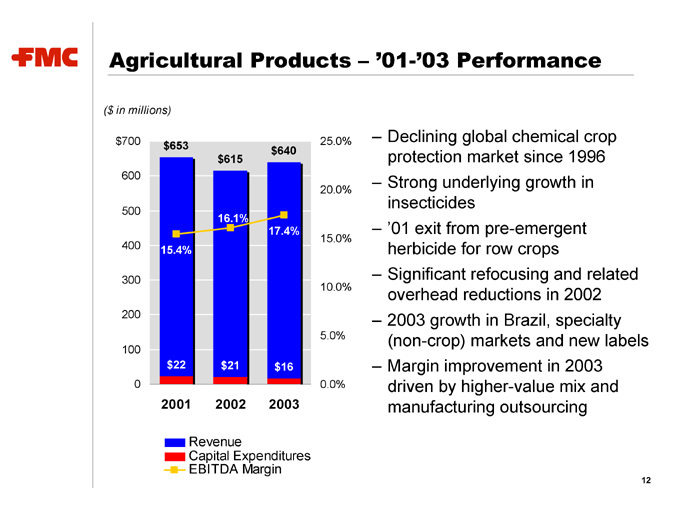

Agricultural Products – ‘01-’03 Performance

($ in millions)

$653 15.4% $22 2001

$615 16.1% $21 2002

$640 17.4% $16 2003

Revenue

Capital Expenditures

EBITDA Margin

– Declining global chemical crop protection market since 1996

– Strong underlying growth in insecticides

– ‘01 exit from pre-emergent herbicide for row crops

– Significant refocusing and related overhead reductions in 2002

– 2003 growth in Brazil, specialty (non-crop) markets and new labels

– Margin improvement in 2003 driven by higher-value mix and manufacturing outsourcing

12

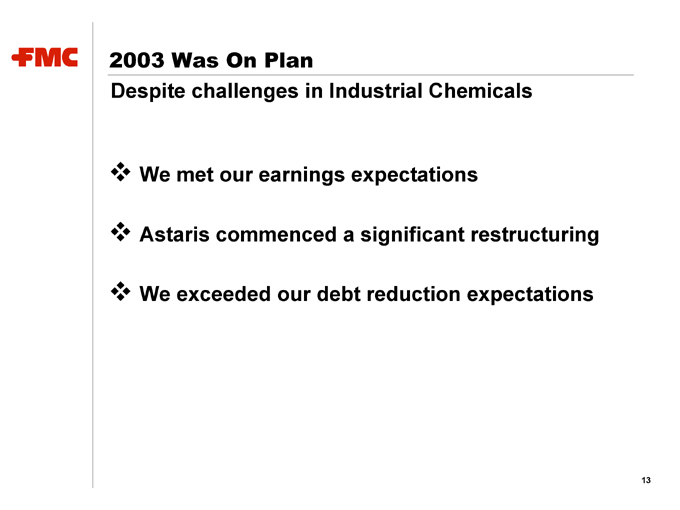

2003 Was On Plan

Despite challenges in Industrial Chemicals

We met our earnings expectations

Astaris commenced a significant restructuring

We exceeded our debt reduction expectations

13

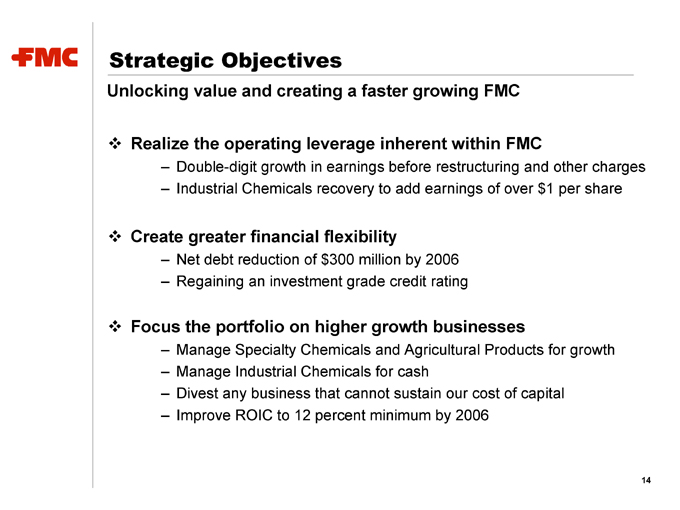

Strategic Objectives

Unlocking value and creating a faster growing FMC

Realize the operating leverage inherent within FMC

– Double-digit growth in earnings before restructuring and other charges

– Industrial Chemicals recovery to add earnings of over $1 per share

Create greater financial flexibility

– Net debt reduction of $300 million by 2006

– Regaining an investment grade credit rating

Focus the portfolio on higher growth businesses

– Manage Specialty Chemicals and Agricultural Products for growth

– Manage Industrial Chemicals for cash

– Divest any business that cannot sustain our cost of capital

– Improve ROIC to 12 percent minimum by 2006

14

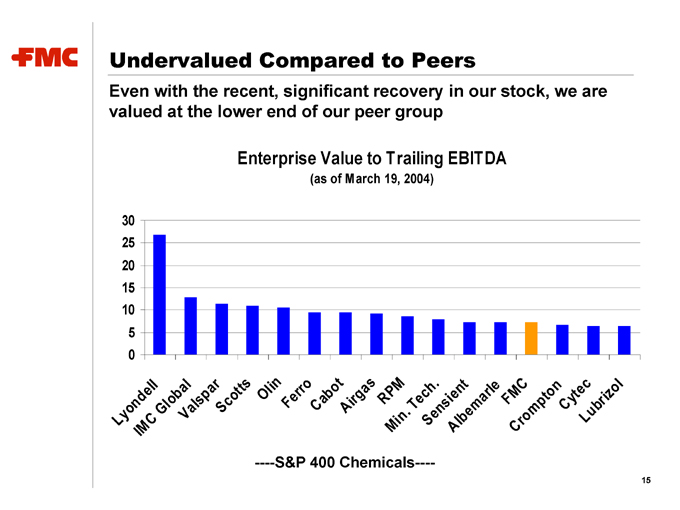

Undervalued Compared to Peers

Even with the recent, significant recovery in our stock, we are valued at the lower end of our peer group

Enterprise Value to Trailing EBITDA

(as of March 19, 2004)

——S&P 400 Chemicals——

15

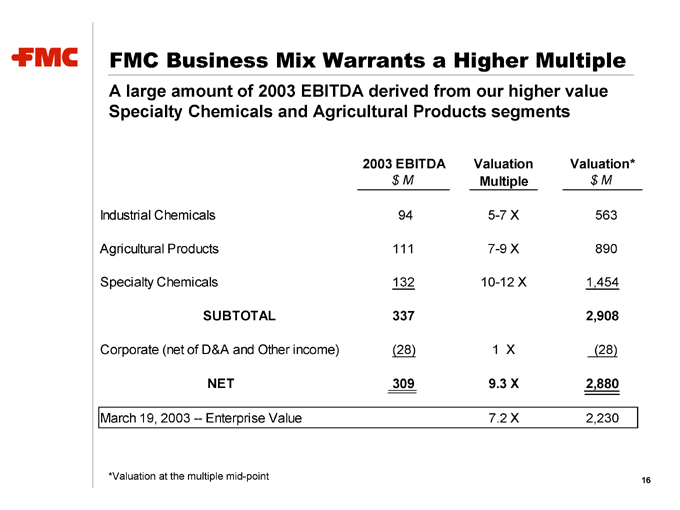

FMC Business Mix Warrants a Higher Multiple

A large amount of 2003 EBITDA derived from our higher value Specialty Chemicals and Agricultural Products segments

2003 EBITDA Valuation Valuation*

$ M Multiple $ M

Industrial Chemicals 94 5-7 X 563

Agricultural Products 111 7-9 X 890

Specialty Chemicals 132 10-12 X 1,454

SUBTOTAL 337 2,908

Corporate (net of D&A and Other income) (28) 1 X (28)

NET 309 9.3 X 2,880

March 19, 2003 — Enterprise Value 7.2 X 2,230

*Valuation at the multiple mid-point

16

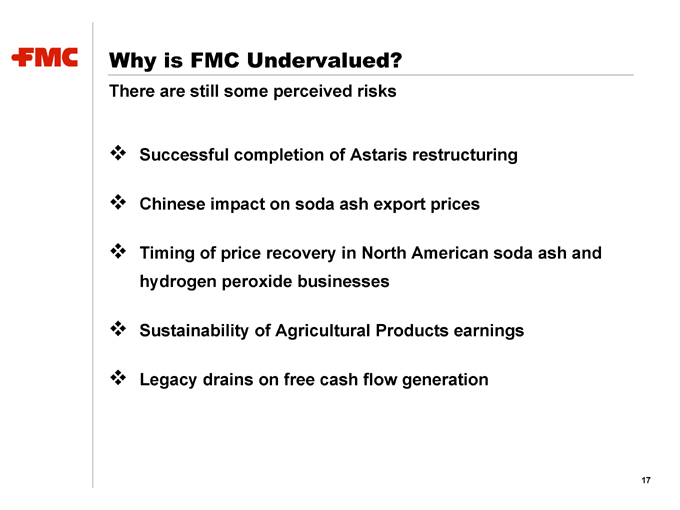

Why is FMC Undervalued?

There are still some perceived risks

Successful completion of Astaris restructuring

Chinese impact on soda ash export prices

Timing of price recovery in North American soda ash and hydrogen peroxide businesses

Sustainability of Agricultural Products earnings

Legacy drains on free cash flow generation

17

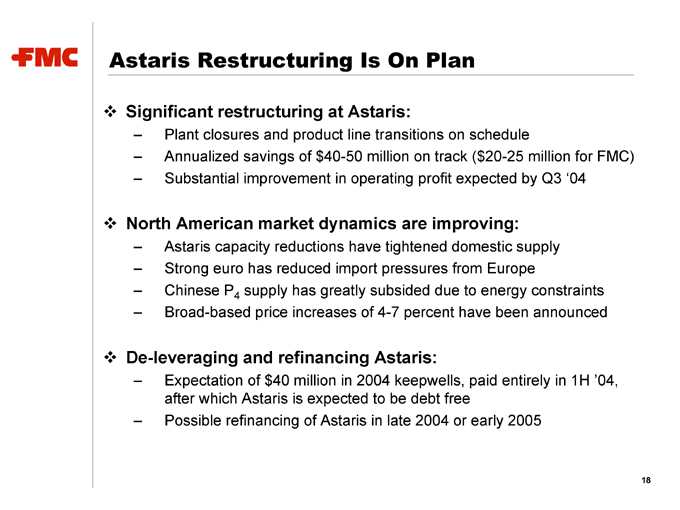

Astaris Restructuring Is On Plan

Significant restructuring at Astaris:

– Plant closures and product line transitions on schedule

– Annualized savings of $40-50 million on track ($20-25 million for FMC)

– Substantial improvement in operating profit expected by Q3 ‘04

North American market dynamics are improving:

– Astaris capacity reductions have tightened domestic supply

– Strong euro has reduced import pressures from Europe

– Chinese P4 supply has greatly subsided due to energy constraints

– Broad-based price increases of 4-7 percent have been announced

De-leveraging and refinancing Astaris:

– Expectation of $40 million in 2004 keepwells, paid entirely in 1H ‘04, after which Astaris is expected to be debt free

– Possible refinancing of Astaris in late 2004 or early 2005

18

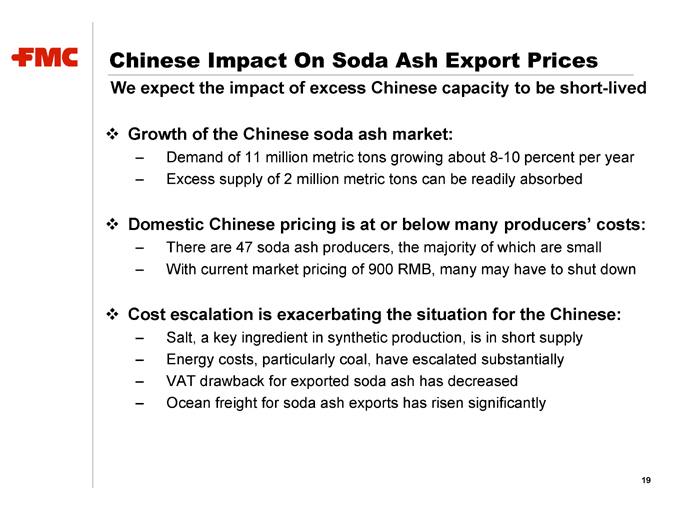

Chinese Impact On Soda Ash Export Prices

We expect the impact of excess Chinese capacity to be short-lived

Growth of the Chinese soda ash market:

– Demand of 11 million metric tons growing about 8-10 percent per year

– Excess supply of 2 million metric tons can be readily absorbed

Domestic Chinese pricing is at or below many producers’ costs:

– There are 47 soda ash producers, the majority of which are small

– With current market pricing of 900 RMB, many may have to shut down

Cost escalation is exacerbating the situation for the Chinese:

– Salt, a key ingredient in synthetic production, is in short supply

– Energy costs, particularly coal, have escalated substantially

– VAT drawback for exported soda ash has decreased

– Ocean freight for soda ash exports has risen significantly

19

Sustainability of Agricultural Products Earnings

Improving global farm economy:

– Rising global crop prices

– Improving U.S. farm income

– Increasing global competitiveness of Brazilian farmers

Significant cost savings from productivity initiatives:

– Manufacturing outsourcing strategies continue to produce savings

– Global supply chain redesign under evaluation

– Network of global partnerships provides low-cost marketing scale

Focused, successful innovation:

– Label expansions in both crop and specialty markets

– Novel ISK chemistry targeting sucking pests to launch 2005

– Discovery efforts have resulted in many promising chemistries, several of which are now entering global field trials

20

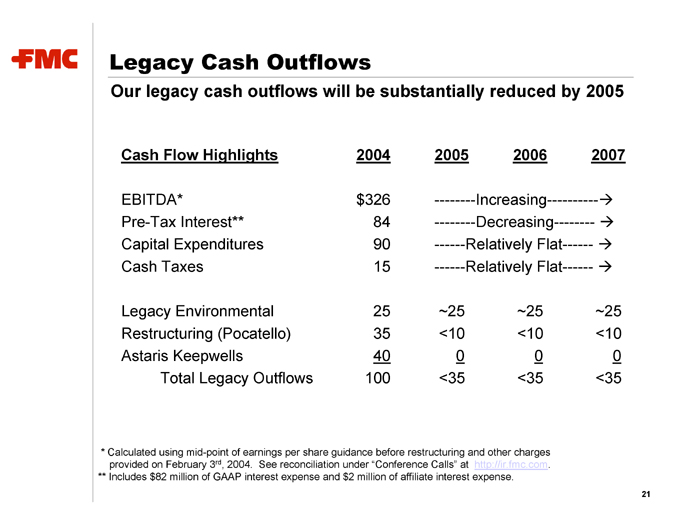

Legacy Cash Outflows

Our legacy cash outflows will be substantially reduced by 2005

Cash Flow Highlights 2004 2005 2006 2007

EBITDA* $ 326 --------Increasing----------Æ

Pre-Tax Interest** 84 - --------Decreasing-------- A

Capital Expenditures 90 ------Relatively Flat------ A

Cash Taxes 15 ------Relatively Flat------ A

Legacy Environmental 25 ~25 ~25 ~25

Restructuring (Pocatello) 35 <10 <10 <10

Astaris Keepwells 40 0 0 0

Total Legacy Outflows 100 <35 <35 <35

* Calculated using mid-point of earnings per share guidance before restructuring and other charges provided on February 3rd, 2004. See reconciliation under “Conference Calls” at http://ir.fmc.com. ** Includes $82 million of GAAP interest expense and $2 million of affiliate interest expense.

21

FMC Corporation