Exhibit 99.1

Exhibit 99.1

FMC Corporation

Boston Road Trip

September 9, 2004

William G. Walter Chairman, President and CEO

Disclaimer

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995

These slides and the accompanying presentation contain “forward-looking statements” that represent management’s best judgment as of the date hereof based on information currently available. Actual results of the Company may differ materially from those contained in the forward-looking statements.

Additional information concerning factors that may cause results to differ materially from those in the forward-looking statements is contained in the Company’s periodic reports filed under the Securities Exchange Act of 1934, as amended.

The Company undertakes no obligation to update or revise these forward-looking statements to reflect new events or uncertainties.

Use of Non-GAAP Terms

These slides contain certain “non-GAAP financial terms” which are defined below and on FMC’s Investor Relations web site (http://ir.fmc.com) in the Glossary of Financial Terms section. In addition, in the Conference Calls and Presentations section of the web site, we have provided reconciliations of non-GAAP terms to the closest GAAP term. Lastly, these slides contain references to segment financial items which are presented in detail in Note 19 of FMC’s 2003 Form 10-K.

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) is the sum of Income (loss) from continuing operations before income taxes and cumulative effect of change in accounting principle and Depreciation and Amortization.

EBITDA Margin is the quotient of EBITDA (defined above) and Revenue.

ROIC (Return on Invested Capital) is the sum of Earnings from continuing operations before restructuring and other charges (gains) and after-tax Interest expense divided by the sum of Short-term debt, Current portion of long-term debt, Long-term debt and Total shareholders’ equity.

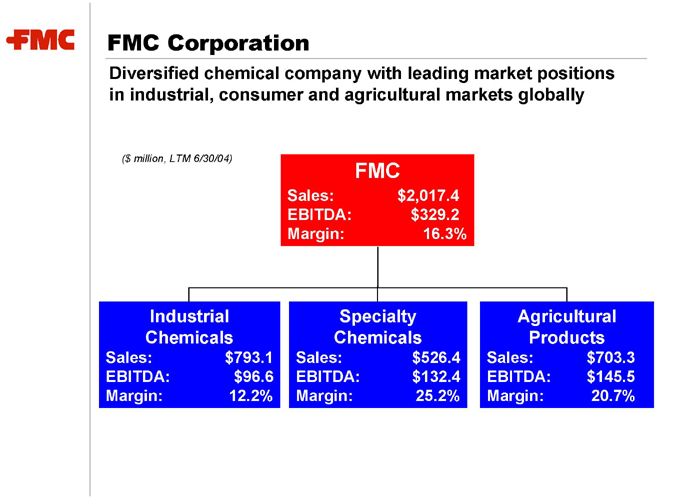

FMC Corporation

Diversified chemical company with leading market positions in industrial, consumer and agricultural markets globally

($ million, LTM 6/30/04)

FMC

Sales: $2,017.4 EBITDA: $329.2 Margin: 16.3%

Industrial Chemicals

Sales: $793.1 EBITDA: $96.6 Margin: 12.2%

Specialty Chemicals

Sales: $526.4 EBITDA: $132.4 Margin: 25.2%

Agricultural Products

Sales: $703.3 EBITDA: $145.5 Margin: 20.7%

FMC Strengths

Leading market positions

Global presence

Diversified business mix and high-quality customer base Diversified and integrated cost structure Focused R&D and strong applications expertise Proven management with extensive industry experience

Industrial Chemicals Overview

2003 Consolidated Sales: $770.6 million

Foret 34%

Alkali (Soda ash) 47%

Peroxygens 19%

Asia 6%

Europe/Middle East/Africa 35%

North America 51%

South America 8%

Excludes phosphorus chemicals sales at Astaris JV of $384.5 million, largely in North America

#1 North American manufacturer of soda ash and peroxygens Backward integration into natural resources Low-cost, proprietary production technology

Industrial Chemicals Financial Performance

Millions $250 $200 $150 $100 $50 $0 $208 $194 $177

$133 $130

$94

25% 20% 15% 10% 5% 0%

Margin

19998 1999 2000 2001 2002 2003 2004

EBITDA Capital Spending EBITDA Margin (%)

Industry over-expansion during the late 1990’s

Declining demand, price erosion and capacity reductions 2000-2002 2003 price improvement in peroxygens offset by continued erosion in phosphorus chemicals

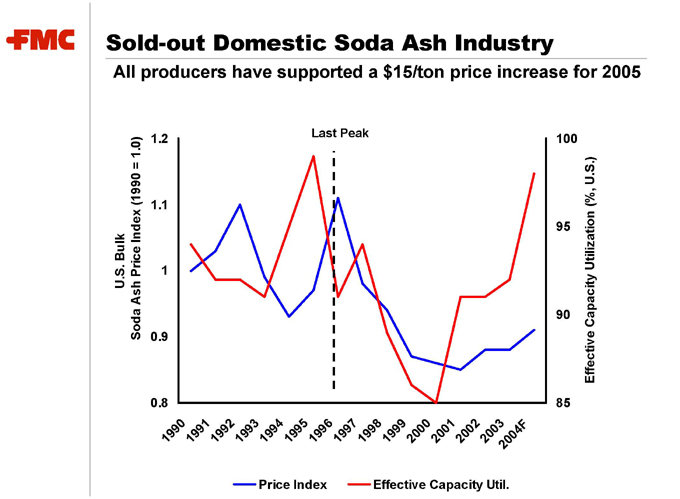

Sold-out Domestic Soda Ash Industry

All producers have supported a $15/ton price increase for 2005

U.S. Bulk

Soda Ash Price Index (1990 = 1.0)

1.2 1.1 1 0.9 0.8

Last Peak

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004F

85 90 95 100

Effective Capacity Utilization (%, U.S.)

Price Index Effective Capacity Util.

Improving Soda Ash Export Market

Chinese have curbed expansions and begun to increase prices

Growth of the Chinese soda ash market

Demand of 11 million metric tons growing about 8-10 percent per year

Excess supply of 2 million metric tons is being readily absorbed

Domestic Chinese pricing is at or below many producers’ costs

There are 47 soda ash producers, the majority of which are small

With market pricing near the cost of less efficient producers, some have shut down; others have postponed capacity increases

Higher costs are limiting Chinese soda ash production

Salt, a key ingredient in synthetic production, is in short supply

Energy costs, particularly coke, have escalated substantially

The VAT drawback for exported soda ash has decreased

Ocean freight for soda ash exports has risen significantly

Chinese exporters recently raised price by $10/metric ton

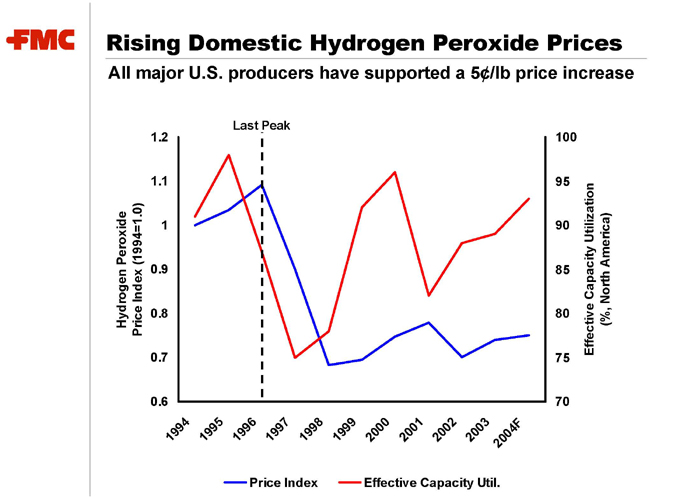

Rising Domestic Hydrogen Peroxide Prices

All major U.S. producers have supported a 5¢/lb price increase

Hydrogen Peroxide Price Index (1994=1.0)

1.2 1.1 1 0.9 0.8 0.7 0.6

Last Peak

100 95 90 85 80 75 70

Effective Capacity Utilization (%, North America)

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004F

Price Index Effective Capacity Util.

Industrial Chemicals Improvement in Europe

Steady recovery across nearly all of Foret’s product lines

After a strong 2003, peroxygens expected to continue to grow

Hydrogen peroxide demand growth of 4% per year driven by strength of Scandinavian pulp industry

Peroxide price increase of 8% in 2003; another 5% expected during 2004

Phosphorus chemicals in a slow recovery driven by capacity reduction

Rhodia’s shutdown of Rouen STPP facility has improved industry capacity utilization

Foret has recovered STPP volume that was lost in 2002

Price recovery is beginning

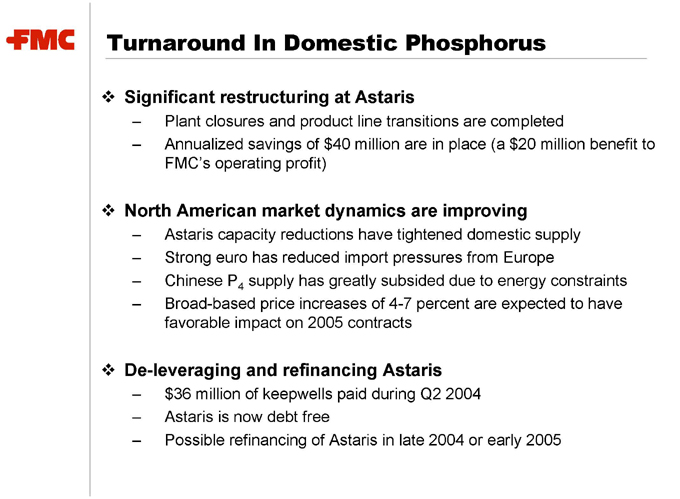

Turnaround In Domestic Phosphorus

Significant restructuring at Astaris

Plant closures and product line transitions are completed

Annualized savings of $40 million are in place (a $20 million benefit to FMC’s operating profit)

North American market dynamics are improving

Astaris capacity reductions have tightened domestic supply

Strong euro has reduced import pressures from Europe

Chinese P4 supply has greatly subsided due to energy constraints

Broad-based price increases of 4-7 percent are expected to have favorable impact on 2005 contracts

De-leveraging and refinancing Astaris

$36 million of keepwells paid during Q2 2004

Astaris is now debt free

Possible refinancing of Astaris in late 2004 or early 2005

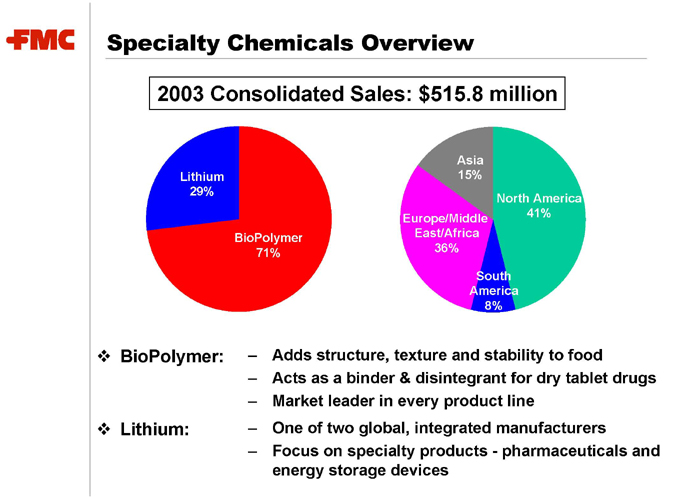

Specialty Chemicals Overview

2003 Consolidated Sales: $515.8 million

Lithium 29%

BioPolymer 71%

Asia 15%

North America 41%

Europe/Middle East/Africa 36%

South America 8%

BioPolymer:Adds structure, texture and stability to food

Acts as a binder & disintegrant for dry tablet drugs

Market leader in every product line

Lithium: One of two global, integrated manufacturers

Focus on specialty products—pharmaceuticals and energy storage devices

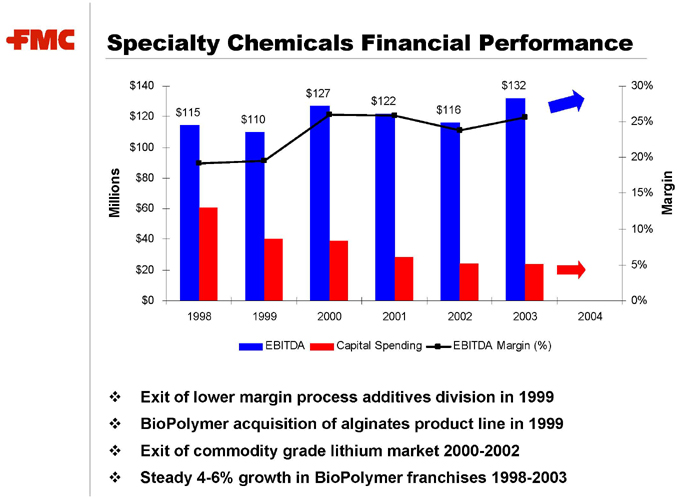

Specialty Chemicals Financial Performance

Millions $140

$120

$100 $80 $60 $40

$20

$0 $132 $127 $122 $115 $116 $110

30% 25% 20% 15% 10% 5% 0%

Margin

1998 1999 2000 2001 2002 2003 2004

EBITDA Capital Spending EBITDA Margin (%)

Exit of lower margin process additives division in 1999 BioPolymer acquisition of alginates product line in 1999 Exit of commodity grade lithium market 2000-2002 Steady 4-6% growth in BioPolymer franchises 1998-2003

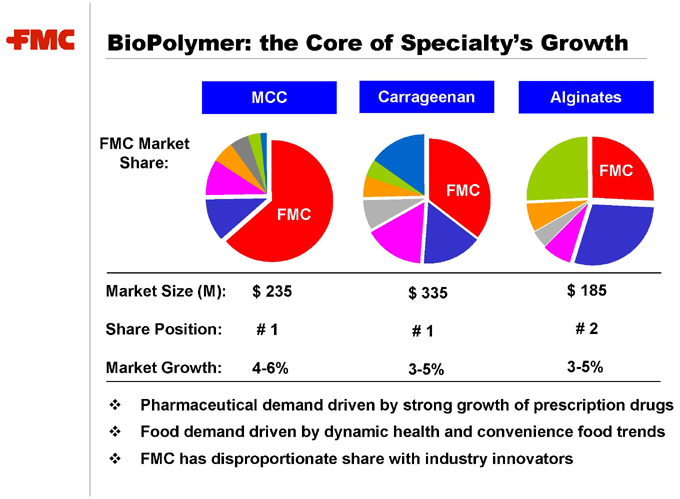

BioPolymer: the Core of Specialty’s Growth

FMC Market Share:

MCC

FMC

Carrageenan

FMC

Alginates

FMC

Market Size (M): $235 $335 $185

Share Position: # 1 # 1 # 2

Market Growth: 4-6% 3-5% 3-5%

Pharmaceutical demand driven by strong growth of prescription drugs Food demand driven by dynamic health and convenience food trends FMC has disproportionate share with industry innovators

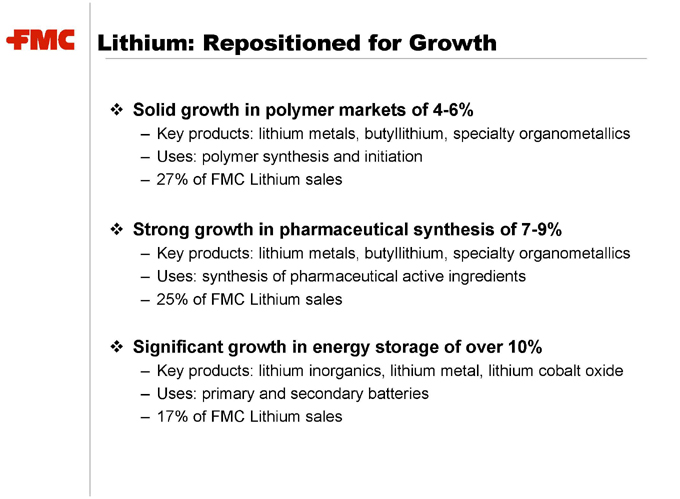

Lithium: Repositioned for Growth

Solid growth in polymer markets of 4-6%

Key products: lithium metals, butyllithium, specialty organometallics

Uses: polymer synthesis and initiation

27% of FMC Lithium sales

Strong growth in pharmaceutical synthesis of 7-9%

Key products: lithium metals, butyllithium, specialty organometallics

Uses: synthesis of pharmaceutical active ingredients

25% of FMC Lithium sales

Significant growth in energy storage of over 10%

Key products: lithium inorganics, lithium metal, lithium cobalt oxide

Uses: primary and secondary batteries

17% of FMC Lithium sales

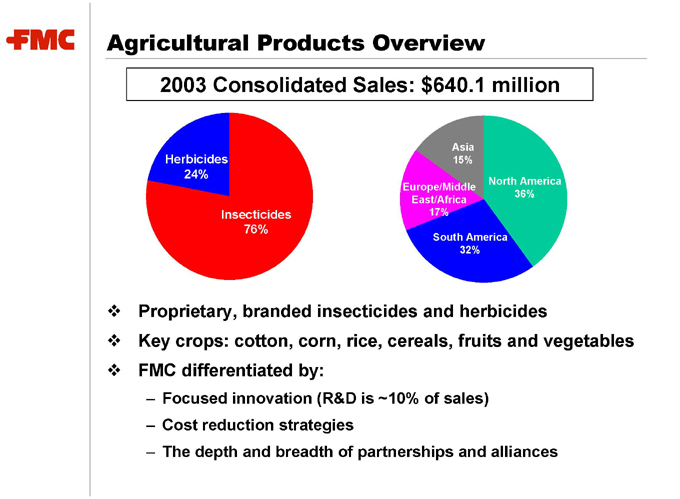

Agricultural Products Overview

2003 Consolidated Sales: $640.1 million

Herbicides 24%

Insecticides 76%

Asia 15%

Europe/Middle East/Africa 17%

North America 36%

South America 32%

Proprietary, branded insecticides and herbicides

Key crops: cotton, corn, rice, cereals, fruits and vegetables

FMC differentiated by:

Focused innovation (R&D is ~10% of sales)

Cost reduction strategies

The depth and breadth of partnerships and alliances

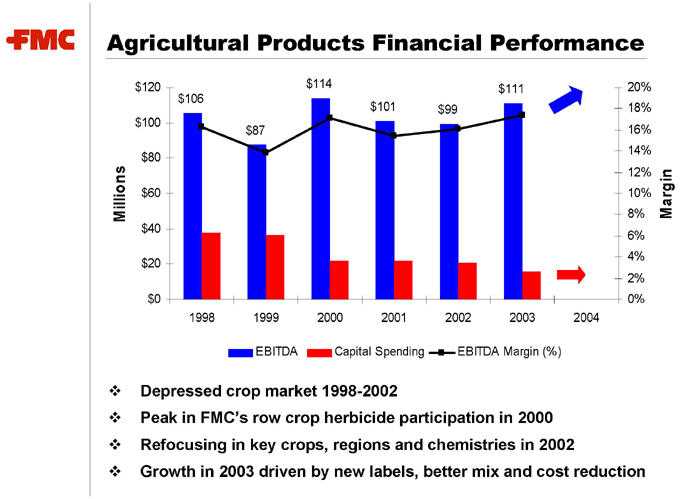

Agricultural Products Financial Performance

Millions $120

$100

$80

$60

$40

$20

$0 $114 $111 $106 $101 $99 $87

20% 18% 16% 14% 12% 10% 8% 6% 4% 2% 0%

Margin

1998 1999 2000 2001 2002 2003 2004

EBITDA Capital Spending EBITDA Margin (%)

Depressed crop market 1998-2002

Peak in FMC’s row crop herbicide participation in 2000 Refocusing in key crops, regions and chemistries in 2002

Growth in 2003 driven by new labels, better mix and cost reduction

Positive Outlook for Ag Products

Driven by robust crop markets and our focused strategy

Improving global farm economy

Rising global crop prices

Significant cost savings from productivity initiatives

Manufacturing initiatives continue to produce savings

Global supply chain redesign implemented

Success of market access strategies (alliances) in key markets

Focused product development

Label expansions in both crop and specialty markets

Novel ISK chemistry targeting sucking pests to launch 2005

Access to two new and complementary chemistries under negotiation

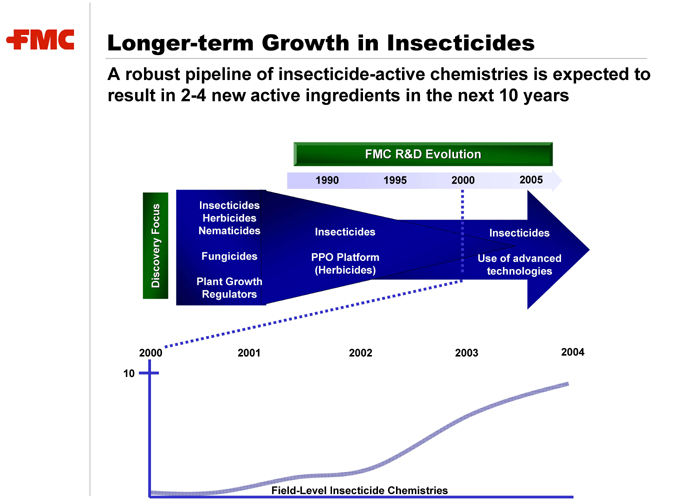

Longer-term Growth in Insecticides

A robust pipeline of insecticide-active chemistries is expected to result in 2-4 new active ingredients in the next 10 years

FMC R&D Evolution

1990 1995 2000 2005

Insecticides Herbicides Nematicides

Fungicides

Plant Growth Regulators

Insecticides

PPO Platform (Herbicides)

Insecticides

Use of advanced technologies

2000 2001 2002 2003 2004 10

Field-Level Insecticide Chemistries

Summary: Great Businesses

Great businesses, each generating EBITDA of over $100 million

Industrial Chemicals earnings that are $50 million below normal and $100 below peak

Steady growth in Specialty Chemicals and Ag Products

Low capital expenditure requirements

Improving free cash flow

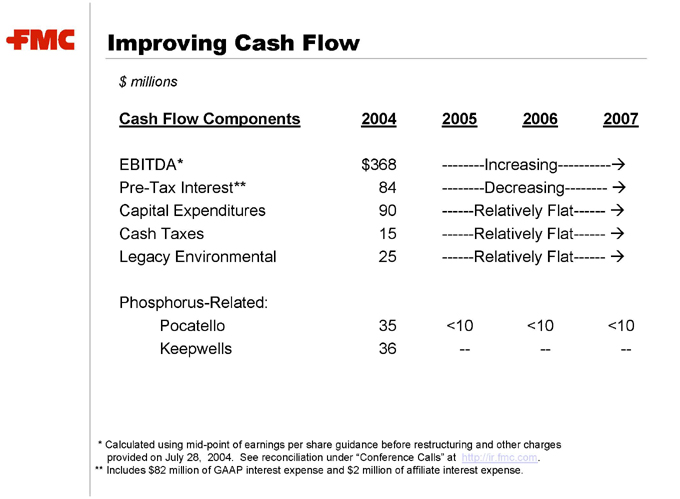

Improving Cash Flow

$ millions

Cash Flow Components 2004 2005 2006 2007

EBITDA* $368 ————Increasing—————

Pre-Tax Interest** 84 ————Decreasing————

Capital Expenditures 90 ———Relatively Flat———

Cash Taxes 15 ———Relatively Flat———

Legacy Environmental 25 ———Relatively Flat———

Phosphorus-Related:

Pocatello 35 <10 <10 <10

Keepwells 36 — — —

* Calculated using mid-point of earnings per share guidance before restructuring and other charges provided on July 28, 2004. See reconciliation under “Conference Calls” at http://ir.fmc.com. ** Includes $82 million of GAAP interest expense and $2 million of affiliate interest expense.

Strategic Objectives

Unlocking value and creating a faster growing FMC

Realize the operating leverage inherent within FMC

Double-digit growth in earnings before restructuring and other charges

Industrial Chemicals recovery to add earnings of over $1 per share

Create greater financial flexibility

Reduce net debt to $600 million by the end of 2006

Regain an investment grade credit rating

Focus the portfolio on higher growth businesses

Manage Specialty Chemicals and Agricultural Products for growth

Manage Industrial Chemicals for cash

Divest any business that cannot sustain our cost of capital

Improve ROIC to 12 percent minimum by 2006

FMC Corporation